inbu 4200 international financial management lecture 3 topic: the foreign exchange market the...

Post on 21-Dec-2015

225 views

TRANSCRIPT

INBU 4200 INTERNATIONAL FINANCIAL MANAGEMENT

Lecture 3

Topic: The Foreign Exchange Market

The Structure of the Market

Loonie Hits Parity with Greenback

The Foreign Exchange Market Defined The market where one currency is traded

(exchanged) for another currency. For example, purchasing pounds by selling dollars. Or, purchasing dollars by selling euros. FX transactions do not involve moving physical

currency (exception: tourist market), but rather represent shifts in commercial bank deposits.

Commercial banks are the major institutions in this market. They act on behalf of their customers (retail market) and

for their own accounts (wholesale market).

Quick Review of Market Characteristics World’s largest financial market.

Estimated at $3.2 trillion dollars per day in trades. NYSE-Euronext currently running about $40 billion per day.

Market is a 24/7 over-the-counter market. There is no central trading location. Trades take place through a network of computer and telephone

connections all over the world. Major trading center is London, England.

34% of all trades take place through London (New York second at 17%).

Most popular traded currency is the U.S. dollar. Accounts for 86% of all trades (euro second at 27%).

Most popular traded currency pair is the U.S. dollar/Euro. Represents 27% of all trades (dollar yen second at 13%)

Currencies are either traded for immediate delivery (spot) or some specified future delivery (forward).

FX Trading Floor, 1920s

FX Trading Floor, 2004 (London)

Source of Data on Foreign Exchange Market The Bank for International Settlements (BIS)

conducts a Central Bank Survey of the foreign exchange markets every three years.

First survey was done in April 1989. The latest (7th) survey was completed in April 2007.

54 central banks and monetary authorities participated in this recent survey, collecting information from approximately market participants (banks, brokers…)

Most of the data in this lecture comes from these BIS surveys. See last two slides for information on the BIS

What is Estimated Size of the Foreign Exchange Market?

1973: $ 10 to 20 billion 1989: $ 590 billion 1992: $ 820 billion (+39%) 1995: $1.190 trillion (+45%) 1998: $1.490 trillion (+25%) 2001: $1.200 trillion (-19%) 2004: $1.880 trillion (+57%) 2007: $3.210 trillion (+71%) Reasons for the recent increase:

Growing role of hedge funds in the market. Trend among institutional investors to hold

internationally diversified portfolios. Increase in technical trading (impact on spot markets).

