institutional presentation - jefferies · disclaimer this release contains forward-looking...

TRANSCRIPT

Institutional Presentation June/2016

V2

Disclaimer

This release contains forward-looking statements that are exclusively related to the prospects of the business, its operating

and financial results, and prospects for growth. These data are merely projections and, as such, based exclusively on our

management's expectations for the future of the business and its continued access to capital to fund its business plan. These

forward-looking statements substantially depend on changing market conditions, government regulations, competitive

pressures, the performance of the Brazilian economy and the industry, among other factors, as well as the risks shown in our

filed disclosure documents, and are therefore subject to change without prior notice.

As a goal to maintain a correlation with the Financial Statements prepared by its external auditors, the considerations and

comments contained herein are prepared on a consolidated viewpoint of the economic group Hypermarcas, and not

necessarily individualized by the various legal entities that compose the group.

In addition, unaudited information herein reflects management's interpretation of information taken from its financial

statements and their respective adjustments, which were prepared in accordance with market practices and for the sole

purpose of a more detailed and specific analysis of our results. Therefore, these additional points and data must also be

analyzed and interpreted independently by shareholders and market agents, who should carry out their own analysis and

draw their own conclusions from the results reported herein. No data or interpretative analysis provided by our management

should be treated as a guarantee of future performance or results and are merely illustrative of our directors' vision of our

results.

Our management is not responsible for compliance or accuracy of the management financial data discussed in this report.

which must be considered as for informational purposes only, and should not override the analysis of our audited

consolidated financial statements for purposes of a decision to invest in our stock, or for any other purpose.

2

Agenda

• Overview

• Brazil Pharma Market

• Our Business

• Financials

3

Business overview

4

38% 30%

32%

Net Rev: R$3.0 bn

Gross Margin: 74.9%

Rankin

g

Key f

acts

Branded

Prescription

Generics

Consumer

Health

#1 Hypermarcas Aché EMS

#2 Sanofi Sanofi Hypermarcas

#3 Bayer Eurofarma Sanofi

#4 Boehringer Novartis Novartis

#5 Takeda Hypermarcas Teuto

1Q16 LTM

Revenue Breakdown Branded

Prescription¹

Consumer

Health

Generics²

Focus in Brazil Long experience

Fast growing/

resilient market Diversified portfolio

SOURCE: Company financials; IMS Health; Hypermarcas. ¹ Ex-patents. ² Generics includes Branded Generics.

Ownership and listings

¹ April 30, 2016 LTM

² April 28, 2016

³ April 31, 2016

SOURCE: BM&F Bovespa; Hypermarcas 5

Ownership structure Listings

• Sao Paulo Stock Exchange: - HYPE3

- BRHYPEACNOR0

• Indexes with Hypermarcas:

• Ibovespa Index Ranking³: 24/59

• Trade volume¹: 2.6 MM shares/day

• ADR (HYPMY)²: 7.6 MM shares outstanding

• Market Cap³: R$18 B (USD5 B)

20.1%

14.8%

6.0%

59.1%

Igarapava Participações S.A.

Maiorem S.A. de C.V

Other Controlling Shareholders

Free Float

Founder

Free Float

Maiorem

Others

Agenda

• Overview

• Brazil Pharma Market

• Our Business

• Financials

6

Pharma market

SOURCE: IMS Health 7

2014 Trends 2019

1st United States

2nd China

3rd Japan

4th Germany

5th France

6th USD24 bn

7th Italy

1st United States

2nd China

3rd Japan

4th Germany

5th USD36 bn

6th France

7th Italy

• Aging

• Underdeveloped health

system

• Treatments’ low levels

• Generics low

penetration of generics

(25% of market)

• Peak in economically

active population

Large and growing pharmaceutical market (R$ billion)

SOURCE: IMS Health – PPP (March 2016). 8

32.4

35.9

40.0

44.2

2012 2013 2014 2015

CAGR 2012-15: 10.9%

High entry barriers

Regulator

• Long approval

process (3-5 years)

• Strict control of

manufacturers,

products and

retailers

9

Fragmented Distribution

• Continental country

(27 states; >200 people)

• ~70k point of sales

• 18 larger chains

• ~200 distributors

Powerful Local Brands • Powerful local brands

• All generics are branded at retail as

most of the world (ex-US & Canada)

1960 2016

USA Brazil

Retail pharma market

# companies to reach 42% of market share Pharma Retail

(% Sales)

42% 58%

Larger

Retail

Chain

Smaller Retail

Chain &

Independent

SOURCE: IMS Health World Review Conference 2016 (May 5, 2016; Dinâmicas e Perspectivas do Mercado Farmacêutico da

América Latina e do Brasil); IMS PMB-PPP February 2016; Hypermarcas. Larger retail chains are the Abrafarma members.

