interim report 2012

DESCRIPTION

ÂTRANSCRIPT

Mighty River Power Limited Interim Report 2012

Mighty River Power is a New Zealand electricity company, with a flexible portfolio of electricity generation assets, a strong national retail presence and a focus on domestic generation and international geothermal development opportunities. More than 90% of our generation is from renewable sources. Our sales to major industrial and commercial users and through our retail brands, Mercury Energy, GLO-BUG, Bosco Connect and Tiny Mighty Power, account for more than 18% of New Zealand’s total electricity consumption.

Cover: Drilling underway at the 82MW Ngatamariki geothermal project near Taupo.

Mighty River Power Limited Interim Report 2012 1

0-910-2930-4950-69

HYDROARATIATIA 78MWOHAKURI 106MWATIAMURI 74MWWHAKAMARU 98MWMARAETAI I & II 360MWWAIPAPA 54MWARAPUNI 182MWKARAPIRO 96MW

GEOTHERMALKAWERAU 100MWROTOKAWA 34MW

*NGA AWA PURUA 140MW*MOKAI 112MW NGATAMARIKI 82MW(UNDER CONSTRUCTION)

*Not 100% owned by Mighty River Power

GASSOUTHDOWN 175MW

RETAIL MARKET SHARE (%)

WINDPUKETOI (CONSENTING)TURITEA (CONSENTED)CAPE CAMPBELL (LAND ACCESS)

Electricity Generation and Retail Sales

2 Mighty River Power Limited Interim Report 2012

Performance Highlights

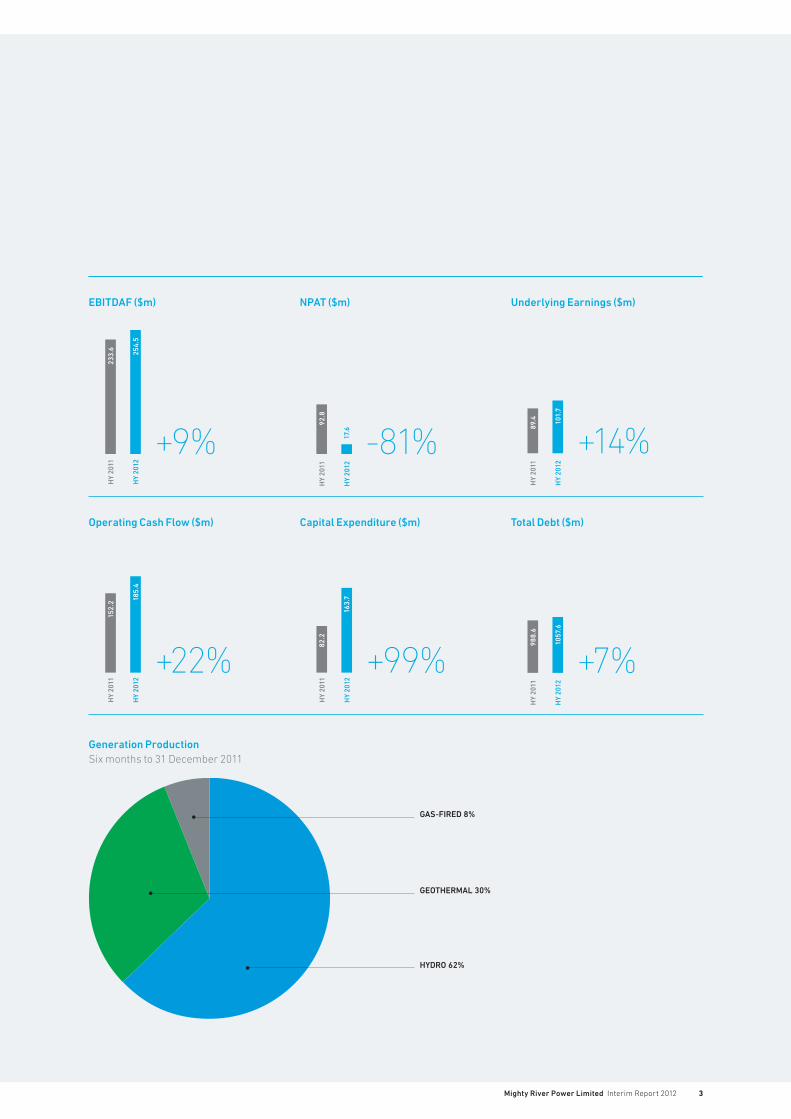

4%Increase in total electricity generation to 3,664GWh, with increased gas-fired production in response to higher wholesale prices.

$81.5mIncrease in capital expenditure with the start of $466m Ngatamariki geothermal project and further deployment of committed funds to international geothermal projects.

$74.8mInterim dividend for the half-year ended 31 December 2011.

9%Lift in operating earnings (EBITDAF) to $254.5 million.

1%Lift in fixed-price variable volume customer sales volumes, despite 5% fall in customer numbers. Average FPVV price up to $113.58/MWh.

49.9MWHudson Ranch Power I project on Salton Sea reservoir in Southern California, US, completed and first full power to grid in March 2012.

$80.16/MWhWeighted average price for electricity generation, up more than $20/MWh, reflecting significantly stronger prices in the wholesale market.

No. 1Deloitte Energy Excellence Awards: Mercury Energy named 2011 Energy Retailer of the Year, following the Company’s wins in 2010 of Overall Energy Company and Energy Project.

$1,360mIn total debt facilities with an average duration of 5.9 years at balance date. BBB+/stable Standard & Poor’s credit rating.

Mighty River Power Limited Interim Report 2012 3

EBITDAF ($m) NPAT ($m)

HY

2011

233.

6

HY

2012

254.

5

HY

2011

92.8

HY

2012

17.6

+9%

Operating Cash Flow ($m)

Generation ProductionSix months to 31 December 2011

152.

2H

Y 20

11

185.

4H

Y 20

12

+22%

-81%

Underlying Earnings ($m)

HY

2011

89.4

HY

2012

101.

7

+14%

GEOTHERMAL 30%

HYDRO 62%

GAS-FIRED 8%

Capital Expenditure ($m)

HY

2011

163.

7H

Y 20

12

+99%

82.2

Total Debt ($m)H

Y 20

1198

8.6

HY

2012

1057

.6

+7%

4 Mighty River Power Limited Interim Report 2012

Drilling activity at the Ngatamariki geothermal project.

Mighty River Power Limited Interim Report 2012 5

We started the new financial year with a clear focus on building on the benchmark set by our 2011 performance.

Mighty River Power’s interim results for 2012 show a healthy lift in operating earnings and underlying performance on the prior comparable period (pcp). We are also pleased to report on positive progress on the commitment we have made to future growth – both in New Zealand and through investments offshore.

We achieved gains in market share and pricing, across both generation and customer sales, in a competitive domestic electricity market which experienced no volume growth during HY2012. Those achievements are a credit to our people and their focus on continued operational improvements across the business.

This Report also marks some key milestones for the Company.

During the half-year, there was clear evidence of the Company’s continued growth, with the start of construction for the Ngatamariki geothermal project near Taupo and, soon after balance date, the commissioning of EnergySource’s Hudson Ranch Power I geothermal project in the United States.

These new projects extend the track record of growth achieved through investment in geothermal generation in New Zealand over the past five years that has underpinned

returns and created significant value for our shareholders.

Reliable base-load geothermal capacity has significantly expanded and diversified our electricity production from renewable low-cost fuels, and with the completion of Ngatamariki will represent around 40% of our domestic generation. Our renewable portfolio is complemented by flexible gas-fired generation.

This differentiates Mighty River Power from our competitors, and provides a stronger earnings base alongside our integrated sales channels which account for more than 18% of total electricity consumption in New Zealand.

The diversity now embedded in our business provides far-greater resilience to the impacts of poor hydrology in the Waikato catchment, and opens up potential market opportunities such as when there are contrasting lower inflows to hydro catchments in the South Island.

Mighty River Power’s financial results for HY2012 are built on this diverse and complementary portfolio.

Highlights:• Operatingearnings(EBITDAF)of

$254.5 million for the six months ended 31 December 2011, up 9%onthefirsthalfofFY2011.

• Netprofitaftertax(NPAT)reportedunderNZIFRSof$17.6millioncompared with $92.8 million inthepcp,asaresultof$106million of non-cash fair value movements on derivatives and financial instruments recognised.

• Underlyingearningsupby14%from$89.4millionto$101.7million.Forcomparativepurposes,thismeasure removes significant one-off items and the change in the fair value of financial instruments from net profit after tax.

• Interimdividendof$74.8million,to be paid on 30 March 2012 (representing75%ofnetprofitaftertax after adjusting for the impact of fair value movements net of tax).

• Increaseincapitalexpenditureto$163.7millionwiththestartofthe$466millionNgatamarikiproject and further deployment of committed funds to international geothermal projects.

• Totaldebtfacilitiesof$1,360millionwith an average duration of 5.9 years at balance date. BBB+/stable Standard & Poor’s credit rating.

BUsINEss OvERvIEWMighty River Power’s operating performance and financial results for HY2012 were achieved in a challenging environment.

New Zealand’s weak economic climate following the lingering effectsoftheGlobalFinancial Crisis and Canterbury earthquakes is very evident in the electricity markets. While there is an expectation across the industry that domestic electricity demand growth will return with a more robust economic recovery, the past year has seen the continuation of flat to declining national demand that hasprevailedsince2007.