Who are the Top Dealers (Market Makers) in the Foreign Exchange Market

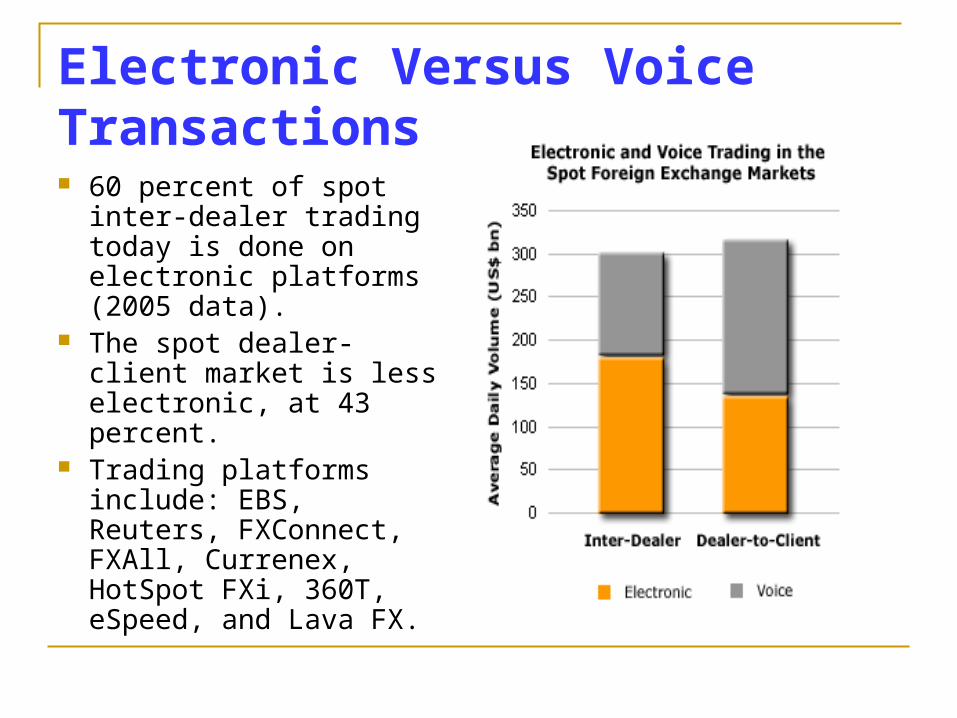

Electronic Versus Voice Transactions 60 percent of spot inter-

dealer trading today is done on electronic platforms (2005 data).

The spot dealer-client market is less electronic, at 43 percent.

Trading platforms include: EBS, Reuters, FXConnect, FXAll, Currenex, HotSpot FXi, 360T, eSpeed, and Lava FX.

Where is the Foreign Exchange Market? Geographically, the foreign exchange market

spans the entire globe, however: The major foreign exchange markets as a

percent of 2007 daily turnover (2004) are: U.K. (London): 34.1%; $1,094 billion (31.1%) U.S. (New York): 16.6%; $ 533 billion (19.2%) Switzerland: 6.6% (3.3%) Japan (Tokyo): 6.0%; (8.3%) Singapore: 5.8% (5.2%) Hong Kong 4.4% (4.2%) Australia (Sydney): 4.2% (3.4%)

Trading Times for the Market Foreign exchange trades on a 24 hour basis, with major

financial centers open Monday through Friday. Weekday trading begins in Sydney, Australia, Monday

morning (6:00am local time). Which is Sunday 4pm EST in New York; Sunday 8pm in London, and

Monday 5:00am in Japan. Weekday trading ends in New York, Friday afternoon

(5pm EST). Which is Friday 10pm in London, and Saturday 6:00am in Japan.

