isu ccee ce 203 eea chap 3 interest and equivalence

TRANSCRIPT

ISU CCEE

CE 203CE 203 EEA Chap 3EEA Chap 3

Interest and EquivalenceInterest and Equivalence

ISU CCEE

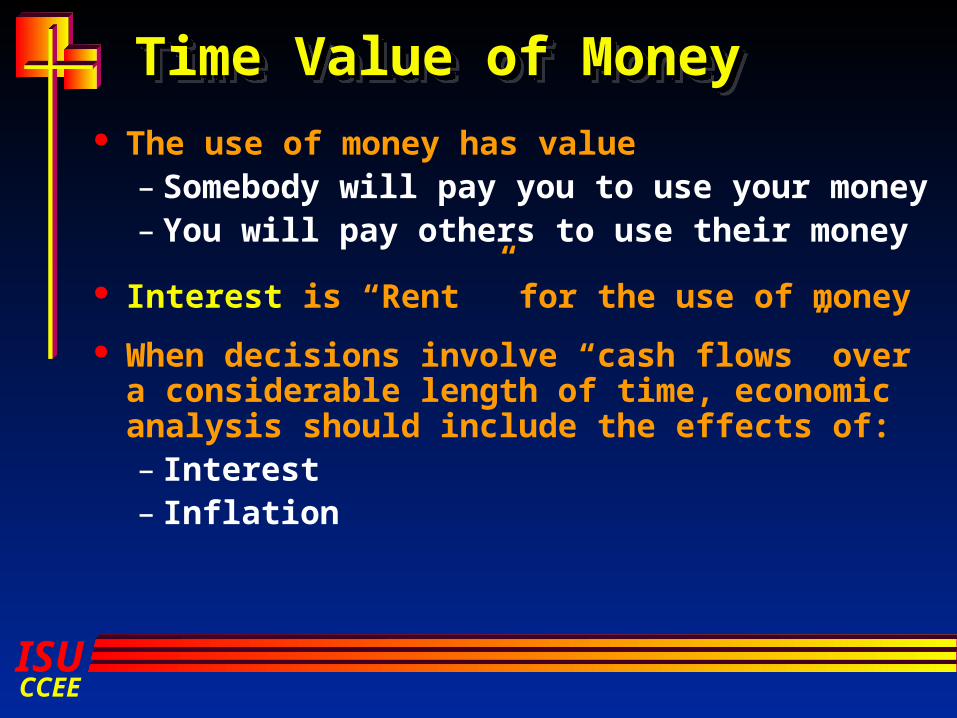

The use of money has value – Somebody will pay you to use your money– You will pay others to use their money

Interest is “Rent ” for the use of money

When decisions involve “cash flows” over a considerable length of time, economic analysis should include the effects of:– Interest– Inflation

Time Value of MoneyTime Value of MoneyTime Value of MoneyTime Value of Money

ISU CCEE

$1000 in savings account at 10% for 1 year?

$1000 per year for 30 years at 10%?

For typical “investment plan”, $1000 per year for 30 years at 10% yields $164,494

(see formula for “sinking fund”)

Pre-Course EEA Pre-Course EEA AssessmentAssessmentPre-Course EEA Pre-Course EEA AssessmentAssessment

