i.r.c. section 174 r&e expenditures 2014 final … presentation prototype regulations...i.r.c....

TRANSCRIPT

I.R.C. Section 174 – R&E Expenditures2014 Final Prototype Regulations

(T.D. 9680)

Hosted by Kim Hopkins, Director

Presented by Peter Mehta, Managing Director

Tax Credit Co.

October, 2015

2

Agenda

Introductions

An Overview of I.R.C. § 174

IRS Issues and Concerns re: Application of I.R.C. § 174 to Prototype Expenses

T.D. 9680: Final § 174 Regulations

Questions

3

Introductions

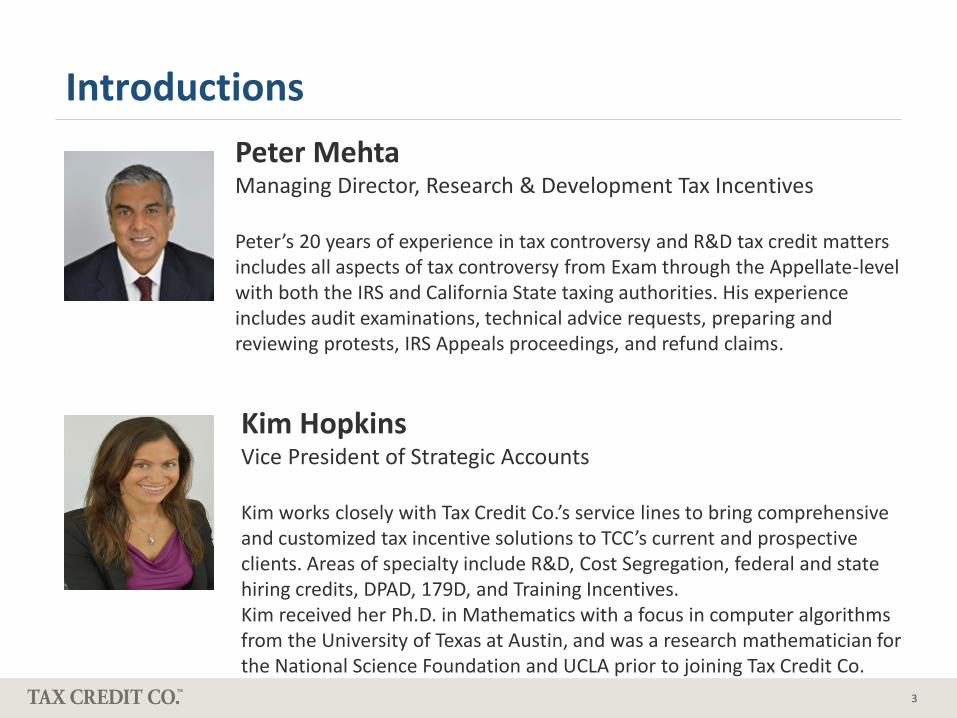

Peter MehtaManaging Director, Research & Development Tax Incentives

Peter’s 20 years of experience in tax controversy and R&D tax credit matters includes all aspects of tax controversy from Exam through the Appellate-level with both the IRS and California State taxing authorities. His experience includes audit examinations, technical advice requests, preparing and reviewing protests, IRS Appeals proceedings, and refund claims.

Kim HopkinsVice President of Strategic Accounts

Kim works closely with Tax Credit Co.’s service lines to bring comprehensive and customized tax incentive solutions to TCC’s current and prospective clients. Areas of specialty include R&D, Cost Segregation, federal and state hiring credits, DPAD, 179D, and Training Incentives. Kim received her Ph.D. in Mathematics with a focus in computer algorithms from the University of Texas at Austin, and was a research mathematician for the National Science Foundation and UCLA prior to joining Tax Credit Co.

