it is a destination based tax - gps...

TRANSCRIPT

It is a destination based taxon consumption of goodsand services. It is proposedto be levied at all stagesright from manufacture upto final consumption withcredit of taxes paid atprevious stages available assetoff. In a nutshell, onlyvalue addition will be taxedand burden of tax is to beborne by the finalconsumer.

10.08.2017GMJ & Co for GPS

2

Central taxes► Additional Customs Duty (in lieu of

Excise Duty)► Central Excise Duty► Special Additional Customs Duty► Service Tax ► Central Sales Tax► Central surcharges and cesses

relating to supply of goods & services

State taxes► State-VAT (sales Tax) ► Purchase Tax► State Entry Tax► Luxury Tax ► Entertainment Tax► Taxes on Lottery, Betting &

Gambling► Octroi

► Basic Customs Duty► Stamp Duties► Electricity Duty

Exclusions (will continue)

Key Features ‐ Taxes to be Subsumed

►Tax on alcoholic liquor for human consumption

►Petroleum products – levy of GST to be made effective at a future date

►Tax on entertainment and amusement levied and collected by Municipal authorities

10.08.2017 GMJ & Co for GPS 3

► Ideally it should be one GST rate on all goods and servicesacross India with few exemptions for basic necessities andreduced rate for some goods and services.

Indian GST

Centre and States to levy GST on common base (CGST & SGST)

Dual-GST

►Potentially aligned to current VAT exemptions

Minimum exemptions

Integrated‐GST (IGST) on inter‐state supplies / import of goods and services

Inter-state supplies / import of goods & services

Dual GST Model

10.08.2017 GMJ & Co for GPS 4

Dual Structure

Dual Levy

Dual Control

Destination Base

10.08.2017 GMJ & Co for GPS 5

•Origin Base

Old

•Destination Base• The tax would accrue to the taxing authority which has jurisdiction over the place of consumption which is also termed as place of supply.

GST

FLOW OF CREDIT UNDER GST LAW

CGST

SGST

10.08.2017 6

IGST IGST CGST SGST UT‐GST

CGST CGST IGST Not against SGST

Not against UT‐GST

SGST SGST IGST Not against CGST

Not against UT‐GST

UT‐GST UT‐GST IGST Not against CGST

Not against SGST

UT‐GSTGMJ & Co for GPS

15th July

Furnishes GSTR –1 Outward Supply

ProvisionalITC

Furnishes GSTR –2 inward Supplyby modifying theauto populatedinformation

Such details available tosupplier in GSTR‐1A. Hemay accept or reject thechanges

10.08.2017 GMJ & Co for GPS 7

Matching Concept

Matching Concept Cont..

Furnishes GSTR-3 by 20th

Electronic Credit

RegisterPayment by

Final ITC available

10.08.2017 GMJ & Co for GPS 8

Furnishes GSTR-3 by 20th

GMJ & Co for GPS 910.08.2017

Supply

All Forms.. for consideration .. In the course /furtherance of

business

Import of Services for

consideration, whether for

business or not

Permanent transfer/disposal of business assets (ITC taken)

Branch Transfer in

another State

Transaction between related person

Transfer to/from Agent

Import of Services from related person

without Consideration

Schedule III

Composite / Mixed Supply

10.08.2017 10GMJ & Co for GPS

Registration• Every supplier who makes a taxable supply of goods/services and his aggregate turnover in financial year exceeds Twenty Lakh Rupees shall be liable to be registered under GST (for special category of state the turnover to be considered is Ten Lakh Rupees )

• Threshold limit of Twenty Lakh Rupees is not in the following case (applicable to travel agent and tour operator):

person making any inter‐sate taxable supplyPerson who makes taxable supply of goods or service or both on behalf of other taxable person whether as an agent or otherwise,

• Air Travel Agent?10.08.2017 GMJ & Co for GPS 11

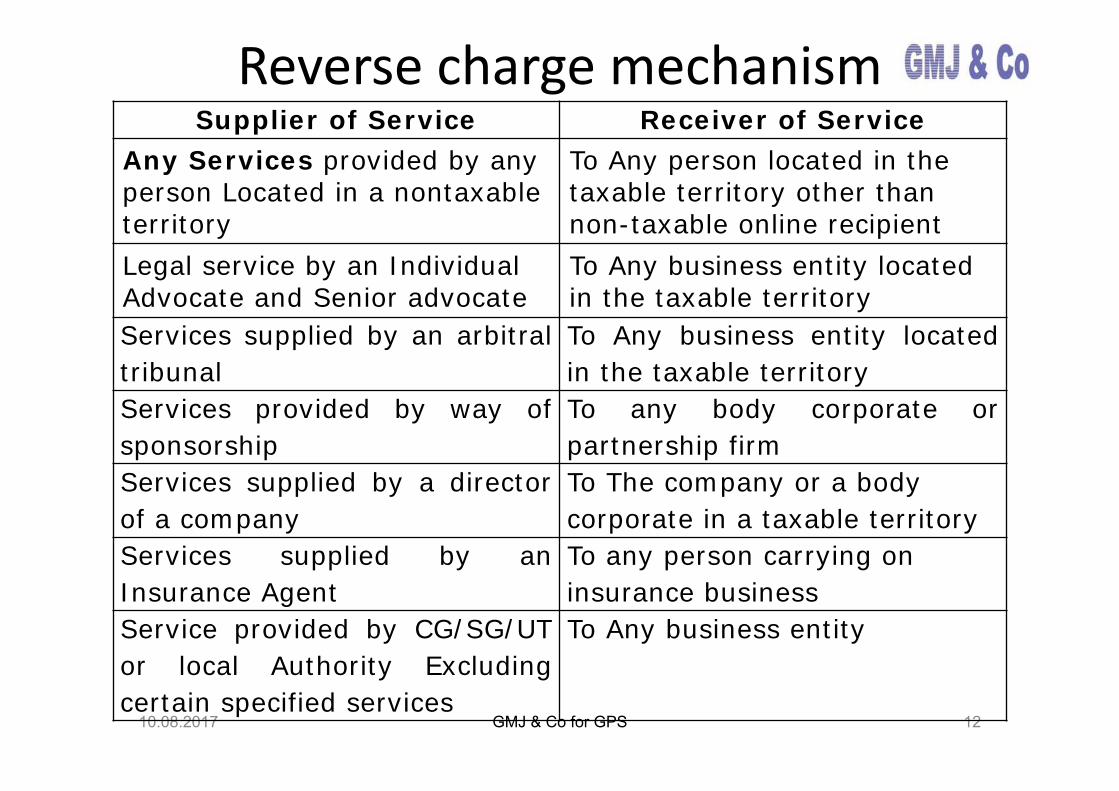

Reverse charge mechanism

10.08.2017 GMJ & Co for GPS 12

Supplier of Service Receiver of ServiceAny Services provided by any person Located in a nontaxable territory

To Any person located in the taxable territory other than non-taxable online recipient

Legal service by an Individual Advocate and Senior advocate

To Any business entity located in the taxable territory

Services supplied by an arbitraltribunal

To Any business entity locatedin the taxable territory

Services provided by way ofsponsorship

To any body corporate orpartnership firm

Services supplied by a directorof a company

To The company or a body corporate in a taxable territory

Services supplied by anInsurance Agent

To any person carrying on insurance business

Service provided by CG/SG/UTor local Authority Excludingcertain specified services

To Any business entity

10.08.2017 GMJ & Co for GPS 13

Supplier of Service Receiver of ServiceTaxable Services or goods from anunregistered person*

To any registered person

• Staff Welfare– Tea/Coffee– Snacks

• Printing and Stationery– Paper– Envelopes– Xerox– Printer Toner/ Cartridge Refilling

– Misc Stationery Items

• Repair and Maintenance– Electrical, Plumbing– AMC (A/C, Computer, etc.)