Chair and Chief Executive’s Report

We achieved gains in market share and pricing, across both generation and customer sales, in a competitive domestic electricity market which experienced no volume growth during HY2012.

Joan Withers Doug Heffernan

6 Mighty River Power Limited Interim Report 2012

TheElectricityAuthority reported a 1% contraction in the New Zealand electricity market in the2011calendaryear.Also,withthe strong supply side in the market over the past few years, there has been a trend of larger commercial consumers increasing their exposure to fluctuating half-hourly wholesale market prices, rather than fixing prices through hedge contracts.

Despite these dynamics, the Company has been able to achieve market share and pricing gains in generation and fixed-price customer sales.

RetailDuring the half-year we achieved an increase in customer pricing and made further gains (up 1% from 2,531GWh to 2,555GWh) in fixed price sales volumes, despite a 5% drop in customer numbers to 383,000 at 31 December 2011.

Mercury Energy has responded to the high levels of customer churn across the industry with a range of pricing and customer retention initiatives.

Our three-year fixed-price offer introducedinFY2011hascontinuedto be popular, attracting around 80,000 mainly higher-use residential customers.Ahighlightofthehalf-year was the strong commercial sales growth, which sustained the overall increase in sales volume, partially offset by a drop in residential volumes. The Company achieved a 4.5%increaseintheaverageFPVV(fixed price variable volume) price to $113.58/MWh for the six months to 31 December compared to the same period a year ago. The Company has also been an active participant in the high-growthASXmarketfor0-3yearcontracts to optimise our integrated generation and sales portfolio.

Alongwithsalesvolumegainsinthecompetitive retail electricity market in New Zealand, and metering innovation

including pre-pay through GLO-BUG, it was also pleasing to have the external recognition of the Company’s flagship retail brand, Mercury Energy – named 2011 Energy Retailer of the Year at the DeloitteEnergyExcellenceAwards–following Mighty River Power’s success

as Overall Energy Company of the Year in 2010, and finalist in 2011.

Post balance date, the Company announced a price increase averaging 5.8% for Mercury Energy’s residentialcustomersfrom1April2012. The price change includes the pass through to customers of lines charges from the local distribution company, which account for around 40% of a customer’s bill.

This year’s lines increase reflected a significant rise in transmission charges from Transpower following regulatory approval of major investments in New Zealand’s National Electricity Grid, improving grid security andreliabilityforcustomers.Afteraccounting for the pass through of distribution and transmission costs, Mercury Energy’s energy price rise represents, on average, an increase of 2.1% on a customer’s total bill.

AnothernotableinitiativeinFebruarywastheMercuryEnergy‘Good Energy’ brand launch, supported by our first television advertising campaign in several years along with online and other promotional activity. The campaign is based on the concept of ‘good energy’ as integral to the Kiwi culture, and something that Mighty River Power and Mercury Energy

harness and share – from the inter-generational benefits of New Zealand’s bountiful endowment of natural renewable energy resources such as geothermal and hydro, through to supporting theStarshipFoundation.

The Company’s other retail brands specialise in targeting niche markets: inner-city apartments (Bosco Connect); pre-pay energy (GLO-BUG); and smaller provincial towns (Tiny Mighty Power).

Bosco Connect continues to make a positive contribution to earnings. The specialty apartment brand maintained its market-leading position in the Aucklandapartmentmarketandcontinues to supply over half of the contestableAucklandCBDapartments.

Over the past three years GLO-BUG has transformed the credit area of our business by providing a modern-day solution that helps meet the needs of customers who struggle to manage theirenergybudgets.Assmartmeters are deployed nationwide by the industry over the coming years, GLO-BUG will enter new geographies to meet the need for this service, and we have recently begun offering the service to customers in Christchurch.

Our metering business, Metrix, has now completed the roll-out of more than 290,000 smart meters in the Aucklandregion,andasreportedat30 June 2011, is moving to focus on providing services over this platform.

Under the provincial-focused Tiny Mighty Power brand, we secured further sales growth in Waikato,

Mercury Energy has responded to the high levels of customer churn across the industry with a range of pricing and customer retention initiatives.

Mighty River Power Limited Interim Report 2012 7

Wairarapa, Marlborough and North Canterbury. Tiny Mighty added more than 2,500 customers during the period, a 30% increase, and ahead of our expectations. Since launch in late 2009, the brand has grown its customer base to more than 10,000.

OperationsThefirsthalfofFY2012wascharacterised by higher wholesale market prices, with national hydro inflows and storage significantly lower than the pcp for most of the half.

The Company’s total generation production was up on what was a strongfirsthalfinFY2011by4% (from3,520GWhto3,664GWh),withtheincrease largely driven by greater use of gas-fired production in response to higher wholesale prices. Geothermal output, at 1098GWh (including our equity share of joint ventures), was just over the prior period’s record level.

Above-averagehydroinflowsandour flexible gas units allowed greater flexibility in our generation production to respond to wholesale market opportunities. The generation portfolio continues to support volume growth in our integrated sales portfolio whilst managing downside earnings risk. The Company’s generation yields were up more than $20/MWh from $56.18/MWhtoanaverage$80.16/MWh, reflecting the significantly stronger prices in the wholesale market during the period, as poor national hydrology more than offset flat or declining national demand.

Fromanoperationalperspective, we noted several significant court and regulatory outcomes over recent months.

During the half-year, the Waikato Regional Council confirmed a consent change for a reduction in the duration ofthedailyhydrospillatAratiatia.This change, which involved extensive discussions with local businesses and other stakeholders, provides for additional generation while enhancing

the local tourism experience from the passage of water down the naturalAratiatiaRapids,temporarilybypassing the hydro station.

In November we received the reserved decision from the Environment Court hearings on Variation6oftheWaikatoRegionalPlan concerning water allocation. The most significant aspect for our business was a small increase in the volume of water allocated for abstraction from the Waikato River (from3.6%to5%ofminimumflowatKarapiro). We were disappointed that the Waikato Regional Council’s original decision to not change the existing allocation, which we supported, was not upheld by the Court.

However, we anticipate that the effects of the additional potential abstraction will be mitigated by ongoing operational and plant efficiency gains from refurbishments underway across the Waikato hydro system. Normal seasonal hydrological variations in the catchment remain the most significant influence on production from our hydro operations.

WewelcomedinFebruarytheHigh Court ruling upholding the ElectricityAuthority’sdecisionthataUTS (Undesirable Trading Situation) occurredonMarch26,2011.Thisrulingsupports our view that the declaration of a UTS and a consequent wholesale price re-set was an appropriate remedy for the events, which had exposed Mighty River Power and other market participants to prices more than 200 times those prevailing at the time. While the ruling remains subject toappeal,theAuthority’sdecisiontoreset prices to around $3,200/MWh is consistent with the Company’s treatmentintheFY2011accounts. We also see the decision as important from a regulatory standpoint, and as positive for electricity customers, current and future investors and the wider economy – confirming that the market has clear rules

and proven and appropriate mechanisms for enforcement.

Anotherpositivedevelopmenton this front was the move by the ElectricityAuthoritytochangethemethodology for selecting offers into the frequency-keeping market (which is run by the system operator to ensure real-time balancing of electricity supply and demand).

Followinganinvestigation,theElectricityAuthorityreportedabnormally high North Island frequency costs due to a change in the way another North Island service provider was structuring their frequency-keeping and energy offer prices,particularlybetweenAugustand October 2011. The Electricity Authorityimplementedachangefrom November 2011 in the selection methodology to ensure the lowest cost solution is now selected.

If this methodology had been in place for the half-year the benefit to Mighty River Power from lower costs and higher revenues would have been approximately $4 million. In addition, industry-wide electricity costs would have been $10 million lower.

DevelopmentWe have committed to geothermal investments domestically and offshore, building on the strong geothermal growth that began with Kawerau in 2008, which are aimed at enhancing shareholder value over the longer term.

The ground-breaking for the new$466m82MWNgatamarikigeothermal plant near Taupo was a clear highlight during the half-year, reflecting further growth in our generation portfolio in New Zealand.

The Ngatamariki construction project is now well underway and the project is on track for full commissioninginmid-2013.Ashighlighted earlier, this will take geothermal’s contribution to more than 40% of our generation production.

8 Mighty River Power Limited Interim Report 2012

Our geothermal growth – based on a core strategy of securing lowest-cost, economic development sites – has been a ‘game-changer’, broadening and strengthening our earnings base with the addition of more than 2,200GWh of annual base-load generation alongside our core hydro assets on the Waikato River. This is a differentiator and competitive advantage for us in growing and diversifying our low fuel cost generation portfolio over the past five years, with the addition of Kawerau(100MW)andNgaAwaPurua(140MW) – and now Ngatamariki.

The recent completion of the 49.9MW Hudson Ranch Power I geothermal project on the Salton Sea reservoir in SouthernCalifornia’sImperialValleywas a key milestone for Mighty River Power’s international geothermal programme. The EnergySource-owned project in which Mighty River Power has a US$92 million investment stake throughtheGeoGlobalPartnersIFund(GGEFund)produceditsfirstfullpowerto grid in early March 2012, twenty-one months after start of construction.

Hudson Ranch Power I, the largest geothermal development in the US in recent years, is the first of Mighty River Power’s international geothermal developments to move into commercial operation. The plant supplies renewable energy under a long-term contract to Salt River Project, an Arizonautilityprovidingelectricitytoaround 900,000 customers, and uses similar technology to Mighty River Power’sKawerauandNgaAwaPuruageothermal stations in New Zealand.

