income tax 101: prognosis - it’s complicated individual income tax introduction for dentists...

TRANSCRIPT

Income Tax 101:Prognosis - It’s Complicated

Individual Income Tax Introduction for Dentists

Presented by:

Matthew S. Smith, CPA, CFE ([email protected])L. Porter Roberts, Jr., CPA ([email protected])

Barr, Anderson & Roberts, PSCHealthcare Division2335 Sterlington Road Suite 100Lexington, KY 40517Telephone: (859) 268-1040Fax: (859) 268-6165www.barcpa.com

Income = Cake

One of the Problems with Income/Cake: The IRS wants a slice.After paying taxes, you often end up feeling like this is what’s left.

Two Keys to Keeping More of Your Cake Having a basic understanding of how

our income tax system works Taking advantage of all available tax

benefits, deductions, credits (if they make sense financially)

Using Part of Your Income to Reduce Taxes

1) Put some cake in the freezer for later / Save for retirement

Using Part of Your Income to Reduce Taxes2) Set aside some cake for unexpected guests / Pay for health, dental, vision insurance costs with pre-tax dollars and utilize a health savings account (H.S.A.) to pay out-of-pocket healthcare costs

Using Part of Your Income to Reduce Taxes

3) Give some cake to your kid(s) / Pay for childcare costs with pre-tax dollars if your employer offers this benefit

Example Single dentist works and earns $125,000 on a

W-2 with $20,000 of Federal income taxes and $10,100 of state and local income taxes withheld.

His savings account earned $100 of interest. He contributed $3,000 to his H.S.A. He contributed $5,000 to an IRA. His employer

does not offer a retirement plan. He paid student loan interest of $8,000,

mortgage interest of $8,000, property taxes of $2,000.

He donated $1,050 to charity. He had unreimbursed work expenses of $2,000.

Basic Formula/Flow of Form 1040 + Income (wages, 1099, interest, dividends, etc.) - Adjustments (HSA, IRA, student loan interest) - Standard or itemized deductions (mortgage interest,

taxes, charitable, medical, misc.) - Exemptions (one exemption for each dependent) = Taxable income (amount taken to tax brackets) X Tax rates = Income tax + Other taxes (self-employment tax, AMT, etc.) - Withholdings, estimates and credits (child tax, dependent

care, education, energy & other credits) = Refund or balance due

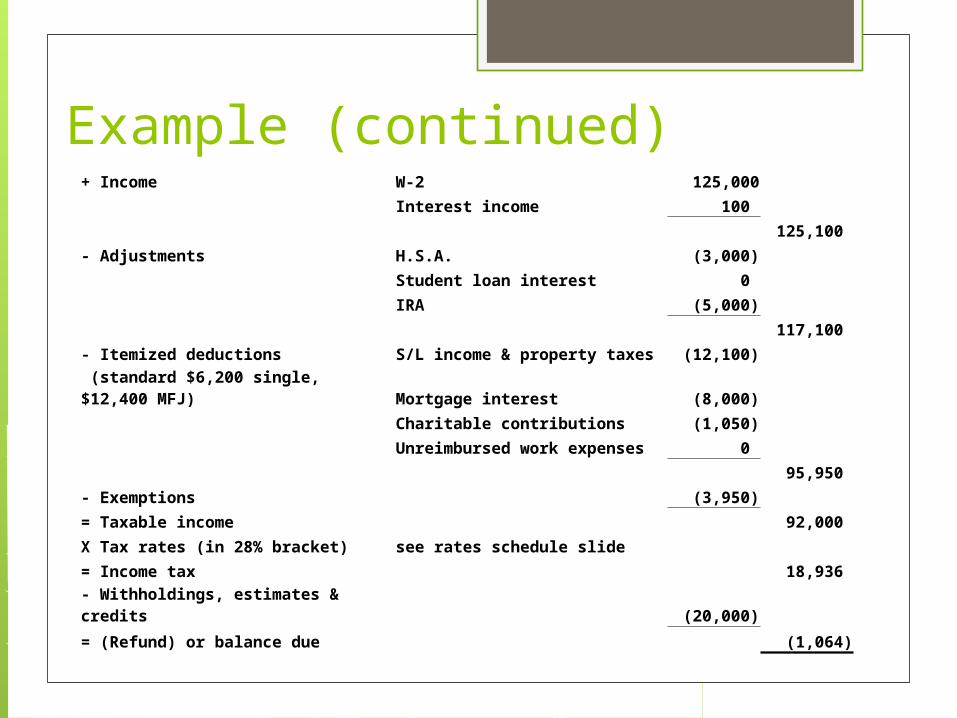

Example (continued)+ Income W-2 125,000

Interest income 100

125,100

- Adjustments H.S.A. (3,000)

