irs exempt organization hot topics, including updates on rulings

TRANSCRIPT

© 2014 Gray Reed & McGraw, P.C.The information contained herein is subject to change without notice

IRS Exempt Organization Hot Topics, Including Updates on Rulings and Court Cases

Monday, May 23, 2016by

Austin C. CarlsonAttorney | CPA

Jennifer L. GurevitzAttorney | CPA

Greg W. SampsonAttorney

© Gray Reed & McGraw, P.C.

Protecting Americans from Tax Hikes (PATH) Act of 2015

• Permanently extended several key tax provisions including:• Qualified charitable distribution provision.• Contributions of real property for easements provision.• Adjustment of S corporation stock on contributions to charity.

• New category for public charity – Agricultural Research Organization• Requirement of 501(c)(4) organizations to provide notice to IRS (name

date purpose) – Form hasn’t come out yet.• Donation to 501(c)(4), (5) and (6) not subject to gift tax.

© Gray Reed & McGraw, P.C.

Recent Revocations of Exempt Status

• Commerciality• Inactivity• Lack of records• Conduit for foreign organization with no control• Failure to operate primarily for exempt purposes

© Gray Reed & McGraw, P.C.

Recent Revocations of Exempt Status

• Commerciality: Private letter rulings (PLRs)) 201503016, 201510059, 201511023, 201514013, 201525011, 201525012, 201526020, 201535019, 201538025, 20154403

• 201503016: Online Charity Ecommerce Platform• 201510059: researching, manufacturing and retailing of

pharmaceutical products (cancer testing “kits”)• 201511023: Business/Start Up help organization, activities different

than 1023, loans to officers

© Gray Reed & McGraw, P.C.

Recent Revocations of Exempt Status

• Inactivity (PLRs 201509040, 201514010, 201514012, 201517009, 201517011, 201534015)

• PLR 201509040. Had dissolved the entity but notified the IRS in case they wanted to restart operations.

• PLR 201514012. no longer conducted any activities, liquidated all assets, and provided no indication of plans to resume operations at any point. Forfeited state law status.

© Gray Reed & McGraw, P.C.

Recent Revocations of Exempt Status

• Lack of records PLR 201449001. Credit repair organization, for profit and not for profit entity with same names. No bank account or other records.

© Gray Reed & McGraw, P.C.

Recent Revocations of Exempt Status

• Conduit for foreign organization with no control. Failure to exercise adequate discretion and control over funds sent to organization operating schools in foreign country (PLRs 201511033, 201539032)

• PLR 201511033. Payments to foreign organizations must be reviewed and approved. Direct salary payments to foreign teachers circumvented foreign income tax laws.

© Gray Reed & McGraw, P.C.

Recent Revocations of Exempt Status

• Failure to operate primarily for exempt purposes PLRs 201514014, 201517008, 201517012, 201517015, 201524026, 201544030.

• PLR 201514014. The purpose of the organization changed from assisting AIDS/HIV patients with their pets.

• PLR 201517008. Providing housing at market rates for an undefined class of individuals.

© Gray Reed & McGraw, P.C.

Private Inurement/Private Benefit Denials

• Scholarships granted to members of one family – class too narrow. Case is on appeal. Educational Assistance Foundation for The Descendants of Hungarian Immigrants in The Performing Arts

• Religious organization’s funds used for president’s clothing, jewelry and other private expenses. “Daily devotional” website, loans between for profit and non profit. PLR 201533022.

© Gray Reed & McGraw, P.C.

UBIT Developments

Overview (from 2009, most recent data):• Unrelated business income tax returns filed by 42,469 tax-

exempt organizations.• Gross unrelated business income reported was $9.7 billion.• Unrelated business income tax paid was $263.1 million, including

certain other taxes

© Gray Reed & McGraw, P.C.

UBIT Developments

i. Fundraising events by alumni organization (TAM 201544025).ii. Proposed regulations on how certain organizations that provide

employee benefits (VEBA) must calculate unrelated business income tax (REG-143874-10)

iii. Rental income held not unrelated business income (IRC §512(b)(3)(A)(i)); proceeds from sale of capital property held not taxable (IRC § 512(b)(5)) (PLR 201435017).

