iom_meeting_tanzania_day_1_v02

DESCRIPTION

http://cddep.org/sites/cddep.org/files/iom_meeting_tanzania_day_1_v02.pdfTRANSCRIPT

Tanzania: AMFm Evaluation and Future Direction

September 2012

1

2

Overall successes and challenges of the AMFm in Tanzania

Successes

• Significant positive response from private sector

• Achieved significant gains on dimensions of availability,

affordability, and market share, particularly in private

for-profit outlets

• All participants are eager to see the program continue

Challenges

• Delay between approval of the program and first orders

actually arriving in country meant the full-scale program

was short, not enough time to evaluate impact

• Lack of transparency

• First Line Buyers have expressed frustration at

lack of transparency in order approval process

• Little information about what comes next

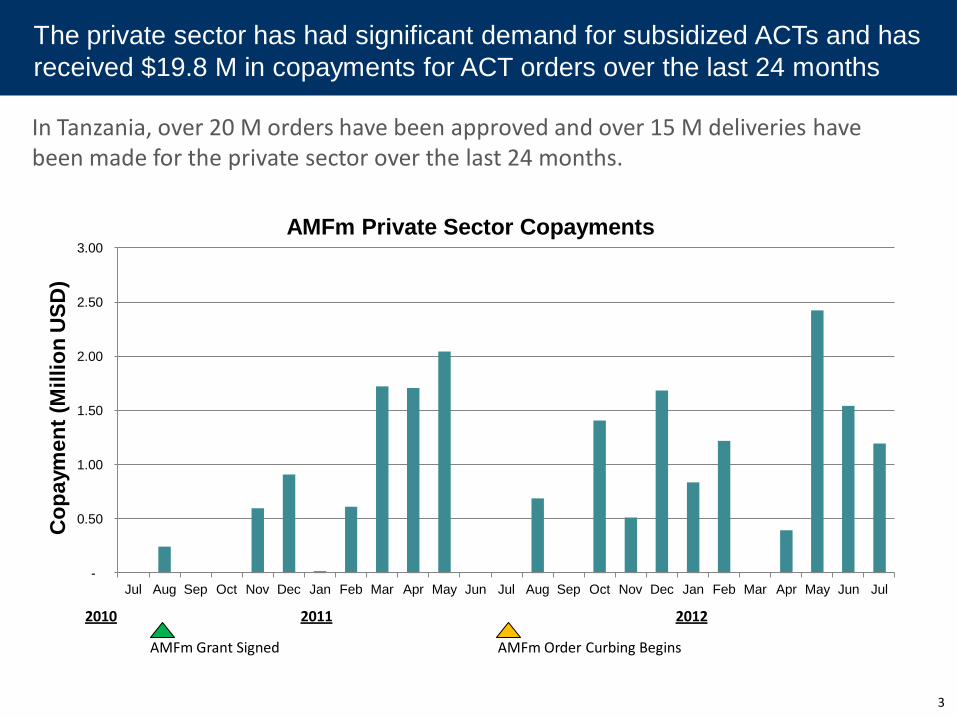

In Tanzania, over 20 M orders have been approved and over 15 M deliveries have been made for the private sector over the last 24 months.

The private sector has had significant demand for subsidized ACTs and has

received $19.8 M in copayments for ACT orders over the last 24 months

AMFm Order Curbing Begins

2010 2012

AMFm Grant Signed

2011

3

-

0.50

1.00

1.50

2.00

2.50

3.00

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

Co

pa

ym

en

t (M

illi

on

US

D)

AMFm Private Sector Copayments

NOT FOR CIRCULATION

The public sector in Tanzania has also benefitted from the AMFm, with an

additional 10 M orders approved, bringing total AMFm orders to 30M

0% 0%0%0%0%

0%

0%0%

Total

30.4

67%

33%

Jul-

12

100%

Jun-

12

1.9

100%

May-

12

4.8

55%

45%

Apr-

12

1.5

29%

71%

Mar-

12

1.6

100%

Feb-

12

1.4

0%

100%

Jan-

12

0.9

100%

Dec-

11

1.6

100%

Nov-

11

0.6

100%

Oct-

11

1.4

0%

100%

Sep-

11

0.0

Aug-

11

0.7

0%

87%

13%

Jul-

11

0.0

Jun-

11

0.0

May-

11

1.9

100%

Apr-

11

6.3

0%

22%

78%

Total

1.4

Feb-

11

0.9

100%

Jan-

11

0.1

100%

Dec-

10

0.9

Mar-

11

Nov-

10

0.8

100%

Oct-

10

0.0

Sep-

10

0.0

Aug-

10

0.2

100% 100%

Private not-for-profit

Private for-profit

Public

Orders approved by sector (M)

Note: Only includes orders uploaded to Global Fund website; Data cleaned to remove repeat approved orders and negative deliveries

