issue 2/2009 highlights - nda.agric.za globefi sh highlights july 2009 shrimp wholesale prices...

TRANSCRIPT

HIGHLIGHTSA quarterly update based on the GLOBEFISH databank

Shrimp markets very slowThe economic crisis continues to influence the world shrimp market. Generally, because of their relatively high price, sales of shrimp products suffer

because of loss of purchasing power.shrimp prices are low at the moment. p. 1

Prices moving upStarting in mid May 2009 tuna prices in all major catching areas began to rise because of fears that upcoming tuna fishing bans in these areas will

squeeze global supply for the canning industry. p. 7

Economic crisis overshadows groundfish marketPrices of all groundfish species declined sharply in the first half of 2009. The main reason was less buying interest by

institutional clients. In addition, cheap cultured fish create strong competition in the market. p. 12

Economic crisis impacts cephalopod marketThe world squid market is in a very difficult situation. Supply is sharply down in the Southwest Atlantic,

which normally would lead to a substantial price hike, especially after the extremely low prices of the previous two years. p. 15

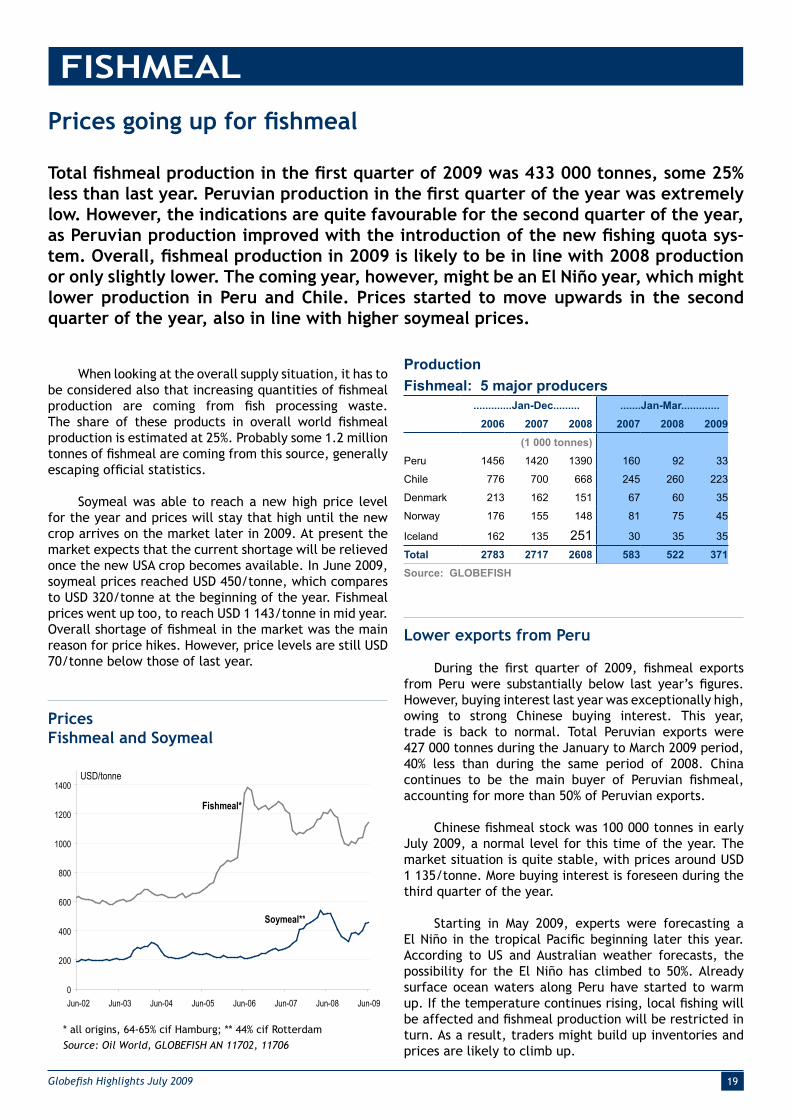

Prices going up for fishmealTotal fishmeal production in the first quarter of 2009 was 433 000 tonnes, some 25% less than last year. Peruvian production in the first quarter

of the year was extremely low. p. 19

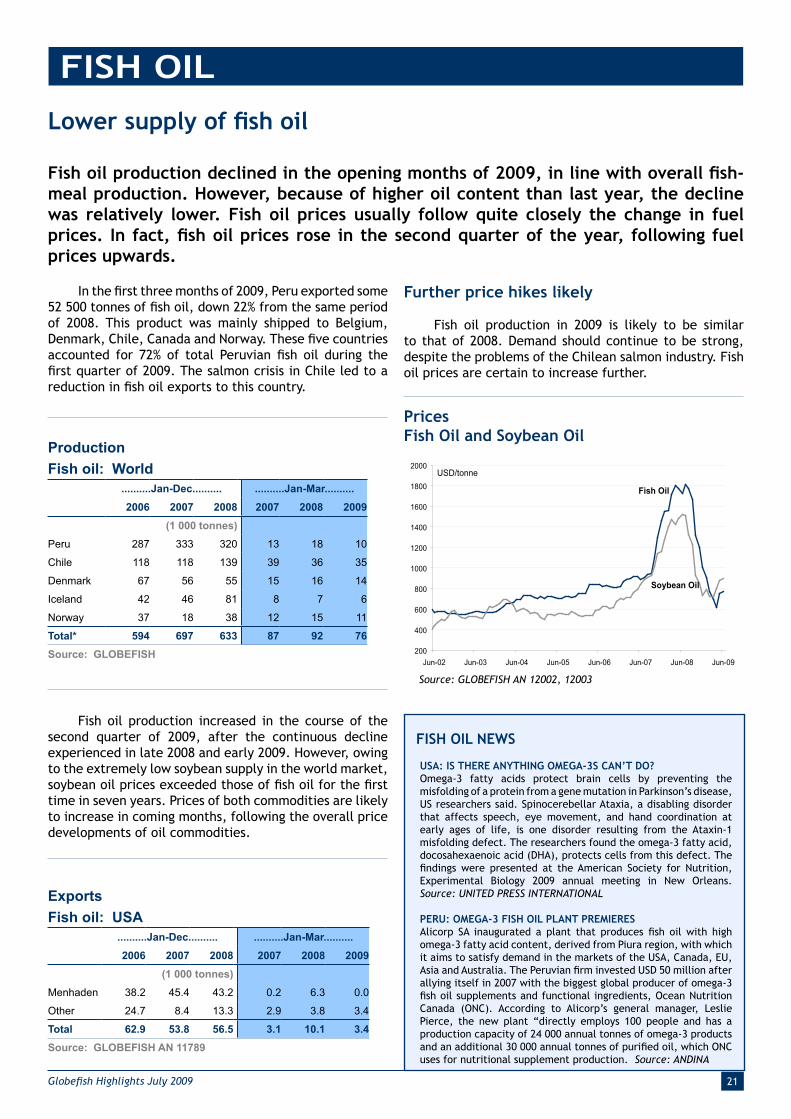

Lower supply of fish oilFish oil production declined in the opening months of 2009, in line with overall fishmeal pro-duction. However, because of higher oil content than last year, the decline was relatively lower.

Fish oil prices usually follow quite closely the change in fuel prices. p. 21

15/07/2009

Tilapia: a good product in the present crisisTilapia is a product with a strong growth rate. China is by far the main producer, but many other Asian countries are also expanding their tilapia outputs. p. 22

Outlook positive for pangasiusDuring the first months of 2009 pangasius was under pressure, as Russia and Egypt banned imports. In addition, negative press coverage in

Italy and Germany scared consumers away from buying of pangasius. p. 24 Disastrous situation for Nile perch

Nile perch resources are under stress and production is going down. The three producing countries report lower exports of fillets to the EU, the main

market for this product. p. 26

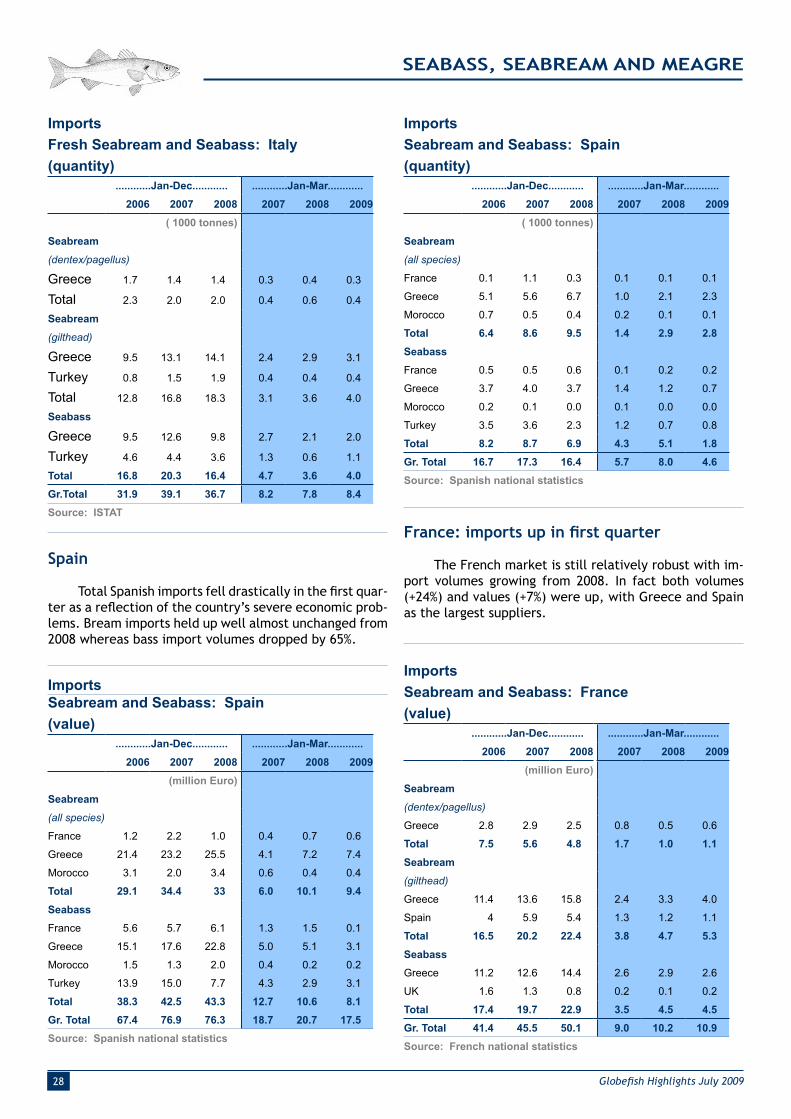

The European market for bass and bream is sur-prisingly good at present

Supplies of bream are lower than previously expected and prices are stable. This is unusual for the season because

in most years, when new supplies come to market in June and July prices fall as a result. p. 27

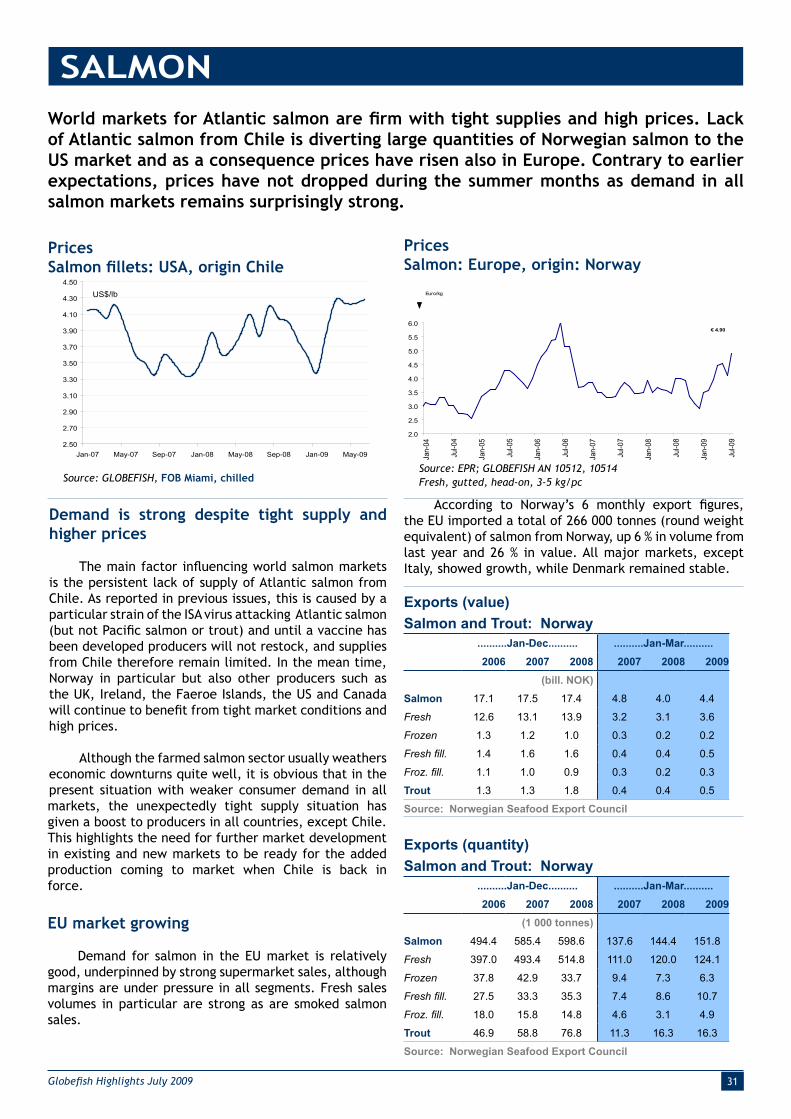

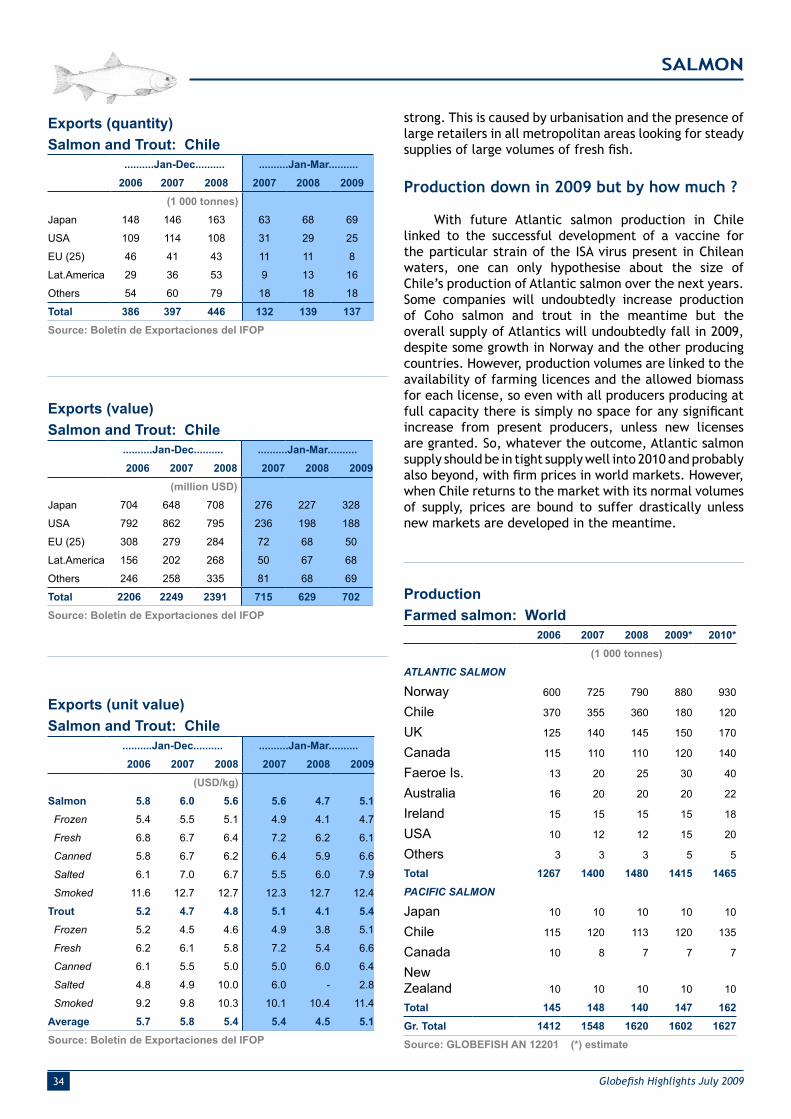

Atlantic SalmonWorld markets for Atlantic salmon are firm with tight supplies and high prices. Lack of Atlantic salmon from Chile

is diverting large quantities of Norwegian salmon to the US market and as a consequence prices have risen also in Europe. p. 31

