incorporating sustainability into business decisions: how

TRANSCRIPT

i

Incorporatingsustainabilityintobusinessdecisions:how

organisationschoosetobuildabetterworld

CatherineElizabethAnneTilley

ChurchillCollege

May2019

ThisdissertationissubmittedforthedegreeofDoctorofPhilosophy

i

Declaration

Thisdissertationistheresultofmyownworkandincludesnothingwhichisthe

outcomeofworkdoneincollaborationexceptasdeclaredinthePrefaceandspecifiedin

thetext.

ItisnotsubstantiallythesameasanythatIhavesubmitted,or,isbeingconcurrently

submittedforadegreeordiplomaorotherqualificationattheUniversityofCambridge

oranyotherUniversityorsimilarinstitutionexceptasdeclaredinthePrefaceand

specifiedinthetext.Ifurtherstatethatnosubstantialpartofmydissertationhas

alreadybeensubmitted,or,isbeingconcurrentlysubmittedforanysuchdegree,

diplomaorotherqualificationattheUniversityofCambridgeoranyotherUniversity

orsimilarinstitutionexceptasdeclaredinthePrefaceandspecifiedinthetext

ItdoesnotexceedtheprescribedwordlimitfortheDegreeCommitteeinEngineering.

ii

Incorporatingsustainabilityintobusinessdecisions:howorganisationschoosetobuildabetterworld

CatherineTilley

Abstract

Businesseshaveacriticalroleinthetransitiontoasustainableeconomy,butthis

requiresthemtoincludesocialandenvironmentalconsiderationsintheirdecision-

making.However,thiscreatestheproblemofresolvingcompetingeconomic,socialand

environmentalcommitmentsoverthelongandshortterm.Scholarshaveexamined

thiseitherasananalyticaloracognitiveproblem,buttheseapproachesmayunderstate

theimportanceoforganisationalinfluences.Thisthesisthereforeaddressestwo

questions:first,howdotheformal,behaviouralandsocialstructuresofanorganisation

interacttoinfluencetheinclusionofsustainabilitycriteriaindecision-makingin

incumbentbusinesses?Second,whatarethepointsofinterventiontoinfluencethese

systems?Toanswerthesequestions,Iundertookthreeconnectedempiricalstudies,

usingmixedqualitativemethods.

Theseinvestigationsproducedfourfindings.First,includingsustainabilitychangesthe

natureofdecisions,leadingtofourspecificarchetypesofdecisions.Second,thewayin

whichdecision-makersresolvethecompetingcommitmentsinthesesituationsis

shapedbyabroaderframingofthetensionbetweenthefundamentallogicofthe

businessandthedemandsofitsenvironment.Third,decision-makingisinfluencedbya

seriesofcontextualfactors,includingthepropertiesofthedecisionitself;thedecision

maker(s);theorganisation;andthebroaderenvironmentalcontext.Fourth,theprocess

ofchangingdecision-makingrequiresacombinationofinterventions,andasetof

foundationalcapabilitiestochange.Companiesundertakingthistypeofchangefind

systemicbarriersthatcanonlyberesolvedthroughco-operationbeyondtheboundaries

oftheorganisation.Thesefindingshaveimplicationsforpractice.

iii

Thisresearchcontributestotheliteratureondecision-makingandsustainabilityby

presentinganovelclassificationofdecisionsandbyaddingdetailtotheunderstanding

ofcontextualfactorsinfluencingdecision-makersandtoparadoxtheoryby

demonstratingtheinfluenceofparadoxesondecision-makinglogicandondriving

change.Thismatters:corporatesustainabilityisanenactedprocessandunless

businessdecision-makingchanges,wewillnotbeabletoachievethesocialand

environmentalchangeweneed.

iv

‘Itisourchoices,Harry,thatshowwhatwetrulyare,farmorethanourabilities’

J.K.RowlingHarryPotterandChamberofSecrets

v

AcknowledgementsAlthoughthisdissertationiswritteninthefirstperson,therearemanypeoplewithout

whomitwouldneverhavebeeneitherstartedorfinished,andinthisshortspaceitwill

notbepossibletothankallofthemtotheextenttheydeserve.Despitethis,I’d

particularlyliketothankmysupervisor(and,Ihope,friend)SteveEvansandthemany

intervieweeswhoIcannotnameforconfidentialityreasons,butwithoutwhomthis

wouldbeathindocumentindeed.

Athesisisasolowork(andanyerrorsareemphaticallymyown),butresearchersneed

communities,andIhavebeenfortunatetobeamemberofseveralwonderfulnetworks.

InCambridge,theInstituteforManufacturingprovidedmewithawelcomingacademic

homeandasplendidcollectionoflunchcompanions;ChurchillCollegegavemean

interdisciplinarycommunityandamagnificentmentorinGeorgiaSorenson;Polly

CourticeandcolleaguesattheCambridgeInstituteforSustainabilityLeadership

introducedmetopeopleandideaswhohavebeeninfluentialinthisworkandtriggered

theideafortheresearch.I’vealsobeensupportedbygroupsofothersustainability

scholars:theEGOSParadoxgroupwelcomedmeearlyinmycareer;theGRONEN

networkintroducedmetoagroupofpeoplewithsharedinterests;andtheIvey/ARCS

fellowshipenabledmetobuildagroupofpeers.TimaBansal,TobiasHahnandmany

morehavebeengenerouswiththeirguidanceandsupportasInavigatedthecomplex

worldoforganisationalscholarship.

Throughoutthis,I’vebeensupported,toleratedandgenerallylookedafterbymyfamily.

MypartnerNic,brotherJames,andfatherPeterhaveseenmethroughthetoughtimes

aswellasthefunofdiscovery,andIamgratefulbeyondwordsfortheirencouragement

andgoodhumour.

Finally,Iwouldliketoacknowledgethreefriendswhowerenotwithmeonthejourney.

JuliaLawrence,KarenTannerandLyndaWoodswerebrilliant,beautifulwomenwhose

liveswereaninspirationtomany.Theirdeathsin2015promptedthereflectionsonlife

thatledtothisthesis,andtheyhaveoftenbeenonmymindalongtheway.Their

memoryhasbeenablessing.

vi

TableofContentsDeclaration..............................................................................................................................................iAcknowledgements............................................................................................................................vAbstract...................................................................................Error!Bookmarknotdefined.TableofContents...............................................................................................................................viIndexofFigures...........................................................................................................................viiiIndexofTables...............................................................................................................................ix

1:INTRODUCTION............................................................................................................................11.1 Thecontext............................................................................................................................11.2Theproblemthiscreates....................................................................................................21.3Theobjectiveofthisresearch...........................................................................................31.4Howthisdocumentisorganised.....................................................................................4

2:THERESEARCHQUESTION......................................................................................................62.1Introduction..............................................................................................................................62.2Threemainschoolsofthoughtindecision-making................................................62.3Sustainabilityinbusinessdecision-making:mappingtheliterature.............82.4Thesustainabilitycontext................................................................................................142.5Literatureonanalysisandinformation......................................................................162.6Sustainabilityandmanagerialcognition....................................................................192.7Sustainabilityandorganisation.....................................................................................222.8Problematisingtheliterature..........................................................................................242.9TheResearchQuestions....................................................................................................26

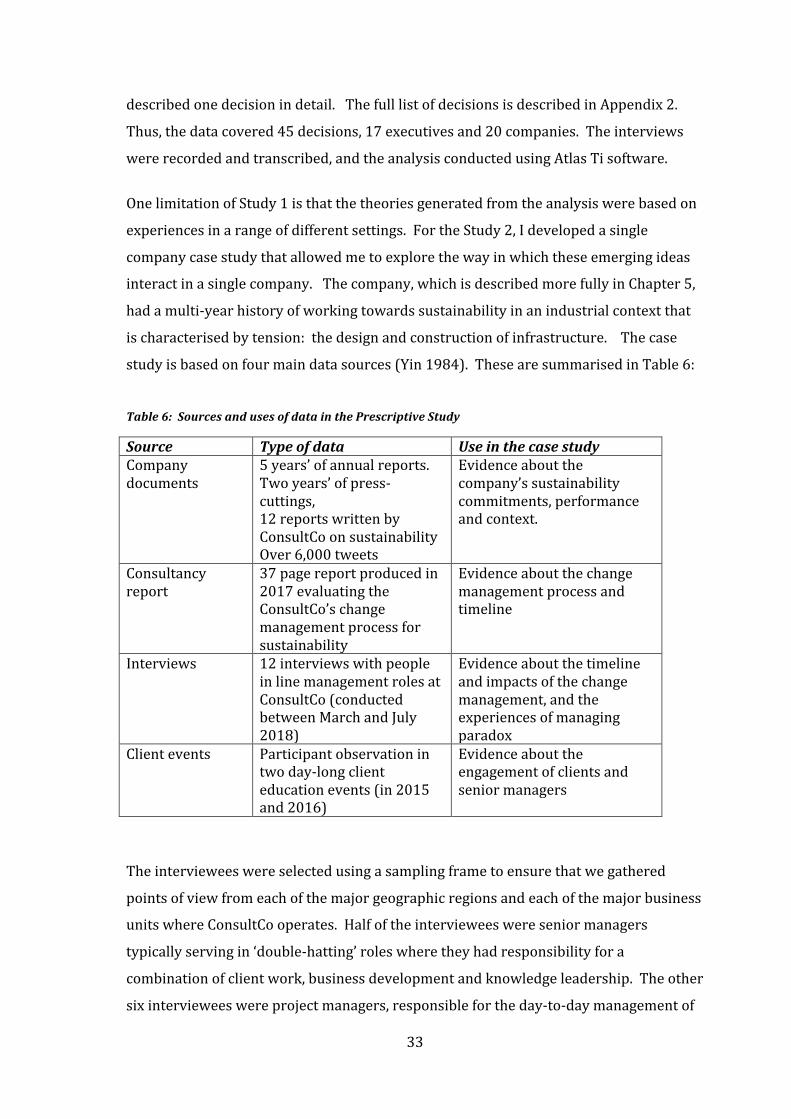

3:METHOD.........................................................................................................................................273.1 Introduction........................................................................................................................273.2Researchapproach............................................................................................................273.2.1 Researchphilosophy..............................................................................................273.2.2Researchprinciples....................................................................................................28

3.3Researchmethods................................................................................................................293.3.1Researcharchitecture................................................................................................293.3.2Choiceofqualitativemixedmethods..................................................................30

3.4Analyticalapproach...........................................................................................................363.5Limitationsofthemethod................................................................................................40

4:STUDY1...........................................................................................................................................444.1Introduction............................................................................................................................444.2Whydosustainabilityconsiderationsmakedecisionsdifficult?.....................454.2.1Analyticalapproach....................................................................................................464.2.2Fourarchetypesofdecisions..................................................................................504.2.3Demandsondecision-makingprocess...............................................................56

4.3Competingcommitmentsandparadoxesinsustainability................................624.3.1Analyticalapproach....................................................................................................654.3.2Howdoexecutivesmanagecompetingdemands?........................................664.3.3Howdoindividualdecision-makersusetheseapproaches?....................674.3.4Howdothecharacteristicsofthedecisionsinformchoiceofapproach? 684.3.5Tensionbetweentheexternalandinternalcontext..................................724.3.6Connectionsbetweenthemacroandmicroleveltensions.......................78

4.4Organisationalinfluencesondecision-making.......................................................794.4.1Theproblemoforganisingforsustainability..................................................80

4.4.2Organisationdesign.........................................................................................................824.4.3Performancemanagement......................................................................................864.4.5Culture..............................................................................................................................87

vii

4.4.5Leadership......................................................................................................................904.4.6Summaryoforganisationalinfluences..............................................................92

4.5Individualdecision-makers.............................................................................................934.5.1Knowledge......................................................................................................................934.5.2Biasesandattitudes...................................................................................................964.5.3Permissionspace.........................................................................................................994.5.4Frameworkofinfluencesondecision-making............................................104

