interest payments to contractors lou etta milstead march 2005 code h

TRANSCRIPT

INTEREST PAYMENTS TO CONTRACTORS

Lou Etta Milstead

March 2005

Code H

2

Why does the Government Pay Interest?

When does the Government Pay Interest to Contractors?

Impact on NASA

3

Why does the Government Pay Interest?

• Prescribed by Congress– Prompt Payment Act of 1982, Revisions made in 1988,

Final Rule Issued September 1999• Adopted, after comment, in Code of Federal Regulations

(CFR), Part 1315 of Title 5

– Debt Collection Improvement Act (DCIA) of 1996• Office of Management and Business (OMB) proposed final

revisions in June 1998

• Requires Payment by Electronic Funds Transfer (EFT)

• Financial Management Services (FMS) is responsible for U.S. Treasury implementation of DCIA

4

Why does the Government Pay Interest?(cont.)

• Good Business Practices– Fundamental Fairness to Contractors– Cash Flow Needs of Contractors

• Contractors must finance shortfalls

• Should receive compensation when we pay late

5

When does the Government Pay Interest to Contractors?

• FAR 52.232-25 Prompt Payment Clause– PAYMENT is to be made 30 days after receipt of

a PROPER INVOICE from Contractor, or 30 days after Government ACCEPTANCE of supplies delivered or services performed. Except for a Final Invoices, when the payment is subject to contract settlement actions.

6

PAYMENT - Due Dates • The later of the 30th day after the designated billing office

receives a proper invoice, or the 30th day after acceptance of supplies delivered or services performed;

• Final Invoices, when subject to contract settlement actions, acceptance occurs on the effective date of contract settlement;

• If invoices are not required (i.e. lease payments), due dates shall be specified in contract;

• Construction invoices are normally paid within 15 days;• Certain Food Products (Perishables) are exempted and are

normally paid not later than the 7th day after product delivery.

7

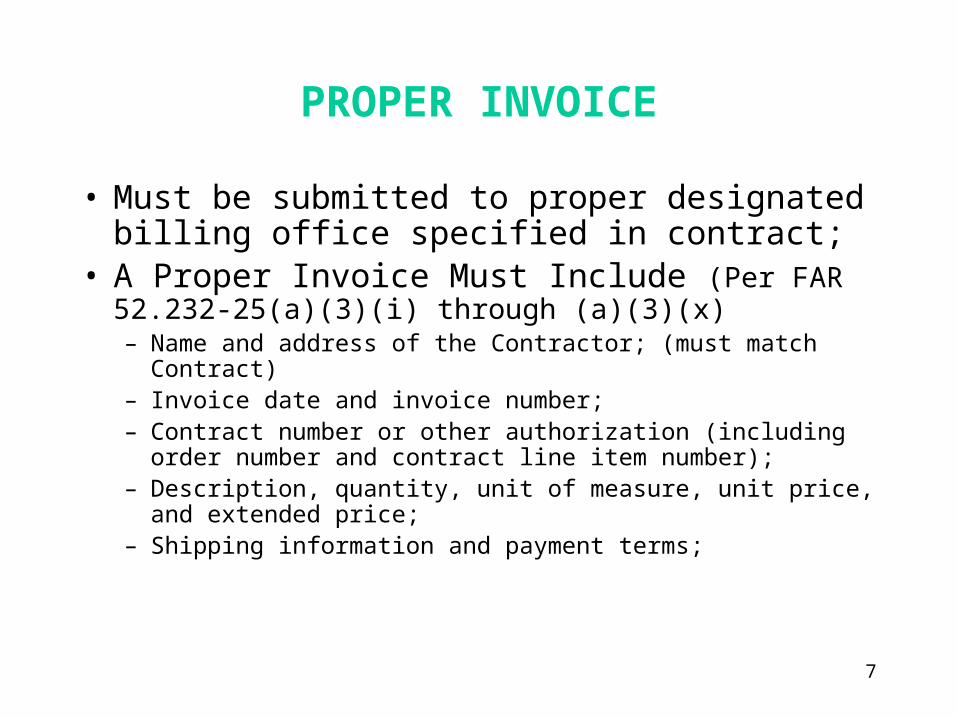

PROPER INVOICE

• Must be submitted to proper designated billing office specified in contract;

