“international finance and payments” lecture ix “international bond market” lect. cristian...

TRANSCRIPT

“International Finance and Payments”

Lecture IX

“International Bond Market”

Lect. Cristian PĂUNLect. Cristian PĂUN

Email: Email: [email protected]

URL: http://www.finint.ase.roURL: http://www.finint.ase.ro

Academy of Economic Studies

Faculty of International Business and Economics

General Situation

CountriesWeight

Developed Countries 96,1 %

Asia 2,3 %

South America 0,8%

Eastern Europe + Africa 0,7%

International Bond Market

Types of Bonds

BondsWeight

T Bonds Peste 50 %

Corporate Bonds 30 %

Foreign Bonds 10 %

Euro Bonds 20 %

Situation by Issuing Institutions

International Bond Market

Issuing Institution Weight

Government Over 50 %

- Public Companies 30 %

Banks 10 %

Private Companies 20 %

International Institutions 12,4 %

Value Lead Manager Maturity Coupon

225 bil USD Merill Lynch 1999 9,75 %

52 000 bil ¥ Nomura Securities 1999 5,20 %

30.000 bil ¥ Nomura Securities 2001 5,05 %

600 mil DM Credit Suisse 2002 7,75 %

Romanian Experience on International Bond Market

International Bond Market

Bonds 1985 1987 1988 2000 2002

Fixed Rate Notes 53 % 63 % 70 % 71,2% 71,3%

Floating Rate Notes 41 % 11 % 10 % 25,1% 25,1%

Convertible Bonds 4 % 9 % 3 % 3,5% 3,4%

Bonds with warrant 2 % 17 % 17 % 0,1% 0,1%

LowerHigherCost

LowerHigherRisk

LowerHigherMaturity

LowerHigherVolum

Foreign currencyLocal currencyDenomination

AnywhereAnywhereInvestors

AnywhereAnywhereIssuers

Euro-BondsForeign BondsDifferences

LowerHigherCost

LowerHigherRisk

LowerHigherMaturity

LowerHigherVolum

Foreign currencyLocal currencyDenomination

AnywhereAnywhereInvestors

AnywhereAnywhereIssuers

Euro-BondsForeign BondsDifferences

Bond Issuing Mechanism - IPO

Beneficiary

Underwritting Group

Co - managers

Lead Manager BankCoordination

and/or guarantee group

Selling group

Private Investors

Step VI

Step III

Step II

Step I

Private Investors

Step VI

Step IV

Tombstone

IPO description: Step 1: Contacting a lead manager bank and this bank will create the

coordinating group (if the amount is too important) Step 2: Creating the Underwriting group that will sign up for 70% from

the total bond’s quantity with the condition of including the unsold bonds in their own portfolio;

Step 3: Creating the Selling group that will try to sell in advance the remaining 30% from the total bonds;

Step 4: Selling the bonds to private investors Step 5: Listing the bonds on capital markets, starting the secondary

market, closing operation (tombstone)

If the private investors will be not interested for IPO of bonds:- Redesigning the bonds conditions (issuing price, call price)- Road Show (promoting the IPO at the level of private investors)- Guarantee for IPO granted by lead bank (the unsubscribed bonds will

be included in its own portfolio)

Bond Definition

- Bond = a security that is issued in connection with a specific borrowing arrangement

-Bond indenture = the contract between the issuer and the borrower

- Main elements of the contract:

- Face value

- Coupon rate

- Issuing price

- Bond premium

- Bond classification:

- T-Bonds

- Municipal Bonds

- Corporate Bonds

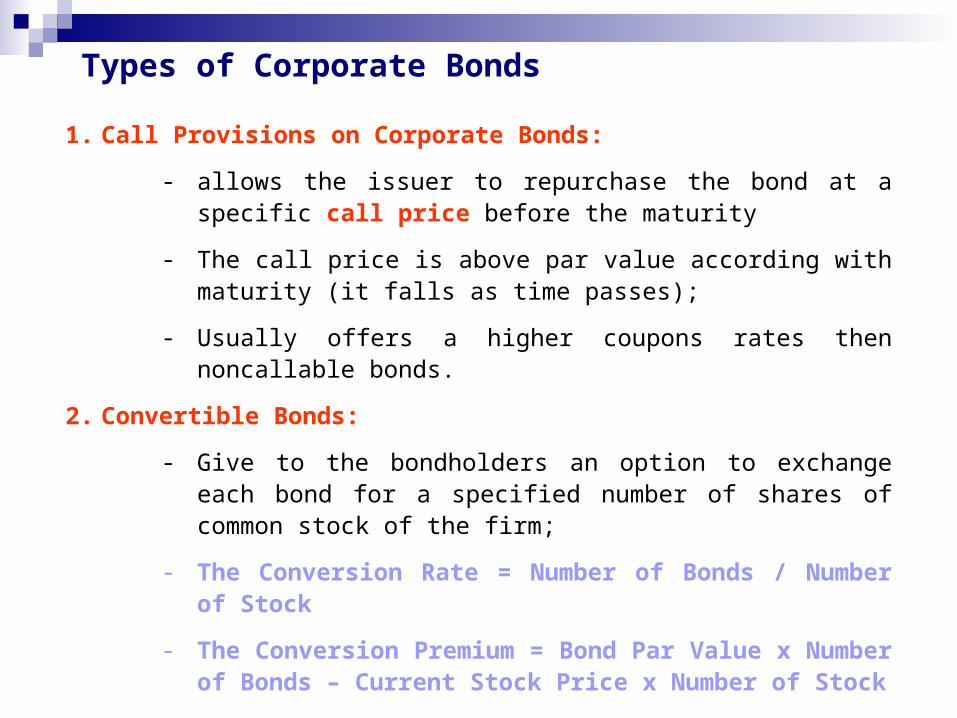

Types of Corporate Bonds

1. Call Provisions on Corporate Bonds:

- allows the issuer to repurchase the bond at a specific call price before the maturity

- The call price is above par value according with maturity (it falls as time passes);

- Usually offers a higher coupons rates then noncallable bonds.