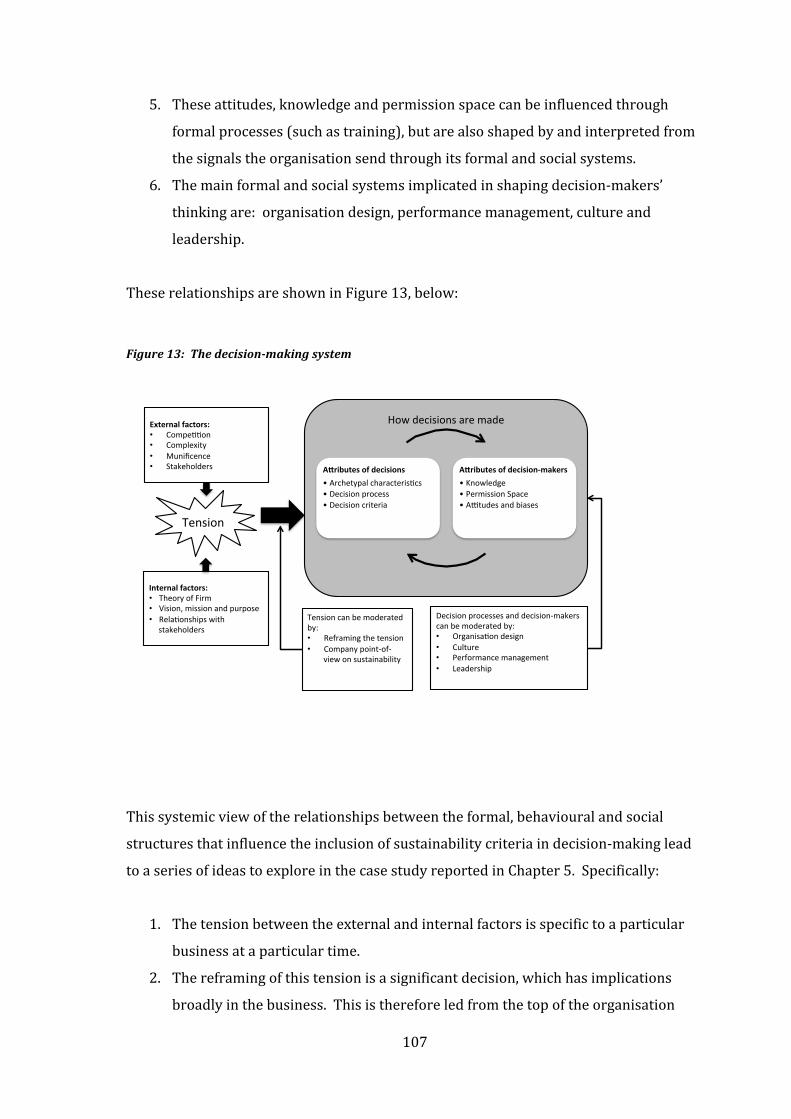

4.6Thesystemfordecision-making................................................................................1055:STUDY2........................................................................................................................................1095.1Introduction........................................................................................................................1095.2Method...................................................................................................................................1105.3TheCaseContext...............................................................................................................1115.4Tensionbetweentheinternalandexternalcontext.......................................1135.5SegmentationofConsultCo’sdecisions.................................................................1175.5.1ThePre-BidStage.....................................................................................................1185.5.2TheBidStage..............................................................................................................1205.5.3ProjectStart-Up........................................................................................................1215.5.4ProjectManagement...............................................................................................1225.5.5HowConsultCo’ssustainabilityagendainfluencesdecisions...............123

5.6ConsultCo’sorganisation...............................................................................................1245.6.1OrganisationalFactors...........................................................................................1255.6.2Individualfactors.....................................................................................................1355.6.3Summary......................................................................................................................142

5.7ConsultCo’snestedparadoxes....................................................................................1445.8Conclusions.........................................................................................................................147

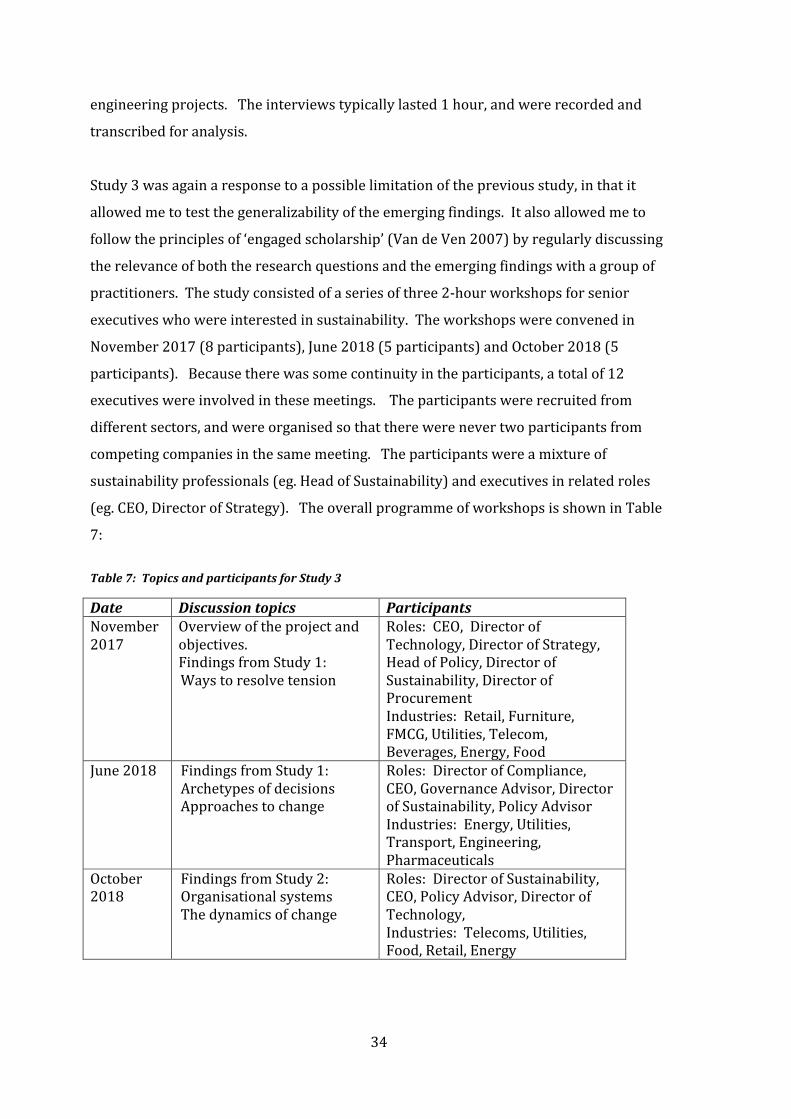

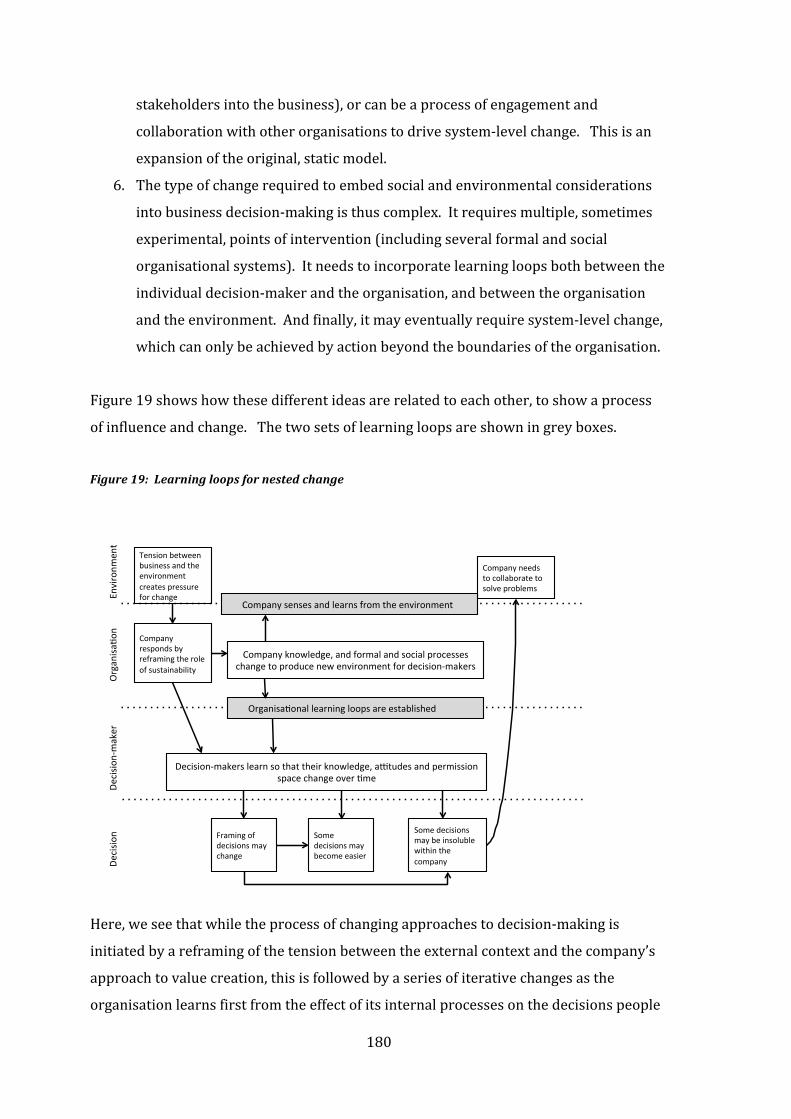

6:STUDY3........................................................................................................................................1516.1Introduction........................................................................................................................1516.2Reframingthecorporate-leveltension...................................................................1526.3Decisionpropertiesandprocess................................................................................1546.4Organisationalinfluencesonchange.......................................................................1636.4.1Individualattributesandbehaviour................................................................1636.4.2Organisationalfactors..........................................................................................1666.4.3Thecriticalroleofknowledgeandlearning.................................................1696.4.4Influencesbeyondtheboundariesoftheorganisation...........................1696.4.5Implicationsforchange.........................................................................................172

6.5Nestedchangeandthewhack-a-moleapproach..............................................1736.5.1Conditionsofthiscase...........................................................................................1736.5.2Thewhack-a-molemetaphor..............................................................................1746.5.3Nestedness..................................................................................................................178

6.6Conclusions.......................................................................................................................1797:CONCLUSIONS..........................................................................................................................1837.1AnsweringtheResearchQuestions..........................................................................1837.2Limitationsoftheresearch...........................................................................................1847.3ContributionstoKnowledge........................................................................................1847.3.1Contributionstothestudyofdecision-making...........................................1847.3.2ContributionstoParadoxtheory.......................................................................185

7.3ImplicationsforPractice...............................................................................................1867.4Futuredirections..............................................................................................................188