• Other Expenses– Housekeeping– Rent Expense– Security

Exemption is given upto Rs.5,000/- per recipient per day

Invoicing For RCM

10.08.2017

• Taxable Supply made by Unregistered Person to a Registered Person; or

• Supplies in which Recipient has to pay tax under Reverse Charge

GMJ & Co for GPS 14

Consolidated Invoice for all such supplies has to be issued by the Recipient at the

month end

Shall issue a Payment Voucher at the Time of

Making Payment to the Supplier

Time of Supply

10.08.2017 15GMJ & Co for GPS

Issue of Invoice by the supplier if the invoice is issued within 30 days of provision of service

Date of Payment

Date of Provision of Service is invoice is not issued within 30days

Date of Payment

Earlier of

OR

10.08.2017 16

Time of supply of Services

Earlier of

GMJ & Co for GPS

• Name, Address and GSTIN of the supplier• Serial Number of Invoices Max16 characters (can contain ‘–’ or

‘/’) unique for a financial year• Date of issue of Invoice• Name, Address and GSTIN/ UIN if the receiver is registered• HSN / Accounting Code of services• Description of Goods/Services• Quantity of Goods• Total Value of Goods/Services• Taxable Value of Goods/Services taking into account any

discount or abatement• Rate of Tax (CGST, SGST or IGST)• Amount of Tax Charged• Place of Supply along with the Name of the state• Whether tax payable on RCM• Signature or Digital Signature of the supplier or his authorized

representative

Details on Tax Invoice Rules

10.08.2017 GMJ & Co for GPS 17

Receipt Voucher‐For Advance Received

• Name, Address and GSTIN of the supplier• Serial Number of Invoices Max16 characters (can contain ‘–’ or ‘/’)• Date of its issue• Name, Address and GSTIN if the receiver is registered• Description of Goods/Services• Amount of advance taken• Rate of Tax (CGST, SGST or IGST)• Amount of Tax Charged• Place of Supply along with the Name of the state if Inter‐state supply• Whether tax payable on RCM• Signature or Digital Signature of the supplier or his authorizedrepresentative

10.08.2017

• Rate of Tax is not Determinable: Tax @ 18%• Nature of Supply is not determinable: Deemed IGST

GMJ & Co for GPS 18

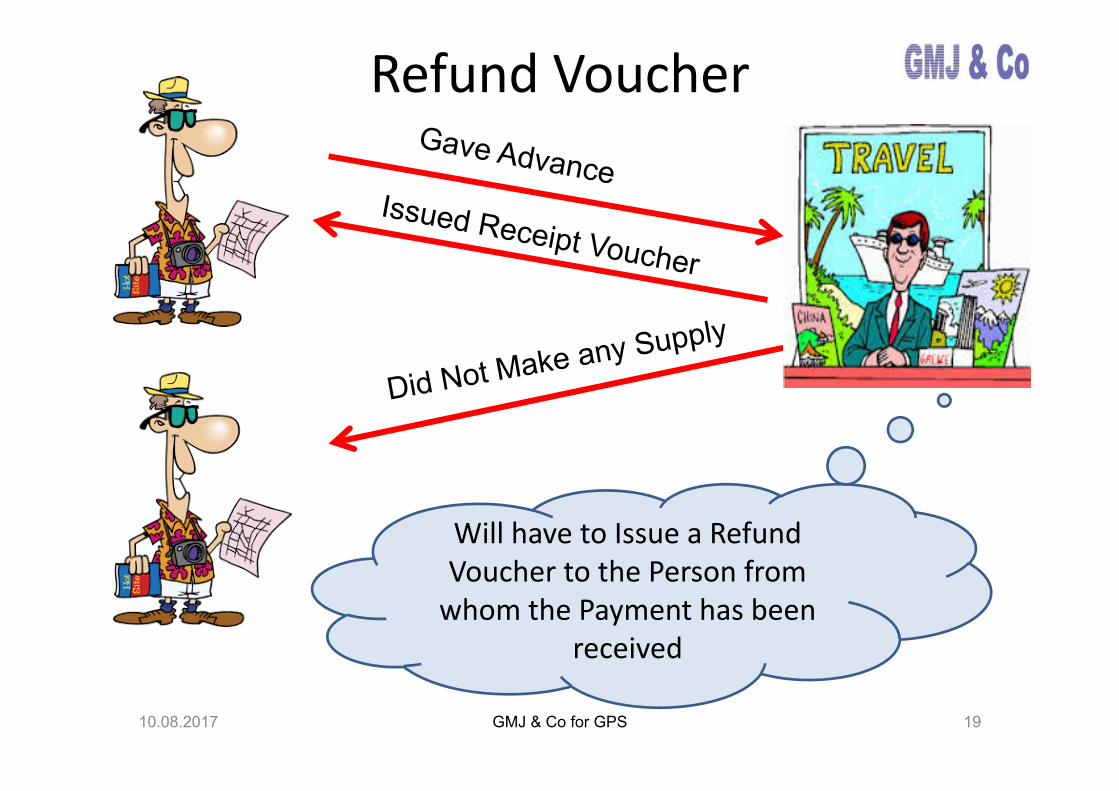

Refund Voucher

10.08.2017

Will have to Issue a Refund Voucher to the Person from whom the Payment has been

received

19GMJ & Co for GPS

10.08.2017

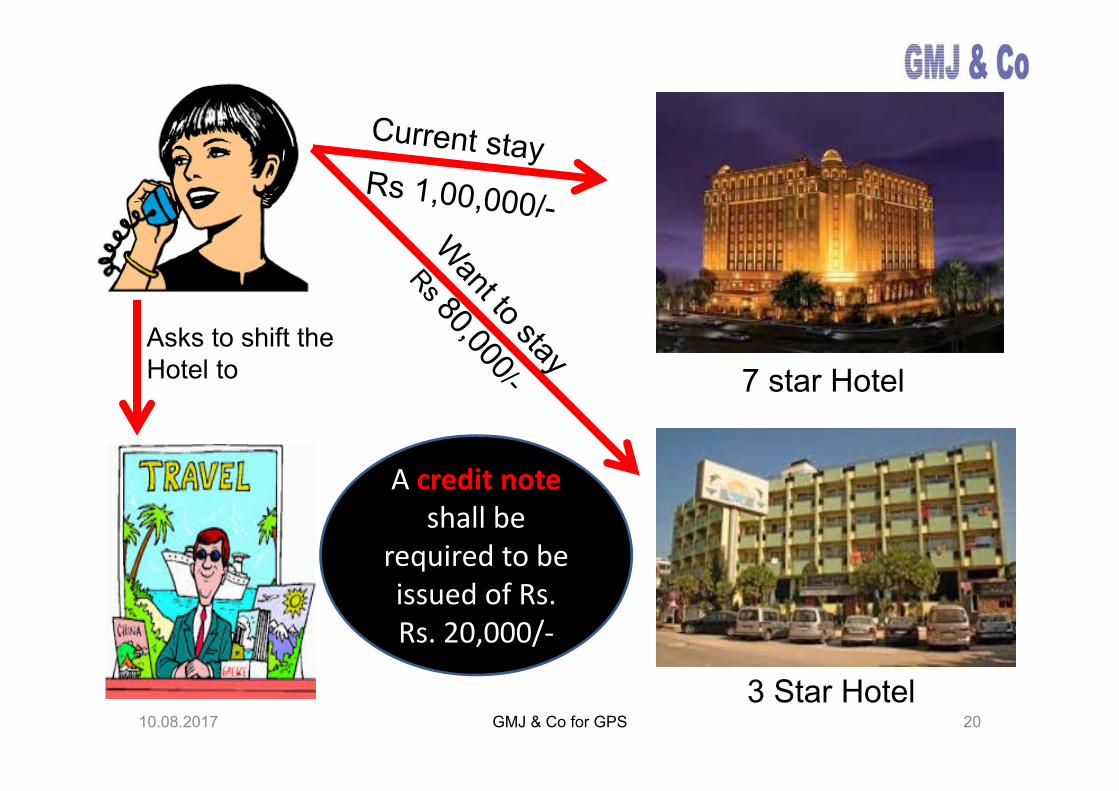

7 star Hotel

3 Star Hotel

Asks to shift the Hotel to

A credit note shall be

required to be issued of Rs. Rs. 20,000/‐

20GMJ & Co for GPS

10.08.2017

Asks the Tour Operator to increase the Tour to 15 Days. The Package will now cost Rs. 2,50,000/-

Books the Tour for 10 Days for Rs. 2,00,000/-

A Debit note shall be

required to be issued of Rs. Rs. 50,000/‐

21GMJ & Co for GPS

2210.08.2017 GMJ & Co for GPS

GMJ & Co for GPS 23

Transaction Value shall include:

• Taxes levied other than GST Acts, if charged separately. • Amount that supplier is liable pay in relation to such supply but incurred by recipient and not included in the price.