ISU CCEE

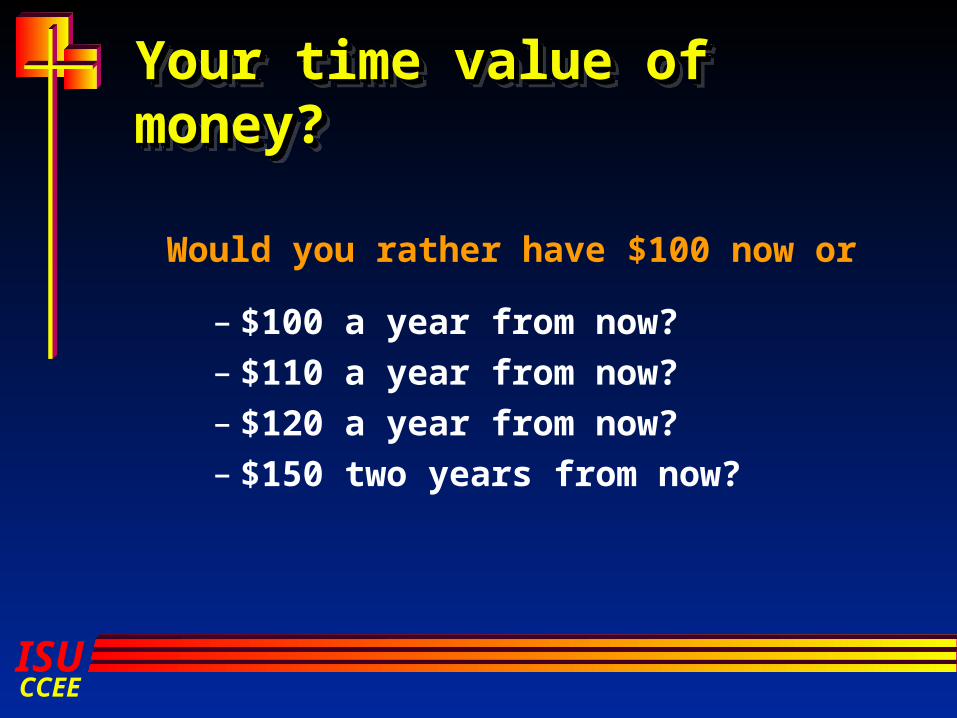

Would you rather have $100 now or

– $100 a year from now?– $110 a year from now?– $120 a year from now?– $150 two years from now?

Your time value of Your time value of money?money?Your time value of Your time value of money?money?

ISU CCEE

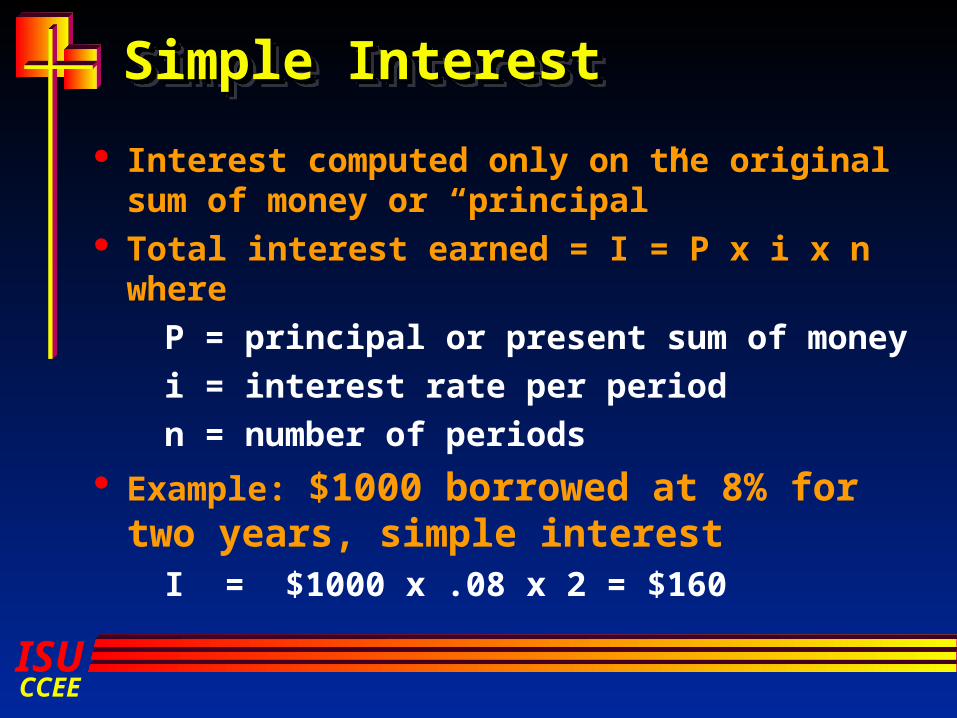

Interest computed only on the original sum of money or “principal”

Total interest earned = I = P x i x n where

P = principal or present sum of money

i = interest rate per period

n = number of periods Example: $1000 borrowed at 8% for two

years, simple interestI = $1000 x .08 x 2 = $160

Simple InterestSimple InterestSimple InterestSimple Interest

ISU CCEE

F = P + P x in = P (1 + in) = P [1 +i(period)]

Example: $1000 borrowed at 8% for five years, simple interest

F = $1000 (1 + .08(5)) = $1400

Simple InterestSimple InterestFuture Value, F, of a Loan, PFuture Value, F, of a Loan, P Simple InterestSimple InterestFuture Value, F, of a Loan, PFuture Value, F, of a Loan, P

ISU CCEE

Compound InterestCompound Interest Compound InterestCompound InterestInterest on original sum + on interest

Example $1000 @ 10% per year, F

F1 (first year) = $1000 + $1000(0.1)or $1000 (1 + 0.1) = $1100

F2 (second year) = $1100 + $1100(0.1)or $1000(1+0.1)(1+0.1) = $1210or $1000(1+0.1)2

F3 = $1000(1+0.1)3;

