in depth - new ifrss for 2017 · investment property • amendments to ifrs 15, ‘revenue from...

TRANSCRIPT

May 2017 2017年5月

English with Chinese Translation中英文对照

www.pwccn.com

In depth - New IFRSs for 2017

洞察—2017年国际 财务报告准则的变化

2 PwC - In depth - New IFRSs for 2017

Contents

Introduction 4

Amended standards 8Recognition of deferred tax assets for unrealised losses - Amendments to IAS 12, ‘Income taxes’ 8

Disclosure initiative - Amendments to IAS 7, ‘Cash flow statements’ 10

Applying IFRS 9 Financial instruments with IFRS 4 Insurance contracts - Amendments to IFRS 4, ‘Insurance contracts’ 12

Classification and measurement of share based payment transactions - Amendment to IFRS 2, ‘Share based payments’ 16

Transfers of investment property - Amendments to IAS 40, ‘Investment property’ 20

New standards 22Financial instruments - IFRS 9 22

Revenue from contracts with customers - IFRS 15 26

Clarifications to IFRS 15 - Amendments to IFRS 15, ‘Revenue from contracts from customers’ 30

Leases - IFRS 16 34

Annual improvements 2014-2016 cycle 38

IFRIC 22 40‘Foreign currency transactions and advance consideration’ 40

普华永道—洞察—2017年国际财务报告准则的变化 3

目录

引言 5

修改的准则 9

对未实现损失确认递延所得税资产—对《国际会计准则第12 号—所得税》的修改 9

披露议案—对《国际会计准则第7号—现金流量表》的修改 11

同时实施《国际财务报告准则第9号—金融工具》和《国际财 务报告准则第4号—保险合同》—对《国际财务报告准则第4 号》的修改 13

股份支付交易的分类与计量—对《国际财务报告准则第2号 —股份支付》的修改 17

投资性房地产转入/转出—对《国际会计准则第40号—投资 性房地产》的修改 21

新准则 23

金融工具—国际财务报告准则第9号 23

与客户之间的合同产生的收入—国际财务报告准则第15号 27

对《国际财务报告准则第15号》的澄清—对《国际财务报告 准则第15号—与客户之间的合同产生的收入》的修改 31

租赁—国际财务报告准则第16号 35

2014-2016年年度改进项目 39

国际财务报告解释公告第22号 41

外币交易和预付/预收对价 41

4 PwC - In depth - New IFRSs for 2017

Introduction

Since March 2016, the IASB has issued the following amendments:

• Amendments to IFRS 4, ‘Insurance contracts’, regarding the implementation of IFRS 9

• Amendments to IFRS 2, ‘Share based payments’, regarding the classification and measurement of share based payment transactions

• Amendments to IAS 40, ‘Investment property’, regarding transfers of investment property

• Amendments to IFRS 15, ‘Revenue from contracts with customers’ regarding clarifications to the standard

• Annual improvements 2014-2016 covering IFRS 12, ‘Disclosure of interests in other entities’, IFRS 1, ‘First-time adoption of IFRS’, and IAS 28, ‘Investments in associates and joint ventures’

• IFRIC 22 - ‘Foreign currency transactions and advance consideration’

This guide summarises these new amendments and IFRIC plus those standards and amendments issued previously that are effective from 1 January 2017.

It is designed to be used by preparers, users and auditors of IFRS financial statements. It includes a quick reference table of each standard/amendment/interpretation categorised by the effective date, whether early adoption is permitted. The publication gives an overview of the impact of the changes, which may be significant for some entities, helping companies understand if they will be affected and to begin their considerations. It will help entities plan more effectively by flagging up where new processes and systems or more guidance may be needed.

普华永道—洞察—2017年国际财务报告准则的变化 5

引言

自2016年3月,国际会计准则理事会发布:

• 对《国际财务报告准则第4号—保险合

同》关于实施《国际财务报告准则第9

号》的修改

• 对《国际财务报告准则第2号—股份支

付》关于股份支付交易分类和计量的修改

• 对《国际会计准则第40号—投资性房地

产》关于投资性房地产转入/转出的修改

• 对《国际财务报告准则第15号—与客户

之间的合同产生的收入》关于准则澄清

的修改

• 2014-2016年年度改进项目覆盖的《国

际财务报告准则第12号—在其他主体

中的权益披露》、《国际财务报告准则第

1号—首次采用国际财务报告准则》及《国

际会计准则第28号—对联营和合营的

投资》

• 《国际财务报告解释公告第22号—外

币交易和预付/预收对价》。

本刊扼要介绍了这些新的修改和国际财务

报告解释公告以及过去发布并于2017年1

月1日或之后生效的准则及修改。

本刊可供国际财务报告准则下的财务报表

编制者、使用者和审计师使用,其中包含一

份按照生效日期分类的各项准则/修改/解

释公告的速查表,并标明是否允许提前采

用。本刊概述了准则变动的影响(这些影响

对于某些主体而言可能是重大的),将帮助

公司理解其是否将受此影响,并开始考虑

如何应对。本刊将通过着重提醒哪些领域

需要引入新程序和系统或更多指引,以帮

助主体提高制定计划的效率。

6 PwC - In depth - New IFRSs for 2017

Standard/amendment/interpretation Effective date Adoption status Page

1 January 2017

Amendment to IAS 12, ‘Income taxes’, regarding recognition of deferred tax assets for unrealised losses’

Annual periods beginning on or after 1 January 2017

Early adoption is permitted

8

Amendment to IAS 7, ‘Cash flow statements’, regarding the Disclosure initiative

Annual periods beginning on or after 1 January 2017

Early adoption is permitted

10

Annual improvements 2014-2016, IFRS 12, ‘Disclosure of interests in other entities’

Annual periods beginning on or after 1 January 2017

Early adoption is permitted

38

1 January 2018

IFRS 9, ‘Financial instruments’ Annual periods beginning on or after 1 January 2018

Early adoption is permitted

12

IFRS 15, ‘Revenue from contracts with customers’ Annual periods beginning on or after 1 January 2018

Early adoption is permitted

26

Amendment to IFRS 15, ‘Revenue from contracts with customers’ regarding clarifications

Annual periods beginning on or after 1 January 2018

Early adoption is permitted

30

Amendments to IFRS 2, ‘Share based payments’, regarding classification and measurement of share-based payment transactions

Annual periods beginning on or after 1 January 2018

Early adoption is permitted

16

Amendments to IFRS 4, ‘Insurance contracts’, regarding implementation of IFRS 9

Annual periods beginning on or after 1 January 2018

Early adoption is permitted

12

Amendment to IAS 40, ‘Investment property’, regarding the transfer of property

Annual periods beginning on or after 1 January 2018

Early adoption is permitted

20

Annual improvements 2014-2016, IFRS 1, ‘First time adoption of IFRS’, regarding IFRS 7, IAS 19 and IFRS 10; IAS 28 ‘Investment in associates and joint ventures’

Annual periods beginning on or after 1 January 2018

Early adoption is permitted

38

IFRIC 22, ‘Foreign currency transactions and advance consideration’

Annual periods beginning on or after 1 January 2018

Early adoption is permitted

40

1 January 2019

IFRS 16, ‘Leases’ Annual periods beginning on or after 1 January 2019

Early adoption is permitted if IFRS 15 is also adopted

34

普华永道—洞察—2017年国际财务报告准则的变化 7

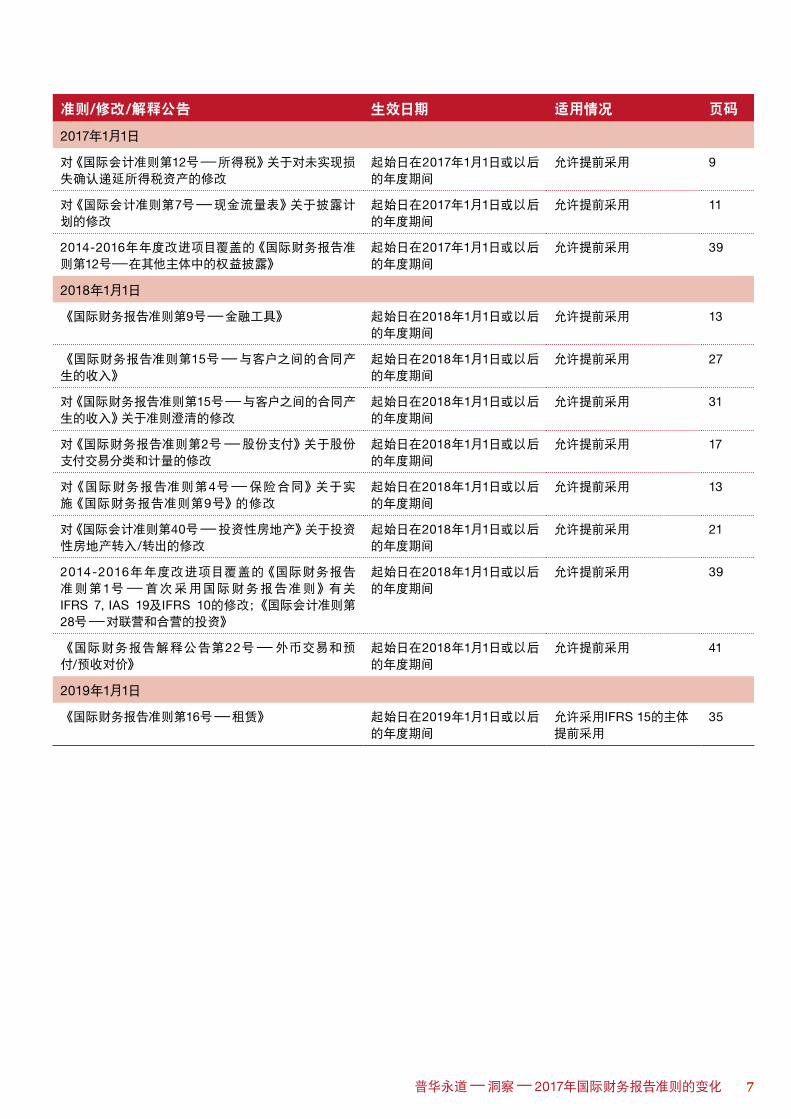

准则/修改/解释公告 生效日期 适用情况 页码

2017年1月1日

对《国际会计准则第12号—所得税》关于对未实现损失确认递延所得税资产的修改

起始日在2017年1月1日或以后的年度期间

允许提前采用 9

对《国际会计准则第7号—现金流量表》关于披露计划的修改

起始日在2017年1月1日或以后的年度期间

允许提前采用 11

2014-2016年年度改进项目覆盖的《国际财务报告准则第12号—在其他主体中的权益披露》

起始日在2017年1月1日或以后的年度期间

允许提前采用 39

2018年1月1日

《国际财务报告准则第9号—金融工具》 起始日在2018年1月1日或以后的年度期间

允许提前采用 13

《国际财务报告准则第15号—与客户之间的合同产生的收入》

起始日在2018年1月1日或以后的年度期间

允许提前采用 27

对《国际财务报告准则第15号—与客户之间的合同产生的收入》关于准则澄清的修改

起始日在2018年1月1日或以后的年度期间

允许提前采用 31

对《国际财务报告准则第2号—股份支付》关于股份支付交易分类和计量的修改

起始日在2018年1月1日或以后的年度期间

允许提前采用 17

对《国际财务报告准则第4号—保险合同》关于实施《国际财务报告准则第9号》的修改

起始日在2018年1月1日或以后的年度期间

允许提前采用 13

对《国际会计准则第40号—投资性房地产》关于投资性房地产转入/转出的修改

起始日在2018年1月1日或以后的年度期间

允许提前采用 21

2014-2016年年度改进项目覆盖的《国际财务报告准则第1号—首次采用国际财务报告准则》有关 IFRS 7,IAS 19及IFRS 10的修改;《国际会计准则第28号—对联营和合营的投资》

