is bitcoin like gold? an examination of the hedging and safe haven properties of the virtual...

DESCRIPTION

Whilst there has been significant focus on the virtual currency bitcoin in the financial media, to date there has been limited academic discourse in the economic and financial literature. This dissertation is a first attempt at exploring the developing correlations between bitcoin and more traditional asset classes. In particular I attempt to answer a specific question: Is bitcoin like gold? I qualitatively discuss the theory underlying this idea with reference to bitcoin’s decentralised nature, fixed money supply and creation by “mining”. In addition I focus on gold’s role as a hedge and a safe haven for stocks, bonds and currencies with a view to determining whether bitcoin could play a similar role. Using a GARCH analysis for the US and EU I find that for the most part bitcoin returns are statistically independent of equity and bond markets due to the low correlations estimated. An interesting finding of my research is that bitcoin may play a weak hedge and safe haven role for sovereign debt markets in the US and Europe, which could be explained by its exogeneity to the global network of financial institutions and governments. I also find that bitcoin may be a hedge for the euro, but not for the dollar. In addition the estimated coefficients for currency markets are consistently larger than those representing equities or bonds, supporting the idea that bitcoin is an alternative monetary asset.TRANSCRIPT

Is Bitcoin like Gold?

An Examination of the Hedging and Safe Haven

Properties of the Virtual Currency

Report on research presented in partial fulfilment of the requirements

of the examination for

MASTER OF SCIENCE IN FINANCE

Cormac Ennis

Supervisor: Dr. Constantin Gurdgiev

Trinity College Dublin

August 2013

i

Abstract

Whilst there has been significant focus on the virtual currency bitcoin in the

financial media, to date there has been limited academic discourse in the

economic and financial literature. This dissertation is a first attempt at

exploring the developing correlations between bitcoin and more traditional

asset classes. In particular I attempt to answer a specific question: Is bitcoin

like gold? I qualitatively discuss the theory underlying this idea with reference

to bitcoin’s decentralised nature, fixed money supply and creation by “mining”.

In addition I focus on gold’s role as a hedge and a safe haven for stocks,

bonds and currencies with a view to determining whether bitcoin could play a

similar role. Using a GARCH analysis for the US and EU I find that for the

most part bitcoin returns are statistically independent of equity and bond

markets due to the low correlations estimated. An interesting finding of my

research is that bitcoin may play a weak hedge and safe haven role for

sovereign debt markets in the US and Europe, which could be explained by

its exogeneity to the global network of financial institutions and governments.

I also find that bitcoin may be a hedge for the euro, but not for the dollar. In

addition the estimated coefficients for currency markets are consistently

larger than those representing equities or bonds, supporting the idea that

bitcoin is an alternative monetary asset.

ii

Executive Summary

Designed and implemented by an anonymous programmer (or team of

programmers), bitcoin is to date the most successful and widely used

example of a virtual currency. It is a “…digital, decentralised, partially

anonymous currency not backed by any government or other legal entity, and

not redeemable for gold or any other commodity” (Grinberg, 2011, p. 160). In

the short time since its inception in 2010 the price of one bitcoin has

fluctuated dramatically against the US dollar from an initial price of $0.05 to a

high of over $260. This exponential growth has attracted attention from

investors and widespread coverage in the financial media. Despite the

significant media coverage, to date there has been an absence of extensive

academic discourse within the economic and financial literature on the topic

of bitcoin. My primary research focus is on exploring bitcoin as an exotic

asset and investigating the developing correlations and informational

dependencies between bitcoin and other markets. In particular, I address the

anecdotal evidence, often featured in the financial media, that bitcoin may

behave like a form of virtual gold. This comparison has led to the idea that:

like gold, bitcoin may perform as a hedge or a safe haven against more

conventional securities.

The dissertation begins by providing an overview of the relevant academic

literature with a focus on the questions: what is bitcoin? And how is bitcoin

like gold? The two most interesting aspects of bitcoin as a currency system

are its decentralised nature and its fixed money supply. Bitcoin is

decentralised as it is not issued or managed by any one central authority.

Bitcoins are instead created by a process called ‘mining’. This involves users

running a program on their computers to solve complex mathematical

problems with the help of other computers on the network. For each problem

solved miners are rewarded with a fixed amount of newly created bitcoins as

an incentive for supporting the security and integrity of the network. The

amount of money created by mining is determined by an algorithm which

ensures that the supply of bitcoins is fixed. The total number of bitcoins in

existence will approach, but never reach, 21 million by approximately the year

iii

2040. This built in scarcity, along with the use of the term mining, has led to

frequent comparisons with gold, and bitcoin’s description as a “synthetic

commodity money” (Selgin, 2013). The fixed supply means that as long as

demand is increasing, through increased adoption by new users, the virtual

currency will be intrinsically deflationary. Whilst this poses problems for its

use as a currency, it is attractive to investors pursuing high returns.

Gold is generally found to be a monetary asset and performs as an effective

hedge against inflation and US dollar devaluations. I argue that bitcoin may

play a similar role due to its deflationary nature and its insulation against the

activities of central banks, which may from time to time debase the currencies

they manage. In addition as it is essentially an alternative currency, intuitively

one would expect that the relationship between bitcoin and currencies to be

the strongest which would support the idea that bitcoin is a monetary asset.

The relationship between gold and equity and bond markets is also well

documented. Generally gold is found to have a clear negative relationship

with stocks and to have little relationship with bonds. A reason put forward for

this by Ciner, Gurdgiev et al. (2010, revised 2012) is that “gold is a market

sentiment proxy that is more likely to impact riskier assets than fixed income

securities.” Due to the low participation in the bitcoin market by institutional

investors, there is a lack of clearly defined capital flows between the virtual

currency and traditional capital markets which intuitively would lead to low

correlations. Bitcoin’s exogeneity to the conventional financial system may

however allow it to play a hedge role against sovereign debt markets as it

does not rely on the reputation or supervision of any national or supranational

body.

Gold’s role as a safe haven in times of extreme negative returns is also well

documented. Historically it has been found to be a safe haven for equities,

bonds, and the dollar. However, in more recent studies the idea of gold as a

safe haven has been challenged with a possible reason being that the rise in

popularity of gold linked products “has caused a decline in its primary

attraction for many financial market participants, which is the notion that gold

iv

can be trusted as a safe haven against [the] equity market volatility” (Ciner,

Gurdgiev et al., 2010, revised 2012).

In order to determine whether bitcoin is a hedge or a safe haven for various

asset classes I use two econometric models based on those used by Baur

and Lucey (2010) and Ciner, Gurdgiev et al. (2010, revised 2012). For

estimation I include variables to represent stocks, bonds and currencies for

both US and EU markets. The equity market proxies are major indices from

both regions, the bond market proxies are benchmark ten year government

bond yields (using German bonds for the EU) and the currencies are the US

dollar and the euro. I estimate two GARCH (1, 1) models, one to determine

bitcoin’s correlations with each asset class, and one focusing on correlations

with periods of extreme negative returns. If bitcoin is a hedge it will be

negatively correlated with other assets on average and if it is a safe haven it

will be negatively correlated with periods of extreme negative returns. For

extreme negative shocks I use quantiles representing the bottom 5 and 10%

of returns for stocks and currencies, and the top 5 and 10% of spikes in yields

for bonds.

My results show that bitcoin does not play a hedge or a safe haven role for

US equity markets and is positively correlated with stock returns on average.

For European markets bitcoin returns are negatively correlated with stock

returns on average, meaning bitcoin could possibly play a hedge role. It is

important to note that the estimated coefficients are small and of varying

significance indicating that bitcoin returns are largely orthogonal to equity

markets in both the EU and US, and suggesting that bitcoin may have a role

as a diversifier.

For US and EU bond markets I find that bitcoin is a hedge as it is positively

correlated with yields. In addition, I find that bitcoin is a safe haven for EU

markets for both quantiles and a safe haven for US markets for the most

extreme periods of spikes in yields (top 5% quantile). The coefficient

estimates for the effect of changes in bond yields on bitcoin are small

indicating a weak relationship between the two markets. Despite the weak

v

relationship, the fact that bitcoin is negatively correlated with bonds on

average (positively correlated with yields) is interesting as this indicates that it

may play a different role in financial markets to that played by gold.

For currency markets, the coefficient estimates representing bitcoin’s

relationship with the dollar are consistently positive, whilst those with the euro

are consistently negative, implying that bitcoin may serve as a hedge against

the euro but not the dollar. I also find that bitcoin may play a safe haven role

for extreme negative returns on the dollar but not on the euro. It is interesting

to note that the estimated coefficients for the currency markets are

consistently larger than those representing equity or bond markets. This is

supportive of the idea that bitcoin is a monetary asset, a similarity it shares

with gold.

My main conclusion from estimation is that currently bitcoin returns are largely

orthogonal to returns in other markets. It is important to realise that as an

asset bitcoin is still in an early development stage. As a result of this the

correlations between it and other markets are much more volatile than those

between more mature asset classes. If bitcoin adoption continues at the

current rate and a clear regulatory framework is put in place, it is likely that

more institutional investors will enter the market, strengthening the

correlations between bitcoin and other more traditional investment vehicles.

Further research could focus on the dynamic nature of these developing

relationships, perhaps using a dynamic conditional correlation (DCC)

methodology similar to that used by Ciner, Gurdgiev et al. (2010, revised

2012). In addition the results from estimating bitcoin’s relationship to bond

markets could be studied further. For the Eurozone in particular the effect of

changes in the spread between core and periphery bond yields on bitcoin

could be examined as these are likely to better reflect negative shocks to the

European bond market.

vi

Acknowledgements

I would like to express my deepest appreciation to all those who provided me

with help in writing my masters dissertation, without whom it would not have

been possible.

In particular, to my supervisor Dr. Constantin Gurdgiev I would like to say

спасибо (thank you) for his advice, guidance and inspiration throughout my

research. Furthermore I would like to thank my parents, Frank and Irene, for

their continued support.

vii

Table of Contents

1: Introduction ............................................................................................................... 1

2: Literature Review ..................................................................................................... 2

2.1: What is bitcoin? ................................................................................................. 2

2.2: How is bitcoin like gold? ................................................................................... 8

3: Data and Descriptive Statistics ............................................................................... 13

3.1: Data .................................................................................................................. 13

3.2: Descriptive Statistics........................................................................................ 14

3.3: Basic Correlation Study ................................................................................... 16

4: Econometric Model................................................................................................. 18

4.1: Hypotheses and Definitions ............................................................................. 18

4.2: Model 1 ............................................................................................................ 18

4.3: Model 2 ............................................................................................................ 20

5: Empirical Analysis .................................................................................................. 23

5.1: Model 1 ............................................................................................................ 23

5.1.1: US Market ................................................................................................. 23

5.1.2: EU Market................................................................................................. 26

5.2: Model 2 ............................................................................................................ 28

5.2.1: US Market ................................................................................................. 28