• Incidental expenses such as commission & packaging and charged by the supplier to the recipient including any amount charged for anything done by the supplier in respect of the supply of goods and/or services at the time of, or before delivery of the goods or, supply of the services

• interest or late fee or penalty for delayed payment of any consideration for any supply

• subsidies directly linked to the price excluding subsidies provided by the CG and SG. The subsidy shall be included in the value of supply of supplier who receives the subsidy

10.08.2017

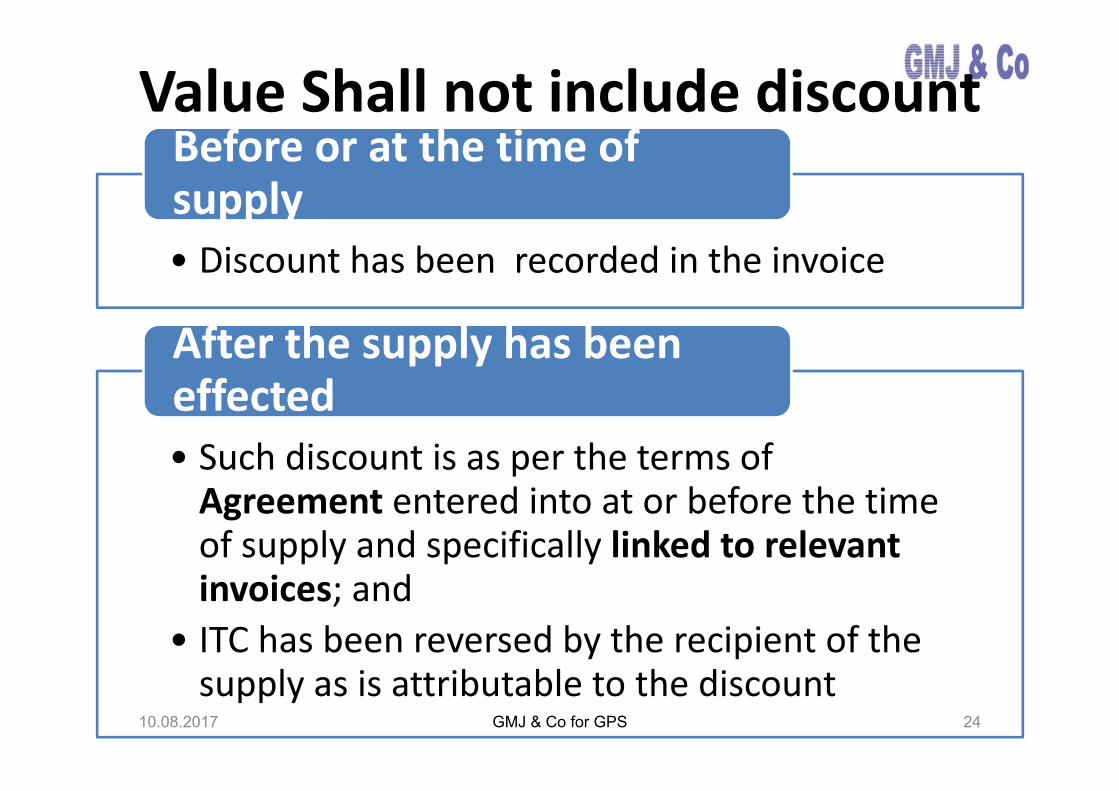

Value Shall not include discount

• Discount has been recorded in the invoice

Before or at the time of supply

• Such discount is as per the terms of Agreement entered into at or before the time of supply and specifically linked to relevant invoices; and

• ITC has been reversed by the recipient of the supply as is attributable to the discount

After the supply has been effected

10.08.2017 GMJ & Co for GPS 24

10.08.2017 GMJ & Co for GPS 25

Air Travel Agent

10.08.2017 GMJ & Co for GPS 26

Nature of Service

10.08.2017 GMJ & Co for GPS 27

Airlines

• Appoints ATA to sale tickets• Transportation of Passengers • Appoints ATA to sale tickets• Transportation of Passengers

ATA

• Sale of Air Tickets• Book ticket for Passengers• Sale of Air Tickets• Book ticket for Passengers

Passengers

• Traveling from one place to another• Approach ATA to book ticket

10.08.2017 GMJ & Co for GPS 28

Order for flower Deliver flower

Recipient of Service

ATAAir line/ IATA Passenger

Entered in to contract to sale ticket on Comm/ upload incentive, etc.

Charge BF

Air / Rail Travel Agent

10.08.2017 GMJ & Co for GPS 29

• ITC of Goods/ Services will be available state wise

• ITC of GST paid on Air / Rail Ticket not available

10.08.2017 GMJ & Co for GPS 30

GST to be paid on

Commission / PLB / upload incentive / any other form of

incentive from airline as well as booking fees from passenger

GST @ 18% on Commission / PLB / upload incentive / any other form of incentive. Issue

invoice on Airline/ Consolidator

Booking Fees @ 18%. Issue invoice on Passenger

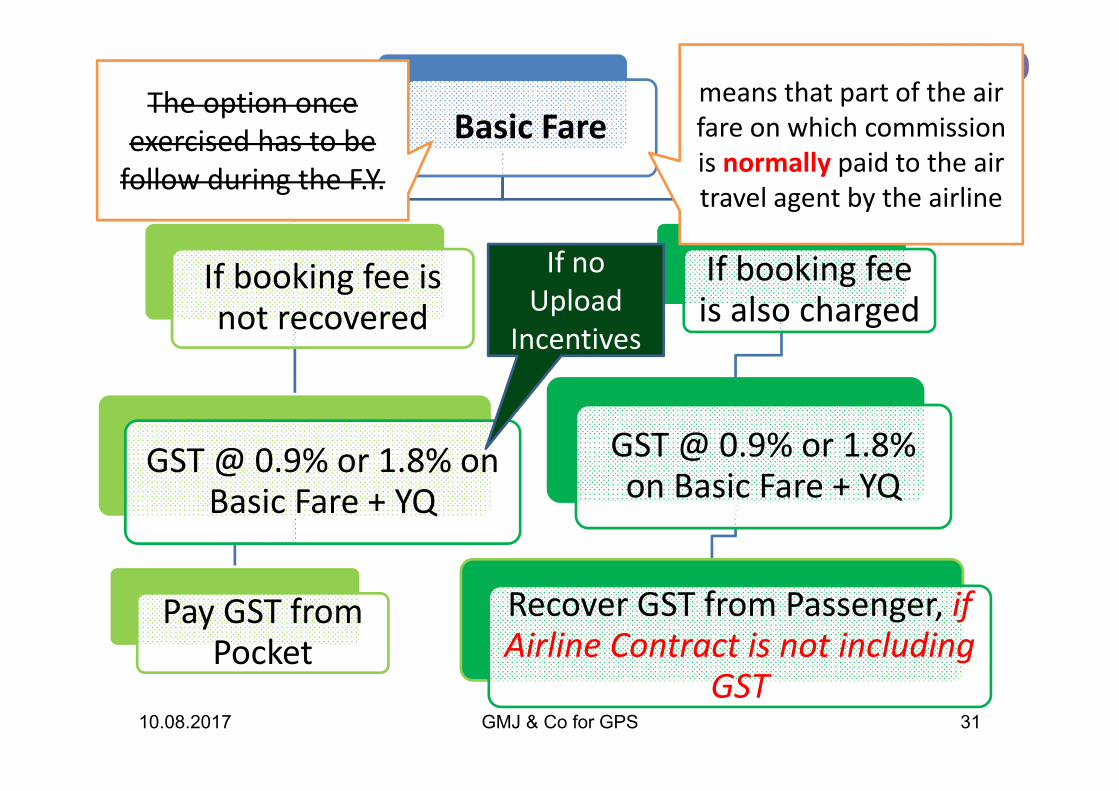

Basic Fare

For Domestic Booking

0.9% of Basic Fare

For International

Booking

1.8% of Basic Fare

ATA has 2 options to pay GST

Basic Fare

If booking fee is not recovered

GST @ 0.9% or 1.8% on Basic Fare + YQ

Pay GST from Pocket

If booking fee is also charged

GST @ 0.9% or 1.8% on Basic Fare + YQ

Recover GST from Passenger, if Airline Contract is not including

GST10.08.2017 GMJ & Co for GPS 31

The option once exercised has to be follow during the F.Y.

means that part of the air fare on which commission is normally paid to the air travel agent by the airline