起始日在2018年1月1日或以后的年度期间

允许提前采用 39

《国际财务报告解释公告第22号—外币交易和预 付/预收对价》

起始日在2018年1月1日或以后的年度期间

允许提前采用 41

2019年1月1日

《国际财务报告准则第16号—租赁》 起始日在2019年1月1日或以后的年度期间

允许采用IFRS 15的主体提前采用

35

8 PwC - In depth - New IFRSs for 2017

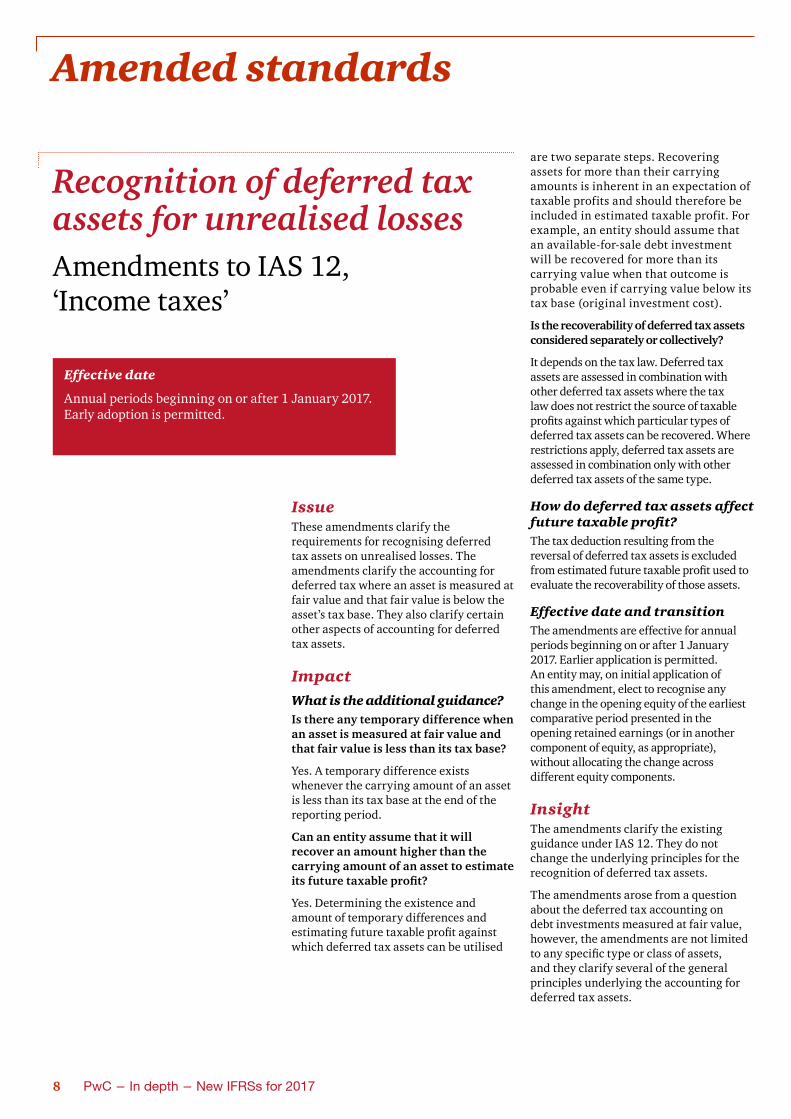

Effective date

Annual periods beginning on or after 1 January 2017. Early adoption is permitted.

Amended standards

IssueThese amendments clarify the requirements for recognising deferred tax assets on unrealised losses. The amendments clarify the accounting for deferred tax where an asset is measured at fair value and that fair value is below the asset’s tax base. They also clarify certain other aspects of accounting for deferred tax assets.

ImpactWhat is the additional guidance?Is there any temporary difference when an asset is measured at fair value and that fair value is less than its tax base?

Yes. A temporary difference exists whenever the carrying amount of an asset is less than its tax base at the end of the reporting period.

Can an entity assume that it will recover an amount higher than the carrying amount of an asset to estimate its future taxable profit?

Yes. Determining the existence and amount of temporary differences and estimating future taxable profit against which deferred tax assets can be utilised

are two separate steps. Recovering assets for more than their carrying amounts is inherent in an expectation of taxable profits and should therefore be included in estimated taxable profit. For example, an entity should assume that an available-for-sale debt investment will be recovered for more than its carrying value when that outcome is probable even if carrying value below its tax base (original investment cost).

Is the recoverability of deferred tax assets considered separately or collectively?

It depends on the tax law. Deferred tax assets are assessed in combination with other deferred tax assets where the tax law does not restrict the source of taxable profits against which particular types of deferred tax assets can be recovered. Where restrictions apply, deferred tax assets are assessed in combination only with other deferred tax assets of the same type.

How do deferred tax assets affect future taxable profit?The tax deduction resulting from the reversal of deferred tax assets is excluded from estimated future taxable profit used to evaluate the recoverability of those assets.

Effective date and transitionThe amendments are effective for annual periods beginning on or after 1 January 2017. Earlier application is permitted. An entity may, on initial application of this amendment, elect to recognise any change in the opening equity of the earliest comparative period presented in the opening retained earnings (or in another component of equity, as appropriate), without allocating the change across different equity components.

InsightThe amendments clarify the existing guidance under IAS 12. They do not change the underlying principles for the recognition of deferred tax assets.

The amendments arose from a question about the deferred tax accounting on debt investments measured at fair value, however, the amendments are not limited to any specific type or class of assets, and they clarify several of the general principles underlying the accounting for deferred tax assets.

Recognition of deferred tax assets for unrealised lossesAmendments to IAS 12, ‘Income taxes’

普华永道—洞察—2017年国际财务报告准则的变化 9

修改的准则

概述

该修改澄清了关于对未实现损失确认递延

所得税资产的要求,按公允价值计量且该公

允价值小于计税基础的资产的递延所得税

的会计处理,以及递延所得税资产会计处

理的某些其他方面。

影响

补充指引的内容

按公允价值计量且该公允价值小于计税基

础的资产是否存在暂时性差异?

是。只要报告期末资产的账面金额小于其计

税基础,即存在暂时性差异。

主体是否能够假设将收回大于资产账面价值

的金额以估计未来应纳税所得额?

是。确定暂时性差异的存在性以及具体金

额与估计可以使用递延所得税资产的未来

应纳税所得额是两个独立的步骤。估计未

来应纳税所得额本质上包含着对主体将能

够收回比账面价值更大金额的预期,因此应

当包含在对未来应纳税所得额的估计中。例

如,如果一项可供出售的债务投资将收回大

于账面价值的金额是很可能的,则即使账面

价值低于计税基础(初始投资成本),主体

应当假设这项可供出售的债务投资将收回

大于账面价值的金额。

对递延所得税资产的可收回性的评估是单

独进行还是合并进行?

这取决于税法规定。如果税法并未对某种类

型的递延所得税资产可使用的应纳税所得

额的来源提出限制,则递延所得税资产可以

与其他递延所得税资产合并进行评估。如果

存在限制,递延所得税资产只能与同类资产

合并评估。

递延所得税资产如何影响未来应纳税所得额?

用以评估递延所得税资产可收回性的预计

未来应纳税所得额不包含递延所得税资产

转回所导致的税项抵减。

生效日期及过渡规定

本次修改自2017年1月1日或以后开始的年

度期间生效,允许提前采用。主体可在首次

应用该修改时选择在最早可比期间期初权

益中的期初留存收益中列报(或视情况在

权益的另一个组成部分中列报),而不在权

益的不同组成部分间分配这些变动。

见解

本次修改对国际会计准则第12号下的现行

指引进行了澄清,并未改变主体确认递延

所得税资产的基本原则。

进行本次修改的起因是一个关于以公允价

值计量的债务投资产生的递延所得税资产

的会计处理问题。然而,本次修改不仅限于

资产的特定类型或类别,并澄清了递延所

得税资产会计的若干基础原则。

对未实现损失确认递延 所得税资产

对《国际会计准则第12号 —所得税》的修改

生效日期

适用于起始日在2017年1月1日或以后开始的年度期间。允许

提前采用。

10 PwC - In depth - New IFRSs for 2017

IssueThese amendments IAS 7 introduce an additional disclosure that will enable users of financial statements to evaluate changes in liabilities arising from financing activities. The amendment is part of the IASB’s Disclosure initiative, which continues to explore how financial statement disclosure can be improved.

ImpactWhat is the additional disclosure?An entity is required to disclose information that will allow users to understand changes in liabilities arising from financing activities. This includes changes arising from:

• cash flows, such as drawdowns and repayments of borrowings; and

• non-cash changes, such as acquisitions, disposals and unrealised exchange differences.

What items should an entity include in the additional disclosure?Is the disclosure limited to debt?

No. Debt is not defined or required to be disclosed by current IFRS, so the IASB decided to require disclosure of changes in liabilities for which cash flows were, or future cash flows will be, classified as financing activities in the statement of cash flows.

Should an entity include financial assets in the disclosure if those assets are used to manage its financing activities?