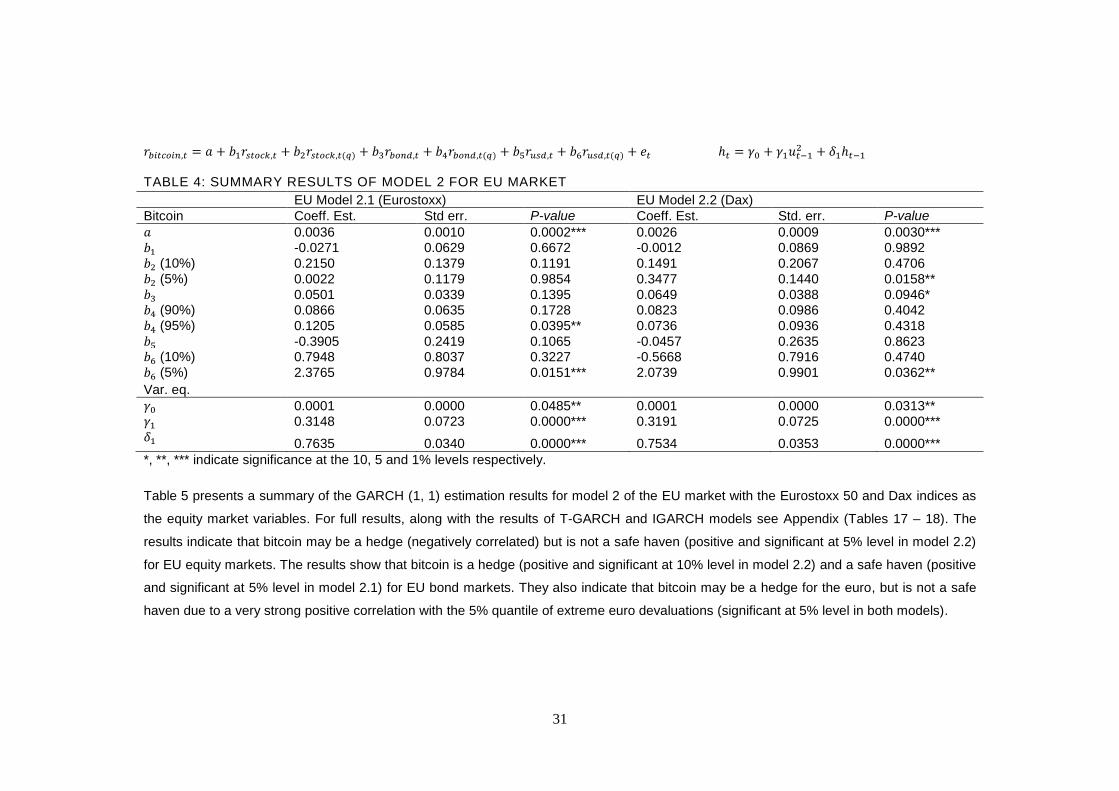

5.2.2: EU Market................................................................................................. 30

6: Conclusion .............................................................................................................. 33

References ................................................................................................................... 36

Appendix ..................................................................................................................... 39

viii

List of Tables

Table 1: Summary Results for Model 1 of US market ................................... 24

Table 2: Summary Results for Model 1 of EU market ................................... 27

Table 3: Summary Results for Model 2 of US market ................................... 29

Table 4: Summary Results for Model 2 of EU market ................................... 31

Table 5: Avg daily volume traded by currency .............................................. 39

Table 6: Descriptive statistics for US market data ......................................... 47

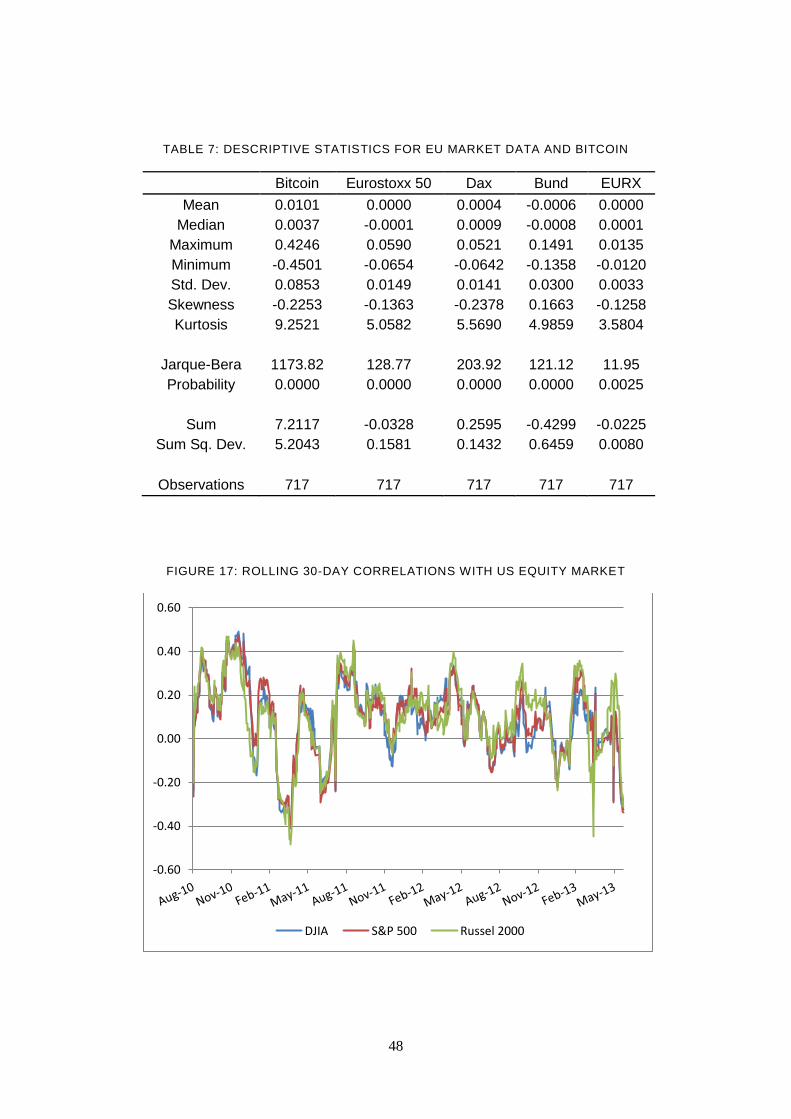

Table 7: Descriptive statistics for EU market data and bitcoin ....................... 48

Table 8: Summary statistics for rolling 30-day correlations ........................... 50

Table 9: Result of GARCH, T-GARCH and IGARCH estimation for Model 1.1

US market (S&P 500) ................................................................................... 51

Table 10: Result of GARCH, T-GARCH and IGARCH estimation for Model 1.2

US market (Dow Jones) ............................................................................... 52

Table 11: Result of GARCH, T-GARCH and IGARCH estimation for Model 1.3

US market (Russell 2000)............................................................................. 53

Table 12: Result of GARCH, T-GARCH and IGARCH estimation for Model 1.1

EU market (Eurostoxx 50) ............................................................................ 54

Table 13: Result of GARCH, T-GARCH and IGARCH estimation for Model 1.2

EU market (Dax) ........................................................................................... 55

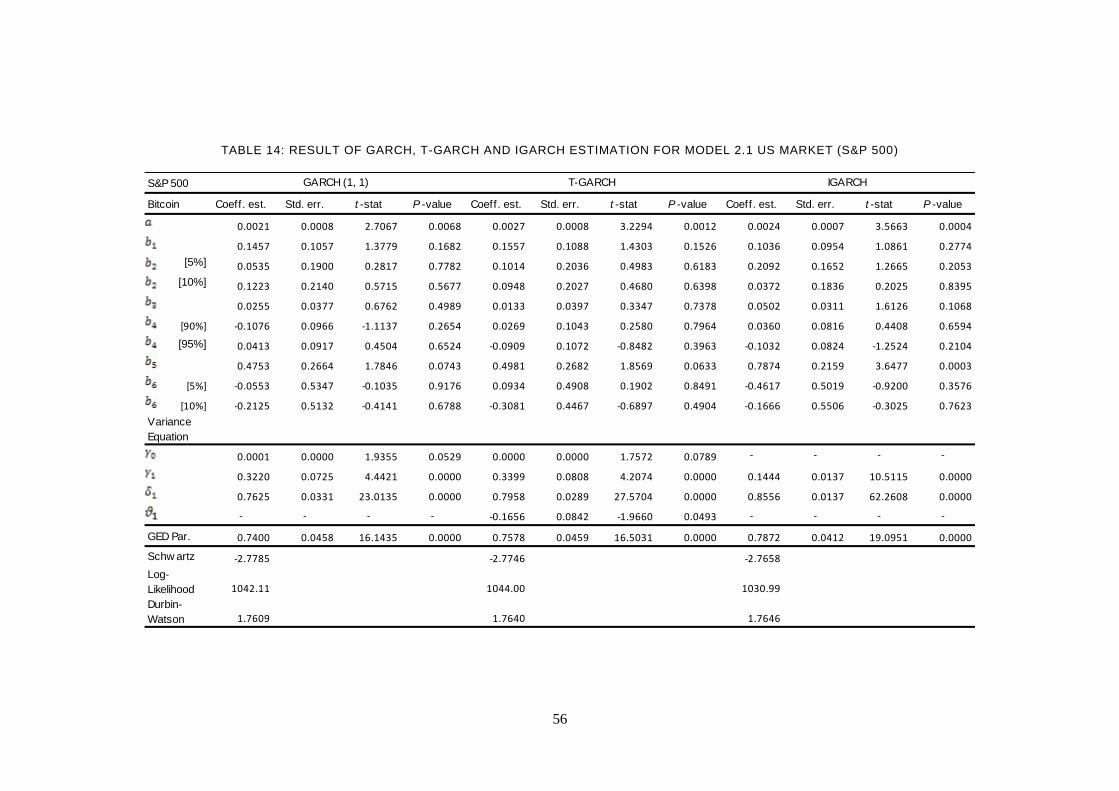

Table 14: Result of GARCH, T-GARCH and IGARCH estimation for Model 2.1

US market (S&P 500) ................................................................................... 56

Table 15: Result of GARCH, T-GARCH and IGARCH estimation for Model 2.2

US market (Dow Jones) ............................................................................... 57

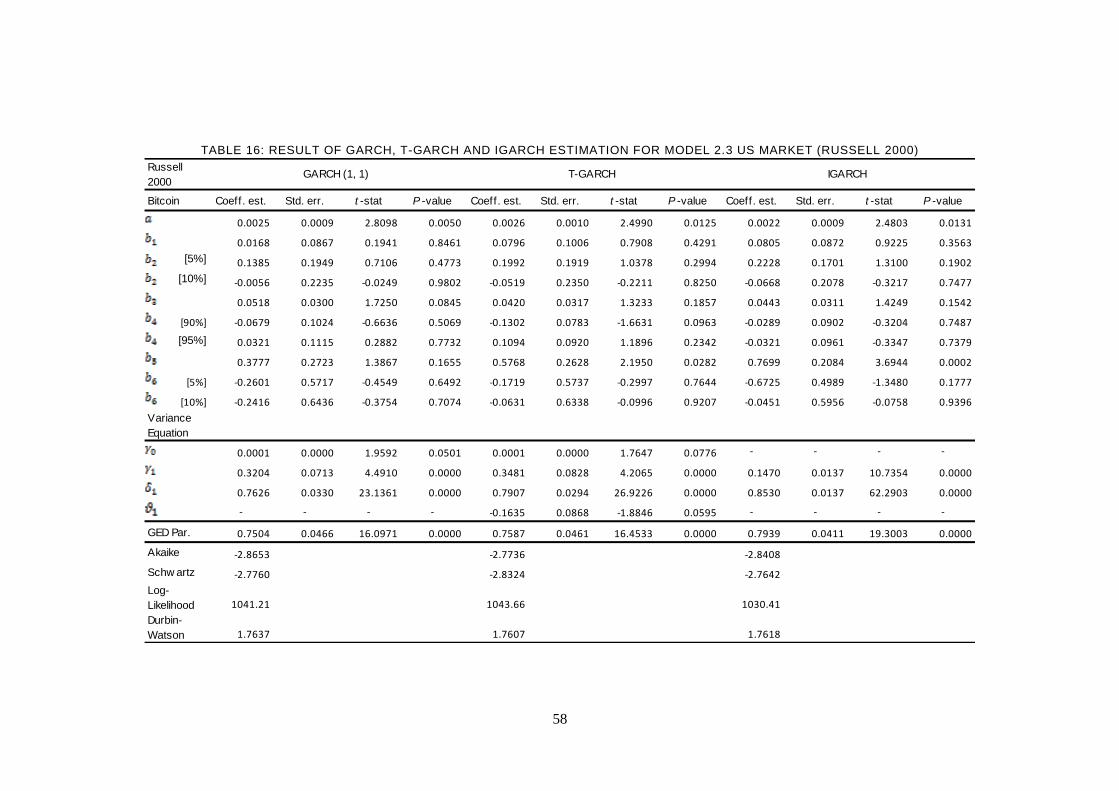

Table 16: Result of GARCH, T-GARCH and IGARCH estimation for Model 2.3

US market (Russell 2000)............................................................................. 58