The Company has taken, and will continue to take, a measured and prudent approach to international development opportunities. Through ourinvestmentintheGGEFund,wenow have a platform for international geothermal growth which leverages Mighty River Power’s experience and competencies in this global niche.

This approach has focused on investing equity capital in early-

stage geothermal exploration and development in Chile and Germany, complemented in the US by the later-stage investments in EnergySource and Hudson Ranch Power I.

While positive progress has been made on most international

geothermal projects, the Tolhuaca project in southern Chile has experienced delays in production-scale well drilling due to abnormally harsh winter conditions and a mechanical incident with the rig in November involving GeoGlobal Energy’s drilling contractor. The first well has now been completed and drilling commenced on the second well. Drilling and final testing of these two wells is due to be completed prior to year-end.

Fueldiversitycontinuestobeakeyfocus of our domestic development strategy. We see geothermal and wind playing a key role in new generation development in New Zealand over the next decade.

InFY2011wereceivedconsents for a 180MW wind project of up to60turbinesatTuriteanearPalmerston North. We have since lodged resource consent applications foraproposed53-turbine326MW wind development on the Puketoi Range, south of Dannevirke, and this is now progressing through a public hearing.

The Company has been testing and assessing wind generation prospects in the area for a number of years and we have confidence in the exceptional quality of the resource at Puketoi. We have based our proposal on best-practice principles, following

extensive consultation with the local communities. We are confident that the Puketoi project will provide significant long-term economic benefits to the local communities, and renewable energy benefits to the whole of New Zealand. However, the current demand situation means any firm capital commitment on these wind projects will be several years away.

During HY2012, Mighty River Power signed a joint development agreement with Okere Incorporation and Ruahine & Kuharua Incorporation for the investigation and development of geothermal power generation on the Taheke field, northeast of Rotorua. The development agreement, for what will be known as the Te ia a Tutea Development, brings together multiple land owners who share an interest in sustainable, integrated development of the resource. The agreement enables initial exploration of the geothermal resource and provides for long-term co-ownership of any subsequent developments. Subject to consenting arrangements, exploration drilling is expected to start on the Taheke field within the next 12 months.

Fueldiversitycontinuestobea key focus of our domestic development strategy. We see geothermal and wind playing a key role in new generation development in New Zealand over the next decade.

Mighty River Power Limited Interim Report 2012 9

Engineers planning maintenance work on the Waikato Hydro system.

10 Mighty River Power Limited Interim Report 2012

Our People and CommunitiesOur people and communities remain key to our future success. The operational and financial results in this Report would not have been possible without the absolute focus and quality of our people, and the deep relationships we have built with local communities including iwi and our commercial partners in New Zealand and internationally.

These cornerstone principles and our values will remain a vital foundation for our commercial sustainability and future growth – reflecting that corporate social responsibility is partofourCompany’sDNA,andisintegral to our business model.

Mighty River Power’s joint development approach with Maori Land Trusts have been the platform for the Company’s significant growth in geothermal over the past decade, supported by our internationally recognised expertise. These highly-valued, long term partnerships will continue to deliver significant mutual benefits.

We have also reinforced our commitment to building a powerful and vigorous health and safety culture across the whole Company and we are tracking well against our key measure.TRIFR(TotalRecordableInjuryFrequencyRate)wasdown18% at 31 December 2011, with a continued focus on our systems, engagement and responding to potentialhazardsinourworkplaces.

With our people, we remain focused on unlocking employee potential and further building high performance in every area of the business. During the half-year we have continued to invest through a range of programmes in employee and leadership development, supporting the retention of people in key areas of organisational capability and ensuring strong alignment to both current and future business requirements.

Anexcellentexampleisourapprentice programme, which is focused on building tomorrow’s workforce. Over the past six years this programme has had a 95% completion rate, and the model has been extended into a partnership with Contact

Energy, establishing the Electricity SupplyApprenticeProgramme.

We are also actively partnering with New Zealand universities. Mighty River Power is one year into its ‘Source to Surface’ programme with the University of Canterbury’s Geology Department. The programme is already providing valuable information back to the Company’s Geothermal Technical Resources team and is resulting in other positive outcomes, such as increased geothermal content in the Department’s undergraduate programme.

During the half-year we broadened our support at a tertiary level. Mighty River Power invested in the continued development of New Zealand’s expertise and research into geothermal power generation by entering into an agreement with TheUniversityofAucklandto sponsor a newly established Chair in Geothermal Reservoir Engineering. The Company’s sponsorship provides funding of $1 million over a five year period – known as the Mighty River Power Chair in Geothermal Reservoir Engineering – supporting the revival of the University’s internationally acknowledged Geothermal Institute.

We see the re-establishment of the Geothermal Institute as providing

impetus to enhancing New Zealand’s geothermal capacity, both in terms of a greater number of graduates with the skills sought by Mighty River Power for its domestic and international strategies, and also in building a greater depth of geothermal knowledge

in New Zealand to ensure New Zealand companies can capitalise on the growing global interest in geothermal utilisation for power and heating.

FINANCIAL REvIEWOur financial results in the half-year highlight Mighty River Power’s diverse and balanced operational base that underpins earnings. The Company continues to take an active approach to managing the balance sheet, ensuring adequate headroom and with no further debt refinancing expected until late in the 2013 calendar year.

EBITDAF(earningsbeforeinterest,taxation, depreciation, amortisation and financial instruments) increased 9% from$233.6millionto$254.5million.This was driven primarily by a 4.5% increase in the weighted average price (FixedPriceVariableVolume)receivedfrom residential and commercial customers during the period, and a $7milliongainfromthesaleofPRE(Projects to Reduce Emissions) credits fromtheNgaAwaPuruajointventure.

NPAT(netprofitaftertax)reportedunderNZIFRSwas$17.6millionwiththe Company recognising non-cash fair value movements on derivatives of $106.0million,bothdomesticallyandthrough its international interests in jointly-controlledentities.Ofthis,$103.7million related to interest rate derivatives

Our financial results in the half-year highlight Mighty River Power’s diverse and balanced operational base that underpins earnings.

Mighty River Power Limited Interim Report 2012 11

which are not hedge accounted – impacted by a fall in wholesale interest rates to record lows in the six months to 31 December 2011 compared with those used to measure fair value at 30 June 2011.Aftertaxprofitwasalsoimpactedbyhigherdepreciation(duetoFY2011asset revaluations) and interest expense reflecting the higher average debt levels and higher average cost of funds.

Mighty River Power’s underlying earnings(thatadjustsNPATforthenon-cash fair value movements of derivatives, impairments and other significant items) for the period increased by $12.3 million (or14%)from$89.4millionto$101.7million. The Company’s Board and management recognise the critical importance of reported profits meeting appropriate accounting standards. In complyingwithNZIFRSaccountingstandards, we believe the additional reporting of underlying earnings is helpful to shareholders and other audiences in making meaningful comparisons of our results over time and between different companies.

In line with the Company’s dividend policy(of75%ofnetprofitaftertaxafter adjusting for the impact of non-cash fair value movements net of tax), the Mighty River Power Board has approved an interim dividend of $74.8million,tobepaidon30March,2012.Thisrepresentsa16%(or$10.1million) increase on the last year’s interimdividendof$64.7million.

While operating expenses, at $115.1 million, were lower than theprevioushalf-yearof$117.2million, largely as a result of the re-scheduling of maintenance projects.

Reflecting the Company’s lift in operating earnings, cash flows for the period improved 22% from $152.2 million to $185.4 million for HY2012.

The Company’s capital expenditure increased $81.5 million on the prior comparable period from $82.2 million to$163.7million,withtheNgatamarikiproject underway and further

deployment of the US$250 million commitmenttotheGGEFund,withUS$205 million drawn at 31 December 2011. The increased capital spend was partially offset by the deferral to FY2013of$12.5millionrelatingtothedrilling of a geothermal well at the 100MW Kawerau geothermal plant.

FollowingasignificantdebtrefinancingprogrammeinFY2011,theCompany increased an existing bank facility with Bank of Tokyo-Mitsubishi by $50 million to $200 million to create additional liquidity headroom. Total debtroseto$1057.6million,up7%onthe pcp. Total facilities at 31 December 2011stoodat$1,360millionwithan average duration of 5.9 years.

The Company’s debt portfolio remains well-diversified with a mix of bank debt, wholesale and retail bonds, and a US private placement. Mighty River Power’s Standard & Poor’s credit rating is BBB+/stable.

Subsequent to the half-year balance date, to reduce the costs of short-term funding the Company established a $200 million Commercial Paper Programme fully backed by committed and undrawn bank facilities, with the first $25 million placedinFebruary2012.

OUTLOOkAlongsidethesignificantachievementsof HY2012, our financial results show a solid start to the financial year.

It was satisfying to be able to announce in March an increase inguidanceforFY2012.Basedon the Company’s interim results and a strong start to the second half, we are forecasting full-year earnings(EBITDAF)intherangeof$460millionto$475million.Thiscompares with our initial guidance forFY2012of$430millionto$450million issued in October 2011.

This improvement reflects the benefit of our geothermal base-load capacity, complemented by relatively favourable hydrology in

the Waikato River catchment, in contrast to poor South Island hydrology.

