islamic money market ppt

TRANSCRIPT

Islamic Money Market

ECON 6862: Islamic Capital Markets

Dr. Zaharuddin Abd Rahman

7th March 2017

Group Members

• Ahmad Tarmizi Bin Abdul Aznan G1620511

• Saliou Boiro G1515999

• Conde Mamoudou G1612561

• Mohd Asraf Abd Wahab G1514689

• Mohamed Moharam Fahmy Abouzeid G1414099

2

1) Overview

2) Functions of Islamic Money Market

3) Comparison between Islamic and Conventional Money Market

4) Islamic Interbank Market

5) Islamic Money Market Instruments

6) Islamic Money Market Calculations

Presentation Outline – Islamic Money Market

3

4

Overview

FLOW OF FUNDS

DIRECT INDIRECT

The investor has full control

over his funds. He is the one

who invest the funds, monitor

its performance, and take

corrective actions in his

investments.

The investor appointed an

agent to invest his funds and

monitor its performance (on his

behalf). In return, the agent will

be compensated with certain

fees for his services.

Eg: Investment in the capital

market (stock exchange), money

market and banks.

Eg: Investment through

intermediaries such as mutual

funds, pension funds and

investment banks.

5

INVESTMENT IN FINANCIAL

MARKET (“Direct” flow of funds)

Medium & Long-term

(Capital market instrument)

Short-term

(Money market instrument)

Between 1 to 10 years

(Medium)

More than 10 years (Long-term)

Less than 1 year (Short-

term)

Instruments: Stocks and bonds

Instruments: Treasury Bills,

Commercial Papers,

Certificate of Deposits

6

So, what is the function of Islamic money market??

7

• The first and foremost important underlying philosophy of Islamic Capital and

Money market is to strengthen the institutional structure of Islamic banking

operations.

• The main function is to facilitate transfer of investable funds from those having

surplus units to those requiring funds to meet short and long term liquidity needs.

• IMM mainly concern with Interbank players, but there are also IMM products such

as Islamic Accepted Bills for importers and exporters to provide short term

working capital financing.

• Beside the main function of channelling surplus units to deficit units, Islamic

Money Market plays also the role of:

Liquidity Management

Facilitate secondary trading of Islamic MM instruments

Channel for Central Bank to conduct their monetary policy

Functions of Islamic Money Market (1)