• A Proper Invoice Must Include (Per FAR 52.232-25(a)(3)(i) through (a)(3)(x)– Name and address of the Contractor; (must match Contract)– Invoice date and invoice number;– Contract number or other authorization (including order number

and contract line item number);– Description, quantity, unit of measure, unit price, and extended

price;– Shipping information and payment terms;

8

PROPER INVOICE (cont.)

– Name and address of Contractor official to whom payment is to be sent;

– Name, title, phone number, and mailing address of person to notify in the event of a defective invoice;

– Taxpayer Identification Number (TIN). Only required if required in the contract;

– EFT banking information;– Any other information or documentation required by the contract

• If invoice does not comply with requirements listed above, the designated billing office is required to return it within 7 days after receipt with the reason why it is not a proper invoice.

9

PROPER INVOICE (cont)

• Cost Contracts– Cost Invoices and Fee Invoices must be

separate invoices.• Administration of cost invoices is delegated to

DCAA on all cost type contracts.– DCAA Reviews and accepts or rejects COST invoices,

unless Contractor has written authorization from DCAA to submit invoices directly.

• Administration of fee invoices is retained by Center on cost + fee (fixed, award, incentive) type contracts.

– Contracting Officer Reviews and accepts or rejects FEE invoices.

10

ACCEPTANCE

• (unless otherwise specified in the contract) Government acceptance is deemed to have occurred constructively on the 7th day after the Contractor delivers the supplies or performs the services in accordance with the terms and conditions of the contract, unless there is a disagreement over quantity, quality, or Contractor compliance with a contract provision.

11

FINANCE OFFICE PROCESS

• The Accounts Payable Office– Receives and dates all invoices;– Reviews all invoices for proper content;– Logs in all invoices (into SAP);– Verifies;

• goods receipt (documented electronically in SAP system by receiving department)

• services performed (from Contracting Officer via payment authorization sheet)

– Posts invoices for payment; • Payments are made on date specified in posting

12

FINANCE OFFICE GUIDELINES

• Treasury EFT Rule (31 CFR Part 208) • Issued by Department of Treasury, Financial Management

Service

• Implements Debt Collection Improvement Act (DCIA) of 1996

• Prompt Payment Act Regulations (5 CFR Part 1315)• Issued by the Office of Management and Business

• EFT Rule (48 CFR Parts 13, 15, 32, and 52)• 48 CFR = Federal Acquisition Regulations

• NASA’s Financial Management Manual• Guidance/Policy manual for Finance Office

13

PROCUREMENT’SRESPONSABILITIES

• Contents of Contract (Uniform Contract Format - Part I - Schedule)

– Proper Clauses • Matrix found at FAR Subpart 52.301

– Acceptance- see FAR Part 46. (Section E of Contract)

– Billing Information-see FAR Part 32 (Section G of Contract)

• Finance Office receives copy of Award Document (Contract) and all Modifications in a timely manner.

• Informing Contractor of their responsibilities as stated in Contract.

14

PROCUREMENT (cont.)

• Assuring Contractor receives Automated Clearing House (ACH) form SF 3831 (or Center equivalent) which must be completed and sent to the Finance Office.– ACH form states correct banking and company

information (CAGE Code, TIN number, etc.) for proper payment of invoices through Electronic Funds Transfer (EFT) by the paying office.

• Responding to the Finance Office in a timely manner– Rejecting invoices with documented reasons for non-

payment; or – authorizing payments.