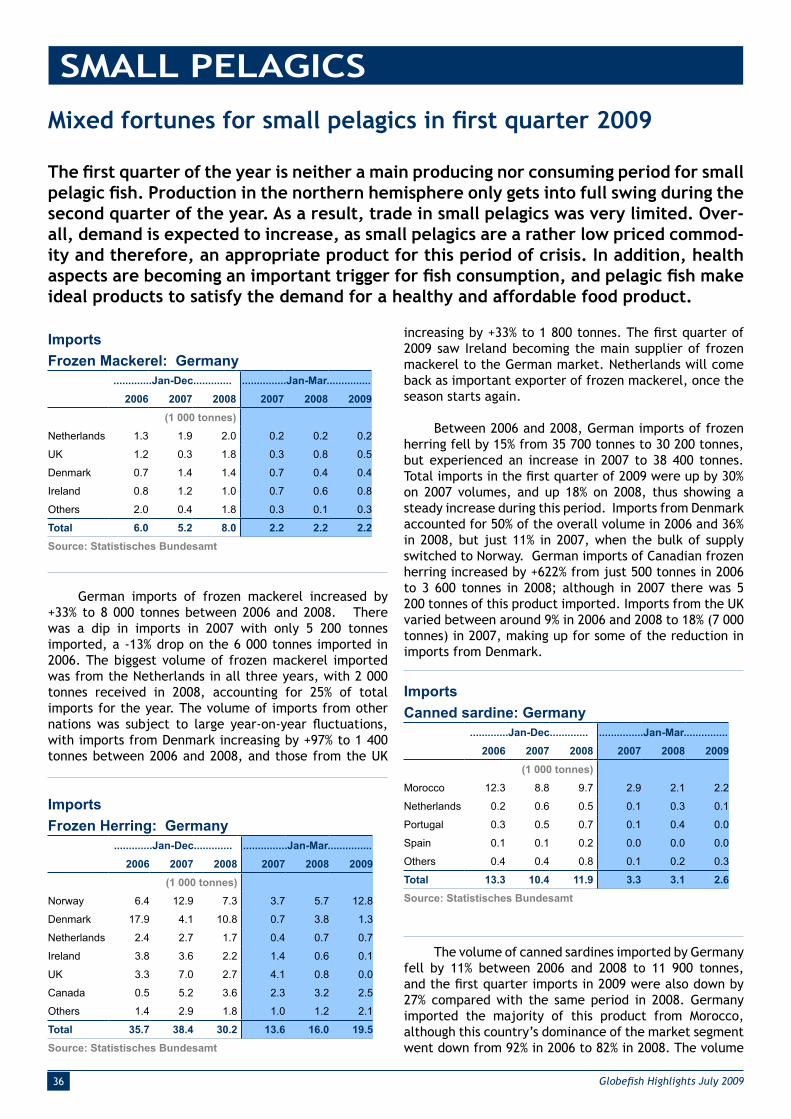

Mixed fortunes for small pelagics in first quarter The first quarter of the year is neither a main producing nor consuming period for small pelagic fish. Production in the

northern hemisphere only gets into full swing during the second quarter of the year. p. 36

Issue 2/2009

Food and Agriculture Organization of the United Nations

Fish Products and Industry DivisionViale delle Terme di Caracalla

00153 Rome, ItalyTel.: +39 06 5705 6313Fax: +39 06 5705 5188

www.globefish.org

About GLOBEFISH

GLOBEFISH forms part of the Fish Utilization and Marketing Service of the FAO Fisheries and Aquaculture Department and is part of the FISH INFOnetwork (see below). It collects information from the main market areas in developed countries. Part of its services is an electronic databank and the distribution of information through the GLOBEFISH European Fish Price Report, the GLOBEFISH Highlights, the GLOBEFISH Research Programme and the GLOBEFISH Commodity Updates.

The GLOBEFISH Highlights are based on information available in the databank, supplemented by market information from six regional services which form the FISH INFOnetwork: INFOFISH (Asia and the Pacific), INFOPESCA (Latin America and the Caribbean), INFOPECHE (Africa), INFOSAMAK (Arab countries), EUROFISH (Central and Eastern Europe) and INFOYU (China).

GLOBEFISH Highlights are distributed to the subscribers of: INFOFISH Trade News, INFOPESCA Noticias Comerciales, INFOPECHE Nouvelles Commerciales, through EUROFISH and INFOYU. GLOBEFISH Highlights are also available in electronic form.

For subscription details please contact:GLOBEFISH, FIIU/FAO Tel: (39-06) 5705 6313

Viale delle Terme di Caracalla Fax: (39-06) 5705 518800153 Rome, Italy

Email: [email protected]: www.globefish.org

All rights reserved. Reproduction and dissemination of material in this information product for educational or other non-commercial purposes are authorized without any prior written permission from the copyright holders provided the source is fully acknowledged. Reproduction of material in this information product for resale or other commercial purposes is prohibited without written permission of the copyright holders. Applications for such permission should be addressed to the Chief, Electronic Publishing Policy and Support Branch, Communication Division, FAO, Viale delle Terme di Caracalla, 00153 Rome, Italy or by e-mail to [email protected] © FAO GLOBEFISH 2009

Bibliographic reference:

GLOBEFISH Highlights

2009

FAO/GLOBEFISH Highlights

(2/2009): p. 38

A quarterly update based on the GLOBEFISH databank

1Globefi sh Highlights July 2009

Shrimp markets very slow

The economic crisis continues to infl uence the world shrimp market. Generally,

because of their relatively high price, sales of shrimp products suffer because of loss of

purchasing power. This means that fewer consumers eat out at restaurants, the main

outlets for shrimp purchases in the major shrimp consuming countries. Prices are low

at the moment, and there is little hope of price increases later this year. Availability is

generally very good from shrimp supplying countries but shrinking demand is creating

a serious problem for the whole sector and particularly to producers, who see their

costs increasing and their income being dramatically reduced.

SHRIMP

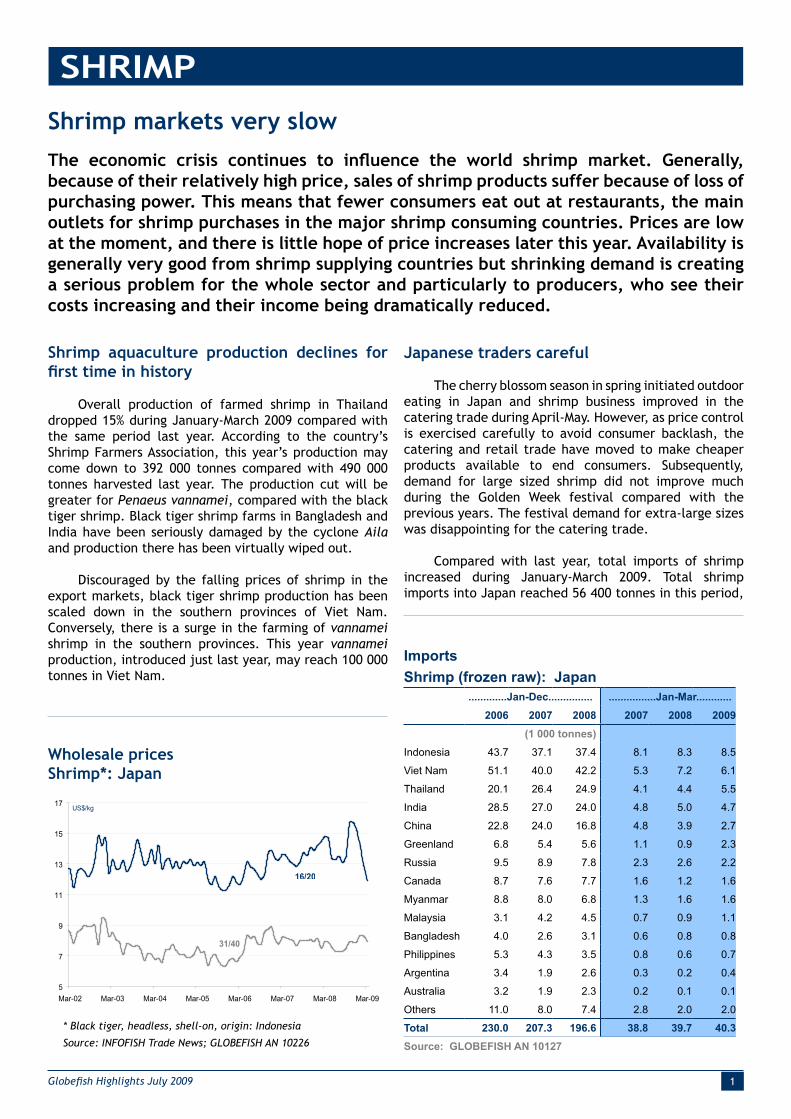

Wholesale prices

Shrimp*: Japan

Source: INFOFISH Trade News; GLOBEFISH AN 10226

* Black tiger, headless, shell-on, origin: Indonesia

Shrimp aquaculture production declines for

fi rst time in history

Overall production of farmed shrimp in Thailand

dropped 15% during January-March 2009 compared with

the same period last year. According to the country’s

Shrimp Farmers Association, this year’s production may

come down to 392 000 tonnes compared with 490 000

tonnes harvested last year. The production cut will be

greater for Penaeus vannamei, compared with the black

tiger shrimp. Black tiger shrimp farms in Bangladesh and

India have been seriously damaged by the cyclone Aila

and production there has been virtually wiped out.

Discouraged by the falling prices of shrimp in the

export markets, black tiger shrimp production has been

scaled down in the southern provinces of Viet Nam.

Conversely, there is a surge in the farming of vannamei

shrimp in the southern provinces. This year vannamei

production, introduced just last year, may reach 100 000

tonnes in Viet Nam.

Japanese traders careful

The cherry blossom season in spring initiated outdoor

eating in Japan and shrimp business improved in the

catering trade during April-May. However, as price control

is exercised carefully to avoid consumer backlash, the

catering and retail trade have moved to make cheaper

products available to end consumers. Subsequently,

demand for large sized shrimp did not improve much

during the Golden Week festival compared with the

previous years. The festival demand for extra-large sizes

was disappointing for the catering trade.

Compared with last year, total imports of shrimp

increased during January-March 2009. Total shrimp

imports into Japan reached 56 400 tonnes in this period,

Imports

Shrimp (frozen raw): Japan

.............Jan-Dec............... ................Jan-Mar............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Indonesia 43.7 37.1 37.4 8.1 8.3 8.5

Viet Nam 51.1 40.0 42.2 5.3 7.2 6.1

Thailand 20.1 26.4 24.9 4.1 4.4 5.5

India 28.5 27.0 24.0 4.8 5.0 4.7

China 22.8 24.0 16.8 4.8 3.9 2.7

Greenland 6.8 5.4 5.6 1.1 0.9 2.3

Russia 9.5 8.9 7.8 2.3 2.6 2.2

Canada 8.7 7.6 7.7 1.6 1.2 1.6

Myanmar 8.8 8.0 6.8 1.3 1.6 1.6

Malaysia 3.1 4.2 4.5 0.7 0.9 1.1

Bangladesh 4.0 2.6 3.1 0.6 0.8 0.8

Philippines 5.3 4.3 3.5 0.8 0.6 0.7

Argentina 3.4 1.9 2.6 0.3 0.2 0.4

Australia 3.2 1.9 2.3 0.2 0.1 0.1

Others 11.0 8.0 7.4 2.8 2.0 2.0

Total 230.0 207.3 196.6 38.8 39.7 40.3

Source: GLOBEFISH AN 10127

5

7

9

11

13

15

17

Mar-02 Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09

US$/kg

31/40

16/20

2 Globefi sh Highlights July 2009

SHRIMP

Wholesale prices

Shrimp*: USA, Japan

Source: INFOFISH Trade News; GLOBEFISH AN 10205, 10206

* Frozen, headless, shell-on, 16-20 count

which compares with 54 800 tonnes last year. The main

product group was frozen raw shrimp with about 40 000

tonnes. The main suppliers of this product are Indonesia,

Viet Nam and Thailand. Viet Nam reported substantial

declines in shipments, while Indonesia and Thailand

managed to increase their frozen shrimp exports to the

Japanese market in the fi rst quarter of 2009.

For home cooking, young consumers prefer semi-

processed and processed shrimp, Western style; they

even prefer cooked shrimp over tempura shrimp. The

older generation still likes the traditional shell-on shrimp

but in easy-to-prepare and ready-to-cook preparations.

Demand for tray-pack shrimp, of all types, has been very

slow in the retail trade.

The H1N1 fl u alarm has created mixed trends in

the market. Because of the health scare, people are

avoiding going out, which is hurting the already weak

restaurant trade. Many schools have cancelled the

outdoor programmes that normally take place in summer.

Overall, shrimp consumption is low in Japan during the

current summer months, a normal feature for this time

of the year.

Low demand for shrimp in the USA continues

The negative economic environment in the USA has

affected consumer habits. One of the most signifi cant

changes is an increase in savings rate, as a reaction to the

uncertainty in the labour market. This implies a reduction

in consumption as consumers are becoming more price-

sensitive. As a reaction to fewer customers, restaurants

are increasingly offering value-oriented items on their

Imports

Shrimp: USA

.................................Jan-March...................................

