insurance and tax changes

TRANSCRIPT

Manulife Professional Advisor ForumTax & Legal Update

Agenda

1. Testamentary trusts, life interest trusts and charitable donations at death – Life insurance aspects

2. 2016 Federal Budget

CDA credit and life insurance proceeds

Transfer of a life insurance policy to a corporation

3. Case Law Update: Beneficiary designations and competing legal interests/principles

3

Testamentary trusts, life interest trusts and charitable donations at death – Life insurance aspects

4

Topics for discussion

Testamentary trust rules

Proceeds of life insurance and the GRE

Insurance trusts as qualified disability trusts

Life interest trust rules

Planning for tax liability on death of the life interest beneficiary in a life interest trust with insurance

Charitable donations at death

Gifts by direct designation of insurance

Funding the redemption of non-qualifying securities with insurance

5

Proceeds of life insurance and the GRE

6

What is the GRE

GRE is an estate that arose on and as a consequence of an individual’s death if:

the estate is no more than 36 months after the death,

the estate is a testamentary trust,

the individual’s Social Insurance Number is provided in the tax return of income for the first taxation year and for each subsequent year,

the estate designates itself as the graduated rate estate of the individual for its first taxation year, and

no other estate designates itself as the graduated rate estate of the individual.

7

GRE Benefits

8

Exempt from paying tax instalments;

Able to make gifts of public securities, ecological gifts or gifts of cultural property to registered charities and other qualified donees without incurring capital gains tax;

Enjoys flexibility in allocation of charitable donation tax credits for donations to registered charities and other qualified donees among:

the year of donation,

an earlier tax year of the GRE,

either of the last 2 taxation years of the deceased individual, and

unused credits may be carried forward for up to five years;

GRE Benefits

9

Eligible for a $40,000 exemption from alternative minimum tax; and

Able to carry back capital losses to the deceased’s terminal return

Including the loss created on the redemption of private company shares.

Loss of GRE

10

Results in deemed year end and loss of benefits associated with GRE

Earlier of:

1. Loss of testamentary status.

Property contributed to trust other than by an individual as a consequence of death.

Estate incurs debt or obligation owed or guaranteed by specified party.

Exemption: GRE repays within 12 months.

2. Estate lasts beyond 36 months.

Some benefits will still accrue up to 60 months.

Life Insurance and GRE

11

Proceeds of life insurance can be part of the GRE

Policyholder designates estate as beneficiary of life insurance policy.

Why would a policyholder consider this?

Proceeds create an instant estate where there might have not been one.

Could be alternative to an insurance trust – enjoy GRE benefits or 36 months.

Life Insurance and GRE

12

Even where there are significant assets in the estate:

Proceeds can create liquidity where estate assets are illiquid.

Life insurance proceeds could be used to:

pay taxes, probate fees, personal representative fees, legacies.

make charitable gift.

equalize estate.

Life Insurance and GRE

13

Useful where it is desirous that the estate benefit from graduated tax rates for the maximum 36 month period.

Also ensure that there is some funds available for estate beneficiaries in the interim.

GRE’s - other

Tips, traps and other considerations

Probate fees.

Potential for a claim under Wills, Estate and Succession Act (WESA).

No creditor protection during the life of the policyholder.

Depending on client circumstances, there may be better options.

14

Insurance trusts as QDT’s

15

What is a QDT

A testamentary trust.

A resident in Canada.

Joint election (annually) to be a QDT with one or more “electing beneficiaries”.

Beneficiary must be named in the trust instrument .

Cannot jointly elect with any other trust.

Must be an individual eligible for the DTC in the year.

16

Insurance trusts as QDT’s

Insurance trusts qualify as testamentary trusts.

Need not arise from a GRE.

More than one testamentary trust can fund a QDT.

Only one QDT per electing beneficiary.

17

Insurance trusts as QDT’s

Tips, traps and other considerations

Only one QDT per electing beneficiary.

E.g. different will-makers cannot create different QDTs for the same electing beneficiary.

Drafting challenges inter-connecting Wills/testamentary trusts.

Watch for pour-over clauses and incorporation by reference issues – Kellogg Estate v. Kellogg, 2013 BCSC 2292 – affirmed 2015 BCCA 201.

