introductory+session+1_sid

DESCRIPTION

Global Capital Markets Lecture 1TRANSCRIPT

Capital Markets and Investments Lecture 1: Introduction

Sid Dastidar

1

Outline for today

Housekeeping

– Introduction

– Course requirements, mechanics

– Overview of course material

Refresher: Discounting and NPV

2

About Me

Siddhartha G Dastidar (Sid)

Email: [email protected], [email protected]

Phone: 212 7459789

Office Hours: by appointment, before / after class

Background…

3

TA

● Responsible for all aspects of the course – homework/ exam

grading, administration, etc. Your first point of contact.

● Fei He

Office hour: TBD

Supported by a capable set of CAs

● Review Sessions: As needed, few times during the semester

4

What you can expect…

Lectures with real examples

Course notes (borrowed heavily from Business School Cap Mkts & Inv

Slides – Thanks Martin Oehmke)

Supported by strong TA

Project?

5

What I expect… (IMPORTANT!)

Attend lectures and keep up (the class will fly by)

Come prepared – print out slides before class, review old slides

Participate, contribute and troubleshoot - Take notes, copy keywords even if you don’t understand completely, so that you can look it up later

Ask questions!

Don’t free-ride on homework, project (?), assignments

Follow the honor code

I try to keep the vibe relaxed – please do not misuse it. If you need to be distracted (laptop, etc.), please sit at the back of the room.

6

Dastidar 7

Readings

●Lecture Notes

●Bodie, Kane and Marcus

Investments

●Fixed Income Markets (Sundaresan)

●Financial Markets (John Donaldson)

●Fabozzi’s books

●Econometrics of Financial Markets (Campbell Lo and

McKinley)

Dastidar 8

Readings (contd…)

●Yahoo finance, Google finance

●Wall Street Journal Opinion pieces

●SIFMA website

●BIS

●Bloomberg account (training in library)

●Get familiar with databases – CRSP, Compustat,

●CFA ?

Dastidar 9

Grades (Approximate – almost always changes)

● Assignments 10-20%

• Group grade

● Midterm 30%

• Cheat Sheet

● Final 30%

• Cheat Sheet

● Project (?) 30%

• Group grade

Dastidar 10

Prerequisites

● Some knowledge of the basics of finance

– The course is self-contained

● Because of the nature of modern practical finance, the course is

quantitative

– But in class and in the exam, I will emphasize INTUITION

Course Material: Courseworks

11

All material will be posted on Courseworks

Slides

Problem sets

Solutions

Other Articles

Please check your email for course updates

Readings

I will upload lecture slides before each class, which will contain all

you need to know

Optional Background reading: Bodie, Kane and Marcus (BKM)

Investments, (old editions are ok)

Articles: I will distribute articles relevant to material in class. These

are important to connect the course to the real world.

12

Prerequisites

● Some knowledge of the basics of finance

– …but the course is self-contained

● Because of the nature of modern practical finance, the course is

quantitative

– Homework will use algebra and use some statistical concepts

(e.g., regressions…)

13

Goal and outline

This course has two main goals

1. To provide you the basic foundational knowledge of the basic

financial markets and methods

2. To whet your appetite for finance

Outline: we will cover the main asset markets and methods

1. Fixed income

2. Equities

3. Options

14

Course Outline

Introductory Concepts:

– Valuing Cash flows – NPV, IRR

– No Arbitrage, Limits to arbitrage

1) Fixed Income

– Pricing Coupon Bonds

– Yield to Maturity

– Duration (Interest rate risk)

– Short-term Interest Rates, Long-term Interest Rates, and Federal Reserve Policy

– Forward Rates, Swap Rates

– Credit Markets: Eurodollar, Libor

– Corporate Credit (Maybe?)

