ipcc paper 6 chapter 6 (vol 1) ca. ranajit kumar pramanik · learning objectives verification of...

TRANSCRIPT

IPCC Paper 6 Chapter 6 (vol‐1)

CA. Ranajit Kumar Pramanik

Learning Objectives Verification Of Assets: An Overview Capital Expenditure Verification Of Fixed Assets Audit of Fixed Assets Fixed Assets And Caro Requirements Verification Of Specific Fixed Assets. Verification Of Investments Verification of Current Assets‐ An overview Current investments Verification of inventories Verification of Book Debts

Learning Objectives Verification of – Bills Receivables Verification of –Advances Verification of – Loans Cash and Cash Equivalents ‐ Cash in hand

‐ Bank Balances Verification of liabilities – An overview Verification of loans and borrowing Verification of trade creditors and other currentliabilities Verification of trade creditors Verification of Bills payables Verification of Other current liabilities

Verification of provisions Verification of contingent liabilities

Verification of Assets

‐ Scope has been limited to inspection of assets‐ It involves the following pre‐requisities and attributes:

•Assets were in existence on the date of the balance sheet;•Assets had been acquired for the purpose of the businessand under a proper authority;•The right of ownership of the assets vested in orbelonged to the undertaking;•They were free from any lien or charge not disclosed inthe balance sheet;•They had been correctly valued having regard to theirphysical condition•Their values are correctly disclosed in the balance sheet.

1. Responsibility of the management2. The auditors function is limited only to an appraisal of the

evidence, their inspection and reporting on mattersaffecting their valuation, existence and title, observed inthe course of such an examination.

3. Assets are valued either on a ‘going concern’ or ‘breakupvalue’ basis.

The capital expenditure is one, the benefit of which is notexhausted in the year in which these are incurred but extends tonumber of years up to which its existence and economic life ofthe asset in which is incurred for the under noted purposes:

Acquiring fixed assets i.e assets of a permanent or a semipermanent nature which are held not for re‐sell but for usewith a view to earning profit.

Making additions to the existing fixed assets. Increasing earning capacity of the business. Reducing the cost of production. Acquiring the benefit of enduring nature of a valuable right.

‐The different forms that capital expenditure takes are : (i)Land.(ii) Building.(iii) Plant and Machinery(iv) Electric Installations(v) Premium paid for the lease of a building;(vi) Development expenditure on land; and (vii) Goodwill etc.

Expenses which are essentially of a revenue nature, if incurredfor creating as assets or adding its value or achieving higherproductivity, are also regarded as expenditure of a capitalnature.

Examples: ‐(i) Materials and wages – Capital expenditure when expendedon the construction of building or erection of machinery.(ii) Legal expenses – Capital expenditure when incurred inconnection with the purchase of land or building.(iii) Freight – Capital Expenditure when incurred in respect ofpurchase of plant and machinery.‐Whenever therefore, a part of the expenditure, ostensively of arevenue nature is capitalized it is the duty of the auditor not only toexamine the precise particulars of the expenditure but also theconsideration on which it has been capitalized.‐As per revised schedule – IV company’s act.1956 effective fromfinancial year 2011‐12, the assets classified as follows:‐

ASSETS

NON CURRENT ASSETS CURRENT ASSETS

FIXED ASSETS

NON CURRENT INVESTMENTS

DEFERRED TAX (ASSETS- NET)

LT LOANS & ADVANCES

OTHER NON CURRENT ASSETS

CURRENT INVESTMENTS

INVENTORIES

TRADE RECEIVABLES

CASH & CASH EQUIPMENTS

ST LOANS AND ADVANCES

OTHER CURRENT ASSETS

TANGIBLE ASSETS

INTANGIBLE ASSETS

CAPITAL WIP

INTANGIBLE ASSETS

Fixed Assets

FIXED ASSETS are categorised as tangible assets. The tangible assets are classified into :

• Land • Building• Plant & Machinery• Furniture & Fixture• Vehicles• Office Equipment • Others (specifying nature)

• It is the duty of the management to ensure that the fixedassets of the company are in existence

• The order issued under Section 227(4A) of the act requires theauditor to report on the physical verification of the fixed assetsby the management, and the treatment of the discrepancies ifany.

‐Verification by the auditor with reference to the documentaryevidence and by evaluation of internal control.

