international finance tuesday 9 june 2009 1. international finance: today, 9.6.09 lecture: 9:00 to...

Post on 19-Dec-2015

214 views

TRANSCRIPT

International Finance

Tuesday

9 June 2009

1

International Finance: Today, 9.6.09

Lecture: 9:00 to 10:50Break: 10:50 to 11:00Lecture: 11:00 to 12:00Break: 12:00 to 1:00Lecture 1:00 to 3:00

2

International Finance: Tomorrow, 10.6.09

Lecture: 9:00 to 10:50Break: 10:50 to 11:00Lecture: 11:00 to 12:00Break: 12:00 to 1:00Lecture 1:00 to 3:00

3

International Finance: Thursday, 10.6.09

Lecture: 9:00 to 10:50Break: 10:50 to 11:00Lecture: 11:00 to 12:00Break: 12:00 to 1:00Lecture 1:00 to 3:00

4

International Finance

Review•Simon Johnson, Sovereign Wealth Funds•Sovereign Wealth Fund Institute•Charts, Evidence and response (end yesterday)•Charts, design flaws•FedEx example of Excel flaws, fedex.com, ARpts, 98•What is primary cause of current crisis•Which country has “largest” economic response•Stiglitz, greatest externality

5

International Finance

Review• If you believe in Efficient Markets how should you

invest?

6

International Finance

Simon Johnson, May, 2009, Atlantic, The Quiet Coup

7

International Finance

Simon Johnson, May, 2009, Atlantic, The Quiet Coup

8

International Finance

Finance joke• John Paul Getty: If you owe the bank $100, that's your

problem. If you owe the bank $100 million, that's the bank's problem.

9

International Finance

Research Topic•For guidelines see pdf file, web site, Guideline 5•Pdf file for papers with research data but still has many important ideas.•Follows McCloskey

10

International Finance

McCloskey

11

International Finance

Lehman Brothers, Barclays, Excel Errorhttp://www.itworld.com/business/56161/excel-error-gives-barclays-more-lehman-assets-it-wanted

12

International Finance

Khan Academy•Many videos•Many topics

FinanceMathPhysics

http://www.khanacademy.org/

13

International Finance

Timeline•Federal Reserve Bank of St Louis•http://timeline.stlouisfed.org/index.cfm?p=timeline

14

International Finance

Video•Charlie Rose Show•Three Economists, Princeton

Wei Xiong, Markus Brunnermeier and Harrison Hong

•14 August 2008•http://www.charlierose.com/view/interview/9221

15

International Finance

Arbitrage

16

International Finance

Arbitrage•Same or equivalent goods (financial assets),•Sold in different markets•At different prices•Buy in market where price is low•And sell in market where price is high