4

About Tax Credit Co. (TCC)

$1+ Billion in tax credits secured

19+ Years in providing tax incentive solutions

100+ Specialists nationwide

‒ Ex Big 4 CPAs

‒ Tax Attorneys

‒ Industry Specialists

‒ Technology Executives

Audit Ready deliverables

Technology platform that leads the industry

We Live By 3 Commitments:

No tax credit left behind

Our clients love us

Innovative solutions to high-value problems

5

Poll Question #1

Have you worked with the Research & Development Tax Credit in the past?

A. Yes

B. No

I.R.C. § 174: Research and Experimental Expenditures

An Overview

7

I.R.C. § 174: Basic Rule

Section 174 provides alternative methods of accounting for research or experimental expenditures:

‒ Deduct in year paid or incurred

‒ Elect to defer and amortize over a period not less than 60 months beginning with the month the taxpayer first realizes benefits from those expenditures

‒ Expenses that are neither expensed nor deferred and amortized must be capitalized

8

I.R.C. § 174: Basic Rule

§ 174 statute does not define the term “research or experimental expenses”

Treas. Reg. § 1.174-2 defines research or experimental expenditures to mean “expenditures incurred in connection with the taxpayer’s trade or business which represent research and development costs in the experimental or laboratory sense.”

2 requirements to satisfy “experimental or laboratory sense” requirement:

‒ “The information available to the taxpayer does not establish the capability or method for developing or improving the product or the appropriate design of the product (i.e., an uncertainty exists);” and

‒ The activity is intended to discover information that would eliminate that uncertainty

9

I.R.C. § 174: Basic Rule

Definition of “product”

‒ Includes any pilot model, process, formula, invention technique, patent or similar property, and includes products to be used by the taxpayer in its trade or business as well as products to be held for

sale, lease, or license. Treas. Reg. § 1.174-2(a)(2).

Section 174 specifically excludes certain expenditures

‒ Quality control testing, efficiency surveys, management studies, consumer surveys, advertising, acquisition of another’s patent, model, production, or process, research in connection with literary, historical projects, etc.

10

I.R.C. § 174: Basic Rule

Treas. Reg. § 1.174-2(a)(2): Pilot models / prototypes

‒ The current § 174 regulations define research or experimental expenditures to include costs incident to the development or improvement of a pilot model (i.e., a prototype).

Depreciable Property Rule

‒ Section 174(c) and Treas. Reg. § 1.174-2(b)(1), and -2(b)(4)

‒ Section 174(c) provides that § 174 does not apply to an expenditure for:

• Acquisition or improvement of land

• Or for the acquisition or improvement of property that is to be used in connection with the research or experimentation and is of a character subject to depreciation

11

Poll Question #2

Can depreciation be claimed as QRE for the Research & Development Tax Credit?

A. Never

B. Under very rare circumstances

C. In many cases

D. Always

I.R.C. 174: Sources of Controversy Between the IRS and Taxpayers

13

Common IRS Objections

IRS interpretation of § 174 and the regulations thereunder as they apply to prototypes has been the source of significant debate between the Service and taxpayers

‒ Not only in § 174 context but also § 41 R&D credits

‒ This is because qualification of an expense under § 174 is a prerequisite to be treated as a qualified research expense (“QRE”) under § 41.

14

Common IRS Objections

IRS often uses depreciable property rule to disallow prototype / pilot model costs (i.e., “if the prototype is of a character subject to depreciation it cannot be deducted as a § 174 expense”)

Supplies must be used and consumed:

‒ IRS often maintains that in order to qualify for the credit, supplies must not only be used but consumed during the research activity.

‒ “To be considered a qualifying supply, the item must be … totally used or consumed in the qualified research activity….” FSA 5488, 12/17/98

15

Common IRS Objections

Supplies cannot include property that is depreciable in the hands of any taxpayer

─ Typical fact patterns

• Taxpayer ultimately sells a prototype to a customer (and customer could depreciate the property)

• Taxpayer ultimately uses the prototype on subsequent projects, or as a demonstration model.

• Property exists for more than one year, even though it was used for one research project that spanned multiple years.

16

Poll Question #3

Can prototype costs that have been treated as COGS be claimed as QRE under § 41?