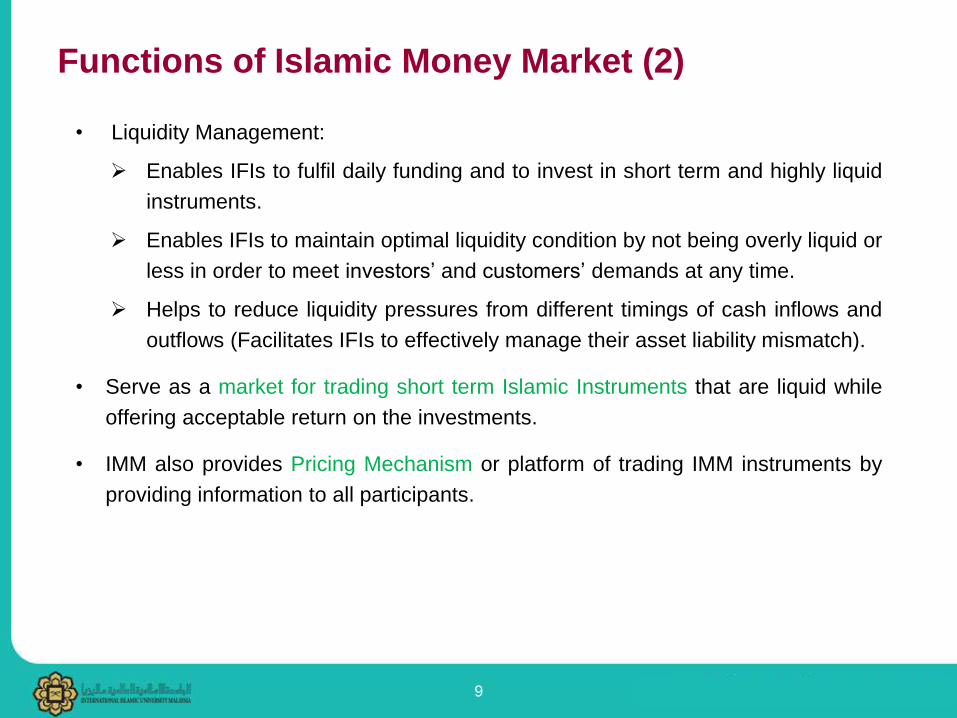

8

• Liquidity Management:

Enables IFIs to fulfil daily funding and to invest in short term and highly liquid

instruments.

Enables IFIs to maintain optimal liquidity condition by not being overly liquid or

less in order to meet investors’ and customers’ demands at any time.

Helps to reduce liquidity pressures from different timings of cash inflows and

outflows (Facilitates IFIs to effectively manage their asset liability mismatch).

• Serve as a market for trading short term Islamic Instruments that are liquid while

offering acceptable return on the investments.

• IMM also provides Pricing Mechanism or platform of trading IMM instruments by

providing information to all participants.

Functions of Islamic Money Market (2)

9

• Tool for CB to conduct their Monetary Policy (indirectly) because the primary objective of BNM’s

monetary operations in the IMM is to ensure sufficient liquidity for the efficient functioning of the

IMM.

• The monetary policy target is only implemented in the conventional money market, where interest

rate based instruments are the primary funding instrument.

• BNM influences Islamic interbank market liquidity through an array of Shariah-compliant

instruments, the main instrument being the Qard (lending) and Commodity Murabahah Program.

• For longer-term liquidity management, the Bank issues Bank Negara Monetary Notes-i (BNMN-i)

which are structured based on Islamic concepts of Murabahah (BNMN-Murabahah), Ijarah (BNMN-

Ijarah), Bai Bithaman Ajil (BNMN-BBA) and Istithmar (BNMN-Istithmar) i.e. investment, combined

structure of Ijarah and Murabahah

• In short, an BNM’s short term Islamic operations:

Provide short term financing to banks and other FIs

Manage liquidity issues and indirectly adjust benchmark rates in MM

Changes in liquidity and benchmark rates in MM will influence the liquidity and rates of return

in other markets.

Functions of Islamic Money Market (3)

10

Difference between Islamic and conventional

money markets

11

Islamic Conventional

Interbank market Utilises shariah compliant contracts

such as murabahah, mudarabah,

and wakalah.

Debt contract is used for

placement of funds

Issuance process Must be shariah compliant and

approved by both SAC of BNM and

SCM

Approved by regulatory authority

only.

Types of structure Structured based on asset,

equity and debt

Structured based on debt only

Investors Both Islamic and conventional Conventional only

Money market

instuments

Deposits type:

Mudharabah Interbank Investment,

Wadiah Acceptance, Qard,

Commodity Murabahah, Wakalah

Deposit, Investment Account

Platform (IAP)

Deposits type:

Interbank placement (deposit),

12

Islamic Conventional

Money market instruments Paper Type:

Bank Negara Monetary Notes-i

(BNMN-i), Sukuk Bank Negara

Malaysia Ijarah (SBNMI), Malaysian

Islamic Treasury bills (MITB),

Islamic Negotiable Instruments of

Deposit (INID) – Mudharabah based,

Negotiable Islamic Debt Certificate

(NIDC) – sales of bank’s asset and

repurchase

Collaterised Lending:

Sell and Buy Back Agreement

(SBBA)

Working Capital:

Islamic Accepted Bills (IAB)

Paper Type:

Bank Negara Monetary Notes

(BNMN), Malaysian Treasury bills

(MTB),

Certificate of deposit, Commercial

paper;

