is asia the answer? dr. brian w tempest the 2008 ims pharma strategy conference new york –12 th...

TRANSCRIPT

Is Asia the Answer?

Dr. Brian W Tempest

www.briantempest.com

The 2008 IMS Pharma Strategy Conference

New York –12th February 2008

DR. BRIAN W. TEMPEST CSci, CChem, MRSC, BSc, PhD

Dr. Brian Tempest advises companies and investment funds on their strategy in Asia based on his wide experience in China, Japan, SE Asia and India where he has

lived for the last 9 years and continues to have a home. Tempest has previously been President, Managing Director, CEO, Chief Mentor and Executive Vice

Chairman of Ranbaxy Laboratories(the leading Indian Pharmaceutical Company) during the 12 years between 1995 and 2007. He is one of the few westerners (if not the only westerner) to lead a Sensex Nifty 50 Indian blue chip MNC and as a result has a valuable insight into India. Tempest has also been Regional Director Far East for Glaxo responsible for Japan, China, Korea and Taiwan. Tempest has worked in the Pharmaceutical Industry for the last 37 years and led Global Healthcare

businesses, R&D and Global Manufacturing Organisations. Tempest has also led Investor meetings across Asia, Europe and USA. He is now a Non Executive

Director of Ranbaxy India, an advisor to the JM Financial India Private Equity Fund and a Honorary Professor of the Management School at Lancaster

University, UK. He speaks at worldwide conferences on the Challenge from India and China and more information on these presentations is available on

www.briantempest.com [email protected] / [email protected] +91-98100-91192 / Tel:+44 1753 864 616

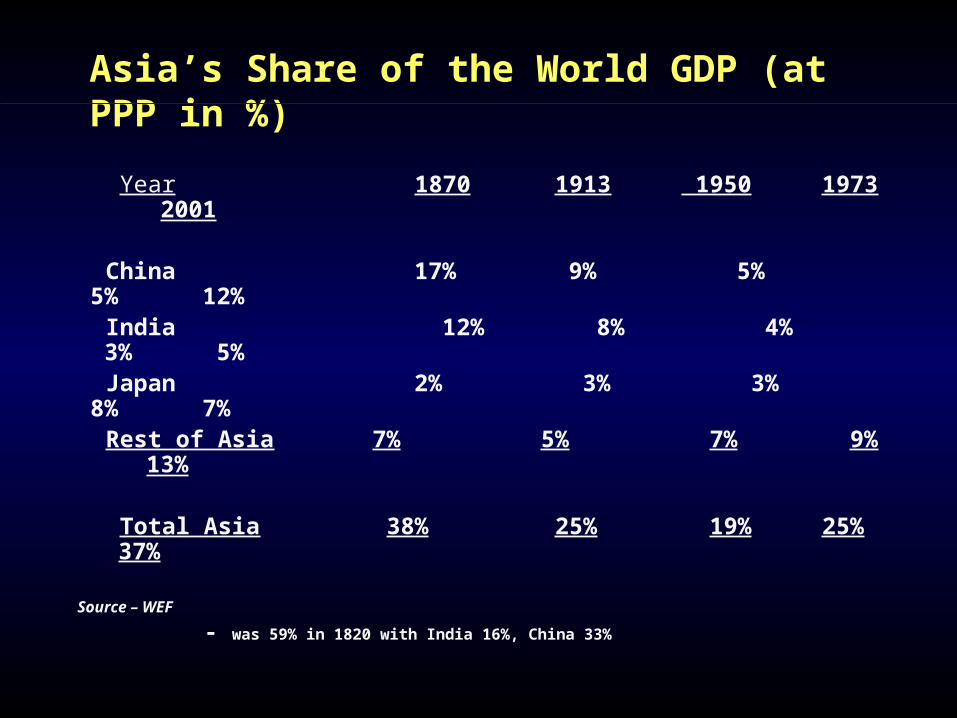

Asia’s Share of the World GDP (at PPP in %)

Year 1870 1913 1950 1973 2001 China 17% 9% 5% 5% 12% India 12% 8% 4% 3% 5% Japan 2% 3% 3% 8% 7%