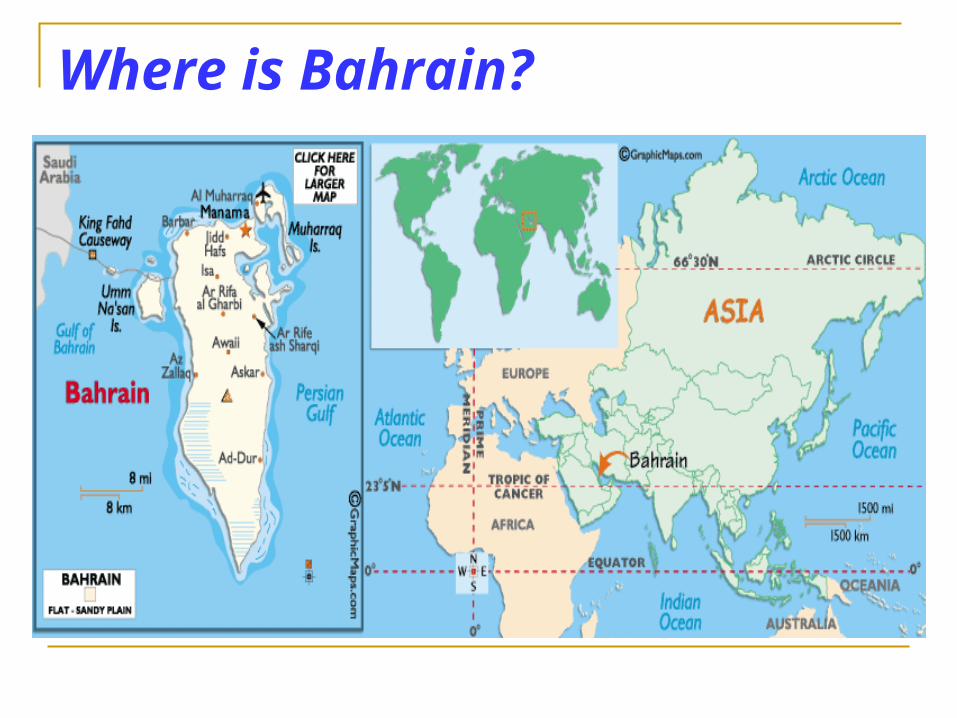

Globally, foreign exchange trading begins Australia, moves to Asia (Tokyo, Hong Kong, and Singapore), then to the Middle East, on to Europe (Paris and London), and finally to North America (New York). Weekend trades take place in the Middle East (e.g., in Bahrain

with 360 offshore banks; 65 US banks).

24-Hour Global Market:Times represent normal trading hours

Europe:LONDON

7:30am – 4pm

Middle East:Bahrain

NEW YORK 5am – early afternoon

Other Asia:TOKYO7am – 7pm

Opens Monday 6 am

Sydney

Closes: Friday 5pm New

York

Where is Bahrain?

London’s Unique Position Due to the geographic positioning of London

in relation to New York and Tokyo, London enjoys a trading day which overlaps with the other two. Thus, London trading in the afternoon

corresponds with New York trading in the morning (8 to noon).

And, London trading in the morning corresponds with Tokyo trading in the late afternoon (5 to 6pm).

However, New York (regular trading times) and Tokyo trading times do NOT overlap. Visit: http://www.eforex-asia.com/time_zones.html

Overlapping of Regions for FX Traders in New York (assuming 8 to 5 in NYC) Times refer to EST in New York City

Trading Patterns During the Day Weekday trading activity is heaviest when the major

markets overlap. As noted this would be: London (pm) and New York (am) overlap London (am) and Tokyo (pm) overlap

Thus, nearly two-thirds of New York foreign exchange trading activity occurs during New York morning hours (when London market is open).

Why these trading patterns? Market participants look to the combined liquidity of two

major centers to provide them with the best prices and quickest transactions.

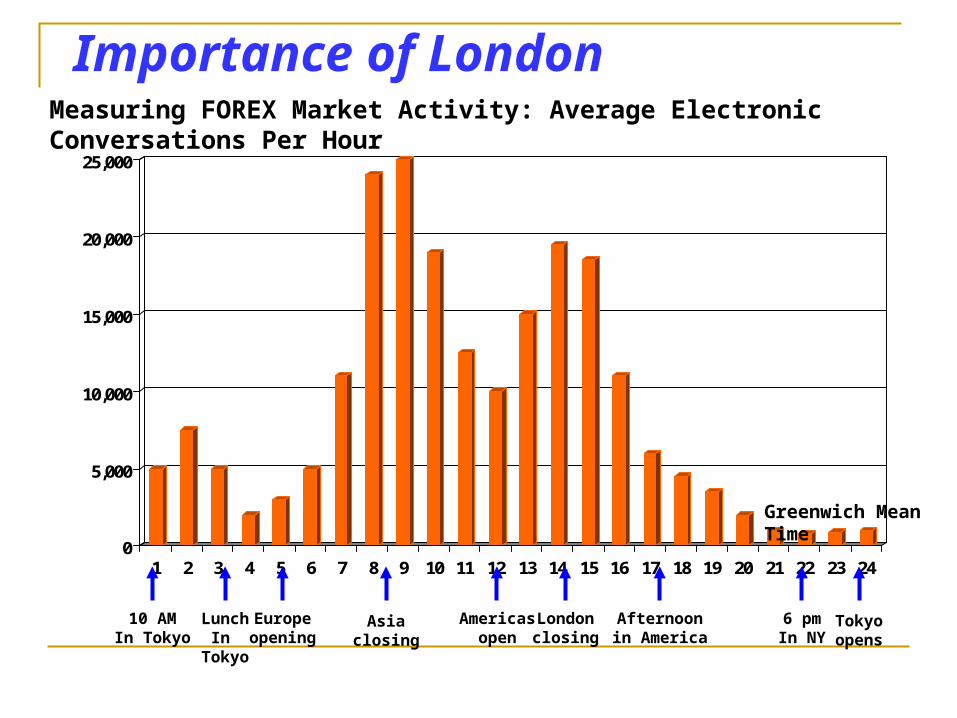

Importance of London

0

5,000

10,000

15,000

20,000

25,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Measuring FOREX Market Activity: Average Electronic Conversations Per Hour