* Chains that are member of Brasil Pharma; also listed in Brazil.

73 K Point of Sales (POS)

10

67 K POS 6 K POS

4.7x

Manufactures (6) Larger Retailers (28)

Companies listed in Brazil

*

*

*

Retail pharma market

11

Business

Segment

Product

Category

Demand

Driver

Market

Size

Patents

Branded

Prescription

Trade

DTC

5%

60%

17%

18%

• RX with/without

prescription retention

• OTX

• Dermocosmetics

R$24.9B Physicians

• OTC

• Nutritionals

• Related products

R$6.9B Consumer

• Innovative patent protected R$2.3B Physicians

• Generics

• Smart Generics R$7.7B Pharmacist

SOURCE: IMS Health Oct. 2015

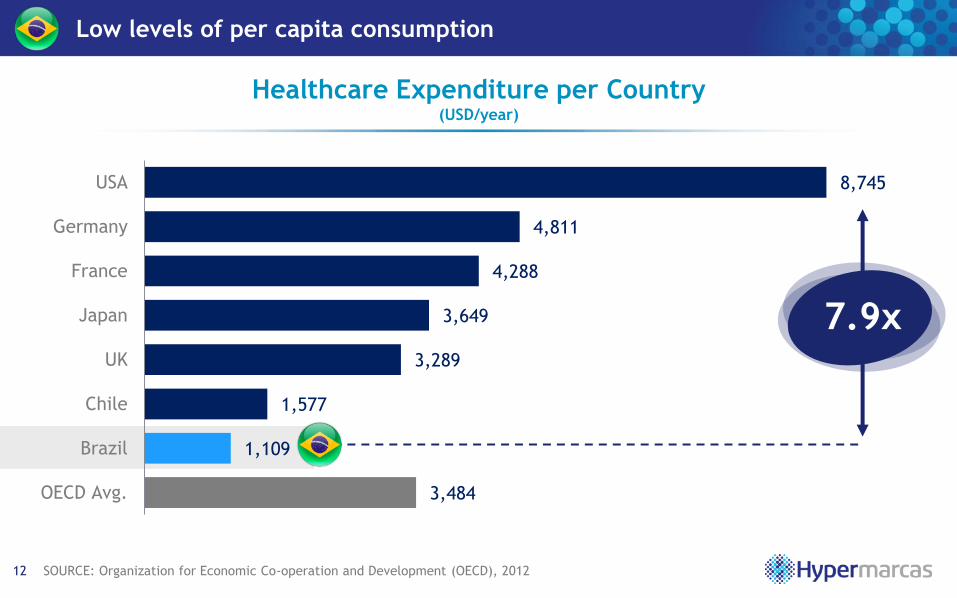

Low levels of per capita consumption

SOURCE: Organization for Economic Co-operation and Development (OECD), 2012 12

3,484

1,109

1,577

3,289

3,649

4,288

4,811

8,745

OECD Avg.

Brazil

Chile

UK

Japan

France

Germany

USA

Healthcare Expenditure per Country (USD/year)