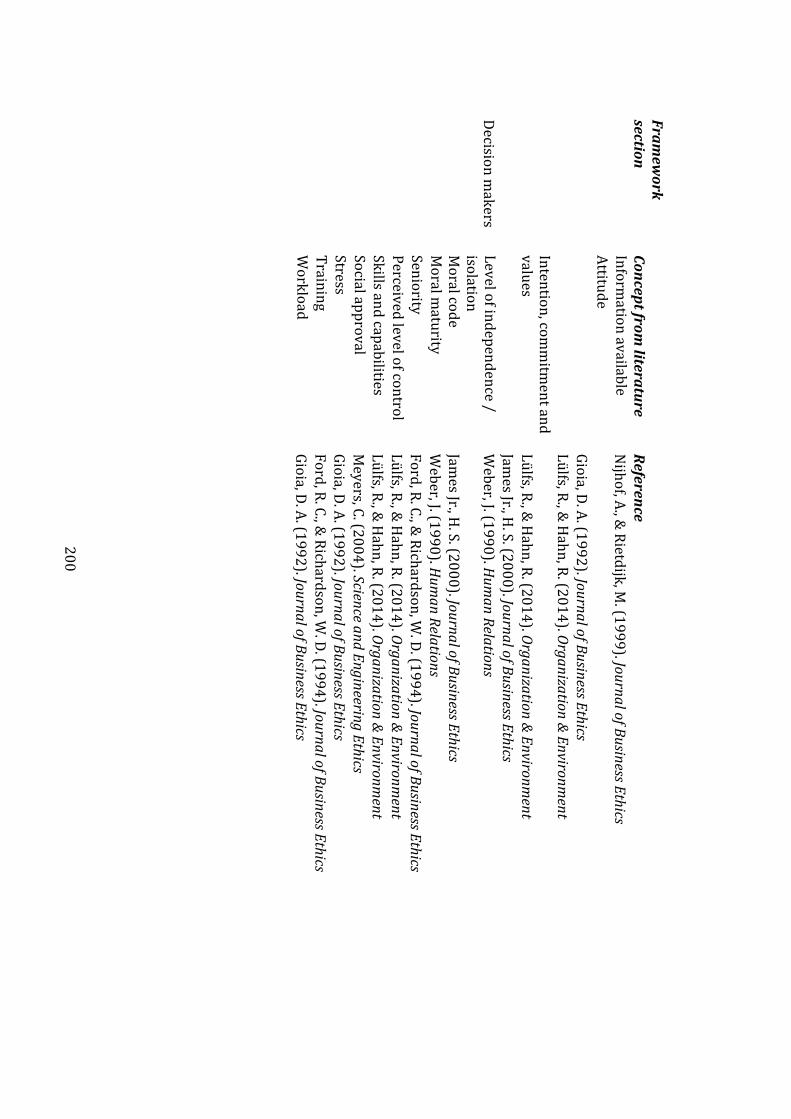

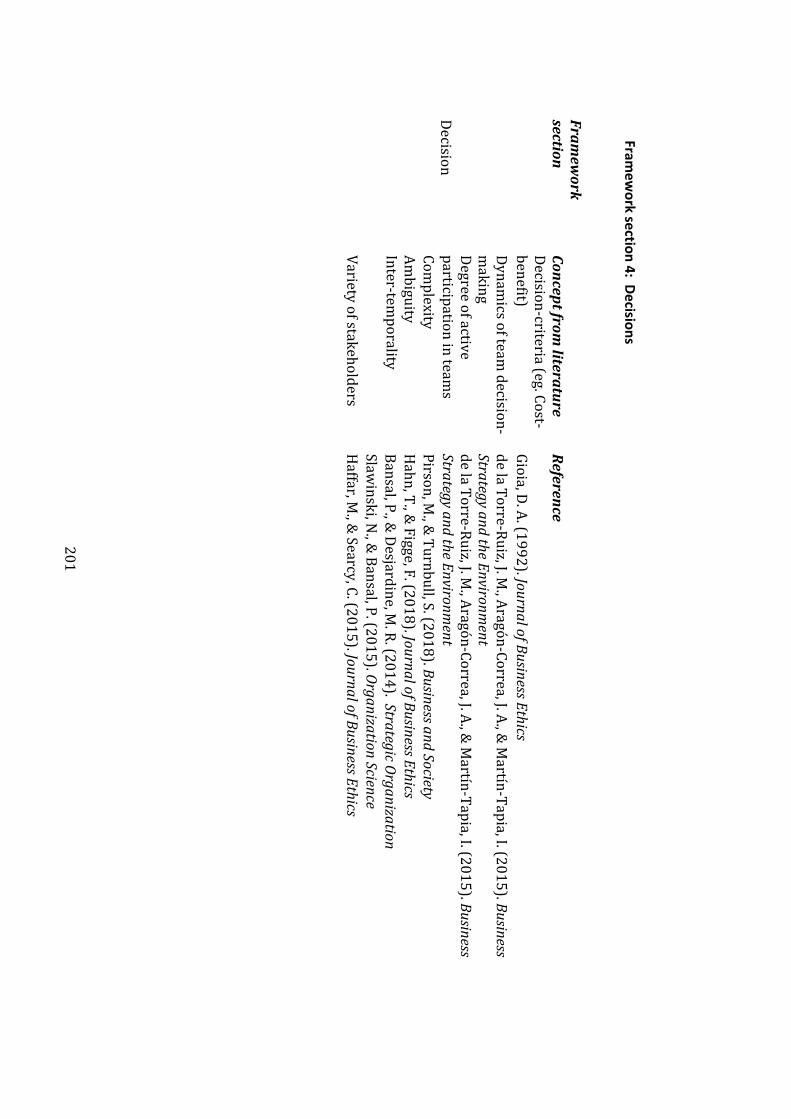

Appendix1:Keyorganisationalconceptsfromtheliterature..................................190Frameworksection1:Environment...............................................................................190Frameworksection2:Organisation................................................................................191

viii

Frameworksection3:Decision-makers........................................................................199Frameworksection4:Decisions.......................................................................................201

Appendix2:ListofDecisions..................................................................................................202Appendix3:Datastructurefrominterviewsandliterature.......................................205References........................................................................................................................................216

IndexofFiguresFigure1:Contextualfactorsinfluencingtheinclusionofsustainabilityindecision-

making.........................................................................................................................................24Figure2:Overallstudydesign..................................................................................................35Figure3:Processfordataanalysis–Study1......................................................................36Figure4:Datastructurefortheouterlayerofthecontextframework...................38Figure5:Datastructurefortheformalelementsoftheorganisationalcontext.38Figure6:Datastructureforthesocialelementsoftheorganisationalcontext...39Figure7:Datastructurefortheindividuallayerofthecontextframework.........39Figure8:Fourcontextsfordecision-making......................................................................44Figure9:Howfrequentlyaredifferentapproachesusedtomanagecompeting

demands?....................................................................................................................................66Figure10:Approachesadoptedincompaniesthatreframetheirbusinessparadox 78Figure11:Fourlevelsofinfluenceondecision-making.................................................80Figure12:Organisationalinfluencesondecision-making.........................................104Figure13:Thedecision-makingsystem.............................................................................107Figure14:KeyinitiativesinConsultCo'schangemanagementprogramme......113Figure15:Keydecisionsduringtheprojectlifecycle..................................................118Figure16:NestedtensionsatConsultCo...........................................................................146Figure17:Fivecapabilitiesneededformakingdecisionsin'messysituations'160Figure18:Organisationaldynamicsshapingdecisionsovertime.........................172Figure19:Learningloopsfornestedchange...................................................................180Figure20:Foundationalandcontextualchange.............................................................182Figure21:Changestepsforcompaniestoincorporatesustainabilityintodecision-

making......................................................................................................................................187

ix

IndexofTables

Table1:Numberofarticlescategorisedbytheme...........................................................10Table2:ThematicanalysisofarticlesbypublicationError!Bookmarknotdefined.Table3:Howanalyticmethodsmapontotensionscreatedbythesustainabilitycontext

........................................................................................................................................................17Table4:Objectivesandapproachforeachresearchstep.............................................30Table5:Listofinterviewees......................................................................................................32Table6:SourcesandusesofdatainthePrescriptiveStudy........................................33Table7:TopicsandparticipantsforStudy3......................................................................34Table8:Intervieweesreflectionsoncharacteristicsofsustainability-relateddecisions

........................................................................................................................................................47Table9:Factorsmakingdecisionsmoredifficult.............................................................49Table10:Fourarchetypesofdecisions.................................................................................51Table11:Differentcharacteristicsanddecision-supportneedsofthefourdecision

archetypes.................................................................................................................................58Table12:Sixtheoreticalapproachestomanagingtension..........................................64Table13:Howpeopletalkabouttheirlogicalapproach...............................................65Table14:Characteristicsofdecisionsassociatedwithdifferentresolutionapproaches

........................................................................................................................................................69Table15:Theroleoforganisationalfactorsinenablingorhinderingsustainabilityat

ConsultCo................................................................................................................................143Table16:Testingthetheoreticalideas..............................................................................148

1

1:INTRODUCTION

1.1 Thecontext

Intwomajorglobalpolicydecisionsin2015,policy-makersdescribedtheworldwe

wanttoseeandcommittedtosubstantialchangetocreateaneconomywhichismore

sociallyandenvironmentallysustainable.InSeptemberthatyear,theUNsignedthe

SustainableDevelopmentGoals(SDGs),whichsetouttargetstoachievebettersocial,

environmentalandeconomicoutcomesfortheworldoverthenext15years,andin

DecembertheConferenceofParties(COP)signedtheParisAgreementtocommitto

reducegreenhousegasemissions.Takentogether,thesecommitmentsdescribethe

worldwewanttolivein.However,achievingtheseoutcomeswillrequireconsiderable

changethroughouttheeconomy.AnalysisbyJohanRockströmetal(2017)showsthat

from2020to2050,weneedtohalveglobalemissionseverydecadeifwearetoachieve

ourcommitmentstoslowingclimatechange.Thelevelofchangerequiredisdramatic

anddemanding.

ThisanalysisisexpandedintheIPCC’s2018report(Rogeljetal.2018),whichidentifies

thesectorsthatneedtochangemostdramaticallyinordertoreducecarbonemissions.

Specifically,theuseofenergybyindustry,transportandbuildingsisaverysignificant

driverofthechangethatisneeded.Muchoftheburdenofthischangefallsupon

incumbentbusinesses.Thesebusinessesarenotonlysignificantemittersofcarbon,but

alsoshapesystemsofsupplyandconsumption.Ifwearetoseeajusttransitiontoa

low-carboneconomy,businesswillbeasignificantplayer.

Aswellastheurgentneedtode-carbonise,companiesarealsoworkingonother

environmentalgoals(forexample,reducingresourceconsumptionandwaste)andon

socialgoals(forexampleworkingtowardshavingamorepositiveimpactonthe

communitiestheyserve).Thisbalancingofenvironmental,economicandsocial

outcomesoverthelongandshorttermisatthebasisofthedefinitionofsustainable

development(WorldCommissiononEnvironmentandDevelopment1987p.16).Inthis

thesis,Iwillbedescribingthisbalanceas‘corporatesustainability’.

2

Thisisacontestedconcept,andbothcorporate‘sustainability’andcorporate

‘responsibility’areideasthatcontinuetoevolve(Bansal&Song2017).Whilethenature

ofthesocialroleofbusinesshasbeendebatedhistorically(Margolis&Walsh2003),

thereisincreasingrecognitionoftheneedforcompaniestoactresponsibly–indeed,

corporatesocialresponsibilityhasgone‘mainstream’(Lyonetal.2018).However,

thereismuchmoretodotoshifttheemphasisfromafocusonsimplymakingthecase

forgreenbusinesstotakingasystemicapproachtocorporatesustainability(Bansal&

Song2017)andtoengagebusinessintacklingtheworld’sgrandchallenges(Georgeet

al.2016).Inthiscontext,thereisalsoaroleformanagementscholarstounderstand

howthesechangescanbeeffected(Eisenhardtetal.2016;Georgeetal.2016;Lyonetal.

2018).Thisdissertationseekstoaddressoneoftheproblemsbusinessesfaceinacting

inawaythatissociallyandenvironmentallysustainable.

1.2Theproblemthiscreates

Corporatesustainabilityisanenactedprocess.Becominganenvironmentally,socially

andeconomicallysustainableorganisationisnotamatterofsimplychangingapolicy–

peoplethroughouttheorganisationneedtodevelopnewhabitsintheirchoicesand

behaviour.Thedecisiontoactsustainablyisnotlimitedtoasinglepointinthe

organisation.Instead,decisionsinmanyfunctionsandatmanylevelsallcontributeto

theorganisation’ssocialandenvironmentalsustainability.AsHerbertSimonwrote:

‘Thetaskof“deciding”pervadestheentireadministrativeorganisationquiteasmuchas

thetaskof“doing”’(Simon1997p.1).