© Gray Reed & McGraw, P.C.

Rev. Proc. 2015-53 Inflation Adjustments

• The exemption of annual dues paid by a member to an agricultural or horticultural organization that shall not be characterized as “unrelated trade or business” income (UTBI) will be $161.

• The UTBI of certain exempt organizations will not include a “low cost article” of $10.60 or less.

• The $5, $25, and $50 guidelines for disregarding insubstantial benefits received by a donor in return for a fully deductible charitable contribution under section 170, as set forth in Rev. Proc. 90-12 (as amplified by Rev. Proc. 92-49, and modified by Rev. Proc. 92-102) will be $10.60, $53, and $106, respectively.

• For tax years beginning in 2016, the annual per person, family, or entity limitation to qualify for the reporting exception for nondeductible lobbying expenses under section 6033(e)(3) will be $112 or less.

© Gray Reed & McGraw, P.C.

501(r) Regulations Issued for Charitable Hospitals

• Final regulations effective in December 2015• IRC §501(r) includes four new requirements that tax-exempt hospital

facilities are required to comply with related to a tax-exempt hospital facility’s:• Community Health Needs Assessment (IRC §501(r)(3));• Financial Assistance Policy (IRC §501(r)(4));• Limitation on amounts charged, to individuals eligible under the

organization’s financial assistance policy, for emergency or other medically necessary care (IRC §501(r)(5)); and

• Billing and collection practices (IRC §501(r)(6)).

© Gray Reed & McGraw, P.C.

501(r) Regulations Issued for Charitable Hospitals

• Penalties for Non-Compliance• Revocation of Tax Exempt Status• Taxation• CHNA Excise Tax• Minor Errors and Omissions (non disclosure requirements):

• such omission or error was minor and either inadvertent or due to reasonable cause;

• the hospital promptly corrects the error or omission; and• such correction includes the establishment (or review and, if necessary,

revision) of practices or procedures that are reasonably designed to promote and facilitate overall compliance with IRC section 501(r).

© Gray Reed & McGraw, P.C.

Update on 1023 Processing

In FY 2016:• Twenty-five tax examiners will review Forms 1023-EZ.• IRS projects about 3 percent increase in application receipts.• IRS anticipates receipts outpacing disclosures and an increased open

application inventory at fiscal year’s end.• Thirty determination specialists will be realigned to EO Examinations.• Division will continue to study data analyzed from Form 1023-EZ

predetermination reviews and will consider future adjustments to percentage of these applications selected for predetermination

© Gray Reed & McGraw, P.C.

1023-EZ Disapproval

• National Taxpayer Advocate disapproves of 1023-EZ Application• IRS defends 1023-EZ due to lack of staffing to review 1023

applications.• IRS intends to review 990s of entities filing 1023-EZs to ensure

entities are good charities.

© Gray Reed & McGraw, P.C.

1023/990 Recent Issues

• Incomplete 1023• Reincorporation in new state• 990 extension• 990N procedure

© Gray Reed & McGraw, P.C.

Type III Supporting Organizations Regulations

• Final Regulations issued December 2015 regarding the distribution requirement for non-functionally integrated Type III supporting organizations.

• Non-functionally integrated Type III supporting organizations are required to distribute the greater of (1) 85% of the supporting organization’s adjusted net income or (2) its “minimum asset amount.” • “Minimum asset amount” is defined as 3.5% of the excess of the aggregate

fair market value of the supporting organization’s non-exempt-use assets over the acquisition indebtedness with respect to such nonexempt use assets.

© Gray Reed & McGraw, P.C.