If no Upload

Incentives

Details to passenger

10.08.2017 GMJ & Co for GPS 32

When ATA is on commission model

Particulars Reimbursem

ent of Exp

Taxable

Value

Total

Value

1. Reimbursement of Air ticket

issued by Airlines

10,000 - 10,000

1a. Value of Basic fare included

above

9500 - -

2. Booking Fees charged to

passengers

- 200 200

3a. Add: CGST @ 9% (OR IGST

@18%)

- 18 18

3b. Add: SGST @ 9% - 18 18

4. Total - 236 10236

10.08.2017 GMJ & Co for GPS 33

Invoice to Airline

When ATA is on commission model

Particulars Reimbur

sement

of Exp

Taxable

Value

Total

Value

1. Commission from Airline - 400 400

2a. Add: CGST @ 9% (OR IGST

@18%)

- 36 36

2b. Add: SGST @ 9% - 36 36

3. Total (to be recovered

from Airlines)

- 472 472

Invoice to passenger (domestic booking)

10.08.2017 GMJ & Co for GPS 34

When ATA is on Basic fare model

Particulars Nontaxab

le Value

Taxable

Value

Total

Value

1. Reimbursement of Air ticket

issued by Airlines

10,000 - 10,000

1a. Value of Basic fare included above - 9500 -

2. Booking Fees charged to

passengers

200 200

3a. Add: CGST @ 0.45% (OR IGST

@0.9%)

- 42.75 42.75

3b. Add: SGST @ 0.45% - 42.75 42.75

4. Total (to be recovered from Client) - - 10285.5

Invoice to Airlines

10.08.2017 GMJ & Co for GPS 35

When ATA is on Basic fare model

Particulars Nontaxable

Value

Taxable

Value

Total

Value

1. Commission from Airline 400 400

2a. Add: CGST @ 9% (OR

IGST @18%)

-

2b. Add: SGST @ 9% -

3. Total(to be recovered

from Airlines)

- - 400

Place of Supply of Service

10.08.2017 GMJ & Co for GPS 36

B2B

Taxable Recipient

Taxable Supplier

State A State B

Place of Supply of Service

B2C Non Taxable Recipient

Place of Supply of Service if address of recipient not available Place of Supply of Service

if address available

ABC & Co

Mr. XYZ

A T A

10.08.2017 GMJ & Co for GPS

ATA

Destination & Location of Passenger

Origin & Location of Airlines

GST Payable in India

37

Since ATA acts as an

Intermediary

Sub Agent buying tickets from consolidator• Sub agent can also avail the option of paying GST at basic fare module or commission module (commission received from consolidator or service fees from client)

• Place of supply for a Sub Agent will be same as of a normal agent i.e.

Location of service receiver (if service receiver is located)If address record on recipient exist, location of service receiverLocation of service provider in any other case

10.08.2017 GMJ & Co for GPS 38

It is advisable to an ATA and a sub agent to provide client’s Email ID while booking the ticket

CRS/GDS

Other ATA in IndiaGet consideration for using the services of

CRS/GDS towards loyalty

ProvidesPlatform/software for booking of tickets/hotels,

etc.

CRS/GDS

10.08.2017 GMJ & Co for GPS 39

POS where the GSA of CRS is in India

10.08.2017 GMJ & Co for GPS 40

GSA of CRS

ATA

POS

10.08.2017 GMJ & Co for GPS 41

POS where the CRS outside India

POS

ATA

CRS

Visa / Passport

10.08.2017 GMJ & Co for GPS 42

GST @ 18% on service charges / fees to be charged to clients

Visa Facilitation Centers

Professional Consultancy

Directly through Embassy

Visa Fees

10.08.2017 43GMJ & Co for GPS

SN Particulars Con VFS VA1 Consulate Fees (proof in record) Draft

Exemption5000 5000 5000

2 VFS 2.1 VFS Fees 10002.2 Courier/DD Charges etc. 3002.3 GST@18% on 2.1+2.2 234

Total 65343 Agents3.1 Visa Fees 5003.2 Reimbursement of VFS fees as per

receipt attached*1534

3.3 GST@ 18% on 3.1 90Total 7124

No GST on visa fees paid to consulates & is shown separately & receipt is also attached with invoice