15

Impact on NASA

• I was unable to find out the Amount of Interest Paid by NASA to Contractors in 2004. (however, consider these figures)

• 9 NASA Centers process invoices– GSFC Processes Invoices for Headquarters, Jet

Propulsion Lab (JPL), and GSFC.• GSFC processed an average of 2,350 Invoices per Month in

2004. (12 x 2,350 = 28,200 Invoices per year)• In the month of August 2004 paid invoices for GSFC & JPL

totaled $175,342,341.00 (this amount does not include paid invoices for Headquarters)

16

INTEREST

• Rate paid is stipulated by Department of Treasury, Financial Management Services– Updated Quarterly

• 1/1/05 – 3/31/05 Rate is 4.25%

• Accrues daily (compounded interest)

17

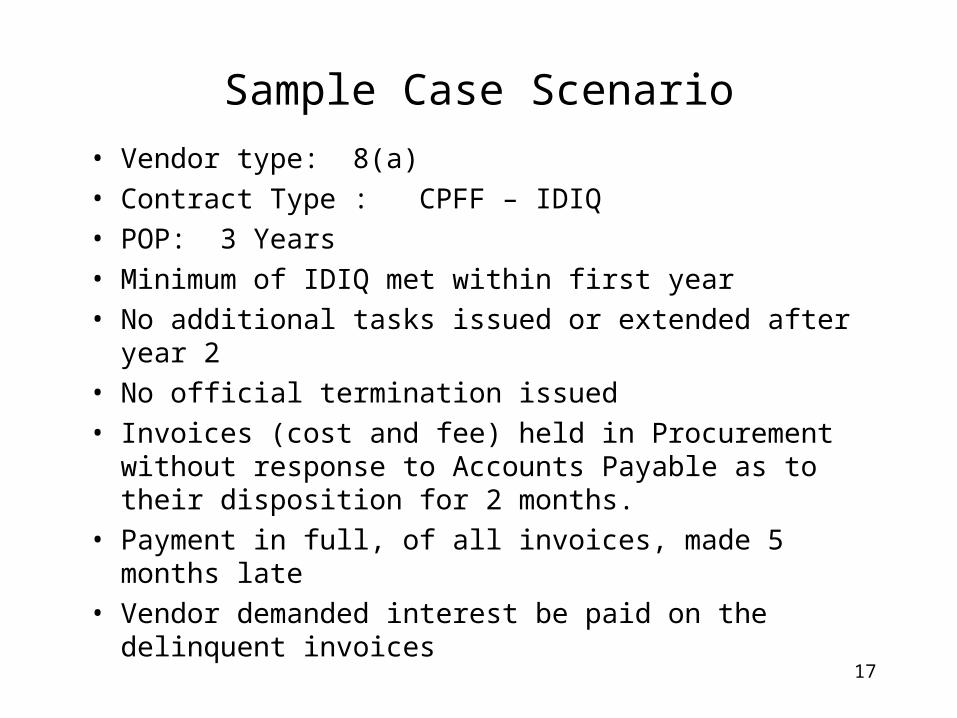

Sample Case Scenario

• Vendor type: 8(a)

• Contract Type : CPFF – IDIQ

• POP: 3 Years

• Minimum of IDIQ met within first year

• No additional tasks issued or extended after year 2

• No official termination issued

• Invoices (cost and fee) held in Procurement without response to Accounts Payable as to their disposition for 2 months.

