insights from fidelity’s portfolio management team › bin-public › 060_ › docum… · 1...

TRANSCRIPT

1

Insights from Fidelity’s Portfolio Management TeamNaveen Malwal, CFAInstitutional Portfolio Manager

JANUARY 21, 2020

22

Common Investor Challenges

3

“The biggest investing errors come not from factors that are informational or analytical, but from those that are psychological.”

HOWARD MARKS

4

Potential Pitfalls

5

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

PETER LYNCH

6

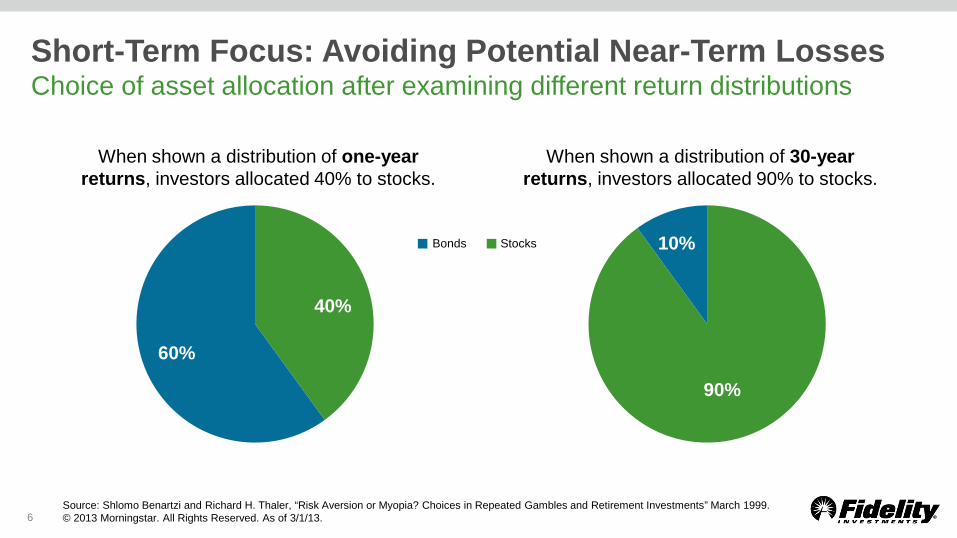

Short-Term Focus: Avoiding Potential Near-Term LossesChoice of asset allocation after examining different return distributions

When shown a distribution of one-year returns, investors allocated 40% to stocks.

When shown a distribution of 30-year returns, investors allocated 90% to stocks.

Source: Shlomo Benartzi and Richard H. Thaler, “Risk Aversion or Myopia? Choices in Repeated Gambles and Retirement Investments” March 1999. © 2013 Morningstar. All Rights Reserved. As of 3/1/13.

60%

40%

90%

10%Bonds Stocks

7

“In this world, nothing can be said to be certain except death and taxes.”

BENJAMIN FRANKLIN

8

Taxes Take a Bite Out of ReturnsImpact of taxes on investment returns, 1926–2018*

Past performance is no guarantee of future results. *This chart is for illustrative purposes only and does not represent actual or future performance of any investment option. Returns include the reinvestment of dividends and other earnings. Stocks are represented by the Ibbotson® Large Company Stock Index. Government bonds are represented by the 20-year U.S. government bond, cash by the 30-day U.S. Treasury bill, and inflation by the Consumer Price Index. An investment cannot be made directly in an index. The data assumes reinvestment of income and does not account for transaction costs. Please see Important Information section for additional information. Taxes Can Significantly Reduce Returns data, © Morningstar, Inc. All rights reserved. As of 2/25/19.

This study evaluated the potential effect of federal income taxes on returns of stocks and bonds, using the historical marginal and capital gains tax rates for a single taxpayer earning $120,000 in 2015 dollars every year, adjusted each year to the Consumer Price Index.

