internal control quality and information asymmetry in the secondary loan market

TRANSCRIPT

ORI GINAL RESEARCH

Internal control quality and information asymmetryin the secondary loan market

Dina F. El-Mahdy • Myung Seok Park

� Springer Science+Business Media New York 2013

Abstract We examine the association between disclosure of internal control deficiencies

(ICDs) and information asymmetry (IA) in the US secondary loan market. We also investi-

gate which types of ICDs intensify or mitigate conditions of information asymmetry in the

same market. Relying on loan syndication, loan credit rating, financial debt covenants and

loan size, we further explore the effect of loan specific characteristics on the association

between ICDs and IA. Consistent with our predictions, we find that while ICDs increase

information asymmetry in the secondary loan market, the inimitable characteristics in the

secondary loan market (e.g., syndication, loan credit rating, financial covenants, and loan

size) help to mitigate such negative consequences of the disclosure of ICDs on the firm’s

informational environment. We further find that disclosures of ICDs for firms in regulated

industries help to mitigate the negative consequences of ICDs disclosures on IA.

Keywords Disclosure of internal control deficiencies � Information asymmetry �Secondary loan market � Loan-specific characteristics

JEL Classification M41 � G10

1 Introduction

Extant literature documents an association between characteristics of the firm’s informa-

tional environment and information asymmetry among managers and investors in the

D. F. El-Mahdy (&)Earl G. Graves School of Business and Management, Morgan State University, McMechen CommerceBuilding, 1700 E. Cold Spring Lane, Baltimore, MD 21251, USAe-mail: [email protected]

M. S. ParkSchool of Business, Virginia Commonwealth University, Snead Hall, 301 W. Main Street,Box 844000, Richmond, VA 23284-4000, USAe-mail: [email protected]

123

Rev Quant Finan AccDOI 10.1007/s11156-013-0389-1

equity market (Richardson 2000; Frankel and Li 2004; Schrand and Verrecchia 2005;

Bharath et al. 2008). For example, Frankel and Li (2004) find relation between the firm’s

future profitability measures (e.g., the informativeness of financial statements, analyst

following, and news) and information asymmetry. Related, Schrand and Verrecchia (2005)

argue that greater frequency of disclosure in the pre-Initial Public Offering (IPO) period is

a tool that reduces adverse selection associated with the IPO issuance. While some studies

examine the impact of the quality of accounting information on the secondary loan market

(e.g., Wittenberg-Moerman 2008; Ball et al. 2008; Gaul and Uysal 2009; Dhaliwal et al.

2011), little research investigates the relationship between characteristics of the firm’s

informational environment and information asymmetry in the debt market, especially in

the secondary loan market.1 By examining the association between disclosure of internal

control (IC) effectiveness as a proxy for financial reporting quality and information

asymmetry in the secondary loan market, our study fills this gap in prior literature.

Our study is motivated by the following two important developments in the US firm’s

informational environment. First, the secondary loan market is vital and distinctive debt

sector in the US economy. The syndicated lending, which initiates in the secondary loan

market, differs substantially from the bilateral lending structure. In the bilateral lending

structure, once the loan is closed, the borrower is fully committed to the lender with the

annual payments of interests and principal. However, syndicated lending offers more

flexible options to borrowers because the close of the primary loan is not the only

opportunity for them to decrease the cost of borrowing (Altman and Suggitt 2000).

Ivashina and Scharfstein (2010) referred to syndicated lending, a modern form of banking,

as the ‘‘originate-to-distribute’’ model. The US legal systems, which are rooted in common

law systems, have stimulated the growth of syndicated lending because debt has histori-

cally been providing the majority of finance to business firms due to the fact that developed

economies are governed by greater legal rules that strengthen creditors’ rights (Esty and

Megginson 2003). Syndicated lending then offers great refinancing opportunity, especially

when interest rates drop significantly, as is the case of the last few years, and is considered

a highly liquid source of financing for medium and large US firms (Altman and Suggitt

2000). Additionally, global interest in the secondary loan market has been continuously

increasing due to the shift in information technology, regulatory practices, the increase in

the informationally special transactions, such as mergers and acquisition (Haubrich and

Thomson 1996), and the passage of Basel III rules in September 2010. Basell III rules

require banks to increase the quality of their capital and improve the asset management

operations. In 2010, the refinance activity constituted 70 % of the US secondary loan

issuance (Braza 2010). In the same year, the secondary loan market volume went up by

131 % compared to 2009. According to Reuters Loan Pricing Corporation (LPC), the

volume of secondary loan market in US grew from $8 billion in 1991 and to $340 billion in

the second quarter of 2009.2

Second, IC disclosures, unlike other types of corporate disclosures, exist in complex

settings under IC provisions of the Sarbanes–Oxley Act 2002 (SOX 2002, hereafter). For

example IC related provisions have been sharply criticized for being uniform across firms

of different sizes, industries and complexities (Irving II 2006). Therefore, concluding that

the consequences of the disclosure of IC on the secondary loan market are similar to those

in the equity market is unwarranted and subject to investigation. Moreover, IC disclosure

1 The secondary loan market is the place where the initial loan is sold by the primary lender (lead arranger)to multiple lenders (multiple arrangers) after the close of the primary loan.2 LPC web page: http://www.loanpricing.com/analytics/pricing_service_volume1.html.

D. F. El-Mahdy, M. S. Park

123

under SOX 2002 provides both unaudited-voluntary (section 302) and audited-mandatory

(section 404) disclosure, each section with its own unique structure differently affects the

degree of uncertainty in the equity market (Beneish et al. 2008; Kim and Park 2009).

Verrecchia (2001) argues that if one disclosure exists, it would normally link disclosure to

its economic consequences: incentives, efficiency, and endogeneity of the market process.

Thus, we are motivated to examine the efficiency of the IC disclosure in the secondary loan

market. Additionally, our study highlights the multi-dimensionality of the association

between disclosure and information asymmetry especially in the secondary market. Bus-

kirk (2012) finds that disclosure quantity is associated with lower information asymmetry

while disclosure frequency is not. In contrast, we provide empirical evidence on the

association between disclosure type and information asymmetry.

Using the average annual bid-ask spread as a proxy for information asymmetry and as a

measure of the net economic benefits of SOX 2002, we examine the association between

the disclosure of IC quality3 and information asymmetry. Specifically, there are four

primary objectives in this study. First, it examines the association between disclosure of

internal control deficiencies (ICDs), under both section 302 and section 404 of SOX 2002,

and information asymmetry (IA) in the secondary loan market. Second, it sheds some

lights into which types of ICDs, internal control material weaknesses (ICMWs) and

company-level ICDs, intensify or mitigate conditions of information asymmetry in the

secondary loan market. Third, prior studies document that among others, four loan-specific

characteristics such as number of lenders (syndication), availability of loan credit rating,

financial debt covenants and loan size are significantly associated with information

asymmetry (Lee and Mullineaux 2004; Sufi 2007; Wittenberg-Moerman 2008; Ball et al.

2008). Thus, this study explores potential moderating effect of these four loan-specific

characteristics on the association between ICDs and IA in the secondary loan market.

Finally, this study investigates whether firms that remediate or take corrective actions to

address ICDs experience a reduction in information asymmetry.

We predict that while ICDs are positively associated with information asymmetry in the

secondary loan market, some types of ICDs intensify or mitigate information asymmetry in

the secondary market. We also predict that some loan characteristics help to mitigate

conditions of information asymmetry associated with ICDs in the same market. We find

that while ICDs are positively associated with information asymmetry in the secondary

loan market, company-level ICDs and ICMWs intensify the level of uncertainty but

remediation of ICDs significantly reduces IA. Interestingly, our results show that the

secondary loan market’s inimitable characteristics such as syndication, credit rating, loan

size, and financial debt covenants mitigate the negative consequences of disclosure of ICDs

on the firm’s informational environment. We further provide evidence that disclosures of

ICDs for firms in regulated industries on average help to reduce IA.

This study contributes to our understanding of the literature in the areas of internal

controls over financial reporting as well as IA in the secondary loan market in a number of

ways. First, prior studies (e.g., Costello and Wittenberg-Moerman 2011; Kim et al. 2011)

examine the effect of ICDs on the choice of monitoring mechanism and cost of debt in the

primary loan market. In contrast, by exploiting the characteristics of the secondary loan

market, our paper incrementally contributes to prior research on the consequences of the

3 An effective IC system is defined as a system that is free from material weaknesses, whereas an ineffectivesystem is a system with one or more significant deficiencies. Quality of IC is disclosed under Sarbanes–Oxley Act 2002—IC related provisions to public registrants accompanying footnotes in various statutoryfilings such as: Item 9A of Form 10-K, Item 4 of Form 10-Q, and 8-K forms (Irving II 2006).