• Payment in full, of all invoices, made 5 months late

• Vendor demanded interest be paid on the delinquent invoices

18

Questions & Answers

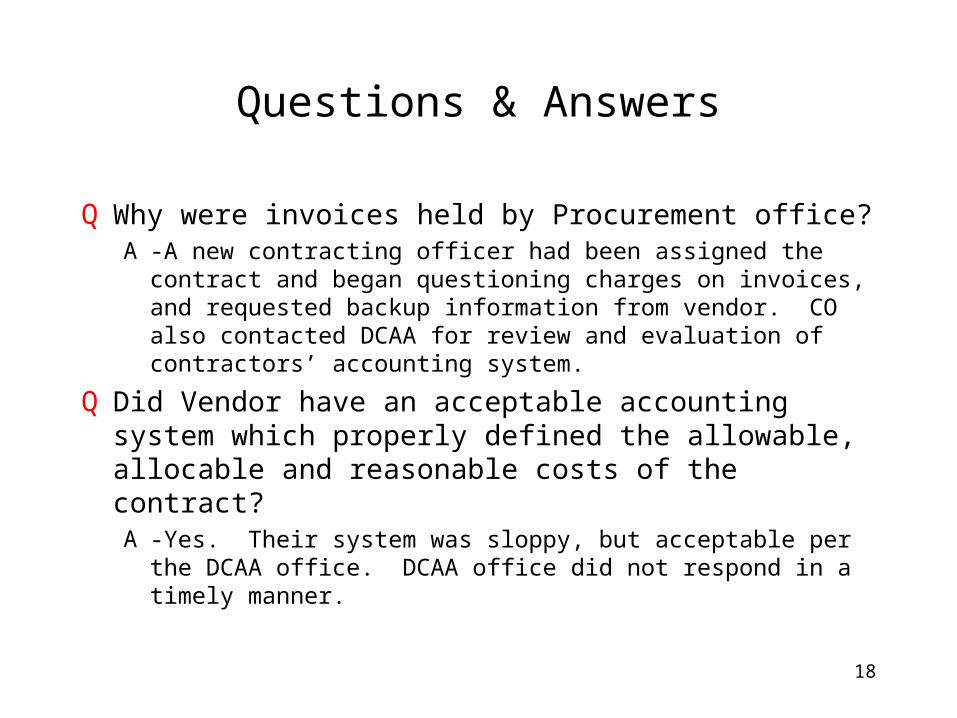

Q Why were invoices held by Procurement office? A -A new contracting officer had been assigned the contract and

began questioning charges on invoices, and requested backup information from vendor. CO also contacted DCAA for review and evaluation of contractors’ accounting system.

Q Did Vendor have an acceptable accounting system which properly defined the allowable, allocable and reasonable costs of the contract? A -Yes. Their system was sloppy, but acceptable per the DCAA

office. DCAA office did not respond in a timely manner.

19

Questions & Answers

Q Had prior invoices been accepted for the same type work?A -Yes, 46 prior invoices had been paid as invoiced.

Q Why did it take 5 months to make the decision?A -Heavy Contract Case load.

A -Low priority set on this contract action, although continuing contact was made by CO with vendor and DCAA office.

Q Why wasn’t the Accounts Payable Office contacted earlier?– Contracting officer presumed the proper actions were being taken.

20

Final Disposition

• Vendor demanded interest be paid on the delinquent invoices.– Withholding payments created financial pressure in his

business

– Upset that future orders were not forthcoming

• Accounts Payable paid interest in the amount of $1,132.76 .– Involved 7 invoices

– Days late ranged from 67 to 160

21

COMMENTS/JUSTIFICATION FROM FINANCE OFFICE

• NASA’s Financial Management Manual– “Interest penalties will be paid for interim payments under

cost-reimbursement service contracts awarded on or after 12/15/2000 that are paid more than 30 days after a proper invoice has been received from the vendor. Interim payments under cost-reimbursement service contracts are treated as invoice payments”

• Prompt Payment Act– “Agencies are required to pay an interest penalty to

contractors whenever they make payments under cost-reimbursement service contracts more than 30 days after the agency receives a proper invoice for payment from the contractor”

22

COMMENTS/JUSTIFICATION (cont.)