2004 2005 2006 2007 2008 2009

(1000 tonnes)

Thailand 49.1 31.6 34.1 39.7 35.0 35.5

Indonesia 6.6 12.8 17.1 12.5 20.7 20.6

Ecuador 11.5 12.0 15.9 17.2 15.7 16.1

China 25.6 9.9 12.8 17.7 12.9 7.3

Viet Nam 14.2 10.5 8.3 5.9 8.6 6.4

Malaysia 0.3 2.9 4.4 4.6 7.1 2.9

Mexico 4.4 4.9 4.9 6.9 6.5 8.0

India 15.2 8.0 7.3 4.1 2.9 4.6

Bangladesh 1.1 2.0 3.4 3.1 2.8 2.6

Guyana 2.7 2.0 2.4 2.6 2.5 2.4

Venezuela 4.4 3.9 2.6 3.0 2.1 0.9

Peru 0.6 1.0 1.1 1.5 1.7 2.6

Others 13.6 10.8 10.3 7.3 5.3 5.0

Total 149.3 112.4 124.6 126.2 123.8 114.8

Source: NMFS

Imports

Shrimp: USA

Jan-March

2008 2009

tonnes 1000 USD tonnes 1000 USD

Peeled frozen 39 985 286 311 37 285 261 794

Other frozen 19 257 139 498 21 497 160 202

Breaded 10 538 49 613 7 791 42 508

Other preparations 329 1 632 302 1 446

Headless shell-on frozen

All sizes 52 287 373 230 46 517 315 543

< 15 5 708 72 061 4 651 53 035

15/20 3 908 39 571 3 793 34 600

21/25 6 011 52 851 6 311 50 738

26/30 7 964 56 330 7 015 46 307

31/40 8 967 53 734 9 807 58 651

41/50 7 190 38 849 5 698 29 341

51/60 6 476 32 770 4 806 23 352

61/70 3 831 17 767 2 375 10 779

> 70 2 229 9 293 2 059 8 740

Other products 1 402 11 631 1 456 13 694

Total 123 799 861 918 114 848 795 188

Source: NMFS

menus, in order to attract guests. Many restaurants are

offering smaller sized menus, often based on shrimp, in

order to reduce costs and therefore prices.

Low demand for shrimp, in conjunction with high

cold storage holdings, has impacted both prices and

imports. Sales of larger sizes have been dramatically

affected by the change in consumer buying patterns.

Prices of US domestic shrimp are signifi cantly lower than

4

5

6

7

8

Mar-02 Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09

USD/lb

Gulf brown, New York

Indian white, Tokyo

3Globefi sh Highlights July 2009

SHRIMP

a year ago, and the same trend, although less severe, can

be observed with imported shrimp.

US imports of shrimp in the fi rst quarter of 2009

totalled 115 000 tonnes worth USD 795.2 million. These

fi gures represent a 7% and 8% drop in total imports in

terms of volume and value respectively compared with the

same period in 2008. The main supplier, Thailand, which

accounted for 31% of total imported volume, managed

to gain market share. However, Thai exporters expressed

their concern about the effect that the strengthening baht

could have on shrimp exports. Exports from Indonesia

remained unchanged while purchases from Ecuador and

Mexico increased.

There was little incentive to fi sh for pink shrimp

on the US West coast, as both fi shermen and packers

were disappointed by current wholesale prices. The few

landings were totally taken up by the local fresh seafood

market. In addition, there still are substantial stocks

of frozen shrimp from the 2008 season. As for the Gulf

of Mexico area, the white shrimp season in Louisiana

started on 18 May 2009. Preliminary data showed a higher

percentage of larger sizes.

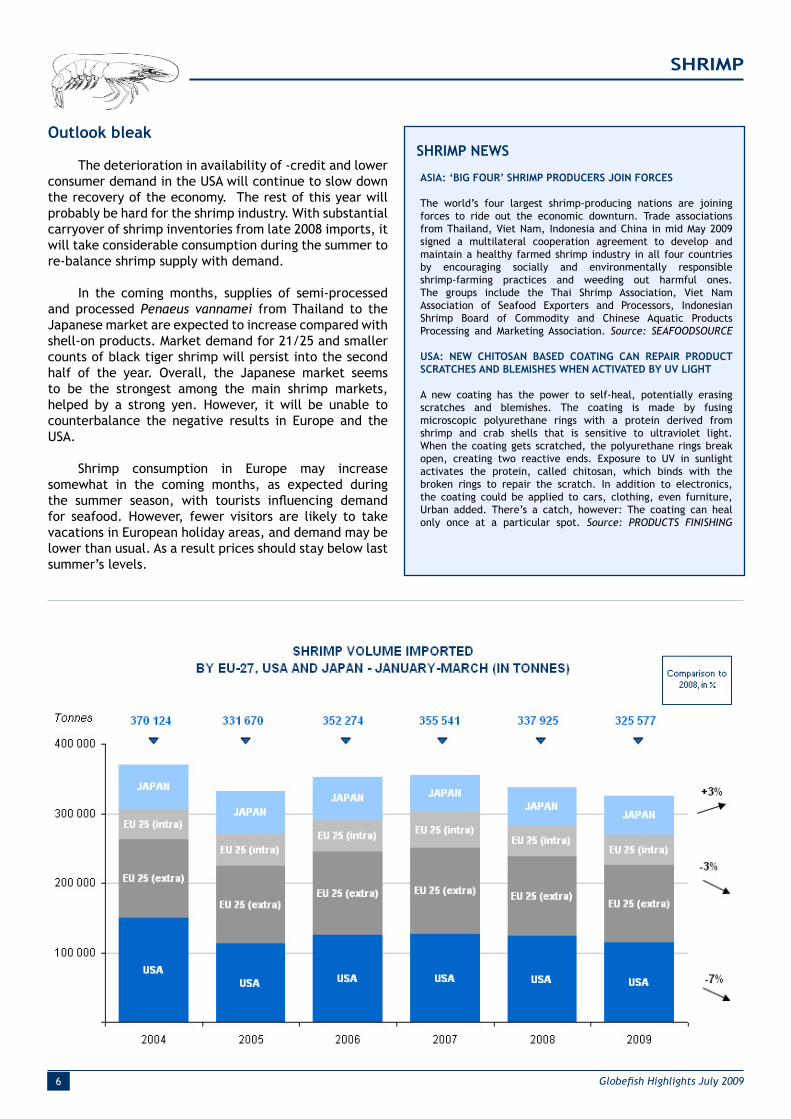

The EU shrimp market is worsening

During the fi rst quarter of 2009, all major key

markets in Europe continued to see their shrimp imports

decrease further and total import fi gures were down

3% compared with the same period last year to 154 500

tonnes. Demand has decreased on the various European

markets although prices are steady at a fairly low level

and therefore more affordable.

The new economic outlook released by OECD in June

this year shows that the euro area is in a deep recession,

“with external demand collapsing and domestic demand

being weakened by tight fi nancial conditions, rising

unemployment and heightened uncertainty”.

In general, because of their relatively high price,

sales of shrimp products suffer during an economic

crisis because consumers have lower purchasing power

and they tend to be more careful regarding the quality

of the product. Aware of this, advertisers in the retail

sector develop product labels referring to quality and

sustainability: “So organic”, “be good to yourself”,

“reduced fat”, “Omega 3”, “best ever prawns”, etc....

Even with the diffi cult situation on the European

market, during the fi rst quarter of 2009 India noticeably

increased its market share in this region with a 24%

growth rate compared with last year fi gures. With 15 200

tonnes of shrimp exported to Europe during the period

January-March 2009, India is presently the largest shrimp

supplier to EU. However, this leading position may not

last, as EU inspectors have found unauthorized residues

in some products imported from India. Crustaceans of

this origin will now enter the European Union only on

presentation of negative results for nitrofurans and other

unauthorized residues.

Greenland’s export fi gures to Europe were also

relatively good during the period under review with 14 700

tonnes corresponding to a 23% increase compared with

2008. Greenland is the second major shrimp supplier to

Europe and the number one supplier of coldwater shrimp.

Almost all the production goes to Denmark through a

large state-controlled group and then is re-exported to

other countries. In June, the new Greenland government

provided help for the group which is presently facing

severe fi nancial diffi culties.

The situation is diffi cult for most shrimp suppliers.

Ecuador, after years of constant expansion on the

European market, is showing signs of weakness. It is

the third shrimp exporter to Europe with 11 900 tonnes

but lost 11% on last years’ shrimp exports. However, it

remains by far the main supplier to the French and Italian

markets thanks to its low-cost products.

Imports

Shrimp: UK

................Jan-Dec............ ..............Jan-Mar..............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Shell-on Coldwater

Denmark 2.8 2.4 2.2 0.6 0.6 0.6

Others 1.4 1.3 1.9 0.3 0.3 0.2

Total 4.6 4.8 4.1 0.9 0.9 0.8

Shell-on Warmwater

India 11.3 10.5 7.6 2.7 1.6 1.5

Indonesia 5.2 6.3 5.9 1.1 1.6 1.4

Bangladesh 6.2 5.7 4.6 1.0 1.1 1.2

Thailand 1.2 4.1 4.8 0.5 1.1 0.8

Viet Nam * * 2.4 0.1 0.4 0.4

Ecuador 3.3 3.3 2.0 0.7 0.7 0.4

Denmark * 1.0 1.1 0.2 0.2 0.4

Honduras 1.2 1.3 1.7 0.2 0.2 0.3

Others 7.4 5.4 5.4 1.1 1.2 0.8

Total 38.0 38.7 35.5 7.6 8.1 7.2

Cooked & Peeled

Iceland 16.9 15.3 13.4 2.0 1.9 1.8

Denmark 6.6 6.9 6.3 1.4 1.3 1.4

Thailand 3.9 5.2 4.9 0.7 0.6 1.2

Indonesia 3.1 2.6 2.8 0.7 0.5 0.7

Norway 3.5 2.7 3.2 0.3 0.6 0.5

Canada 4.5 3.9 2.6 0.3 0.2 0.3

Others 4.7 4.7 7.4 1.7 1.8 1.2

Total 46.6 44.0 40.6 7.1 6.9 7.1

Gr. Total 89.2 87.5 80.2 15.6 15.9 15.1

Source: GLOBEFISH AN 010141

4 Globefi sh Highlights July 2009

SHRIMP

Argentina reported very good landings of Pleoticus

muelleri, but had to sell at discounted prices due to

diminished demand. During the fi rst quarter of 2009

Canada experienced an 11% decrease in exports to the

EU with only 8 700 tonnes. Coldwater shrimp processors

are shutting down in Newfoundland as a consequence of

the decreasing demand and a strong Canadian dollar.

Bangladesh registered a very positive result at the

beginning of 2009 on the UK market, with a 26% increase

of its exports. Unfortunately, the future is very uncertain

for this country after the cyclone Aila destroyed thousands

of shrimp enclosures and ponds on 25 May and also as a

re-sult of the voluntary six-month suspension of exports

following the detection by the EU of harmful veterinary

drug residues in shrimp from Bangladesh.

OECD reports that the fi nancial crisis in the UK is

severely restraining business and household spending.

Latest UK statistics indicate that during the fi rst quarter

of 2009, total shrimp imports decreased by 5% in volume

compared with the same period in 2008, though in

terms of value imports increased by 20% compared with

2008. However, the decrease in import volume did not

affect all products. The average unit value for shrimp

products entering the UK market was GBP 1.00/kg higher

than during the fi rst quarter of 2008. The devaluation

of the British Pound is the main cause and the situation

should change somewhat in the coming months as the UK

currency slowly recovered in the second quarter. While

imports of frozen shrimp products continued to decline

owing to the economic crisis, losing 13% compared with

last year fi gures, volumes of prepared and preserved

shrimp increased notably (+5% compared with 2008). This

is because of increased volumes in processed products

coming from Asia (mainly Thailand and Indonesia). The

proportion of coldwater shrimp imported by the UK market

continued to shrink and now represents only 35% of total

imports in the fi rst quarter of 2009. In contrast, imports

of warmwater shrimp have been stable for the past four

years, including 2009 in spite of present diffi culties.

Total Danish shrimp imports continue to follow the

downward trend of previous years. Imports during the fi rst

quarter of 2009 amounted to 22 800 tonnes corresponding

to a total of DKK 608 million, a 10% decrease in volume

and a 22% decrease in value compared with the same

period of 2008. Denmark imports essentially coldwater

shrimp (95% in the fi rst quarter of 2009). This does not

come as a surprise, as Denmark is mainly a re-exporter

and processor of coldwater shrimp. Greenland, by far the

number one supplier to Denmark, saw its exports to this

country increase by 23% in volume and by 20% in value

compared with the fi rst quarter of 2008. In contrast, during

the fi rst quarter of 2009, due to problemas expereinced

with low shrimp catches, Canada suffered a 41% decrease

in volume and a 49% decrease in value compared with the

same period last year.

Imports

Shrimp: Denmark

..............................Jan-March.......................

2005 2006 2007 2008 2009

(1000 tonnes)

Greenland 15.3 18.3 12.1 11.9 14.6

Canada 8.4 7.6 10.1 7.5 4.4

Faroe Islands 0.8 0.8 0.1 0.8 1.0

UK 0.6 0.7 1.0 0.4 0.5

Netherlands 1.2 0.7 1.4 0.5 0.4

Iceland 0.7 0.7 0.6 1.4 0.3

Thailand 0.0 0.1 0.2 0.3 0.2

Vietnam 0.1 0.1 0.2 0.2 0.2

India 0.1 0.1 0.2 0.2 0.2

Norway 1.3 1.0 0.8 0.6 0.2

China 0.0 0.1 0.1 0.4 0.2

Others 1.8 1.4 2.1 1.2 0.6

Total 30.2 31.7 28.8 25.3 22.8

Source: GLOBEFISH

Spain registered the largest drop ever in shrimp

imports during the fi rst quarter of 2009. With 22 000

tonnes imported at a value of EUR 104 million, Spainish

imports decreased by 15% in volume and 14% in value

compared with the previous year. Chinese and Ecuadorian

shrimp imports, which together represent 35% of total

imports, dropped drastically. On the other hand,

Argentina supplied large quantities of Pleoticus muelleri

(almost double the volume of last year) to the Spanish

market as a consequence of very good landings.

Imports

Shrimp: Spain

......................................Jan-March..............................

2004 2005 2006 2007 2008 2009

(1000 tonnes)

China 0.3 4.3 6.9 7.8 6.6 4.7

Ecuador 1.5 1.5 3.3 4.5 4.2 3.0

Argentina 4.1 0.8 1.1 3.8 1.6 2.7

Morocco 1.6 2.0 1.5 1.6 1.7 1.5

Nicaragua 0.4 0.5 1.0 1.0 0.7 1.2

Colombia 0.9 1.2 1.0 1.2 1.1 0.9

Belgium 0.6 0.7 0.6 1.0 0.8 0.8

Netherlands 0.9 1.1 1.0 1.1 0.7 0.7

Cuba 0.2 0.2 0.9 1.1 0.8 0.6

Others 16.7 11.8 12.4 11.3 7.9 5.9

Total 27.3 24.0 29.7 34.3 26.0 22.0

Source: GLOBEFISH AN 010150

5Globefi sh Highlights July 2009

SHRIMP

Shrimp volumes imported by France during the fi rst

quarter of 2009 were 11% lower in volume and 3% lower

in value compared with the same period last year, thus

increasing the unit value. THis was mainly due to a change

in the composition of shrimp suppliers to the French

market. Demand continues to be mainly for frozen whole

tropical shrimp while coldwater imports represent only

about 15% of the market. Almost all top exporting countries

have seen their volumes to France decrease substantially.

Only Asian countries (India, Thailand and Viet Nam) are

gaining market shares on the French market. India, in

particular, registered a constant expansion on the French

market in the past fi ve years and, notwithstanding the

economic crisis, increased its volumes to France, at the

beginning of this year, by more than 40% compared with

last year’s fi gures.