Companiesthereforefaceahighlycomplexproblemastheyworktowardscorporate

sustainability.First,theyaredealingwithachangethatisbothextremelyurgentand

presentsaglobalthreat(UNEP2018p.xiv).Second,thechangethatisneededis

pervasive:corporateactionswithsustainabilityimpactsarenotlimitedtotheworkof

individualexperts,butcanoccuranywhereinanorganisationwherethereisanimpact

onresourcesorstakeholders.Third,businessesworkingtobecomesustainableare

tryingtoeffectsystemicchangeinasystemcharacterisedbycomplexityand

uncertainty.Thismeansthattheknowledgerequiredtomakefullyinformeddecisions

maynotbeavailable.Wesimplycannotknowthecompleterangeofimpactsofsome

3

actions.Thiscombinationofurgency,uncertaintyandpervasivenessmeansthatthe

contextofcorporatesustainabilityisuniquelyproblematicfordecision-makers.

Withinthiscontext,thedecisionsthemselvesarecomplicatedbecausetheyare‘rifewith

tensions’(VanDerByl&Slawinski2015).Tensionisinevitable:itisencapsulatedinthe

definitionofsustainability,whichinvolvesmanagingeconomic,environmentaland

socialoutcomesforthelongandshortterm(WorldCommissiononEnvironmentand

Development1987p.16).Thisleadstotensionbetweenpublicandprivatevalue

(Haffar&Searcy2015),betweenthelongandshortterm(Slawinski&Bansal2015)and

betweendifferentethicalapproachestotheproblem(Rodeetal.2015).Thesetensions

appearindifferentpermutations(Haffar&Searcy2015),atseverallevelsinthe

organisation,andcanbemutuallyreinforcing(Slawinskietal.2017).Tensionsrelated

tosustainabilityalsoariseatthesystemlevel(Schad&Bansal,2018)whenthereare

multiple,conflictingdemandsfromtheexternalenvironment,whetherfromcustomers,

shareholders,regulatorsorotherstakeholders(Smith&Lewis2011).Howeverthey

becomesalientforexecutivesatamorespecificlevel(Schad&Bansal,2018),for

examplewhentheyneedtomakechoicesbetweenconflictingdemands.

Thusweseethattheworldneedstochange,andthatbusinessisanimportant

constituencyinthistransformation.However,businessesseekingtoactinawaythatis

sociallyandenvironmentallysustainableneedtomakeprofoundchangestothewayin

whichtheymakedecisions.Actingsustainablywillcreatetensionsfordecision-makers,

andtheyneedtofindwaystoresolvetheseinacontextwheretheavailableinformation

maynotbeadequateforthetask.

1.3Theobjectiveofthisresearch

Overthelastcoupleofdecadestherehasbeenaconsiderablebodyofresearchthat

makesthecaseforsustainablebusiness.However,therehasbeenratherlesswork

lookingathowbusinessesneedtoactdifferentlytobesociallyandenvironmentally

sustainable(Zolloetal.2013).Theobjectiveoftheresearchwasthereforetohelpus

betterunderstandhowbusinessescanadapttheirdecision-makingsystemsto

incorporatesocialandenvironmentalconsiderations.

4

Thisquestionsitsattheintersectionbetweentwoquitefragmentedfields:workon

decision-making,andworkoncorporatesustainability.Withintheresearchobjectives

thereareseveralpossiblefieldsofenquiry,andsoIconductedanextensiveliterature

reviewbeforefinalisingtheresearchquestion.ThisisdiscussedinChapter2.

Thisresearchiswarrantedfortwomainreasons.First,theproblemofchangingtheway

corporationsactisurgent(Rogeljetal.2018p.97)andyetthereisrelativelylittleclear

guidanceonhowtheyneedtochange(Zolloetal.2013).Thisleadstoablindspotfor

practitioners.Second,therehavebeencallsintheacademiccommunityforfurther

empiricalworkinthisfield(Epsteinetal.2015;VanDerByl&Slawinski2015;Haffar&

Searcy2015).Theobjectiveofthisworkistoaddressthislacunabytakingan‘engaged

scholarship’approach(VandeVen2007)toensurethattheempiricalapproachnotonly

addressesgapsintheacademicliterature,butalsomeetstheneedsofpractitioners.

1.4Howthisdocumentisorganised

Theorganisationofthisdissertationbroadlyreflectsthesequenceinwhichthework

wasconducted,startingwiththedevelopmentofaresearchquestion,andthen

presentingthemethodsusedandthefindingsfromthreeconnectedqualitativestudies,

andtheconclusionsfromtheresearch.Themainbodyoftheargumentistherefore

organisedinthefollowingchapters:

TheResearchQuestion

Chapter2situatestheresearchinthecontextoftheexistingliterature,whichis

problematizedtoidentifytheresearchquestion.

Methods

Chapter3outlinesthephilosophyandprinciplesunderlyingtheresearchmethod,and

thenexplainstheoverarchingstructureoftheresearchprocess.Theprojectconsisted

ofthree,connectedqualitativestudiesinformedbytheprinciplesofengaged

scholarship(VandeVen2007).Thefollowingthreechapterspresentthefindingsof

thesethreestudies.

5

Study1

Chapter4presentsthefindingsofthefirstofthethreestudies.Thedatainthischapter

isdrawnfromtheanalysisof45decisionscollectedininterviewswithexecutives.

Thesefindingswerecombinedwithasecondliteraturereviewinordertocreatethree

newconceptsforanalysingdecisionsthatincludesocialandenvironmentalaspects.

Study2

Chapter5presentsasinglecasestudythatwasdevelopedtoexploretherelationships

betweentheconceptsemerginginChapter4.Thisstudyshedslightontheway

decision-makinginorganisationscanchangeovertime,astheyrespondtopressuresfor

sustainability.

Study3

Chapter6introducesthefindingsfromthethirdstudy.Thisstudywasaseriesoffocus

groupswithseniorexecutiveswhosedecisionsinvolvedsocialorenvironmental

considerations.Thepurposeofthisstudywastotestandextendtheemergingfindings,

andtoensurethattheworkhadrelevanceforpracticeaswellastheory.

ContributionandConclusions

Inthefinalchapter,Idiscussthefindingsfromthiswork,assessingthelimitationsofthe

work,contributionstoknowledgeandimplicationsforpractice.Thischapteralso

includesasuggestedagendaforfutureresearch.

Inthisseriesofsteps,theresearchprogressesfromaninitialobjective–tounderstand

howbusinesscanadapttheirdecision-makingsystemstoincorporatesocialand

environmentalconsiderations–tothedevelopmentofaclearresearchquestionrooted

incurrentknowledge.Ithendevelopanswerstothisquestionthroughaseriesofthree

relatedempiricalstudies.Finally,thesefindingsarereviewedinthecontextofcurrent

knowledgetoshowboththecontributionstothiscorpusandthefuturedevelopments

suggestedbythiswork.

6

2:THERESEARCHQUESTION

2.1IntroductionThischapterexaminesthecurrentstateoftheliteratureondecision-makingandhow

thisrelatestothefieldofcorporatesustainability.Itakeasystematicapproachtothe

literatureonsustainabilityinbusinessdecision-makingtomapoutthekeythemesin

theliterature.Thesearethenproblematized(Alvesson&Sandberg2011)toidentifythe

researchquestionsandsituatetheminthecontextofexistingknowledge.Iwillreturn

totheliteratureagaininChapter4tocontextualisetheearlyempiricalfindingsfromthe

research.

Thischapterisorganisedinfiveparts.Itbeginswithanoutlineofthebroadschoolsof

thinkingondecision-makingthatemergedintwentieth-centuryacademia.Second,it

exploresthewaysinwhichthesebroadschoolsofthoughthavebeenadoptedinthe

sustainabilityliterature.Third,itshowswhythesustainabilitycontextisparticularly

challengingfordecision-makers.Thisisfollowedbyareviewoftheliterature,following

systematicprinciples(Tranfieldetal.2003)andamapthemajorthemesarisingfrom

this.Finally,Iproblematisethisliteraturetodrawouttheresearchquestionsthat

informthisthesis.

2.2Threemainschoolsofthoughtindecision-making

Decision-makingispartofthehumancondition,andproblemsofchoiceoccurinworks

bymanygreatphilosophers,includingPlato,AristotleandAquinas(Greco,Ehrgott,&

Figueira,2016p.4).Thereisalsoatraditionofanalysingdecisionsfromamathematical

pointofview,andintheseventeenthcenturyPascalandFermatbeganworkthatsowed

theseedsofourunderstandingofprobability(Hodgett,2013p.10).Giventhislong

history,Iintendonlytooutlinethemajorthemesintheliteraturethathaveinformed

currentworkondecision-makinginbusinesses.Ourcurrentthinkingondecision-

makingwassignificantlyshapedbyworkdevelopedfromthemiddleofthetwentieth

centuryonwards,whichreflectsthreefundamentallydifferentviewsofhuman

rationality.

7

ThefirstoftheseviewsisexemplifiedintheworkofgametheoristsVonNeumannand

Morgenstern(1947).Muchofthesubsequentdevelopmentofourideasondecision-

makinghasbeenaresponseorreactiontotheirdevelopmentofgametheory.First,Von

NeumannandMorgensterndevelopedanexpectedutilityfunctionthathasbecomethe

standardmethodtomodelrationalchoice(Hodgett,2013p.11).Thistheoryunderpins

severaltechniquesformakingcomplexdecisions–includingmulti-criteriadecision

analysis(Hodgett,2013p.13),butisbasedonanassumptionthatdecision-makershave

accesstothetimeandinformationthattheyneed,andwillactrationallytomaketheir

decisions.

However,thisviewofhumanrationalitywaschallengedbyHerbertSimon,a

contemporaryofVonNeumann,whenheproposedthetheoryofboundedrationality

(Simon,1945p.121).Simon’sviewwasthatdecisionmakers’abilitytoactrationally

waslimited–orbounded–bytheirorganisationalconditions,thatledtopartial

information(Simon,1945p.88),andhedevelopedthisintoabehaviouralmodelof

rationalchoice(Simon1955),exploringtherelationshipbetweenthedecision-maker

andenvironment.VonNeumannandMorgenstern’sassumptionsaboutrationality

werechallengedstillfurtherin1979byKahnemanandTverskywhodemonstratedthat

peopleviewriskasymmetrically,andthereforedonotconformtotheexpectednormsof

economicallyrationalbehaviour(Kahneman&Tversky1979).Thisledtoasubsequent

streamofworkanalysingcognitivebiasindecision-making.

Thisgivesthreebroadviewsonthenatureofdecision-making.First,onethatsuggests

thatdecision-makingissomethingthatcanbemodelledandsupportedmathematically.

Second,onethatsuggeststhatourdecision-makingisshapedbyanorganisational

contextthatfocusesourattentioninonedirectionandlimitsboththeavailabilityofdata

andthetimeavailabletomakechoices.Third,thereisanapproachthatfocusesonour

cognitivelimitationsandsuggeststhatonlybychangingthewaywethinkcanwe

changethewaywemakedecisions.Essentially,wecancharacterisetheseasanalytical,

organisationalandcognitiveapproachestodecision-making.

Theseleadtoquitedifferentapproachestodecision-support.Whiletheanalytical

schoolhasproducedarangeofdifferenttoolstomanagethecomplexityofdecisions,

workbyGerdGigerenzer(forexample:Gigerenzer&Goldstein,1996),buildingonthe

8

behaviouralviewofdecision-making,suggeststhatsomedecisionscanbesimplifiedto

heuristics,andthatthesecanbeusedforeffectiveorganisationaldecision-making

(Bingham&Eisenhardt2011).Otheracademics–mostnotablyRichardThaler(Thaler

&Sundstein2008)–havedevelopedapproachestodecision-supportthatarebasedon

KahnemanandTversky’srecognitionofcognitivelimitation.Theypointoutthatby

workingwiththesebiases,wecancreateenvironmentsthatencouragepeopletomake

particulardecisions.

Thus,weseethattheliteratureondecision-makingissomewhatfragmented.Workhas

beendrivenbymathematicians,economistsandpsychologists,andisrootedindiffering

viewsofhumanrationality.Thesefracturespersistintheliteratureaboutstrategic

decision-making(Shepherd&Rudd2014).Buthowaretheseapproachesusedinthe

contextofbusinessdecisionsinvolvingsustainability?