Fn = $1000(1+0.1)n

General: Fn = P(1+i)n

ISU CCEE

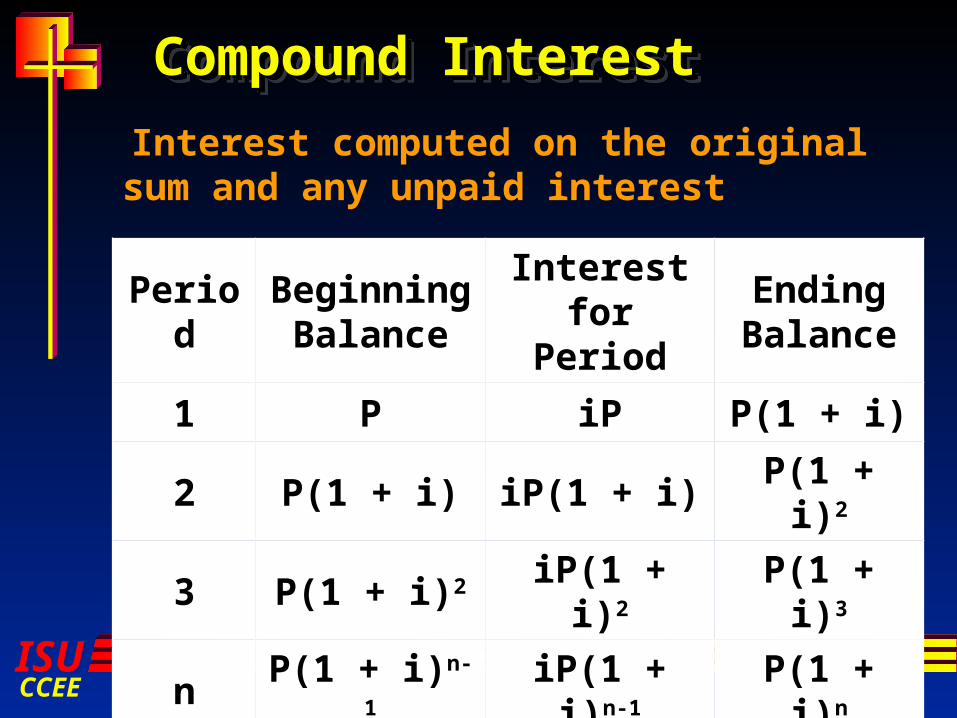

Interest computed on the original sum and any unpaid interest

Compound InterestCompound InterestCompound InterestCompound Interest

Period

Beginning Balance

Interest for Period

Ending Balance

1 P iP P(1 + i)

2 P(1 + i) iP(1 + i) P(1 + i)2

3 P(1 + i)2 iP(1 + i)2 P(1 + i)3

n P(1 + i)n-1 iP(1 + i)n-1 P(1 + i)n

ISU CCEE

Future Value, F, = P (1 + i)n

– P = principal or present sum of money– i = interest rate per period– n = number of periods (years, months, …)

Example: $1000 borrowed at 8% for five years, compound interest, all of principal and interest repaid in 5 years:

F = $1000 (1 +.08)5 = $1469.33F = P (F/P, i, n) = $1000 (F/P, .08, 5) = $1469.00 (see EEA p. 576)

Compound InterestCompound InterestCompound InterestCompound Interest

Note: Simple interestyield would be $1400

ISU CCEE

Total interest earned = In = P (1 + i)n - P

P = principal or present sum of money

i = interest rate

n = number of periods

Example: $1000 borrowed at 8% for five years, compound interest

I = $1000 (1 +.08)5 - $1000 = $469.33

Compound InterestCompound InterestCompound InterestCompound Interest

ISU CCEE

Future value, F, for P = $1000 at 8%

Simple vs. Compound Simple vs. Compound InterestInterestSimple vs. Compound Simple vs. Compound InterestInterest

Periods

F/P, simple i F/P, compound i

1 $1080 $1080

2 $1160 $1166

3 $1240 $1260

4 $1320 $1360

5 $1400 $1469

10 $1800 $2159

15 $2200 $3172

20 $2600 $4661

ISU CCEE

Specification of Interest Specification of Interest Rate, iRate, iSpecification of Interest Specification of Interest Rate, iRate, i1) “8%” - assumed to mean per year and

compounded annually

2) “8% compounded quarterly” - 2% per each 3 months, compounded every 3 months

3) “8% compounded monthly” – 2/3% each month, compounded every month

4) “8%” = .08 in equations NB1000

ISU CCEE

In-class ExampleIn-class ExampleIn-class ExampleIn-class Example

Would you rather have $5000 today or $35,000 in 25 years if the interest rate was 8% compounded yearly/ monthly…

1) yearly?

F = P(F/P, .08, 25) = 5000 (6.848) = $34, 240

2) monthly?