Imports

Shrimp: France

..................................Jan-March....................................

2005 2006 2007 2008 2009

(1000 tonnes)

Ecuador 1.4 2.3 2.9 4.7 3.7

India 1.2 1.9 2.0 2.1 3.0

Colombia 0.7 0.7 1.1 1.8 1.5

Netherlands 2.2 1.4 1.4 1.5 1.4

Brazil 5.1 3.2 3.3 1.9 1.3

Madagascar 1.6 1.3 1.3 1.9 1.2

Thailand 0.5 0.5 1.0 0.8 1.1

Vietnam 0.7 0.7 0.9 0.8 0.8

Indonesia 1.2 1.6 0.8 0.9 0.7

Belgium 1.0 1.3 1.1 1.1 0.7

Spain na na 0.5 0.3 0.7

Denmark 0.9 1.0 1.0 0.6 0.7

Venezuela 0.1 0.2 0.4 0.8 0.6

Bangladesh 0.2 0.1 0.1 0.8 0.6

Others 3.8 3.5 3.5 3.4 3.0

Total 20.6 19.8 21.4 23.5 21.0

Source: GLOBEFISH

In Italy, total shrimp imports for the fi rst quarter

of 2009 decreased by 10% in volume and by 3% in value

compared with the same period last year. Consequently

the average unit value increased by EUR 0.40/kilo

compared with 2008, making shrimp less affordable in

a market where revenues are badly hit by recession.

OECD indicates that the Italian economy is in a strong

recession, mainly because of external developments

linked to the global fi nancial crisis. Unemployment and

budget defi cit are expected to increase further with

negative consequences for household consumption and

subsequently for more expensive food commodities such

as shrimp.

Germany is the only country in Europe to register

a positive shrimp import fi gure in 2009. The increase

is particularly apparent for frozen whole products of

Asian origin. Shrimp demand in Germany has continued

to expand during the past 10 years. The majority of

imports are in whole frozen form but the proportion of

processed products is signifi cant and growing. Products

of Asian origin dominate the German market and imports

from Thailand, Viet Nam, India and Bangladesh (top four

suppliers) represent 60% of total imports.

Imports

Shrimp: Italy

.............................Jan-March.........................

2005 2006 2007 2008 2009

(1000 tonnes)

Ecuador 3.4 3.5 4.5 3.9 3.9

Spain 0.6 0.8 1.2 1.0 1.0

India 1.0 1.0 1.0 1.4 0.9

Denmark 1.4 1.5 1.6 1.3 0.8

Argentina 0.2 0.4 0.7 0.5 0.8

China 0.5 0.4 1.0 0.4 0.7

Netherlands 0.6 0.8 0.8 0.6 0.6

Thailand 0.2 0.2 0.2 0.3 0.5

UK 0.8 0.7 0.6 0.4 0.4

Indonesia 0.3 0.3 0.2 0.2 0.4

Malaysia 0.8 0.7 0.7 0.4 0.0

Others 2.9 3.1 2.8 2.5 1.6

Total 12.7 13.4 15.3 12.8 11.6

Source: GLOBEFISH AN 010148

Imports

Shrimp: Germany

.............Jan-Dec.............. ................Jan-Mar............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Thailand 4.0 8.9 9.3 1.3 2.0 2.2

Viet Nam 4.0 5.7 8.1 1.0 1.5 1.9

India 5.3 6.4 5.7 1.8 1.3 1.5

Bangladesh 3.0 3.1 3.5 0.4 0.6 1.3

Netherlands 4.1 5.7 3.9 1.7 1.3 0.7

Denmark 1.5 2.6 2.7 0.3 0.8 0.6

UK 3.1 2.5 1.6 0.8 0.5 0.6

Belgium 2.8 2.6 2.0 0.7 0.7 0.5

Greenland na 2.6 2.3 0.6 0.6 0.5

Indonesia na 2.1 2.0 0.5 0.4 0.3

Others 12.1 11.4 7.3 1.6 1.2 1.4

Total 39.9 48.8 48.4 10.7 10.9 11.5

Source: GLOBEFISH AN 010146

6 Globefi sh Highlights July 2009

SHRIMP

SHRIMP NEWS

ASIA: ‘BIG FOUR’ SHRIMP PRODUCERS JOIN FORCES

The world’s four largest shrimp-producing nations are joining

forces to ride out the economic downturn. Trade associations

from Thailand, Viet Nam, Indonesia and China in mid May 2009

signed a multilateral cooperation agreement to develop and

maintain a healthy farmed shrimp industry in all four countries

by encouraging socially and environmentally responsible

shrimp-farming practices and weeding out harmful ones.

The groups include the Thai Shrimp Association, Viet Nam

Association of Seafood Exporters and Processors, Indonesian

Shrimp Board of Commodity and Chinese Aquatic Products

Processing and Marketing Association. Source: SEAFOODSOURCE

USA: NEW CHITOSAN BASED COATING CAN REPAIR PRODUCT

SCRATCHES AND BLEMISHES WHEN ACTIVATED BY UV LIGHT

A new coating has the power to self-heal, potentially erasing

scratches and blemishes. The coating is made by fusing

microscopic polyurethane rings with a protein derived from

shrimp and crab shells that is sensitive to ultraviolet light.

When the coating gets scratched, the polyurethane rings break

open, creating two reactive ends. Exposure to UV in sunlight

activates the protein, called chitosan, which binds with the

broken rings to repair the scratch. In addition to electronics,

the coating could be applied to cars, clothing, even furniture,

Urban added. There’s a catch, however: The coating can heal

only once at a particular spot. Source: PRODUCTS FINISHING

Outlook bleak

The deterioration in availability of -credit and lower

consumer demand in the USA will continue to slow down

the recovery of the economy. The rest of this year will

probably be hard for the shrimp industry. With substantial

carryover of shrimp inventories from late 2008 imports, it

will take considerable consumption during the summer to

re-balance shrimp supply with demand.

In the coming months, supplies of semi-processed

and processed Penaeus vannamei from Thailand to the

Japanese market are expected to increase compared with

shell-on products. Market demand for 21/25 and smaller

counts of black tiger shrimp will persist into the second

half of the year. Overall, the Japanese market seems

to be the strongest among the main shrimp markets,

helped by a strong yen. However, it will be unable to

counterbalance the negative results in Europe and the

USA.

Shrimp consumption in Europe may increase

somewhat in the coming months, as expected during

the summer season, with tourists infl uencing demand

for seafood. However, fewer visitors are likely to take

vacations in European holiday areas, and demand may be

lower than usual. As a result prices should stay below last

summer’s levels.

7Globefi sh Highlights July 2009

Prices moving up

Starting in mid May 2009 tuna prices in all major catching areas began to rise because

of fears that upcoming tuna fi shing bans in these areas will squeeze global supply for

the canning industry. Canned tuna prices have been low in recent months, but are

likely to follow raw material prices up-ward very soon. Sustainability is a major con-

cern for the global tuna industry, which is trying to make its voice heard. Closing of

canneries as a result of globalization and out-sourcing is impacting negatively econo-

mies based on tuna, especially in areas where there are very limited job opportuni-

ties. The future for the tuna industry is rather bleak, with higher costs while demand

is somewhat limited.

TUNA

Imports

Canned tuna: UK

............Jan-Dec............ ............Jan-Mar............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Seychelles 32.0 23.9 16.7 6.6 3.2 5.0

Ghana 17.0 18.4 22.7 4.3 6.6 4.6

Thailand 16.9 14.9 14.6 4.1 3.3 3.8

Philippines 10.0 13.0 19.2 3.1 4.1 3.3

Mauritius 25.9 27.8 27.2 6.8 5.6 3.2

Ecuador 6.8 7.8 18.9 1.3 2.5 1.0

France 1.7 3.0 4.0 0.7 0.9 0.5

Maldives 1.9 2.2 1.0 1.3 0.4 0.3

Indonesia 0.9 1.7 1.4 0.6 0.4 0.2

Others 15.5 17.8 18.4 5.2 2.5 2.0

Total 128.6 130.5 144.0 34.0 29.5 23.9

Source: GLOBEFISH AN 11050

Sustainability of tuna resources of major

concern

The International Seafood Sustainability Foundation

(ISSF)- is a partnership between the tuna industry and

World Wildlife Fund (WWF). They are committed to using

sound management based on good science compiled by

regional fi sheries management organizations (RFMOs) to

rate the 19 stocks which support commercial tuna fi shing

used by the canning industry. ISSF has red listed Eastern

Pacifi c bigeye tuna and lobbied during the Inter American

Tropical Tuna Commission (IATTC) meeting in San Diego in

June 2009 to take action to conserve these stocks. IATTC

failed to adopt the conservation measures proposed by

its scientifi c staff, but it did adopt measures that would

provide some conservation benefi ts, in terms of reduction

of fi shing pressure by about 20%, rather than the 30%

recommended. This is, in fact, a positive outcome, as

in the previous two years no decision on catch reduction

measures had been taken.

The fi lm “End of the line” highlighted overfi shing

worldwide, including the overexploitation of bluefi n tuna

in the Mediterranean. Some companies have reacted to

this message already. One major sandwich producer in

the USA decided to stop using tuna in its sandwiches, even

though no bluefi n tuna had ever been used for this type

of product. Marks & Spencer (M&S), one of the biggest

fi sh retailers in the UK, is to stop selling certain types

of tuna following the message of ”End of the Line”. M&S

said it would become the fi rst UK food retailer to source

only pole & line or line-caught tuna for its fresh foods

from sandwiches to fresh steaks and also for canned tuna

by the end of the year. On the other hand, an important

sushi restaurant in London decided to keep bluefi n tuna

on the menu, but to include a footnote saying that it is an

overexploited species.

Imports

Canned tuna: Germany

............Jan-Dec............ ............Jan-Mar............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Ecuador 15.8 21.2 28.6 4.9 4.6 4.0

Philippines 23.4 24.1 18.5 6.1 2.6 5.2

Thailand 18.1 11.9 8.2 2.5 1.4 1.2

Indonesia 6.0 8.1 6.8 1.2 1.6 1.8

Papua NG 4.4 5.7 6.1 1.4 0.4 1.2

Seychelles 6.7 2.1 4.4 0.7 1.0 0.0

France 2.2 1.1 0.9 0.3 0.2 0.0

Others 10.2 10.9 7.0 3.5 1.6 2.8

Total 86.8 85.1 80.6 20.6 13.4 16.2

Source: GLOBEFISH

8 Globefi sh Highlights July 2009

TUNA

0

500

1000

1500

2000

2500

Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09

USD/tonne

Thailand

Africa

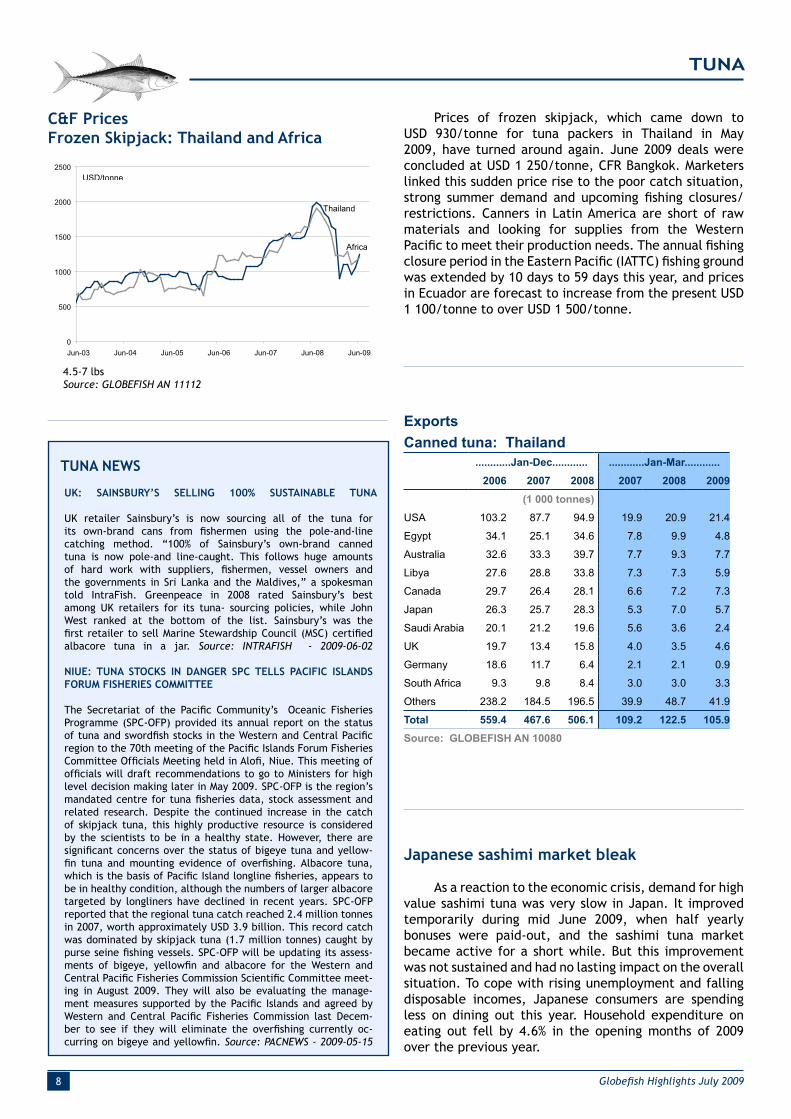

C&F Prices

Frozen Skipjack: Thailand and Africa

4.5-7 lbs

Source: GLOBEFISH AN 11112

Prices of frozen skipjack, which came down to

USD 930/tonne for tuna packers in Thailand in May

2009, have turned around again. June 2009 deals were

concluded at USD 1 250/tonne, CFR Bangkok. Marketers

linked this sudden price rise to the poor catch situation,

strong summer demand and upcoming fi shing closures/

restrictions. Canners in Latin America are short of raw

materials and looking for supplies from the Western

Pacifi c to meet their production needs. The annual fi shing

closure period in the Eastern Pacifi c (IATTC) fi shing ground

was extended by 10 days to 59 days this year, and prices

in Ecuador are forecast to increase from the present USD

1 100/tonne to over USD 1 500/tonne.

