investor day 2018 - s1.q4cdn.coms1.q4cdn.com/793210788/files/doc_news/2018/8/sqm-vertical_15.pdf ·...

TRANSCRIPT

www.sqm.com2018 1

I N V E S T O RD AY2 0 1 8

N Y S E

S e p t e m b e r 5

www.sqm.com2018 2

CUSTOMARY NOTE

REGARDING FORWARD-LOOKING

STATEMENTS

Statements in this presentation concerning the

Company’s business outlook, future economic

performance, anticipated profitability, revenues,

expenses, or other financial items, anticipated cost

synergies and product or service line growth,

together with other statements that are not

historical facts, are “forward-looking statements” as

that term is defined under the U.S. Private

Securities Litigation Reform Act of 1995.

Any forward-looking statements are estimates,

reflecting the best judgment of SQM management

based on currently available information and

involve a number of risks, uncertainties and other

factors that are outside SQM´s control could cause

actual results to differ materially from those stated

in such statements.

Risks, uncertainties, and factors that could affect

the accuracy of such forward-looking statements

are identified in SQM´s public filing made with the

U.S. Securities and Exchange Commission,

specifically SQM´s most recent annual report on

Form 20-F. All forward-looking statements are

based on information available to SQM on the date

hereof and SQM assumes no obligation to update

such statements whether as a result of new

information, future developments or otherwise,

except as required by law.

www.sqm.com2018 3

Patricio de SolminihacCEO

INVESTOR

DAY

PROGRAM

01.

Ricardo Ramos CFO02.

Gerardo Illanes VP Finance & IR03.

Q&A04.

Presentation is available on our website www.sqm.com

www.sqm.com2018 4

PATRICIO DE SOLMINIHAC

CEO

www.sqm.com2018 5

Commercial exploitation of the caliche ore deposits in northern Chile began

1830

Maria Elena begins operations using the

Guggenheim Method

1926

OUR

HISTORY

SQM is incorporated

1968

Listing of ADR Program on New

York Stock Exchange

SQM begins developing the Salar de Atacama

1993

1997

2005

Lean methodology adoption begins company-wide

2014

Joint venture with Kidman resources to develop the Mt. Holland Lithium Project in Australia

2017

New agreement with CORFO; announcement of lithium capacity expansion in Chile from 48k MT/year to

180k MT/year over next few years

2018

Celebrating 25 years

listed on the NYSE

Celebrating its 50th

anniversary

Lithium hydroxide

production begins

1951

SQM constructs crystalized nitrates plant in Coya Sur

Lithium carbonate production begins

1996

SQM begins iodine production

in Nueva Victoria

Production of potassium nitrate begins

1986

www.sqm.com2018 6

CORPORATE STRATEGY

Be a global company with people committed to excellence, dedicated to

the extraction of minerals and selectively integrated in the production and

sale of products for the industries essential for human development

Ensure availability of key

resources required to

support current goals for medium

and long-term business growth

Consolidate a culture of lean operations

(M1 excellence) throughout the

organization, including operations,

sales and supportareas

Significantlyincrease nitrate sales for all its

applications, and ensure

consistency withthe iodine sales

strategy

Successfullydevelop and

implement alllithium expansionprojects, acquire

more assets tocomplement ourcurrent portfolio

Strengthen the organizational structure to support the development of the strategic

plan, focusing on the development of critical capabilities and the application of the

corporate values of excellence, integrity and safety

Develop and actively manage a robust risk control and mitigation process,

while fousing on sustainable operations and the environment

Improve our stakeholder management to establish links with the community, and

communicate to Chile and the world our contribution to industries essential for human

development

Maximize the margins of each

business line through

appropriate pricing strategy

www.sqm.com2018 7

• Water soluble fertilizer market growing at ~10% per

year

• SQM volume growth outpacing the market in 2018,

over 10%, 2019 will see continued increase

• Expanding nitrates production from 1 to 1.5 million

MT/year. Currently at 1.3 million MT/year

• Two new NPK plants: Italy and Mexico

SPECIALTY PLANT

NUTRITION

Potassium Nitrate

(KNO3)• Currently 16

WSNPK plants; further market development

• New production plants

• Continued cost improvement for all products

• Add value to KNO3

As a result of Lean M1 Operations, in May 2018

the port of Tocopilla shipped 250,000 MT, setting a new shipping record

In 2017, SQM and the Ayllu Wine Program worked

with farmers and the Indigenous Association to

produce over 7,500 bottles of wine in the

Salar de Atacama

2017 Recap

SUSTAINABILITY & INNOVATION

LTM CONTRIBUTION TO:

20%34%

G R O S S P R O F I T R E V E N U E S

www.sqm.com2018 8

POTASSIUM

CHLORIDE

Approximately 15% of our employees are

women, more than double the average in the Chilean mining industry

SUSTAINABILITY & INNOVATION

95.8% of the energy required for our

operations is solar

• Low-cost raw material for our growing potassium

nitrate business

• Market growing, expected to reach ~63-64 million

MT

• 2018 sales volumes estimated to be less than 1

million MT, lower in 2019 as result of increased

lithium and potassium nitrate production

• Approximately 1/3 of SQM sales to Brazil in 2018

MOP• Kore Potash project

• Continued cost improvements for all products

2017 Recap MOP(KCL)

LTM CONTRIBUTION TO:

7%14%

G R O S S P R O F I T R E V E N U E S

www.sqm.com2018 9

IODINE &

DERIVATIVES

Best safety record over the last 12 months

New uses for iodine help keep demand growing consistently

SUSTAINABILITY & INNOVATION

• Market demand will grow close to 3% in 2018

• Sales volumes up, expected to surpass 13k MT

in 2018

• Expansion project from 11-14k MT/year was

completed

• More SQM iodine projects in pipeline;

preparing to meet future market demand

IODINE• More than 35%

market share; >12k MT sales volumes in 2017

• New capacity expansion

• Look for new projects in iodine derivatives

2017 Recap MOPIodine

(I2)

LTM CONTRIBUTION TO:

10% 12%

G R O S S P R O F I T R E V E N U E S

www.sqm.com2018 10

INDUSTRIAL

CHEMICALS

Over 61,000 hours of training completed in 2018.

Important geographical growth related to the use of solar salts: Spain, USA, South Africa,

Morocco, Israel, Chile, UAE, Saudi Arabia and others.

SUSTAINABILITY & INNOVATION

• Market growth coming from solar salts for CSP

(concentrated solar power) projects

• Goal for 2020 volumes to reach 200,000 MT

• 2017 sales volumes expected 100,000MT

2017 RecapMOP

Solar Salts

(KNO3, NaNO3)

LTM CONTRIBUTION TO:

6% 6%

G R O S S P R O F I T R E V E N U E S

www.sqm.com2018 11

• Market growth in 2018 expected to surpass 20%

• Sales volumes in 2018 will surpass 50k MT

• First stage of lithium carbonate expansion in Chile

completed on time and on budget (~US$75 million)

• 70k to 120k MT in 2019 (US$200

million)

• 120k to 180k MT in 2021 (US$250

million)

• Lithium hydroxide expansion in Chile from 6k to

13.5k to be completed this year.

LITHIUM &

DERIVATIVES

Will be able to almost quadruple lithium

production without extracting more brine from

the Salar de Atacama

Continued development of large-scalelithium projects in Chile and abroad

SUSTAINABILITY & INNOVATION

• Exar project

• JV with Kidman Resources (Mt. Holland, Australia)

• Look for new lithium projects outside Chile

• Leadership position in the market

2017 RecapMOP

Li2CO3

LiOHLTM CONTRIBUTION TO:

58%

30%

G R O S S P R O F I T R E V E N U E S

www.sqm.com2018 12

• Agreement reached with CORFO to maintain the lease through 2030

• Total production quota: 2.2 million MT of LCE

• New rent scheme became effective April 10, 2018

• Major investments and expansions in Chile

CORFO & CONTRACT

NEGOTIATIONS

IN THE FUTURE

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Fee,

% o

f p

rice

Li2CO3 Price, US$/kg

CORFO RENTAL FEE (LITHIUM CARBONATE)