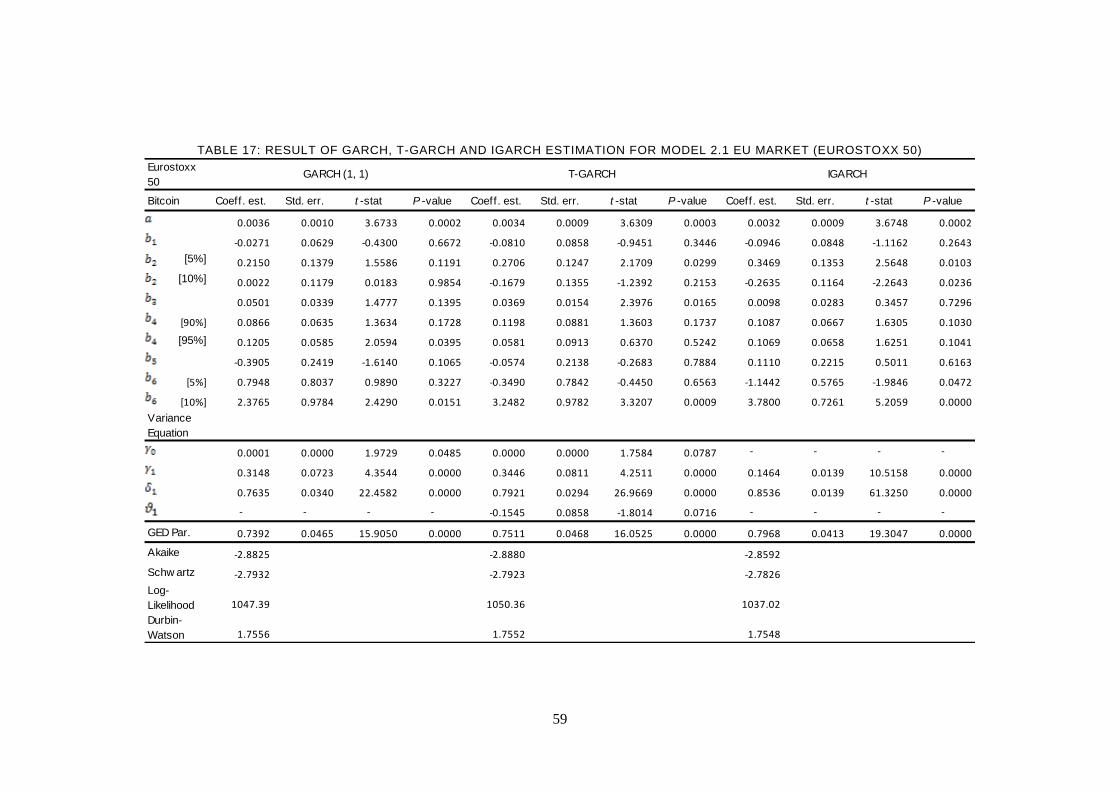

Table 17: Result of GARCH, T-GARCH and IGARCH estimation for Model 2.1

EU market (Eurostoxx 50) ............................................................................ 59

Table 18: Result of GARCH, T-GARCH and IGARCH estimation for Model 2.1

EU market (Dax) ........................................................................................... 60

ix

List of Figures

Figure 1: Volume of bitcoin traded by currency ............................................. 39

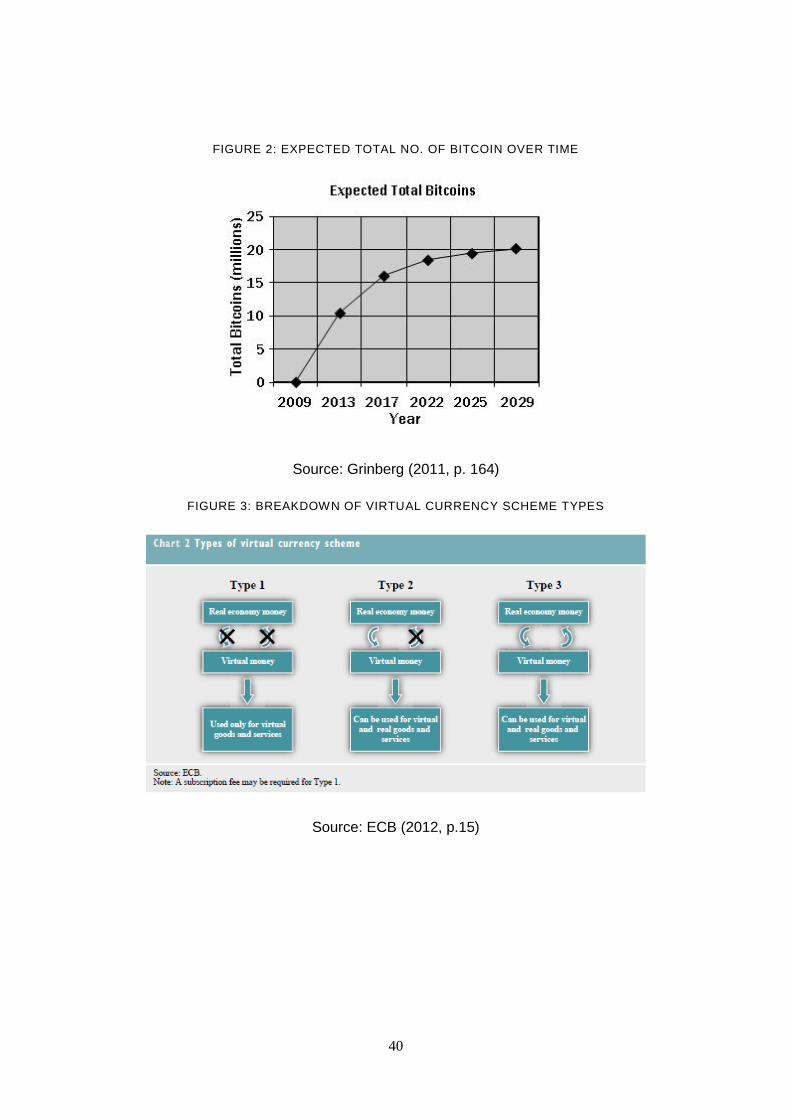

Figure 2: Expected total no. of bitcoin over time ........................................... 40

Figure 3: Breakdown of virtual currency scheme types ................................. 40

Figure 4: Illustration of bitcoin transactions ................................................... 41

Figure 5: Plot of bitcoin price (Linear scale) .................................................. 41

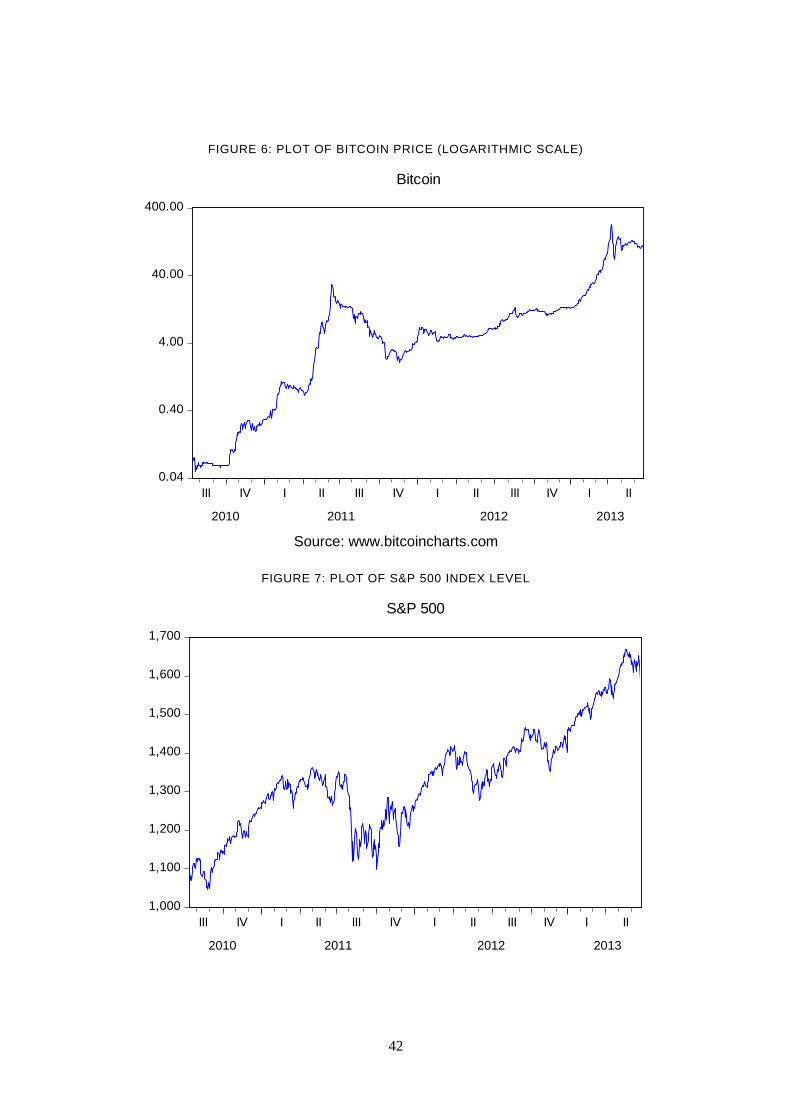

Figure 6: Plot of bitcoin price (Logarithmic scale) ......................................... 42

