infrastructure analysis tools: a focus on cash flow ... main models supporting cash flow analysis...

TRANSCRIPT

NREL is a national laboratory of the U.S. Department of Energy, Office of Energy Efficiency and Renewable Energy, operated by the Alliance for Sustainable Energy, LLC.

Infrastructure Analysis Tools: A Focus on Cash Flow Analysis

Marc Melaina, Michael PenevNational Renewable Energy Laboratory

Presented at the Hydrogen Infrastructure MeetingInternational Council for Clean Transportation (ICCT) Breakthrough Technologies Institute (BTI)Toronto, 5 June 2012

NREL/PR‐5600‐55563

This presentation does not contain any proprietary, confidential, or otherwise restricted information

2

Introduction: Cash flow and related models

Inputs needed to analyze a business case for hydrogen infrastructure:

1. Infrastructure costs2. Realistic market growth scenarios3. Return on investment expectations4. Policy support options

• NREL has been developing multiple analysis tools to address each of these topics for the U.S. Department of Energy for more than 10 years

• Business case analysis is the most recent addition to this tool set, which started with stationary fuel cells

• Major analysis topics are vehicle‐infrastructure interactions and the integration of renewable hydrogen

3

Main models supporting cash flow analysis

Hydrogen Analysis (H2A) models • Production, Delivery, and Fuel Cells• Discounted cash flow framework • Models are transparent and public

http://www.hydrogen.energy.gov/h2a_analysis.html

Scenario Evaluation and Regionalization Analysis (SERA) Model• Optimizes spatial‐temporal infrastructure in response to hydrogen demand

• Runs have optimized on least cost $/kg• H2A cost models “plug in” to SERA• Optimization across all pathway options• Developed over ~7 years• Sub‐models explore finance options

Fuel cell vehicle market projections (ADOPT, MA3T, other models)• Based upon consumer preferences and vehicle attributes• Market share models haven’t been integral to SERA runs

4

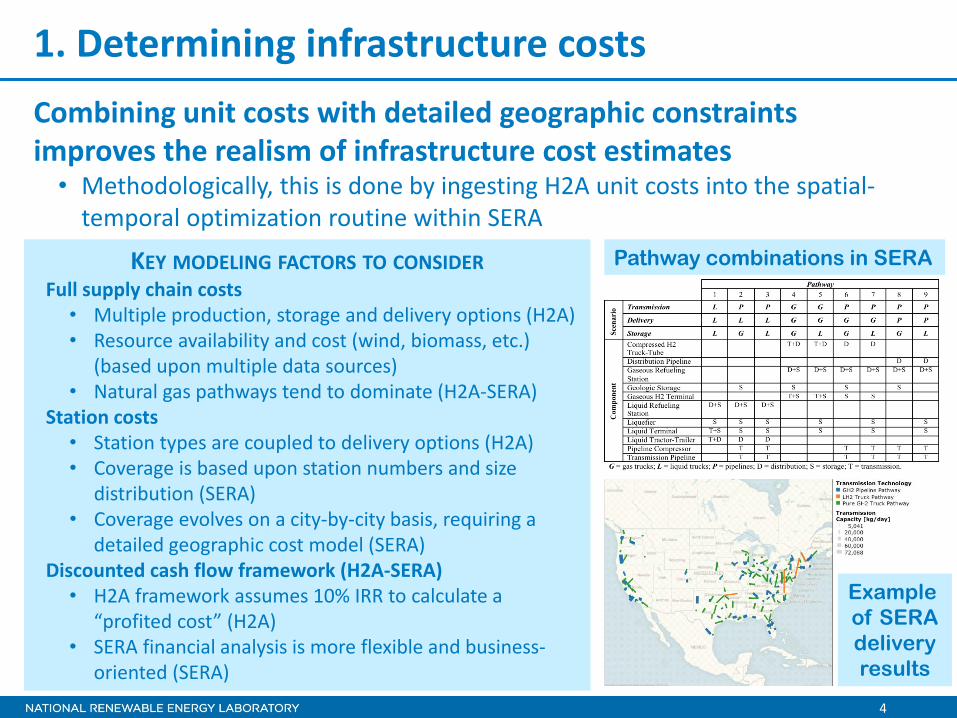

1. Determining infrastructure costs Combining unit costs with detailed geographic constraints improves the realism of infrastructure cost estimates• Methodologically, this is done by ingesting H2A unit costs into the spatial‐temporal optimization routine within SERA

KEY MODELING FACTORS TO CONSIDERFull supply chain costs • Multiple production, storage and delivery options (H2A)• Resource availability and cost (wind, biomass, etc.)