Student loan interest 0

IRA (5,000)

117,100

- Itemized deductions S/L income & property taxes (12,100)

(standard $6,200 single, $12,400 MFJ) Mortgage interest (8,000)

Charitable contributions (1,050)

Unreimbursed work expenses 0

95,950

- Exemptions (3,950)

= Taxable income 92,000

X Tax rates (in 28% bracket) see rates schedule slide

= Income tax 18,936

- Withholdings, estimates & credits (20,000)

= (Refund) or balance due (1,064)

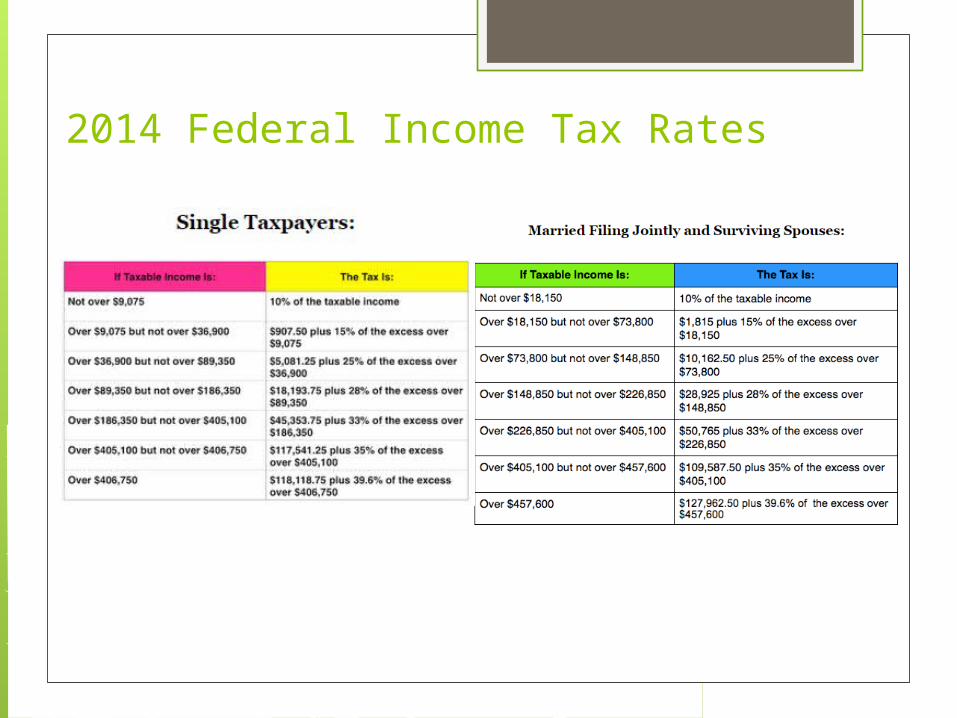

2014 Federal Income Tax Rates

Tax Savings and Planning Techniques Pre-tax deductions reduce taxable earned income.

You can do all of the following with pre-tax dollars: Contribute to retirement plan Contribute to H.S.A. account Pay for health, dental, vision insurance Pay for dependent care services

For example, if your gross wages are $200,000 for 2014, but from these wages you contributed $10,000 to your 401(k), $3,000 to your H.S.A., and paid $7,000 in insurance premiums, your W-2 would show taxable income of $180,000, sheltering $20,000 of these earnings from taxes in 2014.

Tax Savings and Planning Techniques Invest in tax-free or tax-preferred products.

Municipal bonds are frequently exempt from Federal (and some state) income taxes.

Qualified dividends are taxed at a maximum of 20%. If possible, consider refinancing home or taking out a

home equity loan & using funds to pay down student loan debt. These loans usually have a lower rate so less int. paid. The student loan interest tax deduction goes away at AGI of

$75,000 single/$155,000 MFJ. No AGI limit on mortgage interest.

Be aware of AMT add-back which may remove the tax benefit.

Examples of tax savings Switching to an H.S.A. to pay medical expenses

on a pre-tax basis instead of with net pay dollars can save over $2,000 per year for a family.

Paying for dependent care benefits with pre-tax dollars can save $750 per year with 2+ children.

Taking a lower salary in exchange for having your employer reimburse you for business mileage, CME, dues, cell phone, and other business expenses can save you up to 35% of these costs.

Thank you for your attention. Questions? Matthew S. Smith, CPA, CFE (find me on LinkedIn)

[email protected] 859-977-2403

L. Porter Roberts, Jr, CPA [email protected] 859-977-2404

Barr, Anderson & Roberts, PSC 2335 Sterlington Rd, Ste 100, Lexington, KY 40517 www.barcpa.com 859-268-1040 main line 859-268-6165 fax