international assignment services - ahk greater...

TRANSCRIPT

International Assignment Services

PwC

Individual Income Tax Planning for Expatriates23 July 2009

Agenda

• Introduction

• IIT Planning – Revisit

• Local Incentives

• Q&A

Introduction

PwC International Assignment Services Rebecca Lai, Director

Rebecca is a tax director with 13 years of professional experience in expatriate tax compliance and advisory.

Rebecca’s specialization includes:- International assignment management- Tax effective compensation and benefit restructuring - Individual income tax consultation on equity incentive compensation- Cross-border personal taxation - Immigration services

Rebecca graduated from the University of Wisconsin – Madison in the United States of America. Rebecca is a member of the American Institute of Certified Public Accountants and an associate member of the Hong Kong Institute of Certified Public Accountants.

Slide 4PricewaterhouseCoopersJuly 2009

General Economic Environment

• Total Tax Revenue for the months from January to May 2009 reduced by 9.4% as compared to January to May 2008

• The tax collection pressure is going higher, especially during the second half of 2009

• New circulars issued to strengthen tax collection

Slide 5PricewaterhouseCoopersJuly 2009

Individual Income Tax Planning – Revisit

Slide 6PricewaterhouseCoopersJuly 2009

IIT Planning – Revisit

Non-Taxable Expatriate Benefits

Following items if directly paid by the company or structured asreimbursement of actual and reasonable expenses incurred with valid supporting receipts (“fapiao”) and documentation may qualify as non-taxable benefits:• Housing rental • Tuition fees for the employee’s dependent(s) in China• Meals and laundry• Relocation• Chinese language training for the employee• Home leave travel, limited to two round-trips per year for the employee to

his/her or the spouse’s home country or where the parents reside

Slide 7PricewaterhouseCoopersJuly 2009

Non-Taxable Expatriate Benefits – Illustration

Total package: RMB1,000,000 (annual)

IIT is RMB253,340 (tax borne by employee)

Effective tax rate is 25% (i.e. 253,340/1,000,000)

Benefit restructuring:

Base salary: RMB700,000

Housing rental reimbursement: RMB300,000

Total package: RMB1,000,000

IIT is RMB152,220 (tax borne by employee)

Effective tax rate is 15% (i.e. 152,220/1,000,000)

Tax saving: RMB101,120

Slide 8PricewaterhouseCoopersJuly 2009

Non-Taxable Expatriate Benefits – Issues to be Considered

• Documentation• Supported by fapiao• Internal policy • Actual reimbursement basis if not paid directly by the company to the third

party• Reimbursement on a monthly (periodically) basis• Accounting entries• Indemnity by the employees

Slide 9PricewaterhouseCoopersJuly 2009

Non-Taxable Expatriate Benefits – Issues to be Considered

• Would this scheme cause additional administrative burden to the company?

• Is there any competent personnel to review the fapiao submitted?• Are these genuine fapiao? • Would this scheme attract employees who are tax equalized, i.e. they are

only responsible for home country tax?• Who would be liable if this scheme is challenged by the tax bureau? who

bears the under-payment of tax, penalties or interest?