Rental Fee, contract % of price Rental Fee, weighted average %

www.sqm.com2018 13

• Annual contribution of US$11-19 million for R&D efforts

• Annual contribution of US$10-15 million for neighboring communities ofthe Salar de Atacama

• Annual contribution of 1.7% of SQM Salar’s sales per year for regionaldevelopment

CONTRIBUTIONS TO THE

DEVELOPMENT AND

COMMUNITIES

www.sqm.com2018 14

• Mt. Holland, 50/50 JV with Kidman Resources

• Estimated to contain 189 million tons of 1.50% Li2O or 7.03 million tons of LCE(according to JORC Code* standards)

• One of the world’s most significant hard rock lithium deposits. Expected to be atthe low end of the global hard rock cost curve

• Exclusive option to lease a premier site in Kwinana, Western Australia to build arefinery and produce battery-grade refined lithium

• Production focus on lithium hydroxide

• Capacity: 45k MT of LiOH/year

• Estimated commission date: 2020 - spodumene concentrate, 2021 - LiOH

• Current status: advancing on feasibility studies for mine, concentrator andrefinery

LITHIUM EXPANSION

IN AUSTRALIA

*The Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (‘the JORC Code’)

www.sqm.com2018 15

On track to capture opportunities in SPN, lithium, iodine and industrial chemicals business lines

CONCLUSION

01.

02.

03.

Lithium is, and will continue to be, our main business line

We will continue to make decisions to maximize SQM value in the long-term

www.sqm.com2018 16

RICARDO RAMOSCFO

www.sqm.com2018 17

GROSS

PROFIT

EVOLUTION

-

200

400

600

800

1,000

1,200

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Fertilizers (SPN+KCL) Iodine Lithium Industrial Chemicals

2010-2014: Iodine boomMarket growth 2-4%

2016- : Lithium boomMarket growth 15-20%

2007-2013: Fertilizer boomMarket growth 1-2%

www.sqm.com2018 18

Demand growth has been led by energy storage related to electronic devices

and power tools. Further growth will be related to electric vehicles.

Source: SQM Estimates

A CLOSER LOOK

AT THE

LITHIUM MARKET

LITHIUM CHEMICALS DEMAND COMPARISON

0

50

100

150

200

250

2010 2011 2012 2013 2014 2015 2016 2017

KM

T-L

CE

Lithium Demand Evolution 2010-2017

Other applications Energy Storage (kMT-LCE)