Greenwich Mean Time

Tokyoopens

Asiaclosing

10 AMIn Tokyo

Afternoonin America

Londonclosing

6 pmIn NY

Americasopen

Europeopening

LunchIn

Tokyo

Market Participants Five broad categories of participants operate

within the foreign exchange market. They are: Commercial Banks and Investment Banks

Major commercial banks (e.g., Citigroup and Deutsche Bank ) and investment banks (e.g., Merrill Lynch and J.P. Morgan) with a global presence.

These banks are market makers. They profit from their bid and ask quotes (spreads). They also trade for their own accounts.

Business firms involved in cross border commercial transactions and hedging their FX exposures Importers, exporters, multinational firms.

Market Participants -- Continued

Traders: Speculators and arbitragers For Example: Hedge Funds:

As speculators, they seek profit from exchange rate changes (selling short, buying long)

As arbitragers, they seek profit from simultaneous differences in exchange rates in different markets

Hedge fund example: http://www.mangroupplc.com/default.cfm

Governments: Central banks and treasuries Seeking to offset market forces

Investment firms Mutual funds, asset managers, non-market maker banks, and

pension funds Note: The bulk of the Forex Market is between a few

hundred large banks that process transactions from large companies and governments around the world.

Types of Foreign Exchange Transactions The Bank for International Settlements records

three types of FX “traditional” transactions: Spot Transactions

Contracts which call for 2 business day settlements. Exception: North America trades of USD and CAD are 1

day. Outright Forwards

Contracts which call for more than two business day settlements.

Swaps Simultaneous purchase and sale of a given amount of

foreign exchange for two different dates.

Foreign Exchange Swap Transactions Defined: The simultaneous purchase and sale of a given

amount of foreign exchange for two different dates. Both purchase and sale are usually conducted with

the same counterpart (i.e., the same global bank) The most common FX swap is a spot against forward

A bank buys FX in the spot market and simultaneously sells the same amount back in the forward market

Since the swap transaction is an offset, the bank incurs NO exchange rate exposure.

A swap transaction is used to provide bank clients with needed foreign exchange for a specified period of time (e.g., a short term loan).

Example of FX Swap Corporate approaches its bank wanting to borrow

10,000,000 euros for 90 days. Bank negotiates in interbank spot market to purchase

10,000,000 euros, which in turn are lent to the corporate. Bank simultaneously sells 10,000,000 euros 90 days

forward (i.e., for delivery in 90 days) in the interbank market. When loan matures, bank will receive the 10,000,000 euros from

the corporate borrower which provides it with the euros to be delivered at that time to complete the forward agreement.

Thus, the lending bank assumes no exchange risk during the 90 day period.

The bank’s return is the interest on the loan, minus any spot/forward spread not in it’s favor.