Rest of Asia 7% 5% 7% 9% 13% Total Asia 38% 25% 19% 25% 37%

Source – WEF

- was 59% in 1820 with India 16%, China 33%

The View from Europe – the Challenge

Source – FT

The View from India - a Global Competition

The View from the USA – Asian Cars

The View from Japan - a Race to Prosperity

Japan’s Wealth Advantage

Canada2%

Rest of World10%

Japan27%

Germany4% Italy

4%

France5%

UK6%

USA37%

Netherlands2%

Spain1%

Switzerland1%Taiwan

1%

Source: The World Distribution of Household Wealth

Is Asia the Answer?

Market drivers Competition is rising Branded generics from Asia IP changes in USA M&A and Private Equity East-West Alliances Drug Development

The Asian Productivity Advantage

India a usa Pharma view USA India a usa Pharma view USA

1 chemist Better education x 1.3 1 chemist 1 chemist Better education x 1.3 1 chemist

70 hours/week Longer working time x 1.3 50 hours/week 70 hours/week Longer working time x 1.3 50 hours/week

$ 800 monthly Lower cost x 20 $ 12,000 monthly $ 800 monthly Lower cost x 20 $ 12,000 monthly

Sources: IPHMR Conferences, New Delhi August 2004

The Asian Education Advantage

The Asian Education Advantage

Engineers/Science graduates p.a – India 0.7m, China 0.5m, EU 0.5m, USA 0.4m, Japan 0.3m