2. Convertible Bonds:

- Give to the bondholders an option to exchange each bond for a specified number of shares of common stock of the firm;

- The Conversion Rate = Number of Bonds / Number of Stock

- The Conversion Premium = Bond Par Value x Number of Bonds – Current Stock Price x Number of Stock

Types of Corporate Bonds

3. Puttable Bonds:

- Allows the bond holder to extend or to sell bond at a specific date (call date)

- The holder is interest to extend the bond life when the bond current yield exceeds current market yields;

- When the coupon rate is too low the holder will reduce the holding period

4. Floating Rate Note:

- Make interest payments that are tied to some measure of current market rate (T-Bill rate adjusted with 4%)

- Major risk: changes in the company’s financial strength (if the financial situation will be worse the price of the bond would fall because the investor’s will require a greater yield premium than the security can offer).

Innovation in the Bond Market

• Reverse Floater Bonds: the coupon rate falls when the general interest rates

rises (the benefit of the investors is double when the rates falls – higher price

and higher interest rate);

• Asset - Backed Bonds: - issuing a bond with a coupon rate connected to the

financial performance of several firms from the same group (example: Walt

Disney, David Bowie)

• Catastrophe Bonds: - issuing a bond with a final payment that depended on

whether there a catastrophe will be produced (example: Electrolux and a

possible earthquake in Japan).

• Indexed Bonds: - make payments that are tied to a general price index or a

particular commodity price (example: Mexico issued a bond tied to the price of

oil).

Indexed Bonds: Example

Par Value 15 USD

Number 100 Bonds

Coupon 5%

Time Inflation Par Value Coupon Repayments Annuity

0 0 1500 0 0 0

1 2% 1530 76.50 0 76.50

2 3% 1575.9 78.80 0 78.80

3 1% 1591.659 79.58 1591.659 1671.24

Nominal Return=(Interest+Price Appreciation)/Initial Price

Real Return=(1+Nominal Return)/(1+Inflation)

Time Nominal Real

0 - -

1 7.10% 5.00%

2 8.15% 5.00%

3 6.05% 5.00%

Bond Value and Bond Price

Tt i)(1

ValuePar

i)(1

CouponValue Bond

Par Value 100 USDCoupon 9% paid annualy

Time 6% 7% 9% 11% 12%1 year 102.8302 101.869159 100 98.1982 97.32143

10 years 122.0803 114.047163 100 88.22154 83.0493320 years 134.4098 121.188028 100 84.07334 77.5916730 years 141.2945 124.818082 100 82.61241 75.83445

Interest Rate

00 i1

ΔiDUR

p

Δp

Bond Yields – Yield to Maturity

30

1t

130t )k1(

$100

)k1(

$9$08.22

Selling price 122.08 USDCoupon 10%Par value 100 USDMaturity 10 years

Bond Yields – Current Yield

YTM = 6 %

122.08$

9$

Price Selling

InterestYieldCurrent

Bond Yields – Yield to Call

Selling price 122.08 USDCoupon 10%Par value 100 USDMaturity 10 yearsCall Price 110 USD

30

1t

130t )k1(

$110

)k1(

$9$08.22 YTM = 6.23 %

Determinants of Bond Safety

1. Coverage Ratios: ratios of company to fixed costs

• Times – interest – earned ratio (EBIT/Interest Obligations)

• Fixed Charge Coverage Ratio (EBIT/(Interest+Lease)

2. Leverage Ratio (Debt-to-Equity Ratio)

3. Liquidity Ratios:

• Current Ratios = Current Assets / Current Liabilities

• Quick Ratios = (Current Assets – Inventories) / Current Liabilities

4. Profitability Ratios

• ROA = EBIT / Total Asset

5. Cash Flow to Debt Ratio (Cash Flow to Outstanding Debt)

Financial Ratios by Rating Classes

US Industrial Long Term Debt AAA AA A BBB BB B

EBIT interest coverage ratio 17.5 10.8 6.8 3.9 2.3 1.0

EBITDA interest coverage ratio 21.8 14.6 9.6 6.1 3.8 2.0

Funds Flow / Total Debt 105.8 55.8 46.1 30.5 19.2 9.4

Free operating cash flow / Total Debt 55.4 24.6 15.6 6.6 1.9 -4.6

Return on capital 28.2 22.9 19.9 14.0 11.7 7.2

Operating Income / Sales 29.2 21.3 18.3 15.3 15.4 11.2

Long Term Debt / Capital 15.2 26.4 32.5 41.0 55.8 70.7

Total Debt / Capital 26.9 35.6 40.1 47.4 61.3 74.6

Source: Bodie, Kane, Marcus “Investment”, page 437, McGraw-Hill Irwin, 2003