These factors have enabled us to further increase production since the start of 2012 in response to elevated prices in the wholesale market. The structure of our generation portfolio supports ongoing growth in sales volume and yields through a range of channels.

We look forward to updating you further with the release of ourfull-yearresultsinAugust.

JOAN WITHERsChair

DOUG HEFFERNANChief Executive

12 Mighty River Power Limited Interim Report 2012

TO THE sHAREHOLDERs OF MIGHTY RIvER POWER LIMITED REPORT ON THE CONDENsED CONsOLIDATED INTERIM FINANCIAL sTATEMENTs OF MIGHTY RIvER POWER LIMITED FOR THE sIX MONTH PERIOD ENDED 31 DECEMBER 2011

TheAuditor-GeneralistheauditorofMightyRiverPowerLimitedanditssubsidiaries.Wehavecarriedouttheauditofthecondensed consolidated interim financial statements of Mighty River Power Limited (hereafter referred to as the financial statementsofthegroup),onbehalfoftheAuditor-General.

Wehaveauditedthefinancialstatementsofthegrouponpages16to31,thatcomprisetheconsolidatedbalancesheetasat 31 December 2011, the consolidated income statement, the consolidated statement of comprehensive income, the consolidated statement of changes in equity and the consolidated statement of cash flows for the six months period ended on that date and the notes to the financial statements that include accounting policies and other explanatory information.

OpinionOpinion on the financial statements of the group Inouropinionthefinancialstatementsofthegrouponpages16to31:• complywithgenerallyacceptedaccountingpracticeinNewZealandasitrelatestointerimfinancialstatements;• complywithInternationalFinancialReportingStandardsasitrelatestointerimfinancialstatements;and• giveatrueandfairviewofthegroup’s: • financialpositionasat31December2011;and • financialperformanceandcashflowsforthesixmonthperiodendedonthatdate.

Opinion on other Legal RequirementsInaccordancewiththeFinancialReportingAct1993wereportthat,inouropinion,properaccountingrecordshavebeenkept by the group as far as appears from an examination of those records.

Ourauditwascompletedon27March2012.Thisisthedateatwhichouropinionisexpressed.

The basis of our opinion is explained below. In addition, we outline the responsibilities of the Board of Directors and our responsibilities, and explain our independence.

Basis of OpinionWecarriedoutourauditinaccordancewiththeAuditor-General’sAuditingStandards,whichincorporatetheInternationalStandardsonAuditing(NewZealand).Thosestandardsrequirethatwecomplywithethicalrequirementsandplanandcarry out our audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

Material misstatements are differences or omissions of amounts and disclosures that would affect a reader’s overall understanding of the financial statements. If we had found material misstatements that were not corrected, we would have referred to them in our opinion.

Anauditinvolvescarryingoutprocedurestoobtainauditevidenceabouttheamountsanddisclosuresinthefinancialstatements.The procedures selected depend on our judgement, including our assessment of risks of material misstatement of the financial statements whether due to fraud or error. In making those risk assessments, we consider internal control relevant to the preparation of the group’s financial statements that give a true and fair view of the matters to which they relate. We consider internal control in order to design audit procedures that are appropriate in the circumstances but not for the purpose of expressing an opinion on the effectiveness of the group’s internal control.

Anauditalsoinvolvesevaluating:• theappropriatenessofaccountingpoliciesusedandwhethertheyhavebeenconsistentlyapplied;• thereasonablenessofthesignificantaccountingestimatesandjudgementsmadebytheBoardofDirectors;• theadequacyofalldisclosuresinthefinancialstatements;and• theoverallpresentationofthefinancialstatements.

Independent Auditor’sReport

Chartered Accountants

Mighty River Power Limited Interim Report 2012 13

We did not examine every transaction, nor do we guarantee complete accuracy of the financial statements. In accordance withtheFinancialReportingAct1993,wereportthatwehaveobtainedalltheinformationandexplanationswehaverequired. We believe we have obtained sufficient and appropriate audit evidence to provide a basis for our audit opinion.

Responsibilities of the Board of DirectorsThe Board of Directors is responsible for preparing financial statements that:• complywithgenerallyacceptedaccountingpracticeinNewZealand;and•giveatrueandfairviewofthegroup’sfinancialposition,financialperformanceandcashflows.

The Board of Directors is also responsible for such internal control as it determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

TheBoardofDirectors’responsibilitiesarisefromtheState-OwnedEnterprisesAct1986andtheFinancialReportingAct1993.

Responsibilities of the AuditorWe are responsible for expressing an independent opinion on the financial statements and reporting that opinion to you based on our audit.

IndependenceWhencarryingouttheauditwefollowedtheindependencerequirementsoftheAuditor-General,whichincorporatetheindependencerequirementsoftheNewZealandInstituteofCharteredAccountants.

Partners and staff of Ernst & Young may deal with the group on normal terms within the ordinary course of trading activities of the business of the group. Since 31 December 2011, Ernst & Young has been engaged to provide assurance services in relation to prospective financial information. Other than these matters and the audit, we have no relationship with or interests in the company and group.

BRENT PENROsEErnst & YoungOnbehalfoftheAuditor-GeneralAuckland,NewZealand

Matters relating to the electronic presentation of the condensed consolidated interim audited financial statements This audit report relates to the condensed consolidated interim financial statements (“financial statements”) of Mighty River Power Limited (the company) and group for the period ended 31 December 2011 included on the company’s website. The Board of Directors is responsible for the maintenance and integrity of the company‘s website. We have not been engaged to report on the integrity of the company’s website. We accept no responsibility for any changes that may have occurred to the financial statements since they were initially presented on the website. The audit report refers only to the financial statements named above. It does not provide an opinion on any other information which may have been hyperlinked to or from the financial statements. If readers of this report are concerned with the inherent risks arising from electronic data communication they should refer tothepublishedhardcopyoftheauditedfinancialstatementsandrelatedauditreportdated27March2012to confirm the information included in the audited financial statements presented on this website. Legislation in New Zealand governing the preparation and dissemination of financial information may differ from legislation in other jurisdictions.

14 Mighty River Power Limited Interim Report 2012

Mercury Energy – Good Energy Tv Campaign

Condensed Consolidated InterimFinancialStatementsForthesixmonthsended31December2011

16 ConsolidatedIncomeStatement17 ConsolidatedStatementofComprehensiveIncome18 Consolidated Statement of Changes in Equity19 Consolidated Balance Sheet20 ConsolidatedCashFlowStatement21 NotestotheFinancialStatements

Mighty River Power Limited Interim Report 2012 15

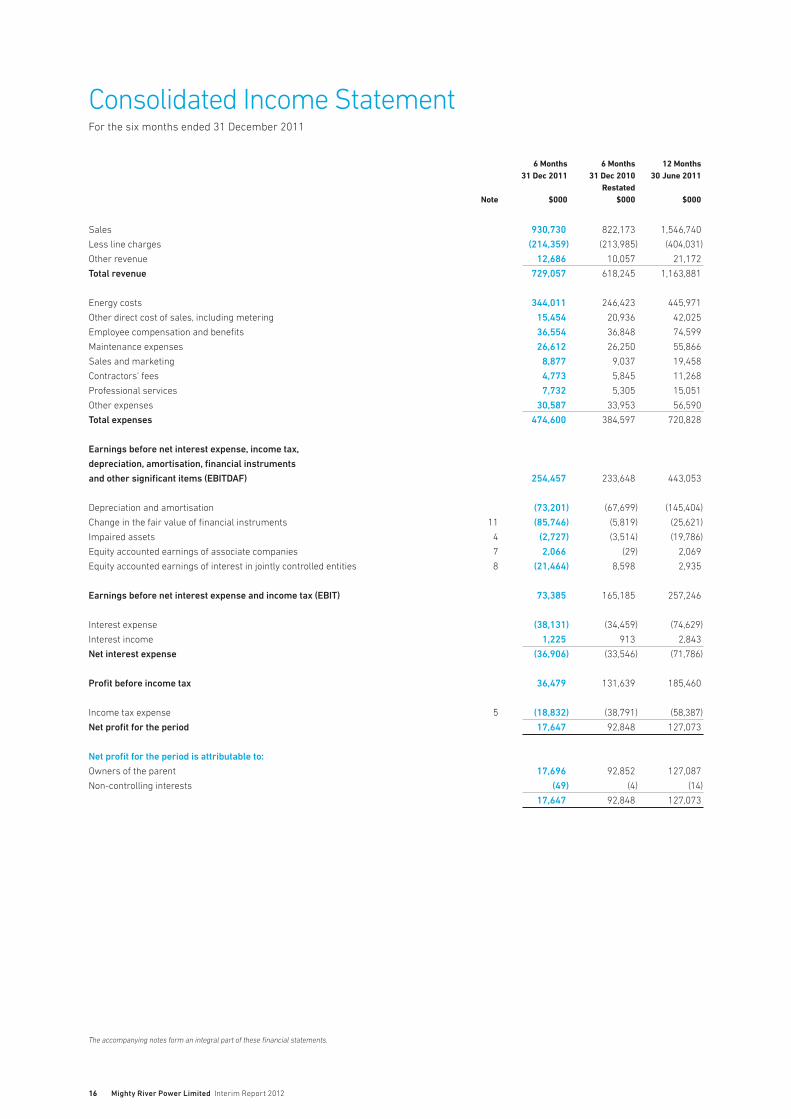

6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 Restated Note $000 $000 $000