• Contract Finance Payments– Defined as “an authorized disbursement of monies prior to

acceptance of goods or services including advance payments, progress payments based on cost, progress payments (other than constructions contracts) based on a percentage or stage of completion, payments on performance-based contracts and interim payment on cost-type contract. Contract financing payments do not include invoice payments, payments for partial deliveries, or lease and rental payments”

– “Invoices that were paid were for services already rendered, and the dispute centered around the amount owed for these services, this does not constitute an advance of monies in any form.”

• Invoices & Acceptance– “Invoices in question were not returned to the vendor

while a final decision was being made, therefore, automatic acceptance of the services occurred.”

23

IFMP

• The automated Accounting System contains essential information for the administration of contracts and for responding to Vendors.

• When Accounts Payable moves to the NASA Shared Services Center your only instant/verifiable information will be online.

• It is possible, with further refinement of the financial system, that interest payments will be calculated and paid automatically.

24

Lessons Learned

• Be sure all scenarios are covered by your contract.

• Be aware of your responsibilities.• Be conscientious about reviewing invoices

and contacting the COTR and Accounts Payable when there is a question about the amounts being claimed.

• Practice “good business” policies.

25

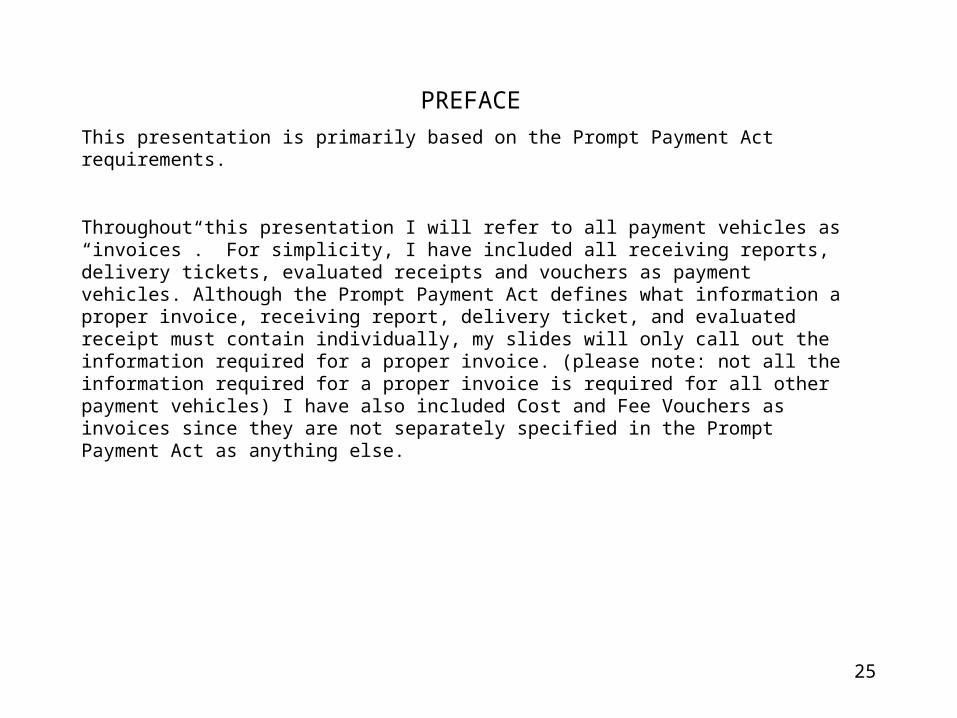

PREFACE

This presentation is primarily based on the Prompt Payment Act requirements.

Throughout this presentation I will refer to all payment vehicles as “invoices”. For simplicity, I have included all receiving reports, delivery tickets, evaluated receipts and vouchers as payment vehicles. Although the Prompt Payment Act defines what information a proper invoice, receiving report, delivery ticket, and evaluated receipt must contain individually, my slides will only call out the information required for a proper invoice. (please note: not all the information required for a proper invoice is required for all other payment vehicles) I have also included Cost and Fee Vouchers as invoices since they are not separately specified in the Prompt Payment Act as anything else.