10.0%

5.5%

8.0%

3.4%

0%

2%

4%

6%

8%

10%

12%

20%

StocksBondsafter taxes

Aver

age

Annu

al R

etur

ns %

Stocksafter taxes Bonds

38%

99

Who We Are and Our Investment Process

10

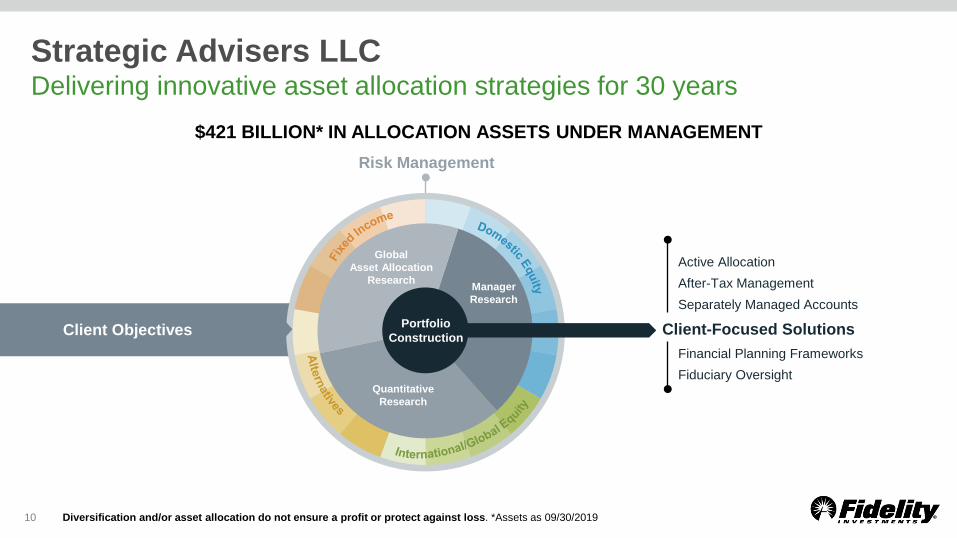

Strategic Advisers LLCDelivering innovative asset allocation strategies for 30 years

Diversification and/or asset allocation do not ensure a profit or protect against loss. *Assets as 09/30/2019

Financial Planning FrameworksFiduciary Oversight

Active AllocationAfter-Tax ManagementSeparately Managed Accounts

$421 BILLION* IN ALLOCATION ASSETS UNDER MANAGEMENT

Client Objectives Client-Focused SolutionsPortfolio Construction

Risk Management

Global Asset Allocation

Research

Quantitative Research

Manager Research

11

Strategic Advisers’ Key Investment Capabilities

Research

Manager AnalysisRisk and Return

Analysis

Portfolio Management

Investment SelectionRisk Management

Custom Investments

Multi-Manager FundsIndex Funds

Separately Managed Accounts

Personalization

Tax-Sensitive Investment Management

Personalized Trading

12

Long-term Asset Allocation Is One of the Most Important Drivers of Reaching Long-Term GoalsKnowing our clients helps inform our asset allocation decisions

For illustrative purposes only. Diversification and/or asset allocation do not ensure a profit or protect against loss.

RANGE OF INVESTMENT STRATEGIESReturn Potential

Potential Risk

Most Conservative

Moderate Growth

Most Aggressive

Domestic Stock International Stock Bonds Short-Term

TIMEFRAME“How much time do you have before you need to use your money?”

APPETITE FOR RISK“How comfortable are you with risk?”

FINANCIAL OUTLOOK“How does your current financial situation look?”

13

Business Cycle Serves as Key Lens for Investment Decisions in Active Asset AllocationUsing the business cycle approach during all phases to adjust asset allocations

For illustrative purposes only. Business cycle above is a hypothetical illustration of a typical business cycle. There is not always a chronological progression in this order, and there have been cycles when the economy has skipped a phase or retraced an earlier one. Past performance is no guarantee of future results.Source: Fidelity Investments (AART). Returns are geometric average annual nominal returns from 1950–2010. *This information represents Fidelity Investments' proprietary analysis of historical asset class performance, which is not indicative of future performance. [Asset class total returns are represented by indexes from the following sources: Fidelity Investments and Ibbotson Associates (U.S. Stocks), Barclays (High Quality Bonds and Short-Term), Bank of America Merrill Lynch (High Yield Bonds), UBS & Bloomberg (Commodities) as of 8/31/16.]Diversification and asset allocation do not ensure a profit or guarantee against loss.

