its regional conference in rome, september 2008 martin lundborg sbr juconomy consulting ag lessons...

Post on 22-Dec-2015

213 views

TRANSCRIPT

ITS Regional Conference in Rome, September 2008

Martin LundborgSBR Juconomy Consulting AG

Lessons learned from the regulation of LLU for the future regulation of NGA networks

2

LLU has been mandated in Europe for about the last ten years as a key tool to deal with competition problems deriving from SMP operators.

Since then there has been substantial uptake in a large number of European countries, leading to more competition in the downstream access markets.

At the same time, the migration of the legacy copper networks to fiber access networks (NGA networks) has started

Are there any lessons to be learned from the past regulation of LLU for the future regulation of NGA networks.

Introduction

3

1. Which factors have been the most important for the development of LLU in the past?

2. How important are the regulated tariffs for the success of LLU?

I.e. regarding the margin between retail and wholesale prices as well as the wholesale tariffs.

3. What are the implications for NRAs regulating fixed access networks, especially within the future deployment of NGA networks?

Research questions

4

Focus on regulation of SMP networks

Study covers EU countries only:

Identical regulatory framework

Consistent and comparable data available

Comparable landscape (at the least for EU-15)

Research method

5

Content

Lessons learned from LLULessons learned from LLU11

Implications for the regulation of NGAImplications for the regulation of NGA22

Summary and conclusionsSummary and conclusions33

Technological changesTechnological changesaa

Level of regulationLevel of regulationbb

Wholesale offersWholesale offerscc

6

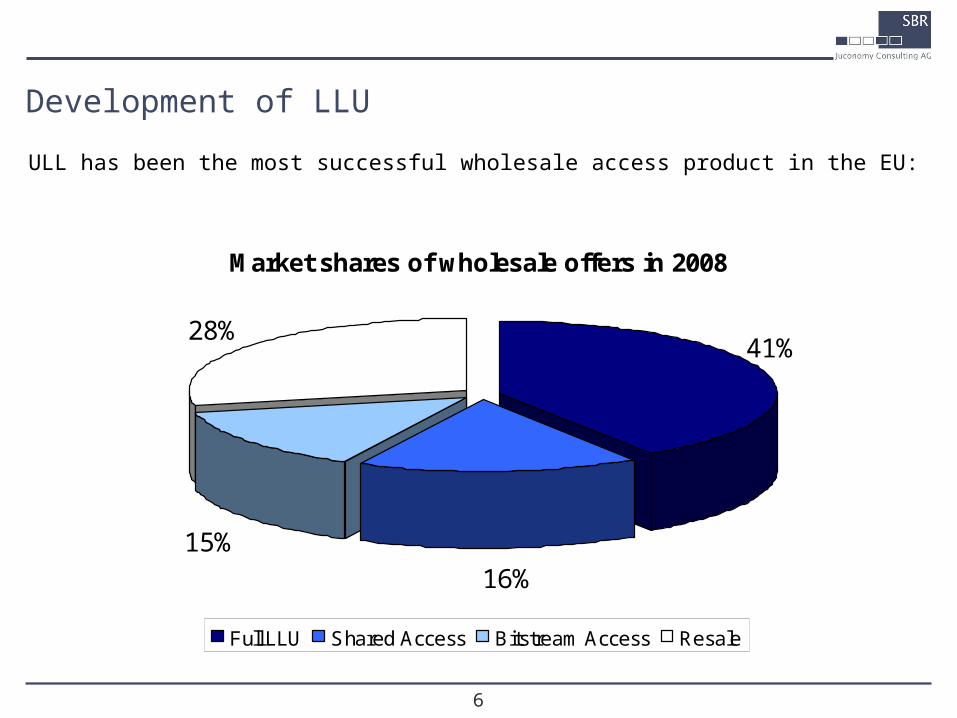

ULL has been the most successful wholesale access product in the EU:

Development of LLU

Market shares of wholesale offers in 2008

16%15%

28%41%

Full LLU Shared Access Bitstream Access Resale

7

LLU is only making up a small proportion of all access lines and the development has been heterogeneous in the EU.

