ind as 116 - leases · ind as 116 - leases . june 2019. overview. 2 . ind as 116 at a glance ....

TRANSCRIPT

IND AS 116 - Leases

June 2019

Overview

2

IND AS 116 at a glance

Topic Description

Effective date 1 April 2019 Lessee accounting model

- Single Lease accounting model - No lease classification test - All leases on balance sheet :

• Lessee recognizes ROU asset and lease liability • Treated as a purchase of an asset on financed basis

Lessor accounting model

- Dual lease accounting model for lessors - Lease classification test - Finance lease accounting model based on IAS 17 - Operating lease accounting model based on IAS 17 operating lease accounting

Practical expedients

- Optional lessee exemption for short term leases - Portfolio level accounting permitted if it does not differ materially from applying

the requirements - Optional lessee exemption for leases of low value

Single lessee accounting model

All major leases on balance sheet

Balance sheet

Asset = ‘Right-of-use’ (ROU) of underlying asset

Liability = Obligation to make lease payments

P&L

Lease expense Depreciation

+ Interest

= Front-loaded total lease expense

4

What’s the impact?

Balance sheet Profit/loss

Asset Liability

Lessees appear to be more asset-rich, but also more heavily indebted.

Depreciation Interest

Cash rental payments

Total lease expense is front-loaded even when cash rentals are constant.

5

Impact on financial ratios

Profit/loss

EBITDA

Balance sheet

Total assets

Ratios

Gearing

EPS (in early years)

Net assets Interest cover Asset turnover

6

Application

7

Applying IND AS 116

Determine when to apply standard Identify the lease

Choose whether to apply the practical expedients Separate lease and non lease components

Apply lease accounting models

Lessee Lessee accounting model

Lessor Lessor accounting model

Apply Other relevant guidance

ADO Ying NO AS 116

Identify the popullation Applyi ng the standard

Full retrospective

Modifi,ed retrospective

Aoo ying Lease definition

Cost Comparability

Apply the definition to all contracts

.. OR

Grandfather existing contracts

and apply the definition only to new or chang,ed contracts

PE - pract ica l ·exped ie n t

Is there a Lease?

No

Identified asset?

Yes

A contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange of consideration

No Lessee obtains substantially all of the

economic benefits?

Yes

No

Lessee directs the use?

Yes

Contract does not contain

a lease

Contract is or contains a lease

13

How long is the lease -Lease term

Non-cancellable period

Lease term Optional renewal periods

if lessee reasonably certain to exercise

Periods after optional termination date if lessee reasonably certain not to exercise

12

Lease Components

If a contract contains lease then the company accounts for each lease component separately from non lease components

Lessee Lessor

When there is an observable standalone price for each component

Unless the practical expedient is elected (see below) separate and allocate based on the relative standalone price of components Example:

Always separate and allocate on a relative standalone selling price basis

When there is not an observable standalone price for some or all components

Maximise the use of observable information

Taxes, insurance on property and administrative costs

Activities (or cost of lessor) that do not transfer a good or service to the lessee are not components in a contract

Practical expedient: Accounting policy election by class of underlying

Combine Lease and any non lease components and account for them as lease components

NA

ADO Ying NO AS 116

Identify the popull.ation Applying the standard

Modified retrospective

••••

Recognition exemotions

Two major opt·onal exemptions make

• •••• I I

the standard easier to apply

Short term leases

Leases, of low

value items

:S 12 months :S USD 5,000 for example

Transition

1 6

nd AS17 to nd AS 116- Transition moact lessee I lessee I lessor I lessor

operating lease finance lease operating lease finance lease P ACJ.I

FuII retrospective

Modified retrospective with practicaexpedients

Modified retros.pe,ctive

No adjustm1 ent on transition exoept for subleases

Lessee Accounting

1 8

+

Lease iabi ity- measurement

Present value of remaining rent.

als

Present value of exp,ected

payments at. end of leas,e

Lease payments

Lessee includes the following payments for use of underlying asset in measurement of the liability:

• Fixed payments (less any incentive receivable and including in-substance fixed payments structured as variable lease payments)