Collaterised Lending:

Repurchase agreements

Working Capital:

Bankers Acceptance

13

Islamic Interbank Market

14

Islamic Banking Represents 23% of Total Banking Asset

presently

92,337.8

320,518.5

572,860.6

1,094,371.0

1,423,879.3

1,870,744.0

0.0

200,000.0

400,000.0

600,000.0

800,000.0

1,000,000.0

1,200,000.0

1,400,000.0

1,600,000.0

1,800,000.0

2,000,000.0

Dec-2007 Dec-2011 Dec-2016

RM mio Banking System Total Asset

Islamic Banks Conventional Banks

8%

92%

Banking System Total Asset, Dec-2007

Islamic Banks Conventional Banks

23%

77%

Banking System Total Asset, Dec-2016

Islamic Banks Conventional Banks

Source: BNM Monthly Statistical Bulletin15

Islamic Interbank Market – The Players

16

• Previously, many are

windows to conventional

banks, but now all are

recognized as proper Islamic

Banks

• 10 locally owned Islamic

banks and 6 foreign owned

• International Islamic Bank –

only operate in non-Ringgit

Malaysia business

Source: BNM website

Islamic Interbank Market Turnover in Malaysia

Source: BNM Monthly Statistical Bulletin17

36,847.241,209.3

37,827.0

10,170.0

0.0 0.00.0

5,000.010,000.015,000.020,000.025,000.030,000.035,000.040,000.045,000.0

MudharabahDeposits

Wadiah/QardDeposits

CommodityMurabahahDeposits

IslamicNegotiableInstrumentof Deposit

WakalahDeposits

IslamicBankers

Acceptance

RM mio

Turnover of Interbank Islamic Money Market in Dec-2016

93,486.7

10,130.6 7,015.8 7,674.2 2,320.0 923.1

-

10,000.0

20,000.0

30,000.0

40,000.0

50,000.0

60,000.0

70,000.0

80,000.0

90,000.0

100,000.0

MudharabahDeposits

Wadiah/QardDeposits

CommodityMurabahahDeposits

IslamicNegotiableInstrumentof Deposit

WakalahDeposits

IslamicBankers

Acceptance

RM mio

Turnover of Interbank Islamic Money Market in Dec-2012

29%

33%

30%

8%

Turnover of Interbank Islamic Money Market in Dec-2016

Mudharabah Deposits

Wadiah/Qard Deposits

Commodity Murabahah Deposits

Islamic Negotiable Instrument of Deposit

77%

8%

6%6%

2%1%

Turnover of Interbank Islamic Money Market in Dec-2012

Mudharabah Deposits

Wadiah/Qard Deposits

Commodity Murabahah Deposits

Islamic Negotiable Instrument of Deposit

Wakalah Deposits

Islamic Bankers Acceptance

Islamic Money Market League Table

Source: BNM’s Bond Info Hub website18

League Table by Instruments

Source: BNM’s Bond Info Hub website19

League Table by Instruments (con’t)

Source: BNM’s Bond Info Hub website20

Islamic Interbank Market Transacted Tenor: Mainly in

Overnight, sparse in 1-week to 3-month tenors

Source: BNM website21

Outright Sales &

Purchases of Securities

Statutory Reserve

Requirement

Qard

(Borrowing)

Sukuk BNM

Ijarah

Commodity

Murabahah

Programme

(CMP)

Conventional Islamic

Bank Negara

Monetary

Notes Islamic

(BNMN-i)

Up to 1-month

Up to 3-months

Up to 6-months

Up to 1-year

Common Instruments

to both Conventional

and Islamic System

Money market

borrowings

Bank Negara

Monetary

Notes

(BNMNs)

Foreign

Currency

Swaps

Shorter term money market transactions of up to 3-month tenor focus on Qard (borrowing) and

Commodity Murabahah

Repo and

Reverse

Repo

Islamic Interbank Money Market Transactions with the

Central Bank (BNM)