Average Annual Return*

Cycle Phases

+Economic Growth

–

-10%0%

10%20%30%40%

Domestic Stocks High Quality Bonds High Yield Bonds Short-Term Commodities

RECOVERY EXPANSION CONTRACTION

14

Our Approach to U.S. Equity Portfolio ConstructionSeek to emphasize manager disciplines throughout business cycle

For illustrative purposes only.

All Weather

Deep Value

Valuation-focused

Aggressive Growth

Momentum

Smaller Cap Larger Cap

Defensive Equity

Opportunistic

Early CycleActivity rebounding

Mid CycleGrowth peaking

Late CycleGrowth moderating

RecessionActivity falling

High Quality

15

RebalancingSeveral rebalancing opportunities in last year

You cannot invest directly in an index. Past performance is no guarantee of future results. Bond performance – Bloomberg Barclays U.S. Aggregate Bond Index, Stock performance – Dow Jones U.S. Total Stock Market Index. PAS model trade activity represented by Legacy PAS Blended Growth with Income model portfolio (NMT). For illustrative purposes only. While these trades may appear at the model level, they may or may not have occurred in individual client accounts. Model portfolio activity shown represents rebalancing of 0.50% or greater in aggregate U.S. stock and/or bond fund exposure. See back for index definitions. Source: Fidelity Investments. Data as of 12/31/19.

PAS TOTAL RETURN BLENDED RETIREMENT MODEL REBALANCE ACTIVITY

-20-10

010203040506070

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Mar

-17

Jun-

17

Sep-

17

Dec

-17

Mar

-18

Jun-

18

Sep-

18

Dec

-18

Mar

-19

Jun-

19

Sep-

19

Dec

-19

Cum

ulat

ive

Ret

urns

(%)

Stock Performance Bond PerformanceBought Stocks Sold StocksBought Bonds Sold Bonds

16

Tax-Smart Investing:1 Keeping More of What You Earn

1 Strategic Advisers LLC applies tax-sensitive investment management techniques on a limited basis, at its discretion, primarily with respect to determining when assets in a client’s account should be bought and sold. As a discretionary investment management service, any assets contributed to an investor’s account that the portfolio does not elect to retain may be sold at any time after contribution. An investor may incur a gain or loss when assets are sold.

2 Seek to avoid realized short term gains in favor of long term gains as appropriate.3 Seek to manage exposure to mutual fund distributions.Tax-smart investing may not provide as high a return before consideration of federal income tax consequences as other funds. Tax-sensitive investing an result in realized capital gains.

KEY STRATEGIES SEEK TO ENHANCE AFTER-TAX RETURNS1

Transition management

Capital gains management2

Tax loss harvesting

123

Distribution management34National and state-specific municipal bonds5

17

Separately Managed AccountsWhat are they and what are the potential benefits?

What is an SMA?• Portfolio of individual security investments

managed by professional asset managers• Generally focused on:

– Single asset class (e.g., U.S. large cap stocks)– Investment objective (e.g., dividend income)

• Designed for investors with a preference for non-pooled vehicles

What are the potential benefits of an SMA?• Direct ownership of individual securities;

investors have their own tax lots • Transparency of positions and activity• Potential for tax management• More concentrated in higher conviction names• Ability to customize portfolio• Fund with existing securities

1818

What We’re Watching For in 2020

19

Change in the Pace of Economic GrowthU.S. and China are key focus

Note: The diagram above is a hypothetical illustration of the business cycle. There is not always a chronological, linear progression among the phases of the business cycle, and there have been cycles when the economy has skipped a phase or retraced an earlier one. * A growth recession is a significant decline in activity relative to a country’s long-term economic potential. We use the “growth cycle” definition for most developing economies, such as China, because they tend to exhibit strong trend performance driven by rapid factor accumulation and increases in productivity, and the deviation from the trend tends to matter most for asset returns. We use the classic definition of recession, involving an outright contraction in economic activity, for developed economies. Source: Fidelity Investments (AART), as of 12/31/19. Refer to additional information on page 31.

BUSINESS CYCLE FRAMEWORK

U.S., Japan, South Korea

China*

Brazil, Australia, CanadaSpain

UK

Mexico, India

France

Germany, Italy

20

U.S. Economy in Late-Cycle ExpansionMost signals pointing to modest but positive growth

Source: Fidelity Investments (AART), Strategic Advisers, as of 12/31/19.