Wills Act not WESA

18

QDT’s - other

Tips, traps and other considerations

Electing disabled beneficiary must be named in trust instrument

Use of generic terms in trust instrument (i.e. children, issue, descendants)

Beneficiary not disabled at the time of preparing Will or trust instrument?

S.122(2) – Anti avoidance rule

Draft to minimize recovery tax

19

QDT’s - other

Tips, traps and other considerations

Does the beneficiary qualify for provincial disability benefits?

Consider Employment and Assistance for Persons with Disabilities Act, S.B.C. 2002

Careful where beneficiary does not qualify for provincial disability, but still qualify for DTC

Joint last to die policies – where the life insureds die simultaneously

Beneficiary designation must consider such scenario.

How are insurance proceeds treated?

20

Tax liability in life interest trusts on death

21

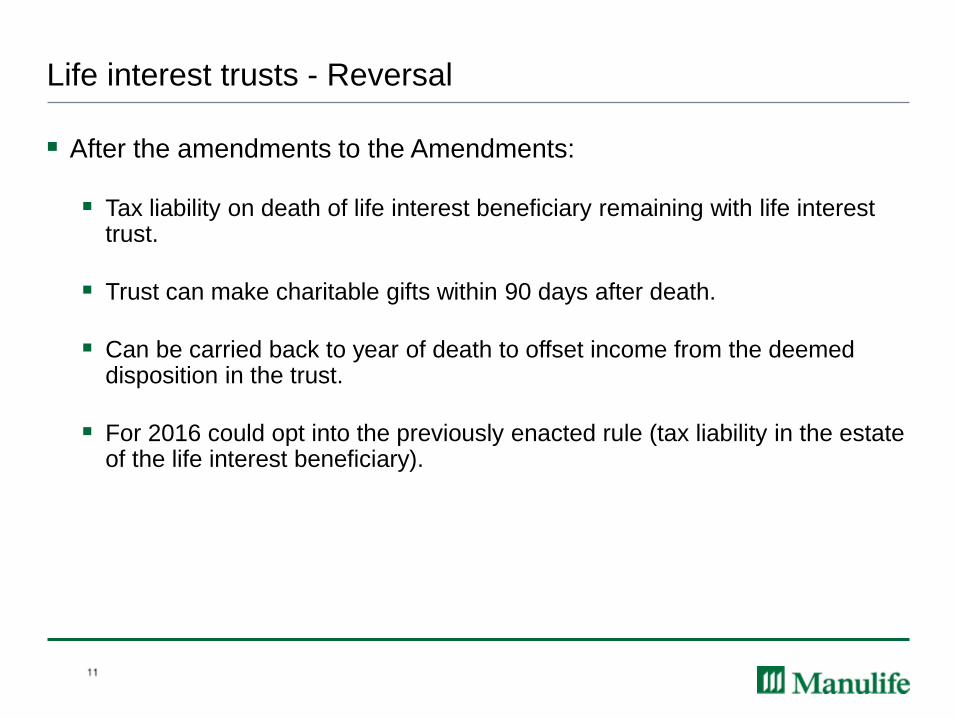

Life interest trusts - Reversal

After the amendments to the Amendments:

Tax liability on death of life interest beneficiary remaining with life interest trust.

Trust can make charitable gifts within 90 days after death.

Can be carried back to year of death to offset income from the deemed disposition in the trust.

For 2016 could opt into the previously enacted rule (tax liability in the estate of the life interest beneficiary).

Life Insurance in life interest trusts?

Insurance proceeds to pay tax liabilities triggered on spouse’s death…

Trust pays

premiums

from trust

capital

Trust is owner

and

beneficiary of

insurance

proceeds

Spouse

beneficiary

is the life

insured

Life

interest

Trust

23

Life insurance in life interest trusts

What’s the problem?

CALU 2012 CRA Roundtable – #2012-0435681

A person other than the spouse/surviving partner/settlor may obtain the use of the trust income or capital

Whether a positive duty or mere ability to pay premium/buy life insurance

Taints the trust – no rollover of capital property

24

Life insurance in life interest trusts

Problem is not resolved

CALU submission in August 2013.

Request for technical interpretation April 2014.

CRA #2014-052936 – confirmed prior response.