TUNA NEWS

UK: SAINSBURY’S SELLING 100% SUSTAINABLE TUNA

UK retailer Sainsbury’s is now sourcing all of the tuna for

its own-brand cans from fi shermen using the pole-and-line

catching method. “100% of Sainsbury’s own-brand canned

tuna is now pole-and line-caught. This follows huge amounts

of hard work with suppliers, fi shermen, vessel owners and

the governments in Sri Lanka and the Maldives,” a spokesman

told IntraFish. Greenpeace in 2008 rated Sainsbury’s best

among UK retailers for its tuna- sourcing policies, while John

West ranked at the bottom of the list. Sainsbury’s was the

fi rst retailer to sell Marine Stewardship Council (MSC) certifi ed

albacore tuna in a jar. Source: INTRAFISH - 2009-06-02

NIUE: TUNA STOCKS IN DANGER SPC TELLS PACIFIC ISLANDS

FORUM FISHERIES COMMITTEE

The Secretariat of the Pacifi c Community’s Oceanic Fisheries

Programme (SPC-OFP) provided its annual report on the status

of tuna and swordfi sh stocks in the Western and Central Pacifi c

region to the 70th meeting of the Pacifi c Islands Forum Fisheries

Committee Offi cials Meeting held in Alofi , Niue. This meeting of

offi cials will draft recommendations to go to Ministers for high

level decision making later in May 2009. SPC-OFP is the region’s

mandated centre for tuna fi sheries data, stock assessment and

related research. Despite the continued increase in the catch

of skipjack tuna, this highly productive resource is considered

by the scientists to be in a healthy state. However, there are

signifi cant concerns over the status of bigeye tuna and yellow-

fi n tuna and mounting evidence of overfi shing. Albacore tuna,

which is the basis of Pacifi c Island longline fi sheries, appears to

be in healthy condition, although the numbers of larger albacore

targeted by longliners have declined in recent years. SPC-OFP

reported that the regional tuna catch reached 2.4 million tonnes

in 2007, worth approximately USD 3.9 billion. This record catch

was dominated by skipjack tuna (1.7 million tonnes) caught by

purse seine fi shing vessels. SPC-OFP will be updating its assess-

ments of bigeye, yellowfi n and albacore for the Western and

Central Pacifi c Fisheries Commission Scientifi c Committee meet-

ing in August 2009. They will also be evaluating the manage-

ment measures supported by the Pacifi c Islands and agreed by

Western and Central Pacifi c Fisheries Commission last Decem-

ber to see if they will eliminate the overfi shing currently oc-

curring on bigeye and yellowfi n. Source: PACNEWS - 2009-05-15

Japanese sashimi market bleak

As a reaction to the economic crisis, demand for high

value sashimi tuna was very slow in Japan. It improved

temporarily during mid June 2009, when half yearly

bonuses were paid-out, and the sashimi tuna market

became active for a short while. But this improvement

was not sustained and had no lasting impact on the overall

situation. To cope with rising unemployment and falling

disposable incomes, Japanese consumers are spending

less on dining out this year. Household expenditure on

eating out fell by 4.6% in the opening months of 2009

over the previous year.

Exports

Canned tuna: Thailand

............Jan-Dec............ ............Jan-Mar............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

USA 103.2 87.7 94.9 19.9 20.9 21.4

Egypt 34.1 25.1 34.6 7.8 9.9 4.8

Australia 32.6 33.3 39.7 7.7 9.3 7.7

Libya 27.6 28.8 33.8 7.3 7.3 5.9

Canada 29.7 26.4 28.1 6.6 7.2 7.3

Japan 26.3 25.7 28.3 5.3 7.0 5.7

Saudi Arabia 20.1 21.2 19.6 5.6 3.6 2.4

UK 19.7 13.4 15.8 4.0 3.5 4.6

Germany 18.6 11.7 6.4 2.1 2.1 0.9

South Africa 9.3 9.8 8.4 3.0 3.0 3.3

Others 238.2 184.5 196.5 39.9 48.7 41.9

Total 559.4 467.6 506.1 109.2 122.5 105.9

Source: GLOBEFISH AN 10080

9Globefi sh Highlights July 2009

TUNA

Imports

Fresh/chilled tuna: Japan

............Jan-Dec............ ............Jan-Mar............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Yellowfi n 19.0 16.9 15.5 4.7 4.2 4.0

Bigeye 15.8 14.5 15 3.8 3.9 4

Bluefi n 7.4 5.1 4.4 1.8 1.2 1.9

S. bluefi n 1.8 1.2 1.2 0.0 0.0 0

Albacore 0.3 0.3 0.3 0.0 0.0 0.0

Skipjack 0.0 0.1 0 0.0 0.0 0

Total 44.3 38.1 36.3 10.3 9.2 9.9

Source: National Statistics

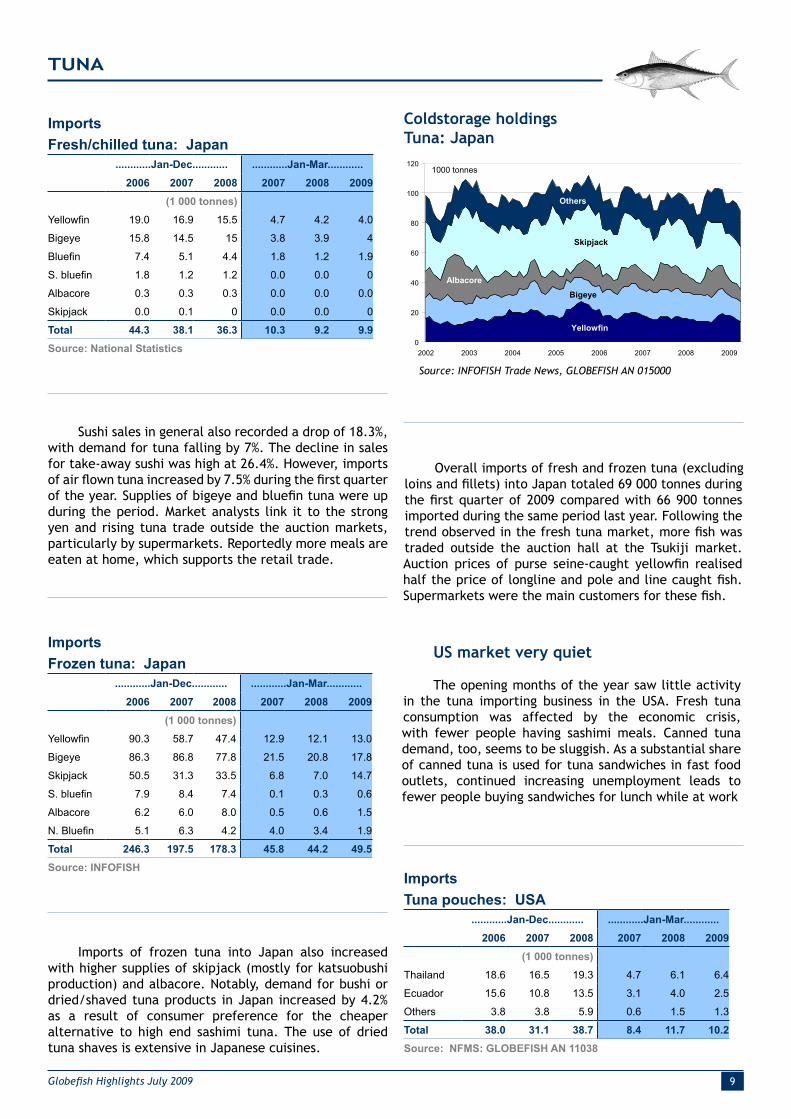

Coldstorage holdings

Tuna: Japan

Source: INFOFISH Trade News, GLOBEFISH AN 015000

Sushi sales in general also recorded a drop of 18.3%,

with demand for tuna falling by 7%. The decline in sales

for take-away sushi was high at 26.4%. However, imports

of air fl own tuna increased by 7.5% during the fi rst quarter

of the year. Supplies of bigeye and bluefi n tuna were up

during the period. Market analysts link it to the strong

yen and rising tuna trade outside the auction markets,

particularly by supermarkets. Reportedly more meals are

eaten at home, which supports the retail trade.

Imports of frozen tuna into Japan also increased

with higher supplies of skipjack (mostly for katsuobushi

production) and albacore. Notably, demand for bushi or

dried/shaved tuna products in Japan increased by 4.2%

as a result of consumer preference for the cheaper

alternative to high end sashimi tuna. The use of dried

tuna shaves is extensive in Japanese cuisines.

Imports

Tuna pouches: USA

............Jan-Dec............ ............Jan-Mar............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Thailand 18.6 16.5 19.3 4.7 6.1 6.4

Ecuador 15.6 10.8 13.5 3.1 4.0 2.5

Others 3.8 3.8 5.9 0.6 1.5 1.3

Total 38.0 31.1 38.7 8.4 11.7 10.2

Source: NFMS: GLOBEFISH AN 11038

Imports

Frozen tuna: Japan

............Jan-Dec............ ............Jan-Mar............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Yellowfi n 90.3 58.7 47.4 12.9 12.1 13.0

Bigeye 86.3 86.8 77.8 21.5 20.8 17.8

Skipjack 50.5 31.3 33.5 6.8 7.0 14.7

S. bluefi n 7.9 8.4 7.4 0.1 0.3 0.6

Albacore 6.2 6.0 8.0 0.5 0.6 1.5

N. Bluefi n 5.1 6.3 4.2 4.0 3.4 1.9

Total 246.3 197.5 178.3 45.8 44.2 49.5

Source: INFOFISH

Overall imports of fresh and frozen tuna (excluding

loins and fi llets) into Japan totaled 69 000 tonnes during

the fi rst quarter of 2009 compared with 66 900 tonnes

imported during the same period last year. Following the

trend observed in the fresh tuna market, more fi sh was

traded outside the auction hall at the Tsukiji market.

Auction prices of purse seine-caught yellowfi n realised

half the price of longline and pole and line caught fi sh.

Supermarkets were the main customers for these fi sh.

US market very quiet

The opening months of the year saw little activity

in the tuna importing business in the USA. Fresh tuna

consumption was affected by the economic crisis,

with fewer people having sashimi meals. Canned tuna

demand, too, seems to be sluggish. As a substantial share

of canned tuna is used for tuna sandwiches in fast food

outlets, continued increasing unemployment leads to

fewer people buying sandwiches for lunch while at work

Yellowfin

Bigeye

Albacore

Skipjack

Others

0

20

40

60

80

100

120

2002 2003 2004 2005 2006 2007 2008 2009

1000 tonnes

10 Globefi sh Highlights July 2009

TUNA

As a result, all tuna imports declined in the fi rst

three months of the year: -13% for tuna pouches, -

15% for fresh tuna, -9% for frozen tuna loins and -10%

for canned tuna. The latter is the most important tuna

product imported into the USA, accounting for over 60%

of total US tuna imports. In the January – March 2009,

total canned tuna imports were 39 300 tonnes, far below

imports during previous years. Thailand continues to be

the main exporter of this product. This country managed

to increase its exports, despite the overall bleak

situation, and accounts for about half of the US canned

tuna import market. The Philippines and Indonesia, other

top exporters, reported lower shipments of canned tuna

to the US market.

Diffi cult situation for Samoa and Galicia

Tuna canning is an important activity in those parts

of the world where species of tuna used in canning are

landed. The closure of factories has a devastating impact

on the economic structure of the country or region. Two

examples are American Samoa and Spain. Globalization,

which leads to re-location of canneries, is impacting

heavily the socio-economic structure in these areas.

Chicken of the Sea decided to close their factory

in American Samoa and the implications of this decision

for the people and the economy of this island cannot be

understated. Over 2 000 people employed by Chicken

of the Sea will lose their jobs, effectively reducing by

a quarter the active workforce in American Samoa. The

apparent culprit for Chicken of the Sea’s cannery closure

was a 2007 mandate from the US Congress for American

Samoa to match the mainland US minimum wage; a

mandate that has boosted wages from an average of USD

4.00/hour, to a minimum of USD 7.25/hour over the course

of two years. In addition, there are many other factors

that impact negatively the competitiveness of canning in

the American Samoa, such as US tariff reductions at the

World Trade Organization (WTO) and through Free Trade

Agreements (FTAs), competition from low-cost producers

in Thailand and Ecuador, highly variable fuel costs, and

the global economic recession.

Imports

Canned tuna (excl. pouches): USA

............Jan-Dec............ ............Jan-Mar............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Thailand 74.3 66.1 64.7 27.4 17.7 19.1

Philippines 35.2 26.6 25.9 8.5 9.9 8.6

Indonesia 16.4 14.1 13.5 5.5 5.5 4.3

Ecuador 4.4 1.9 0.7 3.7 0.4 0.6

Others 22.2 25.3 27.8 8.8 10.6 6.7

Total 152.5 134.0 132.6 53.9 44.1 39.3

Source: NFMS: GLOBEFISH AN 11032

Imports

Fresh Tuna : USA

............Jan-Dec............ ............Jan-Mar............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Albacore 0.9 0.9 0.7 0.2 0.1 0.2

Yellowfi n 17.8 18.0 15.9 4.5 4.2 3.5

Bigeye 4.9 5.6 5.5 1.4 1.5 1.3

Bluefi n 1.1 1.1 0.4 0.3 0.1 0.1

Skipjack 0.1 0.0 0.0 0.0 0.0 0.0

Others 0.4 0.1 0.2 0.1 0.1 0.0

Total 25.2 25.7 22.7 6.5 6.0 5.1

Source: ITN

Imports

Tuna loins: USA

............Jan-Dec............ ............Jan-Mar............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Thailand 12.5 7.8 14.9 1.1 3.3 2.1

Fiji 12.4 11.0 10.7 1.7 2.5 2.6

Trin & Tob 12.3 10.5 9.7 2.3 2.5 2.3

Ecuador 4.0 1.2 0.9 0.6 0.1 0.0

Others 9.9 13.3 9.0 3.2 2.6 2.8

Total 51.1 43.8 45.2 8.9 10.8 9.8

Source: NFMS: GLOBEFISH AN 11056

Imports

Canned tuna: France

............Jan-Dec............ ............Jan-Mar............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

C. d’Ivoire 23.1 27.0 22.0 7.8 7.7 6.8

Spain 22.0 19.9 14.2 4.8 3.7 3.7

Madagascar 15.4 10.9 5.6 3.1 2.6 3.1

Seychelles 14.7 13.6 11.7 2.8 2.4 1.7

Italy 8.9 3.5 2.3 0.7 0.9 0.1

Senegal 1.1 1.7 0.9 0.7 0.3 0.4

Others 35.2 29.7 27.1 6.9 6.2 8.9

Total 120.4 106.3 83.7 26.8 23.8 24.7

Source: GLOBEFISH AN 11030

11Globefi sh Highlights July 2009

TUNA

Chicken of the Sea plans to return some of its tuna

canning activities to the USA, and is spending USD 20

million to open canning operations in Lyons, Georgia. This

new plant will employ 200 people and will take advantage

of the relative decrease in utility costs, shipping costs

and input material costs. American Samoa’s second

cannery, owned and operated by StarKist says that it

currently has no plan to close its Pago Pago cannery.

Spain’s canned seafood industry, concentrated

mainly in Galicia region, needs to be restructured

to remain competitive, according to ANFACO (The

National Fish and Seafood Canners Association).

The restructuring may include a reduction in the industry’s

production capacity that will lead to early retirement,

low incentive bonus and personnel layoffs. According to

the association, the industry is under constant threat

from increasing imports of canned seafood particularly

from Southeast Asian canners and strong competition

from supermarket brands. There are 67 canneries

in the region employing around 10 000 workers.

Many of the canners have stopped producing their

own brands and instead produce canned seafood for

supermarket brands. Spanish tuna canners are also the

largest importers of pre-cooked tuna loins in Europe. From

the total 85 000 tonnes of pre-cooked loins imported into

the EU last year as raw material for canned tuna, more

than 45 000 tonnes went to Spain.

Although current demand from the Spanish market

is described as being soft, skipjack 1.8 kg up is now being

traded at EUR 900/tonne, up from EUR 800/tonne, while

whole round yellowfi n 10 kg up is offered at EUR 1 500/

tonne.