Yes. An entity should include changes in financial assets (for example, assets that hedge liabilities arising from financing liabilities) in the new disclosures if such cash flows were, or will be, included in cash flows from financing activities.

Can an entity include changes in other items as part of the disclosures?

Yes. Changes in other items should be included where an entity considers that such disclosures would meet the objective of the disclosure requirement above. For example, an entity might consider including changes in cash and cash equivalents, pension liabilities and interest payments that are classified as operating activities in the statement of cash flows, etc. However, the amendment requires such disclosure to be separate from the disclosure of changes in liabilities arising from financing activities.

Is a specific disclosure format required?No. The amendment suggests that a reconciliation between the opening and closing balances in the balance sheet for liabilities arising from financing activities would meet the disclosure requirement, but a specific format is not mandated. However, where a reconciliation is used, the disclosure should provide sufficient information to link items included in the reconciliation to the balance sheet and statement of cash flows.

Effective date and transitionThe amendment is effective for annual periods beginning on or after 1 January 2017. Earlier application is permitted. When an entity first applies the amendment, it is not required to provide comparative information in respect of preceding periods.

InsightThe amendment responds to requests from investors for information that helps them better understand changes in an entity’s debt. The amendment will affect every entity preparing IFRS financial statements. However, the information required should be readily available. Preparers should consider how best to present the additional information to explain the changes in liabilities arising from financing activities.

Disclosure initiativeAmendments to IAS 7, ‘Cash flow statements’

Effective date

Annual periods beginning on or after 1 January 2017. Early adoption is permitted.

普华永道—洞察—2017年国际财务报告准则的变化 11

概述

对国际会计准则第7号的本次修改引入一项

补充披露,财务报表使用者据此将能够评

价因融资活动产生的负债变动。此修改是国

际会计准则理事会“披露计划”的一部分,

该计划将继续研究如何进一步改进财务报

表披露问题。

影响

补充披露的内容

主体必须披露能够帮助使用者理解融资活

动产生的负债变动的信息。这包括下列项目

导致的变动:

• 现金流量,比如借款的提取和偿还;及

• 非现金变动,比如收购、处置和未实现

的外汇差异。

主体应当在补充披露中包含哪些项目?

是否仅限于披露债务?

不是。现行国际财务报告准则没有把债务定

义或要求主体披露债务,因此国际会计准则

理事会决定,主体应当针对在现金流量表中

曾被分类为融资活动的现金流或将被分类为

融资活动的未来现金流披露负债的变动。

主体用于管理融资活动的金融资产是否应

当包含在披露中?

是。主体应将金融资产(包括,对金融负债

产生的负债进行套期的资产)的变动包含在

新的披露中,如果此类现金流量曾被或将被

包含在融资活动产生的现金流量中。

主体是否可以将其他项目的变动作为披露的

一部分?

可以。如果主体认为披露其他项目的变动将

符合上述披露要求的目标,则其他项目的变

动应当包含在内。例如,主体可能考虑包含

现金流量表中经营活动类别下的现金及现

金等价物、养老金负债和利息支付款的变动

等。然而,本次修改要求此类披露应当与融

资活动产生的负债变动的披露区分开来。

是否要求使用特定披露格式?

不要求。本次修改并未强制规定任何特定格

式,并指出为融资活动产生的负债所做的从

资产负债表期初余额到期末余额的调节表

可以满足披露要求。然而,一旦使用了调节

表,披露应当提供充足的信息,以使调节表

内包含的项目与资产负债表和现金流量表联

系起来。

生效日期及过渡规定

本次修改自2017年1月1日或以后开始的年度

期间生效,允许提前采用。主体首次应用本

次修改时无需提供以前期间的比较信息。

见解

本次修改是为回应投资者为获得能够帮助

他们更好地理解主体债务变动情况的请求

而进行的。本次修改将影响每个应用国际财

务报告准则编制财务报表的主体。然而,所

需信息应当是随时可获得的。编制人应考虑

如何最佳列示补充信息,以解释融资活动产

生的负债变动。

披露议案

对《国际会计准则第7号 —现金流量表》的修改

生效日期

适用于起始日在2017年1月1日或以后开始的年度期间。允许

提前采用。

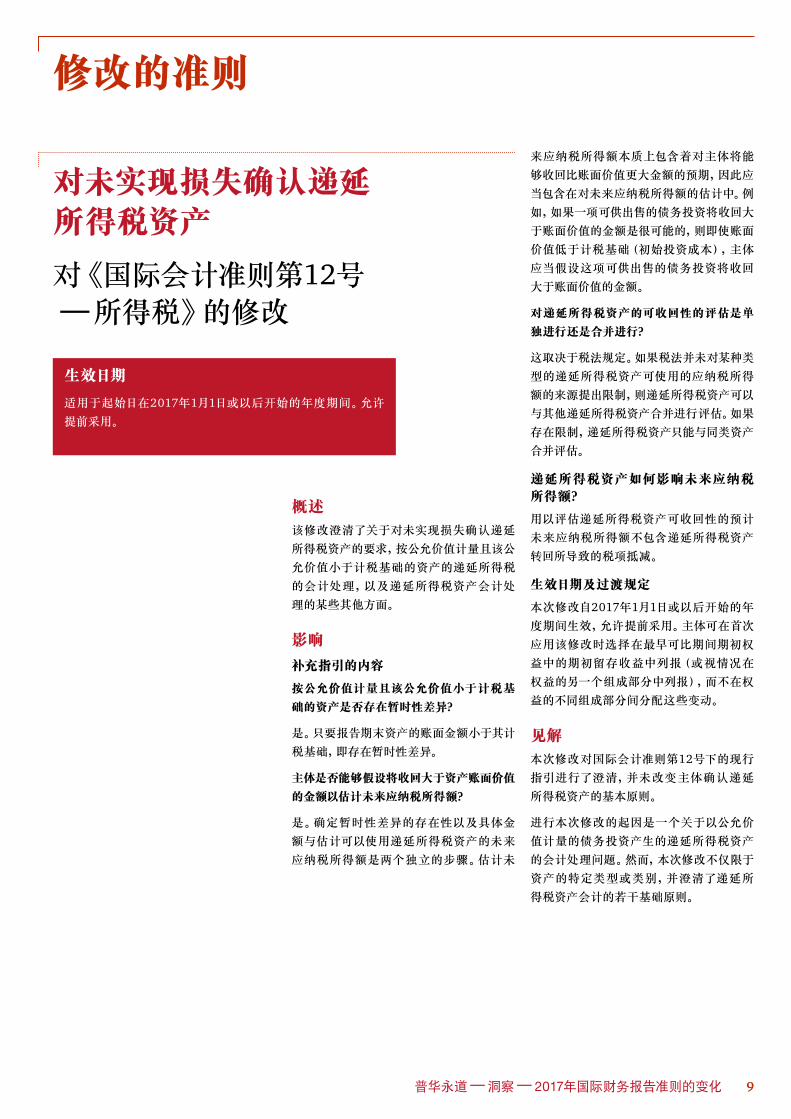

12 PwC - In depth - New IFRSs for 2017

IssueThese amendments address the concerns of insurance companies about the different effective dates of IFRS 9, ‘Financial instruments’, and the forthcoming new insurance contracts standard. The amendment to IFRS 4 provides two different solutions for insurance companies: a temporary exemption from IFRS 9 for entities that meet specific requirements (applied at the reporting entity level); and the ‘overlay approach’. Both approaches are optional.

IFRS 4 (including the amendments that have now been issued) will be superseded by the forthcoming new insurance contracts standard. Accordingly, both the temporary exemption and the ‘overlay approach’ are expected to cease to be applicable when the new insurance standard becomes effective.

Key provisionsTemporary exemption from applying IFRS 9For annual periods beginning before 1 January 2021, the amendment to IFRS 4 allows insurers to continue to apply IAS 39, ‘Financial Instruments: Recognition and measurement’, instead of adopting IFRS 9, if their activities are ‘predominantly connected with insurance’. The exemption can only be applied at the level of the reporting entity. To assess whether activities are ‘predominantly connected with insurance’, two tests have to be performed. Only if both tests are passed are an insurer’s activities considered to be predominantly connected with insurance.

First, an insurer assesses whether the carrying amount of its liabilities arising from contracts within IFRS 4’s scope is significant, compared to the total carrying amount of all of its liabilities.

Secondly, the insurer compares the total carrying amount of its liabilities connected with insurance with the total carrying amount of all of its liabilities. In addition to liabilities arising directly from contracts within IFRS 4’s scope, liabilities connected with insurance include

• non-derivative investment contract liabilities measured at fair value through profit or loss applying IAS 39; and

• liabilities that arise because the insurer issues, or fulfils obligations arising from, those insurance and non-derivative investment contracts.

The second test is passed if the resulting percentage is either: greater than 90%; or if it is less than or equal to 90% but greater than 80%, the insurer is not engaged in a significant activity unconnected with insurance.

The assessment is made, based on the carrying amounts as at the annual reporting date that immediately precedes 1 April 2016. Under certain circumstances, a reassessment is required or permitted.

Applying IFRS 9, ‘Financial instruments’ with IFRS 4, ‘Insurance contracts’ Amendments to IFRS 4, ‘Insurance contracts’

Effective date

Annual periods beginning on or after 1 January 2018. Early adoption is permitted.