POS for Visa Services

10.08.2017 GMJ & Co for GPS 44

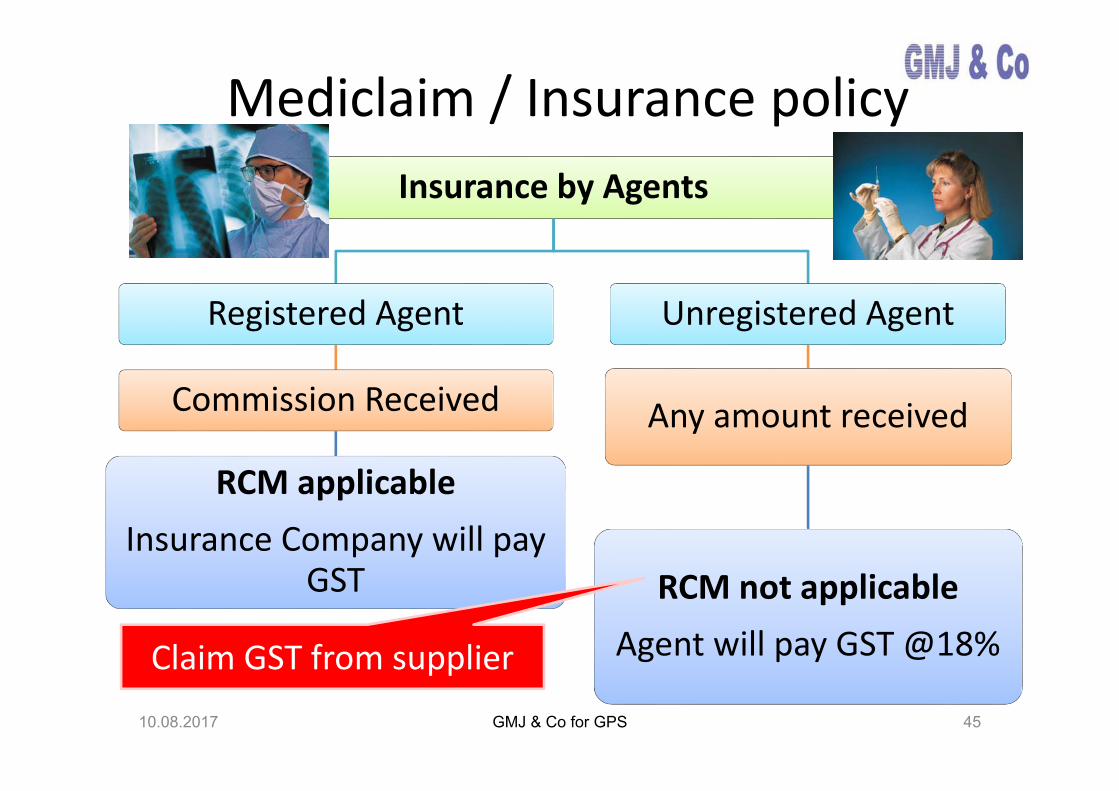

Mediclaim / Insurance policy

10.08.2017 GMJ & Co for GPS 45

Insurance by Agents

Registered Agent

Commission Received

RCM applicableInsurance Company will pay

GST

Unregistered Agent

Any amount received

RCM not applicableAgent will pay GST @18%Claim GST from supplier

International SIM Card

GST is payable on commission or mark‐up

earned @18% by the travel Agent

10.08.2017 GMJ & Co for GPS 46

10.08.2017 GMJ & Co for GPS 47

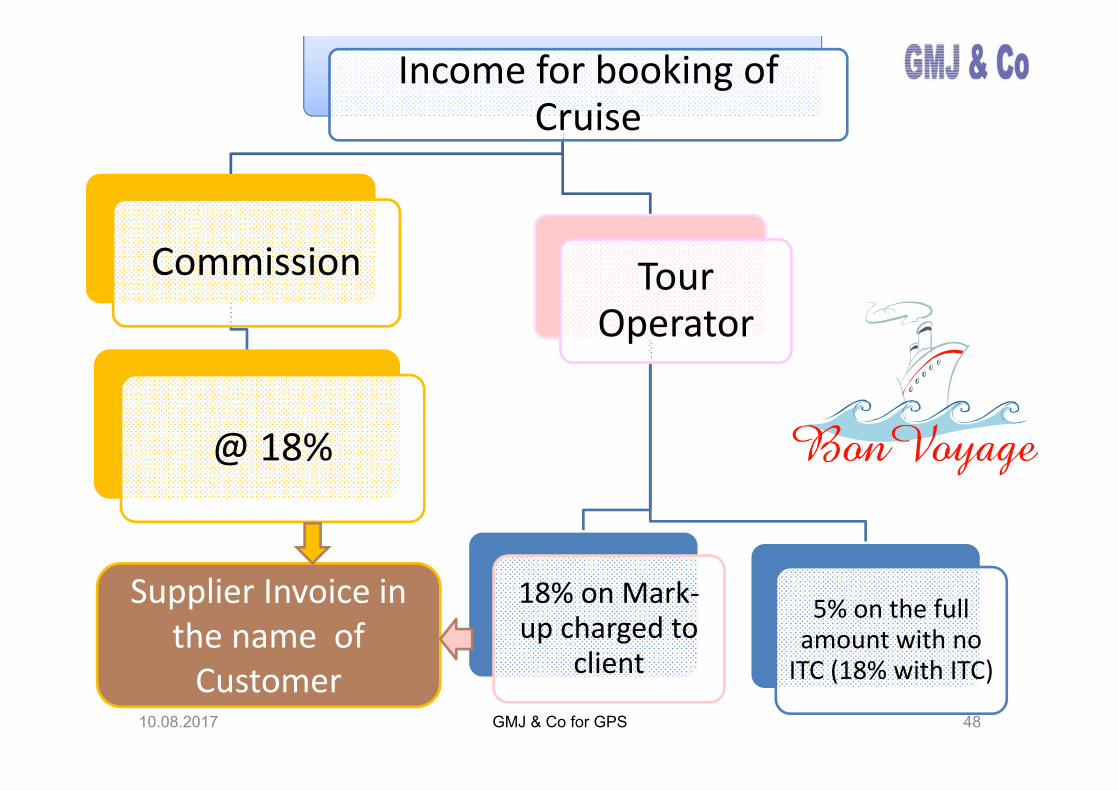

Cruise Booking• Commission from Main / Master Agents

• GST @18% on Commission• To be charged to Main / Master Agent

Booking by Agents

• Commission from Parent Company• GST @18% on Commission• To be charged to Parent Company• Main / Master Agent will claim set‐off of GST paid to Agent against their liability

Booking by Main / Master Agents

10.08.2017 GMJ & Co for GPS 48

Income for booking of Cruise

Commission

@ 18%

Tour Operator

18% on Mark‐up charged to

client

5% on the full amount with no ITC (18% with ITC)

Supplier Invoice in the name of Customer

Hotel/Cruise

10.08.2017

Services directly relating to

Accommodation by a hotel, etc. incl house boat, vessel

Accommodation in any imm. Prop. For any marriage or function etc. incl services provided i.r.t. such function at such property

Any related ancillary service

Location of immovable property or boat or vessel or intended location

Location of the recipient of Service

If in India If outside IndiaIncase the service provider or recipient is outside India, POS shall be the location of such immovable property

49GMJ & Co for GPS

Cruise to Foreign Pax

10.08.2017 GMJ & Co for GPS 50

• Invoice should contain Name, Address and GST Number of Service Recipient

• Luxury Tax will subsume• Place of Supply

Shall be the location of actual performance of service in case

Services provided to an individual who is recipient of service/ person representing

the SR

in the physical presence of the service receiver or a person

acting on behalf of the receiver

With the SP for the provision of service

Service supplied at more than 1 location including a location in taxable territory

Maharashtra

12%

Sri Lanka

13%

Maldives

75%

Place of supply shall be Maharashta

Domestic or International Rail/Bus ticket

Location of SR Bookings Rate

On Commission

Any location, whether in

taxable territory or non‐

taxable territory

Any booking, whether domestic

booking or international booking

18%

On Service Charges or margin (invoice should be in the name of Client)

In taxable territory Domestic 18%

In non‐taxable territory Domestic 18%

In taxable territory International 18%

In non‐taxable territory International 18%10.08.2017 GMJ & Co for GPS 51

Rent a cab

Commission model

GST @ 18%

Net cost and Mark‐up Basis

GST @ 5% on full value of

invoice including value of fuel No

ITC

GST @ 12% on full value of invoice including

value of fuel with ITC

GST @18% on full value of invoice excluding value of fuel with

ITC

10.08.2017 GMJ & Co for GPS 52

As per decision taken on 20thGST Council Meeting

10.08.2017

Car Hire/Air Line/ RailwayPlace of supply for passenger transportation

Location of Supplier and Recipient of Service is in India

Location of Supplier or Recipient of Service is

Outside India

service receiver is registered?

Yes No

Location of Service Receiver

Place where the passenger embarks on the conveyance for a continuous

journey

Place where the passenger embarks on the conveyance for a continuous journey

53GMJ & Co for GPS

10.08.2017 GMJ & Co for GPS 54

Income for Tour Operator

Commission Income from

hotel/transporter/ other agents

18% on commission earned

Tour operator will issue invoice on the hotel/transporter/ other agents for

commission earned

Service charges from the client

18% on the service charges charged to the

client

Tour operator will pay GST on service charges only if the invoice of hotel /transporter is directly in the name

of client

Sale of tour on principal to

Principal Basis

5% (with no ITC) or 18% (with ITC) on whole value

of tour

Here, invoice will be issued by hotel in the name of tour operator and then tour operator will issue invoice in the

name of client

In case of 5% it shall be Inclusive of charges of accommodation and transportation

10.08.2017

Inbound Tour

Tour Operator

Foreign Service receiver

POS

55GMJ & Co for GPS

Tour Operator issues invoice for the whole

value of tour in the name of the foreign service

receiver

10.08.2017

Inbound Tour‐ IGST or CGST/SGST

Tour Operator

Foreign Service receiver56GMJ & Co for GPS

POS

Whether Tour

on the invoice?

Whether Tour operator will charge IGST or CGST/SGST on the invoice?

10.08.2017 GMJ & Co for GPS 57

Inbound Tour at Multiple Places

Tour Operator

Foreign Service receiver

POS Jaipur Delhi Agra

?

10.08.2017 GMJ & Co for GPS 58

Place of Supply if Supply is made in more than one State or Union Territory shall be Treated As Supply in each state

Value of Supply Specific to each State and Union Territory

Place of Tour

Amount Collected

POS

Jaipur Rs, 35,000 JaipurDelhi Rs. 30,000 DelhiAgra Rs. 35,000 Agra

Separately collected

As per the proportion of value

for services Separately collected

Or as per the Terms of Agreement or

Contract

Or as may be

Prescribed

The tour operator will issue separate invoice for all the 3 place of

supply

10.08.2017

Intermediary Services – Inbound Tour

Tour Operator 2

Foreign Service receiverForeign Tour Operator 1

POS

POS

59GMJ & Co for GPS

10.08.2017

Outbound Tour

Tour Operator

Indian Service receiver

POS60GMJ & Co for GPS

10.08.2017

Intermediary Services – Outbound Tour

Tour Operator

Foreign Tour Operator 1

POS

POS

61GMJ & Co for GPS

10.08.2017

Inbound Tour‐Intermediary

Tour Operator

Foreign Service receiver

POS

62GMJ & Co for GPS

Hotel/Transporter issues invoice in the name of the foreign service receiver

for the value of hotel/transport

POS

Tour Operator issues invoice only for its service fees in the name of the foreign service receiver

10.08.2017 GMJ & Co for GPS 63

Tour Operator 1

Indian Service receiver

Tour Operator 2

POS

POS

Tour on Principal Basis‐ In India

10.08.2017 GMJ & Co for GPS 64

Principal Basis – Outside India

Tour Operator 2

Foreign Service receiver

POS

Tour Operator 1

NO GST

10.08.2017

Exemption under Entry no. 54

Tour Operator

Foreign Service receiver

Tour Provided to a foreign tourist

NO GST

65GMJ & Co for GPS

Tour OperatorLocation of Service

ReceiverBookings POS

On CommissionIn taxable territory Domestic or

internationalbooking

India‐

Not in taxable territory IntermediaryOn Service Charges

In taxable territory Domestic India

Not in taxable territory Domestic(inbound) Performance

In taxable territory International(Outbound) India

Not in taxable territory International Exemption10.08.2017 GMJ & Co for GPS 66

10.08.2017 GMJ & Co for GPS 67

E‐commerce operator – Pure agent

PAYMENT

Payment after deducting upto 1% TCS (at present not applicable)