INDICATOR CURRENT TREND LATEST READINGS

Employment/Wages Labor markets tighter, wages higher than 2–3 years ago Pace of improvement has slowed

Monetary Policy Fed policy looser than one year ago Fed staying put, but ready to ease if needed

Yield Curve Flat Stable

Credit Some tightening of lending standards Credit accessible, spreads tight

Corporate Profits Margins lower than 3 years ago Mid-single-digit earnings growth expectations

21

Catalysts That May Change Our Place in the CycleSluggish late-cycle environment remains base case

Source: Strategic Advisers, as of 12/31/19.

Potential Positives • Removal of tariffs• China looks beyond stabilization and reflates• Europe becomes more fiscally proactive• Less regulation for banks

Potential Risks• Additional tariffs• Private equity investments overextended• Real estate issues (commercial, China, etc.)• High levels of corporate borrowing

22

U.S.-China: Strategic Competition Intertwined with TradeNear-term deal is possible, but likely not a panacea

RIGHT: Shaded areas are announced changes as of 9/30/19. Source: Peterson Institute for International Economics, Fidelity Investments (AART) as of 9/30/19.

U.S.-CHINA RELATIONSHIP

Geopolitical Rivalry

Trade

Tariffs/Market Access

Industrial Policy Issues• IP protection• Export controls• Investment restrictions

Strategic Competition

Military Hegemony

in Asia

IT Sector/ Advanced Industrials

Consumer and Other

Goods

AVERAGE TARIFF RATES

0%

5%

10%

15%

20%

25%

30%

2017 2018 Sep-19 Oct-19 Dec-19

U.S. Tariffs on Chinese GoodsChina Tariffs on U.S. Goods

23

Over Time, Stocks Generally Follow EarningsIn short term, stock prices can disconnect from earnings trend

Source: Bloomberg Finance L.P. as of 9/30/19. Past performance is no guarantee of future results.

S&P 500 INDEX VS. OPERATING EARNINGS (LOG SCALE)

$2

$4

$8

$16

$32

$64

$128

$256

20

40

80

160

320

640

1280

2560

1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014 2019

S&P 500 Index S&P 500 Operating Earnings

S&P

500

Inde

xS&P 500 O

perating Earnings

24

Benign Credit Conditions Could Open Door for Slow-Moving Late Cycle

Source: Federal Reserve, Fidelity Investments (AART), as of 6/30/19.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Jan-

1980

Jan-

1982

Jan-

1984

Jan-

1986

Jan-

1988

Jan-

1990

Jan-

1992

Jan-

1994

Jan-

1996

Jan-

1998

Jan-

2000

Jan-

2002

Jan-

2004

Jan-

2006

Jan-

2008

Jan-

2010

Jan-

2012

Jan-

2014

Jan-

2016

Jan-

2018

INTEREST BURDEN, % OF AFTER-TAX PROFITS

U.S. Recession Corporate Interest Burden

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

100.0

Jan-

1991

Jul-1

992

Jan-

1994

Jul-1

995

Jan-

1997

Jul-1

998

Jan-

2000

Jul-2

001

Jan-

2003

Jul-2

004

Jan-

2006

Jul-2

007

Jan-

2009

Jul-2

010

Jan-

2012

Jul-2

013

Jan-

2015

Jul-2

016

Jan-

2018

SENIOR LOAN OFFICER SURVEY (NET % TIGHTENING C&I LENDING STANDARDS)

U.S. RecessionLarge companiesSmall companies

25

Elections: It’s Early, and Economy Matters MoreFocus on policy, not politics

Makeup of Congress matters, but for fodder…Reversal of corporate tax rate• Full reversal ~7% to S&P 500 EPSVarious sectors could be impacted• Financials, technology, health care, energyHigher personal tax rates• Increases the need for tax-smart investment

management

It’s still early……and about 70% of the delegates for the Democratic party get counted in March.LEADERS 385 DAYS BEFORE THE ELECTION