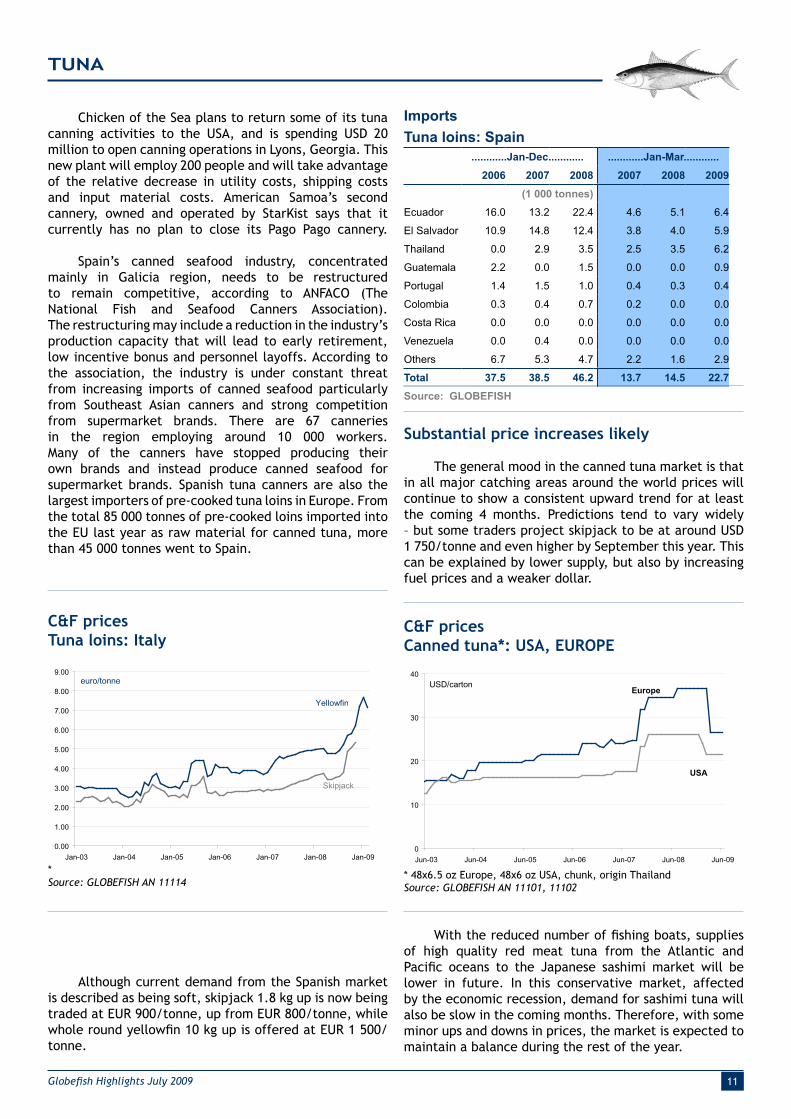

Imports

Tuna loins: Spain

............Jan-Dec............ ............Jan-Mar............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Ecuador 16.0 13.2 22.4 4.6 5.1 6.4

El Salvador 10.9 14.8 12.4 3.8 4.0 5.9

Thailand 0.0 2.9 3.5 2.5 3.5 6.2

Guatemala 2.2 0.0 1.5 0.0 0.0 0.9

Portugal 1.4 1.5 1.0 0.4 0.3 0.4

Colombia 0.3 0.4 0.7 0.2 0.0 0.0

Costa Rica 0.0 0.0 0.0 0.0 0.0 0.0

Venezuela 0.0 0.4 0.0 0.0 0.0 0.0

Others 6.7 5.3 4.7 2.2 1.6 2.9

Total 37.5 38.5 46.2 13.7 14.5 22.7

Source: GLOBEFISH

Substantial price increases likely

The general mood in the canned tuna market is that

in all major catching areas around the world prices will

continue to show a consistent upward trend for at least

the coming 4 months. Predictions tend to vary widely

– but some traders project skipjack to be at around USD

1 750/tonne and even higher by September this year. This

can be explained by lower supply, but also by increasing

fuel prices and a weaker dollar.

C&F prices

Canned tuna*: USA, EUROPE

* 48x6.5 oz Europe, 48x6 oz USA, chunk, origin Thailand

Source: GLOBEFISH AN 11101, 11102

0

10

20

30

40

Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09

USD/carton

USA

Europe

With the reduced number of fi shing boats, supplies

of high quality red meat tuna from the Atlantic and

Pacifi c oceans to the Japanese sashimi market will be

lower in future. In this conservative market, affected

by the economic recession, demand for sashimi tuna will

also be slow in the coming months. Therefore, with some

minor ups and downs in prices, the market is expected to

maintain a balance during the rest of the year.

C&F prices

Tuna loins: Italy

*

Source: GLOBEFISH AN 11114

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

euro/tonne

Yellowfin

Skipjack

12 Globefi sh Highlights July 2009

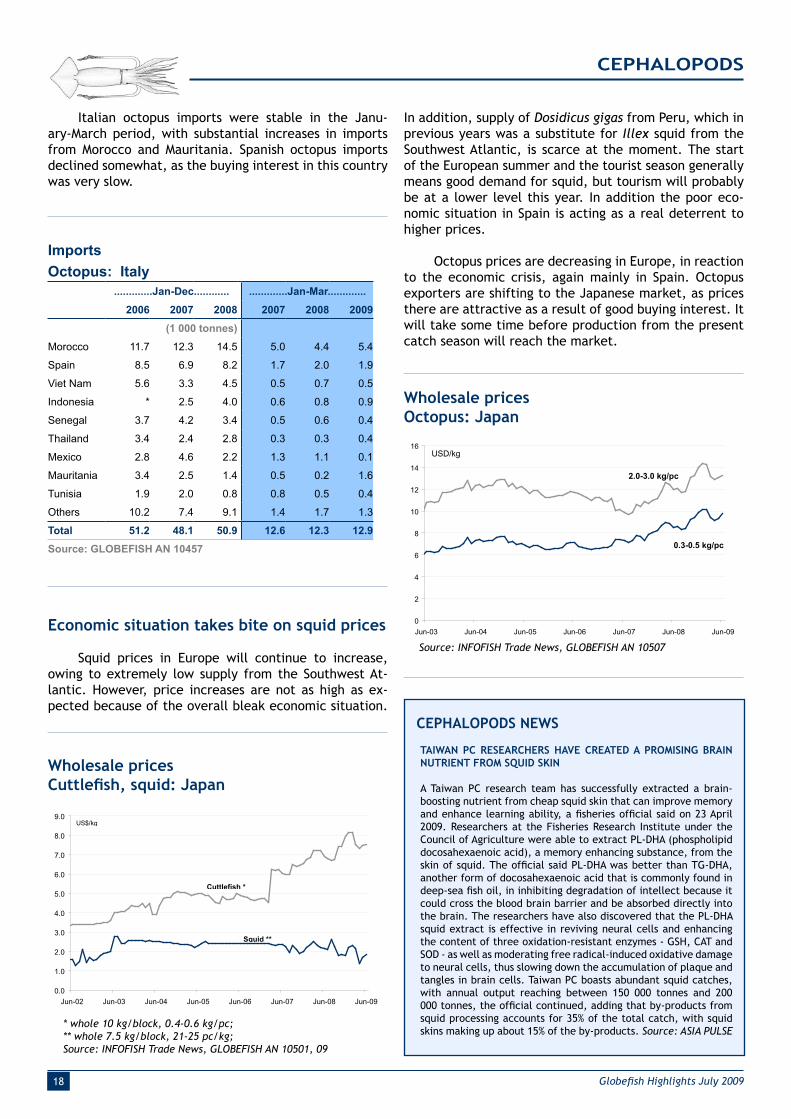

GROUNDFISH

Economic crisis overshadows groundfi sh market

Prices of all groundfi sh species declined sharply in the fi rst half of 2009. The main

reason was lower demand by institutional clients. In addition, cheap cultured fi sh

– pangasius and tilapia – create strong competition in the market. On the positive side,

the return of cod stocks in the Barents Sea and in Newfoundland can be mentioned. In

the latter area, it has taken almost 30 years for the cod stock to recover. Alaska pol-

lack continues to be the main groundfi sh species caught worldwide. For this species,

the situation is bleak in US waters, but higher quotas were given in the Russian fi shing

area. Supply to the market is expected to be abundant in coming months.

C&F prices

Groundfi sh blocks: USA

Source: GLOBEFISH AN 010805, 010806, 010834

Cod stocks recover in Barents Sea

In the Barents Sea, the overall cod biomass is now

the largest it has been since 1968, and the spawning stock

biomass is the highest it has been since the early 1950’s.

The 2008 TAC in the Barents Sea was 430 000 tonnes. For

2009, the TAC is 525 000 tonnes. For 2010 and 2011, it

will increase by another 50 000 tonnes each year.

This means an additional 200 000 tonnes of cod

available in the Barents Sea, between 2008 and 2011 to

which another 30 000 tonnes in Iceland can be added.

Furthermore, surges in cod have been reported

in the Northwestern Atlantic and in parts of Western

Greenland at a time when the market collapse for cod

has bottomed out.

This change in the abundance of cod is caused by

environmental conditions that are making the North

Atlantic a more hospitable habitat. It is interesting to note

that only recently, cod was being red-fl agged on various

environmental lists, and there were demonstrations in

the UK, against retailers who were selling thought to be

‘endangered’ cod.

0.5

1.0

1.5

2.0

2.5

3.0

Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09

USD/lb

Cod

Alaska pollack

Hake

Cod is back in Canada

After almost 30 years cod is back in the the Canadian

Atlantic Ocean. However, this increase in production

in this area has not yet had an impact on the present

groundfi sh market, but it will most likely be felt in the

coming years. The recovery of cod stocks in the Barents

Sea and in the Northwest Atlantic were the subject of a

presentation made at the Brussels Seafood Exhibition. It

reported that cod stocks are at their highest levels in three

decades. While the effect of possible increased catches is

not apparent yet, it could impact the groundfi sh market

signifi cantly in coming years.

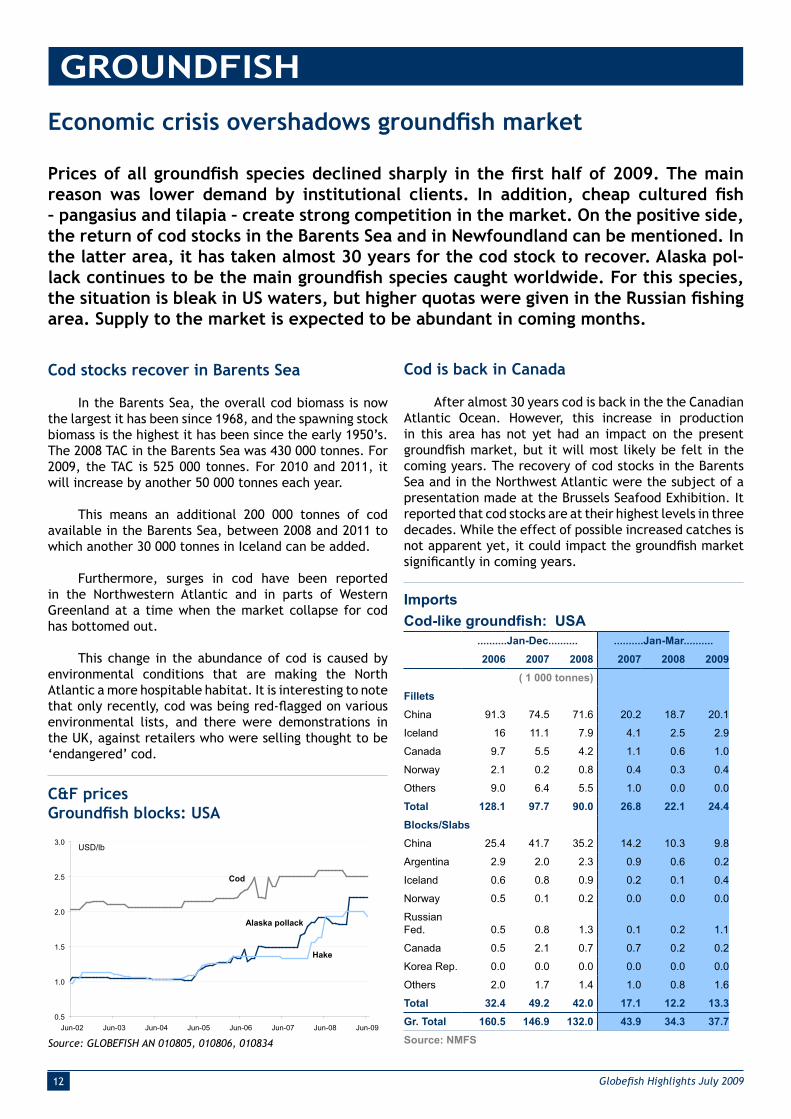

Imports

Cod-like groundfi sh: USA

..........Jan-Dec.......... ..........Jan-Mar..........

2006 2007 2008 2007 2008 2009

( 1 000 tonnes)

Fillets

China 91.3 74.5 71.6 20.2 18.7 20.1

Iceland 16 11.1 7.9 4.1 2.5 2.9

Canada 9.7 5.5 4.2 1.1 0.6 1.0

Norway 2.1 0.2 0.8 0.4 0.3 0.4

Others 9.0 6.4 5.5 1.0 0.0 0.0

Total 128.1 97.7 90.0 26.8 22.1 24.4

Blocks/Slabs

China 25.4 41.7 35.2 14.2 10.3 9.8

Argentina 2.9 2.0 2.3 0.9 0.6 0.2

Iceland 0.6 0.8 0.9 0.2 0.1 0.4

Norway 0.5 0.1 0.2 0.0 0.0 0.0

Russian Fed. 0.5 0.8 1.3 0.1 0.2 1.1

Canada 0.5 2.1 0.7 0.7 0.2 0.2

Korea Rep. 0.0 0.0 0.0 0.0 0.0 0.0

Others 2.0 1.7 1.4 1.0 0.8 1.6

Total 32.4 49.2 42.0 17.1 12.2 13.3

Gr. Total 160.5 146.9 132.0 43.9 34.3 37.7

Source: NMFS

13Globefi sh Highlights July 2009

Cod farming in Norway is experiencing an uncertain

period as it battles to achieve profi tability in the face

of generally poor market conditions and diffi culties in

increasing cod growing rates suffi ciently for economic

production.

Higher imports into US market

Groundfi sh imports into the US maket showed an

increase (10% from 34 300 tonnes to 37 700 tonnes) in the

fi rst quarter of this year compared with the fi rst three

months of 2008 but have not yet recovered to January-

March 2007 levels (43 900 tonnes). This rise refl ects

increased imports by the USA of both frozen fi llets and

blocks. During the fi rst three months of 2009 the quantity

of frozen groundfi sh fi llets imported by the US was 24 400

tonnes, 10% more compared with the same period of the

previous year, whereas imports of blocks went up by 9%.

China is the main supplier of both groundfi sh fi llets and

blocks to the USA with 82% and 74% respectively of total

imports during January-March 2009. This country has

increased its shipments to the US by 7% (fi llets) and 5%

(blocks) in the period under review. China is the major re-

processor of groundfi sh in the world, with strong imports

of raw material from the USA, Russia and Norway.