Slide 10PricewaterhouseCoopersJuly 2009

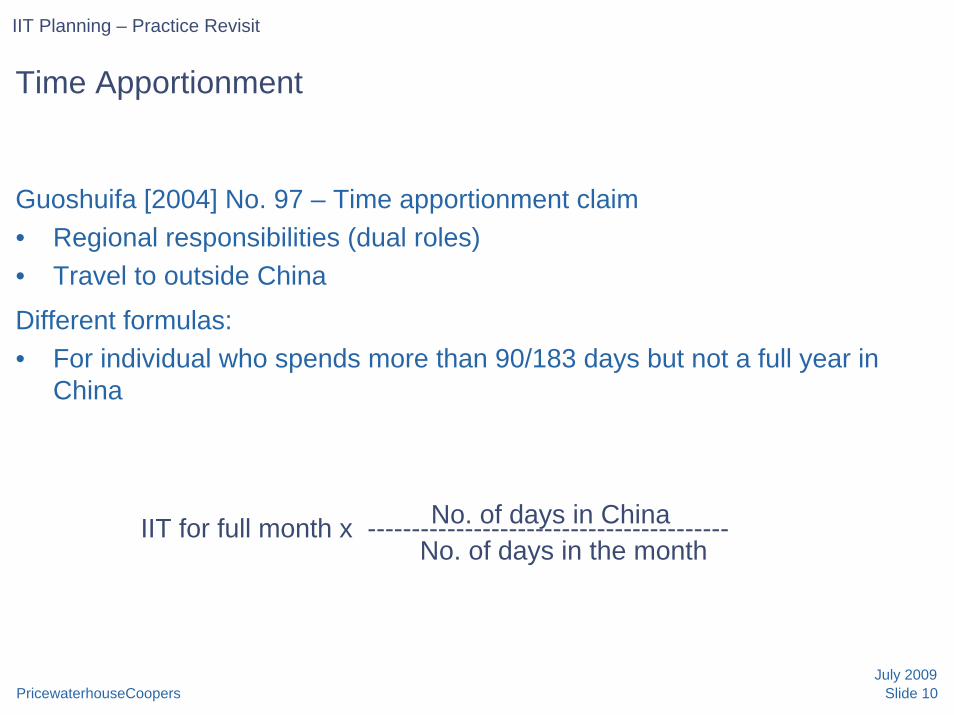

IIT Planning – Practice Revisit

Time Apportionment

Guoshuifa [2004] No. 97 – Time apportionment claim• Regional responsibilities (dual roles)• Travel to outside China

Different formulas: • For individual who spends more than 90/183 days but not a full year in

China

IIT for full month x -----------------------------------------No. of days in ChinaNo. of days in the month

Slide 11PricewaterhouseCoopersJuly 2009

Time Apportionment – Formulas

• For individual who spends not more than 90/183 days in China in a calendar year

• For individual who spends more than 1 full year but less than 5 full years in China

IIT for full month x

IIT for full month x -------------------------------------- x --------------------------------

Remuneration borne by China entity

Total remuneration for the month

Days in ChinaTotal days in the month

(1 - ---------------------------------------- x -----------------------------------------------------------)Remuneration borne by non-China entityTotal remuneration

for the month

Days outside ChinaTotal days in the month

Slide 12PricewaterhouseCoopersJuly 2009

Time Apportionment – Illustration

• Qualified for time apportionment

• Spend 20 days outside China every month

• Monthly IIT based on full month = RMB10,000

• IIT payable after time apportionment = RMB10,000 x 20/30 = RMB6,667

Slide 13PricewaterhouseCoopersJuly 2009

Time Apportionment – Issues to be Considered

• Income is NOT apportioned• Salary cost borne between

overseas and PRC entities respectively

• Dual employment arrangement (e.g. a China contract and a non-China contract) to substantiate regional responsibilities

• Tracking of travel records• Tax bureau practice

Slide 14PricewaterhouseCoopersJuly 2009

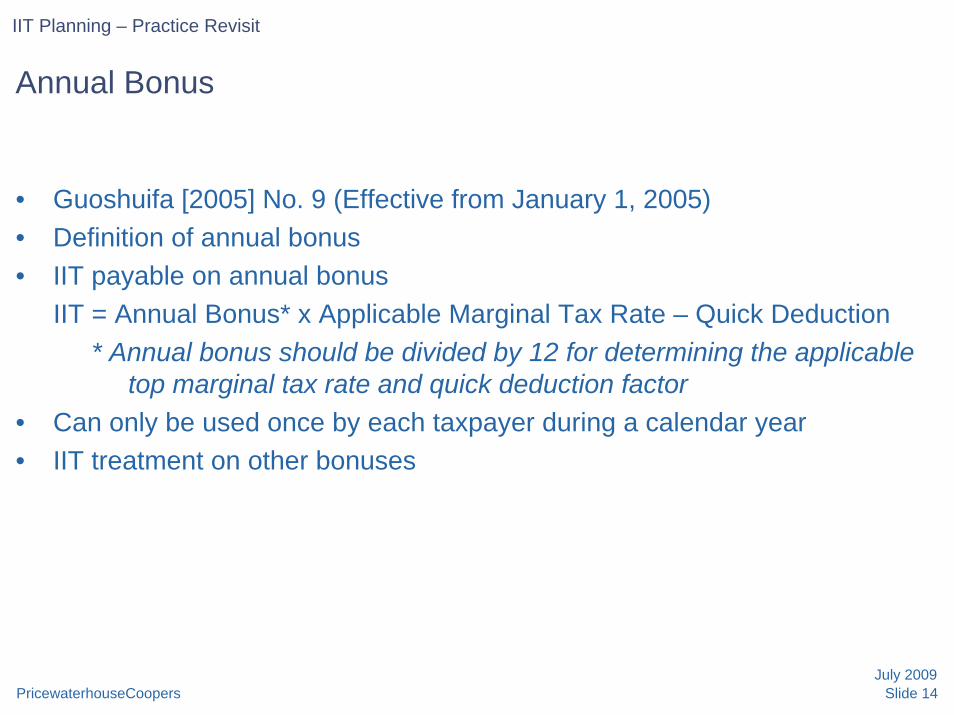

IIT Planning – Practice Revisit

Annual Bonus

• Guoshuifa [2005] No. 9 (Effective from January 1, 2005)• Definition of annual bonus• IIT payable on annual bonus