‐The appropriateness of the accounting policies, including policiesfor determining which costs are capitalized, whether on cost orvaluation model is followed and depreciation appropriatelycalculated is to be considered

‐Verification records to ensure that the assets under construction orpending self constructed fixed assets and capital work in progressshould be verified with reference to the supporting documents suchas construction bills, work order and independent confirmation ofthe work performed from other parties.

• Retirement of fixed assets• Impairment of assets• Ownership of assets• The auditor should test check the book records of fixed assets with

the physically verification reports certified by the management asphysical verification of fixed assets is primarily a responsibility ofthe management.

• The auditor should see that the fixed assets have been valued anddisclosed as per the requirements of law and generally acceptedaccounting principles

• The auditor should test check the calculations of depreciation andthe total deprecation arrived at should be compared with that ofthe preceding years to identify reasons for variations.

• Revaluation of fixed assets

• Clause 4(i) (a) of, CARO, 2003 requires the auditor to commentwhether the company is maintaining proper records showingfull particulars, including quantitative details and situations offixed assets.

• Clause 4(i) (b) of CARO, 2003 requires the auditor to commentwhether the fixed assets of the company have been

physically verified by the management at reasonableintervals. The clause further requires the audit to commentwhether any material discrepancies were noticed on suchverification and, if so, whether these discrepancies have beenproperly dealt with in the book of account.

• Clause 4(i) (c) of CARO, 2003 requires the auditor to comment, incase where a substantial part of the fixed assets has been

disposed off during the year, whether such disposal hasaffected the going concern status of the company.

While the valuation and verification of fixed assets as well asthat of auditors duty therein have been outlined/disclosed above,we would now discuss the aspect of verification of some of thespecific assets:

-

i. Land & Buildingi. Building Subject to depreciation, Land is not.ii. Inspection of the original title deed

ii. Lease Hold Propertyi. Lease deed examination for value and durationii. Capitalization of lease money

iii. Goodwilli. Intangible asset, value depends on earning capacity of

businessii. Never appreciated in books of accounts

iv. Plant & Machineriesv. Furniture, Fittings and Fixturesvi. Motor Lorries, Van etc.vii. Non‐ Current Investment

- Assets held by an entity for accretion ofwealth by way of interest, royalties,dividends and rentals for capitalappreciation or for other benefits to theinvesting entity. An investment may berepresented by Govt. securities, shares,Debentures etc.

Procedure for verification of investments

Obtain schedule of securities and shares in hand at the beginning of the audit period containing description, date of purchase, face value, book value, market value, rate of interest, date of payment of interest, date around which dividend is normally declared etc.

Add to the above list, securities and share purchased and sold during the year, giving the same description in regard to both.

Balance this schedule and compare the closing balance with the control account in the general ledger.

The auditor should ascertain whether the investments made by entity are within the authority.

Procedure for verification of investments The auditor himself should also be satisfied that the transactions for the purchase/sale of investments are supported by due authority and documentation.

The acquisition / disposal of investments should be verified with reference to the broker’s contract note, bill of cost etc, special attention should be paid to the investments purchased or sold, cum‐ dividend, ex‐dividend, cum‐interest/ex‐interest etc. The auditor should also check the price paid/receive with reference to stock‐exchange quotations.

The investments should be physically verified at the last date of the accounting year. In case investments are not

held by the entity in its own custody‐ then certificate should be obtained from the relevant authority to the

effect of holding of investments.

Procedure for verification of investments The auditor should also examine the relevant provisions of

Section 227(1A) and see that a company not doing an investment or banking company whether so much of the assets of the company as represented by the shares and debentures have been sold at a price less than that at which they were purchased by the company.

The auditor should satisfy that the investment have been valued and disclosed in the financial statement in accordance with the recognized accounting policies and relevant statutory requirements. Reference to principles laid down in AS‐13 on “Accounting of Investments” relating to valuation of investments will be necessary.

The auditor may also see that any money raised through shareissue to the extent remains unutilized has been shown underthe head “Investment” and the manner in which the same hasbeen invested should also be indicated.