(based upon multiple data sources)• Natural gas pathways tend to dominate (H2A‐SERA)

Station costs • Station types are coupled to delivery options (H2A)• Coverage is based upon station numbers and size

distribution (SERA)• Coverage evolves on a city‐by‐city basis, requiring a

detailed geographic cost model (SERA)Discounted cash flow framework (H2A‐SERA)• H2A framework assumes 10% IRR to calculate a

“profited cost” (H2A)• SERA financial analysis is more flexible and business‐

oriented (SERA)

Pathway combinations in SERA

Example of SERAdeliveryresults

5

2. Realistic market growth scenarios• Steady‐state infrastructure costs are relatively simple to analyze; rollout dynamics are much more complex

• For early market growth dynamics and interactions, NREL analysts have incorporated guidance from: • Stakeholder workshops (Greene et al. 2008)• Early market coordination activities such as the Hawaii Hydrogen Initiative (H2I), EIN, and CaFCP

• Initial discussions with CCAT• Station rollout is explicit at any level of detail• SERA offers a consistent framework to incorporate regional infrastructure rollout scenarios

Bay Area,

CA

Chicago, IL

Station sizes

New FCEV sales Annual cash flow @ $8/kg

6

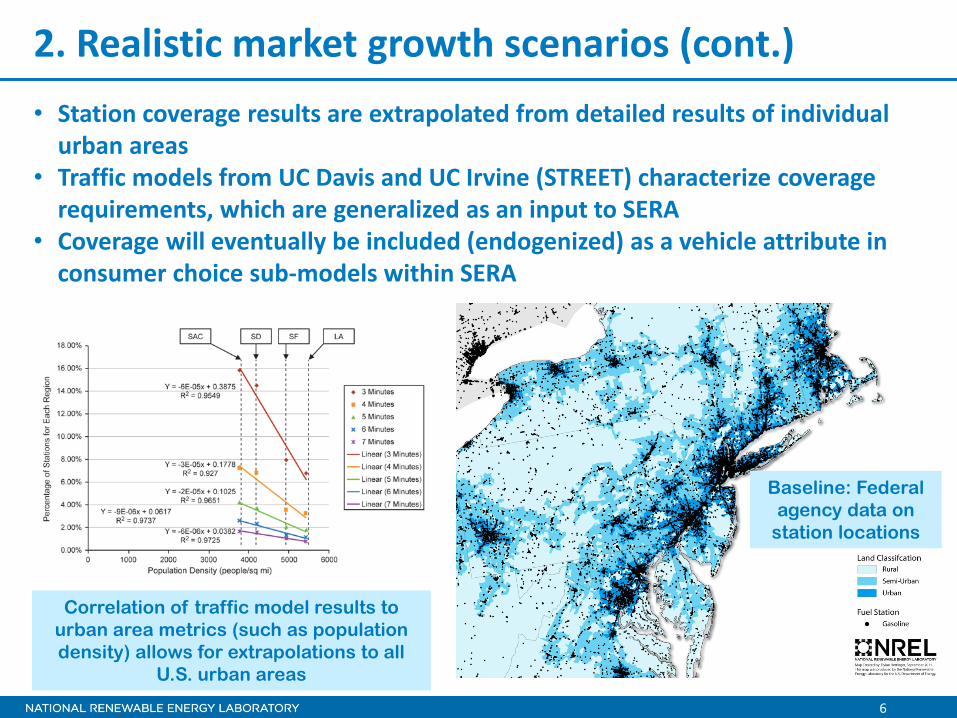

2. Realistic market growth scenarios (cont.)• Station coverage results are extrapolated from detailed results of individual urban areas

• Traffic models from UC Davis and UC Irvine (STREET) characterize coverage requirements, which are generalized as an input to SERA

• Coverage will eventually be included (endogenized) as a vehicle attribute in consumer choice sub‐models within SERA

Baseline: Federal agency data on

station locations

Correlation of traffic model results to urban area metrics (such as population density) allows for extrapolations to all

U.S. urban areas

7

Basic national cash flow results from SERA• Break‐even year is a function of assumed market price ($/kg)• Cash flows determined nationally, by state, by city, or per station