F = P (F/P, .006667, 300) = $36,700

ISU CCEE

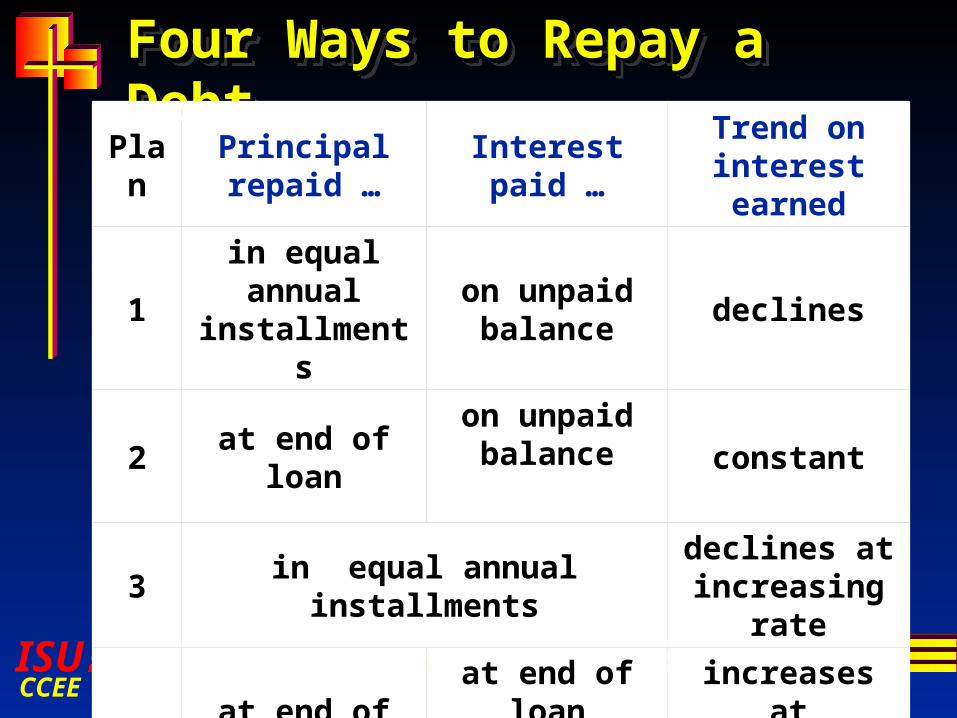

Four Ways to Repay a Four Ways to Repay a DebtDebtFour Ways to Repay a Four Ways to Repay a DebtDebt

Plan

Principal repaid …

Interest paid …

Trend on interest earned

1in equal annual

installments

on unpaid balance

declines

2at end of

loan

on unpaid balance constant

3in equal annual

installments

declines at increasing

rate

4at end of

loan

at end of loan

(compounded)

increases at increasing

rate

ISU CCEE

Loan Repayment Plan 1 Loan Repayment Plan 1 ($5000, 5 ($5000, 5 years, 8%)years, 8%)Loan Repayment Plan 1 Loan Repayment Plan 1 ($5000, 5 ($5000, 5 years, 8%)years, 8%)

Year

Owed at

begin-ning

Annual Interes

t

Total owed at end

Principal Paid

Total pay-ment

1 $5000 $400 $5400 $1000 $1400

2 $4000 $320 $4320 $1000 $1320

3 $3000 $240 $3240 $1000 $1240

4 $2000 $160 $2160 $1000 $1160

5 $1000 $80 $1080 $1000 $1080

$1200 $5000 $6200Bank loans with yearly payments: Principal

repaid in equal installments

ISU CCEE

Loan Repayment Plan 2 Loan Repayment Plan 2 ($5000, 5 ($5000, 5 years, 8%)years, 8%)Loan Repayment Plan 2 Loan Repayment Plan 2 ($5000, 5 ($5000, 5 years, 8%)years, 8%)

Year

Owed at

begin-ning

Annual Interes

t

Total owed at end

Princi-pal

Paid

Total pay-ment

1 $5000 $400 $5400 $0 $400

2 $5000 $400 $5400 $0 $400

3 $5000 $400 $ 5400 $0 $400

4 $5000 $400 $ 5400 $0 $400

5 $5000 $400 $ 5400 $5000 $5400

$2000 $5000 $7000Interest only loans:

used in bonds and international loans

ISU CCEE

Loan Repayment Plan 3 Loan Repayment Plan 3 ($5000, 5 ($5000, 5 years, 8%)years, 8%)Loan Repayment Plan 3 Loan Repayment Plan 3 ($5000, 5 ($5000, 5 years, 8%)years, 8%)