Asia’s Youthful Advantage

Percentage of Population aged 65 and older

6.9

5

8.3

14.714.8

21.5

29.2

12.3

18.7

21.4

13.2

22.7

China India Europe North America

2000 A

2025 E

2050 E

Sources: AXA Framlington

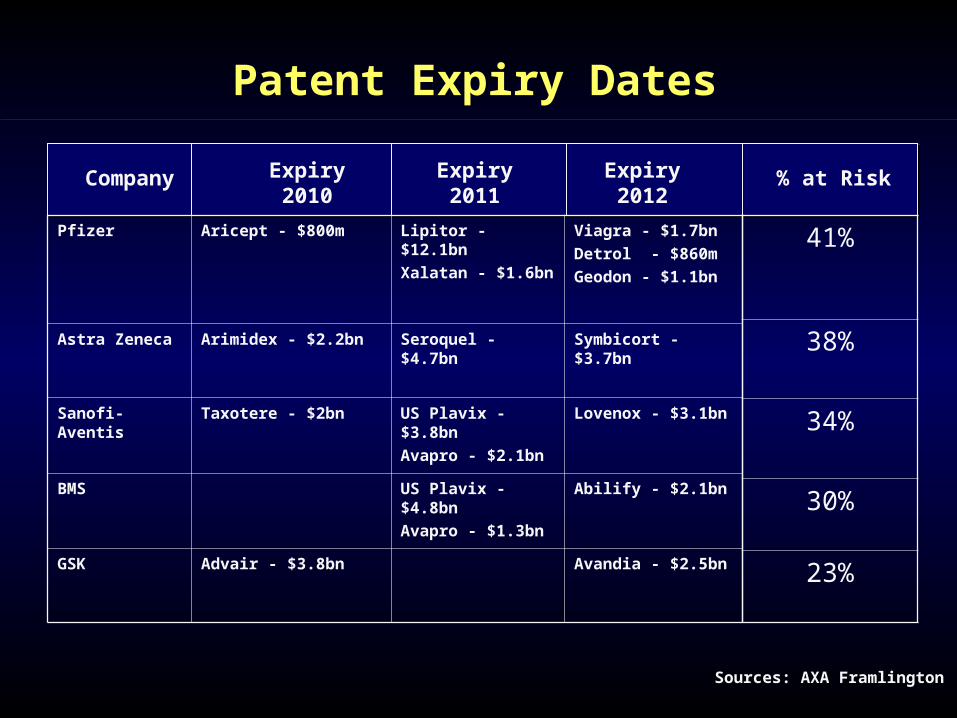

Company Expiry2010

Expiry2012

Expiry2011

Pfizer Aricept - $800m Lipitor - $12.1bn

Xalatan - $1.6bn

Viagra - $1.7bn

Detrol - $860m

Geodon - $1.1bn

Astra Zeneca Arimidex - $2.2bn Seroquel - $4.7bn Symbicort - $3.7bn

Sanofi-Aventis Taxotere - $2bn US Plavix - $3.8bn

Avapro - $2.1bn

Lovenox - $3.1bn

BMS US Plavix - $4.8bn

Avapro - $1.3bn

Abilify - $2.1bn

GSK Advair - $3.8bn Avandia - $2.5bn

Patent Expiry Dates

41%

38%

34%

30%

23%

% at Risk

Asian Competition is Rising CPHI Attendees, Milan, 2nd – 4th Oct’07

1. China 467 – 33%

2. India 189 – 13%

3. Germany 96

4. Italy 80

5. USA 75

6. UK 55

7. France 55

8. ROW 387

Total 1404

As registered on July 25, 2007

Generics – API’s

USA DMF filings by India % Share of USA DMF filings

India China 2005 37% 10% 2006 44% 14%

Q1’07 48% 17% Q2’07 37% 18%

Q3’07 42% 16% Source: US FDA / J P Morgan, 2 may 2007

Source: US FDA, Credit Suisse

India China 2004 187 48 2005 252 87 2006 357 128

Source: US FDA / J P Morgan, 6th August 2006

- One in every four ANDAs filed by Indian Companies in top USA FDA filers Source: KPMG

- No Chinese generic company has yet filed a USA FDA ANDAbut expected in 2008

Generics - ANDAs

0

50

100

150

200

250

300

2002 2003 2004 2005 2006

2446

64

144

ANDA Filings in USA by Indian Companies

250

Sources: Goldman Sachs 2007

Top 5 Global Pharma Markets 2020

Rank Country Size

1.

2.

3.

4.

5.