Current Assets

Current Assets ‐ Inclusions

The current assets, are classified as per the Revised Schedule‐VI of the Companies Act, 1956 (effective from the financial year 2011‐12) broadly as follows:‐

Current investments Inventories i.e. stock in trade Trade receivable i.e. Sundry Debtors Cash and Bank equivalents ST Loans and advances Current Assets

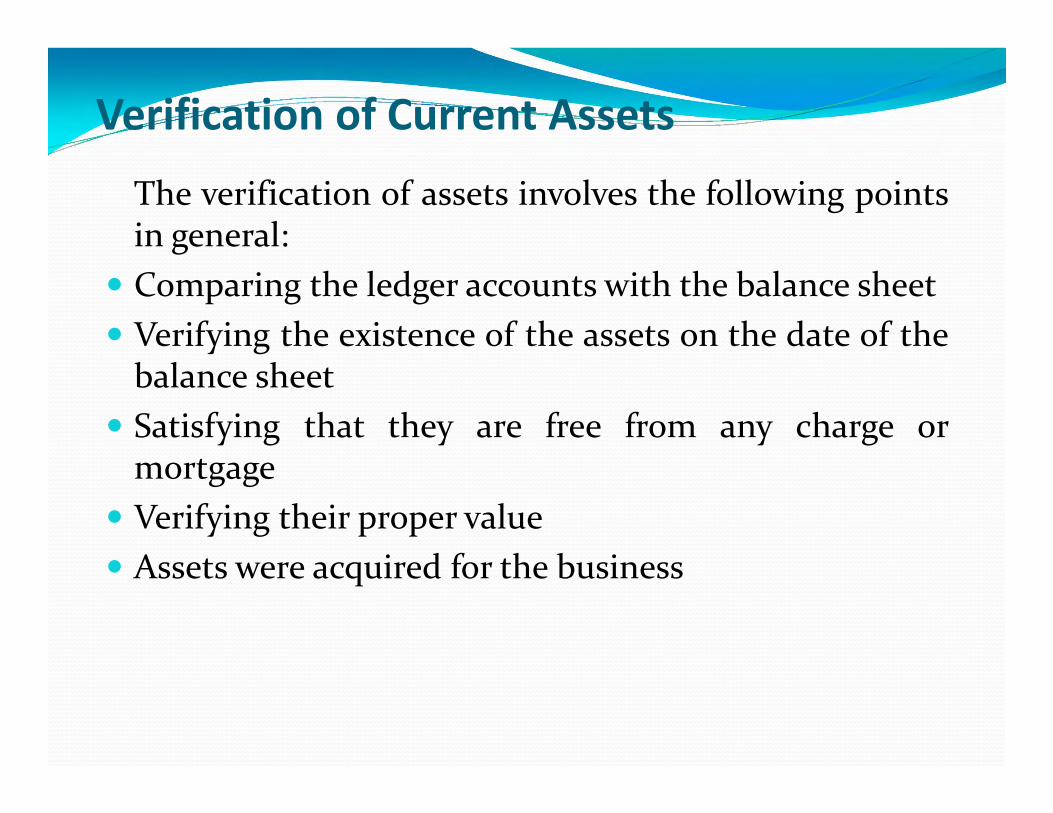

The verification of assets involves the following pointsin general:

Comparing the ledger accounts with the balance sheet Verifying the existence of the assets on the date of thebalance sheet

Satisfying that they are free from any charge ormortgage

Verifying their proper value Assets were acquired for the business

Verification of Current Assets

Verification of some specific current assets has been outlined hereunder:

(1) Current Investments: If the investments are held by acompany as current assets to be sold whenever foundnecessary, the basis of their valuation should be ‘costprice or market price whichever is the lower’‐ If the total market value of the investment is less thanthe total cost price, the whole of the differences may bedebited to depreciation account and credited toinvestment fluctuation Account .‐ The auditor should see that different types ofinvestments are classified in the balance sheetaccording to the schedule‐VI, part‐I of the CompaniesAct‐ Current and non‐current investments are to be

declared separately under current assets and noncurrent assets respectively.

Verification of Specific Current Assets

(ii) Verification of Inventories‐Stock in trade: Inventories shall be classified as :‐Raw materials Work in progressFinished goodsStock in trade (in respect of goods acquired for trading)Stores and SparsLoose toolsOthers (specify nature)

Verification of Specific Current Assets

‐ Verification of inventories may be carried out by employing thefollowing procedures:a) Examination of records in the form of stores/ stock ledgersshowing in respect of major items the receipts, issues and balancesb) Attendance at stock taking, the extent of auditor’s attendance atstock taking would depend upon his assessment of the efficacy ofrelevant internal control proceduresc) Obtaining confirmation from the third parties;d) Examination of valuation and disclosure ; ande) analytical procedures which may include substantive procedure i.ecomparison of significant ratios relating to inventories with the industrynorms if available.