Sales 930,730 822,173 1,546,740

Less line charges (214,359) (213,985) (404,031)

Other revenue 12,686 10,057 21,172

Total revenue 729,057 618,245 1,163,881

Energy costs 344,011 246,423 445,971

Other direct cost of sales, including metering 15,454 20,936 42,025

Employee compensation and benefits 36,554 36,848 74,599

Maintenance expenses 26,612 26,250 55,866

Sales and marketing 8,877 9,037 19,458

Contractors’ fees 4,773 5,845 11,268

Professional services 7,732 5,305 15,051

Other expenses 30,587 33,953 56,590

Total expenses 474,600 384,597 720,828

Earnings before net interest expense, income tax,

depreciation, amortisation, financial instruments

and other significant items (EBITDAF) 254,457 233,648 443,053

Depreciation and amortisation (73,201) (67,699) (145,404)

Change in the fair value of financial instruments 11 (85,746) (5,819) (25,621)

Impaired assets 4 (2,727) (3,514) (19,786)

Equityaccountedearningsofassociatecompanies 7 2,066 (29) 2,069

Equity accounted earnings of interest in jointly controlled entities 8 (21,464) 8,598 2,935

Earnings before net interest expense and income tax (EBIT) 73,385 165,185 257,246

Interest expense (38,131) (34,459) (74,629)

Interest income 1,225 913 2,843

Net interest expense (36,906) (33,546) (71,786)

Profit before income tax 36,479 131,639 185,460

Income tax expense 5 (18,832) (38,791) (58,387)

Net profit for the period 17,647 92,848 127,073

Net profit for the period is attributable to:

Owners of the parent 17,696 92,852 127,087

Non-controlling interests (49) (4) (14)

17,647 92,848 127,073

Consolidated Income StatementForthesixmonthsended31December2011

The accompanying notes form an integral part of these financial statements.

16 Mighty River Power Limited Interim Report 2012

6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 Restated $000 $000 $000

Net profit for the period 17,647 92,848 127,073

Other comprehensive income

Fairvaluerevaluationofhydroandgas-firedgenerationassets - - 219,000

Fairvaluerevaluationofothergenerationassets - (34,500) 193,250

Equity accounted share of movements in associates’ reserves (1,347) 1,320 (3,065)

Fairvaluemovementsonavailable-for-saleinvestmentreserve (429) (24) (858)

Movements in foreign currency translation reserve 6,181 (16,147) (31,146)

Cash flow hedges gain/(loss) taken to equity (1,261) (82,186) (107,445)

Income tax on items of other comprehensive income 472 34,175 (91,184)

Impact of tax rate change - - 6,797

Other comprehensive income/(loss) for the period, net of taxation 3,616 (97,362) 185,349

Total comprehensive income/(loss) for the period 21,263 (4,514) 312,422

Total comprehensive income/(loss) for the period is attributable to:

Owners of the parent 21,312 (4,510) 312,436

Non-controlling interests (49) (4) (14)

21,263 (4,514) 312,422

Consolidated Statement of Comprehensive IncomeForthesixmonthsended31December2011

The accompanying notes form an integral part of these financial statements.

Mighty River Power Limited Interim Report 2012 17

Available- Foreign for-sale currency Asset Cash flow Non- Issued Retained investment translation revaluation hedge controlling Total capital earnings reserve reserve reserve reserve interest equity $000 $000 $000 $000 $000 $000 $000 $000

Balance as at 1 July 2010 377,561 508,266 - 625 1,865,749 (63,390) 1592,688,970

Equity accounted share of movements in associates’

reserves - - - - (3,075) 4,395 - 1,320

Netlossonavailable-for-saleinvestments,netoftaxation - - (17) - - - - (17)

Fairvaluerevaluationofothergenerationassets,netof

taxation - - - - (24,840) - - (24,840)

Movementsinforeigncurrencytranslationreserve - - - (16,147) - - - (16,147)

Cashflowhedgesgain/(loss)takentoequity,netoftaxation - - - - - (57,678) - (57,678)

Other comprehensive income - - (17) (16,147) (27,915) (53,283) - (97,362)

Net profit for the period - 92,852 - - - - (4) 92,848

Total comprehensive income for the period - 92,852 (17) (16,147) (27,915) (53,283) (4) (4,514)

Non-controlling interest - - - - - - 2 2

Dividend - (30,300) - - - - - (30,300)

Balance as at 31 December 2010 (Restated) 377,561 570,818 (17) (15,522) 1,837,834 (116,673) 1572,654,158

Balance as at 1 January 2011 377,561 570,818 (17) (15,522) 1,837,834 (116,673) 1572,654,158

Fairvaluerevaluationofhydroandgas-firedgeneration

assets, net of taxation - - - - 153,300 - - 153,300

Fairvaluerevaluationofothergenerationassets,netof

taxation - - - - 160,115 - - 160,115

Equity accounted share of movements in associates’

reserves - - - - - (4,385) - (4,385)

Net loss on available-for-sale investments, net of taxation - - (583) - - - - (583)

Movements in foreign currency translation reserve - - - (14,999) - - - (14,999)

Cashflowhedgesgain/(loss)takentoequity,netoftaxation - - - - - (17,534) - (17,534)

Impactoftaxratechange - - (17) - 8,245 (1,431) - 6,797

Other comprehensive income - - (600) (14,999) 321,660 (23,350) - 282,711

Net profit for the period - 34,235 - - - - (10) 34,225

Total comprehensive income for the period - 34,235 (600) (14,999) 321,660 (23,350) (10) 316,936

Non-controlling interest - - - - - - 148 148

Dividend - (64,700) - - - - - (64,700)

Balance as at 30 June 2011 377,561 540,353 (617) (30,521) 2,159,494 (140,023) 2952,906,542

Balance as at 1 July 2011 377,561 540,353 (617) (30,521) 2,159,494 (140,023) 295 2,906,542

Equity accounted share of movements in associates’

reserves - - - - - (1,347) - (1,347)

Net loss on available-for-sale investments, net of taxation - - (310) - - - - (310)

Movements in foreign currency translation reserve - - - 6,181 - - - 6,181

Cash flow hedges gain/(loss) taken to equity, net of taxation - - - - - (908) - (908)

Other comprehensive income - - (310) 6,181 - (2,255) - 3,616

Net profit for the period - 17,696 - - - - (49) 17,647

Total comprehensive income for the period - 17,696 (310) 6,181 - (2,255) (49) 21,263

Non-controlling interest - - - - - - 90 90

Dividend - (45,700) - - - - - (45,700)

Balance as at 31 December 2011 377,561 512,349 (927) (24,340) 2,159,494 (142,278) 336 2,882,195

Consolidated Statement of Changes in EquityForthesixmonthsended31December2011

The accompanying notes form an integral part of these financial statements.

18 Mighty River Power Limited Interim Report 2012

31 Dec 2011 31 Dec 2010 30 June 2011 Restated Note $000 $000 $000

sHAREHOLDERs’ EQUITY

Issued capital 377,561 377,561 377,561

Reserves 2,504,298 2,276,440 2,528,686

Non-controlling interest 336 157 295

Total shareholders’ equity 2,882,195 2,654,158 2,906,542

AssETs

CURRENT AssETs

Cash and cash equivalents 43,185 41,821 28,722

Receivables 214,502 208,905 199,868

Inventories 22,245 24,349 23,015

Derivative financial instruments 11 18,114 19,564 20,100

Total current assets 298,046 294,639 271,705

NON-CURRENT AssETs

Property,plantandequipment 6 4,827,246 4,263,168 4,749,506

Intangible assets 45,287 33,202 38,821

Emissions units 794 - 429

Available-for-salefinancialassets 762 2,025 1,191

Investmentandadvancestoassociates 7 76,917 123,937 76,252

Investment in jointly controlled entities 8 84,500 109,241 98,970

Advances 10,470 11,399 10,877

Receivables 402 - 378

Derivative financial instruments 11 160,726 88,761 128,458

Total non-current assets 5,207,104 4,631,733 5,104,882

TOTAL AssETs 5,505,150 4,926,372 5,376,587

LIABILITIEs

CURRENT LIABILITIEs

Payables and accruals 201,268 178,774 180,431

Provisions 9 4,390 2,829 4,200

Current portion loans 12 6,234 5,657 12,081

Derivative financial instruments 11 27,600 23,692 24,498

Taxation payable 20,813 8,926 4,271

Total current liabilities 260,305 219,878 225,481

NON-CURRENT LIABILITIEs

Payables and accruals 21,366 - 21,298

Derivative financial instruments 11 444,100 308,802 374,524

Loans 12 1,051,398 982,941 973,400

Deferred tax 10 845,786 760,593 875,342

Total non-current liabilities 2,362,650 2,052,336 2,244,564

TOTAL LIABILITIEs 2,622,955 2,272,214 2,470,045

NET AssETs 2,882,195 2,654,158 2,906,542

ForandonbehalfoftheBoardofDirectorswhoauthorisedtheissueoftheFinancialStatementson27March2012.

Joan Withers Trevor Janes

Chair Deputy Chair

27March2012 27March2012

Consolidated Balance SheetAsat31December2011

The accompanying notes form an integral part of these financial statements.