USA

China

Japan

France

India

$ 475b

$ 125b

$ 61b

$ 51b

$ 43b

The Rise of the Indian Middle Class

R&D Productivity is Falling

Global Pharmaceuticals Sales Trends

Global Pharmaceuticals Equity Trends

Shareholder Value

BCG 100 Challengers

Country Total State Private

China 41 29 12

India 20 0 20

Brazil 13 1 12

Russia 6 3 3

Source BCG

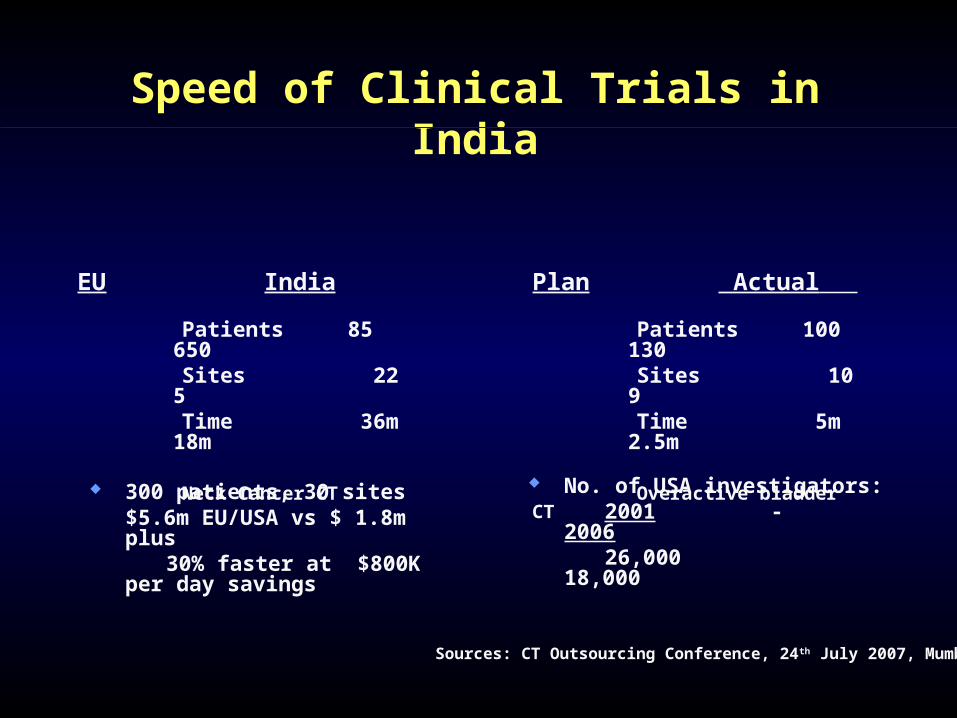

Speed of Clinical Trials in India

EU India

Patients 85 650 Sites 22 5 Time 36m 18m

Neck Cancer CT

Plan Actual

Patients 100 130 Sites 10 9 Time 5m 2.5m

Overactive bladder CT

300 patients, 30 sites$5.6m EU/USA vs $ 1.8m plus

30% faster at $800K per day savings

No. of USA investigators: 2001 - 2006 26,000 18,000

Sources: CT Outsourcing Conference, 24th July 2007, Mumbai

Electronic Data Capture in India

% Trials in EDC

2005 2007 25% 45%

Savings

Paper EDC

$2.8m $ 0.5m

2004 data

Sources: CT Outsourcing Conference, 24th July 2007, Mumbai

Accuracy

- 300 GSK Staff

- 2.2m Clinical Data sheets

- 450 Trials

- No data security issues

- Error rate <0.01 / 100k

Source: BCG report “Looking Eastward, Sept’2006”

Branded Generics

Promotion to doctors rather than pharmacists Consistent sales year on year No huge highs & lows for sales and profits Need field force to promote products Tend to be profitable Promoted in conventional manner Global generic brands Relevant to Central Europe, East Europe, Latam, Asia Ranbaxy half branded generics & half commodity

generics

Branded Generics - the Analyst’s view

“Branded Generics are the most profitable place to be in generics and there are a few markets with better branded characteristics than those of the Middle East and North Africa region”

Frances Cloud Nomura September 14 2007

Different Global Generic Market Sizes $bn

Region Sandoz

2006

IMS

2008USA 23 68

West Europe 14 19

East Europe 13 NA

Japan 3 3

Latam/Canada 10 3 (Canada only)

ROW 37 7

Total 100 100

ROW Top 10 Generic Markets - $bn

IP – USA Pendulum

“A key USA Supreme Court ruling KSR VS Teleflex led to Pharmaceutical patents being more easily challenged on the grounds of obviousness, a ruling which immediately came into play when J&J & Merck had a US patent for Pepcid Complete (Famotodine) found to be obvious”.

Scrip, July 6th 2007, p3

The full beneficial impact of this ruling on the generic industry is yet to be seen .