25

Life insurance in life interest trusts

Query: how does a trustee reconcile CRA’s position with:

BCCA’s decision in Miles v. Vince, the 2014 BCCA 289, or

Section 15.2 of Trustee Act

A trustee ought to use ordinary skill, prudence and common sense to preserve trust assets for the beneficiaries of an insurance trust.

Consider a spousal trust in a blended family scenario where contingent beneficiaries are the children of the deceased spouse.

What if the terms of the trust require the trustee to preserve all or part of the capital for other beneficiaries?

26

What now?

Paid-up policy to a life interest trust – OK

#2012-0453891C6 – Joint-last-to-die policy with premiums to first death transferred to spousal trust does not taint the trust

BUT…

No rollover of policy into the trust (148.2 applies to transfer or distribution to a surviving spouse)

27

What now?

Department of Finance verbal comments at CALU meeting May 3, 2016

May consider rollover to a spousal trust.

Instead of rolling policy to spousal trust, name trustee of the spouse trust as successor owner and beneficiary of the policy?

28

What now?

Corporate-owned insurance – flow capital dividend to trust where trust holds shares of a corporation

Encroach on capital in favour of life interest beneficiary to purchase personally-owned policy naming life interest trust as beneficiary

29

Charitable donations at death

30

Charitable donations at death

For deaths after 2015, where a charitable gift is made by:

“Will”, direct designation, or the estate:

Gift is deemed to be made by the estate (and by no other person)

At the time the property is transferred to the charity (and at no other time)

This is so whether the estate is the GRE or not.

31

Charitable donations at death

If the GRE and gift is made within the first 60 months of death.

Can claim up to:

75% of net income in the year the gift is made or prior year of the GRE.

100% of net income in the deceased’s terminal return with a one year carry back.

75% of net income in the 5 or 10 (depending on the property) years following the year of the gift – the regular estate/trust rule.

Malcolm Burrows – estate donation loop?

32

Potential Problems With GRE Gifts

33

The following could delay estate administration beyond 60 months:

Probate process

Wills variation claims

Creditor claims

Tax clearance process

Complex estates

Illiquid assets

Gift by direct designation is speedy!

118.1(5.2) requirements:

Transfer made as a consequence of death by an insurer to a charity because of obligations under a policy .

The charity is not owner nor assignee.

Policy is on the life of the individual donor.

Individual’s consent required to change the recipient.

Designating the charity as an irrevocable beneficiary not a problem (#2004-65451C6).

34

Direct designations – a Primer

Direct designations – a Primer

Traps: Corporate-owned life insurance naming charity as beneficiary

No gift – proceeds received by operation of contract

No CDA credit (corporation is not beneficiary)

Alternative: Corporation as beneficiary could donate proceeds of life insurance policy to charity

Charitable deduction (subsection 110.1(1))

CDA credit

35

Gift of private company shares at death

Gift of “non-qualifying security” (NQS) ignored unless charity monetizes gift within 60 months.

Common strategy – donate shares to private foundation by Will with insured share redemption.

“The particular time” of the gift for purposes of the NQS rules is when the shares are transferred by the estate to the charity.

The same time that the gift is deemed to be given for the estate donation rules.

If the GRE, then able to flexibly claim the donation credits.

36

Gift of private company shares at death

Another way out of the NQS rules is to be an “excepted gift”

Where gift of private company shares at death to public foundation previously was an “excepted gift”.

STEP 2015 CRA comment – Gift by estate = Non-arm’s length – not “excepted gift”.

Need to monetize gift.

Insured share redemption can monetize the gift

37

2016 Federal Budget and Life Insurance

38

2016 Federal Budget and Life Insurance

1. CDA Credit and Life Insurance

2. Life Insurance Policy Transfers to Related Corporation

39

40

CDA Credit and Life Insurance

Generally Capital Dividend Account (CDA) credit equals

death benefit minus

adjusted cost basis (ACB)

The mischief – in corporate context, separating ownership of policy from beneficiary so that the corporate beneficiary has no cost associated with the policy.

The solution – cost basis follow the death benefit no matter who owns the policy.

41

CDA Credit and Life Insurance

Prior to March 22, 2016

CDA credit reduced by ACB of “the policy to the corporation”

After March 21, 2016

CDA credit reduced by ACB of “a policyholder’s interest in the policy”

Potential double grind in “split dollar”/co-ownership situations?

