ind as: issues and challenges in implementation€¦ · ind as: issues and challenges in...

TRANSCRIPT

© 2016 Grant Thornton India LLP. All rights reserved.

Ind AS: Issues and challenges in implementation

Mumbai12 February 2016

© 2016 Grant Thornton India LLP. All rights reserved.

Agenda

1. Business combinations – Ind AS 1032. Financial instruments – Ind AS 32 and 1093. Consolidation – Ind AS 110 and 1114. Income taxes – Ind AS 12 and ICDS5. First time adoption: exemptions and exceptions – Ind

AS 101

© 2016 Grant Thornton India LLP. All rights reserved.

Ind AS 103 – Business combinations

© 2016 Grant Thornton India LLP. All rights reserved.

Summary of transition from existingIndian GAAP to Ind AS

• Dispersed guidance – AS 10, 14 & 21

• Book-values based accounting in case of mergers and share acquisitions; fair value based accounting in case of amalgamation in nature of acquisitions and business acquisitions

• Goodwill can be amortised

• Intangible assets not recognised by acquiree, are not recognised in the consolidated financial statements also

• Single, principles-based model

• Fair value based accounting –purchase price allocation is a tedious and onerous exercise

• Goodwill can only be tested for impairment

• All identifiable assets and liabilities of acquiree are recognised, even if they were not recognised by acquiree

Existing IGAAP Ind-AS

© 2016 Grant Thornton India LLP. All rights reserved.

Business Combination

Business combinationA transaction or other event in which an acquirer obtains control of one or more businesses.

ControlAn investor controls an investee if and only if the investor has all the following:• power over the investee • exposure, or rights, to variable returns from its involvement with the investee; and• the ability to use its power over the investee to affect the amount of the investor's returns.

If the transaction/ assets acquired are not a busin ess, the reporting entity shall account for the transaction or other event as an asset acquisition

© 2016 Grant Thornton India LLP. All rights reserved.

Comprehensive example

• On 1 January 20X1, Entity A acquired 10% of the voting ordinary shares of Entity B (a pharmaceutical company) for INR 100,000.

• On 31 December 20X2, Entity A acquires 80% of Entity B for cash consideration of INR 2.4 million.

• Fair and book value information is as follows as of 31 December 20X2:– Fair value of the 10% interest of Entity B already owned by Entity A: INR 250,000– Fair value of Entity B's identifiable net assets: INR 4 million, including intangible assets not

recognised by Entity B, INR 0.5 million; book value in books of Entity B: INR 1 million– Fair value of non-controlling interests: INR 200,000

• An additional INR 250,000 to be paid after 2 years if a specified drug receives regulatory approval

• On 31 December 20X2, Entity B has a dispute with the income-tax authorities for a potential tax demand of INR 500,000. Entity B's legal advisors expect a 70% probability of winning the case.

© 2016 Grant Thornton India LLP. All rights reserved.

Accounting under existing Indian GAAP(AS 21)

A's consolidated financial statements INR INR

DR Identifiable net assets of Entity B 1,000,000

DR Goodwill 1,850,000

CR Cash 2,400,000

CR Investment in Entity B 100,000

CR Liability for consideration payable* 250,000

CR Minority interest 100,000

*Paragraph 15 of AS-14:"Many amalgamations recognise that adjustments may have to be made to the consideration in the light of one or more future events. When the additional payment is probable and can reasonably be estimated at the date of amalgamation, it is included in the calculation of the consideration. In all other cases, the adjustment is recognised as soon asthe amount is determinable."

© 2016 Grant Thornton India LLP. All rights reserved.

Determine the consideration transferred

consideration transferred is the sum of the acquisition-date fair values of: – the assets transferred by the acquirer– the liabilities incurred by the acquirer to former owners of the target company and – equity interests issued by the acquirer

in exchange for the acquiree

(includescontingent

consideration)

(excludesacquisition

costs)

© 2016 Grant Thornton India LLP. All rights reserved.