7.9x

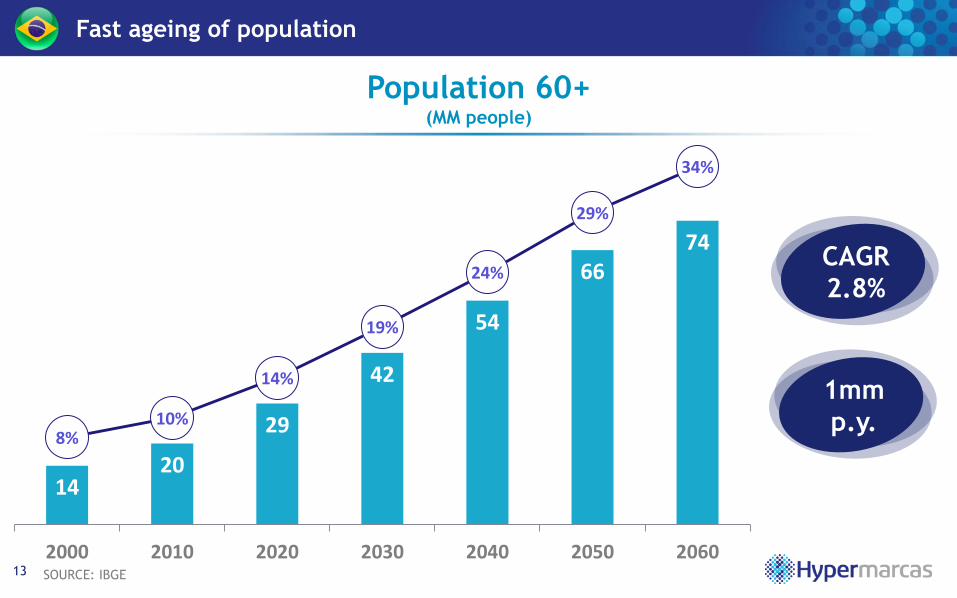

Fast ageing of population

SOURCE: IBGE 13

Population 60+ (MM people)

CAGR

2.8%

14 20

29

42

54

66 74

8% 10%

14%

19%

24%

29%

34%

0%

5%

10%

15%

20%

25%

30%

35%

0

10

20

30

40

50

60

70

80

90

2000 2010 2020 2030 2040 2050 2060

1mm

p.y.

Potential for higher drug consumption

SOURCE: IBGE (Consumer Expenditure Survey 2008-09); Values readjusted by inflation (IPCA) to April 2016. 14

Prescription Drugs Expenditure (R$ per month / family)