A. Yes

B. No

T.D. 9680: The Final Prototype Regulations

18

T.D. 9680

T.D. 9680 addresses many of the concerns raised by the IRS

Effective date:

‒ Applicable to tax years ending on or after July 21,2014

‒ Taxpayer may apply regulations for all taxable years for which assessment SOL has not run

Highlights of T.D. 9680

‒ Subsequent Events: Confirms that § 174 eligibility cannot be reversed by a subsequent event; i.e., the sale or other use of the research or property resulting from the research is not relevant to a determination of eligibility under § 174

19

T.D. 9680

‒ Pilot Model Definition: Defines the term “pilot model” as any representation or model of a product that is produced to evaluate and resolve uncertainty concerning the product during the development or improvement of the product

‒ Scope of Pilot Model: Confirms that a pilot plant may include a fully-functional representation or model of the product or a component of the product (to the extent that shrinking-back rule applies)

‒ Shrinking-back Rule: Provides a rule similar to Treas. Reg. § 1.41-4(b)(2) to address situations in which the requirements of § 174 are met with respect to only a component part and not met with respect to the overall product itself

‒ The final regulations include numerous examples applying the above principles

20

Subsequent Events

Per the new final regulations, Section 1.174-2(a)(1) revised to include the following language:

‒ “…The ultimate success, failure, sale or use of the product is not relevant to a determination of eligibility under § 174. Costs may be eligible under section 174 if paid or incurred after production begins but before uncertainty concerning the development or improvement of the product is eliminated.”

21

Subsequent Events

‒ Example 7. Disposition of a pilot model

• Facts:

o X is an aircraft manufacturer.

o X is researching and developing a new, experimental aircraft that can take off and land vertically.

o X produces a aircraft at a cost of $5,000,000 to test the appropriate design of the aircraft.

o The aircraft works.

o In a later year, X sells the aircraft.

• Analysis:

o X may treat the entire $5,000,000 as R&E

o The purpose of building the aircraft was to evaluate and resolve uncertainty regarding the appropriate design of the aircraft.

o Example concludes that it would not matter if X sold the pilot model or incorporated it in its own business as a demonstration model.

22

Subsequent Events

T.G. Missouri Company v. Commissioner, 133 T.C. 278 (2009)

‒ New rules reference T.G. Missouri case and outlines principles consistent with the case

‒ § 41 research credit case in which the Tax Court held that automotive production molds that the taxpayer purchased from third parties and later sold to its customers (after performing additional engineering and design work on them) are supplies for purposes of the § 41 tax credit.

‒ Court rejected the IRS argument that because the production molds were of a character that could be depreciated by a taxpayer, even if a taxpayer did not depreciate them, they were not eligible § 174 expenses.

‒ The Tax Court held that the § 174(c) exclusion applies only to property that is depreciable in the hands of the taxpayer.

‒ The Tax Court found it irrelevant that the taxpayer had sold the prototypes.

23

Pilot Models/Prototypes

Section 1.174-2(a)(4) defines the term pilot model:

‒ As any representation or model of a product that is produced to evaluate and resolve uncertainty concerning the product during the development or improvement of the product.

‒ Includes a fully-functional representation or model of the product

• Example 7. The entire aircraft was treated as the pilot model / prototype.

• The taxpayer had to build the entire aircraft to evaluate and test it for appropriateness of design.