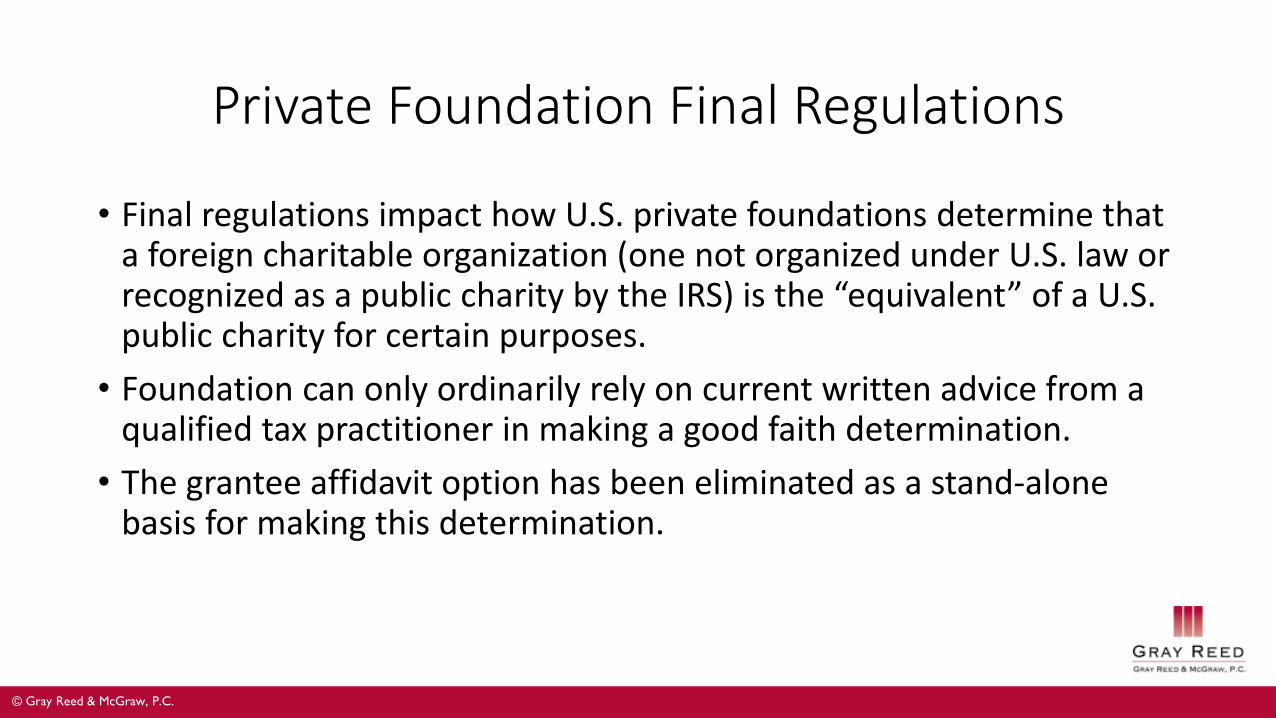

Private Foundation Final Regulations

• Final regulations impact how U.S. private foundations determine that a foreign charitable organization (one not organized under U.S. law or recognized as a public charity by the IRS) is the “equivalent” of a U.S. public charity for certain purposes.

• Foundation can only ordinarily rely on current written advice from a qualified tax practitioner in making a good faith determination.

• The grantee affidavit option has been eliminated as a stand-alone basis for making this determination.

© Gray Reed & McGraw, P.C.

Jeopardizing Investments

• Treasury Regulation 144267-11 (issued May 21, 2012) provided 9 new categories of “Program Related Investments” that avoid Sec. 4944 excise taxes.

• Notice 2015-62 Published guidance on application of rules in mission related investing. The notices explains Private Foundation investments are not jeopardizing investments “…if in making the investment, the foundation managers exercise ordinary business care and prudence…in providing for the long-term and short-term financial needs of the foundation to carry out its charitable purposes.”

© Gray Reed & McGraw, P.C.

Proposed Legislation

• S. 2750 – CHARITY Act• S. 2648 CREATE Act of 2016• H. Res. 668• H.R. 4706 – Interest for Others Act of 2016• H.R. 4311 – Protecting Charitable Contributions Act of 2015• H.R. 4281 – Charitable Giving Private Protection Act• Corporate Integration Proposal by Senator Hatch• CRS Report regarding changing tax treatment of endowments

© Gray Reed & McGraw, P.C.