205.2

198.2

134.1

99.7

73.1

60.0

46.4

70+

60-69

50-59

40-49

30-39

20-29

10-19

4.3x

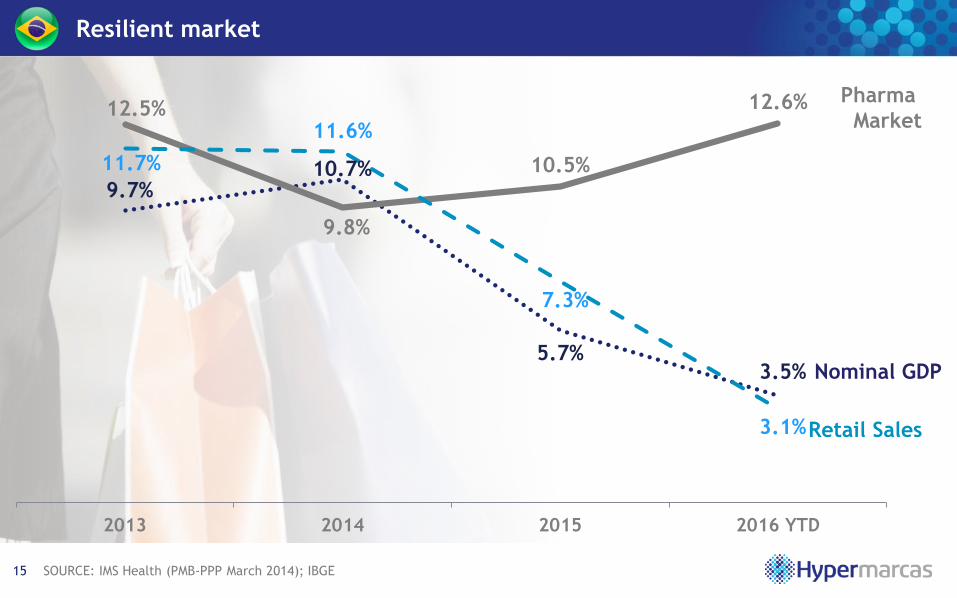

Resilient market

SOURCE: IMS Health (PMB-PPP March 2014); IBGE 15

9.7% 10.7%

5.7% 3.5%

12.5%

9.8%

10.5%

12.6%

11.7%

11.6%

7.3%

3.1%

2013 2014 2015 2016 YTD

Pharma

Market

Nominal GDP

Retail Sales

Agenda

• Overview

• Brazil Pharma Market

• Our Business

• Financials

16

Pharma scope

17

Pharmaceuticals

Cosmetics Food

Dermo-

cosmetics

Nutra-

ceuticals

Nutritionals

Nutri-

cionals

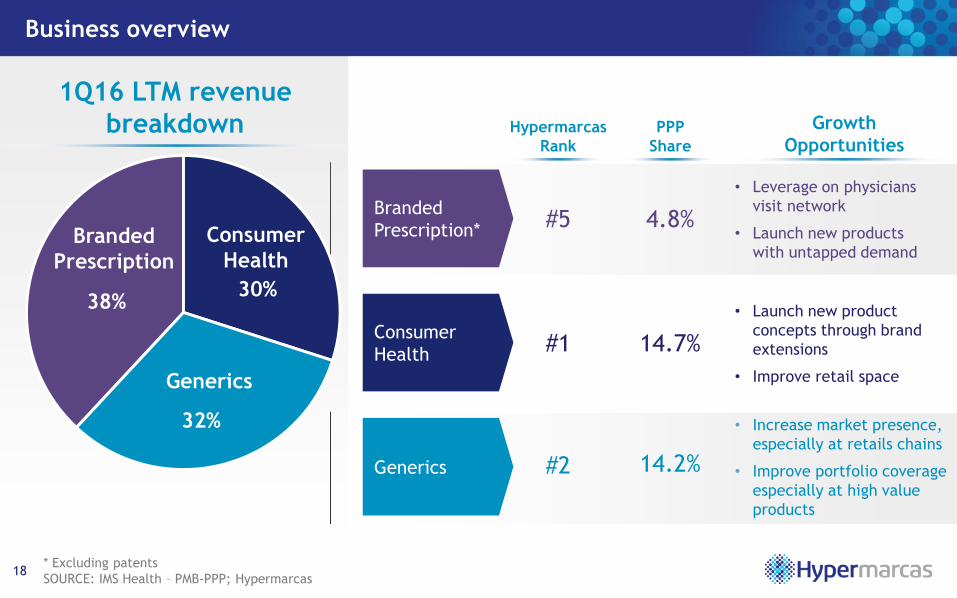

Business overview

* Excluding patents

SOURCE: IMS Health – PMB-PPP; Hypermarcas 18

Hypermarcas

Rank

PPP

Share

Growth

Opportunities

Consumer

Health

Generics

Branded

Prescription*

#1

#2

#5

14.7%

14.2%

4.8%

• Launch new product

concepts through brand

extensions

• Improve retail space

• Increase market presence,

especially at retails chains

• Improve portfolio coverage

especially at high value

products

• Leverage on physicians

visit network

• Launch new products

with untapped demand

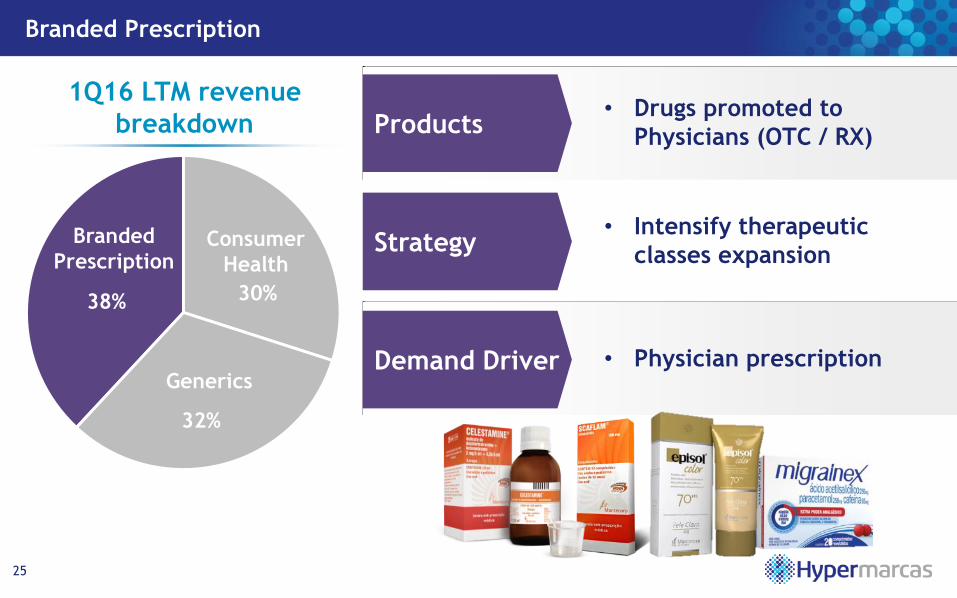

1Q16 LTM revenue

breakdown

38% 30%

32%

Branded

Prescription

Generics

Consumer

Health

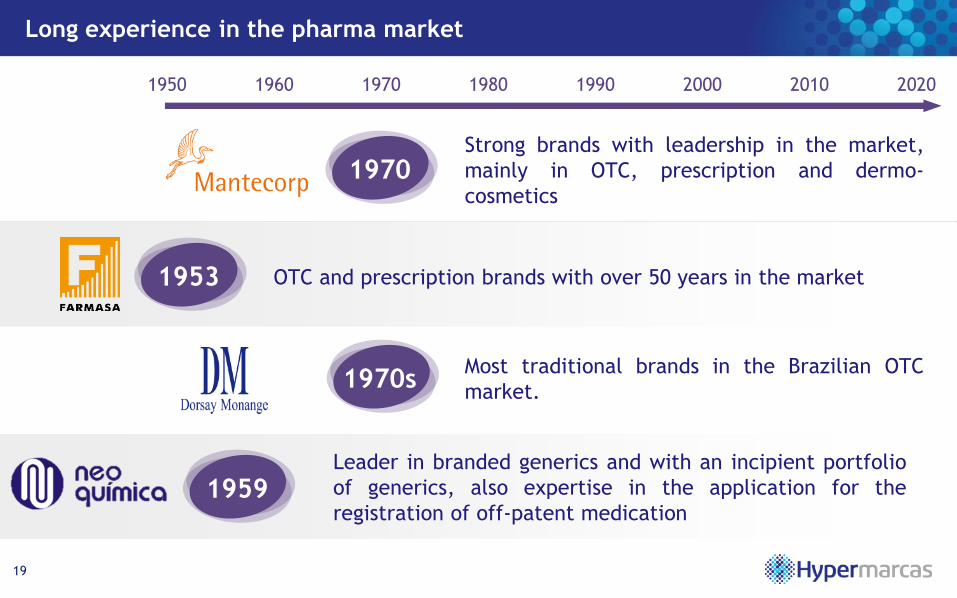

Long experience in the pharma market

19

1950 1970 1980 1990 2000 2010 2020 1960

1970

1953

1970s

1959

Strong brands with leadership in the market,

mainly in OTC, prescription and dermo-

cosmetics