22 Source: BNM

Interbank Market with BNM: BNM announces money market

transactions to be conducted every morning @9.30 am

• Table showed how much

Islamic balances that will be

placed with BNM (RM12.03

billion):

• RM3.3 billion = Qard of 7 to

28 days

• RM0.5 billion = Commodity

Murabahah of 28 days

• Balance of RM8.2 billion =

Overnight Qard (1-day)

23 Source: Fully Automated System for Issuing/Tendering (FAST)

Islamic Money Market Instruments

24

Types of Instruments in Islamic Money Market

• Mudarabah Interbank Investment (MII)

• Wadiah acceptance

• Qard

• Commodity Murabahah Program

• Bank Negara Monetary Notes-i (BNMN-i)

• Islamic Accepted Bills (IAB)

• Islamic Negotiable Instruments (INI)

• These are among the more popular IMM instruments presently traded in

Malaysia

25

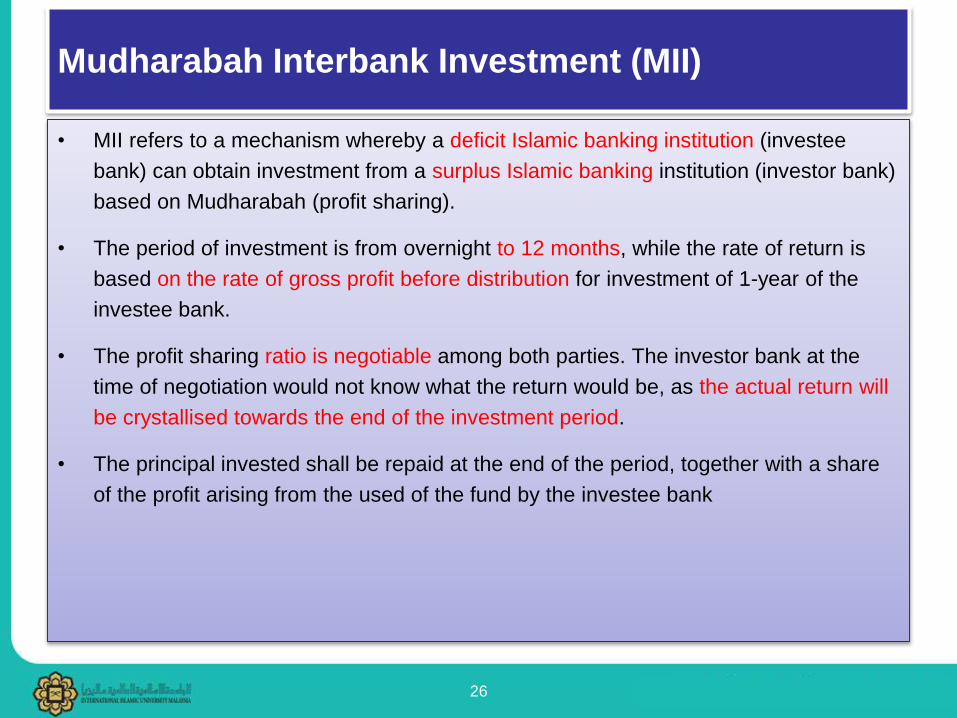

Mudharabah Interbank Investment (MII)

• MII refers to a mechanism whereby a deficit Islamic banking institution (investee

bank) can obtain investment from a surplus Islamic banking institution (investor bank)

based on Mudharabah (profit sharing).

• The period of investment is from overnight to 12 months, while the rate of return is

based on the rate of gross profit before distribution for investment of 1-year of the

investee bank.

• The profit sharing ratio is negotiable among both parties. The investor bank at the

time of negotiation would not know what the return would be, as the actual return will

be crystallised towards the end of the investment period.

• The principal invested shall be repaid at the end of the period, together with a share

of the profit arising from the used of the fund by the investee bank

26

Wadiah Acceptance

• Wadiah Acceptance, is a transaction between BNM and the Islamic banking

institutions.