15

Course Outline

2) Equity Markets

– What do we know? Empirical facts on Equity Markets

– Valuation of Equity

– Portfolios and Diversification

– CAPM, Theory and Applications

– State of the Art Pricing Models

16

Course Outline

3) Option Valuation

– Binomial Model

– Black-Scholes Model

– Options Terminology – Implied Volatility, Skew

17

18

Course Concepts

● Institutional Features (NOT in class notes) – see BKM, WSJ, FT

● Valuation

– Principles

– Techniques

● Other applications of financial valuation

– Hedging

Dastidar

Dastidar 19

The Religion of Finance

Finance Valuation Axioms

• Investors Prefer More to Less

• Investors are risk-averse

• Money paid in the future is worth less than the same amount today

• Financial markets are competitive; investors are rational

Present/Future Values

● What is the amount of money I will get in the future when

compounding at rate r? This is the future value

20

Today (time 0) Future (time N)

$1 (1+r)N Future Value

(1+r)-N $1 Present Value

Compound Interest Formulas

Annual Compounding

(10% per year)

Semi-annual

(5% every 6 months)

Daily

Continuous

21

1)1.1(

)05.1)(05.1(2

1.12

365

3651.1

)1exp(.m

1.1limm

m

Effect of Compounding

● How long does it take (in years) for your money to double when we

increase the compounding frequency?

22

Interest rate = 10.00% 50.00%

Annual 7.2725 1.7095

Semi-Annual 7.1033 1.5531

Daily 6.9324 1.3872

Continuous 6.9315 1.3863

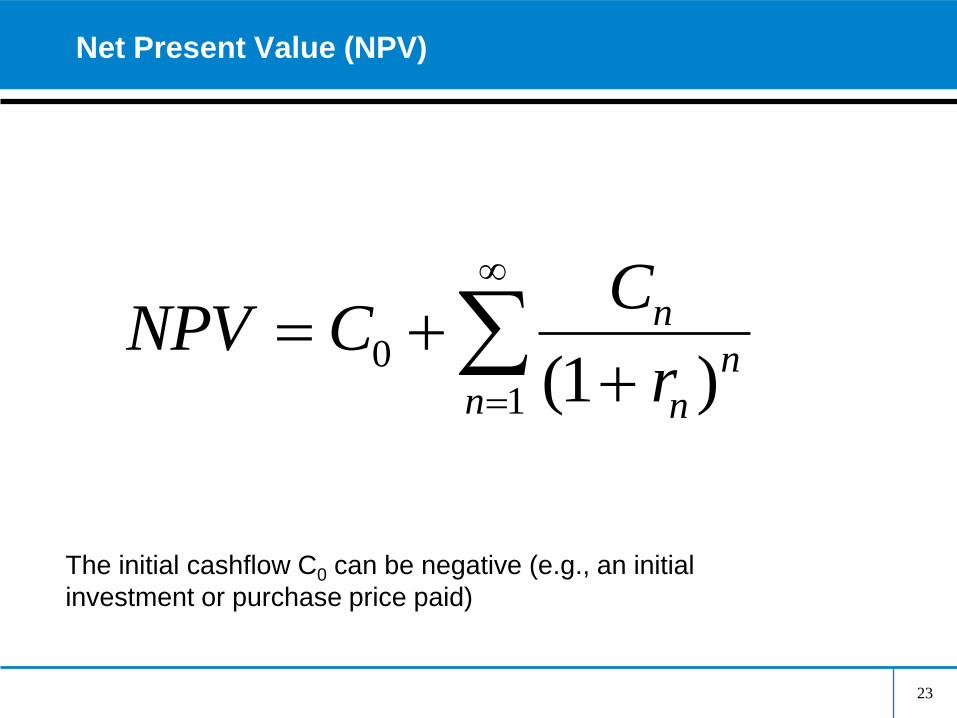

Net Present Value (NPV)

23

1

0)1(n

n

n

n

r

CCNPV

The initial cashflow C0 can be negative (e.g., an initial

investment or purchase price paid)

An investor can buy a 10 year bond, face-value $100 paying an

annual 10% coupon. If the price of the bond is $100, should the

investor buy the bond? Assume a constant discount rate of 5%

nn

n

)r1(

1δ

%5rr

Discount Rate = 5.00%

C(n) dn

Time Cashflows Discount C(n)xdn

0 -100 1 -100

1 10 0.952381 9.52381

2 10 0.907029 9.070295

3 10 0.863838 8.638376

4 10 0.822702 8.227025

5 10 0.783526 7.835262

6 10 0.746215 7.462154

7 10 0.710681 7.106813

8 10 0.676839 6.768394

9 10 0.644609 6.446089

10 110 0.613913 67.53046

NPV = 38.60867

24

The Net Present Value (NPV) Rule

The Rule:

Take all projects that have a positive NPV

The Logic:

The contribution of a project to the value of the firm is equal to its NPV

Projects can be ranked according to NPV

25

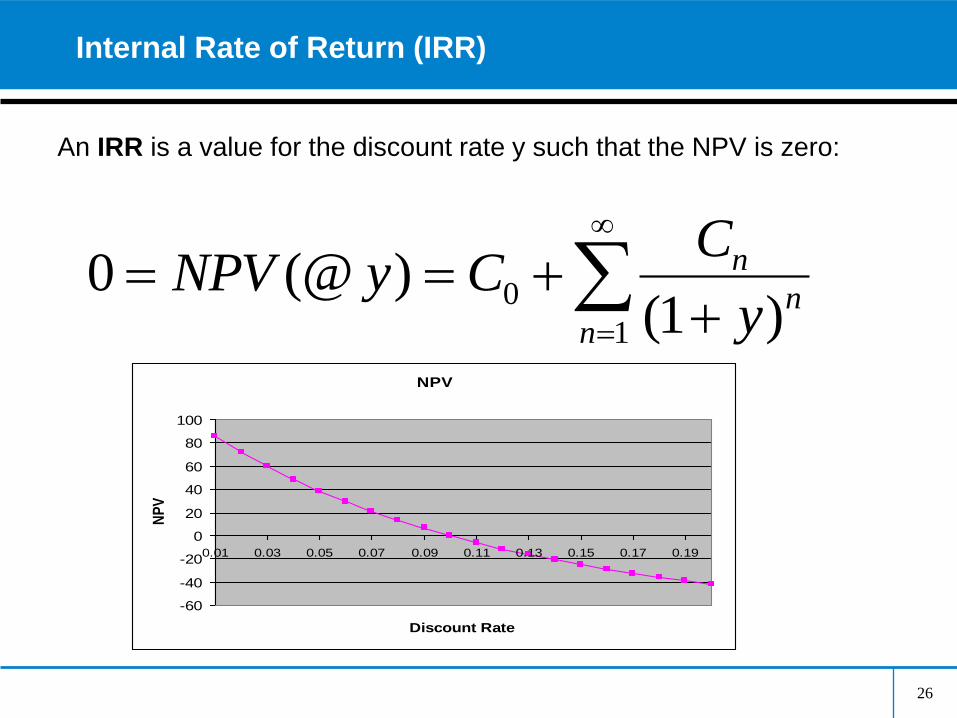

Internal Rate of Return (IRR)

An IRR is a value for the discount rate y such that the NPV is zero:

26

1

0)1(

)(@0n

n

n

y

CCyNPV

NPV

-60

-40

-20

0

20

40

60

80

100

0.01 0.03 0.05 0.07 0.09 0.11 0.13 0.15 0.17 0.19

Discount Rate

NP

V

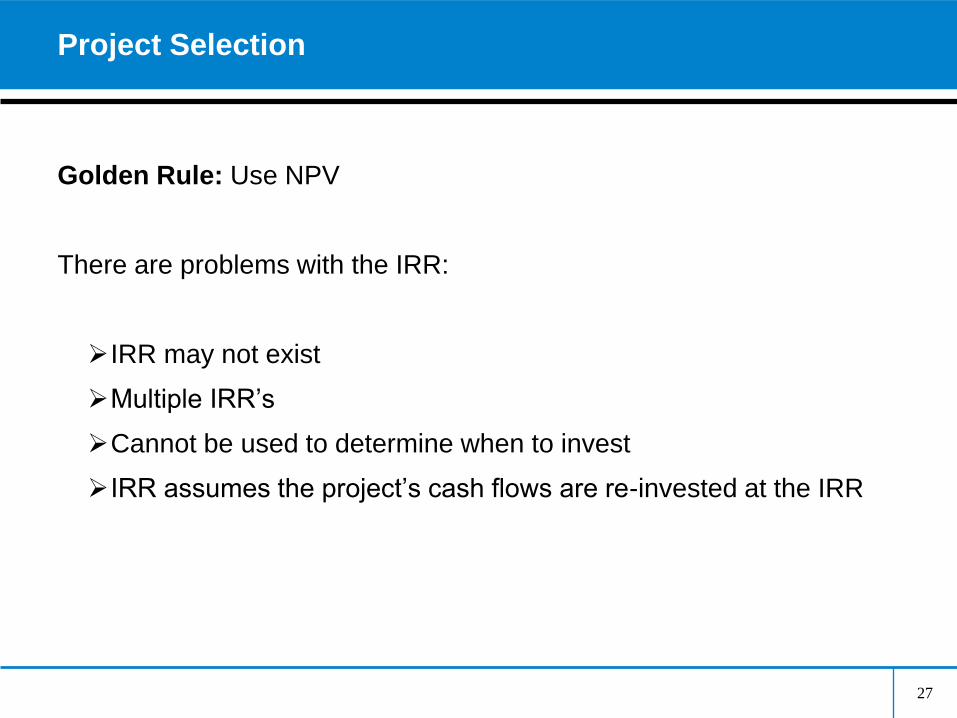

Project Selection

Golden Rule: Use NPV

There are problems with the IRR:

IRR may not exist

Multiple IRR’s

Cannot be used to determine when to invest

IRR assumes the project’s cash flows are re-invested at the IRR

27

IRR may not exist

Cashflows

Year 0 100

Year 1 -300

Year 2 250

0 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6 1.8 20

5

10

15

20

25

30

35

40

45

50

NP

V

Discount Rate

28

Multiple IRR’s may exist

0 1 2 3 4 5 6-200

-150

-100

-50

0

50

100

NP

V

Discount Rate

Cashflows

Year 0 -160

Year 1 1000

Year 2 -1000

29

Why NPV?

● Consistent with maximizing shareholder wealth

● Given cash flows and discount rates, the NPV always gives an unambiguous answer

● NPV can be used for sensitivity and breakeven analysis

● NPV rankings are appropriate for selecting among mutually exclusive projects

● NPV rule can guide investment decisions in every context if the correct yield curve is used to discount cash flows

30

Dastidar 31

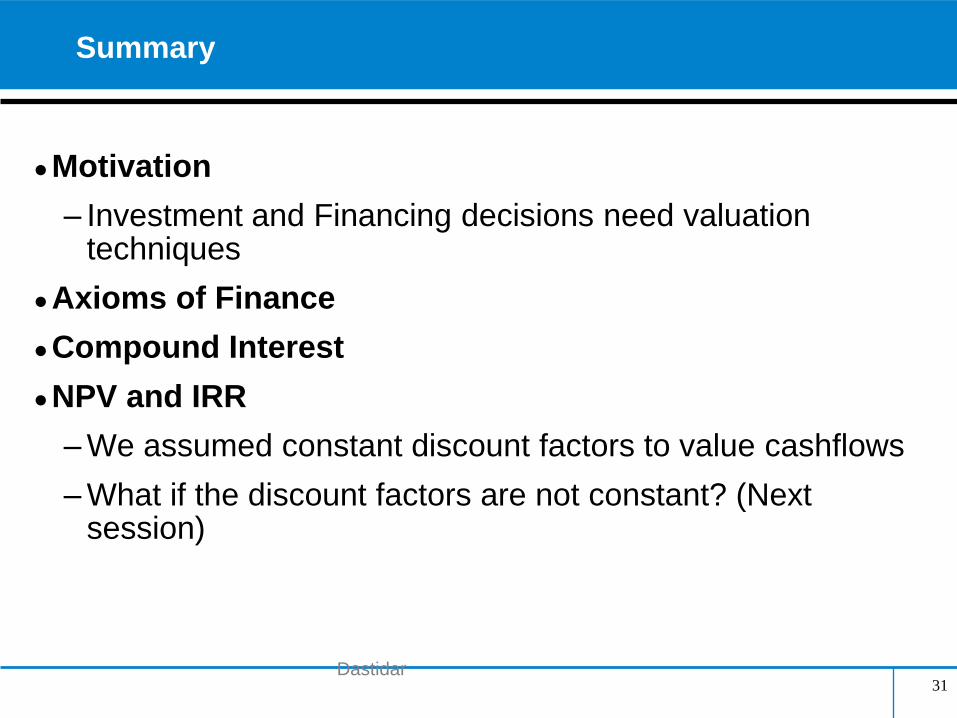

Summary

●Motivation

– Investment and Financing decisions need valuation techniques

●Axioms of Finance

●Compound Interest

●NPV and IRR

– We assumed constant discount factors to value cashflows

– What if the discount factors are not constant? (Next session)