Year

Owed at

begin-ning

Annual Interes

t

Total owed at end

Princi-pal

Paid

Total pay-ment

1 $5000 $400 $5400 $852 $1252

2 $4148 $331 $4479 $921 $1252

3 $3227 $258 $ 3485 $994 $1252

4 $2233 $178 $ 2411 $1074 $1252

5 $1159 $93 $ 1252 $1159 $1252

$2000 $5000 $6260Equal annual installments:

Auto/home loans (but usually monthly payments)

ISU CCEE

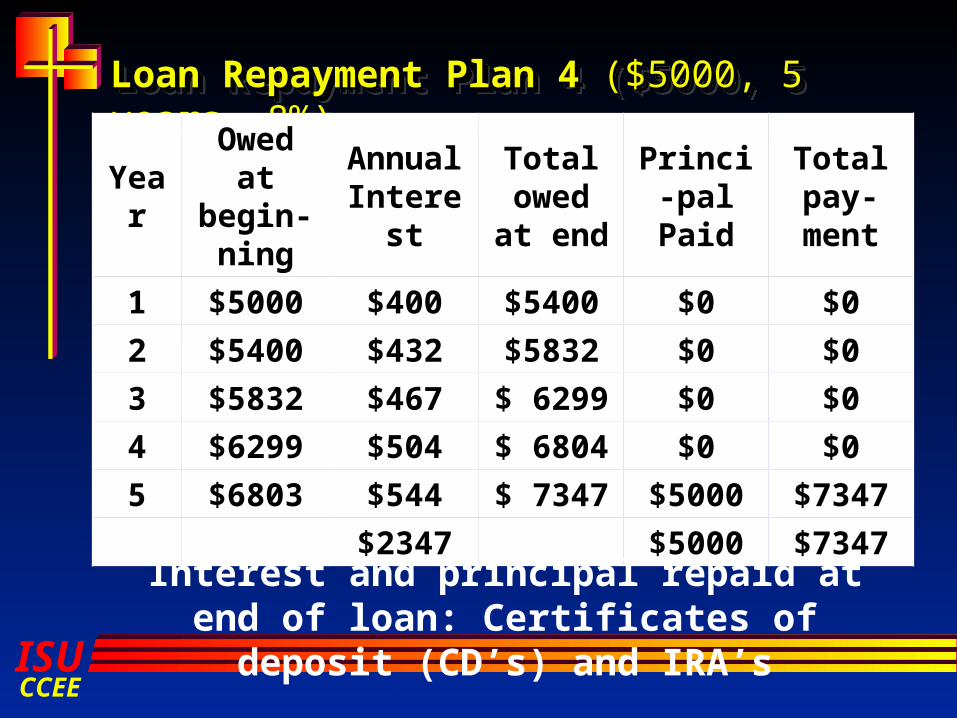

Loan Repayment Plan 4 Loan Repayment Plan 4 ($5000, 5 ($5000, 5 years, 8%)years, 8%)Loan Repayment Plan 4 Loan Repayment Plan 4 ($5000, 5 ($5000, 5 years, 8%)years, 8%)

Year

Owed at

begin-ning

Annual Interes

t

Total owed at end

Princi-pal

Paid

Total pay-ment

1 $5000 $400 $5400 $0 $0

2 $5400 $432 $5832 $0 $0

3 $5832 $467 $ 6299 $0 $0

4 $6299 $504 $ 6804 $0 $0

5 $6803 $544 $ 7347 $5000 $7347

$2347 $5000 $7347Interest and principal repaid at end of loan:

Certificates of deposit (CD’s) and IRA’s

ISU CCEE

Loan repayment plans 1-4Loan repayment plans 1-4Loan repayment plans 1-4Loan repayment plans 1-4

Are all equivalent to $5000 now in terms of time value of money,

May not be equally attractive to loaner or borrower

Have different cash flow diagrams “Equivalent in nature but different in

structure”

ISU CCEE

The present sum of money is equivalent to the future sum(s) (from our perspective), if..

..we are indifferent as to whether we have a quantity of money now or the assurance of some sum (or series of sums) of money in the future (with adequate compensation)

EquivalenceEquivalenceEquivalenceEquivalence

ISU CCEE

Used to make a meaningful engineering economic analysis

Apply by finding equivalent value at a common time for all alternatives– value now or “Present Worth”– value at some logical future time or