2.3Sustainabilityinbusinessdecision-making:mappingtheliterature.

Tounderstandthisproblembetter,Iundertookaliteraturereviewinformedbythe

principlesofsystematicreview(Tranfieldetal.2003).Systematicreviewhasits

originsinthefieldofmedicine(Kitchenhametal.2009)andwasdevelopedasawayto

compileevidencefrommultiplestudies.Sincethen,ithasbeenadaptedfordifferent

fields,includingsoftwareengineering(Kitchenhametal.2009)socialsciencesand

publicpolicy(Tranfieldetal.2003).However,theobjectivesofthesystematic

approachvarybyfield:inmedicineandsoftwareengineering,theintentistocreatean

evidencebaseforpractitioners,drawingonasynthesisofscientificevidence;by

contrast,Tranfieldetal(2003)intheirworkonapplyingsystematicliteraturereviewto

management,observethatsomeofthenorms(suchasontologicalorepistemological

consistency)thatapplyinotherfieldsdonotapplytomanagement,andsowhilea

systematicapproachtoliteraturecanbehelpful,itisunlikelytoproducethetypeof

evidencebasethatisavailableinotherfields.Becausedecision-makingisamulti-

disciplinaryfield,Iexpectedtofindthattheliteraturewouldbequitefragmented,and

thattherewouldbeepistemologicalinconsistenciesinthefield.Ithereforedecidedto

usethesystematicapproachonlytomaptheliteratureanduncoverthemainthemesor

perspectives,ratherthantocompareindividualstudies.Ihavethereforeadopteda

systematicapproachtothesearchandmappingofexistingworkinordertodevelopa

9

researchquestion,ratherthanusingthisasasteptoaccumulateevidencefora

particularfinding.

Thisworkcomprisedthreesteps.ThefirststepwasasearchintheThomsonReuters

WebofSciencedatabaseforallmaterialspublishedinEnglishbeforetheendof2018

usingthestring:businessANDdecision-makingANDsustainab*.Thisproducedalistof

820articles(includingconferencepapers,journalarticlesandbookchapters).Forthe

secondstep,Ireviewedthetitlesandabstractsofthesearticlestoremovethosethat

were:

• Notfocusedondecision-making(eg.Articlesaboutgenderdifferenceinwhich

differencesindecision-makingwereaverysmallpartofthediscussion)

• Notfocusedonsocialorenvironmentalsustainability(eg.Articlesthatwere

assessingwhetherasectorcouldcontinueinthelongterm)

• Notfocusedontheinternalworkingsofanorganisation(eg.Articlesabout

consumerdecision-making)

• Focusedonthegreensupplychain(thisisalarge,andgrowingbodyof

specialisedliterature)

• Focusedonveryspecificsituationssuchashealthcare,communityinterventions

oragriculture,thatmightnotbegeneralizabletobusinesssettings

• Focusedonmulti-organisationdecision-making(eg.Managementofcommon

resourcessuchaswatersupplies)

• Focusedoneducationalsettings(eg.Provisionofbettersustainabilityeducation

forMBAstudents)

• Focusedonscienceasatopic(eg.Howsciencecanbeusedtoinformpolicy

decisions).

Thisfilteringleftasetof234articlestoreview.

Becausesomewritersuse‘sustainability’and‘corporatesocialresponsibility’moreor

lessinterchangeably,Iconductedasecondsearchusingthestring

‘organisationANDdecisionmakingAND(sustainab*ORcorporatesocial

responsibility)’intheWebofScience’sbusinessandmanagementdatabases.This

searchproduced583articles.Ireadthetitles(andwherenecessarytheabstracts)to

10

applythesamefilteringcriteria,creatingalistof107articles.Ithenmergedthetwo

lists,removinganyoverlapstobuildafinalsetof325documents.

Thethirdstepwastoreadandcategorisethearticles.Becauseofthebroadnatureof

theenquiry,thearticleswereverydiverseandsoIgroupedthearticlesthematicallyinto

fourmaingroups.Oneofthesegroupswasabouttheoverallcontextforbusinessand

sustainability;theremainingthreebroadlyreflectedthethreeschoolsofthought

outlinedabove–therewasagroupaboutinformationandanalysis;agroupabout

managerialcognition;andagroupaboutorganisation.Theoveralldistributionofthe

articlesisshowninTable1below:

Table1:Numberofarticlescategorisedbytheme

Theme Numberofarticles %oftotalSustainabilitycontext 51 16Informationandanalysis 187 58Managerialcognition 29 9Organisation 46 14Other(forexample,specificindustries)

12 4

Theliteratureisstrikinglyfragmented.Thearticleswerespreadacross191journals,

conferenceproceedingsorbooks,ofwhichonly14includedmorethanthreearticles.

Ofthegeneralistmanagementjournalsthatareoftenusedasthebasisforaliterature

review(forexampleVanDerByl&Slawinski2015),onlyone–theAcademyof

ManagementReview–includedmorethantwoarticlesaboutsustainabilityand

decision-making.Themorespecialisedjournals,suchasJournalofCleanerProduction,

JournalofBusinessEthicsandSustainabilityweremostprolific,buteventheyaccounted

collectivelyforonly25%ofthearticles.151Journalsincludedonlyonerelevantarticle.

ThebibliometricsareshowninTable2:

Table2:Thematicanalysisofarticlesbypublication

JournalContext

CognitionOrganisation

Information

ToolsOther

TotalJournalofCleanerProduction

73

213

34JournalofBusinessEthics

611

62

2

27Sustainability

21

21

141

21InternationalJournalofLifecycleAssessm

ent

7

7

Managem

entDecision1

2

11

5

BusinessStrategyandtheEnvironm

ent

1

21

4

OrganisationandEnvironment

1

21

4ResourcesConservationandRecycling

1

1

2

4

SustainabilityAccountingManagem

entandPolicyJournal1

1

2

4

AcademyofM

anagementReview

2

1

3

BusinessEthics-AEuropeanReview

2

1

3EcologicalEconom

ics

11

13

EuropeanJournalofOperationalResearch

1

2

3

GroupDecisionandNegotiation

1

11

3

11

14

Journalshadaneditorialslanteithertowardsthe‘human’aspectsofdecision-making

(thecontext,cognitionandorganisationarticles),orthe‘technical’aspects(information

andanalysis).ThissuggeststhatthedistinctionmadebyBansal&Song(2017)

betweenworkon‘responsibility’,whichisbasedonanormativeormoralimperative,

andworkon‘sustainability’,basedonanunderstandingofecologicalsystems,persists,

with‘responsibility’representedinthejournalsemphasisingcontext,cognitionand

organisation,and‘sustainability’representedinthemoretechnicallyfocusedjournals.

Iusedthisinitialclassificationasabasistoreviewandproblematizetheliteratureto

identifymyresearchquestion,expandingthesearchusinga‘snowballing’approach

whennecessary.Thisanalysisformsthebasisfortherestofthischapter.

2.4Thesustainabilitycontext

Businessesthataspiretoworkinawaythatissociallyandenvironmentallyresponsible

faceaparticularorganisationalchallenge,specifically,howtocopewiththeadditional

complexitythispresents(Pirson&Turnbull2018).Itisimportanttounderstandhow

thechoicetoactinawaythatissociallyandenvironmentallysustainablecanmake

decision-makingmorecomplicated,asindividuals–andindeedorganisations–are

workingwithmultipleobjectives(Epsteinetal.2015;Mitchelletal.2016)thatmaybe

intensionwitheachother.ThisisdiscussedbrieflyintheIntroduction(Section1.2,

above).

Thesetensionsareoftennestedwithinabroaderquestionaboutthepurposeofthefirm

(Dyck&Greidanus2017;Bentoetal.2017).Theycanbegeneralisedasatension

betweenprivatevalueandsharedvalue(Haffar&Searcy2015;Porter&Kramer2011),

essentiallycontrastingtheimmediateneedsofthecompanywiththelong-termneedsof

stakeholders,whichcanincludeotherspeciesorfuturegenerations.Thistension

betweentheexternalenvironmentandthecompany’svaluecreationsystemcancreate

aparadox–‘apersistentcontradictionbetweenindependentelements’(Schadetal.

2016)–forthecompany.Thiscanbeachallengetocompaniesseekingtoactmore

sustainablyasitcreatesaparadoxattheheartoftheiroperations.

15

Thisisparticularlywellillustratedindecision-making:eachdecisionpresentsspecific

tensions,butthesearelocatedinanorganisationalcontextthatmaypresentalargerset

ofenduringtensions(Smith2014).Thesetensionsmaybelatent,orunseenuntila

choiceneedstobemade(Smith&Lewis2011;Bansaletal.2018).However,atthis

point,theycomplicatedecision-makinginfourdistinctways.First,decision-makers

findthattheymayneedtomanage

conflictingdemandsfromtheexternalenvironment,whetherfromcustomers,

shareholders,regulatorsorotherstakeholders(Smith&Lewis2011).Second,they

needtofindwaystobalancethelong-termandtheshort-termwhichmaybeintension

(Bansal&Desjardine2014).Thesetwofactorsinteracttocreateathirdproblemof

complexity(Pirson&Turnbull2018).Finally,somesustainability-relateddecisions

havethecharacteristicsofwickedproblems(Rittel&Webber1973)sothattheyare

characterisedbyhighlevelsofambiguity.

Notonlydodecision-makersfindthatthesefourfactorsmaketheirdecisions

intrinsicallymorecomplex,theymayfindthatthereisatensionbetweenthedemands

oftheexternalenvironmentandthedominantorganisationallogic,the‘practices,

assumptions,valuesandbeliefsthatshapecognitionandbehaviour’(Besharov&Smith

2014)usedtomakechoicesintheorganisation.Therehasbeenlittleempiricalresearch

intohowexecutivesactuallyexperiencetheseclustersoftensions(Sheepetal.2017)

andtherehavebeencallsformoreempiricalresearchtounderstandhowexecutives

resolvethetensionsarisingfromincorporatingsustainabilityindecision-making

(Epstein&Widener2011;Haffar&Searcy2015;VanDerByl&Slawinski2015).

Therearedivisionsintheliteratureaboutthewaythesetensionscanbehandled.The

threemaintheoreticalperspectives–analytical,cognitiveandorganisational–that

dominatetheacademicworkondecision-makingpersist.HerbertSimon(1997p.56)

notedthatdecisionswerealways‘acombinationoffactsandjudgement’.Thethree

literaturesIwillreviewapproachthisindifferentways:theliteratureonanalysisand

informationfocusesonthefacts;literatureoncognitionfocusesontheprocesses

underlyingjudgement;andtheworkonorganisationfocusesonthebroadercontext

withinwhichtheseinteract.

