india research - karvy onlinecontent.karvyonline.com/contents/content_20149231688.pdf · india...

TRANSCRIPT

Cement July 22, 2014

UltraTech

Bloomberg: UTCEM IN Reuters: UTCEM.BO

BUY

Institutional Equities

India Research

RESULT REVIEW

Recommendation

CMP: Rs2,528

Target Price: Rs2,837

Previous Target Price Rs2,837

Upside (%) 12%

Stock Information Market Cap. (Rs bn / US$ mn) 692/11,478

52-week High/Low (Rs) 2,872/1,402

3m ADV (Rs mn /US$ mn) 967/16

Beta 1.1

Sensex/ Nifty 25,715/7,684

Share outstanding (mn) 274

Stock Performance (%) 1M 3M 12M YTD

Absolute (7.5) 13.7 30.7 43.0

Rel. to Sensex (9.7) 0.6 2.4 17.7

Performance

Source: Bloomberg

Earnings Revision (%) (%) FY15E. FY16E. FY17E.

Sales 4.2. 7.3 7.3

EBITDA 3.5. 6.0 6.8

PAT 4.6. 1.1 2.9

Source: Karvy Institutional Research

Analysts Contact Rajesh Kumar Ravi

022 6184 4313

1,550

2,050

2,550

3,050

15,500 17,500 19,500 21,500 23,500 25,500 27,500

Jul-

13

Sep

-13

Oct

-13

No

v-1

3

Dec

-13

Feb

-14

Mar

-14

Ap

r-1

4

Jun

-14

Jul-

14

Sensex (LHS) Ultartech Cement (RHS)

Strong Volume Growth Drives Profitability UltraTech’s standalone 1QFY15 net Sales rose 14% YoY to Rs59.6 bn while

EBITDA & PAT declined 2% & 7% YoY respectively to Rs10.5 bn and Rs6.3

bn respectively. On QoQ basis, Sales, EBITDA & PAT declined 5%, 17%

and 16%. EBITDA per MT at Rs879 is down 15% YoY & 14% QoQ.

Strong volume growth drives profitability: Its net sales realization (NSR)

declined 1% YoY (flat QoQ) vs our estimate of 1.7% QoQ higher NSR.

However, its sales volume (+15% YoY & -4% QoQ) came in 2% ahead of our

estimates on account of amalgamation of JP Gujarat operational performance

during the quarter. Subsequently, net sales came in-line with our estimates.

Double digit volume growth came at slightly lower NSR growth. Operating

costs per MT rose 3.6% QoQ and 3% YoY (vs our estimates of 2% QoQ

increase) driven primarily by higher fixed costs per MT which rose 10% QoQ.

Input costs per MT rose a modest 1.5% QoQ on stable fuel costs and INR

appreciation. Subsequently, EBITDA declined 2% YoY and 17% QoQ to

Rs10.5 bn – 12% lower than our estimates led primarily by lower NSR. PAT

declined 7% YoY and 16% QoQ to Rs6.3 bn (our estimate Rs7.1 bn).

Re-iterate “BUY”: We have amalgamated the JP Gujarat (4.8 mn MT)

financials in UltraTech wef FY15E. Subsequently, we increase our

FY15E/16E/17E EBITDA estimates by 3.5%, 6%, 6.8% respectively. Our FY15E

upgrade is lower as we have adjusted the financials for lower than estimated

1QFY15 performance. On account of higher capital charges on amalgamation

of JP Gujarat unit, we cut our FY15E/16E PAT estimates by 4.6% & 1.1%

respectively and increase FY17E PAT by 3%. We expect UltraTech to deliver

29% EBITDA and PAT CAGRs during FY14-17E period led by 13% volume

growth. UltraTech has 80% CPP capability on its current capacity of 59

mnMT (India). The capacity will increase to 65 mn MT by end of FY15E. We

re-iterate our “BUY” recommendation with a TP of Rs2837 (no change)

valuing it at 11.5x its FY16E EBITDA. The TP discounts FY17E EBITDA at

8.9x and implies replacement cost valuations of USD194/187 on FY16E/17E

basis.

Financial Summary (Standalone)

Year to March (Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Revenues 201,800 202,798 248,206 297,118 341,849

EBITDA 46,755 38,179 51,165 66,952 82,364

EBITDA margin (%) 23.2 18.8 20.6 22.5 24.1

Net profit 26,555 20,489 25,958 34,766 44,263

EPS (Rs) 96.9 74.7 94.6 126.7 161.3

RoE (%) 18.9 18.2 14.2 16.6 18.1

RoCE (%) 19.4 13.0 15.4 18.0 21.0

P/E (x) 26.0 33.8 26.7 19.9 15.6

EV/EBITDA (x) 14.2 17.6 13.9 10.2 7.8

Source: Company, Karvy Institutional Research

2

July 22, 2014

UltraTech

Quarterly Performance Trend

Exhibit 1: Key Standalone Operational Trend

Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 YoY (%) QoQ (%)

Total sales volume (mn mt) 11.8 10.5 9.5 10.2 11.4 10.4 9.5 10.1 12.5 12.0 15.2 (4.4)

Trends (Rs/mt)

Net sales realization 4,564 4,842 4,956 4,785 4,787 4,798 4,779 4,762 4,765 4,761 (0.8) (0.1)

Raw material cost 651 708 683 651 743 752 800 807 778 737 (1.9) (5.2)

Power and fuel cost 1,007 1,033 1,126 1,061 924 953 1,011 991 949 1,010 5.9 6.4

Employee cost 186 213 251 240 228 242 301 241 188 231 (4.5) 22.7

Transport cost 922 986 974 1,038 1,046 1,061 1,051 1,106 1,092 1,112 4.8 1.9

Other expenses 681 659 836 768 724 757 899 830 742 792 4.5 6.7

Operating cost 3,447 3,598 3,871 3,757 3,665 3,765 4,061 3,975 3,749 3,882 3.1 3.6

RM and Fuel combined 1,658 1,741 1,809 1,712 1,667 1,705 1,811 1,798 1,727 1,747 2.5 1.2

Variable cost 2,580 2,726 2,784 2,750 2,713 2,766 2,861 2,904 2,819 2,860 3.4 1.5

Fixed costs 867 871 1,087 1,007 953 999 1,199 1,071 930 1,022 2.4 9.9

EBITDA 1,117 1,244 1,085 1,028 1,121 1,032 718 786 1,016 879 (14.9) (13.5)

Source: Company, Karvy Institutional Research

Exhibit 2: Key Quarterly Financials (Standalone)

Financials (Rs mn) Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 YoY (%) QoQ (%)

Net Sales 53,916 50,909 47,274 48,821 54,720 49,802 45,219 48,179 59,599 56,921 14.3 (4.5)

Total Expenditure 40,725 37,830 36,922 38,331 41,900 39,084 38,424 40,222 46,889 46,416 18.8 (1.0)

Raw Materials 7,689 7,444 6,518 6,639 8,495 7,803 7,568 8,169 9,735 8,818 13.0 (9.4)

Power and Fuel 11,902 10,862 10,741 10,827 10,559 9,896 9,566 10,023 11,869 12,076 22.0 1.7

Employee 2,195 2,236 2,395 2,444 2,609 2,507 2,844 2,443 2,352 2,758 10.0 17.3

Transport 10,889 10,363 9,292 10,587 11,956 11,018 9,942 11,193 13,655 13,300 20.7 (2.6)

Others 8,049 6,925 7,975 7,834 8,280 7,860 8,504 8,394 9,279 9,464 20.4 2.0

EBITDA 13,191 13,079 10,352 10,489 12,820 10,718 6,795 7,956 12,709 10,505 (2.0) (17.3)

EBITDA margins (%) 24.5 25.7 21.9 21.5 23.4 21.5 15.0 16.5 21.3 18.5 (307) (287)

Other Income 1,450 688 406 965 1,005 1,656 376 681 577 2,131 28.7 269.1

Depreciation 2,332 2,281 2,325 2,388 2,460 2,521 2,573 2,645 2,785 2,645 4.9 (5.0)

EBIT 12,309 11,485 8,434 9,066 11,365 9,852 4,598 5,993 10,502 9,991 1.4 (4.9)

EBIT margins (%) 22.8 22.6 17.8 18.6 20.8 19.8 10.2 12.4 17.6 17.6 (223) (7)

Interest 586 498 600 521 478 660 888 905 739 1,002 51.8 35.5

Taxes 3,150 3,203 2,334 2,537 3,626 2,466 1,070 1,391 2,340 2,733 10.8 16.8

Adjusted Net Profits 8,573 7,784 5,500 6,008 7,261 6,726 2,641 3,698 7,423 6,256 (7.0) (15.7)

PAT margins (%) 15.9 15.3 11.6 12.3 13.3 13.5 5.8 7.7 12.5 11.0 (252) (147)

EPS (Rs) 31.3 28.4 20.1 21.9 26.5 24.5 9.6 13.5 27.1 22.8 (7.1) (15.8)

Source: Company, Karvy Institutional Research

3

July 22, 2014

UltraTech

Outlook and Valuation

We have amalgamated the JP Gujarat (4.8 mn MT) financials in UltraTech wef

from FY15E. Subsequently, we increase our FY15E/16E/17E EBITDA estimates by

3.5%, 6%, 6.8% respectively. Our FY15E upgrade is lower as we have adjusted the

financials for lower than estimated 1QFY15 performance. On account of higher

capital charges on amalgamation of JP Gujarat unit, we cut our FY15E/16E PAT est

by 4.6% and 1.1% respectively and increase FY17E PAT by 3%.

We expect UltraTech to deliver 29% EBITDA and PAT CAGRs during FY14-17E

period led by 13% volume growth. UltraTech has 80% captive power capability on

its current capacity of 59 mnMT (India). The capacity will increase to 65 mn MT by

end of FY15E.

We re-iterate our “BUY” recommendation with a TP of Rs2837 (no change)

valuing it at 11.5x its FY16E EBITDA. The TP discounts FY17E EBITDA at 8.9x and

implies replacement cost valuations of USD194/187 on FY16E/17E basis.

Exhibit 3: Key Operational Estimates and Assumptions

FY12 FY13 FY14 FY15E FY16E FY17E

Total Sales Volume (mn MT) 41.7 41.7 42.6 49.8 56.2 60.7

Net sales realization 4,395 4,843 4,759 4,980 5,283 5,635

Raw material cost 618 698 781 739 776 814

Power and Fuel cost 1,033 1,032 970 1,010 1,051 1,093

Freight cost 800 909 1,075 1,105 1,161 1,219

Employee cost 199 232 238 245 250 260

Other Expenses 651 745 799 854 856 892

Opex 3,302 3,616 3,863 3,953 4,093 4,278

EBITDA 995 1,122 896 1,027 1,191 1,358

Source: Company, Karvy Institutional Research

Exhibit 4: Estimates revision to factor in amalgamation of JP Gujarat unit; in FY15E the revenue and EBITDA upgrade

has been moderated as we factor in the lower than estimated 1QFY15 results

FY15E FY16E FY17E FY15E FY16E FY17E

Comments

(Rs mn) Revision YoY (%)

Net Revenues 248,206 297,118 341,849 4.2 7.3 7.3 Increase revenue and EBITDA to

factor in sales volume from the JP

Gujarat unit

Operating expenditure 197,041 230,167 259,485 4.3 7.6 7.5

EBITDA 51,165 66,952 82,364 3.5 6.0 6.8

Depreciation 13,092 15,786 17,631 14.0 20.7 12.4 Higher capital charges on account of

the new unit addition which has

Gross debt of ~Rs36bn; New plant

hence depreciation is higher

Other Income 4,031 4,300 4,600 26.0 26.5 35.3

EBIT 42,104 55,466 69,333 2.3 3.7 7.0

Interest expenditure 6,052 6,500 6,100 81.2 124.1 110.3

PBT 36,052 48,966 63,233 (4.6) (3.2) 2.1 Subsequently, the amalgamation

should moderate PAT growth Tax 10,095 14,200 18,970 (4.6) (7.9) 0.5

Adjusted PAT 25,958 34,766 44,263 (4.6) (1.1) 2.9

Source: Karvy Institutional Research

4

July 22, 2014

UltraTech

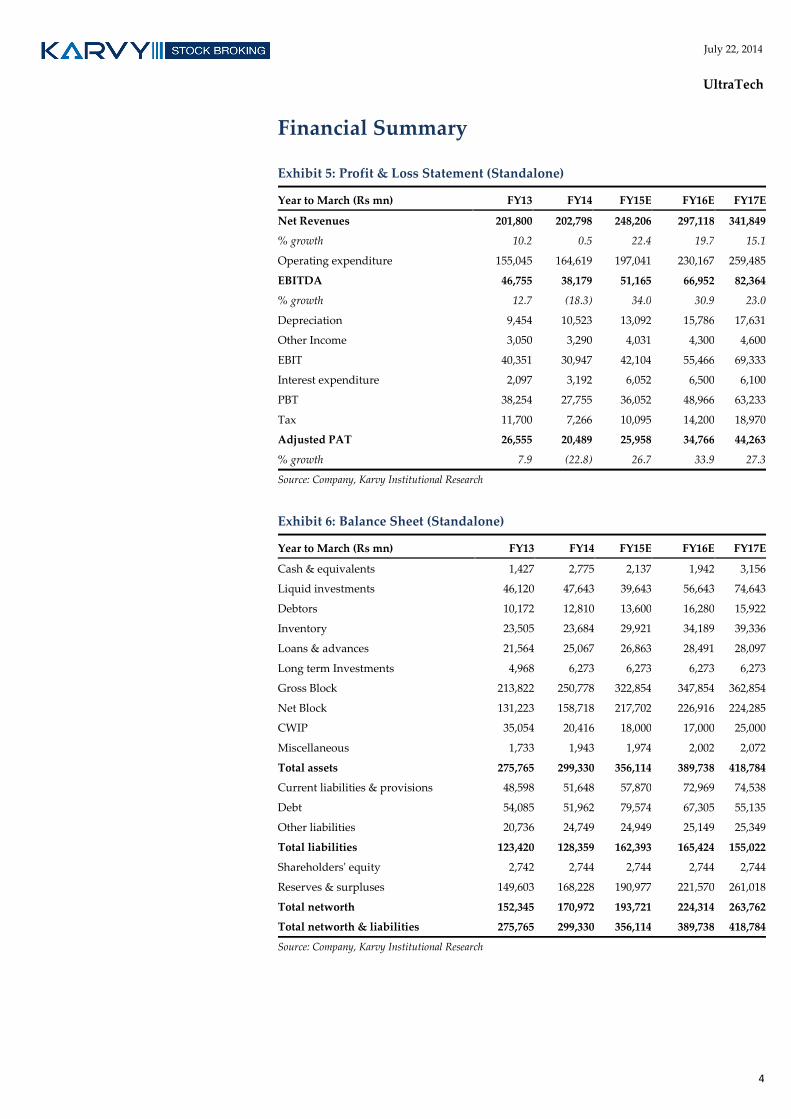

Financial Summary

Exhibit 5: Profit & Loss Statement (Standalone)

Year to March (Rs mn) FY13 FY14 FY15E FY16E FY17E

Net Revenues 201,800 202,798 248,206 297,118 341,849

% growth 10.2 0.5 22.4 19.7 15.1

Operating expenditure 155,045 164,619 197,041 230,167 259,485

EBITDA 46,755 38,179 51,165 66,952 82,364

% growth 12.7 (18.3) 34.0 30.9 23.0

Depreciation 9,454 10,523 13,092 15,786 17,631

Other Income 3,050 3,290 4,031 4,300 4,600

EBIT 40,351 30,947 42,104 55,466 69,333

Interest expenditure 2,097 3,192 6,052 6,500 6,100

PBT 38,254 27,755 36,052 48,966 63,233

Tax 11,700 7,266 10,095 14,200 18,970

Adjusted PAT 26,555 20,489 25,958 34,766 44,263

% growth 7.9 (22.8) 26.7 33.9 27.3

Source: Company, Karvy Institutional Research

Exhibit 6: Balance Sheet (Standalone)

Year to March (Rs mn) FY13 FY14 FY15E FY16E FY17E

Cash & equivalents 1,427 2,775 2,137 1,942 3,156

Liquid investments 46,120 47,643 39,643 56,643 74,643

Debtors 10,172 12,810 13,600 16,280 15,922

Inventory 23,505 23,684 29,921 34,189 39,336

Loans & advances 21,564 25,067 26,863 28,491 28,097

Long term Investments 4,968 6,273 6,273 6,273 6,273

Gross Block 213,822 250,778 322,854 347,854 362,854

Net Block 131,223 158,718 217,702 226,916 224,285

CWIP 35,054 20,416 18,000 17,000 25,000

Miscellaneous 1,733 1,943 1,974 2,002 2,072

Total assets 275,765 299,330 356,114 389,738 418,784

Current liabilities & provisions 48,598 51,648 57,870 72,969 74,538

Debt 54,085 51,962 79,574 67,305 55,135

Other liabilities 20,736 24,749 24,949 25,149 25,349

Total liabilities 123,420 128,359 162,393 165,424 155,022

Shareholders' equity 2,742 2,744 2,744 2,744 2,744

Reserves & surpluses 149,603 168,228 190,977 221,570 261,018

Total networth 152,345 170,972 193,721 224,314 263,762

Total networth & liabilities 275,765 299,330 356,114 389,738 418,784

Source: Company, Karvy Institutional Research

5

July 22, 2014

UltraTech

Exhibit 7: Cash Flow Statement (Standalone)

Year to March (Rs mn) FY13 FY14 FY15E FY16E FY17E

PBT 38,254 27,755 36,052 48,966 63,233

Depreciation 9,454 10,523 13,092 15,786 17,631

Interest 2,097 3,192 6,052 6,500 6,100

Tax paid (7,165) (6,549) (9,895) (14,000) (18,770)

(Incr) / decr in net working capital (4,089) 685 (2,954) 5,531 (3,538)

Other income (3,052) (3,266) (4,031) (4,300) (4,600)

Cash flow from operating activities 35,524 32,416 38,316 58,483 60,055

(Incr) / decr in capital expenditure (32,676) (22,284) (69,660) (24,000) (23,000)

(Incr) / decr in investments (10,911) (322) 10,000 (14,900) (15,900)

Others 562 511 2,031 2,200 2,500

Cash flow from investing activities (43,025) (22,096) (57,629) (36,700) (36,400)

Incr / (decr) in borrowings 12,557 (2,092) 27,612 (12,269) (12,170)

Issuance of equity 79 44 2 - -

Dividend paid (3,268) (4,046) (6,052) (6,500) (6,100)

Interest paid (2,539) (2,878) (2,887) (3,209) (4,172)

Cash flow from financing activities 6,829 (8,972) 18,675 (21,978) (22,442)

Net change in cash (672) 1,348 (638) (195) 1,214

Source: Company, Karvy Institutional Research

Exhibit 8: Key Ratios

Year to March (%) FY13 FY14 FY15E FY16E FY17E

EBITDA margin 23.2 18.8 20.6 22.5 24.1

EBIT margin 20.2 15.4 17.1 18.8 20.4

Net profit margin 13.3 10.2 10.6 11.8 13.0

Dividend payout ratio 10.9 14.1 12.4 12.0 10.9

Net debt: equity 0.0 0.0 0.2 0.0 (0.1)

RoCE 19.4 13.0 15.4 18.0 21.0

RoIC 17.5 12.8 13.9 15.8 19.1

RoE 18.9 18.2 14.2 16.6 18.1

Source: Company, Karvy Institutional Research

Exhibit 9: Valuation Parameters

Year to March FY13 FY14 FY15E FY16E FY17E

EPS (Rs) 96.9 74.7 94.6 126.7 161.3

DPS (Rs) 9.0 9.0 10.0 13.0 15.0

Book value per share (Rs) 556 623 706 818 961

P/E (x) 26.0 33.8 26.7 19.9 15.6

P/BV (x) 4.5 4.0 3.6 3.1 2.6

EV/EBITDA (x) 14.2 17.6 13.9 10.2 7.8

EV/Sales (x) 3.3 3.4 2.9 2.3 1.9

EV/mt (USD) 215 202 179 172 162

Source: Company, Karvy Institutional Research

Institutional Equities Team Rahul Sharma

Head – Institutional Equities /

Research / Pharma +91-22 61844310 [email protected]

Gurdarshan Singh Kharbanda Head - Sales-Trading +91-22 61844368/69 [email protected]

INSTITUTIONAL RESEARCH

Analysts Industry / Sector Desk Phone Email ID

Mitul Shah Automobiles/Auto Ancillary +91-22 61844312 [email protected]

Parikshit Kandpal Infra / Real Estate / Strategy/Consumer +91-22 61844311 [email protected]

Rajesh Kumar Ravi Cement/ Logistics/ Paints +91-22 61844313 [email protected]

Rupesh Sankhe Power/Capital Goods +91-22 61844315 [email protected]

Varun Chakri Research Associate +91 22 61844326 [email protected]

Vinesh Vala Research Associate +91 22 61844325 [email protected]

INSTITUTIONAL SALES

Celine Dsouza Sales +91 22 61844341 [email protected]

Edelbert Dcosta Sales +91 22 61844344 [email protected]

INSTITUTIONAL SALES TRADING & DEALING

Aashish Parekh Institutional Sales/Trading/ Dealing +91-22 61844361

Prashant Oza Institutional Sales/Trading/ Dealing +91-22 61844370 /71 [email protected]

Pratik Sanghvi Institutional Dealing +91-22 61844366 /67 [email protected]

For further enquiries please contact:

Tel: +91-22-6184 4300

Disclosures Appendix

Analyst certification

The following analyst(s), who is (are) primarily responsible for this report, certify (ies) that the views expressed

herein accurately reflect his (their) personal view(s) about the subject security (ies) and issuer(s) and that no part of

his (their) compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views

contained in this research report.

Disclaimer

The information and views presented in this report are prepared by Karvy Stock Broking Limited. The information

contained herein is based on our analysis and upon sources that we consider reliable. We, however, do not vouch for

the accuracy or the completeness thereof. This material is for personal information and we are not responsible for any

loss incurred based upon it. The investments discussed or recommended in this report may not be suitable for all

investors. Investors must make their own investment decisions based on their specific investment objectives and

financial position and using such independent advice, as they believe necessary. While acting upon any information

or analysis mentioned in this report, investors may please note that neither Karvy nor Karvy Stock Broking nor any

person connected with any associate companies of Karvy accepts any liability arising from the use of this information

and views mentioned in this document.

The author, directors and other employees of Karvy and its affiliates may hold long or short positions in the above

mentioned companies from time to time. Every employee of Karvy and its associate companies are required to

disclose their individual stock holdings and details of trades, if any, that they undertake. The team rendering

corporate analysis and investment recommendations are restricted in purchasing/selling of shares or other securities

till such a time this recommendation has either been displayed or has been forwarded to clients of Karvy. All

employees are further restricted to place orders only through Karvy Stock Broking Ltd. This report is intended for a

restricted audience and we are not soliciting any action based on it. Neither the information nor any opinion

expressed herein constitutes an offer or an invitation to make an offer, to buy or sell any securities, or any options,

futures nor other derivatives related to such securities.

Karvy Stock Broking Limited Institutional Equities

Office No. 702, 7th Floor, Hallmark Business Plaza, Opp.-Gurunanak Hospital, Mumbai 400 051 Regd Off : 46, Road No 4, Street No 1, Banjara Hills, Hyderabad – 500 034.

Karvy Stock Broking Research is also available on: Bloomberg - KRVY <GO>, Thomson Publisher & Reuters.

Stock Ratings Absolute Returns Buy : > 15% Hold : 5 - 15% Sell : < 5%