2010 Total Demand: 98k 2017 Total Demand: 212k

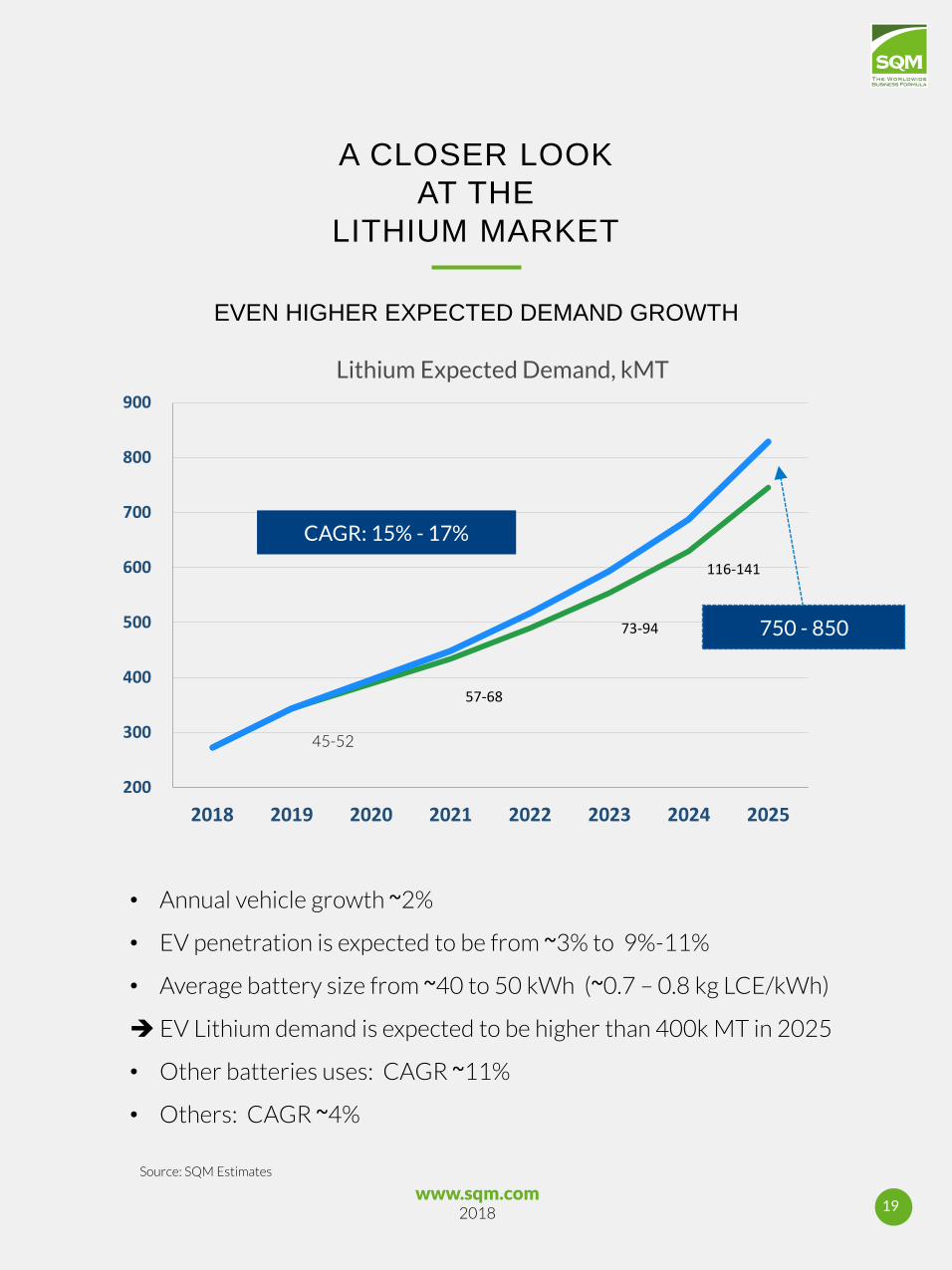

www.sqm.com2018 19

• Annual vehicle growth ~2%

• EV penetration is expected to be from ~3% to 9%-11%

• Average battery size from ~40 to 50 kWh (~0.7 – 0.8 kg LCE/kWh)

EV Lithium demand is expected to be higher than 400k MT in 2025

• Other batteries uses: CAGR ~11%

• Others: CAGR ~4%

Source: SQM Estimates

A CLOSER LOOK

AT THE

LITHIUM MARKET

EVEN HIGHER EXPECTED DEMAND GROWTH

200

300

400

500

600

700

800

900

2018 2019 2020 2021 2022 2023 2024 2025

57-68

73-94

116-141

Lithium Expected Demand, kMT

750 - 850

CAGR: 15% - 17%

45-52

www.sqm.com2018 20

A CLOSER LOOK

AT THE

LITHIUM MARKET*

Demand is growing, and new capacity is needed.

SQM´s Strategy:

• Chile: capacity increase

(48k 70k 120k 180k MT)

• Australia: 45k MT

Be prepared for higher demand growthrates

• The best quality (physical and chemical), looking at the long-term requirements

• Focus on technological development, costreduction and environmentalsustainability

• Value-added relationships with ourcustomers

• Potential M&A activities

*Source: SQM Estimates

www.sqm.com2018 21

KEY ASSUMPTIONS:

• Other Players: Wodgina, Pilbara, other minerals and other brines

From 155 to 385k MT CAGR ~14%

• Big Players: SQM, Albemarle & Tianqi (Salar de Atacama & Talison)

CAGR: ~11% (~8% in 2019/2020, ~3% in 2021/2022, ~15% in 2023/2024, ~25% in 2025)