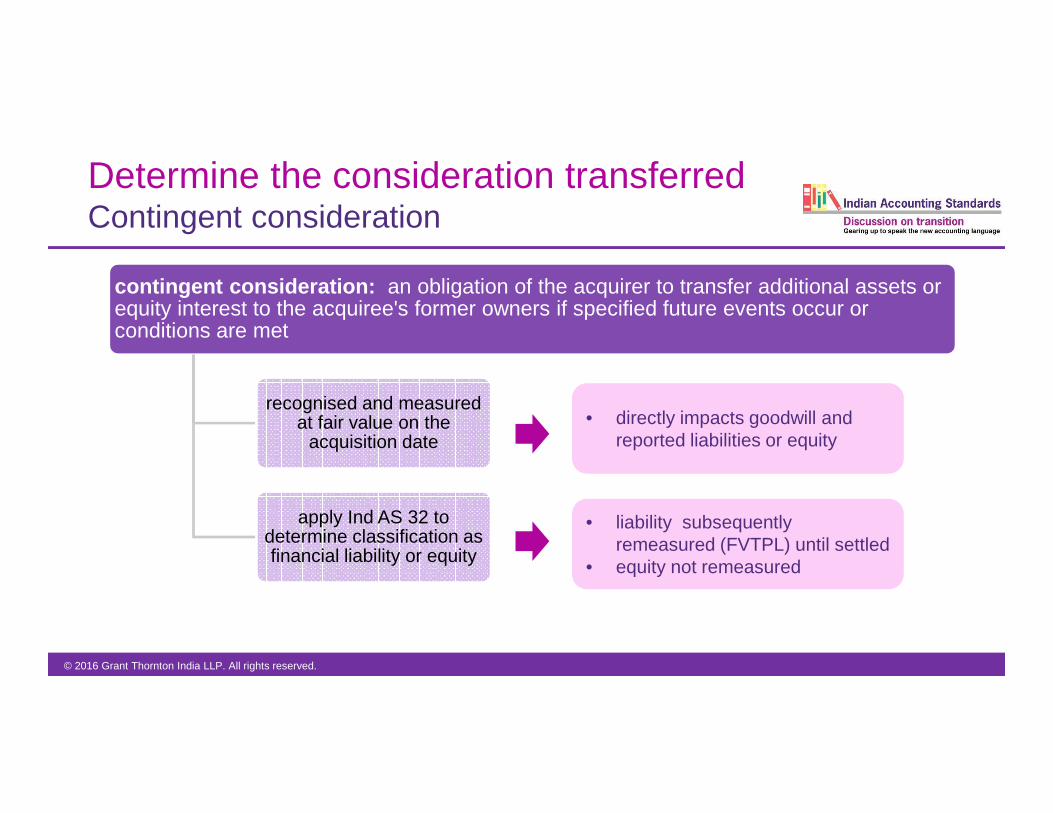

Determine the consideration transferredContingent consideration

contingent consideration: an obligation of the acquirer to transfer additional assets or equity interest to the acquiree's former owners if specified future events occur or conditions are met

recognised and measured at fair value on the

acquisition date

apply Ind AS 32 to determine classification as financial liability or equity

• directly impacts goodwill and reported liabilities or equity

• liability subsequently remeasured (FVTPL) until settled

• equity not remeasured

© 2016 Grant Thornton India LLP. All rights reserved.

contractual purchase price (based on the

SPA)

adjustments for transactions

not part of the business

combination

consideration transferred in exchange for the acquiree

Determine the consideration transferred

or

• remuneration for employees or former owners for future services• reimbursement of the acquiree or former owners for paying the acquirer's acquisition-related costs• settlement of pre-existing relationships• replacement of acquiree share-based payment awards • contracts to acquire shares from non-selling shareholders

© 2016 Grant Thornton India LLP. All rights reserved.

Recognising and measuring any non-controlling interest (NCI)

Category Description Example Measurement option?

present ownershipinstrument

acquiree's shares held by non-selling shareholders that entitle them to a proportionate share of the acquiree's net assets in the event of liquidation

common or ordinary shares

yes - fair value orproportionate share of recognised assets and liabilities

other componentsof NCI

other financial instruments issued by the acquiree that meet Ind AS 32's definition of equity

warrants or call options (on fixed-for-fixed terms)

no - fair value

non-controlling interest: the equity in a subsidiary not attributable, directly or indirectly, to a parent

© 2016 Grant Thornton India LLP. All rights reserved.

Measurement of identifiable assets acquired/liabilities assumed

Assets acquired and liabilities assumed are recognised at fair value if:

– meet the definition of an asset or liability at the acquisition date– are part of exchange in the business combination

Exception to recognition principles in a business c ombination:

Ind AS 37

• a contingent liability is…a present obligation that arises from past events but is not recognised because: (i) it is not probable …or (ii) the amount of the obligation cannot be measured with sufficient reliability

Ind AS 103

• recognised only if a present obligation exists and fair value can be measured reliably • recognised even if an outflow of economic benefits is not probable (uncertainty is

considered in the determination of fair value)

© 2016 Grant Thornton India LLP. All rights reserved.

Accounting for business combinations

consideration transferred

plus amount of Non Controlling Interest (NCI)

plus Fair Value of previously held equity interest

less net of assets acquired and liabilities assumed

equals goodwill (or gain on bargain purchase)

Double check accounting if bargain gain; recognise in OCI

© 2016 Grant Thornton India LLP. All rights reserved.

Accounting under Ind AS 103

A's consolidated financial statements INR INR

DR Identifiable net assets of Entity B (including intangible assets, net of fair value of contingent liability, INR 500,000 * 30%)

3,850,000

CR Cash 2,400,000

CR Investment in Entity B 100,000

CR Gain on fair valuation of previously held equity interest (P&L) 150,000

CR Liability for consideration payable 250,000

CR Non-controlling interest (either at fair value, INR 200,000 or proportionate fair value of net assets, INR 385,000)

385,000

CR Gain on bargain purchase (other comprehensive income or directly in reserves) – balancing figure

565,000

© 2016 Grant Thornton India LLP. All rights reserved.