普华永道—洞察—2017年国际财务报告准则的变化 13

同时实施《国际财务报告准则第9号—金融工具》和《国际财务报告准则第4号—保险合同》

对《国际财务报告准则第4号—保险合同》的修改

问题

该修改消除了保险公司关于《国际财务报告

准则第9号—金融工具》和即将发布的新

保险合同准则生效时间不同的担忧。本次

对国际财务报告准则第4号的修改为保险公

司提供了两种不同的解决方法:一是为满

足特定要求的主体提供了对IFR S 9的豁

免(在报告主体层面适用),二是“叠加法”。

这两种方法供主体任选。

国际财务报告准则第4号(包括已发布的修

改)将被即将发布的新保险合同准则取代。

因此,当新保险合同准则生效时,暂时性豁

免和“叠加法”预计都将不再适用。

主要要求

关于采用国际财务报告准则第9号的暂时性豁免

国际财务报告准则第4号的修改允许保险公

司在2021年1月1日以前开始的年度期间,继

续运用《国际会计准则第39号—金融工具:

确认和计量》,而不采用国际财务报告准则

第9号,前提是主体的活动需满足“显著与保

险有关”的要求。这项豁免仅在报告主体层

面适用。为了评估活动是否“显著与保险有

关”,主体需要执行两项测试。当且仅当两

项测试都能通过时,保险公司的活动才被视

为显著与保险有关。

第一,保险公司评估因属于国际财务报告准

则第4号范围的合同而产生的债务的账面金

额与所有负债的总账面金额相比是否重大。

第二,保险公司对其与保险有关的负债总账

面金额与所有负债的总账面金额进行比较。

除直接属于国际财务报告准则第4号范围的

合同而产生的债务以外,与保险相关的负债

还包括:

• 适用国际会计准则第39号以公允价值计

量且其变动计入损益的非衍生投资合同

负债;及

• 保险公司因发行上述保险及非衍生投资

合同或因履行此类合同导致的义务而产

生的负债。

如果得出的百分比在下述范围内,即视为通

过第二项测试:百分比大于90%;或者,小于

或等于90%但大于80%且保险公司从事的与

保险无关联的任何活动均不重大。

主体应根据2016年4月1日前最近的年度报

告日的账面金额做出上述评估。在特定情况

下,主体必须或允许重新进行评估。

生效日期

适用于起始日在2018年1月1日或以后开始的年度期间。允许

提前采用。

14 PwC - In depth - New IFRSs for 2017

Overlay approachUnder IFRS 9, certain financial assets have to be measured at fair value through profit or loss; whereas, under IFRS 4, the related liabilities from insurance contracts are often measured on a cost basis. This mismatch creates volatility in profit or loss. By using the ‘overlay approach’, the effect is eliminated for certain eligible financial assets. For these financial assets, an insurer is permitted to reclassify - from profit or loss to other comprehensive income - the difference between the amount that is reported in profit or loss under IFRS 9 and the amount that would have been reported in profit or loss under IAS 39.

Financial assets are eligible for designation for the ‘overlay approach’ if they are measured at fair value through profit or loss under IFRS 9, but not so measured under IAS 39. In addition, the asset cannot be held in respect of an activity that is unconnected with contracts within IFRS 4’s scope. If a designated financial asset no longer meets the eligibility criteria (for example, because it is transferred so that it is now held in respect of an entity’s banking activities or because the entity ceases to be an insurer), it shall be de-designated; in that case, any balance accumulated in other comprehensive income relating to this financial asset is reclassified to profit or loss.

The ‘overlay approach’ is applied retrospectively. Accordingly, the difference between the fair value of the designated financial assets and its carrying amount is recognised as an adjustment to the opening balance of accumulated other comprehensive income. Following the same logic, if the entity stops using the overlay approach, it adjusts the opening balance of retained earnings for the balance of accumulated other comprehensive income.

ImpactBoth the temporary exemption and the ‘overlay approach’ allow entities to avoid temporary volatility in profit or loss that might result from adopting IFRS 9 before the forthcoming new insurance contracts standard. Furthermore, by using the temporary exemption, an entity does not have to implement two sets of major accounting changes within a short period, and it can take into account the effects of the new insurance standard when first applying the classification and measurement requirements of IFRS 9.

Groups that contain insurance subsidiaries should be aware that the temporary exemption only applies at the level of the reporting entity. So, unless the whole group is eligible for the temporary exemption, whilst an eligible insurance subsidiary can continue to apply IAS 39 in its individual financial statements, the subsidiary will have to prepare IFRS 9 information for consolidation purposes. Furthermore, it should be noted that, under both approaches, significant additional disclosures are required.

普华永道—洞察—2017年国际财务报告准则的变化 15

叠加法

国际财务报告准则第9号要求某些金融资产

必须以公允价值计量且其变动计入损益;而

在国际财务报告准则第4号下,保险合同产

生的相关负债常常以成本为基础计量。这

种错配导致损益表产生波动。使用“叠加

法”可消除某些符合条件的金融资产错配

的影响。对于此类金融资产,保险公司可以

对根据国际财务报告准则第9号在损益中列

报的金额与本可根据国际会计准则第39号

在损益中列报的金额之间的差额,进行重

分类—从损益到其他综合收益。

在国际财务报告准则第9号下须以公允价值

计量且其变动计入损益,但在国际会计准

则第39下并非如此分类的金融资产符合指

定为“叠加法”的条件。此外,该资产不得

为与属于国际财务报告准则第4号范围的合

同无关联的活动而持有。如果所指定的一

项金融资产不再满足符合的条件(例如,由

于金融资产被转让,现在这项资产由主体

的银行类活动持有,或者因为主体不再是

一家保险公司),应解除指定;在这种情况

下,其他综合收益中与该金融资产相关的

任何累计余额应重分类计入损益。

“叠加法”追溯适用。因此,所指定的金融

资产的公允价值与其账面金额之间的差异

作为累计其他综合收益的期初余额的调整

确认。同理,如果主体停止使用叠加法,其

应根据累计其他综合收益余额调整留存收

益的期初余额。

影响

暂时性豁免和“叠加法”均允许主体避免可

能因在发布新保险合同准则以前采用国际财

务报告准则第9号而引起的损益的临时性波

动。而且,使用暂时性豁免的主体无需在短

期内先后实施两套主要的会计变更,并能在

首次运用国际财务报告准则第9号的分类与

计量要求时,考虑新保险准则的影响。

包含保险子公司的集团应当注意,暂时性豁

免仅在报告主体层面适用。因此,除非整个

集团满足暂时性豁免的条件,否则,符合条

件的保险子公司可继续在其单独的财务报表

中运用国际会计准则第39号,而该子公司还

将需要根据国际财务报告准则第9号编制用

于报表合并的财务信息。而且,应注意,在这

两种方法下均要求做出大量的补充披露。

16 PwC - In depth - New IFRSs for 2017

Classification and measurement of share-based payment transactions Amendments to IFRS 2, ‘Share based payments’

Effective date

Annual periods beginning on or after 1 January 2018. Early adoption is permitted.

IssueThis amendment addresses the accounting for cash-settled, share-based payments and equity-settled awards that include a ‘net settlement’ feature in respect of withholding taxes.

ImpactThe amendment clarifies the measurement basis for cash-settled, share-based payments and the accounting for modifications that change an award from cash-settled to equity-settled. It also introduces an exception to the principles in IFRS 2 that will require an award to be treated as if it was wholly equity-settled, where an employer is obliged to withhold an amount for the employee’s tax obligation associated with a share-based payment and pay that amount to the tax authority.

InsightMeasurement of cash-settled awardsUnder IFRS 2, the measurement basis for an equity-settled, share-based payment should not be ‘fair value’ in accordance with IFRS 13. However, ‘fair value’ was not defined in connection with a cash-settled, share-based payment, and there has been diversity in practice. The amendment clarifies that the fair value of a cash-settled award is determined on a basis consistent with that used for equity-settled awards. Market-based performance conditions and non-vesting conditions are reflected in the ‘fair value’, but non-market performance conditions and service conditions are reflected in the estimate of the number of awards expected to vest.

This change has most impact where an award vests (or does not vest) based on a non-market condition. Previously, some argued that the fair value of a cash-settled award was determined using the guidance in IFRS 13 and reflected the probability that non-market and service vesting conditions would be met. The amendment clarifies that non-market and service vesting conditions are ignored in the measurement of fair value.

Modification of cash-settled awardsIFRS 2 includes guidance on how to account for a modification that adds a cash alternative to an equity-settled award, but it did not include guidance on how to account for a modification from cash-settled to equity-settled.

A modification to a cash-settled award is reflected immediately in the measurement of fair value. Any incremental value added to an equity-settled award is recognised over any remaining vesting period, and

普华永道—洞察—2017年国际财务报告准则的变化 17

股份支付交易的分类与计量

对《国际财务报告准则第2号—股份支付》的修改

问题

本次修改解决了包含代扣代缴所得税“净

额结算”特征的以现金结算的股份支付及

以权益结算的支付奖励的会计处理问题。

影响 本次修改澄清了以现金结算的股份支付的

计量基础以及将一项以现金结算的支付奖

励变更为权益结算的合同修改的会计处

理。此外,本次修改针对国际财务报告准则

第2号中的原则引入了一项例外规定,该例

外规定当雇主有义务代扣代缴雇员与股份

支付相关的所得税义务金额并上交税务机

关时,支付奖励需完全以权益结算。

见解

以现金结算的支付奖励的计量

在国际财务报告准则第2号下,以权益结算

的股份支付的计量基础不应当是根据国际

财务报告准则第13号确定的“公允价值”。

然而,准则并未对以现金结算的股份支付

的“公允价值” 进行定义,实务中存在不一

致的情况。本次修改澄清了以现金结算的

支付奖励的公允价值根据以权益结算的支

付奖励所用的基础确定。以市场为基础的

业绩条件和非赋权条件均应反映在“公允

价值”中,但非市场业绩条件和服务条件反

映在预计行权的支付奖励数量的估计中。

本次修改对于根据非市场条件行权(或不

行权)的支付奖励的影响最大。以前,有人

提出,以现金结算的支付奖励的公允价值

使用国际财务报告准则第13号的指引确

定,并反映在满足非市场及服务行权条件

的概率中。本次修改澄清,公允价值计量不

考虑非市场及服务行权条件。

以现金结算的支付奖励的修改

国际财务报告准则第2号包含关于以权益结

算的支付奖励增加一项现金备选方案的修

改如何核算的指引,但不包含关于从以现金

结算变更为以权益结算的修改如何核算的

指引。

对以现金结算的支付奖励的修改立即反映

在公允价值计量中。以权益结算的支付奖

励增加的任何增量价值在剩余行权期内确

认,不考虑价值的下跌。

生效日期

适用于起始日在2018年1月1日或以后开始的年度期间。允许

提前采用。

18 PwC - In depth - New IFRSs for 2017

any reduction in value is ignored. The amendment addresses the accounting for a modification that changes both the value and the classification of a cash-settled award and, in particular, clarifies the order in which the changes are applied.

The amendment requires any change in value to be dealt with before the change in classification. The cash-settled award is remeasured, with any difference recognised in the income statement before the remeasured liability is reclassified into equity.

Awards with net settlement featuresTax laws or regulations may require the employer to withhold some of the shares to which an employee is entitled under a share-based payment award, and to remit the tax payable on the award to the tax authority. The Basis for Conclusions paragraphs added to IFRS 2 by the amendments note that IFRS 2 would require such an award to be split into a cash settled component for the tax payment and an equity settled component for the net shares issued to the employee. However the amendment adds an exception that requires the award to be treated as equity-settled in its entirety. The cash payment to the tax authority is treated as if it was part of an equity settlement. The exception would not apply to any equity instruments that the entity withholds in excess of the employee’s tax obligation associated with the share-based payment.