OTC and prescription brands with over 50 years in the market

Most traditional brands in the Brazilian OTC

market.

Leader in branded generics and with an incipient portfolio

of generics, also expertise in the application for the

registration of off-patent medication

Consistent gains in market share

SOURCE: IMS Health – PMB–PF (2015) 20

7.5%

8.0%

8.5%

9.2%

9.9%

10.5%

2010 2011 2012 2013 2014 2015

Increasing importance of innovation

7.7% 8.4%

11.4%

17.7%

2012 2013 2014 2015

21 SOURCE: Company data, 2015. % Revenues from pharmaceutical products launched over the past 3 years.

Innovation (% Net Revenues)

Diversified distribution

22

32%

Direct

channel

Indirect

channel

57%

Distributor/

Wholesaler

Logistics

Operation

Retailer

Warehouse 11%

Distributor

delivers

Hypermarcas

takes

orders

Store SOURCE: Company Data, 2015

Large scale production facility

23

323,000 m2 land 120,000 m2 constructed area 3,700 employees

Distribution

Center

Solids/

Raw

Materials

Quality

Control

Aerosol

Efervecent

Dermo Liquids

Semisolids

Injectables

R&D

Penicilin Solids

Semisolids

Liquids

R&D

High production capacity

SOURCE: Hypermarcas, per year 24

Tablets,

capsules,

coated tablets,

pills and

effervescent

10 billion

Injectable and

ophthalmic

45 million

Aerosols

11 million

Liquids,

creams, oils,

ointments,

lotions and

jellies

276 million

Branded Prescription

25

Products

Strategy

Demand Driver

• Drugs promoted to

Physicians (OTC / RX)