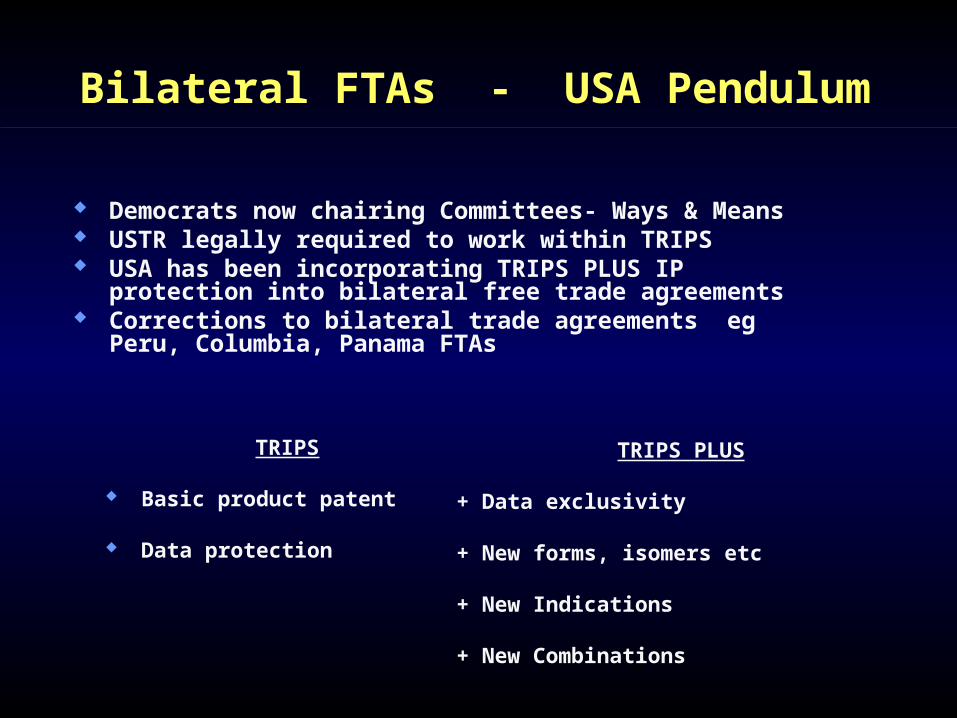

Bilateral FTAs - USA Pendulum

Democrats now chairing Committees- Ways & Means USTR legally required to work within TRIPS USA has been incorporating TRIPS PLUS IP protection into

bilateral free trade agreements Corrections to bilateral trade agreements eg Peru, Columbia,

Panama FTAs

TRIPS

Basic product patent

Data protection

TRIPS PLUS + Data exclusivity

+ New forms, isomers etc

+ New Indications

+ New Combinations

Sources: 1. IMS Midas, March 20052. Earth Trend Data Tables 2005

82% of the world population accounts for only 12% of the Global pharmaceutical sales

Region Pharma Sales Population

North America

Europe

Japan

$255 b 47%

$158 b 30%

$59 b 11%

332 5%

725 11%

128 2%

Asia/Africa/Aus

Latam

88%

$41 b 8%

$20 b 4%

18%

4711 73%

558 9%

12% 82%

Worldwide $533 b 100% 6454 100%

Should IP be the same across all Countries?

0

1000

2000

3000

4000

5000

6000

USA Thai China IndiaBrazil

USD

Sources: World Health Report 2005

Per Capita Expenditure on Healthcare 2002

Enforcement or Evergreening ?

India IP 02/03 06//07 Filed 11466 28882 Examined 9538 14119 Granted 1379 7359

- 140 patent examiners 2007- 600 more planned- Attrition an issue- Weekly patent journal- IP Appellate Court

Source: Business Standard, 16th Aug’2007

• 1995 – 2005 FDA cleared 327 drugs

• 95% pre 1995 – before WTO deal

• 16 basic patent molecules possible

• However 9000 Pharma applications - for evergreen changes

- for new indications

Source: Gopa Kumar “Centre for Trade & Development, Delhi”

PCT Filings from Asia

PCT Files from Developing Countries 2006

1. Huawei - China2. LG - Korea3. Samsung - Korea4. LG Cem - Korea5. Elec Telecom – Korea6. 2TE – China7. STR – Singapore8. Ranbaxy – India9. CSIR – India10. NHN - Korea

