integration of reporting system using accounting

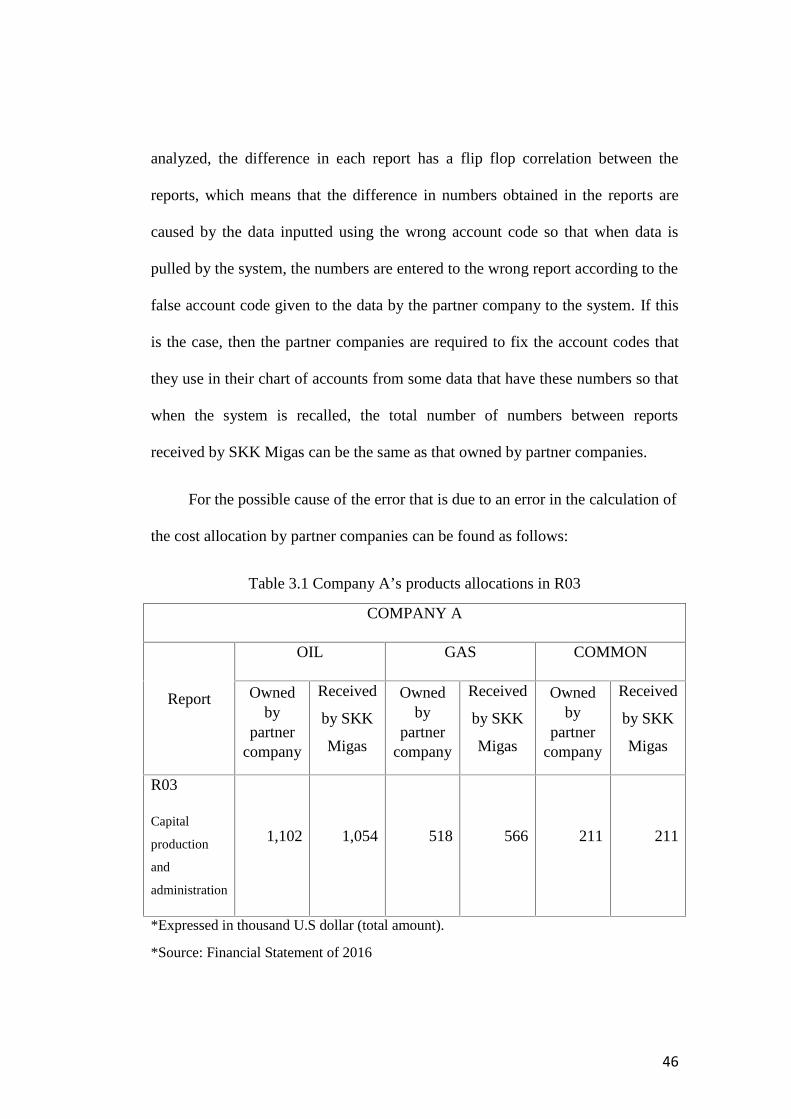

TRANSCRIPT

i

INTEGRATION OF REPORTING SYSTEM USING

ACCOUNTING INFORMATION SYSTEM FOR

FINANCIAL REPORT IN SKK MIGAS

SKRIPSI

By:

Riano Reza Gozali Tjahyono

008201400088

Presented to: The Faculty of Economics, President University

In partial fulfillment of the requirements

For

Bachelor’s Degree in Accounting

PRESIDENT UNIVERSITY

Cikarang Baru – Bekasi

Indonesia

2018

ii

PANEL OF EXAMINERS APPROVAL SHEET

Herewith, the Panel of Examiners declare that the skripsi entitled “The Effects

and Contributions of the Integrated of Reporting System Using Accounting

Information System for Financial Performance in SKK Migas” submitted by

Riano Reza Gozali Tjahyono majoring in Accounting, Faculty of Economics was

assessed and proved to have passed the Oral Examination on March 2018.

Chair, Panel of Examiner,

…………………………………..

Andi Ina Yustina, M.Sc., CIBA, CMA

Examiner 1

…………………………………...

Setyarini Santosa, SE., MAFIS., Ak.

Examiner 2

……………………………………

Drs. Asep Supriatna, MBA.

iii

CONSENT FOR INTELLECTUAL PROPERTY RIGHT

Title of Skripsi: The Effects and Contributions of the Integrated of Reporting

System Using Accounting Information System for Financial

Performance in SKK Migas

1. The Writer hereby assigns to President University the copyright to the

Contribution named above whereby the University shall have the

exclusive right to publish the Contribution and translations of it wholly or

in part throughout the world during the full term of copyright including

renewals and extensions and all subsidiary rights.

2. The Writer retains the right to re-publish the preprint version of the

Contribution without charge and subject only to notifying the University

of the intent to do so and to ensuring that the publication by the University

is properly credited and that the relevant copyright notice is repeated

verbatim.

3. The Writer retains moral and all proprietary rights other than copyright,

such as patent and trademark rights to any process or procedure described

in the Contribution.

4. The Writer guarantees that the Contribution is original, has not been

published previously, is not under consideration for publication elsewhere

and that any necessary permission to quote or reproduce illustrations from

iv

another source has been obtained (a copy of any such permission should

be sent with this form).

5. The Writer guarantees that the Contribution contains no violation of any

existing copyright or other third-party right or material of an obscene,

indecent, libellous or otherwise unlawful nature and will indemnify the

University against all claims arising from any breach of this warranty.

6. The Writer declares that any named person as co-author of the

Contribution is aware of this agreement and has also agreed to the above

warranties.

Name Riano Reza Gozali Tjahyono

Date

Signature

v

DECLARATION OF ORIGINALITY

I hereby declare that the skripsi entitled “The Effects and Contributions of the

Integrated of Reporting System Using Accounting Information System for

Financial Performance in SKK Migas” is originally written by myself based on

my own research and has never been used for any other purpose before.

I, therefore, request for Oral Defense of the Skripsi.

Cikarang, Indonesia, 15 March 2018

Researcher,

Riano Reza Gozali Tjahyono

008201400088

vi

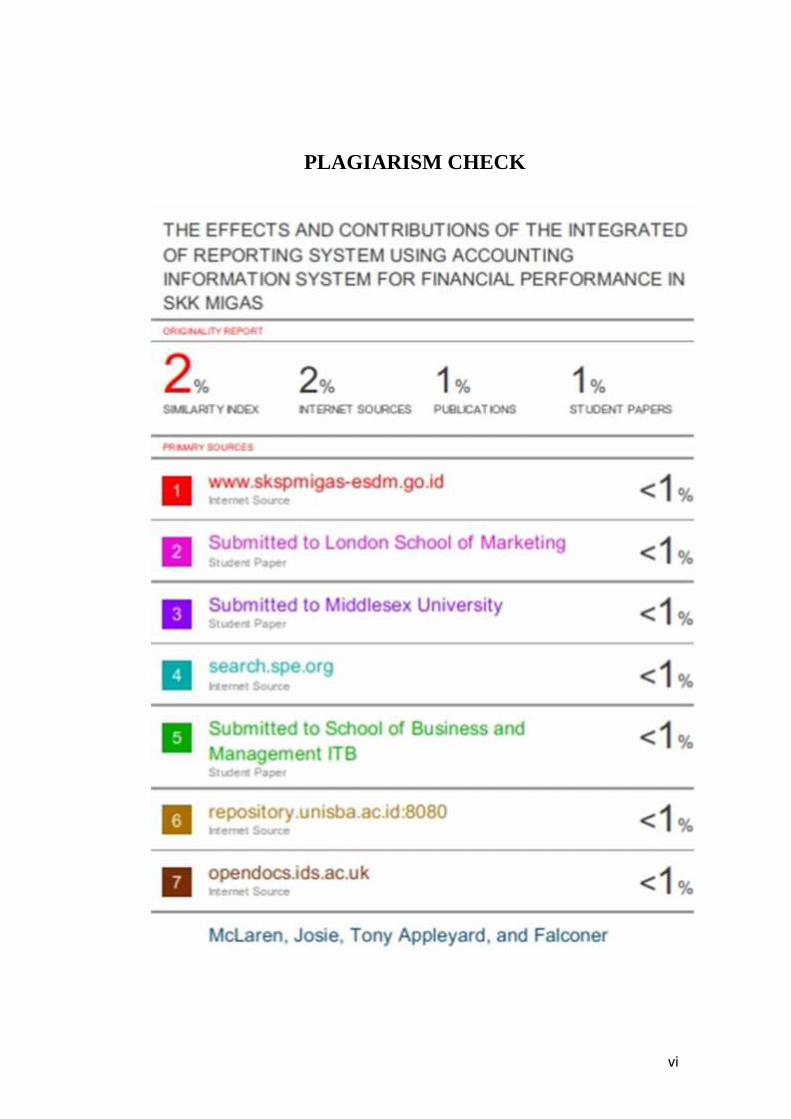

PLAGIARISM CHECK

vii

viii

ix

ACKNOWLEDGEMENT

First of all, writer would like to express my gratitude to God Almighty for all the

inclusion and strength He has given me in order to finish my research just in time.

Writer also want to thank some people who have been really supportive and

always give me a passion in completing my research:

1. My family who has always been an encouragement and reminder during

the process of completion of this research so writer can be on time.

2. My mentor, Mr. Asep Supriatna, who is always patient and has been very

helpful in accelerating the process of my thesis.

3. To my accounting classmates and friends who make thesis together that

helped each other and work together, especially for Pinto Raynanda,

Ghifari, Melisa Dengah, Frederika (Rere), Anju, and others which writer

can not say one by one.

4. To my juniors in accounting who have helped in reminding and

encouraging to immediately complete the research, especially Novia

Amanda D., and others that writer can not say one by one.

5. Friends who have been willing to give me a chance to occupy his room so

that writer can do guidance and do my research, namely Ricky Arya P. and

Timothy D.

x

6. Friends of PUSC, especially its PRM (Karina, Amar, Prisca, Krina, Zahra,

Zilfa) who always support me to complete this research as soon as

possible.

7. To all my classmates and also lecturers who have always reminded and

asked when the completion of this research that became my trigger in

completing this research as soon as possible.