IIT = Annual Bonus* x Applicable Marginal Tax Rate – Quick Deduction * Annual bonus should be divided by 12 for determining the applicable

top marginal tax rate and quick deduction factor• Can only be used once by each taxpayer during a calendar year• IIT treatment on other bonuses

Slide 15PricewaterhouseCoopersJuly 2009

Annual Bonus – Illustration Different mix of regular salary and annual bonus amounts

Total package: RMB1,000,000 (annual)

Salary: RMB900,000 (12 monthly installments)

Annual Bonus: RMB100,000

IIT on salary: RMB218,340 (Total on 12 installments)

IIT on annual bonus: RMB19,625

Total IIT: RMB237,965

Total package: RMB1,000,000 (annual)

Salary: RMB760,000 (12 monthly installments)

Annual bonus: RMB240,000

IIT on salary: RMB170,220 (Total on 12 installments)

IIT on annual bonus: RMB47,625

Total IIT: RMB217,845

Tax difference: RMB20,120

Slide 16PricewaterhouseCoopersJuly 2009

Annual Bonus – Issues to be Considered

• Annual bonus is usually discretionary• Company salary grid will need to be

observed• Benefits calculated based on regular

salary• Can affect cash flow• Proper documentation • Be consistent with accounting records,

corporate tax deduction, etc.

Slide 17PricewaterhouseCoopersJuly 2009

IIT Planning – Practice Revisit

Company Car

• Instead of paying a transportation allowance, company leases the car and makes payments to the car leasing company directly

• Need to substantiate the business purpose of the company car

Slide 18PricewaterhouseCoopersJuly 2009

IIT Planning – Practice Revisit

Five-year Rule

• World-wide taxation from the 6th year onwards, if already spent more than 5 consecutive “full” calendar years in China

• How to break: - before the end of the 5th year, leave China for consecutive 31 days or

total 91 days- If this cannot be done:

• To have an employment outside China and not to reside in China for more than 183 days (or 90 days for non tax treaty residents) during the 6th year; or

• Leave China for consecutive 31 days or total of 91 days during the 6th year and each year thereafter so that only the income sourced in China for those years will be taxable.

Slide 19PricewaterhouseCoopersJuly 2009

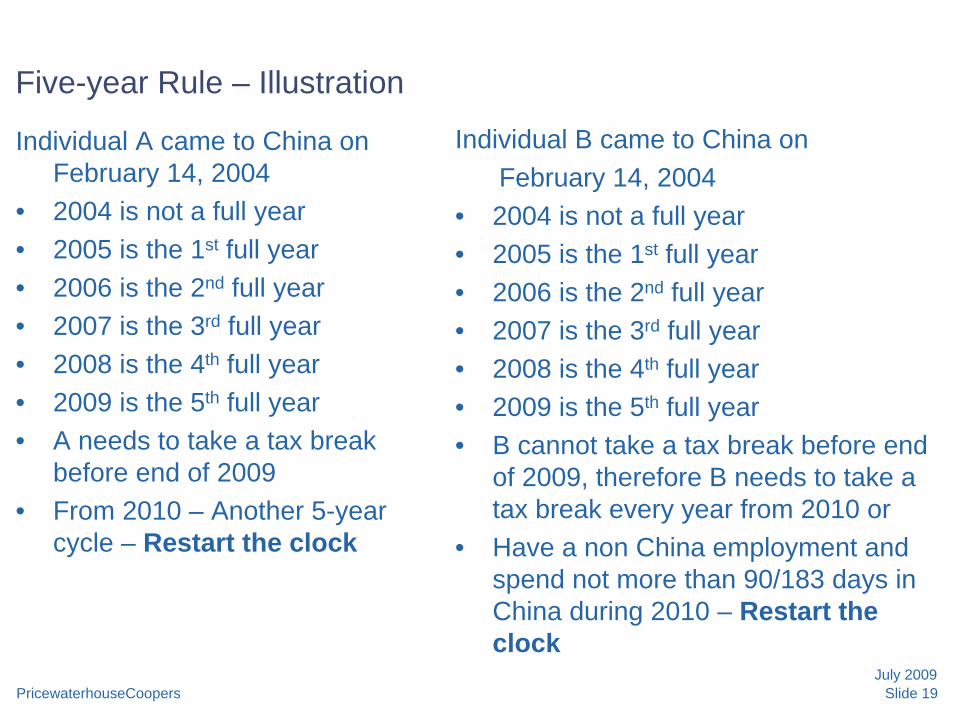

Five-year Rule – Illustration

Individual B came to China on February 14, 2004

• 2004 is not a full year• 2005 is the 1st full year• 2006 is the 2nd full year• 2007 is the 3rd full year• 2008 is the 4th full year• 2009 is the 5th full year• B cannot take a tax break before end

of 2009, therefore B needs to take a tax break every year from 2010 or

• Have a non China employment and spend not more than 90/183 days in China during 2010 – Restart the clock