Mighty River Power Limited Interim Report 2012 19

6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 Restated

Note $000 $000 $000

CAsH FLOWs FROM OPERATING ACTIvITIEs

Receipts from customers 731,419 580,169 1,123,166

Payments to suppliers and employees (473,221) (357,742) (691,283)

Interest received 1,225 1,515 2,534

Interest paid (42,675) (36,396) (78,578)

Taxes paid (31,378) (35,300) (63,013)

Net cash provided by operating activities 13 185,370 152,246 292,826

CAsH FLOWs FROM INvEsTING ACTIvITIEs

Acquisitionofproperty,plantandequipment (140,748) (87,709) (174,091)

Proceeds from sale of property, plant and equipment 2 772 312

Advancestoassociate - (16,139) (52,251)

Advancestoassociatesrepaid - 1,875 27,005

Repayment from joint venture partner 407 442 964

Investment in jointly controlled entities (2,188) (1,342) (4,130)

Acquisitionofintangibles (8,560) (6,141) (20,776)

Acquisitionofsubsidiaries - - 18,448

Dividends received 1,613 - 1,525

Proceeds from disposal of other non-current assets - - 600

Net cash used in investing activities (149,474) (108,242) (202,394)

CAsH FLOWs FROM FINANCING ACTIvITIEs

Proceeds from loans 30,000 260,212 266,212

Repayment of loans (6,000) (240,000) (240,000)

Dividends paid (45,700) (30,300) (95,000)

Net cash used in financing activities (21,700) (10,088) (68,788)

Net increase in cash and cash equivalents held 14,196 33,916 21,644

Net foreign exchange movements 267 - (827)

Cash and cash equivalents at the beginning of the period 28,722 7,905 7,905

Cash and cash equivalents at the end of the period 43,185 41,821 28,722

ConsolidatedCashFlowStatementForthesixmonthsended31December2011

The accompanying notes form an integral part of these financial statements.

20 Mighty River Power Limited Interim Report 2012

NotestotheFinancialStatementsForthesixmonthsended31December2011

NOTE 1. ACCOUNTING POLICIES

(1) Reporting entity

MightyRiverPowerLimitedisacompanyincorporatedinNewZealand,registeredundertheCompaniesAct1993andisareportingentityforthe

purposesoftheFinancialReportingAct1993.Thecondensedconsolidatedinterimfinancialstatementshavebeenpreparedinaccordancewiththe

FinancialReportingAct1993andtheCompaniesAct1993.

The condensed consolidated interim financial statements are for Mighty River Power Limited Group (the “Group”). The condensed consolidated

interim financial statements comprise the Company, its subsidiaries, associates and interests in jointly controlled assets and entities.

Mighty River Power Limited is wholly owned by Her Majesty the Queen in Right of New Zealand (the Crown). Consequently, the Company is bound

bytherequirementsoftheState-OwnedEnterprisesAct1986.

The liabilities of the Company are not guaranteed in any way by the Crown.

The Group’s principal activities are to invest in, develop and produce electricity from renewable and other energy sources and to sell energy and

energy related services and products to retail and wholesale customers.

2) Basis of preparation

(a) statement of compliance

ThesecondensedconsolidatedinterimfinancialstatementshavebeenpreparedinaccordancewithNewZealandGenerallyAcceptedAccounting

Practice(“NZGAAP”)asapplicabletointerimfinancialstatementsandasappropriatetoprofit-orientedentities.

ThesecondensedconsolidatedinterimfinancialstatementscomplywithNZIAS34InterimFinancialReportingandIAS34InterimFinancial

Reporting. These condensed consolidated interim financial statements do not include all the information and disclosures required in the annual

financial statements, and should therefore be read in conjunction with the annual financial statements for the year ended 30 June 2011, which

havebeenpreparedinaccordancewiththeNewZealandequivalentstoInternationalFinancialReportingStandardsandcomplywithInternational

FinancialReportingStandards.

(b) Accounting policies

The accounting policies and methods of computation are consistent with those of the annual financial statements for the year ended 30 June 2011,

as described in those annual financial statements.

(c) Estimates and judgements

ThepreparationofinterimfinancialstatementsinconformitywithNZIAS34andIAS34requiresManagementtomakejudgements,estimatesand

assumptionsthataffecttheapplicationofpoliciesandthereportedamountsofassetsandliabilities,incomeandexpenses.Actualresultsmay

differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which

the estimate is revised and in any future periods affected.

In particular, information about significant areas of estimation uncertainty and critical judgements in applying accounting policies that have the most

significant effect on the amount recognised in the financial statements are described below:

Generation plant and equipment

The Group’s generation assets are stated at fair value based on a periodical valuation by an independent valuer. The basis of the valuation is the net

present value of the future earnings of the assets, excluding any reduction for costs associated with restoration and environmental rehabilitation.

The major inputs and assumptions that are used in the valuation model that require judgment include the forecast of the future electricity price path,

sales volume forecasts, projected operational and capital expenditure profiles, capacity and life assumptions for each generation plant and discount

rates. The last revaluation was performed in June 2011. Management expect to engage an independent valuer in June 2012 to test whether carrying

values remain materially consistent with fair value.

Retail revenue

Management has exercised judgement in determining estimated retail sales for unread gas and electricity meters at balance date. Specifically this

involves an estimate of consumption for each unread meter, based on the customer’s past consumption history. The estimated balance is recorded

in sales and as an accrual balance within receivables.

Restoration and environmental rehabilitation

Liabilities are estimated for the abandonment and site restoration of areas from which natural resources are extracted. Such estimates are valued

at the present value of the expenditures expected to settle the obligation. Key assumptions have been made as to the expected expenditures to

remediate based on the expected life of the assets employed on the sites and an appropriate discount rate.

Mighty River Power Limited Interim Report 2012 21

Valuation of financial instruments

EnergycontractsarevaluedbyreferencetotheGroup’sfinancialmodelforfutureelectricityprices.Foreignexchangeandinterestratederivatives

are valued based on quoted market prices. Detailed information about assumptions and risk factors relating to financial instruments and their

valuation are included in the annual financial statements.

Impairment of non-financial assets

Assetsthathaveanindefinateusefullifearenotsubjecttoamortisationandaretestedannuallyforimpairment.Otherassetsthataresubjectto

amortisation are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable.

Evaluation and exploration assets are assessed for impairment when there is an indication that the carrying amount of the asset may exceed its

recoverable amount.

Deferred tax

In May 2010 the Government announced that tax depreciation deductions for buildings would be disallowed effective for the Group from 1 July 2011.

AsthereisnodefinitionofabuildingintheIncomeTaxAct,Managementhaveusedjudgement,andsoughtexpertindependentadvice,toassess

whether those generation assets, which have historically been classified as buildings, have been appropriately classified or whether they would

more appropriately be classified as plant. While the government has issued some additional guidance about what constitutes a building several

areaswereleftopenforfurtherdiscussion.AsaconsequenceManagementhasnotalteredthepositiontakenat30June2011.Intheeventthe

Inland Revenue Department disagrees with the position Management takes when filing the 2012 tax returns in 2013, then an additional deferred tax

liability and tax expense of $21.3 million would need to be recognised associated with the portion of the powerhouses that Management considered

should be more appropriately classified as plant.

(d) Functional and presentation currency

These financial statements are presented in New Zealand Dollars ($). The functional currency of Mighty River Power Limited and all its subsidiaries,

apart from Mighty Geothermal Power Limited and its direct subsidiaries and PT ECNZ Services Indonesia, is New Zealand Dollars. The functional

currency of PT ECNZ Services Indonesia and Mighty Geothermal Power Limited, and its subsidiaries except the German subsidiaries, is the United

States Dollar. The German subsidiaries have a functional currency of Euro. The financial statements of these entities have been translated to the

presentationcurrencyfortheseGroupAccounts.Allfinancialinformationhasbeenroundedtothenearestthousand.

(e) seasonality of operations

Theenergybusinessoperatesinanenvironmentthatisdependentonweatherasoneofthekeydriversofsupplyanddemand.Fluctuations

in seasonal weather patterns, particularly over the short term, can have a positive or negative effect on the reported result. It is not possible to

consistently predict this seasonality and some variability is common.

(f) segment reporting

Operating segments are reported in a manner consistent with the internal reporting provided to the chief operating decision-maker. The chief

operating decision-maker, who is responsible for allocating resources and assessing performance of the operating segments, has been identified

as the Chief Executive.

NOTE 2. SEGMENT REPORTING

Identification of reportable segments

The operating segments are identified by Management based on the nature of the products and services provided. Discrete financial information

about each of these operating businesses is available to the chief operating decision-maker on at least a monthly basis.

Operating segments are aggregated into reportable segments only if they share similar economic characteristics.

Types of products and services

Wholesale

The wholesale segment encompasses activity associated with the production of energy from all power stations, the purchase of energy related

products and services, and the sale of power to the retail segment, generation development activities together with activities such as risk and asset

management. The wholesale segment is exposed to volatility in wholesale prices which may result in significant fluctuations in segmental results

from year to year.

Retail

The retail segment encompasses activity associated with the purchase of power from the wholesale segment and the subsequent sale of energy

and energy related services and products to customers. The retail segment is also exposed to fluctuation in wholesale prices relating to energy

purchases, electricity sales at spot and the settlement of electricity price derivatives. The results of wholesale price volatility will have a partially

offsetting impact between the wholesale and retail segments.

Other segments

Otheroperatingsegmentsthatarenotconsideredtobereportingsegmentsaregroupedtogetherinthe“OtherSegments”column.Activities

include metering, upstream gas and other corporate support activities.