24

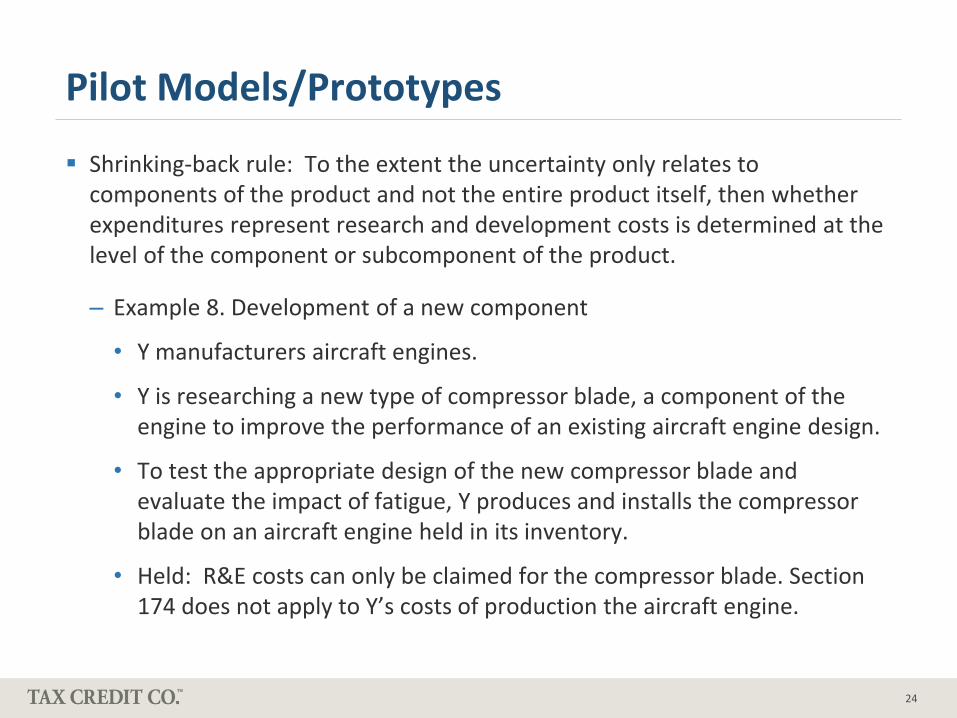

Pilot Models/Prototypes

Shrinking-back rule: To the extent the uncertainty only relates to components of the product and not the entire product itself, then whether expenditures represent research and development costs is determined at the level of the component or subcomponent of the product.

‒ Example 8. Development of a new component

• Y manufacturers aircraft engines.

• Y is researching a new type of compressor blade, a component of the engine to improve the performance of an existing aircraft engine design.

• To test the appropriate design of the new compressor blade and evaluate the impact of fatigue, Y produces and installs the compressor blade on an aircraft engine held in its inventory.

• Held: R&E costs can only be claimed for the compressor blade. Section 174 does not apply to Y’s costs of production the aircraft engine.

25

Scope of the pilot model/prototype rule

Issue: What is the pilot model when a new component is integrated into a larger product?

Trinity Industries, Inc. v. United States, 691 F. Supp 2d 698

‒ Facts:

• Research credit case under I.R.C. section 41.

• Taxpayer was a ship builder. Taxpayer claimed qualified research expenses (“QREs”) for 6 ships.

• Each ship was treated as a separate business component or project.

• The taxpayer argued that the design and construction of each ship was sufficiently experimental that the whole project constitutes QREs.

• Taxpayer did not attempt to apply the shrinking-back rule. Under this theory, to treat any expenses as QREs, the taxpayer had to show that 80 percent or more of a prototype vessel was part of a process of experimentation. Thus, either all the expenses for a particular prototype would qualify or none would.