Ranbaxy Patent Filings to 2005

24 32 49 86 146 170 185

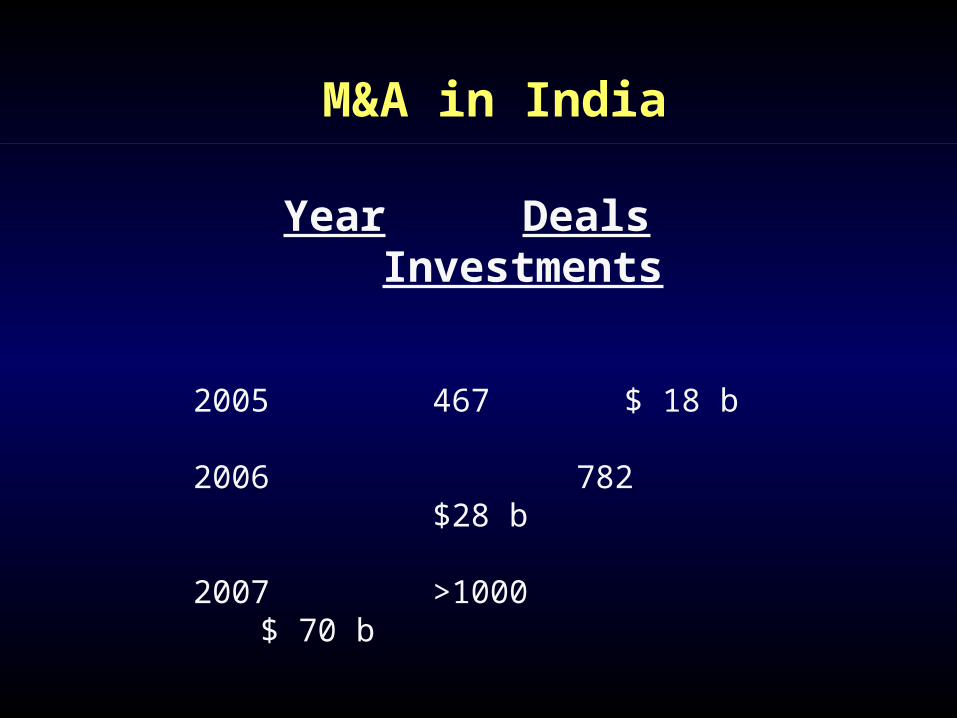

M&A activity in India is rising

M&A in India

Year Deals Investments

2005 467 $ 18 b

2006 782 $28 b

2007 >1000 $ 70 b

Source Grant Thornton Deal Tracker

M&A Building the Top Players in the Global Generic Market

% PE/VC Share of all Global M&A Deals

0

5

10

15

20

25

2000 2001 2002 2003 2004 2005

5%6%

9%

16%17%

21%

Sources: Thomson One Banker, BCG Analysis

Asian PE Deals

Country No. of deals Sum Invested - $mChina 103 1489

India 90 1369

Hong Kong 5 186

Australia 26 71

Taiwan 6 33

S.Korea 30 29

Thailand 2 29

Singapore 4 16

New Zealand 9 3

Total 278 3233

Sources: Thomson Financial in H1 2007 excluding Japan

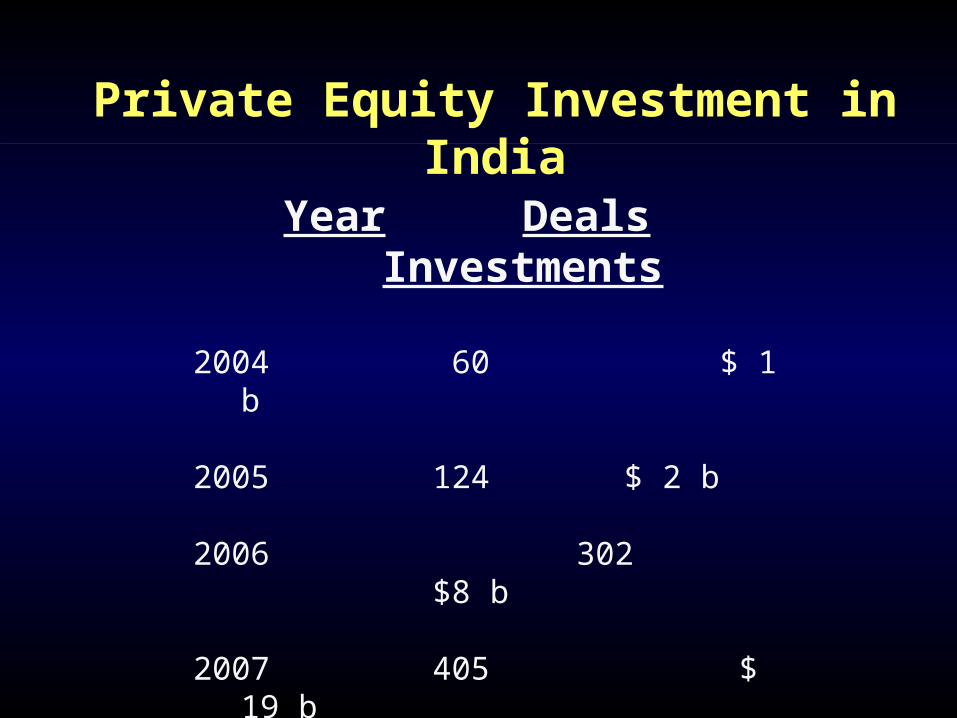

Private Equity Investment in India

Year Deals Investments