Internal control quality and information asymmetry

123

disclosure of IC quality on the firm’s information asymmetry in the debt market. For

example, Costello and Wittenberg-Moerman (2011) examine the impact of IC disclosure

on choice of monitoring mechanisms used by lenders. Our study differs in that it compares

the relationship between IC quality and IA under both sections 302 and 404, while Costello

and Wittenberg-Moerman (2011) focus on the association between the choice of moni-

toring mechanisms and IC material weaknesses only under section 302. In a similar vein,

focusing only on section 404 from 2005 to 2009, Kim et al. (2011) examine the cost of

debt in the primary loan market. In contrast, as an extension of Dhaliwal et al. (2011),4 our

study investigates potential different effects of IC quality under sections 302 and 404 on

information asymmetry in the secondary loan market. Second, our study contributes to

resolving the mixed evidence on the association between disclosure of material weaknesses

and cost of capital, as a proxy for information asymmetry. For example, Ashbaugh-Skaife

et al. (2009) find a positive association between the cost of capital and disclosure of

material weaknesses under sections 302 and section 404. However, Ogneva et al. (2007)

do not find such linkage under section 404. Third, unlike prior studies, we delve into the

moderating effect of the unique characteristics of the secondary loan market on the

association between ICDs (and severity rank of weaknesses) and information asymmetry.

Finally, our study has an important implication regarding the effects of the severity and

remediation of ICDs on information asymmetry in the secondary loan market.

The remainder of this paper is structured as follows. Section 2 describes literature

review and hypothesis development. Research design is discussed in Sect. 3. Section 4

presents the empirical results and Sect. 5 concludes the study.

2 Literature review and hypothesis development

2.1 Internal control disclosure under SOX 2002

The Committee of Sponsoring Organizations of the Treadway Commission (COSO 1992)

defines internal control as: ‘‘a process, effected by an entity’s board of directors, man-

agement and other personnel designed to provide reasonable assurance regarding the

achievement of objectives in the following categories: effectiveness and efficiency of

operations, reliability of financial information, and compliance with the applicable laws

and regulations.’’ By definition, there is no alternative method of preventing material

errors, fraud or both other than maintaining an effective internal control system. The main

purpose of maintaining internal control systems is to prevent, detect, and eliminate

irregularities and fraud in financial reporting (Yu and Neter 1973). Failure to detect

material weaknesses in internal controls will end up with potential restatement of financial

statements and can affect many users of financial reporting including, but not limited to,

employees, regulators, investors, and creditors. This is because accounting restatement

contributes to increased market uncertainty and information asymmetry (Nguyen and Puri

2013). History of IC systems shows that government regulations required companies to

establish systems of IC as early as 1977 (Byington and Christensen 2005; Ge and McVay

2005). The Foreign Corrupt Practices Act (FCPA) of 1977 was the first law which required

IC disclosure. The FCPA required public firms to disclose IC deficiencies when

announcing a change in auditors (Irving II 2006). However, statutory regulations that

4 Dhaliwal et al. (2011) examine the association between the disclosure of the firm’s credit spread andmaterial weaknesses disclosed under section 404 in the secondary bond market, a public debt market.

D. F. El-Mahdy, M. S. Park

123

govern the disclosure of ICs over financial reporting in the past have not been clear to SEC

registrants and in most cases were not ‘‘cost effective’’ in terms of the net benefit of these

statutory regulations to the US firm. Corporate governance failures by the onset of the

1990s reinvigorated the need for corporate reforms to address fraud. Therefore, SOX 2002

was enacted on July 30, 2002 to curb business fraud and corruption. There are two

important SOX 2002 regulations related to IC disclosure, section 302 and section 404.

SOX 2002 section 302 was issued first followed by section 404, Auditing Standard

(AS) No. 2,5 AS No. 5,6 and AS No. 7. The main purpose of the IC related provisions of

SOX 2002 is to inform investors and various stakeholders about weaknesses in the IC

structure of the firm.7 SOX 2002—Section 302 requires the CEO and CFO to certify that

the financial reports are free from material errors and weaknesses. Section 302 became

effective on August 29, 2002. Section 302 requires voluntary disclosure of ICDs as well as

management evaluation of the effectiveness of controls and procedures. However, sec-

tion 302 was not clear to either management or auditors. Management could not find clear

guidelines on how to evaluate the effectiveness of ICs. Moreover, auditors were confused

regarding whether to report the assessment of IC systems to shareholders, management, or

both. Also, under section 302, no independent audit evaluation of a firm’s ICs was

required. Section 404 became effective on or after November 15, 2004 for only accelerated

filers.8 Section 404 requires public firms to file forms 10-K and 10-Q containing an

evaluation by management of its IC. It also requires external auditors to provide an opinion

regarding the management assessment of IC on an annual basis.

Following the issuance of section 404, the SEC established the Public Company

Accounting Oversight Board (PCAOB) to provide oversight for the implementation of

section 404. Subsequently, PCAOB issued AS No. 2 followed by AS No. 5: ‘‘An Audit of

Internal Control over Financial Reporting (ICFR) Performed in Conjunction with an Audit

of Financial Statements’’, establishing the rules for auditor attestation of firms’ ICs. Sec-

tion 404 imposes a burden on SEC registrants and carries costs and benefits to the US firm.

For example, Engel et al. (2007) find that section 404 has increased the frequency with

which firms are going private to avoid the costly consequences of being a public firm.

Moreover, section 404 imposes substantial cost to large-size firms. In 2003, the initial

estimation by SEC of the financial burden associated with section 404 was approximately

($91,000) per firm (Bedard 2006). Section 404 has thus been called the section of unin-

tended consequences (Gupta and Nayar 2006).

5 The Public Company Accounting Oversight Board (PCAOB) issued AS No. 2 (PCAOB 2004): ‘‘An Auditof Internal Control over Financial Reporting Performed in Conjunction with an Audit of Financial State-ments’’. AS No. 2 was issued following the issuance of SOX 2002—section 404 to assist auditors in issuingan opinion on the effectiveness of their public company clients’ internal control. It provides new detailedresponsibilities and extensive procedures on both auditors and their clients (public firms). It further dif-ferentiates between the external auditors’ and management’s responsibilities regarding evaluating andreporting internal control material weaknesses.6 The PCAOB released Auditing Standard No. 5 (PCAOB 2007): ‘‘An Audit of Internal Control Over FinancialReporting That Is Integrated with An Audit of Financial Statements-and Related Independence Rule and Con-forming Amendments’’—to amend the previously issued AS No. 2. AS No. 5 is issued to provide additionalclarity, direct the external auditors’ focus on the most important matters in auditing the internal control overfinancial reporting, and further eliminate unnecessary audit work previously stipulated by AS No. 2.7 Prior to IC disclosures (section 302 and section 404) related to SOX 2002, disclosure of internal controlwas only required when changing auditors (Haron et al. 2010).8 On July 1, 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act (the Dodd-Frank Act)was enacted and permanently exempted non-accelerated filers from section 404(b); however, non-acceler-ated filers are still required to comply with Section 404(a).

Internal control quality and information asymmetry

123

2.2 Information asymmetry in the secondary loan market

The basic structure of the syndicated loan consists of the borrower (e.g., corporation), lead

bank (lead arranger) and followers (multiple arrangers). Syndicated lending is beneficial to

both lenders and borrowers in the US market. For example, syndicated loans are cheaper

because they provide borrowers access to capital and are more flexible than borrowing

from one lender. Lenders benefit from syndicated loans because they can easily transfer the

risk of the loans by syndicating them to multiple lenders. Syndicated loans are attractive to

junior lenders because they can easily syndicate the loans to senior lenders to diversify

credit risk and facilitate geographic and institutional sharing of risk for banks or multiple

lenders (Gadanecz 2004). Moreover, syndicated lending eliminates the costs associated

with bond issuance, disclosure and marketing fees.

Syndicated lending offers a wide array of information (e.g., the reputation of the

arranger of the syndication, various types of loans with different maturities, purposes, and

characteristics) not traditionally offered in the equity market (Wittenberg-Moerman 2008).

The secondary loan market features two types of traders: informed and uninformed traders.

Informed traders usually possess more information than uninformed traders, creating an

adverse selection problem.9 For example, Aboody and Lev (2000) find that insiders with

knowledge of their firm’s R&D expenditures may profit from this private information.

Information asymmetry in the syndicated lending exists because the lead arranger has

privileges over other syndicate arrangers such as: a priority to other claims on the firms’

assets, and imposes restrictive covenants on the firm (Allen and Gottesman 2006; Wit-

tenberg-Moerman 2008). Information asymmetry of this nature affects the loan value,

interest rates, maturities, covenants and other aspects of the contract. Using a sample of

syndicated loans from 1993 to 2004, Ivashina (2009) finds that asymmetric information

arising from the lead bank’s share of the loan ends up with significant economic cost to the

borrower and accounts for 4 % of the total cost of credit, after accounting for the reputation

of the lead bank and other determinants of information asymmetry.

To the extent that the loan is risky, lead arranger will try to retain a small portion of the

loan and syndicate the remainder in the secondary loan market, thereby reducing his/her

exposure to risk. The existence of information asymmetry in the secondary loan market is

undesirable and affects the total demand and supply of loans in the market. Moreover,

Angbazo et al. (1998), Richardson (2000), and Kim and Park (2009) argue that information

asymmetry is a sign of market imperfection.