Writer realize that this research is still far from perfection. Thus, any

recommendations and suggestions are very welcome in order to establish a better

research in the future.

xi

TABLE OF CONTENT

COVER PAGE .........................................................................................................i

PANEL OF EXAMINERS APPROVAL SHEET.................................................. ii

CONSENT FOR INTELLECTUAL PROPERTY RIGHT ................................... iii

DECLARATION OF ORIGINALITY ................................................................... v

PLAGIARISM CHECK......................................................................................... vi

ACKNOWLEDGEMENT ..................................................................................... ix

TABLE OF CONTENT ......................................................................................... xi

ABSTRACT............. ............................................................................................ xiv

INTISARI.................. ............................................................................................. xv

CHAPTER 1 - INTRODUCTION.......................................................................... 1

1.1 Research Background ............................................................1

1.2 Research Questions................................................................9

1.3 Research Objectives.............................................................11

1.4 Significance Of The Study...................................................11

1.5 Thesis Organization .............................................................12

CHAPTER 2 - LITERATURE REVIEW............................................................. 14

2.1 Accounting Information System..........................................14

2.2 AIS with Financial Performance..........................................15

xii

2.3 Reporting System.................................................................17

2.4 Extensible Business Reporting Language (XBRL) .............18

CHAPTER 3 - METHODOLOGY ....................................................................... 20

3.1 Data Collection ....................................................................20

3.2 Company Profile ..................................................................21

CHAPTER 4 – RESULT AND DISCUSSIONS.................................................. 24

4.1 Current Condition of the Company .....................................24

4.2 The Causes of the Implementation of System .....................28

4.3 Discussion About Implementing the Reporting System......31

4.3.1 Things Need to be Prepared by SKK Migas During

System Development Process ............................................ 31

4.3.2 Stages of System Development Process ................. 32

4.3.3 Steps in Generating Report Using the System ........ 35

4.3.4 Ways to Validate Data Between Data Sent by Partner

Companies with Those Received by SKK Migas .............. 38

4.3.5 Constraints that Hinder the Process of Developing and

Implementing Reporting System ....................................... 54

4.3.6 Benefits from Implementing the Reporting System 56

CHAPTER 5 – CONCLUSIONS, RECOMMENDATIONS, AND

LIMITATIONS.................................................................... 59

xiii

5.1 Conclusions..........................................................................59

5.2 Recommendations................................................................60

5.3 Limitation.............................................................................61

LIST OF REFERENCES ...................................................................................... 62

APPENDIX............... ............................................................................................ 64

xiv

ABSTRACT

The purpose of the writer in making this research is to compare about theconditions and issues of the company when the company use manual method andwhen they implement AIS for making report purpose. Also to analyze thepreparation and what need to be learnt before proceed and during the developmentof the system.

In making this research, writer uses primary data collection method toanalyze the events, problems, and results from before and after implementation ofreporting system. The methods that writer use to collect the data are observation,interviews, voice taping, and testing data. The period of time used by the author tobe examined is the time at which the company has not and after implementing thereporting system.

The conclusion of this research is how important for company to implementthe reporting system because by using this system, they can maximaize theirfunction as supervisor and analyzer. Their function can be maximized due to thesystem that has been automatically pulled all the data needed to perform theanalysis, then no need the process of data request anymore that spend time. Thereare some factors that can make the process of development system more eficientand faster, they are experienced and skilled employees, sufficient number ofemployees, and fixed regulations and rules. SKK (Satuan Kontraktor Kerja)Migas and partner companies play a crucial role for before, during, and after theprocess of system development.

After looking at the factors above, the writer want to provide somerecommendations for the future of the company, that is the need for additionalworkers, regular training, adequate budget addition, limiting the frequency ofchanging rules and decisions.

Keywords: Accounting system, financial reporting, reporting system, XBRL.

xv

INTISARI

Tujuan penulis dalam membuat penelitian ini adalah untuk membandingkankondisi dan permasalahan perusahaan ketika perusahaan menggunakan metodemanual dan pada saat sudah mengimplementasikan AIS untuk pembuatan laporan.Juga untuk mengetahui hal-hal yang perlu dipersiapkan dan dipelajari sebelummelanjutkan dan selama pengembangan sistem.

Dalam pembuatan penelitian ini, penulis menggunakan metodepengumpulan data primer untuk menganalisa kejadian, permasalahan, dan hasildari sebelum dan sesudah implementasi sistem pelaporan. Metode yang penulisgunakan untuk mengumpulkan data adalah observasi, wawancara, rekaman suara,dan pengujian data. Periode waktu yang digunakan oleh penulis untuk penelitianini adalah waktu dimana perusahaan sebelum dan setelah menerapkan sistempelaporan.

Kesimpulan dari penelitian ini adalah betapa pentingnya perusahaanmenerapkan sistem pelaporan karena dengan menggunakan sistem ini, merekadapat memaksimalkan fungsinya sebagai supervisor dan penganalisis. Fungsimereka bisa dimaksimalkan karena sistem yang telah otomatis menarik semuadata yang dibutuhkan untuk melakukan analisis sehingga tidak perlu lagi prosespermintaan data yang menghabiskan waktu. Ada beberapa faktor yang dapatmembuat proses pengembangan sistem lebih efisien dan cepat, mereka adalahkaryawan yang berpengalaman dan terampil, jumlah pegawai yang cukup, danperaturan dan peraturan yang tetap. SKK (Satuan Kontraktor Kerja) Migas danperusahaan partner memiliki peran penting pada saat sebelum, selama, dan setelahproses pengembangan sistem.

Setelah melihat faktor-faktor di atas, penulis ingin memberikan beberaparekomendasi untuk masa depan perusahaan, yaitu kebutuhan akan tenaga kerjatambahan, pelatihan reguler, penambahan anggaran yang memadai, pembatasanfrekuensi perubahan peraturan dan keputusan.

Kata kunci: sistem akuntansi, pelaporan finansial, sistem pelaporan, XBRL.

1

CHAPTER 1

INTRODUCTION

1.1Research Background

In general, Information and Control Technology, or better known as ICT,

has helped to improve the quality in professional services. Information and

Control Technology has become valuable tools and assets of company that are

needed to arrange and produce an accurate data about the company itself.

Information and Control Technology has a wide scope, for the example

Information and Control Technology can be used for preparing the information

and control tools to maintain about infrastructure, human resource, training,

policies, financial conditions, business processes, and the others.

In this research, I decide to analyze Information and Control Technology

which is used to arrange and provide the information and as a supervision tool

over financial performance. Information and Control Technology which is used to

provide information and help to perform control of financial condition better

known by the name AIS (Accounting Information System). AIS can be interpreted

as an information system that shows changes in corporate accounting activities

where the data used are financial transactions that are converted into information

using system procedures and become reports that show the overall results. In

2

order to improve the quality of financial and accounting information generated

and provided by the company, a good Accounting Information System is needed

to be used, and the result can show as accurate information and has high reliability

measurement. A good and mature approach of AIS used to improve financial and

accounting information is closely related to the management quality of the

company. For example, if a company does not have good management quality it

will be difficult for the company to create good Accounting Information System,

because in order to create good AIS, the company must be able to compose a

complete first business process that is used and implemented, then it can be seen

clearly business processes of the company. The use of AIS in organizational and

social factors owned by the company can also be used to determine the AIS that is

computerized within different financial institutions in Indonesia

The fair value used by Special Task Force for Upstream Oil and Gas

Business Activities Republic of Indonesia (Satuan Kerja Khusus Pelaksana

Kegiatan Usaha Hulu Minyak dan Gas Bumi or SKK Migas) to evaluate the

performance of partner companies is to look at the historical cost of partner

companies sent to the SKK Migas, and then conducted a review with the

provisions of the cut-off date that has been determined. While the accounting

treatment used to calculate asset recording and asset classification of partner

companies is to use the concept of production sharing contract (PSC) Accounting.

However, in production sharing contract there is no formulation to regulate the

fair value of assets, so that the government together with the SKK Migas needs to

3

make adjustments and alignment between the principles used in government in the

management of public assets with the production sharing contract scheme used.

One of the highlights of the production sharing contract concept is the

transfer of ownership of Indonesian government’s assets from partner companies.

In the production sharing contract concept, the transfer of ownership is not

completed at the wellhead, but at the export stage. Here explains that SKK Migas

uses a concept whereby the government will recognize the asset not when it is

formed (example, a wellhead is built), but when the asset is able to produce and

release oil or gas (example, the wellhead succeeds in removing the oil sought

from within earth). With the use of the production sharing contract concept,

ownership and control are located and controlled by the government, and the

distribution of the percentage of proceeds between the government and the partner

company in accordance with what has been discussed and mutually agreed

between the two parties. Within the concept of production sharing contract, there

is a known mechanism of calculation called “cost recovery”, which is a system

that organizes and processes data on the costs used by a partner company during

the mining activities that can be claimed to SKK Migas. Before approving the

claim of “cost recovery”, SKK Migas will undertake an audit upon “cost

recovery”.

Cost recovery is the operational costs spent by a partner company that can

be reimbursed by the Indonesian government. Cost recovery itself has its own

rules that are set in the WP&B (Work Program and Budget). The simple concept

that is owned by cost recovery is what costs can be accepted by the partner

4

company must be in accordance with what has been planned and budgeted in

accordance with the agreement with SKK Migas. Costs that may be included in

cost recovery are all costs used by the partner company for the operational

activities (development and exploration) along with supporting activities as

agreed between SKK Migas and all partner companies to be claimed and replaced

(paid) by government through SKK Migas. One of the basic rules that serve as a

guideline in the cost that can be claimed by the Indonesian government is the

regulations contained in UUD 1945 pasal 33 ayat 3 “bumi, air dan kekayaan alam

yang terkandung didalamnya dikuasai oleh negara dan dipergunakan untuk

sebesar-besarnya kemakmuran rakyat (Constitution Article 33 paragraph 3 "the

earth, water, and natural resources contained therein are controlled by the state

and used for the greatest prosperity of the people").

There is example of production sharing contract and cost recovery

implementation. A mutually agreed share between the government of Indonesia

and the partner company is 70:30, meaning that 70% of the oil and gas yields

already earned will be given to the government of Indonesia and the remaining

30% may be taken by partner company and may be traded on behalf of their

company. Also cost recovery is included in this production sharing contract

agreement if indeed the process of extracting and withdrawing oil and gas

conducted by the partner company is successful. Therefore, if a partner company

has managed to withdraw some oil and gas, then the company must divide

according to the agreement in the contract that is 70:30. Then the partner company

can calculate the cost that used to process the drilling and lifting of oil and gas, if

5

the cost used is 20% by the partner company, then the Indonesian government will

pay by using the oil that has been divided, and the government will only get 50%

of (50% obtained from 70% minus 20% of cost of production by partner

companies that paid by the government/ cost recovery). All of the above sharings

of the costs and products is calculated and given not in the form of money, but in

the form of oil and gas that has been withdrawn by the partner company.

This paragraph tells about examples of cost recovery rules and terms.