“Future Worth” Assume the same time value of money

(interest rate) for all alternatives

EquivalenceEquivalenceEquivalenceEquivalence

ISU CCEE

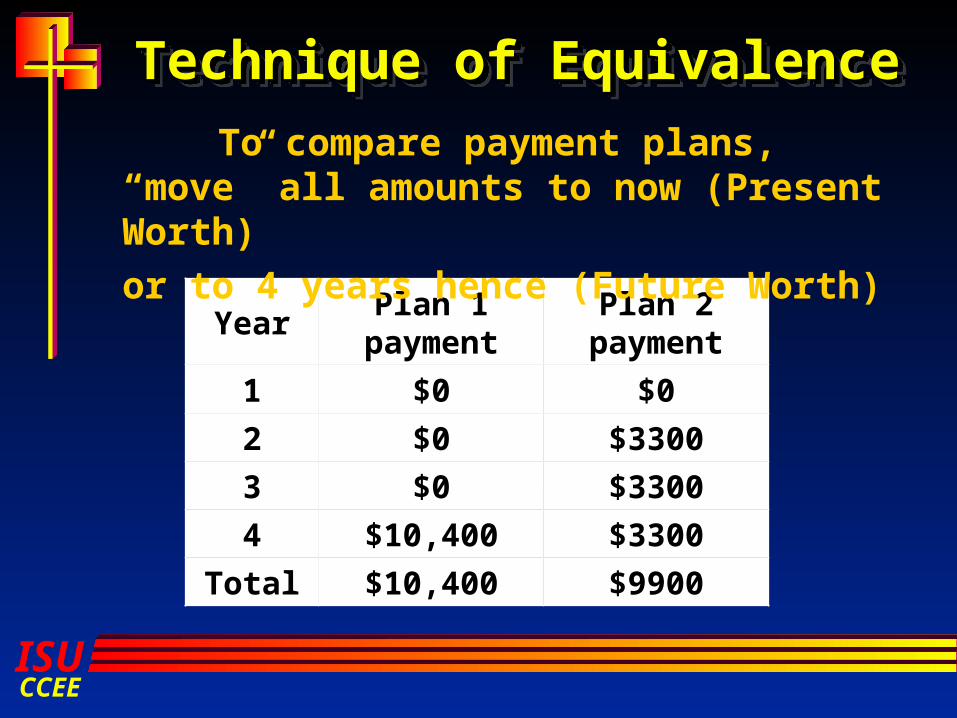

You borrow $8000 to help pay for You borrow $8000 to help pay for senior year at ISU – the bank offers senior year at ISU – the bank offers you two repayment plans for paying you two repayment plans for paying off the loan in four years:off the loan in four years:

You borrow $8000 to help pay for You borrow $8000 to help pay for senior year at ISU – the bank offers senior year at ISU – the bank offers you two repayment plans for paying you two repayment plans for paying off the loan in four years:off the loan in four years:

YearPlan 1

paymentPlan 2

payment

1 $0 $0

2 $0 $3300

3 $0 $3300

4 $10,400 $3300

Total $10,400 $9900

Which would you choose?

ISU CCEE

“Technique of Equivalence” requires that we

1)Determine our “time value of money”2)Determine a single equivalent value at a

selected time for Plan 13) Determine a single equivalent value at

the same selected time for Plan 24) Compare the two values

Comparing Economic Comparing Economic AlternativesAlternativesComparing Economic Comparing Economic AlternativesAlternatives