2004 60 $ 1 b

2005 124 $ 2 b

2006 302 $8 b

2007 405 $ 19 b

Source Grant Thornton Deal Tracker

Key Challenges to the Asian Scenario

Potential Challenge – Asian Flu*

*50% of world chickens bred in Asia

CO2 emission - % of World total in 1990-2000

USA 23%EU 25 17%China 14%Russia 7%Japan 5%India 4%

– source: WRI, EIA

Potential Challenge – Climate Change

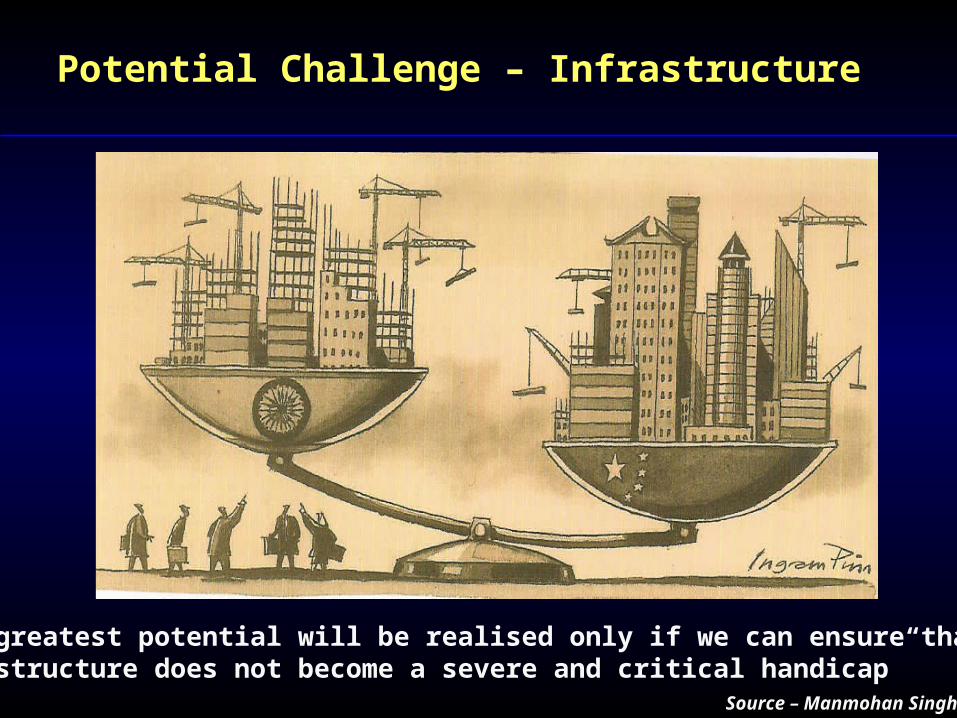

Potential Challenge – Infrastructure

Source – Manmohan Singh

“Our greatest potential will be realised only if we can ensure that ourInfrastructure does not become a severe and critical handicap”

Corruption Perception Index

Rank Country

1 Finland, Iceland, NZ5 Singapore11 Austria, Luxemburg, UK16 Germany20 Belgium, Chile, USA42 Mauritius, S.Korea51 South Africa, Tunisia70 Brazil, China, India, Mexico121 Philippines, Russia