Foreign partner companies are allowed to undertake and work on projects within

Indonesia to extract and take natural oil and gas resources. If we take point of

view from the results caused by excavation and drilling activities by partner

companies, these activities are actually activities that damage the environment

owned by Indonesia. Therefore, the partner companies which majorities come

from outside countries are required to be able to prosper the people living around

the excavation and drilling areas, as well as restoring the environment when it is

completed. As an example of this is the human labor used to build drill and

withdraw the products are must be local people living around the oil drilling area

and since this activity is included for the welfare of the people of Indonesia, the

cost of the workers used can be put into cost recovery. There are also other rules

that partner companies are required to contribute to the welfare of local

communities around their projects, such as school construction, regional

environmental infrastructure development, and so forth. Actually, partner

companies are allowed to use experts from abroad, but there are special terms and

conditions that are given if indeed want to recruit workers from abroad, like

6

workers from abroad are people who are proficient and experts in the field and

such expertise indeed cannot be found and not owned by local people. This means

that if there is actually a cost of skills training for foreign workers, then the cost

will not be allowed to be included into the budget of cost recovery, except for

language training.

Other example of rules that determine a fee may be included in cost

recovery or not are costs that can be claimed to the government as cost recovery

are operational costs used for successful drilling and withdrawal of oil and gas. In

other words, if it turns out that a project conducted by a partner company to drill

and withdraw oil and gas is fails, or commonly referred to as dry hole project,

then the operational costs will be borne by the company itself, because the shares

are using oil yields and gas that is successfuly obtained, if it fails, then nothing

can be shared. This also makes the partner companies will do a serious

observation and exploration and companies cannot just do random drilling

activities.

Those calculations and rules in production sharing contract and cost

recovery are then used as calculations and components used to form the report to

be prepared and produced by The Integrated Operating System of Financial

Quarterly Report (or reporting system).

The Integrated Operating System Financial Quarterly Report ("SOT [Sistem

Operasi Terpadu] FQR") is a collaborative activity between the Accounting

Division and the System Information (MSI) Division of SKK Migas, with the

7

support of partner companies related to the withdrawal of quarterly financial

statements and transactions of the partner companies’ financial system to SKK

Migas using a combination of accounts, components of Chart of Account or CoA

(Cost Center, WBS, etc.), using XBRL data exchange standard to maintain the

accuracy or validity of data / information from partner contractor companies to

SKK Migas. With integrated operating system (reporting system), partner

companies' financial statements and quarterly data will always be available on

SKK Migas regularly and can be scheduled as needed.

The calculations used in this reporting system, which use the rules of

Production Sharing Contract and cost recovery, are also run using an application

called XBRL with its own component, the taxonomy.

XBRL (Extensible Business Reporting Language) is an external file used to

help the delivery process and as storage of financial data using a programming

language that can be modified and shaped according to the needs of the user by

using coding method. Actually, a technology like XBRL already exists, but not

yet have this XBRL-resistant security level, so this is what distinguishes XBRL

from other technologies. XBRL has encryption layers that can store financial data

and sent securely to other parties. One of the security components owned by

XBRL is taxonomy. In general, XBRL’s sending process outline as follows: the

data you want to send is drawn by XBRL, then converted by XBRL into

programming language, then in XBRL the data will be encrypted, and finally the

data is sent to destination.

8

There are many components that owned by XBRL. However, the best

known and commonly used is taxonomy. Taxonomy is a component in XBRL that

has a function as the rules used to form the processing of data stored in XBRL.

For example, in column A in Microsoft Excel entitled "Company's Name" must

be filled with text format, whereas in column B which titled "Date" must be filled

with the format number with the order of DD/MM/YYYY, the next column which

titled "Type of Data" must be filled between actual or budget, and others.

By looking at the function of the taxonomy, it can be assessed if the

taxonomy is the one who determines the instance file will produce what kind of

financial data. Taxonomy will read the data which retrieved by XBRL whether it

is in accordance with the criteria that it has or not, if not then XBRL will send

back the data to the partner company, as the sender, and the notification that

stating the data failed to pass XBRL criteria and cannot be sent to SKK Migas.

The example is the column titled "Date" in Microsoft Excel provided from three

different companies, 1) "DD / MM / YY", 2) "MM / DD / YY", and 3) "YY / DD

/ MM ". But the taxonomy criterion is "DD / MM / YYYY", and then the three

companies will get a failed notification from XBRL for the withdrawal of its data

and cannot be forwarded to SKK Migas.

The process of forming XBRL until it is ready for use by SKK Migas is as

follows:

1. The first stage is the development of the taxonomy of XBRL because

this taxonomy is the component used to put the criteria of such data so

9

that the data before it is sent can be adjusted first as desired by the user.

In SKK Migas, this taxonomy is tasked to standardize the data, meaning

that the Chart of Accounts of a different partner companies are changed

to Chart of Account owned by SKK Migas which has the same account

activity characteristic.

2. The next stage is the establishment of the interface system. What is

meant by the interface system is a system built for how to draw data

from AIS owned by partner companies, then connected and delivered to

the destination of SKK Migas’ AIS.

Then combine between the first and second stage, the process called the

establishment of XBRL instance. For example, the column entitled "Chart of

Account of Company" drawn by XBRL is then mapped and paired to SKK

Migas's Chart of Account with the same nature of activity, resulting in what is

called an XBRL instance. So that the meaning of the XBRL instance is the

process of altering and processing data drawn by the system in accordance with

the criteria and rules contained in XBRL using taxonomy to release the desired

results by the user and then when it is completed it will be sent to the user.

1.2Research Questions

The role of accountants under computerized AIS becomes different, easier

and more efficient in collecting the data needed to perform further analysis steps.

By using a computerized system, accountants can reduce manual efforts made by

people and can reduce the likelihood of human errors, as well as repeating

activities that make them less effective and efficient. However, by using AIS, it

10

should be noted also that the required skill must be owned by the accountant, the

skills in processing and processing data using a computer, for example is the skill

in operating Microsoft excel applications and so on the most basic. Also the

accountant is expected to have the skills in maintaining, updating, and backups of

data owned in the computer. Accountants are also expected to be able to

understand the environment and consider the characteristics of AIS in each

process they undergo, because each company has the character and character of its

AIS respectively, and it will also have an impact on the design of the accounting

system and the selection of what kind of internal control that can be relied upon

and suitable for the company. Because of this transformation, in information

systems it is important to keep pace with developments in accounting by the fact

that most companies rely on automated systems and move away from manual

systems, but there are still questions to ask about reliability, accuracy of

information, and the ability to generate information and financial data to be used

to carry out control and oversight functions.

RQ1. What are the differences between using manual steps and using AIS in

generating financial reports?

RQ2. How AIS can generate financial statements more quickly and efficiently?

RQ3. How does the accounting system owned by the company can produce

accurate financial statements and have high reliability?

RQ4. What is the effect on performance of report making? Is there a significant

effect?

11

1.3Research Objectives

The objective of this research is to analyze and to study the issues that can

arise with no implementation of AIS in the institution at the present time. Also to

realize what employees have to learn when the development of AIS on process

and when it has been implemented. Every point that employees need to aware can

be known and determined by looking at the case studies that occur in the company

itself and the areas that are still, noticeable, required development of AIS. This

study contains the current AIS condition of the institution used to collect, produce,

and supervise financial statement report along with its business process. Here we

will also get the ideas about the differences between before and after

implementing AIS.

1.4Significance Of The Study

This research is expected to contribute to the parties concerned and be used as a

recommendation for the future:

1. Institution’s management

This research will certainly help the company in finding the right system used by

this institution. Also this research can help find out what aspects need to be

improved and automated using a computerized system.

2. Internal Accountants of Institution

Especially for the internal accountant owned by the institution, with the

implementation of AIS, it will be very helpful in the process while making the

12

finalization of financial statements, both revenue and expense. These

developments of Accounting Information System will make the work more

efficient when it will do the audit control, because by using the AIS, it will reduce

the chance of human errors and also facilitate the collection of data needed to

perform the audit.

3. Financial Performance

By having a good AIS and functioning thoroughly, the financial report and audit

quality control produced by the institution will be more accurate as well as less of

human errors so that will make the report and audit quality control can be more

reliable and trustworthy. Thus, the institution can improve the financial

performance rapidly because of the data processing more quickly, precisely, and

efficiently.

1.5Thesis Organization

In this research, I divided into five parts of works, they are Chapter 1 until

Chapter 5. In the first chapter, there are five sub-chapters, they are research

background, research question, research objectives, significance of study, and

thesis organization. Research background tells the reader about general idea that

explain about the basic knowledge of the main topic of research. Research

question contains of brief introduction about writer’s analysis and what questions

that writer want to get the answers after conduct this research. Research objectives

gives glince about what is the purpose of writer making this paper. Significance of

13

study explains what are the benefits that writer can give by making this paper for

other parties.

Chapter 2 is about literature review and there are two sub-chapter, they are

theoretical review and company profile. Theoretical review states about theories

that writer used as the basis in doing the research, then the writer can analyze

about the previous researches that have been conducted. Company profile tells

about the background and biography of the company that used as the object of this

research. Chapter 3 is about methodology which explains to the reader how the

writer can get and collect the information and data for doing this survey.

Chapter 4 contains of the data that writer gets from the respondent and all

the analysis results which writer did after collected the data and processing them.

In chapter 5, the writer summarizes of the research by provides with conclusion,

recommendations for the object of research, also there is limitation that writer has

in preparing this paper.

14

CHAPTER 2

LITERATURE REVIEW

2.1Accounting Information System

Accounting Information System (AIS) has a lot of understanding. However,

according to Surmeli (2006), AIS is an information system that has a function to

direct a change that occurs to assets, capital, as well as debts owned by the

company, where the data source that created the change is obtained from the

transformation of data from financial transactions into information by passing the

processing stage and summarizing the merged information.

The main advantages gained from using a good and maximized Accounting

Information System are to improve the ease of conducting transaction supervision

by the company management, increasing the speed in adapting to changes in the

company, whether caused by internal factors or external factors, and improve the

competitive degree between one company to another. By implementing the

appropriate AIS, companies can also create a dynamic environment in terms of

movement and information sharing in the event of a shift or change of

organizational structure or staff at all levels with new business relationships

(Estebanez et al., 2010).

AIS has a function as a tool that operates the collection, processing, and

categorization of data, also records the activities of financial transactions to

15

provide information used for planning, recording, and decision making

(Boochholdt, 1999). According to Demir (2005), AIS has other functions that are

used to generate sources of information used for evaluation and show information

about the company about its own process business and financial situation.

AIS has an important role in shaping a management strategy that serves as a

mechanism that is capable of processing, storing, and providing information on

company performance and a good strategy for the company (Gerdin and Greve,

2004). Therefore, it is very important for a company to be able to produce,

provide and implement a quality Accounting Information System (Demir, 2005).

2.2AIS with Financial Performance

The previous research has shown that AIS that has been designed and

finally implemented into the organization or company can be used to support the

matching and selection of strategies to be used, as well as improve the financial

performance (Gerdin and Greve, 2004).

According to Zulkarnain (2009), Information provided by good AIS has a

positive effect on the effectiveness of strategy selection and the improvement of

financial performance owned by the company or organization. For example,

success in implementing good AIS can keep the money and time shareholder.