New reporting obligation where beneficiary is different than policyholder.

Valid business reasons may include:

Creditor protection from the creditors of Opco’s during life

Funding differences accommodated based on shareholders’ preferences while still funding redemption buy-sell

No need to transfer policy out of Opco on sale

42

CDA Credit and Life Insurance – Does this structure work?

Shareholder

Opco

Beneficiary

Holdco

Policy Owner

Additional issue:

Prior CRA commentary re: potential benefit conferral.

Will reporting mechanism allow CRA to find places to apply this logic?

43

CDA Credit and Life Insurance – Does this structure work?

Shareholder

Opco

Beneficiary

Holdco

Policy Owner

44

Life Insurance Policy Transfers to Related Corporation

The Mischief - Prior to March 22, 2016

Transferor’s proceeds = CSV (ss 148(7))

Transferee’s ACB = CSV

Allowed shareholder to extract FMV proceeds tax free

Transferor policy gain where CSV > ACB

Shareholder

Life

Insurance

Policy

Holdco

$$

45

Life Insurance Policy Transfers to Related Corporation

The Solution - After March 21, 2016

Transferor’s proceeds = greater of:

i. CSV of interest in the policy;

ii. FMV of consideration given; and

iii. ACB of interest in the policy immediately before the disposition

Should consider taking proceeds equal to greater of ACB and CSV

All proceeds in excess of ACB now fully taxable

Shareholder

Life

Insurance

Policy

Holdco

$$

46

Life Insurance Policy Transfers to Related Corporation

The Solution - After March 21, 2016

Transferee’s ACB = transferor’s proceeds

Could be higher than CSV

Shareholder

Life

Insurance

Policy

Holdco

$$

47

Life Insurance Policy Transfers to Related Corporation

Retroactive Application

Permanent CDA Reduction where:

Policy transferred

After 1999

Before March 22, 2016

Consideration > CSV received

CDA credit at death reduced by excess consideration

Shareholder

Life

Insurance

Policy

Holdco

$$

48

Life Insurance Policy Transfers to Related Corporation

CRA always considered “tax-free excess consideration” inappropriate.

Unusual “catch-up” proposal to “fix” situations where excess consideration was previously taken.

Shareholder

Life

Insurance

Policy

Holdco

$$

Transfer of Life Insurance Policy to Related Corporation

Consider the following fact pattern:

Jack owns an Innovision policy issued in 1999

$1,000,000 death benefit

CSV = $383 (say $400)

ACB = $54,572 (say $55,000)

FMV of policy = $505,000

49

Jack

HOLDCO

Life

Insurance

Policy

$505,000

100%

Transfer of Life Insurance Policy to Related Corporation

Jack

Owns 100% of Holdco

Transfers policy to Holdco

Takes $505,000 of consideration

50

Jack

HOLDCO

Life

Insurance

Policy

$505,000

100%

Transfer of Life Insurance Policy to Related Corporationfor Consideration = FMV = $505,000

51

Pre Budget Post Budget

Implications to: Transfer & Death

Before

3/22/16

Transfer after 1999 &

before 3/22/16 & Death on

or after 3/22/16

Transfer & Death After

3/21/16

Jack

Proceeds $400 $400 $505,000

Policy Gain $0 $0 $450,000

Tax-free amount $505,000 $505,000 $0

Holdco

Initial ACB $400 $400 $505,000

Maximum future CDA

credit $1,000,000 $495,000 $1,000,000

Transfer of Life Insurance Policy to Related Corporationfor Consideration = Nil

52

Death after March 21, 2016

Implications to: Transfer Before

3/22/16

Transfer After

3/21/16

Jack

Deemed

Proceeds

$400 $55,000

Policy Gain $0 $0

Tax-free amount $0 $0

Holdco

Initial ACB $400 $55,000

Maximum future

CDA credit $1,000,000 $1,000,000

Assume:

FMV = $505,000

CSV = $400

ACB = $55,000

Old Rules:

Proceeds to Jack = CSV

New Rules:

Proceeds to Jack = greater of:1. FMV of Consideration Given;

