inês cunha rocha pereira - repositorium.sdum.uminho.ptªs... · long-term post-performance in...

TRANSCRIPT

Universidade do MinhoEscola de Economia e Gestão

Inês Cunha Rocha Pereira

abril de 2016

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

Inês

Cun

ha R

ocha

Per

eira

A

nn

ou

nce

me

nt

retu

rns

an

d p

ost

-me

rge

r p

erf

orm

an

ce:

evid

en

ce o

f M

&A

mo

me

ntu

m in

th

e E

uro

pe

an

Un

ion

ma

rke

t U

Min

ho|2

016

Inês Cunha Rocha Pereira

abril de 2016

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

Trabalho efetuado sob a orientação doProfessor Doutor Gilberto Ramos Loureiro

Dissertação de MestradoMestrado em Finanças

Universidade do MinhoEscola de Economia e Gestão

ii| Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

DECLARAÇÃO

Nome: Inês Cunha Rocha Pereira

Endereço eletrónico: [email protected]

Número do Cartão de Cidadão: 14415485

Título da Dissertação: Announcement returns and post-merger performance: evidence of M&A

momentum in the European Union market

Orientador: Professor Doutor Gilberto Ramos Loureiro

Ano de conclusão: 2016

Designação do Mestrado: Mestrado em Finanças

É AUTORIZADA A REPRODUÇÃO INTEGRAL DESTA DISSERTAÇÃO APENAS PARA

EFEITOS DE INVESTIGAÇÃO, MEDIANTE DECLARAÇÃO ESCRITA DO INTERESSADO, QUE

A TAL SE COMPROMETE.

Universidade do Minho, 29 de abril de 2016

Assinatura: ________________________________________________

Inês Cunha Rocha Pereira

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market |iii

Acknowledgments

At the end of one of the most important stages of my academic career, I wish to leave a

sign of appreciation and special thanks to some people.

Firstly, I would like to thank my supervisor, Professor Gilberto Ramos Loureiro, all his help,

dedication and patience. His exhaustive comments and constructive recommendations as well as

his willingness to give his time so generously are much appreciated. Additionally, I would like to

thank my friends, especially Joana Ferreira and Tânia Fernandes, for their encouragement and

help, and lastly, a special thanks to my parents and my brother for their understanding and

reinforcement when it was most necessary.

iv| Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market |v

Announcement returns and post-merger performance: evidence of M&A momentum in the

European Union market

Abstract

This study examines the short-term stock price reaction to an acquisition announcement and the

long-term post-performance in order to test the existence of a momentum effect in mergers and

acquisitions (M&A). The stock price reaction to the announcement of an acquisition is measured

by the cumulative abnormal announcement returns (CAARs), while the long-run performance is

estimated using the buy-and-hold abnormal returns (BHARs). Using a sample of 3,496 European

Union (EU) completed acquisitions between 2002 and 2012, I find evidence of merger momentum

by showing that (1) acquirers are more likely to obtain higher CAARs in period of “hot merger

markets” (i.e., when previous recent acquirers have also earned higher announcement returns)

and (2) the higher abnormal announcement returns tend to revert in the long-run, with acquirers

exhibiting lower BHARs. These results are in line with the investor sentiment (optimism) hypothesis

in hot merger markets. Further, the findings hold after several robustness tests, including industry

fixed effects and the elimination of consecutive acquisitions by the same acquirer that occur in a

small time window.

Keywords: Mergers & Acquisitions; Merger Momentum; Long-run Reversal; Over-optimism

Hypothesis

vi| Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market |vii

Rendibilidades anormais acumuladas e a performance no longo prazo após fusões e aquisições:

evidência de momentum na União Europeia

Resumo

Este estudo tem como objetivo analisar a existência de momentum em fusões e aquisições (F&A).

Consistente com a literatura, este fenómeno é analisado através da comparação das rendibilidades

anormais acumuladas com as rendibilidades a 3 anos das empresas envolventes na compra da

aquisição. Usando uma amostra de 3496 F&A efetuadas por empresas pertencentes à União

Europeia entre 2002 e 2012, encontra-se evidência de momentum, observando-se que (1)

acquirers obtêm rendibilidades positivas e elevadas na presença de hot merger markets (isto é,

quando recentes aquisições tem sido bem sucedidas) e (2) as elevadas rendibilidades tendem a

reverter no longo prazo, com as empresas adquirentes reportando rendibilidades negativas a 3

anos. Os resultados são consistentes com a teoria do sentimento do investidor (otimismo). Após

vários testes de robustez, incluindo efeitos fixos por indústria e a eliminação de aquisições

consecutivas realizadas pela mesma empresa num pequeno espaço de tempo, os resultados

mantêm-se consistentes.

Palavras-chave: Fusões e Aquisições, Rendibilidades Anormais, Momentum, Excesso de Otimismo

viii| Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market |ix

Table of Contents

Acknowledgments ..................................................................................................................... iii

Abstract ..................................................................................................................................... v

Resumo ................................................................................................................................... vii

Table of Contents ..................................................................................................................... ix

Index of figures and Tables ....................................................................................................... xi

1. Introduction ...................................................................................................................... 1

2. Literature review and hypotheses development .................................................................. 3

3. Empirical model related methodology ................................................................................ 7

3.1. Methodology for short-term announcement returns .................................................. 10

3.2. Methodology for long-term buy-and-hold abnormal returns ........................................ 11

4. Data description .............................................................................................................. 13

5. Results ........................................................................................................................... 17

5.1. Short-term announcement returns ........................................................................... 17

5.1.1. Discussion ....................................................................................................... 20

5.2. Long-term buy-and-hold abnormal returns ................................................................ 21

5.2.1. Discussion ....................................................................................................... 24

6. Robustness tests ............................................................................................................. 25

7. Additional analysis: Acquirers from the UK vs non UK ...................................................... 29

8. Conclusion ...................................................................................................................... 31

References ............................................................................................................................. 33

Appendix A - List of variables ................................................................................................... 37

x| Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market |xi

Index of figures and Tables

Figure 1-The trailing 12-month average CAAR and the trailing 12-month number of acquisitions for

acquisitions announced between 2002 and 2012. ............................................................................ 16

Table 1- Description of M&A sample by year ..................................................................................... 14

Table 2-Description of M&A sample by country .................................................................................. 15

Table 3-Summary Statistics ............................................................................................................. 17

Table 4-Regression results for the CAAR as dependent variable .......................................................... 19

Table 5-Regression results for the BHAR as dependent variable. ......................................................... 23

Table 6-Regression results for the CAAR as dependent variable: robustness test .................................. 26

Table 7-Regression results for the BHAR as dependent variable: robustness test .................................. 28

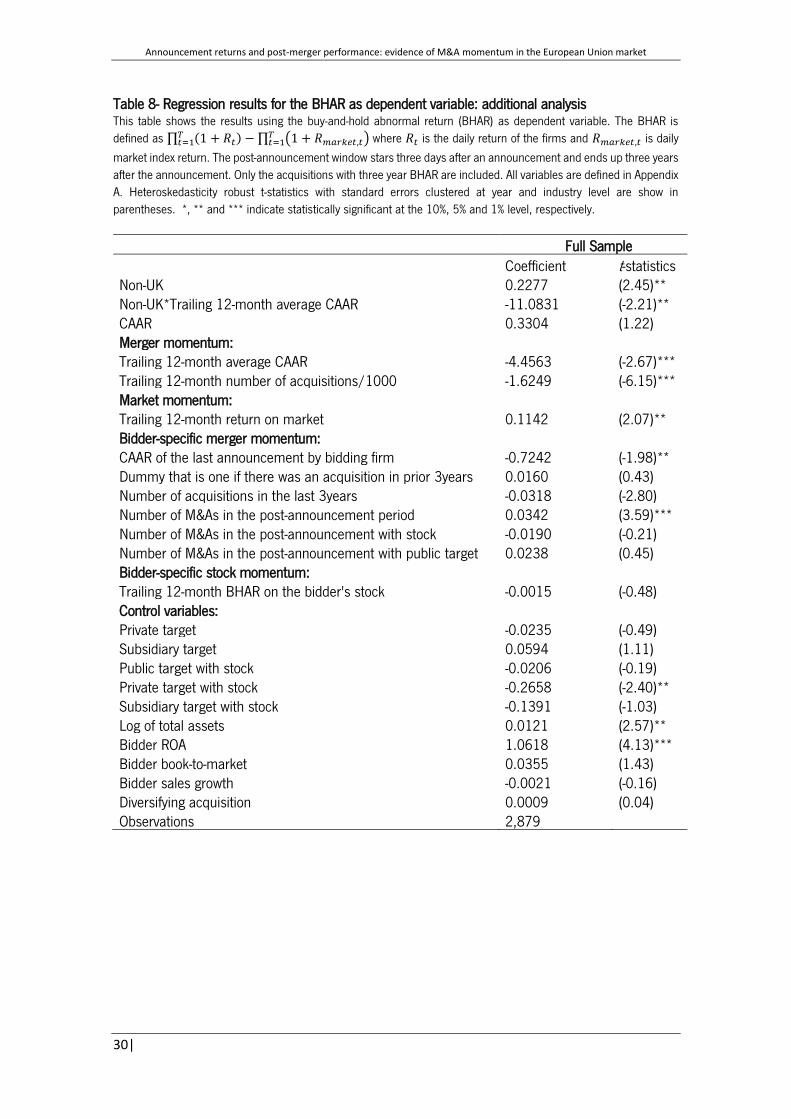

Table 8-Regression results for the BHAR as dependent variable: additional analysis ............................. 30

xii| Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

|1

1. Introduction

With the strengthened competition in the capital markets, corporate organizations have put

an increased attention on their value creation strategies to ensure an advantage over competitors.

Mergers and acquisitions (M&A)1 are appointed as one of the most popular corporate strategies

through which companies create value and improve their competitiveness by achieving synergies

such as economies of scale and scope (Brealey, Myers, and Allen, 2011). Thus, M&As become an

integral part of the long-term business strategy of corporations all over the world (Mallikarjunappa

and Nayak, 2007).

The volume of mergers and acquisitions has greatly expanded over the past quarter century

and are now commonly used by corporations throughout the world to pursue their goals and

objectives related to strategic growth (Gaughan, 2005). Once a phenomenon seen primarily in the

United States (US), M&As have taken an important role in the European market as result of the

introduction of the 1992 Single Market program, the European Monetary Union, the development

of new European stock exchanges and further deregulation, privatization, and growth in the

technological industries (Weston, Mitchell, and Mulherin, 2013).

Although M&A activity should be viewed as value-enhancing strategic decisions, empirical

studies have not always shown positive wealth effects for the acquirer’s shareholders. The

overriding conclusion, in most of the studies, is that the announcement returns of the bidding firms

are slightly positive, but in the long-run they are significantly negative (Agrawal, Jaffe, and

Mandelker, 1992; Agrawal and Jaffe, 2000). Additionally, studies demonstrate that this negative

abnormal performance does not seem to be explained by specific characteristics of either the firms

involved or the acquisition deal. For instance, Harris, Frank, and Mayer (1987) analyse the

differences in the type of payment (cash or stock); Gregory (1997) studies the attitude of the

bidders and the type of acquisition. All of them find that bidders’ negative long-run performance is

not diminished or eliminated because of the type of deal.

Several recent studies on M&As have focused on merger momentum2, offering a number

of different insights into several acquisition theories. I examine these theories that are in line with

1 The concepts of merger and acquisition differs from each another as the first usually described a “friendly” union of two firms while the second is

used to describe a more hostile takeover. Although, throughout this work, these two concepts are used as synonyms. 2 Rosen (2006) defines merger momentum as a correlation between the market reaction to an acquisition announcement and previous market

conditions.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

2|

the notion of merger momentum, but have different expectations about the return of the bidding

firm in the long-run. The neoclassical theory considers that managers act in the best interest of the

shareholders and that merger momentum may be a response to numerous industry shocks that

increase synergies and therefore there is no long-term reversal. A second theory is that there are

managerial motivations behind M&A waves that are typically not aligned with shareholder’s interest.

If managerial goals drive merger decisions, then acquisitions during waves may be worse than

other acquisitions (Gorton, Kahl, and Rosen, 2005). The last theory is that momentum results from

the excessive optimism from shareholders and probably managers. According to Rosen (2006) this

is a suitable explanation for momentum and, at the same time, for the negative abnormal

performance in the long-run. Any increase in the returns of the bidding firm at the announcement

should reverse in the long-run as beliefs are substituted by outcomes.

The purpose of this study is to analyse the existence of a momentum effect in M&A in

periods of merger waves or hot M&A markets. Consistent with the literature, I evaluate the existence

of momentum in M&A by comparing the short-term announcement returns to the long-term

performance post M&A. If the long-term performance exhibits a downward reverse pattern with

respect to the announcement returns, then we may infer that the market overreacted to the

announcement of the acquisition, which suggests that investor sentiment may be a possible

explanation for merger momentum. This phenomenon may be more frequent during bull markets

or waves of acquisitions in certain industries.

Using a sample of 3,496 completed acquisitions by public firms announced between 2002

and 2012, I analyse the initial market reaction to the announcement of the acquisitions following

Brown, and Warner (1985) and long-run returns to acquisitions following Loughran and Vijh’s

(1997) methodology.

My results suggest the existence of merger momentum. For instance, the initial stock price

reaction to the announcement of an acquisition is positively correlated with the announcement

returns of previous recent acquisitions. However, in the long-run, there is a reversal effect. This

suggests that firms announcing an acquisition during a hot merger market perform no better and

possibly worse, all else equal, than those announcing at other times (Rosen, 2006). The results

are consistent with the overoptimism hypothesis in hot merger markets, showing that the effects

of investor optimism on the bidder performance is a phenomenon that also affects the European

Union market.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

|3

This study contributes to the literature on the impact that investor sentiment has on the

market reaction to M&A announcements, by exploring the effects on the European Union market.

The majority of the studies on this topic are focused mainly in the US, Canada and the UK, giving

little importance to M&A activity in the rest of Europe (Bruner, 2004; Brealey, Cooper, and Kaplanis,

2010; Sudarsanam, 2003). To the best of my knowledge, this is the first study of M&A momentum

in the EU market.

The study is organized as follows: Section 2 discusses related literature and the hypotheses

development; section 3 presents the empirical model and related methodology; section 4 describes

the sample selection and the data; the results of short-term announcement returns are discussed

in section 4 and the results for long-term returns in section 5. Section 6 presents some robustness

checks and section 7 compares the reversal effect on the UK and non-UK countries. The main

conclusions of the study are discussed in section 8.

2. Literature review and hypotheses development

It is a well-established fact that M&As come in waves and that some waves are strongly

clustered by industry (Mitchell and Mulherin, 1996). One of the most important challenges in the

M&A activity has been the explanation of this persistent pattern that is consistent with merger

momentum.

Rosen (2006) defines “merger momentum” as a correlation between the market reaction

to an acquisition announcement and recent market conditions. Thus, according to him, a “hot

merger market” is one in which recent acquisitions by other firms have been well received. Even

though “hot” markets are correlated with merger waves, they are not necessarily the same. As

Rosen (2006) refers, waves are traditionally measured by the number or value of acquisitions

rather than by the market’s reaction to acquisition announcements3.

The market reaction to an M&A announcement of the bidding firm depends naturally on

the synergies created by the acquisition. There are, however, other factors that may also explain

M&A announcement returns, such as the capacity of the managers to capture some of the

synergies created for their shareholders, whether the market anticipates or not the announcement,

or whether the shareholders react rationally to the announcement of M&As. Following Rosen

(2006), I assume, throughout this study, that the acquisitions are not fully anticipated by the market

3 The market reaction to acquisition announcements is gauged by the return of the bidding firms.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

4|

and that the managers of the bidding firms gain at least part of the surplus. These two assumptions

must hold, otherwise we should see no relationship between “hot merger markets” and M&A

announcements.

A sizeable stream of theoretical research attempts to explain the source of momentum

under different theories. The neoclassical theory, simplified by Andrade, Mitchell, and Stafford

(2001), advocates that acquisition waves emerge from economic, regulatory and industrial shocks.

According to this theory, shocks create high synergies and thus acquisitions following positive

shocks are better, on average, than others, leading to correlated announcement returns. In other

words, it is a reflection of merger momentum as the market reaction to M&A announcements is

positively correlated to previous market conditions with positive shocks. This hypothesis implies

that firms act in the interest of shareholders, making only acquisitions that increase the firm value.

In short, if the neoclassical theory holds, the positive abnormal returns from acquisition

announcements should not be reverted in the long-run.

A second theory for the increase in M&A activity is that there are managerial motivations

for acquisitions. For instance, some researchers claim that the “eat or be eaten” hypothesis,

proposed by Gorton, Kahl, and Rosen (2005), might explain the existence of acquisition waves.

The idea behind this theory is that managers can reduce their chances of being acquired by

acquiring other firms. A manager is willing to acquire defensively even when the acquisition is not

profitable (Rosen, 2006). If defensive aims are behind merger waves, then acquisitions during

these waves may be worse than acquisitions at other times (Gorton, Kahl, and Rosen, 2005).

Additionally, the hubris hypothesis, formulated by Roll (1986), is also appointed to explain

irrationality of the managerial behaviour. Roll advocates that managers are excessively self-

confident, mainly in bull markets, and so being misled by their overoptimism when evaluating M&A

opportunities. Driven by their excessive optimism, managers make acquisitions even when they

predict that the announcement will bring a decline in stock prices because they believe that they

will be proven correctly in the long-run. Since the acquisition hurts the value of the firm, there is

no reason to expect that the initial stock price will reverse in the long-run. Alternatively, managers

may exploit shareholders if they are compensated by increases in stock prices. They may have an

incentive to make bad acquisitions in “hot markets” since even a bad acquisition may increase the

stock price temporarily.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

|5

Taking into account that shareholders are rational, as assumed before, both the

neoclassical and managerial theories may explain merger momentum but in a distinct way. If the

neoclassical hypothesis holds, we should verify a positive correlation between merger waves and

the market reaction to the announcement of the acquisition, as the waves are a response to

common stocks that positively affect the potential synergies from the acquisitions. On the other

hand, if managerial motivations drive merger decisions, this correlation could be negative, i.e, may

actually exist acquisition waves, motivated by irrational or opportunistic behaviour of managers,

but the market reaction to these waves may be negative. Assuming that the market recognizes the

motivations of managers, it revises the acquisition’s valuation down when it is announced.

Another explanation that warrants further attention is the hot markets theory (Thomas and

Coakley, 2004) that was developed to explain the presence of investors’ optimism (Ljugqvist,

Nanda, and Singh, 2006). In fact, empirical studies find that, investors may be overly optimistic in

hot (bull) markets. For instance, Loughran and Ritter (1995) associate high returns on seasoned

equity offerings (SEO) to optimistic beliefs from investors. This theory was further applied by Rosen

(2006) to the market of mergers and acquisitions. He finds evidence that bidder stock prices are

more likely to increase when the acquisition is announced in a hot market as compared to a cold

market. Rosen explains this by the excessive optimism of investors, who in the presence of bull

markets or when recent M&As are well received, systematically misperceive the synergy gains from

the acquisitions.

If the investors’ overoptimism influences the market reaction to M&A announcements, then

we should see autocorrelation in bidding firms’ returns (Rosen, 2006). In the presence of bull

markets, where optimism empires, the market reaction to M&A announcements should be more

positive than other times, causing merger momentum, i.e., positive abnormal returns in the short-

run. However, this tendency should reverse, in the long-run, as the market recognizes through

results that acquisitions initiated in hot markets were not prudently evaluated and were, in fact,

bad deals, leading to negative abnormal long-run returns.

In addition to these theories, empirical studies find that acquisitions take place when the

overall stock market is hot. This relation is not new, dating back at least to Nelson’s (1959) study

of merger waves in the US, who observed that M&A activity seems to increase when the stock

prices are high: ‘‘It appears that merger expansion was not only a phenomenon of prosperity, but

that it was also closely related to the state of the capital market. Two reference cycle expansions,

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

6|

unaccompanied by a strong upswing in stock prices, were marked by the absence of a merger

revival’’ (Nelson, 1959, p.7). Javanovic and Rousseau (2001) also confirmed this evidence on their

study. According to Rosen (2006), the positive correlation between the stock prices and the

intensity of merger activity could give support to the neoclassical theory if a raising stock market

reflects the increasing potential merger synergies.

Other reasons are appointed to explain the relation between hot stock markets and

acquisition waves. For instance, managers are more likely to make acquisitions during stock market

booms to take advantage of overvalued stocks (Dong, Hirshleifer, Richardson, and Teoh, 2006;

Rhodes-Kropf, Robinson, and Viswanathan, 2005). In that case, in a rational market, the reaction

to the announcement already considers that firm’s stock is overvalued. Thus, we would expect a

negative announcement return with no reversal in the long-run. Alternatively, this positive

correlation can also be a reflection of excessive optimism from investors. If so, we would observe

a more positive reaction to the acquisition announcement in the short-run, especially during hot

markets, with reversal in the long-run.

In sum, the previous theories of why acquisitions happen provide us different explanations

for merger momentum. Both the neoclassical and the overoptimism hypotheses indicate that the

market reaction to the announcement of the acquisitions should be more positive in the presence

of hot markets. However, while in the first theory we expect no reversal in the long-run returns, in

the second we expect a reversal in the stock returns of the bidding firms. On the other hand, if

merger decisions are motivated by managerial motivations, acquisitions during waves may be

worse than acquisitions at other times, i.e, we should verify a negative market reaction to M&A

announcements.

In light of the literature reviewed above, I formulate the following hypotheses that will be

tested in this study:

H1: The stock price reaction to M&A announcements is positively correlated with the

response to other acquisitions in the recent past, especially during hot markets.

H2: Long-term performance post-acquisition is negatively correlated with the

announcement returns in series of M&As that occur during hot markets.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

|7

3. Empirical model related methodology

The empirical model that I use to test the existence of merger momentum is adopted from

Rosen (2006). The model examines how recent merger activity and stock market conditions affect

the market reaction to an acquisition announcement. As in Rosen (2006), I focus only on the

acquiring firm. The market reaction to an M&A announcement, which is measured by the return of

the bidding firm, is analysed over two different horizons, in the short and long-run. It is through the

comparison of these two periods that I can infer about the existence of momentum. The

methodology used for the short-term announcement returns and long-term buy-and-hold returns is

presented in the subsection 3.1 and 3.2, respectively.

To test the first hypothesis of this study the regression model used is the following:

AcquirerCAAR=ƒ(Merger Activity, Market Momentum, Bidder-Specific Merger

Momentum, Bidder-Specific Stock Momentum, Deal-Specific and Bidder

Control Variables)

(1)

Where AcquirerCAAR is the initial market reaction to the acquisition announcements, measured by

the average five-day cumulative abnormal announcement returns (CAARs) for the bidding firms

surrounding the announcements.

The first independent variable of the model is the recent overall merger activity. As Rosen

(2006) suggests, two measures are included for this variable, one to capture merger momentum

and one to capture waves. The variable used to proxy for merger momentum is the trailing 12-

month average cumulative abnormal announcement return (CAAR), that is, the average five-day

CAAR for all sample acquisitions in the 12-month ending five days prior to the announcement. This

is the main measure of hot merger markets. If recent acquisitions created strong announcement

returns we can infer that we are in the presence of a hot merger market. Thus, per hypothesis 1,

I expect the coefficient on the trailing 12-month average CAAR to be positive and statistically

significant.

The second measure of previous merger conditions, intended to capture merger waves, is

the number of acquisitions in the previous 12-month before an announcement (hereby, trailing 12-

month number of acquisitions). According to Shughart and Tollison (1984), there is autocorrelation

between the number of acquisitions in a given year and the number of acquisitions in the following

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

8|

year. As the factors that lead to an autocorrelation in the number of acquisitions might affect the

market reaction to an M&A announcement, this variable is used as an alternative proxy for hot

merger market (the intensity of M&A activity). Thus, I expect a positive relation between the prior

number of M&As and current announcement returns.

The next independent variable of the model (Market Momentum) considers that the market

reaction to an announcement may be affected by the existing conditions in the stock market. As

discussed early, in the literature review section, there is evidence that acquisitions tend to occur

when the overall stock market is overvalued. Thus, to measure if we are in the presence of a rising

stock prices, the return of each market in the year ending five days before an acquisition

announcement (trailing 12-month market return) is included. This variable is the proxy for the

market momentum.

The bidder-specific merger momentum factor is controlled by three variables, as suggested

by Rosen (2006). In order to evaluate the quality of the acquisitions taken by the bidder, I use the

five-day CAAR on the last acquisition by the bidding firm if it made an announcement in the previous

three years. Otherwise, it is assumed to be zero. To analyse how active the firm is, the number of

acquisitions announced in the previous three years by the bidder firm is considered. In my sample,

I have firms that make several acquisitions, the so called serial acquirers, while others make only

one. Finally, to distinguish frequent acquirers from occasional ones, a variable dummy that is one

if the bidding firm makes an acquisition in the last three years is included.

The bidder-specific returns have also an effect on the market reaction to the

announcement, as considered in the model. To account for this impact, I use the bidder’s buy-and-

hold abnormal return (BHAR) starting one year prior to the acquisition announcement and ending

five days before the announcement (bidder trailing 12-month BHAR).

Finally, to test the market reaction as correctly as possible, some control variables are

present in the model to account for characteristics related with the specific situation of the bidding

firm as well as specific conditions of the acquisitions. Firstly, I divide the means of payments in

stock, cash or mixed financing in order to control the differences reported by the types of payments.

For instance, Asquith, Bruner, and Mullins, 1983; Travlos, 1987; Servaes 1991, all document a

negative market reaction to an acquisition financed with stock, when compared to a cash offer.

Furthermore, the differences stated by Fuller, Netter and Stegemoller (2002) between public and

other type of targets are controlled. They find that bidding firm shareholders have a negative return

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

|9

when purchasing a public target and have a positive return when buying subsidiary or private

targets.

In what concerns to the specific characteristics of the bidding firm, the size effect is

considered using the logarithm of the total assets of the firms. According to Loderer and Martin

(1997), there is a negative correlation between the size of the acquirer firm and its CAARs in the

short-run. The financial situation of the bidding firm is controlled using the book-to-market ratio

and the return on assets (ROA). Studies demonstrate that high book-to-market ratio, which is

correlated with a low Tobin’s Q, is related with higher short-run CAAR (Lang, Stulz, and Walkling,

1989). The ROA is used as a measure of the financial performance of the company, as there is

evidence that firms with a better prior performance make better acquisitions (Morck, Shleifer, and

Vishny, 1990). Additionally, I include the sales growth of the bidding firm as a proxy for the

company's growth opportunities.

Finally, Maquieira, Megginson, and Nail (1998) suggest that the returns of the acquirers

are lower when the acquisition is diversified4. So, I compare the two-digit SIC code of the bidding

firm with the two-digit SIC code of the target. A dummy variable is then included, which equals one

if the acquisition is diversified (that is, the acquirer’s industry two-digit SIC code differs from that

of the target’s).

To examine the second hypothesis, I estimate a similar regression to the previous one, but

using the 3-year buy-and-hold abnormal returns for the acquirer following the acquisition,

AcquirerBHAR, as dependent variable. Specifically, I estimate the following model to examine the

long-term performance post-acquisition:

AcquirerBHAR=ƒ(AcquirerCAAR, Merger Activity, Market Momentum, Bidder-Specific

Merger Momentum, Bidder-Specific Stock Momentum, Deal-Specific and

Bidder Control Variables)

(2)

All the remaining variables are the same described earlier and used in Model 1, with four

additional independent variables. One of them is the CAAR surrounding the announcement, which

is included as a control variable. According to the author of the model (Rosen, 2006), it allows

another test for the reversal hypothesis. The other three control variables are included under the

4 This evidence is also advocated by Morck, Shleifer, and Vishny (1990).

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

10|

Bidder-Specific Merger Momentum5 group with the purpose to consider that firms can make

additional M&As in the post-announcement period. This decision may be affected by the return

obtained by the bidding firm after its initial acquisition announcement. According to Rosen (2006),

this “feedback effect” could inflate the long-run result of an M&A announcement. Thus, to account

for this, the number of acquisitions made by the bidding firm in the post-announcement period is

used as a control variable. Additionally, since empirical studies report differences within the method

of payment as well as in the type of target, the number of acquisitions in the post-announcement

period that use stock and those in which the target is public are also included.

If the phenomenon of merger momentum is present in my sample, I can expect a reversal in

the acquirer BHAR. Therefore, the main measure of hot merger markets, the trailing 12-month

average CAAR, should present a negative and statistically significant coefficient to confirm

hypothesis 2. The same arrangement should be analysed in the measure of merger waves, (trailing

12-month number of acquisitions).

3.1. Methodology for short-term announcement returns

To examine the initial market reaction to the acquisition announcement, I follow Browns

and Warner (1985) standard event study methodology and calculate the cumulative abnormal

announcement returns (CAARs) for the five-day (-2, +2) period surrounding the acquisition

announcement. The methodology is based on the assumption that the effect of the acquisition

announcement will be reflected immediately in the stock prices. Therefore, the stock price reaction

should incorporate any new information, including synergies created by the acquisitions, as well

as the effect of investor sentiment such as overoptimism.

Following the event study methodology, the abnormal announcement return (AAR) is

computed as the difference between the actual return of the bidding firm over the event window

and the expected return without considering the event (normal return). The expected return is

calculated using the market model, estimated over an estimation window ranging from -250 to -25

days prior to the M&A announcement date6. The market model assumes a stable linear relation

between the market return and the security return of the firm:

5 The variables are not stated in the model for reasons of brevity. 6 This period is considered a sufficiently long period for the estimation of the coefficients as suggested by Brown and Wagner, 1995, and Kothari

and Warner, 2007.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

|11

𝑅𝑖𝑡 = 𝛼𝑖 + 𝛽𝑖𝑅𝑚𝑡 + 𝜀𝑖𝑡 (2)

Where 𝑅𝑖𝑡 is the daily stock return of firm i in day t and 𝑅𝑚𝑡 is the daily market index return.

The model is estimated using daily stock returns and, as a proxy for the market, I use the

stock market index of each firm’s country, provided by DataStream.

With the estimates of 𝛼𝑖 and 𝛽𝑖, I compute the expected (normal) return over the 5-day (-2, +2)

event window as follows:

𝐴𝐴�̂�𝑖𝑡 = 𝑅𝑖𝑡 − 𝛼�̂� − 𝛽�̂�𝑅𝑚𝑡 (3)

To obtain the cumulative abnormal announcement return (CAAR), the daily AAR are summed over

the select event window.

𝐶𝐴𝐴𝑅 = ∑ 𝐴𝐴�̂�𝑖𝑡

𝑡=2

𝑡=−2

(4)

3.2. Methodology for long-term buy-and-hold abnormal returns

In order to test my second hypothesis, I extend the time horizon of the dependent variable

and compute long-term returns. If the initial market reaction to the M&A announcement

incorporates all the information related to the acquisition, then the post-announcement abnormal

return should be zero, on average. Deviations from this value may be partially explained by investor

sentiment in the form of over or underreaction. In fact, if the neoclassical theory holds, the CAAR

should be an unbiased estimate of the value of the acquisition as there are no deviations in the

post-announcement period. The same happens if managerial motivations drive acquisitions and

the markets knows that.7 However, if the overoptimism among investors is the source of the positive

relationship between the CAAR and merger momentum variable, then there should be a reversal

of the CAAR in the long-run.

7 If managerial motivations are responsible for acquisitions, the initial market reaction, measured by the CAARs of the bidding firms, should be

negative. Since the acquisition hurts the value of the firms, there is no reason to suppose that, in the long-run, exists a reversal. It is important to

note that the managerial motivations hypothesis is not an alternative explanation for merger momentum as high CAARs, it only justifies the existence

of waves.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

12|

To analyse the post-acquisition long-term performance, I follow Loughran and Vijh’s (1997)

methodology and compute the buy-and-hold abnormal return (BHAR) over a three-year horizon8.

Recent empirical evidence shows that long-horizon abnormal returns can be seriously

misspecified (Kothari and Warner, 1997). For instance, the implementation of BHAR is likely to

under-estimate the significance of long-run negative abnormal return and to over-estimate the

significance of long-run positive abnormal return (Gregory, 1997). Nevertheless, the skewness bias

associated with this methodology is not a serious problem in the context of this study because it

works against finding evidence of a reversal effect in stock returns post-acquisition. Thus, should

the results show a negative relation between BHAR and short-term announcement returns, my

confidence in the existence of a reversal effect is even stronger.

Another caveat of this methodology, referred by Fama (1998), is that the BHAR approach

ignores cross-sectional correlation in abnormal returns among firm events. This can lead to

overstated test statistics and thus produce less reliable inferences (Mitchell and Stafford, 2000).

In order to mitigate, in some way, this problem, I cluster the standard errors of the regressions at

the country and year level. Despite the criticism that involves this approach, Lyon, Barber, and Tsai

(1999, p. 166) support the use of BHAR as it “precisely measures investor experience”.

To compute the BHAR, I require that all the firms in my sample have three years of returns

after the announcement. This restriction could lead to survivorship bias as I may exclude some

non-surviving firms within the three-year period post-announcement. Although I acknowledge that

this may create a problem, I rely on Baker and Limmack (2001) as well as Higson and Elliott

(1998), who demonstrate that in their studies, the survivorship bias does not appear to have a

significant impact on the results.

The three-year BHAR is computed as a difference between buy-and-hold returns of the

firms that engaged in M&As and the buy-and-hold return of the market from the country where the

firm belongs to. The formulation is given by the following equation:

𝐵𝐻𝐴𝑅 = ∏(1 + 𝑅𝑡) − ∏(1 + 𝑅𝑚𝑎𝑟𝑘𝑒𝑡,𝑡)

𝑇

𝑡=1

𝑇

𝑡=1

8 Consistent with Rosen (2006), I adopt the three year time window as it is considered to be long enough to capture the abnormal performance of

the bidding firms.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

|13

Where BHAR is the compounded abnormal return for holding a stock of a firm that has engaged in

an acquisition across t periods, the 𝑅𝑡 is the daily return of the firm and 𝑅𝑚𝑎𝑟𝑘𝑒𝑡,𝑡 is daily of the

firm’s country market index. The BHAR are computed over the period that starts three days after

the announcement of the acquisition and ends three years after.

4. Data description

The sample used consists of 3,496 completed acquisitions undertaken by European Union

(EU) firms between January 1st 2002 and December 31st 2012, as provided by Securities Data

Company (SDC) database. Both targets and acquirers are members of the EU. Consistent with the

literature, I require that the acquirer purchases at least 50% of the shares of the target and after

the purchase the bidder owns at least 90% of the target company. Additionally, acquirers need to

be public firms and deals with deal value below $10 million are excluded.

For each deal, I collect the announcement date, the SIC codes, names and countries of

the acquirers and targets as well as other deal characteristics, such as the target type (public,

private or subsidiary) and the method of payment (pure cash, pure stock, or mixed9). As SDC does

not provide stock price information, I combine this sample with Thomson Reuters’ DataStream.

Further, to access the performance of the bidder firm, a set of accounting data are extracted from

Thomson Financial’s WorldScope database such as the total assets, sales, EBIT and book value of

equity. The market value of equity is collected from DataStream.

Within the group of 28 countries that compose the European Union, I only consider 21 as

the data related to the other 7 is unavailable in the pre-adoption period10. Also, I consider only deals

where the acquirers have at least five days of return data surrounding the announcement of the

acquisition. In addition, I exclude deals in which the acquirer announced more than one acquisition

in the same day. As this sample involves a set of different countries spanned over 11 years, I have

to take into account the inflation effect, so, I adjusted the dollar value of total assets to reflect 2010

prices using the Consumer Price Index (CPI) collected from the World Bank database.

9 Mixed payment acquisitions are those in which the method of financing is neither pure stock nor pure cash and integrate methods classified as

“other” by SDC. 10 M&A Deals announced in Croatia, Estonia, Hungary, Latvia, Lithuania, Malta and Slovakia were excluded.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

14|

Finally, any firm with a negative book value of equity is dropped and, in order to reduce

the influence of outliers, I winsorize some of the variables11 at the top and bottom 1% of the

distribution.

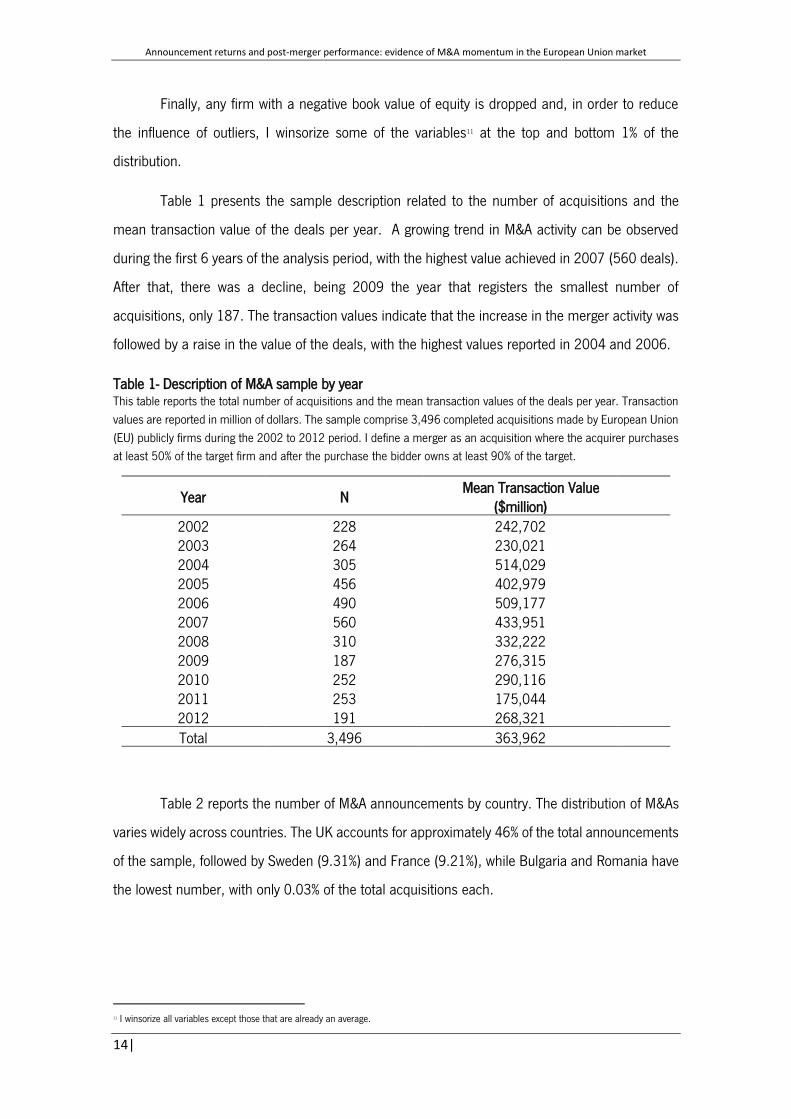

Table 1 presents the sample description related to the number of acquisitions and the

mean transaction value of the deals per year. A growing trend in M&A activity can be observed

during the first 6 years of the analysis period, with the highest value achieved in 2007 (560 deals).

After that, there was a decline, being 2009 the year that registers the smallest number of

acquisitions, only 187. The transaction values indicate that the increase in the merger activity was

followed by a raise in the value of the deals, with the highest values reported in 2004 and 2006.

Table 1- Description of M&A sample by year This table reports the total number of acquisitions and the mean transaction values of the deals per year. Transaction

values are reported in million of dollars. The sample comprise 3,496 completed acquisitions made by European Union

(EU) publicly firms during the 2002 to 2012 period. I define a merger as an acquisition where the acquirer purchases

at least 50% of the target firm and after the purchase the bidder owns at least 90% of the target.

Year N Mean Transaction Value

($million)

2002 228 242,702 2003 264 230,021 2004 305 514,029 2005 456 402,979 2006 490 509,177 2007 560 433,951 2008 310 332,222 2009 187 276,315 2010 252 290,116 2011 253 175,044 2012 191 268,321 Total 3,496 363,962

Table 2 reports the number of M&A announcements by country. The distribution of M&As

varies widely across countries. The UK accounts for approximately 46% of the total announcements

of the sample, followed by Sweden (9.31%) and France (9.21%), while Bulgaria and Romania have

the lowest number, with only 0.03% of the total acquisitions each.

11 I winsorize all variables except those that are already an average.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

|15

Table 2- Description of M&A sample by country The table lists the number of acquisitions announcements by each of the countries involved in the sample during the

2002 to 2012 period. Within the group of 28 countries that compose the European Union only 21 are considered as

the data relative to the remaining is unavailable in the pre-adoption period.

Country N Percentage

Austria 58 1.66 Belgium 86 2.46 Bulgaria 1 0.03 Cyprus 5 0.14 Czech Republic 2 0.06 Denmark 66 1.89 Finland 119 3.40 France 322 9.21 Germany 198 5.66 Greece 36 1.03 Ireland-Rep 90 2.57 Italy 208 5.95 Luxembourg 10 0.29 Netherlands 140 4.00 Poland 41 1.17 Portugal 24 0.69 Romania 1 0.03 Slovenia 2 0.06 Spain 151 4.32 Sweden 326 9.32 United Kingdom 1,610 46.05 Total 3,496 100.00

Table 3 shows descriptive statistics for all the variables used in the model. Some of them

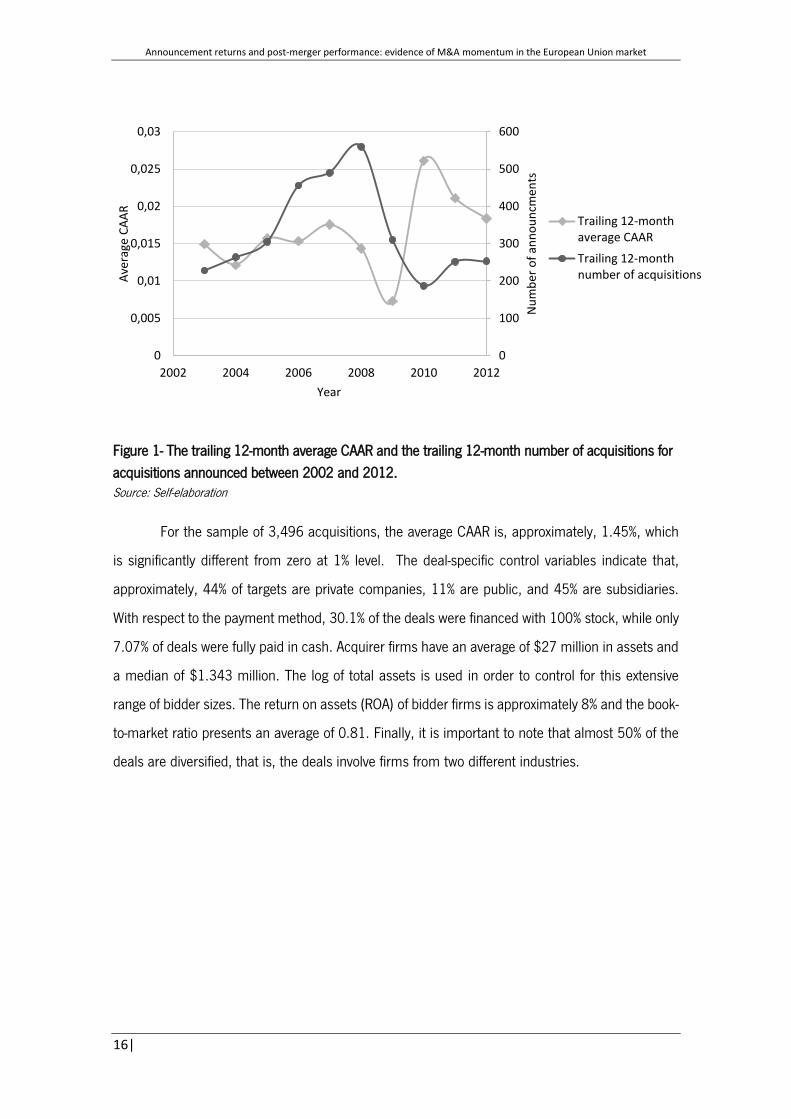

are worth being discussed briefly. The first two variables, the trailing 12-month average CAAR and

the trailing 12-month number of acquisitions, which are the ones used to proxy for merger activity,

can be analysed in Figure 1. They are positively correlated in the first years of the sample period

(2004 a 2009). A clear uptrend in the number of acquisitions during this period is verified, with

the highest number achieved in 2008 (560 acquisitions). This evidence identifies the first period

(2002-2008) as a hot merger market when compared to the rest of the sample period. Although

the two variables show a different pattern after 2009, it is important to note that both of them

describe the conditions of the merger market but in different aspects. While the number of

acquisitions declined, the trailing 12-month CAAR had a significant increase after 2009. This may

be due to the intrinsic value of the deals. Although the number of acquisitions decreased, the deal

value of each acquisition can be higher, leading to this increase in the CAAR.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

16|

For the sample of 3,496 acquisitions, the average CAAR is, approximately, 1.45%, which

is significantly different from zero at 1% level. The deal-specific control variables indicate that,

approximately, 44% of targets are private companies, 11% are public, and 45% are subsidiaries.

With respect to the payment method, 30.1% of the deals were financed with 100% stock, while only

7.07% of deals were fully paid in cash. Acquirer firms have an average of $27 million in assets and

a median of $1.343 million. The log of total assets is used in order to control for this extensive

range of bidder sizes. The return on assets (ROA) of bidder firms is approximately 8% and the book-

to-market ratio presents an average of 0.81. Finally, it is important to note that almost 50% of the

deals are diversified, that is, the deals involve firms from two different industries.

0

100

200

300

400

500

600

0

0,005

0,01

0,015

0,02

0,025

0,03

2002 2004 2006 2008 2010 2012

Nu

mb

er o

f an

no

un

cmen

ts

Ave

rage

CA

AR

Year

Trailing 12-monthaverage CAAR

Trailing 12-monthnumber of acquisitions

Figure 1- The trailing 12-month average CAAR and the trailing 12-month number of acquisitions for

acquisitions announced between 2002 and 2012. Source: Self-elaboration

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

|17

Table 3- Summary Statistics The table provides descriptive statistics of the main variables used. Target is private, subsidiary and public indicate the

percentage of acquisitions with that kind of target; Pure stock and pure cash financing is the percentage of acquisitions

that are 100% financed with stock and cash, respectively; Mixed financing is the percentage of acquisitions in which

the financing method is neither pure stock nor pure cash and methods categorized as “others” by SDC; Total assets

are in US$ million, reflecting 2010 prices; Diversifying acquisition is the percentage of acquisitions in which the

acquirer and the target firms are in different industries. The remaining variables are defined in Appendix A. All variables,

except those that are already an average, are winsorized at top and bottom 1% of the distribution.

Variables N Mean Median Std. Dev CAAR 3,496 1.45% 0.46% 8.03% Trailing 12-month average CAAR 3,488 1.56% 1.60% 0.67% Trailing 12-month number of acquisitions 3,493 354 325 136 Trailing 12-month return on market 3,496 16.81% 20.16% 32.69% CAAR of the last announcement by bidding firm 3,496 0.47% 0 3.15% Dummy that is 1 if there was a M&A in prior 3years 3,496 43.85% 0 49.63% Number of acquisitions in the last 3years 3,496 0.98 0 1.63 Trailing 12-month BHAR on the bidder's stock 3,464 15.33% 5.35% 179.50% Target is private 3,496 44.42% 0 49.70% Target is subsidiary 3,496 44.99% 0 49.76% Target is public 3,496 10.58% 0 30.77% Pure stock financing 3,496 30.09% 0 45.87% Pure cash financing 3,496 7.07% 0 25.63% Mixed financing 3,496 62.84% 1 48.33% Total assets of the bidding firm ($million) 3,404 27.1 1.343 1.16E+08 Log (total assets) 3,404 14.27 14.11 2.249 Bidder ROA 3,102 7.97% 7.82% 7.83% Bidder book-to-market 3,149 0.81 0.64 0.70 Sales growth 3,144 49.54% 12.08% 181.67% Diversifying acquisition 3,496 49.06% 0 50.00%

5. Results

5.1. Short-term announcement returns

Table 4 shows the CAAR regression results for all the acquisitions during the sample

period. The regression includes control variables that account for the type of target involved, the

method of the payment of the acquisition, the specific characteristics of the bidding firm and a

dummy that equals one if the acquisition is diversified and zero otherwise.

The regression results confirm the existence of merger momentum at the overall merger

market-level. The variable used as a proxy for merger momentum, which is the trailing 12-month

average CAAR, has a positive (0.398) and statistically significant coefficient at the 5% significance

level. This means that the average CAAR of recent M&A announcements influences positively the

initial market reaction to an acquisition announcement. A one percentage point increase in the

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

18|

trailing 12-month CAAR increases the bidder’s CAAR by 0.398 percentage points, all else equal.

The second variable used, which aims to capture merger waves (the trailing 12-month number of

acquisitions), has also a positive and statistically significant coefficient at the same significance

level. This result shows that the initial market response to an M&A announcement is positively

related to the intensity of the M&A activity during the prior 12-months period. Rosen (2006) does

not find this effect in the US as the coefficient is described to be insignificant.

There is also evidence of merger momentum at the firm level. The CAAR on the last

announcement by the bidding firm, which is one of the proxies for bidder specific merger

momentum, is positive and statistically significant at 5% significance level. Therefore, the current

market reaction to an acquisition announcement is positively correlated with the quality of the

previous acquisitions undertaken by the firm. This value means that one percentage point in the

bidder’s previous announcement return boosts the CAAR of the current announcement by 8.1

basis points, approximately, all else equal. The number of acquisitions in the previous three years

by the bidder and the first acquisition dummy have a negative and statistically significant coefficient

at 10% and 5% significance level, respectively. This indicates that the market reaction to current

acquisitions is negatively correlated with the quantity of previous acquisitions.

As for the stock market, there is not any evidence that announcing an acquisition in a bull

stock market leads to a better CAAR than announcing an acquisition in a bear market. The

coefficient on the trailing 12-month return on market is not statistically different from zero. In

contrast, Rosen (2006) finds that the stock return of the US market influences positively the CAAR

of the acquisition announcement.

The coefficient on the idiosyncratic return of the bidding firm in the previous 12-month

(trailing 12-month BHAR) is negative and strongly significant at the 1% significance level. When the

return of the bidding firm in the last 12-month to an acquisition announcement increases by one

percentage point, the average CAAR from the announcement is 0.23 basis points lower, all else

equal.

Regarding to the control variables, the results show that both the dummy variable for

private target as well as for subsidiary target are positively and strongly correlated with the CAARs.

These results are consistent with Fuller, Netter, and Stegemoller (2002), who argue that bidders

get a better price when they purchase non-public firms. The attractive price in this type of

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

|19

acquisitions could be justified by the liquidity discount12 and negotiation power of public targets

comparing to subsidiary or private targets. Moreover, the coefficient on the log of the total assets

is negative and statistically significant, meaning that smaller acquirer firms have, on average, larger

CAARs. This result is also consistent with the literature.

Table 4- Regression results for the CAAR as dependent variable

This table shows the cumulative abnormal announcement returns (CAARs) of acquirers over the 2002 and 2012

period. The dependent variable, the CAAR, is calculated for the five days (-2; +2) surrounding the announcement day

(day 0) of the acquisition. Abnormal returns are computed using the market model approach. All variables are defined

in Appendix A. Heteroskedasticity robust t-statistics are show in parentheses. *, ** and *** indicate statistically

significant at the 10%, 5% and 1% level, respectively. Full Sample

Coefficient t-statistics Merger momentum: Trailing 12-month average CAAR 0.3981 (1.98)** Trailing 12-month number of acquisitions/1000 0.0190 (2.10)** Market momentum: Trailing 12-month return on market -0.0008 (-0.19) Bidder-specific merger momentum: CAAR of the last announcement by bidding firm 0.0809 (2.34)** Dummy that is 1 if there was an acquisition in prior 3years -0.0060 (-2.21)** Number of acquisitions in the last 3years -0.0010 (-1.68)* Bidder-specific stock momentum: Trailing 12-month BHAR on the bidder's stock -0.0023 (-4.24)*** Control variables: Private target 0.0234 (5.59)*** Subsidiary target 0.0239 (5.61)*** Public target with stock -0.0035 (-0.46) Private target with stock 0.0015 (0.10) Subsidiary target with stock -0.0004 (-0.03) Log of total assets -0.0012 (-3.52)*** Bidder ROA -0.0175 (-0.97) Bidder book-to-market 0.0016 (0.89) Bidder sales growth 0.0002 (0.20) Diversifying acquisition -0.0012 (-0.54) Observations 2,879 Adjusted R-square 0.0688

12 The liquidity discount exists because private and subsidiaries firms cannot be bought and sold as easily as publicly traded firms (Fuller, Netter,

and Stegemoller, 2002).

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

20|

5.1.1. Discussion

The results in the CAAR regression indicate evidence of merger momentum. The variable

used to proxy for this phenomenon is positively correlated with the CAARs. So, the short-term stock

price reaction to an acquisition announcement tends to be larger the larger is the average reaction

to other M&As that have been recently announced. Also, the overall number of acquisitions in the

recent year is positively related with the CAARs. So, the short-term stock price reaction to an M&A

announcement appears to be positively related not only with quality13 of previous acquisitions but

also with the number of acquisitions in the last 12 months.

These results provide strong support for the first hypothesis of this study. The short-term

stock price reaction to an M&A announcement is positively related to the reaction to other recent

acquisition announcements. This finding puts the overoptimism theory as one possible explanation

for merger momentum. According to it, the positive autocorrelation in announcement returns is

due to the excessive optimism from investors, who in the presence of hot merger markets,

systematically misperceive the synergy gains from the acquisitions. Although, to confirm this

theory, the long-term performance, analysed in the next section, has to exhibit a downward reverse

pattern with respect to the announcement returns.

Contrary to the results of Morck, Shleifer, and Vishny (1990), there is evidence of a negative

relation between the bidder-specific stock momentum and the initial market reaction to an

acquisition announcement. One possible explanation for the negative coefficient on the trailing 12-

month BHAR on the bidder’ stock may be the hubris hypothesis postulated by Roll (1986).

According to Roll, managers of bidding firms that had good outcomes from recent acquisitions may

be afflicted with overconfidence and so they over-estimate their ability to create value even when

they anticipate a decline in the stock price at the acquisition announcement. Managers act in this

way because they believe that the market will prove their perception in the long-run. As

shareholders have not a perfect control over managers’ decisions, they are not able to prevent

such acquisitions. Thus, if the overconfidence of managers leads to making bad acquisitions, the

stock price will be discounted and there is no reason to expect a reversal in the long-run (Rosen,

2006). This suggest a non-positive coefficient on the trailing 12-month BHAR variable in the long-

run regression. I will turn to this issue in the next section.

13 Note that the term “quality” refers to the returns obtained by the bidding firms.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

|21

An additional possible reason for the negative relationship between the CAAR and the

trailing 12-month BHAR variable is the use of stock to financing the acquisition when it is overvalued

(Travlos, 1987). A firm is more likely to make an acquisition with stock financing when its stock

price has been rising. This fact is recognized by the market, which leads to the negative return at

the acquisition announcement. However, when I delete the acquisitions financed with 100% of

stock and run the previous regression14, this value remains strongly negative, which indicates that

this explanation finds weak support in the data.

5.2. Long-term buy-and-hold abnormal returns

Table 5 presents the BHAR regression results. In order to avoid contamination in returns, I

focus only in the post-announcement period, which starts 3 days after the acquisition

announcement date and ends three years after. The variables in the regression are the same used

to analyse the initial market reaction, with four additional independent variables, which are the

CAAR surrounding the announcement and the bidder’s future acquisitions variables15, included

under the Bidder-Specific Merger Momentum group, (see discussion in methodology section). The

inclusion of the CAAR, as a control variable, offers another test for the long-run reversal hypothesis,

while the other three variables consider the number and type of acquisitions made by the bidding

firms in the post-announcement period.

Despite the coefficient on the CAAR being insignificant, the coefficient on the trailing 12-month

average CAAR, the variable used as a proxy for merger momentum, is negative and statistically

significant at 5% significance level. This suggests that firms that announced an acquisition in a hot

merger market have, in the post-announcement period, a downward drift on their stock prices.

Also, the coefficient on the other variable used to analyse the intensity of merger activity, the trailing

12-month number of acquisitions, is strongly negative at 1% significance level. Once again, this

evidence suggests that acquisitions announced during waves perform worse in the long-run than

acquisitions announced at other times.

14 The results are not reported for reasons of brevity. They are similar as those reported in table 4. 15 Number of M&As in the post-announcement period, number of M&As in the post-announcement with stock and number of M&As in the post-

announcement with public target.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

22|

In what concerns to the market momentum variable, there is no evidence of reversal. The

result is similar with that found in my regression of CAAR, but contrary to the finding of Rosen

(2006), who shows that an acquisition announced during a hot stock market performs worse than

one announced in a cold stock market, evidencing that the market participants are affected by the

investor’s optimism.

The coefficients on bidder specific merger momentum variables indicate evidence of

reversal at the firm level. The CAAR of the last announcement by the bidding firm is negative and

statistically significant at 5% significance level. The number of acquisitions in the previous three

years undertaken by the firm has also a negative and statistically significant impact at 1% level on

the post-announcement long-term returns.

Consistent with the literature, the coefficient on the number of acquisitions in the post-

announcement period is strongly positive and statistically significant at 1% significance level. This

indicates that firm that make additional acquisitions in the post-announcement have a higher buy-

and-hold abnormal return.

Some of the coefficients on the control variables are in line with the literature, such as the

return on assets of the bidding firm, the log of total assets as well as the dummy variable that

considers acquisitions of private target with stock financing.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

|23

Table 5- Regression results for the BHAR as dependent variable. This table shows the results using the buy-and-hold abnormal return (BHAR) as dependent variable. The BHAR is

defined as ∏ (1 + 𝑅𝑡) − ∏ (1 + 𝑅𝑚𝑎𝑟𝑘𝑒𝑡,𝑡)𝑇𝑡=1

𝑇𝑡=1 where 𝑅𝑡 is the daily return of the firms and 𝑅𝑚𝑎𝑟𝑘𝑒𝑡,𝑡 is daily

market index return. The post-announcement window stars three days after an announcement and ends up three years

after the announcement. Only the acquisitions with three year BHAR are included. All variables are defined in Appendix

A. Heteroskedasticity robust t-statistics with standard errors clustered at year and industry level are show in

parentheses. *, ** and *** indicate statistically significant at the 10%, 5% and 1% level, respectively.

Full Sample

Coefficient t-statistics CAAR 0.3668 (1.34) Merger momentum: Trailing 12-month average CAAR -5.5703 (-2.13)** Trailing 12-month number of acquisitions/1000 -0.7686 (-6.01)*** Market momentum: Trailing 12-month return on market 0.0829 (1.48) Bidder-specific merger momentum: CAAR of the last announcement by bidding firm -0.7357 (-2.01)** Dummy that is 1 if there was an acquisition in prior 3years 0.0126 (0.34) Number of acquisitions in the last 3years -0.0327 (-2.83)*** Number of M&As in the post-announcement period 0.0340 (3.51)*** Number of M&As in the post-announcement with stock -0.0146 (-0.16) Number of M&As in the post-announcement with public target 0.0235 (0.46) Bidder-specific stock momentum: Trailing 12-month BHAR on the bidder's stock -0.0020 (-0.64)

Control Variables: Private target -0.0161 (-0.33) Subsidiary target 0.0716 (1.33) Public target with stock -0.0059 (-0.05) Private target with stock -0.2651 (-2.36)** Subsidiary target with stock -0.1247 (-0.89) Log of total assets 0.0144 (2.59)*** Bidder ROA 1.0316 (4.03)*** Bidder book-to-market 0.0326 (1.33) Bidder sales growth -0.0021 (-0.16) Diversifying acquisition 0.0056 (0.22) Observations 2,879 Adjusted R-square 0.0098

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

24|

5.2.1. Discussion

The BHAR regression results confirm the hypothesis 2, as there is evidence of reversal in

the long-run. The main measure of hot merger markets, the trailing 12-month average CAAR, is

positively correlated with the announcement returns but closely negative with the long-run return

of the bidding firms. In other words, there is evidence that acquirers are more likely to obtain higher

CAARs in period of hot merger markets but the higher abnormal announcement returns tend to

revert in the long-run, with acquirers exhibiting lower BHARs. The same arrangement is analysed

in the measure of merger waves (trailing 12-month number of acquisitions), showing that

acquisitions announced during waves are more likely to be worse, in the long-run, than those

announced at other times.

As the long-term performance exhibits a downward reverse pattern with respect to the

announcement returns, it is possible to infer that the market overreacted to the announcement of

the acquisition. Then, the results are in line with the hypothesis that merger momentum is caused

by excessive optimism from investors, putting aside the neoclassical hypothesis as it does not

predict a reversal effect in the long-run. However, this does not imply that acquisitions do not occur

as a consequence of shocks in economy, just that something else must be going as well. For

instance, it could be that the shocks result in overoptimsm from investors (Rosen, 2006).

Another result is worth observing. The CAAR regression results demonstrate a strongly

negative relationship between the bidder specific stock momentum and the market reaction to the

announcement of the acquisition, while in the BHAR regression, the coefficient on the trailing 12-

month BHAR is not statistically different from zero. As I have mentioned before, a non-positive

coefficient on this variable in the long-run may be an indication of Roll’s hypothesis. So, there is

some evidence that a portion of the gains is truncated due to bidder managerial hubris.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

|25

6. Robustness tests

In this section, I present some robustness tests for the main results of this study. First, I

delete from the analysis deals in which the acquirer announced two or more acquisitions within

eight days. This requirement avoids overlapping effects on the returns of the bidding firms across

different deals. Additionally, industry fixed effects16 are included in the regression to control the

differences on the returns across industries.

The table 6 presents the regression results for short-term announcement returns. The

findings uncovered in previous sections continue to hold. The coefficient on the merger momentum

variable is positive and statistically significant at 10% significance level. The number of acquisitions

in the prior 12-month, the measure of merger waves, has also a positive and statistically significant

coefficient. Although with a lower significance level, both the measures of merger activity continue

to be positively correlated with the market reaction to an acquisition announcement.

At the firm level, the coefficient used as a proxy for bidder merger momentum is positive

and (weakly) significant. So, with a lower significance level when compared to the values shown in

table 4, the CAAR of the bidder’s last acquisition continues to affect positively the initial market

reaction to an acquisition. Overall, the rest of the coefficients on the other variables remain similar

to the coefficients on the main CAAR regression.

16 Industry fixed effects are considered by including industries dummies based on 1-digitc SIC code.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

26|

Table 6- Regression results for the CAAR as dependent variable: robustness test This table shows the cumulative abnormal announcement returns (CAARs) of acquirers over the 2002 and 2012

period. The dependent variable, the CAAR, is calculated for the five days (-2; +2) surrounding the announcement day

(day 0) of the acquisition. Abnormal returns are computed using the market model approach. All variables are defined

in Appendix A. Heteroskedasticity robust t-statistics are show in parentheses. *, ** and *** indicate statistically

significant at the 10%, 5% and 1% level, respectively. Industry dummies are included in the regression but not shown

in the table.

Full Sample Coefficient t-statistics Merger momentum: Trailing 12-month average CAAR 0.3698 (1.85)* Trailing 12-month number of acquisitions/1000 0.0159 (1.67)* Market momentum: Trailing 12-month return on market -0.0015 (-0.34) Bidder-specific merger momentum: CAAR of the last announcement by bidding firm 0.0601 (1.70)* Dummy that is 1 if there was an acquisition in prior 3years -0.0047 (-1.65)* Number of acquisitions in the last 3years -0.0010 (-1.31) Bidder-specific stock momentum: Trailing 12-month BHAR on the bidder's stock -0.0022 (-4.21)*** Control variables: Private target 0.0207 (4.83)*** Subsidiary target 0.0228 (5.25)*** Public target with stock -0.0060 (-0.76) Private target with stock -0.0008 (-0.05) Subsidiary target with stock -0.0008 (-0.07) Log of total assets -0.0012 (-3.11)*** Bidder ROA -0.0367 (-1.90)* Bidder book-to-market -0.0000 (-0.09) Bidder sales growth 0.0001 (0.08) Diversifying acquisition -0.0001 (-0.06) Observations 2,832 Adjusted R-square 0.0753

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

|27

Table 7 shows the same type of robustness check for the regression of BHAR. The

coefficient on the merger momentum variable, the trailing 12-month average CAAR, is negative

and still statistically significant. The conclusions are the same, that is, firms that announced an

acquisition in a hot merger market have a worse performance in the long-run, all else equal. Also,

the coefficient on the number of acquisitions in the prior 12-months is negative and strongly

significant, which provides some evidence that acquisitions announced during waves are worse

than those announced at other times.

Contrary to the result found in the main BHAR regression, there is no strong evidence of

reversal in regarding to the bidder specific merger momentum. The coefficient on the CAAR of the

bidder’s last announcement is not statistically different from zero. However, the coefficient on the

number of acquisitions in the prior three years undertaken by the firm is negative and statistically

significant at 1% level, which indicates that the number of previous acquisitions has a negative

impact in the BHAR of the bidding firm. The signals of the other coefficients are consistent with the

results found previously.

Overall, the results in both the short and long-run regressions are robust when I consider

the industry fixed effect and the exclusion of multiple acquisitions of the same bidding firms that

were announced very close together.

Announcement returns and post-merger performance: evidence of M&A momentum in the European Union market

28|

Table 7- Regression results for the BHAR as dependent variable: robustness test This table shows the results using the buy-and-hold abnormal return (BHAR) as dependent variable. The BHAR is

defined as ∏ (1 + 𝑅𝑡) − ∏ (1 + 𝑅𝑚𝑎𝑟𝑘𝑒𝑡,𝑡)𝑇𝑡=1

𝑇𝑡=1 where 𝑅𝑡 is the daily return of the firms and 𝑅𝑚𝑎𝑟𝑘𝑒𝑡,𝑡 is daily

market index return. The post-announcement window stars three days after an announcement and ends up three years

after the announcement. Only the acquisitions with three year BHAR are included. All variables are defined in Appendix

A. Heteroskedasticity robust t-statistics are show in parentheses. *, ** and *** indicate statistically significant at the

10%, 5% and 1% level, respectively. Industry dummies are included in the regression but not shown in the table.

Full Sample