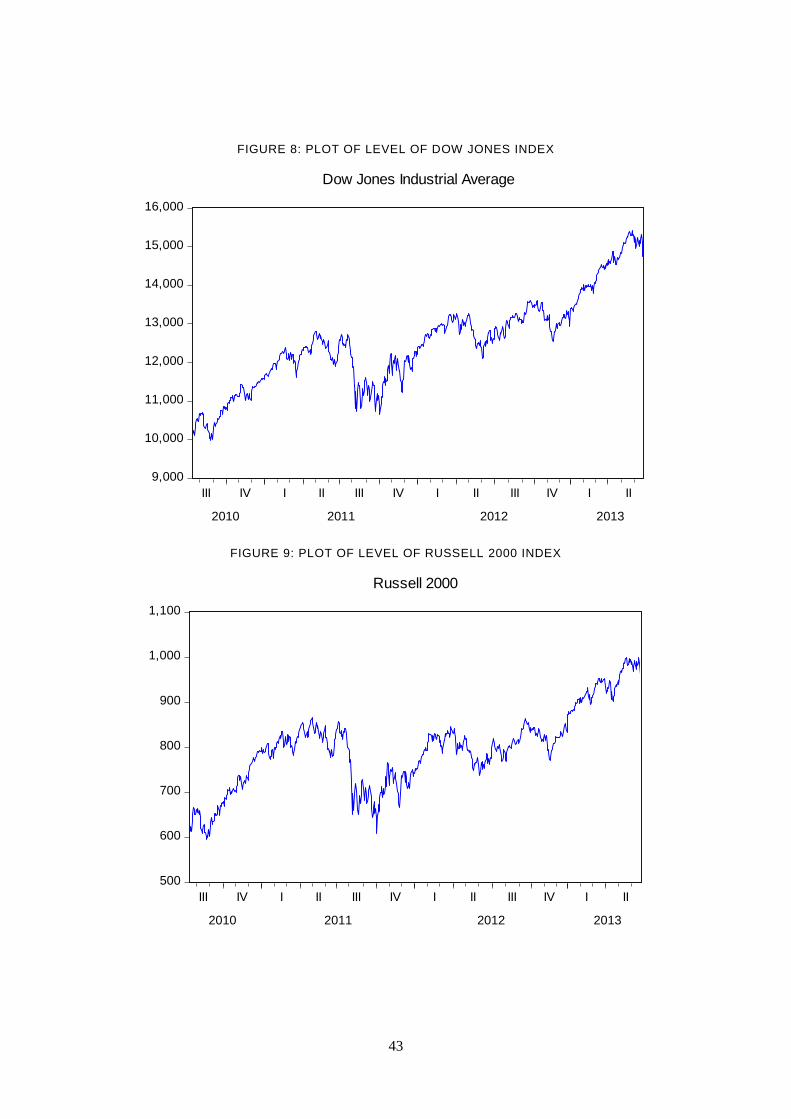

Figure 7: Plot of level of S&P 500 Index ....................................................... 42

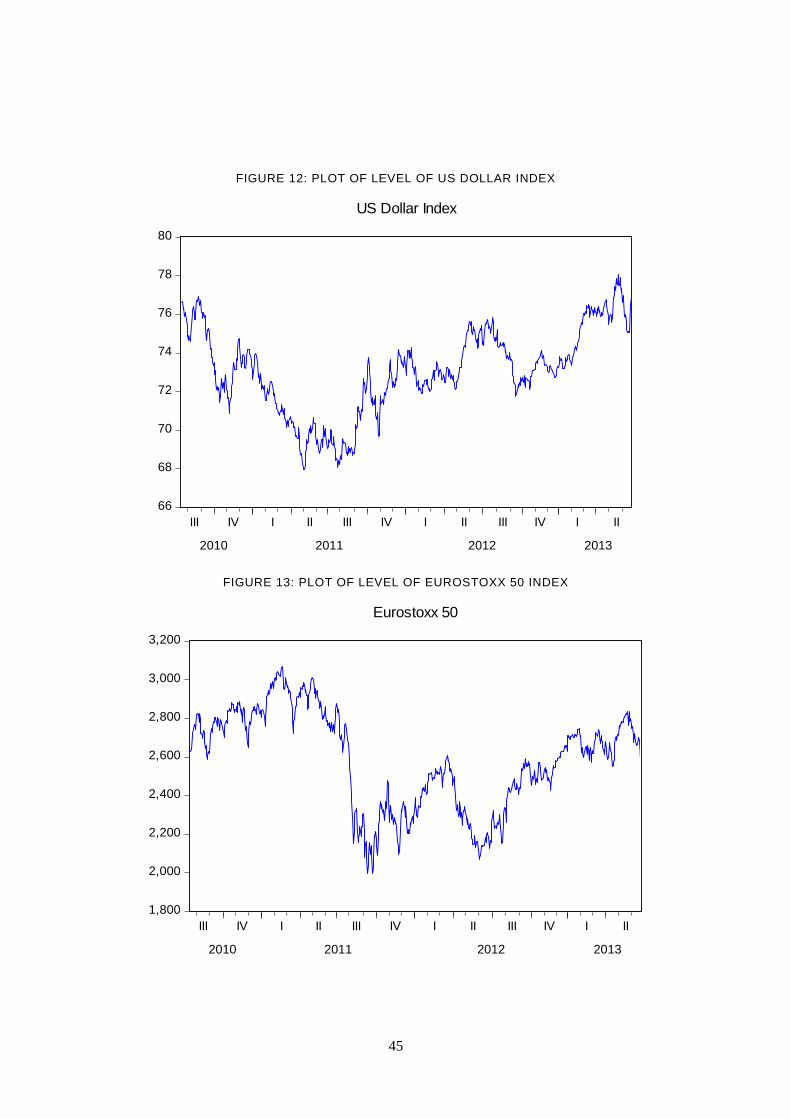

Figure 8: Plot of level of Dow Jones index .................................................... 43

Figure 9: Plot of level of Russell 2000 index ................................................. 43

Figure 10: Plot of US government ten year bond yield .................................. 44

Figure 11: Plot of US 10 year yield (left axis) and S&P 500 (right axis) ......... 44

Figure 12: Plot of level of US Dollar index .................................................... 45

Figure 13: Plot of level of Eurostoxx 50 index ............................................... 45

Figure 14: Plot of level of German dax index ................................................ 46

Figure 15: Plot of German government ten year bond yield .......................... 46

Figure 16: Plot of level of euro currency index .............................................. 47

Figure 17: Rolling 30-day correlations with US equity market ....................... 48

Figure 18: Rolling 30-day correlations with EU equity market ....................... 49

Figure 19: Rolling 30-day correlations with bond yields ................................ 49

Figure 20: Rolling 30-day correlations with currency markets ....................... 50

1

1: Introduction

The objective of this dissertation is to conduct an in-depth economic and

financial study of the virtual currency Bitcoin. A comprehensive econometric

analysis of the currency will be undertaken so as to determine bitcoin’s

position within the universe of investable assets and to contribute to the

limited academic literature on the topic. The study of informational

dependencies across asset classes is of benefit to market participants in that

it can guide and inform their investment strategies. Bitcoin as it exists

currently is an exotic asset unlikely to feature in many investors portfolios.

However, already since its inception it has seen exponential growth along

with widespread media coverage. This dissertation is therefore a first attempt

at exploring the developing correlations that exist between bitcoin and other

more traditional investment vehicles. In particular, I address the anecdotal

evidence, often featured in the financial media, that bitcoin may behave like a

form of virtual gold. This comparison is often based on commentator’s

opinions that part of bitcoin’s value as an investment, like gold, is a result of

its ability to perform as a hedge or a safe haven against more conventional

securities. I formally address this issue empirically through the use of

econometric techniques.

The remainder of this dissertation is organised as follows: Chapter 2 will

provide an overview of the academic literature relevant to bitcoin attempting

to answer the questions: What is bitcoin? and how is bitcoin like gold?

Chapter 3 will discuss the data to be used in estimation and the summary

descriptive statistics. Chapter 4 will discuss the econometric methodology

used. Chapter 5 will outline and infer meaning from the results of estimation

and finally Chapter 6 will contain my concluding remarks.

2

2: Literature Review

In this chapter I will discuss most of the relevant scholarly literature that exists

on the topic of bitcoin. As previously stated as a motivation for research,

whilst there has been significant coverage of bitcoin in the financial media; the

quantity of academic discourse on the topic has been limited. As a result I

have been forced to widen the scope of what are acceptable sources for

review, with a good degree of material coming from within the online bitcoin

community. Due to the source of much of my material, care has been taken to

screen for any bias which may be present.

2.1: What is bitcoin?

Bitcoin is to date the most successful and widely used example of a virtual

currency. It is “…a digital, decentralized, partially anonymous currency not

backed by any government or other legal entity, and not redeemable for gold

or any other commodity” (Grinberg, 2011, p. 160). It was developed and

implemented by an anonymous programmer (or team of programmers) under

the pseudonym Satoshi Nakamoto in 2009 and has since achieved a certain

degree of international recognition as a result of widespread media coverage.

The bitcoin system operates at a global level and enables users to purchase

both real and virtual goods and services in exchange for units of the currency,

thereby competing with traditional currencies such as the US dollar and the

euro. Bitcoin is not pegged to any currency, with the exchange rate being set

by supply and demand in the market. All major currencies can be exchanged

for bitcoins on a number of online exchanges with Mt.Gox the most popular,

handling approximately 65% of all Bitcoin exchange trading1. As of writing,

the majority of all Bitcoin exchange transactions are with the US dollar2. An

interesting development in the distribution of bitcoin exchange transactions is

the digital currencies surge in popularity in China. In the first two quarters of

2013 the Chinese Yuan’s share has risen from approximately 1% of global

1 Source: www.bitcoincharts.com

2 See Figure 1 and Table 4 in appendix. Approximately 80% of all bitcoin exchange

transactions are with the US dollar at time of writing. (Source: www.bitcoincharts.com)

3

exchange volume to close to 6%. This is largely attributed to a short

documentary on bitcoin which aired on state-run broadcaster CCTV at the

end of March. Some bitcoin commentators have viewed this as a deliberate

move by the Chinese government to undermine the dollar’s reserve status, as

they have repeatedly called for a move away from the current dollar

dominated system3.

Since its inception in 2009 the value of one bitcoin has fluctuated dramatically

against the US dollar from an initial price of approximately $0.05 for one

bitcoin to a high of over $260. As of the time of writing over 11 million bitcoins

have been created and the current “market cap” of all bitcoins is close to one

billion US dollars. The price appreciation of bitcoin has been staggering given

that a “coin” has no intrinsic value, making bitcoin in some respects the most

trust based of all currencies. The use of the term “market cap”, taken from a

major bitcoin data publishing website, outlines one of the issues with bitcoin’s

status as a currency. Many users view the bitcoins they hold less as a

currency and more as a share on any and all developments in the whole

bitcoin space. This view of bitcoin as an investment is one of the primary

motivations for this research as a first attempt to estimate bitcoins relative

position within the universe of financial assets.

The “protocol” under which the bitcoin system operates was originally outlined

in a paper published online by Nakamoto (2009) in the aftermath of the global

financial crisis. Trust in the financial system is a recurring theme in the paper

with Nakamoto drawing attention to the “inherent weaknesses of the trust

based model” and stating that “What is needed is an electronic payment

system based on cryptographic proof instead of trust” (p. 1). Whilst Nakamoto

is explicitly referring to the online payments system, many bitcoin proponents

have latched on to the fact that the virtual currency is exogenous to the well-

established global financial system as one of its major strengths, allowing

users to insulate themselves against the interventionist policies of central

banks.

3 See Wall Street Journal article on comments of Governor of Bank of China Zhou Xiaochuan.

(http://online.wsj.com/article/SB123780272456212885.html)

4

The bitcoin system functions similarly to Bit Torrent, the popular peer-to-peer

file sharing software. According to the Oxford English Dictionary Online a

peer-to-peer network is:

“…[a network] in which each computer can act as a server for the others,

allowing shared access to files and peripherals without the need for a central

server.”