2. CSV; and

3. ACB

Transfer of Life Insurance Policy to Related Corporationfor Consideration = ACB

53

Death after March 21, 2016

Implications to: Transfer Before

3/22/16

Transfer After

3/21/16

Jack

Deemed

Proceeds

$400 $55,000

Policy Gain $0 $0

Tax-free amount $55,000 $55,000

Holdco

Initial ACB $400 $55,000

Maximum future

CDA credit $1,000,000 $1,000,000

Assume:

FMV = $505,000

CSV = $400

ACB = $55,000

Old Rules:

Proceeds to Jack = CSV

New Rules:

Proceeds to Jack = greater of:1. FMV of Consideration Given;

2. CSV; and

3. ACB

Conclusion re Transfer from Individual to Corporation

Always consider taking back consideration equal to the greater of CSV and ACB

It will be your deemed proceeds anyway

But watch if ACB greater than FMV

54

Retrospective rule applies to all transfers where consideration in excess of CSV was paid.

E.g. Opco to Holdco transfer where Holdco paid FMV to Opco to avoid a shareholder benefit.

For current transfers at FMV (for example in Opco to Holdco situation) ACB to Holdco reset to FMV may give an unfair result if death occurs prematurely.

Tax to Opco on gain using FMV as proceeds of disposition.

CDA credit to Holdco ground down by high (starting from FMV) ACB.

Dividend in kind – no excess consideration may be the best answer (Provided 55(2) is not a concern!)

55

Transfer rules – Other Issues/Observations

56

Case Law Update

Beneficiary designations and competing legal interests/principles

Separation agreements or court orders sometimes include a clause requiring one former spouse to maintain a life insurance policy on his or her life naming the other as the beneficiary.

What happens if, contrary to a separation agreement or court order, the party required to maintain the life insurance cancels the policy or changes

the beneficiary? Milne Estate v. Milne 2014 BCSC 2112

Spouses often acquire life insurance on their lives and designate each other as the beneficiaries.

What happens where on the breakdown of a spousal relationship one spouse fails to change the beneficiary designation? Schiller-Arsenault v. Proudman 2015 BCSC 1924

57

Beneficiary designations and competing legal interests/principles

Milne Estate v. Milne 2014 BCSC 2112

What happens if, contrary to a separation agreement or court order, the party required to maintain the life insurance cancels the policy or changes the beneficiary?

58

Beneficiary designations and competing legal interests/principles

Milne Estate v. Milne 2014 BCSC 2112

Following the breakdown of their relationship, Scott Milne entered in a consent order to maintain a $500,000 life insurance with Sherry Milne as the beneficiary.

Mr. Milne changed the beneficiary to his new partner, Albertina Vincente.

Mr. Milne died, while still obligated to pay child support to Ms. Milne for their son.

Ms. Milne claimed that:

She was entitled to the insurance proceeds because Mr. Milne was in breach of the consent order.

If she wasn’t entitled to the proceeds, then she was entitled to the $500,000 out of estate.

59

A breach of an agreement to designate and maintain the supported spouse as a beneficiary is actionable in damages against the personal representatives of the supporting spouse’s estate

(Phillips v. Spooner (1980), 7 E.T.R. 157 (Sask. C.A.); Re Taylor (1985), 48 R.F.L. (2d) 214 (B.C.S.C.); Fraser v. Fraser (1995), 9 E.T.R. (2d) 136 (B.C.S.C.); Munro v. Munro Estate (1995), 4 B.C.L.R. (3d) 250 (C.A.)).

Such a breach may also result in life insurance proceeds being impressed with a trust in the supported spouse’s favour

(Fraser v. Fraser; Gregory v. Gregory (1994), 92 B.C.L.R. (2d) 133 (S.C.); Re Ladner Estate (sub nom. Ladner v. Ladner), 2004 BCCA 366.

60

Beneficiary designations and competing legal

interests/principles

Ms. Vincente entitled to retain the insurance proceeds.

Ms. Milne entitled to receive the $500,000 from Mr. Milne’s estate.

Query whether the result would have been the same if the estate did not have enough funds to pay Ms. Milne?

61

Beneficiary designations and competing legal

interests/principles

Lessons

Consider irrevocable beneficiaries, or

An assignment of the life insurance policy, or

Both?

62

Beneficiary designations and competing legal

interests/principles

Schiller-Arsenault v. Proudman 2015 BCSC 1924

Does a separation agreement extinguish a former spouse’s right to receive insurance proceeds?

