inventory planning & control

TRANSCRIPT

Inventory Planning

&

Control

Inventory Planning

• The process of determining the optimal quantity and timing of Inventory for the purpose of aligning it with sales and production capacity .

•Inventory planning has direct impact a company's cash flow and profit margins especially for smaller businesses that rely upon a quick turnover of goods or materials.

Objectives of Inventory Planning Customer Satisfaction

Forecasting Needs

Controlling Costs

Successful Storage

Objectives of Inventory Planning

Forecasting Needs

Controlling Costs

Successful Storage

Customer Satisfaction

Advantages of inventory planning

You know your stock levels

You can conduct stock rotation

You can optimize and reduce stock of items that don’t move that quickly

You can move you quick moving items to the front thereby speeding up picking

You can quick identify items that are not moving that you can remove from your inventory

Disadvantages of inventory planning

It doesn’t stop staff stealing stock

It can waste a lot of effort if not implemented and maintained correctly

It doesn’t replace incompetent management

It can be very expensive and the return on investment can take a long time

It requires a lot of staff training and you may loose some staff on the way

Material Requirement Planning Material requirements

planning (MRP) is a production planning and inventory control system used to manage manufacturing processes. Most MRP systems are software-based, while it is possible to conduct MRP by hand as well.

What can MRP do ? Reduce Inventory Levels

Reduce Component shortages

Improve Shipping Performance

Improve Customer Service

Improve Productivity

Simplified and Accurate Scheduling

Reduce Purchasing Cost

Improve Production Schedules

Conti…. Reduce Manufacturing Cost

Reduce Lead Times

Less Scrap and Rework

Higher Production Quality

Improve Communication

Improve Plant Efficiency

Reduce Fright Cost

Reduction in Excess Inventory

Reduce Overtime

Three Basic Steps Of MRP

Identifying Requirements

Running MRP – Creating the Suggestions

Framing the Suggestions

Step 1: Identifying the Requirements Quantity on Hand

Quantity on Open Purchase Order

Quantity in/or Planned for Manufacturing

Quantity Committed to Existing Orders

Quantity Forecasted

Step 2: Running MRP – Creating the Suggestions Critical Items

Expedite Items

Delay Items

Step 3: Framing the suggestions Manufacturing Orders

Purchasing Orders

Various Reports

Types Of MRP Reports

Primary MRP Reports

Secondary MRP Reports

Primary MRP Reports Planned orders to be released at a future time. Order release notices to execute the planned orders. Changes in due dates of open orders due to

rescheduling. Cancellations or suspensions of open orders due to

cancellation or suspension of orders on the master production schedule.

Inventory status data.

Secondary MRP Reports Planning reports, for example, forecasting inventory

requirements over a period of time. Performance reports used to determine agreement

between actual and programmed usage and costs. Exception reports used to point out serious

discrepancies, such as late or overdue orders.

What is Master Production Schedule ? A Master Production Schedule or MPS is the plan that

a company has developed for production, inventory, staffing, etc. It sets the quantity of each end item to be completed in each week of a short-range planning horizon. A Master Production Schedule is the master of all schedules. It is a plan for future production of end items.

The Master Production Schedule gives production, planning, purchasing, and top management the information needed to plan and control the manufacturing operation. The application ties overall business planning and forecasting to detail operations through the Master Production Schedule.

Bill of Materials (BOM)

A listing of all the subassemblies, intermediates, parts, and raw materials that go into a parent assembly showing the quantity of each required to make an assembly.

Basically, a bill of material (BOM) is a complete list of the components making up an object or assembly.

Bills of materials come in different types specific to engineering (used in the design process), manufacturing (used in the manufacturing process), and so on. A manufacturing BOM is of vital importance in materials requirement planning (MRP) and enterprise resource planning (ERP) systems.

Benefits of a BOM Improve material management by responding to changes

in production.

Reduce inventory levels and obsolete parts.

Reduce manufacturing costs.

Minimize clerical and engineering efforts by optimizing the tasks of maintaining and changing multi-level bills.

Supports variable length part numbers and unlimited descriptive text.

Easy methods for accessing part information

Inventory Control is the supervision of supply, storage and accessibility of items in order to ensure an adequate supply without excessive oversupply

Objectives of inventory control Protection against fluctuations in demand

Better use of men, material & machines

Protection against fluctuations in output

Control of stock volume

Control of stock distribution

Major activities of inventory control Planning the inventories

Procurement of inventories

Receiving and inspecting the inventories

Storing and issuing the inventory

Recording the receipt and issues of inventories

Physical verification of inventories

Follow-up function

Material standardisation and substitution

Steps in Inventory Control Deciding the maximum-minimum limits of

inventory

Determination of Reorder point

Determination of Reorder quantity

ABC Analysis

ABC analysis (Inventory) ABC analysis is an inventory categorization

method which consists in dividing items into three categories, A, B and C: A being the most valuable items, C being the least valuable ones. This method aims to draw managers’ attention on the critical few (A-items) and not on the trivial many (C-items).