Measurement period Initial accounting incomplete at the reporting date

Measurement period adjustments

• limited to those that arise from new information obtained about facts and circumstances that existed at the acquisition date

Accounting:• retrospectively adjust the

provisional amounts and/or recognise new assets/liabilities to reflect the new information

• adjust goodwill

Other adjustments during measurement period

• include adjustments for developments after the acquisition date but during the measurement period (eg changes in estimates)

Accounting:• prospectively adjust

provisional amounts to reflect new information arising after the acquisition date

• no adjustment to goodwill • correct errors retrospectively

in accordance with Ind AS 8

Post-measurement period adjustments

Accounting:

• no adjustment to the accounting for the business combination allowed except for the correction of an error in accordance with Ind AS 8

© 2016 Grant Thornton India LLP. All rights reserved.

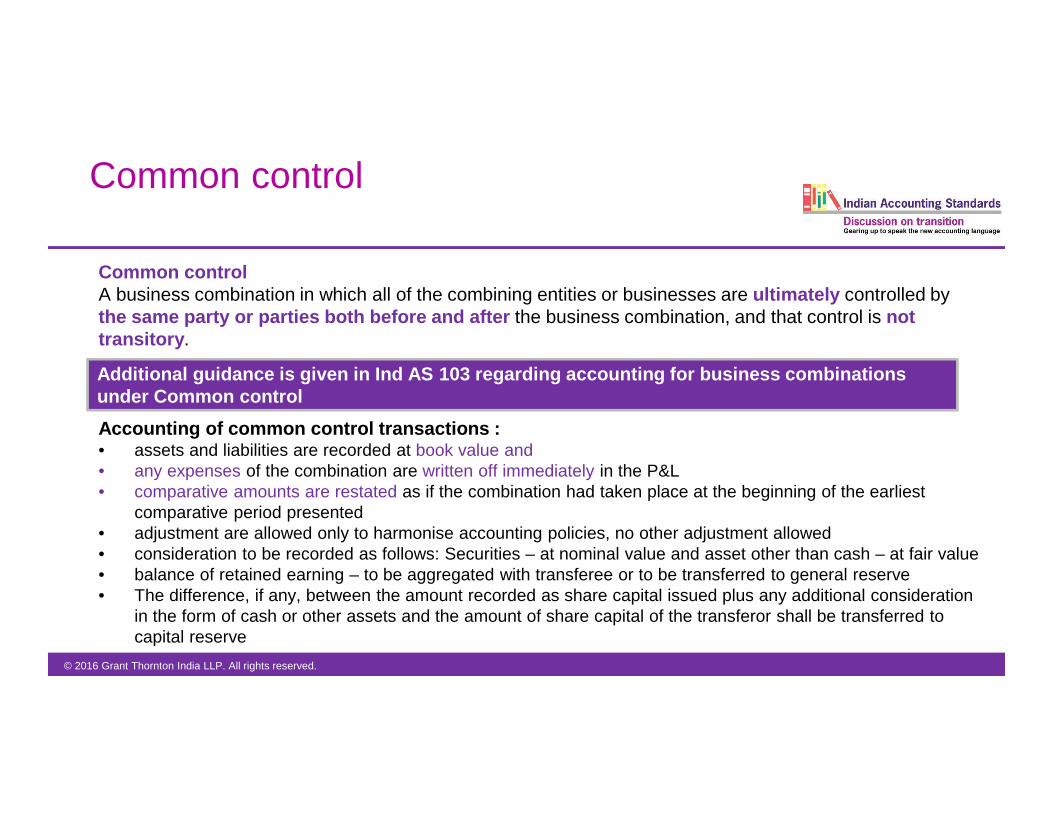

Common control

Common control A business combination in which all of the combining entities or businesses are ultimately controlled by the same party or parties both before and after the business combination, and that control is not transitory .

Accounting of common control transactions :• assets and liabilities are recorded at book value and • any expenses of the combination are written off immediately in the P&L• comparative amounts are restated as if the combination had taken place at the beginning of the earliest

comparative period presented• adjustment are allowed only to harmonise accounting policies, no other adjustment allowed• consideration to be recorded as follows: Securities – at nominal value and asset other than cash – at fair value• balance of retained earning – to be aggregated with transferee or to be transferred to general reserve• The difference, if any, between the amount recorded as share capital issued plus any additional consideration

in the form of cash or other assets and the amount of share capital of the transferor shall be transferred to capital reserve

Additional guidance is given in Ind AS 103 regarding accounting for business combinations under Common control

© 2016 Grant Thornton India LLP. All rights reserved.

Impact of new guidance

• Significant involvement of fair valuation specialists and correspondingly, impact on the size of balance sheets

• Since adjustments relating to business combination transactions are not pushed down to the subsidiary, parallel financial records are required to be maintained

• Accounting for business combination transactions also affects deferred tax balances

© 2016 Grant Thornton India LLP. All rights reserved.

Ind AS 109Financial Instruments

© 2016 Grant Thornton India LLP. All rights reserved.