After the E-Commerce Operator Files the return Credit for the TCS deducted can be claimed

Tour Operator

Discloses details of hotel or airlines on the website

Airlines are not ready for

TCS deduction

10.08.2017 GMJ & Co for GPS 68

E‐commerce

Tour Operator

Buys from hotel for Rs. 1,00,000

Discloses details of hotel on the website

Sells to the customer for Rs. 1,50,000

No need to deduct

TCS

Where the tour operator sells its services through its website, he will not be termed as an

Electronic Commerce Operator

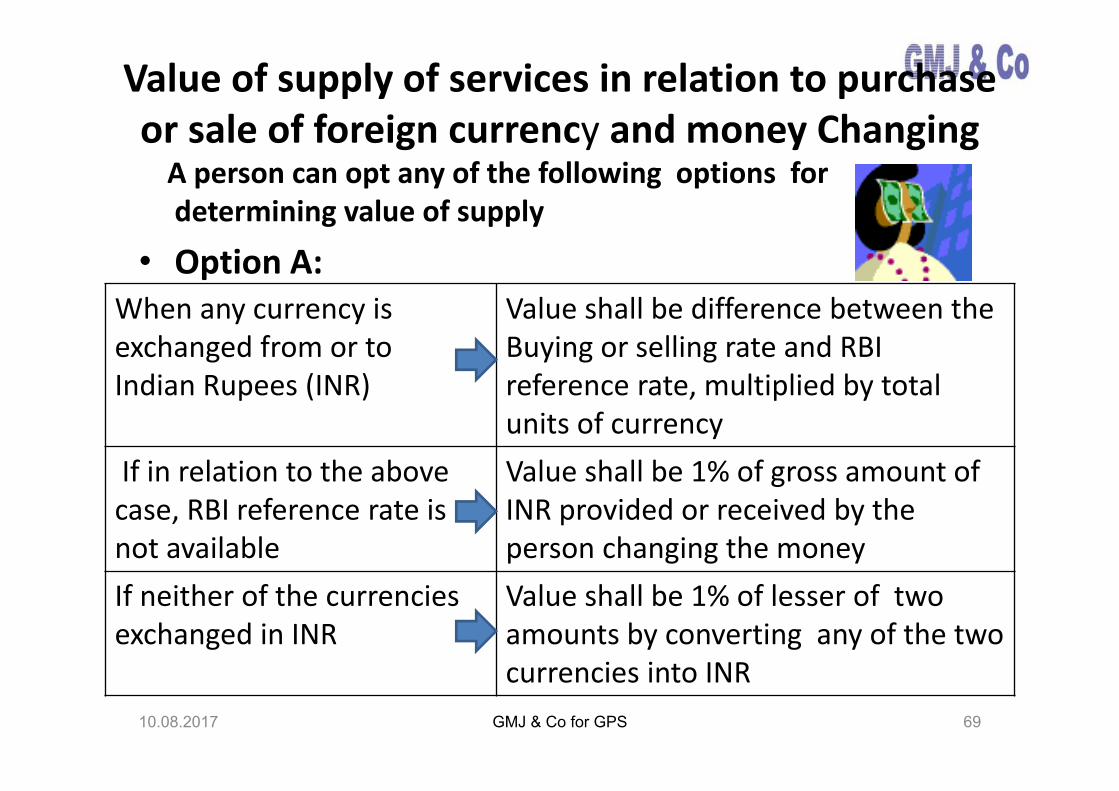

Value of supply of services in relation to purchase or sale of foreign currency and money ChangingA person can opt any of the following options for determining value of supply

• Option A:

10.08.2017

When any currency is exchanged from or to Indian Rupees (INR)

Value shall be difference between the Buying or selling rate and RBI reference rate, multiplied by total units of currency

If in relation to the above case, RBI reference rate is not available

Value shall be 1% of gross amount of INR provided or received by the person changing the money

If neither of the currencies exchanged in INR

Value shall be 1% of lesser of two amounts by converting any of the two currencies into INR

69GMJ & Co for GPS

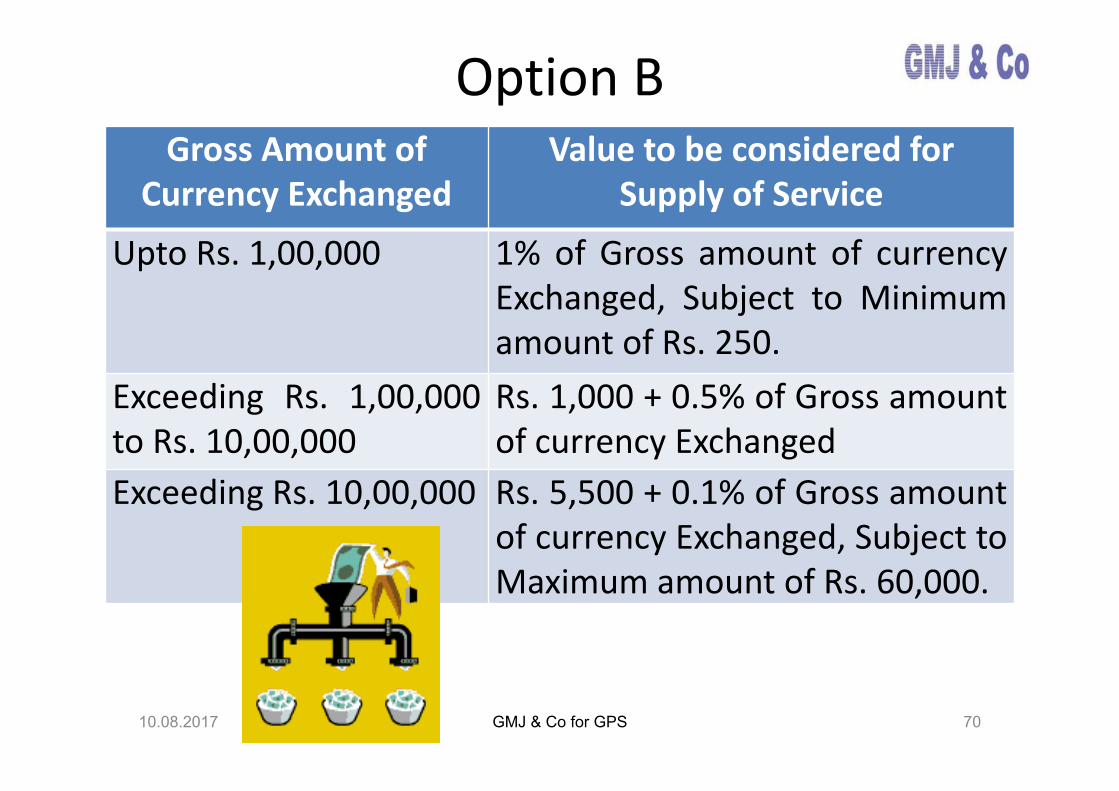

Option B

10.08.2017

Gross Amount of Currency Exchanged

Value to be considered for Supply of Service

Upto Rs. 1,00,000 1% of Gross amount of currencyExchanged, Subject to Minimumamount of Rs. 250.

Exceeding Rs. 1,00,000to Rs. 10,00,000

Rs. 1,000 + 0.5% of Gross amountof currency Exchanged

Exceeding Rs. 10,00,000 Rs. 5,500 + 0.1% of Gross amountof currency Exchanged, Subject toMaximum amount of Rs. 60,000.