• Variable payments that depend on index or a rate

• Amounts expected to be payable by the lessee under residual value guarantees

• Exercise price of purchase option , lessee is reasonably certain to exercise

• Payments to terminate the lease if the lease term reflects early termination

20

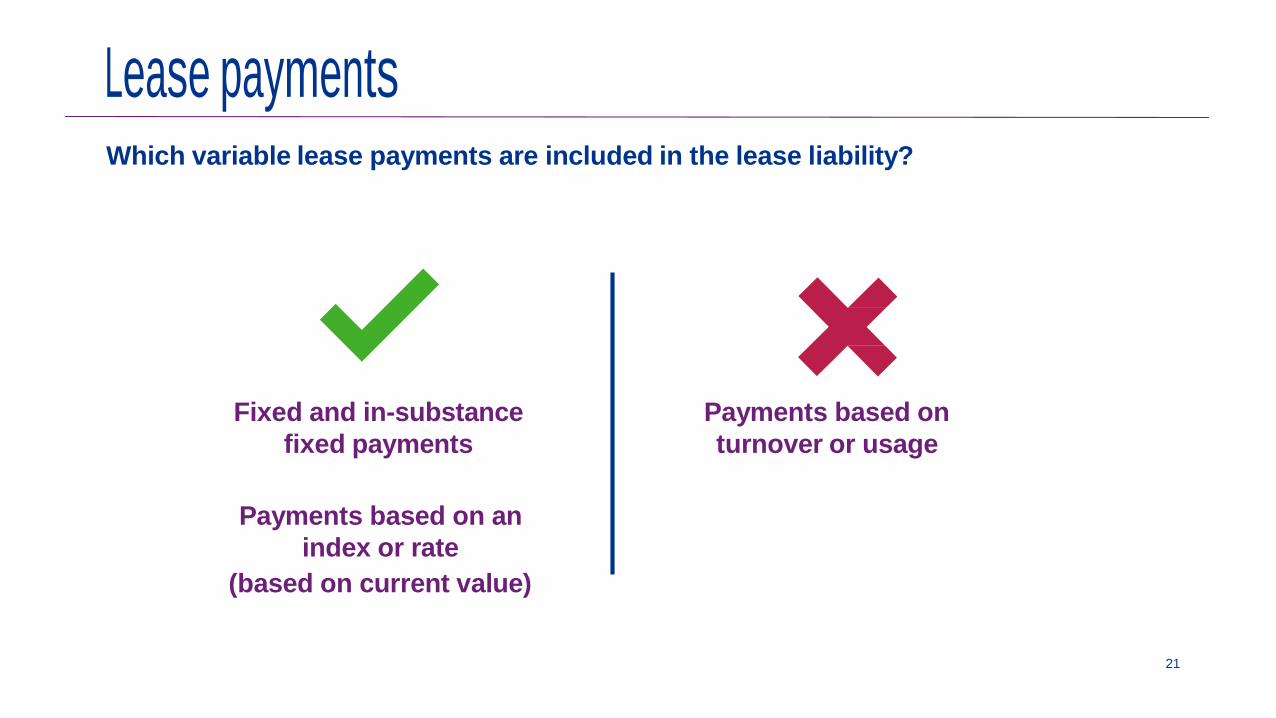

Lease payments

Which variable lease payments are included in the lease liability?

Fixed and in-substance fixed payments

Payments based on an index or rate

(based on current value)

Payments based on turnover or usage

21

Discount Rate

Lessee calculates the present value of the lease payments using the interest rate implicit in the lease.

If implicit rate is not determinable then lessee uses its incremental borrowing rate i.e this is the rate that lessee would pay on the commencement date of lease for a loan of a similar term and security to obtain similar value to the right of use asset in similar economic environment

22

Initial measurement of Right of use (ROU) asset

Lease liability +

Initial Direct cost +

Prepaid lease payments +

Estimate cost to dismantle, remove or restore –

Lease incentives received =

Right of use asset

Measurement of Right of use [ROUJ asset on transition

,Option 1 .. ...... Option2

Apply lnd AS 36 at

Transition approach - Illustration

Measuring the lease liability: Modified retrospective approach

For leases previously classified as operating leases, a lessee measures the lease liability at the date of initial application as the present value of the remaining lease payments. The discount rate is the lessee’s incremental borrowing rate at that date.

Lease commences on 1 April 2014. • Non-cancellable lease period:

10 years • Option to renew for further five

years.

Fixed rental of INR100 per annum

Incremental borrowing rate on: • Transition date: 5% p.a. • Commencement of

lease: 7% p.a.

At the time of lease commencement:

It is not reasonably certain to exercise renewal options

Remaining term of lease is five years

Analysis: Lease liability on transition is calculated based on the lease payments over the remaining lease term (five years at INR100 per annum) discounted at its incremental borrowing rate at that date-5% – giving a lease liability of INR433.

25

Transition approach – Illustration (cont.)

Measuring ROU asset

Option 1: Measure retrospectively using transition discounting rate

Option 2: Lease liability +/ - prepaid/accrued payments

Apply this option on a lease-by-lease basis

Option 1: Retrospective but using the incremental borrowing rate on transition date

Analysis: Assuming there are no initial direct costs, ROU asset is calculated on lease commencement (1 April 2014) as the present value of the lease payments over the 10-year term (10 years at INR100 per annum) discounted at ABC’s incremental borrowing rate on transition of 5% – giving an amount of INR772.