GLOBAL LITHIUM SUPPLY

EVOLUTION

-

100

200

300

400

500

600

700

800

900

2018 2019 2020 2021 2022 2023 2024 2025

Expected Supply, kMT

Other Producers Big Players

310

385

*Source: SQM Estimates

150

155

www.sqm.com2018 22

• 2024-2025, market will need new projects or the big players will have toincrease their market share

• Systematically, new projects have been delayed longer than expected andrelated production has been less than projected

• High quality battery grade lithium is very difficult to obtain during the earlyproduction years. Quality restrictions in the future are expected to be greaterthan today

• In the past we have underestimated the demand. Small variations in thepenetration of the EVs can have significant effect on lithium demand

GLOBAL LITHIUM

SUPPLY & DEMAND

EVOLUTION

*Source: SQM Estimates

200

300

400

500

600

700

800

2018 2019 2020 2021 2022 2023 2024 2025

Supply & Demand, kMT

Supply Demand at CAGR 15% Demand at CAGR 17%

www.sqm.com2018 23

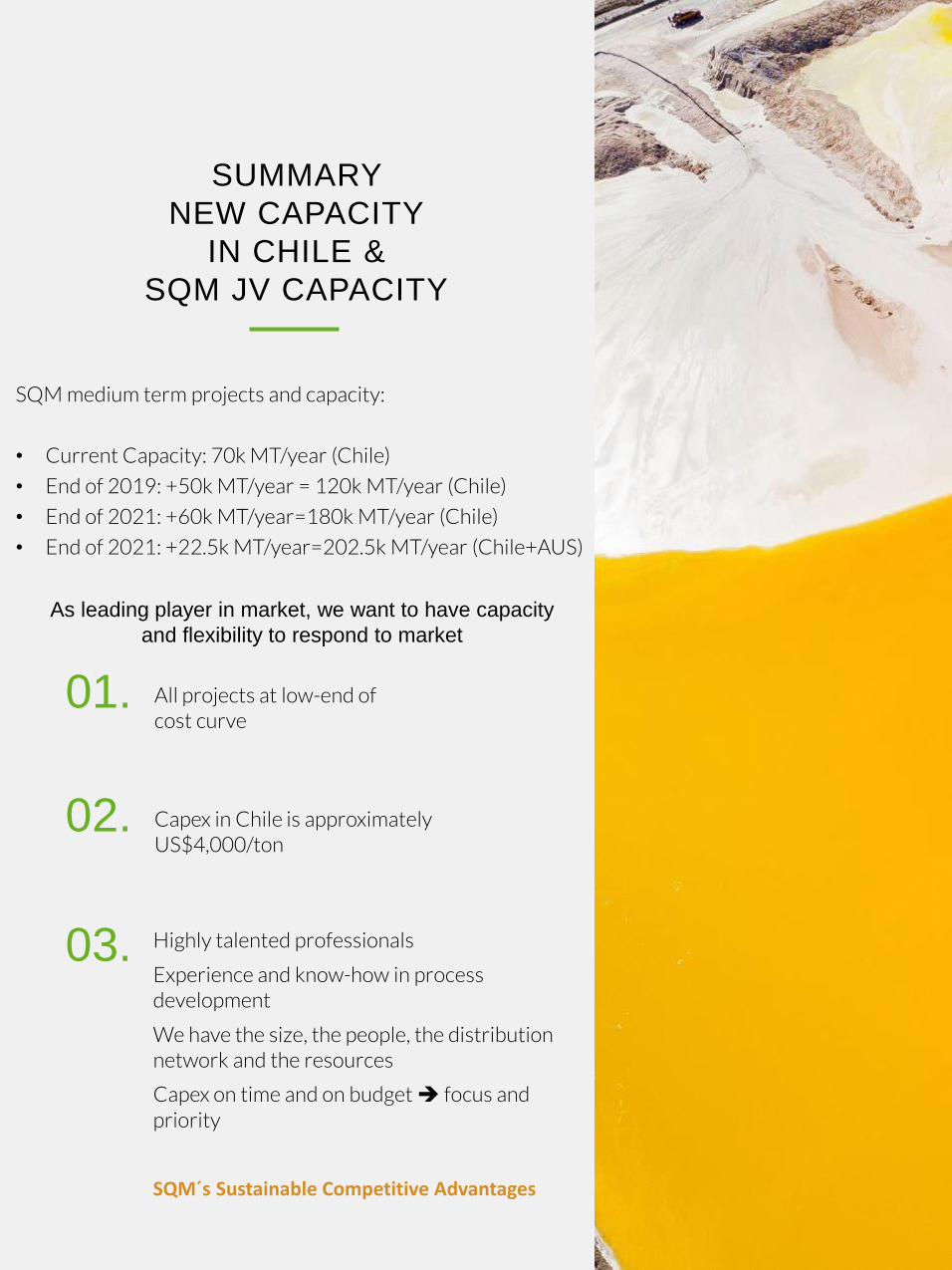

SUMMARY

NEW CAPACITY

IN CHILE &

SQM JV CAPACITY

All projects at low-end of cost curve

01.

02. Capex in Chile is approximately US$4,000/ton

As leading player in market, we want to have capacity

and flexibility to respond to market

SQM medium term projects and capacity:

• Current Capacity: 70k MT/year (Chile)

• End of 2019: +50k MT/year = 120k MT/year (Chile)

• End of 2021: +60k MT/year=180k MT/year (Chile)

• End of 2021: +22.5k MT/year=202.5k MT/year (Chile+AUS)

Highly talented professionals

Experience and know-how in process development

We have the size, the people, the distribution network and the resources

Capex on time and on budget focus and priority

SQM´s Sustainable Competitive Advantages