16

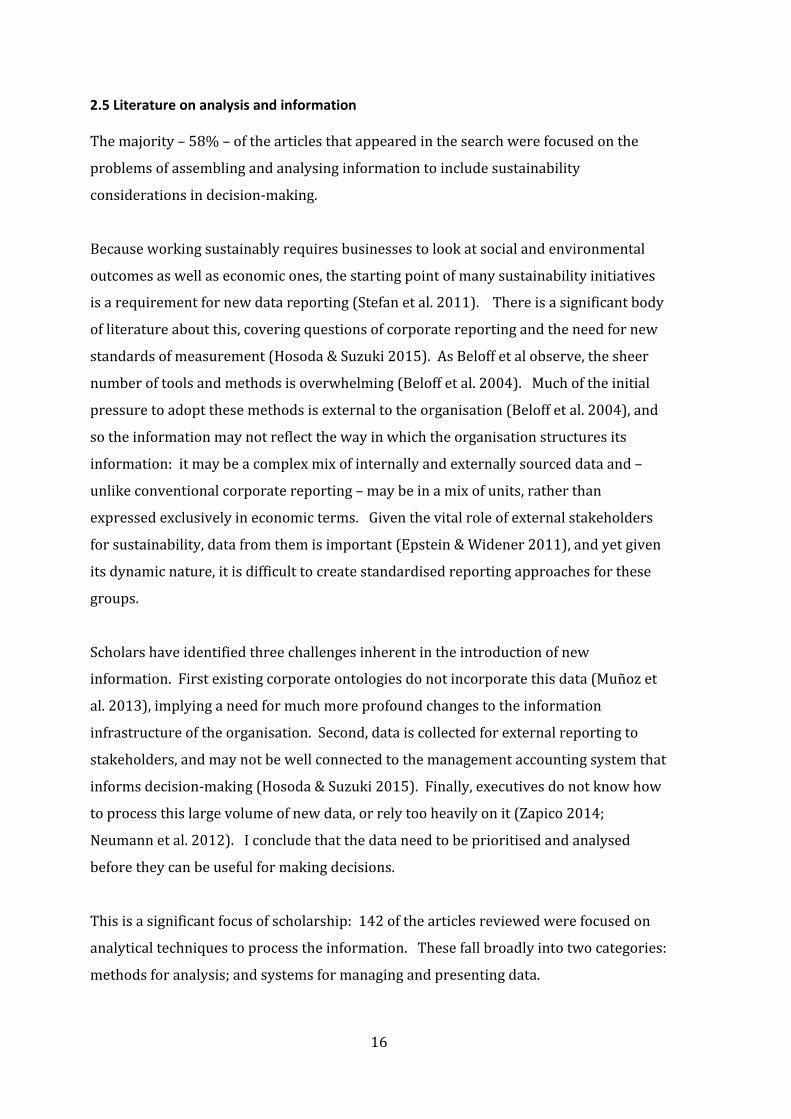

2.5LiteratureonanalysisandinformationThemajority–58%–ofthearticlesthatappearedinthesearchwerefocusedonthe

problemsofassemblingandanalysinginformationtoincludesustainability

considerationsindecision-making.

Becauseworkingsustainablyrequiresbusinessestolookatsocialandenvironmental

outcomesaswellaseconomicones,thestartingpointofmanysustainabilityinitiatives

isarequirementfornewdatareporting(Stefanetal.2011).Thereisasignificantbody

ofliteratureaboutthis,coveringquestionsofcorporatereportingandtheneedfornew

standardsofmeasurement(Hosoda&Suzuki2015).AsBeloffetalobserve,thesheer

numberoftoolsandmethodsisoverwhelming(Beloffetal.2004).Muchoftheinitial

pressuretoadoptthesemethodsisexternaltotheorganisation(Beloffetal.2004),and

sotheinformationmaynotreflectthewayinwhichtheorganisationstructuresits

information:itmaybeacomplexmixofinternallyandexternallysourceddataand–

unlikeconventionalcorporatereporting–maybeinamixofunits,ratherthan

expressedexclusivelyineconomicterms.Giventhevitalroleofexternalstakeholders

forsustainability,datafromthemisimportant(Epstein&Widener2011),andyetgiven

itsdynamicnature,itisdifficulttocreatestandardisedreportingapproachesforthese

groups.

Scholarshaveidentifiedthreechallengesinherentintheintroductionofnew

information.Firstexistingcorporateontologiesdonotincorporatethisdata(Muñozet

al.2013),implyinganeedformuchmoreprofoundchangestotheinformation

infrastructureoftheorganisation.Second,dataiscollectedforexternalreportingto

stakeholders,andmaynotbewellconnectedtothemanagementaccountingsystemthat

informsdecision-making(Hosoda&Suzuki2015).Finally,executivesdonotknowhow

toprocessthislargevolumeofnewdata,orrelytooheavilyonit(Zapico2014;

Neumannetal.2012).Iconcludethatthedataneedtobeprioritisedandanalysed

beforetheycanbeusefulformakingdecisions.

Thisisasignificantfocusofscholarship:142ofthearticlesreviewedwerefocusedon

analyticaltechniquestoprocesstheinformation.Thesefallbroadlyintotwocategories:

methodsforanalysis;andsystemsformanagingandpresentingdata.

17

Thearticlesaboutanalyticalmethodsfallbroadlyintofourcategories,eachofwhich

addressaspecificprobleminherentinthesustainabilitycontext.Lifecycleanalysisis

anapproachdevelopedtoreducetheproblemofdecision-methodsthatfavourthe

short-term(suchasdiscountedcashflowmethods)bycomparingtheimpactofprojects

orproductsovertheirentirelifecycle.Thiswasthefocusof20ofthearticles.The

secondcategorywasagroupofanalyticmethodsthatenabletheevaluationofdecisions

basedonmultipledifferentcriteria,andwasdescribedin37articles.Thethird

categorywasagroupofanalyticmethodsthathelpanalysedecisionsunderconditions

ofuncertainty,forexamplebyanalysingoptions,andtherewere12articlesfocusedon

theseapproaches.Finally,therewere11articlesthatdescribedmodelsorsystems

dynamicsapproachestoexploringthecomplexityindecisions.Broadly,theanalytical

methodseachaddressparticularproblemsposedbythetensionsimplicitinintroducing

sustainabilityconsiderationstobusinessdecision-making,thus:

Table3:Howanalyticmethodsmapontotensionscreatedbythesustainabilitycontext

Problem ApproachTensionbetweentheshortandlong-termindecision-making

Lifecycleanalysisallowsdecision-makerstoexaminethecompleteimpactofadecision

Tensionbetweeneconomic/environmental/socialoutcomes(orcombinationsofthese

Multi-criteriadecisionanalysis,analytichierarchyprocessandTOPSISallenabledecision-makerstoexaminemultiplecriteria

Highlevelsofuncertaintyaboutinputvariablesandoutcomes

Greydecision-making,fuzzylogicanddataenvelopmentallallowdecision-makerstoanalysetherangeofoutcomesofadecision.

Complexityofrelationshipsbetweensystemelements

Systemdynamicsandmodelling.

Theproblemtheseanalyticalmethodspresentisthatmanydecisionshaveallofthese

tensions,andsothetoolswouldneedtobeusedinconjunctionwitheachother.Several

authorshavedescribedsituationsusingcombinationsofanalyticalmethods,asmore

thanoneisrequiredtosolvethefullsetofproblemsposedbyagivendecision

(Hoogmartensetal.2014;Bakshi2011).

Thishasledtothedevelopmentofworkonbuildingsustainabilityinformationinto

enterprise-levelsystems.Chofrehetal,inaliteraturereviewoftheworkonsustainable

18

enterpriseresourceplanning(Chofrehetal.2014)makethecaseforembedding

sustainabilityintobusinesssystems.However,theadditionofextrainformation

complicatestheunderlyingmodelandmayendupconfusingusers(Oertwigetal.2015),

andtherearesignificantchallengesinimplementingthesesystems(McIntoshetal.

2011).Thereisstillafocusinenterprise-levelsystemsondata,ratherthanthe

decisionstowhichthesewillbeapplied(Stefanetal.2011).

Inmanyorganisations,managersalreadyreceivelargequantitiesofinformationeven

withoutadditionalfactsrelatedtosustainability,leadingtotheriskofcognitive

overload(Neumannetal.2012).Itisthereforehelpfultohavepresentationaltoolsto

helpsummariseandsynthesisethecoredata,andensurethatmanagementattentionis

focusedonthemostsalientfacts.Thewayinwhichmanagersreceivethedataneedsto

reflecttheorganisationalontologyandwayinwhichthecompanysignalswhatis

important.Interestingly,thereisrelativelylittleaboutthisintheacademicliterature,

andalmostallofwhathasbeenwrittenisaboutversionsofonetool:theBalanced

Scorecard,mentionedinsevenofthearticles.PistoniandSongini(2016)pointoutthat

theBalancedScorecardhasbeenproposedasavehicleforsignallingthecompany’s

prioritiesandthatthereareseveraloptionsforprovidingthedata,rangingfroman

entirelyseparatescorecardforsustainabilityquestionstothecompleteintegrationof

sustainabilityintothebusinessscorecard.

Despitetheextentofthisliteratureanditsprominenceinacademicworkondecision-

makingforsustainability,ithassomelimitations.First,theseapproachesallseekto

solveproblemswithintheexistingbusinesssystem(Zapico2014).Thismeansthat

tensionsarisingfromthefirm’sfundamentalvaluecreationmethodarenotaddressed.

Rather,thesymptomatictensions–differencesinstakeholderviews,forexample–are

managedeitherthroughindividualanalyticalapproachesdescribedabove,orthrough

combinationsofapproaches.Theseapproachestendtobequiteresource-intensive,

andthereforeusedfordecisionsthatareexceptionalintheircomplexity(Arvaietal.

2012).Whentheyaresuccessfullyembeddedincorporateinformationsystemsthey

alsobecomerelativelyinflexible(Brynjarsdottiretal.2012).Theythereforemaynotbe

appropriatefortheorganisationalrealityofverydistributed,rapiddecision-makingthat

needstoresponddynamicallytostakeholders.Finally,theyplacesignificantcognitive

19

demandsonmanagers(Neumannetal.2012):Zapico(2014)suggeststhatthisleadsto

ablinddependenceondatathatcanleadtounwittingshort-termism.

Thus,whileimproveddatamayhelppeoplemakebetter-informeddecisions,thereisno

evidencethatitfundamentallychangespeople’swaysofmanagingthetensionsinherent

insustainability.Whilethebalancedscorecardiseffectiveformanagingmultiple

objectives,itreinforcestheFirm’sexistingstrategyandsodoesnothelpexecutives

addressproblemsthattheyarenotalreadythinkingabout(Hahn&Figge2018).People

aretherefore‘lockedinto’aparticularwayofseeingthesocialandenvironmentalissues

facingabusiness,andrespondingaccordingly.Thepresentationofdatainabalanced

scorecarddoesnotseemtochangeethicalperspectives(Wynder&Dunbar2016).This

questionofhowpeoplethinkisanimportantpartofthedecision-makingprocess,and

hasbeenextensivelydiscussedinaseparatebodyofliteratureonmanagerialcognition.

2.6Sustainabilityandmanagerialcognition

SinceHambrickandMasondevelopedtheupperechelonstheoryinordertodescribe

thewayinwhichthecharacteristicsandattitudesofseniormanagersshapecorporate

decision-making(Hambrick&Mason1984),scholarshavebeeninterestedintheway

thatsociallyandenvironmentallyresponsiblebehaviourinbusinessesoriginatesinthe

ethicalorientationofindividualleaders(Yinetal.2016).Ifsustainabilityisamoral

issue(Margolis&Walsh2003;Mazutis&Eckardt2017),thenitmakessenseto

understandwhetherpeopleactmorally.However,historically,therehasbeen

relativelylittleempiricalexaminationofthisphenomenon(Aguinis&Glavas2012).

Therehasthereforebeenatrendinrecentyearstowardsexplorationofthesemicro-

foundationsofsustainability,focusedonmanagerialcognition.

Researchonmanagerialcognitionhasitsrootsintheproblemofuncertaintyinthe

externalenvironment(Kaplan2011)andincorporatesboththeknowledgeandthe

valuesandbeliefsofdecision-makers(Hambrick&Mason1984).Becausepeopleare

notabletoknoweverythingaboutasituation(Simon,1997p.78),theydevelop

cognitiveframes,definedas‘awell-learnedsetofmentalassociationsthatexcludes

someinterpretationsofenvironmentalstimuliandreinforcesothers’(Porac&Rosa

1996).Theseframeshelpdirectattentiontoparticularissuesinasituation(Kaplan&

Tripsas2008),effectivelyactingasfiltersindecision-making.Peoplehavearepertoire

20

offrames,or‘schemataofinterpretation’(Goffman1974p.21),buttheytendtobefairly

stable(Porac&Rosa1996),changinginresponsetouncertaintyandexternalpressure

(Kaplan2008).

Giventheimportanceofthesecognitiveframesforsensemaking,thereisagrowing

bodyofscholarshipexploringthewaysinwhichtheyenableexecutivestomakesenseof

thetensionsinherentinthecontextofsustainablebusiness.Hahnetalsuggestthat

therearetwodominantcognitiveframesamongexecutives,andcharacterisetheseasa

‘businesscaseframe’anda‘paradoxframe’(Hahn,Preuss,Pinkse&Figge,2014).