Development of LLU

Penetration of fully unbundled lines

0%

2%

4%

6%

8%

10%

12%

14%

16%

Germ

any

Finlan

dIta

ly

Franc

e

Austri

a

Portu

gal

Denm

ark

Nethe

rland

sUK

Sloven

ia

Luxe

mbo

urg

Sweden

Spain

Greec

e

Cypru

s

Estonia

Belgium

Czech

Irelan

d

Hunga

ry

Latvi

a

Lithu

ania

Pen

etra

tion

in %

8

Independent variables Comment

- Monthly fee for LLU- One-time fees for LLU

Examines direct price elasticity and the relevance of prices for the success of LLU

- Retail residential prices- Retail business prices

Examines relevance of prices in downstream markets (cnf. to price-margin-squeeze tests)

- Penetration of DSL- Penetration of retail broadband lines

Is there a relationship between uptake of DSL and the success of LLU (importance of techology and value creation of the local loop)

- Penetration of broadband via alternative technologies

Examines if the infrastructure competition has been relevant for the success of LLU

Quantitative model - Description Hypothesis: The success of LLU is depending on:

The wholesale prices for the LLU The price margins between retail and wholesale prices The success of DSL because of the higher value creation via the local loop Absence of alternative access technologies (e.g. CATV)

9

Quantitative model - Results

Wholesale prices Monthly fee for LLU One-time fee for LLU

Retail prices of the incumbent Retail residential monthly charge Retail business monthly charge

Controlling variables Broadband/DSL penetration Penetration of alternative technologies (negative)

Corellation between take-up of LLU and

following independent variables

Results are significant

Results are significant at 95%-level and the correlation coefficient is high R2: 0,86 Effects can only be seen after several years of implementation (no results for 2004) For details, we refer to our paper

10

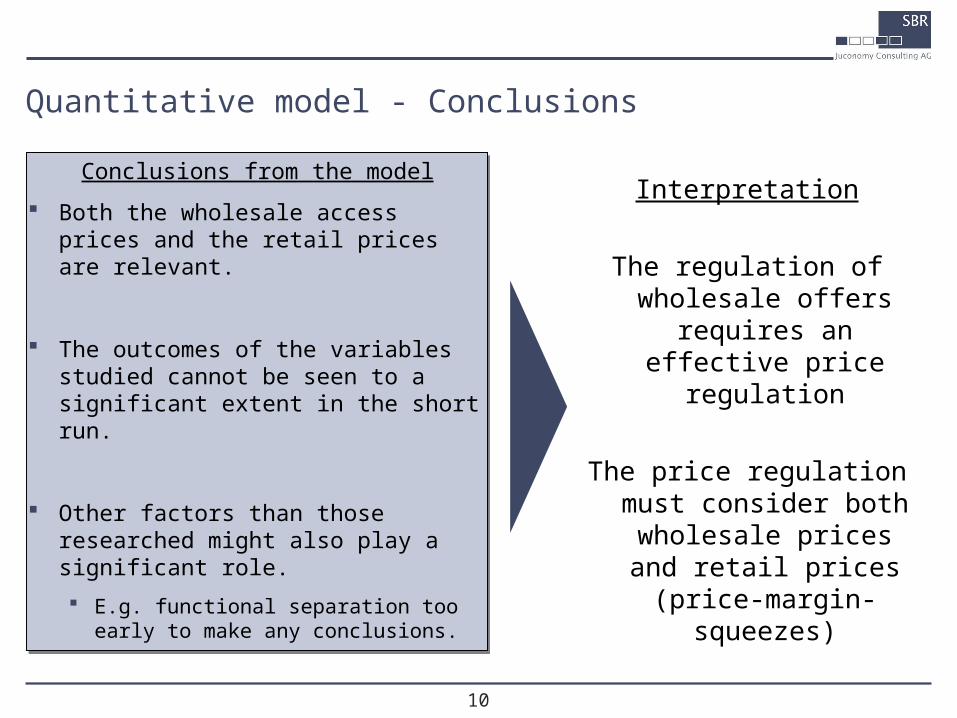

Conclusions from the model

Both the wholesale access prices and the retail prices are relevant.

The outcomes of the variables studied cannot be seen to a significant extent in the short run.

Other factors than those researched might also play a significant role.

E.g. functional separation too early to make any conclusions.

Conclusions from the model

Both the wholesale access prices and the retail prices are relevant.

The outcomes of the variables studied cannot be seen to a significant extent in the short run.

Other factors than those researched might also play a significant role.

E.g. functional separation too early to make any conclusions.