NotestotheFinancialStatementsForthesixmonthsended31December2011

22 Mighty River Power Limited Interim Report 2012

Accounting Policies and inter-segment transactions

The accounting policies used by the Group in reporting segments are the same as those contained in note 1 to the annual financial statements and

inthepriorcomparativeperiods.TheChiefExecutiveassessestheperformanceoftheoperatingsegmentsonameasureofEBITDAF.Segment

EBITDAFrepresentsprofitearnedbyeachsegmentexclusiveofanyallocationofcentraladministrationcosts,depreciationandamortisation,share

of profits of associates and jointly controlled entities, change in fair value of financial instruments, impairment of exploration expenditure, finance

costs and income tax expense.

Transactions between segments are carried out on an arm's length basis. Other Wholesale Retail segments Total

six months ended 31 December 2011 $000 $000 $000 $000

Total segment revenue 626,107 410,080 21,229 1,057,416

Inter-segment revenue (311,633) - (16,726) (328,359)

Revenue from external customers 314,474 410,080 4,503 729,057

segment EBITDAF 227,875 41,462 (14,880) 254,457

segment Assets 4,888,676 178,462 438,012 5,505,150

Other Wholesale Retail segments Total

six months ended 31 December 2010 (Restated) $000 $000 $000 $000

Totalsegmentrevenue 494,539 378,292 18,275 891,106

Inter-segmentrevenue (258,141) - (14,720) (272,861)

Revenuefromexternalcustomers 236,398 378,292 3,555 618,245

segment EBITDAF 183,061 63,153 (12,566) 233,648

segment Assets 4,426,519 152,176 347,120 4,925,815

Other Wholesale Retail segments Total

Twelve months to 30 June 2011 $000 $000 $000 $000

Totalsegmentrevenue 905,867 750,734 37,894 1,694,495

Inter-segmentrevenue (500,069) - (30,545) (530,614)

Revenuefromexternalcustomers 405,798 750,734 7,349 1,163,881

segment EBITDAF 336,483 133,661 (27,091) 443,053

segment Assets 4,836,993 208,836 330,758 5,376,587

Reconciliation of segment revenue to the income statement 6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 $000 $000 $000

Total segment revenue 1,057,416 891,106 1,694,495

Inter-segment sales elimination (328,359) (272,861) (530,614)

Total revenue per the income statement 729,057 618,245 1,163,881

Reconciliation of segment assets to total assets 6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 $000 $000 $000

Segment assets 5,505,150 4,925,815 5,376,587

Current tax assets - - -

Total assets 5,505,150 4,925,815 5,376,587

NotestotheFinancialStatementsForthesixmonthsended31December2011

Mighty River Power Limited Interim Report 2012 23

NOTE 3. UNDERLYING EARNINGS

Underlying earnings after tax is presented to enable stakeholders to make an assessment and comparison of underlying earnings after removing

significant one-off items, impairments and the change in the fair value of financial instruments.

6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 Restated $000 $000 $000

Net profit for the period 17,647 92,848 127,073

Change in the fair value of financial instruments 85,746 5,819 25,621

Change in the fair value of financial instruments of associate entities (374) (214) 1,429

Change in the fair value of financial instruments of jointly controlled entities 20,601 (9,854) 1,962

Impaired assets 2,727 3,514 19,786

Adjustmentsbeforeincometaxexpense 108,700 (735) 48,798

Income tax expense on adjustments (24,668) (2,736) (12,874)

Impact of deferred tax rate change through the consolidated income statement - - (823)

Adjustmentsafterincometaxexpense 84,032 (3,471) 35,101

Underlying earnings after tax 101,679 89,377 162,174

Tax has been applied on all taxable adjustments at 28% or 30% in comparative periods.

Note 15 provides details of the restatement in the 31 December 2010 comparative period.

NOTE 4. IMPAIRED EXPENDITURE

6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 $000 $000 $000

Impaired property, plant and equipment - - 11,476

Impaired exploration and development expenditure 3,604 3,514 4,933

Impaired intangible asset - - 2,500

Impaired investment in associate (877) - 877

Total impaired assets 2,727 3,514 19,786

NotestotheFinancialStatementsForthesixmonthsended31December2011

24 Mighty River Power Limited Interim Report 2012

NOTE 5. INCOME TAX EXPENSE

6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 Restated

$000 $000 $000

Income tax expense

Profit before income tax 36,479 131,639 185,460

Prima facie income tax expense at 28% (comparative periods: 30%) on profit before tax (10,214) (39,492) (55,638)

Increase/(decrease) in income tax due to:

•effectoftaxratechangeondeferredtax - - 823

•shareofassociates’taxpaidearnings 578 (9) 621

•shareofjointlycontrolledentities’taxpaidearnings (6,010) 2,579 881

•foreignentities’taxlossesnotrecognisedfordeferredtax (3,725) (2,209) (3,792)

•capitalloss - - (1,440)

•otherdifferences 345 (6) 164

Over/(under) provision in prior period 194 346 (6)

Income tax expense attributable to profit from ordinary activities (18,832) (38,791) (58,387)

Represented by:

Current tax expense (46,535) (44,185) (69,935)

Deferred tax expense recognised in the consolidated income statement 27,703 5,394 11,548

Total income tax expense (18,832) (38,791) (58,387)

Note 15 provides details of the restatement in the 31 December 2010 comparative period.

NOTE 6. PROPERTY, PLANT AND EQUIPMENT

6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 Restated $000 $000 $000

Assetsacquiredatcost 152,956 57,341 143,360

Net book value of assets disposed 28 1,072 1,039

Gain/(loss) on disposal (26) (300) (727)

Assetrevaluations - (34,500) 412,250

Note 15 provides details of the restatement in asset valuation in the 31 December 2010 comparative period.

NOTE 7. INVESTMENT AND ADVANCES TO ASSOCIATES 6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 Restated $000 $000 $000

Balance at the beginning of the period 76,252 113,614 113,614

Additionsduringtheperiod - 16,148 52,251

Equity accounted earnings 2,066 (29) 2,069

Equity accounted share of movements in reserves (1,347) 1,320 (3,065)

Dividends received during the period (1,613) - (1,525)

Repayment of advances during the period - (1,875) (27,006)

Loans converted to equity by GeoGlobal Partners 1 Limited Partnership - - (54,289)

Accruedinterestonadvances - 166 339

Exchange movements 682 (5,407) (5,259)

Impaired investment in associate reversed 877 - -

Impaired investment in associate - - (877)

Balance at the end of the period 76,917 123,937 76,252

NotestotheFinancialStatementsForthesixmonthsended31December2011

Mighty River Power Limited Interim Report 2012 25

NOTE 8. INVESTMENTS IN JOINTLY CONTROLLED ENTITIES

6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 Restated $000 $000 $000

Balance at the beginning of the period 98,970 111,926 111,926

Additionsduringtheperiod 2,188 2,601 4,130

Equity accounted earnings (21,464) 8,598 2,935

Exchange movements 4,806 (13,884) (20,021)

Balance at the end of the period 84,500 109,241 98,970

NOTE 9. PROVISIONS

6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 $000 $000 $000

Balance at the beginning of the period 4,200 2,673 2,673

Provisions made during the period 9 - 1,215

Movement in effect of discounting 181 156 312

Balance at the end of the period 4,390 2,829 4,200

Provisions have been recognised for the abandonment and subsequent restoration of areas from which geothermal resources have been extracted.

The provision is calculated based on the present value of management’s best estimate of the expenditure required, and the likely timing of

settlement. The increase in provision resulting from the passage of time (the discount effect) is recognised as an interest expense.

NOTE 10. DEFERRED TAX

6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 Restated $000 $000 $000

Balance at the beginning of the period (875,342) (789,594) (789,594)

Current period changes in temporary differences affecting tax expense 27,703 5,394 10,725

Current period changes in temporary differences affecting reserves 1,853 23,607 (104,258)

Balance transferred to joint venture partner - - 165

Change in tax rate recognised in tax expense - - 823

Change in tax rate recognised in reserves - - 6,797

Balance at the end of the period (845,786) (760,593) (875,342)

Note 15 provides details of the restatement in the 31 December 2010 comparative period.

NotestotheFinancialStatementsForthesixmonthsended31December2011

26 Mighty River Power Limited Interim Report 2012

NOTE 11. DERIVATIVE FINANCIAL INSTRUMENTS

Assets Liabilities Assets Liabilities Assets Liabilities 31 Dec 2011 31 Dec 2011 31 Dec 2010 31 Dec 2010 30 June 2011 30 June 2011 Restated Restated Restated Restated $000 $000 $000 $000 $000 $000

Interest rate derivatives 31,291 239,418 16,381 121,554 21,106 144,431

Cross currency interest rate derivatives 19,161 - - 16,030 - 30,287

Cross currency interest rate derivatives – margin - 9,507 - 8,636 - 12,037

Electricity price derivatives 125,878 216,910 91,915 178,487 127,448 201,863

Foreignexchangeratederivatives 2,510 5,865 29 7,787 4 10,404

178,840 471,700 108,325 332,494 148,558 399,022

Current 18,114 27,600 19,564 23,692 20,100 24,498

Non-current 160,726 444,100 88,761 308,802 128,458 374,524

178,840 471,700 108,325 332,494 148,558 399,022

The current/non-current split of the fair value of interest rate derivatives has been restated and the treatment of movements in the fair value of

cross currency interest rate swaps has also been restated. Refer to note 15 for details.