Prices of all groundfi sh on the US market have

remained stable in the fi rst half of 2009. The cod market,

where prices had been in free fall since November 2008,

seems to have stabilized at a low level. Fillets were

quoted at USD 2.50/lb. Hake fi llets, which followed

the same trend as cod, had a value of USD 2.20/lb for

the whole of this period. Only the Alaska pollack price

declined in June 2009 from USD 2.00/lb to USD 1.93/lb,

back to November 2008 levels.

China dominates European Alaska pollack

market

Moving on to the European groundfi sh market,

German imports of Alaska pollack fi llets which remained

unchanged between the fi rst quarters of 2007 and 2008

only slightly increased (by 5 % to 42 200 tonnes) its

income of this product during January-March 2009. As in

the USA, China is the main exporter to Germany, with

24 200 tonnes of Alaska pollack fi llets in the fi rst months

of 2009, 16% more compared to 2008 and up 23% from

2007. However, the USA, the second main suppplier to

Germany, decreased its exports of Alaska pollack fi llets

to Germany quite strongly (by 53% to 8 300 tonnes during

January-March 2009 compared with the same months of

2008).

Alaska pollack fi llets imports into France have

dropped to 10 100 tonnes (6%) compared with the same

months of 2008 despite the 14% increase in Chinese

supplies. The fi gures indicate that the decrease in imports

can be ascribed to the other suppliers, namely the USA

(-9%), Germany (-7%) and the Russian Federation (-20%).

Imports

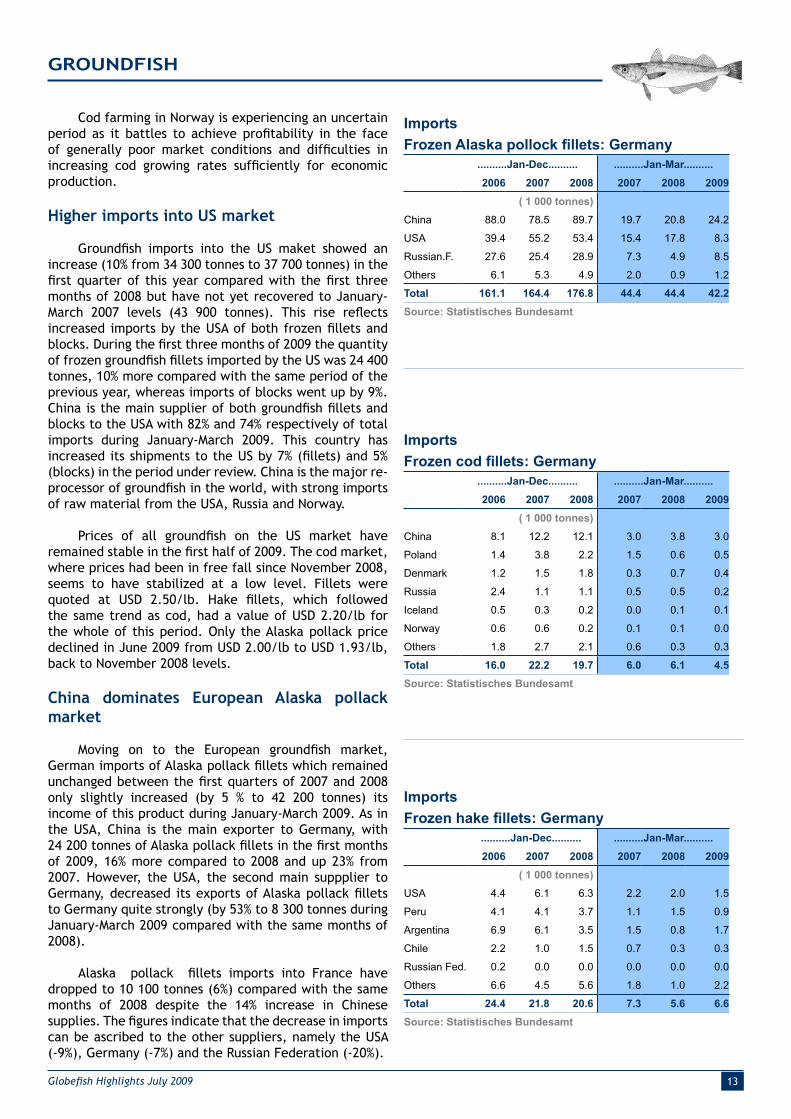

Frozen Alaska pollock fi llets: Germany

..........Jan-Dec.......... ..........Jan-Mar..........

2006 2007 2008 2007 2008 2009

( 1 000 tonnes)

China 88.0 78.5 89.7 19.7 20.8 24.2

USA 39.4 55.2 53.4 15.4 17.8 8.3

Russian.F. 27.6 25.4 28.9 7.3 4.9 8.5

Others 6.1 5.3 4.9 2.0 0.9 1.2

Total 161.1 164.4 176.8 44.4 44.4 42.2

Source: Statistisches Bundesamt

Imports

Frozen cod fi llets: Germany

..........Jan-Dec.......... ..........Jan-Mar..........

2006 2007 2008 2007 2008 2009

( 1 000 tonnes)

China 8.1 12.2 12.1 3.0 3.8 3.0

Poland 1.4 3.8 2.2 1.5 0.6 0.5

Denmark 1.2 1.5 1.8 0.3 0.7 0.4

Russia 2.4 1.1 1.1 0.5 0.5 0.2

Iceland 0.5 0.3 0.2 0.0 0.1 0.1

Norway 0.6 0.6 0.2 0.1 0.1 0.0

Others 1.8 2.7 2.1 0.6 0.3 0.3

Total 16.0 22.2 19.7 6.0 6.1 4.5

Source: Statistisches Bundesamt

Imports

Frozen hake fi llets: Germany

..........Jan-Dec.......... ..........Jan-Mar..........

2006 2007 2008 2007 2008 2009

( 1 000 tonnes)

USA 4.4 6.1 6.3 2.2 2.0 1.5

Peru 4.1 4.1 3.7 1.1 1.5 0.9

Argentina 6.9 6.1 3.5 1.5 0.8 1.7

Chile 2.2 1.0 1.5 0.7 0.3 0.3

Russian Fed. 0.2 0.0 0.0 0.0 0.0 0.0

Others 6.6 4.5 5.6 1.8 1.0 2.2

Total 24.4 21.8 20.6 7.3 5.6 6.6

Source: Statistisches Bundesamt

GROUNDFISH

14 Globefi sh Highlights July 2009

Less cod on German market

German imports of frozen cod fi llets have dropped by

26% in 2009 reaching 4 500 tonnes, mainly caused by the

decline in Chinese exports (by 21% to 3 000 tonnes) but

also by reduced shipments from Denmark and Russia.

During the fi rst quarter of 2009, the UK

imported 15 400 tonnes of frozen cod, the culmination

of a downward trend, fi nishing almost 18% below the

corresponding 2008 fi gure and 43% below the 2007. Again,

the main reason for this decline is the drop in imports

from China (-52% to 3 000 tonnes), the main supplier of

cod to the UK market.

The German market reported a strong positive

trend (+18%) for frozen hake fi llet imports, compared

to 2008, although not achieving 2007 levels. USA (the

leading supplier) and Peru have decreased their exports

of this product to Germany (by 25% and 40% respectively).

Argentina thus accounted for the increase in total hake

fi llet imports.

Italian frozen hake import fi gures show that the

overall situation has not changed at all in the fi rst three

Imports

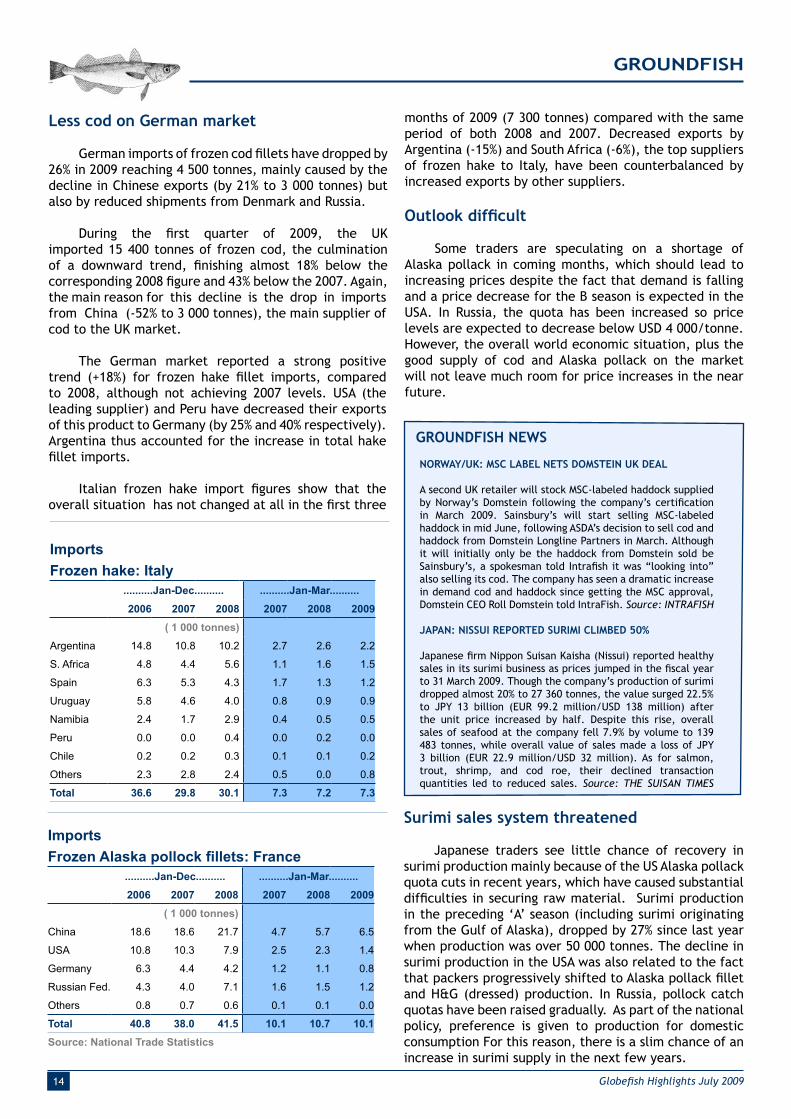

Frozen hake: Italy

..........Jan-Dec.......... ..........Jan-Mar..........

2006 2007 2008 2007 2008 2009

( 1 000 tonnes)

Argentina 14.8 10.8 10.2 2.7 2.6 2.2

S. Africa 4.8 4.4 5.6 1.1 1.6 1.5

Spain 6.3 5.3 4.3 1.7 1.3 1.2

Uruguay 5.8 4.6 4.0 0.8 0.9 0.9

Namibia 2.4 1.7 2.9 0.4 0.5 0.5

Peru 0.0 0.0 0.4 0.0 0.2 0.0

Chile 0.2 0.2 0.3 0.1 0.1 0.2

Others 2.3 2.8 2.4 0.5 0.0 0.8

Total 36.6 29.8 30.1 7.3 7.2 7.3

months of 2009 (7 300 tonnes) compared with the same

period of both 2008 and 2007. Decreased exports by

Argentina (-15%) and South Africa (-6%), the top suppliers

of frozen hake to Italy, have been counterbalanced by

increased exports by other suppliers.

Outlook diffi cult

Some traders are speculating on a shortage of

Alaska pollack in coming months, which should lead to

increasing prices despite the fact that demand is falling

and a price decrease for the B season is expected in the

USA. In Russia, the quota has been increased so price

levels are expected to decrease below USD 4 000/tonne.

However, the overall world economic situation, plus the

good supply of cod and Alaska pollack on the market

will not leave much room for price increases in the near

future.

Imports

Frozen Alaska pollock fi llets: France

..........Jan-Dec.......... ..........Jan-Mar..........

2006 2007 2008 2007 2008 2009

( 1 000 tonnes)

China 18.6 18.6 21.7 4.7 5.7 6.5

USA 10.8 10.3 7.9 2.5 2.3 1.4

Germany 6.3 4.4 4.2 1.2 1.1 0.8

Russian Fed. 4.3 4.0 7.1 1.6 1.5 1.2

Others 0.8 0.7 0.6 0.1 0.1 0.0

Total 40.8 38.0 41.5 10.1 10.7 10.1

Source: National Trade Statistics

Surimi sales system threatened

Japanese traders see little chance of recovery in

surimi production mainly because of the US Alaska pollack

quota cuts in recent years, which have caused substantial

diffi culties in securing raw material. Surimi production

in the preceding ‘A’ season (including surimi originating

from the Gulf of Alaska), dropped by 27% since last year

when production was over 50 000 tonnes. The decline in

surimi production in the USA was also related to the fact

that packers progressively shifted to Alaska pollack fi llet

and H&G (dressed) production. In Russia, pollock catch

quotas have been raised gradually. As part of the national

policy, preference is given to production for domestic

consumption For this reason, there is a slim chance of an

increase in surimi supply in the next few years.

GROUNDFISH

GROUNDFISH NEWS

NORWAY/UK: MSC LABEL NETS DOMSTEIN UK DEAL

A second UK retailer will stock MSC-labeled haddock supplied

by Norway’s Domstein following the company’s certifi cation

in March 2009. Sainsbury’s will start selling MSC-labeled

haddock in mid June, following ASDA’s decision to sell cod and

haddock from Domstein Longline Partners in March. Although

it will initially only be the haddock from Domstein sold be

Sainsbury’s, a spokesman told Intrafi sh it was “looking into”

also selling its cod. The company has seen a dramatic increase

in demand cod and haddock since getting the MSC approval,

Domstein CEO Roll Domstein told IntraFish. Source: INTRAFISH

JAPAN: NISSUI REPORTED SURIMI CLIMBED 50%

Japanese fi rm Nippon Suisan Kaisha (Nissui) reported healthy

sales in its surimi business as prices jumped in the fi scal year

to 31 March 2009. Though the company’s production of surimi

dropped almost 20% to 27 360 tonnes, the value surged 22.5%

to JPY 13 billion (EUR 99.2 million/USD 138 million) after

the unit price increased by half. Despite this rise, overall

sales of seafood at the company fell 7.9% by volume to 139

483 tonnes, while overall value of sales made a loss of JPY

3 billion (EUR 22.9 million/USD 32 million). As for salmon,

trout, shrimp, and cod roe, their declined transaction

quantities led to reduced sales. Source: THE SUISAN TIMES

15Globefi sh Highlights July 2009

Economic crisis impacts world cephalopod market

The world squid market is in a very diffi cult situation. Supply is sharply down in the

Southwest Atlantic, which normally would lead to a substantial price hike, especially

after the extremely low prices of the previous two years. However, the economic crisis

is putting a brake on these price expectations, and even though prices are moving up

somewhat, they are still well below potential levels. Demand for octopus is strong in

Japan, while the European market is rather reluctant to offer higher prices. Future

price developments will depend on the outcome of the fi shing season in the East central

Atlantic, which has just started.

CEPHALOPODS

Squid catches extremely low

The 2009 squid season in the Southwest Atlantic was

a disaster. In the whole area, only 65 000 tonnes of squid

were caught in the fi rst fi ve months of the year, which

compares with 334 000 tonnes of squid caught in the area

during the same period last year. Squid catches around the

Falklands/Malvinas were extremely low, only 45 tonnes

of Illex squid were caught in January to May 2009, which

compares with 94 000 tonnes during the same period of

2008. For Loligo squid the decline was slightly less

dramatic, down from 25 000 tonnes to 13 000

tonnes. Argentina Mainland reported squid catches during

the fi rst fi ve months of the year of 53 000 tonnes, down

from last year’s 220 000 tonnes. In June 2009 there is

practically no more squid fi shing, as the fuel costs are

higher than income.