• Intensify therapeutic

classes expansion

• Physician prescription

38% 30%

32%

Branded

Prescription

Generics

Consumer

Health

1Q16 LTM revenue

breakdown

Branded Prescription Leverage on physician visit network

SOURCE: IMS Health (Factory Price); Hypermarcas 26

10.4%

1.1%

9.7%

11.9%

0.6%

2.7%

4.8%

87%

74%

85%

74%

78%

55%

69%

Orthopaedics

Psychiatry

Dermatology

Paediatrics

Cardiology

Gynecology

General Practice

Largest

Specialties Coverage

(% of prescriptions; Value) Market Share Portfolio

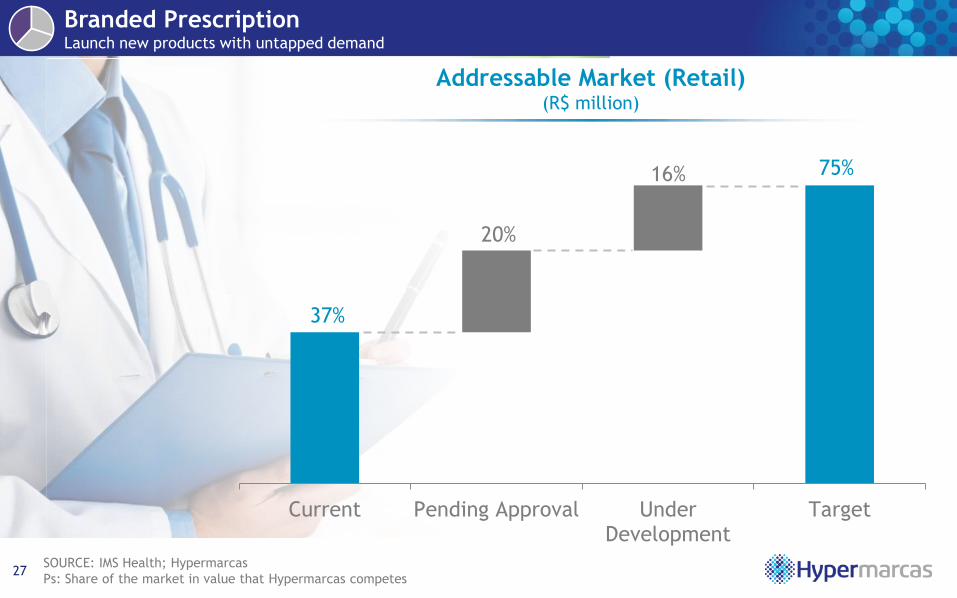

Branded Prescription Launch new products with untapped demand

27

Current Pending Approval UnderDevelopment

Target

37%

75%

20%

16%

Addressable Market (Retail) (R$ million)

SOURCE: IMS Health; Hypermarcas

Ps: Share of the market in value that Hypermarcas competes

Branded Prescription Launch new products with untapped demand

28 SOURCE: IMS Health – PMB PF Oct15 YTD

Concept

• Hypovitaminosis D

- Fractures

- Muscular strength

- Cardio diseases

• Treatment dosage

- Supplementation

- Attack dosage 10.4

12.5 14.3 14.9

12.9 15.4

25.0

32.2 31.2

36.7

50.1

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

290%

Pills

(Mar-2014)