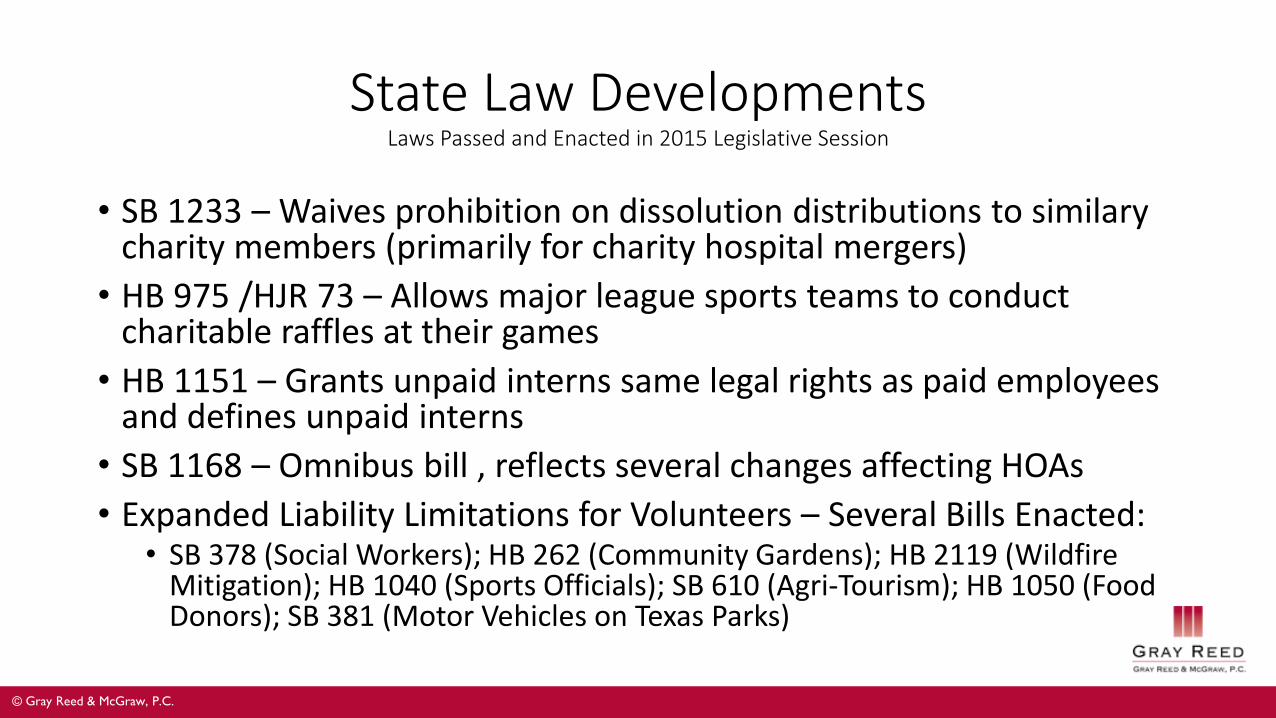

State Law DevelopmentsLaws Passed and Enacted in 2015 Legislative Session

• SB 1233 – Waives prohibition on dissolution distributions to similarycharity members (primarily for charity hospital mergers)

• HB 975 /HJR 73 – Allows major league sports teams to conduct charitable raffles at their games

• HB 1151 – Grants unpaid interns same legal rights as paid employees and defines unpaid interns

• SB 1168 – Omnibus bill , reflects several changes affecting HOAs• Expanded Liability Limitations for Volunteers – Several Bills Enacted:

• SB 378 (Social Workers); HB 262 (Community Gardens); HB 2119 (Wildfire Mitigation); HB 1040 (Sports Officials); SB 610 (Agri-Tourism); HB 1050 (Food Donors); SB 381 (Motor Vehicles on Texas Parks)