The cash payment to the tax authority might be much greater than the expense that has been recognised for the share-based payment. The amendment says that the entity should disclose an estimate of the amount that it expects to pay to the tax authority in respect of the withholding tax obligation where that is necessary to inform users about the future cash flows.

Who is affected?Entities that have employee share-based payments will need to consider whether or not these changes will affect their accounting. In particular entities with the following arrangements are likely to be effected:

• Cash-settled share-based payments that include performance conditions;

• Equity-settled awards that include net settlement features relating to tax obligations; and

• Cash-settled arrangements that are modified to equity-settled share-based payments.

The changes are effective from 1 January 2018, with early adoption permitted. The transition provisions, in effect, specify that the amendments apply to awards that are not settled as at the date of first application or to modifications that happen after the date of first application, without restatement of prior periods. There is no income statement impact as a result of any reclassification from liability to equity in respect of ‘net settled awards’; the recognised liability is reclassified to equity without any adjustment.

The amendments can be applied retrospectively, provided that this is possible without hindsight and that the retrospective treatment is applied to all of the amendments.

普华永道—洞察—2017年国际财务报告准则的变化 19

本次修改说明了使以现金结算的支付奖

励的价值和分类同时变更的修改如何核

算,以及特别澄清了应用这些变更的顺序。

本次修改要求任何价值的变更应当先于分

类的变更处理。以现金结算的支付奖励重

新计量,任何差异在重新计量的负债重分

类计入权益之前在利润表中确认。

具有净额结算特征的奖励

所得税法律法规可能要求雇主对雇员在股

份支付下有权取得的某些股份代扣代缴所

得税,并向税务机关支付奖励的应付所得

税。本次修改为国际财务报告准则第2号增

加了“结论基础”段,其中指出,该准则将

要求此类支付奖励分成 税金的现金结算部

分和向雇员发行的净额股份的权益结算部

分。但是,本次修改增加了一项例外规定,

要求该奖励完全按照权益结算处理。向税

务机关支付的现金付款视为权益结算的一

部分进行会计处理。 此项例外规定不适用

于主体代扣金额超出与该股份支付相关的

纳税义务的任何权益工具。

向税务机关支付的现金付款可能远远大于

为股份支付确认的费用。本次修改规定,

如果有必要告知使用者主体的未来现金流

量,主体应当披露其预计向税务机关支付

的代扣所得税金额。

哪些主体受到影响?

作出股份支付的主体将需要考虑这些变更

是否会影响其会计处理。特别是,具有下列

安排的主体很可能受到影响:

• 以现金结算的股份支付包含业绩条件;

• 以权益结算的支付奖励包含与所得税义

务相关的净额结算特征;及

• 以现金结算的安排变更为以权益结算的

股份支付。

本次变更自2018年1月1日起生效,允许提

前采用。过渡条款实质上规定,本次修改

适用于首次采用日没有结算的支付奖励,或

在首次执行日后发生的修改,且以前期间无

需重述。“净额结算支付奖励”从负债重分

类计入权益对利润表无影响;所确认的负

债重分类计入权益,且无需进行任何调整。

本次修改可追溯适用,条件是在不使用后

见之明的情况下追溯适用是很可能的,并且

追溯处理应当适用于所有修改。

20 PwC - In depth - New IFRSs for 2017

Transfers of investment propertyAmendments to IAS 40, ‘Investment property’

Effective date

Annual periods beginning on or after 1 January 2018. Early adoption is permitted.

IssueThese amendments clarify when assets are transferred to, or from, investment properties.

ImpactThe amendment clarified that to transfer to, or from, investment properties there must be a change in use. To conclude if a property has changed use there should be an assessment of whether the property meets the definition of an investment property. This change must be supported by evidence. The Board confirmed that a change in intention, in isolation, is not enough to support a transfer.

The issue arose from confusion over whether an entity transfers property under development from inventory to investment property when there is evidence of a change in use that was not explicitly included in the standard. The list of evidence was therefore re-characterised as a non-exhaustive list of examples to help illustrate the principle. The examples were expanded to include assets under construction and development and not only transfers of completed properties.

The Board provided two options for transition.

1. Prospective application. Any impact from properties that are reclassified would be treated as an adjustment to opening retained earnings as at the date of initial application. There are also special disclosure requirement if this option is selected.

2. Retrospective application. This option can only be selected without the use of hindsight.

普华永道—洞察—2017年国际财务报告准则的变化 21

问题

本次修改澄清了资产在什么情况下转入或

转出投资性房地产。

影响

本次修改澄清,转入或转出投资性房地产

必须发生用途变更。为了确定房地产的用

途是否改变了,主体应当评估该房地产是否

满足投资性房地产的定义。变更必须有证

据支持。理事会确认,单纯的意图变更不足

以支持转入/转出。

这一问题产生的背景是,由于没有被修改前

准则列示的用途变更证据清单明确包含,当

有证据支持的用途变更发生时,主体对于

是否能将在建房地产从存货转入投资性房

地产存在疑惑。因此,本次修改将证据清单

重新定性为帮助说明该原则的非完全示例

清单。扩展后的示例清单包含了在建和开发

中的资产,而不仅是已完工房地产的转移。

理事会提供了两项可选择的过渡条款。

1. 未来适用法。房地产重分类产生的任何

影响将作为初始采用日对期初留存收益

的调整。如果选择采用这一方法,还需

要满足特殊的披露要求。

2. 追溯调整法。这一选择权仅可在不使用

后见之明的条件下选用。

投资性房地产转入/转出

对《国际会计准则第40号

—投资性房地产》的修改

生效日期

适用于起始日在2018年1月1日或以后开始的年度期间。允许

提前采用。

22 PwC - In depth - New IFRSs for 2017

IssueIn July 2014, the IASB published the complete version of IFRS 9, ‘Financial instruments’, which replaces the guidance in IAS 39. This final version includes requirements on the classification and measurement of financial assets and liabilities; it also includes an expected credit losses model that replaces the incurred loss impairment model used currently. It also includes the final hedging part of IFRS 9 that was issued in November 2013.

Key provisionsClassification and measurementIFRS 9 has three classification categories for debt instruments: amortised cost, fair value through other comprehensive income (‘FVOCI’) and fair value through profit or loss (‘FVPL’). Classification under IFRS 9 for debt instruments is driven by the entity’s business model for managing the financial assets and whether the contractual cash flows represent solely payments of principal and interest (‘SPPI’). An entity’s business model is how an entity manages its financial assets in order to generate cash flows and create value for the entity. That is, an entity’s business model determines whether the cash flows will result from collecting contractual cash flows, selling financial assets or both.

If a debt instrument is held to collect contractual cash flows, it is classified as amortised cost if it also meets the SPPI requirement. Debt instruments that meet the SPPI requirement that are held both to collect assets’ contractual cash flows and to sell the assets are classified as FVOCI. Under the new model, FVPL is the residual category - financial assets should therefore be classified as FVPL if they do not meet the criteria of FVOCI or amortised cost. Regardless of the business model assessment, an entity can elect to classify a financial asset at FVPL if doing so eliminates or significantly reduces a measurement or recognition inconsistency (‘accounting mismatch’).

Expected credit lossesIFRS 9 introduces a new model for the recognition of impairment losses - the expected credit losses (ECL) model. The ECL model constitutes a change from the guidance in IAS 39 and seeks to address the criticisms of the incurred loss model which arose during the economic crisis. In practice, the new rules mean that entities will have to record a day 1 loss equal to the 12-month ECL on initial recognition of financial assets that are not credit impaired (or lifetime ECL for trade receivables). IFRS 9 contains a ‘three stage’ approach which is based on the change in credit quality of financial assets since initial recognition. Assets move through the three stages as credit quality changes and the stages dictate how an entity measures impairment losses and applies the effective interest rate method. Where there has been a significant increase in credit risk, impairment is measured using lifetime ECL rather than 12-month ECL. The model includes operational simplifications for lease and trade receivables.

DisclosuresExtensive disclosures are required, including reconciliations from opening to closing amounts of the ECL provision, assumptions and inputs and a reconciliation on transition of the original classification categories under IAS 39 to the new classification categories in IFRS 9.

Financial instrumentsIFRS 9

New standards

Effective date

Annual periods beginning on or after 1 January 2018. Early adoption is permitted (see detail below).

普华永道—洞察—2017年国际财务报告准则的变化 23

生效日期 适用于起始日在2018年1月1日或以后的年度期间。允许提前

采用(详情如下)。

金融工具

国际财务报告准则第9号

新准则

问题 I ASB于2014年7月发布了《国际财务报告

准则第9号—金融工具》的完成版,替代了

IAS 39中的指引。这一终版包括金融资产和

负债分类和计量的规定;还包括取代目前所

用的已发生损失减值模型的预期信用损失

模型。它还包括2013年11月发布的IFRS 9

关于套期的终稿。

主要要求

分类和计量

IFRS 9将债务工具分为三类:以摊余成本计

量、以公允价值计量且其变动计入其他

综合收益(“F VOCI”)以及以公允价值计

量且其变动计入当期损益(“F V PL”)。

IFRS 9中对于债务工具的分类主要基于主体

管理金融资产的业务模型,以及合同现金流

是否仅代表本金和利息的支付(“SPPI”)。

主体的业务模式是其管理金融资产以产生现

金流和为自身创造价值的方式。主体的业务

模式决定了现金流来自于以下哪种方式:收

取合同现金流、出售金融资产或两者兼有。

如果持有一项债务工具的目的是为了收取合

同现金流量,且该现金流量满足SPPI的要

求,则该债务工具被分类为以摊余成本计

量的金融资产。如果债务工具的合同现金流

量满足SPPI的要求,且主体的持有目的既

是为了收取资产的合同现金流量又是为了

出售资产,则该债务工具被分类为FVOCI。

新模型下,FVPL是剩余类别—对于既不满

FVOCI,也不满足以摊余成本计量的金融资

产,应当被分类为FVPL。无论业务模式的评

估结果如何,只要可以消除或显著减少计量

或确认上的不一致(“会计错配”),主体即

可选择将一项金融资产分类为FVPL。

预期信用损失

IFRS 9引入了新的减值损失确认模型—预

期信用损失(“ECL”)模型。与IAS 39的要

求相比,预期信用损失模型是一个新的变

化,并且这也是在寻求回应经济危机期间对

已发生损失模型的批判。在实务中,新规定

意味着主体在对未发生信用减值的金融资

产,在初始确认后的首个报告日,将计入相

当于12个月预期信用损失的首日损失(或对

于应收账款确认整个存续期内的预期信用

损失)。IFRS 9采用了基于自初始确认后信

用质量变化的“三阶段”法。随着信用质量

的变化,资产会落入不同的阶段,而对于主

体如何计量减值损失和应用实际利率法,

各阶段有其相应的要求。当信用风险显著

增加时,主体应采用整个存续期内的预期

信用损失而非12个月的预期信用损失计量

减值。对于租赁和应收账款,减值模型中有

相应的简化操作方法。

披露

新准则要求主体进行大量的披露,包括对预

期信用损失准备从期初至期末金额的调节

表、假设和参数的信息,以及从IAS 39中原

分类过渡至IFRS 9中新类别时的调节表。

24 PwC - In depth - New IFRSs for 2017

Hedge accountingHedge effectiveness tests and eligibility for hedge accountingIFRS 9 relaxes the requirements for hedge effectiveness and, consequently to apply hedge accounting. Under IAS 39, a hedge must be highly effective, both going forward and in the past (that is, a prospective and retrospective test, with results in the range of 80%-125%). IFRS 9 replaces this bright line with a requirement for an economic relationship between the hedged item and hedging instrument, and for the ‘hedged ratio’ to be the same as the one that the entity actually uses for risk management purposes. Hedge ineffectiveness will continue to be reported in profit or loss (P&L). An entity is still required to prepare contemporaneous documentation; however, the information to be documented under IFRS 9 will differ.