163 Haiti

Sources: Transparency International 2006, selected countries only

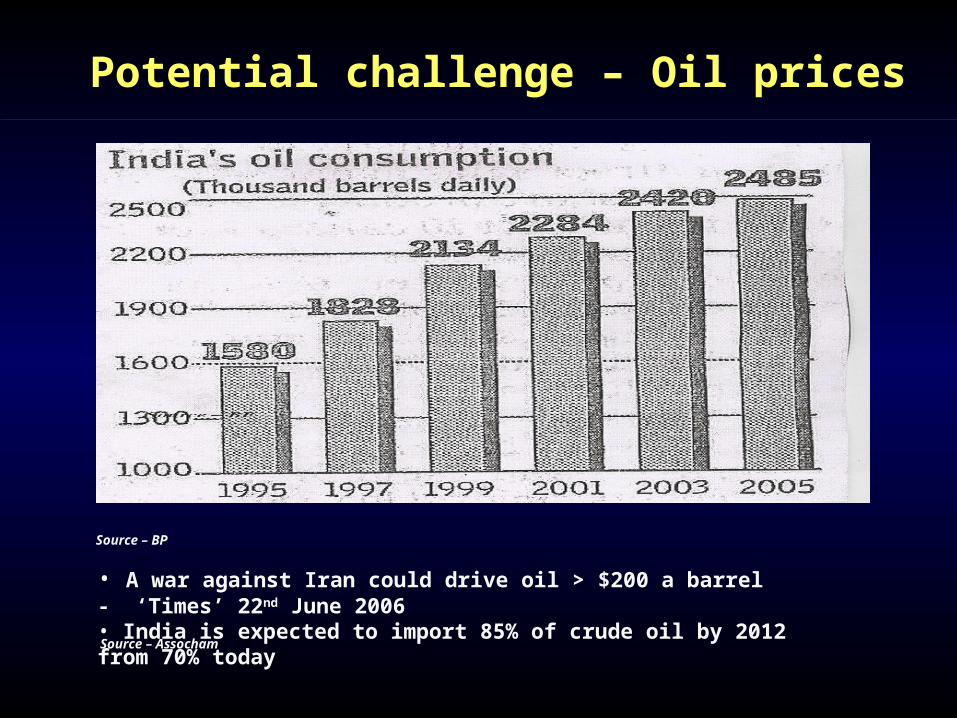

Potential challenge – Oil prices

Source – Assocham

• A war against Iran could drive oil > $200 a barrel - ‘Times’ 22nd June 2006• India is expected to import 85% of crude oil by 2012 from 70% today

Source – BP

Potential Challenge – over the border

Potential Challenge - Currency Volatility

The Tempest Crystal Ball

•India will continue to be a Key Driver in the Global Generic Industry

•Competition is rising – Post TRIPs Indian companies will evolve

•Discovery companies will continue to be attracted to India for CT, EDC, MO. China will be perceived to be stronger in biology/ toxicology

•IP changes in US will slowly favor Generics

•Alliances between Western Biotech and Asians companies will expand. M&A PE deals will grow. Singapore, Vietnam, Bangladesh & Nepal will take a rising importance

•How to use Asia in Drug Development will become the key opportunity

Early discovery leads from USA, Europe or Singapore Molecular optimisation from India

Toxicology from China, Central Europe, Singapore Electronic Data Capture India

API Manufacture India

Drug Formulation Manufacture India, USA

Phase 1 Clinical Trials Europe

Phase 2,3 heavy use of India

Corporate back office India

Is Asia the Answer for Drug

Development?

“The Indian System looks ramshackleand improvised. But at its best it is capable of brilliance”

“When we say the Silicon Valley isbuilt on ICs we don’t mean integratedcircuits – we mean Indians & Chinese”

“The UK needs to wake up to whatIndia is becoming”

Source: DEMOS report – January 2007

Perceptions of Asia

Asia economic strength is returning to levels seen in the past India is a global strategic asset for developed markets having

many advantages with some challenges. India is a rich location for R&D alliances and CT outsourcing

MNCs will dip in & out of India & China South East Asian economies will be driven by India & China

Japan will continue to represent a huge share of global wealth “China & India represent the future of Asia and quite possibly

the future for the global economy” – Steve Roach, Morgan Stanley

Summary

Thank You