The key aspect of this definition as it relates to bitcoin is “without the need for

a central server”. Bitcoin is “designed as a decentralised system where no

central monetary authority is involved” (ECB, 2012, p. 24). This means that

the currency is not issued or managed by any one central organisation such

as the US Federal Reserve or the European Central Bank, nor is there a need

for the involvement of any other financial institutions in bitcoin transactions.

The technical aspects of the bitcoin payment system are difficult to

understand for most people not from a relevant technical background.

However, for my purposes a basic description of the process, drawing on that

featured in the ECB’s (2012) paper, will suffice4. In order to conduct bitcoin

transactions users must download and run the free and open-source software

(the bitcoin client). Users “coins” are then stored on their computers in a file

called a wallet, with all responsibilities regarding securing and backing up

these digital wallets falling to the individual user. Nakamoto (2009) defines an

electronic coin (bitcoin) “as a chain of digital signatures.” Each owner has two

“keys”, one public and one private, which are used to digitally “sign” any

transactions. Each computer on the network contains a ledger (called the

“block chain5”) of all previous transactions, which is one way the system

avoids the need for any trusted third party. Figure 4 in the appendix provides

a simplified illustration of how a bitcoin transaction works. First the future

owner must send his public key to the current owner . The original

4 For a full technical discussion of how the bitcoin system operates see Nakamoto, S. (2009)

‘Bitcoin: A Peer-to-Peer Electronic Cash System’, 5 “A block chain is a transaction database that is shared by all nodes participating in a system

based on the Bitcoin protocol. A full copy of a currency’s block chain contains every

transaction ever executed in the currency.” (https://en.bitcoin.it/wiki/Block_chain)

5

owner then transfers the bitcoins by “digitally signing a hash6 of the previous

transaction and the public key of the next owner” (Nakamoto, 2009, p. 2).

Each individual bitcoin contains a record of all previous transactions, with

each additional transaction becoming embedded as part of this code. All

transactions are then broadcast to the network, which verifies that a bitcoin

transfer has taken place by looking at the “timestamp7” which is contained in

the transaction hash, in a process called “mining”. These verified transactions

then become a matter of public record and are added to the block chain.

The ECB (2012) defines “mining” as:

“…the process of validating transactions by using computing power to find

valid blocks8 (i.e. to solve complicated mathematical problems)”.

“Miners” are incentivised to support the security and integrity of the network

by verifying transactions, as for each new block that is solved the successful

miner is rewarded with a set amount of newly created bitcoins. This process

is how bitcoins are initially distributed in the absence of any central authority.

Nakamoto (2009, p. 4) describes the mining process as “analogous to gold

miners expending resources to add gold to circulation”, with the resources in

question being computational and electrical power. The system is designed

so that as more miners join the network, the “problem difficulty adjusts to

ensure that bitcoins are created at a predetermined rate and not faster or

slower.” (Grinberg, 2011, p. 163) In addition, the algorithm which determines

the rate of creation of bitcoins is set to half four times over the life of the

currency as the total monetary base reaches certain predetermined levels910.

The total number of bitcoins in existence will approach, but never reach, 21

6 “A hash, or hash value, is the value returned by an algorithm that maps large data sets to

smaller data sets of fixed length.” (ECB, 2012, p. 23) “The same hash will always result from

the same data, but modifying the data by even one bit will completely change the hash.”

(https://en.bitcoin.it/wiki/Hash) 7 A timestamp is simply the time of day recorded in a digital transaction, so as to determine

transaction order in electronic payment systems. 8 “A block is a record of some or all of the most recent Bitcoin transactions that have not yet

been recorded in any prior blocks.” (https://en.bitcoin.it/wiki/Block_chain) 9 See Fig. 2 in Appendix.

10 The first of these levels was reached in November 2012 when the mining reward halved

from 50 bitcoins per successful block to 25 bitcoins.

6

million by approximately the year 2040, from which point on “miners are

expected to finance themselves through transaction fees.” (ECB, 2012, p. 25)

As a result of the ever-increasing difficulty of successful bitcoin mining

purpose built “mining rigs” have been developed with vastly superior

computational ability to the average PC. In addition, miners have also

organised themselves into profit sharing “pools” to hedge against the risk of

running the bitcoin client for long periods of time and receiving no reward due

to the stochastic element involved in the mining process.

The built-in scarcity in the bitcoin system, along with the frequent

comparisons with gold (mining, etc.) has led to bitcoin’s description as a

“synthetic commodity money” (Selgin, 2013) and is one of the most

interesting aspects of the currency from a monetary point of view. The fixed

money supply means that as long as bitcoins use is growing the currency will

be intrinsically deflationary, resulting in accusations that it may lead to a

deflationary spiral. This deflationary nature also contributes to users views of

bitcoin as more of an asset than a currency and has drawn large numbers of

speculators to bitcoin, resulting in two major boom and bust cycles.

Economists generally agree that constant deflation is a very destructive force

in modern economies, leading to hoarding as the value of money is expected

to increase over time. However, in the case of bitcoin as it “is not the currency

of a country or currency area and is therefore not directly linked to the goods

and services produced in a specific economy” the negative macro-economic

impact of any deflation are unlikely to pose a major issue (ECB, 2012, p.25).

As part of the transaction process users never have to disclose their identity

leading to a high degree of anonymity in the system with the result that bitcoin

is often described as “digital cash” (ECB, 2012, p. 25). Bitcoin has

experienced its fair share of controversy because of this anonymity with early

users latching on to its ability “to facilitate money laundering, tax evasion, and

trade in illegal drugs and child pornography.” (Grinberg, 2011, p. 161) These

illicit activities have of course brought the virtual currency to the attention of

regulatory bodies, such as the ECB and FinCEN (a bureau of the US

Department of Treasury).

7

The ECB paper, which I have used extensively as a resource so far, focuses

largely on the relevance of virtual currency schemes for central banks.

Although the paper refers generally to “virtual currency schemes”, “bitcoin”

appears over 100 times throughout the document and takes up the majority of

the discussion11. The authors identify a number of ways through which bitcoin

may impact central banks key responsibilities of maintaining price and

financial stability. They conclude that bitcoin does not pose a risk to price

stability due to its stable (fixed) money supply, and does not pose a risk to

financial stability due to its limited connection to the real world economy. With

regard to regulation they determine that bitcoin does fall within central banks

responsibilities and that the lack of supervision could pose an issue in the

future, highlighting difficulties arising from the legal uncertainty surrounding

the currency. So far US regulatory bodies have remained relatively quiet

regarding the legality of bitcoin, however, FinCEN “issued guidance clarifying

that bitcoin exchanges are considered Money Transmitters and are required

to obtain all proper licenses to conduct business in the US.” (TGB, 2013, p.

21)

The infrastructure surrounding bitcoin has developed rapidly in the years

since its inception and includes “exchanges, transaction service providers,

market information and chart providers, escrow providers, joint mining

operations and so on.” (Grinberg, 2011, p. 165) A surprising consequence of

this according to a study by Christin and Moore (2013) is that the majority of

“risk Bitcoin holders face stems from interacting with these intermediaries,

who act as de facto central authorities” (p. 9). They find that approximately

45% of bitcoin exchanges have closed often resulting in customers losing

money that they are unable to withdraw. This exchange risk has led to wild

periods of market volatility with both major bitcoin price crashes attributed to

problems with the most popular bitcoin exchange Mt. Gox, however, this

statement is based on anecdotal evidence.

11

The paper also features a second case study of another virtual currency, Linden Dollars,

which are an in-game currency featured in popular online role playing game Second Life.

8

The degree of uncertainty regarding the safety of funds transferred to online

exchanges is a serious barrier to the development of bitcoin as a currency or

an asset, and highlights the need for some form of regulatory framework. Any

regulation is likely to come hand in hand with a tax treatment, which will

remove one of bitcoins major strengths as an asset, its tax free nature. In May

2013 the US Government Accountability Office (GAO) published a report to

the US Senate Committee on Finance in relation to the tax compliance of

virtual currencies. They recommended that the IRS provide additional

guidance regarding online currencies and highlighted uncertainties with how

to characterise income and how to calculate the basis for gains as possible

issues. They find that the uncertainty in relation to how to characterise income

“depends on whether the virtual economy activity or virtual currency unit is to

be treated as property, barter, foreign currency, or a financial instrument”

(GAO, 2013, p. 13). Any form of regulatory or tax treatment represents a

double edged sword for bitcoin proponents who are largely attracted by the

currencies independence from the global financial system, but who also hope

for a more widespread adoption which will only happen should the fears of

more conventional investors be allayed.

2.2: How is bitcoin like gold?

The majority of my discussion so far has been of a descriptive nature

regarding how bitcoin works and the major issues it may face in future.

However, my main research focus is on determining bitcoins relative

relationships with conventional asset classes such as stocks, bonds and

currencies. From my survey of the available academic literature and

publications in the financial media I have come across various comparisons

between bitcoin and gold. The ECB lays the economic foundations of bitcoin

with the Austrian school of economics, well known proponents of a return to

the gold standard, and it can be argued that bitcoin represents an ultimate

form of denationalised money given that it is not controlled by any

government or other central authority. They further develop this relationship

by stating that bitcoin is “inspired by the former gold standard” (2012, p. 22).

Whilst I have briefly discussed the unique monetary aspects of the currency a

9

full discussion of the economic philosophy underlying bitcoin is outside the

scope of this paper. In this section, I intend to develop the comparison

between bitcoin and gold not as a form of money but as an asset class.

Exponents of bitcoin’s virtues argue that as it is an alternative currency and

payment system that does not depend on a network of financial institutions,

but rather is “based on cryptographic proof instead of trust” (Nakamoto, 2009,

p. 1). As a result users are insulated against the risks posed by sovereign

currencies and debt such as inflation and default risk. This is particularly

relevant when we consider bitcoin was created in the aftermath of the global

financial crisis in 2008 when public trust in governments and financial

institutions was at a low. This also gives weight to the comparison between

bitcoin and gold, as gold is in theory used to protect against similar risks.

Capie, Mills and Wood (2005) argue that gold has remained attractive as an

asset as:

“It is durable, divisible, and, for many years over a large part of the world, was

indeed the ultimate standard of value.”

Like gold bitcoin is durable, it cannot be destroyed easily, although it can be

lost or stolen but the same can be said for physical gold. Bitcoins are also

“divisible to eight decimal places enabling their use in any kind of transaction,

regardless of the value” (ECB, 2012, p. 21). Unlike gold however, bitcoin

obviously lacks the historical significance resulting from hundreds of years of

use as a store of value. Interestingly bitcoin has gained significant popularity

among libertarians and others from similar ideological backgrounds that have

traditionally been seen as major “gold bugs”. The philosophical links between

bitcoin and the Austrian school are likely to play a major role here and no

doubt fears about the effects of the unconventional monetary policies being

pursued by central banks since the financial crisis have added fuel to the fire.

One major advantage of investing in bitcoin rather than gold are the much

lower costs involved. To gain exposure to gold investors main options are

physical gold, the futures market and gold-linked funds. As of the time of

10

writing to gain exposure to bitcoin investors can only purchase bitcoins. One

of the main issues with buying physical gold is the cost of storage, for bitcoin

these costs are basically zero. Gold futures contracts involve physical delivery

so to gain exposure investors who only wish to speculate on the market must

enter into and close out positions to avoid taking delivery and having to pay

storage costs. For longer term investors in the futures market, they must roll

out of the expiring month contract and into the next active contract which

compounds the fees they must pay to the exchange. As bitcoin is basically

free to hold this is not an issue for investors and in addition bitcoin exchange

fees are much lower in comparison to those charge by conventional financial

exchanges. Gold-linked funds, such as ETFs, have seen a major surge in

popularity in recent years; however, these also charge transaction and

storage fees. As a result of its low cost nature, if bitcoin could serve a similar

purpose in the markets, i.e. as a hedge and safe-haven, it could offer a much

cheaper alternative to gold, benefitting investors.