Individual A came to China on February 14, 2004

• 2004 is not a full year• 2005 is the 1st full year• 2006 is the 2nd full year• 2007 is the 3rd full year• 2008 is the 4th full year• 2009 is the 5th full year• A needs to take a tax break

before end of 2009• From 2010 – Another 5-year

cycle – Restart the clock

Slide 20PricewaterhouseCoopersJuly 2009

Five-year Rule

• Impact on non China source personal passive income, e.g. interest, dividend, rental, etc.

Slide 21PricewaterhouseCoopersJuly 2009

Local Incentives

Slide 22PricewaterhouseCoopersJuly 2009

IIT Incentives in Beijing and Shanghai

Beijing (Jingzhengbanhan [2003] No. 7)

• IIT refund of up to the lesser of RMB300,000 or 80% of the IIT payment retained by the Beijing Municipality (i.e., 40% x 80%) on the purchase of one real estate property or one automobile

Shanghai (Hupufagaijingtiao [2008] No. 301)

• Senior executives of newly set up financial institutions can apply for a housing subsidy of up to RMB200,000

• Senior executives can apply for refund of up to 40% of his IIT paid in a year• Managers and professionals can apply for refund of up to 20% of his IIT

paid in a year• The incentives program will expire on December 31, 2010

Slide 23PricewaterhouseCoopersJuly 2009

IIT Incentives in Tianjin

Tianjin (different areas of the Tianjin Municipality offered various incentive programs)

Tianjin Economic and Technological Development Area (“TEDA”)

• Senior executives and technicians can apply for refund of the IIT payment retained at TEDA finance level

• Additional IIT refund can be granted to the qualified individuals who purchase real estate property in TEDA

Slide 24PricewaterhouseCoopersJuly 2009

IIT Incentives in Tianjin

Tianjin (different areas of the Tianjin Municipality offered various incentive programs)

Tianjin Binhai New Area

• Senior executives employed by the financial institutions for more than 2 years• Can apply for refund of up to the IIT payment retained by the Tianjin

Municipality on the purchase of the first real estate property or automobile, or training expenses on professional study in the Tianjin Municipality, but not more than the actual expenses paid; or

• Can apply for refund of up to 50% of the IIT payment retained by the Tianjin Municipality

Slide 25PricewaterhouseCoopersJuly 2009

IIT Incentives in Tianjin

Tianjin (different areas of the Tianjin Municipality offered various incentive programs)

Tianjin Binhai New Area

• Senior executives employed by headquarters or regional headquarters can apply for refund of up to 50% of the IIT payment retained by the Tianjin Municipality

• This incentive program took effect from January 2006 and will expire by the end of 2012.

Slide 26PricewaterhouseCoopersJuly 2009

IIT Incentives in Tianjin

Tianjin (different areas of the Tianjin Municipality offered various incentive programs)

Tianjin Hi-tech Industry Park

• Senior executives and senior technicians with an employment contract of duration for more than 5 years can apply for refund of 50% of the IIT payment for the first four years, then 100% of the IIT payment in the fifth year and simultaneously receive the 50% balance of the previous four years, as retained at the local level

• This incentive will expire on 5 December 2013

Please refer to the specific notice for details of the application procedures and requirement issued by the relevant authorities

Q&AEdmund Yang, Partner

PricewaterhouseCoopers

Direct Tel: (10) 6533 2812

Email: [email protected]

Runzhi Zhang, Manager

PricewaterhouseCoopers

Direct Tel: +86 (22) 2318 3030

Email: [email protected]

Rebecca Lai, Director

PricewaterhouseCoopers

Direct Tel: (10) 6533 3065

Email: [email protected]

Jackie Hou, Manager

PricewaterhouseCoopers

Direct Tel: +86 (22) 2318 3033

Email: [email protected]

Slide 27PricewaterhouseCoopersJuly 2009

Thanks!

© 2009 PricewaterhouseCoopers. All rights reserved. "PricewaterhouseCoopers" refers to the China firm of PricewaterhouseCoopers or, as the context requires, the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity. *connectedthinking is a trademark of PricewaterhouseCoopers.

PwC

The information contained in this presentation is for general guidance on matters of interest only and is not meant to be comprehensive. The application and impact of laws can vary widely based on the specific facts involved. Before taking any action, please ensure that you obtain advice specific to your circumstances from your usual PricewaterhouseCoopers client service team or your other tax advisers.

The materials contained in this presentation were assembled on 20 July 2009 and were based on the law enforceable and information available at that time.

.