Summary of transition from existingIndian GAAP to Ind AS

• Effective guidance in respect of selective financial instruments -investments (AS 13) and foreign currency forward contracts (AS 11)

• Accounting driven by conservatism:

– Investments valued at lower of cost and fair value

– Gains on fair valuation of derivatives are not recognised

• Detailed guidance is available on all aspects of various financial instruments

• Fair value based accounting on initial recognition; extensive guidance on impairment of financial assets

• Guidance on accounting for financial liabilities

• Derivative and embedded derivative accounting

• Hedge Accoutning

Existing IGAAP Ind-AS

© 2016 Grant Thornton India LLP. All rights reserved.

Definition

© 2016 Grant Thornton India LLP. All rights reserved.

Definition – Financial Instrument

Financial instrument is

Any contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity.

© 2016 Grant Thornton India LLP. All rights reserved.

Definition – Financial Asset

Financial asset is• cash

• an equity instrument of another entity

• a contractual right: – to receive cash or another financial asset from another entity– to exchange financial assets or financial liabilities under favourable conditions

• a contract that will or may be settled in the entity's own equity instruments and is– a non-derivative for which the entity is or may be obliged to receive a variable number of

the entity's own equity instruments; or– a derivative that will or may be settled other than by the exchange of a fixed amount of

cash or another financial asset for a fixed number of the entity's own equity instruments

© 2016 Grant Thornton India LLP. All rights reserved.

Definition – Financial Liability

Financial liability is

• A contractual obligation

– to deliver cash or other financial assets to another entity

– to exchange financial assets/ liabilities under potentially unfavourable conditions ; or

• a contract that will or may be settled in the entity’s own equity instruments and is:

– a non-derivative for which the entity is or may be obliged to deliver a variable number of the entity’s own equity instruments; or

– a derivative that will or may be settled other than by the exchange of a fixed amount of cash or another financial asset for a fixed numb er of the entity’s own equity instruments

© 2016 Grant Thornton India LLP. All rights reserved.

Case study 1

1. Shares of subsidiary companies-

Yes. However, investment in subsidiary is not covered under IAS 39

2. Advance given for purchase of goods

No. There is no contractual right to receive cash/ other financial assets

3. Perpetual debt carrying interest at fixed rate

Yes. Instrument contains contractual right to receive interest at stated rate

4. Prepaid expense

No. There is no contractual right to receive cash/ other financial assets

5. Deferred tax asset

No. Not arising because of contractual arrangement

© 2016 Grant Thornton India LLP. All rights reserved.

Case study 1

6. CENVAT credit receivable

No. Not arising because of contractual arrangement

7. Lease deposit paidYes. Lessee has contractual right to receive deposit at the end of term

8. USD-INR option held by the entity. The entity is buyer of the option Yes. Financial instruments also include derivatives instruments. Since the entity is option buyer, it is potentially favourable to the entity

9. Tax liabilityNo. Tax liability arises as per the law and not contractually

© 2016 Grant Thornton India LLP. All rights reserved.

Classification & Measurement

© 2016 Grant Thornton India LLP. All rights reserved.

Categories of financial assets – based on subsequent measurement

1Amortised

cost

2Fair Value

2AFair value

through OCI

2BFair value

through P&L

© 2016 Grant Thornton India LLP. All rights reserved. 28

Application to investments in debt securities

Debt investments

Contractual cash flows solely payments of principal and interest

Business model (BM) test(at entity level)

Fair value option elected?

Amortised cost

FVOCI (with recycling)

FVPL

FailPass

1Hold to collect contractual cash flows

2BM to collect contractual cash flows and sell asset

No No

Yes

Derivative investments Equity investments

Held for trading?

FVOCI option elected?

FVOCI (no recycling)

Fail Fail

Yes

No

No

Yes

3 -Neither 1 or 2

(A)

(B)

© 2016 Grant Thornton India LLP. All rights reserved. 29

Application to derivatives

Debt investments Derivative investments Equity investments

Contractual cash flows solely payments of principal and interest

Business model (BM) test(at entity level)

Held for trading?

Fair value option elected? FVOCI option elected?

Amortised cost

FVOCI (with recycling)

FVOCI (no recycling)

FVPL

Fail Fail FailPass

1Hold to collect contractual cash flows

2BM to collect contractual cash flows and sell asset

No No

Yes

Yes

No

No

Yes

Neither 1 or 2

© 2016 Grant Thornton India LLP. All rights reserved. 30

Application to equity investments

Debt investments Derivative investments Equity investments

Contractual cash flows solely payments of principal and interest

Business model (BM) test(at entity level)

Held for trading?

Fair value option elected? FVOCI option elected?