Intuitively one would expect that the relationship between bitcoin and

currencies be the strongest, as bitcoin is in essence an alternative currency.

The academic literature on gold’s role as a monetary asset is well developed

and it is consistently found that gold is an effective hedge against inflation12,

and against US dollar devaluations13. One possible explanation given for this

role as provided by Capie, Mills et al. (2005) is that:

“…gold cannot be produced by the authorities that produce currencies. This

means that those who can increase the supply of money and therefore, from

time to time, debase its value cannot by similar means debase the value of

gold.” (p. 351)

The same can be argued for bitcoin as a result of its fixed money supply and

decentralised nature which could make it a natural hedge for currencies.

12

See Fortune (1987), Moore (1990), Taylor (1998), Ghosh, Levin et al. (2004), Worthington

and Pahlavani (2007), Blose (2010), and Wang, Lee et al. (2010). 13

See Johnson and Soenen (1997), Capie, Mills et al. (2005), Tully and Lucey (2007),

Sjaastad (2008), Hammoudeh, Sari et al. (2009), and Ciner, Gurdgiev et al. (2010, revised

2012).

11

Gold’s role as a hedge14 for stock and bond markets has also been tested

extensively. Baur and Lucey (2010), Baur and McDermott (2010), and Ciner,

Gurdgiev et al. (2010, revised 2012) find a clear negative relationship

between gold and stock returns on average indicating that gold is a hedge for

equity markets. However, they find that “there is little relation between gold

and bond prices, in general” (Ciner, Gurdgiev, et al., 2010, revised 2012, p.

9). A potential explanation they provide is that “gold is a market sentiment

proxy that is more likely to impact riskier assets than fixed income securities”

(Ciner, Gurdgiev et al. (2010, revised 2012, p. 9).

Another well documented role that gold plays in financial markets is as a safe

haven in times of extreme negative returns. Baur and Lucey (2010), and Baur

and McDermott (2010) find that gold “can and does act as a safe haven for

bonds as well as stocks” (Lucey, 2011, p. 12). Ciner, Gurdgiev et al. (2010,

revised 2012) also find the same relationship to hold for gold, bonds, and the

dollar. However, they found that “gold in fact does not act as a safe haven for

equities” (p. 11). They present a possible reason for this as being that the rise

in popularity of gold based ETFs and other gold-linked indices “has caused a

decline in its primary attraction for many financial market participants, which is

the notion that gold can be trusted as a safe haven against [the] equity market

volatility” (p. 11).

Although the degree of informational dependency between bitcoin and

traditional capital markets needs to be tested statistically, intuitively a low

correlation is likely. This may be due to the fact that as of yet there are

unlikely to be many institutional investors in the bitcoin market, due to the low

liquidity and lack of regulation, which could make the virtual currency a

natural hedge against equity and bond markets. Whilst bitcoin’s monetary

structure could make it a hedge against currency depreciations and inflation,

its exogeneity to the conventional financial system could allow it to play a

hedge role against sovereign debt markets as it does not rely on the

reputation or supervision of any national or supranational body, and should be

14

See Baur and Lucey (2010), Baur and McDermott (2010) and Ciner, Gurdgiev et al. (2010,

revised 2012).

12

insulated to some degree from the contagion which allowed the spread of the

2008 crisis from the subprime market in the US to the rest of the world.

13

3: Data and Descriptive Statistics

3.1: Data

The data to be examined consists of daily observations and covers the period

between 19 July 2010 and 21 June 2013. As bitcoin was only established in

2010 this is the earliest date from which reliable data is available. The end

date was chosen to both maximise the size of the data set whilst allowing

sufficient time to conduct econometric analyses. I include a broad range of

variables to represent stock, bond, and currency markets. The data are drawn

from both US and European markets.

The Bitcoin data consists of the bitcoin-US dollar exchange rate and is quoted

in dollars per bitcoin. The raw daily data is in seven-day week format;

however, as the data for the other assets are in five-day week format the

weekend data was dropped. All bitcoin data was obtained from

www.bitcoincharts.com, a leading source of Bitcoin exchange rate and

volume data.

To represent the US equity market I use the Standard & Poor’s 500 Index

(S&P 500), the Dow Jones Industrial Average Index (DJIA), and the Russell

2000 Index. The S&P 500 was chosen as it is widely regarded as one of the

best gauges of blue chip companies in the US. The Dow Jones Industrial

Average is one of the longest running stock indices in the world. It represents

30 of the largest US companies drawn from a diverse range of industries. It is

often quoted as a leading index due to the fact that its component companies

are some of the most actively traded in the US equity market. The inclusion of

the Russell 2000 allows estimation of the relationship between bitcoin and the

broader US stock market. Whereas the S&P 500 and the Dow Jones only

feature large-cap companies, the Russell 2000 also features small- and mid-

cap companies.

To represent the European equity market I use the Eurostoxx 50 Index and

the Deutsche Aktien Index (DAX). The Eurostoxx 50 is an index containing 50

14

of the largest blue chip European companies. It covers equities from 12

different Eurozone countries and as such is a good indicator of the overall

European equity market. The German stock index (the Dax) is an index

featuring 30 of the largest companies traded on the Frankfurt stock exchange.

Germany is the largest economy in the Eurozone and so its main stock index

is again a good indicator of the general health of European markets. All equity

index data was obtained from Bloomberg.

To represent the US bond market I use Bloomberg’s US generic government

ten year yield, which provides a rolling, constant maturity series of the yield

on the benchmark US government bond. For the European bond market I use

Bloomberg’s German generic government ten year yield, which again

provides a rolling, constant maturity series of the yield on the benchmark core

Eurozone bond.

To represent currencies I use the Federal Reserve’s trade weighted US dollar

index which is an index of the US dollars relative strength against a basket of

foreign currencies. For the euro I use Bloomberg’s Correlation Weighted

Index which is an index of the euro’s relative strength against a representative

basket of world currencies.

The series were grouped by geographic location with the US equity, bond and

currency data to be used together for group estimation, and the EU equity,

bond and currency data also to be used together. As bitcoin is currently tax

free in most jurisdictions none of the series to be used for estimation are tax

adjusted.

3.2: Descriptive Statistics

Figures 5 to 16 in the Appendix present plots of the price (level) of each asset

over time. Figure 5 is a plot of the price of bitcoin in US dollars over time on a

linear scale. The price of bitcoin was less than $1 until the beginning of 2011.

The first speculative bubble and crash in the virtual currency occurred in June

2011 when the price peaked at around $30. The price then crashed due to an

attack on one of the main exchanges which resulted in the theft of a large

15

quantity of bitcoins. The price of bitcoin began to grow at a parabolic rate at

the beginning of 2013. It eventually reached an all-time high of $266 per

bitcoin before plummeting sharply. It has since levelled off and is trading in a

range of approximately $80 to $100 at the time of writing. Figure 6 presents a

plot of the price of bitcoin against a logarithmic scale. It displays a definite

upward trend with the price seeming to revert to the mean following each of

the bubbles and crashes. It makes more sense to view Bitcoin prices on a log

scale since the price has grown exponentially due to constant adoption by

new users.

US stock prices as measured by the S&P 500, the Dow Jones and the

Russell 2000 have increased over the period of the sample and are all close

to their all-time highs. Equity prices in the US experienced a sharp downward

correction in Q3 2011 due to fears of a Eurozone breakup as a result of talk

that Greece may be the first country forced to leave the monetary union.

Yields on benchmark US treasury notes have fallen over the period of the

sample, due largely to the US Federal Reserve’s policy of ultra-low interest

rates, reaching their all-time low in Q2/3 2012. Figure 11 in the appendix

shows a plot of ten year yield and the S&P 500. In it we can clearly see that

the sharp drop in yields in Q3 2011 corresponds with a fall in the aggregate

level of stock prices (as measured by the S&P) for the same period. This is

representative of “risk-off” behaviour in the markets as investors leave riskier

investments and gravitate towards the perceived lower risk of US

Government securities, bidding up prices and pushing down yields. Figure 12

shows that the US dollar depreciated against a representative basket of

foreign currencies up until Q3 2011, following which it appreciated, again

likely due to the policies of the Fed.

European equity markets as measured by the Eurostoxx 50 have fallen over

the period of the sample and are still well below pre-crisis (2007) highs. The

German Dax index has increased over the period of the sample and is

currently close to its all-time highs similar to the US indices. The spread

between the German and aggregate European equity markets reflects the

economic imbalance between Germany, a core Eurozone country, and the

16

more peripheral nations. Both the Eurostoxx and the Dax experienced a

sharp downward correction in Q3 2011, due to the escalating Eurozone crisis,

with the Eurostoxx correcting most severely. Yields on the ten year German

Bund have fallen over the period of the sample. A sharp move down in Q3

2011 has been followed by a continuing downward trend, with yields reaching

their all-time lows in Q3 2012. The Euro weakened against a representative

basket of foreign currencies up until Q3 2012, following which it appreciated.

Much of this down trend can likely be attributed to the strengthening US dollar

(from Q3 2011) along with the escalating Eurozone crisis.

Tables 6 and 7 in the appendix present a summary of descriptive statistics for

the log returns of each series for both the US and EU markets. If we take the

standard deviation of returns to measure an asset’s riskiness, then Bitcoin is

by far the riskiest over the sample period. This is followed by equities, with the

Russell 2000 index the riskiest and the Dow Jones the least risky. For this

sample EU equity markets are also riskier on average than US markets. The

US dollar is more volatile than the Euro over the sample period. Finally bonds

are the least risky investment as the returns examined represent a change in

yield and not overall returns. A student’s t-test on each of the sample means

indicates that the mean returns of each of the series representing stocks,

bonds and currencies are not statistically different from zero. However, the

mean return on bitcoin is positive and statistically different from zero at the

0.02% level indicating a positive trend in the data.

3.3: Basic Correlation Study

Figures 17 to 20 in the appendix present plots of rolling thirty-day correlations

between the log returns on each asset class and bitcoin. Figure 17 presents

the correlations between bitcoin returns and returns on US equity market

indices. There does not appear to be any clear trend in the data and the

correlation fluctuates from negative to positive over time. The correlation

remains generally low and positive between August 2011 and August 2012,

and appears to be on average more positive than negative. In general the

correlation appears to be negatively skewed, as more extreme negative

17

values are observed than positive. The correlations between bitcoin returns

and returns on European equity markets are presented in figure 18. Again

there does not appear to be any clear trend in the data with the series

fluctuating between negative and positive values. The plot appears to be

positively skewed with more extreme positive values observed than negative

ones.

Figure 19 presents a plot of rolling 30-day correlations between bitcoin

returns and changes in bond yields for the US and Germany. The series

again oscillate between negative and positive values with more positive

values observed, which implies a negative correlation with bond prices,

however, this will need to be tested empirically. Finally figure 20 presents the

rolling 30-day correlations between bitcoin and returns on the US dollar and

euro currency indices. The clear negative correlation between the dollar and

euro is apparent as both series are generally moving in opposite directions.