2.3 Disclosure of ICDs and information asymmetry

Prior studies that investigate the relationship between disclosure quality and cost of capital

as a proxy for information asymmetry extend from pre-SOX 2002 (Botosan 1997; Francis

et al. 2004, 2005; DeBoskey and Gillett 2013) to post-section 404 (Ogneva et al. 2007,

Kim et al. 2011; Costello and Wittenberg-Moerman 2011). The primary purpose of this

9 Adverse selection is a situation where buyers and sellers have different information about the sameproduct. Ivashina (2009) argue that adverse selection problem in the syndicated lending is due to the leadbank’s incentives to syndicate high risk loans. Also, a moral hazard problem exists because of the leadbank’s less rigorous monitoring incentives after selling high risk loans. Although the lead bank resells theloan after its closing, the lead bank still responsible for monitoring the borrower. When lead bank retainlarger portion of the loan, the loan is less syndicated, the information asymmetry between lead bank andparticipants is expected to go down because participant bank will demand lower premium.

D. F. El-Mahdy, M. S. Park

123

stream of research is to serve as an intermediate step towards understanding the ex ante

impact of disclosure quality on investor’s welfare and hence the economy (Gao 2010).

Botosan (1997) finds no relation between disclosure and the cost of capital in the pre-

SOX 2002 period and same results are confirmed by Ogneva et al. (2007) under SOX 2002,

section 404. In contrast, other stream of research provides evidence that poor financial

reporting quality increases cost of capital and information asymmetry. For example,

Francis et al. (2004, 2005) find that firms with good earnings quality enjoy lower cost of

capital and cost of debt relative to firms with poor earnings quality. In a similar vein,

Brown and Hillegeist (2007) findings suggest that quality of disclosure associated with

annual reports and investor relations activities are negatively associated with information

asymmetry. Bushee et al. (2010) find that as an information intermediary, business press

plays an important role in reducing information asymmetry. DeBoskey and Gillett (2013)

document that greater disclosure transparency is associated with lower cost of debt capital

and better credit rating. Wittenberg-Moerman (2008) also provides evidence that timely

loss recognition reduces information asymmetry in the secondary loan market.

Kim et al. (2011) and Costello and Wittenberg-Moerman (2011) find that disclosure of

ICDs affects loan monitoring mechanism and increases loan pricing. Moreover, disclosure

of ICDs signals incremental risk to the market, thereby increasing uncertainty (Beneish

et al. 2008). In the loan market, ICDs increase uncertainty through increasing interest rate

because the disclosure of ICDs makes lenders distrust debt covenants and replace them

with higher interest rates (Jensen and Meckling 1976; Myers 1977; Costello and Witten-

berg-Moerman 2011). This higher uncertainty leads to higher information asymmetry due

to the informational privilege given to managers versus lenders (see Costello and Wit-

tenberg-Moerman 2011). We therefore predict a positive significant association between

the disclosure of ICDs and IA under both section 302 and section 404 (H1) as follows:

H1 In the secondary loan market, ICDs under both Sections 302 & 404 are positively

associated with information asymmetry.

2.4 Ranks of ICDs and information asymmetry

ICDs can be classified into two main subgroups in terms of the severity rank of weak-

nesses: (1) in order of decreasing severity: ICMWs, significant deficiencies, and control

deficiencies; (2) according to the scope of the weaknesses: company-level (CL) and

account-specific (AS) weaknesses. The first classification of ICDs was discussed in AS No.

2. Unspecified or control deficiencies have been defined by AS No. 2 as those deficiencies

resulting from a lack of operational control that hinders management or employees from

preventing or detecting misstatements in a timely manner. A significant deficiency indi-

cates that there is a remote likelihood that a more than inconsequential misstatement of the

firm’s financial statement will not be either detected or prevented. If there is more than a

remote likelihood that a material misstatement will not be prevented or detected, then the

significant deficiency is classified as a material weakness. Hammersley et al. (2008) find

that the market reacts to the disclosure of significant deficiencies and material weaknesses,

but they did not detect the same reaction to the disclosure of control deficiencies.

The second classification of ICDs is used by both academicians and practitioners (AS

No. 2; PCAOB; Moody’s 2004; Ettredge et al. 2006). CL internal control issues are those

weaknesses that impact a wide range of general control issues (e.g., the audit committee,

risk assessment, revenue recognition, and the internal audit function). AS weaknesses are

Internal control quality and information asymmetry

123

those that affect a narrow activity inside the IC system such as account-specific balances

(e.g., inventory, accounts payable, accounts receivable). Prior literature provides evidence

that disclosure of severe types of ICDs would increase the cost of debt and hence infor-

mation asymmetry. For example, Gupta and Nayar (2006) contend that disclosure of

ICMWs may lead banks and short-term lenders to distrust the collateral potential of the

borrowing firms’ financial assets. Moody’s Investor Service (2004) and Fitch Ratings

(2005) also claim that material weaknesses might trigger debt rating changes which in turn

increase the probability of default as well as borrowing costs.

Prior research suggests that firms with company-level IC weaknesses have less accurate

analysts forecasts and upward bias among financial analysts (Xu and Tang 2012), thereby

paying significantly higher loan prices (Kim et al. 2011), are associated with lower accrual

quality (Doyle et al. 2007b), and significant negative stock returns for accelerated filers

under section 302 (Beneish et al. 2008). However Beneish et al. (2008) find that non-

accelerated filers are having significant negative stock returns under both company-level

and account specific weaknesses. Overall, the more severe the IC weakness, the more

likely investors will experience higher information asymmetry. In this case, the disclosure

of severe types of ICDs will be perceived by uninformed traders as a sign of increased

uncertainty about the firm’s future growth and profitability and would stimulate unin-

formed traders to seek more private information to reduce that asymmetry. Therefore, we

predict that, in the secondary loan market, the company-level ICDs are more likely to lead

to higher information asymmetry than account-specific ICDs. Based on this conjecture, we

posit our second hypothesis as follows:

H2a In the secondary loan market, ICMWs under both sections 302 & 404 increase

information asymmetry.

H2b In the secondary loan market, company-level ICDs under both sections 302 & 404

are more likely to increase information asymmetry than account-specific ICDs.

2.5 Effect of secondary loan market characteristics on the association between ICDs

and information asymmetry

The secondary loan market offers distinctive information (e.g., number of lenders, repu-

tation of arrangers, various types of loans with different maturities, purposes, and char-

acteristics) not traditionally offered by the equity market (Sufi 2007; Wittenberg-Moerman

2008). Among the loan specific characteristics of interest to our study are the number of

lenders or syndication, availability of loan credit rating, loan size, and existence of debt

covenants. Recent studies find that these four loan-specific characteristics have negative

statistical association with information asymmetry (Lee and Mullineaux 2004; Sufi 2007;

Wittenberg-Moerman 2008; Ball et al. 2008).

2.5.1 Syndication

Syndication is the process of reselling the loan to multiple lenders to diversify the credit

risk by the lead bank/arranger. Sufi (2007) finds that the lead arranger retains a larger share

of the loan when the borrower needs thorough monitoring and due diligence. Alternatively,

Kim and Song (2011) find that the lead arranger retains a smaller percentage of the

syndicated loan of borrowing firms when the latter are audited by Big 4 auditors. Further,

D. F. El-Mahdy, M. S. Park

123

when information asymmetry between the borrower and lead arranger is high, the lead

arranger and participant lenders try to be as close as possible (geographically) to the

borrower (Sufi 2007). That is, syndication is more likely to be concentrated when the

information available about the borrower is very poor (Lee and Mullineaux 2004). How-

ever, from the borrower’s point of view, loan syndication to a large number of lenders

makes the loan more costly to restructure and hence increases the probability of loan

default (Esty and Megginson 2003).

Kim and Song (2011) assert that the effect of audit quality on syndication structure

lessens when the lender collects more information about the borrower to alleviate infor-

mation asymmetry. Ball et al. (2008) argue that the proportion of the loan held by the lead

arranger is dependent on the increasing adverse selection and moral hazard problems

created by information asymmetry. Taken together, evidence from prior literature suggests

that higher borrower’s opacity is a key factor contributing to less loan syndication or lesser

number of syndication and higher cost of capital. This suggests that relatively higher

number of syndication is an indication of low information asymmetry. We therefore expect

that loan syndication is likely to alleviate the effect of ICDs on information asymmetry in

the secondary loan market.

2.5.2 Loan credit rating

Independent credit rating agencies provide credible information about company perfor-

mance and thus help reduce the asymmetric information between the lead arranger and

borrower (Ball et al. 2008). Likewise, loan credit rating motivates trading on loans because

it expresses an opinion of default risk. When firms have high default probability, the loan is

more concentrated and less syndicated (Lee and Mullineaux 2004). Ball et al. (2008)

document that availability of loan credit ratings moderate the relationship between debt

contracting value and the percentage of the loan retained by the lead arranger. Wittenberg-

Moerman (2008) provides clear evidence that loans with an available credit rating are

associated with lower bid-ask spreads. We therefore predict that the existence of loan

credit rating contributes to a decrease in information asymmetry and helps lessen the

negative impact of disclosure of ICDs in the secondary loan market.