70GMJ & Co for GPS

INPUT TAX CREDIT

10.08.2017 71GMJ & Co for GPS

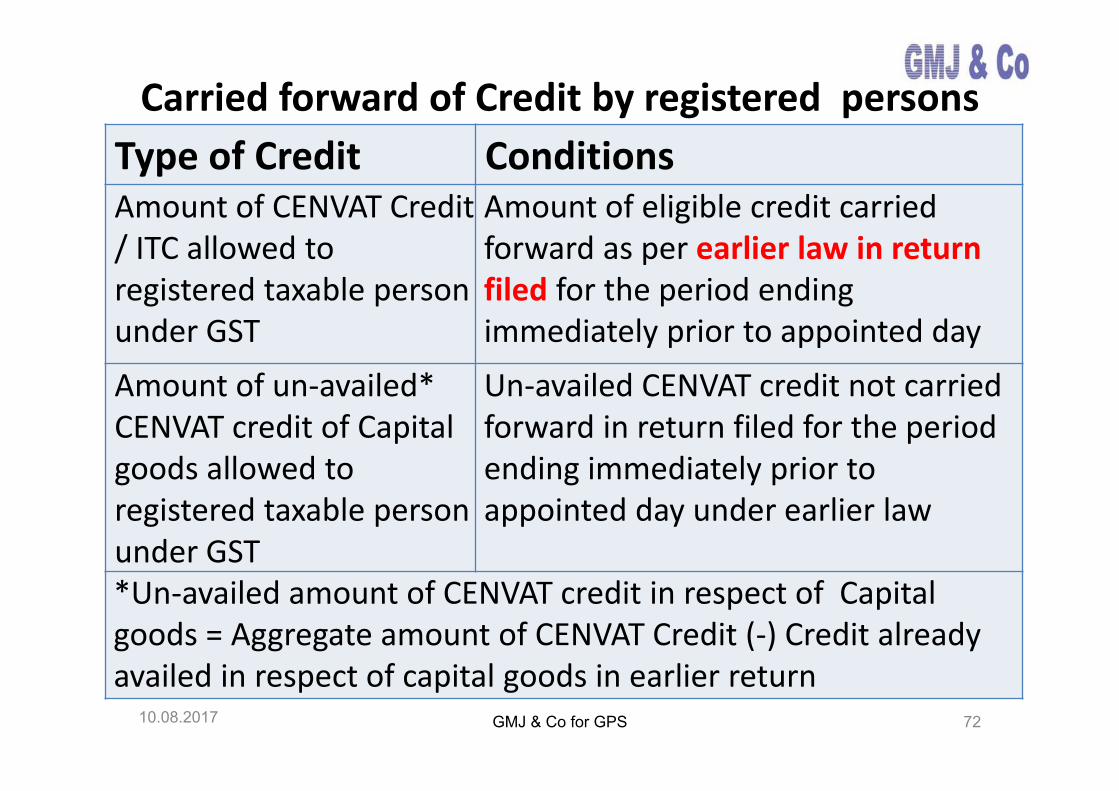

Carried forward of Credit by registered personsType of Credit Conditions Amount of CENVAT Credit / ITC allowed to registered taxable person under GST

Amount of eligible credit carried forward as per earlier law in return filed for the period ending immediately prior to appointed day

Amount of un‐availed* CENVAT credit of Capital goods allowed to registered taxable person under GST

Un‐availed CENVAT credit not carried forward in return filed for the period ending immediately prior to appointed day under earlier law

*Un‐availed amount of CENVAT credit in respect of Capital goods = Aggregate amount of CENVAT Credit (‐) Credit already availed in respect of capital goods in earlier return

10.08.2017 GMJ & Co for GPS 72

Possession of a tax invoice, etc., issued by a supplier registered under GST

Received the goods and/or services

The tax charged in respect of such supply has been actually paid to the credit of the appropriate Government,

Furnished the return under section 39

10.08.2017

When is ITC available 16(2)

Time of Supply

GMJ & Co for GPS 73

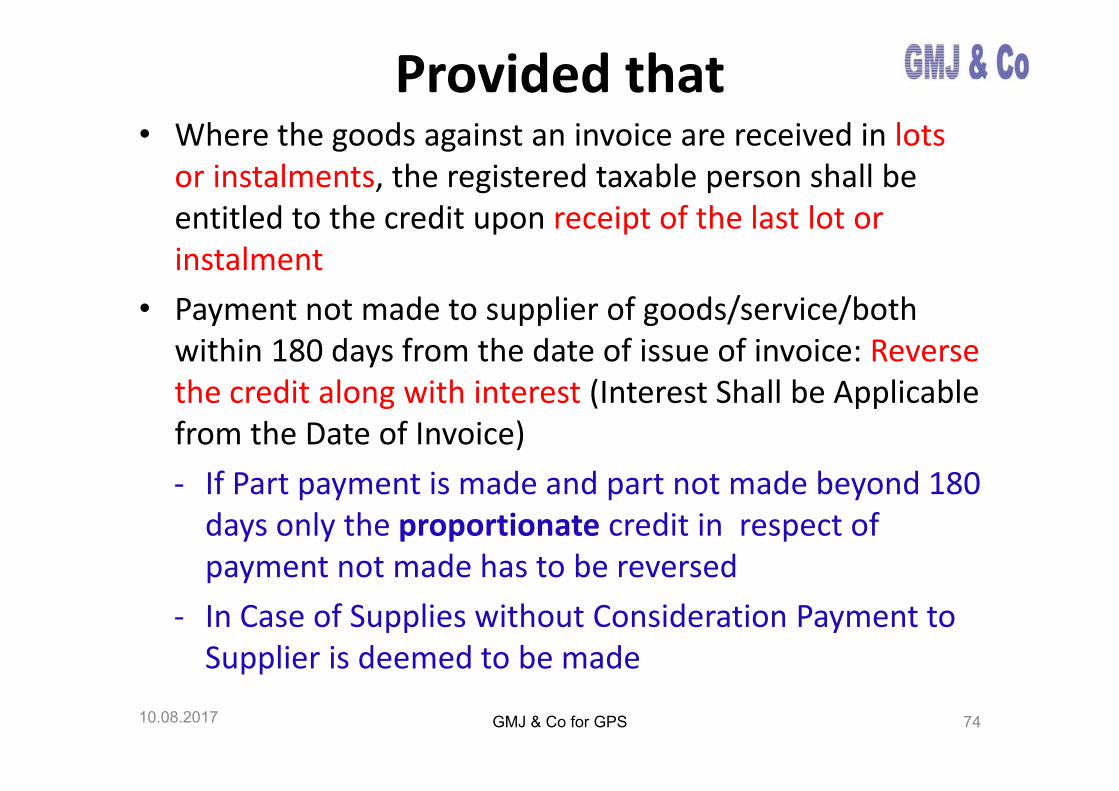

Provided that• Where the goods against an invoice are received in lots

or instalments, the registered taxable person shall be entitled to the credit upon receipt of the last lot or instalment

• Payment not made to supplier of goods/service/both within 180 days from the date of issue of invoice: Reverse the credit along with interest (Interest Shall be Applicable from the Date of Invoice)‐ If Part payment is made and part not made beyond 180 days only the proportionate credit in respect of payment not made has to be reversed

‐ In Case of Supplies without Consideration Payment to Supplier is deemed to be made

10.08.2017 GMJ & Co for GPS 74

Credit not allowed 17(5)• motor vehicles and other conveyances

• except when they are used for making the following taxable supplies, namelyfurther supply of such vehicles or conveyancestransportation of passengers/goodsimparting training on driving, flying, navigating such vehicles or conveyances

10.08.2017 GMJ & Co for GPS 75

Credit not allowed 17(5)

10.08.2017 76

Travel benefitstravel benefits extended to employees on vacation such as leave or home

travel concession

Allowed only if mandatory as per law /Allowed only for outward supply of same category or as element of composite/mixed supply

rent‐a‐cab, life insurance, health insurance

Membership of

club, health and fitness centre

Allowed only for outward supply of same category or as element of composite/mixed supply

food and beverages, outdoor catering, beauty treatment, health services, cosmetic and plastic surgery

GMJ & Co for GPS

Credit not allowed 17(5)• Works contract services when supplied for construction of

immovable property, other than plant and machinery, except where it is an input service for further supply of works contract service;

• Goods or services received by a taxable person for construction of an immovable property on his own account, other than plant and machinery,

• Construction includes to the extent of capitalization• Tax paid under Composition• Goods or services or both received by a non‐resident taxable

person except on goods imported by him

10.08.2017 GMJ & Co for GPS 77

Credit not allowed• Tax paid under Composition• Used for personal consumption• Goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples

• ITC wrongly availed or utilised by reason of fraud etc.

• Detention, seizure and release of goods and conveyances in transit

• Confiscation of goods and/or conveyances10.08.2017 78GMJ & Co for GPS

HSN codes

10.08.2017 GMJ & Co for GPS 79

Chapter Heading Description of Service

Heading 9966 Renting of motorcab where the cost of fuel is included inthe consideration charged from the service recipient.Rental services of transport vehicles with or withoutoperators, other than above

Heading 9985 Supply of tour operators services Explanation‐ "tour operator" means any person engaged in the business of planning, scheduling, organizing, arranging tours (which may include arrangements for accommodation, sightseeing or other similar services) by any mode of transport, and includes any person engaged in the business of operating tours.