Cognitiveframesarevitalindecision-makingastheyshapeboththeinterpretationof

theproblemandthechoiceofaction(Kaplan2008;Grewatsch&Kleindienst2018),and

Hahnetal’sworksuggeststhatexecutiveswiththesetwodifferentframeswillbehave

verydifferentlybothintheirwayofseeingthetensionsincorporatesustainabilityand

intheirresponsestothem(Hahnetal.2014).

Inthefirstoftheseframes–the‘BusinessCase’frame–Hahnetalproposethat

managersarefocusingonenvironmentalandsocialactionsthatwillsupporteconomic

outcomes(forexample,improvingresourceefficiencyisbeneficialtotheenvironment

andreducescosts).Thisenablesthemtomakerelativelystraightforwarddecisions:

somethingeitherworkseconomically,oritdoesnot.Theycontrastthiswitha‘Paradox

frame’,inwhichtheexecutiveshaveamorecomplexandambivalentattitudetowards

thetensionsinsustainability.Thisleadsthemtoconsidermorecomprehensive

responsestotensions,butatthesametimetheyaremoreawareoftherisksassociated

withthese(Hahnetal.2014).Thisisnotdissimilartothetwoworldviews(mechanic

andorganic)proposedbyIms&Jakobsen(2011).Thisconceptualisationhasbeen

influential(todate,theoriginalarticlebyHahnet.al.hasbeencited110times),buthas

notsofarbeentestedempirically.

Thedistinctionbetweenthesetwoframingsunderpinsafractureintheliterature:while

theanalyticalliteraturereviewedinsection2.5isframedintermsofabusinesscase,

thereisalsoabodyofworkwithitsrootsinthecorporatesocialresponsibilityliterature

thathasamuchdeeperfocusonethical,values-basedperspectives(Bansal&Song

2017),whichreflectsthecomplexitiessuggestedbyHahnetal’s‘Paradoxframe’.The

tensionbetweenthesetwoframescanbeusedproductively–forexampletomanage

21

biasingroupdecision-making(Mazutis&Eckardt2017;Hahn&Aragón-Correa2015)

andsoarriveatbettersolutions.However,itcanalsobeacauseofstressforindividuals

whentheircognitiveframeclasheswiththedominantframeintheirorganisation(Zollo

etal.2013).

Whilecognitiveframesareeffectiveatdirectingattention,theycanalsocreateblind

spots–importantissuesthatdecision-makersfailtoattendtobecausetheyfalloutside

thecognitiveframe.Thiscanbebecausetheissueis‘toolarge’–forexamplesystemic

problemssuchasclimatechange–or‘toosmall’tobeofinteresttothecorporation

(Bansaletal.2018).Failuretoattendtosustainabilitycanalsobecausedbycognitive

biases(Mazutis&Eckardt2017),andbyhabitsofmindandactionthatarecreatedby

‘organisationalscripts’(Gioia1992).Thesescriptsoffernotonlyacognitiveframing,

butanestablishedpatternofbehaviour(Gioia1992).Theyhavethebenefitofreducing

thecognitivecostofdecision-making,andmayenablenon-specialiststomakedecisions,

whichmeanstheyarehelpfulinsituationswheresustainabilityissuesarepervasivein

theorganisation.Thedisadvantageisthattheygiveconfidencewhereitmaynotbe

warranted(Gioia1992),andmayallowdecision-makerstoglossoverinconvenient

truths.

Theresultofthisisthatmanyorganisationaldecisionsare‘scripted’–thatistosaythey

followparticularcognitivepatternsandsequencesofbehaviourrangingfromthevery

sophisticated(‘whenwehaveabusinesscaseforaninvestmentgivingapositivenet

presentvalue,wereferittotheinvestmentcommitteeforapproval’)tothetrivial

(‘whenIleavetheofficeIswitchthelightsout’).Thesepatternsareoftenefficientand

reducethecognitiveloadfordecision-makers,buttheyarenotnecessarilywelladapted

tohandlingthecomplexityofthetensionsraisedbysustainability.These‘scripts’or

schemasareembeddedintheorganisation,sothisraisesthequestion:howdo

organisationalsystemsshapedecision-makingroutines?

22

2.7SustainabilityandorganisationThereisanextensivebodyofworkaboutorganisationalcontextandthewayit

influencescorporateapproachestosustainability.Scholarsrecognisethatthebroader

contextisimportantinshapingdecision-making(Shepherd&Rudd2014;Deanetal.

1991).Organisationsexertinfluence–eitherthroughformalprocesses,habitsand

routines–onthewayinwhichpeopleunderstanddecisionsevenbeforetheymake

them.Workonethicaldecision-makingidentifiesorganisationalcontextasadominant

forceindecision-making(Blome&Paulraj2013;Lietal.2018),overridingthe

individualpreferencesofmanagers(Chenetal.1997).AsLülfsandHahn(2014)write:

‘Thecreationofanorganizationalculturefosteringsustainabilityorientationseemsto

bemoreimportantthanformalexpressionsofcorporatesustainability(Howard-

Grenville,2006;Linnenluecke&Griffiths,2010;Tudoretal.,2008).’(Lülfs&Hahn,2014

p.52)How,then,isthisachieved?

Althoughmanyissuesareidentifiedintheliteratureasinfluencesindecision-making,

noneofthearticlesreviewedofferedacomprehensivemodelconnectingtheseconcepts

toshowtheorganisationalinfluencesondecision-makers.Instead,scholarshave

focusedonspecificissuessuchastheroleofsub-cultures(Howard-Grenville2006),the

creationoforganisationalclimate(Ardichvilietal.2009)ortheimpactofformal

systems(Ford&Richardson1994).Therewasaparticularlylargebodyofliterature

aboutthecharacteristicsofindividualleaders(Forexample:Aguinis&Glavas,2012;

Ardichvilietal.,2009;Blome&Paulraj,2013;Stubbs&Cocklin,2008),andageneral

tendencytoemphasisethe‘softsystems’,suchascultureandethicalclimate,ratherthan

themoreformalprocessesoftheorganisation,althoughthesedoappearinliterature

reviews(Ford&Richardson1994;Verbosetal.2007;Nawaz&Koç2018).AsSchrettle

etalwrite:‘Tothebestofourknowledge,thereisnodescriptivemodel,whichsupports

decision-makingoffirmsfacingasustainabilitychallengebylinkingallrelevant

dimensionsinatransparentway’(Schrettleetal.2014p.74).

Thisreadingoftheliteratureonorganisationgeneratedalistof107factorsthatcould

influencedecision-processes.ThesourcesforthesearelistedinAppendix1.These

107conceptsoperateatdifferentorganisationallevels:somedescribethebehaviourof

individuals(forexample:moralresponsibility);othersoperateatthelevelofthe

organisation,ororganisationalunit(forexample:culture);somedescribethe

23

relationshipbetweentheinternalandexternalaspectsofthefirm(forexample:theory

ofthefirm).Ithereforeorganisedthemintoabroadconceptualframeworkdrawingon

thefourcontextsidentifiedbyDean,SharfmanandFordintheirreviewoftheliterature

onstrategicdecision-making(Deanetal.1991p.89).Deanetaldidnotelaborateon

themoredetailedaspectsofthesecontexts(forexample,thespecificorganisational

elementsinfluencingdecisions).Ithereforeadaptedtheiroriginalframeworkandused

thisasabasisformappingthefactorsidentifiedinthesustainabilityliterature.Imade

twoalterationstothismapping:first,Deanetalputthedecisionprocessandproblemat

twodifferentorganisationallevels(onthegroundsthattheprocessisaninteraction

betweenthedecision-makerandtheproblem).Whilethismaybethecaseforstrategic

decisions,theuseoforganisationalscriptsforsomesustainability-relateddecisions

meansthattheprocessismorecloselyrelatedtotheproblemthantothedecision-

maker.Ihavethereforegroupedthedecisionproblemandprocessinthesamelayer.

ThesecondchangethatIproposeinthisframeworkisthatIhavechangedDeanetal’s

‘team’to‘decision-maker’,assomesustainability-relateddecisionsaremadeby

individualsratherthangroups.Thismappingisthusadevelopmentoftheiroriginal

proposedframeworkandisshowninFigure1.

24

Figure1:Contextualfactorsinfluencingtheinclusionofsustainabilityindecision-making

Thissynopticmodelshowsthattherearemanypossibleinfluencesondecision-makers.

Manyofthemunderpintheorganisationallogicthatshapesbehaviourandcognition

(Besharov&Smith2014).However,thereisnoindicationoftherelativesignificanceof

these,northerelationshipsbetweenthesefactorstoshowhowbusinessesmightshape

theirorganisationstobettermanagethechallengesofactingsustainably.Iwilldevelop

thisideafurtherinChapter4.

2.8Problematisingtheliterature

ThemappingoftheliteratureinTable2showsthatthereisnotacoherentliterature

abouthowcompaniesincorporatesocialandenvironmentalconsiderationsintotheir

decision-making.Itisclearthatthereisnotsomuchagapintheliteratureasaseries

ofproblemstobesolved(Alvesson&Sandberg2011).Thesewillinformtheresearch

question.

Thefirstproblemintheliteratureisanapparentdisconnectbetweenthecomplex,

systemicproblemofincorporatingsocialandenvironmentalcriteriaintodecision-

Environment

Decisionproper/es

Decisionprocess

Organisa/on

Decision-maker

Environment/BusinessCharacteris3cs• TheoryoftheFirm • Ownershipstructure/Shareholders• BoardaAen/on/governance• Compe//veintensity/

Compe//veness • Regulatoryenvironment• Geopoli/calenvironment• Size • History/pathdependency• Munificence• Materialityofsustainability • Purpose,MissionandVision• Customerandmarketdemand• NGOinterest• Corporategoals• Corporateiden/ty

Organisa3on• Accountability• Accoun/ngpolicies,sustainability

reportsandtriple-boAomline• Problem-solvingapproach• AOtudesandbeliefs• Cultureandclimate• Codesofconduct,corporatepolicyand

rules• Complexity• Communica/on• Controlsystem• Co-opera/onandcollabora/on• Conflict-resolu/on• Corporateaffairs• Culture• Organisa/ondesignandstructure• Empowerment• Environmentalmanagementsystem• Ethicalclimate,cultureandnorms• Heroesandrolemodels• Historicalantecedents• HRprocesses• Incen/vesandrewards• Inclusionandindependence• InfluenceofexternalgroupsOrganisa3on• Instrumentalism Opera/ngprocedures• Jobdesign Organisa/onalepistemology• Knowledgemanagement Rou/nesandscripts• Language Peergroups• Leadership Performancemanagement• Organisa/onallearning Managerialinterpreta/onsofCSR• Leadership Processes• Long-termperspec/ve Removalofemo/onalcontent• Myths Rituals• Normsandvalues Stories• Stakeholderrela/ons Socialisa/on• Sub-cultures Sustainabilitymindset• Tradi/ons CommitmenttoCSR• Trainingandcapabili/es

DecisionMakers• Abilitytoseekassistance• AOtudesandbeliefs• Timeperspec/ve• Decisionrights• Desires• Iden/fica/onwiththeorganisa/on• FocusofaAen/onandpriori/es• Habits• Informa/on• Inten/on,commitmentandvalues• Independence/isola/on• Moralcodeandmaturity• Perceivedlevelofcontrol• Seniority• Skill,capabili/esandtraining• Socialapproval• Stressandworkload• Careerorienta/on

Decisioncharacteris3cs• Decisioncriteria• Dynamicsofprocess• Par/cipa/oninprocess• Complexity• Ambiguity• Inter-temporality• Varietyofstakeholders

25

making(Pirson&Turnbull2018)andthetypeofsolutionsproposed.Manyarticles

describesingleapproachestoamulti-facetedproblem(seeTable3,above),andthe

fragmentationoftheliteraturehaslimitedtheoreticaldevelopment(Shepherd&Rudd

2014).Whatisneededisthereforeamoreintegrativeapproachtothetopictomake

connectionsbetweentheanalytical,cognitiveandorganisationalliteratures.