2.5.3 Financial debt covenants

Theoretically, financial debt covenants should mitigate the asymmetric information

because they restrict earnings manipulation and hence provide reliable and quality financial

reporting, which decreases asymmetric information. However, According to the debt

covenant hypothesis, which underlies the Positive Accounting Theory (Watts and Zim-

merman 1986), firms are more likely to shift the future earnings to current period if they

are closer to compromise their debt covenants. Related, Dichev and Skinner (2002) provide

evidence that management is more likely to manipulate earnings when they are about to

violate debt covenants. Bradley and Roberts (2004) argue that bond yield is lower when

there are debt covenants in the loan contract. They also suggest that high growth firms with

high information asymmetry are more likely to have covenants to restrict their use of

funds. Syndicated lending is more likely to have rigid financial debt covenants due to the

importance of syndicated lending as a major source of finance. Hence, we conjecture that

existence of debt covenants mitigates the impact of ICDs on information asymmetry in

secondary loan market.

Internal control quality and information asymmetry

123

2.5.4 Loan size

Wittenberg-Moerman (2008) argues that loan size is a proxy for the quality of the firm’s

informational environment. Jones et al. (2005) and Wittenberg-Moerman (2008) also find

empirical evidence on the significant negative association between loan size and infor-

mation asymmetry. Lenders are more capable to monitor firms with large loans due to the

resources offered by these firms, which are big in size by definition. Hence, cost of

monitoring and information asymmetry would be lower in such firms. Loan size of deals in

the syndicated lending is very important for successful syndication process. Unlike smaller

loans, big loans are more likely to syndicate to multiple lenders. Therefore, we expect loan

size to moderate the negative consequences of disclosure of ICDs or ICMWs on infor-

mation asymmetry. Taken together, we use the four unique syndicated loan-characteristics

(syndication, financial covenants, debt rating, and loan size) as a mediator to mitigate the

positive significant association between information asymmetry and IC weaknesses, and

hypothesize as follows:

H3a In the secondary loan market, loan specific characteristics, such as syndication, loan

credit rating, loan size, and debt covenants mitigate the positive association between ICDs

and information asymmetry.

H3b In the secondary loan market, loan specific characteristics, such as syndication, loan

credit rating, loan size, and debt covenants mitigate the positive association between

ICMWs and information asymmetry.

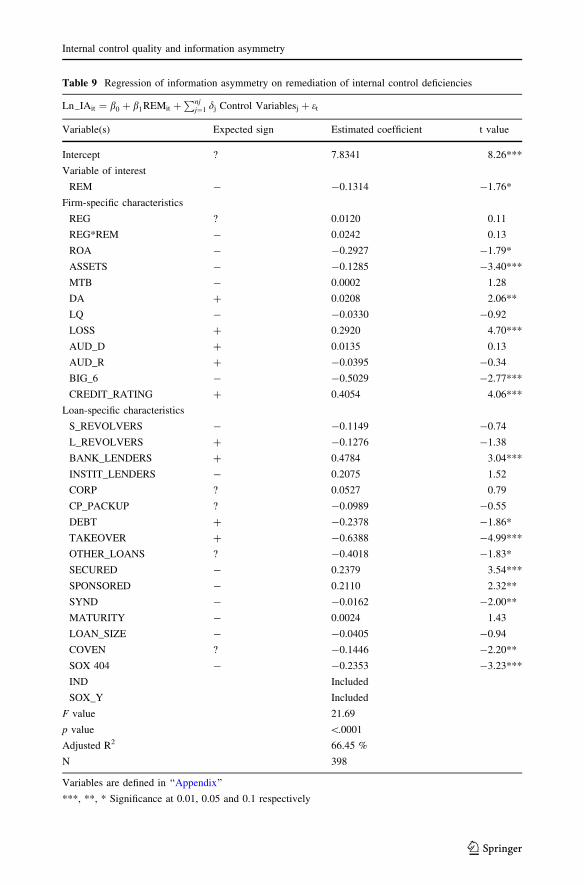

2.6 Remediation of ICDs and information asymmetry

Gupta and Nayar (2006) argue that documented negative stock price reaction to voluntary

disclosure of material weakness is mitigated when the disclosing firms also report reme-

diation action to resolve disclosed material weaknesses. In a related study, Ashbaugh-

Skaife et al. (2008) report that firms improving their IC systems show a significant increase

in the quality of financial statements. Kim et al. (2011) document that remediating IC

weaknesses significantly reduces cost of bank loans while Costello and Wittenberg-

Moerman (2011) find no pricing effect from remediation. We therefore are interesting in

resolving the conflicting evidence regarding the impact of remediating ICDs in the sec-

ondary loan market. We expect a negative association between remediation of ICDs and

information asymmetry in the secondary loan market. In other words, firms that take

corrective actions to fix IC weaknesses are more likely to reduce uncertainty among

uninformed traders and resolve asymmetric information regarding IC weaknesses. Based

on these discussions, our fourth hypothesis is as follows:

H4 In the secondary loan market, remediation of ICDs under both sections 302 & 404

decreases information asymmetry.

3 Research design

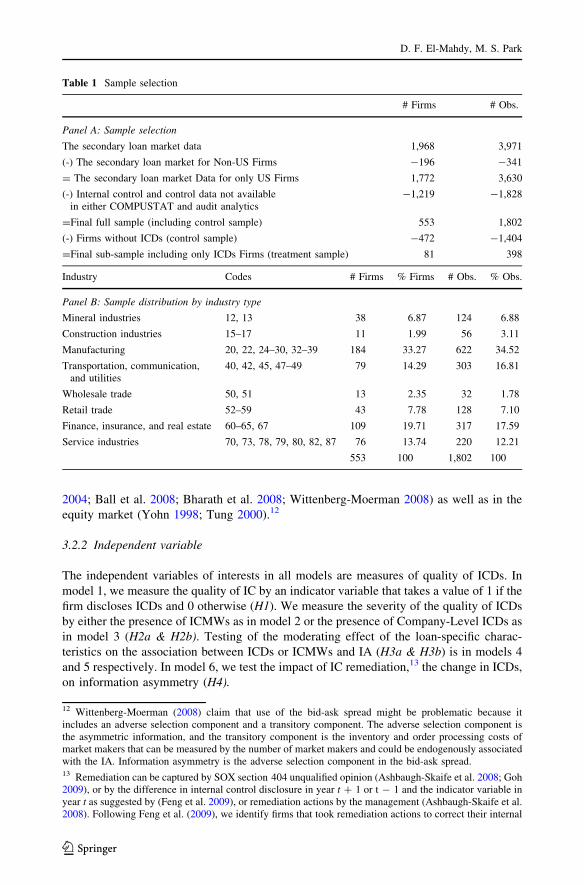

3.1 Sample size and selection

Our sample period covers only 4 years from 2002 to 2005 because of limited access to the

secondary loan market data post 2005. We obtain data pertaining to IC from AUDIT

D. F. El-Mahdy, M. S. Park

123

ANALYTICS (AA). We further obtain data for information asymmetry (Bid-Ask Spread)

and loan-specific characteristics from Loanware database.

We start with 3971 firm-year facilities10 or observations of secondary loan data. We

delete 341 firm-year observations pertaining to non-US firms. The remaining sample is

comprised of 3630 firm-year observations for US firms from 2002 to 2005. We manually

insert the key identifiers (e.g., CUSIP and CIK) to the secondary loan market data to

facilitate merging with COMPUSTAT and AA. Using discretionary accruals data from

COMPUSTAT, we estimate discretionary accrual according to Dechow, Sloan, and

Sweeney (1995); we further winsorize discretionary accruals data at 10 %. We only

include disclosure control data for accelerated filers firms (firms with more than $75

million market capitalization). We obtain data on audit characteristics such as, auditor

name, auditor resignation, and auditor dismissal from AA. We also obtain the control

variables such as: ROA, MTB, ASSETS,11 and LOSSES firms from COMPUSTAT. We

merge the IC data with the control variable data and audit characteristics data. The final

sample is composed of 533 firms and 1802 firm-years facilities/observations.

Our final sample represents a wide variety of sectors in the economy. Table 1 (panel B)

lists sample firms by industry category. Almost one-third, 184 (or 33.27 %) of our sample

firms are manufacturing firms. 109 firms (19.71 %) were in finance, insurance, and real

estate sector, while 79 firms (14.29 %), almost a fifth of our sample, are in transportation,

communication and utilities sector. Other sectors were represented as follows; service

industries 76 firms (13.74 %), retail trade 43firms (7.78 %), mineral industries 38 firms

(6.87 %), wholesale trade 13 firms (2.35 %), and construction industries 11 firm (1.99 %).

3.2 Research models

We use multivariate analysis regression to examine the association between ICDs and IA

in the secondary loan market. The dependent variable in our models is IA as measured by

the difference between the average annual bid and ask spread of the traded facility. The

independent variables are various measures of quality of ICFR as variables of interest in

addition to a set of control variables. We also classify ICDs into different types of

weaknesses, in terms of severity such as ICMWs and Company-Level IC and examine the

impact of the remediation of IC weaknesses on information asymmetry. Taken together,

we measure ineffective IC by the presence of ICDs under sections 302 and 404. We

measure ineffective IC using both the level of severity of a deficiency and the change in the

level of deficiency (the remediation actions) to address the economic consequences of the

disclosure of IC weaknesses.