Zero cumulative cash flow is achieved between 2018 and 2025 if hydrogen is priced at

$11.00/kg or $6.75/kg

8

More elaborate and detailed cash flows

• Developed in response to partner/stakeholder requirements in H2I and discussions with EIN/CaFCP

• Hydrogen price assumed to be equal to gasoline price on a per‐mile‐driven basis (need mpg assumptions to determine)

• Short‐fall results from high fixed costs and underutilization of infrastructure in early years

$‐

$1

$2

$3

$4

$5

Millions

Financing

Maintenance

Labor

Utilities

Feedstock

Revenue

Mon

thly Cash Flow

s

Analysis Period

Expenses & Revenue Projections vs. Year

$‐

$1

$2

$3

$4

$5

Millions

Financing

Maintenance

Labor

Utilities

Feedstock

Revenue

Mon

thly Cash Flow

s

Analysis Period

Expenses & Revenue Projections vs. Year

Revenue short‐fall (barrier to market entry)

9

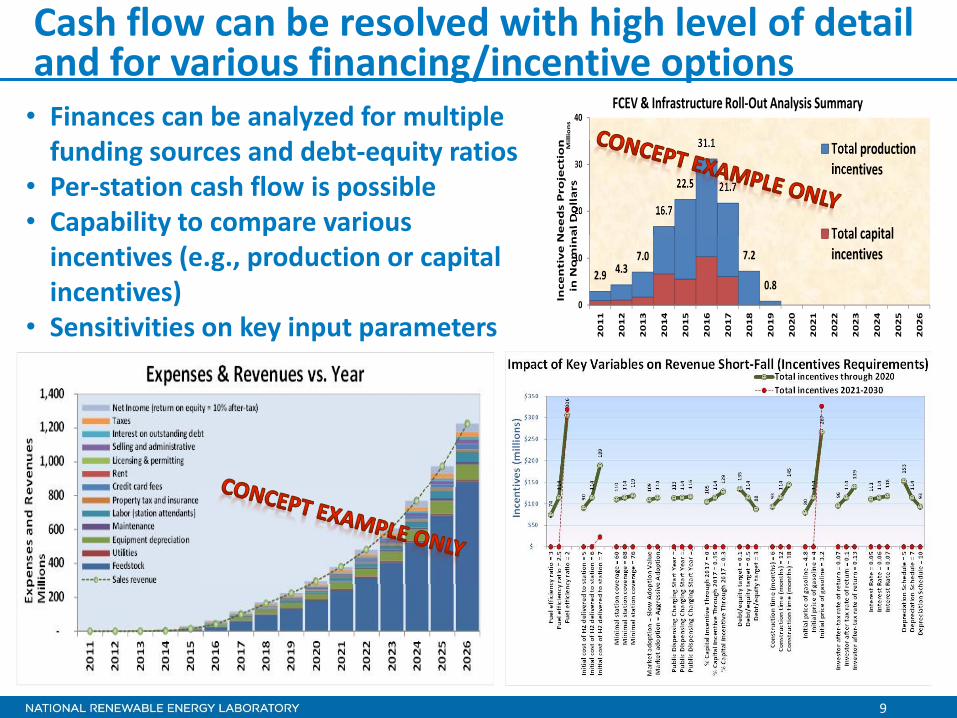

Cash flow can be resolved with high level of detail and for various financing/incentive options

2.9 4.37.0

16.7

22.5

31.1

21.7

7.2

0.80

10

20

30

40

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

Millions

Total productionincentives

Total capitalincentives

IncentiveNeeds Projection

in Nominal Dollars

FCEV & Infrastructure Roll‐Out Analysis Summary• Finances can be analyzed for multiple funding sources and debt‐equity ratios

• Per‐station cash flow is possible• Capability to compare various incentives (e.g., production or capital incentives)

• Sensitivities on key input parameters

10

SummaryNREL models• NREL has developed and maintains a variety of infrastructure analysis models for the U.S. Department of Energy

• Business case analysis has recently been added to this tool set

Cash flow analysis• Cash flows depend upon infrastructure costs, optimized spatially and temporally, and assumptions about financing and revenue

• Detailed metrics have been incorporated on financing/incentives

Next steps in modeling• Continue to collect feedback on regional/local infrastructure development activities and “roadmap” dynamics

• Incorporate consumer preference assumptions on infrastructure to provide direct feedback between vehicles and station rollout