Election and Party Poll Leader Led for another…

2008 Democrats Clinton (+26.6) 119 days

2008 GOP Giuliani (+9.5) 82 days

2012 GOP Cain (+0.5) 25 days

2016 Democrats Clinton (+22.1) Rest of primary

2016 GOP Trump (+5.9) Rest of primary

Source: RealClearPolitics and Cowen and Company

2626

Questions

27

28

Important InformationThe Bloomberg Barclays US Treasury Index is an index which covers public obligations of the US Treasury with a remaining maturity of one year or more. The Bloomberg Barclays US Aggregate Bond Index is an unmanaged market value weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed, and mortgage-backed securities with maturities of at least one year. The Bloomberg Barclays US Credit Bond Index—Publicly issued US corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered. The Bloomberg Barclays US Agency Index—Publicly issued debt of U.S. Government agencies, quasi-federal corporations, and corporate or foreign debt guaranteed by the U.S. Government.The Bloomberg Barclays Investment Grade CMBS Index is an index designed to mirror commercial mortgage back securities of investment grade quality (Baa3/BBB-/BBB- or above) using Moody’s, S&P, and Fitch respectively, with maturity of at least one year. The Bloomberg Barclays MBS Index covers agency mortgage-backed pass-through securities (both fixed-rate and hybrid ARMs) issued by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). The Bloomberg Barclays U.S. Municipal Bond Index covers the USD-denominated long term tax exempt bond market with four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and pre-refunded bonds. The Bloomberg Barclays U.S. TIPS Index represents an unmanaged market index made up of U.S. Treasury Inflation Linked Index securities. The Bank of America Merrill Lynch High-Yield Bond Master II Index is an unmanaged index that tracks the performance of below investment grade U.S. dollar-denominated corporate bonds publicly issued in the U.S. domestic market.The Bloomberg Barclays U.S. 3-Month Treasury Bellwether Index is unmanaged market value-weighted index of investment-grade fixed-rate public obligations of the U.S. Treasury with Maturities of 3 months. It includes zero-coupon strips.The National Association of Real Estate Investment Trusts (NAREIT) Equity Index is a market-value-weighted index based upon the last closing price of the month for tax-qualified REITs listed on the NYSEThe S&P/LSTA Leveraged Performing Loan Index Standard & Poor's/Loan Syndications and Trading Association Leveraged Performing Loan Index is a market value-weighted index designed to represent the performance of U.S. dollar-denominated institutional leveraged performing loan portfolios (excluding loans in payment default) using current market weightings, spreads and interest payments.J.P. Morgan Emerging Markets Bond Index (EMBI) Global is a market value–weighted index of U.S. dollar–denominated Brady bonds, Eurobonds, traded loans, and local market debt instruments issued by emerging markets’ sovereign and quasi-sovereign entities. JPMorgan GBI Global Ex-U.S. Index (US $UnHedged) is an unmanaged market index representative of the total return performance in U.S. dollars on an unhedged basis of non-U.S. bond markets.Merrill Lynch U.S. High Yield Master II Constrained Index is a market value–weighted index of all domestic and Yankee high–yield bonds, including deferred interest bonds and payment–in–kind securities. Issues included in the index have maturities of one year or more and have a credit rating lower than BBB-/Baa3, but are not in default. The Merrill Lynch U.S. High Yield Master II Constrained Index limits any individual issuer to a maximum of 2% benchmark exposure. The Ibbotson US Long-Term Corporate Bond Index is a custom index designed to measure the performance of long-term U.S. corporate bonds.