Interest rate derivatives, short term low value foreign exchange rate derivatives, and short term low value electricity price derivatives, while

economichedges,arenotdesignatedashedgesunderNZIAS39butaretreatedasatfairvaluethroughprofitandloss.Allotherforeignexchange

rateandelectricitypricederivatives(excepttheTuaropakiPowerCompanyFoundationHedge,VirtualAssetSwapwithMeridian,theNgaAwaPurua

outagecontractandtheGenesisswaption)aredesignatedascashflowhedgesunderNZIAS39.Crosscurrencyinterestrateswaps,whichareused

to manage the combined interest and foreign currency risk on borrowings issued in foreign currency, have been split into two components for the

purposes of hedge designation. The hedge of the benchmark interest rate is designated as a fair value hedge and the hedge of the issuance margin

is designated as a cash flow hedge.

The changes in fair values of derivative financial instruments recognised in the income statement and equity are summarised below:

Income Income Income statement statement statement Equity Equity Equity 6 Months 6 Months 12 Months 6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 31 Dec 2011 31 Dec 2010 30 June 2011 Restated Restated $000 $000 $000 $000 $000 $000

Cross currency interest rate derivatives 49,302 (16,030) (30,141) - - -

Borrowings – fair value change (47,638) 9,399 19,084 - - -

1,664 (6,631) (11,057) - - -

Interest rate derivatives (84,802) 3,745 (13,822) - - -

Cross currency interest rate swaps – margin - - - 3,001 (8,636) (11,604)

Electricity price derivatives (691) (1,474) 2,397 (15,766) (41,696) (56,851)

Foreignexchangederivatives 108 (3) (588) 11,504 (31,854) (38,990)

Income tax on changes taken to equity - - - 353 24,508 32,233

(83,721) (4,363) (23,070) (908) (57,678) (75,212)

Ineffectiveness of cash flow hedges (2,025) (1,456) (2,551)

Total fair value movements recognised

through the consolidated income statement (85,746) (5,819) (25,621)

NotestotheFinancialStatementsForthesixmonthsended31December2011

Mighty River Power Limited Interim Report 2012 27

NOTE 12. LOANS

31 Dec 2011 31 Dec 2010 30 June 2011 Restated $000 $000 $000

Notional value of bank loans 771,235 740,660 747,081

Notional value of US Private Placement 260,212 260,212 260,212

Deferred financing costs (2,369) (2,875) (2,728)

Fairvalueadjustments 28,554 (9,399) (19,084)

Carrying value of loans 1,057,632 988,598 985,481

Current 6,234 5,657 12,081

Non-current 1,051,398 982,941 973,400

1,057,632 988,598 985,481

Fordetailsoftherestatementpleaserefertonote15.

In September 2011 the Group increased an existing facility with the Bank of Tokyo-Mitsubishi by $50 million to $200 million which matures in

December2015.ThisincreasestheGroup’sfacilitiesto$1,360millionwithanaveragedurationof5.9years.

Subsequent to 31 December 2011 the Group established a $200 million Commercial Paper programme which is fully backed by committed and

undrawn bank facilities. The Group also entered into $200 million of new bank facilities to address the refinancing of $200 million Retail Bonds

whichwillmatureinMay2013.ThisfurtherincreasestheGroup’sfacilitiesto$1,560million.RefertoNote17forfurtherdetails.

NOTE 13. RECONCILIATION OF PROFIT FOR THE PERIOD TO NET CASH FLOWS FROM OPERATING ACTIVITIES

6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 Restated $000 $000 $000

Net profit for the period 17,647 92,848 127,073

Items classified as investing/financing activities

• Fixed,intangibleandinvestmentassetcharges (5,573) (2,447) (6,870)

• Loancharges 370 1,108 1,835

Non-cash items

Depreciation and amortisation 73,201 67,699 145,404

Net loss on sale of property, plant and equipment 26 300 727

Change in the fair value of financial instruments 85,746 5,819 25,621

Impaired assets 2,727 3,514 19,786

Movement in effect of discounting on long-term provisions 190 156 312

Share of earnings of associate companies (2,066) 29 (2,069)

Share of earnings of jointly controlled entities 21,464 (8,598) (2,935)

Other non-cash items 504 909 1,996

Net cash provided by operating activities before change in assets and liabilities 194,236 161,337 310,880

Change in assets and liabilities during the period:

• Increaseintradereceivablesandprepayments (9,611) (33,676) (21,402)

• Decrease/(increase)ininventories 771 (4,123) (2,790)

• Increaseintradepayablesandaccruals 12,508 25,209 10,880

• Increase/(decrease)inprovisionfortaxation 16,550 (1,670) (6,325)

•(Decrease)/increase in deferred taxation (29,084) 5,169 1,583

Net cash inflow from operating activities 185,370 152,246 292,826

NotestotheFinancialStatementsForthesixmonthsended31December2011

28 Mighty River Power Limited Interim Report 2012

NOTE 14. RELATED PARTY TRANSACTIONS

Ultimate shareholder

TheultimateshareholderofMightyRiverPowerLimitedistheCrown.AlltransactionswiththeCrownandotherState-OwnedEnterprisesareat

arm’s length and at normal market prices and on normal commercial terms.

Transactions with related parties

Notes15,16,17and18fromthe30June2011annualfinancialstatementsprovidedetailsofsubsidiaries,associates,jointlycontrolledassetsand

jointlycontrolledentities.Alloftheseentitiesarerelatedparties.Thefollowingoffshoregeothermaldevelopmententitieshavebeenincorporated

subsequent to 30 June 2011 and are also related parties:

Erdwärme Chiemgau GmbH

ErdwärmeAyingGmbH

ErdwärmeAlzGmbH

Erdwärme Isar GmbH

Astheseareconsolidatedfinancialstatementstransactionsbetweenrelatedpartieswithinthegrouphavebeeneliminated.Consequently,only

those transactions between entities which have parties external to the Group have been reported below:

Transaction Value 6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 $000 $000 $000

Management fees and service agreements received (paid)

Associates (4,560) (4,884) (8,077)

Jointly controlled assets 2,429 2,407 4,817

Energy contract settlements received (paid)

Associates (183) (429) (3,618)

Jointly controlled assets 205 (3,102) (25,610)

Interest income (expense)

Associates - 166 339

Jointly controlled assets 863 1,029 1,929

Forthetermsandconditionsoftheserelatedpartytransactionspleaserefertonote29ofthe30June2011annualfinancialstatements.

key management personnel

key management personnel compensation comprised: 6 Months 6 Months 12 Months 31 Dec 2011 31 Dec 2010 30 June 2011 $000 $000 $000

Directors fees 317 251 502

Salary and other short term benefits of the Chief Executive and Senior Management 2,004 1,805 3,245

2,321 2,056 3,747

Other transactions with key management personnel

Directors and employees of the Group deal with Mighty River Power Limited as electricity consumers on normal terms and conditions within the

ordinary course of trading activities.

Anumberofkeymanagementpersonnelprovidedirectorshipservicestootherentitiesaspartoftheiremploymentwithoutreceivinganyadditional

remuneration.AnumberoftheseentitiestransactedwiththeGroupinthereportingperiod.Thetermsandconditionsofthetransactionswithkey

management personnel were conducted on an arms length basis.

NotestotheFinancialStatementsForthesixmonthsended31December2011

Mighty River Power Limited Interim Report 2012 29

NOTE 15. CORRECTION OF ERRORS, REVISIONS OF ACCOUNTING ESTIMATES AND RECLASSIFICATIONS

Restatements impacting the income statement or other comprehensive income

Asreportedinthe30June2011financialstatementsthejointventurepartnerintheRotokawaandNgaAwaPuruaJointVenturesnotified

theirintentiontoexerciseanoptiontoacquireanadditional10%interestinthejointventureswhichwouldreducetheGroup’sinterestto65%.

Managementanticipatethisoccurringinthenextsixmonths.AsaconsequenceareductioninthecarryingvalueintheGroup’sinterestinjointly

controlled assets of $34.5 million, with an offsetting reduction in the Group’s share of the asset revaluation reserve net of deferred tax, was

recognised. This adjustment was not undertaken in the previously reported 31 December 2010 balance sheet so this has been adjusted to align

with the 30 June 2011 treatment.

The Group entered into forward starting cross-currency interest rate swaps in November 2010 as a hedge of the US Private Placement issued in

December2010.Thehedgeaccountingforthesetypesofderivativesiscomplex.Aprudentpositionwastakeninthe31December2010interim

financial statements which, upon further analysis, proved to be incorrect based on the final treatment recognised in the 30 June 2011 annual

financial statements. Consequently an adjustment has been recognised as at 31 December 2010 which reduces the fair value loss in the income

statementby$4,373,000,reducesthecashflowhedgereserveof$7,419,000andincreasesthecarryingvalueoftheforeigncurrencydebtby

$3,046,000.Theassociateddeferredtaxadjustmentsimpactingtaxexpenseandthecashflowhedgereservewhichisreportednetofdeferred

tax were also recognised.

Asat31December2010theGrouphadtorecogniseitsearningsfromjointlycontrolledentitiesbasedonunauditedfinancialstatements.Audit

adjustments were subsequently recognised, primarily relating to the fair value measurement of interest rate derivatives. The Group’s share of

earnings from interests in jointly controlled entities recognised through the income statement has been increased by $4,593,000 ($3,905,000 of