Because by using the right AIS, it can generate information for investors quickly

and accurately to be used as a determinant in deciding investment decisions.

AIS also plays an important role for financial managers in a company

because financial managers need to evaluate the company's financial performance

16

using the financial and accounting data provided by AIS by measuring ROA

(Return of Assets) and ROE (Return of Equity). Both ratios can be used as a

measuring tool to see how good or bad the company's financial performance

(Sadia, 2011).

Accounting Information System, when viewed from its usefulness and

function, has four important factors to support AIS quality, they are scope,

timeliness, level of aggregation, and integration. Scope means the size of the area

and area of information that AIS needs and can provide. An example is whether

the scope that AIS wants to generate is more toward predicting future or more

performance in the direction of evaluating historical events, and then whether the

scope to be obtained from AIS is the data used to assess the situation outside the

company (external events) or to assess the situation within the company itself

(internal events). Timeliness talks about the time required by AIS to process and

produce the required data, over a period of time when AIS is used and operated

(daily, monthly, etc.), as well as its use for short or long runs. Aggregation

contains about how data can aggregate in the timeframe that is prepared and

needed, according to its function, and based on its decision model. As for

integration, it talks about the ability of AIS to provide information to show the

interaction and coordination effects that have been performed by some function

within the organization or company. The above four attributes have passed the

process of analysis and provide results that these attributes can be used to

compare AIS with the performance and financial strategy of a company or

organization (Gerdin and Greve, 2004).

17

According to Demir (2005), AIS that is good for improving financial

performance is AIS which can provide financial information that has high

reliability, can be known the sources and truth, is timely and on time, contains

information as needed, and easy to understand.

2.3Reporting System

Accounting reporting system can be seen as a living enviroment system,

because the characteristics of a good accounting reporting system is that the

system must adapt, evolve, and develop periodically according to its need to

record and produce financial statements. Accounting reporting that is easily

adaptable can improve process performance in collecting, analyzing, and

disclosure of data needed to be able to assess company performance (Sadia,

2011).

Based on Dierkes and Preston’s (1977) research, Accounting reporting

system is expected to identify the factual data obtained; must be built and have a

clear structure and plot for measuring, analyzing, and so on; built on the

importance of the results that can be given; provide results on the comparison and

evaluation of other information, either with the objective of obtaining the results

of internal company comparisons (for example between divisions, inter-levels, or

between mechanisms) or to obtain comparisons with other companies that have

similar types of activities. Similar to AIS, an important factor for the Accounting

reporting system is that information generated by the system should be easy to

understand as well as containing a wealth of information, not only in part but in

18

overall information on the performance of the company, for investors and internal

companies.

2.4Extensible Business Reporting Language (XBRL)

XBRL (eXtensible Business Reporting Language) is the development of a

programming language based on the concept of XML (eXtensible Markup

Language) that become an effective problem solver on prepare, exchange, and

provide financial statements that have international standards (Stergiaki et al.,

2013). According to Cohen et al. (2005), XBRL can be developed to prepare and

provide financial reports, taxes and other business reports that have been

standardized in detail but easy to read. Also according to them, XBRL provides

several benefits to companies that implement it, they are to increase data exchange

activities (both within and outside the company), to improve efficiency in the

process of making business reports, maximizing the control function at the

company, to assist in facilitating the comparative activity and analysis of business

reports, and to help reduce paper transfer activity (reducing paper waste). The

benefits of XBRL are also supported by research by Gomaa et al. (2011), which,

according to their research, one of the benefits that can be gained from using

XBRL is to facilitate the analysis of financial activities and performance of the

company compared to using reports that are still generated manual. Another

benefit that can be provided by XBRL according to research by Chen (2012) is to

increase the transparency and accountability of the business reports and financial

reports generated. XBRL has a function to manipulate the data contained therein

which aims to prepare and provide reports that have better information and more

19

easily understood by people who read it, so as to produce better decisions and

analysis results (Alles and Piechocki, 2012).

20

CHAPTER 3

METHODOLOGY

3.1Data Collection

The writer used primary data collection method in order to get and gather

the data that writer need to analyze the events, problems, and results that can arise.

All of the data was collected from the people who work in the company itself, as

the finance and system consultant. The primary data collection methods that

writer used for this study are observations, interviews, voice taping, and testing.

Observations were conducted by writer while the writer still worked in the

company as the intern. From the observations, the writer could be able to get and

analyze the process business, to get any rules and procedures in the company, and

to get the documents that company need to accomplish the goals. In the

observation period, the writer made observations directly by doing analysis and

processing of data that the company have, also performing quality test control and

training for the users. Throughout these stages, the writer could recognize the

most current situation of the company, the necessary needs, as well as any

development that can still be undergone by the company. Interview were

completed with high level manager and senior manager of consultant. In

interview, the writer asked several question that officers could not find after did

the observations in the company, the goal of this interview is to get the most

21

current conditions, more details, and reliable data of the company. Voice taping is

carried out while the interviews were held. The writer made a voice recording of

the interviewees, to avoid any detail informations missed during the interviews.

Testing is the last stage of the methods where writer was reviewing, checking, and

controlling testing of the system that have been developed. In this stage, the writer

was able to understand the functions that are given by the systems and to be aware

what results can be prepared and generated by from running the system.

The first step that writer took for this research is how comprehend the

company’s condition in doing the financial and reporting activities and how the

working environment in the company. The purpose in doing this step for writer is

to gain the information and more understand about the current company’s

conditions, especially in finance area. After knowing and understanding about the

state of the company, the writer carried out analysis to achieve the purposes of

this research. The writer could achive those objectives by performing data

analysis that has been obtained using the above stages and then made a

comparison with existing theories and performed in previous studies. The writer

could also recognize about what part of the area that is still needing enhancement

dan development for further function.

3.2 Company Profile

Special Task Force for Upstream Oil and Gas Business Activities Republic

of Indonesia or better known as SKK Migas (Satuan Kerja Khusus Pelaksana

Kegiatan Usaha Hulu Minyak dan Gas Bumi) is one of the institutions created by

22

the government of the Republic of Indonesia as a tangible form in realizing what

is contained in Government Regulation (PP) no. 6 of 2006, Law (UU) Number 1

of 2004, also Presidential Regulation (Perpres) number 9 of 2013 which contains

the management of upstream oil and gas business activities

(https://skkmigas.go.id/). As an institution established under the above regulation,

SKK Migas has the primary task of implementing the management of upstream

oil and gas business activities located in Indonesia and already based on the

Cooperation Contracts that have been made by the Indonesian government.

Therefore, if SKK Migas can perform its duties properly, it is expected to take

natural resources of oil and gas located and owned by the government of

Indonesia can provide the full benefits for the country in order to welfare the

people of Indonesia.

To be able to do its job well, there are some functions that need to be

considered by SKK Migas. SKK Migas is expected to give its thoughts to the

minister of Energy and Mineral Resources (ESDM) on its decision to provide site

planning and quote to undertake oil exploration and drilling under the

Cooperation Contract. The institution also gains full trust and responsibility by the

government to become a Signatory of Cooperation Contract which indicates that a

company is allowed to operate and conduct activities in Indonesia. SKK Migas is

also expected to make the formulation and provide the first plan regarding

development in employment in the work areas that have been determined to the

minister of Energy and Mineral Resources (ESDM) in order to obtain approval

from the minister. If it is already approved and enforceable, it shall have the

23

authority to prepare and provide work plans which will be undertaken during the

ongoing exploration and drilling project, as well as having the authority to assess

and limit the budget. SKK Migas is also required to supervise every gas and oil

exploration and drilling work in Indonesia and report it to ESDM’s Minister. The

last function to be considered by these institutions is that they are allowed and

gain the confidence to be able to select and appoint oil and / or gas sellers, both

from outside and within the country, based on the main objective of maximizing

profit for the country. When looking at the functions owned by SKK Migas, it can

be concluded that SKK Migas has a role as a supervisor and regulator, not as a

party to drill or extract oil and gas. They need a second party as executors in

drilling and extracting oil and gas, they are known as partner companies.

24

CHAPTER 4

RESULTS AND DISCUSSIONS

In chapter 4, the writer begin with a brief presentation of the current state of

the company which still uses manual methods and has not implemented a

reporting system, as well as a brief explanation of what triggers the company so

that it has a desire to implement reporting system so that readers can understand

the current state of the company. The final part of this chapter contains the results

of the discussion and analysis of the data obtained by the author, they are the

things that need to be prepared to start development, the stages of system

development, the steps in reporting using the reporting system, the ways in

validate reports received, obstacles that can extend the development process, and

profit in using the system.

4.1 Current Condition of the Company

The financial statements are still distributed manually between partner

companies to SKK Migas and also SKK Migas internally, like sent using flash

disc or email. There are three general level of process which can be seen from the

beginning of data receipt until finally the report is approved by SKK Migas, they

are:

1. Starting from the data provider that is partner company

2. Reviewer is performed by accounting division of SKK Migas

25

3. Approval by top level managers or senior managers

4. Approval by head of division

At the end of the year, in the fourth quarter, the partner companies must be

able to provide and submit to SKK Migas financial statements before and after the

audit process. So that can be seen in the first, second, and third quarters of the

year, the partner companies only sends Financial Quaterly Report (FQR) 1, 2, and

3 along with its revisions if any, whereas in the fourth quarter, the partner

companies sends FQR 4 along with its revision + report after the audit process.

This applies only to FQR collection, not applicable to FMR (Financial Monthly

Report).

By looking at information above, as partner companies in collaboration with

SKK Migas, partner companies must prepare two financial statements to be sent

to SKK Migas, namely FMR (Financial Monthly Report) and FQR (Financial

Quarterly Report). As the name implies, FMR is sent monthly by the partner

company to the SKK Migas while for FQR shipped per three months. In every 3-

month period (March, June, September, and December), partner companies will

prepare and submit two financial reports at once, namely FMR and FQR.

Because still using manual method, the partner company sends FQR and

FMR data using Ms. Excel that the format has been changed in accordance with

the form of FMR and FQR format that has been given by SKK Migas using flash

disc or via email. In Ms. Excel, there are only provided data formers FQR and

FMR which means the data provided is data that has been combined and contain

26

general information, there is no detailed transaction data as a support in it. SKK

Migas then checks and analyzes the report manually to find out whether there is a

peculiarity of numbers or the possibility of fraud on reports that have been given

by the partner companies in Ms. Excel. Checking and analyzing is calculated

based on the assessment of over and under budget analysis. If an indication of

fraud or anomaly is found in the numbers in the submitted report, SKK Migas will

proceed to the next stage of requesting detailed transaction data used as

supporting and proof of the figures generated in the report. SKK Migas will ask

the partner companies through a manual ways, using email or by conducting

direct discussions, in order to obtain supporting data required by SKK Migas.