29

Important InformationThe Ibbotson US Intermediate-Term Government Bond Index is a custom index designed to measure the performance of intermediate-term US government bonds.The Ibbotson US 30-day Treasury Bill Index is a custom index designed to measure the performance of 30-day U.S. Treasury bills.Slide 8: Taxes Can Significantly Reduce Returns data, Morningstar, Inc., 2/25/2019.This image illustrates how much the federal government withheld from one hypothetical investor who follows a simple long-term investment strategy. Stocks after taxes assumes that the stocks purchased were held for five years, then sold, and the capital gains realized. The net proceeds from the sale were reinvested. Dividends were taxed when earned and reinvested. From 1926 to 2018, the average return on stocks after taxes was 8.0%, compared with 10.0% before taxes. Bonds were turned over 28 times within the 93-year period. Capital gains were realized at the time of sale and reinvested. Bonds averaged a 3.4% return after taxes, compared with 5.5% before taxes. After taxes, on average, bonds barely outpaced the inflation rate. Government bonds and Treasury bills are guaranteed by the full faith and credit of the U.S. government as to the timely payment of principal and interest, while stocks are not guaranteed and have been more volatile than the other asset classes.Federal income tax is calculated using the historical marginal and capital gains tax rates for a single taxpayer earning $120,000 in 2015 dollars every year. This annual income is adjusted using the Consumer Price Index in order to obtain the corresponding income level for each year. Income is taxed at the appropriate federal income tax rate as it occurs. When realized, capital gains are calculated assuming the appropriate capital gains rates. The holding period for capital gains tax calculation is assumed to be five years for stocks, while government bonds are held until replaced in the index. No state income taxes are included. Stocks are represented by the Ibbotson Large Company Stock Index. Government bonds are represented by the 20-year U.S. government bond. An investment cannot be made directly in an index. The data assumes reinvestment of income and does not account for transaction costs. The MSCI® EAFE® Index (Morgan Stanley Capital International Europe, Australasia, Far East Index) is an unmanaged market capitalization-weighted index designed to represent the performance of developed stock markets outside the United States and Canada. MSCI EAFE (N) index is net of Massachusetts taxes.MSCI Emerging Markets (MSCI EM) Index is a market capitalization–weighted index of equity securities of companies domiciled in various countries. The Index is designed to represent the performance of emerging stock markets throughout the world and excludes certain market segments unavailable to U.S.-based investors.MSCI EAFE (Europe, Australasia, Far East) Small Cap Index is a market capitalization-weighted index that is designed to measure the investable equity market performance of small cap stocks for global investors in developed markets, excluding the U.S. & Canada.MSCI Europe Index is a market capitalization weighted index of over 550 stocks traded in 14 European markets.S&P GSCI Commodities Index is a world-production weighted index composed of 24 widely traded commodities. All sub-indices of the S&P GSCI™ sub-indices (Energy, Industrial Metals, Precious Metals, and Agriculture and Livestock) follow the same rules regarding world production weights, methodologyMSCI Japan Index is an unmanaged index of over 317 foreign stock prices, and reflects the common stock prices of the index companies translated into U.S. dollars, assuming reinvestment of all dividends paid by the index stocks net of any applicable foreign taxes. MSCI World Index is a market capitalization weighted index that is designed to measure the investable equity market performance for global investors of developed markets. MSCI World ex USA Index is a market capitalization-weighted index designed to measure the equity market performance of developed markets excluding the U.S. The S&P 500® Index is a registered service mark of The McGraw-Hill Companies, Inc. and has been licensed for use by Fidelity Distributors Company LLC. It is an unmanaged index of the common stock prices of 500 widely held U.S. stocks that includes the reinvestment of dividends.

30

Important InformationMSCI Europe Index is a market capitalization weighted index that is designed to measure the investable equity market performance for global investors of the developed markets in Europe. Russell 2000 Index is a market capitalization–weighted index of the stocks of the 2,000 smallest companies included in the 3,000 largest U.S. domiciled companies. Russell 3000 Growth Index is a market capitalization–weighted index of those stocks of the 3,000 largest U.S. domiciled companies that exhibit ex growth–oriented characteristics. Russell 3000 Value Index is a market capitalization–weighted index of those stocks of the 3,000 largest U.S. domiciled companies that exhibit value–oriented characteristics.Consumer Price Index is a widely recognized measure of inflation calculated by the US Government.Organization for Economic Co-operation and Development (OECD) Composite Leading Indicator (CLI) is designed to provide early signals of turning points in business cycles - fluctuation in the output gap, i.e. fluctuation of the economic activity around its long term potential level – for the 34 member countries of the OECD. This approach, focusing on turning points (peaks and troughs), results in CLIs that provide qualitative rather than quantitative information on short-term economic movements.This presentation is provided for informational use only and should not be considered investment advice or an offer for a particular security. Views and opinions expressed are as of December 31, 2019 and may change based on market and other conditions.Investment decisions should be based on an individual’s own goals, time horizon, and tolerance for risk.Diversification does not ensure a profit or guarantee against loss.All indices are unmanaged and performance of the indices include reinvestment of dividends and interest income, unless otherwise noted, are not illustrative of any particular investment and an investment cannot be made in any index.Index (CPI) is a monthly inflationary indicator that measures the change in the cost of a fixed basket of products and services, excluding food and energy prices.A Purchasing Managers’ Index (PMI) is a survey of purchasing managers in a certain economic sector. A PMI over 50 represents expansion of the sector compared to the previous month, while a reading under 50 represents a contraction, and a reading of 50 indicates no change. The Institute for Supply Management (ISM) reports U.S. PMIs. Market compiles non-U.S. PMIs.Information provided herein is for educational purposes only and should not be construed or relied upon by you as advice or guidance as to the appropriateness of any investment decision.Generally, among asset classes stocks are more volatile than bonds or short-term instruments and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Although the bond market is also volatile, lower-quality debt securities including leveraged loans generally offer higher yields compared to investment grade securities, but also involve greater risk of default or price changes. Foreign markets can be more volatile than U.S. markets due to increased risks of adverse issuer, political, market or economic developments, all of which are magnified in emerging markets.Past performance does not guarantee future results.