Considering that company choses to depreciate ROU assets on a straight-line basis over the lease term, the carrying amount of the ROU asset on transition date is 5 / 10 x INR772 = INR386.

Journal entry on initial recognition of this lease on date of transition is:

Particulars Debit (INR) Credit (INR)

ROU asset 386

Retained earnings 47

Lease liability 433

26

Transition approach – Illustration (cont.)

Option 2: ROU asset equal to the lease liability

Analysis: Under option 2, on the date of transition, the ROU asset is equal to the lease liability of INR433.

Journal entry on initial recognition of this lease on date of transition is:

Particulars Debit (INR) Credit (INR)

ROU asset 433

Retained earnings -

Lease liability 433

Overall transition choice: Option 1 typically results in a lower depreciation charge and lower risk of impairment. In the above example, the depreciation charge under both options is: Option 1: 1/5 x INR386 = INR77 Option 2: 1/5 x INR433 = INR87

Full retrospective approach: Requires companies to determine the carrying amount of all leases in existence at the earliest comparative period as if those leases had always been accounted for under IFRS 16 using incremental borrowing rate at the inception of the contract.

27

Practical Expedients

2 8

'-J c.;J

\...::7

Practica Exoadiants

8 Account for l eases expiri ng withi n 12 months as short term leases.

Lease liability

Apply single discount rate to leases with similar characteristics.

Use of h i ndsi ght e.g. determini ng lease term.

Exclude initial direct costs from ROU asset measurement.

Onerous contracts - alternative to pe1formi n g impa i rment revi ew.

Modified retrospective approach only!

PE # 3 use of hindsight

Issue

• Entity A leases a building with a lease commencement date of 1September 2006.

• Leas·e payments are based on CPl.

• Entity A intends to use the modif1ied retrospective approach with the ROU asset measured as if lnd AS 116 had

been appli·ed since 1September 2006 (lnd AS 116.C8(b)(i)).

Question

Can hindsight be used for the changes iin CPI that occur after lease commenoement but before tlhe date of

init1ial appllication.

Presented views.

• View A: Yes

• View B: No

PE# 4- Transition ootions- examo e 2

7-yea rs eq u i pme nt lease f rom 1J a n

20.16

CUlO,OOO per a n num 1 n a rrea rs

InitiaI di rect costs: CU7,000

ROU asset de preciated on a st raight-l i ne basis '

I

PE# 4- Transition ootions examo e 2

Amount incllude i n the ROU asset fo:r the initial direct costs?

CU7,000

CU4000

Nil

CU7,000*4/7 8

Unamortised a1mount of

Exclude initial PE#4 direct costs

from ROU asset measurement.

PE# 5- onerous contracts

I

i Issue I I I

i • Retailer R leases 100 stores u nder leases classified as l nd AS 17 operating leases. R has ceased trad i ng at 20 stores I I

I and is seeking to sublet these.

• In March 2018, R assesses whether t he leases on the vacant 20 stores are onerous u nde·r lnd AS 37 a nd conclludes tlhat 12 are onerous and 8 are not.

• Ruses the 1 modif ii ed retrospective transit1 i on method with a DI A of 1April 2019. R plans to use the practical exped;ent to r,ely on its assessment of onerous contracts u nder lnd AS 37, instead of impai rme nt review..

Question 1

What is the maximum nUimber of leases to wh ich R can appll ythe practical exped ient?

Presented views

• View 1: 100 l eases.

• View 2: 20 leases- i.e. those that were assessed to determine if they were onerous. I I