Hedged itemsThe new requirements change what qualifies as a hedged item, primarily removing restrictions that currently prevent some economically rational hedging strategies from qualifying for hedge accounting. For example:

• Risk components of non-financial items can be designated as hedged items, provided they are separately identifiable and reliably measurable. This is good news for entities that hedge for only a component of the overall price of non-financial items such as the oil price component of jet fuel price exposure), because it is likely that more hedges will now qualify for hedge accounting.

• Aggregated exposures (that is, exposures that include derivatives) can be hedged items.

• IFRS 9 makes the hedging of groups of items more flexible, although it does not cover macro hedging (this will be the subject of a separate discussion paper in the future). Treasurers commonly group similar risk exposures and hedge only the net position (for example, the net of forecast purchases and sales in a foreign currency). Under IAS 39, such a net position cannot be designated as the hedged item; but IFRS 9 permits this

if it is consistent with an entity’s risk management strategy. However, if the hedged net position consists of forecast transactions, hedge accounting on a net basis is only available for foreign currency hedges.

• IFRS 9 allows hedge accounting for equity instruments measured at fair value through other comprehensive income (OCI), even though there will be no impact on P&L from these investments.

Hedging instrumentsIFRS 9 relaxes the rules on the use of some hedging instruments as follows:

• Under IAS 39, the time value of purchased options is recognised on a fair value basis in P&L, which can create significant volatility. IFRS 9 views a purchased option as similar to an insurance contract, such that the initial time value (that is, the premium generally paid for an at or out of the money option) must be recognised in P&L, either over the period of the hedge (if the hedge item is time related, such as a fair value hedge of inventory for six months), or when the hedged transaction affects P&L (if the hedge item is transaction related, such as a hedge of a forecast purchase transaction). Any changes in the option’s fair value associated with time value will be recognised in OCI.

• A similar accounting treatment to options can also be applied to the forward element of forward contracts and to foreign currency basis spreads of financial instruments. This should result in less volatility in P&L.

• Under IAS 39, non-derivative financial items were allowed for hedging of FX risk. The eligibility of non-derivative financial items as hedging instruments is extended to non-derivative financial items accounted for at fair value through P&L.

Accounting, presentation and disclosureThe accounting and presentation requirements for hedge accounting in IAS 39 remain largely unchanged in IFRS 9. However, entities will now be required to reclassify the gains and losses accumulated in equity on a cash flow hedge to the carrying amount of a non-financial hedged item when it is initially recognised. This was permitted under IAS 39, but entities could also choose to accumulate gains and losses in equity. Additional disclosures are required under the new standard.

Own credit risk in financial liabilitiesAlthough not related to hedge accounting, the IASB has also amended IFRS 9 to allow entities to early adopt the requirement to recognise in OCI the changes in fair value attributable to changes in an entity’s own credit risk (from financial liabilities that are designated under the fair value option). This can be applied without having to adopt the remainder of IFRS 9.

Effective date and transitionIFRS 9 is effective for annual periods beginning on or after 1 January 2018. Earlier application is permitted. IFRS 9 is to be applied retrospectively but comparatives are not required to be restated. If an entity elects to early apply IFRS 9 it must apply all of the requirements at the same time.

InsightIFRS 9 applies to all entities. However, financial institutions and other entities with large portfolios of financial assets measured at amortised cost or FVOCI will be the most effected and in particular, by the ECL model. It is critical that these entities assess the implications of the new standard as soon as possible. It is expected that the implementation of the new ECL model will be challenging and might involve significant modifications to credit management systems. An implementation group has been set up by the IASB in order to deal with the most challenging aspects of implementation of the new ECL model.

普华永道—洞察—2017年国际财务报告准则的变化 25

套期会计

套期有效性测试和符合套期会计的条件

IFRS 9放宽了对套期有效性的要求,从而也

放松了对套期会计应用的规范。根据IAS 39,

套期必须在未来和过去均高度有效(即无论

是在预期性和回顾性的测试中,其有效性结

果必须在80%-125%的范围内)。IFRS 9以被

套期项目与套期工具之间须存在经济关系,

及套期比率需与主体实际用于风险管理目的

的套期比率一致的要求替代了IAS 39 内明确

的量化范围。套期无效部分将继续在损益中

反映。主体仍须编制同期的文件记录;但根

据IFRS 9所记录的信息将会有所不同。

被套期项目

新的要求更改了符合被套期项目的条件,主

要是取消了目前使一些经济上合理的套期策

略无法符合套期会计条件的限制。例如:

• 非金融项目的风险成分可被指定为被套

期项目,只要它们可以单独辨认和可靠

计量。这对于仅对非金融项目整体价格

的某一组成部分(例如航空燃料价格中

原油价格敞口部分)进行套期的主体而

言是个好消息,因为这可能将使得更多

的套期符合套期会计的条件。

• 汇总后的风险敞口(即包括衍生工具在

内的风险敞口)可以成为被套期项目。

• IFRS 9中尽管不包括宏观套期(这将在

未来的单独讨论稿中进行探讨),但它使

项目组合套期具有更高的灵活性。企业

司库部门通常将相似的风险敞口进行组

合,并仅对净头寸进行套期(例如,预期

外汇购销的净额)。根据IAS 39,此类净

头寸不能被指为被套期项目;但IFRS 9允

许对此类包括净头寸的项目进行套期会

计处理,前提是这一做法与主体的风险

管理策略相一致。然而,如果被套期净

头寸由预期交易组成,则仅有外币套期

可以净额进行套期会计处理。

• IFRS 9允许对以公允价值计量且其变动计

入其他综合收益的权益工具应用套期会

计,尽管这些投资不会对损益产生影响。

套期工具

IFRS 9放松了关于套期工具使用的规定,具

体如下:

• 根据IAS 39,购入期权的时间价值以公

允价值为基础计入损益,而这可能导致

重大波动性。IFRS 9将购入期权视为类

似于保险合同,从而其初始时间价值(即

一般的情况下为平价期权或价外期权支

付的期权费)必须在套期期间(如果套

期项目与时间相关,例如六个月的存货公

允价值套期)或在被套期交易影响损益

时(如果套期项目与交易相关,例如针对

预期购买交易的套期)计入损益。任何与

时间价值相关的期权公允价值变化将计

入其他综合收益。

• 与期权类似的会计处理也可被应用于远

期合同的远期要素以及金融工具的外汇

基差。这应当会降低利润表的波动性。

• 根据IAS 39,仅允许对外汇风险套期采

用非衍生金融项目作为套期工具。套期

工具的条件有所延伸,以公允价值计量

且其变动计入损益的非衍生金融项目可

以作为套期工具。

会计处理、列报和披露

IAS 39中套期会计的会计处理和列报要求

在IFRS 9中大体保持不变。然而,主体如今

必须将在权益中累计的现金流量套期利得

和损失重分类至非金融性的被套期项目初

始确认时的账面价值。IAS 39中允许这一做

法,但是主体也可选择将利得和损失在权益

中累计。在新准则中要求进行额外披露。

金融负债的自身信用风险

尽管与套期会计不相关,IASB还对IFRS 9

进行了修改,以允许主体提前采用将可归属

于其自身信用风险变化(来自于根据公允价

值选择权指定的金融负债)的公允价值变

动计入其他综合收益的要求。主体可以不

采用IFR S 9中其余的规定,单独采用这一

要求。

生效日期和过渡IFRS 9适用于在2018年1月1日或以后开始

的年度期间。允许提前采用。IFRS 9适用于

追溯调整法,但不要求主体重述比较信息。

如果主体选择提前采用IFRS 9,必须同时

采用所有的要求。

见解IFRS 9适用于所有的主体。但是,对于拥有

大量金融资产组合,而且以摊余成本或公

允价值计量且其变动计入其他综合收益的

金融机构和其他主体,影响将最为显著,特

别是预期信用损失模型的影响。对于这些

主体,尽快评估新准则的影响是至关重要

的。新预期信用损失模型的实施将会相当

具有挑战性,并且可能涉及对信用管理系统

进行重大的修改。IASB已成立一个实施小

组,以应对新的预期信用损失模型实施中

最具有挑战性的方面。

26 PwC - In depth - New IFRSs for 2017

IssueIn May 2014, the IASB issued their long-awaited converged standard on revenue recognition. There are potentially significant changes coming for certain industries, and some level of change for almost all entities.

ImpactThe new standard will affect most entities that apply IFRS. Entities that currently follow industry-specific guidance should expect the greatest impact. Summarised below are some of the areas that could create the most significant challenges for entities as they transition to the new standard.

Transfer of controlRevenue is recognised when a customer obtains control of a good or service. A customer obtains control when it has the ability to direct the use of and obtain the benefits from the good or service. Transfer of control is not the same as transfer of risks and rewards, nor is it necessarily the same as the culmination of an earnings process as it is considered today. Entities will also need to apply new guidance to determine whether revenue should be recognised over time or at a point in time.