Source: Global Fund website

Sector

4

Month order approved

100%

1.9

5

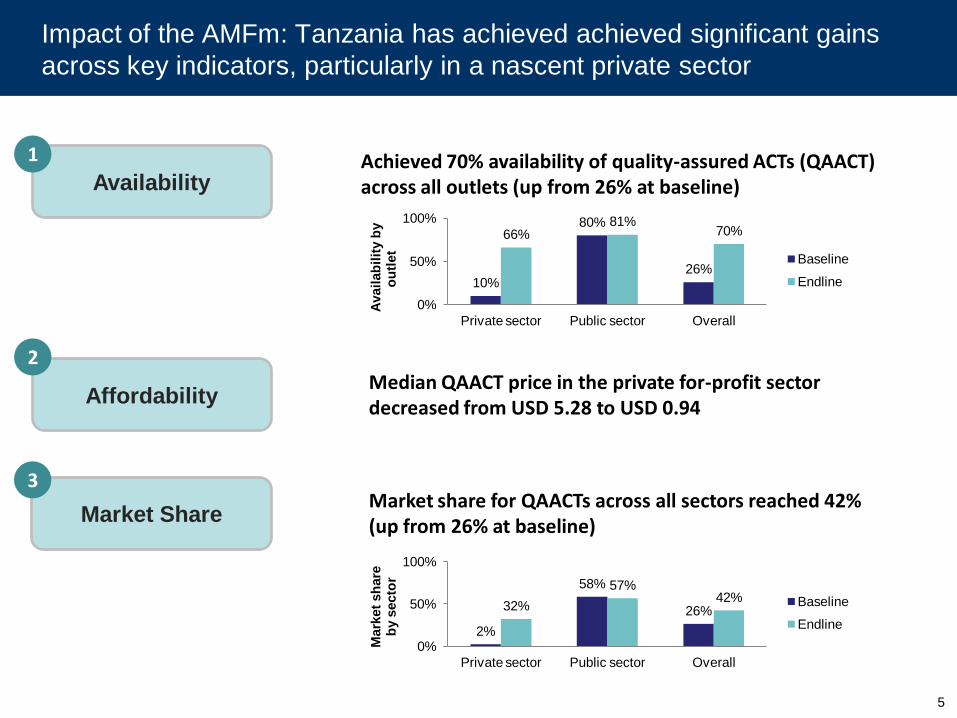

Diarrhea and pneumonia treatment offer perhaps the greatest untapped opportunities to further progress towards MDG 4…

Availability

1

Affordability

Achieved 70% availability of quality-assured ACTs (QAACT) across all outlets (up from 26% at baseline)

2

Market Share

3

Median QAACT price in the private for-profit sector decreased from USD 5.28 to USD 0.94

Market share for QAACTs across all sectors reached 42% (up from 26% at baseline)

10%

80%

26%

66% 81%

70%

0%

50%

100%

Private sector Public sector Overall

Avail

ab

ilit

y b

y

ou

tlet

Baseline

Endline

2%

58%

26% 32%

57% 42%

0%

50%

100%

Private sector Public sector Overall

Mark

et

sh

are

b

y s

ecto

r

Baseline

Endline

Impact of the AMFm: Tanzania has achieved achieved significant gains

across key indicators, particularly in a nascent private sector

As we look forward, transition planning will need to address Tanzania’s

specific country context

Variation in Pf prevalence across Tanzania

Tanzania’s target:

Reduce burden of

malaria by 80% from

2007 levels by end of

2015

Tanzania is working to develop an integrated private sector management

strategy that will both achieve the country’s goals for malaria reduction

and improve value for money

6 Source: Malaria Atlas Project, which combines several surveys of malaria prevalence. A new Malaria Indicator Survey will be coming out later

this year (most recent was 2007).

Internal Document Internal Document

Tanzania has established a Private Sector Case Management Task Force to

address the AMFm transition as well as case management strategy broadly

Respond to

changing

epidemiology

by

strategically

scaling up

diagnosis

Sustain and

improve upon

treatment

gains made

during AMFm

Phase I

Align

regulatory

policies

with case

management

targets

Task Force

Launch

Diagnosis

Sessions

Final

Review

Treatment

Sessions

Regulatory

Approval

Costing

the

Strategy

Where we are now June 2012 December

2012

First

draft

Global Fund

decision

Estimate

needed

funding and

calculate gap

7

Outputs:

1) Private Sector Case Management Strategy document

2) Model for financing

3) Funding gap analysis

8

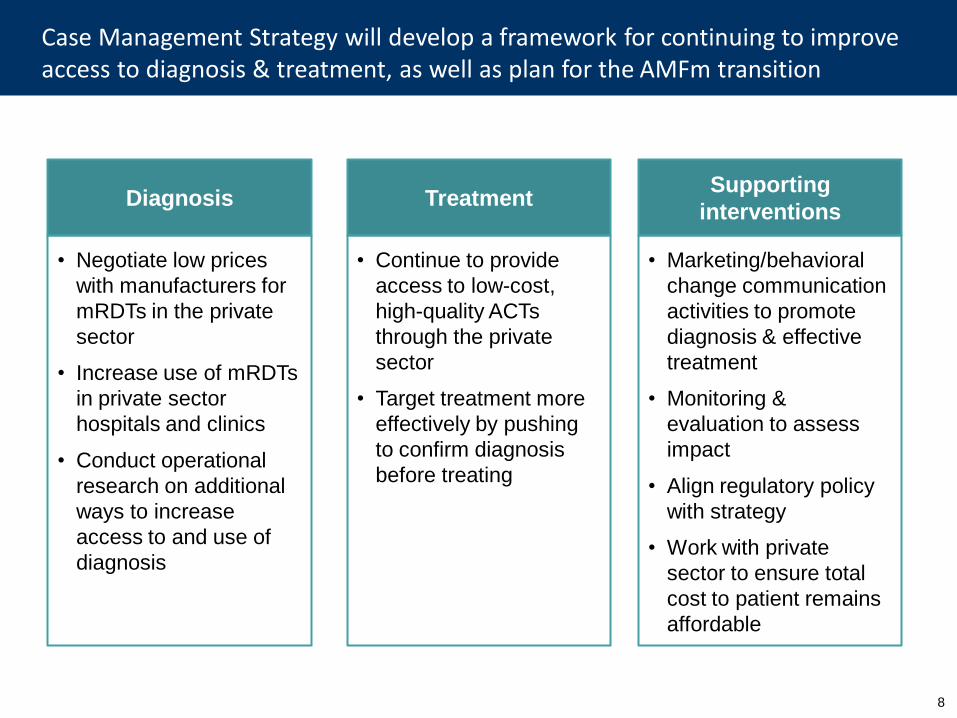

Case Management Strategy will develop a framework for continuing to improve access to diagnosis & treatment, as well as plan for the AMFm transition

Diagnosis

• Negotiate low prices

with manufacturers for

mRDTs in the private

sector

• Increase use of mRDTs

in private sector

hospitals and clinics

• Conduct operational

research on additional

ways to increase

access to and use of

diagnosis

Treatment

• Continue to provide

access to low-cost,

high-quality ACTs

through the private

sector

• Target treatment more

effectively by pushing

to confirm diagnosis

before treating

Supporting

interventions

• Marketing/behavioral

change communication

activities to promote

diagnosis & effective

treatment

• Monitoring &

evaluation to assess

impact

• Align regulatory policy

with strategy

• Work with private

sector to ensure total

cost to patient remains

affordable

9

Future of the AMFm: reactions to “semi-integrated” modification

options, in the context of Tanzania’s private sector

Scenario Pros Cons Summary / Preliminary

evaluation

Diagnosis focus

Fits with current policies and overall strategy

Potential problems with access, compliance, perceptions, total final cost to patients

Promising, but need to think about access problems and final total price to patient

Age targeting Targets a share of population with disproportionate malaria burden

Difficult to monitor/regulate at retail level, possible pack stacking, shift burden to adults

Could be implemented, but have to acknowledge that leakage would occur

Geographic targeting

Deals with problem of varying malaria endemicity; supplier networks could handle regional targeting

Difficult to monitor/regulate at retail level, likely leakage to non-target regions

Could be implemented, but have to acknowledge that leakage would occur

Partial subsidy Relatively easy to implement – same structure as current program

Potential drop in ACT use with higher price and shift to lower-quality treatments

Feasible, but have to consider impact on number of people treated

10

Task Force has begun to address how various AMFm modification

options could be implemented

Scenario Actions needed for implementation Additional ways to target limited

funding

Diagnosis focus

• Increase access to mRDTs through informal drug outlets (would require operational research & eventual policy change)

• Select ADDOs and pharmacies for scale-up based on a particular profile (e.g. geographic location, facilities, health background)

• Reduce ACT subsidy level

Age targeting • To monitor & enforce, would need ground-up change in regulation & reporting systems

• Lower age limit for subsidy

• Combine age + geographic targeting

Geographic targeting

• To monitor & enforce, would need ground-up change in regulation & reporting systems

• Could package drugs to show intended region

• Rank regions by highest malaria burden

Partial subsidy • Work with private sector to keep margins down so that final price is not prohibitively expensive

• Combine with other types of targeting to give different subsidy levels to different groups (though harder to implement)

11

Questions for the group

1) How can the country case management strategy & transition planning

process better align with the on-going transition planning work at the global

level?

2) If the modified AMFm program does not meet our country’s funding needs

to implement our case management strategy plan, where else could we

seek funds? How can we plan for this now?

3) Are there other groups we should coordinate with, or which we could seek

technical assistance from, as we work to build our case management

strategy?

4) Do other countries have experiences we could learn from regarding best

practices for implementing targeted subsidies or diagnosis scale-up?

12

Summary

Tanzania looks forward to getting input from the global community as we

plan our strategy to reduce malaria mortality & morbidity

AMFm

results

• AMFm has resulted in significant gains in availability, affordability,

and market share of ACTs, particularly in the private sector

• Program participants are eager to see it continue

• There is a strong interplay between the public and private sector

that should continue in future programs

Planning

for the

future

• A Private Sector Case Management Task Force has started

planning for future private sector case management strategy and

the AMFm transition

• Initial strategy plans include a scale-up of diagnosis in the private

sector

• Out of the semi-integrated AMFm modification options under

discussion, age and geographic targeting would pose the most

challenges for implementation, but we have begun to discuss how

we could manage the implementation of all options