Then the partner companies that have received the request SKK Migas, they must

be able to provide detailed data that has been requested by the SKK Migas.

However, the partner companies can provide the details in a short or long time,

according to how much effort that the partner companies needs to prepare and

send them to SKK Migas. This has resulted in some partner companies that have

poor internal systems becoming more time consuming to collect and provide these

data. Also from the SKK Migas does not have a definite collection deadline, the

deadline can be changeable and uncertain for each partner companies. If SKK

Migas has received the transaction details that they have requested to the partner

companies, then SKK Migas will start the analysis process by comparing the

numbers contained in the transaction data with the numbers contained in the

financial statements of the partner companies. If the number is the same, then it

can proceed to the approval stage. However, if there are differences and

27

unreasonable numbers, then SKK Migas will return back the financial statements

of the company's partner in the form of Ms. Excel by adding some records and

notes that are needed to known and explained by the partner company to be

repaired and adjusted. What usually makes the numbers on the financial

statements false is because of the effort, intentionally or otherwise, by the partner

company to include some transactions that should not be included in the cost

recovery into the calculation that will be claimed by the partner company through

that financial statement. In this revision phase, what usually happens in the field,

the revision is not only happen once, but it is possible and often back and forth to

send revisions by partner companies and responses by SKK Migas.

The way that SKK Migas teams need to get the anomaly of numbers

performed in the reporting process is by performing the analysis per transaction

contained in the report. It is necessary to provide a source of transaction which

contains detail information to support the speed and accuracy in performing

financial statement analysis. It is possible that the fraud that passed from the

analysis of SKK Migas team could be caused by two things. The first is level of

experience and critical thinking possessed by analysts from SKK Migas, if the

analyzer has not had any experience in finding fraud or fraud in the financial

statements or the analyzer has no critical thinking in assessing and analyzing the

financial statements, it will increase the possibility cheating by partner companies

can escape and undetectable. The second is the long time required by partner

companies to provide detailed data requested by SKK Migas. Analysis team from

SKK Migas has limitation of time to collect reports of the partner company to get

28

the signing of approval from their superiors. If the partner company gets longer in

preparing and sending the required data, then the time owned by SKK Migas team

to analyze their report become shorter and their analysis becomes rushed and not

deep or detail.

4.2 The Causes of the Implementation of System

The real thing that triggers SKK Migas want to implement report-making

system is because by using the manual steps makes the function of SKK Migas

which is become a supervisor of partner companies less than maximum because

too time consuming in requesting and collecting data manually from partner

companies, also there is increasing amount of oil and gas partner companies that

entering and developing in Indonesia. While using manual methods, the exchange

of data conducted between companies using flash disc or CD. Because of this, the

partner companies must back and forth to provide data required by SKK Migas.

Actually if it is urgent, it can be sent by email, but if really urgent, because by

using email, data that is sent very easy to be hacked and do not have enough level

of security which means that important financial data owned by partner

companies can leak and causing the investment price of the partner companies to

fall and become low. Then for the number of partner companies in Indonesia

which initially only three partner companies that need to be supervised, it is still

under control if SKK Migas using the manual method. But after there are

increasing amount of partner companies year by year, then it means the

documents and reports that need to be analyzed and reviewed by SKK Migas also

increased, then SKK Migas need necessary assistance from system that can

29

simplify and accelerate the process of performance SKK Migas. If the

development of the system is performed when there are only three partner

companies, where the SKK Migas can still maximize their function, then the

development will become more problematic and adding a high cost, because the

development process and the price is fairly high but the benefits that SKK Migas

get are only small (it is called high cost because of the use of services from other

companies for its development and the cost of buying and maintaining the

necessary computers and software, its cost and benefits does not have comparable

value).

Because of the above issues, the inefficient process and the increasing

number of partner companies, that is slowing the process of carrying out duties

owned by SKK Migas which is to be able to monitor and assess the performance

of partner companies that demand SKK Migas must be able to analyze in detail

the transaction activities which is performed by partner companies that can be

inputted into cost recovery, SKK Migas started looking for an effective and

efficient way so as to maximize their performance. Then with the emergence of a

technology called XBRL, a technology that can provide security in the exchange

and delivery of information, can be a report or raw data, SKK Migas finally has

the initiative to develop their reporting system.

SKK Migas actually already has its own AIS used to process their own

financial statements, but SKK Migas and partner companies are using AIS that

different from each other. The function of AIS owned by each partner company

also by SKK Migas is to coordinate and produce internal financial report for each

30

company respectively. This issue is also become one of the triggers that SKK

Migas required the development of a system that still maintains the interests of

each company without disclosing any secret owned by each company.

SKK Migas once had an idea for each of its partner companies to open and

give access to SKK Migas to see the whole of the company's financial statements

through their AIS. However, the partner companies feel that the policy is beyond

the limits of privacy and fairness limits in an inter-company cooperation

relationship (because the relationship between SKK Migas and its partner

companies is not like the mother company with the subsidiary, but the companies

that work together as a partner). Because of that policy, the partner companies

have been asked SKK Migas about what they need from partner companies, then

partner companies will provide those data required by SKK Migas, no need to

open the whole financial data owned by the partner companies. The thing which

required by SKK Migas from partner companies according to the meeting

conducted as above is to submit their financial statements accordance with the

format given by SKK Migas in the form of Ms. Excel, manually, that can show

the results of the value of the cost included in the category of cost recovery from

the financial activities of partner companies, and then if required, the partner

companies will send transaction details, like form of reimbursement along with

other notes and attachments. However, because AIS that is owned by each partner

companies is different and generate transaction details and transaction accounts

that have different properties, then this is what makes difficulties in process for

SKK Migas to be able to quickly analyze each partner companies’ reports.

31

Therefore, to be able to speed up and make efficient in the process of analysis,

SKK Migas requires an accounting system that can standardize all accounts

owned by partner companies in accordance with those owned by SKK Migas.

4.3 Discussion About Implementing the Reporting System

4.3.1 Things Need to be Prepared by SKK Migas During System Development

Process

a) Determine who are become decision-makers

SKK Migas should provide a clear structure to the development team about

whom and what positions are necessary and able to make decisions on the

changes that have been discussed. Development team required to understand the

structure and patterns in getting approval of the decision so that there is no

misunderstanding between the two parties.

b) Provide time and dedication during the process of system’s development

In working on a project such as this development of system, there is a need

for considerable time and dedication to the project, as in developing this system

necessary inputs are needed such as checking and adding criteria and Chart of

Accounts entered into the system, as well as in different views with partner

companies, then SKK Migas should be able to take the time to become the

midpoint and decide which one is more appropriate and can be implemented into

the system.

c) Prepare the required data

32

SKK Migas must provide some data needed by the development team to be

a real example in testing whether the system is working properly or not. The data

provided must be real data because if there is an error, then the error can be easily

detected because it has passed the previous checking process, when using data

that is made-up then if there is an error, it will not look obvious at the point where

the error in the system.

d) Follow up the performance of partner companies in process of development

system

It cannot be denied that SKK Migas is an institution under the supervision

of the government directly, and partner companies will feel more reluctant when

reminded directly by SKK Migas than by the development team. Therefore, it is

necessary to get assist from SKK Migas in conducting follow-up to partner

companies on deadlines that have passed the limit, for example if the partner

companies has not collected data or Chart of Account development work required

immediately for the process of development, then SKK Migas must be willing to

helps the development team to remind the partner companies to get the job

finished immediately related to the system development project.

4.3.2 Stages of System Development Process

a) Requirement analysis and design

Referred to in this stage is the need to do data collection on what criteria and

design the desired system in accordance with the necessary needs. Then after the

33

data collection is obtained, it is necessary to analyze the criteria so that it can get

the initial picture or draft design as desired.

b) Flow chart of making design

At this stage, it begins with making a flow chart of the process stages per

stage in making the system. It is divided into three parts in making flow chart,

they are for the IT, accounting and reporting, and the Chart of Account (CoA)

Mapping. An example of the IT section in creating a flowchart of system is about

how data will be withdrawn per date, its acceptance system from the beginning to

where and where it wants to be generated. The example of the accounting and

reporting section in creating a flowchart of system is the format and form of the

report as desired, what data to be viewed, drawn, and included in the report, what

level of detail should be included and collected to SKK Migas which is needed to

perform a thorough and in-depth analysis. As for the example of the CoA

Mapping section in creating a flowchart of system is about to level detail what

chart of account mapping will be created and accommodate the transaction data

for inclusion in the report, what accounts need to be made in accordance with the

activities undertaken by partner companies included in cost recovery.

c) Finalization of system’s design draft

At this stage, it starts for the initial draft of the design of the system to be

created and has been designed based on shared criteria and analysis in the

previous stage. It is at this stage that it takes the longest time because the

continuous development is executed based on cases occurring during the

34

development process until finally the design can be recognized as the best and can

be realized by building the actual system. This stage requires more intervention

from the accounting department because in the process of development of this

design, the team who became the developer must understand exactly what

information and form of report desired by the accounting, as well as any criteria

that need to be given in the system appropriate with accounting terms owned by

SKK Migas in forming its report.

d) Development and realization of design

In this stage, the designs that have been made in the previous stage and

completed is start to be physically created and then implemented into the

company based on what has been designed and developed previously. In this stage

more activities are completed by the IT because they are the main axis at this

stage to form its system.

e) Testing system

Testing conducted in this stage is divided into two, namely SIT (System

Integration Testing) and UAT (User Acceptance Testing). What is meant by SIT

(system integration testing) is an activity to test the results of merging components

that have been made to form a system. This test is carried out when the software

has been completed and tested directly the whole operation, no longer tested one

by one component. What is meant by UAT (user acceptance testing) is an activity

performed by the actual user of the system to determine whether the results and

performance of the system that has been produced is in accordance with what is

35

desired by the user. This test has an important point on the results of documents

and reports provided by the software system that has been made and this test

method is also to analyze the functions contained in the software system so that it

can be assured that the system that has been formed according to the criteria

indeed owned by the user.

f) Training

At this stage, training is provided for SKK Migas users. In this training,

users are given an exercise on the concept of working from a system that has been

created with the purpose of the user to know how the system works and logic used

in the system they use to generate reports, then the user is also given training on

how to operate and use his system so that users will not feel confused while

running the system.