26

Scope of the pilot model/prototype rule

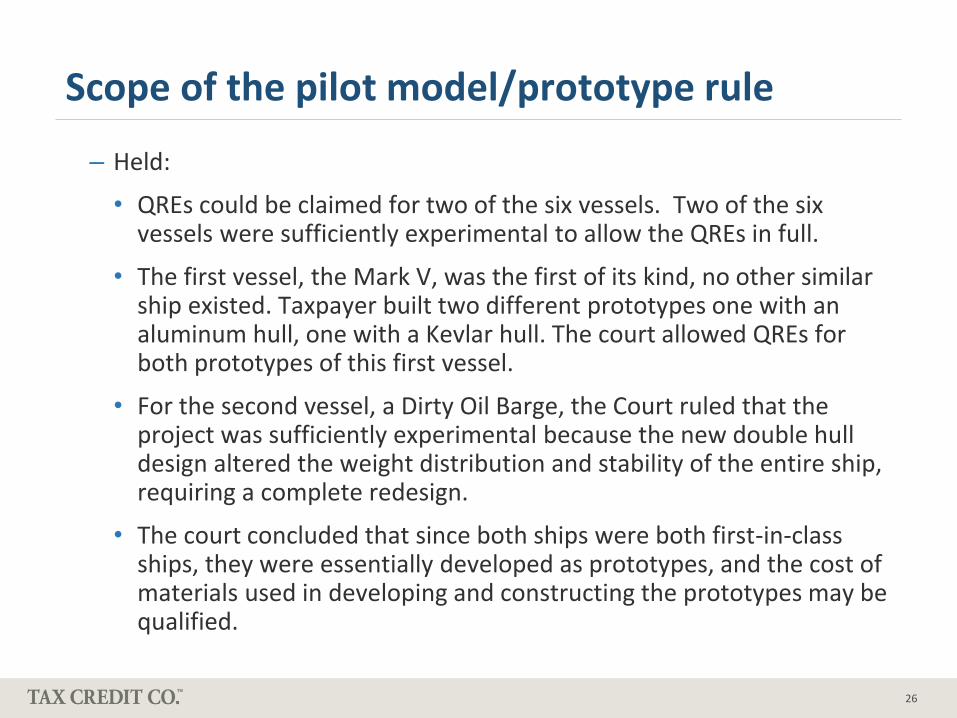

‒ Held:

• QREs could be claimed for two of the six vessels. Two of the six vessels were sufficiently experimental to allow the QREs in full.

• The first vessel, the Mark V, was the first of its kind, no other similar ship existed. Taxpayer built two different prototypes one with an aluminum hull, one with a Kevlar hull. The court allowed QREs for both prototypes of this first vessel.

• For the second vessel, a Dirty Oil Barge, the Court ruled that the project was sufficiently experimental because the new double hull design altered the weight distribution and stability of the entire ship, requiring a complete redesign.

• The court concluded that since both ships were both first-in-class ships, they were essentially developed as prototypes, and the cost of materials used in developing and constructing the prototypes may be qualified.

27

Scope of the pilot model/prototype rule

‒ Observations:

• The Court’s analysis is consistent with the new final regulations regarding the definition of a pilot model/prototype.

• It is also consistent with the “subsequent events” principle. The Court found that the fact that the prototype was successful and ultimately sold was irrelevant.

• Finally, the Court held that integrating existing components could result in significant technical challenges and experimentation to allow the entire product to be treated as a prototype:

o “…the simple fact that a new vessel incorporates existing systems does not resolve the QRE issue against Trinity. Determining the degree of QRE involved requires an examination of the overall scope of the effort required to specify the components and integrate them into the overall design of the ship.”

• Observation: Compare the Court’s decision with Example 8 of the final prototype regulations (compressor blade integrated with engine, but only costs associated with blade allowable as QREs).

28

Scope of the pilot model/prototype rule

Factors to consider when determining whether the entire product should be treated as a prototype or whether only certain components should be treated as the prototype:

‒ Degree of integration risk

‒ The number of new components vs. existing component designs

‒ Whether the product’s functional and performance requirements could only be tested and evaluated once the product was built

‒ Root cause of any failures that occurred during testing (component level vs. product level)

29

Open Issues

What is the pilot model when the “prototype” consists of new component designs integrated with existing designs?

Will the IRS use the shrinking-back rule to disallow prototypes where the prototype is the entire product?

How can a taxpayer substantiate its prototype costs

When should project activities related to the building and development of the prototype be considered post-production vs. development activities?

30

Poll Question #4

What action step do you plan to take as a result of this webinar?

A. Research further

B. Talk to my clients about this

C. I'm not sure

D. Not applicable

31

Questions and Contact Information

Kim Hopkins| VP, Strategic Accounts | Tax Credit Co.

6255 Sunset Blvd., Suite 2200 | Los Angeles, CA 90028

(323) 927-0767 phone | (323) 927-0756 fax

[email protected] | www.taxcreditco.com