Amortised cost

FVOCI (with

recycling)

FVOCI (no recycling)

FVPL

Fail Fail FailPass

1 Hold to collect contractual cash flows

2BM to collect contractual cash flows and sell asset

No No

Yes

Yes

No

No

Yes

Neither 1 or 2

© 2016 Grant Thornton India LLP. All rights reserved. 31

'Solely payment of principal and interest' ('SPPI') test – (A)

• Contractual cash flows that are SPPI are consistent with a basic lending arrangement

• Principal is the fair value of the financial asset at initial recognition – principal amount may change over the life of the financial asset (for example, if there are repayments of principal)

• Interest elements – consideration consistent with basic lending arrangement:‒ time value of money‒ credit risk‒ other basic lending risks (example, liquidity risk)‒ costs associated with holding the financial asset for a particular period of time‒ profit margin that is consistent with a basic lending arrangement

• Assessment done in the currency in which financial asset is denominated

© 2016 Grant Thornton India LLP. All rights reserved. 32

Business model

What it is…• a matter of fact and not merely an assertion• determined by entity’s key management personnel (KMP)• determined at a level that reflects how groups of financial assets are managed together

to achieve a particular business objective• observable through the activities that the entity undertakes to achieve the objective of the

business model• a single entity may have more than one business model for managing its financial

instruments

What it is not…• does not depend on management’s intentions for an individual instrument• need not be determined at the reporting entity level• not determined on the basis of scenarios that the entity does not reasonably expect to occur

(‘worst case’ or ‘stress case’ scenarios)

© 2016 Grant Thornton India LLP. All rights reserved. 33

'Hold to collect' business model (B - 1)

• collect contractual payments over life of the instrument• entity manages the assets held within the portfolio to collect those particular

contractual cash flowsObjective

• policy to sell assets when there is an increase in the asset's credit risk or to manage credit concentration risk

• sales close to maturity of the assets where proceeds approximate remaining contractual cash flows

• increased sales in a particular period if the entity can explain the reasons for the sales

Examples of exceptions

Factors to consider

Frequency of sales in prior

periods

Value of sales in prior periods

Timing of sales in prior periods

Reason for such sales

Expectations about future

© 2016 Grant Thornton India LLP. All rights reserved. 34

'Hold to collect and sell' business model (B-2)

• KMP's decision – both:‒ collecting contractual cash flows and ‒ selling financial assets are integral to achieving the objective of the business model

• compared to 'hold to collect' business model, this business model will typically involve greater frequency and value of sales

• no threshold for the frequency or value of sales

• Examples of objectives consistent with 'hold to collect and sell' business model:‒ manage everyday liquidity needs‒ maintain a particular interest yield profile‒ match the duration of the financial assets to the duration of the liabilities that those

assets are funding

© 2016 Grant Thornton India LLP. All rights reserved. 35

'Other' business models – the residual category (B – 3)

• Financial assets are measured at fair value through profit or loss if they are not held within a business model whose objective is:

‒ to hold assets to collect contractual cash flows, or‒ achieved by both collecting contractual cash flows and selling financial assets

• Examples

− assets managed with the objective of realising cash flows through sale

− a portfolio that is managed, and whose performance is evaluated, on a fair value basis

− a portfolio that meets the definition of ‘held-for-trading’

© 2016 Grant Thornton India LLP. All rights reserved. 36

Subsequent measurement –financial liabilities

Sub

sequ

ent m

easu

rem

ent -

finan

cial

liab

ilitie

s

At fair value through Profit or loss

Carried at fair value, changes taken to income statement

Other Liabilities Carried at amortisedcost

© 2016 Grant Thornton India LLP. All rights reserved. 37

Initial measurement – transaction costs

Transaction costs

Financial instruments carried at other than FVTPL

Financial assetsTo be added to the amount originally

recognised

Financial liabilitiesTo be deducted from

amount originally recognised

Financial instruments Measured at FVTPL

Immediately recognised in profit or loss on initial

recognitionan entity shall measure a financial asset or financial liability at its fair value plus or minus, in the case of a financial asset or financial liability not at fair value through profit or loss, transaction costs that are directly attributable to theacquisition or issue of the financial asset or financial liability.

Transaction costs are incremental costs that are directly attributabl e to the acquisition or issue or disposal of a financial asset or financial liability.

Example of transaction cost are regulatory and registration fees, loan processing fees, brokerage, etc.

Note : Transaction costs expected to be incurred on a financial instrument's transfer or disposal are not included in the financial instrument's measurement.

© 2016 Grant Thornton India LLP. All rights reserved.

Derivatives and Embedded derivatives

© 2016 Grant Thornton India LLP. All rights reserved. 39

Definition of a derivative

'underlying'

• value changes in response to the change in a specified interest rate, financial instrument price, commodity price, foreign exchange rate, index of prices or rates, credit rating or credit index, or other variable

• exception for a non-financial variable that the variable is not specific to a party to the contract

initial net investment

future

Settlement

• requires:‒ no initial net investment; or ‒ initial net investment smaller than would be required for other types of contracts that

would be expected to have a similar response to changes in market factors

• settled at a future date

© 2016 Grant Thornton India LLP. All rights reserved. 40

Embedded derivatives –where can they arise?

• Contracts may not meet the definition of a derivative on standalone basis, but may have features of both financial instruments as well as embedded derivatives.