17

International Finance

Financial Derivatives•Forward contracts and futures contracts•Options

CallsPuts

•Swaps

18

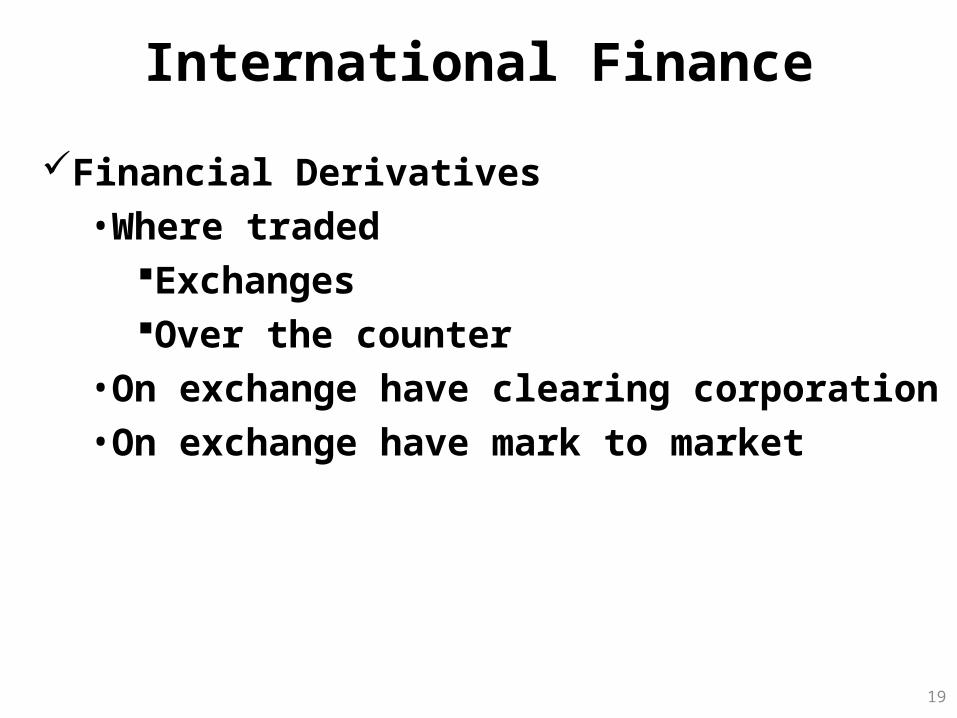

International Finance

Financial Derivatives•Where traded

ExchangesOver the counter

•On exchange have clearing corporation•On exchange have mark to market

19

International Finance

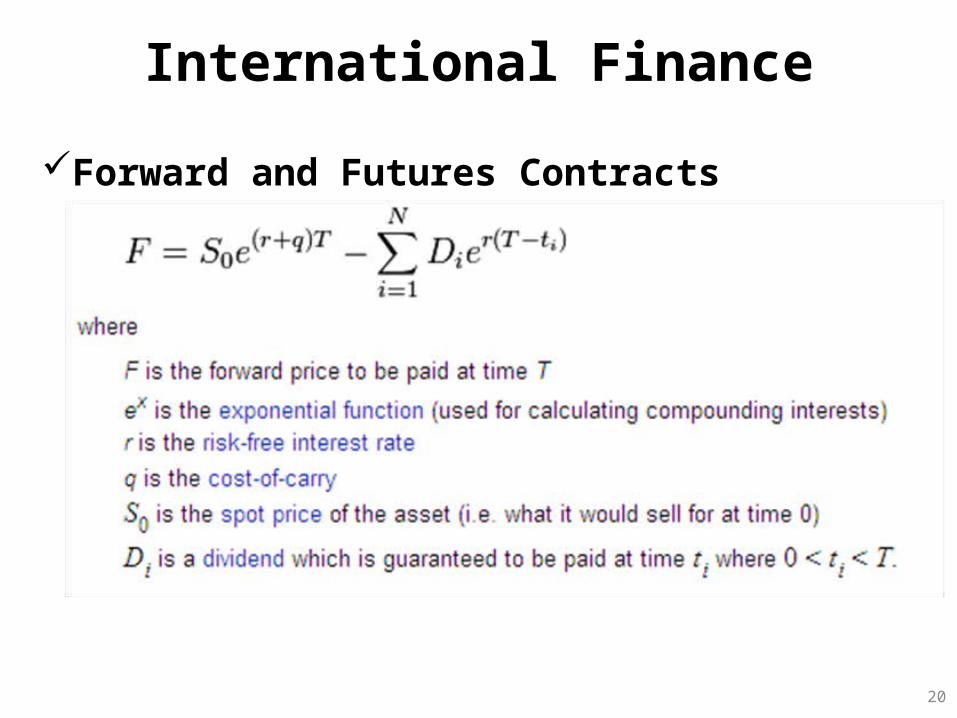

Forward and Futures Contracts

20

International Finance

Forward and Futures Contracts•If actual futures greater than mathematical relationship.

21

International Finance

Calls, Black Scholes

S = stock price, K = Exercise price, T = maturity date, t = current date, r = risk free rate, = standard deviation

22

International Finance

Calls, Arbitrage•Close to expiration•Stock price is 50•Exercise price is 45•Call option price is 4.5

You have no position, how to make money.

23

International Finance

Calls, Arbitrage•Close to expiration•Stock price is 50•Exercise price is 45•Call option price is 4.5

You have no position, how to make money•Buy Call, - 4.5•Exercise Call, - 45•Have one share (cost is 49.5), sell in market, + 50•Net gain is 0.5 (+ 50 – 49.5)