Verification of Specific Current Assets

CARO,2003 & Inventory Requirements:‐a) Clause 4 (ii) (a) requires the auditor to commentwhether the management has conducted physicalverification of inventory at reasonable intervals.b) Clause 4 (ii) (b) requires the auditor to commenton the reasonableness and adequacy of the inventoryverification procedure followed by the management ofthe company.c) Clause 4 (iii) (c) requires the auditor to commentwhether the company is maintaining proper records ofinventory.

Verification of Specific Current Assets

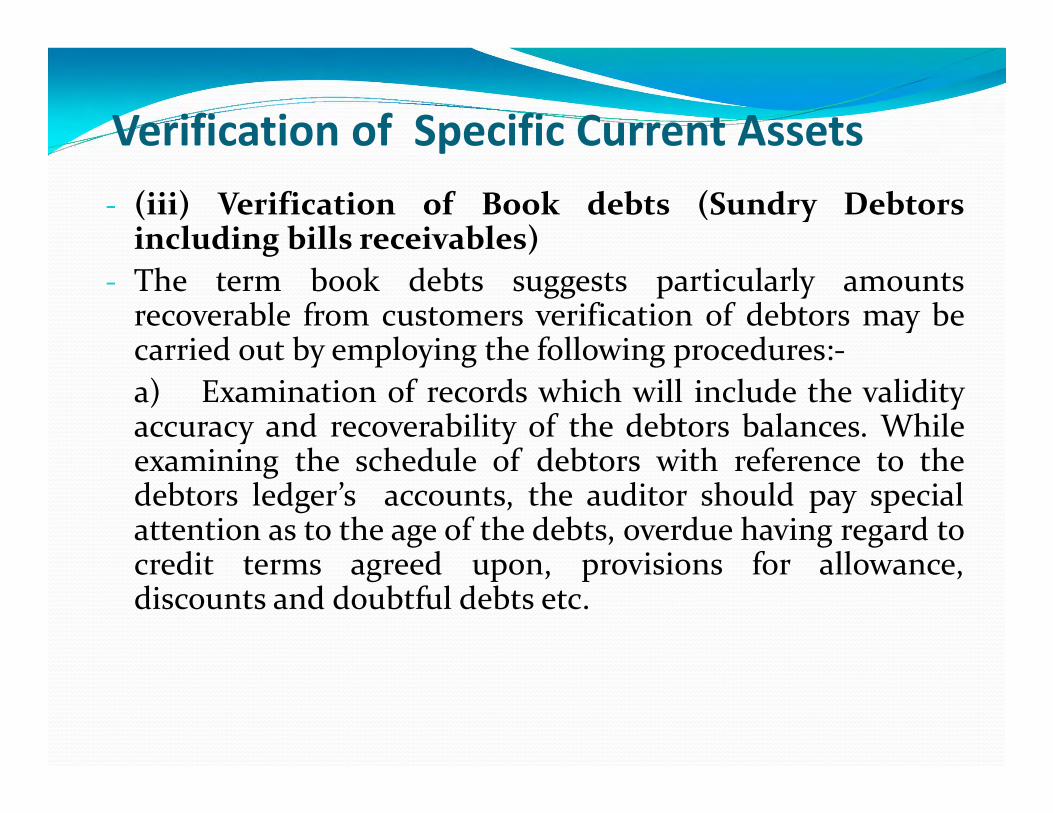

‐ (iii) Verification of Book debts (Sundry Debtorsincluding bills receivables)

‐ The term book debts suggests particularly amountsrecoverable from customers verification of debtors may becarried out by employing the following procedures:‐a) Examination of records which will include the validityaccuracy and recoverability of the debtors balances. Whileexamining the schedule of debtors with reference to thedebtors ledger’s accounts, the auditor should pay specialattention as to the age of the debts, overdue having regard tocredit terms agreed upon, provisions for allowance,discounts and doubtful debts etc.

Verification of Specific Current Assets

b) Direct confirmation procedure (also known ascircularization procedure). The verification of balances bydirect communication with debtors is theoretically the bestmethod of ascertaining whether the balances are genuine,accurately stated and undisputed.

c)Analytical Review procedures in respect of significantratios relating to the debtors, loans and advances,comparison of the relationship between current yeardebtor balances with current years sale and budgetedfigure

‐ According to Revised schedule‐VI to the Companies Act,1956, debts outstanding for more than six months have tobe shown separately.