i • View 3: 12 1eases- i.e. those for which a provisi on was recognised . I I

Lessee Finance Lease

FuIll retrospective

Modified retrospective with

practicaI expedlients

Full retrospecti1 ve

Modifi·ed retrospective

No adjustm1 ent on transition except for subleases

Transition- Lessee Finance Lease

Identify the population Applying the standard

*lnd AS 116 ROU asset and lease liability = lnd AS 17 carrying amounts

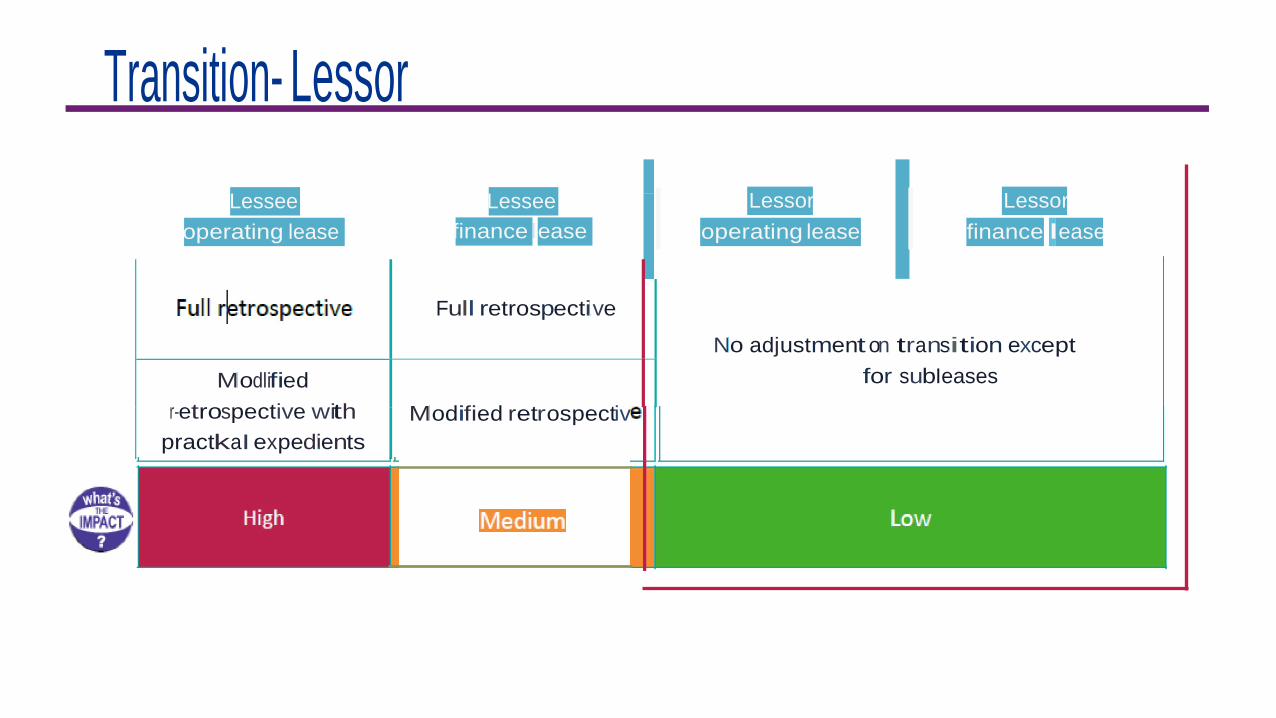

Transition- Lessor

3 6

Lessee Lessee operating lease finance llease

Full retrospecti1 ve

Mlodlified

r-etrospective with practkaI expedi1 ents

I I Transition- Lessor

Lessor operating lease

Lessor finance lease

Mlodified retrospectiv

Nlo adjustment on trans.ition except for subII eases

Lease and non-lease components

A lessor uses IND AS 115 to allocate consideration between:

Lease components and Non-lease components

Items that do not transfer a good or service to the lessee are not components

No practical expedient to combine lease and non-lease components

38

Example – identifying components

Right to use an office building

Cleaning and maintenance services

Property taxes and insurance

39

Example – identifying components

Right to use an office building

Cleaning and maintenance services

Property taxes and insurance

Lease component Non-lease component Not a component

46

Example – allocating consideration

SSP = 90 SSP = 10 Cost = 5

Assume annual rental charge by the lessor to the lessee is 105

47

Example – allocating consideration

SSP = 90 SSP = 10 Cost = 5

Assume annual rental charge by the lessor to the lessee is 105

IND AS 116 income

90/(90+10) x 105

IND AS 115 revenue

10/(90+10) x 105

Not a component

48

Sub-lease

4 3

Sub-lease – IAS 17

Head lessor

Head lease:

30-year lease of land

Sub lease:

30-year lease of land

Bank (intermediate lessor)

Operating lease

— Recognise straight line expense

Operating lease

— Recognise straight line income

Fast Retail Co (sub-lessee)

53

Sub-lease – IND AS 116

Head lease:

30-year lease of land

Sub lease:

30-year lease of land

Head lessor

Bank (intermediate lessor)

Fast Retail Co (sub-lessee)

ROU model

— Dr ROU asset — Cr Lease liability

Finance lease

— Dr Lease receivable

— Cr ROU asset

54

?

Wrap Up

Wrap Up

•IND AS 116 impact

•Lease definition

•Lessee- operating lease accounting

•Lessee- Finance lease accounting

•Lessor – accounting

•Sub leases

•Intercompany leases

•Disclosures

50

What questions do you have?