3.2.1 Dependent variable

Our dependent variable in all empirical models is IA as measured by the average annual

bid-ask spread. Verrecchia (2001) defines IA as ‘‘the difference in the cost of capital in the

presence versus absence of an adverse selection problem that arises from information

asymmetry (p. 171).’’ Similarly, IA in the secondary loan market can be defined as the ex-

ante quality, and/or quantity of differential information between borrowers and lenders or

among lenders themselves. The bid-ask spread has been used extensively in prior studies

that examine information asymmetry in the secondary loan market (e.g., Frankel and Li

10 Facility is a loan granted to a firm. A firm might have a number of facilities during one accounting period.11 We used the log transformation for key variables such as: Assets and Loan size.

Internal control quality and information asymmetry

123

2004; Ball et al. 2008; Bharath et al. 2008; Wittenberg-Moerman 2008) as well as in the

equity market (Yohn 1998; Tung 2000).12

3.2.2 Independent variable

The independent variables of interests in all models are measures of quality of ICDs. In

model 1, we measure the quality of IC by an indicator variable that takes a value of 1 if the

firm discloses ICDs and 0 otherwise (H1). We measure the severity of the quality of ICDs

by either the presence of ICMWs as in model 2 or the presence of Company-Level ICDs as

in model 3 (H2a & H2b). Testing of the moderating effect of the loan-specific charac-

teristics on the association between ICDs or ICMWs and IA (H3a & H3b) is in models 4

and 5 respectively. In model 6, we test the impact of IC remediation,13 the change in ICDs,

on information asymmetry (H4).

Table 1 Sample selection

# Firms # Obs.

Panel A: Sample selection

The secondary loan market data 1,968 3,971

(-) The secondary loan market for Non-US Firms -196 -341

= The secondary loan market Data for only US Firms 1,772 3,630

(-) Internal control and control data not availablein either COMPUSTAT and audit analytics

-1,219 -1,828

=Final full sample (including control sample) 553 1,802

(-) Firms without ICDs (control sample) -472 -1,404

=Final sub-sample including only ICDs Firms (treatment sample) 81 398

Industry Codes # Firms % Firms # Obs. % Obs.

Panel B: Sample distribution by industry type

Mineral industries 12, 13 38 6.87 124 6.88

Construction industries 15–17 11 1.99 56 3.11

Manufacturing 20, 22, 24–30, 32–39 184 33.27 622 34.52

Transportation, communication,and utilities

40, 42, 45, 47–49 79 14.29 303 16.81

Wholesale trade 50, 51 13 2.35 32 1.78

Retail trade 52–59 43 7.78 128 7.10

Finance, insurance, and real estate 60–65, 67 109 19.71 317 17.59

Service industries 70, 73, 78, 79, 80, 82, 87 76 13.74 220 12.21

553 100 1,802 100

12 Wittenberg-Moerman (2008) claim that use of the bid-ask spread might be problematic because itincludes an adverse selection component and a transitory component. The adverse selection component isthe asymmetric information, and the transitory component is the inventory and order processing costs ofmarket makers that can be measured by the number of market makers and could be endogenously associatedwith the IA. Information asymmetry is the adverse selection component in the bid-ask spread.13 Remediation can be captured by SOX section 404 unqualified opinion (Ashbaugh-Skaife et al. 2008; Goh2009), or by the difference in internal control disclosure in year t ? 1 or t - 1 and the indicator variable inyear t as suggested by (Feng et al. 2009), or remediation actions by the management (Ashbaugh-Skaife et al.2008). Following Feng et al. (2009), we identify firms that took remediation actions to correct their internal

D. F. El-Mahdy, M. S. Park

123

3.2.3 Control variables

We control for a wide set of variables in all regression models to avoid having omitted

correlated variables. This increases the internal validity of our results, and enables the external

validity (generalization) of the research outcomes. For example, we control for firm-specific

characteristics (e.g., ROA, loss, profitability, firm size, growth, industry, credit rating), loan-

specific characteristics (e.g., types of loans, maturity, loan credit rating, number of lenders, loan

size, debt covenants, purpose of loans), regulations (e.g., SOX 2002—IC related provisions,

regulated industries), the interaction terms between regulated industries and internal control

measures as well as loan-specific characteristics, financial reporting quality (e.g., accounting

accruals, Big 614 audit firms, auditor change ‘‘resignation and dismissal’’), and determinants of

the bid-ask spread (e.g., liquidity as measured by amount or volume of stock traded).

We use Big 6 audit firms instead of Big 4 because after the passage of SOX 2002, big

audit firms have been continuously calling for more protection to reduce their litigation

risk. This call is not only restricted to Big 4 audit firms, namely, KPMG, Deloitte, Ernst

and Young, PricewaterhouseCoopers, but also extends to other non-Big 4 firms such as the

second-tier audit firms: BDO Seidman and Grant Thornton (Blokdijk et al. 2006). Fur-

thermore, Big 4 audit firms rejected risky firms post SOX 2002, and these risky firms

selected the next two largest audit firms (Turner 2010). Overall, the second-tier audit firms

are of increased value post SOX 2002 because they probably provide quality services and

lower cost relative to Big 4 firms.

3.2.4 Firm-specific characteristics

Firm specific characteristics include firm size, MTB ‘growth ratio’, ROA, credit rating,

profitability, and loss. For example, firms with debt are characterized by fewer growth

opportunities as implied by the pecking order theory (Bharath et al. 2008). Brown and

Hillegeist (2007) find the effect of disclosure quality on information asymmetry varies

across firms, industries and even within firms (quarterly versus annual reports).

3.2.5 Loan-specific characteristics

Wittenberg-Moerman (2008) and Sufi (2007) find that loans of profit, public firms with

available credit ratings, or syndicated by reputable arrangers are traded at low bid-ask

spreads. Likewise, Wittenberg-Moerman (2008) finds that distressed loans, revolver loans,

and loans issued by institutional investors are traded at high bid-ask spread. While we do

not have access to the reputation of the arranger, we include other available variables such

Footnote 13 continuedcontrol deficiencies. We only include firms that took serious steps to correct their internal control defi-ciencies. For example, in period t - 1, a firm might disclose internal control deficiencies related to com-petency of their human resources, merger and acquisition and foreign-related issues. In period t, the samefirm might disclose internal control deficiencies related to only merger and acquisition. In this latter case, thefirm partially remediated their internal control deficiencies and we consider this case ‘‘remediation’’.Alternatively, in period t, the firm might disclose effective internal control system and in this case, the firmfully remediated their internal control deficiencies and we considered this case ‘‘remediation’’. Althoughthere could be some firms in the process of remediating their internal control deficiencies that include suchstatements in their financial statements to outsiders, such disclosed intent to correct ICDs was not recognizedas remediation.14 The Big-6 audit firms include: Deloitte, KPMG, Ernst & Young, PricewaterhouseCoopers, BDO Seidmanand Grant Thornton.

Internal control quality and information asymmetry

123

as: types of loans, maturity, loan credit rating, identity of lenders, loan size, financial debt

covenants, and purpose of loans as control variables for loan-specific characteristics in our

regression models.

3.2.6 Financial reporting quality

Wittenberg-Moerman (2008) finds that timely loss recognition reduces information

asymmetry in the secondary loan market. In other words, timely loss recognition increases

debt contracting efficiency and reduces the agency cost through underestimating the net

asset value and hence facilitates the monitoring process by debt holders. The market

response to ICDs is also dependent on audit quality (Gupta and Nayar 2006; Beneish et al.

2008). Therefore, we use the absolute value of discretionary accruals as a measure of the

firm’s financial reporting quality.

3.2.7 Determinants of the bid-ask spread

Determinants of the bid-ask spread are liquidity (amount or volume of stock traded), and

volatility or market risk. Liquidity is argued to be negatively associated with information

asymmetry and the cost of capital (Diamond and Verrecchia 1991; Botosan 1997; Healy

et al. 1999; Leuz and Verrecchia 2000; Botosan and Plumlee 2002). Therefore, we include

the volume of traded stock as a proxy for liquidity in our regression model.

3.3 Empirical models

Our first hypothesis deals with the relationship between the disclosure of ICDs and IA in

the secondary loan market. We use model 1 to test our first hypothesis. In model 1, we use

ICDs (firms that disclose significant deficiency, control deficiency, and/or material

weaknesses under section 302 or section 404) as the independent variable of interest, and

information asymmetry as the dependent variable. In all models, we also use a set of

control variables that explain information asymmetry as described in the previous section.

Model 1 is described below:

Ln IAit ¼ b0 þ b1ICDsit þXnj

j¼1

dj Control Variablesj þ et ð1Þ

where Ln_IAit = natural logarithm of information asymmetry as measured by the bid-ask

spread in the secondary loan market; and ICDsit = an indicator variable that takes a value

of 1 if the firm disclosed any types of ICDs, 0 otherwise. Other variables are as defined in

‘‘Appendix’’.