4.3.3 Steps in Generating Report Using the System

a) What needs to be performed for the system can pull data from AIS owned by

the partner company is on a predetermined date, there must be someone from

the partner company who press the software button in his computer for XBRL

system can pull the data owned and provided by the partner company to be

given to SKK Oil and Gas. Here the important thing is the person who will

press the software button must be able to ensure that the data available to be

withdrawn by the system is data that has passed the monthly closing stage by

each company, so that required cooperation and communication with the

accounting party. If the software button is not pressed by a person in partner

36

company, then the assumption that is owned by the system is the partner

company has not sent because SKK Migas has not received. There are

actually two possible problems, between forgetting to press the software

button or the monthly closing by the partner company has not been

completed. The system then sends the reminder to the partner company to

notify that the deadline of the report collection has arrived and must be sent

immediately. Reminder is sent to two parties, the partner company that has

not sent and the SKK Migas to realize which partner companies who have not

collected in accordance with the time specified.

b) Reporting system owned by SKK Migas will draw the data that has been

prepared by partner companies automatically from each company's AIS,

which is then drawn by and into XBRL.

c) Then the validation of data will be completed by the system that has been

formed to determine whether the data that has been prepared and pulled by

the system is a data with the content and the correct format or not. If it is not

correct, the system will refuse to accept the data and will give it back to the

partner company who has the data.

d) If the data sent is correct and passes the system validation stage, then the

system will encrypt the data so that during the data transmission process, both

then and in the future, can be maintained properly and cannot be hacked by

other parties.

e) After that, the data will pass through the casing encryption stage. This is to

check whether the data received by the SKK Migas is really the same as that

37

has been sent by the partner company. Authentication is also checked,

whether the recorded to the sender in the system is the same as the already

recorded as whom already send the data. And integrity check to check the

amount of data, the number of row and column, the amount of its contents

whether it is already the same between which has been received by SKK

Migas with which has been sent by the partner company.

f) The data that has passed the stages of encryption and testing the truth by

using the system and successfully accepted by SKK Migas, then the data

which containing the different Chart of Account mapping of each partner

companies was changed into mapping Chart of Account owned by SKK

Migas by using developed system.

g) Furthermore, from the data that has been changed to follow the mapping of

Chart of Account owned by SKK Migas, is forwarded to be formed of report

(FMR or FQR) by using the code functions and criteria that have been

running in the system.

h) The next step is discussion and approval activity conducted by SKK Migas.

Here the analysis is still visible using the manual but the data that needs to be

viewed to perform the analysis is automatically available immediately and it

is not necessary to manually return to the partner companies like before using

the reporting system, which can take a long time. Here it is seen that reporting

system makes SKK Migas can maximize and become more effective and

efficient in performing its duties as a monitoring and analyzing the activities

of partner companies, because when still using manual method, too much

38

spend time just only for ask supporting documents, but by already using

reporting system, the time to analyze and conduct financial oversight can be

more and more thorough.

4.3.4 Ways to Validate Data Between Data Sent by Partner Companies with

Those Received by SKK Migas

SKK Migas need to do quality control to the data obtained to analyze

whether the data submitted by the partner company and obtained by SKK Migas

is the same or different data, also to determine whether there is error on the

system after being run or not. For example, if the system has succeeded in pulling

data from AIS of partner company but when compared between data already

submitted by partner company with data obtained by SKK Migas there are still

difference, then there are two possibilities that can happen. The first possibility is

the occurrence of errors in the reporting system that has been made due to further

development that is performed on the system by SKK Migas. While the second

possibility is there are mistakes in processing the data in the system that caused by

input errors made by the partner companies.

If an error occurs because there is an error in the reporting system that is

executed, then SKK Migas need to perform re-checking and tracking into the

reporting system. It can be found on which part of the system that makes the

results made by the system are different from the data sent by the partner

company and cause an error. If the difference in numbers in the same two reports

is caused by data that is different after being withdrawn by the system and

received by SKK Migas, then there are three possibilities that could cause this

39

error. The first is the difference in the amount of data inputted by the partner

company with the one that the partner company owned or prepared, thus causing

the system at the time of pulling the data that has been prepared become lesser

and different. The second is that inputs by partner companies use incorrect codes

that result in multiple numbers moving to different reports and causing differences

between reports. The third possibility is that there is an incorrect cost allocation

calculation between the cost sharing included in the oil, gas, or common types, as

well as the calculation of the cost allocations held by the partner companies that

have more than one working area.

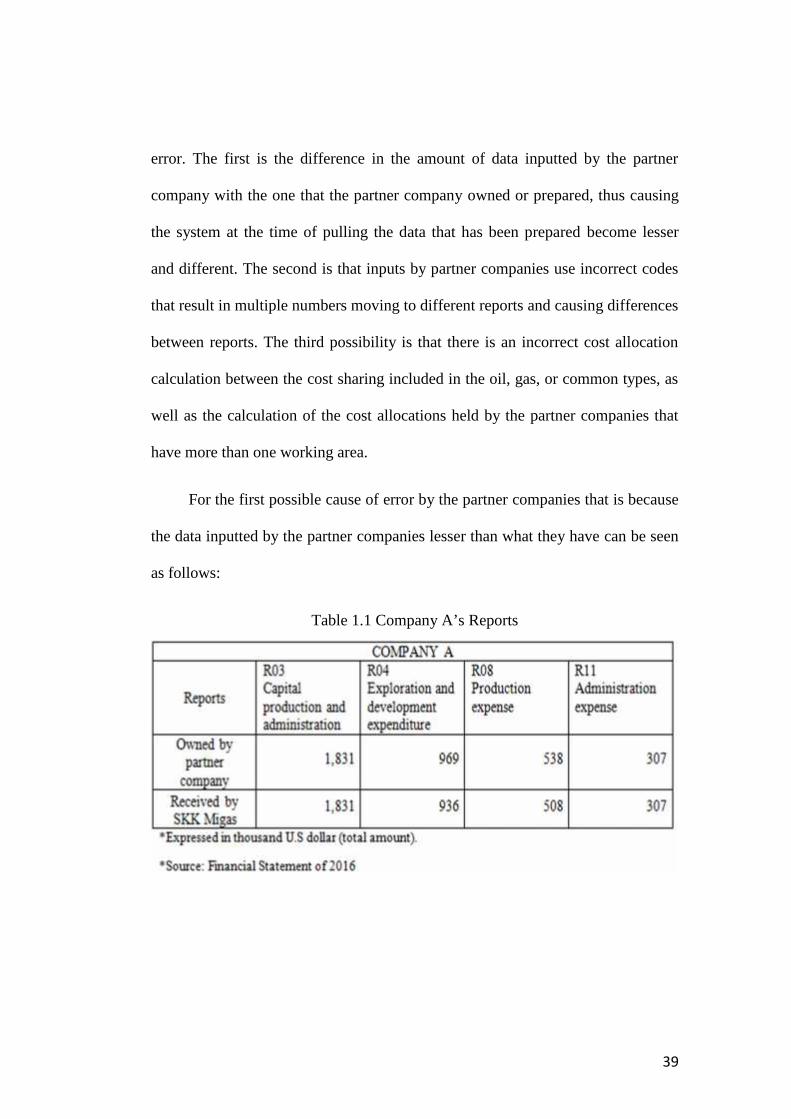

For the first possible cause of error by the partner companies that is because

the data inputted by the partner companies lesser than what they have can be seen

as follows:

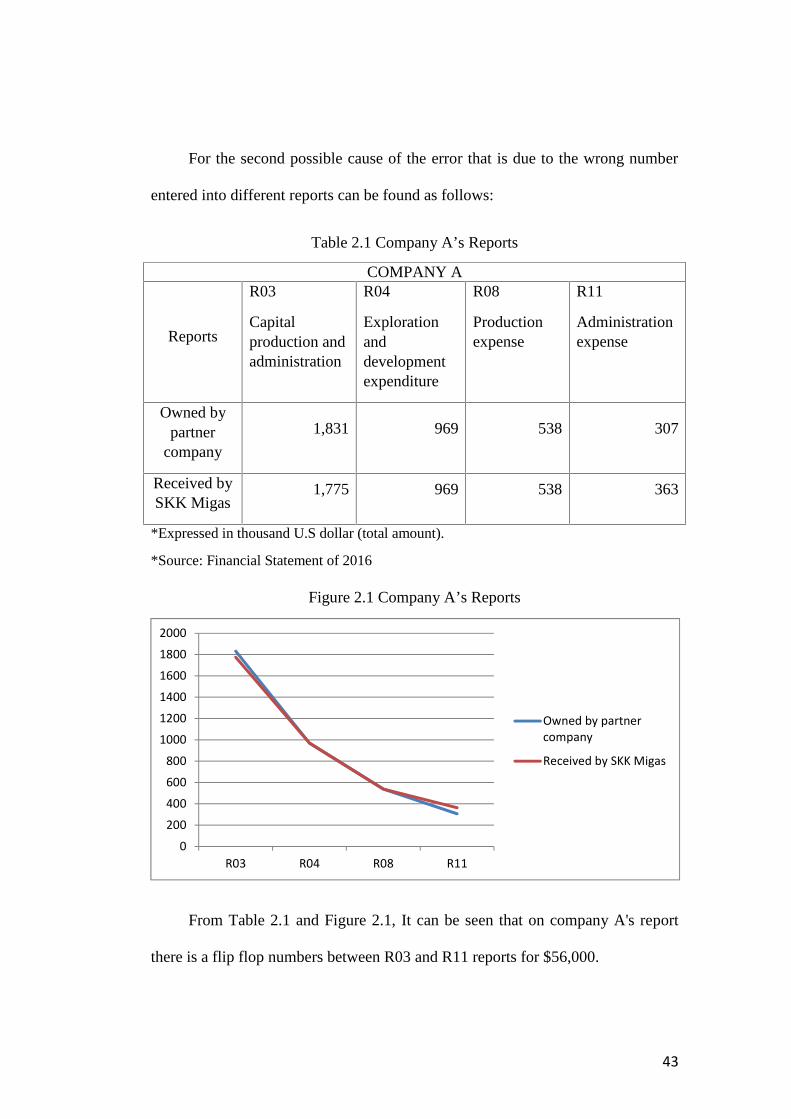

Table 1.1 Company A’s Reports

40

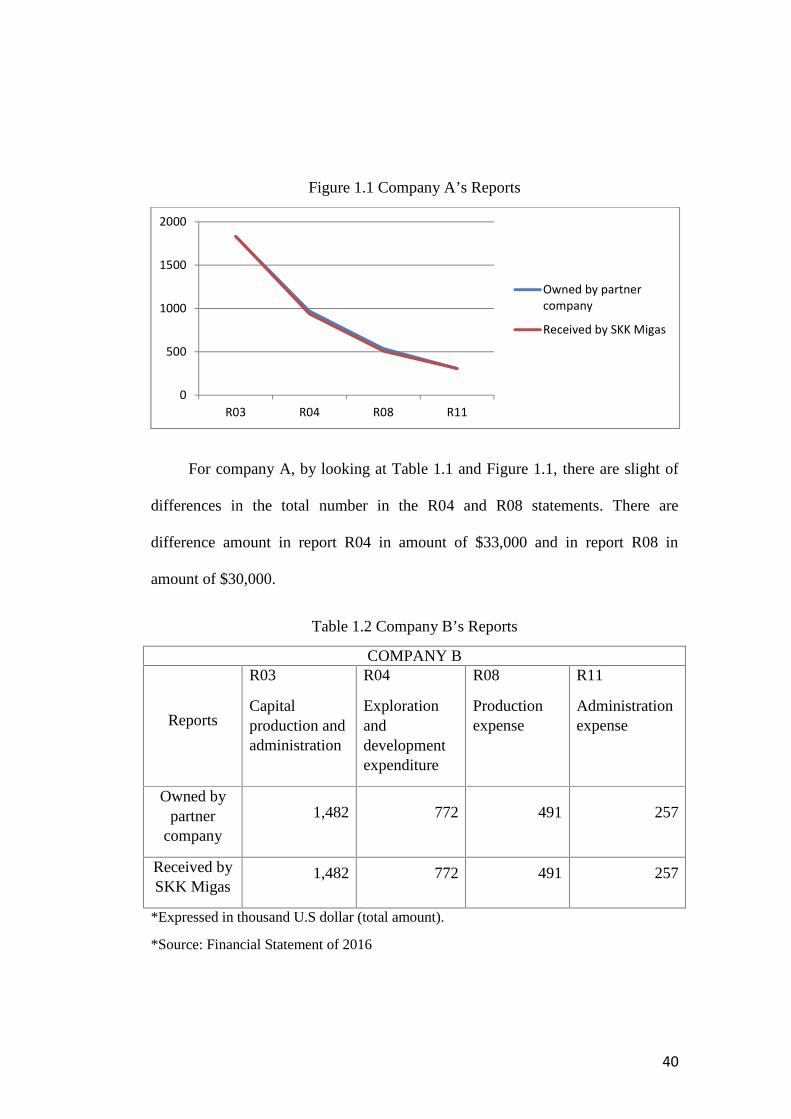

Figure 1.1 Company A’s Reports

For company A, by looking at Table 1.1 and Figure 1.1, there are slight of

differences in the total number in the R04 and R08 statements. There are

difference amount in report R04 in amount of $33,000 and in report R08 in

amount of $30,000.

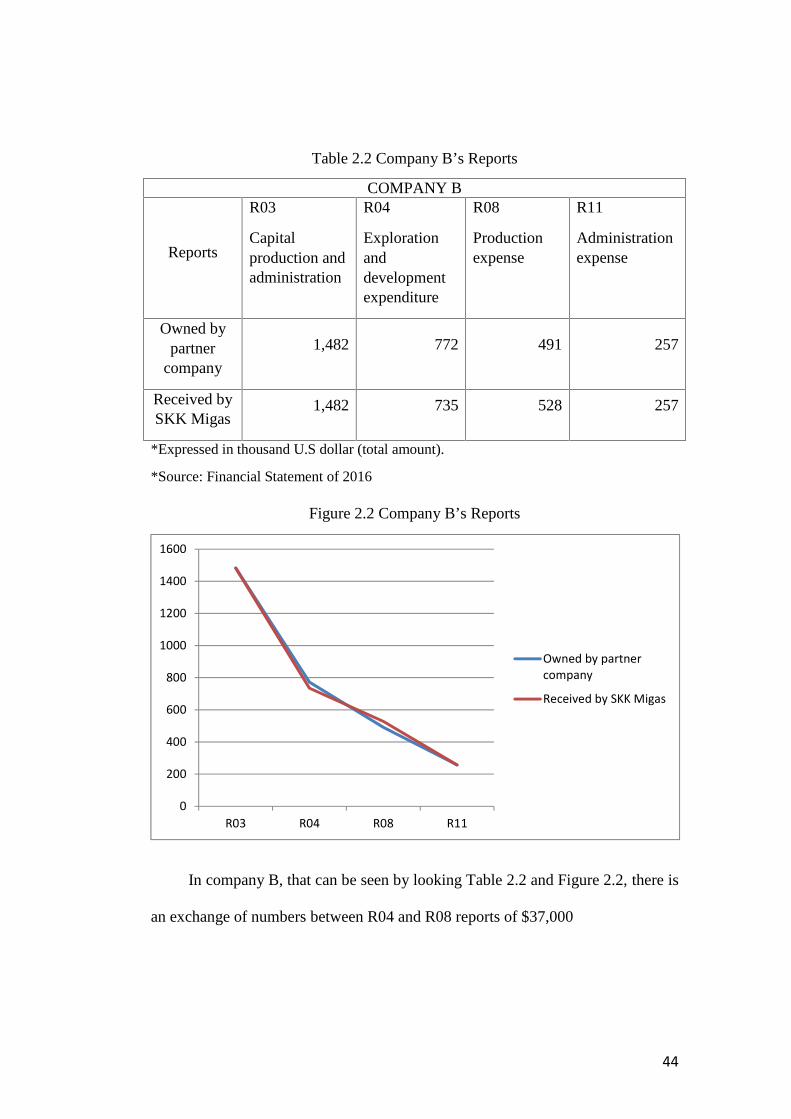

Table 1.2 Company B’s Reports

COMPANY B

Reports

R03

Capitalproduction andadministration

R04

Explorationanddevelopmentexpenditure

R08

Productionexpense

R11

Administrationexpense

Owned bypartner

company

1,482 772 491 257

Received bySKK Migas

1,482 772 491 257

*Expressed in thousand U.S dollar (total amount).

*Source: Financial Statement of 2016

0

500

1000

1500

2000

R03 R04 R08 R11

Owned by partnercompany

Received by SKK Migas

41

Figure 1.2 Company B’s Reports

In the Figure 1.2 that have content from company B (Table 1.2), the two

lines have formed in an exact line location indicating that the data owned by the

partner company with those received by SKK Migas are the same and there is no

difference and SKK Migas can continue the analysis process. In this case,

company B did not make any mistake in delivering the data.

Table 1.3 Company C’s Reports

COMPANY C

Reports

R03

Capitalproduction andadministration

R04

Explorationanddevelopmentexpenditure

R08

Productionexpense

R11

Administrationexpense

Owned bypartner

company

1,669 545 416 295

Received bySKK Migas

1,635 545 416 248

*Expressed in thousand U.S dollar (total amount).

*Source: Financial Statement of 2016

0200400600800

1000120014001600

R03 R04 R08 R11

Owned by partnercompany

Received by SKK Migas

42

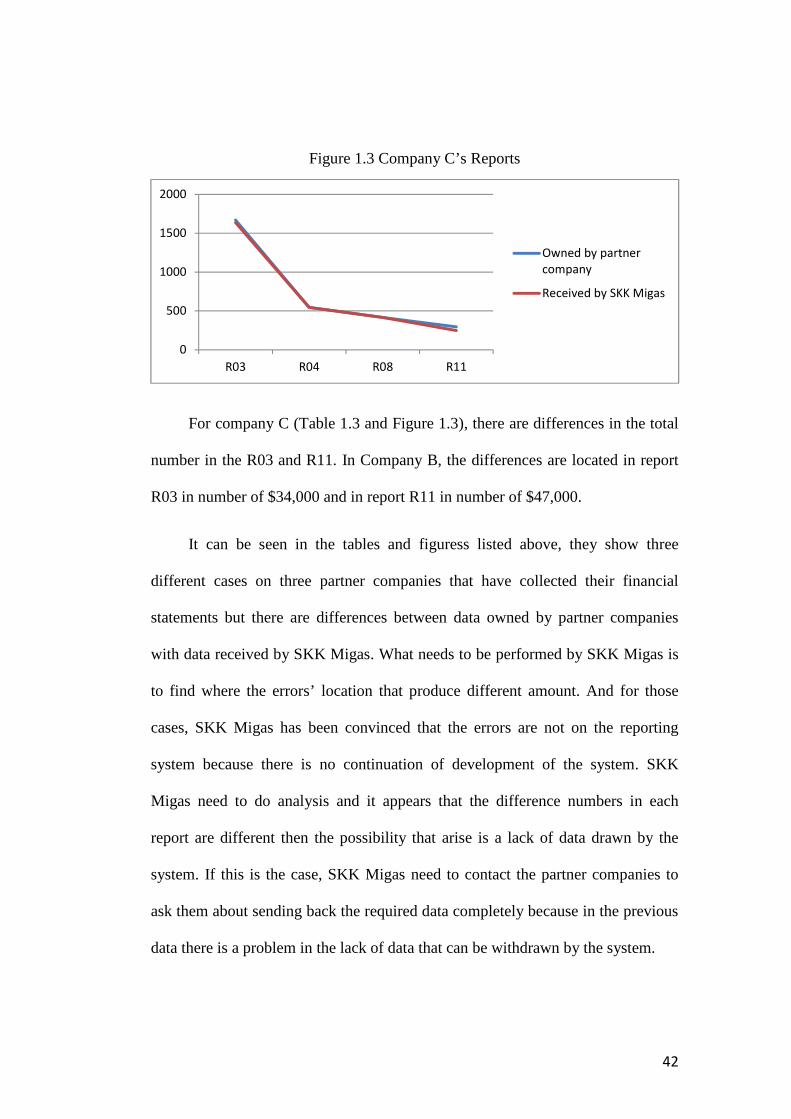

Figure 1.3 Company C’s Reports

For company C (Table 1.3 and Figure 1.3), there are differences in the total

number in the R03 and R11. In Company B, the differences are located in report

R03 in number of $34,000 and in report R11 in number of $47,000.

