industry report: restaurant review - cfra report_final.pdfpage 11 of this report for additional cfra...

TRANSCRIPT

1 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

Restaurant Review: Scrutinizing Same Store Sales SUMMARY

Same-Store Sales (SSS) is a key metric used by investors to evaluate the performance of restaurants and other retailers. As an unaudited non-GAAP metric, however (with no universal definition), SSS is subject to a higher degree of management discre-tion than most GAAP metrics. It is helpful, then, to appreciate the varying definitions of SSS employed by different companies, and -- more importantly -- it is vital for investors to recognize when a company makes a change to its own SSS definition. For example, PNRA changed its definition of SSS beginning in 2010 to restaurants that have been open 12 months as opposed to 18 months. While management stated this would negatively impact reported SSS, this was not the case in the 3/10 quarter

when the change was made. Further analysis is hindered as PNRA stopped disclosing the impact in subsequent quarters.

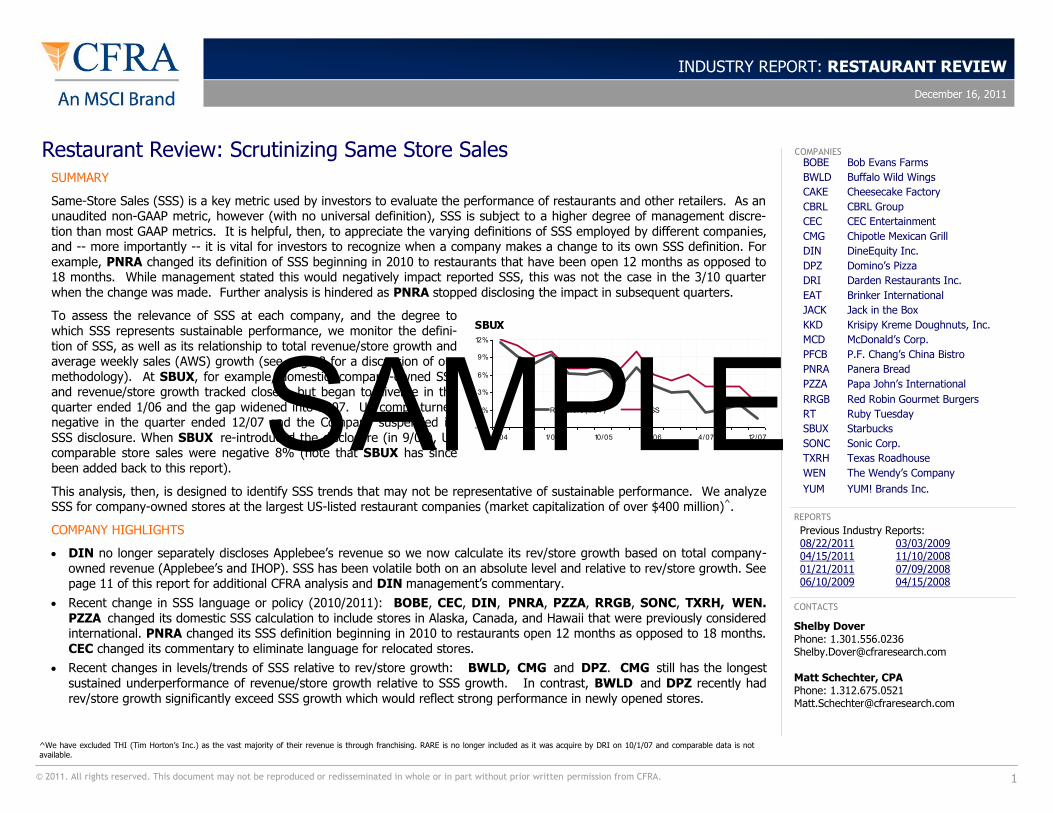

To assess the relevance of SSS at each company, and the degree to which SSS represents sustainable performance, we monitor the defini-tion of SSS, as well as its relationship to total revenue/store growth and average weekly sales (AWS) growth (see page 2 for a discussion of our methodology). At SBUX, for example, domestic, company-owned SSS and revenue/store growth tracked closely, but began to diverge in the quarter ended 1/06 and the gap widened into 2007. US comps turned negative in the quarter ended 12/07 and the Company suspended its SSS disclosure. When SBUX re-introduced the disclosure (in 9/08), US comparable store sales were negative 8% (note that SBUX has since been added back to this report).

This analysis, then, is designed to identify SSS trends that may not be representative of sustainable performance. We analyze SSS for company-owned stores at the largest US-listed restaurant companies (market capitalization of over $400 million)^.

COMPANY HIGHLIGHTS

DIN no longer separately discloses Applebee’s revenue so we now calculate its rev/store growth based on total company-owned revenue (Applebee’s and IHOP). SSS has been volatile both on an absolute level and relative to rev/store growth. See page 11 of this report for additional CFRA analysis and DIN management’s commentary.

Recent change in SSS language or policy (2010/2011): BOBE, CEC, DIN, PNRA, PZZA, RRGB, SONC, TXRH, WEN. PZZA changed its domestic SSS calculation to include stores in Alaska, Canada, and Hawaii that were previously considered international. PNRA changed its SSS definition beginning in 2010 to restaurants open 12 months as opposed to 18 months. CEC changed its commentary to eliminate language for relocated stores.

Recent changes in levels/trends of SSS relative to rev/store growth: BWLD, CMG and DPZ. CMG still has the longest sustained underperformance of revenue/store growth relative to SSS growth. In contrast, BWLD and DPZ recently had rev/store growth significantly exceed SSS growth which would reflect strong performance in newly opened stores.

CONTACTS

COMPANIES

REPORTS

Previous Industry Reports: 08/22/2011 03/03/2009 04/15/2011 11/10/2008 01/21/2011 07/09/2008 06/10/2009 04/15/2008

BOBE Bob Evans Farms

BWLD Buffalo Wild Wings

CAKE Cheesecake Factory

CBRL CBRL Group

CEC CEC Entertainment

CMG Chipotle Mexican Grill

DIN DineEquity Inc.

DPZ Domino’s Pizza

DRI Darden Restaurants Inc.

EAT Brinker International

JACK Jack in the Box

KKD Krisipy Kreme Doughnuts, Inc.

MCD McDonald’s Corp.

PFCB P.F. Chang’s China Bistro

PNRA Panera Bread

PZZA Papa John’s International

RRGB Red Robin Gourmet Burgers

RT Ruby Tuesday

SBUX Starbucks

SONC Sonic Corp.

TXRH Texas Roadhouse

WEN The Wendy’s Company

YUM YUM! Brands Inc.

^We have excluded THI (Tim Horton’s Inc.) as the vast majority of their revenue is through franchising. RARE is no longer included as it was acquire by DRI on 10/1/07 and comparable data is not available.

Shelby Dover Phone: 1.301.556.0236 [email protected] Matt Schechter, CPA Phone: 1.312.675.0521 [email protected]

INDUSTRY REPORT: RESTAURANT REVIEW

December 16, 2011

SBUX

-3%

0%

3%

6%

9%

12%

12/074/077/0610/051/053/04

Rev/Store (YoY) SSSSAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

2 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

For each company surveyed, we analyze:

The level of Same-Store Sales relative to Revenue per Store Growth

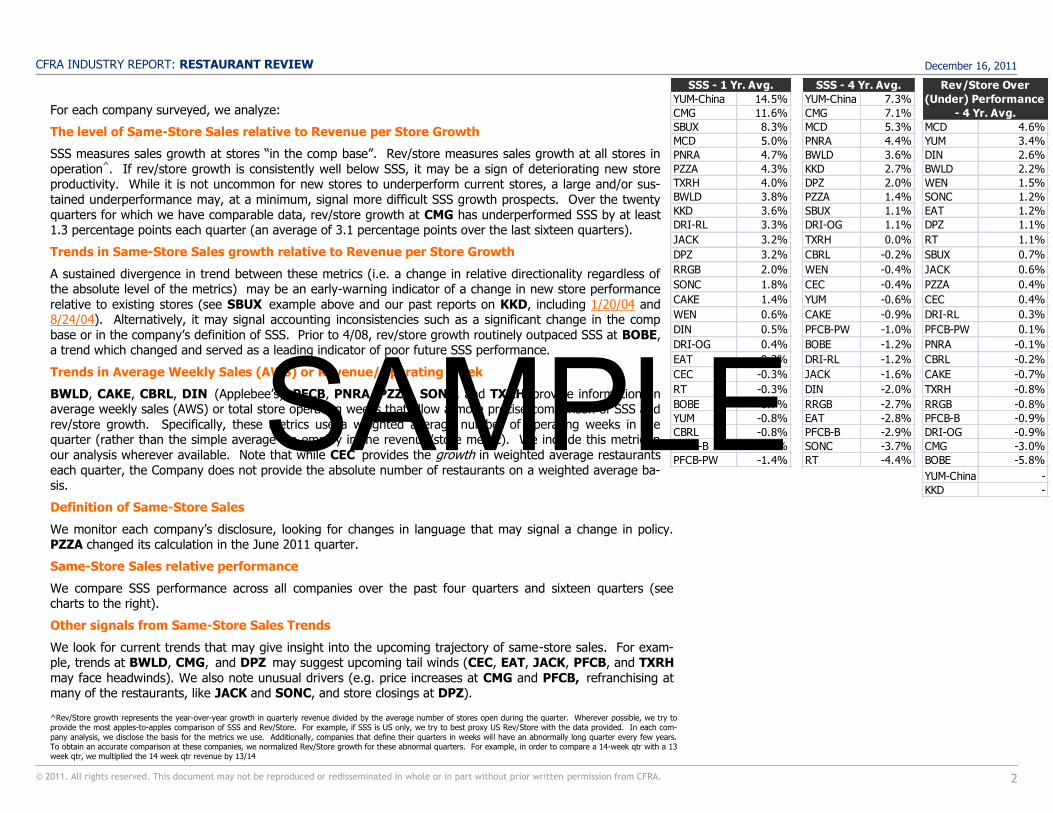

SSS measures sales growth at stores ―in the comp base‖. Rev/store measures sales growth at all stores in operation^. If rev/store growth is consistently well below SSS, it may be a sign of deteriorating new store productivity. While it is not uncommon for new stores to underperform current stores, a large and/or sus-tained underperformance may, at a minimum, signal more difficult SSS growth prospects. Over the twenty quarters for which we have comparable data, rev/store growth at CMG has underperformed SSS by at least 1.3 percentage points each quarter (an average of 3.1 percentage points over the last sixteen quarters).

Trends in Same-Store Sales growth relative to Revenue per Store Growth

A sustained divergence in trend between these metrics (i.e. a change in relative directionality regardless of the absolute level of the metrics) may be an early-warning indicator of a change in new store performance relative to existing stores (see SBUX example above and our past reports on KKD, including 1/20/04 and 8/24/04). Alternatively, it may signal accounting inconsistencies such as a significant change in the comp base or in the company’s definition of SSS. Prior to 4/08, rev/store growth routinely outpaced SSS at BOBE, a trend which changed and served as a leading indicator of poor future SSS performance.

Trends in Average Weekly Sales (AWS) or Revenue/Operating Week

BWLD, CAKE, CBRL, DIN (Applebee’s), PFCB, PNRA, PZZA, SONC, and TXRH provide information on average weekly sales (AWS) or total store operating weeks that allow a more precise comparison of SSS and rev/store growth. Specifically, these metrics use a weighted average number of operating weeks in the quarter (rather than the simple average we employ in the revenue/store metric). We include this metric in our analysis wherever available. Note that while CEC provides the growth in weighted average restaurants each quarter, the Company does not provide the absolute number of restaurants on a weighted average ba-sis.

Definition of Same-Store Sales

We monitor each company’s disclosure, looking for changes in language that may signal a change in policy. PZZA changed its calculation in the June 2011 quarter.

Same-Store Sales relative performance

We compare SSS performance across all companies over the past four quarters and sixteen quarters (see charts to the right).

Other signals from Same-Store Sales Trends

We look for current trends that may give insight into the upcoming trajectory of same-store sales. For exam-ple, trends at BWLD, CMG, and DPZ may suggest upcoming tail winds (CEC, EAT, JACK, PFCB, and TXRH may face headwinds). We also note unusual drivers (e.g. price increases at CMG and PFCB, refranchising at many of the restaurants, like JACK and SONC, and store closings at DPZ).

^Rev/Store growth represents the year-over-year growth in quarterly revenue divided by the average number of stores open during the quarter. Wherever possible, we try to provide the most apples-to-apples comparison of SSS and Rev/Store. For example, if SSS is US only, we try to best proxy US Rev/Store with the data provided. In each com-

pany analysis, we disclose the basis for the metrics we use. Additionally, companies that define their quarters in weeks will have an abnormally long quarter every few years. To obtain an accurate comparison at these companies, we normalized Rev/Store growth for these abnormal quarters. For example, in order to compare a 14-week qtr with a 13 week qtr, we multiplied the 14 week qtr revenue by 13/14

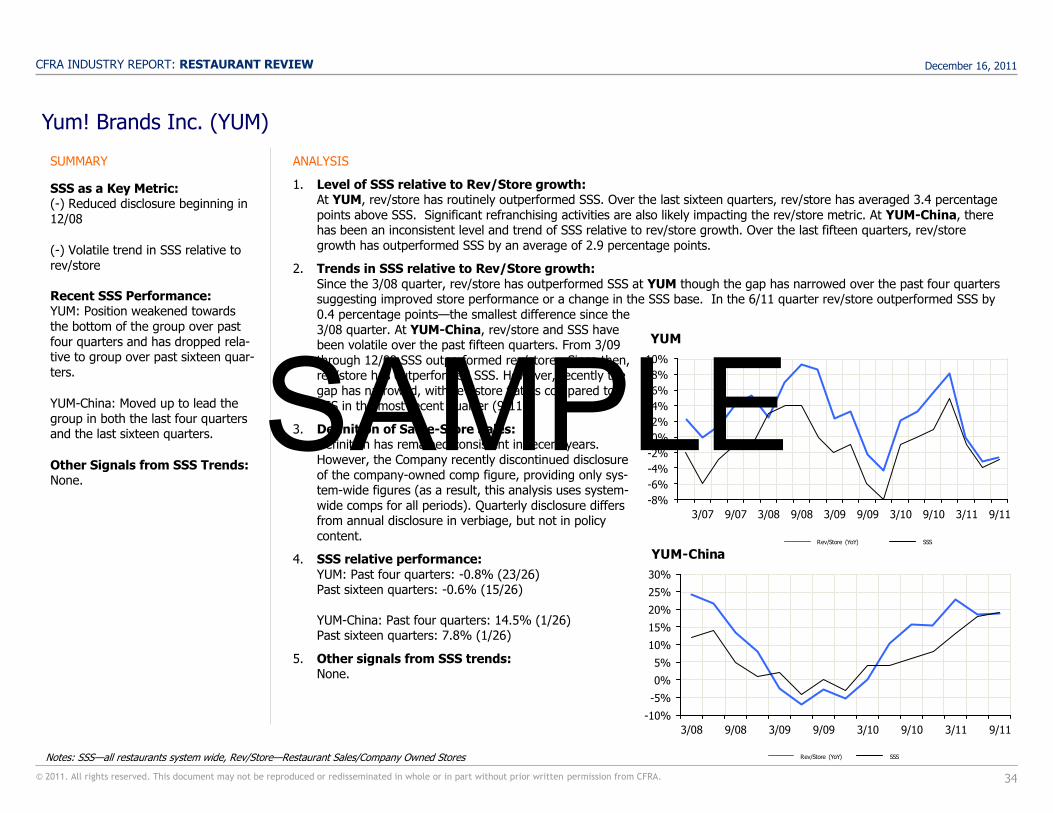

YUM-China 14.5%

CMG 11.6%

SBUX 8.3%

MCD 5.0%

PNRA 4.7%

PZZA 4.3%

TXRH 4.0%

BWLD 3.8%

KKD 3.6%

DRI-RL 3.3%

JACK 3.2%

DPZ 3.2%

RRGB 2.0%

SONC 1.8%

CAKE 1.4%

WEN 0.6%

DIN 0.5%

DRI-OG 0.4%

EAT 0.3%

CEC -0.3%

RT -0.3%

BOBE -0.7%

YUM -0.8%

CBRL -0.8%

PFCB-B -1.4%

PFCB-PW -1.4%

SSS - 1 Yr. Avg.

YUM-China 7.3%

CMG 7.1%

MCD 5.3%

PNRA 4.4%

BWLD 3.6%

KKD 2.7%

DPZ 2.0%

PZZA 1.4%

SBUX 1.1%

DRI-OG 1.1%

TXRH 0.0%

CBRL -0.2%

WEN -0.4%

CEC -0.4%

YUM -0.6%

CAKE -0.9%

PFCB-PW -1.0%

BOBE -1.2%

DRI-RL -1.2%

JACK -1.6%

DIN -2.0%

RRGB -2.7%

EAT -2.8%

PFCB-B -2.9%

SONC -3.7%

RT -4.4%

SSS - 4 Yr. Avg.