• An embedded derivative is a component of a hybrid financial instrument that includes both– a derivative and – a host contract

• For example – Convertible bond– Host contract The bond– Embedded derivative Call option on shares

• Effect of embedded derivatives– Some of the cash flows of the combined instrument vary in a similar way to a stand-

alone derivative.

HostEmbedded

derivative

Hybrid

instrument+ =

© 2016 Grant Thornton India LLP. All rights reserved.

Impairment of financial assets

© 2016 Grant Thornton India LLP. All rights reserved. 42

Credit losses increase as credit risk increases

Stage 1Deterioration in credit quality

Stage 2 Stage 3

12-month expected credit losses when asset originated or purchased

lifetime expected credit losses when credit quality deteriorates significantly

lifetime expected credit losses when credit losses are incurred or asset is credit impaired

Interest based on gross carrying amount of asset

Interest based on gross carrying amount of asset

Interest based on net carrying amount of asset

Recognition of expected credit losses

Recognition of interest

Performing Under-performing Non-performing

Credit qualityNot deteriorated significantly since initial recognition or have low credit risk at reporting date

deteriorated significantly in credit quality since initial recognition but that do not have objective evidence of a credit loss event

have objective evidence of impairment at the reporting date

if the financial instrument is determined to have l ow credit risk at reporting date, it may be assumed that the credit risk on a financial inst rument has not increased significantly

© 2016 Grant Thornton India LLP. All rights reserved. 43

The new impairment model

Is the asset credit impaired at initial recognition

nIs the asset a trade receivable / contract asset with

significant financing component / lease receivable, for which the lifetime expected credit loss measurement has been

elected

nIs the asset a trade receivable / contract asset without a

significant financing component

Has there been a significant increase in credit risk since initial recognition

Recognise 12 months credit losses

Recognize lifetime expected credit losses

y

y

y

y

Recognise changes in lifetime expected credit losses

© 2016 Grant Thornton India LLP. All rights reserved.

Thank you!

© 2016 Grant Thornton India LLP. All rights reserved.

Ind AS 110:Consolidated Financial Statements

© 2016 Grant Thornton India LLP. All rights reserved.

Summary of transition from existingIndian GAAP to Ind AS

• Control evaluated based on ownership interest or governance indicators

• If less than a majority of voting rights are held, control does not exist, unless control over governing body

• Exclusion from consolidation if control is temporary or subsidiary under severe long-term restrictions

• No guidance available for change in ownership interest without loss of control

• Principles-based evaluation of control –may enhance scope of consolidation

• Considers potential voting rights and de facto control (eg. single largest shareholder with dispersed minority)

• No exceptions to consolidation

• Impact of change in ownership interest without loss of control is accounted for in equity

Existing IGAAP Ind-AS

© 2016 Grant Thornton India LLP. All rights reserved.

The definition of control

Control

Power over the investee

Ability to use its power over the investee to affect returns

Exposure, or rights, to variable returns from its

involvement with the investee

All three elements of control must be present to conclude that an investor controls an investee

© 2016 Grant Thornton India LLP. All rights reserved.

Applying the control model - focus on 'power'

Control

Power over the investee

Ability to use its power over the

investee to affect returns

Exposure, or rights, to variable returns from its

involvement with the investee

Power = Existing rights that give the current ability to direct the relevant activities

Current ability does not necessarily require the rights to be exercisable immediately. Instead, the key factor is whether the rights can be exercised before decisions about relevant activities need to be taken.

© 2016 Grant Thornton India LLP. All rights reserved.

Identifying relevant activities

Relevant Activities

Major capital expenditures

Acquiring/ Disposing

subs

Approving budgets /

determining funding

Dividend and remuneration

decisions

Selling/ buying goods and

services

Appointing Board

members

Who appoints the Board and

key management personnel?

Who can change the strategic direction of

the entity?

Relevant activities are those activities that significantly affect the investee's return.

© 2016 Grant Thornton India LLP. All rights reserved.

Rights that can give an investor power over an investee

Voting rights

Potential voting rights

Rights to appoint/remove KMP/Board

Rights to enter into/veto transactions

Other rights

To have power over an investee, an investor must have existing rights that give it the current ability to direct the relevant activities .

© 2016 Grant Thornton India LLP. All rights reserved.

De facto control(In reality, actually, from the fact)

More likely that investor has control of investee

Number of voting rights held by investor

Size of investor’s holding of voting rights relative to other

vote-holders

Number of other parties that would have to act

together to outvote investor

Less likely that investor has control of investee

Increasing size/number

Decreasing size/number

Investor with less than a majority of voting rights may have defacto control

---

Indi

cato

rs -

--

© 2016 Grant Thornton India LLP. All rights reserved.

Potential voting rights

Rights to obtain voting rights of an investee

Substantive or

protective?

Purpose and design of

instrument and

involvement

Potential voting rights

Other voting or decision

rights

• Practical ability to exercise ‒ (in/out of money

options)

• Non-currently exercisable rights

© 2016 Grant Thornton India LLP. All rights reserved.