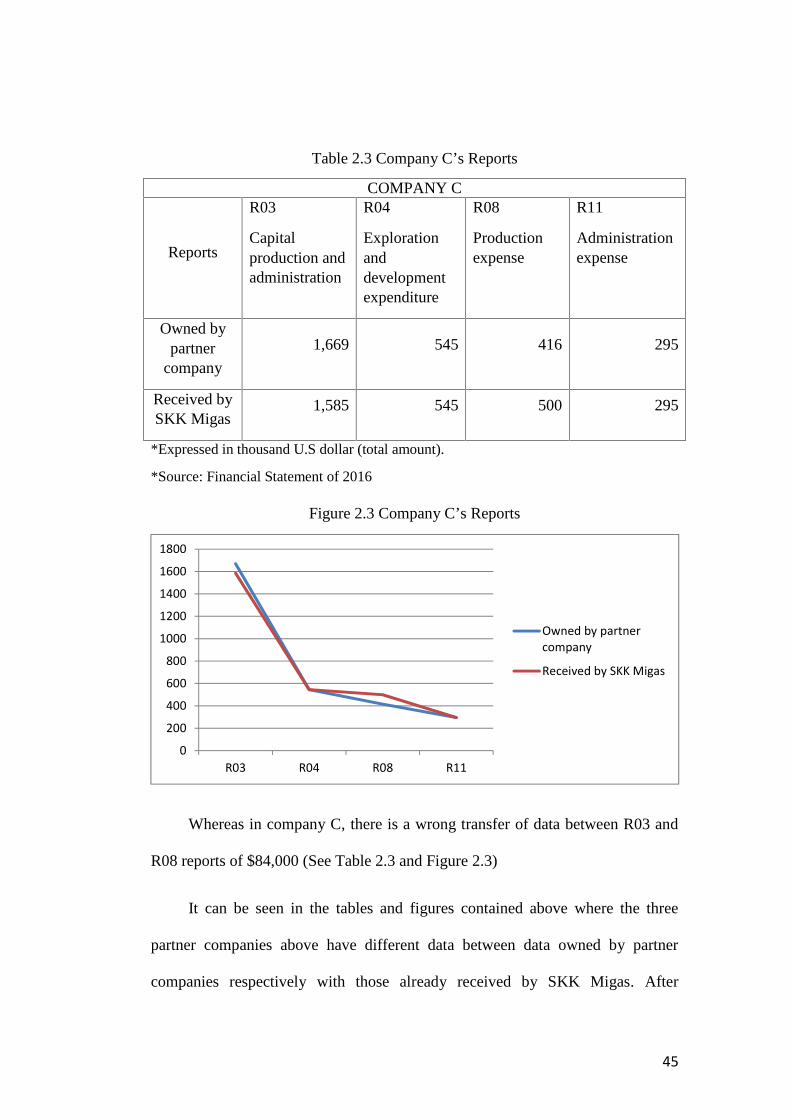

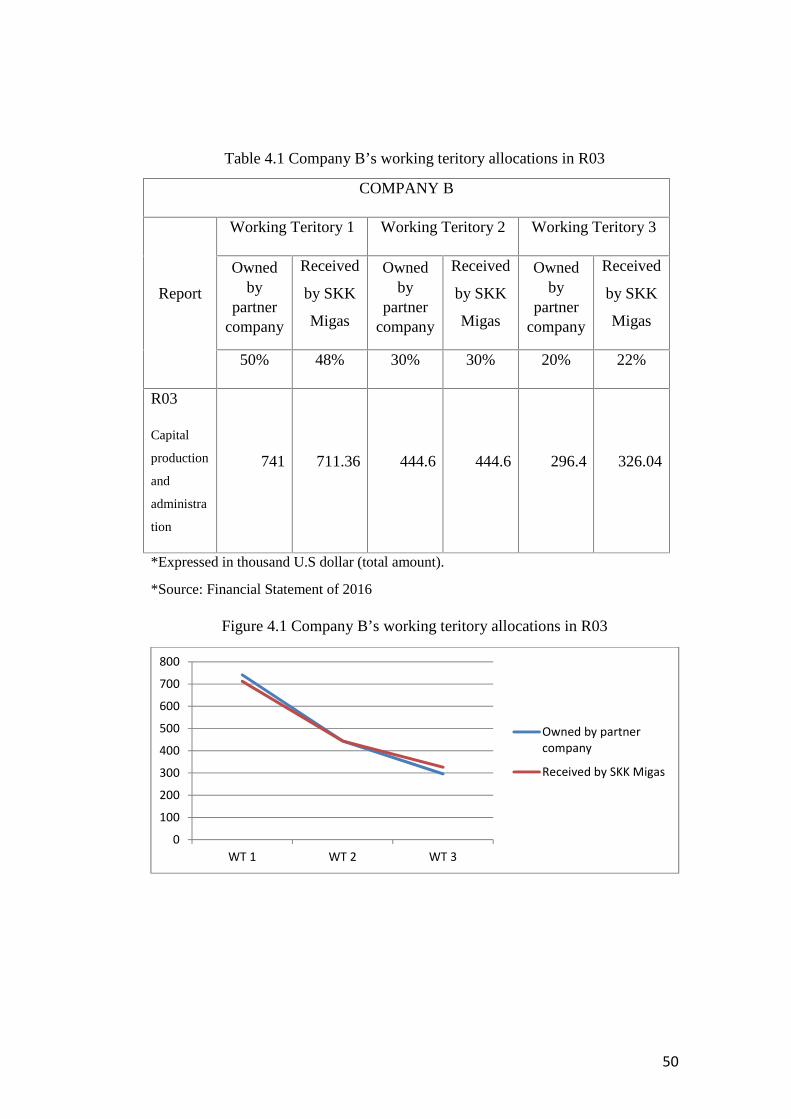

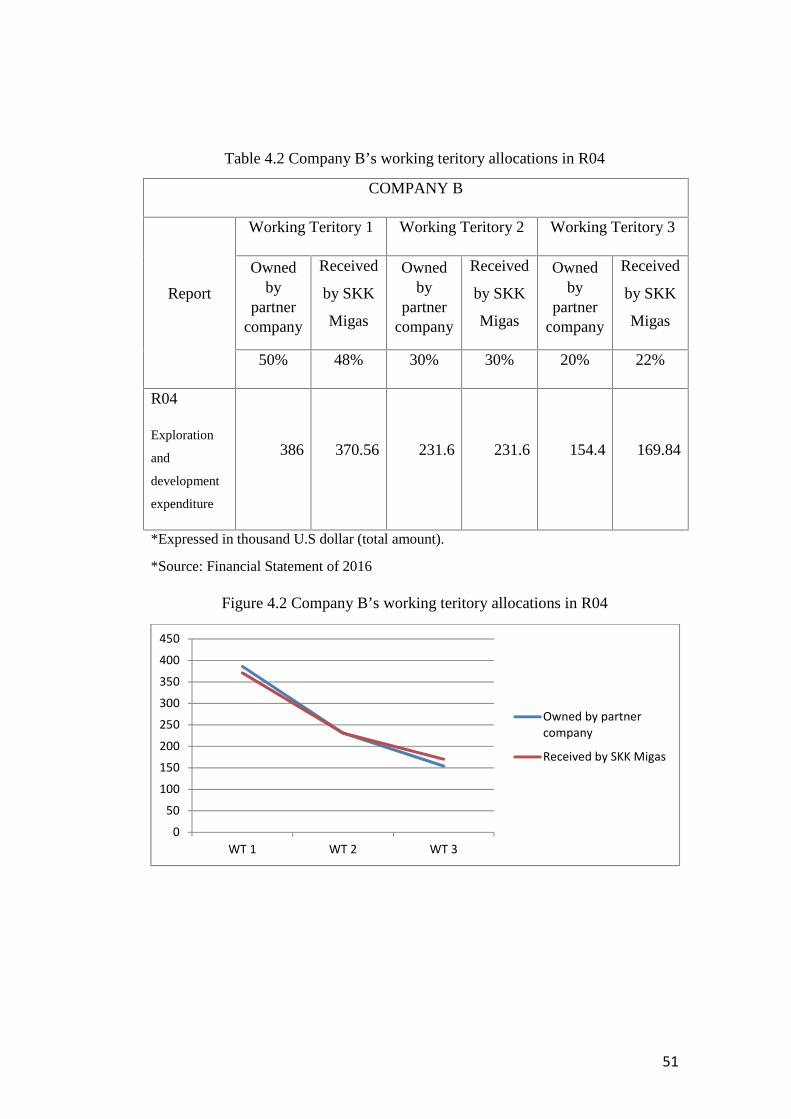

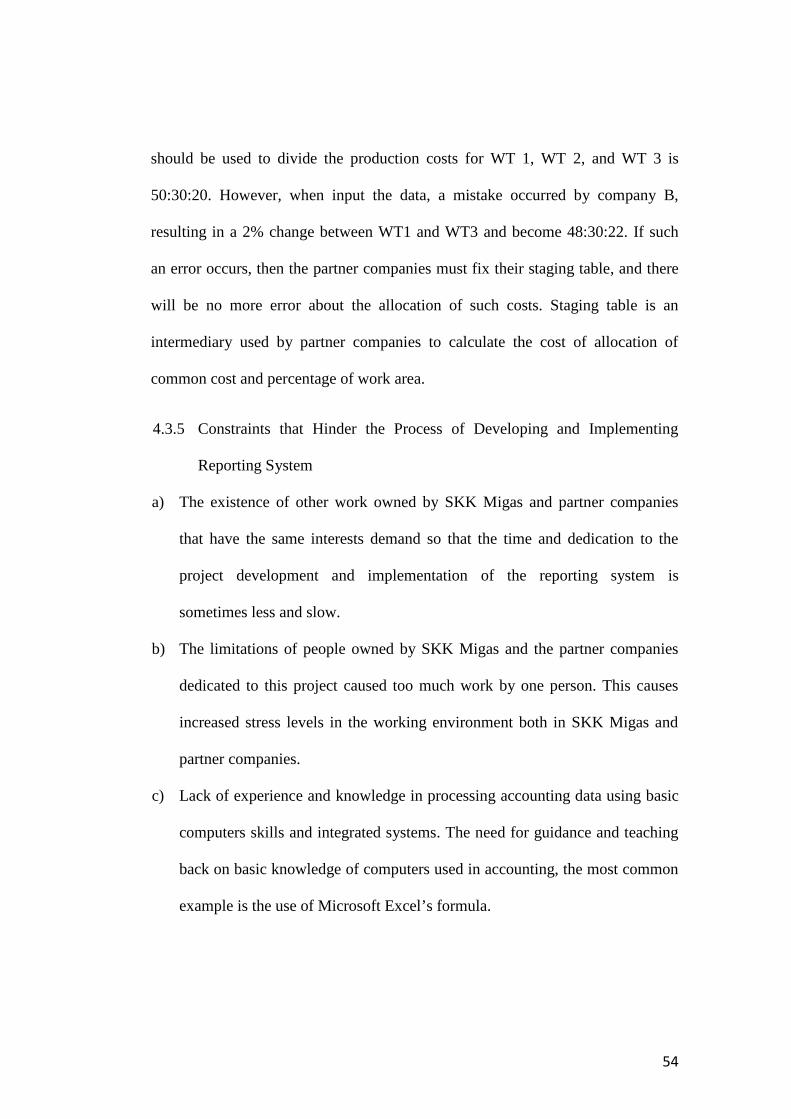

It can be seen in the tables and figuress listed above, they show three

different cases on three partner companies that have collected their financial

statements but there are differences between data owned by partner companies

with data received by SKK Migas. What needs to be performed by SKK Migas is

to find where the errors’ location that produce different amount. And for those

cases, SKK Migas has been convinced that the errors are not on the reporting

system because there is no continuation of development of the system. SKK

Migas need to do analysis and it appears that the difference numbers in each

report are different then the possibility that arise is a lack of data drawn by the

system. If this is the case, SKK Migas need to contact the partner companies to

ask them about sending back the required data completely because in the previous

data there is a problem in the lack of data that can be withdrawn by the system.

0

500

1000

1500

2000

R03 R04 R08 R11