Verification of Specific Current Assets

‐ Further all the sundry debtors; loans/advances includingthese advanced to subsidiary companies are broadlyclassified as under

Debts considered good in respect of which the company isfully secured.

Debts considered good for which the company holds nosecurity other than the debtors personal security.

Debts considered doubtful or bad

Verification of Specific Current Assets

(iv) Bills Receivable: Debts, when covered by acceptance ofbill of exchange for an usance period, shall be known asBills receivable. The verification of bills receivable may beas under:‐

‐ If possible, the auditor should attend on the last day of theaccounting period to inspect the bills in hand and agreetheir total with the balance in the bills receivable account.

‐ If some bills were discounted after the date of the balancesheet, the collection of their proceeds should be verified ;

‐ If any bills were dishonoured after the date of the balancesheet, the auditor should ascertain what portion, if any, ofthe amount will not be recovered and ensure that provisionfor the same has been made.

‐ If some of the bills are with the bankers for collection, theauditor should obtain a certificate from them.

Verification of Specific Current Assets

(v) Advances: These include amounts recoverable either incash or in kind for value to be received e.g. rates, taxes andinsurance.

‐ The auditor should obtain a list of all advances andcompare them with balances in the ledger. He shouldascertain that advances were made under proper authorityand were being recovered regularly by agreed terms.

‐ In the case of old balances the auditor should ensure thatprovision has been made in respect of the irrecoverableadvances. Particulars mentioned above in respect of bookdebts must also be given for advances.

Verification of Specific Current Assets

(vi) Loans: In general the procedure out lined in regard todebtors is also applicable in the case of loans and advances.

‐ Apart from verification of the balances of loans, the auditorshould inspect the loan agreements and acknowledgementof parties in respect of outstanding loans.

‐ A loan or an advance, if material can be granted only ifauthorised by the Memorandum and Articles ofAssociation in the case of company. In addition, he shouldconfirm that the loans advanced were within thecompetence of persons who had advanced the same.

‐ If any security is deposited against due repayment of theloan, the same should be inspected. The loans should beclassified for purpose of balance sheet in the same way asother debts.

Verification of Specific Current Assets

‐ In order to ascertain that loans and advances are properlysecured auditors should make inquiries to ascertain thatprima‐facie;

The company holds a legally enforceable security andThe value of the security fully covers the amount of the loan oradvance and is reasonably ascertained

Verification of Specific Current Assets ‐Loans

(vii) Cash and cash equivalents: classification of cash and cashequivalents into:

Balances with banks Cheques and drafts or hand Cash on handOthers (specifying nature)

Verification of Specific Current Assets

‐ The auditor should satisfy himself that cash and bankbalances have been valued and disclosed in the financialstatement in accordance with recognised accountingpolicies and practices and relevant statutory requirements.In this regard, the auditor should examine that followingitems are not included in cash and bank balances Temporary advances Stale or dishonored of cheques, postage and revenue stamps, ifmaterial in amounts may be shown separately instead of beingincluded under cash and bank balances.

Cash & Bank Balances

a) Cash in hand: In a Balance Sheet all the undermentionedcash balance are included under the above head; cash balancein hand; petty cash balance in hand, balances of stamps inhand; cash in transit ; cash at branches; and, cash withagents;

‐ The first three items are verified by actual count. The cash intransit and that with branches and agents is verified fromdocumentary evidence available and advice in respect of theirsubsequent remittance in whole or partIf the auditor finds any slip, chit or 1.0 U.S in respect oftemporary advances paid to the employees included as part ofthe cash balance he should have them initiated by aresponsible official and debited to appropriate accounts.

Cash & Bank Balances

b) Bank Balances: These should be verified by reference to bankreconciliation statement and the balance certificate receivedfrom banks. The auditor should examine the bankpassbook/bank statement and compare it with the balance asshown by the bank column of the cash book.

‐ If a Bank reconciliation statement includes a large number ofuncleared items as on the date of the balance sheet, the auditorshould verify that the items were subsequently collected. Onother hand where a cheque issued for more than six monthsbefore the close of the year, is shown in the bank reconciliationstatement the entry has to be reversed.