ISU CCEE

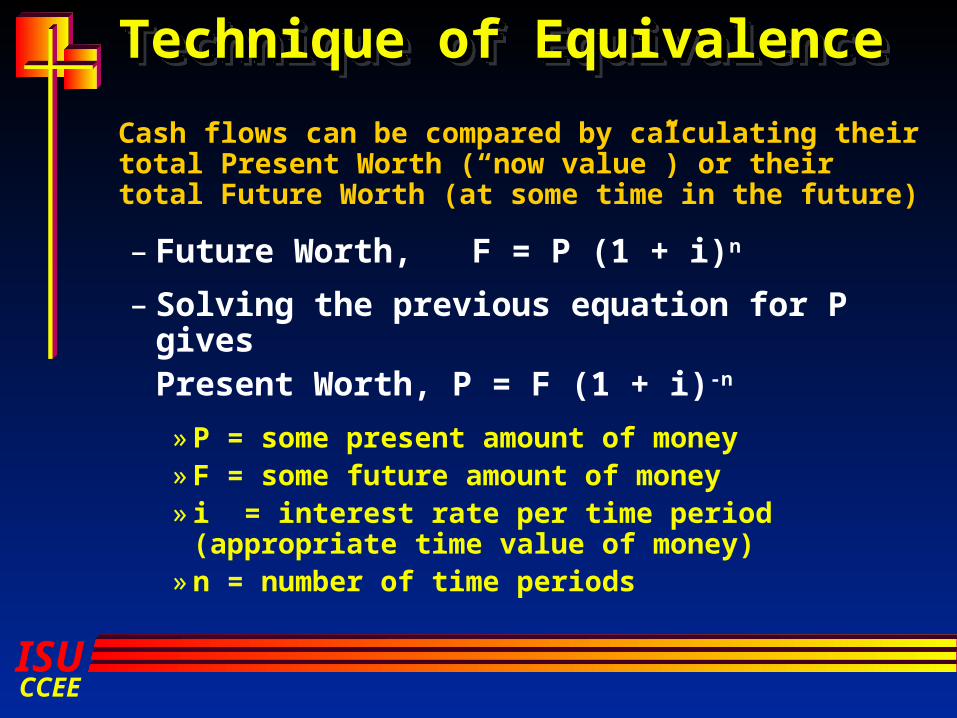

Cash flows can be compared by calculating their total Present Worth (“now value”) or their total Future Worth (at some time in the future)

– Future Worth, F = P (1 + i)n

– Solving the previous equation for P gives Present Worth, P = F (1 + i)-n

» P = some present amount of money» F = some future amount of money» i = interest rate per time period

(appropriate time value of money)» n = number of time periods

Technique of EquivalenceTechnique of EquivalenceTechnique of EquivalenceTechnique of Equivalence

ISU CCEE

Technique of EquivalenceTechnique of EquivalenceTechnique of EquivalenceTechnique of Equivalence

YearPlan 1

paymentPlan 2

payment

1 $0 $0

2 $0 $3300

3 $0 $3300

4 $10,400 $3300

Total $10,400 $9900

To compare payment plans, “move” all amounts to now (Present Worth)

or to 4 years hence (Future Worth)

ISU CCEE

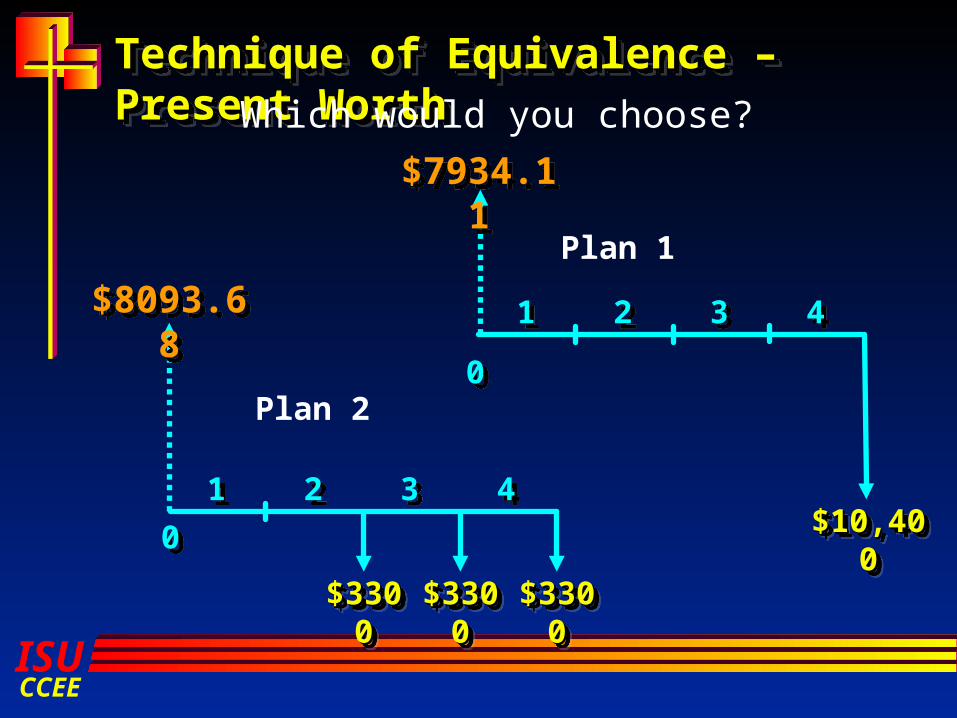

Technique of Equivalence – Technique of Equivalence – Present WorthPresent WorthTechnique of Equivalence – Technique of Equivalence – Present WorthPresent WorthAssume our “time value of money” is 7% APR

00

11 22 33 44

P4 = 10,400(1 + .07)-4 = 7,934.11

Total PW = $7,934.11

Or P = $10,400 (P/F, .07, 4) = .7629 (10,400) = $7934.16

$10,4$10,40000

$10,4$10,40000

Present Worth:Payment Plan 1

P = F(1 + i)-n

PW?PW?

ISU CCEE

Technique of Equivalence – Technique of Equivalence – Present WorthPresent WorthTechnique of Equivalence – Technique of Equivalence – Present WorthPresent WorthAssume our “time

value of money” is 7% APR

0011 22 33 44

$330$33000

$330$33000P2 = 3300(1 + .07)-2 = 2882.35

P3 = 3300(1 + .07)-3 = 2693.78P4 = 3300(1 + .07)-4 = 2517.55Total PW = $8093.68

$330$33000

$330$33000

$330$33000

$330$33000

PW?PW?

