inflation targeting and financial stability

TRANSCRIPT

Inflation Targeting and

Financial Stability

Benjamin Tabak, Dimas Fazio, and Daniel Cajueiro

Introduction and MotivationWhat?

This paper answers three questions:

Q1 Are banks from countries that adopt Inflation Targeting (IT)more stable?

Q2 Are these banks more stable during times of global illiquidity?

Q3 Do systemically important banks from IT countries take morerisk?

Recent criticism of IT: central bankers overlooked the bankingsystem and the development of asset bubbles.

Counter-arguments:

(a) IT regime comprises of more dimensions than just controllinginflation.

(b) United States of America, where the crisis originated, is notconsidered an IT country.

Introduction and MotivationHow?

We employ a database from BankScope containing 3964 com-mercial banks from 71 countries (22 of which are IT) duringthe period 1998-2012.

Richness of the data: results are not specific of any country andtime period.

First study to analyze IT’s impact on financial stability usingbank-level data.

Methodology: (Q1) regress a dummy that equals one if thecountry is IT on a bank stability variable.

We also interact this variable with (Q2) TED spread (a proxyof global financial distress) and (Q3) a SIFI dummy.

Introduction and MotivationLiterature

IT consists in four elements (Mishkin, 2004; Heenan et al.,2006):

(i) CB mandate to pursue price stability as a primary objective;

(ii) an explicit inflation target;

(iii) policy action based on a forward looking assessment of inflationpressures;

(iv) increased transparency of monetary policy strategy and imple-mentation.

Large evidence that IT has reduced inflationary pressures andanchored price expectations in countries that implement it.

The effects of IT on financial stability, however, are not thatclear.

Introduction and MotivationLiterature (Cont.)

On one side lower levels of inflation have positive effects onfinancial stability, ceteris paribus.

On the other hand, the recent financial crisis has made economistsrealize that price stability is not a sufficient condition forfinancial stability.

Central banks have overlooked financial imbalances and the de-velopment of asset bubbles in the pursuit of price stability.

“Paradox of credibility” (Borio et al. 2003).

Critics suggest authorities include a financial stability goal onthe IT framework.

Few empirical works, however, have been done to provide evi-dence to either view.

Data

We take balance-sheet data of 3964 commercial banks during1998-2012 from BankScope.

In order to avoid loosing several observations due to missingdata, we average relevant balance sheet data by trienniums.

If there is missing data for a specific bank and year, the obser-vation for that triennium is the average value of the remainingtwo years.

Data on countries that employ IT as well as the year of adoptionfrom Roger (2009) and authors’ own research.

The variable of global illiquidity is the TED spread (Eurodollar- Treasury Bill), calculated using US Federal Reserve Data.

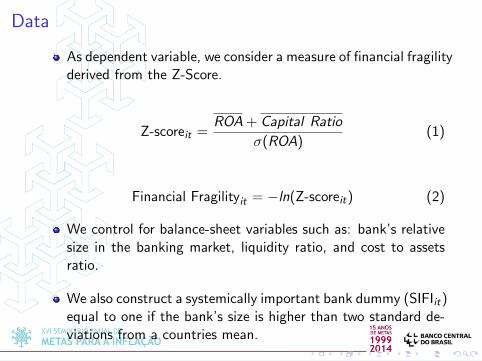

Data

As dependent variable, we consider a measure of financial fragilityderived from the Z-Score.

Z-scoreit =ROA + Capital Ratio

σ(ROA)(1)

Financial Fragilityit = −ln(Z-scoreit) (2)

We control for balance-sheet variables such as: bank’s relativesize in the banking market, liquidity ratio, and cost to assetsratio.

We also construct a systemically important bank dummy (SIFIit)equal to one if the bank’s size is higher than two standard de-viations from a countries mean.

Data

In addition to controlling for balance-sheet data, we also includetwo different types of controls:

Economic indicators:

Financial Freedom and Property Rights indices (Heritage Foun-dation); and

the GDP growth (World Bank’s WDI).