Applying the control model -- exposure or rights to variable returns

Control

Power over the investee

Ability to use its power over the investee to affect returns

Exposure, or rights, to variable returns from its

involvement with the investee

All three elements of control must be present to conclude that an investor controls an investee.

© 2016 Grant Thornton India LLP. All rights reserved.

Variable returns

Variable returns are returns that are not fixed and have the potential to vary as a result of the performance of an investee . Variable returns can be only positive , only negative or both positive and negative.

'returns' not 'benefits'…think

broadly

look again! substance over form

existence vs amount

© 2016 Grant Thornton India LLP. All rights reserved.

Applying the control model -- ability to use its power over the investee to affect returns

Control

Power over the investee

Ability to use its power over the investee to affect returns

Exposure, or rights, to variable returns from its

involvement with the investee

© 2016 Grant Thornton India LLP. All rights reserved.

Principal vs. agent considerations

An agent is a party primarily engaged to act on behalf of and for the benefit of another party or parties (the principal(s)) and therefore does not control the investee when it exercises its

decision-making authority.

principal vs. agent

rights held by other parties

remunerationscope of decision-making authority

over investee

exposure to variable returns

from other interests that it

holds in the investee

© 2016 Grant Thornton India LLP. All rights reserved.

Accounting requirements

• Line by line addition, intercompany elimination, translation of foreign operations

Consolidation procedures

• Accounting policies of all entities consolidated need to be harmonisedUniform accounting

policies

• Profit/loss allocation is between controlling and non-controlling interest is based on actual share ownership

Profit / loss allocation

• NCI is shown separately within equity• Loss is allocated even if NCI balance is negative

Non-controlling interest (NCI)

• Gain/loss arising on loss of control is recognised in income statement• No P&L impact where no loss of control

Loss of control

© 2016 Grant Thornton India LLP. All rights reserved.

Thank you!

© 2016 Grant Thornton India LLP. All rights reserved.

Income Taxes

© 2016 Grant Thornton India LLP. All rights reserved.

Income taxes (Ind AS 12)

• Income statement approach to deferred tax recognition; deferred tax not recognised for permanent differences.

• No deferred tax recognised on difference in investment amount in subsidiaries, joint ventures and associates and parent/investor's share in their net assets

• Deferred tax on unrealised intragroup profits is not recognised

• Balance sheet approach to deferred tax recognition; barring few defined exceptions, deferred taxes are always recognised

• Barring a defined exception, deferred tax is recognised in respect of such differences

• Deferred taxes on elimination of intragroup profits and losses are calculated with reference to the tax rate of the buyer

Existing IGAAP Ind-AS

© 2016 Grant Thornton India LLP. All rights reserved.

Ind AS 101: First-time Adoption

© 2016 Grant Thornton India LLP. All rights reserved.

Scope and applicability

Ind AS 101 shall be applied in the following instan ces:

• when the entity is preparing its first Ind AS financial statements

• for interim financial statements covered by the first period for which Ind AS financial statements are being prepared

First Ind AS financial statements are the first annual financial statements in which the entity adopts Ind AS and makes an explicit and unreserved statement of compliance with Ind AS

© 2016 Grant Thornton India LLP. All rights reserved.

Transition Date

• Transition date refers to:

‒ The beginning of the earliest period for which an entity presents full comparative information under Ind AS in its first Ind AS financial statements

• As on the transition date, an entity shall:

‒ prepare and present an opening Ind AS statement of financial position

‒ apply optional exemptions and mandatory exceptions of Ind AS 101

‒ recognise / derecognise all assets and liabilities as required by Ind AS

‒ reclassify items that are recognised in accordance with previous GAAP *, where required

‒ apply Ind AS in measuring all recognised assets and liabilities

* the basis of accounting that a first-time adopter used immediately before adopting Ind AS for complying with the reporting requirements in India.

© 2016 Grant Thornton India LLP. All rights reserved.

Group Question – Determination of transition date

Entity A decides to commence preparation of financial statements as per Ind AS.

The first financial statements will be prepared for the year ended 31 March 2017.

What will be the date of transition for Entity A?

The first Ind AS financials: 31 March 2017

Comparative information: 31 March 2016

Date of transition to Ind AS: 1 April 2015

© 2016 Grant Thornton India LLP. All rights reserved.

Optional exemptions

Exemption Impact

Business combinations For all transactions qualifying as business combinations under Ind AS 103, a company can choose to:• not restate business combinations before the date of transition.• restate business combinations before the date of transition.• restate a particular business combination, in which case all subsequent business

combinations must also be restated

Changes in existingdecommissioning,restoration (AROs),and similar liabilitiesincluded in the costof property, plant andEquipment

For AROs, first-time adopter may elect to:• measure the liability at transition date in accordance with Ind AS 37.• estimate the amount of the liability that would have been included in the cost of

the related asset when the liability first arose.• calculate the accumulated depreciation on that discounted amount, as of the

date of transition to Ind AS.

© 2016 Grant Thornton India LLP. All rights reserved.