12

Additional Slides

13

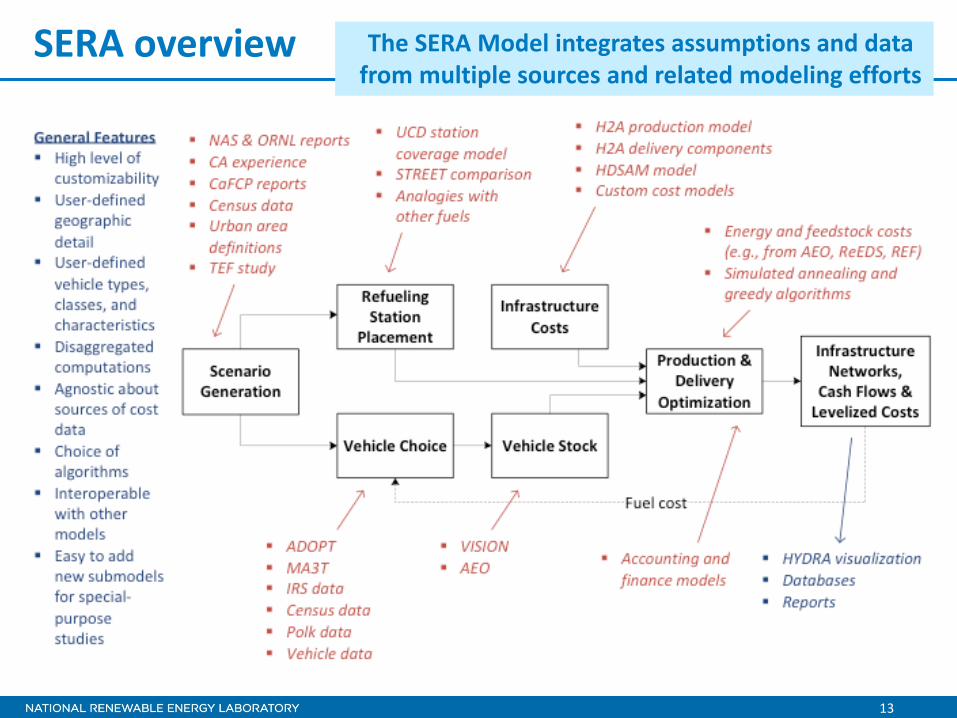

SERA overview The SERA Model integrates assumptions and data from multiple sources and related modeling efforts