Financial Depth variables:

Density of deposits (BankScope and WDI);

The banking system’s equity to assets ratio (Bankscope);

The domestic credit to the private sector as % of the GDP(Bankscope); and

A banking market competition index known as the Lerner index(Bankscope and authors‘ estimation).

ResultsQ1: Are banks from IT countries more stable?

[1] [2] [3] [4]Variables Fin. Fragilityit Fin. Fragilityit Fin. Fragilityit Fin. Fragilityit

Inf. Targett -0.777*** -0.540*** -0.562*** -0.420***(0.077) (0.076) (0.078) (0.078)

Controls

Bank-Level Vars. Yes Yes Yes YesFinancial Depth No No Yes YesEconomic Activity No Yes No Yes

Observations 13,663 13,663 13,663 13,663R-squared 0.064 0.093 0.080 0.100Number of Banks 3,964 3,964 3,964 3,964

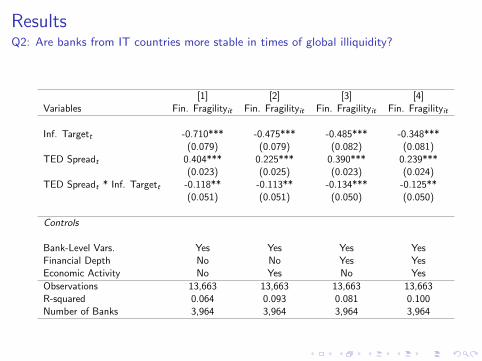

ResultsQ2: Are banks from IT countries more stable in times of global illiquidity?

[1] [2] [3] [4]Variables Fin. Fragilityit Fin. Fragilityit Fin. Fragilityit Fin. Fragilityit

Inf. Targett -0.710*** -0.475*** -0.485*** -0.348***(0.079) (0.079) (0.082) (0.081)

TED Spreadt 0.404*** 0.225*** 0.390*** 0.239***(0.023) (0.025) (0.023) (0.024)

TED Spreadt * Inf. Targett -0.118** -0.113** -0.134*** -0.125**(0.051) (0.051) (0.050) (0.050)

Controls

Bank-Level Vars. Yes Yes Yes YesFinancial Depth No No Yes YesEconomic Activity No Yes No Yes

Observations 13,663 13,663 13,663 13,663R-squared 0.064 0.093 0.081 0.100Number of Banks 3,964 3,964 3,964 3,964

ResultsQ3: Are systemically important banks from IT countries more stable?

[1] [2] [3] [4]Variables Fin. Fragilityit Fin. Fragilityit Fin. Fragilityit Fin. Fragilityit

Inf. Targett -0.767*** -0.524*** -0.558*** -0.409***(0.076) (0.076) (0.078) (0.078)

SIFIit 0.211*** 0.176** 0.179** 0.154*(0.082) (0.080) (0.081) (0.079)

SIFIit * Inf. Targett -0.501*** -0.509*** -0.481*** -0.485***(0.165) (0.152) (0.165) (0.155)

Controls

Bank-Level Vars. Yes Yes Yes YesFinancial Depth No No Yes YesEconomic Activity No Yes No Yes

Observations 13,663 13,663 13,663 13,663R-squared 0.064 0.093 0.080 0.100Number of Banks 3,964 3,964 3,964 3,964

ResultsRobustness tests

Results are robust to whether we compare banks from coun-tries with similar legal system origins (English, French, Ger-man/Nordic).

Then, IT countries have stronger banking systems even whencompared to other countries with same economic and legal char-acteristics.

Also robust if we compare the soundness between banks fromIT countries where the central bank is also responsible for banksupervision, and banks from other countries.

This test suggests that arguments from IT critics are not thecase.

Conclusion

Contrary to recent criticism, countries that adopt IT presentsounder banking systems, even during times of economics un-certainty.

Possible reasons for the results:

(a) Price stability together with enhanced communication and ac-countability might play a role in reducing banks’ risk;

(b) IT central banks have not ignored the build up of financial im-balances in their respective markets.

(c) Others?

However, this paper argues neither that central banks mustonly attain and maintain price stability nor that no trade-offsbetween monetary policy and financial stability exist.