63

Beneficiary designations and competing legal interests/principles

Schiller-Arsenault v. Proudman 2015 BCSC 1924

In 2008, Deceased purchased a policy on her life.

Mr. Proudman designated as a revocable beneficiary.

Their relationship broke down and they entered into a separation agreement.

Deceased removed Mr. Proudman as a beneficiary of her will, pension plan, RRSPs and other benefits.

Did not remove designation on the insurance policy.

Ms. Schiller-Arsenault brought and Mr. Proudman filed a claim to the proceeds of the policy.

64

Beneficiary designations and competing legal interests/principles

Schiller-Arsenault v. Proudman 2015 BCSC 1924

Position of Ms. Schiller-Arsenault

Deceased took all steps to change beneficiaries of her estate.

Court should infer that a change of beneficiary was submitted.

Mr. Proudman is:

Barred by reason of the separation of agreement.

In breach of the terms of the separation agreement.

Court should remedy breach through a constructive trust or damages in equivalent to the value of the policy.

65

Schiller-Arsenault v. Proudman 2015 BCSC 1924

Position of Mr. Proudman

Named beneficiary of the policy.

No evidence that deceased filed a change of beneficiary.

No documentary evidence sufficient to act as a revocation under the Insurance Act (BC).

Separation agreement does not specifically refer to life insurance policies.

66

Schiller-Arsenault v. Proudman 2015 BCSC 1924

The court’s analysis:

The leading case BCCA decision in Roberts v. Martindale (1998 case):

Deceased and the defendant (Mr. Martindale) were former spouses.

Divorced prior to the death of the deceased.

During the marriage deceased designated defendant as beneficiary of group life insurance.

Deceased and Mr. Martindale entered into a separation agreement.

At all times after separation and divorce, deceased intended to arrange her affairs so that Ms. Roberts would inherit her estate.

Deceased and Ms. Roberts believed that beneficiary designation had been revoked.

67

Beneficiary designations and competing legal interests/principles

The court’s decision:

The court followed the decision in Roberts v. Martindale.

Mr. Proudman was under an equitable obligation to refrain from taking any steps to pursue a claim o the insurance proceeds.

He filed a claim to the insurance proceeds in breach of his contractual obligations under the separation agreement.

It does not matter that the separation agreement does not refer specifically to policies of insurance.

It is clear that it was intended to be a full and final settlement of entitlement to any and all property, including life insurance.

Proceeds be paid to Ms. Schiller-Arsenault.

68

Beneficiary designations and competing legal interests/principles

What if the beneficiary designation was irrevocable?

Tarr Estate v. Tarr, 2013 BCSC 1994

Deceased’s former wife named irrevocable beneficiary of pension benefits.

Deceased and former wife entered into a separation agreement.

69

Beneficiary designations and competing legal interests/principles

Agreement purported to be final resolution of all issues between the spouses, including:

Division of property and debts,

Life insurance and succession rights, and

Included a general release of all claims.

After death of Mr. Tarr, his former wife refused to release her claim to the pension benefits.

In this case, specific mention is made to the pension in the separation agreement.

70

What if the Beneficiary Designation was Irrevocable

Court's findings:

Pension administrator cannot change the beneficiary designation.

But the beneficiary can waive her rights to the benefits.

Court has the power to order that the beneficiary not entitled to benefits.

Beneficiary has a duty to hold benefits in trust for a newly designated beneficiary.

By virtue of the separation agreement, Ms. Tarr relinquished her right to benefits.

Retaining the benefits in breach of the agreement.

Gives rise to remedial constructive trust to enforce the bargain the Tarrs have made.

71

Cases Going the Other Way

Wilson Estate v. Wysoski, 2014 BCSC 675

No separation agreement.

The former spouse had not contractually renounced her claim.

No breach of contract.

72

Cases Going the Other Way

Soulos v. Korkontzilas [1997] 2 S.C.R. 217

There has to be wrongful conduct on the part of defendant in order to find a good conscience trust.

73

Lessons

A separation agreement should clearly state intention to resolve all issues between the parties, including life insurance policies.

If agreement does so, claiming proceeds under a beneficiary designation will likely constitute wrongful conduct.

May give rise to a remedy under contract or equity.

74

Thank you