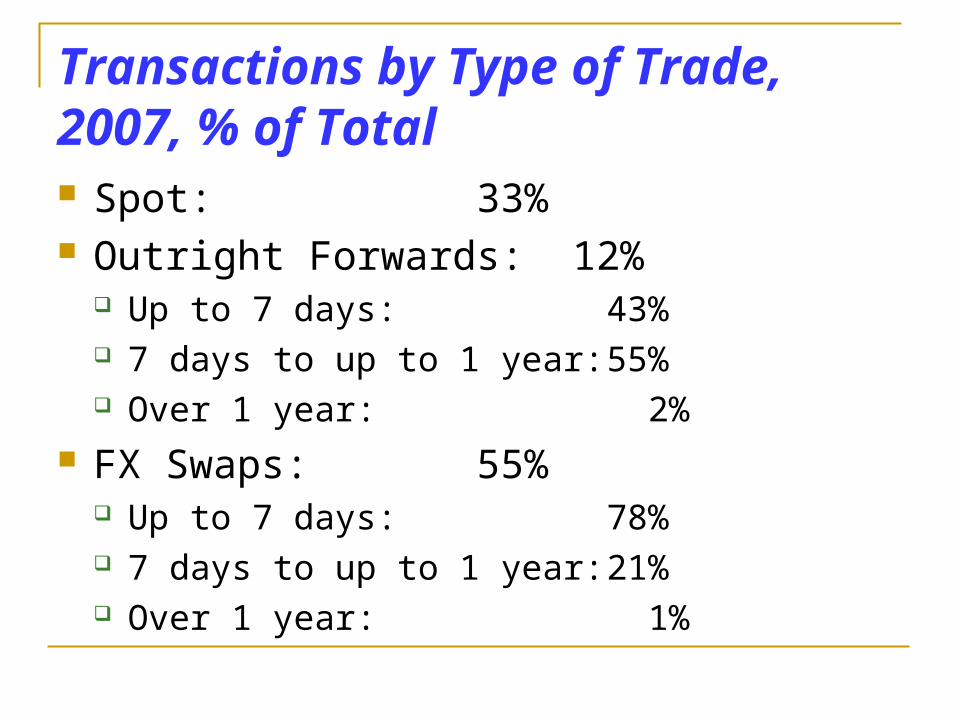

Transactions by Type of Trade, 2007, % of Total Spot: 33% Outright Forwards: 12%

Up to 7 days: 43% 7 days to up to 1 year: 55% Over 1 year: 2%

FX Swaps: 55% Up to 7 days: 78% 7 days to up to 1 year: 21% Over 1 year: 1%

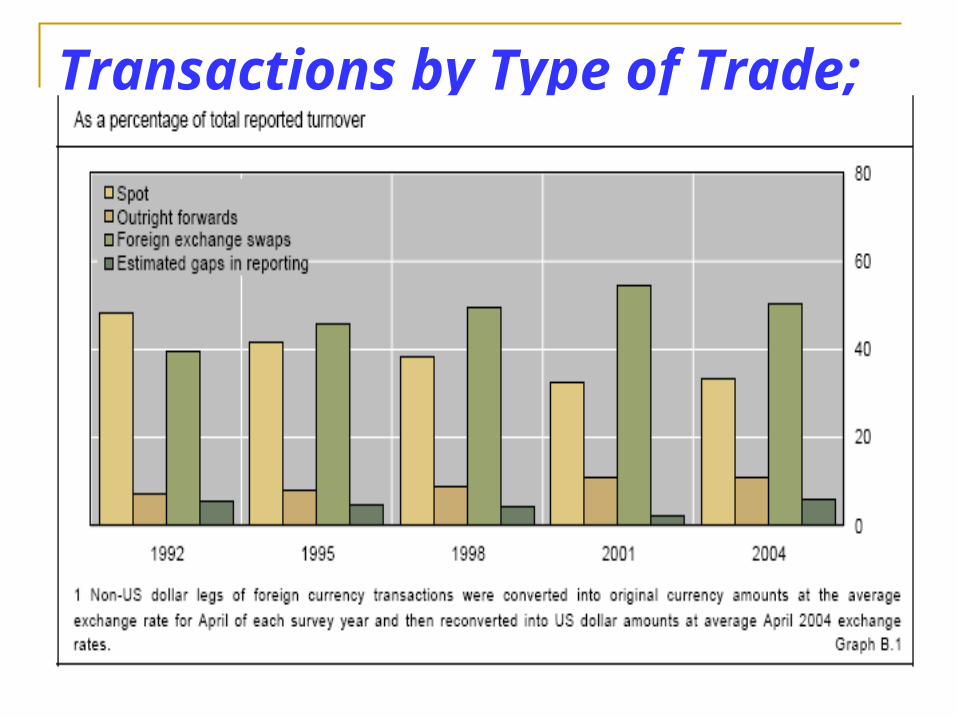

Transactions by Type of Trade; %

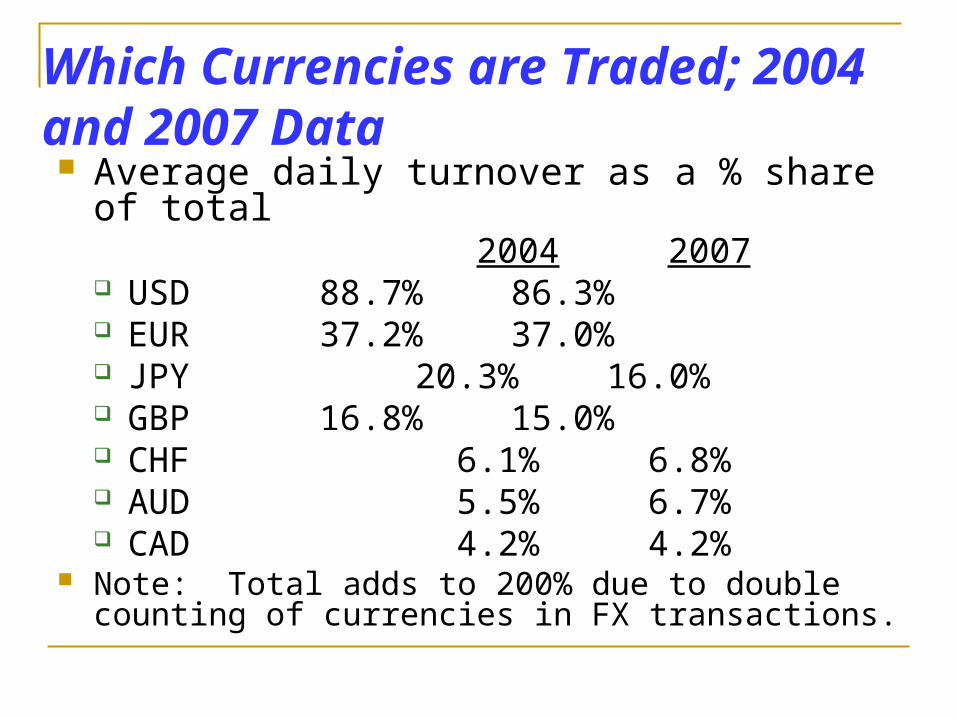

Which Currencies are Traded; 2004 and 2007 Data Average daily turnover as a % share of total 2004 2007

USD 88.7% 86.3% EUR 37.2% 37.0% JPY 20.3% 16.0% GBP 16.8% 15.0% CHF 6.1% 6.8% AUD 5.5% 6.7% CAD 4.2% 4.2%

Note: Total adds to 200% due to double counting of currencies in FX transactions.

Which Currency Pairs are Traded Average daily turnover as a % share of total 2004 2007 USD/EUR 28% 27% USD/JPY 17% 13% USD/GBP 14% 12% USD/AUD 5% 6% USD/CHF 4% 5% USD/CAD 4% 4%

Wholesale (Interbank) and Retail Markets The FX market is a two-tier financial market: Wholesale (Interbank) market

Large transactions (>$10 million) involving 100 to 200 large “market-maker” global banks (>$400 billion) and large non-bank financial institutions (e.g., investment banks).

Represents about 80% of the market. Retail (client) market

Transactions between banks and their retail customers (includes multinational firms, money managers, private speculators).

Represents about 20% of the market.

Bank for International Settlements The Bank for International Settlements (BIS) is

an international organization which aims to promote "international monetary and financial cooperation and serve as a bank for central banks."

The BIS was originally established under the Hague agreements in January 1930 to facilitate Germany's payment of reparations following World War I, and to promote cooperation between central banks. It began operating in Basel, Switzerland, on May 17,

1930, and is the world's oldest international financial organization.

Useful BIS Web-sites

BIS main web site: http://www.bis.org/index.htm

BIS central bank web-site: The following BIS web-site has links to most

of the central banks around the world! http://www.bis.org/cbanks.htm