14

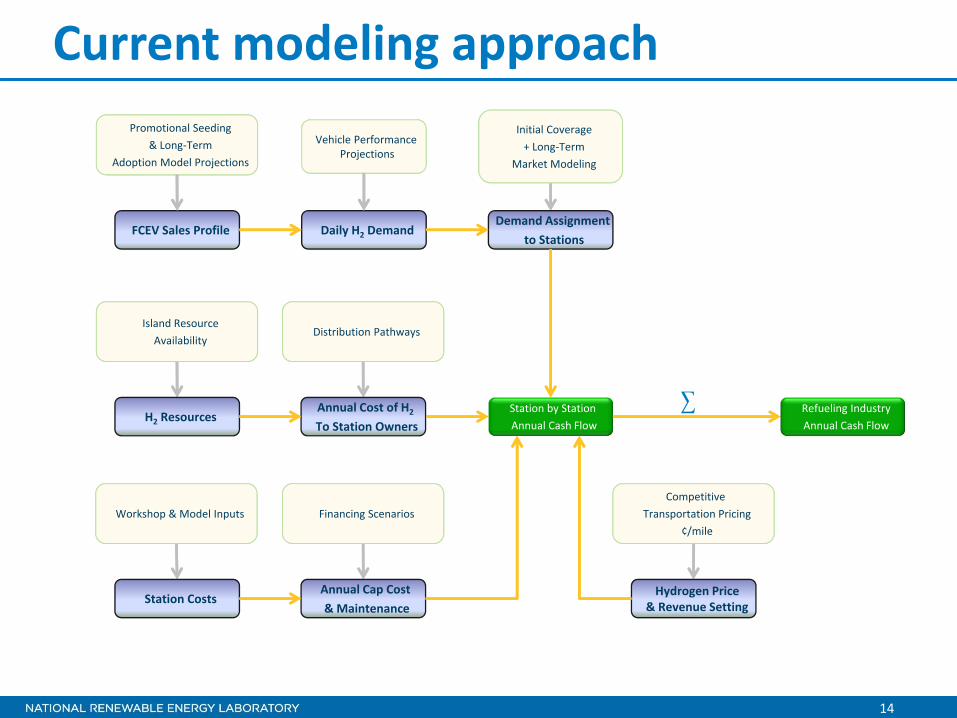

Current modeling approach

FCEV Sales Profile Daily H2 Demand

Vehicle Performance Projections

Demand Assignment to Stations

Promotional Seeding& Long‐Term

Adoption Model Projections

Initial Coverage+ Long‐Term

Market Modeling

Station by Station Annual Cash Flow

H2 Resources

Island ResourceAvailability

Annual Cost of H2

To Station Owners

Distribution Pathways

Station Costs

Workshop & Model Inputs

Annual Cap Cost & Maintenance

Financing Scenarios

Refueling IndustryAnnual Cash Flow

∑

Hydrogen Price& Revenue Setting

Competitive Transportation Pricing

¢/mile

15

On‐going effort

FCEV Sales Profile Daily H2 Demand

Vehicle Performance Projections

Demand Assignment to Stations

Promotional Seeding& Long‐Term

Adoption Model Projections

Initial Coverage+ Long‐Term

Market Modeling

Station by Station Annual Cash Flow

H2 Resources

Island ResourceAvailability

Annual Cost of H2

To Station Owners

Distribution Pathways

Station Costs

Workshop & Model Inputs

Annual Cap Cost & Maintenance

Financing Scenarios

Refueling IndustryAnnual Cash Flow

∑

Hydrogen Price& Revenue Setting

Competitive Transportation Pricing

¢/mile

Introduce sales projectionsbased on:• Station coverage• Fueling costs• Vehicle prices• Vehicle size• Vehicle acceleration

16

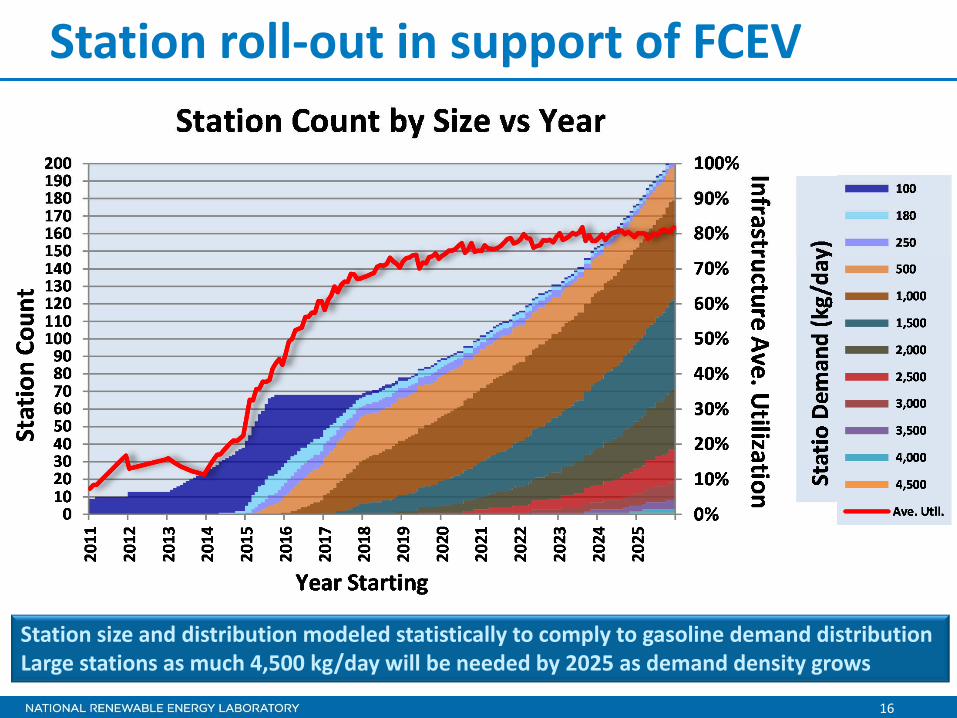

Station roll‐out in support of FCEV

Station size and distribution modeled statistically to comply to gasoline demand distributionLarge stations as much 4,500 kg/day will be needed by 2025 as demand density grows