24

International Finance

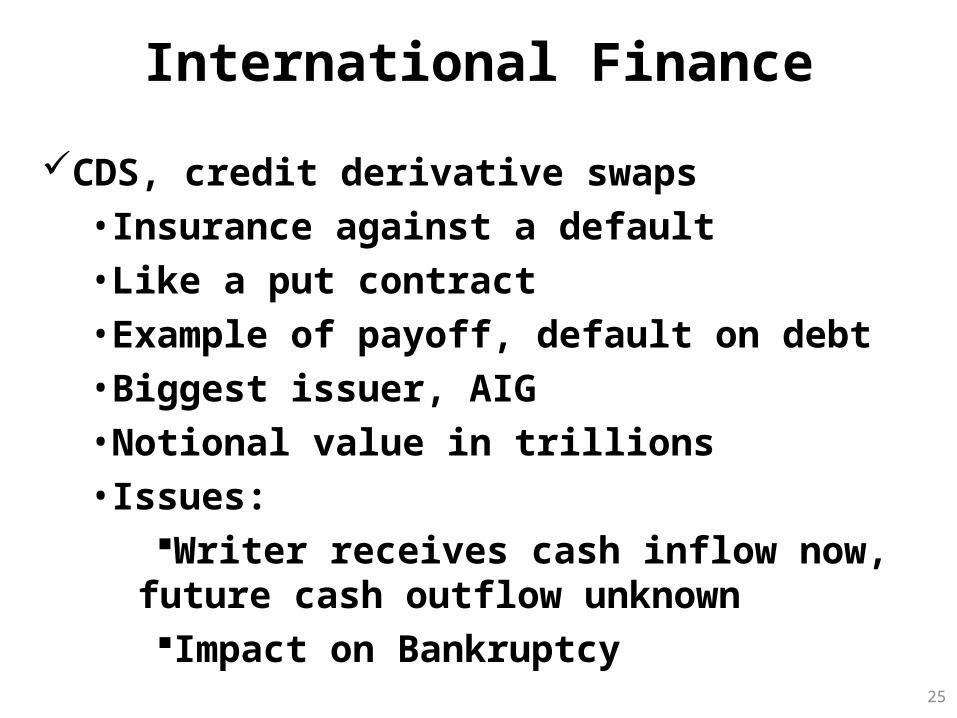

CDS, credit derivative swaps•Insurance against a default•Like a put contract•Example of payoff, default on debt•Biggest issuer, AIG•Notional value in trillions•Issues:

Writer receives cash inflow now, future cash outflow unknownImpact on Bankruptcy

25

International Finance

CDS, credit derivative swapsThe buyer of these contracts pays a periodic fixed fee in exchange for a contingent payment in the event of credit default.

Estimates of the gross notional amount of outstanding credit default swaps in 2007 range from $45 trillion to $62 trillion.

Source: Deciphering the Liquidity and Credit Crunch 2007–2008, Markus K. Brunnermeier

26

International Finance

Video•Princeton University

Hyun ShinMarkus Brunnermeier and Harrison HongPaul KrugmanAlan Blinder

•23 September 2008•http://www.youtube.com/watch?v=Wj_JNwNbETA

27

International Finance

Variance or Standard deviationCorrelation/Covariance

28

International Finance

VaR, Value at RiskIn financial mathematics and financial risk management, Value at Risk (VaR) is a widely used measure of the risk of loss on a specific portfolio of financial assets. For a given portfolio, probability and time horizon, VaR is defined as a threshold value such that the probability that the mark-to-market loss on the portfolio over the given time horizon exceeds this value (assuming normal markets and no trading in the portfolio) is the given probability level.

29

International Finance

CoVar (Tobias Adrian and Markus K. Brunnermeier)We define CoVaR as the value at risk (VaR) of financial institutions conditional on other institutions being in distress. The increase of CoVaR relative to VaR measures spillover risk among institutions. We estimate CoVaR using quantile regressions and document significant CoVaR increases among financial institutions. We identify six risk factors that allow institutions to offload tail risk and show that such hedging reduces the wedge between CoVaR and VaR. We argue that financial institutions should report CoVaR in addition to VaR, and we draw implications for risk management, regulation, and systemic risk. We define co-expected shortfall as a sum of CoVaRs.http://www.newyorkfed.org/research/staff_reports/sr348.html

30

International Finance

Repo (Repurchase Agreement)A Repurchase agreement (also known as a repo or Sale and Repurchase Agreement) allows a borrower to use a financial security as collateral for a cash loan at a fixed rate of interest. In a repo, the borrower agrees to sell immediately a security to a lender and also agrees to buy the same security from the lender at a fixed price at some later date. A repo is equivalent to a cash transaction combined with a forward contract.

31

International Finance

Repo (Repurchase Agreement, continued)The cash transaction results in transfer of money to the borrower in exchange for legal transfer of the security to the lender, while the forward contract ensures repayment of the loan to the lender and return of the collateral of the borrower. The difference between the forward price and the spot price is the interest on the loan while the settlement date of the forward contract is the maturity date of the loan.

http://en.wikipedia.org/wiki/Repurchase_agreement

32

International Finance

TED SpreadThe TED spread is the difference between the interest rates on interbank loans and short-term U.S. government debt ("T-bills").TED spread is calculated as the difference between the three-month T-bill interest rate and three-month LIBOR.The TED spread is an indicator of perceived credit risk in the general economy.http://en.wikipedia.org/wiki/TED_spread

33

International Finance

34

International Finance

Video•Bear Sterns and Financial & Economic Crisis

William CohanKate Kelly

•28 May 2009•http://www.charlierose.com/view/interview/10338

35