The ABC approach states that, when reviewing inventory, a company should rate items from A to C, basing its ratings on the following rules:

A-items are goods which annual consumption value is the highest. The top 70-80% of the annual consumption value of the company typically accounts for only 10-20% of total inventory items.

B-items are the interclass items, with a medium consumption value. Those 15-25% of annual consumption value typically accounts for 30% of total inventory items.

C-items are, on the contrary, items with the lowest consumption value. The lower 5% of the annual consumption value typically accounts for 50% of total inventory items.

Purpose of inventory To maintain independency of operation

To meet variation in product demand

To allow flexibility in product scheduling

To provide a safeguard for variation in raw material delivery time

To take advantages of economic purchase order size

Types of inventory

control

Independent Demand

Dependent Demand

Independent Demand

An inventory of an item is said to be falling into the category of independent demand when the demand for such an item is not dependant upon the demand for another item.

Finished goods Items, which are ordered by External Customers or manufactured for stock and sale, are called independent demand items.

Independent demands for inventories are based on confirmed Customer orders, forecasts, estimates and past historical data.

Dependant Demand

If the demand for inventory of an item is dependant upon another item, such demands are categorized as dependant demand.

Raw materials and component inventories are dependant upon the demand for Finished Goods and hence can be called as Dependant demand inventories.

Difference between independent demand & dependent demand:

One of the biggest differences in inventory is between dependent and independent demand. Understanding this difference is important as the entire inventory policy for an item is based on this.

Independent demand is demand for a finished product, such as a computer, a bicycle, or a pizza. Dependent demand, on the other hand, is demand for component parts or subassemblies.

For example, this would be the microchips in the computer, the wheels on the bicycle, or the amount of cheese on the pizza.

Inventory System

A set of policies and controls that monitors levels of inventory and determines what levels should be maintained, when stock should be replenished, and how large orders should be

Single Period Inventory Models A single period inventory model is used to identify the

amount of inventory to purchase given a perishable good or single opportunity to purchase.

The amount of the single order is based on balancing the cost of over- and under-estimating demand. This is a very common problem in areas such as:

Overbooking of airline seats or hotel rooms

Ordering of fashion items

Any type of one-time order (t-shirts for a sporting event)

Multi period inventory system Demand for the product is constant and uniform throughout the period

Lead time (time from ordering to receipt) is constant

Price per unit of product is constant

Inventory holding cost is based on average inventory

Ordering or setup costs are constant

All demands for the product will be satisfied (No back orders are allowed)

Fixed- time periods

models/p-model

Fixed- order quantity models/ EOQ(Economic Order Quantity)

multi period inventory

system

Economic Order Quantity(EOQ) Economic order quantity is the order quantity that

minimizes total inventory holding costs and ordering costs.

The framework used to determine this order quantity is also known as Wilson EOQ Model or Wilson Formula

The model was developed by Ford W. Harris in 1913

Fixed-time periods models/p-model

This is similar to the fixed–order quantity model;it is used when the item should be in-stock and ready to use.In this case, rather than monitoring the inventory level and ordering when the level gets down to a critical quantity, the item is ordered at certain intervals of time,

for example, every Friday morning. This is often convenient when a group of items is ordered together. An example is the delivery of different types of bread to a grocery store. The bakery supplier may have 10 or more products stocked in a store, and rather than delivering each product individually at different times, it is much more efficient to deliver all 10 together at the same time and on the same schedule.

Assumptions

The ordering cost is constant.

The rate of demand is known, and spread evenly throughout the year.

The lead time is fixed.

The purchase price of the item is constant i.e. no discount is available

Only one product is involved.

To find EOQ

TC=DC+D/S

Basic Fixed-Order Quantity (EOQ) Model Formula

H 2

Q + S

Q

D + DC = TC

Total Annual =Cost

AnnualPurchaseCost

AnnualOrderingCost

AnnualHoldingCost

+ +

TC=Total annual

cost

D =Demand

C =Cost per unit

Q =Order quantity

S =Cost of placing

an order or setup

cost

R =Reorder point

L =Lead time

H=Annual holding

and storage cost

per unit of inventory

17-40

Deriving the EOQ

Using calculus, we take the first derivative of the total cost function with respect to Q, and set the derivative (slope) equal to zero, solving for the optimized (cost minimized) value of Qopt

Q = 2DS

H =

2(Annual D em and)(Order or Setup Cost)

Annual Holding CostO PT

R eorder point, R = d L_

d = average daily demand (constant)

L = Lead time (constant)

_

We also need a

reorder point to

tell us when to

place an order

17-41

EOQ Example (1) Problem Data

Annual Demand = 1,000 unitsDays per year considered in average

daily demand = 365Cost to place an order = $10Holding cost per unit per year = $2.50Lead time = 7 daysCost per unit = $15

Given the information below, what are the EOQ and

reorder point?