The relationship between currencies and bitcoin appears to be the most

volatile which intuitively makes sense as bitcoin is in essence an alternative

currency. Also it is interesting to note that while the correlations with both

series fluctuate between negative and positive, the relationship with the euro

seems to be on average more positive, whilst the relationship with the dollar

appears to be more negative.

These plots of rolling correlations are useful for gaining an insight into what, if

any, informational dependencies exist between bitcoin and other asset

classes. It must be noted that the correlations fluctuate a lot over time,

implying weak relationships in general. A possible explanation for this is that

bitcoin is still in its development stage; if more institutional investors enter the

market then its relationships with other asset classes will become more

defined.

18

4: Econometric Model

4.1: Hypotheses and Definitions

This section outlines the econometric models I will use to test whether bitcoin

is a hedge, a diversifier, or a safe haven drawing on the econometric models

featured in papers by Capie, Mills and Wood (2005), Baur and Lucey (2010)

and Ciner, Gurdgiev and Lucey (2010, revised 2012). Through these tests I

hope to address the question: as an asset, does bitcoin behave like gold? My

null and alternate hypotheses are therefore:

(4.1.1)

(4.1.2)

Here the condition “behave like gold” explicitly refers to whether bitcoin works

as a safe haven or a hedge for other assets.

Baur and Lucey (2010) define a hedge as:

“…an asset that is uncorrelated or negatively correlated with another asset or

portfolio on average.” (p. 219)

They go on to define a safe haven as:

“…an asset that is uncorrelated or negatively correlated with another asset or

portfolio in times of market stress or turmoil.” (p. 219)

Finally, it may be the case that bitcoin is a diversifier which they define as:

“…an asset that is positively (but not perfectly) correlated with another asset

or portfolio on average.” (p. 219)

4.2: Model 1

To address these questions I will run two separate models. The first model, to

test whether bitcoin is a hedge or a diversifier against stocks, bonds and

currencies, has a mean equation of the form:

19

(4.2.1)

Where the returns on each asset are calculated by taking the first difference

of the logarithm to ensure each series were stationary 15 and ,

, , and are the returns on bitcoin, stocks, bond yields and

currencies respectively. For this model the hypotheses are therefore:

(4.2.2)

(4.2.3)

An examination of the residuals of an ordinary least squares (OLS) estimation

of the mean equation for each group of series suggested the use of a

GARCH16 model, which is consistent with the work done by previous papers

(Capie et al. 2005 etc.). Financial time series often “exhibit periods of

unusually high volatility followed by more tranquil periods of low volatility”

(Asteriou and Hall, 2006, p. 249); this is known as volatility clustering. When

this is the case the assumption of the OLS methodology, that the variance of

the error term is constant and time-invariant (is homoskedastic) is violated

and we say that the variance is heteroskedastic (Hill, Griffiths and Lim, 2012,

p. 299). When time series exhibit heteroskedasticity it is often best to

dynamically model the variance using the ARCH17 class of models. GARCH

models are generalised ARCH models which allow for the capture of “long

lags in the shocks with only a few parameters” (Hill et al., 2012, p. 526),

allowing for more parsimonious estimation. I estimated a number of different

15

To formally test for stationarity Augmented Dickey Fuller unit root tests were applied to

each series. Cointegration was also tested for as non-stationary series can be related to one

another if they are cointegrated. The logarithm of each series was found to be not cointegrated

with any of the other series. 16

Further testing was performed on the residuals to confirm the presence of autoregressive

heteroskedasticity such as an ARCH-LM test and an examination of a correlogram of the

squared residuals. 17

Auto-Regressive Conditional Heteroskedasticity

20

forms of GARCH model including GARCH (1, 1) 18 , T-GARCH 19 and

IGARCH20. The chosen model was a GARCH (1, 1) with a generalised error

distribution (GED) of the form:

(4.2.4)

The GARCH model and lag length were selected using the Akaike and

Schwartz (Bayesian) information criterion, and the log likelihood function. The

error distribution was chosen from an examination of the residuals21.

4.3: Model 2

The second model, to test whether bitcoin is a safe haven, has mean

equation of the form:

(4.3.1)

This model was chosen using the same criteria as for model 1 and is again a

GARCH (1, 1) model, with variance equation of the same form as equation

(4.2.4) above. The terms , , and are quantiles

used to account for extreme shocks, and represent the bottom 10 and 5

percent of daily returns for stocks and currencies, and the top 10 and 5

percent of changes in bond yields. When estimated simultaneously the

parameters , and can be thought of as vectors. For stocks and

currencies if the return is larger than the q% quantile, the value is zero. For

18

GARCH (1, 1) is the simplest form of GARCH model which allows the variance of the

residual of the estimated mean equation to depend on the “past values of the shocks, which

are captured by the lagged squared residual terms, and on past values of itself” (Asteriou and

Hall, 2006, p. 260). 19

T-GARCH is a threshold GARCH model where “positive and negative news are treated

asymmetrically.” (Hill, Griffiths, and Lim, 2012, p. 527) It adds in a multiplicative dummy

variable into the variance equation to determine whether there is a statistically significant

difference when shocks are negative, as is often the case in financial time series (Asteriou et

al., 2006, p. 267). 20

IGARCH is an integrated GARCH model used when the variance of the residuals is very

persistent. This again is very common for financial returns data. 21

This included looking at a correlogram of the Q-statistics (test for serial correlation), a

Histogram-Normality test and an ARCH-LM heteroskedasticity test.

21

bonds, if the change in yield is smaller than the q% quantile, the value is zero.

Following work done by Baur and Lucey, these quantiles can be used to

analyse the role of bitcoin in times of extreme market stress. Baur and

Lucey’s paper used quantiles of 5%, 2.5% and 1%, however, as there is just

over 3 full years of data available for bitcoin, I chose 10% and 5% in order to

ensure adequate data for estimation. The theory behind the use of quantiles

to examine the safe haven hypothesis is:

“If stocks or bonds exhibit extreme negative returns, investors buy gold

[bitcoin] and bid up the price of gold [bitcoin]. If the price of gold [bitcoin] is not

affected, investors neither purchase nor sell gold [bitcoin] in such adverse

market conditions.” (Baur and Lucey, 2010, p. 220)

The hypotheses tested using model 2 are:

(4.3.2)

(4.3.3)

As far as I am aware, there are no academic papers discussing the

fundamental relationship between bitcoin and other financial assets.

Determining whether there is a relationship and the nature of that relationship

is therefore an important first step in understanding the role bitcoin plays in

the universe of investable assets, although admittedly the role is likely to be a

small one. In particular an econometric evaluation of whether bitcoin has

played a safe haven role, as portrayed in the financial media during the recent

banking crisis in Cyprus, will be examinable through the use of Eurozone data

series.

The following section will discuss the results obtained from estimating the

models discussed above. For Equation 4.2.1 if the estimated of a variable is

zero or negative, and statistically significant, then it implies that bitcoin is a

22

hedge for that asset on average. So if is zero or negative then bitcoin is a

hedge for stocks. For Equation 4.3.1 if the values of the coefficient estimate

for one of the quantiles of an asset class (i.e. for stocks and for

currencies) is non-positive and statistically significant then bitcoin serves as a

safe haven for those assets in times of market turmoil. For bonds, if the value

of is positive and statistically significant then bitcoin is a safe haven. The

reason the inverse of stocks and currencies is true for bonds is due to the use

of yields rather than prices. If we assume that bond yields and prices are

perfectly negatively correlated, then the top 5 or 10% of extreme positive

changes in bond yields represent a spike in yields (sharp drop in prices) and

generally occur when the market risk premium increases.

23

5: Empirical Analysis

This section outlines the results obtained from estimating the models

described in Chapter 4. The results are broken down into those obtained from

each model by market.

5.1: Model 1

5.1.1: US Market

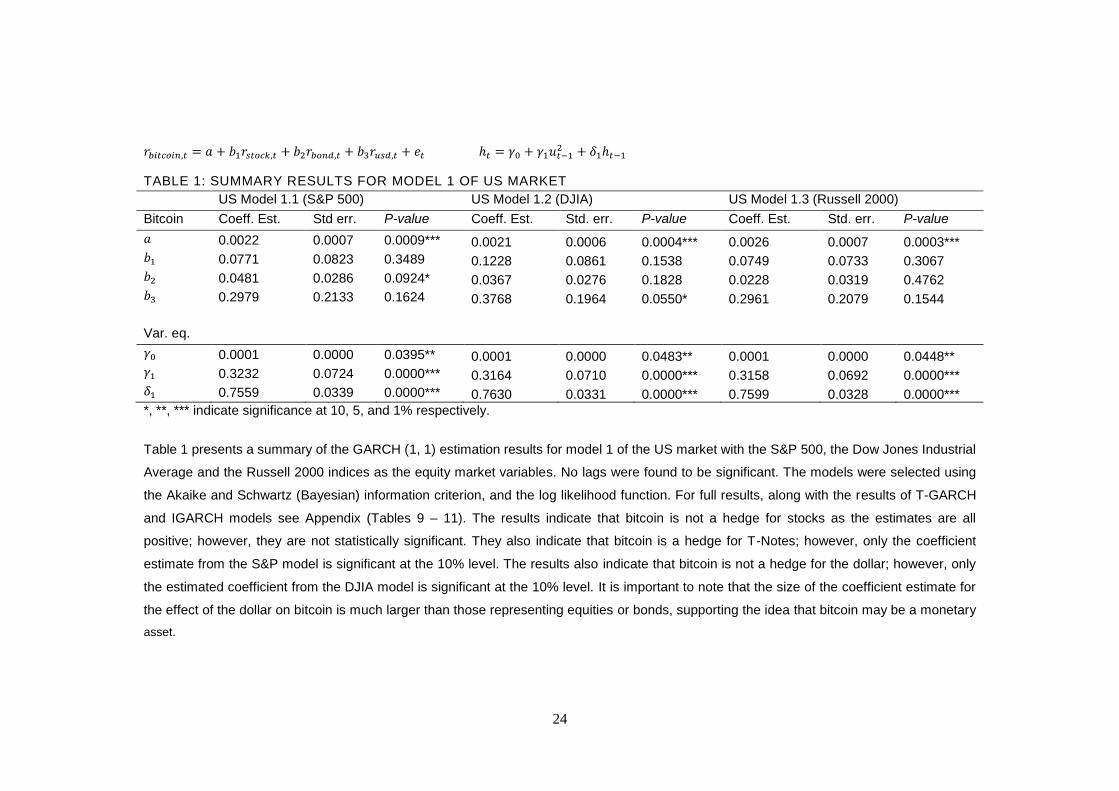

The summary results from estimating model 1 for the US market are

presented in table 1 below. The coefficient estimates for the average effects

of stock returns on bitcoin returns are not statistically significant. However,

they are all positive on average implying that whilst for the sample tested the

relationship between bitcoin and the US equity market is weak the direction of

this relationship may be positive. The coefficient estimates for the average

effect of a change in bond yields on bitcoin returns are significant at the 10%

level only in model 1.1 with the S&P 500 as the equity market proxy. They are

however, consistently low and positive implying a negative relationship

between bitcoin returns and bond prices. This means that bitcoin could serve

as a hedge for the US bond market. The estimates for the average effect of

returns on the US dollar are only significant (at the 5% level) in model 1.2 with

the Dow Jones as the equity market variable. However, the estimates are all

consistently positive and the effect is much stronger than for equities or bonds

which supports the idea that bitcoin is a monetary asset.