Variable considerationEntities might agree to provide goods or services for consideration that varies upon certain future events occurring or not occurring. Examples include refund rights, performance bonuses and penalties. These amounts are often not recognised as revenue today until the contingency is resolved. Now, an estimate of variable consideration is included in the transaction price if it is highly probable that the amount will not result in a significant revenue reversal if estimates change. Even if the entire amount of variable consideration fails to meet this threshold, management will need to consider whether a portion (a minimum amount) does meet the criterion. This amount is recognised as revenue when goods or services are transferred to the customer. This could affect entities in multiple industries where variable consideration is currently not recorded until all contingencies are resolved. Management will need to reassess estimates each reporting period, and adjust revenue accordingly.

There is a narrow exception for intellectual property (IP) licences where the variable consideration is a sales-or usage-based royalty.

Allocation of transaction price based on relative stand-alone selling priceEntities that sell multiple goods or services in a single arrangement should allocate the consideration to each of those goods or services on a relative stand-alone selling price basis. This allocation is based on the price an entity would charge a customer on a stand-alone basis for each good or service.

Revenue from contracts with customersIFRS 15

Effective date

Annual periods beginning on or after 1 January 2018. Early adoption is permitted.

普华永道—洞察—2017年国际财务报告准则的变化 27

与客户之间的合同产生的收入

国际财务报告准则第15号

问题

于2014年5月,IASB发布了期待已久的趋同

的收入确认准则。几乎所有的主体均会受

到不种程度的影响,而对于特定行业将面

临潜在重大的变化。

影响

采用国际财务报告准则的大部分主体将会

受到新准则的影响。而目前遵循特定行业

指引的主体受到的影响预计将最为重大。下

面汇总了主体在向新准则过渡时可能面临

最严峻挑战的一些领域。

控制权的转移

收入于客户取得商品或服务的控制权时予

以确认。当客户能够主导商品或服务的使

用并从中取得收益时即获取了控制权。控制

权的转移不同于风险和报酬的转移,也不一

定与目前所认为的盈利过程的成果相同。

主体还需要应用新指引确定收入是在一段

时间内确认还是在某一时点确认。

可变对价

主体所提供的商品或服务的对价可能会随

着未来某一事项的发生与否而变化。示例

包括退款权利、绩效奖金和罚款。在或有

事项解决之前,该或有金额通常不被确认

为收入。现在,当该金额在估计发生变化

时极可能不会导致收入的重大转回时,对

可变对价的估计才会包括于交易价格中。

即使可变对价的金额不能全部满足这一条

件,管理层仍需考虑是否一部分(最低金

额)能够满足条件,并于商品或服务转移至

客户时将其确认为收入。目前,很多行业中

的主体仅当所有的或有事项解决后方才记

录可变对价,这些主体将受到影响。管理层

将需要在每个报告期间重新评估估计值,

并对收入作出相应调整。

对于知识产权使用许可,当其可变对价是

基于销售额或使用情况的特许权使用费

时,准则对此存在小范围的豁免。

基于相对独立售价分摊交易价格

主体在一项安排中销售多项商品或服务

时,必须将对价分摊至每项商品或服务。这

一分摊是以主体单独向客户收取的每项商

品或服务价格为基础。

生效日期

适用于起始日在2018年1月1日或以后的年度期间。允许提前

采用。

28 PwC - In depth - New IFRSs for 2017

LicencesEntities that license their IP to customers will need to determine whether the licence transfers to the customer over time or at a point in time. A licence that is transferred over time allows a customer access to the entity’s IP as it exists during the licence period. Licences that are transferred at a point in time allow the customer the right to use the entity’s IP as it exists when the licence is granted. The customer should be able to direct the use of and obtain substantially all of the remaining benefits from the licensed IP to recognise revenue when the licence is granted. The standard includes several examples to assist entities making this assessment.

Time value of moneySome contracts provide the customer or the entity with a significant financing benefit (explicitly or implicitly). This is because performance by an entity and payment by its customer might occur at significantly different times. An entity should adjust the transaction price for the time value of money if the contract includes a significant financing component. The standard provides certain exceptions to applying this guidance and a practical expedient which allows entities to ignore time value of money if the time between transfer of goods or services and payment is less than one year.

Contract costsEntities sometimes incur costs (such as sales commissions or mobilisation activities) to obtain or fulfil a contract. Contract costs that meet certain criteria are capitalised as an asset and are amortised as revenue is recognised. More costs are expected to be capitalised in some situations. Management will also need to consider how to account for contract costs incurred for contracts that are not completed upon the adoption of the standard.

DisclosuresExtensive disclosures are required to provide greater insight into both revenue that has been recognised, and revenue that is expected to be recognised in the future from existing contracts. Quantitative and qualitative information will be provided about the significant judgements and changes in those judgements that management made to determine revenue that is recorded.

Effective date and transitionIFRS 15 is effective for annual periods beginning on or after 1 January 2018. Earlier application is permitted.

Entities can apply the revenue standard retrospectively to each prior reporting period presented (full retrospective method) or retrospectively with the cumulative effect of initially applying the standard recognised at the date of initial application in equity (modified retrospective method). Entities that elect to apply the standard using the full retrospective method can apply certain practical expedients.

InsightFinalise nowEntities should ensure that they have identified the key terms of their revenue contracts and determined the impact on their accounting before the effective date of IFRS 15. They should also have implemented the systems and processes to capture the information needed to determine the measurement of revenue, and to prepare the new disclosures.

普华永道—洞察—2017年国际财务报告准则的变化 29

使用许可

向客户授予知识产权使用许可的主体将需

要确定使用许可是在一段时间内还是在某

一时点转移至客户。在一段时间内转移的使

用许可,客户在使用许可期间获得使用主

体存在的知识产权。在某一时点转移的使

用许可,客户在授予使用许可的时点即取得

了该知识产权的使用权力。如果在授予时

点即确认收入,客户必须在被授予时就能

够支配被许可使用的知识产权并获取几乎

全部的剩余收益。准则中包括了多个示例以

帮助主体进行这一评估。

货币的时间价值

一些合同为客户或主体(明确或隐含地)提

供了重大的融资收益。这是因为主体履行

义务的时点和客户付款的时点可能存在显

著不同。如果合同中包括重要的融资成分,

主体应根据货币的时间价值调整交易价

格。如果商品或服务的转移和付款之间的

时间短于一年,准则提供了应用本指引的一

些豁免及实务中的简易处理方法,使主体

免于考虑货币的时间价值。

合同成本

主体有时会发生获取或履行合同的成

本(例如,销售佣金或准备活动)。满足特

定条件的合同成本应被资本化形成资产,并

在收入确认时进行摊销。在一些情况下,预

计会有更多的费用予以资本化。管理层还将

需要考虑对于准则采用时尚未完成的合同

所发生的合同成本如何进行核算。

披露

准则要求主体进行大量的披露,以提供更

多关于现有合同中已确认的收入和预计未

来将确认的收入的信息。对于管理层为所

确认所的收入而做出的重大估计和估计变

更,主体需要提供定量和定性信息。

生效日期及过渡规定

国际财务报告准则第15号自2018年1月1

日或以后开始的年度期间生效,允许提前

采用。

主体可对已列报的每个前期追溯采用新收

入准则(完全追溯法),或追溯采用新收入

准则时将初始应用准则的累积影响在最初

采用日确认在权益中(修正追溯法)。选择

采用完全追溯法的主体可运用某些实务简

便操作方法。

见解

现已终稿

主体应当确保,在国际财务报告准则第15号

的生效日期前识别其收入合同的关键条款,

并确定对其会计处理的影响。此外,主体还

应执行相关系统和程序,以收集必要信息,

用于确定收入的计量及准备新披露。

30 PwC - In depth - New IFRSs for 2017

These amendments comprise clarifications of the guidance on identifying performance obligations, accounting for licences of intellectual property and the principal versus agent assessment (gross versus net revenue presentation permitted). New and amended illustrative examples have been added for each of these areas of guidance. The IASB has also included additional practical expedients related to transition to the new revenue standard. The amendments are effective for annual reporting periods beginning on or after 1 January 2018, with early application permitted.

The amendments do not change the core principles of IFRS 15 however, they clarify some of the more complex aspects of the standard. The amendments could be relevant to a broad range of entities and should be considered as management evaluates the impact of IFRS 15.

ImpactIdentifying performance obligationsThe amendments clarify the guidance for determining when the promises in a contract are ‘distinct’ goods or services and, therefore, should be accounted for separately. The amendments specifically address how an entity determines whether goods or services are ‘separately identifiable’ from other promises in the contract and clarify that the objective is to determine whether the nature of an entity’s promise is to transfer individual goods or services to

the customer, or to transfer a combined item (or items) to which the individual goods and services are inputs.

Licences of IPThe amendments to the licensing guidance clarify when revenue from a licence of IP should be recognised ‘over time’ and when it should be recognised at a ‘point in time’. An entity should be expected to undertake activities that significantly affect the IP to conclude that revenue is recognised over time. The amendment clarifies that activities significantly affect the IP when: (a) the activities are expected to change the form or functionality of the IP or (b) the ability of the customer to obtain benefit from the IP is substantially derived from, or dependent upon, those activities (for example, a brand or logo).

The amendments also clarify when to apply the guidance on recognising revenue for licences of IP with fees in the form of a sales- or usage-based royalty. This guidance only applies when the licence is the predominant item.

Principal versus agent guidanceThe IASB has clarified that the principal in an arrangement controls a good or service before it is transferred to a customer. The amendments make targeted improvements to clarify the relationship between the control principle and the indicators, the ‘unit of account’ for the assessment and how to apply the control principle to services. The IASB also revised the structure of the indicators so that they indicate when the entity is the principal rather than indicate when it is an agent, and eliminated two of the indicators (‘the entity’s consideration is in the form of a commission’ and ‘the entity is not exposed to credit risk’).

Practical expedients on transitionThe amendments introduce additional practical expedients to simplify transition. One expedient allows entities to use hindsight at the beginning of the earliest period presented or the date of initial application (additional option under modified transition method) to account for contract modifications before that date. The second expedient allows entities applying the full retrospective method to elect not to restate contracts that are completed at the beginning of the earliest period presented. In addition, the IASB also allows entities applying modified retrospective method opting out completed contract practical expedient.

Clarifications to IFRS 15Amendments to IFRS 15, ‘Revenue from contracts from customers’

Effective date

Annual periods beginning on or after 1 January 2018. Early adoption is permitted.