Quantitative model - Conclusions

Interpretation

The regulation of wholesale offers requires an

effective price regulation

The price regulation must consider both wholesale prices and retail prices

(price-margin-squeezes)

11

Content

Lessons learned from LLULessons learned from LLU11

Implications for the regulation of NGAImplications for the regulation of NGA22

Summary and conclusionsSummary and conclusions33

Technological changesTechnological changesaa

Level of regulationLevel of regulationbb

Wholesale offersWholesale offerscc

12

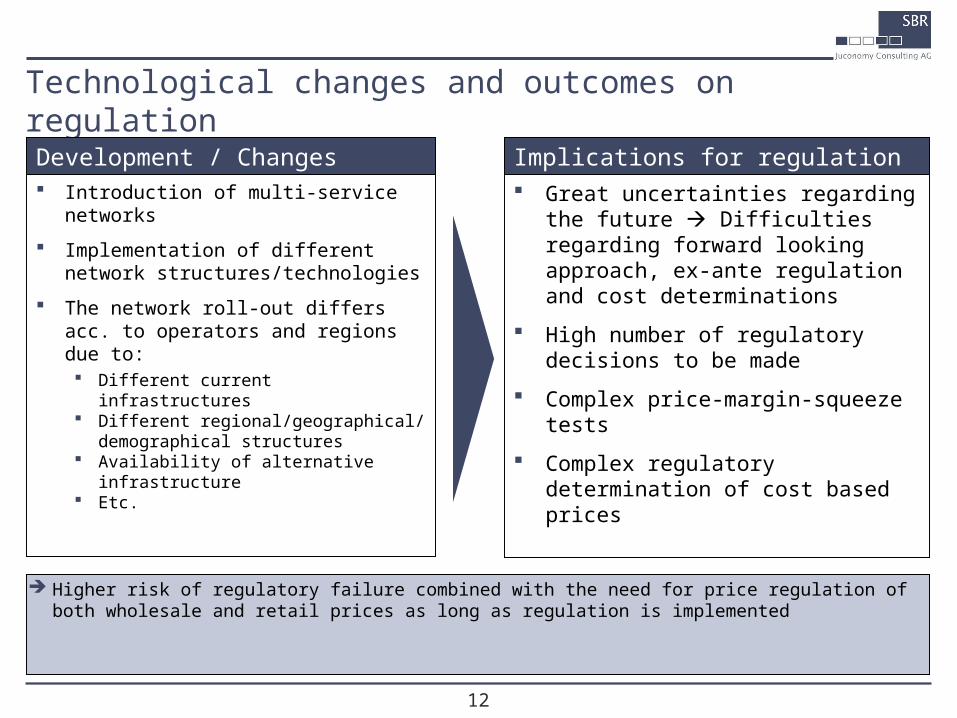

Technological changes and outcomes on regulation

Implications for regulationDevelopment / Changes

Introduction of multi-service networks

Implementation of different network structures/technologies

The network roll-out differs acc. to operators and regions due to: Different current infrastructures Different regional/geographical/

demographical structures Availability of alternative

infrastructure Etc.

Great uncertainties regarding the future Difficulties regarding forward looking approach, ex-ante regulation and cost determinations

High number of regulatory decisions to be made

Complex price-margin-squeeze tests

Complex regulatory determination of cost based prices

Higher risk of regulatory failure combined with the need for price regulation of both wholesale and retail prices as long as regulation is implemented

13

Content

Lessons learned from LLULessons learned from LLU11

Implications for the regulation of NGAImplications for the regulation of NGA22

Summary and conclusionsSummary and conclusions33

Technological changesTechnological changesaa

Level of regulationLevel of regulationbb

Wholesale offersWholesale offerscc

14

Appropriate level of regulation

Alternative decisions regarding levels of regulation

DeregulationDeregulationContinue current

regulationContinue current

regulationRegulatory

holidaysRegulatory

holidays

No/less regulation

Improves incentives for SMP operators to invest (e.g. Jorde, Sidak and Teece AND De Bijl and Peitz).

The introduction of NGA tends to make regulation more difficult and might therefore increases risks of regulatory failures.

Continued regulation

Regulation of SMP operators required to safeguard competition.

E.g. Marcus and Elixman concludes that the lightening of regulation in USA has lead to non-geographic overlapping duopolies and disenvestments by ANOs.

15

Appropriate level of regulation

Need for case by case regulation to prevent over- or underregulation Argument for the European

regulatory framework

Considerations in case of existance of SMP

Trade-off between investment incentives by SMP operators (by less regulation) and safeguarding of competition (including price regulation)

SMP problems will remain (extensive investment requirements in access networks, economies of scales etc.)

More difficult regulation due to complex NGA environment

16

Content

Lessons learned from LLULessons learned from LLU11

Implications for the regulation of NGAImplications for the regulation of NGA22

Summary and conclusionsSummary and conclusions33

Technological changesTechnological changesaa

Level of regulationLevel of regulationbb

Wholesale offersWholesale offerscc

17

Wholesale offers will change due to NGA

Possible wholesale offers Current network

FTTC FTTH - PtP

FTTH - PON

FTTB

Unbundling at the MDF Unbundling at the street cabinet Unbundling at the building/basement Unbundling at the ODF ? Wholesale broadband access at the Broadband PoP or MSN

Duct sharing/Dark fiber

The current unbundling at the MDF might disappear, but there are still other more or less practical potential wholesale offers for all network structures.