The estimated ARCH (1) and GARCH (1) terms in the variance equations are

all positive and highly statistically significant. In addition they are all very

similar in size indicating that the model is relatively robust and is an

appropriate selection for modelling the conditional variance of the system.

24

TABLE 1: SUMMARY RESULTS FOR MODEL 1 OF US MARKET

US Model 1.1 (S&P 500) US Model 1.2 (DJIA) US Model 1.3 (Russell 2000)

Bitcoin Coeff. Est. Std err. P-value Coeff. Est. Std. err. P-value Coeff. Est. Std. err. P-value

0.0022 0.0007 0.0009*** 0.0021 0.0006 0.0004*** 0.0026 0.0007 0.0003*** 0.0771 0.0823 0.3489 0.1228 0.0861 0.1538 0.0749 0.0733 0.3067 0.0481 0.0286 0.0924* 0.0367 0.0276 0.1828 0.0228 0.0319 0.4762 0.2979 0.2133 0.1624 0.3768 0.1964 0.0550* 0.2961 0.2079 0.1544

Var. eq.

0.0001 0.0000 0.0395** 0.0001 0.0000 0.0483** 0.0001 0.0000 0.0448** 0.3232 0.0724 0.0000*** 0.3164 0.0710 0.0000*** 0.3158 0.0692 0.0000*** 0.7559 0.0339 0.0000*** 0.7630 0.0331 0.0000*** 0.7599 0.0328 0.0000***

*, **, *** indicate significance at 10, 5, and 1% respectively.

Table 1 presents a summary of the GARCH (1, 1) estimation results for model 1 of the US market with the S&P 500, the Dow Jones Industrial

Average and the Russell 2000 indices as the equity market variables. No lags were found to be significant. The models were selected using

the Akaike and Schwartz (Bayesian) information criterion, and the log likelihood function. For full results, along with the results of T-GARCH

and IGARCH models see Appendix (Tables 9 – 11). The results indicate that bitcoin is not a hedge for stocks as the estimates are all

positive; however, they are not statistically significant. They also indicate that bitcoin is a hedge for T-Notes; however, only the coefficient

estimate from the S&P model is significant at the 10% level. The results also indicate that bitcoin is not a hedge for the dollar; however, only

the estimated coefficient from the DJIA model is significant at the 10% level. It is important to note that the size of the coefficient estimate for

the effect of the dollar on bitcoin is much larger than those representing equities or bonds, supporting the idea that bitcoin may be a monetary

asset.

25

Overall the results from estimating model 1 for the US market are

inconclusive given the varying significance of the estimated coefficients. I fail

to reject the null hypothesis that bitcoin is not negatively correlated with

equities on average. For model 1.2 the coefficient estimate for the relationship

between bitcoin and the dollar is positive and significant at the 10% level, in

which case I accept the null that bitcoin is not negatively correlated with the

US dollar on average. In the case of bonds, for model 1.1 I reject the null and

accept the alternate hypothesis at the 10% level as bitcoin is positively

correlated with changes in bond yields (negatively correlated with prices).

One positive result from estimation is that the direction and strength of the

relationships between bitcoin returns and the returns on other assets are

relatively consistent. The fact that for the most part the estimated coefficients

are not significant implies that bitcoin returns may be orthogonal to equities,

bonds and the US dollar. This may mean that while bitcoin is not strictly a

hedge, using the definition supplied by Baur and Lucey (2010), it may be a

natural hedge due to the low and insignificant correlations with other asset

classes. In addition the low correlations imply that bitcoin is a diversifier.

26

5.1.2: EU Market

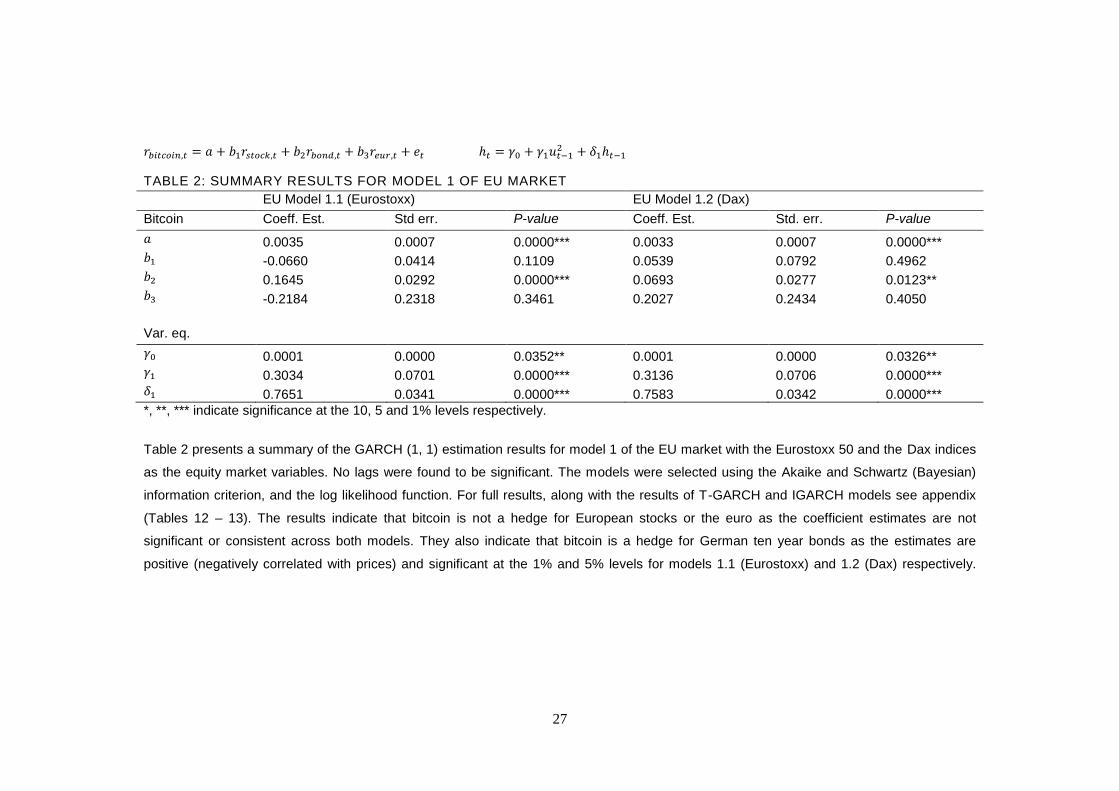

The summary results from estimating model 1 for the EU market are

presented in table 2. The coefficient estimates for the average effect of bitcoin

returns on European equity market returns are never significant implying that

no clear relationship exists. In addition, the relationships represented by the

coefficient estimates from models 1.1 and 1.2 are in opposing directions

making interpretation more difficult. The coefficient estimates for the average

effect of a change in bond yields on bitcoin returns are positive and

statistically significant at the 5% level in both models, and at the 1% level in

model 1.1. These estimates are 0.1645 and 0.0692 for models 1.1 and 1.2

respectively. This implies that bitcoin is a hedge for Eurozone bond markets

on average, as represented by German ten year bond yields. The coefficient

estimates for the average effect of returns on the euro index on bitcoin returns

are not statistically significant. In addition the signs vary across both models

again causing interpretation difficulties. The ARCH and GARCH coefficients

from estimating the variance equation are all positive and statistically

significant at the 1% level.

Overall the results from estimating model 1 for the EU market are

inconclusive regarding equity and currency markets as a result of the

insignificant and contradictory coefficient estimates. I therefore fail to reject

the null hypothesis that bitcoin returns are not negatively correlated with EU

equity markets and the euro on average. However, in the case of European

bond markets I can reject the null, and accept the alternate hypothesis as

bitcoin returns are positively correlated with changes in German bond yields

(negatively correlated with prices) meaning that bitcoin appears to be a hedge

for European bond markets. It is important to note that the strength of this

relationship varies a good deal across both models meaning that whilst the

direction of the relationship may be statistically significant, the degree to

which changes in bond yields affect changes in bitcoin returns is uncertain.

27

TABLE 2: SUMMARY RESULTS FOR MODEL 1 OF EU MARKET

EU Model 1.1 (Eurostoxx) EU Model 1.2 (Dax)

Bitcoin Coeff. Est. Std err. P-value Coeff. Est. Std. err. P-value

0.0035 0.0007 0.0000*** 0.0033 0.0007 0.0000*** -0.0660 0.0414 0.1109 0.0539 0.0792 0.4962 0.1645 0.0292 0.0000*** 0.0693 0.0277 0.0123** -0.2184 0.2318 0.3461 0.2027 0.2434 0.4050

Var. eq.

0.0001 0.0000 0.0352** 0.0001 0.0000 0.0326** 0.3034 0.0701 0.0000*** 0.3136 0.0706 0.0000*** 0.7651 0.0341 0.0000*** 0.7583 0.0342 0.0000***

*, **, *** indicate significance at the 10, 5 and 1% levels respectively.

Table 2 presents a summary of the GARCH (1, 1) estimation results for model 1 of the EU market with the Eurostoxx 50 and the Dax indices

as the equity market variables. No lags were found to be significant. The models were selected using the Akaike and Schwartz (Bayesian)

information criterion, and the log likelihood function. For full results, along with the results of T-GARCH and IGARCH models see appendix

(Tables 12 – 13). The results indicate that bitcoin is not a hedge for European stocks or the euro as the coefficient estimates are not

significant or consistent across both models. They also indicate that bitcoin is a hedge for German ten year bonds as the estimates are

positive (negatively correlated with prices) and significant at the 1% and 5% levels for models 1.1 (Eurostoxx) and 1.2 (Dax) respectively.

28

5.2: Model 2

5.2.1: US Market

The summary results from estimating model 2, to test whether bitcoin serves

as a safe haven for the US market are presented in table 3. The reactions in

the bitcoin market following periods of extreme negative stock returns are

positive22 and not significant23, indicating that bitcoin is not a safe haven for

US equities. The estimated coefficients for the effect of extreme positive

spikes in US bond yields (falls in prices) on the bitcoin market are negative for

the 90% quantile and positive for the 95% quantile. This implies that bitcoin

can function as a safe haven for the most extreme spikes in bond yields;

however, none of the coefficients are statistically significant. The coefficient

estimates for the average effect of extreme dollar devaluations are negative

on average24. This implies that bitcoin may function as a safe haven in times

of extreme returns against the dollar; however, none of these estimates are

statistically significant.

The estimated coefficients for the average effect of returns on equities, bond

yields and the dollar are consistent with those found in model 1 indicating that

the direction of the relationships may be correct, although they are for the

most part insignificant. It is worth noting that for models 2.1 and 2.2 the

coefficients representing the relationship between bitcoin and the dollar are

positive and statistically significant at the 10 and 5% levels respectively. The

effect of a change in the relative strength of the dollar on bitcoin are again

stronger than the effects of changes in equity or fixed income markets, which

supports the notion that bitcoin is a monetary asset.

22

For the model using the Russell 2000 index as the equity market proxy the variable

representing the 5% quantile is negative, however, the sign of this result is not consistent with

the other coefficients estimated. 23

For the model using the Dow Jones index as the equity market proxy the variable

representing the 5% quantile is positive and significant at the 5% level, however, the

significance of this result is not consistent with the other coefficients estimated. 24

Apart from the coefficient estimate of the 5% quantile in the Dow Jones model which is

positive.

29

TABLE 3: SUMMARY RESULTS OF MODEL 2 FOR US MARKET