Sell-Out (R$ million) 2016

Consumer Health

29

Products

Strategy

Demand Driver

• OTC

• Sweeteners

• Intensify brand extensions

• Mass media

38% 30%

32%

Branded

Prescription

Generics

Consumer

Health

1Q16 LTM revenue

breakdown

SOURCE: IMS Health – PMB Oct’15 30

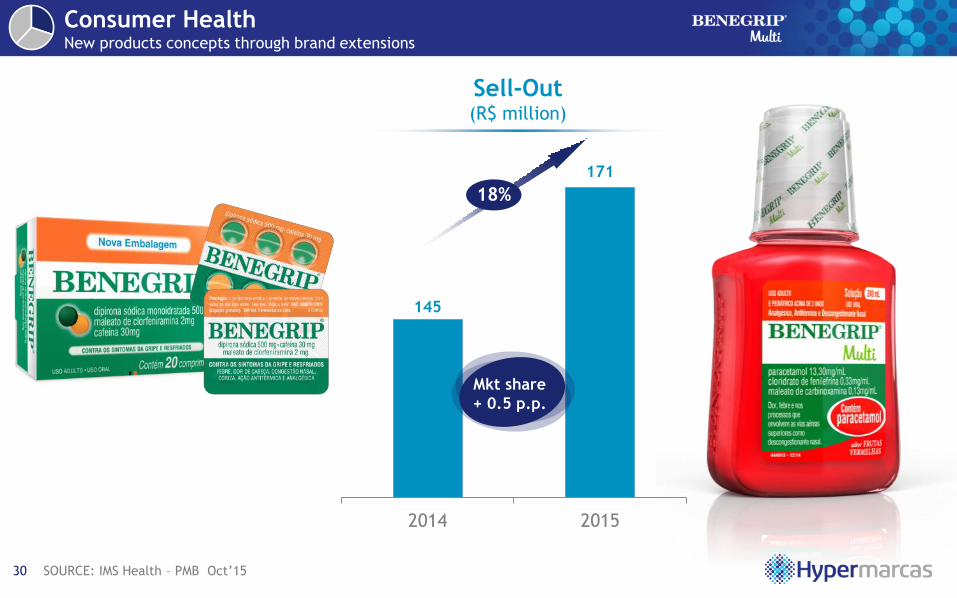

Consumer Health New products concepts through brand extensions

145

171

2014 2015

18%

Mkt share

+ 0.5 p.p.

Sell-Out (R$ million)

31

Consumer Health Improve retail space

Before After

Alphabetical Order

• All drugs (OTC & Prescriptions) were

mixed behind the counter

• OTC is organized per category and

“over the counter”

• Sales increase

• 30% in Value

• 23% in Volume

OTC behind the counter Counter removed

Generics

32

Products

Strategy

Demand Driver

• Generics (Large Chains)

• Smart Generics

(a.k.a. Similars; M&Ps)