• It refers to a mechanism whereby the Islamic banking institutions placed their surplus

fund with BNM based on the concept of Al- Wadiah.

• Under this concept, the acceptor of funds is viewed as the custodian for the funds

and there is no obligation on the part of the custodian to pay any return on the

account.

• However, if there is any dividend paid by the custodian, is perceived as 'hibah' (gift).

• The Wadiah Acceptance facilitates BNM's liquidity management operation as it gives

flexibility for BNM to declare dividend without having to invest the funds received.

27

Qard

28

Commodity Murabahah Program (CMP)

29

Bank Negara Monetary Notes (BNMN-i)

• BNMN-i are Islamic securities issued by BNM replacing previous Bank Negara

Negotiable Notes (BNNN) for purposes of managing liquidity in the Islamic financial

market

• The maturity has also been lengthened from one year to three years.

• Issued either on a discounted (usually) or a coupon-bearing basis depending on

investors' demand.

• Discount-based BNMN-i will be traded using the same market convention as the

existing BNMN and Malaysian Islamic Treasury Bills (MITB) while the profit-based

BNMN-i will adopt the market convention of Government Investment Issues (GII).

• Highly attractive because: they are default risk free + highly liquid with a relatively

deep secondary market

• Central Bank use it to soak up or inject liquidity into an Islamic banking system or

conduct open market operations.

30

Islamic Accepted Bills (IAB)

• Objective: to encourage and promote both domestic and foreign trade, by providing

Malaysian traders with an attractive Islamic financing product.

• The IAB is formulated on the Islamic principles of Al-Murabahah (deferred lump-sum

sale or cost-plus) and Bai ad-Dayn (debt-trading).

• Al-Murabahah refers to the selling of merchandise at a price based on cost-plus profit

margin agreed to by both parties (importer/exporter with banks)

• Bai Al-Dayn refers to the sale of a debt arising from a trade transaction in the form of

a deferred payment sale.

31

Islamic Negotiable Instruments (INI)

i) Islamic Negotiable Instruments of Deposit (INID)

• The applicable concept is Al-Mudharabah. It refers to a sum of money deposited with

the Islamic banking institutions and repayable to the bearer on a specified future date

at the nominal value of INID plus declared dividend.

ii) Negotiable Islamic Debt Certificate (NIDC)

• The transaction involves the sale of banking institution's assets to the customer at an

agreed price on cash basis. Subsequently the assets is purchased back from the

customer at principal value plus profit and to be settled at an agreed future date.

32

Islamic Money Market Calculations

33

Mudarabah Interbank Investment

34

Wadiah and Qard

35

• Hibah computation is based on the followings:-

• Principal (P) X Time (T) X Rate quoted *

Example:

Tier Range Rate (% p.a)

Tier 1 Up to RM 1,000 1.05 %

Tier 2 RM 1,001 to RM 5,000 1.85 %

Tier 3 RM 5,001 and above 2.54 %

Hence compute WSA with balance of RM 7,000 for whole of January 03 based on the above hibah rates.

31/365 X 1.05% X 1,000 = RM 0.89

31/365 X 1.85% X 4,000 = RM 6.28

31/365 x 2.54% x 2,000 = RM 4.31

Total hibah = RM 11.48

Commodity Murabahah Program

36

Profit = Principal (P) X Rate (R)

Discounted Notes = BNMN-I and MITB

37

Discount = (Par Value – Purchase Price) X 365 x 100Par Value T

3.22 = (100 – 96.893) X 365 x 100 Yield96.893 364

3.116 = (100 – 96.893) X 365 x 100 Discount100 364

Islamic Accepted Bills (IAB) - Import

38

Islamic Accepted Bills (IAB) - Export

39

Islamic Negotiable Instruments (INI)

40

Profit = Principal (P) X Time

(T) X Rate quoted net Profit

Sharing Ratio

Thank you and Q&A

41