Support services other than above (Commission, fees received for hotel booking, ATA, visa fees shall be included here)

10.08.2017

Rates

Specific services

Transport of

passengers by air, rail and road

Renting of hotels, inns, guest houses, clubs, campsites or other commercial places meant for residential or lodging purposes

Admission to events/ monuments

Tour operator services

5%NO ITC on the value of Accommodation and

transportation

18% With Full ITC

For Other services

18% with Full ITC available

80GMJ & Co for GPS

Major Expenses and Their Credit Available to Tour Operators

10.08.2017

Air Tickets

Credit Will not be

available if the Invoice will be in the name of the Passenger

Rent A Cab Service

Credit Available

Hotel Accommodation / Admission

81GMJ & Co for GPS

Tour Operator

10.08.2017 GMJ & Co for GPS 82

Place of Supply Location of Hotel – NO ITC

CustomerState C

Place of SupplyLocation of Customer

State A

State B

State AState BState A

CustomerState C

Place of Supply Location of HotelITC available to State A operator

Place of SupplyState B

Place of SupplyLocation of Customer

10.08.2017 GMJ & Co for GPS 83

Exemptions• Services by a specified organisation in respect of a religious pilgrimage

facilitated by the MoEA, under bilateral arrangement• Transport of passengers, with or without accompanied belongings, by - air,

embarking from or terminating in an airport located in North Eastern states.• Transport of passengers, with or without accompanied belongings, by -non-

air conditioned contract carriage other than radio taxi excluding tourism,conducted tour, charter or hire.

• Transport of passengers, with or without accompanied belongings, by Stagecarriage other than air-conditioned stage carriage

• Services by way of admission to a museum, national park, wildlife sanctuary,tiger reserve or zoo.

• Service of transportation of passengers, with or without accompaniedbelongings, by Railway(other than first class or an air-conditioned coach),metro, monorail, tramway, inland waterways, public transport other than fortourism purpose, metered cabs or auto rickshaws.

• Services by a hotel, inn, guest house, club or campsite, by whatever namecalled, for residential or lodging purposes, having declared tariff of a unit ofaccommodation less than one thousand rupees per day or equivalent

GST

10.08.2017 84

What we thought What we received

GMJ & Co for GPS

DISCLAIMER• The discussions and interpretations set forth in this material are based on the GST laws prevailing as of the date of this material. If there is a change, including a change having a retrospective effect, in the statutory laws, the discussions and comments expressed in this material would necessarily have to be re‐evaluated in light of the changes. We do not have responsibility of updating this note.

• This material is giving only general guidelines covering general situations our answer may differ on specific situation. Before taking any decision the users are required to obtain the opinion of the firm. Neither the firm nor any partner/employee is responsible for any action taken on the basis of this material.

• This material is not binding and acceptance of it including any subsequent and resultant planning or action will be at their own sole discretion and risk, without recourse.

• This material and comments mentioned there in are based on our understanding and interpretation of the legislations, and are not binding on any regulators, court and there can be no assurance that the regulators or court will not take a position, contrary to our opinion and comments.

• This material is the Copyright of GMJ.

10.08.2017 GMJ & Co for GPS 85

CA Manish [email protected]

Ph : +91 22 61919200

Information contained herein is of ageneral nature and is not intended toaddress the circumstances of anyparticular individual or entity. Although weendeavor to provide accurate and timelyinformation, there can be no guaranteethat such information is accurate as of thedate it is received or that it will continue tobe accurate in the future. No one shouldact on such information withoutappropriate professional advice after athorough examination of particularsituation.

GMJ & Co for GPS 8610.08.2017

10.08.2017 GMJ & Co for GPS 87

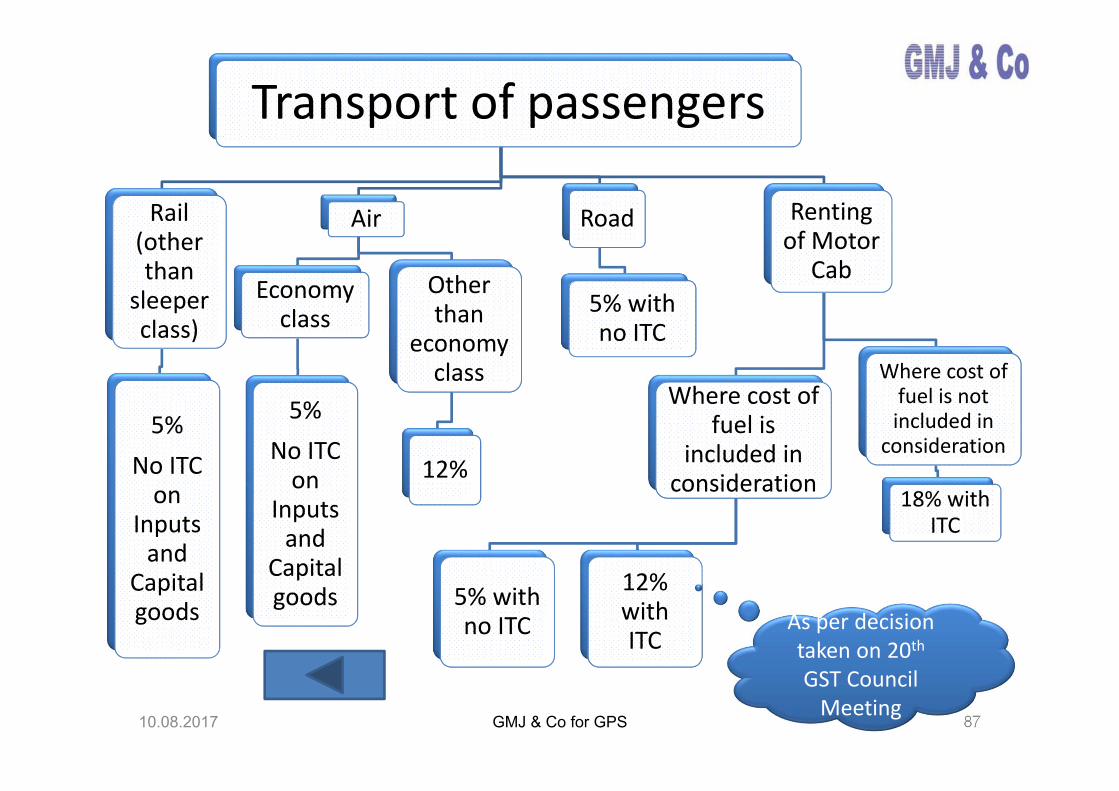

Transport of passengersTransport of passengers

Rail (other than

sleeper class)

Rail (other than

sleeper class)

5%No ITC on

Inputs and

Capital goods

5%No ITC on

Inputs and

Capital goods

AirAir

Economy class

Economy class

5%No ITC on

Inputs and

Capital goods

5%No ITC on

Inputs and

Capital goods

Other than

economy class

Other than

economy class

12%12%

RoadRoad

5% with no ITC5% with no ITC

Renting of Motor

Cab

Renting of Motor

Cab

Where cost of fuel is

included in consideration

Where cost of fuel is

included in consideration

5% with no ITC5% with no ITC

12% with ITC

12% with ITC

Where cost of fuel is not included in

consideration

Where cost of fuel is not included in

consideration

18% with ITC

18% with ITC

As per decision taken on 20thGST Council Meeting

10.08.2017 GMJ & Co for GPS 88

Renting

Declared Tariff>=Rs.1000<Rs.2500 per room per day

12%

Declared Tariff>=Rs.2500<Rs.7500 per room per day

18%

Declared Tariff>=Rs.7500 per room per day

28%

10.08.2017 GMJ & Co for GPS 89

Admission to events/ monuments

admission or access to circus, Indian classical dance

including folk

dance, theatrical performa

nce, drama.

18%

Entertainment events or access to

amusement facilities including

exhibition of cinematograph films, theme

parks, water parks, joy rides, merry‐go rounds, go‐carting,

casinos, race‐course, ballet, any sporting event such as Indian Premier League and the like

28%

Services provided by a race

club by way of

totalisatoror a license

to bookmaker in such club or

Gambling

28%

Admission to

planetarium

18%

Recreational, cultural

and sporting services not covered elsewhere

18%

exhibition of cinematograph films

where price of admission ticket is one hundred rupees or

less.

18% As per decision taken on 20thGST Council Meeting