03.

www.sqm.com2018 24

GERARDO ILLANESVP FINANCE & IR

www.sqm.com2018 25

REVIEW OF RESULTS

SPN Iodine Lithium I.Chem. Potassium

PRICE

QUANTITY

Prices increased in all business lines in the 2Q2018 compared to the same period of 2017.

Significantly increased lithium prices outweighed the impact of lower sales volumes in the 1H2018.

US

$ M

illio

n

180

1213

159 (5) 1

224

100

150

200

250

300

350

Gross Profit Contribution 2Q2018/2Q2017

Revenue Contribution 2Q2018/2Q2017

505

3722

3331

8 3

639

400

500

600

700

800

US

$ M

illio

n

www.sqm.com2018 26

STRONG FINANCIAL POSITION

2.4 2.4

2.4 2.1

1.0

2.0

3.0

4.0

Jun 17 Dec 17 Mar 18 Jun 18

Accounts Receivables(Months of Sales)

8.3 7.8 8.0 7.4

4.0

8.0

12.0

16.0

Jun 17 Dec 17 Mar 18 Jun 18

Inventory(Months of Sales)

4.2

3.3 3.2 3.6

2.0

3.0

4.0

5.0

6.0

Jun 17 Dec 17 Mar 18 Jun 18

Liquidity(Current Assets/Current Liabilities)

6.1 4.5

7.3 6.2

0.0

2.0

4.0

6.0

8.0

10.0

Jun 17 Dec 17 Mar 18 Jun 18

Cash / Short-Term Financial Debt

0.4 0.2 0.1

0.4

0.0

0.5

1.0

1.5

2.0

Jun 17 Dec 17 Mar 18 Jun 18

Net Financial Debt/ EBITDA

0.8 0.9 0.9

1.0

0.5

1.0

1.5

2.0

Jun 17 Dec 17 Mar 18 Jun 18

Leverage

www.sqm.com2018 27

Historical Maintenance CAPEX: ~US$100

million

2016-2018: Lithium Hydroxide Expansion to

13.5k MT: ~US$30 million

2017-2018: Potassium Nitrate Expansion to

1.5m MT: ~US$50 million

2017-2021: Lithium Carbonate Expansion to

180k MT: ~US$525 million

2017-2018: Iodine capacity expansion to 14k

MT: ~US$30 million

2018 CAPEX in Chile: ~US$360 million

CAPEX

www.sqm.com2018 28

CONTACT

INFORMATION

Gerardo Illanes

VP OF FINANCE

Kelly O’Brien

HEAD OF INVESTOR RELATIONS

Irina Axenova

INVESTOR RELATIONS