17

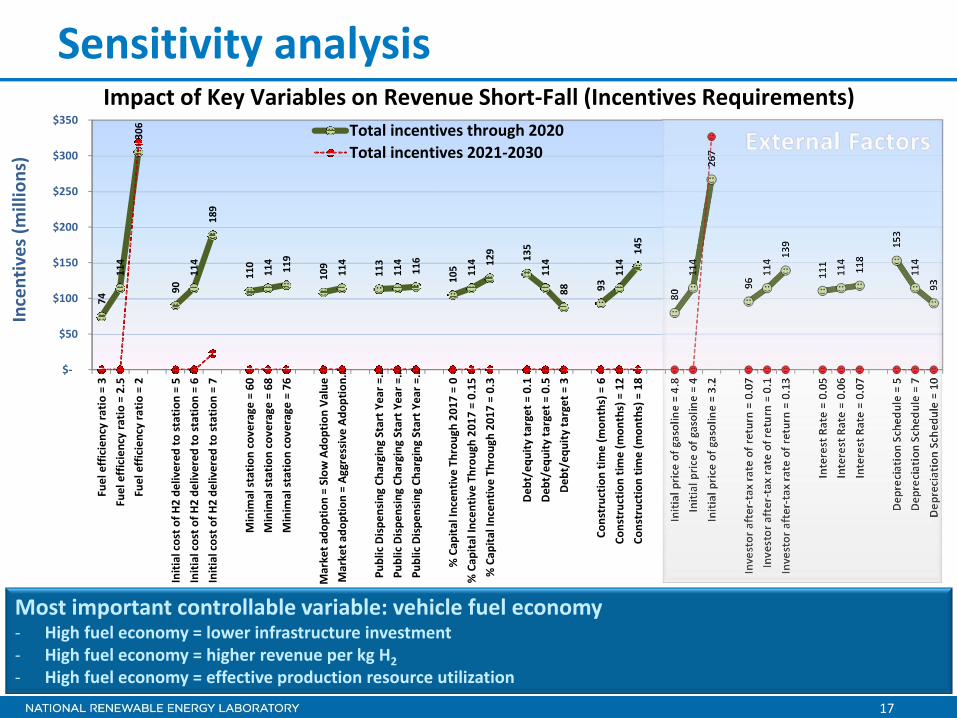

Sensitivity analysis74

114

306

90

114

189

110

114

119

109

114

113

114

116

105 114 129 135

114

88 93

114

145

80

114

267

96

114 13

9

111

114

118

153

114

93

$‐

$50

$100

$150

$200

$250

$300

$350Fuel efficiency ratio

= 3

Fuel efficiency ratio

= 2.5

Fuel efficiency ratio

= 2

Initial cost o

f H2 de

livered

to statio

n = 5

Initial cost o

f H2 de

livered

to statio

n = 6

Initial cost o

f H2 de

livered

to statio

n = 7

Minim

al statio

n coverage

= 60

Minim

al statio

n coverage

= 68

Minim

al statio

n coverage

= 76

Market a

doption = Slow

Ado

ption Va

lue

Market a

doption = Ag

gressive Ado

ption…

Public Dispe

nsing Ch

arging

Start Year =

…Pu

blic Dispe

nsing Ch

arging

Start Year =

…Pu

blic Dispe

nsing Ch

arging

Start Year =

…

% Cap

ital Incen

tive Th

roug

h 20

17 = 0

% Cap

ital Incen

tive Th

rough 20

17 = 0.15

% Cap

ital Incen

tive Th

roug

h 20

17 = 0.3

Deb

t/eq

uity ta

rget = 0.1

Deb

t/eq

uity ta

rget = 0.5

Deb

t/eq

uity ta

rget = 3

Constructio

n tim

e (m

onths) = 6

Constructio

n tim

e (m

onths) = 12

Constructio

n tim

e (m

onths) = 18

Initial pric

e of gasoline = 4.8

Initial pric

e of gasoline = 4

Initial pric

e of gasoline = 3.2

Investor after‐tax ra

te of return = 0.07

Investor after‐tax ra

te of return = 0.1

Investor after‐tax ra

te of return = 0.13

Interest Rate = 0.05

Interest Rate = 0.06

Interest Rate = 0.07

Dep

reciation Sche

dule = 5

Dep

reciation Sche

dule = 7

Dep

reciation Sche

dule = 10

Total incentives through 2020Total incentives 2021‐2030

Incentives

(millions)

Impact of Key Variables on Revenue Short‐Fall (Incentives Requirements)

