indiachem gujarat - tata strategic management group · federation house, 1 tansen marg ......

TRANSCRIPT

INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Mr. R K Bhatia (Head - Chemicals & Pharmaceuticals Division, FICCI)

Federation House, 1 Tansen MargNew Delhi-110 001

Tel. : 91-11-23316540 (D)/23357350 (D)EPBX : 91-11-23738760-70 (Extn.395/474)Fax : 91-11-23320714/233721504

E-mail : [email protected]

Ms. Ranjita C Sood (Asst. Director-Chemicals & Pharmaceuticals Division, FICCI)E-mail : [email protected]

Website : www.ficci.com

Pratik Kadakia (Practice Head - Chemical & Energy)E-mail : [email protected]

Abhishek Nigam E-mail : [email protected]

Nirmal, 18th Floor, Nariman PointMumbai-400021

Tel No. : 91-22-66376789Fax No. : 91-22-66376600Website : www.tsmg.com

Federation of Indian Chambers of Commerce and Industry

Disclaimer: All rights reserved. Includes copyrighted material.The same may not be reproduced, distributed, modified or in any manner communicated to any third party except with the written approval of Tata Strategic Management Group.This report is for information purpose only. While due care has been taken during the compilation of this report to ensure that the information is accurate to the best of Tata Strategic Management Group's knowledge and belief, the content is not to be construed in any manner whatsoever as a substitute for professional advice. Tata Strategic Management Group accepts no responsibility for any loss arising from any action taken or not taken by anyone basis this report.

INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Contents

Executive Summary

Introduction

Industry Reports

Thought Notes

About Tata Strategic Management Group

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Agrochemicals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Colourants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Other Specialty Chemicals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Indian Specialty Chemicals: When will growth return? . . . . . . . . 47

Green Chemistry: Building a greener future. . . . . . . . . . . . . . . . . 55

Outlook for personal care ingredients industry:. . . . . . . . . . . . . . 61

An Indian perspective

v

v

v

v

v

v

About (FICCI)

1INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Executive Summary

T

Agrochemicals

his FICCI report on the Indian Specialty Chemical Industry, prepared by Tata

Strategic Management Group, provides an overview of the Agrochemicals,

Colourants and Other Specialty Chemicals industry segments. The report

highlights the market size and growth, demand-supply scenario, trade overview and

market, technological & regulatory trends, ending with a brief future outlook for each

segment.

The Indian Chemical Industry forms the backbone of the industrial and agricultural

development of India and provides building blocks for downstream industries. The

industry has registered a growth of ~10% p.a. over the last few years and is currently

estimated to be around USD 50 billion. Specialty and knowledge chemicals put

together account for about half of the chemical industry and could grow at a higher

rate of ~14%-15% over the next few years.

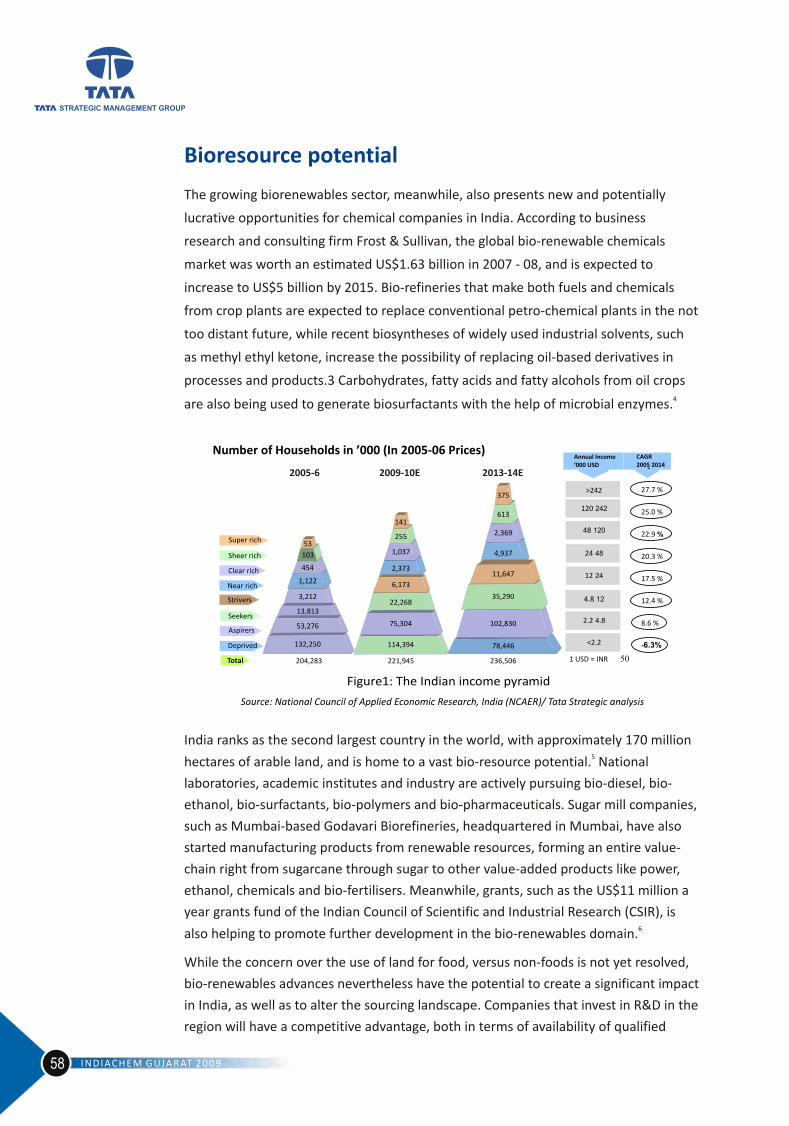

Over the years, Gujarat has become one of the most preferred locations for industrial

investment in India. Apart from having sound infrastructure facilities, skilled

manpower, excellent domestic and international connectivity and rich natural

resources, what works for Gujarat is a focus on industrial development in the state.

Gujarat has achieved an annual growth rate of 10.5% p.a. over the past five years and

contributes ~16% to the industrial production of the country. The chemical and

petrochemical industry in Gujarat is the fastest growing sector in the State's economy.

Gujarat is the leading producer of major chemicals in the country accounting for

almost half of national production.

As an allied industry of agriculture, which accounts for about one fifth of India's GDP,

the agrochemicals industry is a significant industry for the Indian economy. The Indian

agrochemicals market grew at a rate of 11% from around USD 1.22 billion in 2008 to

an estimated USD 1.36 billion in 2009. With 125 technical grade manufacturers and

800 formulators, India is the fourth largest producer of agrochemicals in the world

after USA, Japan and China. Indian agrochemical exports have shown an impressive

growth in the past few years driven by excess capacity and availability of cheap labor.

Exports account for almost 50% of the industry revenues. Government focus on

achieving food grain self sufficiency coupled with limited farmland availability is

expected to provide a further impetus to the industry.

1INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Executive Summary

T

Agrochemicals

his FICCI report on the Indian Specialty Chemical Industry, prepared by Tata

Strategic Management Group, provides an overview of the Agrochemicals,

Colourants and Other Specialty Chemicals industry segments. The report

highlights the market size and growth, demand-supply scenario, trade overview and

market, technological & regulatory trends, ending with a brief future outlook for each

segment.

The Indian Chemical Industry forms the backbone of the industrial and agricultural

development of India and provides building blocks for downstream industries. The

industry has registered a growth of ~10% p.a. over the last few years and is currently

estimated to be around USD 50 billion. Specialty and knowledge chemicals put

together account for about half of the chemical industry and could grow at a higher

rate of ~14%-15% over the next few years.

Over the years, Gujarat has become one of the most preferred locations for industrial

investment in India. Apart from having sound infrastructure facilities, skilled

manpower, excellent domestic and international connectivity and rich natural

resources, what works for Gujarat is a focus on industrial development in the state.

Gujarat has achieved an annual growth rate of 10.5% p.a. over the past five years and

contributes ~16% to the industrial production of the country. The chemical and

petrochemical industry in Gujarat is the fastest growing sector in the State's economy.

Gujarat is the leading producer of major chemicals in the country accounting for

almost half of national production.

As an allied industry of agriculture, which accounts for about one fifth of India's GDP,

the agrochemicals industry is a significant industry for the Indian economy. The Indian

agrochemicals market grew at a rate of 11% from around USD 1.22 billion in 2008 to

an estimated USD 1.36 billion in 2009. With 125 technical grade manufacturers and

800 formulators, India is the fourth largest producer of agrochemicals in the world

after USA, Japan and China. Indian agrochemical exports have shown an impressive

growth in the past few years driven by excess capacity and availability of cheap labor.

Exports account for almost 50% of the industry revenues. Government focus on

achieving food grain self sufficiency coupled with limited farmland availability is

expected to provide a further impetus to the industry.

2 INDIACHEM GUJARAT 2009

Colourants

Other Specialty Chemicals

The Indian dyes and pigments industry valued at ~ USD 3.7 billion dollars is about 7%

of the global market, supplying various dyes and organic pigments to the export

markets like Europe and United States. The slump in global demand and commodity

nature of several products has resulted in margin pressures for industry participants.

Also, there is a growing need for environment friendly products and processes driven

by regulations such as REACH (Registration, Evaluation and Authorization of Chemical

substances).

An innovative approach is required to help the industry overcome the above

challenges. Greater investments in research & development would help improve the

product portfolio focussing on specialty and high performance colourants. Adoption of

green chemistry practices could help the industry reduce its environmental footprint

and ensure continued access to export markets. This integrated approach will enable

the Indian colourants industry to maintain its growth momentum at over 8% p.a. over

the next few years.

Other specialty chemicals primarily consist of APIs (Active Pharmaceutical Ingredients),

paints & coatings chemicals, construction chemicals, polymer additives, water

treatment chemicals and personal care ingredients. API is the biggest segment valued

at ~USD 5 billion and is also the fastest growing at ~ 21% p.a. over the last 4 years

driven largely by CRAMS (Contract Research & Manufacturing Services). Paints &

coatings chemicals segment with a market size of ~USD 1.2 billion in 2008 is another

large segment. Other key segments include water treatment chemicals valued at ~USD

475 million, personal care ingredients valued at ~USD 300 million, construction

chemicals valued at USD 265 million and polymer additives valued at ~ USD 240

million in 2008. All these segments are expected to grow at rates above the chemical

industry average, based on growth in their respective end use industries and evolving

applications.

A separate section containing recent Thought Notes published by Tata Strategic

Management Group has been included. This section provides key insights on

contemporary trends and issues related to select segments of the Indian chemical

industry in general and specialty chemicals in particular.

Introduction

2 INDIACHEM GUJARAT 2009

Colourants

Other Specialty Chemicals

The Indian dyes and pigments industry valued at ~ USD 3.7 billion dollars is about 7%

of the global market, supplying various dyes and organic pigments to the export

markets like Europe and United States. The slump in global demand and commodity

nature of several products has resulted in margin pressures for industry participants.

Also, there is a growing need for environment friendly products and processes driven

by regulations such as REACH (Registration, Evaluation and Authorization of Chemical

substances).

An innovative approach is required to help the industry overcome the above

challenges. Greater investments in research & development would help improve the

product portfolio focussing on specialty and high performance colourants. Adoption of

green chemistry practices could help the industry reduce its environmental footprint

and ensure continued access to export markets. This integrated approach will enable

the Indian colourants industry to maintain its growth momentum at over 8% p.a. over

the next few years.

Other specialty chemicals primarily consist of APIs (Active Pharmaceutical Ingredients),

paints & coatings chemicals, construction chemicals, polymer additives, water

treatment chemicals and personal care ingredients. API is the biggest segment valued

at ~USD 5 billion and is also the fastest growing at ~ 21% p.a. over the last 4 years

driven largely by CRAMS (Contract Research & Manufacturing Services). Paints &

coatings chemicals segment with a market size of ~USD 1.2 billion in 2008 is another

large segment. Other key segments include water treatment chemicals valued at ~USD

475 million, personal care ingredients valued at ~USD 300 million, construction

chemicals valued at USD 265 million and polymer additives valued at ~ USD 240

million in 2008. All these segments are expected to grow at rates above the chemical

industry average, based on growth in their respective end use industries and evolving

applications.

A separate section containing recent Thought Notes published by Tata Strategic

Management Group has been included. This section provides key insights on

contemporary trends and issues related to select segments of the Indian chemical

industry in general and specialty chemicals in particular.

Introduction

5INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Federation of Indian Chambers of Commerce and Industry

Indian Chemical Industry

The Indian Chemical Industry forms the backbone of the industrial and agricultural

development of India and provides building blocks for downstream industries. The

chemical industry which includes, as per National Industrial Classification, basic

chemicals and its products, petrochemicals, fertilizers, paints and varnishes, gases,

soaps, perfumes and toiletries and pharmaceuticals is one of the most diversified of all

industrial sectors covering thousands of commercial products. The industry has

registered a growth of ~8-10% over the last few years and is currently estimated to be

around USD 50 billion.

The relevance of the chemical industry to the overall manufacturing sector can be

gauged by the fact that 'Basic chemicals and chemical products' account for 14% in

overall Index of Industrial Production (IIP). On an average the chemicals segment has

grown at a higher rate than the overall manufacturing industry. From the trade flow

perspective, exports of chemicals and petrochemicals together accounted for 10.9% of

country's total exports in the latest fiscal year. The corresponding figure for imports is

only 6.7%.

The Indian Chemicals Industry comprises both small and large-scale units. The fiscal

concessions granted to the small sector in mid-eighties led to the establishment of a

large number of units in the Small Scale Industries (SSI) sector. A large number of

MNCs also participate in the industry. In the Chemical Sector, 100 percent FDI is

permissible. Manufacture of most chemical products including organic/ inorganic,

dyestuffs and pesticides is delicensed.

Introduction

Indian Chemical Industry(USD billion)

Source: Tata Strategic Estimates

28

50

2003 2008

5INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Federation of Indian Chambers of Commerce and Industry

Indian Chemical Industry

The Indian Chemical Industry forms the backbone of the industrial and agricultural

development of India and provides building blocks for downstream industries. The

chemical industry which includes, as per National Industrial Classification, basic

chemicals and its products, petrochemicals, fertilizers, paints and varnishes, gases,

soaps, perfumes and toiletries and pharmaceuticals is one of the most diversified of all

industrial sectors covering thousands of commercial products. The industry has

registered a growth of ~8-10% over the last few years and is currently estimated to be

around USD 50 billion.

The relevance of the chemical industry to the overall manufacturing sector can be

gauged by the fact that 'Basic chemicals and chemical products' account for 14% in

overall Index of Industrial Production (IIP). On an average the chemicals segment has

grown at a higher rate than the overall manufacturing industry. From the trade flow

perspective, exports of chemicals and petrochemicals together accounted for 10.9% of

country's total exports in the latest fiscal year. The corresponding figure for imports is

only 6.7%.

The Indian Chemicals Industry comprises both small and large-scale units. The fiscal

concessions granted to the small sector in mid-eighties led to the establishment of a

large number of units in the Small Scale Industries (SSI) sector. A large number of

MNCs also participate in the industry. In the Chemical Sector, 100 percent FDI is

permissible. Manufacture of most chemical products including organic/ inorganic,

dyestuffs and pesticides is delicensed.

Introduction

Indian Chemical Industry(USD billion)

Source: Tata Strategic Estimates

28

50

2003 2008

6 INDIACHEM GUJARAT 2009

Specialty Chemicals Overview

Specialty chemicals are defined as a "group of relatively high value, low volume

chemicals known for their end use applications and/ or performance enhancing

properties." In contrast to base or commodity chemicals, specialty chemicals are

recognized for 'what they do' and not 'what they are'. It is a highly knowledge driven

industry with raw materials cost as percentage of net sales much lower than for

commodity chemicals. The critical success factors for the industry include

understanding of customer needs and product/ application development to meet the

same at a favourable price-performance ratio.

The specialty chemicals segment including the knowledge chemicals constitutes about

half of the Indian Chemical industry. The specialty chemicals segment caters to a large

number of end use industries including construction, automotive, polymers, personal

care, water treatment, textile, paints and coatings, etc. The knowledge chemicals

segment caters to the key end use industries of pharmaceuticals, agrochemicals and

bio- technology.

The specialty and knowledge chemicals industry combined has been growing at rates

higher than the overall chemical industry and is expected to continue to grow at 14%-

15% p.a. to reach 40 billion USD by 2012. The growth slowdown, demand contraction

and recovery witnessed over the last year or so have not impacted the long-term

growth prospects of the industry.

Industry Report

12

18

40

2002 2006 2012

Indian Specialty & KnowledgeChemicals Industry(USD million)

11%

xx%

CAGR

14%

Source: Tata Strategic Estimates

6 INDIACHEM GUJARAT 2009

Specialty Chemicals Overview

Specialty chemicals are defined as a "group of relatively high value, low volume

chemicals known for their end use applications and/ or performance enhancing

properties." In contrast to base or commodity chemicals, specialty chemicals are

recognized for 'what they do' and not 'what they are'. It is a highly knowledge driven

industry with raw materials cost as percentage of net sales much lower than for

commodity chemicals. The critical success factors for the industry include

understanding of customer needs and product/ application development to meet the

same at a favourable price-performance ratio.

The specialty chemicals segment including the knowledge chemicals constitutes about

half of the Indian Chemical industry. The specialty chemicals segment caters to a large

number of end use industries including construction, automotive, polymers, personal

care, water treatment, textile, paints and coatings, etc. The knowledge chemicals

segment caters to the key end use industries of pharmaceuticals, agrochemicals and

bio- technology.

The specialty and knowledge chemicals industry combined has been growing at rates

higher than the overall chemical industry and is expected to continue to grow at 14%-

15% p.a. to reach 40 billion USD by 2012. The growth slowdown, demand contraction

and recovery witnessed over the last year or so have not impacted the long-term

growth prospects of the industry.

Industry Report

12

18

40

2002 2006 2012

Indian Specialty & KnowledgeChemicals Industry(USD million)

11%

xx%

CAGR

14%

Source: Tata Strategic Estimates

9INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Industry Report

Gujarat: A Favoured Investment Destination

Chemical Industry in Gujarat

Over the years, Gujarat has become one of the most preferred locations for industrial

investment in India. Gujarat is spearheading Indian march for global economic

superpower status due to its inherent entrepreneurial spirit. Apart from having sound

infrastructure facilities, skilled manpower, excellent domestic and international

connectivity and rich natural resources, what works for Gujarat is a government that

has focused on industrial development in the state. Besides progressive reforms,

annual industrial summits and seminars are conducted to boost industrial

development in the state. These summits offer a perfect platform for business leaders,

investors, corporations, thought leaders, policy and opinion makers to understand and

explore business opportunities with the state of Gujarat. Gujarat has achieved an

annual growth rate of 10.5% over the past five years and contributes ~16% to the

industrial production of the country. As per the Vibrant Gujarat Summit 2009 report,

MOUs worth over USD 250 billion were signed across various industrial sectors.

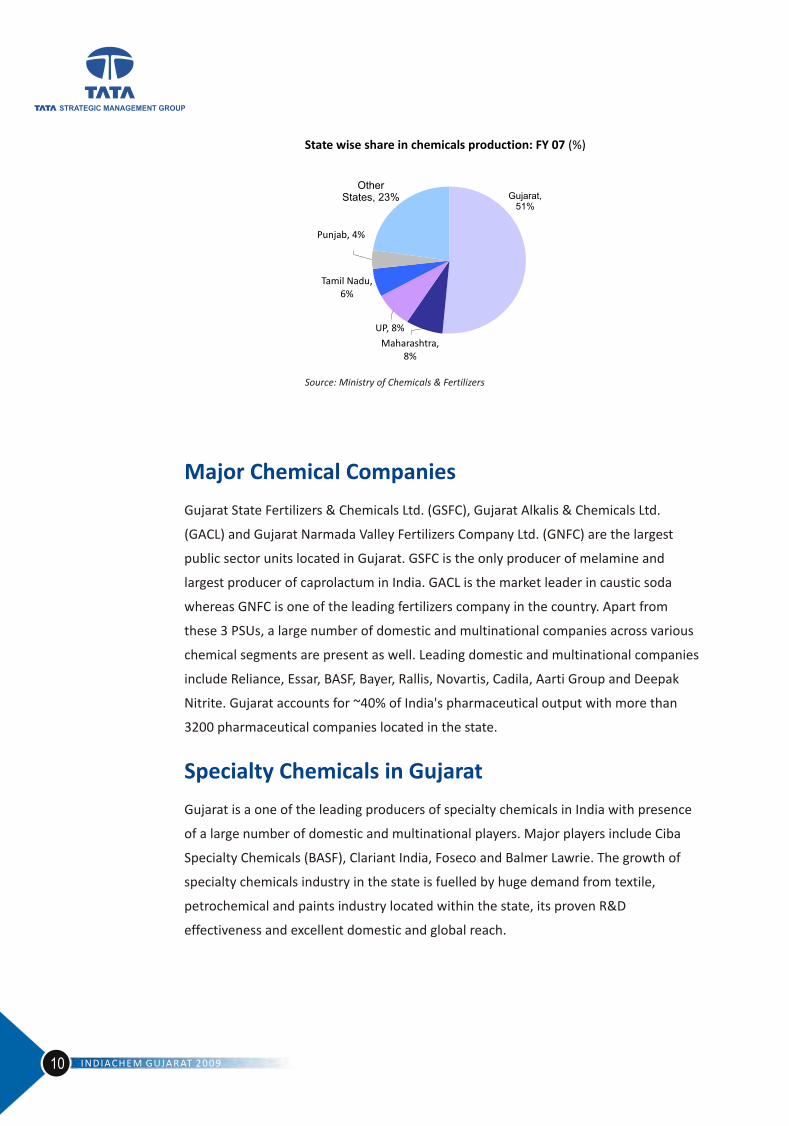

The chemical and petrochemical industry in Gujarat is the fastest growing sector in the

State's economy and Gujarat is the leading producer of major chemicals in the country

with a share of 51% in FY 07. Major chemical industries located in Gujarat include

pharmaceutical, dyestuff, paints, bulk, specialty and fine chemicals. Key characteristics

of the chemical industry in Gujarat include high focus on domestic demand and limited

focus on exports as well as high fragmentation.

100

5040

23

40

Infrastructure Manufacturing InvestmentRegions

UrbanDevelopment

Others

MOUs signed by sector: 2009 (USD billion)

Source: Vibrant Gujarat

Chemicals & Petrochemicals:~ USD 9 billion

Oil & Gas, Power:~ USD 73 billion

9INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Industry Report

Gujarat: A Favoured Investment Destination

Chemical Industry in Gujarat

Over the years, Gujarat has become one of the most preferred locations for industrial

investment in India. Gujarat is spearheading Indian march for global economic

superpower status due to its inherent entrepreneurial spirit. Apart from having sound

infrastructure facilities, skilled manpower, excellent domestic and international

connectivity and rich natural resources, what works for Gujarat is a government that

has focused on industrial development in the state. Besides progressive reforms,

annual industrial summits and seminars are conducted to boost industrial

development in the state. These summits offer a perfect platform for business leaders,

investors, corporations, thought leaders, policy and opinion makers to understand and

explore business opportunities with the state of Gujarat. Gujarat has achieved an

annual growth rate of 10.5% over the past five years and contributes ~16% to the

industrial production of the country. As per the Vibrant Gujarat Summit 2009 report,

MOUs worth over USD 250 billion were signed across various industrial sectors.

The chemical and petrochemical industry in Gujarat is the fastest growing sector in the

State's economy and Gujarat is the leading producer of major chemicals in the country

with a share of 51% in FY 07. Major chemical industries located in Gujarat include

pharmaceutical, dyestuff, paints, bulk, specialty and fine chemicals. Key characteristics

of the chemical industry in Gujarat include high focus on domestic demand and limited

focus on exports as well as high fragmentation.

100

5040

23

40

Infrastructure Manufacturing InvestmentRegions

UrbanDevelopment

Others

MOUs signed by sector: 2009 (USD billion)

Source: Vibrant Gujarat

Chemicals & Petrochemicals:~ USD 9 billion

Oil & Gas, Power:~ USD 73 billion

10 INDIACHEM GUJARAT 2009

Major Chemical Companies

Specialty Chemicals in Gujarat

Gujarat State Fertilizers & Chemicals Ltd. (GSFC), Gujarat Alkalis & Chemicals Ltd.

(GACL) and Gujarat Narmada Valley Fertilizers Company Ltd. (GNFC) are the largest

public sector units located in Gujarat. GSFC is the only producer of melamine and

largest producer of caprolactum in India. GACL is the market leader in caustic soda

whereas GNFC is one of the leading fertilizers company in the country. Apart from

these 3 PSUs, a large number of domestic and multinational companies across various

chemical segments are present as well. Leading domestic and multinational companies

include Reliance, Essar, BASF, Bayer, Rallis, Novartis, Cadila, Aarti Group and Deepak

Nitrite. Gujarat accounts for ~40% of India's pharmaceutical output with more than

3200 pharmaceutical companies located in the state.

Gujarat is a one of the leading producers of specialty chemicals in India with presence

of a large number of domestic and multinational players. Major players include Ciba

Specialty Chemicals (BASF), Clariant India, Foseco and Balmer Lawrie. The growth of

specialty chemicals industry in the state is fuelled by huge demand from textile,

petrochemical and paints industry located within the state, its proven R&D

effectiveness and excellent domestic and global reach.

Punjab, 4%

Tamil Nadu, 6%

OtherStates, 23%

Maharashtra,8%

Gujarat,51%

UP, 8%

State wise share in chemicals production: FY 07 (%)

Source: Ministry of Chemicals & Fertilizers

Agrochemicals

10 INDIACHEM GUJARAT 2009

Major Chemical Companies

Specialty Chemicals in Gujarat

Gujarat State Fertilizers & Chemicals Ltd. (GSFC), Gujarat Alkalis & Chemicals Ltd.

(GACL) and Gujarat Narmada Valley Fertilizers Company Ltd. (GNFC) are the largest

public sector units located in Gujarat. GSFC is the only producer of melamine and

largest producer of caprolactum in India. GACL is the market leader in caustic soda

whereas GNFC is one of the leading fertilizers company in the country. Apart from

these 3 PSUs, a large number of domestic and multinational companies across various

chemical segments are present as well. Leading domestic and multinational companies

include Reliance, Essar, BASF, Bayer, Rallis, Novartis, Cadila, Aarti Group and Deepak

Nitrite. Gujarat accounts for ~40% of India's pharmaceutical output with more than

3200 pharmaceutical companies located in the state.

Gujarat is a one of the leading producers of specialty chemicals in India with presence

of a large number of domestic and multinational players. Major players include Ciba

Specialty Chemicals (BASF), Clariant India, Foseco and Balmer Lawrie. The growth of

specialty chemicals industry in the state is fuelled by huge demand from textile,

petrochemical and paints industry located within the state, its proven R&D

effectiveness and excellent domestic and global reach.

Punjab, 4%

Tamil Nadu, 6%

OtherStates, 23%

Maharashtra,8%

Gujarat,51%

UP, 8%

State wise share in chemicals production: FY 07 (%)

Source: Ministry of Chemicals & Fertilizers

Agrochemicals

13INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Agrochemicals

Introduction

Global Agrochemicals Industry

Indian Agrochemicals Industry

Agrochemicals or pesticides are chemical substances used to ward off, kill or control

pests, unwanted plants or animals that may harm or damage the crops. Agrochemicals

can be classified into the following key segments:

1. Insecticides

2. Herbicides/ Weedicides

3. Fungicides

4. Bio-pesticides

5. Others (Nematocides, Rodenticides etc.)

Global Agrochemical industry grew at a CAGR of 9.3% from 2003 to reach USD 41.7

billion in 2008.

North America, European Union and Asia Pacific together consume over 75% of the

world's agrochemicals. Globally, herbicides are the largest consumed agrochemical

with a share of 45% followed by insecticides at 33%.

Industry Overview

As an allied industry of agriculture, which accounts for 18.5 percent of India's GDP, the

agrochemicals industry is a significant industry for the Indian economy. The Indian

agrochemicals market grew at a rate of 11% from USD 1.22 billion in 2008 to an

estimated USD 1.36 billion in 2009.

25.8 25.2 26.730.7 31.2 30.4

33.4

41.7

-2.4

6.2

15

1.5-2.5

9.7

25

2001 2002 2003 2004 2005 2006 2007 2008

Market Size % yoy growth

Source : Industry Report

Market Size (USD Bn)

25.8 25.2 26.730.7 31.2 30.4

33.4

41.7

-2.4

6.2

15

1.5-2.5

9.7

25

2001 2002 2003 2004 2005 2006 2007 2008

Market Size % yoy growth

Source : Industry Report

Market Size (USD Bn)

13INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Agrochemicals

Introduction

Global Agrochemicals Industry

Indian Agrochemicals Industry

Agrochemicals or pesticides are chemical substances used to ward off, kill or control

pests, unwanted plants or animals that may harm or damage the crops. Agrochemicals

can be classified into the following key segments:

1. Insecticides

2. Herbicides/ Weedicides

3. Fungicides

4. Bio-pesticides

5. Others (Nematocides, Rodenticides etc.)

Global Agrochemical industry grew at a CAGR of 9.3% from 2003 to reach USD 41.7

billion in 2008.

North America, European Union and Asia Pacific together consume over 75% of the

world's agrochemicals. Globally, herbicides are the largest consumed agrochemical

with a share of 45% followed by insecticides at 33%.

Industry Overview

As an allied industry of agriculture, which accounts for 18.5 percent of India's GDP, the

agrochemicals industry is a significant industry for the Indian economy. The Indian

agrochemicals market grew at a rate of 11% from USD 1.22 billion in 2008 to an

estimated USD 1.36 billion in 2009.

25.8 25.2 26.730.7 31.2 30.4

33.4

41.7

-2.4

6.2

15

1.5-2.5

9.7

25

2001 2002 2003 2004 2005 2006 2007 2008

Market Size % yoy growth

Source : Industry Report

Market Size (USD Bn)

25.8 25.2 26.730.7 31.2 30.4

33.4

41.7

-2.4

6.2

15

1.5-2.5

9.7

25

2001 2002 2003 2004 2005 2006 2007 2008

Market Size % yoy growth

Source : Industry Report

Market Size (USD Bn)

15INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

14 INDIACHEM GUJARAT 2009

India is the fourth largest producer of agrochemicals in the world after the United

States, Japan and China. On the other hand India's agrochemicals consumption is one

of the lowest in the world with per hectare consumption of just 0.38 kg compared to

US (4.5 Kg/hectare) and Japan (11 Kg/hectare).

In India, there are about 125 technical grade manufacturers (10 multinationals), 800

formulators, over 145,000 distributors. 60 technical grade pesticides are being

manufactured indigenously.

Technical grade manufacturers sell high purity chemicals in bulk (generally in drums of

200-250 Kgs) to formulators. Formulators, in turn, prepare formulations by adding

inert carriers, solvents, surface active agents, deodorants etc. These formulations are

packed for retail sale and bought by the farmers.

Considering the high dependence upon monsoons, the market for agrochemicals is

expected to grow at a conservative growth rate of 7.5% to reach ~ USD 1.7 billion by

2012. Key market drivers include:

1. Growth in demand for food grains: Increasing population and high emphasis on

achieving food grain self-sufficiency as highlighted in the 2009-10 budget, is

expected to drive growth.

2. Limited farmland availability: Exports are a significant fraction of the Indian

agrochemical output. Available arable land per capita has been reducing globally

and is expected to reduce further.

Indian agriculture has the daunting task of feeding and clothing 16 percent of the

world's population from less than 2 percent of the total landmass. With already 190

million hectares of gross cultivated area, the scope for bringing new areas under

cultivation is severely limited. Thus the pressure is to increase yield per hectare by

increasing usage of agrochemicals

Industry Structure

Growth Forecast & Drivers

3. Growth of horticulture & floriculture: While the Indian floriculture industry has

grown by 50% in last 3 years, Government of India has launched a national

horticulture mission to double production by 2012. Flourishing horticulture &

floriculture industries will need increasing amounts of agrochemicals, especially

fungicides.

Industry Structure

RawMaterialSupplier

TechnicalGrade

Manufacturer

Distributor/Retailer

EndUser

Formulator

0.15

0.27

1998 2015E

Source: Yara Fertilizer Handbook, PotashCorp

World- Available arable land per capita (Hectare)

Fungicides,21%

Herbicides,18%

Biopesticides &Ohers, 8%

Insecticides,53%

Product Shares 2008 (%)

Source: Industry Report, Tata Strategic Estimates

4. Increasing awareness: Government of India estimates suggest that the total value

of crops lost due to non-use of pesticides is around USD 17 billion every year.

Companies are increasing their marketing efforts in order to train farmers about

the right use of agrochemicals in terms of quantity to be used, the right application

methodology and which chemicals to use for which kind of pest problems. With

increased awareness, the use of agrochemicals will also increase.

Key Segments

146

205

300

2002 2007 2012E

Source: Horticulture Commissioner, National Horticulture Mission

Horticultural Production, India (MnTonnes)

C AGR : 7. 5%:

15INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

14 INDIACHEM GUJARAT 2009

India is the fourth largest producer of agrochemicals in the world after the United

States, Japan and China. On the other hand India's agrochemicals consumption is one

of the lowest in the world with per hectare consumption of just 0.38 kg compared to

US (4.5 Kg/hectare) and Japan (11 Kg/hectare).

In India, there are about 125 technical grade manufacturers (10 multinationals), 800

formulators, over 145,000 distributors. 60 technical grade pesticides are being

manufactured indigenously.

Technical grade manufacturers sell high purity chemicals in bulk (generally in drums of

200-250 Kgs) to formulators. Formulators, in turn, prepare formulations by adding

inert carriers, solvents, surface active agents, deodorants etc. These formulations are

packed for retail sale and bought by the farmers.

Considering the high dependence upon monsoons, the market for agrochemicals is

expected to grow at a conservative growth rate of 7.5% to reach ~ USD 1.7 billion by

2012. Key market drivers include:

1. Growth in demand for food grains: Increasing population and high emphasis on

achieving food grain self-sufficiency as highlighted in the 2009-10 budget, is

expected to drive growth.

2. Limited farmland availability: Exports are a significant fraction of the Indian

agrochemical output. Available arable land per capita has been reducing globally

and is expected to reduce further.

Indian agriculture has the daunting task of feeding and clothing 16 percent of the

world's population from less than 2 percent of the total landmass. With already 190

million hectares of gross cultivated area, the scope for bringing new areas under

cultivation is severely limited. Thus the pressure is to increase yield per hectare by

increasing usage of agrochemicals

Industry Structure

Growth Forecast & Drivers

3. Growth of horticulture & floriculture: While the Indian floriculture industry has

grown by 50% in last 3 years, Government of India has launched a national

horticulture mission to double production by 2012. Flourishing horticulture &

floriculture industries will need increasing amounts of agrochemicals, especially

fungicides.

Industry Structure

RawMaterialSupplier

TechnicalGrade

Manufacturer

Distributor/Retailer

EndUser

Formulator

0.15

0.27

1998 2015E

Source: Yara Fertilizer Handbook, PotashCorp

World- Available arable land per capita (Hectare)

Fungicides,21%

Herbicides,18%

Biopesticides &Ohers, 8%

Insecticides,53%

Product Shares 2008 (%)

Source: Industry Report, Tata Strategic Estimates

4. Increasing awareness: Government of India estimates suggest that the total value

of crops lost due to non-use of pesticides is around USD 17 billion every year.

Companies are increasing their marketing efforts in order to train farmers about

the right use of agrochemicals in terms of quantity to be used, the right application

methodology and which chemicals to use for which kind of pest problems. With

increased awareness, the use of agrochemicals will also increase.

Key Segments

146

205

300

2002 2007 2012E

Source: Horticulture Commissioner, National Horticulture Mission

Horticultural Production, India (MnTonnes)

C AGR : 7. 5%:

17INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

16 INDIACHEM GUJARAT 2009

Insecticides: Insecticides are used to ward off or kill insects. Consumption of

insecticides for cotton has come down to 50% from 63% of total volume after

introduction of BT cotton.

Fungicides: Fungicides are used to control disease attacks on crops. The growing

horticulture market in India owing to the government support has given a boost to

fungicide usage. The market share of fungicides has increased from 17% in 2005 to

21% in 2008.

Herbicides: Herbicides are the fastest growing segment of agrochemicals. Their main

competition is cheap labor which is employed to manually pull out weeds. Sales are

seasonal, owing to the fact that weeds flourish in damp, warm weather and die in cold

spells.

Supply Overview and Trade Flow

The Indian agrochemicals market is characterized by low capacity utilization. The

industry suffers from high inventory (owing to seasonal & irregular demand on

account of monsoons) and long credit periods to farmers, thus making operations

'working capital' intensive.

Stored produceZinc Phosphide

Phosphide, AluminiumOthers

Rice, Tobacco

Maize,Spinosyns, neem-based Bio-pesticides

Rice, Wheat Glyphosate, Isoproturon, 2,4-DHerbicides

Fruits, Vegetables,Rice

MancozebZiram

, Copper Oxychloride,Fungicides

Cotton, Rice Acephate, Cypermethrin

Monocrotophos,Insecticides

Main ApplicationsMajor ProductsSegment

Bio-pesticides: Bio-pesticides are pesticides derived from natural materials like

animals, plants, bacteria and certain minerals. For instance, neem has pesticidal

properties and is used for production of certain bio-pesticides. Currently a small

segment, bio-pesticides market is expected to grow in the future owing to government

support and increasing awareness about use of non-toxic, environment friendly

pesticides.

Others: Plant growth regulators, Nematocides, Rodenticides, Fumigants etc.

Rodenticides and plant growth regulators are the stars of this segment.

Change in Share (% of total)

10%

21%

10%

18%

8%

80%

53%

2000 2007

Insecticides HerbicidesFungicides Biopesticides & others

Source: Industry Report, Tata Strategic Estimates

Installed Capacity and production

148 145 146

82 85 83

2005 2006 2007

Capacity Production

Source: Department of Chemicals, Government of India

The total installed capacity in 2007 was 146,000 MT and total production was 83,430

MT leading to a low capacity utilization of 57%.

The Indian export market has grown from ~ USD 180 million in 1999 to ~ USD 600

million in 2008 with a CAGR of ~ 14% driven by underutilized capacity and shut down

of production capacity in China before Olympics 2008. Key export destinations are

USA, U.K., Russia, France, Netherlands, Belgium, Spain, South Africa, Bangladesh,

Malaysia and Singapore. Imports in the agrochemical sector are around 2.5% in

volume. Imports mainly consist of new generation pesticides and patented molecules.

82.2 84.7 83.4

2.2 2.2 1.8

24.2

33.025.0

60.253.9

60.3

2005 2006 2007

Production Import Export Consumption

Import-Export Overview

(‘000 MT)

Note: Consumption = Production + Import-

Export

Source: Department of Chemicals, Government of India

17INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

16 INDIACHEM GUJARAT 2009

Insecticides: Insecticides are used to ward off or kill insects. Consumption of

insecticides for cotton has come down to 50% from 63% of total volume after

introduction of BT cotton.

Fungicides: Fungicides are used to control disease attacks on crops. The growing

horticulture market in India owing to the government support has given a boost to

fungicide usage. The market share of fungicides has increased from 17% in 2005 to

21% in 2008.

Herbicides: Herbicides are the fastest growing segment of agrochemicals. Their main

competition is cheap labor which is employed to manually pull out weeds. Sales are

seasonal, owing to the fact that weeds flourish in damp, warm weather and die in cold

spells.

Supply Overview and Trade Flow

The Indian agrochemicals market is characterized by low capacity utilization. The

industry suffers from high inventory (owing to seasonal & irregular demand on

account of monsoons) and long credit periods to farmers, thus making operations

'working capital' intensive.

Stored produceZinc Phosphide

Phosphide, AluminiumOthers

Rice, Tobacco

Maize,Spinosyns, neem-based Bio-pesticides

Rice, Wheat Glyphosate, Isoproturon, 2,4-DHerbicides

Fruits, Vegetables,Rice

MancozebZiram

, Copper Oxychloride,Fungicides

Cotton, Rice Acephate, Cypermethrin

Monocrotophos,Insecticides

Main ApplicationsMajor ProductsSegment

Bio-pesticides: Bio-pesticides are pesticides derived from natural materials like

animals, plants, bacteria and certain minerals. For instance, neem has pesticidal

properties and is used for production of certain bio-pesticides. Currently a small

segment, bio-pesticides market is expected to grow in the future owing to government

support and increasing awareness about use of non-toxic, environment friendly

pesticides.

Others: Plant growth regulators, Nematocides, Rodenticides, Fumigants etc.

Rodenticides and plant growth regulators are the stars of this segment.

Change in Share (% of total)

10%

21%

10%

18%

8%

80%

53%

2000 2007

Insecticides HerbicidesFungicides Biopesticides & others

Source: Industry Report, Tata Strategic Estimates

Installed Capacity and production

148 145 146

82 85 83

2005 2006 2007

Capacity Production

Source: Department of Chemicals, Government of India

The total installed capacity in 2007 was 146,000 MT and total production was 83,430

MT leading to a low capacity utilization of 57%.

The Indian export market has grown from ~ USD 180 million in 1999 to ~ USD 600

million in 2008 with a CAGR of ~ 14% driven by underutilized capacity and shut down

of production capacity in China before Olympics 2008. Key export destinations are

USA, U.K., Russia, France, Netherlands, Belgium, Spain, South Africa, Bangladesh,

Malaysia and Singapore. Imports in the agrochemical sector are around 2.5% in

volume. Imports mainly consist of new generation pesticides and patented molecules.

82.2 84.7 83.4

2.2 2.2 1.8

24.2

33.025.0

60.253.9

60.3

2005 2006 2007

Production Import Export Consumption

Import-Export Overview

(‘000 MT)

Note: Consumption = Production + Import-

Export

Source: Department of Chemicals, Government of India

18 INDIACHEM GUJARAT 2009 19INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Competitive Landscape

With 800 formulators, the Indian agrochemicals market is highly fragmented in nature.

The competition is fierce with large number of organized sector players and a

significant spurious pesticides market. Market entry barriers are low with low start-up

costs. The market has been witnessing mergers and acquisitions with large players

buying out small manufacturers.

Market Trends

Technology Trends

The market is gradually moving towards environmentally safe options. This may lead

to increasing R&D in Biopesticides segment. The Government of India is promoting

research on the use of alternative and safe pesticides using neem seeds. The

Department of Chemicals has initiated a nationwide programme for “Development

and production of neem products as Environment Friendly Pesticides” with financial

assistance from United Nations Development Programme (UNDP).

Large market players are focusing on brand building by conducting awareness camps

for farmers and providing complete solutions. Strategic alliances with other players,

backward integration and increased marketing efforts are the key trends in the

agrochemicals industry.

On the technology front, increased R&D is expected for development of new

molecules and low dosage, high potency molecules.

New segments like Seed treatment chemicals, Bio-pesticides and Semiochemicals will

see technological advancements.

Brief Profile of key companies

21 manufacturing sites – 9 in India with licensed capacity of 91,000 onnes for pesticides and 41,000 Tonnes for pesticide intermediates

Production Capacity

Integration of Advanta with UPL to realize acquisition synergies

Future Plans

Acquisition of Advanta BV, Netherlands (2006), Cerexagri, France (2007)

Key Alliances

Key Brands

Sales (FY 2009)

Market Segments

Player

Insecticide –Viraat

Herbicide –Devrinol, Orrja

Fungicide –Saafe, Zeemil

Rs. 2100 Crores (Crop protection)

Crop Protection, Industrial & Specialty Chemicals, Seeds

United Phosphorous Ltd. (UPL)

21 manufacturing sites – 9 in India with licensed capacity of 91,000 onnes for pesticides and 41,000 Tonnes for pesticide intermediates

Production Capacity

Integration of Advanta with UPL to realize acquisition synergies

Future Plans

Acquisition of Advanta BV, Netherlands (2006), Cerexagri, France (2007)

Key Alliances

Key Brands

Sales (FY 2009)

Market Segments

Player

Insecticide –Viraat

Herbicide –Devrinol, Orrja

Fungicide –Saafe, Zeemil

Rs. 2100 Crores (Crop protection)

Crop Protection, Industrial & Specialty Chemicals, Seeds

United Phosphorous Ltd. (UPL)

Production facilities at Thane, Himatnagarand Ankleshwar with combined capacity of 6300 Tons for Active ingredients and 7650 Tons for powder formulations and 10,000 KL for liquid formulations

Production Capacity

R&D focus on environmentally safe products

Fungicides - Fluopyram, Bixafen and Isotianilscheduled for launch in 2010 and 2011, three other candidates at an advanced stage of development

Future Plans

R&D alliance with GVK Biosciences for active ingredients

Key Alliances

Key Brands

Sales (FY 2009)

Market Segments

Player

Fungicide –Antracol, Folicur

Insecticide –Confidor, Calypso

Herbicide –Atlantis, Topstar

Rs. 1482 Crores

Crop Protection, Non-agricultural pest management, Plant & seeds biotechnology

Bayer CropScience Ltd.

Production facilities at Thane, Himatnagarand Ankleshwar with combined capacity of 6300 Tons for Active ingredients and 7650 Tons for powder formulations and 10,000 KL for liquid formulations

Production Capacity

R&D focus on environmentally safe products

Fungicides - Fluopyram, Bixafen and Isotianilscheduled for launch in 2010 and 2011, three other candidates at an advanced stage of development

Future Plans

R&D alliance with GVK Biosciences for active ingredients

Key Alliances

Key Brands

Sales (FY 2009)

Market Segments

Player

Fungicide –Antracol, Folicur

Insecticide –Confidor, Calypso

Herbicide –Atlantis, Topstar

Rs. 1482 Crores

Crop Protection, Non-agricultural pest management, Plant & seeds biotechnology

Bayer CropScience Ltd.

Factories at Akola, Ankleshwar, Lote, Turbhe, Patancheru with production capacity of 10,000 MTPA for technical grades and 30,000 Tons/Litres for formulations

Production Capacity

Eight new molecules under R&D

Plans to become Global supplier for Active Ingredients (AI). Target of cumulative sales of Rs. 1000 Crores from AI in the next 5 years. New AI plant in Dahej to be ready by June 2010

Future Plans

Marketing alliances with FMC, Dupont, Syngenta, Bayer, Nihon Nohayaku

Key Alliances

Key Brands

Sales (FY 2009)

Market Segments

Player

Fungicide –Contaf, Contaf Plus, Master

Insecticide –Rogor, Daksh, Tata Mida

Herbicide –Fateh, Tata Metri

Domestic: Rs. 541.7 Crores,

Export: Rs 295 Crores

Pesticides, Plant Nutrients, Seeds, Leather Chemicals

Rallis India Ltd.

Factories at Akola, Ankleshwar, Lote, Turbhe, Patancheru with production capacity of 10,000 MTPA for technical grades and 30,000 Tons/Litres for formulations

Production Capacity

Eight new molecules under R&D

Plans to become Global supplier for Active Ingredients (AI). Target of cumulative sales of Rs. 1000 Crores from AI in the next 5 years. New AI plant in Dahej to be ready by June 2010

Future Plans

Marketing alliances with FMC, Dupont, Syngenta, Bayer, Nihon Nohayaku

Key Alliances

Key Brands

Sales (FY 2009)

Market Segments

Player

Fungicide –Contaf, Contaf Plus, Master

Insecticide –Rogor, Daksh, Tata Mida

Herbicide –Fateh, Tata Metri

Domestic: Rs. 541.7 Crores,

Export: Rs 295 Crores

Pesticides, Plant Nutrients, Seeds, Leather Chemicals

Rallis India Ltd.

18 INDIACHEM GUJARAT 2009 19INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Competitive Landscape

With 800 formulators, the Indian agrochemicals market is highly fragmented in nature.

The competition is fierce with large number of organized sector players and a

significant spurious pesticides market. Market entry barriers are low with low start-up

costs. The market has been witnessing mergers and acquisitions with large players

buying out small manufacturers.

Market Trends

Technology Trends

The market is gradually moving towards environmentally safe options. This may lead

to increasing R&D in Biopesticides segment. The Government of India is promoting

research on the use of alternative and safe pesticides using neem seeds. The

Department of Chemicals has initiated a nationwide programme for “Development

and production of neem products as Environment Friendly Pesticides” with financial

assistance from United Nations Development Programme (UNDP).

Large market players are focusing on brand building by conducting awareness camps

for farmers and providing complete solutions. Strategic alliances with other players,

backward integration and increased marketing efforts are the key trends in the

agrochemicals industry.

On the technology front, increased R&D is expected for development of new

molecules and low dosage, high potency molecules.

New segments like Seed treatment chemicals, Bio-pesticides and Semiochemicals will

see technological advancements.

Brief Profile of key companies

21 manufacturing sites – 9 in India with licensed capacity of 91,000 onnes for pesticides and 41,000 Tonnes for pesticide intermediates

Production Capacity

Integration of Advanta with UPL to realize acquisition synergies

Future Plans

Acquisition of Advanta BV, Netherlands (2006), Cerexagri, France (2007)

Key Alliances

Key Brands

Sales (FY 2009)

Market Segments

Player

Insecticide –Viraat

Herbicide –Devrinol, Orrja

Fungicide –Saafe, Zeemil

Rs. 2100 Crores (Crop protection)

Crop Protection, Industrial & Specialty Chemicals, Seeds

United Phosphorous Ltd. (UPL)

21 manufacturing sites – 9 in India with licensed capacity of 91,000 onnes for pesticides and 41,000 Tonnes for pesticide intermediates

Production Capacity

Integration of Advanta with UPL to realize acquisition synergies

Future Plans

Acquisition of Advanta BV, Netherlands (2006), Cerexagri, France (2007)

Key Alliances

Key Brands

Sales (FY 2009)

Market Segments

Player

Insecticide –Viraat

Herbicide –Devrinol, Orrja

Fungicide –Saafe, Zeemil

Rs. 2100 Crores (Crop protection)

Crop Protection, Industrial & Specialty Chemicals, Seeds

United Phosphorous Ltd. (UPL)

Production facilities at Thane, Himatnagarand Ankleshwar with combined capacity of 6300 Tons for Active ingredients and 7650 Tons for powder formulations and 10,000 KL for liquid formulations

Production Capacity

R&D focus on environmentally safe products

Fungicides - Fluopyram, Bixafen and Isotianilscheduled for launch in 2010 and 2011, three other candidates at an advanced stage of development

Future Plans

R&D alliance with GVK Biosciences for active ingredients

Key Alliances

Key Brands

Sales (FY 2009)

Market Segments

Player

Fungicide –Antracol, Folicur

Insecticide –Confidor, Calypso

Herbicide –Atlantis, Topstar

Rs. 1482 Crores

Crop Protection, Non-agricultural pest management, Plant & seeds biotechnology

Bayer CropScience Ltd.

Production facilities at Thane, Himatnagarand Ankleshwar with combined capacity of 6300 Tons for Active ingredients and 7650 Tons for powder formulations and 10,000 KL for liquid formulations

Production Capacity

R&D focus on environmentally safe products

Fungicides - Fluopyram, Bixafen and Isotianilscheduled for launch in 2010 and 2011, three other candidates at an advanced stage of development

Future Plans

R&D alliance with GVK Biosciences for active ingredients

Key Alliances

Key Brands

Sales (FY 2009)

Market Segments

Player

Fungicide –Antracol, Folicur

Insecticide –Confidor, Calypso

Herbicide –Atlantis, Topstar

Rs. 1482 Crores

Crop Protection, Non-agricultural pest management, Plant & seeds biotechnology

Bayer CropScience Ltd.

Factories at Akola, Ankleshwar, Lote, Turbhe, Patancheru with production capacity of 10,000 MTPA for technical grades and 30,000 Tons/Litres for formulations

Production Capacity

Eight new molecules under R&D

Plans to become Global supplier for Active Ingredients (AI). Target of cumulative sales of Rs. 1000 Crores from AI in the next 5 years. New AI plant in Dahej to be ready by June 2010

Future Plans

Marketing alliances with FMC, Dupont, Syngenta, Bayer, Nihon Nohayaku

Key Alliances

Key Brands

Sales (FY 2009)

Market Segments

Player

Fungicide –Contaf, Contaf Plus, Master

Insecticide –Rogor, Daksh, Tata Mida

Herbicide –Fateh, Tata Metri

Domestic: Rs. 541.7 Crores,

Export: Rs 295 Crores

Pesticides, Plant Nutrients, Seeds, Leather Chemicals

Rallis India Ltd.

Factories at Akola, Ankleshwar, Lote, Turbhe, Patancheru with production capacity of 10,000 MTPA for technical grades and 30,000 Tons/Litres for formulations

Production Capacity

Eight new molecules under R&D

Plans to become Global supplier for Active Ingredients (AI). Target of cumulative sales of Rs. 1000 Crores from AI in the next 5 years. New AI plant in Dahej to be ready by June 2010

Future Plans

Marketing alliances with FMC, Dupont, Syngenta, Bayer, Nihon Nohayaku

Key Alliances

Key Brands

Sales (FY 2009)

Market Segments

Player

Fungicide –Contaf, Contaf Plus, Master

Insecticide –Rogor, Daksh, Tata Mida

Herbicide –Fateh, Tata Metri

Domestic: Rs. 541.7 Crores,

Export: Rs 295 Crores

Pesticides, Plant Nutrients, Seeds, Leather Chemicals

Rallis India Ltd.

20 INDIACHEM GUJARAT 2009 21INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Regulatory Trends

Outlook

Key Opportunities

The Indian crop protection industry is regulated by the Insecticide Act, 1968 and

Insecticide Rules, 1971. While the Insecticide Act focuses on regulating manufacture,

sale, distribution, use and import of pesticides, the Insecticide Rules deal with

registration procedure.

The Indian Patent Act 2005, brought agrochemical products under patent protection,

thus making the Indian market attractive for International companies with regards to

intellectual property protection. It also provided Indian companies an opportunity to

explore new molecule development options and make R&D a strategic component.

However, patent registration does not ensure monopoly in the Indian market for more

than 3 years owing to lax regulatory control and counterfeit chemical manufacturers.

The future prospects of the agrochemicals industry look promising in the near term

on account of the increasing need to protect farm produce from pests, increasing

awareness amongst farmers and India's export competency. Further the growing

varieties of various pests, diseases, and their growing resistance to various pesticides

will keep the demand for new products going. The agrochemical space offers enough

scope for growth for both innovators as well as generic players.

1. Scope for increase in usage: Since just about 35-40% of the total farmland is under

crop protection, there is a significant unserved market to tap into. By conducting

special training programmes for farmers regarding the need to use agrochemicals,

Indian companies can hope to increase pesticide consumption.

2. Excess capacity: The excess production capacity is a perfect opportunity to

increase exports by utilizing India's low cost producer status.

3. Patent expiry: Agrochemicals are protected by patents to encourage innovation.

Between 2009 and 2014 many molecules are likely to go off patent throwing the

market open for generic players. The estimated total likely viable opportunity

through patent expiry is over USD 3 billion.

Key Challenges

1. R&D: R&D to develop a new agrochemical molecule takes an average of 9 years

and USD 180 million. Indian companies will find it difficult to build such R&D

capabilities and still compete on cost and maintain margins.

2. GM Seed threat: Genetically modified seeds possess self-immunity towards

natural adversaries. This can be a potential threat to the business of agrochemicals.

Best example of such an introduction in the Indian market is "BT Cotton", which

resulted in a decline in the consumption of agrochemicals by cotton crop. However,

there have been few reports of BT Cotton being unable to develop immunity

towards new type of pests.

3. Need for efficient distribution system: The number of end users is large and

widespread. High penetration and effective distribution is essential to ensure

product availability. Also, generally the retailer is the only point of contact with

the end user and hence has the most influence on the purchase decision.

However, the retailer in not likely to possess the technological knowledge about

the chemicals and will be unable to assist the farmer in identifying the problem

and offer the right solution. Lately, Agrochemical companies have been directly

dealing with retailers by cutting the distributor from the value chain thereby

reducing distribution costs and offering competitive prices to farmers. Direct

contact with retailers also enables the companies to train them in the correct use

and application of the products.

4. Government support for safer alternatives (IPM) & rising demand for organic

farming: Government is aggressively promoting Integrated Pest Management

(IPM) and zero budget farming. National Center for Integrated Pest Management

has been working since 1988 with the mission to promote adoption of IPM

Technologies to reduce the environmental and public health hazards due to

excessive reliance on chemical pesticides. NGOs are educating farmers about the

advantages of bio-pesticides. With increasing demand for organic food, farmers in

certain states like Karnataka have reduced chemical usage and have adopted

organic farming. Agrochemical companies will have to tackle the rising

environmental awareness and concern about the negative impacts of pesticide

usage.

5. Excise Duty: While seeds and fertilizers are exempt from excise duty, pesticides

attract excise duty at 8%. The PMFAI had requested a reduction in excise duty to

4% in the 2009 budget but failed to get the same.

20 INDIACHEM GUJARAT 2009 21INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Regulatory Trends

Outlook

Key Opportunities

The Indian crop protection industry is regulated by the Insecticide Act, 1968 and

Insecticide Rules, 1971. While the Insecticide Act focuses on regulating manufacture,

sale, distribution, use and import of pesticides, the Insecticide Rules deal with

registration procedure.

The Indian Patent Act 2005, brought agrochemical products under patent protection,

thus making the Indian market attractive for International companies with regards to

intellectual property protection. It also provided Indian companies an opportunity to

explore new molecule development options and make R&D a strategic component.

However, patent registration does not ensure monopoly in the Indian market for more

than 3 years owing to lax regulatory control and counterfeit chemical manufacturers.

The future prospects of the agrochemicals industry look promising in the near term

on account of the increasing need to protect farm produce from pests, increasing

awareness amongst farmers and India's export competency. Further the growing

varieties of various pests, diseases, and their growing resistance to various pesticides

will keep the demand for new products going. The agrochemical space offers enough

scope for growth for both innovators as well as generic players.

1. Scope for increase in usage: Since just about 35-40% of the total farmland is under

crop protection, there is a significant unserved market to tap into. By conducting

special training programmes for farmers regarding the need to use agrochemicals,

Indian companies can hope to increase pesticide consumption.

2. Excess capacity: The excess production capacity is a perfect opportunity to

increase exports by utilizing India's low cost producer status.

3. Patent expiry: Agrochemicals are protected by patents to encourage innovation.

Between 2009 and 2014 many molecules are likely to go off patent throwing the

market open for generic players. The estimated total likely viable opportunity

through patent expiry is over USD 3 billion.

Key Challenges

1. R&D: R&D to develop a new agrochemical molecule takes an average of 9 years

and USD 180 million. Indian companies will find it difficult to build such R&D

capabilities and still compete on cost and maintain margins.

2. GM Seed threat: Genetically modified seeds possess self-immunity towards

natural adversaries. This can be a potential threat to the business of agrochemicals.

Best example of such an introduction in the Indian market is "BT Cotton", which

resulted in a decline in the consumption of agrochemicals by cotton crop. However,

there have been few reports of BT Cotton being unable to develop immunity

towards new type of pests.

3. Need for efficient distribution system: The number of end users is large and

widespread. High penetration and effective distribution is essential to ensure

product availability. Also, generally the retailer is the only point of contact with

the end user and hence has the most influence on the purchase decision.

However, the retailer in not likely to possess the technological knowledge about

the chemicals and will be unable to assist the farmer in identifying the problem

and offer the right solution. Lately, Agrochemical companies have been directly

dealing with retailers by cutting the distributor from the value chain thereby

reducing distribution costs and offering competitive prices to farmers. Direct

contact with retailers also enables the companies to train them in the correct use

and application of the products.

4. Government support for safer alternatives (IPM) & rising demand for organic

farming: Government is aggressively promoting Integrated Pest Management

(IPM) and zero budget farming. National Center for Integrated Pest Management

has been working since 1988 with the mission to promote adoption of IPM

Technologies to reduce the environmental and public health hazards due to

excessive reliance on chemical pesticides. NGOs are educating farmers about the

advantages of bio-pesticides. With increasing demand for organic food, farmers in

certain states like Karnataka have reduced chemical usage and have adopted

organic farming. Agrochemical companies will have to tackle the rising

environmental awareness and concern about the negative impacts of pesticide

usage.

5. Excise Duty: While seeds and fertilizers are exempt from excise duty, pesticides

attract excise duty at 8%. The PMFAI had requested a reduction in excise duty to

4% in the 2009 budget but failed to get the same.

22 INDIACHEM GUJARAT 2009

6. Counterfeit Products: Presence of a flourishing counterfeit market with spurious

products eats into the margins of the organized sector. The spurious pesticides

market size in India is estimated to be USD 233 million in 2009. There is no

provision in the Indian Insecticide Act to deal with counterfeit pesticides.

Threats like genetically modified seeds, Integrated Pest Management, organic farming

etc. can be turned into opportunities if the industry re-orients itself such that its

product offering includes a broader range of agri-inputs instead of only agrochemicals.

22 INDIACHEM GUJARAT 2009

6. Counterfeit Products: Presence of a flourishing counterfeit market with spurious

products eats into the margins of the organized sector. The spurious pesticides

market size in India is estimated to be USD 233 million in 2009. There is no

provision in the Indian Insecticide Act to deal with counterfeit pesticides.

Threats like genetically modified seeds, Integrated Pest Management, organic farming

etc. can be turned into opportunities if the industry re-orients itself such that its

product offering includes a broader range of agri-inputs instead of only agrochemicals.

INDIACHEM GUJARAT 2009 25INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Colourants

Introduction

The colourant industry is a major component of the global chemical industry. A

colourant has the property of causing a change in the colour of the substrate.

Colourants(USD 28 Bn)

Dyes(USD 7.7 Bn)

Pigments(USD 20.3 Bn)

Organic(USD 5.6 Bn)

Inorganic(USD 14.7 Bn)

Global markets for dyes & pigments

Source: Chemical Weekly

The global colourants market is roughly estimated at ~ USD 28 billion excluding an

additional USD 7 billion of dye intermediates.

According to the US International Trade Commission, dyes are broadly classified based

on their usage/ technology as shown in the chart below.

Reactive,26%

Disperse,21%

Direct, 11%

Vat, 11%

Others,31%

Dyes by usage (% volume)

Source: Industry reports

Pigments are broadly classified as organic and inorganic. The global pigment industry is

estimated at ~7.4 million tons including white pigment such as Titanium Dioxide (TiO2)

and carbon black which is used as a black colourant.

INDIACHEM GUJARAT 2009 25INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Colourants

Introduction

The colourant industry is a major component of the global chemical industry. A

colourant has the property of causing a change in the colour of the substrate.

Colourants(USD 28 Bn)

Dyes(USD 7.7 Bn)

Pigments(USD 20.3 Bn)

Organic(USD 5.6 Bn)

Inorganic(USD 14.7 Bn)

Global markets for dyes & pigments

Source: Chemical Weekly

The global colourants market is roughly estimated at ~ USD 28 billion excluding an

additional USD 7 billion of dye intermediates.

According to the US International Trade Commission, dyes are broadly classified based

on their usage/ technology as shown in the chart below.

Reactive,26%

Disperse,21%

Direct, 11%

Vat, 11%

Others,31%

Dyes by usage (% volume)

Source: Industry reports

Pigments are broadly classified as organic and inorganic. The global pigment industry is

estimated at ~7.4 million tons including white pigment such as Titanium Dioxide (TiO2)

and carbon black which is used as a black colourant.

26 INDIACHEM GUJARAT 2009 27INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Pigments (7.4)

Titanium Dioxide(4.7)

Carbon Black(0.8)

Iron Oxide (1.3)

Other Inorganic(0.2)

Colour Organic & Special Effect (0.4)

Azo-Red(0.08)

Diarylide-Yellow(0.08)

Phthalocyanine-Blue,Green (0.08)

Performance & Special Effect(0.11)

HPP (0.05)

Metal Effect (0.04)

Pearlescent(0.02)

Global pigments market(Mn tons)

Source: Chemical Weekly

Colour & Special Effect(1.9)

Due to a large demand base in Asian countries, availability of cheaper manpower and

less stringent environmental norms there has been a gradual shift in production, with

Asia now accounting for more than 40% of the global supply.

Regional production of dyestuffs(% volume)

Asia, 42%

US, 24%

Others, 12%

Europe, 22%

Source: Industry reports

Industry overview

India accounts for ~7% of the global share of the dyestuffs industry and produces

~150,000 tons. The Indian dyestuff industry is highly fragmented and characterised by

a large number of players in the unorganized sector. Around 1000 units fall under the

small scale industry category and only about 50 are large organized units. These units

are mainly present in the western states of Gujarat and Maharashtra, with Gujarat

accounting for almost 80% of capacity.

In India the dyes industry supplies the majority of its production, almost 80%, to the

textile industry. The balance is consumed by the paper and leather industry. Also,

these dyestuffs are exported to Europe, South East Asia and Taiwan to cater to the

textile industries in these countries.

Printing inks and coatings account for greater than 70% of consumption of pigments.

Titanium dioxide is a major raw material used in the manufacture of paints. The

domestic production of TiO2 in India is ~60,000 tons. The requirement of pigments for

the growing domestic ink and coating market is estimated at greater than USD 20

million each and the requirements of these sectors are helping to drive the demand

for pigments.

Pigments by end use (% volume)

Plastics,10%

Others, 9%

Inks, 47%Textiles,10%

Coatings,24%

Source: Industry reports

Inks, 47%

There are a wide variety of dyestuffs being manufactured in the country. However,

almost 80% of these are commodities and face intense pricing pressures reducing the

margins of the industry.

The per-capita consumption of dyestuffs at ~50 gms is much lower than the world

average of over 400 gms demonstrating a largely untapped domestic market. India has

largely been an exporting country and has emerged as a global supplier of reactive,

acid, vat and direct dyes accounting for ~10% of world trade.

India has grown significantly as a producer and exporter of organic pigments,

particularly phthalocyanine blue, green and some high performance pigments. India is

amongst the largest sources of coloured organic pigments, competing with China for a

dominant share of the export market.

Within India, the major players in the pigments industry are Sudarshan Chemicals and

Clariant India while in the dyestuff industry companies such as are Atul, Clariant India,

Dystar, Ciba (BASF) and IDI are large players present in the organized sector.

Fiscal policies and excise concessions led to a high level of fragmentation in the Indian

dyestuffs market. However, a gradual reduction in the excise duties has resulted in a

more balanced pricing differential between the organized and unorganized sectors.

The organised sector, with a better product range, technology and marketing reach,

Supply Overview

26 INDIACHEM GUJARAT 2009 27INDIACHEM GUJARAT 2009

Federation of Indian Chambers of Commerce and Industry

Pigments (7.4)

Titanium Dioxide(4.7)

Carbon Black(0.8)

Iron Oxide (1.3)

Other Inorganic(0.2)

Colour Organic & Special Effect (0.4)

Azo-Red(0.08)

Diarylide-Yellow(0.08)

Phthalocyanine-Blue,Green (0.08)

Performance & Special Effect(0.11)

HPP (0.05)

Metal Effect (0.04)

Pearlescent(0.02)

Global pigments market(Mn tons)

Source: Chemical Weekly

Colour & Special Effect(1.9)

Due to a large demand base in Asian countries, availability of cheaper manpower and

less stringent environmental norms there has been a gradual shift in production, with

Asia now accounting for more than 40% of the global supply.

Regional production of dyestuffs(% volume)

Asia, 42%

US, 24%

Others, 12%

Europe, 22%

Source: Industry reports

Industry overview

India accounts for ~7% of the global share of the dyestuffs industry and produces

~150,000 tons. The Indian dyestuff industry is highly fragmented and characterised by

a large number of players in the unorganized sector. Around 1000 units fall under the

small scale industry category and only about 50 are large organized units. These units

are mainly present in the western states of Gujarat and Maharashtra, with Gujarat

accounting for almost 80% of capacity.

In India the dyes industry supplies the majority of its production, almost 80%, to the

textile industry. The balance is consumed by the paper and leather industry. Also,

these dyestuffs are exported to Europe, South East Asia and Taiwan to cater to the

textile industries in these countries.

Printing inks and coatings account for greater than 70% of consumption of pigments.

Titanium dioxide is a major raw material used in the manufacture of paints. The

domestic production of TiO2 in India is ~60,000 tons. The requirement of pigments for

the growing domestic ink and coating market is estimated at greater than USD 20

million each and the requirements of these sectors are helping to drive the demand

for pigments.

Pigments by end use (% volume)