In models 2 and 3, we compare the effect of strictness of the disclosure of ICDs under

both section 302 and section 404 on IA. Therefore, we use ICMWs as an indicator variable

that takes a value of 1 if the firm disclosed ICMWs, and zero otherwise in model 2. We

also use Company-Level ICDs as an indicator variable that takes the value of 1 if the firm

disclosed Company-Level ICDs, and zero otherwise in model 3. We expect the coefficients

on CL and ICMWs to be significant positive. We also add a set of control variables that

explain information asymmetry. Models 2 and 3 are described below:

Ln IAit ¼ b0 þ b1ICMWsit þXnj

j¼1

dj Control Variablesj þ et ð2Þ

D. F. El-Mahdy, M. S. Park

123

where Ln_IAit = natural logarithm of information asymmetry as measured by the bid-ask

spread in the secondary loan market; and ICMWit = an indicator variable that takes a

value of 1 if the firm disclosed ICMWs under section 302 or section 404, and 0 otherwise.

Other variables are as defined in ‘‘Appendix’’.

Ln IAit ¼ b0 þ b1CLit þXnj

j¼1

dj Control Variablesj þ et ð3Þ

where Ln_IAit = natural logarithm of information asymmetry as measured by the bid-ask

spread in the secondary loan market; and CLit = an indicator variable that takes a value of

1 if the disclosed IC weaknesses on the company level, and 0 otherwise. Other variables

are as defined in ‘‘Appendix’’.

To test the effect of the secondary loan market unique characteristics (LS_CHARit) on

the hypothesized relationship between the disclosure of ICDs (ICMWs) and IA, we use

models 4 and 5. Our variable of interest in models 4 and 5 are the interaction terms

ICDs*LS_CHARit and ICMWs*LS_CHARit respectively. Loan specific characteristics

used in these two models are loan credit rating, syndication, loan size, and financial debt

covenants. We expect the interaction terms to have significant negative coefficients.

Ln IAit ¼ b0 þ b1ICDsit þ b2LS CHARit þ b3ICDs � LS CHARit

þXnj

j¼1

dj Control Variablesj þ et ð4Þ

where Ln_IAit = natural logarithm of information asymmetry as measured by the bid-ask

spread in the secondary loan market; ICDsit = an indicator variable that takes a value of 1

if the firm disclosed any types of ICDs, and 0otherwise; LS_CHARit = proxies for loan

characteristics, such as syndication or number of lenders, the availability of loan credit

rating, existence of financial debt covenants, and loan size; and ICDs*LS_CHARit = the

interaction term between LS_CHARit and ICDs.

Other variables are as defined in ‘‘Appendix’’.

Ln IAit ¼ b0 þ b1ICMWsit þ b2LS CHARit þ b3ICMWs � LS CHARit

þXnj

j¼1

dj Control Variablesj þ et ð5Þ

where Ln_IAit = natural logarithm of information asymmetry as measured by the bid-ask

spread in the secondary loan market; ICMWsit = an indicator variable that takes a value of

1 if the firm disclosed ICMWs, and 0 otherwise; LS_CHARit = proxies for loan charac-

teristics, such as syndication or number of lenders, the availability of loan credit rating,

existence of financial debt covenants, and loan size; and ICMWs*LS_CHARit = the

interaction term between LS_CHARit and ICMWs.

Other variables are as defined in ‘‘Appendix’’.

Finally, in model 6, we examine the association between the remediation of ICDs and

IA. We expect a negative significant association of REM with information asymmetry.

Ln IAit ¼ b0 þ b1REMit þXnj

j¼1

dj Control Variablesj þ et ð6Þ

where Ln_IAit = natural logarithm of information asymmetry as measured by the bid-ask

spread in the secondary loan market; and REMit = an indicator variable that takes a value

Internal control quality and information asymmetry

123

of 1 if the firm remediated part or all the disclosed IC weaknesses in the year t - 1, and 0

otherwise.

Other variables are defined in ‘‘Appendix’’.

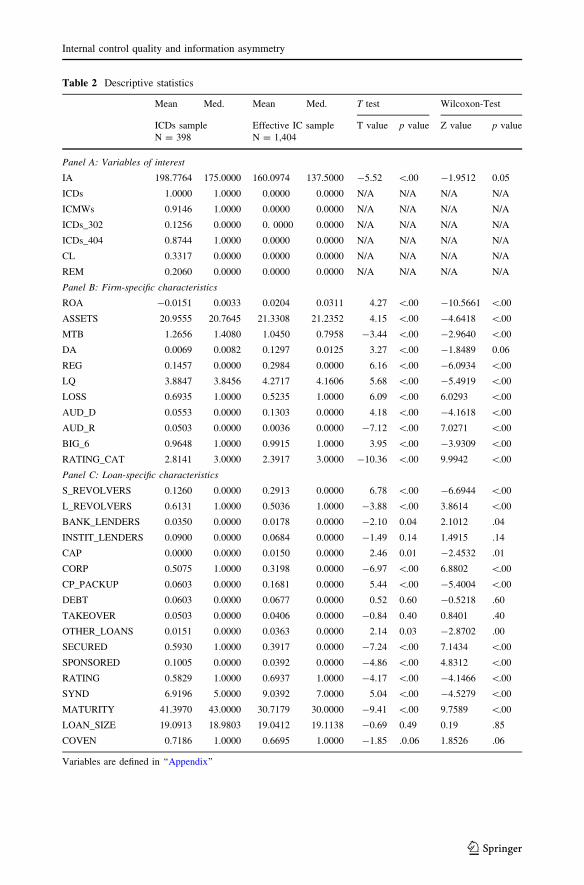

3.4 Descriptive analysis

The descriptive statistics of the final sample of 533 firms (1802 firm-years observations)

are shown in Table 2. Table 2 consists of three panels with a decomposed full sample

(1802 firm-year facilities) into ICDs (398 firm-years observations) and effective IC sam-

ples (1404 firm-years observations). Panel A summarizes descriptive statistics of the

variables of interest such as the bid-ask spread and ICDs variables, Panel B summarizes

descriptive statistics of firm-specific characteristics, and Panel C summarizes statistics for

loan specific characteristics.

The bid-ask spread for the full sample (untabulated) ranges from 10 to 975 basis points

with standard deviation of 124.3958. Panel A indicates that the average (median) bid-ask

spread for firms with ICDs 198.7764 (175) is statistically significantly higher at 1 %

(10 %) p value than that of firms with effective IC 160.0974 (137.5). ICDs (Internal

Control Material Weaknesses ‘‘ICMWs’’) represent 22.09 % (20.20 %) of the full sample.

Of the 20.20 % of firms with ICMWs in the full sample, 1.44 % (18.76 %) are firms with

ICMWs reported under section 302 (404). For the ICDs sample, as shown in panel A,

91.46 % are firms with ICMWs. The majority of ICMWs (87 %) seems to be clustered post

section 404 of the ICDs sample. 33.17 % of the ICDs sample are firms with CL internal

control and 20.60 % are firms that took remediation actions from year t - 1 to year t to

correct the documented deficiency in their IC system.

Panel B of Table 2 shows summary statistics of the firm-specific characteristics of ICDs

and effective ICs samples. As expected, the comparison of the firm-specific characteristics of

firms with ICDs versus firms with effective IC shows that firms with ICDs have lower

statistically significant means of ROA, firm size and liquidity (all at p value \0.01). On

average, ICDs firms also experience significantly higher auditor resignation, less audit

involvement from Big 6 firms and more loss firms than firms with effective ICDs, all p value

of these variables are\0.01. Firms with ICDs are rated significantly lower (2.81) by credit

rating agencies than effective IC sample firms (2.39) at p value\0.01. 20.31 % of the full

sample of firms is post section 404. Consistent with prior research (Bryan and Lilien 2005; Ge

and McVay 2005; Doyle et al. 2007a, b; Ashbaugh-Skaife et al. 2007, 2008; Xu and Tang

2012), the descriptive statistics for firms with ICDs in panel B reveal that firms with reported

ICDs are generally smaller, poor performers, and financially weaker, with higher market risk.

Tests of differences in medians (Wilcoxon-test) reveal that firms with ICDs have lower

statistically significant median ROA, assets and liquidity than firms with effective ICDs.

Table 2 Panel C shows the summary statistics of the loan-specific characteristics. It

shows that firms with ICDs are composed of significantly lower percentage (12.60 %) of

short-term revolver loans than firms with effective IC (29.13 %). 9 % of the ICDs firms are

loans by institutional investors compared to 6.84 % for effective ICDs firms. However,

3.5 % of ICDs firms are loans by banks compared to 1.78 % of loans financed by banks for

the effective IC sample. On average, 68.04 % of the full sample has debt covenants but

ICDs firms have significantly higher debt covenants (71.86 %), compared to firms with

effective IC (66.95 %). This latter statistic is consistent with the findings by Kim et al.