Exports

Argentina: Squid

....................Jan-April....................

2007 2008 2008 2009

(1 000 tonnes)

Spain 58.4 61.2 26.1 9.7

China 37.6 66.8 15.1 6.4

Brazil 2.3 2.4 0.6 1.6

Japan 10.7 6.2 2.5 2.1

Italy 11.5 9.3 4.2 1.8

Korea, Rep 4.4 4.0 0.7 1.3

Others 24.3 25.5 5.3 5.8

Total 149.2 175.3 54.5 28.7

Source: GLOBEFISH

Imports

Cuttlefi sh: Japan

.............Jan-Dec............ .............Jan-Mar.............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Thailand 12.5 11.5 8.3 2.7 1.8 1.6

Viet Nam 4.7 5.1 4.5 1.3 0.9 1.0

Morocco 3.5 3.9 2.2 0.6 0.3 0.2

Malaysia 2.2 1.6 1.7 0.4 0.3 0.4

Korea Rep. 0.4 0.3 0.6 0.2 0.1 0.1

China 1.5 0.4 0.1 0.1 0.0 0.0

Ghana 0.2 0.5 0.0 0.0 0.0 0.0

Mauritania 0.0 0.1 0.0 0.0 0.0 0.0

Others 3.1 2.6 2.3 0.7 0.6 0.5

Total 28.1 26.0 19.7 6.0 4.0 3.8

Source: GLOBEFISH AN 10439

Squid exports from Argentina were 28 700 tonnes

in the fi rst four months of 2009, almost half the amount

Imports

Squid: USA

.............Jan-Dec............ .............Jan-Mar.............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

China 32.9 28.8 27.7 7.2 5.3 5.5

Thailand 7.4 7.2 8.2 1.6 2.8 1.4

India 8.2 4.5 6.9 1.2 0.9 0.9

Taiwan PC 5.6 5.9 5.4 0.9 1.4 1.5

New Zealand 2.2 2.5 1.0 0.4 0.3 0.2

Rep. Korea 2.8 3.1 5.4 0.6 0.9 1.0

Peru 1.7 0.1 2.0 0.6 0.4 0.7

Others 8.4 10.3 8.5 1.7 1.2 1.2

Total 69.2 62.4 65.1 14.2 13.2 12.4

Source: GLOBEFISH AN 10459

16 Globefi sh Highlights July 2009

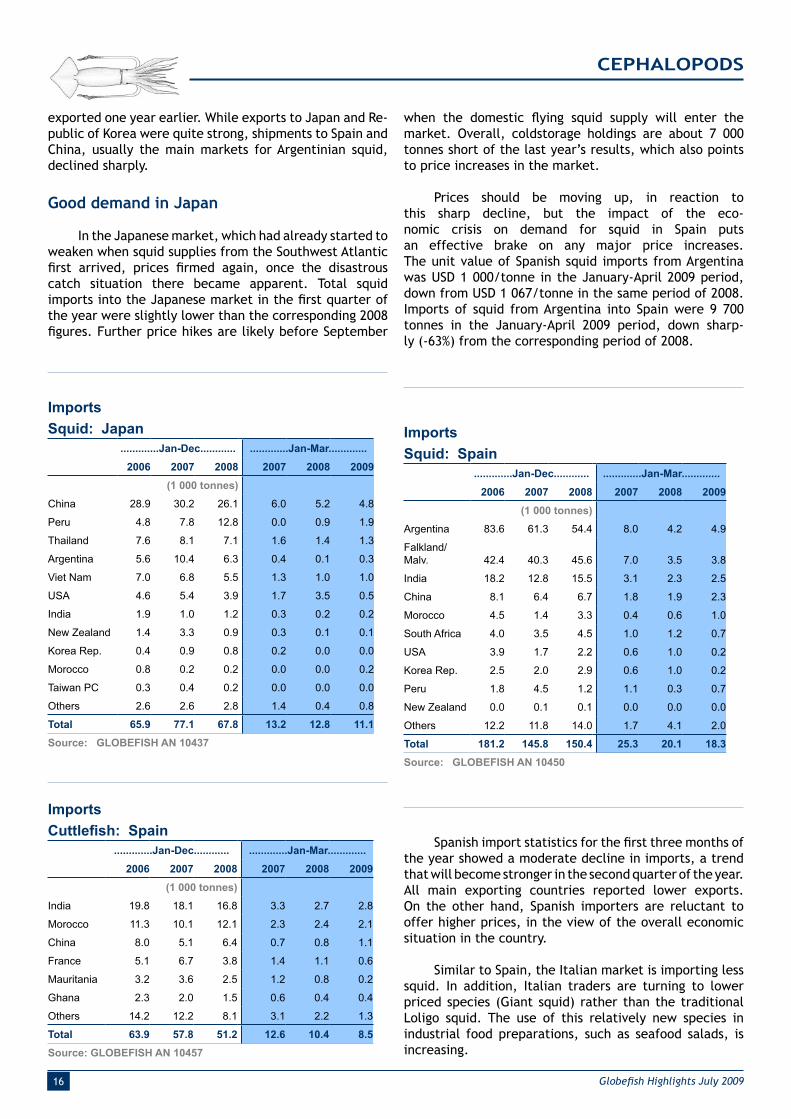

CEPHALOPODS

Imports

Squid: Japan

.............Jan-Dec............ .............Jan-Mar.............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

China 28.9 30.2 26.1 6.0 5.2 4.8

Peru 4.8 7.8 12.8 0.0 0.9 1.9

Thailand 7.6 8.1 7.1 1.6 1.4 1.3

Argentina 5.6 10.4 6.3 0.4 0.1 0.3

Viet Nam 7.0 6.8 5.5 1.3 1.0 1.0

USA 4.6 5.4 3.9 1.7 3.5 0.5

India 1.9 1.0 1.2 0.3 0.2 0.2

New Zealand 1.4 3.3 0.9 0.3 0.1 0.1

Korea Rep. 0.4 0.9 0.8 0.2 0.0 0.0

Morocco 0.8 0.2 0.2 0.0 0.0 0.2

Taiwan PC 0.3 0.4 0.2 0.0 0.0 0.0

Others 2.6 2.6 2.8 1.4 0.4 0.8

Total 65.9 77.1 67.8 13.2 12.8 11.1

Source: GLOBEFISH AN 10437

Imports

Squid: Spain

.............Jan-Dec............ .............Jan-Mar.............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Argentina 83.6 61.3 54.4 8.0 4.2 4.9

Falkland/Malv. 42.4 40.3 45.6 7.0 3.5 3.8

India 18.2 12.8 15.5 3.1 2.3 2.5

China 8.1 6.4 6.7 1.8 1.9 2.3

Morocco 4.5 1.4 3.3 0.4 0.6 1.0

South Africa 4.0 3.5 4.5 1.0 1.2 0.7

USA 3.9 1.7 2.2 0.6 1.0 0.2

Korea Rep. 2.5 2.0 2.9 0.6 1.0 0.2

Peru 1.8 4.5 1.2 1.1 0.3 0.7

New Zealand 0.0 0.1 0.1 0.0 0.0 0.0

Others 12.2 11.8 14.0 1.7 4.1 2.0

Total 181.2 145.8 150.4 25.3 20.1 18.3

Source: GLOBEFISH AN 10450

Imports

Cuttlefi sh: Spain

.............Jan-Dec............ .............Jan-Mar.............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

India 19.8 18.1 16.8 3.3 2.7 2.8

Morocco 11.3 10.1 12.1 2.3 2.4 2.1

China 8.0 5.1 6.4 0.7 0.8 1.1

France 5.1 6.7 3.8 1.4 1.1 0.6

Mauritania 3.2 3.6 2.5 1.2 0.8 0.2

Ghana 2.3 2.0 1.5 0.6 0.4 0.4

Others 14.2 12.2 8.1 3.1 2.2 1.3

Total 63.9 57.8 51.2 12.6 10.4 8.5

Source: GLOBEFISH AN 10457

exported one year earlier. While exports to Japan and Re-

public of Korea were quite strong, shipments to Spain and

China, usually the main markets for Argentinian squid,

declined sharply.

Good demand in Japan

In the Japanese market, which had already started to

weaken when squid supplies from the Southwest Atlantic

fi rst arrived, prices fi rmed again, once the disastrous

catch situation there became apparent. Total squid

imports into the Japanese market in the fi rst quarter of

the year were slightly lower than the corresponding 2008

fi gures. Further price hikes are likely before September

Spanish import statistics for the fi rst three months of

the year showed a moderate decline in imports, a trend

that will become stronger in the second quarter of the year.

All main exporting countries reported lower exports.

On the other hand, Spanish importers are reluctant to

offer higher prices, in the view of the overall economic

situation in the country.

Similar to Spain, the Italian market is importing less

squid. In addition, Italian traders are turning to lower

priced species (Giant squid) rather than the traditional

Loligo squid. The use of this relatively new species in

industrial food preparations, such as seafood salads, is

increasing.

when the domestic fl ying squid supply will enter the

market. Overall, coldstorage holdings are about 7 000

tonnes short of the last year’s results, which also points

to price increases in the market.

Prices should be moving up, in reaction to

this sharp decline, but the impact of the eco-

nomic crisis on demand for squid in Spain puts

an effective brake on any major price increases.

The unit value of Spanish squid imports from Argentina

was USD 1 000/tonne in the January-April 2009 period,

down from USD 1 067/tonne in the same period of 2008.

Imports of squid from Argentina into Spain were 9 700

tonnes in the January-April 2009 period, down sharp-

ly (-63%) from the corresponding period of 2008.

17Globefi sh Highlights July 2009

Coldstorage holdings

Cuttlefi sh and Squid: Japan

*NEI

Source: INFOFISH Trade News, GLOBEFISH AN 10507

0

20

40

60

80

100

120

140

160

Apr-01 Apr-02 Apr-03 Apr-04 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09

1 000 MT

Cuttlefish

NEI*

Squid

Imports

Octopus: Japan

.............Jan-Dec............ .............Jan-Mar.............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Mauritania 16.6 14.0 12.6 3.8 4.0 4.2

Morocco 8.7 10.3 10.9 1.6 0.5 0.5

China 8.2 7.2 6.7 1.3 2.3 1.0

Viet Nam 5.5 4.8 5.5 1.1 0.8 1.1

Spain 4.0 1.8 2.7 0.5 1.2 0.4

Thailand 1.9 1.8 1.2 0.5 0.3 0.3

Others 3.5 6.9 5.1 0.5 2.3 0.4

Total 48.4 46.8 44.7 9.3 11.4 7.9

Source: GLOBEFISH AN 10438

Imports

Octopus: Spain

.............Jan-Dec............ .............Jan-Mar.............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Morocco 20.2 19.6 23.2 7.9 6.3 5.1

Mauritania 4.9 4.9 4.5 1.3 1.0 2.3

China 2.8 1.6 1.8 0.4 0.4 0.3

Viet Nam 1.9 2.2 1.6 0.9 0.3 0.4

Portugal 1.4 1.7 2.2 0.2 0.9 0.3

Senegal 0.5 0.5 0.6 0.1 0.1 0.1

Others 8.6 8.8 8.7 2.6 2.3 1.0

Total 40.3 39.3 42.6 13.4 11.3 9.5

Source: GLOBEFISH AN 10452

Imports

Squid: Italy

.............Jan-Dec............ .............Jan-Mar.............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

Thailand 21.2 22.8 23.4 4.6 5.5 4.7

Spain 30.3 25.2 22.1 7.6 6.3 6.8

Argentina 8.9 10.7 10.0 0.7 0.6 0.4

S. Africa 5.0 3.7 3.7 1.4 0.7 0.7

India 3.8 2.9 3.5 0.7 0.6 1.0

Peru 3.4 3.4 0.9 0.6 0.1 1.1

New Zealand 2.3 0.1 0.1 0.0 0.0 0.0

Others 22.8 32.8 23.2 5.2 6.0 4.1

Total 97.7 101.6 86.9 20.8 19.8 18.8

Source: GLOBEFISH AN 10455

Imports

Cuttlefi sh: Italy

.............Jan-Dec............ .............Jan-Mar.............

2006 2007 2008 2007 2008 2009

(1 000 tonnes)

France 5.9 6.7 5.6 1.1 1.7 1.1

Spain 4.8 3.7 4.6 0.8 1.0 0.9

Tunisia 3.1 5.1 4.1 1.3 1.2 0.9

Senegal 2.2 2.4 1.9 0.5 0.5 0.4

Viet Nam 1.7 0.8 1.0 0.3 0.2 0.1

Morocco 1.1 0.8 1.0 0.1 0.1 0.2

India 2.9 0.9 0.7 0.3 0.2 0.3

China 0.5 0.1 0.6 0.0 0.1 0.1

Thailand 1.6 0.3 0.2 0.0 0.1 0.1

Others 9.1 5.9 5.5 1.4 1.1 0.5

Total 32.9 26.7 25.2 5.8 6.2 4.6

Source: GLOBEFISH AN 10439

High prices offered for octopus

Octopus fi shing has recently started in Mauritania

and Morocco. As usually at the beginning of the catch-

ing season, after a long period of fi shing bans, catches

are good and specimens are large. However, the expec-

tations are for smaller octopus to be caught soon, and

lower catches to be reported.

Octopus traders in Japan are offering higher prices

than Europe at the moment, and there was a substantial

shift in exports towards this market during the second

quarter of the year. During the fi rst quarter of 2009, oc-

topus imports into Japan declined sharply. As a result,

coldstorage holdings went down in recent months, and

traders are fi lling the gap. Prices of octopus in the Japa-

nese market are moving up, helped by a relatively strong

yen.

CEPHALOPODS

18 Globefi sh Highlights July 2009

CEPHALOPODS NEWS

TAIWAN PC RESEARCHERS HAVE CREATED A PROMISING BRAIN

NUTRIENT FROM SQUID SKIN

A Taiwan PC research team has successfully extracted a brain-

boosting nutrient from cheap squid skin that can improve memory

and enhance learning ability, a fi sheries offi cial said on 23 April

2009. Researchers at the Fisheries Research Institute under the

Council of Agriculture were able to extract PL-DHA (phospholipid

docosahexaenoic acid), a memory enhancing substance, from the

skin of squid. The offi cial said PL-DHA was better than TG-DHA,

another form of docosahexaenoic acid that is commonly found in

deep-sea fi sh oil, in inhibiting degradation of intellect because it

could cross the blood brain barrier and be absorbed directly into

the brain. The researchers have also discovered that the PL-DHA

squid extract is effective in reviving neural cells and enhancing

the content of three oxidation-resistant enzymes - GSH, CAT and

SOD - as well as moderating free radical-induced oxidative damage

to neural cells, thus slowing down the accumulation of plaque and

tangles in brain cells. Taiwan PC boasts abundant squid catches,

with annual output reaching between 150 000 tonnes and 200

000 tonnes, the offi cial continued, adding that by-products from

squid processing accounts for 35% of the total catch, with squid

skins making up about 15% of the by-products. Source: ASIA PULSE

Imports