Thenaturalstartingpointfortheseconnectionswouldbearesearchquestionstemming

fromtheorganisationalliterature.Theattentionbasedviewofthefirmsuggeststhat

theorganisationshapesandinfluenceswaysofseeinginformationandthinkingaboutit

(Ocasio1997).Ithereforetaketheorganisationalliteratureasmystartingpoint.I

interprettheorganisationbroadlytoencompassarangeofformal,behaviouraland

socialfactorsthatshapetheorganisationallogic,theinformationandthecognitive

processofthedecision-maker.

Thesecondproblemintheliteratureisatrade-offbetweentheoreticalcomplexityand

empiricism.Thearticlesdescribingthecomplex,paradoxicalnatureofsustainability

(forexample:Hahnetal.2015;Hahnetal.2017)tendtobeconceptual.Bycontrast,the

empiricalarticlesinthiscollectiontendedtofocusonnarrowerissues–forexample

casestudiesshowingtheuseofanalyticalmethods,orsurveybasedstudiesofethical

leadership.Theempiricalsettingsareveryvaried.However,giventhattheindustries

thatmostneedtodecarbonise(Rogeljetal.2018p138-148)areoftendominatedby

incumbents,thereisvalueinfocusingonlarge,establishedbusinessesasanempirical

setting.

Thethirdproblemisrelatedtothefirst.Becausedecision-makingbehaviourin

organisationsarisesfromabroadsystem,itisdifficulttoidentifythepointsof

interventionwheredecisionscanbechangedorimproved.Researchtodatehas

identifiedarangeofapproaches,rangingfromimprovinginformation(Chofrehetal.

2014)toinfluencingleadership(Epsteinetal.2010),buttheseneedtobesetinthe

broadercontextofthesystemthatshapesdecision-making.

Byusingtheseproblemsasastartingpoint,Ihavedefinedtworesearchquestionsto

addressinthisthesis.

26

2.9TheResearchQuestions

Q1:Howdotheformal,behaviouralandsocialstructuresofanorganisationinteract

toinfluencetheinclusionofsustainabilitycriteriaindecision-makinginincumbent

businesses?

Q2:Whatarethepointsofinterventiontoinfluencethesesystems?

27

3:METHOD

3.1 Introduction

Havingconcludedthelastchapterwithtworesearchquestions,thischapterdescribes

themethodsusedtoanswerthese.Thechapterisorganisedinfourmainsections.The

firstintroducesthefundamentalbeliefs–theresearchphilosophyandprinciples–

underlyingtheresearchapproach.Thesecondintroducestheoverallarchitectureof

theprojectandthechoiceofqualitativemixedmethodsused.Thethirdcommentson

theanalyticalmethodsusedtoderiveinsightfromthedata.Finally,thereisashort

commentaryonthelimitationsofthesemethodsandthemitigationstrategiesadopted

intheresearch.

3.2Researchapproach

3.2.1 ResearchphilosophyManyfieldshaveestablishedontologicalandepistemologicalconventions.However,as

IestablishedinChapter2,thefieldsofdecision-makingandsustainabilityare

fragmented,andthereareavarietyofperspectives.SchadandBansal(2018)suggest

thattheinconsistencyforsustainabilitywritersarisesbecauseweareworkingatthe

interfacebetweenthematerial(suchasemissionsorphysicalresources)andthe

sociallyconstructed.Thereisthereforearealchoiceforscholarsinthisfieldboth

ontologicallyandepistemologically.

TheresearchphilosophyIhaveadoptedisrootedinthenatureoftheproblem

examined.Inthisstudy,Ihavetakenaconstructionistontologicalapproach.Thisis

becausebasedonthereviewoftheliterature,therearetwoforcesshapingdecision-

makinginorganisations:aformalortechnicalapproach(forexampleinthesystematic

analysisofproblems);andanapproachrootedinsocialinteractionsandbehavioural

models(forexamplethepersonalstancetakenbyleaders).HerbertSimonin

‘AdministrativeBehaviour’(Simon1997p.119)pointedoutthatpeoplelimitthe

amountofinformationtheytakeintoaccountindecision-making.Theirthinkingis

constrainedbycircumstance.Tounderstandthenatureoftheseconstraints,Iseekto

28

understandthewayinwhichtheyareinterpretedbythedecision-makers.Myviewthat

aconstructionistapproachisbettersuitedtounderstandingthisproblembecauseofthe

significantroleofpersonalconstructsinthephenomenonobserved.

Justasdecision-makerslimittheinformationtheytakeintoaccount,researchersalso

operatefromapositionofincompleteknowledgeandboundedrationality(Mantere&

Ketokivi2013).Theepistemologicalapproachisthereforeinterpretivist.Again,this

choiceisrootedinthesubjectoftheresearch.ThedecisionsIaminterestedincreatea

problemofdatacollection:muchoftheheavyworkofdecision-makinghappensinside

people’sheadsastheyevaluatetheinformationandoptionsavailable.Myviewisthat

thiscanonlybeunderstoodphenomenologically:‘inordertograspthemeaningsofa

person’sbehaviour,thephenomenologistattemptstoseethingsfromthatperson’s

pointofview’(Taylor&Bogdan,1975p.14).

Thisphilosophicalapproachmeansthattheresearchisgroundedintheexperiencesof

theinformants.Thishasinfluencedaseriesofchoicesabouttheprinciples,architecture

andmethodsusedtoaddresstheresearchquestion.

3.2.2ResearchprinciplesAkeyprinciplethathasinformedtheresearchdesignisaneedtoinvolvedecision-

makersasactiveparticipantsintheprocess.Thisisfortworeasons.First,one

observationfromthereviewoftheliteratureinChapter2isthatmuchoftheworkon

thewaythatdecision-makersresolvethetensionsbroughtaboutbytryingtoact

sustainablyisconceptualinnature.Therehasbeenrelativelylittleworkthatactually

engagesthedecision-makersthemselves,andIseektoaddressthisgapinour

understanding.Second,theproblemofincorporatingsocialandenvironmentalthinking

intocorporatedecision-makingisarealone:oneaimofthisresearchisthereforeto

generatepracticalinsightsfordecision-makers.

Toachievethis,thestudyfollowsan‘engagedscholarship’approach(VandeVen2007),

andindeedthisprincipleinformedotherdesignchoices,suchastheuseofqualitative

mixedmethodsandanabductiveapproachtoreasoning,inwhichItogglebetween

empiricaldatafrommyinformantsandtheory(Alvesson&Kärrenman2007).The

intentionwastounderstandthenatureofaspecificproblem(thefirstwordsofmytwo

29

researchquestionsare‘how’and‘what’)thathasnotbeenwelldescribedfromthepoint

ofviewofthoseexperiencingit,andtoexplorethisfrommultipleperspectives.InVan

deVen’sterms,thisis‘informedbasicresearch’inwhichtheacademicresearcheris

clearlypositioned‘asanoutsider’(VandeVen,2007p.271)butconsultsstakeholdersat

eachstepoftheresearchprocess.Thisprocessofconsultationwasbuiltintothe

researchdesign.

Acorollaryofengagingcloselywithhumansubjectsistheneedtoworktohigh

standardsofconfidentialityinboththedatamanagementandthereporting.Datathat

couldidentifyindividualsorcompanies(suchasjobtitlesfortheindividualsorthe

numberofstaff,orsizeofturnoverforthecompanies)hasbeenwithheldthroughout

thisthesis.Ifiledadatamanagementplanatthebeginningoftheprogrammeinwhich

Icommittedtoseparatingthedataaboutrespondentsfromthedatatheysupplied.All

participantswereinvitedtoparticipateandhadtheoptiontorefuse.Theygave

informedconsentforanyrecordings(oneparticipantwithheldconsent,butgave

permissionformetotakenotesduringtheinterview).

3.3Researchmethods

3.3.1Researcharchitecture

Justastheresearchphilosophyandprincipleswerechosentoreflectthecharacteristics

oftheresearchquestionandthecurrentknowledgeinthefield,theresearch

architecturewasdevelopedtorespondtothreespecificcharacteristicsofcurrent

knowledge.First,theknowledgeissomewhatfragmented,andsoitwasimportantto

takeabroadapproachtoidentifyingthefactorsthatcouldinfluencedecision-making.

Second,someofthemostinfluentialworkinthefieldwasdevelopedconceptually,and

sohadnotbeentestedbypractitioners.Thisapproachthereforecombinedaseriesof

qualitativeinvestigationstofirst,generatetheoriesfromthebroadexperienceof

decision-makersworkingtoincludesustainabilityintheirchoices,thentestthese

theoriesinasinglecase,andfinallyexploretheirgeneralizabilitythroughdiscussions

withpractitioners.Thisledtothedevelopmentofaseriesofinterconnectedstudies

describedinTable4,below.

30

Table4:Objectivesandapproachforeachresearchstep

Stage Objective OutputResearchclarification

Understandthecurrentstateofknowledgeandidentifytheresearchquestions

LiteraturereviewdescribedinChapter2.

Study1 Understandthecurrentexperienceofdecision-makersanddeveloptheoreticalmodelsofdecision-makingandorganisation

Analysesofthetypesofdecisions,logicsusedandfactorsinfluencingdecision-makingdescribedinChapter4.

Study2 Testandextendthedevelopingtheoryandexploretheinteractionsbetweenmodelsinacasestudy

ApplicationoftheanalysisinChapter4,anddevelopmentofamodelshowinghowdecision-makingchangedovertimeinanorganisation,describedinChapter5.

Study3 Testtheemergingfindingswithpractitioners,followingtheengagedscholarshipapproach.

TestingandextensionoftheideasdevelopedinStudies1and2,describedinChapter6.

Iselecteddifferentresearchmethodsforeachofthesestudies..

3.3.2ChoiceofqualitativemixedmethodsGiventhenatureofthegapintheliteraturedescribedinChapter2,Idecidedtotakean

abductiveapproachtotheorybuilding.AsAlvesson&Kärrenman(2007)observe,

researchersoftencombinedeductive,inductiveandabductiveapproachesinthecourse

oftheirthinking,andthisworkisnoexception.However,thefocusonanabductive

approachinthisstudyisfortwomainreasons.First,astheliteratureisfragmented,it

wasnotpossibletotakeadeductiveapproach,buildingacoherentsetofhypothesesfor

testingdeductively.However,therearesometheoreticalframeworksthatcaninform

thiswork–particularlyfromthefieldofparadoxtheory.BlessingandChakrabarti

(2009)emphasiseaparallelprocessofexploringtheliteratureandempiricaldata,

whichcreatestheconditionsforanabductiveapproach(Alvesson&Kärrenman2007).

Abductionalsoenablestheresearchertofocusonsolvingaproblem,ratherthantesting

ahypothesis(Bryman&Bell2015)whichiscongruentwithmyresearchobjectives.

Becausetheworkisexploratory,Ihaveusedacombinationofqualitativemethods

(Edmondson&McManus2007),usingdifferentmethodsfordatacollectionandanalysis

ineachofthethreestudies.

31

ForStudy1,Iconducted17interviews,usingcriticalincidenttechnique.Critical

incidenttechniquehassomedistinctstrengthsasamethodforunderstandingthe

featuresofaphenomenon.Theapproachenables‘theconsciousreflectionsofthe

incumbent,theirframeofreference,feelings,attitudesandperspectiveonmatters

whichareofcriticalimportancetothem’(Chell,1998p.68).Thistendstoproducedata

attwolevels:descriptionsofthespecificincident(inthiscasedecisions);and

reflectionsonthebroadercontextforthisincident,allowingtheresearchertomake

connectionsbetweentheincidentandbroadercontext(Chell,1998p.55).Itisnotan

uncomfortableorexcessivelytime-consumingprocessforinterviewees.Ratherthan