Optional exemptions

Exemption Impact

Fair value as deemed cost for property, plant and equipment (PP&E), investment property and intangible assets

An entity can choose to measure PP&E at the transition date, as per:• fair value at the date of transition as deemed cost.• a revaluation carried out at a previous date (like a IPO) less accumulated

depreciation till the date of transition as deemed cost, subject to certain conditions.

• carrying value as on the date of transitionThe exemption can also be applied to intangible assets that meet the criteria for recognition and revaluation as per Ind AS 38 and to investment properties meeting the criteria for Ind AS 40

Cumulative translation differences

The cumulative translation differences for all foreign operations are deemed to be zero at the date of transition to Ind AS• The gain or loss on a subsequent disposal of any foreign operations shall

exclude translation differences that arose before the date of transition to Ind AS and shall include later translation differences

© 2016 Grant Thornton India LLP. All rights reserved.

Optional exemptions

Exemption Impact

Assets and liabilities of subsidiaries, associates and joint ventures

A subsidiary, that adopts Ind AS later than its parent, can elect to apply Ind AS 101 to use either:• the carrying amounts of its assets and liabilities included in the consolidated

financial statements, subject to eliminating any consolidation adjustments based on parent's date of transition, or

• carrying amount based on subsidiaries date of transitionIf a parent adopts Ind AS later than its subsidiary, the parent, in its consolidated financial statements, must measure the assets and liabilities of the subsidiary at the same carrying amounts as in the Ind AS financial statements of the subsidiary, adjusting for normal consolidation entries.

Compound instruments A compound financial instrument does not need to be bifurcated if the liability component is not outstanding at the transition date.

Employee benefits An entity can recognize all cumulative actuarial gains and losses subsequent to the date of transition to Ind AS in other comprehensive income.

© 2016 Grant Thornton India LLP. All rights reserved.

Optional exemptions

Exemption Impact

Investments in subsidiaries, jointly controlled entities and associates

In the separate financial statements, entities can measure investments in subsidiaries, jointly controlled entities and associates at either:• cost, determined in accordance with Ind AS;• deemed cost, defined as fair value (determined in accordance with Ind AS 39) at

the company’s Ind AS transition date, or• deemed cost, defined as previous GAAP carrying amount at the Ind AS

transition date.

Leases A company may elect to assess whether an arrangement contains a lease at the date of transition, rather than at the inception of the arrangement.

© 2016 Grant Thornton India LLP. All rights reserved.

Optional exemptions

Exemption Impact

Designation of previously recognized financial instruments

• A company may choose to designate a financial instrument as “at fair value through profit or loss” or may designate a financial asset as available-for-sale at its transition date.

• Financial instruments carried at amortized cost should be measured in accordance with Ind AS 109 from the date of recognition unless impracticable.‒ If impracticable then the fair value at the date of transition to Ind AS shall

be the new amortised cost

Service concessionArrangements

Companies may, if impracticable:• recognise financial assets and intangible assets that existed at the date of

transition• use their previous carrying amounts as carrying amount on date of transitionHowever, the financial and intangible assets recognized at that date shall be tested for impairment.

© 2016 Grant Thornton India LLP. All rights reserved.

Estimates

Non controlling interest

De-recognition of Financial Asset /Liability

Hedge Accounting

Mandatory exceptions

© 2016 Grant Thornton India LLP. All rights reserved.

Mandatory exceptions - Estimates

• Estimates under Ind AS as on date of transition :

‒ shall be consistent with previous GAAP, unless there were errors‒ after adjusting the differences in accounting policies‒ shall be made in accordance with Ind AS requirement if not required under previous GAAPs

Estimate required by previous GAAP Any evidence of error under

previous GAAPConsistent with Ind AS

Make estimate reflecting conditions at transition date Use previous estimate

Use previous estimate and make adjustments to reflect

Ind AS

No

Yes No

Use previous estimate Yes Yes

No

© 2016 Grant Thornton India LLP. All rights reserved.

Non – controlling interests

An entity shall apply the following prospectively:

• total comprehensive income is attributed even if it results in the non-controlling interests having a deficit balance;

• accounting for changes in the parent’s ownership interest in a subsidiary that do not result in a loss of control

Mandatory exceptions (Contd.)

© 2016 Grant Thornton India LLP. All rights reserved.

Other requirements – Comparative information

The first Ind AS financial statements shall include:

• 3 statements of financial position

‒ including the opening statement of financial position as on the transition date

• two statements of profit or loss

• two statements of cash flows

• two statements of changes in equity and related notes

© 2016 Grant Thornton India LLP. All rights reserved.

Other requirements - reconciliation

The financial statements shall contain the following reconciliation:

• equity reported as per previous GAAP to equity as per Ind AS as on:

‒ transition date

• profit and loss reported as per previous GAAP to total comprehensive income as per Ind AS

• material adjustments to the statement of cash flows

• in case of company voluntarily adopting Ind AS - comparatives are provided as per Ind AS and reconciliation to be provided

© 2016 Grant Thornton India LLP. All rights reserved.

Thank you!