Present Worth:Payment Plan 1

P = F(1 + i)-n

ISU CCEE

Technique of Equivalence – Technique of Equivalence – Present WorthPresent WorthTechnique of Equivalence – Technique of Equivalence – Present WorthPresent WorthWhich would you choose?

0011 22 33 44

$330$33000

$330$33000

$330$33000

$330$33000

$330$33000

$330$33000

$8093.68$8093.68

00

11 22 33 44

$10,4$10,40000

$10,4$10,40000

$7934.11$7934.11

Plan 2

Plan 1

ISU CCEE

Technique of Equivalence – Future Technique of Equivalence – Future WorthWorthTechnique of Equivalence – Future Technique of Equivalence – Future WorthWorthAssume our “time value of money” is 7% APR

00

11 22 33 44

F4 = 10,400(1 + .07)0 = 10,400

Total FW = $10,400.00$10,4$10,4

0000$10,4$10,4

0000

Future Worth:Payment Plan 1

F = P(1 + i)n

ISU CCEE

Technique of Equivalence – Technique of Equivalence – Future WorthFuture WorthTechnique of Equivalence – Technique of Equivalence – Future WorthFuture WorthAssume our “time value of money” is 7% APR

0011 22 33 44

$330$33000

$330$33000

F2 = 3300(1 + .07)2 = 3778.17F3 = 3300(1 + .07)1 = 3531.00F4 = 3300(1 + .07)0 = 3300.00Total FW = $10609.17

Again, larger than Plan 1

$330$33000

$330$33000

$330$33000

$330$33000

Future Worth:Payment Plan 2

P = F(1 + i)-n

FW?FW?

ISU CCEE

In-class ExampleIn-class ExampleIn-class ExampleIn-class Example

You deposit $3000 in an account that earns 5%, compounded daily.

How much could you withdraw from the account at the end of two years?

F = 3000 (F/P, .05/365, 730) = $3,315.49

How much could you withdraw if the compounding were monthly?

F = 3000 (F/P, .05/12, 24) = $3,314.82

ISU CCEE

In-class ExampleIn-class ExampleIn-class ExampleIn-class Example

You are considering two designs for a wastewater treatment facility.

Plan 1: Costs $1,700,000 to construct and will have to be replaced every 20 years.

Plan 2: Costs $2,100,000 to construct and will have to be replaced every 30 years.

Which is the better of the two designs?

Assume 7% APR and neglect inflation and operating, maintenance and disposal costs.

Sketch CFD’s for each plan and compare.

ISU CCEE

How to compare two How to compare two schemes with different livesschemes with different livesHow to compare two How to compare two schemes with different livesschemes with different lives

One plant lasts 20y and the other 30y Could we make a comparison over 20y? Could we make a comparison over 30y? What would be a decent period over

which to compare?The smallest common denominator,

i.e. in this case 60y.

ISU CCEE

Technique of Equivalence – Technique of Equivalence – Present WorthPresent WorthTechnique of Equivalence – Technique of Equivalence – Present WorthPresent WorthBased on dollars only, which is the better plan?

00

1010

$1.7 $1.7 MM

$1.7 $1.7 MM

$2.254 M (if provision is made for final replacement, $ 2.283M)$2.254 M (if provision is made for final replacement, $ 2.283M)

Plan 12020

3030

4040

5050

6060

$1.7 $1.7 MM

$1.7 $1.7 MM

$1.7 $1.7 MM

$1.7 $1.7 MM

repeats

repeats

P = $ 1.7 + $ 1.7 (1.07)-20 + $ 1.7 (1.07)-40 [ + $ 1.7 (1.07)-60]*

[$1.7 M]*[$1.7 M]*[$1.7 M]*[$1.7 M]*

•This term will only apply when it is a requirement to replace at the end, not normally and it has been excluded from this analysis. You could get to 60 years without a final replacement.

ISU CCEE

Technique of Equivalence – Technique of Equivalence – Present WorthPresent WorthTechnique of Equivalence – Technique of Equivalence – Present WorthPresent WorthBased on dollars only, which is the better plan?

00

1010

$2.1 $2.1 MM

$2.1 $2.1 MM

$2.376 M$2.376 M

Plan 2

2020 3030 4040 5050 6060

$2.1 $2.1 MM

$2.1 $2.1 MM

repeats

repeats

Other option was $2.254 M

Not Not requiredrequired

Not Not requiredrequired

= P = 2.1 + 2.1(1.07)-30 + the 60y replacement, which does not apply