Most important controllable variable: vehicle fuel economy‐ High fuel economy = lower infrastructure investment‐ High fuel economy = higher revenue per kg H2‐ High fuel economy = effective production resource utilization

18

0

1000000

2000000

3000000

4000000

15 20 25 30 40 50

Annu

al Sales

Fuel Economy (MPG)

Sales By MPG(listed by max in bin)

Actual

Model

0.0%

5.0%

10.0%

15.0%

20.0%

Actual Model

Percent HEV Sales

ADOPT matches historical sales

0

1000000

2000000

3000000

4000000

5000000

12 9 7

Annu

al Sales

Max Bin Accel Time (secs 0‐60 MPH)

Sales By Acceleration

Actual

Model0

1000000200000030000004000000

Annu

al Sales

Vehicle Price (MSRP)

Sales By MSRP (listed by max in bin)

Actual

Model0

5000001000000150000020000002500000

Annu

al Sales

Sales By Class

Actual

Model

0%

20%

40%

60%

80%

100%

National Model

HEV Buyers with Income Over $100k

$‐

$50,000

$100,000

$150,000

National Model

Average Income of HEV Buyers

• ADOPT has been calibrated for U.S. markets• Model predicts historical sales with a relatively high degree of accuracy• Range of FCEV sizes and performances will be modeled to provide wide variety of market choices

19

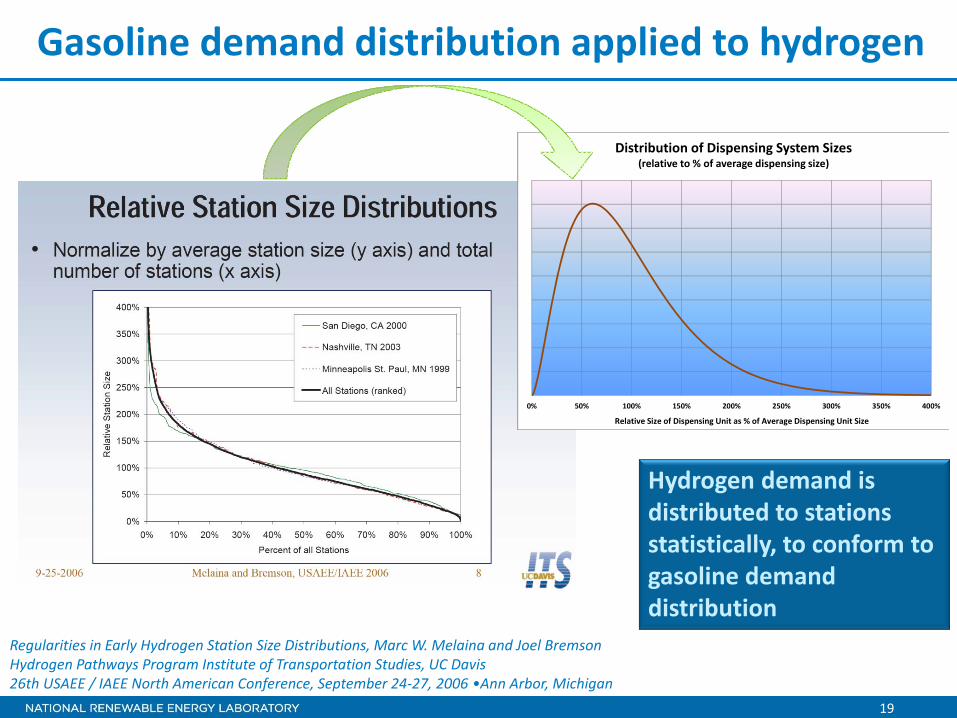

Gasoline demand distribution applied to hydrogen

Regularities in Early Hydrogen Station Size Distributions, Marc W. Melaina and Joel BremsonHydrogen Pathways Program Institute of Transportation Studies, UC Davis26th USAEE / IAEE North American Conference, September 24‐27, 2006 •Ann Arbor, Michigan

0% 50% 100% 150% 200% 250% 300% 350% 400%

Distribution of Dispensing System Sizes(relative to % of average dispensing size)

Relative Size of Dispensing Unit as % of Average Dispensing Unit Size

0% 50% 100% 150% 200% 250% 300% 350% 400%

Distribution of Dispensing System Sizes(relative to % of average dispensing size)

Relative Size of Dispensing Unit as % of Average Dispensing Unit Size

Hydrogen demand is distributed to stations statistically, to conform to gasoline demand distribution