31

Important InformationThe tax information contained herein is general in nature, is provided for informational purposes only, and should not be construed as legal or tax advice. Fidelity does not provide legal or tax advice. Fidelity cannot guarantee that such information is accurate, complete, or timely. Laws of a particular state or laws which may be applicable to a particular situation may have an impact on the applicability, accuracy, or completeness of such information. Federal and state laws and regulations are complex and are subject to change. Changes in such laws and regulations may have a material impact on pre- and/or after-tax investment results. Fidelity makes no warranties with regard to such information or results obtained by its use. Fidelity disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information. Always consult an attorney or tax professional regarding your specific legal or tax situation.Slide 19: Current Position of the U.S. in Business Cycle' depicts the general pattern of economic cycles throughout history, though each cycle is different and specific commentary on the current stage is provided in the summary and outlook section above. In general, the typical business cycle demonstrates the following: During the typical early-cycle phase, the economy bottoms and picks up steam until it exits recession, then begins the recovery as activity accelerates. Inflationary pressures are typically low, monetary policy is accommodative, and the yield curve is steep. Economically sensitive asset classes such as stocks tend to experience their best performance during the cycle. During the typical mid-cycle phase, the economy exits recovery and enters into expansion, characterized by broader and more self-sustaining economic momentum but a more moderate pace of growth. Inflationary pressures typically begin to rise, monetary policy becomes tighter, and the yield curve experiences some flattening. Economically sensitive asset classes tend to continue benefitting from a growing economy, but their relative advantage narrows. During the typical late-cycle phase, the economic expansion matures, inflationary pressures continue to rise, and the yield curve may eventually become flat or inverted. Eventually, the economy contracts and enters recession, with monetary policy shifting from tightening to easing. Less economically sensitive asset categories tend to hold up better, particularly right before and upon entering recession. Please note there is no uniformity of time among phases, nor is there always a chronological progression in this order. For example, business cycles have varied between two and 10 years in the U.S., and there have been examples when the economy has skipped a phase or retraced an earlier one.The Chartered Financial Analyst (CFA) designation is offered by the CFA Institute. To obtain the CFA charter, candidates must pass three exams demonstrating their competence, integrity, and extensive knowledge in accounting, ethical and professional standards, economics, portfolio management, and security analysis, and must also have at least four years of qualifying work experience, among other requirements. CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.Fidelity® Wealth Services provides non-discretionary financial planning and discretionary investment management through one or more Portfolio Advisory Services accounts for a fee. Advisory services offered by Fidelity Personal and Workplace Advisors LLC (FPWA), a registered investment adviser, and Fidelity Personal Trust Company, FSB (FPTC), a federal savings bank. Nondeposit investment products and trust services offered through FPTC and its affiliates are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency, are not obligations of any bank, and are subject to risk, including possible loss of principal. Discretionary portfolio management services provided by Strategic Advisers LLC (Strategic Advisers), a registered investment adviser. Brokerage services provided by Fidelity Brokerage Services LLC (FBS), and custodial and related services provided by National Financial Services LLC (NFS), each a member NYSE and SIPC. FPWA, Strategic Advisers, FPTC, FBS, and NFS are Fidelity Investments companies.Fidelity Brokerage Services LLC, Member NYSE and SIPC, 900 Salem Street, Smithfield, RI 02917© 2019 FMR LLC. All rights reserved.911388.1.0