(2011). However, it is in contrast to Costello and Wittenberg-Moerman (2011) who find

that borrowers decrease their use of financial debt covenants as a monitoring tool in the

presence of ICDs in the borrower’s financial statements. Additionally, tests of differences

D. F. El-Mahdy, M. S. Park

123

Table 2 Descriptive statistics

Mean Med. Mean Med. T test Wilcoxon-Test

ICDs sample

N = 398

Effective IC sample

N = 1,404

T value p value Z value p value

Panel A: Variables of interest

IA 198.7764 175.0000 160.0974 137.5000 -5.52 \.00 -1.9512 0.05

ICDs 1.0000 1.0000 0.0000 0.0000 N/A N/A N/A N/A

ICMWs 0.9146 1.0000 0.0000 0.0000 N/A N/A N/A N/A

ICDs_302 0.1256 0.0000 0. 0000 0.0000 N/A N/A N/A N/A

ICDs_404 0.8744 1.0000 0.0000 0.0000 N/A N/A N/A N/A

CL 0.3317 0.0000 0.0000 0.0000 N/A N/A N/A N/A

REM 0.2060 0.0000 0.0000 0.0000 N/A N/A N/A N/A

Panel B: Firm-specific characteristics

ROA -0.0151 0.0033 0.0204 0.0311 4.27 \.00 -10.5661 \.00

ASSETS 20.9555 20.7645 21.3308 21.2352 4.15 \.00 -4.6418 \.00

MTB 1.2656 1.4080 1.0450 0.7958 -3.44 \.00 -2.9640 \.00

DA 0.0069 0.0082 0.1297 0.0125 3.27 \.00 -1.8489 0.06

REG 0.1457 0.0000 0.2984 0.0000 6.16 \.00 -6.0934 \.00

LQ 3.8847 3.8456 4.2717 4.1606 5.68 \.00 -5.4919 \.00

LOSS 0.6935 1.0000 0.5235 1.0000 6.09 \.00 6.0293 \.00

AUD_D 0.0553 0.0000 0.1303 0.0000 4.18 \.00 -4.1618 \.00

AUD_R 0.0503 0.0000 0.0036 0.0000 -7.12 \.00 7.0271 \.00

BIG_6 0.9648 1.0000 0.9915 1.0000 3.95 \.00 -3.9309 \.00

RATING_CAT 2.8141 3.0000 2.3917 3.0000 -10.36 \.00 9.9942 \.00

Panel C: Loan-specific characteristics

S_REVOLVERS 0.1260 0.0000 0.2913 0.0000 6.78 \.00 -6.6944 \.00

L_REVOLVERS 0.6131 1.0000 0.5036 1.0000 -3.88 \.00 3.8614 \.00

BANK_LENDERS 0.0350 0.0000 0.0178 0.0000 -2.10 0.04 2.1012 .04

INSTIT_LENDERS 0.0900 0.0000 0.0684 0.0000 -1.49 0.14 1.4915 .14

CAP 0.0000 0.0000 0.0150 0.0000 2.46 0.01 -2.4532 .01

CORP 0.5075 1.0000 0.3198 0.0000 -6.97 \.00 6.8802 \.00

CP_PACKUP 0.0603 0.0000 0.1681 0.0000 5.44 \.00 -5.4004 \.00

DEBT 0.0603 0.0000 0.0677 0.0000 0.52 0.60 -0.5218 .60

TAKEOVER 0.0503 0.0000 0.0406 0.0000 -0.84 0.40 0.8401 .40

OTHER_LOANS 0.0151 0.0000 0.0363 0.0000 2.14 0.03 -2.8702 .00

SECURED 0.5930 1.0000 0.3917 0.0000 -7.24 \.00 7.1434 \.00

SPONSORED 0.1005 0.0000 0.0392 0.0000 -4.86 \.00 4.8312 \.00

RATING 0.5829 1.0000 0.6937 1.0000 -4.17 \.00 -4.1466 \.00

SYND 6.9196 5.0000 9.0392 7.0000 5.04 \.00 -4.5279 \.00

MATURITY 41.3970 43.0000 30.7179 30.0000 -9.41 \.00 9.7589 \.00

LOAN_SIZE 19.0913 18.9803 19.0412 19.1138 -0.69 0.49 0.19 .85

COVEN 0.7186 1.0000 0.6695 1.0000 -1.85 .0.06 1.8526 .06

Variables are defined in ‘‘Appendix’’

Internal control quality and information asymmetry

123

of medians show that firms with ICDs have significantly lower median values of syndi-

cation and loan sizes compared to firms with effective ICDs. Firms with ICDs also have

higher significant median of loan maturity than firms with effective ICDs.

3.5 Univariate analysis

Table 3 summarizes the results of the univariate analysis. Table 3 is composed of four

panels. Panel A summarizes the results of the differences in means and medians of IA

across firms with effective IC systems versus firms with ICDs. Results of panel A support

the first hypothesis (H1) that firms with ICDs have significantly higher IA than firms with

effective IC; and the p value is \0.01 (significant at 1 %). Wilcoxon-test shows also a

significant difference between the median and distribution of IA for ICDs firms and IA of

the effective IC sample, with the ICDs having a higher median.

Table 3 Panel B summarizes the differences of IA across two samples of firms, firms

with ICDs reported under section 302 versus ICDs reported under section 404. Although

ICDs reported under 302 have higher mean and median IA than ICDs reported under

section 404, the differences are insignificant. Firms with more severe types of ICDs such as

CL-ICDs have non-significant lower mean and median IA than firms with AS-ICDs, as

suggested by panel C. Firms that took actions to correct their ICDs have lower but non-

significant mean IA as shown in panel D.

The descriptive statistics by year (untabulated) for the variables of interest within only

the ICDs sample of firms shows that the average IA in 2002 is 147.5 and ranges from 50 to

300 with standard deviation of 93.6544. It also shows that 71.43 % of ICDs sample in 2002

are firms with ICMWs, 28.57 % (42.86 %) with ICMWs reported under section 302

(section 404). Within the same year, 85.71 % of firms with reported weaknesses have CL

weaknesses and only 42.86 % were able to remediate their ICDs. The descriptive statistics

for the year 2003 indicates that IA increases to an average 191.667 with standard deviation

of 52.8594 and ranges from 100 to 250. 66.67 % of the sample firms are firms with

ICMWs, of which 44.44 % are firms with ICMWs reported under section 302, and

22.22 % were ICMWs reported under section 404. 66.67 % are firms with CL and 55.56 %

of the reported weaknesses were remediated by the firm or auditor. The average IA goes

down in year 2004 relative to 2003. Average IA in 2004 is 176.0714 with standard

deviation of 95.7838 and ranges from 19 to 400. The ICMWs in 2004 are 93.65 % of the

ICDs sample, while 3.17 % (90.48 %) are firms with ICMWs reported under section 302

(section 404). 26.98 % of firms in 2004 are with CL weaknesses and almost one-third of

the reported firms with ICMWs remediated their ICDs. IA reported the highest average in

2005 (214.2208). The average IA in 2005 ranges from 18 to 650 with standard deviation

132.9292 and median of 187.5, the highest among all IA for all years.

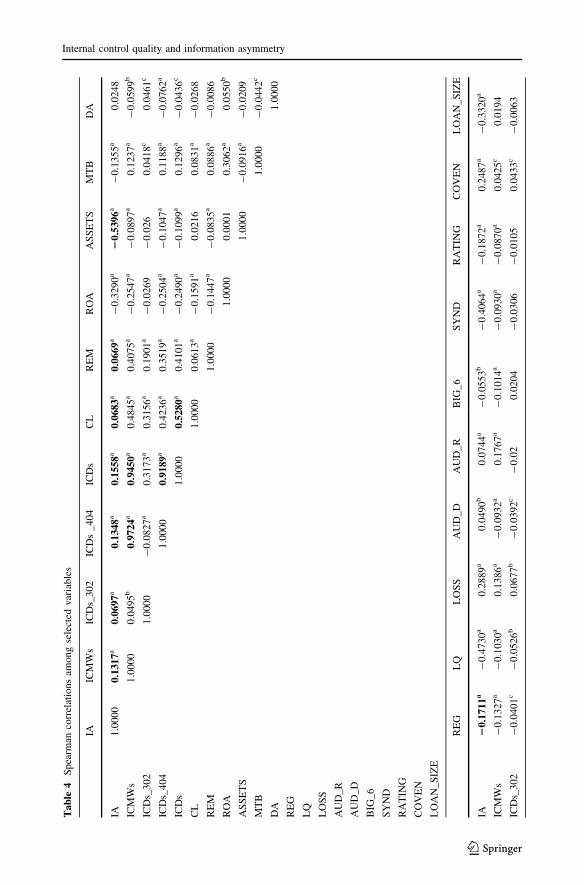

The correlation matrix is presented in Table 4. It summarizes the correlations among

IA, ICDs proxies, firm-specific characteristics and loan-specific characteristics. As pre-

dicted, it shows a statistically significant positive correlation at 1 % with p value \0.01

between IA and ICDs variables such as ICMWs, ICDs, ICDs_302, ICDs_404, and CL. It

also shows a significant positive correlation at 1 % with p value \0.01 among ICDs

variables such as between ICMWs_404 and ICMWs and between ICDs and ICMWs,

suggesting a probable multicollinearity among the ICDs measures. This multicollinearity

would be an obstacle to run a model with an interaction term between measures of ICDs.

Table 4 shows a significant negative correlation between IA and ROA, assets, MTB,

liquidity at 1 % with p value \0.01 and Big 6 audit firms at 5 % with p value \0.05.