17-42

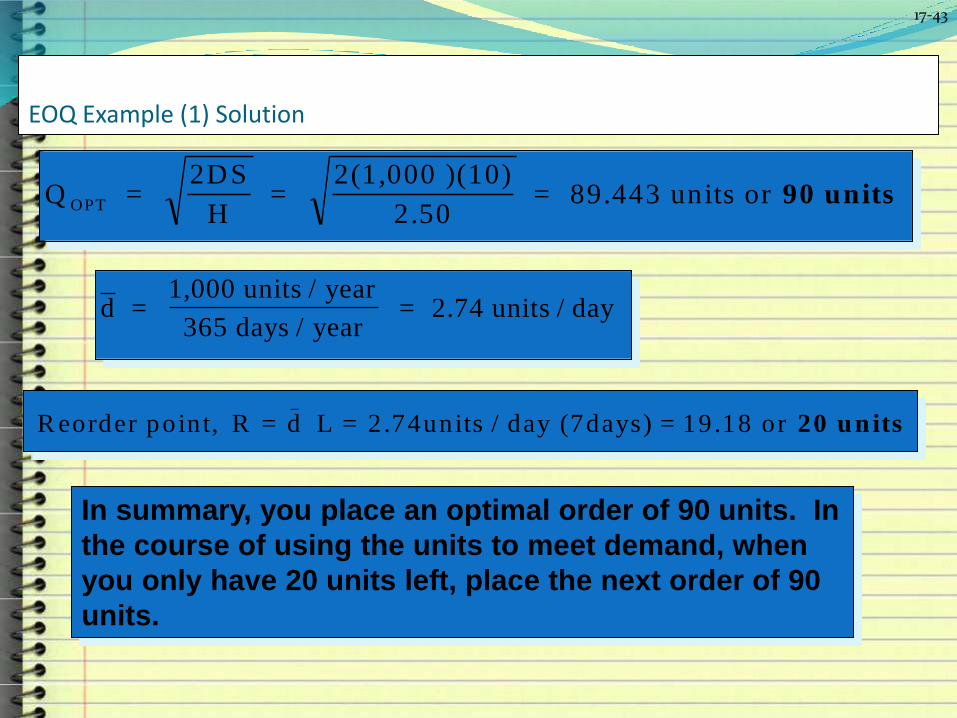

EOQ Example (1) Solution

Q = 2DS

H =

2(1,000 )(10)

2.50 = 89.443 units or OPT 90 units

d = 1,000 units / year

365 days / year = 2.74 units / day

R eorder point, R = d L = 2.74units / day (7days) = 19.18 or _

20 units

In summary, you place an optimal order of 90 units. In

the course of using the units to meet demand, when

you only have 20 units left, place the next order of 90

units.

17-43

Carrying Cost Of Inventory

This is the cost a business incurs over a certain period of time, to hold and store its inventory

Businesses use this figure to help them determine how much profit can be made on current inventory.

It also helps them find out if there is a need to produce more or less, in order to keep up with expenses or maintain the same income stream.

Different Types of Inventory Costs1. Holding\Carrying cost

2. Ordering costs:

3. Storage costs:

4. Setup/production change costs :

Holding\Carrying cost They are expenses such as storage, handling, insurance,

taxes, obsolescence, and interest on funds financing the goods.

These charges increase as inventory levels rise. To minimize carrying costs, management makes frequent orders of small quantities.

Holding costs are commonly assessed as a percentage of unit value, rather than attempting to derive monetary value for each of these costs individually.

This practice is a reflection of the difficulty inherent in deriving a specific per unit cost, for example, obsolescence or theft.

Ordering costs: Ordering costs are those fees associated with placing

an order, including expenses related to personnel in purchasing department, communications, and the handling of related paper work.

Lowering these costs would be accomplished by placing small number of orders, each for a large quantity.

Unlike carrying costs, ordering expenses are generally expressed as a monetary value per order.

Storage costs: When the stock of the item is depleted, an order for

that item must wait until the stock is replenished or be cancelled

There is a trade off between carrying stock to satisfy demand and the cost resulting from stock out

Setup/production change costs To make each different product involves obtaining the

necessary material, arranging specific equipment setup, filling out the required papers, appropriately charging time and materials, and moving out the previous stock of material

If there were no cost or loss of time in changing from one product to another, many small lots would be produced.

These would reduce inventory levels, with a resulting saving in cost.

Thank you