• Defend & grow selectively

• Pharmacist

recommendation

38% 30%

32%

Branded

Prescription

Generics

Consumer

Health

1Q16 LTM revenue

breakdown

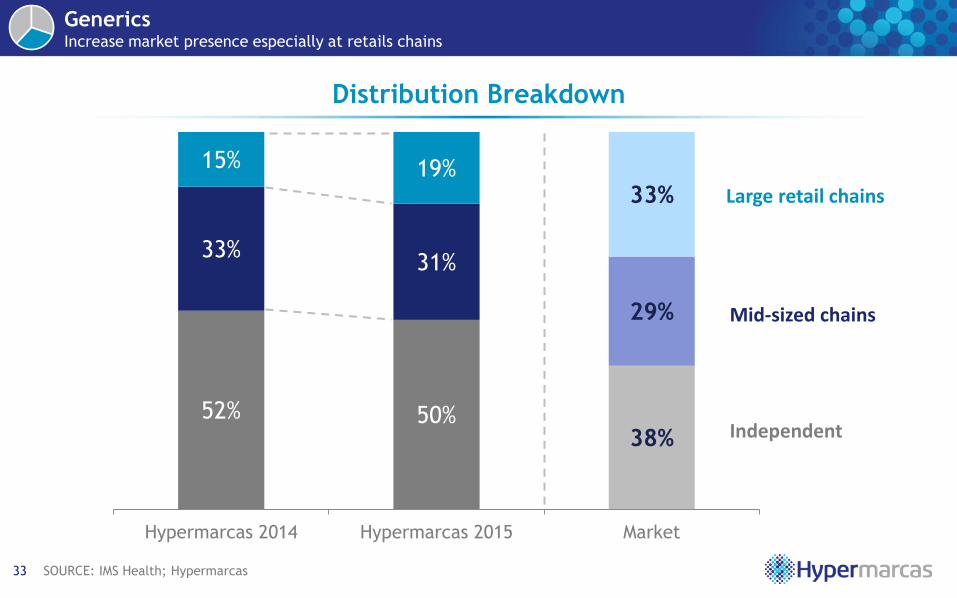

SOURCE: IMS Health; Hypermarcas 33

52% 50% 38%

33% 31%

29%

15% 19% 33%

Hypermarcas 2014 Hypermarcas 2015 Market

Distribution Breakdown

Large retail chains

Mid-sized chains

Independent

Generics Increase market presence especially at retails chains

Agenda

• Overview

• Brazil Pharma Market

• Our Business

• Financials

34

35

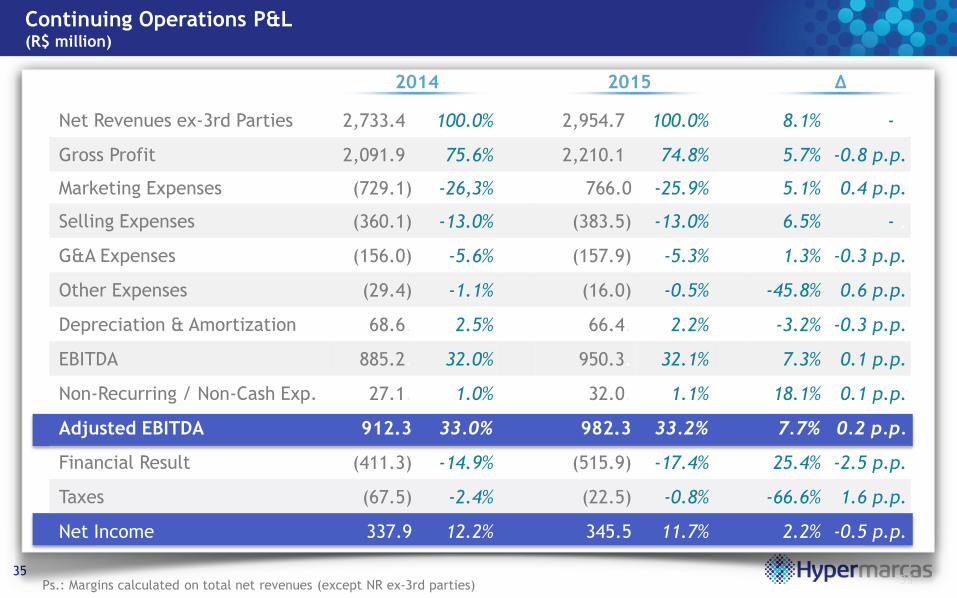

* Calculado com o EBITDA Ajustado dos últimos 12 meses

35

2014 ∆ 2015

Ps.: Margins calculated on total net revenues (except NR ex-3rd parties)

Net Revenues ex-3rd Parties 2,733.4. 100.0% 2,954.7. 100.0% 8.1% - .

Gross Profit 2,091.9. 75.6% 2,210.1. 74.8% 5.7% -0.8 p.p.

Marketing Expenses (729.1) -26,3% 766.0 -25.9% 5.1% 0.4 p.p.

Selling Expenses (360.1) -13.0% (383.5) -13.0% 6.5% - .

G&A Expenses (156.0) -5.6% (157.9) -5.3% 1.3% -0.3 p.p.

Other Expenses (29.4) -1.1% (16.0) -0.5% -45.8% 0.6 p.p.

Depreciation & Amortization 68.6. 2.5% 66.4. 2.2% -3.2% -0.3 p.p.

EBITDA 885.2. 32.0% 950.3. 32.1% 7.3% 0.1 p.p.

Non-Recurring / Non-Cash Exp. 27.1. 1.0% 32.0. 1.1% 18.1% 0.1 p.p.

Adjusted EBITDA 912.3 33.0% 982.3 33.2% 7.7% 0.2 p.p.

Financial Result (411.3) -14.9% (515.9) -17.4% 25.4% -2.5 p.p.

Taxes (67.5) -2.4% (22.5) -0.8% -66.6% 1.6 p.p.

Net Income 337.9 12.2% 345.5 11.7% 2.2% -0.5 p.p.

Continuing Operations P&L (R$ million)

Net Debt Reduction (R$ million)

36

Net Debt / EBITDA* Debt Profile

3.9x

3.1x 2.9x

2.6x

1.7x

-0.7x

2011 2012 2013 2014 2015 LTMProforma

3T15

Gross Debt 2,190.4

Cash (2,054.9)

Net Debt 135.5

Hedge (352.0)

Net Debt after Hedge (216.6)

(540.0)

Net Debt after RB Deal (756.6)

Remaining Proceeds from RB Deal

1Q16

* Until 2015, Adjusted EBITDA (EBITDA before non-recurring expenses and other non-cash expenses)

Company’s Main Tax Shields (1/4)

37

EV/EBITDA P/E Cash flow Returns Net income Possible analysis impacts

Tax Shield Summary

R$ MillionExpense for

Tax onlyTax Rate Cash Value* Origin

Goodwill 2.519 34% 857 - Acquisitions; Amortizable for tax purporses only

- It does NOT impact the PnL, only the Cash Flow

Income Losses 1.192 - Negative pretax due to Goodwill amortization

Federal Credits 630 - Withholding tax from investments

- Credits from Acquisitions

Total 2.678

1,878 639

1,011

291

1,941

Source: Hypermarcas

¹ Federal tax credits are usable to pay any federal tax payment

38

Phone: +55 (11) 3627-4242

http://www.hypermarcas.com.br/ir