Regulated industries show a significant negative correlation with IA at 1 %. Table 4 also

D. F. El-Mahdy, M. S. Park

123

exhibits a significant positive correlation between IA and losses, audit resignation, and

dismissal (auditor changes) as well as significant negative correlation between IA, ROA,

assets, and liquidity. The previous correlations suggest that firms with good financial

performance as measured by ROA, big size firms as measured by total assets, firms with

higher liquidity, and firms that involve Big 6 in the audit process are correlated with lower

IA. Similarly, firms with losses and that experience auditor changes are associated with

higher IA. Table 4 also suggests a significant positive correlation between liquidity and

assets, ICDs_404 and post-section 302 periods, ICDs and post-section 302 periods, indi-

cating a possible multicollinearity among ICDs variables. This multicollinearity limited

our research models from using models with ICDs interaction terms. The correlation

between loan specific-characteristics and either ICDs or ICMWs are as predicted. It is

Table 3 Univariate analysis of IA

Effective IC ICDs Difference tests

Mean Median Mean Median t test(p value)

Wilcoxon-test(z value)

Panel A: Effective IC versus ICDs samples

IA 158.20712 137.5000 198.5251 175.000 -6.11*** 6.52***

N 1404 398

ICDs_404 ICDs_302 Difference Tests

Mean Median Mean Median t test(p value)

Wilcoxon-test(z value)

Panel B: 404 ICDs versus 302 ICDs samples

IA 196.3592 175.0000 213.6000 200.0000 -0.96 1.14

N 348 50

AS CL Difference Tests

Mean Median Mean Median t test(p value)

Wilcoxon-test(z value)

Panel C: AS versus CL

IA 199.9549 200.0000 195.6440 175.0000 .34 .68

N 266 132

REM No REM Difference Tests

Mean Median Mean Median t test(p value)

Wilcoxon-test(z value)

Panel D: REM versus No REM

IA 184.7805 200.0000 202.0918 175.0000 1.18 .30

N 82 316

IAit = information asymmetry as measured by bid-ask spread in the secondary loan market. The bid-askspread is winsorized at 1 and 99 %. In Panel C, CL = company level (CL) internal control weaknesses andAS = account-specific internal control weaknesses. In Panel D, REM = An indicator variable that takes avalue of 1 if the firm remediated part or all the disclosed IC weaknesses in the year t - 1, and 0 otherwise.Significance of means and medians are evaluated based on the t test and Wilcoxon test, respectively(p values for the t-statistic and Z-statistic are two-tailed)

Internal control quality and information asymmetry

123

negative significant between ICDs (ICMWs) and syndication and the existence of loan

credit rating. However, we observe a positive significant correlation between ICDs (IC-

MWs) and financial debt covenants.

4 Empirical results

4.1 Effect of ICDs disclosure on information asymmetry (Hypothesis 1)

Table 5 summarizes the results on the regression of IA on the disclosure of ICDs in the

secondary loan market for 533 firms (1802 facilities) from 2002 to 2005. It shows a

statistically significant positive association between the disclosure of ICDs and IA with a

slope of 0.3020 (p value \0.01). With respect to economic significance, our results sug-

gests that the bid-ask spread increases by 30 basis points when ICD is disclosed. We use

the full sample (1802) to test model 1 and included in the regression a large pool of control

variables to control for firm and loan-specific characteristics.

The results also show that IA has a significant negative association with ROA, assets,

liquidity, post-SOX 2002, section 404 period and loan size. This latter result supports the

notion that big firms, high performing firms, well established, large loans and profitable

firms experience lower IA than small firms, or low performing firms. These results make

sense, especially in the secondary loan market where big firms are, in most cases, able to

reduce their overall IA. This also implies that IA is not uniform across different firm sizes.

Additionally, big firms are more likely to have more resources and able to invest in IC

systems, announce interim reports and hence enhance transparency and disclosure of

information. They also have top tier audit firms, which endorse their financial reporting. IA

shows a statistically significant and positive association with loss firms, regulated indus-

tries, auditor resignation, and maturity. Furthermore, the results reveal that the coefficient

on REG*ICDs is negative and significant at the 5 % level, indicating that the monitoring

mechanisms in regulated industries on average mitigate the negative consequences of ICDs

disclosure on IA by 16 basis points. This evidence is in line with prior findings that

regulated industries release significant amount of publicly available information to the debt

market, compared to non-regulated industries (Choy et al. 2006) and that regulated

industries are more likely to issue long-term debt (Barclay and Smith 1995). This suggests

that regulated industries may have lower information asymmetry than non-regulated

industries. Overall, results in Table 5 support our H1.

Results in Table 5 can also be explained by Beneish et al. (2008) who claim that when a

weakness in the IC system is disclosed to the public, it increases the uncertainty about the

firm’s internal operations and activities since the disclosure of ICDs is symptomatic of

increased business risk (Ogneva et al. 2007). Additionally, uncertainty increases the

demand for risk-taking actions by investors and traders. Hence, informed traders in the

secondary loan market will demand more private information about unsecured collateral

and increase the cost of borrowing to the firm relative to the cost demanded by informed

traders. Furthermore, these results suggest that the quality of accounting information

matters in the secondary loan market. In other words, an effective IC system might play the

same role that other proxies of the quality of accounting information do, such as the role

timely loss recognition plays in the secondary loan market (Wittenberg-Moerman 2008).

Wittenberg-Moerman (2008) suggests that timely loss recognition increases debt con-

tracting efficiency and reduces the agency cost through underestimating the net asset value

and hence facilitates the monitoring by debt holders.

D. F. El-Mahdy, M. S. Park

123

Tab

le4

Spea

rman

corr

elat

ions

among

sele

cted

var

iable

s

IAIC

MW

sIC

Ds_

30

2IC

Ds

_4

04

ICD

sC

LR

EM

RO

AA

SS

ET

SM

TB

DA

IA1

.000

00

.131

7a

0.0

697

a0

.134

8a

0.1

55

8a

0.0

683

a0

.066

9a

-0

.329

0a

20

.539

6a

-0

.13

55

a0

.024

8

ICM

Ws

1.0

00

00

.049

5b

0.9

724

a0

.94

50

a0

.484

5a

0.4

07

5a

-0

.254

7a

-0

.089

7a

0.1

23

7a

-0

.059

9b

ICD

s_3

02

1.0

00

0-

0.0

82

7a

0.3

17

3a

0.3

15

6a

0.1

90

1a

-0

.026

9-

0.0

26

0.0

41

8c

0.0

46

1c

ICD

s_4

04

1.0

00

00

.91

89

a0

.423

6a

0.3

51

9a

-0

.250

4a

-0

.104

7a

0.1

18

8a

-0

.076

2a

ICD

s1

.00

00

0.5

280

a0

.410

1a

-0

.249

0a

-0

.109

9a

0.1

29

6a

-0

.043

6c

CL

1.0

00

00

.061

3a

-0

.159

1a

0.0

21

60

.08

31

a-

0.0

26

8

RE

M1

.000

0-

0.1

44

7a

-0

.083

5a

0.0

88

6a

-0

.008

6

RO

A1

.000

00

.000

10

.30

62

a0

.055

0b

AS

SE

TS

1.0

00

0-

0.0

91

6a

-0

.020

9

MT

B1

.00

00

-0

.044

2c

DA

1.0

00

0

RE

G

LQ

LO

SS

AU

D_

R

AU

D_

D

BIG

_6

SY

ND

RA

TIN

G

CO

VE

N

LO

AN

_S

IZE

RE

GL

QL

OS

SA

UD

_D

AU

D_R

BIG

_6

SY

ND

RA

TIN

GC

OV

EN

LO

AN

_S

IZE

IA2

0.1

71

1a

-0

.47

30

a0

.28

89

a0

.04

90

b0

.07

44

a-

0.0

55

3b

-0

.406

4a

-0

.187

2a

0.2

48

7a

-0

.332

0a

ICM

Ws

-0

.13

27

a-

0.1

03

0a

0.1

38

6a

-0

.09

32

a0

.17

67

a-

0.1

01

4a

-0

.093

0a

-0

.087

0a

0.0

42

5c

0.0

19

4

ICD

s_3

02

-0

.04

01

c-

0.0

52

6b

0.0

67

7b

-0

.03

92

c-

0.0

20

.02

04

-0

.030

6-

0.0

10

50

.043

3c

-0

.006

3

Internal control quality and information asymmetry

123

Tab

le4

con

tin

ued

RE

GL

QL

OS

SA

UD

_D

AU

D_R

BIG

_6

SY

ND

RA

TIN

GC

OV

EN

LO

AN

_S

IZE

ICD

s_4

04

-0

.13

42

a-

0.1

14

1a

0.1

21

1a

-0

.08

67

a0

.18

24

a-

0.1

05

9a

-0

.099

4a

-0

.098

3a

0.0

27

80

.007

4

ICD

s-

0.1

43

6a

-0

.12

94

a0

.14

21

a-

0.0

98

1a

0.1

65

6a

-0

.09

26

a-

0.1

06

7a

-0

.097

7a

0.0

43

7c

0.0

04

5

CL

-0

.02

39

0.0

19

20

.12

85

a-

0.0

73

9a

0.0

03

1-

0.0

01

7-

0.0

19

00

.025

60

.055

7b

0.0

57

5b

RE

M-

0.0

70

7a

-0

.04

38

c0

.10

73

a-

0.0

27

90

.20

18

a-

0.1

07

6a

-0

.060

8a

-0

.027

60

.081

1a

-0

.038

4

RO

A-

0.0

14

50

.04

35

c-