MCD 4.6%

YUM 3.4%

DIN 2.6%

BWLD 2.2%

WEN 1.5%

SONC 1.2%

EAT 1.2%

DPZ 1.1%

RT 1.1%

SBUX 0.7%

JACK 0.6%

PZZA 0.4%

CEC 0.4%

DRI-RL 0.3%

PFCB-PW 0.1%

PNRA -0.1%

CBRL -0.2%

CAKE -0.7%

TXRH -0.8%

RRGB -0.8%

PFCB-B -0.9%

DRI-OG -0.9%

CMG -3.0%

BOBE -5.8%

YUM-China -

KKD -

Rev/Store Over

(Under) Performance

- 4 Yr. Avg.

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

3 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

Bob Evans Farms Inc. (BOBE)

ANALYSIS

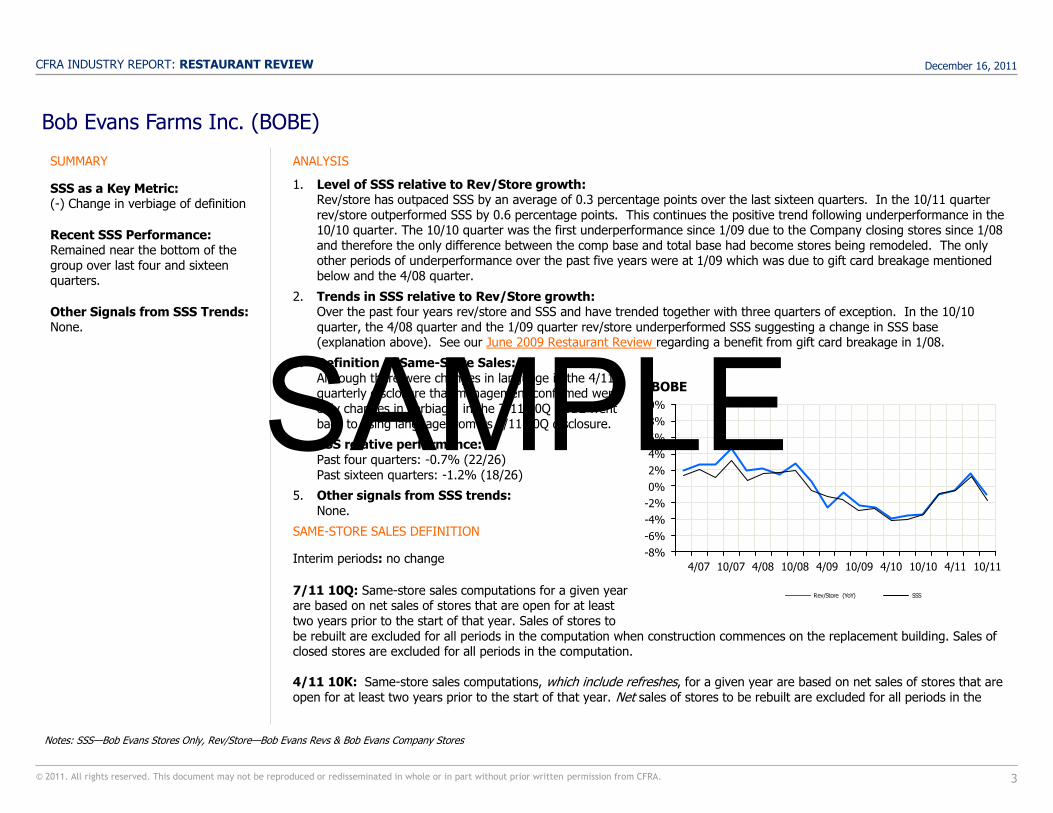

1. Level of SSS relative to Rev/Store growth: Rev/store has outpaced SSS by an average of 0.3 percentage points over the last sixteen quarters. In the 10/11 quarter rev/store outperformed SSS by 0.6 percentage points. This continues the positive trend following underperformance in the 10/10 quarter. The 10/10 quarter was the first underperformance since 1/09 due to the Company closing stores since 1/08 and therefore the only difference between the comp base and total base had become stores being remodeled. The only other periods of underperformance over the past five years were at 1/09 which was due to gift card breakage mentioned below and the 4/08 quarter.

2. Trends in SSS relative to Rev/Store growth: Over the past four years rev/store and SSS and have trended together with three quarters of exception. In the 10/10 quarter, the 4/08 quarter and the 1/09 quarter rev/store underperformed SSS suggesting a change in SSS base (explanation above). See our June 2009 Restaurant Review regarding a benefit from gift card breakage in 1/08.

3. Definition of Same-Store Sales: Although there were changes in language in the 4/11 quarterly disclosure that management confirmed were only changes in verbiage, in the 7/11 10Q BOBE went back to using language from its 1/11 10Q disclosure.

4. SSS relative performance: Past four quarters: -0.7% (22/26) Past sixteen quarters: -1.2% (18/26)

5. Other signals from SSS trends: None.

SAME-STORE SALES DEFINITION

Interim periods: no change

7/11 10Q: Same-store sales computations for a given year are based on net sales of stores that are open for at least two years prior to the start of that year. Sales of stores to be rebuilt are excluded for all periods in the computation when construction commences on the replacement building. Sales of closed stores are excluded for all periods in the computation. 4/11 10K: Same-store sales computations, which include refreshes, for a given year are based on net sales of stores that are open for at least two years prior to the start of that year. Net sales of stores to be rebuilt are excluded for all periods in the

SUMMARY

SSS as a Key Metric: (-) Change in verbiage of definition

Recent SSS Performance: Remained near the bottom of the group over last four and sixteen quarters.

Other Signals from SSS Trends: None.

Notes: SSS—Bob Evans Stores Only, Rev/Store—Bob Evans Revs & Bob Evans Company Stores

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

10/114/1110/104/1010/094/0910/084/0810/074/07

BOBE

Rev/Store (YoY) SSS

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

4 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

Bob Evans Farms Inc. (BOBE)

same-store sales computation when construction commences on the replacement building. Net sales of closed stores are ex-cluded for all periods in the same-store sales computation. [emphasis added by CFRA]

Interim periods: no change

4/04 10K: Same-store sales computations for a given year are based on net sales of stores that are open for at least two years prior to the start of that year. Sales of stores to be rebuilt are excluded for all periods in the computation when construc-tion commences on the replacement building. Sales of closed stores are excluded for all periods in the computation.

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

5 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

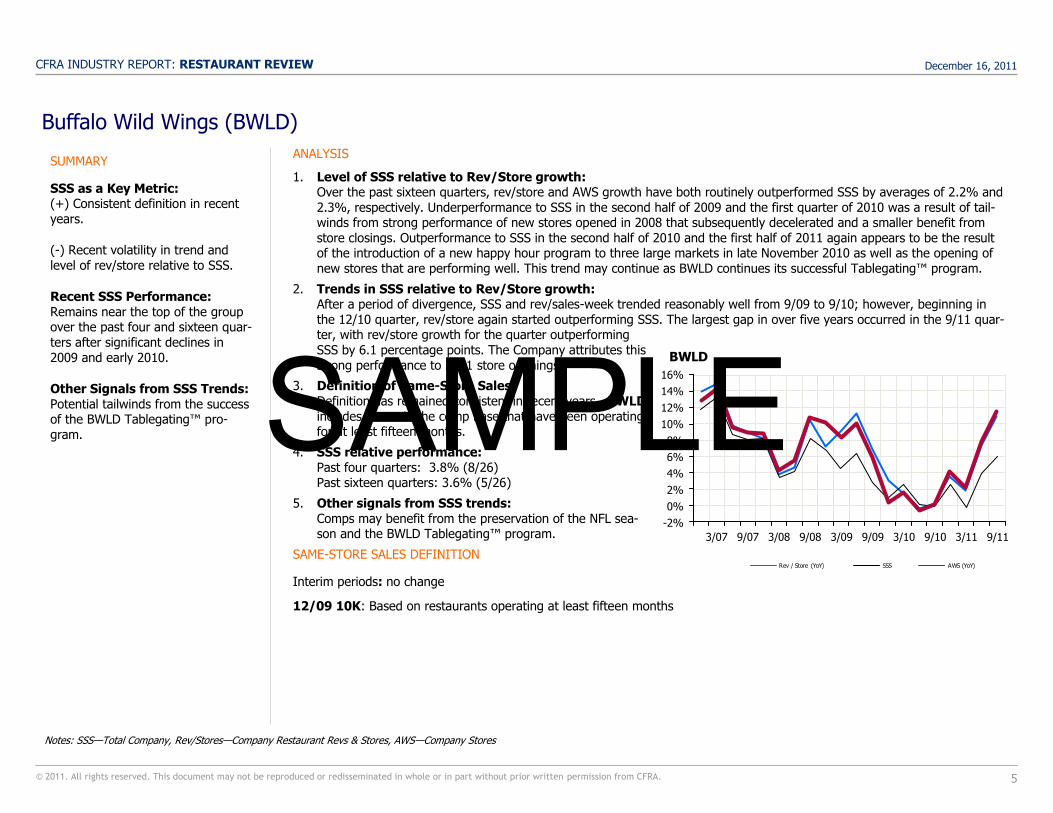

Buffalo Wild Wings (BWLD)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: Over the past sixteen quarters, rev/store and AWS growth have both routinely outperformed SSS by averages of 2.2% and 2.3%, respectively. Underperformance to SSS in the second half of 2009 and the first quarter of 2010 was a result of tail-winds from strong performance of new stores opened in 2008 that subsequently decelerated and a smaller benefit from store closings. Outperformance to SSS in the second half of 2010 and the first half of 2011 again appears to be the result of the introduction of a new happy hour program to three large markets in late November 2010 as well as the opening of new stores that are performing well. This trend may continue as BWLD continues its successful Tablegating™ program.

2. Trends in SSS relative to Rev/Store growth: After a period of divergence, SSS and rev/sales-week trended reasonably well from 9/09 to 9/10; however, beginning in the 12/10 quarter, rev/store again started outperforming SSS. The largest gap in over five years occurred in the 9/11 quar-ter, with rev/store growth for the quarter outperforming SSS by 6.1 percentage points. The Company attributes this strong performance to 2011 store openings.

3. Definition of Same-Store Sales: Definition has remained consistent in recent years. BWLD includes stores in the comp base that have been operating for at least fifteen months.

4. SSS relative performance: Past four quarters: 3.8% (8/26) Past sixteen quarters: 3.6% (5/26)

5. Other signals from SSS trends: Comps may benefit from the preservation of the NFL sea-son and the BWLD Tablegating™ program.

SAME-STORE SALES DEFINITION

Interim periods: no change

12/09 10K: Based on restaurants operating at least fifteen months

SUMMARY

SSS as a Key Metric: (+) Consistent definition in recent years.

(-) Recent volatility in trend and level of rev/store relative to SSS.

Recent SSS Performance: Remains near the top of the group over the past four and sixteen quar-ters after significant declines in 2009 and early 2010.

Other Signals from SSS Trends: Potential tailwinds from the success of the BWLD Tablegating™ pro-gram.

Notes: SSS—Total Company, Rev/Stores—Company Restaurant Revs & Stores, AWS—Company Stores

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

9/113/119/103/109/093/099/083/089/073/07

BWLD

Rev / Store (YoY) SSS AWS (YoY)

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

6 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

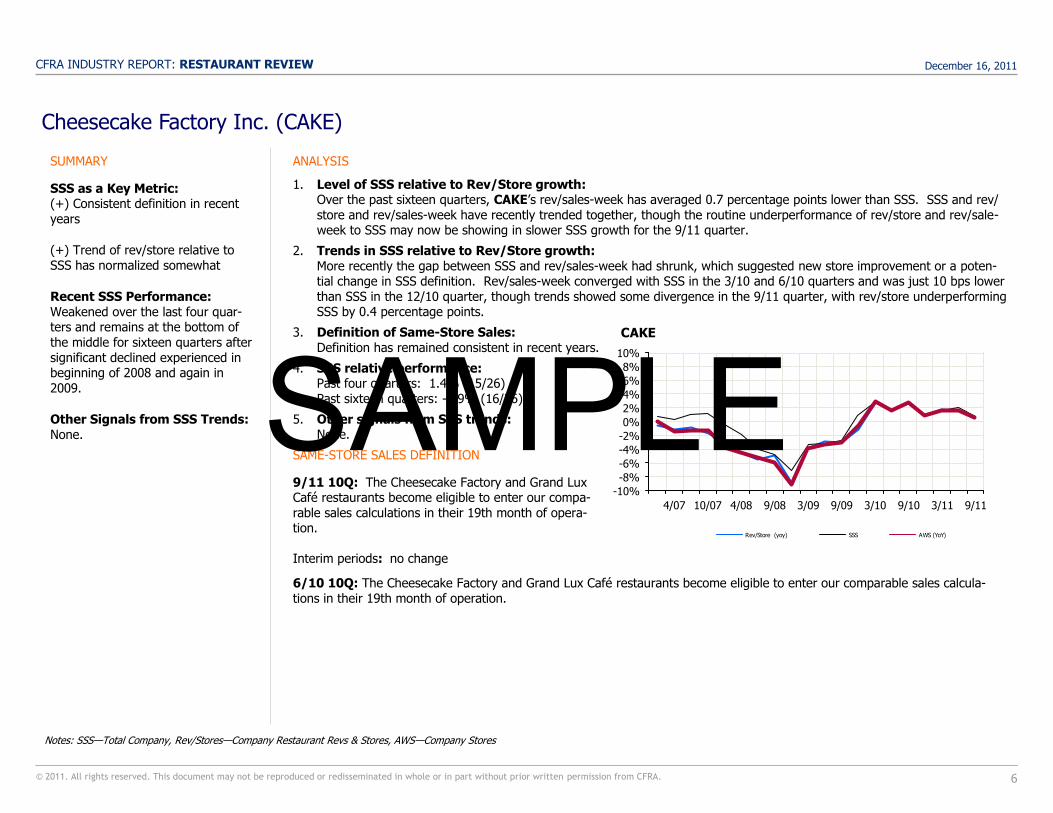

Cheesecake Factory Inc. (CAKE)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: Over the past sixteen quarters, CAKE’s rev/sales-week has averaged 0.7 percentage points lower than SSS. SSS and rev/store and rev/sales-week have recently trended together, though the routine underperformance of rev/store and rev/sale-week to SSS may now be showing in slower SSS growth for the 9/11 quarter.

2. Trends in SSS relative to Rev/Store growth: More recently the gap between SSS and rev/sales-week had shrunk, which suggested new store improvement or a poten-tial change in SSS definition. Rev/sales-week converged with SSS in the 3/10 and 6/10 quarters and was just 10 bps lower than SSS in the 12/10 quarter, though trends showed some divergence in the 9/11 quarter, with rev/store underperforming SSS by 0.4 percentage points.

3. Definition of Same-Store Sales: Definition has remained consistent in recent years.

4. SSS relative performance: Past four quarters: 1.4% (15/26) Past sixteen quarters: -0.9% (16/26)

5. Other signals from SSS trends: None.

SAME-STORE SALES DEFINITION

9/11 10Q: The Cheesecake Factory and Grand Lux Café restaurants become eligible to enter our compa-rable sales calculations in their 19th month of opera-tion. Interim periods: no change

6/10 10Q: The Cheesecake Factory and Grand Lux Café restaurants become eligible to enter our comparable sales calcula-tions in their 19th month of operation.

SUMMARY

SSS as a Key Metric: (+) Consistent definition in recent years

(+) Trend of rev/store relative to SSS has normalized somewhat

Recent SSS Performance: Weakened over the last four quar-ters and remains at the bottom of the middle for sixteen quarters after significant declined experienced in beginning of 2008 and again in 2009.

Other Signals from SSS Trends: None.

Notes: SSS—Total Company, Rev/Stores—Company Restaurant Revs & Stores, AWS—Company Stores

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

9/113/119/103/109/093/099/084/0810/074/07

CAKE

Rev/Store (yoy) SSS AWS (YoY)

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

7 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

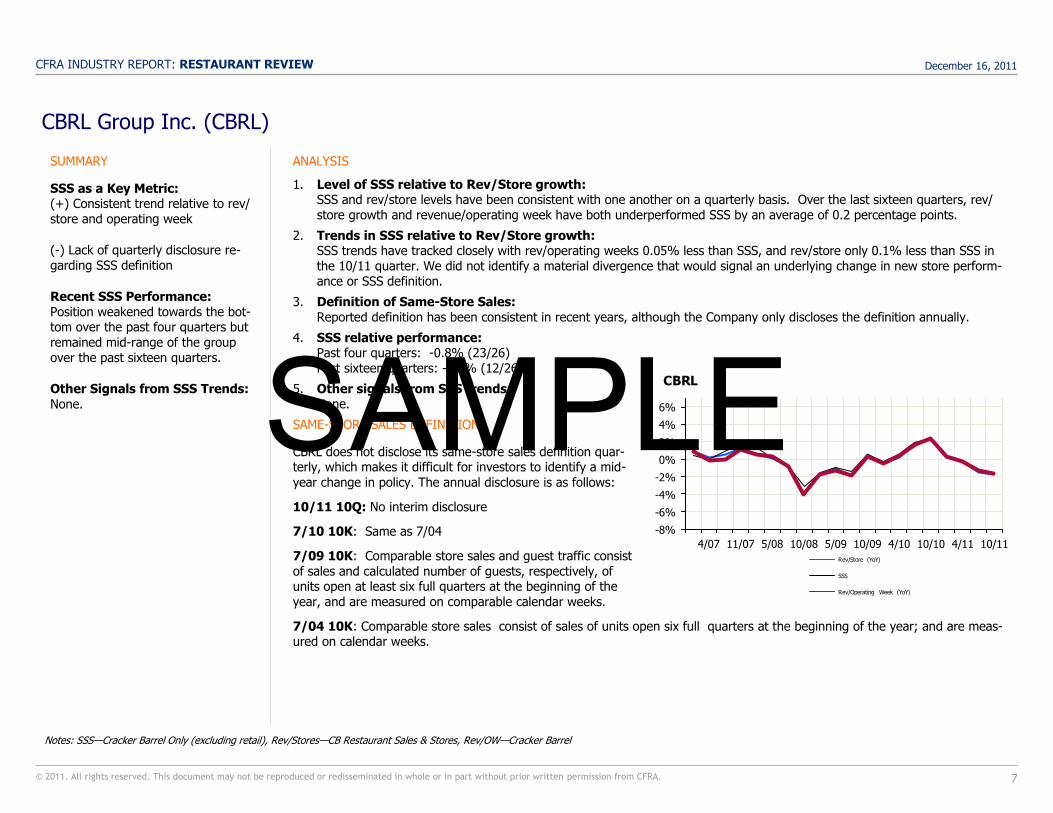

CBRL Group Inc. (CBRL)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: SSS and rev/store levels have been consistent with one another on a quarterly basis. Over the last sixteen quarters, rev/store growth and revenue/operating week have both underperformed SSS by an average of 0.2 percentage points.

2. Trends in SSS relative to Rev/Store growth: SSS trends have tracked closely with rev/operating weeks 0.05% less than SSS, and rev/store only 0.1% less than SSS in the 10/11 quarter. We did not identify a material divergence that would signal an underlying change in new store perform-ance or SSS definition.

3. Definition of Same-Store Sales: Reported definition has been consistent in recent years, although the Company only discloses the definition annually.

4. SSS relative performance: Past four quarters: -0.8% (23/26) Past sixteen quarters: -0.2% (12/26)

5. Other signals from SSS trends: None.

SAME-STORE SALES DEFINITION

CBRL does not disclose its same-store sales definition quar-terly, which makes it difficult for investors to identify a mid-year change in policy. The annual disclosure is as follows:

10/11 10Q: No interim disclosure

7/10 10K: Same as 7/04

7/09 10K: Comparable store sales and guest traffic consist of sales and calculated number of guests, respectively, of units open at least six full quarters at the beginning of the year, and are measured on comparable calendar weeks.

7/04 10K: Comparable store sales consist of sales of units open six full quarters at the beginning of the year; and are meas-ured on calendar weeks.

SUMMARY

SSS as a Key Metric: (+) Consistent trend relative to rev/store and operating week

(-) Lack of quarterly disclosure re-garding SSS definition

Recent SSS Performance: Position weakened towards the bot-tom over the past four quarters but remained mid-range of the group over the past sixteen quarters.

Other Signals from SSS Trends: None.

Notes: SSS—Cracker Barrel Only (excluding retail), Rev/Stores—CB Restaurant Sales & Stores, Rev/OW—Cracker Barrel

-8%

-6%

-4%

-2%

0%

2%

4%

6%

10/114/1110/104/1010/095/0910/085/0811/074/07

CBRL

Rev/Store (YoY)

SSS

Rev/Operating Week (YoY)

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

8 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

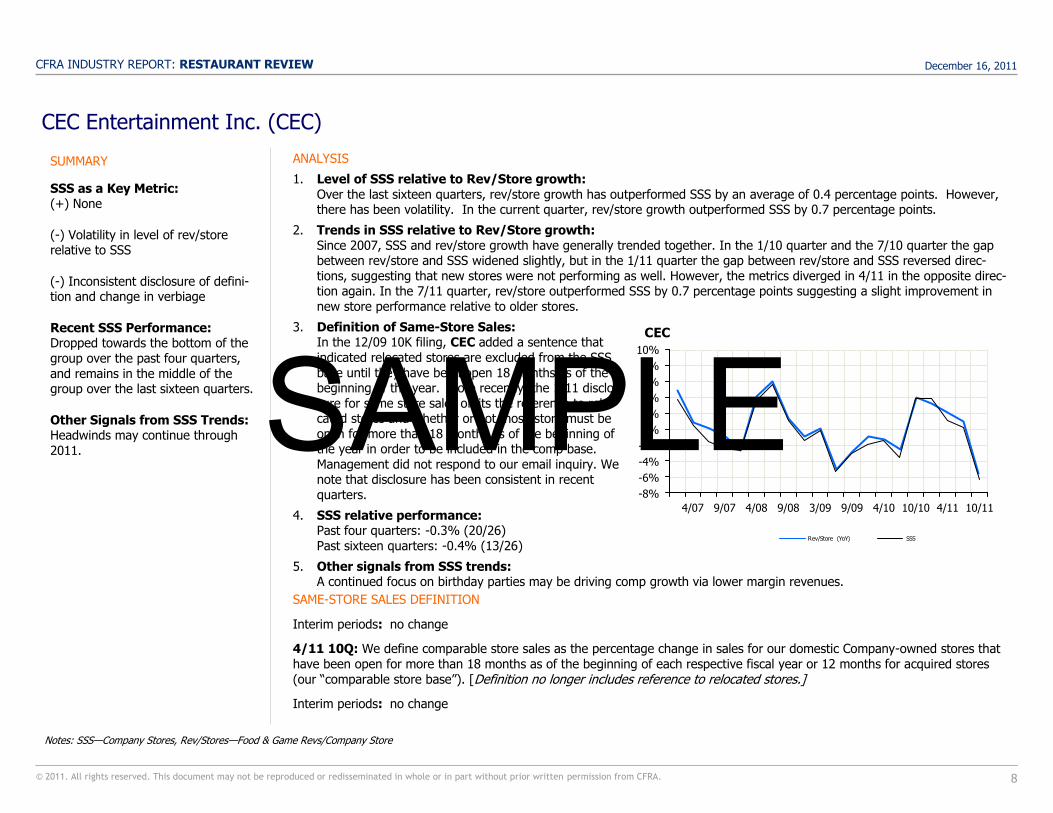

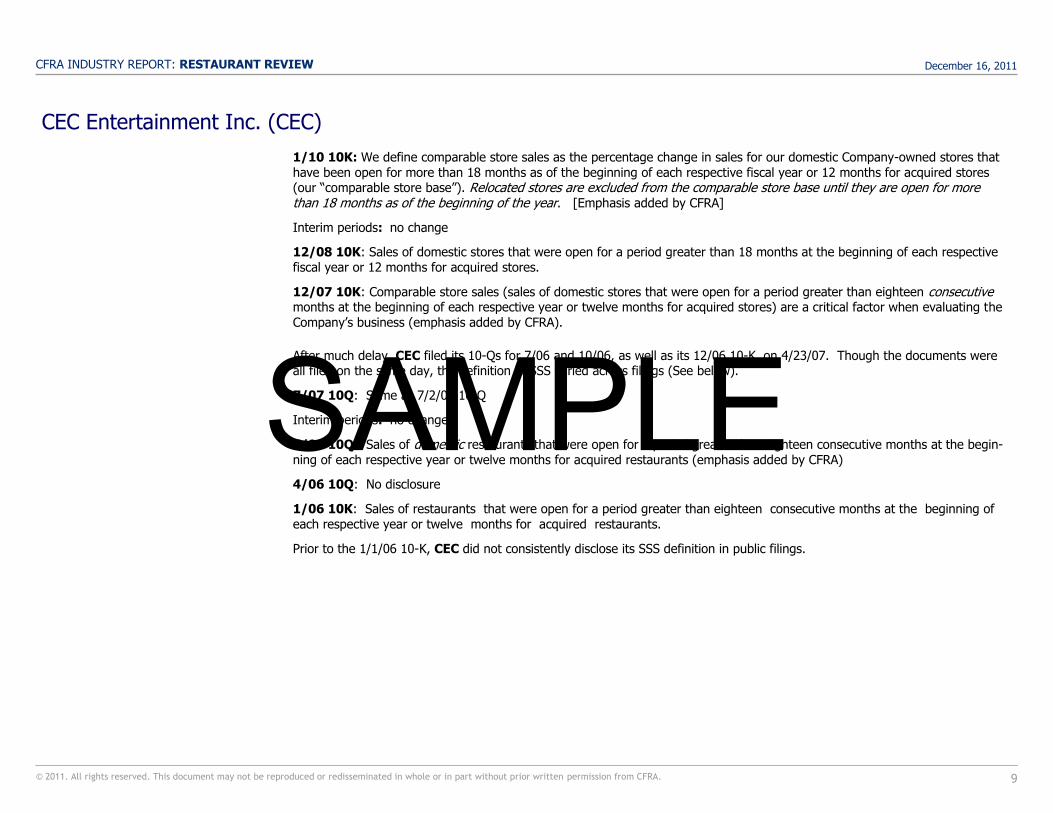

CEC Entertainment Inc. (CEC)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: Over the last sixteen quarters, rev/store growth has outperformed SSS by an average of 0.4 percentage points. However, there has been volatility. In the current quarter, rev/store growth outperformed SSS by 0.7 percentage points.

2. Trends in SSS relative to Rev/Store growth: Since 2007, SSS and rev/store growth have generally trended together. In the 1/10 quarter and the 7/10 quarter the gap between rev/store and SSS widened slightly, but in the 1/11 quarter the gap between rev/store and SSS reversed direc-tions, suggesting that new stores were not performing as well. However, the metrics diverged in 4/11 in the opposite direc-tion again. In the 7/11 quarter, rev/store outperformed SSS by 0.7 percentage points suggesting a slight improvement in new store performance relative to older stores.

3. Definition of Same-Store Sales: In the 12/09 10K filing, CEC added a sentence that indicated relocated stores are excluded from the SSS base until they have been open 18 months as of the beginning of the year. More recently, the 1/11 disclo-sure for same store sales omits the reference to relo-cated stores and whether or not those store must be open for more than 18 months as of the beginning of the year in order to be included in the comp base. Management did not respond to our email inquiry. We note that disclosure has been consistent in recent quarters.

4. SSS relative performance: Past four quarters: -0.3% (20/26) Past sixteen quarters: -0.4% (13/26)

5. Other signals from SSS trends: A continued focus on birthday parties may be driving comp growth via lower margin revenues.

SAME-STORE SALES DEFINITION

Interim periods: no change

4/11 10Q: We define comparable store sales as the percentage change in sales for our domestic Company-owned stores that have been open for more than 18 months as of the beginning of each respective fiscal year or 12 months for acquired stores (our ―comparable store base‖). [Definition no longer includes reference to relocated stores.]

Interim periods: no change

SUMMARY

SSS as a Key Metric: (+) None

(-) Volatility in level of rev/store relative to SSS

(-) Inconsistent disclosure of defini-tion and change in verbiage

Recent SSS Performance: Dropped towards the bottom of the group over the past four quarters, and remains in the middle of the group over the last sixteen quarters.

Other Signals from SSS Trends: Headwinds may continue through 2011.

Notes: SSS—Company Stores, Rev/Stores—Food & Game Revs/Company Store

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

10/114/1110/104/109/093/099/084/089/074/07

CEC

Rev/Store (YoY) SSS

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

9 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

CEC Entertainment Inc. (CEC)

1/10 10K: We define comparable store sales as the percentage change in sales for our domestic Company-owned stores that have been open for more than 18 months as of the beginning of each respective fiscal year or 12 months for acquired stores (our ―comparable store base‖). Relocated stores are excluded from the comparable store base until they are open for more than 18 months as of the beginning of the year. [Emphasis added by CFRA]

Interim periods: no change

12/08 10K: Sales of domestic stores that were open for a period greater than 18 months at the beginning of each respective fiscal year or 12 months for acquired stores.

12/07 10K: Comparable store sales (sales of domestic stores that were open for a period greater than eighteen consecutive months at the beginning of each respective year or twelve months for acquired stores) are a critical factor when evaluating the Company’s business (emphasis added by CFRA).

After much delay, CEC filed its 10-Qs for 7/06 and 10/06, as well as its 12/06 10-K, on 4/23/07. Though the documents were all filed on the same day, the definition of SSS varied across filings (See below).

7/07 10Q: Same as 7/2/06 10-Q

Interim periods: no change

7/06 10Q: Sales of domestic restaurants that were open for a period greater than eighteen consecutive months at the begin-ning of each respective year or twelve months for acquired restaurants (emphasis added by CFRA)

4/06 10Q: No disclosure

1/06 10K: Sales of restaurants that were open for a period greater than eighteen consecutive months at the beginning of each respective year or twelve months for acquired restaurants.

Prior to the 1/1/06 10-K, CEC did not consistently disclose its SSS definition in public filings.

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

10 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

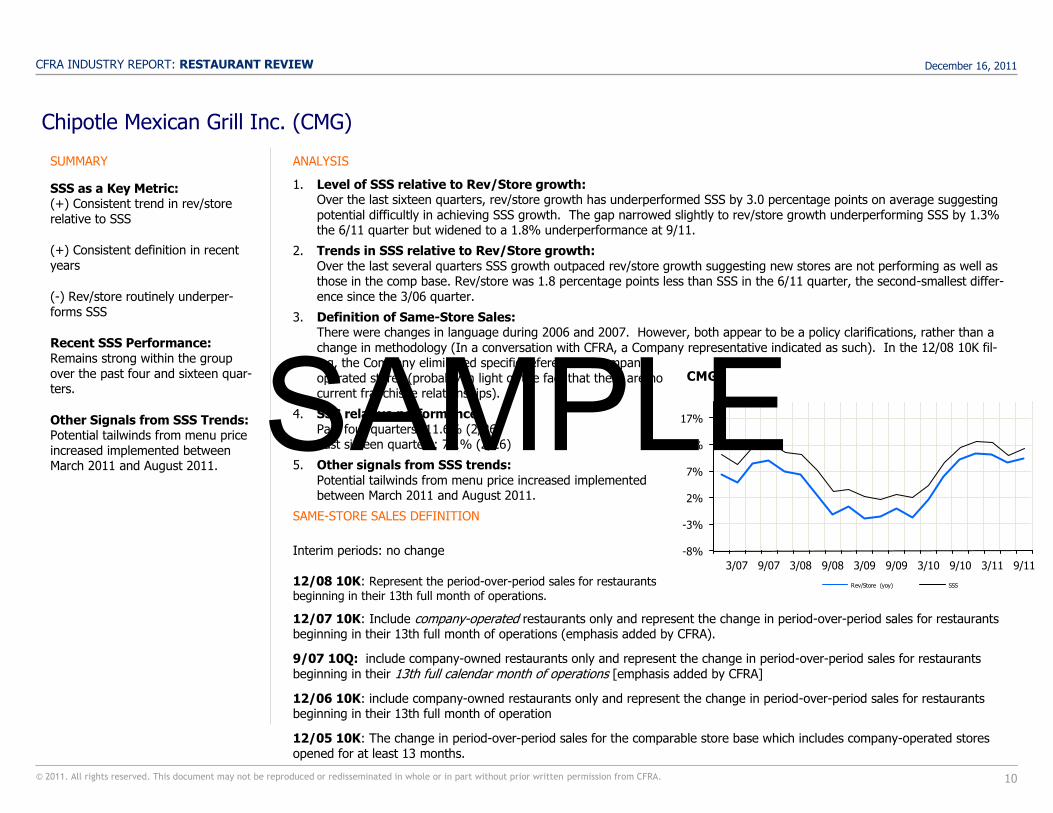

Chipotle Mexican Grill Inc. (CMG)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: Over the last sixteen quarters, rev/store growth has underperformed SSS by 3.0 percentage points on average suggesting potential difficultly in achieving SSS growth. The gap narrowed slightly to rev/store growth underperforming SSS by 1.3% the 6/11 quarter but widened to a 1.8% underperformance at 9/11.

2. Trends in SSS relative to Rev/Store growth: Over the last several quarters SSS growth outpaced rev/store growth suggesting new stores are not performing as well as those in the comp base. Rev/store was 1.8 percentage points less than SSS in the 6/11 quarter, the second-smallest differ-ence since the 3/06 quarter.

3. Definition of Same-Store Sales: There were changes in language during 2006 and 2007. However, both appear to be a policy clarifications, rather than a change in methodology (In a conversation with CFRA, a Company representative indicated as such). In the 12/08 10K fil-ing, the Company eliminated specific reference to company-operated stores (probably in light of the fact that there are no current franchisee relationships).

4. SSS relative performance: Past four quarters: 11.6% (2/26) Past sixteen quarters: 7.1% (2/26)

5. Other signals from SSS trends: Potential tailwinds from menu price increased implemented between March 2011 and August 2011.

SAME-STORE SALES DEFINITION

Interim periods: no change 12/08 10K: Represent the period-over-period sales for restaurants beginning in their 13th full month of operations.

12/07 10K: Include company-operated restaurants only and represent the change in period-over-period sales for restaurants beginning in their 13th full month of operations (emphasis added by CFRA).

9/07 10Q: include company-owned restaurants only and represent the change in period-over-period sales for restaurants beginning in their 13th full calendar month of operations [emphasis added by CFRA]

12/06 10K: include company-owned restaurants only and represent the change in period-over-period sales for restaurants beginning in their 13th full month of operation

12/05 10K: The change in period-over-period sales for the comparable store base which includes company-operated stores opened for at least 13 months.

SUMMARY

SSS as a Key Metric: (+) Consistent trend in rev/store relative to SSS

(+) Consistent definition in recent years

(-) Rev/store routinely underper-forms SSS

Recent SSS Performance: Remains strong within the group over the past four and sixteen quar-ters.

Other Signals from SSS Trends: Potential tailwinds from menu price increased implemented between March 2011 and August 2011.

-8%

-3%

2%

7%

12%

17%

9/113/119/103/109/093/099/083/089/073/07

CMG

Rev/Store (yoy) SSS

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

11 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

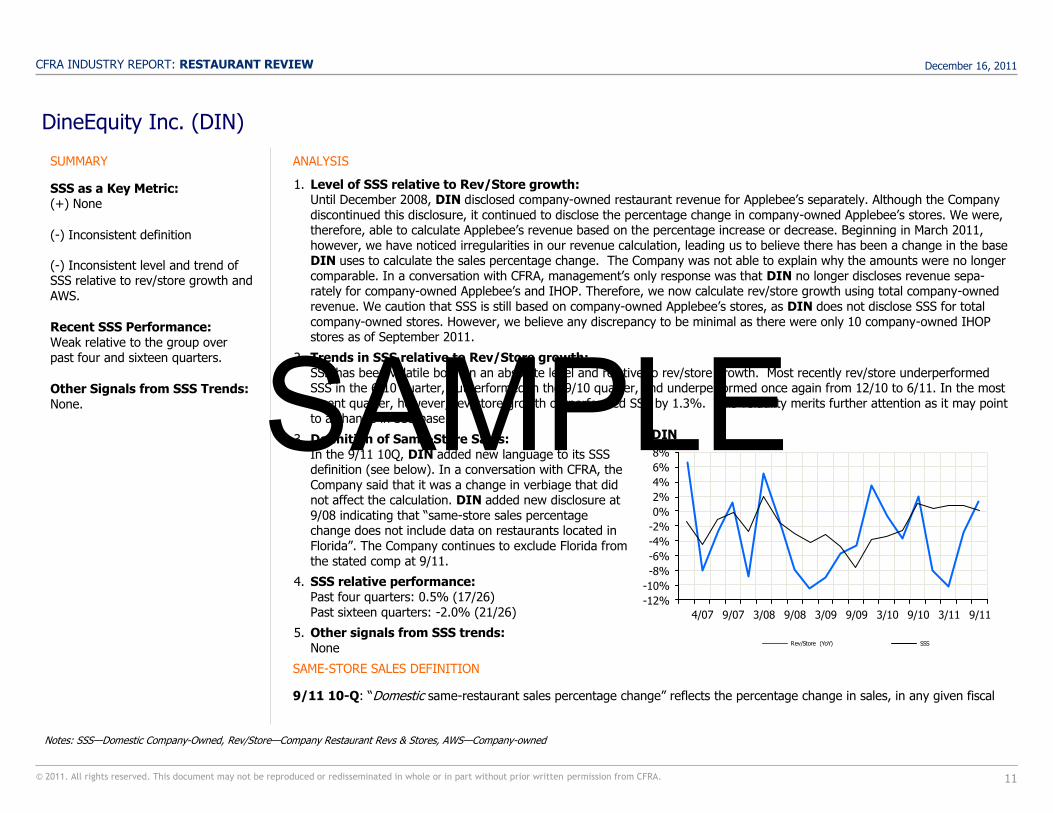

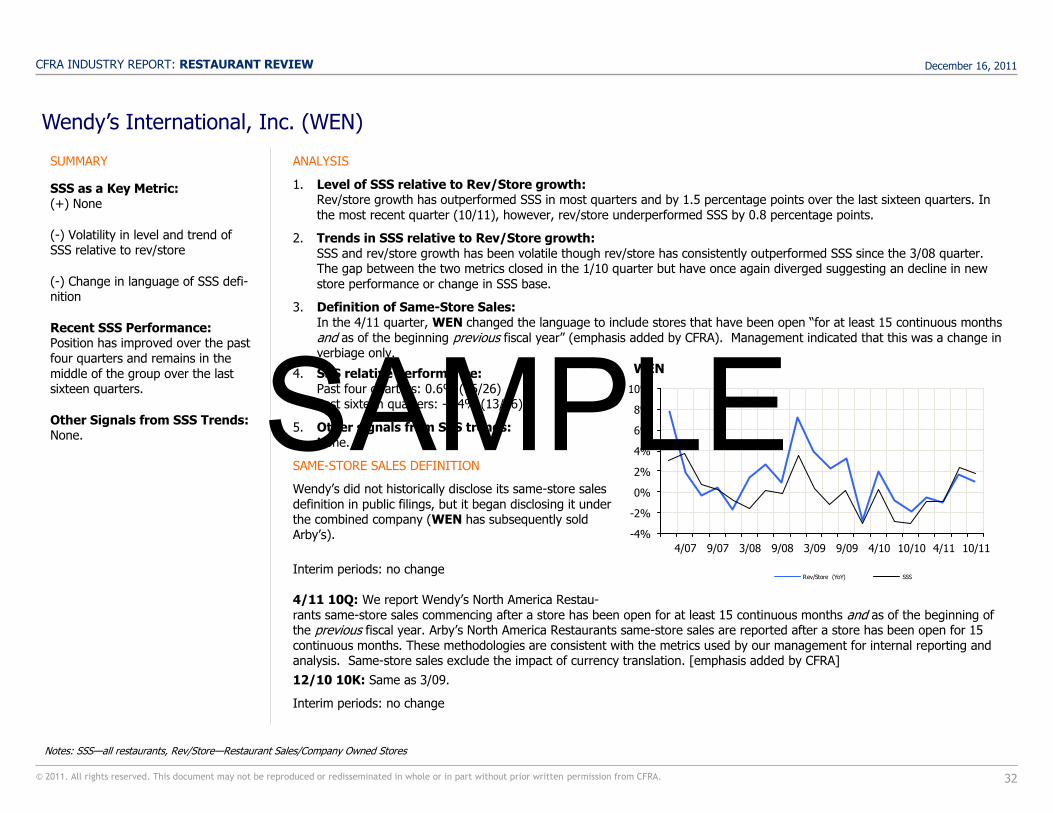

DineEquity Inc. (DIN)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: Until December 2008, DIN disclosed company-owned restaurant revenue for Applebee’s separately. Although the Company discontinued this disclosure, it continued to disclose the percentage change in company-owned Applebee’s stores. We were, therefore, able to calculate Applebee’s revenue based on the percentage increase or decrease. Beginning in March 2011, however, we have noticed irregularities in our revenue calculation, leading us to believe there has been a change in the base DIN uses to calculate the sales percentage change. The Company was not able to explain why the amounts were no longer comparable. In a conversation with CFRA, management’s only response was that DIN no longer discloses revenue sepa-rately for company-owned Applebee’s and IHOP. Therefore, we now calculate rev/store growth using total company-owned revenue. We caution that SSS is still based on company-owned Applebee’s stores, as DIN does not disclose SSS for total company-owned stores. However, we believe any discrepancy to be minimal as there were only 10 company-owned IHOP stores as of September 2011.

2. Trends in SSS relative to Rev/Store growth: SSS has been volatile both on an absolute level and relative to rev/store growth. Most recently rev/store underperformed SSS in the 6/10 quarter, outperformed in the 9/10 quarter, and underperformed once again from 12/10 to 6/11. In the most recent quarter, however, rev/store growth outperformed SSS by 1.3%. This volatility merits further attention as it may point to a change in SSS base.

3. Definition of Same-Store Sales: In the 9/11 10Q, DIN added new language to its SSS definition (see below). In a conversation with CFRA, the Company said that it was a change in verbiage that did not affect the calculation. DIN added new disclosure at 9/08 indicating that ―same-store sales percentage change does not include data on restaurants located in Florida‖. The Company continues to exclude Florida from the stated comp at 9/11.

4. SSS relative performance: Past four quarters: 0.5% (17/26) Past sixteen quarters: -2.0% (21/26)

5. Other signals from SSS trends: None

SAME-STORE SALES DEFINITION

9/11 10-Q: ―Domestic same-restaurant sales percentage change‖ reflects the percentage change in sales, in any given fiscal

SUMMARY

SSS as a Key Metric: (+) None

(-) Inconsistent definition (-) Inconsistent level and trend of SSS relative to rev/store growth and

AWS.

Recent SSS Performance: Weak relative to the group over past four and sixteen quarters.

Other Signals from SSS Trends: None.

Notes: SSS—Domestic Company-Owned, Rev/Store—Company Restaurant Revs & Stores, AWS—Company-owned

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

9/113/119/103/109/093/099/083/089/074/07

DIN

Rev/Store (YoY) SSS

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

12 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

DineEquity Inc. (DIN)

period compared to the same weeks in the prior year, for restaurants that have been operated throughout both fiscal periods that are being compared and have been open for at least 18 months. Because of new unit openings and restaurant closures, the restaurants open throughout both fiscal periods being compared may be different from period to period. Same-restaurant sales percentage change does not include data on IHOP restaurants located in Florida. [emphasis added by CFRA]

Interim periods: no change

12/08 10-K (DIN): Same-store sales percentage change" reflects the percentage change in sales, in any given fiscal year compared to the prior fiscal year, for restaurants that have been operated throughout both fiscal periods that are being com-

pared and have been open for at least 18 months. Because of new unit openings and store closures, the restaurants open throughout both fiscal periods being compared will be different from period to period. Same-store sales percentage change does not include data on IHOP restaurants located in Florida.

9/08 10Q (DIN): ―Same-store sales percentage change‖ reflects the percentage change in sales, in any given fiscal period compared to the prior fiscal period, for restaurants that have been operated throughout both fiscal periods that are being com-pared and have been open for at least 18 months. Because of new unit openings and store closures, the restaurants open throughout both fiscal periods being compared will be different from period to period. Same-store sales percentage change does not include data on restaurants located in Florida (emphasis added by CFRA).

6/08 10Q (DIN):―Same-store sales percentage change‖ reflects the percentage change in sales, in any given fiscal year com-pared to the prior fiscal year, for restaurants that have been operated throughout both fiscal periods that are being compared and have been open for at least 18 months. Because of new unit openings and store closures, the restaurants open throughout both fiscal periods being compared will be different from period to period.

03/08 10Q (DIN): Same as 12/07

12/07 10K (IHP): ―Same-store sale percentage change‖ reflects the percentage change in sales, in any given fiscal year com-pared to the prior fiscal year, for restaurants that have been operated through both fiscal periods that are being compared and have been open for at least 18 months

Interim Periods: No Change

12/03 10K (APPB): When computing comparable restaurant sales, restaurants open for at least 18 months are compared from period to period.

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

13 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

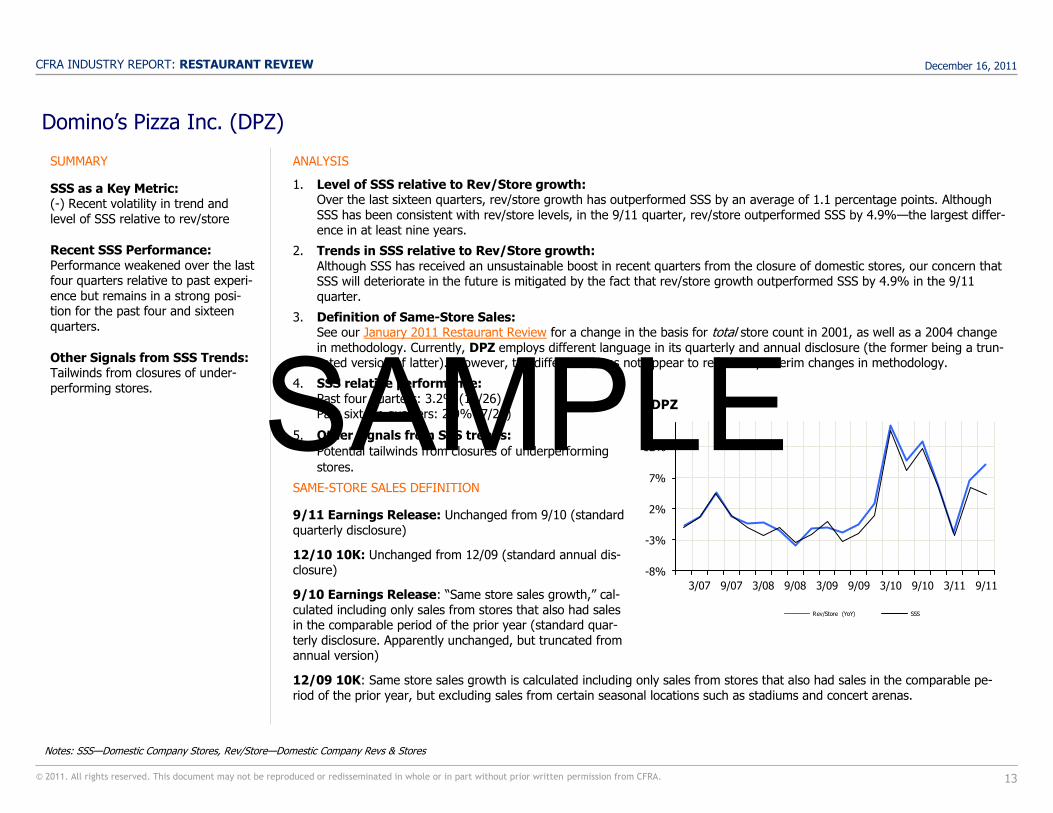

Domino’s Pizza Inc. (DPZ)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: Over the last sixteen quarters, rev/store growth has outperformed SSS by an average of 1.1 percentage points. Although SSS has been consistent with rev/store levels, in the 9/11 quarter, rev/store outperformed SSS by 4.9%—the largest differ-ence in at least nine years.

2. Trends in SSS relative to Rev/Store growth: Although SSS has received an unsustainable boost in recent quarters from the closure of domestic stores, our concern that SSS will deteriorate in the future is mitigated by the fact that rev/store growth outperformed SSS by 4.9% in the 9/11 quarter.

3. Definition of Same-Store Sales: See our January 2011 Restaurant Review for a change in the basis for total store count in 2001, as well as a 2004 change in methodology. Currently, DPZ employs different language in its quarterly and annual disclosure (the former being a trun-cated version of latter). However, the difference does not appear to reflect any interim changes in methodology.

4. SSS relative performance: Past four quarters: 3.2% (11/26) Past sixteen quarters: 2.0% (7/26)

5. Other signals from SSS trends:

Potential tailwinds from closures of underperforming

stores.

SAME-STORE SALES DEFINITION

9/11 Earnings Release: Unchanged from 9/10 (standard quarterly disclosure)

12/10 10K: Unchanged from 12/09 (standard annual dis-closure)

9/10 Earnings Release: ―Same store sales growth,‖ cal-culated including only sales from stores that also had sales in the comparable period of the prior year (standard quar-terly disclosure. Apparently unchanged, but truncated from annual version)

12/09 10K: Same store sales growth is calculated including only sales from stores that also had sales in the comparable pe-riod of the prior year, but excluding sales from certain seasonal locations such as stadiums and concert arenas.

SUMMARY

SSS as a Key Metric: (-) Recent volatility in trend and level of SSS relative to rev/store

Recent SSS Performance: Performance weakened over the last four quarters relative to past experi-

ence but remains in a strong posi-tion for the past four and sixteen quarters.

Other Signals from SSS Trends: Tailwinds from closures of under-performing stores.

Notes: SSS—Domestic Company Stores, Rev/Store—Domestic Company Revs & Stores

-8%

-3%

2%

7%

12%

9/113/119/103/109/093/099/083/089/073/07

DPZ

Rev/Store (YoY) SSS

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

14 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

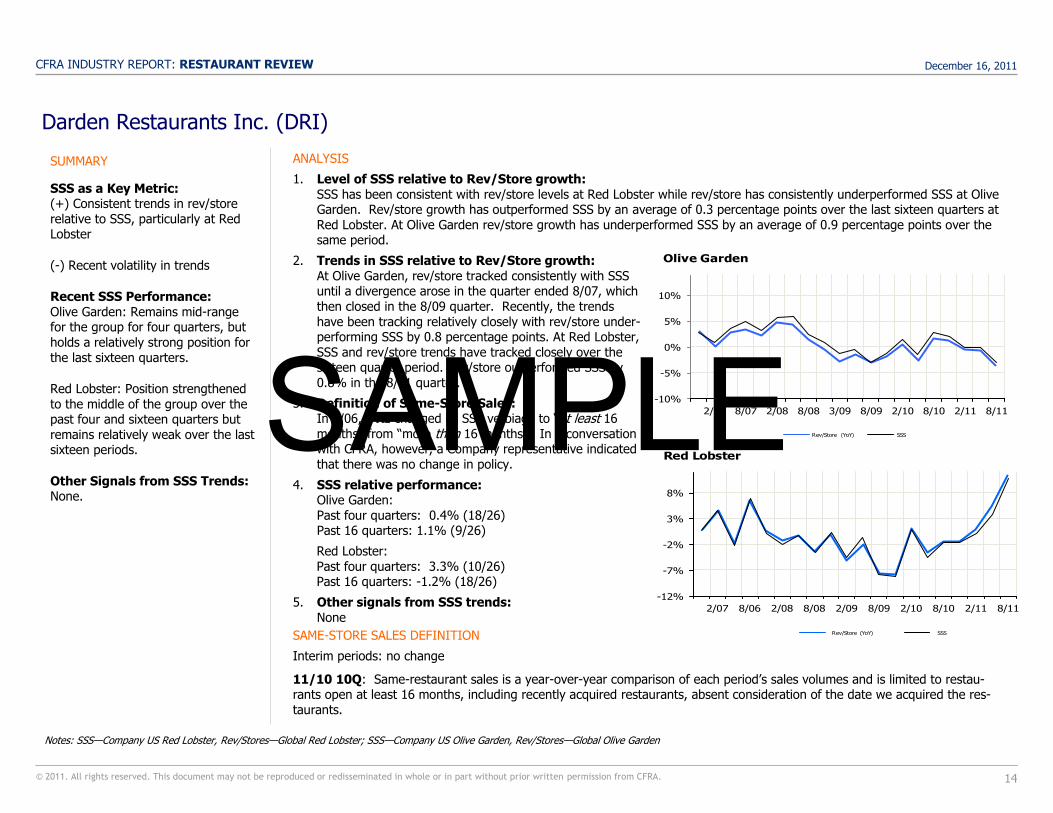

Darden Restaurants Inc. (DRI)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: SSS has been consistent with rev/store levels at Red Lobster while rev/store has consistently underperformed SSS at Olive Garden. Rev/store growth has outperformed SSS by an average of 0.3 percentage points over the last sixteen quarters at Red Lobster. At Olive Garden rev/store growth has underperformed SSS by an average of 0.9 percentage points over the same period.

2. Trends in SSS relative to Rev/Store growth: At Olive Garden, rev/store tracked consistently with SSS until a divergence arose in the quarter ended 8/07, which then closed in the 8/09 quarter. Recently, the trends have been tracking relatively closely with rev/store under-performing SSS by 0.8 percentage points. At Red Lobster, SSS and rev/store trends have tracked closely over the sixteen quarter period. Rev/store outperformed SSS by 0.8% in the 8/11 quarter.

3. Definition of Same-Store Sales: In 5/06, DRI changed its SSS verbiage to ―at least 16 months‖ from ―more than 16 months.‖ In a conversation with CFRA, however, a Company representative indicated that there was no change in policy.

4. SSS relative performance: Olive Garden: Past four quarters: 0.4% (18/26) Past 16 quarters: 1.1% (9/26)

Red Lobster: Past four quarters: 3.3% (10/26) Past 16 quarters: -1.2% (18/26)

5. Other signals from SSS trends: None

SAME-STORE SALES DEFINITION

Interim periods: no change

11/10 10Q: Same-restaurant sales is a year-over-year comparison of each period’s sales volumes and is limited to restau-rants open at least 16 months, including recently acquired restaurants, absent consideration of the date we acquired the res-taurants.

SUMMARY

SSS as a Key Metric: (+) Consistent trends in rev/store relative to SSS, particularly at Red Lobster

(-) Recent volatility in trends

Recent SSS Performance: Olive Garden: Remains mid-range for the group for four quarters, but holds a relatively strong position for the last sixteen quarters.

Red Lobster: Position strengthened to the middle of the group over the past four and sixteen quarters but remains relatively weak over the last sixteen periods.

Other Signals from SSS Trends: None.

Notes: SSS—Company US Red Lobster, Rev/Stores—Global Red Lobster; SSS—Company US Olive Garden, Rev/Stores—Global Olive Garden

-12%

-7%

-2%

3%

8%

8/112/118/102/108/092/098/082/088/062/07

Red Lobster

Rev/Store (YoY) SSS

-10%

-5%

0%

5%

10%

8/112/118/102/108/093/098/082/088/072/07

Olive Garden

Rev/Store (YoY) SSSSAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

15 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

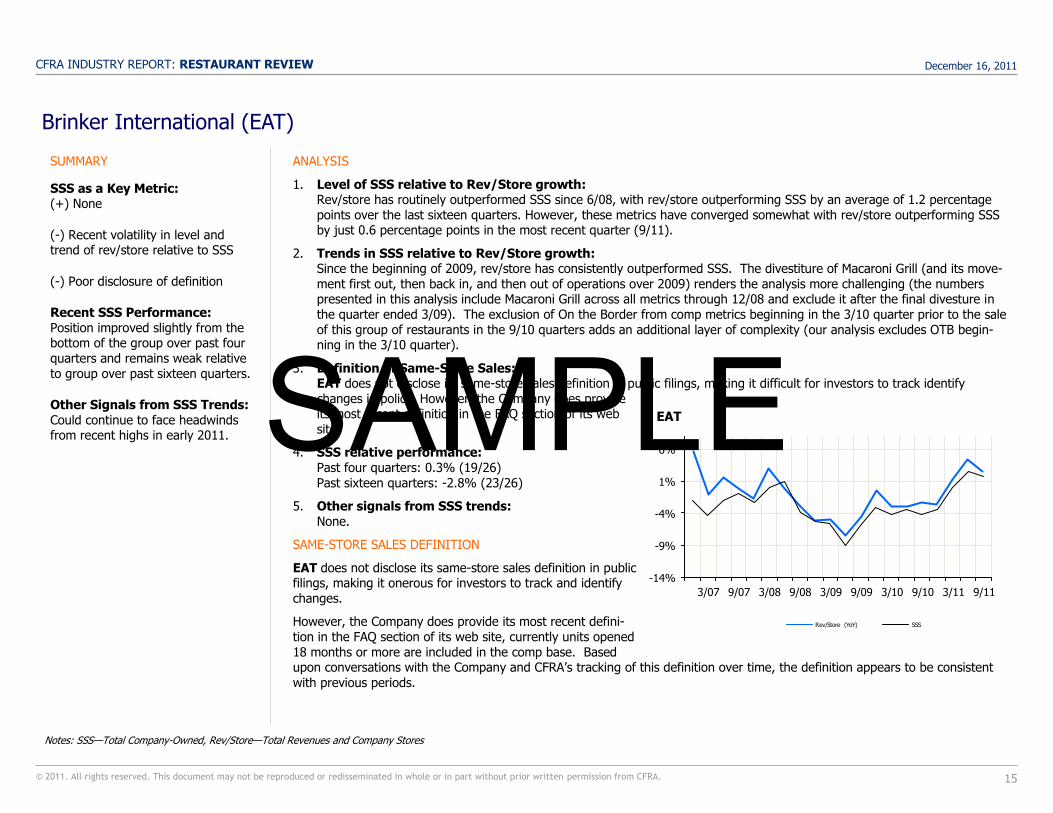

Brinker International (EAT)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: Rev/store has routinely outperformed SSS since 6/08, with rev/store outperforming SSS by an average of 1.2 percentage points over the last sixteen quarters. However, these metrics have converged somewhat with rev/store outperforming SSS by just 0.6 percentage points in the most recent quarter (9/11).

2. Trends in SSS relative to Rev/Store growth: Since the beginning of 2009, rev/store has consistently outperformed SSS. The divestiture of Macaroni Grill (and its move-

ment first out, then back in, and then out of operations over 2009) renders the analysis more challenging (the numbers presented in this analysis include Macaroni Grill across all metrics through 12/08 and exclude it after the final divesture in the quarter ended 3/09). The exclusion of On the Border from comp metrics beginning in the 3/10 quarter prior to the sale of this group of restaurants in the 9/10 quarters adds an additional layer of complexity (our analysis excludes OTB begin-ning in the 3/10 quarter).

3. Definition of Same-Store Sales: EAT does not disclose its same-store sales definition in public filings, making it difficult for investors to track identify changes in policy. However, the Company does provide its most recent definition in the FAQ section of its web site.

4. SSS relative performance: Past four quarters: 0.3% (19/26) Past sixteen quarters: -2.8% (23/26)

5. Other signals from SSS trends: None.

SAME-STORE SALES DEFINITION

EAT does not disclose its same-store sales definition in public filings, making it onerous for investors to track and identify changes.

However, the Company does provide its most recent defini-tion in the FAQ section of its web site, currently units opened 18 months or more are included in the comp base. Based upon conversations with the Company and CFRA’s tracking of this definition over time, the definition appears to be consistent with previous periods.

SUMMARY

SSS as a Key Metric: (+) None

(-) Recent volatility in level and trend of rev/store relative to SSS

(-) Poor disclosure of definition

Recent SSS Performance: Position improved slightly from the bottom of the group over past four quarters and remains weak relative to group over past sixteen quarters.

Other Signals from SSS Trends: Could continue to face headwinds from recent highs in early 2011.

Notes: SSS—Total Company-Owned, Rev/Store—Total Revenues and Company Stores

-14%

-9%

-4%

1%

6%

9/113/119/103/109/093/099/083/089/073/07

EAT

Rev/Store (YoY) SSS

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

16 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

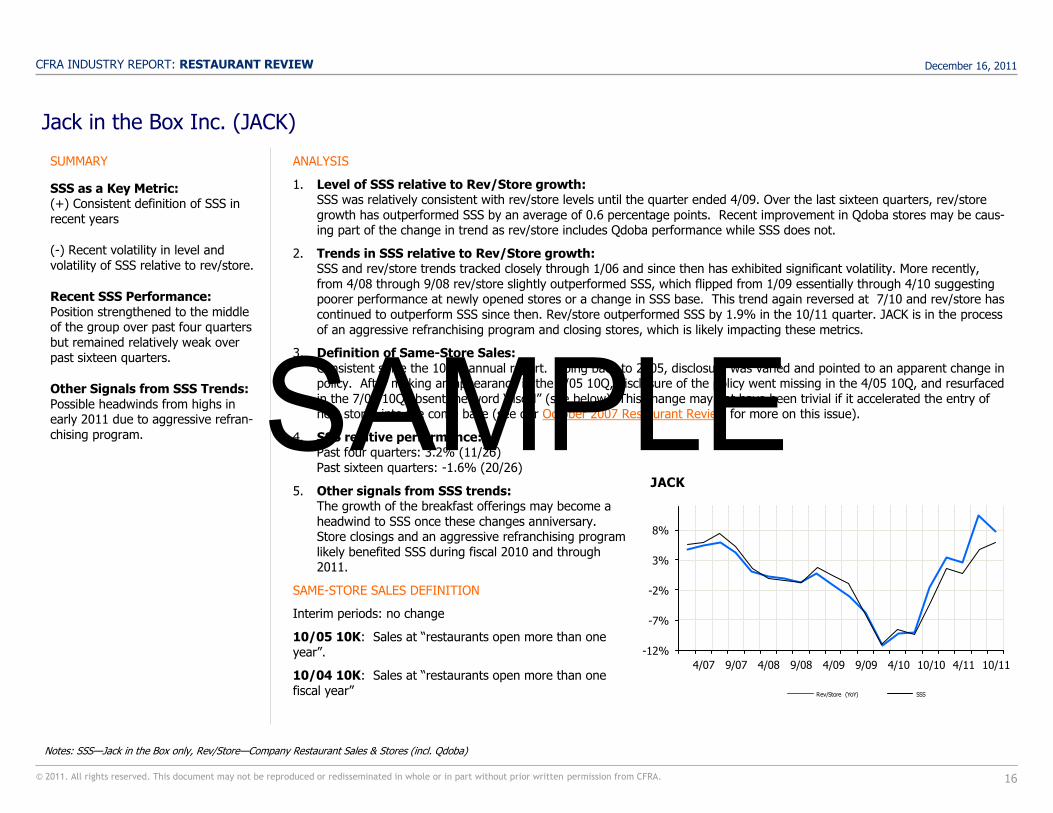

Jack in the Box Inc. (JACK)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: SSS was relatively consistent with rev/store levels until the quarter ended 4/09. Over the last sixteen quarters, rev/store growth has outperformed SSS by an average of 0.6 percentage points. Recent improvement in Qdoba stores may be caus-ing part of the change in trend as rev/store includes Qdoba performance while SSS does not.

2. Trends in SSS relative to Rev/Store growth: SSS and rev/store trends tracked closely through 1/06 and since then has exhibited significant volatility. More recently,

from 4/08 through 9/08 rev/store slightly outperformed SSS, which flipped from 1/09 essentially through 4/10 suggesting poorer performance at newly opened stores or a change in SSS base. This trend again reversed at 7/10 and rev/store has continued to outperform SSS since then. Rev/store outperformed SSS by 1.9% in the 10/11 quarter. JACK is in the process of an aggressive refranchising program and closing stores, which is likely impacting these metrics.

3. Definition of Same-Store Sales: Consistent since the 10/05 annual report. Going back to 2005, disclosure was varied and pointed to an apparent change in policy. After making an appearance in the 1/05 10Q, disclosure of the policy went missing in the 4/05 10Q, and resurfaced in the 7/05 10Q absent the word ―fiscal‖ (see below). This change may not have been trivial if it accelerated the entry of new stores into the comp base (see our October 2007 Restaurant Review for more on this issue).

4. SSS relative performance: Past four quarters: 3.2% (11/26) Past sixteen quarters: -1.6% (20/26)

5. Other signals from SSS trends: The growth of the breakfast offerings may become a headwind to SSS once these changes anniversary. Store closings and an aggressive refranchising program likely benefited SSS during fiscal 2010 and through 2011.

SAME-STORE SALES DEFINITION

Interim periods: no change

10/05 10K: Sales at ―restaurants open more than one year‖.

10/04 10K: Sales at ―restaurants open more than one fiscal year‖

SUMMARY

SSS as a Key Metric: (+) Consistent definition of SSS in recent years

(-) Recent volatility in level and volatility of SSS relative to rev/store.

Recent SSS Performance: Position strengthened to the middle of the group over past four quarters but remained relatively weak over past sixteen quarters.

Other Signals from SSS Trends: Possible headwinds from highs in early 2011 due to aggressive refran-chising program.

Notes: SSS—Jack in the Box only, Rev/Store—Company Restaurant Sales & Stores (incl. Qdoba)

-12%

-7%

-2%

3%

8%

10/114/1110/104/109/094/099/084/089/074/07

JACK

Rev/Store (YoY) SSS

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

17 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

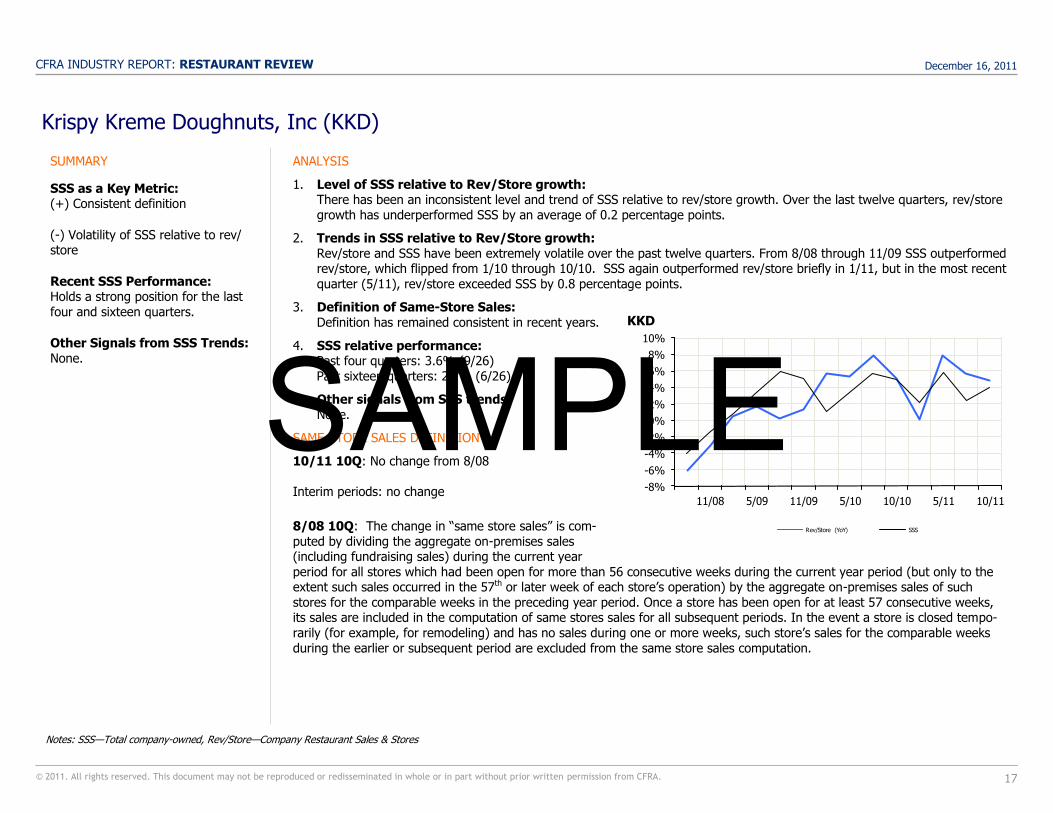

Krispy Kreme Doughnuts, Inc (KKD)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: There has been an inconsistent level and trend of SSS relative to rev/store growth. Over the last twelve quarters, rev/store growth has underperformed SSS by an average of 0.2 percentage points.

2. Trends in SSS relative to Rev/Store growth: Rev/store and SSS have been extremely volatile over the past twelve quarters. From 8/08 through 11/09 SSS outperformed rev/store, which flipped from 1/10 through 10/10. SSS again outperformed rev/store briefly in 1/11, but in the most recent

quarter (5/11), rev/store exceeded SSS by 0.8 percentage points.

3. Definition of Same-Store Sales: Definition has remained consistent in recent years.

4. SSS relative performance: Past four quarters: 3.6% (9/26) Past sixteen quarters: 2.7% (6/26)

5. Other signals from SSS trends: None.

SAME-STORE SALES DEFINITION

10/11 10Q: No change from 8/08 Interim periods: no change

8/08 10Q: The change in ―same store sales‖ is com-puted by dividing the aggregate on-premises sales (including fundraising sales) during the current year period for all stores which had been open for more than 56 consecutive weeks during the current year period (but only to the extent such sales occurred in the 57th or later week of each store’s operation) by the aggregate on-premises sales of such stores for the comparable weeks in the preceding year period. Once a store has been open for at least 57 consecutive weeks, its sales are included in the computation of same stores sales for all subsequent periods. In the event a store is closed tempo-rarily (for example, for remodeling) and has no sales during one or more weeks, such store’s sales for the comparable weeks during the earlier or subsequent period are excluded from the same store sales computation.

SUMMARY

SSS as a Key Metric: (+) Consistent definition

(-) Volatility of SSS relative to rev/store

Recent SSS Performance: Holds a strong position for the last four and sixteen quarters.

Other Signals from SSS Trends: None.

Notes: SSS—Total company-owned, Rev/Store—Company Restaurant Sales & Stores

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

10/115/1110/105/1011/095/0911/08

KKD

Rev/Store (YoY) SSS

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

18 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

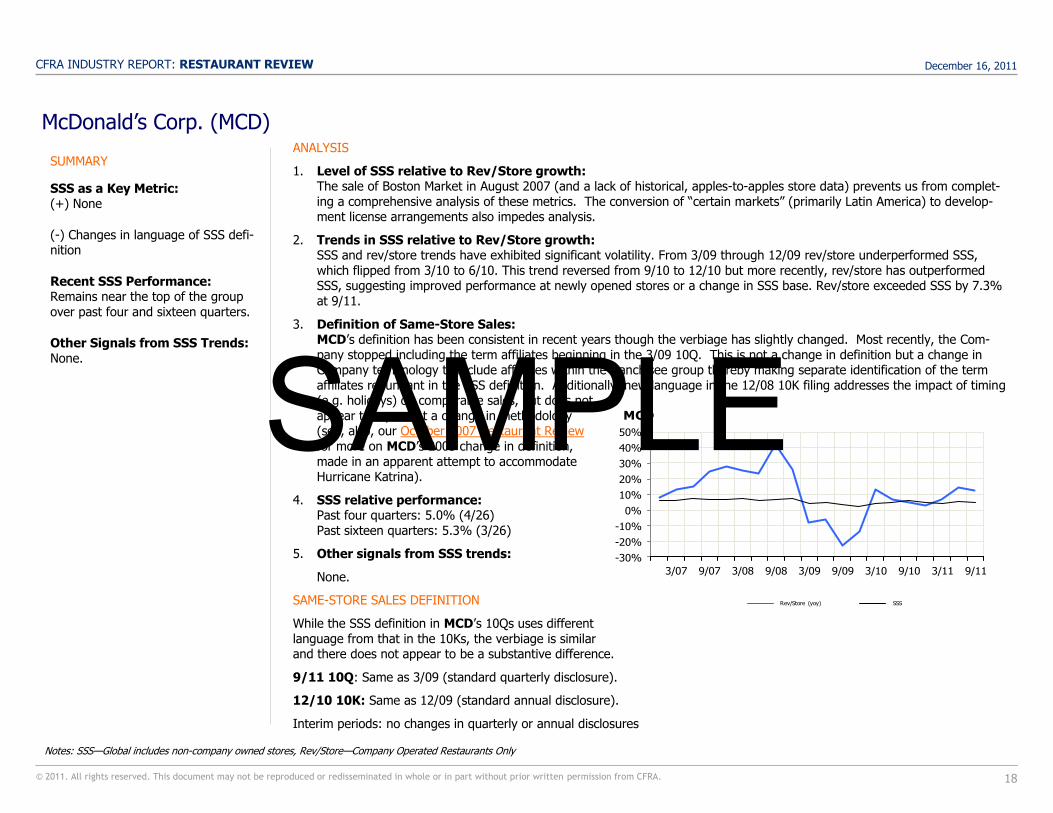

McDonald’s Corp. (MCD) ANALYSIS

1. Level of SSS relative to Rev/Store growth: The sale of Boston Market in August 2007 (and a lack of historical, apples-to-apples store data) prevents us from complet-ing a comprehensive analysis of these metrics. The conversion of ―certain markets‖ (primarily Latin America) to develop-ment license arrangements also impedes analysis.

2. Trends in SSS relative to Rev/Store growth: SSS and rev/store trends have exhibited significant volatility. From 3/09 through 12/09 rev/store underperformed SSS, which flipped from 3/10 to 6/10. This trend reversed from 9/10 to 12/10 but more recently, rev/store has outperformed SSS, suggesting improved performance at newly opened stores or a change in SSS base. Rev/store exceeded SSS by 7.3% at 9/11.

3. Definition of Same-Store Sales: MCD’s definition has been consistent in recent years though the verbiage has slightly changed. Most recently, the Com-pany stopped including the term affiliates beginning in the 3/09 10Q. This is not a change in definition but a change in Company terminology to include affiliates within the franchisee group thereby making separate identification of the term affiliates redundant in the SSS definition. Additionally, new language in the 12/08 10K filing addresses the impact of timing (e.g. holidays) on comparable sales, but does not appear to represent a change in methodology (see, also, our October 2007 Restaurant Review for more on MCD’s 2005 change in definition, made in an apparent attempt to accommodate Hurricane Katrina).

4. SSS relative performance: Past four quarters: 5.0% (4/26) Past sixteen quarters: 5.3% (3/26)

5. Other signals from SSS trends:

None.

SAME-STORE SALES DEFINITION

While the SSS definition in MCD’s 10Qs uses different language from that in the 10Ks, the verbiage is similar and there does not appear to be a substantive difference.

9/11 10Q: Same as 3/09 (standard quarterly disclosure).

12/10 10K: Same as 12/09 (standard annual disclosure).

Interim periods: no changes in quarterly or annual disclosures

SUMMARY

SSS as a Key Metric: (+) None

(-) Changes in language of SSS defi-nition

Recent SSS Performance: Remains near the top of the group over past four and sixteen quarters.

Other Signals from SSS Trends: None.

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

9/113/119/103/109/093/099/083/089/073/07

MCD

Rev/Store (yoy) SSS

Notes: SSS—Global includes non-company owned stores, Rev/Store—Company Operated Restaurants Only

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

19 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

McDonald’s Corp. (MCD)

3/09 10Q: Comparable sales represent sales at all restaurants and comparable guest counts represent the number of transac-tions at all restaurants, including those operated by the Company or by franchisees, in operation at least thirteen months in-cluding those temporarily closed. Comparable sales exclude the impact of currency translation. [eliminated affiliates following franchisees]

No changes to quarterly language in interim periods.

3/06 10-Q: Comparable sales represent sales at all McDonald’s restaurants, including those operated by the Company, fran-chisees and affiliates, in operation at least thirteen months including those temporarily closed, excluding the impact of currency

translation.

12/05 10K: The percent change in constant currency sales from the same period in the prior year for all McDonald’s restau-rants in operation at least thirteen months, including those temporarily closed.

12/04 10K: The percent change in constant currency sales from the same period in the prior year for all McDonald’s restau-rants in operation at least thirteen months.

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

20 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

P. F. Chang’s China Bistro Inc. (PFCB)

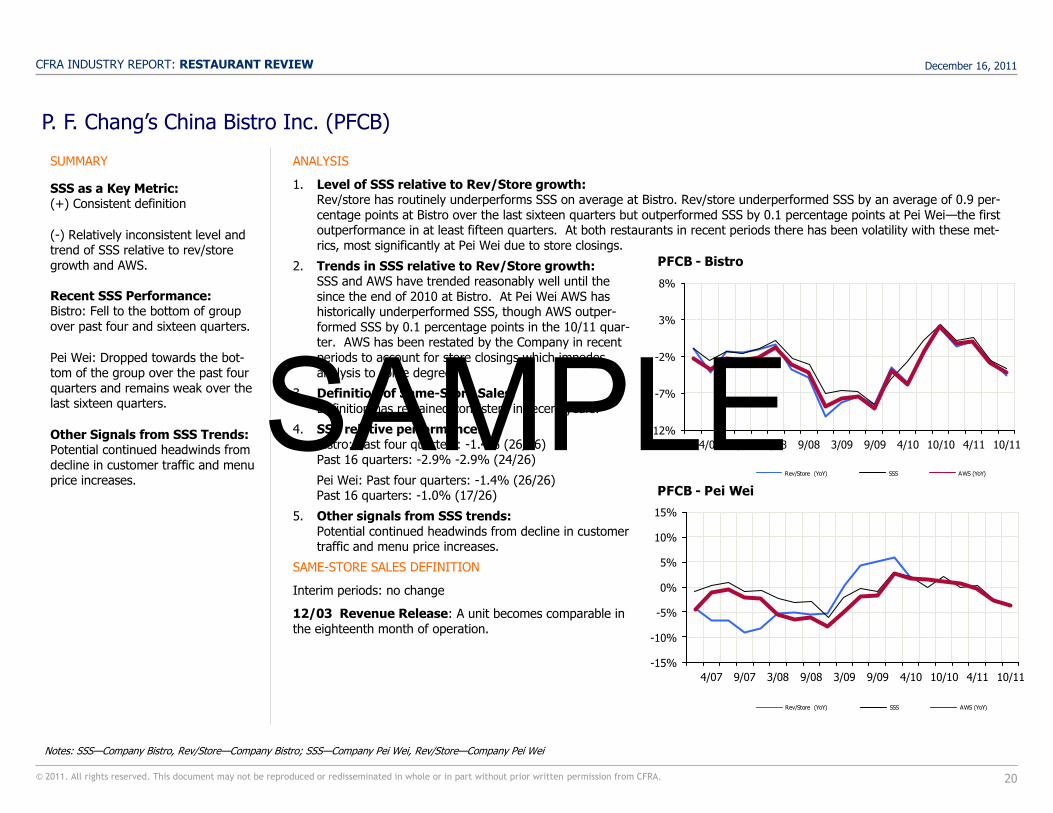

ANALYSIS

1. Level of SSS relative to Rev/Store growth: Rev/store has routinely underperforms SSS on average at Bistro. Rev/store underperformed SSS by an average of 0.9 per-centage points at Bistro over the last sixteen quarters but outperformed SSS by 0.1 percentage points at Pei Wei—the first outperformance in at least fifteen quarters. At both restaurants in recent periods there has been volatility with these met-rics, most significantly at Pei Wei due to store closings.

2. Trends in SSS relative to Rev/Store growth: SSS and AWS have trended reasonably well until the since the end of 2010 at Bistro. At Pei Wei AWS has historically underperformed SSS, though AWS outper-formed SSS by 0.1 percentage points in the 10/11 quar-ter. AWS has been restated by the Company in recent periods to account for store closings which impedes analysis to some degree.

3. Definition of Same-Store Sales: Definition has remained consistent in recent years.

4. SSS relative performance: Bistro: Past four quarters: -1.4% (26/26) Past 16 quarters: -2.9% -2.9% (24/26)

Pei Wei: Past four quarters: -1.4% (26/26) Past 16 quarters: -1.0% (17/26)

5. Other signals from SSS trends: Potential continued headwinds from decline in customer traffic and menu price increases.

SAME-STORE SALES DEFINITION

Interim periods: no change

12/03 Revenue Release: A unit becomes comparable in the eighteenth month of operation.

SUMMARY

SSS as a Key Metric: (+) Consistent definition

(-) Relatively inconsistent level and trend of SSS relative to rev/store growth and AWS.

Recent SSS Performance: Bistro: Fell to the bottom of group over past four and sixteen quarters.

Pei Wei: Dropped towards the bot-tom of the group over the past four quarters and remains weak over the last sixteen quarters.

Other Signals from SSS Trends: Potential continued headwinds from decline in customer traffic and menu price increases.

Notes: SSS—Company Bistro, Rev/Store—Company Bistro; SSS—Company Pei Wei, Rev/Store—Company Pei Wei

-12%

-7%

-2%

3%

8%

10/114/1110/104/109/093/099/083/089/074/07

PFCB - Bistro

Rev/Store (YoY) SSS AWS (YoY)

-15%

-10%

-5%

0%

5%

10%

15%

10/114/1110/104/109/093/099/083/089/074/07

PFCB - Pei Wei

Rev/Store (YoY) SSS AWS (YoY)

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

21 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

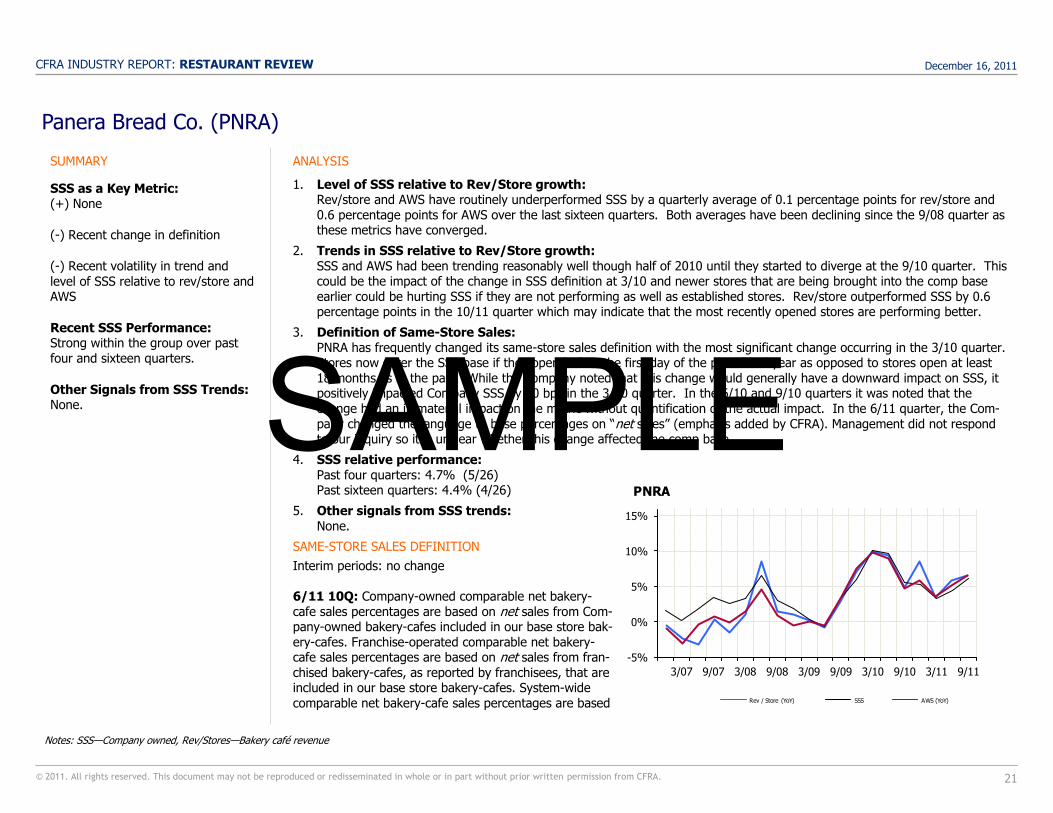

Panera Bread Co. (PNRA)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: Rev/store and AWS have routinely underperformed SSS by a quarterly average of 0.1 percentage points for rev/store and 0.6 percentage points for AWS over the last sixteen quarters. Both averages have been declining since the 9/08 quarter as these metrics have converged.

2. Trends in SSS relative to Rev/Store growth: SSS and AWS had been trending reasonably well though half of 2010 until they started to diverge at the 9/10 quarter. This could be the impact of the change in SSS definition at 3/10 and newer stores that are being brought into the comp base earlier could be hurting SSS if they are not performing as well as established stores. Rev/store outperformed SSS by 0.6 percentage points in the 10/11 quarter which may indicate that the most recently opened stores are performing better.

3. Definition of Same-Store Sales: PNRA has frequently changed its same-store sales definition with the most significant change occurring in the 3/10 quarter. Stores now enter the SSS base if they open before the first day of the prior fiscal year as opposed to stores open at least 18 months as in the past. While the Company noted that this change would generally have a downward impact on SSS, it positively impacted Company SSS by 10 bps in the 3/10 quarter. In the 6/10 and 9/10 quarters it was noted that the change had an immaterial impact on the metric without quantification of the actual impact. In the 6/11 quarter, the Com-pany changed the language to base percentages on ―net sales‖ (emphasis added by CFRA). Management did not respond to our inquiry so it is unclear whether this change affected the comp base.

4. SSS relative performance: Past four quarters: 4.7% (5/26) Past sixteen quarters: 4.4% (4/26)

5. Other signals from SSS trends: None.

SAME-STORE SALES DEFINITION

Interim periods: no change 6/11 10Q: Company-owned comparable net bakery-cafe sales percentages are based on net sales from Com-pany-owned bakery-cafes included in our base store bak-ery-cafes. Franchise-operated comparable net bakery-cafe sales percentages are based on net sales from fran-chised bakery-cafes, as reported by franchisees, that are included in our base store bakery-cafes. System-wide comparable net bakery-cafe sales percentages are based

SUMMARY

SSS as a Key Metric: (+) None

(-) Recent change in definition

(-) Recent volatility in trend and

level of SSS relative to rev/store and AWS

Recent SSS Performance: Strong within the group over past four and sixteen quarters.

Other Signals from SSS Trends: None.

Notes: SSS—Company owned, Rev/Stores—Bakery café revenue

-5%

0%

5%

10%

15%

9/113/119/103/109/093/099/083/089/073/07

PNRA

Rev / Store (YoY) SSS AWS (YoY)

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

22 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

Panera Bread Co. (PNRA)

on net sales at Company-owned and franchise-operated bakery-cafes that are included in our base store bakery-cafes. Acquired Company-owned and franchise-operated bakery-cafes and other restaurant or bakery-cafe concepts are included in our compa-rable net bakery-cafe sales percentages after we have acquired a 100 percent ownership interest and such acquisition occurred prior to the first day of our prior fiscal year. Comparable net bakery-cafe sales exclude closed locations. [Emphasis added by CFRA.] 3/11 10Q: No change 12/10 10K: In fiscal 2010, we modified the method by which we determine bakery-cafes included in our comparable net bak-

ery-cafe sales percentages to include those bakery-cafes with an open date prior to the first day of our prior fiscal year, which we refer to as our base store bakery-cafes. Previously, comparable net bakery-cafe sales percentages were based on bakery-cafes that had been in operation for 18 months. While this methodology modification did not have a material impact on previ-ously reported amounts, prior periods have been updated to conform to current methodology. Company-owned comparable net bakery-cafe sales percentages are based on sales from Company-owned bakery-cafes included in our base store bakery-cafes. Franchise-operated comparable net bakery-cafe sales percentages are based on sales from franchise-operated bakery-cafes, as reported by franchisees, that are included in our base store bakery-cafes. System-wide comparable net bakery-cafe sales per-centages are based on sales at Company-owned and franchise-operated bakery-cafes that are included in our base store bakery-cafes. Acquired Company-owned and franchise-operated bakery-cafes and other restaurant or bakery-cafe concepts are in-cluded in our comparable net bakery-cafe sales percentages after we have acquired a 100 percent ownership interest and such acquisition occurred prior to the first day of our prior fiscal year. Comparable net bakery-cafe sales exclude closed locations. [Emphasis added by CFRA.] 9/10 10Q: No change from 3/10. 3/10 10Q: Company-owned comparable bakery-cafe sales percentages are based on sales from Company-owned bakery-cafes included in our base store bakery-cafes. In fiscal 2010 we modified the method by which we determine bakery-cafes included in our comparable bakery-cafe sales percentages to include those bakery-cafes with an open date prior to the first day of our prior fiscal year. Previously, comparable bakery-cafe sales percentages were based on bakery-cafes that had been in operation for 18 months. Similarly, for fiscal 2010, franchise-operated bakery-cafes include only those bakery-cafes with an open date prior to the first day of our prior fiscal year. Franchise-operated comparable bakery-cafe sales percentages are based on sales from franchised bakery-cafes, as reported by franchisees, that are included in our base store bakery-cafes. Acquired Company-owned and franchise-operated bakery-cafes and other restaurant or bakery-cafe concepts are included in our comparable bak-ery-cafe sales percentages after we have acquired a 100 percent ownership interest and such acquisition date occurred prior to the first day of our prior fiscal year. Comparable bakery-cafe sales exclude closed locations. [Emphasis added by CFRA.]

Interim periods: no change

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

23 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

Panera Bread Co. (PNRA)

9/09 10Q: We include in this report information on Company-owned, franchise-operated and system-wide comparable bakery-cafe sales percentages. Company-owned comparable bakery-cafe sales percentages are based on sales from bakery-cafes that have been in operation and Company-owned for at least 18 months. Franchise-operated comparable bakery-cafe sales percent-ages are based on sales from franchised bakery-cafes, as reported by franchisees, that have been in operation and franchise-operated for at least 18 months. System-wide comparable bakery-cafe sales percentages are based on sales at both Company-owned and franchise-operated bakery-cafes that have been in operation and Company-owned or franchise-operated for at least 18 months. Acquired Company-owned and franchise-operated bakery-cafe locations and other restaurant or bakery-cafe con-cepts are excluded from comparable bakery-cafe sales until we have held a 100 percent ownership interest therein for at least 18 months. Comparable bakery-cafe sales exclude closed locations and currently, Paradise Bakery & Café, Inc., or Paradise, locations (emphasis added by CFRA).

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

24 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

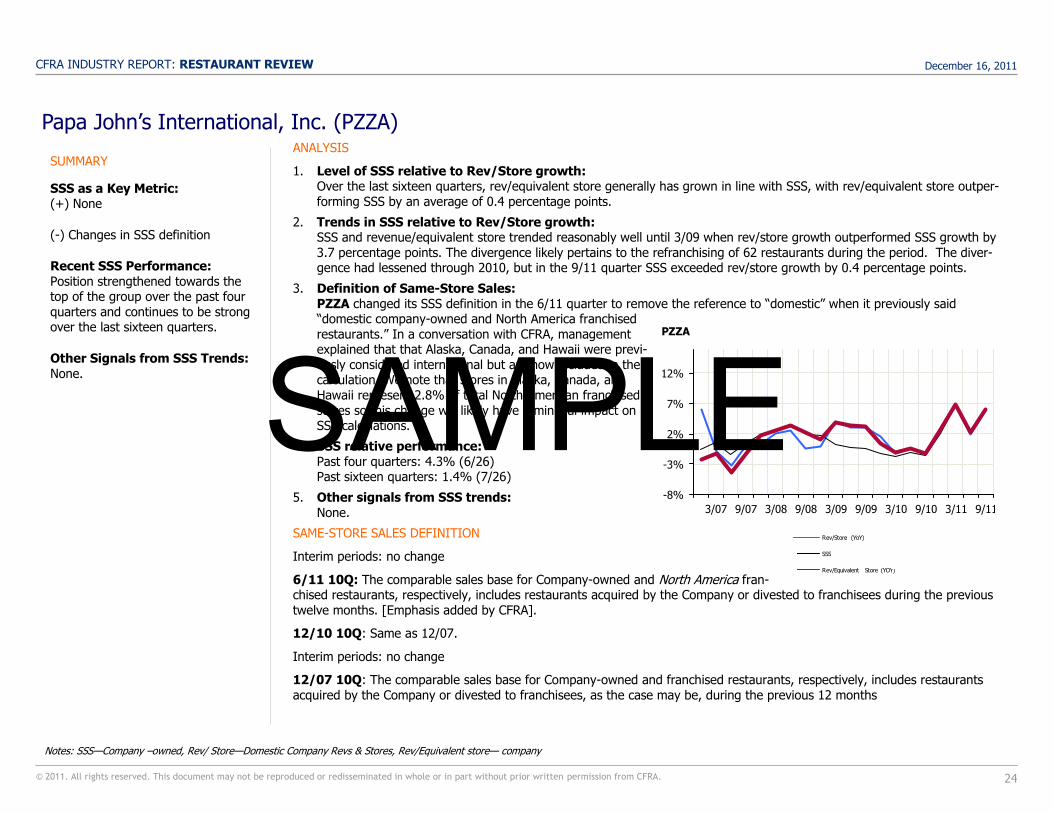

Papa John’s International, Inc. (PZZA) ANALYSIS

1. Level of SSS relative to Rev/Store growth: Over the last sixteen quarters, rev/equivalent store generally has grown in line with SSS, with rev/equivalent store outper-forming SSS by an average of 0.4 percentage points.

2. Trends in SSS relative to Rev/Store growth: SSS and revenue/equivalent store trended reasonably well until 3/09 when rev/store growth outperformed SSS growth by 3.7 percentage points. The divergence likely pertains to the refranchising of 62 restaurants during the period. The diver-gence had lessened through 2010, but in the 9/11 quarter SSS exceeded rev/store growth by 0.4 percentage points.

3. Definition of Same-Store Sales: PZZA changed its SSS definition in the 6/11 quarter to remove the reference to ―domestic‖ when it previously said ―domestic company-owned and North America franchised restaurants.‖ In a conversation with CFRA, management explained that that Alaska, Canada, and Hawaii were previ-ously considered international but are now included in the calculation. We note that stores in Alaska, Canada, and Hawaii represent 2.8% of total North American franchised stores so this change will likely have a minimal impact on SSS calculations.

4. SSS relative performance: Past four quarters: 4.3% (6/26) Past sixteen quarters: 1.4% (7/26)

5. Other signals from SSS trends: None.

SAME-STORE SALES DEFINITION

Interim periods: no change

6/11 10Q: The comparable sales base for Company-owned and North America fran-chised restaurants, respectively, includes restaurants acquired by the Company or divested to franchisees during the previous twelve months. [Emphasis added by CFRA].

12/10 10Q: Same as 12/07.

Interim periods: no change

12/07 10Q: The comparable sales base for Company-owned and franchised restaurants, respectively, includes restaurants acquired by the Company or divested to franchisees, as the case may be, during the previous 12 months

SUMMARY

SSS as a Key Metric: (+) None

(-) Changes in SSS definition

Recent SSS Performance:

Position strengthened towards the top of the group over the past four quarters and continues to be strong over the last sixteen quarters.

Other Signals from SSS Trends: None.

Notes: SSS—Company –owned, Rev/ Store—Domestic Company Revs & Stores, Rev/Equivalent store— company

-8%

-3%

2%

7%

12%

9/113/119/103/109/093/099/083/089/073/07

PZZA

Rev/Store (YoY)

SSS

Rev/Equivalent Store (YOY)

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

25 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

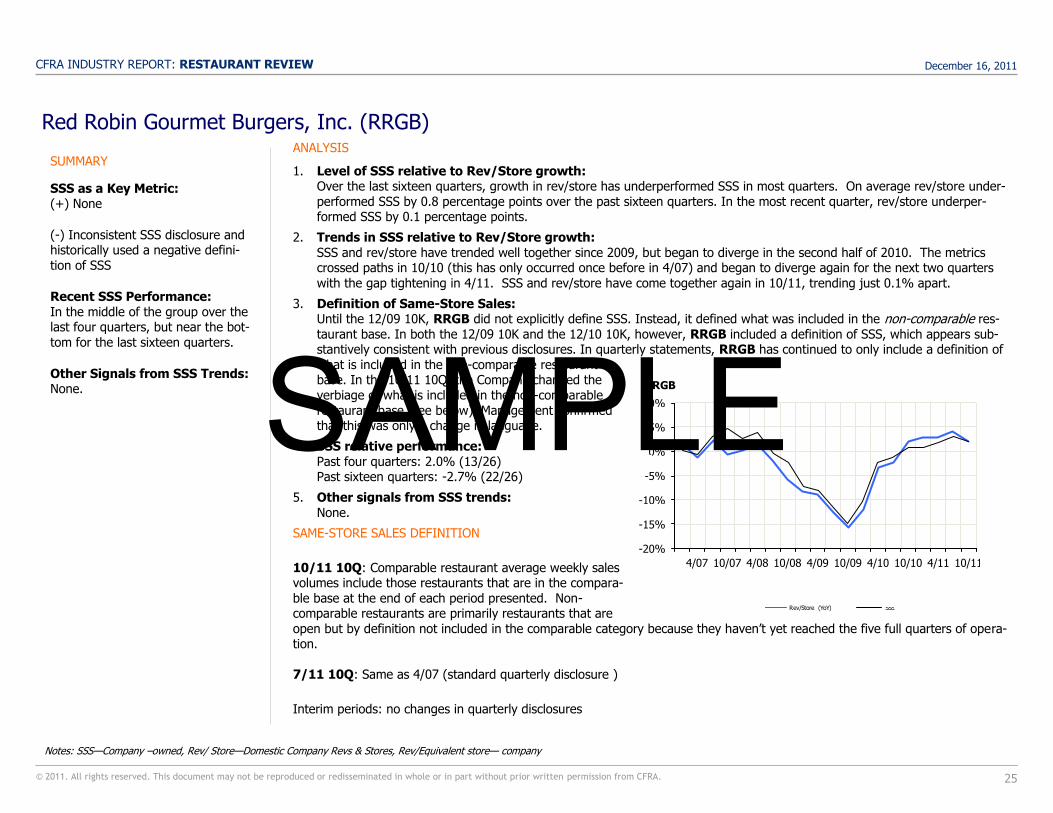

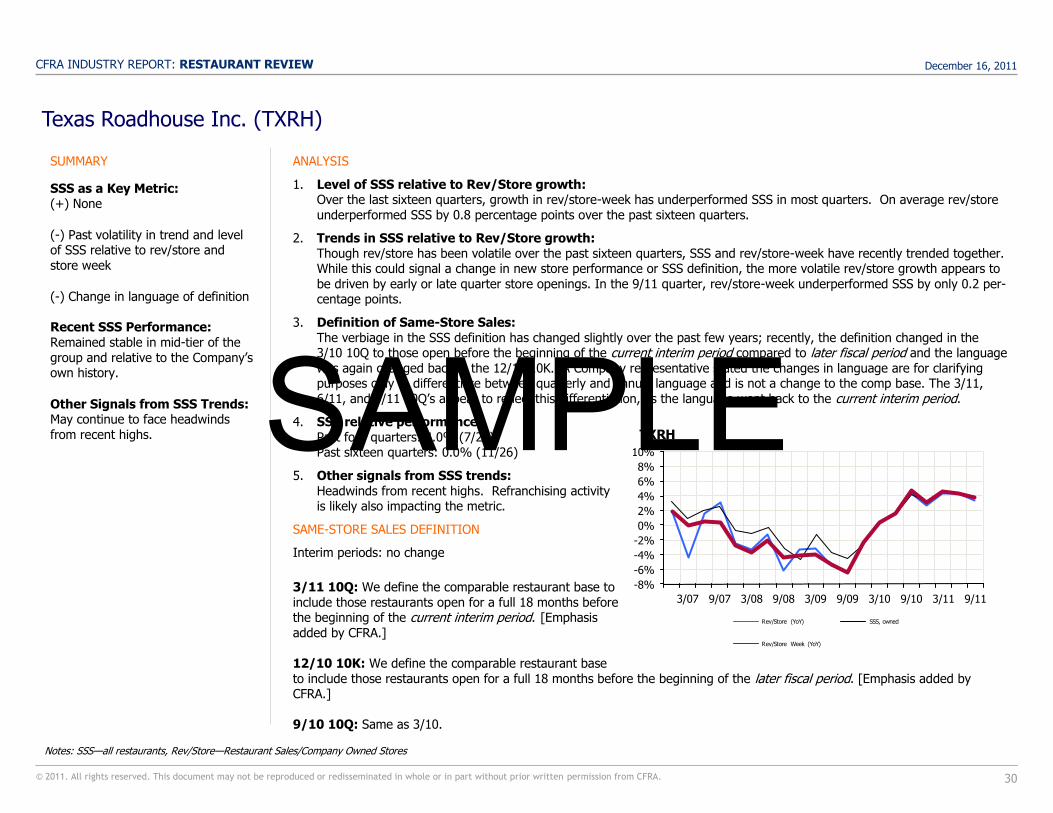

Red Robin Gourmet Burgers, Inc. (RRGB) ANALYSIS

1. Level of SSS relative to Rev/Store growth: Over the last sixteen quarters, growth in rev/store has underperformed SSS in most quarters. On average rev/store under-performed SSS by 0.8 percentage points over the past sixteen quarters. In the most recent quarter, rev/store underper-formed SSS by 0.1 percentage points.

2. Trends in SSS relative to Rev/Store growth: SSS and rev/store have trended well together since 2009, but began to diverge in the second half of 2010. The metrics crossed paths in 10/10 (this has only occurred once before in 4/07) and began to diverge again for the next two quarters

with the gap tightening in 4/11. SSS and rev/store have come together again in 10/11, trending just 0.1% apart.

3. Definition of Same-Store Sales: Until the 12/09 10K, RRGB did not explicitly define SSS. Instead, it defined what was included in the non-comparable res-taurant base. In both the 12/09 10K and the 12/10 10K, however, RRGB included a definition of SSS, which appears sub-stantively consistent with previous disclosures. In quarterly statements, RRGB has continued to only include a definition of what is included in the non-comparable restaurant base. In the 10/11 10Q, the Company changed the verbiage of what is included in the non-comparable restaurant base (see below). Management confirmed that this was only a change in language.

4. SSS relative performance: Past four quarters: 2.0% (13/26) Past sixteen quarters: -2.7% (22/26)

5. Other signals from SSS trends: None.

SAME-STORE SALES DEFINITION

10/11 10Q: Comparable restaurant average weekly sales volumes include those restaurants that are in the compara-ble base at the end of each period presented. Non-comparable restaurants are primarily restaurants that are open but by definition not included in the comparable category because they haven’t yet reached the five full quarters of opera-tion. 7/11 10Q: Same as 4/07 (standard quarterly disclosure )

Interim periods: no changes in quarterly disclosures

SUMMARY

SSS as a Key Metric: (+) None

(-) Inconsistent SSS disclosure and historically used a negative defini-tion of SSS

Recent SSS Performance: In the middle of the group over the last four quarters, but near the bot-tom for the last sixteen quarters.

Other Signals from SSS Trends: None.

Notes: SSS—Company –owned, Rev/ Store—Domestic Company Revs & Stores, Rev/Equivalent store— company

-20%

-15%

-10%

-5%

0%

5%

10%

10/114/1110/104/1010/094/0910/084/0810/074/07

RRGB

Rev/Store (YoY) SSS

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

26 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

Red Robin Gourmet Burgers, Inc. (RRGB)

12/10K: Same definition as 12/09 Interim periods: no changes in quarterly disclosures 12/09 10K: Comparable restaurants include those Company-owned restaurants that have achieved five full quarters of opera-tions during the periods presented. Interim periods: no change

4/07 10Q: Comparable restaurant average weekly sales volumes include those restaurants that are in the comparable base at the end of each period presented. Non-comparable restaurants presented include those restaurants that had not yet achieved the five full quarters of operations during the periods presented.

Notes: SSS—Company –owned, Rev/ Store—Domestic Company Revs & Stores, Rev/Equivalent store— company

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

27 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

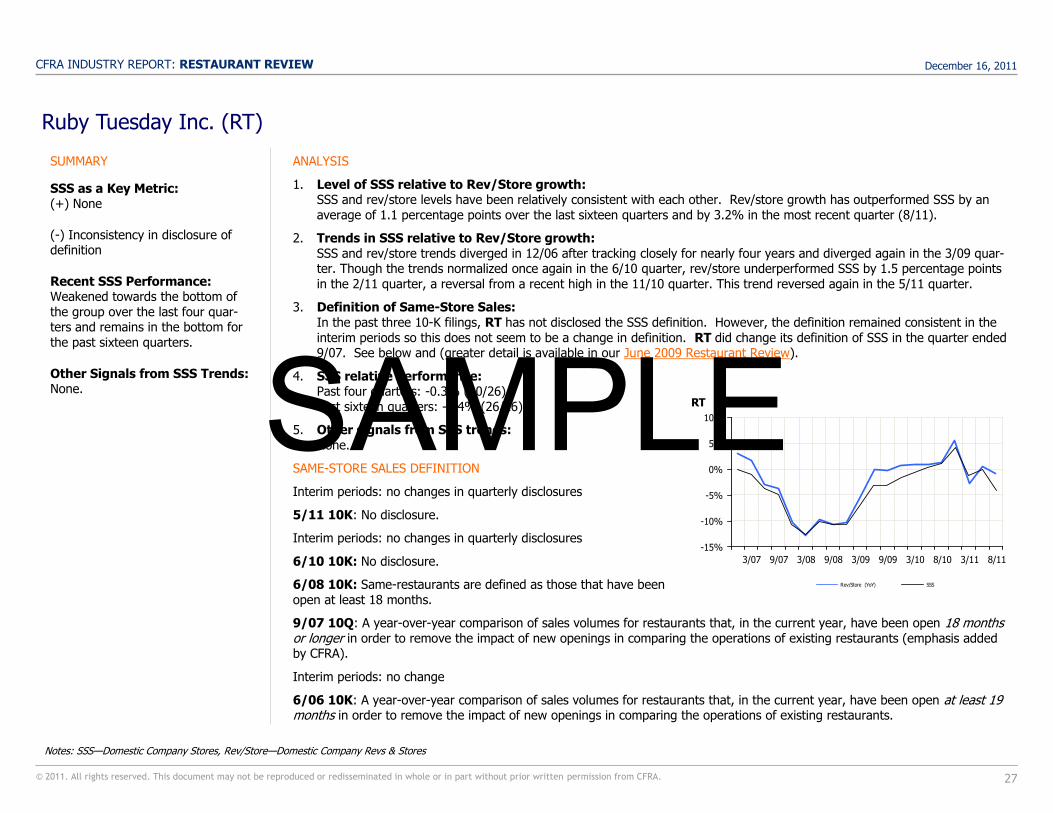

Ruby Tuesday Inc. (RT)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: SSS and rev/store levels have been relatively consistent with each other. Rev/store growth has outperformed SSS by an average of 1.1 percentage points over the last sixteen quarters and by 3.2% in the most recent quarter (8/11).

2. Trends in SSS relative to Rev/Store growth: SSS and rev/store trends diverged in 12/06 after tracking closely for nearly four years and diverged again in the 3/09 quar-ter. Though the trends normalized once again in the 6/10 quarter, rev/store underperformed SSS by 1.5 percentage points

in the 2/11 quarter, a reversal from a recent high in the 11/10 quarter. This trend reversed again in the 5/11 quarter.

3. Definition of Same-Store Sales: In the past three 10-K filings, RT has not disclosed the SSS definition. However, the definition remained consistent in the interim periods so this does not seem to be a change in definition. RT did change its definition of SSS in the quarter ended 9/07. See below and (greater detail is available in our June 2009 Restaurant Review).

4. SSS relative performance: Past four quarters: -0.3% (20/26) Past sixteen quarters: -4.4% (26/26)

5. Other signals from SSS trends: None.

SAME-STORE SALES DEFINITION

Interim periods: no changes in quarterly disclosures

5/11 10K: No disclosure.

Interim periods: no changes in quarterly disclosures

6/10 10K: No disclosure.

6/08 10K: Same-restaurants are defined as those that have been open at least 18 months.

9/07 10Q: A year-over-year comparison of sales volumes for restaurants that, in the current year, have been open 18 months or longer in order to remove the impact of new openings in comparing the operations of existing restaurants (emphasis added by CFRA).

Interim periods: no change

6/06 10K: A year-over-year comparison of sales volumes for restaurants that, in the current year, have been open at least 19 months in order to remove the impact of new openings in comparing the operations of existing restaurants.

SUMMARY

SSS as a Key Metric: (+) None

(-) Inconsistency in disclosure of definition

Recent SSS Performance: Weakened towards the bottom of the group over the last four quar-ters and remains in the bottom for the past sixteen quarters.

Other Signals from SSS Trends: None.

Notes: SSS—Domestic Company Stores, Rev/Store—Domestic Company Revs & Stores

-15%

-10%

-5%

0%

5%

10%

8/113/118/103/109/093/099/083/089/073/07

RT

Rev/Store (YoY) SSS

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

28 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

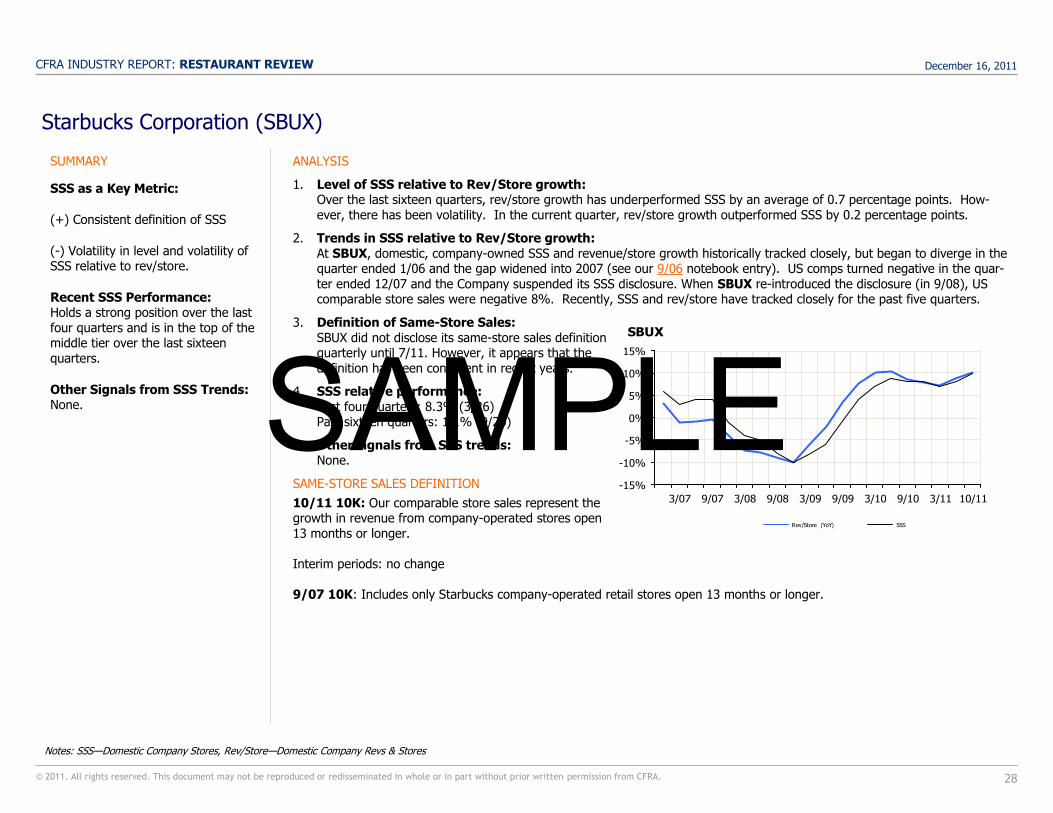

Starbucks Corporation (SBUX)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: Over the last sixteen quarters, rev/store growth has underperformed SSS by an average of 0.7 percentage points. How-ever, there has been volatility. In the current quarter, rev/store growth outperformed SSS by 0.2 percentage points.

2. Trends in SSS relative to Rev/Store growth: At SBUX, domestic, company-owned SSS and revenue/store growth historically tracked closely, but began to diverge in the quarter ended 1/06 and the gap widened into 2007 (see our 9/06 notebook entry). US comps turned negative in the quar-

ter ended 12/07 and the Company suspended its SSS disclosure. When SBUX re-introduced the disclosure (in 9/08), US comparable store sales were negative 8%. Recently, SSS and rev/store have tracked closely for the past five quarters.

3. Definition of Same-Store Sales: SBUX did not disclose its same-store sales definition quarterly until 7/11. However, it appears that the definition has been consistent in recent years.

4. SSS relative performance: Past four quarters: 8.3% (3/26) Past sixteen quarters: 1.1% (9/26)

5. Other signals from SSS trends: None.

SAME-STORE SALES DEFINITION

10/11 10K: Our comparable store sales represent the growth in revenue from company-operated stores open 13 months or longer. Interim periods: no change 9/07 10K: Includes only Starbucks company-operated retail stores open 13 months or longer.

SUMMARY

SSS as a Key Metric:

(+) Consistent definition of SSS

(-) Volatility in level and volatility of SSS relative to rev/store.

Recent SSS Performance: Holds a strong position over the last four quarters and is in the top of the middle tier over the last sixteen quarters.

Other Signals from SSS Trends: None.

Notes: SSS—Domestic Company Stores, Rev/Store—Domestic Company Revs & Stores

-15%

-10%

-5%

0%

5%

10%

15%

10/113/119/103/109/093/099/083/089/073/07

SBUX

Rev/Store (YoY) SSS

SAMPLE

December 16, 2011 CFRA INDUSTRY REPORT: RESTAURANT REVIEW

29 © 2011. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA.

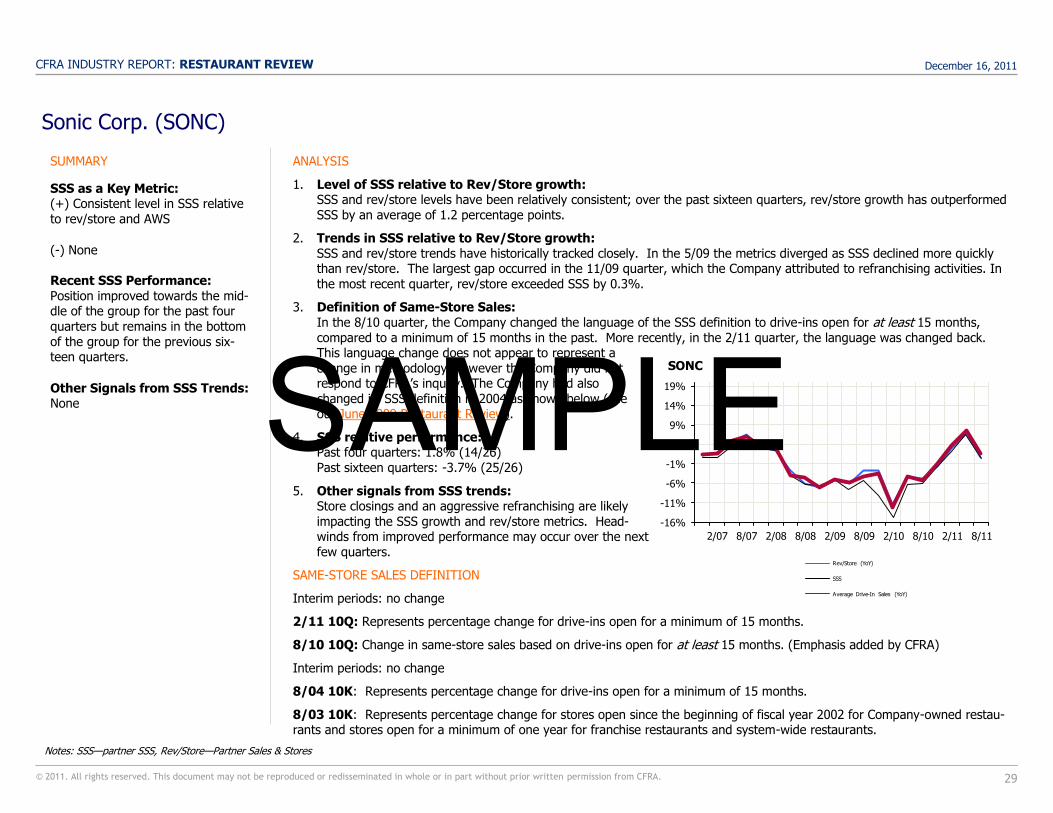

Sonic Corp. (SONC)

ANALYSIS

1. Level of SSS relative to Rev/Store growth: SSS and rev/store levels have been relatively consistent; over the past sixteen quarters, rev/store growth has outperformed SSS by an average of 1.2 percentage points.

2. Trends in SSS relative to Rev/Store growth: SSS and rev/store trends have historically tracked closely. In the 5/09 the metrics diverged as SSS declined more quickly than rev/store. The largest gap occurred in the 11/09 quarter, which the Company attributed to refranchising activities. In

the most recent quarter, rev/store exceeded SSS by 0.3%.

3. Definition of Same-Store Sales: In the 8/10 quarter, the Company changed the language of the SSS definition to drive-ins open for at least 15 months, compared to a minimum of 15 months in the past. More recently, in the 2/11 quarter, the language was changed back. This language change does not appear to represent a change in methodology, however the Company did not respond to CFRA’s inquiry. The Company had also changed its SSS definition in 2004 as shown below (see our June 2009 Restaurant Review).

4. SSS relative performance: Past four quarters: 1.8% (14/26) Past sixteen quarters: -3.7% (25/26)

5. Other signals from SSS trends: Store closings and an aggressive refranchising are likely impacting the SSS growth and rev/store metrics. Head-winds from improved performance may occur over the next few quarters.

SAME-STORE SALES DEFINITION

Interim periods: no change

2/11 10Q: Represents percentage change for drive-ins open for a minimum of 15 months.

8/10 10Q: Change in same-store sales based on drive-ins open for at least 15 months. (Emphasis added by CFRA)

Interim periods: no change

8/04 10K: Represents percentage change for drive-ins open for a minimum of 15 months.

8/03 10K: Represents percentage change for stores open since the beginning of fiscal year 2002 for Company-owned restau-rants and stores open for a minimum of one year for franchise restaurants and system-wide restaurants.

SUMMARY

SSS as a Key Metric: (+) Consistent level in SSS relative to rev/store and AWS

(-) None Recent SSS Performance:

Position improved towards the mid-dle of the group for the past four quarters but remains in the bottom of the group for the previous six-teen quarters.

Other Signals from SSS Trends: None

Notes: SSS—partner SSS, Rev/Store—Partner Sales & Stores

-16%

-11%

-6%

-1%

4%

9%

14%

19%