‐ If audit is undertaken long after the close of the year, theauditor should reconcile the bank balances right upto the dateon which he undertakes the audit.

Cash & Bank Balances

Verification of Liabilities

Overview

Liabilities are the financial obligations of an enterpriseother than the owner’s fund. Liabilities include loans andborrowings, trade creditors and other current liabilitiesdeferred payment credits, instalments payable under thehigher purchase agreement and provisions.

‐ An important feature of liabilities which has a significanteffect on the related audit procedure is that these arerepresented only by documentary evidence whichoriginates mostly from third parties in their dealings withthe entity.

‐ The auditor should besides verifying the liabilities asshown in the Balance Sheet should get a certificate fromthe management that all the liabilities for purchases as wellas for expenses or on any other account have beenincluded in the books of accounts and that the contingentliabilities have been shown by way of a foot note to thebalance sheet or have been provided for.

1. Loans and Borrowings: Verification of liabilitiesmay be carried out by employing the followingprocedures:For Audit of loans and borrowings, certain steps, vig.Examination of records, direct confirmation procedure,examination of disclosure; analytical review proceduresand obtaining management representations areinvolved.

Verification of Liabilities

2. Trade creditors and other current liabilities:a) Trade creditors: The auditor should check the

adequacy of cut‐off procedures adopted by the entity inrelation to transactions affecting the creditors account.The auditor should check that the total of the creditor’sbalance agrees with the related control accounts, if any,the difference, if any , should be examined.

‐ The auditor should examine the correspondence andother relevant documentary evidence to satisfy himselfabout the validity , accuracy and completeness ofcreditors/acceptances.

Verification of Liabilities

b) Bills payable: The auditor should verify this item fromthe bills payable book and the bills payable accounts.

‐ The bills payable already paid should be checked from thecash book and examine the returned bills payable.

‐ To see the genuineness of the bills payable in hand on thedate of the balance sheet, the auditor should check thecash book of the succeeding year as to whether anypayment has been made in respect of such bills.

Verification of Liabilities

c) Other current liabilities: While examining schedule of creditors and other schedules such as those relating to advance payments, unclaimed dividends and other liabilities, the auditor should pay special attention to the following aspectsLong outstanding items;Unadjusted claims for short suppliers, poor quality,discount, commission, etc.

Liabilities not corelated/adjusted against related advancesAuthorisation and correctness of transfers from oneaccount to another.

‐ Based on his examination as aforesaid, the auditor shoulddetermine whether any adjustment in accounts arerequired.

Verification of Liabilities

(d) Provisions: The term provisions mean amount retained byway of providing for depreciation or diminution in value ofassets or retained by way of providing for any known liability,the amount of which cannot be determined with substantialaccuracy and provision also include product warranties,service contracts and guarantees, taxes and levies, gratuity,proposed dividend etc.

‐ The audit of provisions primarily involves examining thereasonableness and adequacy of the amounts provided for.The auditor should also examine that the provisions madeare not in excess of what is reasonably required as also as perstatutory provisions etc.

Verification of Liabilities

(e) Contingent Liabilities: The term contingent liabilities refers topast transactions or other events or conditions that may arise inconsequence of one or more future events which are presentlydeemed possible but not probable. Contingent liabilities may or maynot crystallise into actual liabilities. If they do become actualliabilities, they give rise to loss or expenses. The uncertainty as towhether there will be any legal allegation differentiates a contingentliability from a liability that has crystalised.

Verification of Liabilities

‐ The following general procedures may be useful inverifying contingent liabilities

(i) Review of minutes of the meetings of Board of Directors,Committee of Board of directors

(ii) Review of contacts agreements and arrangements(iii) Reviews of pending legal case correspondence relating to

taxes(iv) Review of terms and conditions of grants and subsidies

availed under various scheme.(v) Review of records relating to contingent liabilities(vi) Enquiry of and discussions with, the management and

senior officials of the entity(vii) Representation from the management

Verification of Liabilities

‐ (f) Disclosure: The auditor should satisfy himself that the liabilitieshave been disclosed properly in the financial statements where therelevant statute lays down any disclosure requirements in this behalf, theauditor should examine whether the same have been complied with .

‐‐ The auditor should examine that the following have been disclosed in

respect of contingent liabilities :(i) The nature of each contingent liability(ii) The uncertainties which may affect the future outcome(iii) An estimate of the financial effect or a statement that such estimate

cannot be made.

Verification of Liabilities