E.g. FTTB: This means that the ANO has to roll-out his network to the basement/building, which is costly Additional access obligations for ducts/dark fibre might be required.

18

Regulation of wholesale offers will change due to NGA

Price regulation required to safeguard success of

wholesale access offers

Large number of new wholesale offers to regulate

Complex regulation with a large number of regulatory decisions

+

As wholesale offers and networks are new, there are almost no accounting data

or „cost experience“ to rely on

19

Content

Lessons learned from LLULessons learned from LLU11

Implications for the regulation of NGAImplications for the regulation of NGA22

Summary and conclusionsSummary and conclusions33

Technological changesTechnological changesaa

Level of regulationLevel of regulationbb

Wholesale offersWholesale offerscc

20

If regulation of wholesale access should be successful, wholesale and resale prices must be subject to regulation to prevent too high access prices and price margin squeezes

This implies, that for countries and regions without a sufficient number of access networks and with SMP operators, price regulation is required if the wholesale access offers should experience a significant uptake.

Summary and conclusions regarding LLU regulation

Lessons lerned from regulation of LLU

Outcomes on regulation of NGA

The complexity of regulation tends to be much more complex due to sub-national markets, multiple technologies, high number of wholesale access offers and multi-service networks.

Further, as networks are (or will be) rolled-out, the regulators must strike the balance between investment incentives for SMP operators and development of competition.

This calls for a flexible regulation such as the European Framework.

21

SBR JUCONOMY Consulting AGSBR Attorneys-at-Law

Vienna OfficeParkring 10/1/101010 ViennaAustriaTel: + 43-1-513 514 0-0 Fax: + 43-1-513 514 0-95

Düsseldorf HeadquartersNordstrasse 17740477 DüsseldorfGermanyTel: + 49-211-68 78 88-0Fax: + 49-211-68 78 88-33

[email protected]@[email protected]@sbr-net.com

22

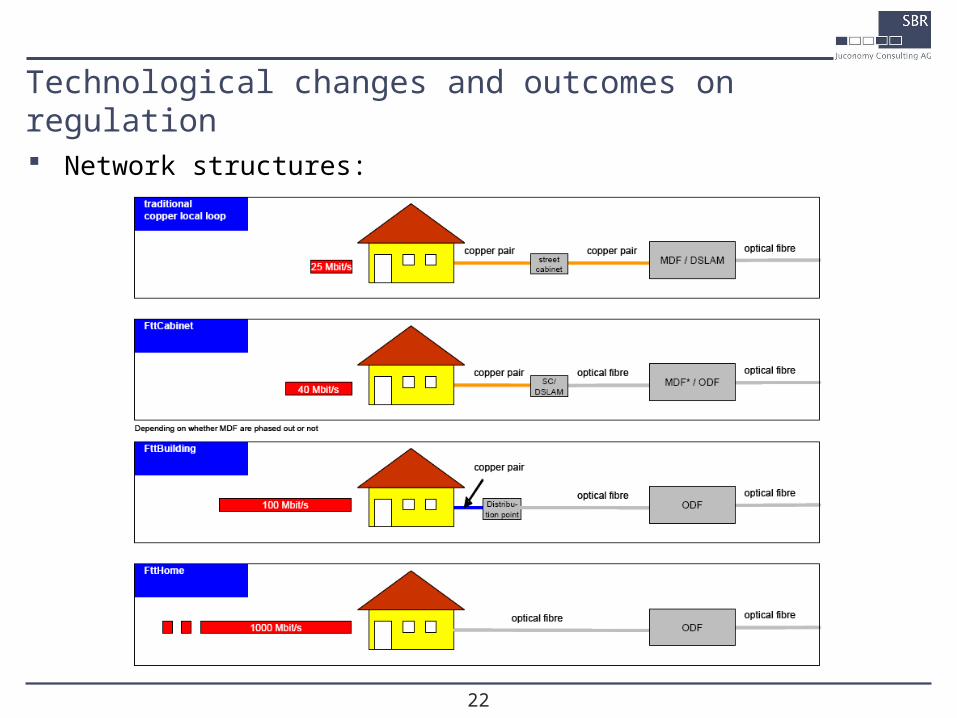

Technological changes and outcomes on regulation

Network structures: