india daily, february 13, 2012 - kotaksecurities.com · for private circulation only. for important...

TRANSCRIPT

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL.

INDIA DAILYFebruary 13, 2012 India 10-Feb 1-day1-mo 3-mo

Sensex 17,749 (0.5) 9.9 3.2

Nifty 5,382 - 10.6 4.1

Global/Regional indices

Dow Jones 12,801 (0.7) 3.1 5.3

Nasdaq Composite 2,904 (0.8) 7.1 8.4

FTSE 5,852 (0.7) 3.8 5.5

Nikkie 8,963 0.2 5.5 5.3

Hang Seng 20,837 0.3 8.5 8.9

KOSPI 2,003 0.5 6.8 7.5

Value traded – India

Cash (NSE+BSE) 185 166 70

Derivatives (NSE) 1,371 1,079 1,107

Deri. open interest 1,372 1,112 1,260

Forex/money market

Change, basis points

10-Feb 1-day 1-mo 3-mo

Rs/US$ 49.4 (5) (204) (97)

10yr govt bond, % 8.3 1 (8) (64)

Net investment (US$mn)

9-Feb MTD CYTD

FIIs 294 1,810 3,994

MFs (77) (95) (282)

Top movers -3mo basis

Change, %

Best performers 10-Feb 1-day 1-mo 3-mo

IVRC IN Equity 56.7 (4.4) 48.0 51.0

TTMT IN Equity 257.4 0.0 23.3 41.8

WLCO IN Equity 133.6 1.9 20.6 38.7

MMTC IN Equity 875.2 (1.1) (8.0) 36.5

TGBL IN Equity 119.0 (3.3) 26.3 34.7

Worst performers

UNSP IN Equity 670.3 (2.3) 11.8 (19.8)

BHEL IN Equity 260.6 (0.5) (2.3) (19.7)

ESOIL IN Equity 66.0 (3.1) 6.5 (18.6)

MM IN Equity 691.6 (1.5) (0.1) (17.8)

NMDC IN Equity 189.2 (0.8) 8.0 (14.2)

Contents

Daily Alerts

Results

DLF: Right course but still in rough waters

Oil India: Country cousin steals a march

Tata Power: Coal production ramps up, low cost coal gives Mundra hope

IDFC: Growth strong, core in line

Reliance Communications: Weak results but do they matter?

Shriram Transport: A flat quarter

Reliance Capital: A mixed quarter

Eros International: Growing up

MTNL: Operational strife continues

Puravankara Projects: In-line results, poor sales

Results, Change in Reco

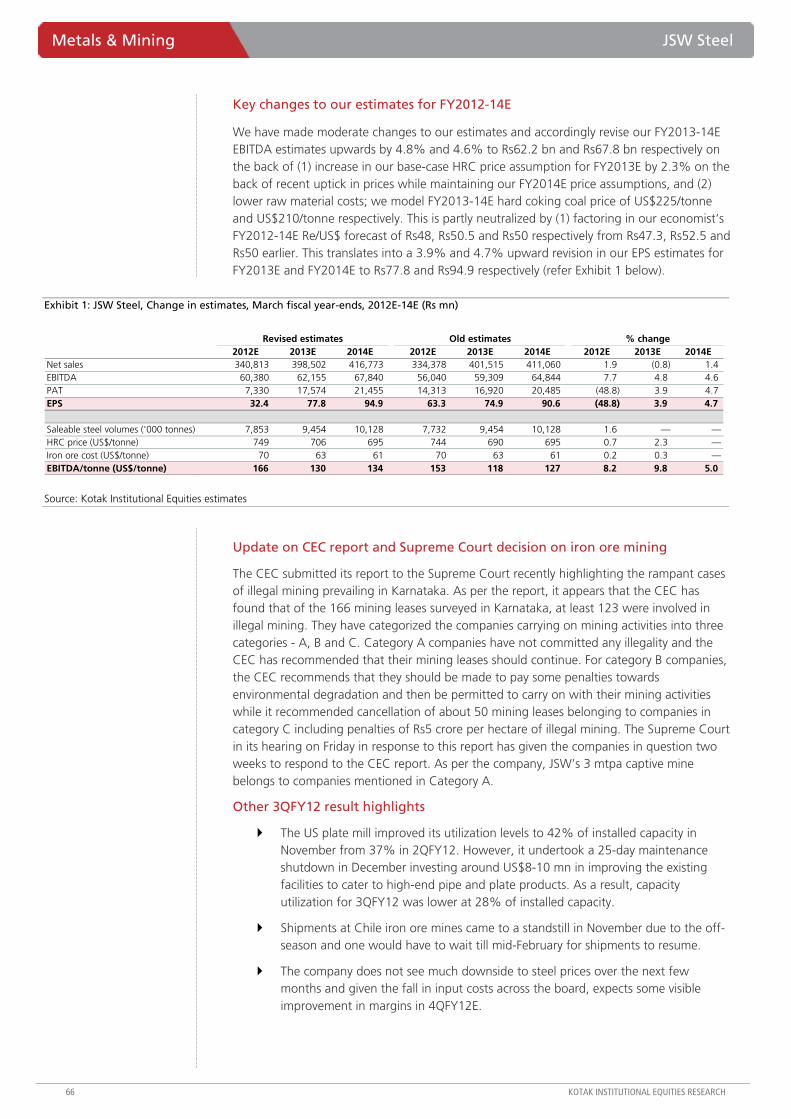

JSW Steel: Reports consolidated loss; stock expensive

Sun TV Network: A rainy quarter; Sun hides behind the clouds

Change in Reco

Tata Steel: Negatives out of the way

IndusInd Bank: Limited risks to business; valuations cap returns in the near term

Sector

Consumer products: Hale and hearty, for now

Economy

Economy: IIP growth likely to be near the bottom

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Reported financials disappoint on lower execution

DLF reported revenues of Rs20.3 bn (-18% yoy, -20% qoq) and PAT of Rs2.6 bn (-45% yoy, -31% qoq) due to slowdown in execution (revenue recognition) as the company moved over to third-party contractors from in-house construction which caused associated delays. EBITDA came in at Rs8.2 bn (-30% yoy and qoq) while EBITDA margins dropped by 5.9% qoq and 7.1% yoy to 40.4% due to an increase in construction cost and other expenditure as a proportion of sales (53% versus 48% in 2QFY12 and 47% in 3QFY11). PAT also got impacted by increase in interest costs (average COD is now 12.75% on a debt of Rs250 bn) and lower interest capitalization of 25%.

Sales and deliveries have picked up and debt is marginally down qoq

DLF sold 3.3 mn sq. ft in 3QFY12 versus 1.3 mn sq. ft in 2QFY12 and 2.5 mn sq. ft in 3QFY11 and the company has guided for a slow and cautious 4QFY12/1QFY13 due to high interest rates. DLF has plans to launch 9.25 mn sq. ft under plots, 6 mn sq. ft under group housing and 0.5 mn sq. ft of commercial space and has indicated that approvals for several micro-markets are already in place. DLF’s area under execution has declined to 45 mn sq. ft from 53 mn sq. ft in 2QFY12 due to handovers of 10.5 mn sq. ft in the quarter. DLF’s handover of projects (both development and rental) in 3QFY12 is higher than total of FY2010 and FY2011 (9.2 mn sq. ft) and is now targeting to deliver >1.5 mn sq. ft in 4QFY12E and >12 mn sq. ft in FY2013E.

Asset sales release cash though debt reduction not as much as expected

DLF raised Rs12 bn through assets sales in 3QFY12 – (1) Rs7.9 bn from Noida and Pune IT Park, (2) Rs3.4 bn from FSI sales in Gurgaon and (3) Rs0.8 bn from other assets. Net debt, however, has only reduced by Rs4.9 bn as the company utilized (1) Rs4.5 bn in capex and land buying, (2) Rs1.2 bn to purchase Hilton stake in hotel JV and (3) Rs0.8 bn on new launches. DLF is now targeting Rs60 bn of asset sales by end-FY2013E from – (1) Aman Resorts (Rs20 bn), (2) Wind/utilities/miscellaneous (Rs20 bn) and (3) Chennai and Mumbai project disposal including Hindoostan Mills land (Rs35-40 bn).

DLF (DLFU)

Property

Right course but still in rough waters. We believe DLF is moving in the right direction with (1) aggressive asset sale plans and visible intent of sticking to core areas, (2) outsourcing of construction once again and (3) a pick-up in deliveries and sales. Key negatives include (1) weak revenue recognition, (2) a subdued demand (residential and office space) environment and (3) high D/E of 0.9X. We cut our FY2012E/13E/14E earnings by 19%/19%/15% and maintain ADD rating at a revised target price of Rs260/share (earlier Rs270) factoring delays in execution and revised debt estimates.

DLFStock data Forecasts/Valuations 2012 2013E 2014E

52-week range (Rs) (high,low) EPS (Rs) 9.7 12.7 16.9Market Cap. (Rs bn) 395.9 EPS growth (%) 6.5 31.5 33.1

Shareholding pattern (%) P/E (X) 23.9 18.2 13.6Promoters 78.6 Sales (Rs bn) 97.5 117.7 155.4FIIs 15.5 Net profits (Rs bn) 16.4 21.6 28.7MFs 0.1 EBITDA (Rs bn) 41.6 51.1 64.2

Price performance (%) 1M 3M 12M EV/EBITDA (X) 15.2 12.3 9.5Absolute 25.0 (1.0) (6.1) ROE (%) 6.1 7.6 9.5Rel. to BSE-30 13.8 (3.2) (7.6) Div. Yield (%) 1.1 1.3 1.5

Company data and valuation summary

281-173

ADD

FEBRUARY 13, 2012

RESULT

Coverage view: Cautious

Price (Rs): 231

Target price (Rs): 260

BSE-30: 17,749

QUICK NUMBERS

• Revenues of Rs20.3 bn in 3QFY12 (-18% yoy, -20% qoq)

• EBITDA of Rs8.2 bn in 3QFY12 (-30% yoy and qoq)

• Sales of 3.3 mn sq. ft versus 1.3 mn sq. ft in 2QFY12

DLF Property

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

Revenue impacted due to slowdown in execution Interim results, DLF, March fiscal year-ends (Rs mn)

3QFY12 3QFY12E 2QFY12 3QFY11 3QFY12E qoq yoy 9HFY12 9HFY11 % changeNet sales 20,344 25,505 25,324 24,799 (20) (20) (18) 70,126 68,775 2Total cost (12,116) (13,805) (13,594) (13,020) (12) (11) (7) (39,059) (37,910) 3Construction cost (8,103) (9,466) (9,526) (14) (15) (26,991) (27,005) (0)Staff cost (1,379) (1,539) (1,338) (10) 3 (4,374) (4,250) 3Other expenditure (2,635) (2,589) (2,156) 2 22 (7,694) (6,656) 16EBITDA 8,227 11,699 11,730 11,780 (30) (30) (30) 31,067 30,865 1Other income 3,617 511 448 1,143 608 708 216 4,638 3,973 17Interest costs (6,199) (5,300) (5,263) (4,277) 17 18 45 (16,426) (12,499) 31Depreciation (1,797) (1,775) (1,753) (1,612) 1 3 11 (5,252) (4,650) 13Pretax profits 3,848 5,135 5,161 7,034 (25) (25) (45) 14,027 17,688 (21)Tax (1,353) (1,489) (1,475) (2,026) (9) (8) (33) (4,106) (4,439) (7)Net income 2,495 3,646 3,686 5,008 (32) (32) (50) 9,921 13,249 (25)Minority interest 109 0 (284) (57) (385)Share of profit/(loss) in associates (17) (5) (2) 259 725 20 51 (60)Net income before prior period adjustments 2,587 3,646 3,682 4,722 (29) (30) (45) 9,885 12,916 (23)Prior period adjustments (4) 42 (65) (94) 7 35Reported net income 2,584 3,646 3,724 4,657 (29) (31) (45) 9,891 12,951 (24)

Key ratiosEBITDA margin (%) 40.4 45.9 46.3 47.5 44.3 44.9PAT margin (%) 12.7 14.3 14.7 18.8 14.1 18.8Effective tax rate (%) 35.2 29.0 28.6 28.8 29.3 25.1

(% change)

Source: Company, Kotak Institutional Equities estimates

EBITDA margin declines to 40.4% Quarterly revenues, EBITDA, EBITDA margins and gross margins, DLF, March fiscal year-ends

0

10

20

30

40

50

1QFY

08

2QFY

08

3QFY

08

4QFY

08

1QFY

09

2QFY

09

3QFY

09

4QFY

09

1QFY

10

2QFY

10

3QFY

10

4QFY

10

1QFY

11

2QFY

11

3QFY

11

4QFY

11

1QFY

12

2QFY

12

3QFY

12

01020304050607080

Revenues (Rs bn) EBITDA (Rs bn) EBITDA margins (%) Gross margins (%)

Source: Company, Kotak Institutional Equities

Property DLF

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Operational performance

Development for sale. After declining to 1.3 mn sq. ft in 2QFY12 (lowest since 4QFY09) sales picked up to 3.3 mn sq. ft versus 2.5 mn sq. ft in 3QFY11. The company has, however, guided for a cautious 4QFY12/1QFY13 due to high interest rates which is making buyers delay their purchases. Majority of the sales have happened from plotted development launches in 3QFY12 in Lucknow and Mullanpur, New Chandigarh. DLF is targeting to launch 9.25 mn sq. ft of plots, 6 mn sq. ft of group housing and 0.5 mn sq. ft of commercial projects and has indicated that it has approvals to launch in most of the target micro-markets. DLF is in a good position to scale up its launches once approvals are in place since – (1) it has embarked on a strategy to use third-party contractors and so scaling up should not be a problem and (2) area under execution has declined to 44.9 mn sq. ft from 52.5 mn sq. ft at end-2QFY12 as DLF has readied 10.5 mn sq. ft for handing over.

Plans launches of 16 mn sq. ft Status of launch plans of DLF as of end-Jan 2012

Product type Location Launched Pipeline

Plots Gurgaon 1.8 2.3

Plots Lucknow 2.5 2.5

Plots Mullanpur, New Chandigarh - Ph 2 0.5 1.0

Plots Panchkula - Ph 2 1.0

Plots Hyderabad 2.5 2.5

Subtotal plots 7.3 9.3

Group Housing New Gurgaon 2.0

Group Housing Bengaluru 0.7 1.0

Group Housing Jallandhar 0.5 0.5

Super Premium Golf Links, Gurgaon 2.5

Subtotal 1.2 6.0

Commercial Delhi 0.5

Source: Company, Kotak Institutional Equities

Lease portfolio. On a net basis, incremental leasing (including 2.4 mn sq. ft sold which was earlier meant to be leased) increased to 2.6 mn sq. ft versus 0.2 mn sq. ft in 2QFY12 and 1.7 mn sq. ft in 3QFY11. DLF earned Rs 3.9 bn (Rs15.7 bn annualized) rental income from its retail and commercial offices in 3QFY12 which is steady qoq.

Execution. On the conference call, the company indicated that it is targeting 28 mn sq. ft of deliveries over the next two years. In 3QFY12, DLF handed over 10.5 mn sq. ft of projects (both development and rental) which is higher than FY2010 and FY2011 combined (9.2 mn sq. ft) and is targeting to deliver >1.5 mn sq. ft in 4QFY12E and >12 mn sq. ft in FY2013E. As a result of the deliveries in the quarter (readies 10.5 mn sq. ft for deliveries, adds 5 mn sq. ft of projects and suspends 2.2 mn sq. ft), area under execution has declined by 7.6 mn sq. ft qoq to 45 mn sq. ft which puts DLF in a good position to launch and add more projects to its portfolio from an execution angle.

DLF Property

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

Area under execution declines as DLF readies 10.5 mn sq. ft for handover Area under execution, DLF, March fiscal year-ends

3QFY12 2QFY12 3QFY11

Gurgaon 12.6 21.5 21.5

Super Metro 8 8 7.2

Rest of India 15.1 10.5 12

Rental Company 9.2 12.5 15.7

Total 44.9 52.5 56.4

Source: Company, Kotak Institutional Equities

Targeting to deliver 28 mn sq. ft over next two years Delivery plans of DLF

Project Segment Area (mn sq. ft)

Phase V, Gurgaon Group Housing 9.5

SIEL, Delhi Commercial Complex 0.5

OMR, Chennai (21 Towers) Group Housing 3

Kolkata Group Housing and Commercial C 2

Corporate Greens, Kolkata Commercial Complex 1.8

NTH, Gurgaon Group Housing 10

Rental Company Offices 1.5

Total 28.3

Source: Company, Kotak Institutional Equities

Asset monetization. Non-core asset monetization yielded Rs12 bn in 3QFY12 versus Rs2.4 bn in 2QFY12 as the company raised - (1) Rs7.9 bn from Noida and Pune IT Park, (2) Rs3.4 bn from FSI sales in Gurgaon and (3) Rs0.8 bn. DLF is now targeting Rs60 bn of asset sales by end-FY2013 from – (1) Aman Resorts (Rs20 bn), Wind/utilities/miscellaneous (Rs20 bn) and (3) Chennai and Mumbai project disposal including Hindoostan Mills land (Rs35-40 bn). The management has indicated that the company is in advanced talks for the sale of Aman Resorts and several buyers are waiting for global conditions to improve/stabilize before taking a decision.

Property DLF

6 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Asset disposal plans – targeting Rs60 bn from asset sales by March 2013 Visible non-core asset disposal plans

Non-core asset Description

Hospitality 20 In deep negotiations; delays due to adverse global macro conditions

Wind/Utilities 10

Misc. assets 10

Strategic proects in Mumbai and Chennai 35-40 Includes Hindoostan Mills land in Lower Parel

Total across medium term 75-80 Targetting Rs60 bn by March 2013 from 3 key assets

Value realizable (Rs bn)

Source: Company, Kotak Institutional Equities

Land bank. DLF’s land bank has now been declining since 3QFY10 and now stands at 349 mn sq. ft (due to land sales, handovers, business proposition changes from group housing to plotted which has a lower FSI). The company spends Rs3-4 bn every quarter on land purchases associated with plot sales (land aggregation).

Land bank declines as 10.3 mn sq. ft is ready for handing over Land bank details, DLF, March fiscal year-ends, 1QFY10-3QFY12 (mn sq. ft)

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11 2QFY11 3QFY11 4QFY11 1QFY12 2QFY12 3QFY12

Total land (mn sq. ft)

Gross area (beginning of quarter) 425 423 432 430 416 413 406 399 367 363 359

Add: New Land 10

Less: Projects disposed off (net) 2 0 3 13 3 7 7 12 2 4

Less: Handed over/Business proposition changes 19 2 0.2 10.3

Net land bank (end of quarter) 423 432 430 416 413 406 399 367 363 359 349

Other land (mn sq. ft)

Gross area (beginning of quarter) 412 411 421 418 405 402 395 388 359 355 351

Add: New Land 10

Less: Projects disposed off (net) 1 0 2.8 12 3 7 7 12 2 4

Less: Handed over/Business proposition changes 16 2 0.2 10.3

Net land bank (end of quarter) 411 421 418 405 402 395 388 359 355 351 341

Hotel land (mn sq. ft)

Gross area (beginning of quarter) 13 12 12 12 12 11 11 11 8 8 8

Add: New Land

Less: Projects disposed off (net) 1 0 0 0

Less: Handed over/Business proposition changes 3

Net land bank (end of quarter) 12 12 12 12 12 11 11 8 8 8 8

Source: Company, Kotak Institutional Equities

DLF Property

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

Sales subdued due to high interest rates and high property prices while leasing is subdued due to global uncertainty DLF, March fiscal year-ends

4QFY09 1QFY10 2QFY10 3QFY10 4QFY10 1QFY11 2QFY11 3QFY11 4QFY11 1QFY12 2QFY12 3QFY12Development businessSales status (mn sq. ft)Opening balance 27.5 28.3 30.1 32.8 35.2 38.9 40.2 42.3 44.8 46.4 48.7 49.7Add: sales booked during quarter 0.8 2.7 2.7 3.1 3.6 1.9 2.1 2.5 3.8 2.3 1.3 3.3Less: handed over/suspended 0.0 0.8 0.0 0.7 0.0 0.5 0.0 0.0 2.2 0.0 0.2 9.5Closing balance 28.3 30.1 32.8 35.2 38.9 40.2 42.3 44.8 46.4 48.7 49.7 43.5Under Construction (mn sq. ft)Opening Balance 17.3 18.3 25.0 31.6 33.4 38.8 38.3 40.7 40.7 39.4 39.4 39.6Add: new launches/additions/suspended 1.0 7.5 6.6 2.6 5.4 0.0 2.4 0.0 0.9 0.0 0.5 4.9Less: handed Over 0.0 0.8 0.0 0.7 0.0 0.5 0.0 0.0 2.2 0.0 0.2 9.5Closing Balance 18.3 25.0 31.6 33.4 38.8 38.3 40.7 40.7 39.4 39.4 39.6 35.0

Rental businessLease status (mn sq. ft)Opening balance 17.5 17.5 17.0 16.5 18.7 19.4 20.4 22.1 23.7 23.8 24.5 24.7Add: lease booked during quarter (0.1) 0.0 (0.4) 0.4 0.7 1.2 2.0 2.0 1.4 1.0 0.7 0.4Less: cancellation/adjustment/sold 0.0 0.6 0.0 0.0 0.0 0.2 0.3 0.3 1.3 0.2 0.5 2.6Closing balance 17.4 17.0 16.5 16.9 19.4 20.4 22.1 23.7 23.8 24.5 24.7 22.5Under Construction (mn sq. ft)Opening Balance 37.2 17.7 17.1 17.1 17.1 17.1 16.3 15.8 15.7 14.5 12.5 12.5Add: new launches/additions 0.0 0.0 0.0 0.0 0.0 0.0 0.9 0.9 0.0 (0.2) 0.0 0.0Less: handed Over 0.4 0.6 0.0 0.0 0.0 0.86 1.3 1.0 1.2 1.9 0.0 1.0Less: Suspension/adjustment 19.1 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 2.2Closing balance 17.7 17.1 17.1 17.1 17.1 16.3 15.8 15.7 14.5 12.5 12.5 9.2

Source: Company, Kotak Institutional Equities

Net-debt declines 2%; cost of debt at 12.75%

DLF’s net debt has dropped by 2% qoq to Rs238 bn as DLF utilized cash from assets sales to reduce its debt burden and net-D/E is now at 0.86X versus 0.88X at end-2QFY12 and 0.82X at end-3QFY11. DLF’s average cost of debt is now at 12.75% on a gross debt of Rs250 bn out of which Rs12 bn is linked to rental properties and likely funded through lease rental inflows. Net fixed assets declined by Rs6.3 bn due to sale of the IT Parks in Pune and Noida. Loans and advances have increased by Rs4.3 bn as the company had to pay Rs1-1.5 bn while shifting to third party contractors and tax outflow connected to properties under litigation (taxes on SEZs) have been classified under loans and advances.

Property DLF

8 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Consolidated summary statement of assets and liabilities Quarterly Balance Sheet, DLF, March fiscal year-ends (Rs mn)

Particulars Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 yoy qoqNet fixed assets 143,540 277,300 278,040 262,224 263,460 281,841 284,110 285,070 278,690 15,230 (6,380)Investments 29,750 55,200 30,060 16,816 13,110 9,958 9,610 15,039 11,800 (1,310) (3,239)Current assets, loans and advances 309,390 280,740 279,640 301,524 305,810 332,717 334,710 343,632 346,350 40,540 2,718

Stocks 115,500 124,120 130,960 143,974 147,850 150,388 152,610 152,338 154,690 6,840 2,352Sundry debtors 19,830 16,660 14,390 19,177 19,460 17,257 18,180 19,540 18,480 (980) (1,060)Cash and bank balances 8,140 9,130 12,970 15,560 11,780 13,461 11,040 11,820 12,460 680 640Other current assets 82,630 44,830 47,680 47,337 49,720 78,900 77,030 79,361 75,870 26,150 (3,491)Loans and advances 83,290 86,000 73,640 75,477 77,000 72,712 75,850 80,572 84,850 7,850 4,278

Goodwill 20,070 12,670 12,580 12,769 13,730 13,840 15,060 15,086 15,200 1,470 114Total use of funds 502,750 625,910 600,320 593,334 596,110 638,357 643,490 658,827 652,040 55,930 (6,787)

Total loans 171,680 216,770 233,740 232,388 236,110 239,903 238,630 254,498 250,260 14,150 (4,238)Secured loans 146,840 193,020 209,460 208,100 219,470 222,762Unsecured loans 24,840 23,750 24,280 24,288 16,640 17,141

Current liabilities and provisions 70,580 92,510 86,110 89,146 88,840 131,014 133,600 129,414 126,450 37,610 (2,964)Deferred tax liability (net) (800) 2,620 2,970 (774) (820) (1,633) (1,260) (1,469) (1,840) (1,020) (371)Shareholders funds 261,290 314,010 277,500 272,574 271,980 269,073 272,520 276,384 277,170 5,190 786Total sources of fund 502,750 625,910 600,320 593,334 596,110 638,357 643,490 658,827 652,040 55,930 (6,787)

Change

Source: Company, Kotak Institutional Equities

Changes to our model – maintain ADD at a revised target price of Rs260/share

We make the following changes to our model –

Delay execution in projects noting (1) delay in launches, (2) the shift over to third-party contractors from in-house construction which implies projects were likely delayed than earlier expected.

Increase gross debt to Rs260 bn for FY2012E from Rs235 bn earlier.

We are cutting our revenues and earnings estimate by 12%/15%/16% and 19%/19%/15% for FY2012E/13E/14E respectively.

Cut revenue estimates by 12%/15%/16% for FY2012E/13E/14E Changes in estimates, DLF

2012E 2013E 2014E 2012E 2013E 2014E 2012E 2013E 2014ERevenue (Rs mn) 97,464 117,734 155,352 110,891 137,989 184,744 (12) (15) (16) EBITDA (Rs mn) 41,630 51,142 64,237 47,624 62,124 73,566 (13) (18) (13) Net income (Rs mn) 16,402 21,576 28,720 20,224 26,649 33,985 (19) (19) (15)

New estimates Old estimates % change

Source: Company, Kotak Institutional Equities estimates

DLF Property

KOTAK INSTITUTIONAL EQUITIES RESEARCH 9

We set our target price at Rs260/share NAV-based valuation, DLF, March fiscal year-ends (Rs bn)

Valuation Methodology 0% 3% 5% 10%Valuation of land reserves 458 559 635 857 Residential 191 244 284 402 Retail 113 139 159 215 Commercial (sold) 80 102 118 164 Commercial (leased) 79 84 88 99Add: 22 Hotel sites 1X land acquisition cost 25 25 25 25Add: Construction JV 10X FY2013E P/E 8 8 8 8Add: Investments in power business 15 15 15 15Less: Net debt as on March 31, 2013 (235) (235) (235) (235)Less: Land cost to be paid (1) (1) (1) (1)NAV (Rs bn) 270 372 448 669NAV/share (Rs) 157 217 261 390Total no. of shares including ESOPs of 17 mn shares (mn) 1,716Target price/share (Rs) 260

Growth rate in selling pricesMarch '13 based NAV

Source: Kotak Institutional Equities estimates

Profit model of DLF March fiscal year-ends, 2008-2014E (Rs mn)

2008 2009 2010 2011 2012E 2013E 2014ETotal revenues 144,329 100,354 74,229 95,606 97,464 117,734 155,352 Land and construction cost (39,998) (32,295) (25,795) (42,999) (39,750) (48,758) (70,375) Employee costs (2,998) (4,537) (4,668) (5,721) (6,825) (8,651) (11,420) SG&A costs (4,229) (7,622) (8,650) (9,358) (9,259) (9,183) (9,321) EBITDA 97,105 55,900 35,116 37,527 41,630 51,142 64,237 Other income 2,464 3,960 4,280 5,839 5,314 6,762 7,222 Interest (3,100) (5,548) (11,100) (17,056) (16,818) (17,929) (20,239) Depreciation (901) (2,390) (3,249) (6,307) (6,855) (10,259) (12,926) Pretax profits 95,568 51,922 25,046 20,002 23,271 29,715 38,294 Current tax (17,146) (6,754) (7,762) (4,594) (8,114) (10,210) (12,613) Deferred tax (176) 739 - 1,246 2,071 3,039 Net income 78,247 45,168 18,024 15,408 16,402 21,576 28,720 Reported net income 78,156 44,682 18,140 15,424 16,402 21,576 28,720

EPS (Rs)Primary 47.1 26.2 10.1 9.1 9.7 12.7 16.9 Fully diluted 46.6 26.2 10.1 9.0 9.6 12.6 16.8 Shares outstanding (mn)Year end 1,705 1,697 1,697 1,698 1,698 1,698 1,698 Primary 1,661 1,697 1,697 1,698 1,698 1,698 1,698 Fully diluted 1,678 1,714 1,714 1,715 1,715 1,715 1,715 Cash flow per share (Rs)Primary 46.4 18.1 4.6 18.1 5.3 9.6 15.9 Fully diluted 45.9 17.9 4.6 18.0 5.3 9.5 15.7 Growth (%)Net income (adjusted) 302 (43) (59) (15) 6 32 33 EPS (adjusted) 259 (44) (61) (11) 6 32 33 DCF/share 1,000 (61) (75) 294 (71) 79 66 Cash tax rate (%) 18 13 31 23 35 34 33 Effective tax rate (%) 18 13 28 23 30 27 25 DPS 4 3 3 2.0 2.5 3.0 3.5

Source: Company, Kotak Institutional Equities estimates

Property DLF

10 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Balance Sheet of DLF March fiscal year-ends, 2008-2014E (Rs mn)

2008 2009 2010 2011 2012E 2013E 2014EEquityShare capital 12,905 17,354 62,593 21,498 21,498 21,498 21,498 Reserves/surplus 183,977 224,184 241,734 241,823 253,386 269,155 291,100 Total equity 196,883 241,538 304,327 263,321 274,884 290,653 312,598 Deferred tax liability/(asset) 359 (414) 2,515 (1,633) (2,878) (4,949) (7,989) LiabilitiesSecured loans 80,534 132,623 193,016 239,903 250,903 247,903 236,903 Unsecured loans 42,237 30,578 23,751 — — — — Total borrowings 122,771 163,201 216,766 239,903 250,903 247,903 236,903 Currrent liabilities 72,157 78,244 87,771 131,014 100,357 108,240 122,869 Total capital 396,065 488,906 617,658 638,357 629,017 647,598 670,134 AssetsCash 21,421 11,956 9,282 13,461 12,794 13,227 22,857 Current assets 244,579 304,268 263,775 319,257 343,632 364,932 382,549 Gross block 51,626 84,867 178,845 190,687 195,865 205,182 215,431 Less: accumulated depreciation 3,435 5,743 13,265 19,572 22,853 33,113 46,038 Net fixed assets 48,191 79,124 165,580 171,115 173,011 172,069 169,392 Capital work-in-progress 51,840 56,882 111,288 110,727 75,782 73,572 71,538 Total fixed assets 100,031 136,006 276,868 281,841 248,794 245,641 240,930 Intangible assets 20,931 22,651 12,680 13,840 13,840 13,840 13,840 Investments 9,102 14,025 55,052 9,958 9,958 9,958 9,958 Misc. expenses — — — — — — — Total assets 396,065 488,906 617,658 638,357 629,017 647,598 670,134

Leverage ratios (%)Debt/equity 62.2 67.7 70.6 91.7 92.2 86.8 77.8 Debt/capitalization 38.4 40.4 41.4 47.8 48.0 46.5 43.7 Net debt/equity 51.4 62.7 67.6 86.5 87.5 82.1 70.3 Net debt/capitalization 33.9 38.5 40.3 46.4 46.7 45.1 41.3 RoAE 65.9 20.4 6.6 5.4 6.1 7.7 9.7 RoACE 35.3 13.8 5.4 5.6 5.1 5.9 7.3

Source: Company, Kotak Institutional Equities estimates

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Better-than-expected EBITDA led by lower operating costs; net income boosted by lower DD&A

OIL reported 3QFY12 EBITDA of `14.3 bn (-27% qoq and +8.8% yoy), 11% higher than our estimate of `12.9 bn. 3QFY12 reported net income was `10.1 bn (-16.2% qoq and +11.7% yoy), 15.5% higher than our estimate of `8.8 bn. The positive variance against our estimates reflects (1) higher-than-expected oil and gas sales volumes, (2) lower staff costs and other expenditure and (3) lower DD&A expenses. The qoq decline in net income reflects (1) lower net realized price of US$57/bbl (-US$29.3/bbl qoq) and (2) a sharp decline in DD&A expense to `2.9 bn (-51% qoq).

Stock trades at 2.9X FY2012E EBITDA despite assuming a conservative subsidy burden

We highlight that OIL stock trades at an inexpensive 2.9X FY2012E EBITDA of `68 bn, out of which the company reported `58 bn in 9MFY12. Besides, we have modeled a fairly conservative scenario of upstream companies bearing 45% of gross under-recoveries of `1.4 tn in FY2012E versus actual sharing of ~38% in 9MFY12. We note that OIL has a large net cash balance of `552/share (as of September 30, 2011). More important, OIL continues to perform well operationally with its 9MFY12 crude sales volumes growing 9% yoy and gas sales volumes jumping 19% yoy. We note that OIL’s volume trajectory is better than ONGC’s.

Maintain BUY with a target price of `1,750 (`1,720 previously)

We maintain our BUY rating on the stock with a revised target price of `1,750 (`1,720 previously) based on 9X FY2013E EPS plus value of investments, potential upside of 32% from current levels. We find OIL’s valuations attractive with the stock trading at 9X FY2012E EPS and 7X FY2013E EPS. The earnings are rather depressed given higher subsidy burden assumed by us.

Revise earnings for FY2012-14E

We have revised our FY2012-14 EPS estimates to `146 (-5.4%), `190 (+1.6%) and `219 (+14.2%) respectively to reflect (1) higher subsidy sharing by upstream companies, (2) higher crude price assumptions, (3) revised exchange rates and (4) other minor changes. We have assumed that upstream companies will bear 45% of total under-recoveries in FY2012 and 50% in FY2013-14 versus 37.9% in 9MFY12 and 38.7% in FY2011.

Oil India (OINL)

Energy

Country cousin steals a march. OIL reported better-than-expected net income of `10.1 bn (-16% qoq and +12% yoy) in 3QFY12 versus our estimate of `8.8 bn, led by (1) higher oil and gas sales volumes, (2) lower operating costs and (3) lower DD&A expenses. The company reported EPS (adjusted) of `128 in 9MFY12, higher than FY2011 EPS of `120. We reiterate our BUY rating on OIL with a revised target price of `1,750 (`1,720 previously) noting (1) attractive valuations with the stock trading at 9X FY2012E EPS and (2) strong long-term growth prospects.

Oil IndiaStock data Forecasts/Valuations 2011 2012E 2013E

52-week range (Rs) (high,low) EPS (Rs) 120.0 146.1 189.9Market Cap. (Rs bn) 317.7 EPS growth (%) 4.2 21.8 30.0

Shareholding pattern (%) P/E (X) 11.0 9.0 7.0Promoters 78.4 Sales (Rs bn) 83.0 100.2 121.3FIIs 2.3 Net profits (Rs bn) 28.8 35.1 45.7MFs 4.2 EBITDA (Rs bn) 48.0 67.7 81.8

Price performance (%) 1M 3M 12M EV/EBITDA (X) 4.2 2.9 2.2Absolute 19.0 3.6 2.4 ROE (%) 16.2 17.5 20.1Rel. to BSE-30 8.4 1.3 0.7 Div. Yield (%) 2.8 4.2 5.7

Company data and valuation summary

1,424-1,101

BUY

FEBRUARY 12, 2012

RESULT

Coverage view: Attractive

Price (Rs): 1,321

Target price (Rs): 1,750

BSE-30: 17,749

QUICK NUMBERS

• 13.6% yoy growth in gas sales; 4.1% yoy growth in crude oil sales

• OIL’s share of the subsidy burden on upstream in 9MFY12 was 12.1%

• 32% potential upside from current levels

Energy Oil India

12 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Key highlights of 3QFY12 results

We highlight the key highlights of 3QFY12 results (see Exhibit 1) below.

OIL interim results, March fiscal year-ends, (` mn)

(% chg.) yoy3QFY12 3QFY12E 3QFY11 2QFY12 3QFY12E 3QFY11 2QFY12 9MFY12 9MFY11 (% chg.) 2012E

Net sales 25,898 25,405 24,734 33,571 1.9 4.7 (22.9) 83,130 65,148 27.6 100,233 Total expenditure (11,616) (12,532) (11,606) (14,020) (7.3) 0.1 (17.1) (36,885) (31,149) 18.4 (47,244) Increase/(decrease) in stock 5 129 267 207 216 —Raw materials (a) (381) (443) (375) (335) (14.1) 1.7 13.7 (1,015) (1,066) (4.8) (1,265) Staff expenditure (2,611) (3,233) (2,867) (3,502) (19.2) (8.9) (25.4) (9,117) (7,635) 19.4 (12,086) Statutory levies (7,172) (7,019) (6,762) (8,784) 2.2 6.1 (18.3) (22,716) (18,341) 23.9 (27,334) Other expenditure (1,457) (1,836) (1,732) (1,666) (20.6) (15.9) (12.5) (4,244) (4,323) (1.8) (6,560) EBITDA 14,282 12,873 13,128 19,551 10.9 8.8 (27.0) 46,245 33,999 36.0 52,988 Other income 3,756 3,615 2,773 4,555 3.9 35.4 (17.5) 11,337 6,857 65.3 14,690 Interest (11) (59) (12) (5) (104) (27) 278.8 (162) DD&A (2,887) (3,433) (2,261) (5,901) (15.9) 27.7 (51.1) (11,572) (6,065) 90.8 (15,136) Depletion (1,040) (896) (932) 16.0 11.7 (2,830) (2,344) 20.7 Depreciation (388) (427) (373) (9.3) 3.8 (1,119) (1,296) (13.7) Dry wells (including provision) (1,459) (938) (4,596) 55.6 (68.3) (7,624) (2,425) 214.3 Pretax profits 15,140 12,996 13,629 18,201 16.5 11.1 (16.8) 45,906 34,764 32.1 52,381 Extraordinary/Prior period adjustment — — (1,081) (1,081) — (1,081) Tax (5,000) (4,228) (4,549) (5,734) 18.3 9.9 (12.8) (14,804) (11,513) 28.6 (16,891) Deferred tax — 11 — — — — (4) Net income 10,140 8,780 9,080 11,385 15.5 11.7 (10.9) 30,021 23,251 29.1 34,405 Adjusted net income 10,140 8,780 9,080 12,104 15.5 11.7 (16.2) 30,754 23,251 32.3 35,137 EPS (Rs) 42.2 36.5 37.8 50.3 127.9 96.7 146.1 Tax rate (%) 33.0 32.4 33.4 33.5 32.2 33.1 32.3

Volume dataSubsidy loss 18,530 18,529 5,586 8,444 231.7 119.4 44,781 16,877 165.3 74,060 Crude sales ('000 tons) 950 938 913 966 1.3 4.1 (1.7) 2,883 2,645 9.0 3,832 Gas sales (mcm) 544 525 479 543 3.7 13.6 0.2 1,595 1,344 18.7 2,123 Crude production ('000 tons) 962 928 991 3.7 (2.9) 2,918 2,665 9.5 Gas production (mcm) 676 616 677 9.7 (0.1) 1,994 1,752 13.8

Pricing data (US$/bbl)Gross crude price realization 110.1 109.0 85.7 112.5 28.5 (2.1) 112.8 79.7 41.5 112.8 Subsidy discount 53.1 52.7 18.5 26.2 186.1 102.4 45.5 19.2 137.3 54.7 Net crude price realization 57.0 56.3 67.1 86.3 (15.1) (33.9) 67.3 60.6 11.1 58.0

Notes:(a) Represents consumption of stores & spares.

Source: Company, Kotak Institutional Equities estimates

A sharp decline in net realized price for crude oil. OIL’s 3QFY12 net realized crude price was US$57bbl versus US$86.3/bbl in 2QFY12 and US$67.1/bbl in 3QFY11. OIL’s subsidy burden in 3QFY12 was `18.5 bn or US$53.1/bbl in crude price oil equivalent terms versus crude price equivalent of US$26.2/bbl in 2QFY12 and US$18.5/bbl in 3QFY11.

Oil and gas sales volumes increase yoy. 3QFY12 gas sales volume increased 13.6% yoy and 0.2% qoq to 544 mcm (equivalent of 5.9 mcm/d). 3QFY12 crude sales volume increased 4.1% yoy and declined 1.7% qoq to 0.95 mn tons.

Lower employee cost. OIL’s employee cost declined 25.4% qoq and 8.9% yoy to `2.6 bn in 3QFY12. The employee cost in 3QFY12 includes a provision of `192 mn due to differential superannuation benefits to employees versus `376 mn accounted in the previous quarter.

Other expenditure declines. OIL’s other expenditure declined 12.5% qoq and 15.9% yoy to `1.5 bn.

Oil India Energy

KOTAK INSTITUTIONAL EQUITIES RESEARCH 13

Lower DD&A expenses qoq. DD&A expenses declined sharply by 51.1% qoq to `2.9 bn (+27.7% yoy). The sharp qoq decline in DD&A expenses represents lower write-off of dry wells and provisions, which declined to `1.5 bn (-68.3% qoq and +55.6% yoy). We note that the company made a provision of ~`4 bn in 2QFY12 to cover prospective liabilities related to Minimum Work Program (MWP) requirements for its NELP blocks.

Other income declines qoq. OIL’s adjusted other income declined by 17.5% qoq to `3.8 bn (+35.4% yoy). We note that reported other income in 2QFY12 included pipeline revenues of `1.4 bn for FY2008-11 due to revision in forward pumping transportation tariff effective from April 2008.

Additional interim dividend and bonus issue. OIL’s Board declared a second interim dividend of `10/share in addition to the interim dividend of `25/share paid earlier. The Board has also recommended a bonus issue of 3:2 scheduled to be completed by April 10, 2012, subject to shareholder approval.

Key assumptions behind our earnings model

We discuss the key assumptions behind our earnings model below. Exhibit 2 gives the major assumptions behind our earnings model and Exhibit 3 gives sensitivity of OIL’s EPS to key variables (INR/USD rate, crude oil price, natural gas price).

Strong growth in net crude price realizations over the next few years Key assumptions, March fiscal year-ends, 2007-2014E

2007 2008 2009 2010 2011 2012E 2013E 2014E Rs/US$ rate 45.3 40.3 45.8 47.4 45.6 48.0 50.5 50.0 Subsidy share scheme loss (Rs mn) 19,938 23,051 30,233 15,488 32,931 74,060 53,400 33,571 Import tariff on crude oil (%) 5.1 5.2 0.9 0.4 5.2 1.2 — —

Crude/natural gas pricesCrude priceCrude price, Bonny Light (US$/bbl) 64.8 78.9 83.0 67.1 84.0 113.0 105.0 100.0 Net crude price, OIL-India (US$/bbl) 47.0 59.8 55.6 56.2 58.5 58.0 67.8 76.7

Natural gas priceCeiling natural gas price, India (Rs/cu m) 3.20 3.20 3.20 3.20 6.78 7.54 7.94 7.86Ceiling natural gas price, India (US$/mn BTU) 1.89 2.12 1.87 1.80 3.98 4.20 4.20 4.20Net natural gas price, OIL-India (Rs/cu m) 2.88 2.88 2.88 2.88 5.49 6.10 6.42 6.36Net natural gas price, OIL-India (US$/mn BTU) 1.70 1.91 1.68 1.62 3.22 3.40 3.40 3.40

Sales volumes—Domestic fieldsCrude oil (mn tons) 3.0 3.0 3.4 3.5 3.6 3.8 3.9 4.0Natural gas (bcm) 1.8 1.8 1.7 1.9 1.8 2.1 2.2 2.4Total sales (mn toe) 4.6 4.7 4.9 5.2 5.2 5.7 5.9 6.1Total sales (mn boe) 34 35 37 39 39 43 44 45Crude oil (%) 66 65 69 68 69 67 67 65Natural gas (%) 34 35 31 32 31 33 33 35

Source: Company, Kotak Institutional Equities estimates

Energy Oil India

14 KOTAK INSTITUTIONAL EQUITIES RESEARCH

OIL's earnings are highly sensitive to crude and gas price assumptions Earnings sensitivity of OIL to key variables

2012E 2013E 2014EDownside Base case Upside Downside Base case Upside Downside Base case Upside

Exchange rateRs/US$ 47.0 48.0 49.0 49.5 50.5 51.5 49.0 50.0 51.0Net profits (Rs mn) 33,126 35,137 37,149 43,753 45,670 47,587 50,824 52,706 54,588Earnings per share (Rs) 137.8 146.1 154.5 182.0 189.9 197.9 211.4 219.2 227.0% upside/(downside) (5.7) 5.7 (4.2) 4.2 (3.6) 3.6Average crude pricesCrude price (US$/bbl) 111.0 113.0 115.0 103.0 105.0 107.0 98.0 100.0 102.0Net profits (Rs mn) 33,568 35,137 36,706 43,998 45,670 47,343 51,018 52,706 54,394Earnings per share (Rs) 139.6 146.1 152.7 183.0 189.9 196.9 212.2 219.2 226.2% upside/(downside) (4.5) 4.5 (3.7) 3.7 (3.2) 3.2CessCess on domestic crude (Rs/ton) 3,090 2,575 2,060 3,090 2,575 2,060 3,090 2,575 2,060Net profits (Rs mn) 33,821 35,137 36,453 44,328 45,670 47,013 51,337 52,706 54,075Earnings per share (Rs) 140.7 146.1 151.6 184.4 189.9 195.5 213.5 219.2 224.9% upside/(downside) (3.7) 3.7 (2.9) 2.9 (2.6) 2.6Natural gas pricesNatural gas price (US$/mn BTU) 3.2 4.2 5.2 3.2 4.2 5.2 3.2 4.2 5.2Net profits (Rs mn) 33,053 35,137 37,221 43,408 45,670 47,932 50,280 52,706 55,132Earnings per share (Rs) 137.5 146.1 154.8 180.5 189.9 199.3 209.1 219.2 229.3% upside/(downside) (5.9) 5.9 (5.0) 5.0 (4.6) 4.6

Source: Kotak Institutional Equities estimates

Subsidy amount. We model a subsidy amount for FY2012, FY2013 and FY2014 of `74.1 bn, `53.4 bn and `33.6 bn respectively. We assume that upstream companies will bear 45% of gross under-recoveries in FY2012 and 50% in FY2013-14 versus 37.9% in 9MFY12 and 38.7% in FY2011. We assume (1) moderate price increases in diesel, kerosene and LPG, and (2) lower crude oil prices, which result in gross under-recoveries declining to `921 bn in FY2013E versus `1.4 tn in FY2012E. We model OIL bearing 12.2% of the subsidy burden on upstream companies in FY2012 and ~12% in FY2013-14 versus 12.1% in 9MFY12. We assume a modest decline in OIL’s share in FY2013-14 due to an increase in GAIL’s share, given a lower proportion of under-recoveries on diesel in the overall under-recoveries over the next two years, led by lower crude prices.

Oil and gas volumes. We model crude oil sales volumes of 3.83 mn tons in FY2012, 3.91 mn tons in FY2013 and 3.98 mn tons in FY2014 versus a run-rate of 3.84 mtpa in 9MFY12 and 3.6 mn tons in FY2011. We model gas volumes at 5.8 mcm/d for FY2012, 6 mcm/d in FY2013 and 6.5 mcm/d in FY2014 versus 5.8 mcm/d in 9MFY12 and 5 mcm/d for FY2011. Implementation of EOR/IOR techniques in OIL’s existing producing fields will contribute to higher volumes. We note that OIL’s 2P reserves are meaningfully higher than its 1P reserves (see Exhibit 4 for details of OIL’s reserves), which offers OIL scope to increase its production volumes significantly from current levels.

Oil India Energy

KOTAK INSTITUTIONAL EQUITIES RESEARCH 15

2P reserves are 87% higher than proven reserves for Oil India Oil India’s reserves, March fiscal year-ends, 2007-11 (mn boe)

2007 2008 2009 2010 20111P reservesCrude oil 283 296 285 282 280 Natural gas 169 233 247 239 225 Overall 452 529 532 521 505 2P reservesCrude oil 540 588 575 580 584 Natural gas 289 345 399 377 360 Overall 829 933 974 957 944 3P reservesCrude oil 1,000 1,039 999 915 867 Natural gas 471 472 543 522 505 Overall 1,471 1,511 1,542 1,437 1,372

Source: Company, Kotak Institutional Equities

Crude oil price assumption. We have assumed higher crude oil (Dated Brent) prices for FY2012, FY2013 and FY2014 at US$113/bbl, US$105/bbl and US$100/bbl respectively versus US$110/bbl, US$100/bbl and US$95/bbl previously. However, we would focus more on OIL’s net realized crude price and our long-term crude price assumption. Exhibit 5 gives OIL’s historical net realized price and our expectations for FY2012 (US$58/bbl), FY2013 (US$67.8/bbl) and FY2014 (US$76.7/bbl).

OIL’s net realization has improved over the past few years OIL's net crude price realization, March fiscal year-ends, 2004-14E (US$/bbl)

28.234.4

48.8 47.0

59.855.6 56.2 58.5 58.0

67.8

76.7

0

15

30

45

60

75

90

2004

2005

2006

2007

2008

2009

2010

2011

2012

E

2013

E

2014

E

(US$/bbl)

Source: Company, Kotak Institutional Equities estimates

The lower net realization for FY2012E (US$58/bbl) versus 9MFY12’s US$67.3/bbl reflects our assumption of higher subsidy burden on upstream companies at 45% of gross under-recoveries in FY2012E.

Natural gas price assumption. We assume FY2012-14 natural gas price at US$4.2/mn BTU.

INR-USD exchange rate. We have revised our exchange rate assumptions for FY2012, FY2013 and FY2014 to `48/US$, `50.5/US$ and `50/US$ respectively versus `48.7/US$, `52.5/US$ and `51/US$ previously.

Energy Oil India

16 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Fair value of OIL (`/share)

FY2013E EPS 190 P/E (X) 9 Valuation 1,709 Investments 41 Numaligarh Refinery Limited 24 Other investments 17

Fair value 1,750

Source: Kotak Institutional Equities estimates

Profit model, balance sheet, cash model of OIL, March fiscal year-ends, 2006-2014E (` mn)

2007 2008 2009 2010 2011 2012E 2013E 2014EProfit model (Rs mn)Net sales 53,892 60,819 72,414 79,056 83,034 100,233 121,348 136,321EBITDA 22,280 23,812 28,400 34,486 36,160 52,988 67,679 77,505Other income 5,335 6,770 9,372 9,371 11,851 14,690 14,090 15,450Interest (140) (344) (87) (37) (139) (162) (2) —Depreciation and depletion (2,595) (3,093) (3,768) (4,811) (4,781) (15,136) (14,162) (14,935)Pretax profits 24,881 27,145 33,916 39,010 43,091 52,381 67,605 78,019Tax (7,406) (8,538) (11,910) (11,598) (12,973) (16,891) (21,917) (25,300)Deferred tax (1,020) (707) (343) (1,211) (1,282) (4) (17) (14)Adjusted net profits 16,436 17,897 21,646 26,169 28,850 35,137 45,670 52,706Earnings per share (Rs) 76.8 83.6 101.1 115.2 120.0 146.1 189.9 219.2

Balance sheet (Rs mn)Total equity 68,491 79,330 93,310 137,638 156,019 175,053 199,764 228,716Deferred tax liability 8,033 8,655 8,998 10,209 11,491 11,495 11,512 11,526Liability for abandonment cost 11 11 15 19 1,645 1,645 1,645 1,645Total borrowings 8,140 1,749 565 375 10,268 50 — —Currrent liabilities 10,320 17,541 30,914 32,693 33,216 32,180 37,194 38,671Total liabilities and equity 94,995 107,286 133,801 180,934 212,638 220,423 250,115 280,558Cash 32,757 42,808 60,700 85,429 117,693 114,359 131,425 148,182Current assets 22,350 18,957 22,853 37,266 30,318 29,447 31,735 33,357Total fixed assets 35,813 40,633 45,361 49,460 55,723 67,712 78,050 90,115Investments 4,075 4,887 4,887 8,594 8,904 8,904 8,904 8,904Deferred expenditure — — — 184 — — — —Total assets 94,995 107,286 133,801 180,934 212,638 220,422 250,115 280,558

Free cash flow (Rs mn)Operating cash flow, excl. working capital 18,357 20,104 27,246 23,621 26,353 25,104 38,510 45,205Working capital changes (8,696) 7,435 2,368 (9,113) 4,034 (166) 2,726 (145)Capital expenditure (9,370) (9,492) (8,496) (11,485) (9,518) (17,374) (17,250) (20,000)Investments 226 (811) — (3,201) (310) — — —Other income 2,892 4,214 5,470 7,268 6,343 14,690 14,090 15,450Free cash flow 3,409 21,450 26,587 7,091 26,902 22,254 38,076 40,510

Ratios (%)Debt/equity 11.9 2.2 0.6 0.3 6.6 — — —Net debt/equity (32.8) (31.9) (31.9) (38.3) (54.1) (46.9) (47.2) (47.9)RoAE 23.1 21.8 22.8 20.9 18.3 19.8 23.0 23.3RoACE 23.0 21.5 22.7 20.9 18.1 19.6 22.8 23.2

Key assumptionsRs/dollar rate 45.3 40.3 45.8 47.4 45.6 48.0 50.5 50.0 Crude fob price (US$/bbl) 64.8 78.9 83.0 67.1 84.0 113.0 105.0 100.0 Ceiling/actual natural gas price (Rs/'000 cm) 3,200 3,200 3,200 3,200 6,783 7,544 7,937 7,858 Subsidy loss (Rs bn) 19.9 23.1 30.2 15.5 32.9 74.1 53.4 33.6

Source: Company, Kotak Institutional Equities estimates

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

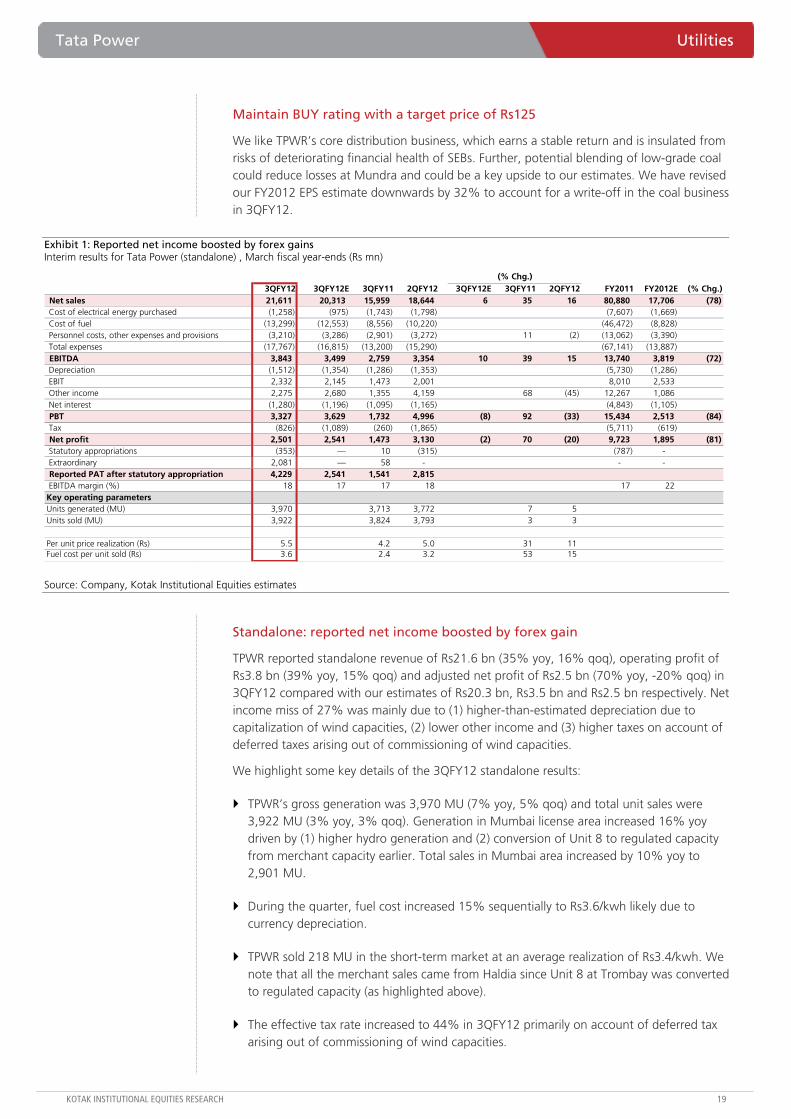

Consolidated operations hit by write-offs in the coal business

TPWR reported standalone revenue of Rs21.6 bn (35% yoy, 16% qoq), operating profit of Rs3.8 bn (39% yoy, 15% qoq) and adjusted net profit of Rs2.5 bn (70% yoy, -20% qoq) in 3QFY12 against our estimates of Rs20.3 bn, Rs3.5 bn and Rs2.5 bn respectively. TPWR posted consolidated revenues of Rs66.5 bn (51% yoy, 6% qoq), operating profit of Rs9.9 bn (-4% yoy, -27% qoq) and adjusted net profit of Rs2 bn (-50% yoy, -45% qoq) in 3QFY12. Despite robust volume and realization in the coal business (aided further by currency depreciation), consolidated profitability was dented by a Rs6.5 bn write-off of deferred stripping costs in the coal business.. We discuss key highlights of the performance subsequently.

Bumi guidance of 80-85 mn tons production in CY2012, ramp-up to 100 mn tons by CY2013

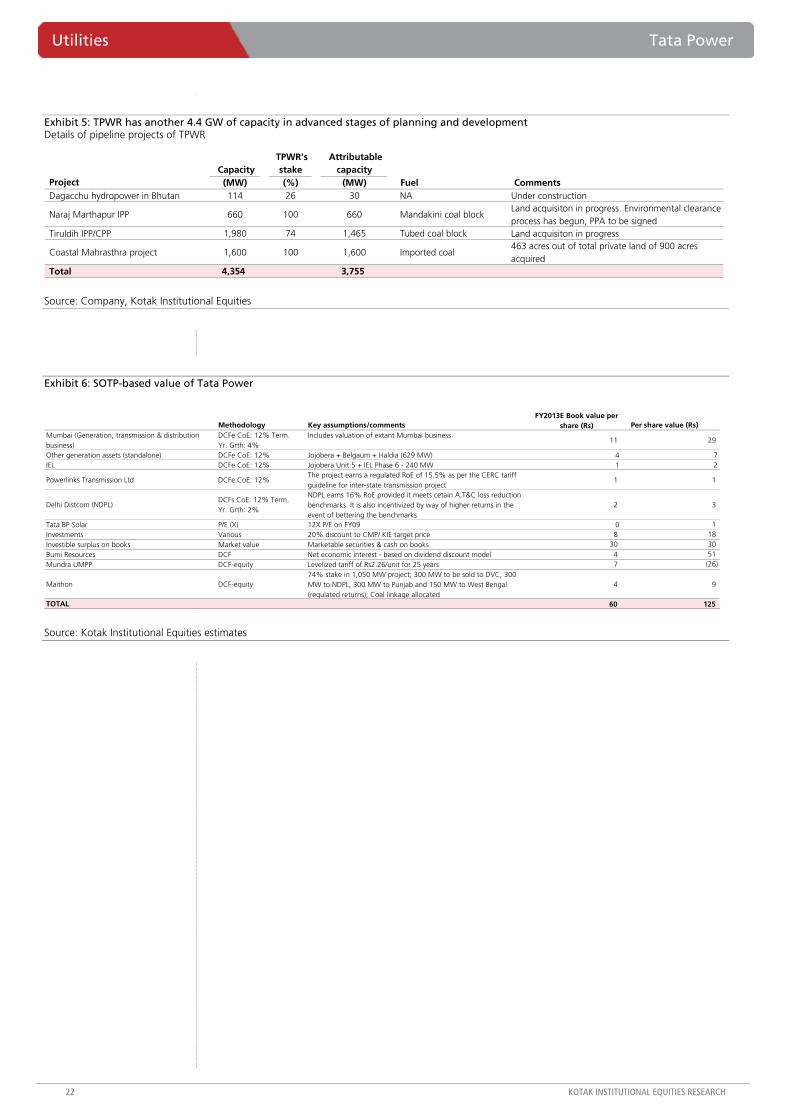

According to media reports, Bumi Resources’ guidance is for production of 80-85 mn tons in CY2012 from 63 mn tons in CY2011—to be subsequently ramped up to 100 mn tons from KPC and Arutmin (mines in which TPWR has effective stake of 30%) by CY2013E. As we highlighted in our note dated August 24, 2011, “Revisiting the coal equation”, higher production at coal mines is crucial for TPWR to absorb losses at Mundra and maximize benefits of higher coal prices. We note that our estimates factor 70 mn tons in FY2013 and sustainable volumes of 80 mn tons. Higher-than-estimated production volumes at Bumi could be the key upside to earnings and a strong catalyst for the stock.

Mundra losses contained through low costs, better tariffs could be a strong trigger

Our interactions with industry sources and power and coal companies highlighted increased deliberations on a way to compensate power producers with fixed-price tariffs for the increased cost of imported coal. While we are skeptical about such an arrangement coming through, the same could be significantly beneficial for TPWR. We are however more optimistic about prospects of blending low-grade Indonesian coal available at 10-30% lower energy-adjusted value to help to contain generation costs. The management indicated that it was successfully blending low-grade coal during the first few days of operations at Mundra.

Tata Power (TPWR)

Utilities

Coal production ramps up, low cost coal gives Mundra hope. An aggressive production ramp-up at the Indonesian mines could tilt the equation between losses at Mundra and profitability of coal mines in favor of the latter. Contained losses at Mundra through low cost coal or compensation through tariffs could significantly alter the earnings profile. We maintain our BUY rating and target price of Rs125 as ownership of resources and stable utility business better insulate TPWR from macro-risks affecting the power sector.

Tata PowerStock data Forecasts/Valuations 2011 2012E 2013E

52-week range (Rs) (high,low) EPS (Rs) 7.6 4.9 8.7Market Cap. (Rs bn) 273.5 EPS growth (%) 21.5 (36.3) 77.6

Shareholding pattern (%) P/E (X) 14.5 22.7 12.8Promoters 31.8 Sales (Rs bn) 194.5 260.0 288.9FIIs 23.3 Net profits (Rs bn) 18.9 12.0 21.4MFs 4.3 EBITDA (Rs bn) 47.0 55.9 66.5

Price performance (%) 1M 3M 12M EV/EBITDA (X) 10.8 9.3 8.0Absolute 17.9 8.3 (8.8) ROE (%) 13.8 8.4 14.4Rel. to BSE-30 7.4 5.9 (10.3) Div. Yield (%) 1.3 1.4 1.5

Company data and valuation summary

136-80

BUY

FEBRUARY 13, 2012

RESULT

Coverage view: Cautious

Price (Rs): 111

Target price (Rs): 125

BSE-30: 17,749

Tata Power Utilities

KOTAK INSTITUTIONAL EQUITIES RESEARCH 19

Maintain BUY rating with a target price of Rs125

We like TPWR’s core distribution business, which earns a stable return and is insulated from risks of deteriorating financial health of SEBs. Further, potential blending of low-grade coal could reduce losses at Mundra and could be a key upside to our estimates. We have revised our FY2012 EPS estimate downwards by 32% to account for a write-off in the coal business in 3QFY12.

Exhibit 1: Reported net income boosted by forex gains Interim results for Tata Power (standalone) , March fiscal year-ends (Rs mn)

(% Chg.)3QFY12 3QFY12E 3QFY11 2QFY12 3QFY12E 3QFY11 2QFY12 FY2011 FY2012E (% Chg.)

Net sales 21,611 20,313 15,959 18,644 6 35 16 80,880 17,706 (78) Cost of electrical energy purchased (1,258) (975) (1,743) (1,798) (7,607) (1,669) Cost of fuel (13,299) (12,553) (8,556) (10,220) (46,472) (8,828) Personnel costs, other expenses and provisions (3,210) (3,286) (2,901) (3,272) 11 (2) (13,062) (3,390) Total expenses (17,767) (16,815) (13,200) (15,290) (67,141) (13,887) EBITDA 3,843 3,499 2,759 3,354 10 39 15 13,740 3,819 (72) Depreciation (1,512) (1,354) (1,286) (1,353) (5,730) (1,286) EBIT 2,332 2,145 1,473 2,001 8,010 2,533 Other income 2,275 2,680 1,355 4,159 68 (45) 12,267 1,086 Net interest (1,280) (1,196) (1,095) (1,165) (4,843) (1,105) PBT 3,327 3,629 1,732 4,996 (8) 92 (33) 15,434 2,513 (84) Tax (826) (1,089) (260) (1,865) (5,711) (619) Net profit 2,501 2,541 1,473 3,130 (2) 70 (20) 9,723 1,895 (81) Statutory appropriations (353) — 10 (315) (787) - Extraordinary 2,081 — 58 - - - Reported PAT after statutory appropriation 4,229 2,541 1,541 2,815 EBITDA margin (%) 18 17 17 18 17 22

Key operating parametersUnits generated (MU) 3,970 3,713 3,772 7 5 Units sold (MU) 3,922 3,824 3,793 3 3

Per unit price realization (Rs) 5.5 4.2 5.0 31 11 Fuel cost per unit sold (Rs) 3.6 2.4 3.2 53 15

Source: Company, Kotak Institutional Equities estimates

Standalone: reported net income boosted by forex gain

TPWR reported standalone revenue of Rs21.6 bn (35% yoy, 16% qoq), operating profit of Rs3.8 bn (39% yoy, 15% qoq) and adjusted net profit of Rs2.5 bn (70% yoy, -20% qoq) in 3QFY12 compared with our estimates of Rs20.3 bn, Rs3.5 bn and Rs2.5 bn respectively. Net income miss of 27% was mainly due to (1) higher-than-estimated depreciation due to capitalization of wind capacities, (2) lower other income and (3) higher taxes on account of deferred taxes arising out of commissioning of wind capacities.

We highlight some key details of the 3QFY12 standalone results:

TPWR’s gross generation was 3,970 MU (7% yoy, 5% qoq) and total unit sales were 3,922 MU (3% yoy, 3% qoq). Generation in Mumbai license area increased 16% yoy driven by (1) higher hydro generation and (2) conversion of Unit 8 to regulated capacity from merchant capacity earlier. Total sales in Mumbai area increased by 10% yoy to 2,901 MU.

During the quarter, fuel cost increased 15% sequentially to Rs3.6/kwh likely due to currency depreciation.

TPWR sold 218 MU in the short-term market at an average realization of Rs3.4/kwh. We note that all the merchant sales came from Haldia since Unit 8 at Trombay was converted to regulated capacity (as highlighted above).

The effective tax rate increased to 44% in 3QFY12 primarily on account of deferred tax arising out of commissioning of wind capacities.

Utilities Tata Power

20 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Reported net income of Rs4.2 bn includes forex gain of Rs2.7 bn, mainly due to a retrospective (effective April 2011) change in accounting policy to capitalize forex gain/loss arising out of revaluation of long-term foreign currency monetary items. We note that as per the previous policy (such forex gain/losses being carried through P&L), forex loss for the quarter would have been Rs1.7 bn.

Consolidated: profitability hit by write-off of deferred stripping costs

TPWR reported consolidated revenues of Rs66.5 bn (51% yoy, 6% qoq), operating profit of Rs9.9 bn (-4% yoy, -27% qoq) and adjusted net profit of Rs2 bn (-50% yoy, -45% qoq) in 3QFY12. Despite robust volume and realization in the coal business (aided further by currency depreciation), consolidated profitability was dented by (1) a Rs6.5 bn write-off of deferred stripping costs in one of the coal companies (KPC), (2) unscheduled outage of the generation plant for Delhi distribution and (3) losses at Maithon.

We note that during the quarter, KPC, in light of uncertainty involved in estimated strip ratio, wrote off the entire stripping cost accumulated over years. We note that adjustment from stripping costs would henceforth be done only in Arutmin.

Reported net income of Rs2.6 bn includes a forex gain of Rs3.9 bn, mainly due to a retrospective (effective April 2011) change in accounting policy to capitalize forex gain/loss arising out of revaluation of long-term foreign currency monetary items. We note that as per the previous policy (such forex gain/losses being carried through P&L), forex loss for the quarter would have been Rs1.7 bn. Further, reported net income also includes Rs1.6 bn of provision for impairment of assets of the Mundra project.

We discuss below performance of businesses in detail

Coal: robust volume and realizations, margins dented

TPWR’s coal business reported volumes of 17.5 mn tons (9.5% yoy, 9.5% qoq) and realization of US$95/ton (30% yoy, flat qoq) and cash cost declined sequentially from US$46/ton to US$40.9/ton. The management attributed the reduction in cash costs to automation capex being carried out in coal mines and expects the full impact to flow in from September 2011.

We note that during the quarter, KPC, in light of uncertainty involved in estimates of strip ratio, wrote down the entire stripping cost (Rs6.5 bn) accumulated over years. We note that adjustment from stripping cost would henceforth be done only for Arutmin.

Delhi distribution

TPWR’s Delhi distribution reported revenues of Rs10.6 bn (35% yoy, -39% qoq), operating profit of Rs1.3 bn (41% yoy, -26% qoq) and PAT of Rs304 mn (-13% yoy, -65% qoq). The decline in PAT was primarily on account of unscheduled outage of generation assets. The management indicated that at current costs, once the tariff hike is carried out (as per automatic adjustment to be carried out with a lag of a quarter), NDPL would operationally break even.

Maithon: still stabilizing operational efficiencies

Maithon reported revenues of Rs1 bn, operating loss of Rs1 mn and losses before taxes of Rs858 mn. Loss at Maithon was mainly due to (1) higher fuel and O&M cost on account of stabilization of unit 1, (2) lower PLFs due to unavailability of coal during 3QFY12. The management has highlighted that Unit 1 has completely stabilized and coal supply has ramped up and is stable. The management’s guidance for synchronization of the second unit is 4QFY12.

Tata Power Utilities

KOTAK INSTITUTIONAL EQUITIES RESEARCH 21

Exhibit 2: Impairment provisioning and forex losses mar consolidated result Interim results for Tata Power (consolidated) , March fiscal year-ends, (Rs mn)

3QFY12 3QFY11 2QFY12 (qoq) (yoy) FY2011 FY2012E (% Chg.)Net sales 66,459 44,129 62,483 6 51 194,508 259,983 34

Employee cost (3,104) (2,304) (3,026) (8,259) (11,638) Royalty towards coal mine (3,168) - (2,673) (7,658) (11,819) Cost of power purchased (12,850) (8,499) (16,769) (49,143) (57,916) Cost of coal purchased (297) (209) (2) (484) (581) Cost of fuel (17,574) (10,563) (14,154) (43,231) (62,032) Coal processing charges (4,705) (4,395) (5,408) (16,675) (20,001) Cost of raw material and components 220 (1,226) (317) - - Other expenditure (15,091) (6,669) (6,628) (23,101) (41,266) EBITDA 9,889 10,266 13,508 (27) (4) 45,956 54,730 19 Depreciation (3,469) (2,490) (3,066) (9,802) (12,586) EBIT 6,421 7,776 10,442 36,153 42,144 Other income 819 742 1,414 2,386 3,727 Net interest (4,213) (2,109) (3,313) (8,684) (14,769) PBT 3,028 6,409 8,543 (65) (53) 29,856 31,102 4 Tax (1,026) (2,089) (4,535) (9,756) (17,728) Minority interest and share of associates 38 (227) (283) (1,223) (1,341) Net profit 2,039 4,093 3,725 (45) (50) 18,877 12,033 (36) Extraordinary 940 321 (15,599) 1,719 (13,760) Statutory appropriations (353) 10 (315) 285 - Reported profit after statutory appropriation 2,627 4,424 (12,189) 20,881 (1,727) EBITDA margin (%) 15 23 22 24 21 Effective tax rate (%) 34 33 53 33 57

Segment revenuesPower 39,099 26,113 39,344 (1) 50 128,885 157,553 22 Coal 27,007 16,723 21,673 25 61 64,005 98,490 54 Others 1,701 2,125 2,138 (20) (20) 1,618 3,939 143 Total 67,807 44,961 63,155 7 51 194,508 259,983 34 Less: Inter segment revenues (1,208) (552) (333) - - Net revenues 66,599 44,409 62,823 194,508 259,983 EBITPower 4,819 4,018 4,622 4 20 21,646 21,557 (0) Coal 1,353 4,326 5,962 (77) (69) 16,731 24,314 45 Others/ Unallocated 58 26 (152) (138) 121 162 - (100) Total 6,229 8,370 10,432 (40) (26) 38,540 45,871 19 EBIT margin (%)Power 12.3 15.4 11.7 16.8 13.7 Coal 5.0 25.9 27.5 26.1 24.7 Others 3.4 1.2 (7.1) 10.0 - Total 9.2 18.6 16.5 19.8 17.6

(% Chg.)

Source: Company, Kotak Institutional Equities estimates

Exhibit 3: Coal prices have shown signs of moderation recently Coal prices at Richard Bay (US$/ton)

50

70

90

110

130

150

170

Feb-

09

May

-09

Aug

-09

Nov

-09

Feb-

10

May

-10

Aug

-10

Nov

-10

Feb-

11

May

-11

Aug

-11

Nov

-11

Feb-

12

Source: Bloomberg, Company, Kotak Institutional Equities

Exhibit 4: Bumi’s realizations have followed the trend in international coal prices Comparison of Bumi’s average realization and average Richard Bay index, 1QFY09– 3QFY12 (US$/ton)

0

40

80

120

160

200

1QFY

09

2QFY

09

3QFY

09

4QFY

09

1QFY

10

2QFY

10

3QFY

10

4QFY

10

1QFY

11

2QFY

11

3QFY

11

4QFY

11

1QFY

12

2QFY

12

3QFY

12

-100

0

100

200

300

400

500

600

Richard Bay (US$/ton) [LHS]

Bumi realization (US$/ton) [LHS]

EBIT/ton (Rs/ton) [RHS] (Rs/ton)(US$/ton)

Source: Bloomberg, Company, Kotak Institutional Equities

Utilities Tata Power

22 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 5: TPWR has another 4.4 GW of capacity in advanced stages of planning and development Details of pipeline projects of TPWR

Capacity TPWR's

stake Attributable

capacity Project (MW) (%) (MW) Fuel Comments Dagacchu hydropower in Bhutan 114 26 30 NA Under construction

Naraj Marthapur IPP 660 100 660 Mandakini coal blockLand acquisiton in progress. Environmental clearance process has begun, PPA to be signed

Tiruldih IPP/CPP 1,980 74 1,465 Tubed coal block Land acquisiton in progress

Coastal Mahrasthra project 1,600 100 1,600 Imported coal463 acres out of total private land of 900 acres acquired

Total 4,354 3,755

Source: Company, Kotak Institutional Equities

Exhibit 6: SOTP-based value of Tata Power

Methodology Key assumptions/commentsFY2013E Book value per

share (Rs) Per share value (Rs)Mumbai (Generation, transmission & distribution business)

DCFe CoE: 12% Term. Yr. Grth: 4%

Includes valuation of extant Mumbai business11 29

Other generation assets (standalone) DCFe CoE: 12% Jojobera + Belgaum + Haldia (629 MW) 4 7 IEL DCFe CoE: 12% Jojobera Unit 5 + IEL Phase 6 - 240 MW 1 2

Powerlinks Transmission Ltd DCFe CoE: 12%The project earns a regulated RoE of 15.5% as per the CERC tariff guideline for inter-state transmission project

1 1

Delhi Distcom (NDPL)DCFs CoE: 12% Term. Yr. Grth: 2%

NDPL earns 16% RoE provided it meets cetain A,T&C loss reduction benchmarks. It is also incentivized by way of higher returns in the event of bettering the benchmarks

2 3

Tata BP Solar P/E (X) 12X P/E on FY09 0 1 Investments Various 20% discount to CMP/ KIE target price 8 18 Investible surplus on books Market value Marketable securities & cash on books 30 30 Bumi Resources DCF Net economic interest - based on dividend discount model 4 51 Mundra UMPP DCF-equity Levelized tariff of Rs2.26/unit for 25 years 7 (26)

Maithon DCF-equity74% stake in 1,050 MW project; 300 MW to be sold to DVC, 300 MW to NDPL, 300 MW to Punjab and 150 MW to West Bengal (regulated returns); Coal linkage allocated

4 9

TOTAL 60 125

Source: Kotak Institutional Equities estimates

Tata Power Utilities

KOTAK INSTITUTIONAL EQUITIES RESEARCH 23

Exhibit 7: Tata Power: Profit model, balance sheet, cash model (consolidated) 2009-2014E, March fiscal year-ends (Rs mn)

2009 2010 2011 2012E 2013E 2014EProfit model (Rs mn)Net sales 175,875 189,858 194,508 259,983 288,942 317,658EBITDA 36,496 38,379 45,956 54,730 65,287 68,113Other income 2,266 1,841 2,671 3,727 5,618 5,671Interest (8,129) (7,818) (8,684) (14,769) (18,909) (23,513)Depreciation (6,565) (8,777) (9,802) (12,586) (17,858) (21,066)Pretax profits 24,069 23,625 30,141 31,102 34,138 29,205Tax (11,651) (6,287) (9,756) (17,728) (11,948) (10,160)Minority interest (800) (1,718) (1,223) (1,341) (824) (863)Net profits 11,618 15,620 19,162 12,033 21,365 18,181Extraordinary items 1,023 3,984 1,719 (12,441) — —Earnings per share (Rs) 5 6 8 5 9 7

Balance sheet (Rs mn)Total equity 92,576 120,403 137,442 132,703 149,159 162,431Deferred taxation liability 5,154 4,308 4,753 4,066 3,380 3,380Total borrowings 141,434 184,469 247,624 305,735 318,468 319,673Currrent liabilities 67,812 74,080 95,087 106,968 111,143 122,525Capital contribution from Consumers 2,030 3,664 3,823 3,823 3,823 3,823Minority interest 9,444 12,098 14,143 15,483 16,308 17,171Total liabilities and equity 318,450 399,021 502,871 568,779 602,281 629,003Cash 11,780 23,108 22,066 73,257 70,649 81,078Current assets 62,686 73,794 88,862 82,450 97,651 108,545Total fixed assets 201,076 267,402 356,124 374,867 395,775 401,174Investments 32,512 30,823 28,410 30,797 30,797 30,797Deferred expenditure 10,397 3,896 7,409 7,409 7,409 7,409Total assets 318,450 399,021 502,871 568,779 602,281 629,003

Free cash flow (Rs mn)Operating cash flow, excl. working capital 22,396 29,242 31,888 12,887 39,146 40,079Working capital 10,724 (10,899) (769) 18,035 (11,285) 519Capital expenditure (65,047) (78,368) (97,932) (31,329) (38,767) (26,465)Investments (4,684) 3,486 (1,100) (2,387) — —Free cash flow (36,612) (56,540) (67,913) (2,793) (10,906) 14,134

Source: Company, Kotak Institutional Equities estimates

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Core expansion promising

IDFC reported PAT of Rs3.8 bn, up 19% yoy but 6% below estimates. Growth in net operating income was strong at 15% yoy and 7% above estimates on the back of 25% loan growth and higher capital gains. While provisions were higher than expected, PBT was up 19% yoy and 1% below estimates.

Loans grow well

IDFC reported a loan book of Rs439 bn, up 25% yoy and 12% qoq. Gross disbursements increased by 16% yoy and 60% qoq to Rs58 bn. Repayment rate (repayments/opening loan book) declined to 3% for the quarter from 5% in 2QFY12 and 13% in 3QFY11. Notably, repayment rate in 3QFY12 was the lowest in the past four years. We believe that the competitive scenario has been favorable as most public banks (primarily SBI) currently charge higher interest rates on infrastructure loans as compared to IDFC.

Loans to telecom sector have increased by 31% yoy and 22% qoq. Telecom was the biggest growth driver accounting for 43% of qoq loan book accretion. This was followed by transportation at 30%. The management has highlighted that most of their telecom exposure is towards top three telecom companies.

Approvals were up 108% yoy and down 5% qoq. Most of the approvals are likely for refinancing, and general business activity in the sector was low during the quarter.

NIM improves marginally

IDFC reported NIM (as per KS estimates) of 4.5% as compared to 4.3% in 2QFY12 and 3QFY11.

The share of bonds increased to 65% of total borrowings from 53% in 2QFY12, short-tem loans increased to 12% from 10% qoq while bank loan declined to 10% from 25% for the same period.

IDFC (IDFC)

Banks/Financial Institutions

Growth strong, core in line. IDFC’s 3QFY12 performance was broadly as per our expectations. Highlights to focus on are—(1) loan growth accelerated to 25% from 15% in 2QFY12 and (2) NPLs inched up marginally. NIMs were somewhat ahead of expectations but fees were lower. Higher-than-expected provisions and tax rate pulled down reported earnings. We will revisit our estimates and target price after the conference call with the management.

IDFCStock data Forecasts/Valuations 2012 2013E 2014E

52-week range (Rs) (high,low) EPS (Rs) 10.3 12.1 14.7Market Cap. (Rs bn) 202.0 EPS growth (%) 17.1 18.2 20.9

Shareholding pattern (%) P/E (X) 13.0 11.0 9.1Promoters 0.0 NII (Rs bn) 21.0 24.9 30.3FIIs 47.2 Net profits (Rs bn) 15.5 18.3 22.2MFs 4.1 BVPS 82.4 91.7 103.0

Price performance (%) 1M 3M 12M P/B (X) 1.6 1.5 1.3Absolute 31.3 9.4 6.4 ROE (%) 13.6 13.9 15.1Rel. to BSE-30 19.6 7.0 4.6 Div. Yield (%) 1.5 1.8 2.2

Company data and valuation summary

167-90

ADD

FEBRUARY 10, 2012

RESULT

Coverage view: Attractive

Price (Rs): 134

Target price (Rs): 150

BSE-30: 17,749

QUICK NUMBERS

• PAT up 19%

• Loan growth up 25%

• Gross NPLs at 0.33%

IDFC Banks/Financial Institutions

KOTAK INSTITUTIONAL EQUITIES RESEARCH 25

Fees below expectations, capital gains high

Despite the traction in loan growth, IDFC booked lower loan-related fees—Rs300 mn, down from Rs480 mn in 2QFY12. While income from asset management was almost stable, IDFC Capital’s income was weak largely due to sharp decline in broking income even as investment banking income increased qoq.

During the quarter, IDFC sold 25% stake in IDFC AMC. Consequently, the company booked capital gains of Rs910 mn.

NPLs and provisions increase

IDFC’s gross NPLs inched up by Rs700 mn to 0.33% from 0.22%. The management highlighted that the slippage does not pertain to core infrastructure sectors like energy, transportation or telecom.

IDFC reported provisions of Rs978 mn, up from Rs631 in 2QFY12. This comprised excess provisions of Rs400 mn, specific provisions of Rs100 mn and provisions on equity/other fees etc. of Rs470 mn.

IDFC - Quarterly results March fiscal year-ends, 3QFY11-3QFY12 (Rs mn)

3Q11 4Q11 1Q12 2Q12 3Q12 YoY (%) 3Q12E Actual vs

KS (%) Consolidated financialsTotal Income 13,100 13,066 13,580 17,149 16,392 Interest and other charges 6,500 6,835 7,539 8,259 8,802

Net operating income 6,600 6,231 6,040 8,997 7,597 15 7,075 7 Net operating inc excl cap gains 6,020 5,941 6,060 6,407 6,687 11 6,350 5 Net interest income on infra 4,130 4,250 4,280 4,390 4,730 15 4,500 5

Treasury (incl secu and others) 470 490 550 590 730 55 600 22 Fees and advisory 1,370 1,170 1,120 1,310 1,220 (11) 1,125 8

Asset management 630 880 620 650 680 8 625 9 IDFC SSKI / Investment banking 80 280 80 60 160 100 50 220

Institutional brokerage 140 100 110 120 80 (43) 100 (20) Advisory and other fees 520 (90) 310 480 300 (42) 350 (14)

Profit on sale of equity 580 290 (20) 2,590 910 57 850 7 Total expenditure 2,018 2,016 1,436 1,948 2,147 6 1,550 39

Staff expenses 874 841 649 771 726 (17) 750 (3) Other expenses 657 230 387 546 443 (33) 500 (11) Provisions and contingencies 487 945 399 631 978 101 300 226

PBDT 4,582 4,215 4,605 7,049 5,449 19 5,525 (1) Depreciation 103 99 95 97 96 (6) 100 (4) Profit before Tax 4,480 4,117 4,510 6,953 5,353 19 5,425 (1) Provision for Tax 1,272 1,252 1,378 1,712 1,537 21 1,356 13 Profit after tax 3,207 2,865 3,132 5,241 3,816 19 4,069 (6) Share of profit in associates / minority interest (8) — (6) (1) (1) (87) (1) —PAT (incl minorities share/ after minority share) 3,215 2,865 3,138 5,242 3,817 19 4,070 (6) PBT bef treasury and provisions and extra ordinary items 4,110 4,495 4,653 4,717 5,144 25 4,598 12 Tax rate 28 30 31 25 29 — 25 —

Balance sheet (Rs mn)Shareholders funds 113,900 112,480 115,510 120,730 124,300 Loan funds 366,330 363,040 386,690 395,760 437,290 Total 480,300 475,540 502,200 516,490 561,590 Fixed assets 4,500 4,470 — — —Investments 350,210 375,520 375,270 393,130 438,970 25 412,893 6

Equity 22,160 21,190 19,430 30,900 31,120 Treasury 88,220 61,840 86,650 71,110 66,540

Infrastructure loans 350,210 375,520 375,270 393,130 438,970 Deferred Tax 2,240 2,500 — — —Net current assets 1,380 (16,100) 9,220 21,360 24,960 Total 480,310 461,060 502,210 516,500 561,590

Source: Company, Kotak Institutional Equities estimates

Banks/Financial Institutions IDFC

26 KOTAK INSTITUTIONAL EQUITIES RESEARCH

IDFC - Quarterly results March fiscal year-ends, 3QFY11-3QFY12

3Q11 4Q11 1Q12 2Q12 3Q12 YoY (%) 3Q12E Actual vs

KS (%) Other details Gross approvals (Rs bn) 37 62 58 81 77 108 Gross disbursements (Rs bn) 50 43 30 36 58 16 Loan book (Rs bn) 350 376 375 393 439 25 Repayment (% of opening loan book) 13 5 8 5 3 Outstanding disbursements (Rs bn)Loans 353 378 377 396 442 25 Project loans 206 223 223 237 269 31

Corporate loans 140 149 144 143 154 10 Loans against shares 7 7 9 15 18 154 Mezzanine products 4 3 3 3 3 (25) Equity/ pref shares 23 20 21 20 21 (10)Non-funded 17 16 24 24 23 38

Total 396 417 425 443 488 23

Sectorwise break upsTotal exposure (Rs bn) 576 582 616 627 660 15

Energy 270 267 267 269 275 2 Transportation 159 167 162 151 166 5 Telecom 86 92 129 135 147 72 Others 62 56 57 71 71 15

O/s disbursements 396 416 423 442 488 90 Energy 167 174 187 195 204 22 Telecom 85 90 89 91 111 31 Transportation 93 105 100 102 115 24 Others 51 47 47 54 58 13

Breakup of outstanding borrowings (% of total)Short term 14 5 10 10 12LT Rupee loans 18 18 18 25 10LT bonds 63 67 63 53 65Foreign currency loans 4 8 8 10 11Sub debt 2 2 2 2 1

ROA analysis (%)Net interest income 3.8 3.8 3.9 4.0 4.0 Infrastructure 3.5 3.5 3.5 3.5 3.5

Treasury 0.3 0.3 0.4 0.4 0.5 Non Interest income 2.5 2.0 1.6 1.8 1.7

Fees, syndication and advisory 1.4 1.2 1.0 1.0 1.0 Capital gains & dividend 0.5 0.4 0.1 0.7 0.7

Mis. Fees 0.6 0.5 0.1 0.1 - Operating income 6.4 5.9 5.5 5.8 5.7

Operating expenses 1.6 1.2 1.1 1.1 1.1 Pre- provisioning profits 4.8 4.7 4.4 4.7 4.7 Provisions and losses 0.5 0.5 0.5 0.5 0.6 PBT 4.3 3.1 3.9 4.2 4.1 Tax 1.1 1.2 1.1 1.2 1.2 Associate co profit — — — — —Net Income (PAT) 3.1 3.0 2.8 3.0 3.0

NIMs (KS calc- %) 4.3 4.3 4.3 4.3 4.5

Source: Company

IDFC Banks/Financial Institutions

KOTAK INSTITUTIONAL EQUITIES RESEARCH 27

IDFC—1-year fwd rolling PER and PBR (X) August 2005-Feb 2012

-

9

18

27

36

45

Aug

-05

Feb-

06

Aug

-06

Feb-

07

Aug

-07

Feb-

08

Aug

-08

Feb-

09

Aug

-09

Feb-

10

Aug

-10

Feb-

11

Aug

-11

Feb-

12

0

2

4

6Rolling PER (X) (LHS) Rolling PBR (X) (RHS)

Source: Bloomberg, Kotak Institutional Equities estimates

IDFC: Sum-of-the-parts based valuation

ValuationValue per

share Comments (Rs mn) (Rs)

IDFC (core) 171,419 114Based on residual growth model- implies 1.8X core PBR for medium term RoE of 16-17%

IDFC (Private equity) 6,862 5 10% of FY2013E AUM - US$1.8 bnIDFC (Project equity) 7,500 5 10% of FY2013E AUM - US$1.4 bnIDFC MF 10,143 7 3.5% of FY2013E AUMsIDFC Capital 5,345 4 10X FY2013E PATIDFC's investment in NSE 10,200 7 12X FY2013E PERValue of market investments 14,437 10 At book valueTotal 212,181 150

Source: Kotak Institutional Equities estimates

Banks/Financial Institutions IDFC

28 KOTAK INSTITUTIONAL EQUITIES RESEARCH

IDFC (consolidated), key ratios March fiscal year-ends, 2007-13E (%)

2007 2008 2009 2010 2011E 2012E 2013EIncome Statement growth rate (%)Operating income 64 70 38 4 31 29 21 Net fund based income 51 63 35 26 45 24 18 Fee income 160 64 8 16 31 (16) 23

On AUM 84 5 287 (8) 25 (5) 23 Other operating income 7 29 (15) 81 (30) 15 12 Operating expenses 43 228 55 9 46 0 26 Net profit 60 21 1 44 17 21 18 Core operating profit (PBT-treasury+provisions)

84 42 16 26 36 20 18

Balance Sheet growth rate (%)AssetsInvestments 52 174 40 (24) 40 (1) 8 Infrastructure loans 37 43 3 22 50 17 21 Total assets 44 61 7 13 42 15 18 LiabilitiesLoan funds 57 57 7 13 41 14 21 Total liabilities 52 55 6 12 41 14 20 Shareholders equity 14 90 10 14 48 19 11 Key ratios (%)Yield on

Earning assets exld treasury assets 9.1 10.2 11.3 10.7 10.7 10.8 11.1 Earning assets incl treasury income and assets

9.7 10.5 11.1 10.9 10.6 10.8 11.1

Infrastructure loans 9.3 10.2 11.8 11.3 11.0 11.3 11.6 Interest on bank deposits 8.4 16.0 10.0 15.4 19.9 14.7 16.5 Average cost of funds 7.2 8.1 9.1 7.8 7.5 8.0 8.4 Capital gains to eqty investments 21.3 20.6 10.1 14.1 9.1 10.3 11.5 NIM (excl capital gains) 2.8 3.0 3.2 3.6 4.1 4.0 4.1 Employee .exp to income 0.5 1.1 1.3 1.3 1.4 11.7 12.9 Operating expnses/ income 9.0 18.9 24.8 20.7 23.3 20.6 21.9 Du Pont (%age of average assets)Net interest income 2.8 3.0 3.1 3.6 4.0 4.0 4.0 Loan loss provisions 0.1 0.3 0.5 0.4 0.6 0.5 0.4 Other operating income 2.7 2.7 2.1 2.6 2.2 1.6 1.6 Operating expenses 0.5 1.1 1.3 1.3 1.4 1.1 1.2 ROA 4.1 3.2 2.6 3.4 3.1 2.9 3.0 Average assets/average equity 5.5 5.5 5.0 4.9 4.8 4.6 4.7 ROE 22.6 17.6 12.9 16.6 14.7 13.6 13.9

Source: Company, Kotak Institutional Equities estimates

IDFC Banks/Financial Institutions

KOTAK INSTITUTIONAL EQUITIES RESEARCH 29

IDFC (consolidated): Income statement and balance sheet March fiscal year-ends, 2007-13E (Rs mn)

2007 2008 2009 2010 2011E 2012E 2013E

Total income 16,917 27,928 36,338 39,446 50,015 61,301 74,037 Operating income 12,778 21,700 30,032 31,132 40,762 52,770 63,927 Dividend 91 62 542 1,321 819 818 817

Other charges 136 101 - 15 15 15 15 Net fund based income 4,223 6,866 9,237 11,630 16,897 21,025 24,878 Less: provisions for NPLs 174 688 1,495 1,304 2,349 2,453 2,439 Net fund based income post provisions 4,049 6,178 7,742 10,326 14,548 18,572 22,440

Fee income 2,406 3,944 4,253 4,951 6,498 5,433 6,692 SSKI 1,873 1,070 1,793 1,818 1,253 1,616 On guarantees/commissions- standalone 656 1,515 1,032 1,184 2,212 1,840 2,195 Fees on AMC 528 556 2,150 1,975 2,468 2,340 2,881

Net operating income 8,137 12,288 13,835 18,608 23,386 26,689 32,135 Operating expenses 745 2,447 3,795 4,121 5,997 6,000 7,557 Profit before tax 7,444 9,959 10,254 14,519 17,804 21,104 24,992 Tax 1,235 2,463 2,697 3,611 4,991 5,607 6,672 Net profit 6,209 7,496 7,557 10,908 12,813 15,497 18,320 % growth 60 21 1 44 17 21 18 Net profit post minority interest 6,209 7,353 7,495 10,908 12,813 15,497 18,320 PBT - treasury 5,710 7,675 8,200 11,157 15,049 18,005 21,575 % chg 112 34 7 36 35 20 20 PBT - treasury + provisions 5,884 8,363 9,695 12,190 16,598 19,958 23,514 No. of shares 1,126 1,294 1,295 1,301 1,461 1,509 1,509 Balance SheetAssets

Mutual Funds 3,477 7,148 100 1,378 23 14 14 Equity Shares 6,147 12,606 19,652 20,910 21,973 20,875 21,918 Venture Capital Units 954 1,273 2,983 3,784 4,541 4,531 5,061 Infrastructure loans 139,155 199,024 205,918 250,270 376,523 441,141 534,309 Current assets 18,287 28,674 17,950 30,358 26,556 35,274 39,003 Fixed assets 486 3,812 4,438 4,131 3,907 4,038 4,222 Other assets 854 953 1,393 1,743 2,449 2,571 2,700

Total assets 178,506 286,600 305,583 344,291 490,519 563,067 666,367 LiabilitiesSubordinated debt (unsecured) 6,500 6,500 6,500 6,500 6,500 6,500 6,500 Loan funds 137,136 214,784 228,791 257,401 363,640 415,088 503,492 Current liabilities and provisions 5,561 9,484 8,622 10,290 16,295 17,138 18,029 Total liabilities 149,197 230,767 243,913 274,191 386,435 438,726 528,020 Paid-up capital 11,259 12,943 12,953 13,006 14,609 15,087 15,087 Reserves and surplus 18,049 42,889 48,717 57,094 89,474 109,254 123,259 Shareholders equity 29,308 55,832 61,670 70,100 104,084 124,341 138,346

Source: Company, Kotak Institutional Equities estimates

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

3QFY12 consolidated results below expectations

RCOM reported a disappointing set of numbers for the Dec 2011 quarter. Consolidated revenues at Rs50.5 bn (flat qoq, +1% yoy) missed our estimate by 3.7% while EBITDA at Rs16.1 bn (flat qoq, down 3.4% yoy) missed expectations by 6.2%. Net income of Rs1.9 bn (down 26% qoq and 61% yoy) came in ahead of our estimated Rs1.3 bn on the back of (1) depreciation write-back at one of the subsidiaries, RTL, driven by change in accounting policy; this aided PBT to the tune of Rs3.1 bn, and (2) lower-than-expected net finance cost – this line item continues to remain difficult to forecast, in any case (see Exhibit 3). We note that RCOM would have reported a net loss but for the depreciation write-back. ETR remained low at 5.5%.

Operational performance weak across segments

Wireless – revenues of Rs44.5 bn (+0.7% qoq, +9.4% yoy) missed our estimate by 2.6%. EBITDA of Rs11.8 bn (flat qoq as well as yoy) came in 4% below expectations. EBITDA margin was flat qoq. Network traffic grew a modest 1% qoq (weak in the context of strong seasonality), while RPM was flat qoq at Rs0.446/min. We note that RCOM’s voice RPM continues to be substantially lower than the GSM incumbents as the company’s non-voice revenues (as % of revenues) are at least 6-7% points higher and overall RPM similar. ARPU and MOU both came down 1.4% qoq to Rs100 and 224 per sub per month, respectively.

Global Enterprise – revenues were flat qoq and down 7.5% yoy at Rs23.5 bn while EBITDA declined 8.6% yoy (flat qoq) to Rs5.7 bn. Margins were flat qoq as well as yoy at a little over 24%. The company saw sequential decline in both NLD as well as ILD volumes while it stopped disclosing its Fixed-Line/ Broadband ARPU.

‘Others segment’ – revenues fell sharply (19% qoq and 26% yoy) to Rs2.3 bn. DTH forms a major part of this segment and we presume the revenue weakness reflects loss of market share (loss of subs, possibly) in this segment.

Reliance Communications (RCOM)

Telecom

Weak results but do they matter? RCOM reported a weak set of numbers for the Dec 2011 quarter with revenues and EBITDA missing our estimates by a good margin. Depreciation write-back on account of change in accounting policy at one of the subsidiaries helped the company stay in the black at the net income level. We cut estimates, maintain TP at Rs60 and reiterate SELL. Nonetheless, the stock could continue to trade ahead of fundamentals in anticipation of positive news flow as it has in the recent past. To that extent, the fundamental challenges and expensive valuations may not matter much till the anticipated events are out or the market loses patience.

Reliance CommunicationsStock data Forecasts/Valuations 2012 2013E 2014E

52-week range (Rs) (high,low) EPS (Rs) 3.9 1.0 3.9Market Cap. (Rs bn) 194.0 EPS growth (%) (39.7) (73.5) 270.5

Shareholding pattern (%) P/E (X) 23.9 90.1 24.3Promoters 67.9 Sales (Rs bn) 202.1 221.5 239.0FIIs 8.5 Net profits (Rs bn) 8.1 2.2 8.0MFs 0.8 EBITDA (Rs bn) 65.2 73.2 81.3

Price performance (%) 1M 3M 12M EV/EBITDA (X) 8.1 6.9 5.9Absolute 16.0 12.3 (2.7) ROE (%) 2.0 0.6 2.0Rel. to BSE-30 5.6 9.9 (4.3) Div. Yield (%) 0.0 0.0 0.0

Company data and valuation summary

114-61

SELL

FEBRUARY 10, 2012

RESULT

Coverage view: Cautious

Price (Rs): 94

Target price (Rs): 60