普华永道—洞察—2017年国际财务报告准则的变化 31

本次修改包括关于识别履约义务、知识产权

使用许可的会计处理以及主要责任人还是

代理人评估(允许按总额还是净额收入列

报)的指引的澄清,并针对这些指引增加了

新的及修改的示例。国际会计准则理事会

还增加了新收入准则过渡期的相关简易实

务处理方法。本次修改自2018年1月1日或

以后开始的年度报告期间生效,允许提前

采用。

本次修改没有改变国际财务报告准则第15

号的核心原则,但澄清了准则中某些特别复

杂的方面。本次修改适用的主体范围可能

较为广泛,因此,管理层评估国际财务报告

准则第15号的影响时应当予以考虑。

影响

识别履约义务

本次修改澄清关于确定合同承诺是否是“可

明显区分的”商品或服务及因此应当单独进

行会计处理的指引。本次修改还专门述及主

体如何确定商品或服务与其他合同承诺是

否“可单独识别”,并澄清其目的在于确定

主体承诺的性质是向客户转移单项商品或

服务,还是转移由单项商品和服务作为投入

物的合并项目。

知识产权使用许可

关于许可指引的修改澄清了什么情况下知

识产权许可产生的收入应当“在一段时间

内”确认,以及什么情况下应在“某个时

点”确认。主体从事的活动预计对知识产权

产生重大影响的,收入应当在一段时间内

确认。本次修改澄清,当(1)活动预计改变

知识产权的形式或功能,或者(2)客户从

知识产权获得利益的能力源自或取决于这

些活动(例如,品牌或商标)时,活动对知

识产权产生重大影响。

本次修改还澄清了什么情况下适用关于确

认以基于销量或使用情况的特许权使用费

形式收取费用的知识产权产生的收入。此

指引仅适用于使用许可作为占主导地位的

项目的情况。

主要责任人还是代理人的指引

国际会计准则理事会澄清,一项安排的主要

责任人在商品或服务转移给客户之前对该

商品或服务拥有控制权。本次修改做出了针

对性改进,以澄清控制原则与迹象之间的关

系,进行评估的“记账单位”,及控制原则

如何适用于服务。国际会计准则理事会还修

改了“迹象结构”,以表明什么情况下主体

是主要责任人,而不是代理人,并删除两项

迹象(“主体的对价采取佣金形式”及“主

体不承担信用风险”)。

过渡期的简易实务处理方法

本次修改引入额外的简易实务处理方

法,以简化过渡处理。一种简易方法允许

主体在最早列报期间的期初或初始采用日

使用后见之明(在改良过渡法下的补充选

择权),以对该日期前的合同修改进行会

计处理。第二种简易方法允许主体适用完

全追溯调整法,以选择不重述那些在最早

列报期间的期初已完工的合同。此外,国

际会计准则理事会还允许主体运用改良的

追溯调整法,而不采用已完工合同的简易

实务处理方法。

对国际财务报告准则第15号的澄清

对《国际财务报告准则第15号—与客户之间的合同产生的收入》的修改

生效日期

适用于起始日在2018年1月1日或以后开始的年度期间。允许

提前采用。

32 PwC - In depth - New IFRSs for 2017

IssueIn January 2016, the IASB finished its long-standing project on lease accounting and published IFRS 16, ‘Leases’, which replaces the current guidance in IAS 17. This will require far-reaching changes in accounting by lessees in particular.

Key provisionsUnder IAS 17, lessees were required to make a distinction between a finance lease (on balance sheet) and an operating lease (off balance sheet). IFRS 16 now requires lessees to recognise a lease liability reflecting future lease payments and a ‘right-of-use asset’ for virtually all lease contracts. The IASB has included an optional exemption for certain short-term leases and leases of low-value assets; however, this exemption can only be applied by lessees.

LeasesIFRS 16

For lessors, the accounting stays almost the same. However, as the IASB has updated the IAS 17 guidance on the definition of a lease (as well as the guidance on the combination and separation of contracts), lessors will also be affected by the new standard. At the very least, the new accounting model for lessees is expected to impact negotiations between lessors and lessees.

Under IFRS 16, a contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration.

ImpactIFRS 16 is likely to have a significant impact on the financial statements of a number of lessees.

Statement of financial positionThe new standard will affect both the balance sheet and related ratios, such as debt/equity ratios. Depending on the particular industry and the number of lease contracts previously classified as operating leases under IAS 17, the new approach will result in a significant increase in debt on the balance sheet.

Statement of comprehensive incomeLessees will have to present interest expense on the lease liability and depreciation on the right-of-use asset in their income statement. In comparison with operating leases under IAS 17, this will change not only the allocation of expenses but also the total amount of expenses recognised for each period of the lease term. The combination of a straight-line depreciation of the right-of use asset and the effective interest rate method applied to the lease liability will result in a higher total charge to profit or loss in the initial years of the lease, and decreasing expenses during the latter part of the lease term.

Effective date

Annual periods beginning on or after 1 January 2019. Early adoption is permitted if IFRS 15 is applied.

普华永道—洞察—2017年国际财务报告准则的变化 33

租赁

国际财务报告准则第16号

概述

国际会计准则理事会(“I A SB”)完成了

旷日持久的租赁会计项目,并于2 016年1月13日发布了《国际财务报告准则第16

号—租赁》(“IFRS 16”),以此取代现行

指引—IAS 17。这将对特别是承租人的会

计处理产生深远的变化。

主要规定

根据IAS 17规定,承租人应把租赁区分为融资

租赁(上表)和经营租赁(不上表)IFRS 16则

要求承租人将几乎所有的租赁合同,按未来

租赁付款额确认为一项租赁负债和相对应

的“使用权资产”。IASB针对短期租赁和价值

较低资产的租赁进行了豁免,但仅适用于承

租人。

生效日期

适用于起始日在2019年1月1日或以后开始的年度期间。允许

已采用IFRS 15的主体提前采用。

出租人的会计处理几乎保持不变。但是,因

为IASB更新了租赁的定义、转租以及合同的

合并和分拆等指引,出租人仍可能受到新准

则的影响。至少,新的承租人会计处理模型

预计将影响出租人与承租人之间租赁安排

的商业谈判。

IFRS 16规定,如果相关合同赋予在一段时间

内控制一项已识别资产的使用权来换取对

价,则该合同中包含租赁。

影响

IFRS 16将会对很多承租人的财务报表产生

重大影响。

资产负债表

新准则将影响资产负债表以及相关的比

率,如负债权益率。视乎行业的类型和根据

IAS 17分类为经营租赁的合同数量,新的会

计方法将会导致资产负债表中的负债大幅

增加。

综合收益表

承租人需在利润表中列报租赁负债的利息

费用以及使用权资产的折旧。与IAS 17的经

营租赁相比,有关改变不仅是费用的科目名

称,而且还将影响每个租赁期间所确认的

费用总额。对使用权资产按照直线法计提

折旧,并对租赁负债采用实际利率法,将导

致较高的费用总额在租赁期的前几年计入

损益,而降低租赁后期的费用。

34 PwC - In depth - New IFRSs for 2017

Statement of cash flowsThe new guidance will also change the cash flow statement, because lease payments that relate to contracts that have previously been classified as operating leases are no longer presented as operating cash flows in full. Only the part of the lease payments that reflects interest on the lease liability can be presented as an operating cash flow (if it is the entity’s policy to present interest payments as operating cash flows). Cash payments for the principal portion of the lease liability are classified within financing activities. Payments for short-term leases, for leases of low-value assets and variable lease payments not included in the measurement of the lease liability are presented within operating activities.

TransitionIFRS 16 is effective for annual reporting periods beginning on or after 1 January 2019. Earlier application is permitted, but only in conjunction with IFRS 15, ‘Revenue from Contracts with Customers’. In order to facilitate transition, entities can choose a ‘simplified approach’ that includes certain reliefs related to the measurement of the right-of-use asset and the lease liability, rather than full retrospective application; furthermore, the ‘simplified approach’ does not require a restatement of comparatives. In addition, as a practical expedient entities are not required to reassess whether a contract is, or contains, a lease at the date of initial application (that is, such contracts are ‘grandfathered’).

InsightStart preparing nowEntities should ensure that they have implemented systems and processes to identify all lease contracts, to capture the information needed to determine the measurement of the right-of-use asset and the lease liability, and to prepare the new disclosures.

普华永道—洞察—2017年国际财务报告准则的变化 35

现金流量表

新指引还将改变现金流量表。之前被分类

为经营租赁的合同相关的租赁付款不再全

额列报为经营活动现金流量,只有租赁负

债利息支出的部分才可以作为经营活动现

金流量进行列报(如果主体选择将利息支

付作为经营活动现金流量列报的会计政

策)。租赁负债本金的支付将作为融资活动

现金流。短期租赁、价值较低的资产租赁及

未包含在租赁负债中的可变租赁款则列示

为经营活动现金流。

过渡

IFRS 16适用于起始日在2019年1月1日或以

后开始的年度报告期间。只有在已采用《国

际财务报告准则第15号—收入》时才允许

提前应用IFRS 16。为了便于过渡,主体可选

择“简易法”而不使用追溯调整法,该方法

包含一些使用权资产和租赁负债计量相关

的豁免;此外,“简易法”不要求重述比较数

据。同时,作为实务的豁免,对于初始采用日

已存在的合同,主体无需重新按照新的准则

评估其是否包含租赁(即,豁免该类合同)。

见解

现在开始准备

主体应确保其系统和程序能识别所有的租

赁合同,并获取确定使用权资产和租赁负

债的计量及编制新的披露所需的信息。

36 PwC - In depth - New IFRSs for 2017

Annual improvements 2014-2016 cycle

Annual improvements 2014-2016

Standard/Interpretation Amendment Effective date

Amendment to IFRS 1, ‘First time adoption of IFRS’.

This amendment deletes the short-term exemptions covering transition provisions of IFRS 7, IAS 19, and IFRS 10. These transition provisions were available to entities for passed reporting periods and are therefore no longer applicable.

Annual periods starting on or after 1 January 2018.

IFRS 12, ‘Disclosure of interests in other entities’.

This amendment clarifies that the disclosure requirement of IFRS 12 is applicable to interest in entities classified as held for sale except for summarised financial information (para B17 of IFRS 12). Previously, it was unclear whether all other IFRS 12 requirements were applicable for these interests.

The objective of IFRS 12 was to provide information about nature of interests in other entities, risks associated with these interests, and the effect of these interests on financial statements. The Board noted that this objective is relevant to interests in other entities regardless of whether they are classified as held for sale.

Should be applied retrospectively for annual periods beginning on or after 1 January 2017.

IAS 28, ‘Investments in associates and joint ventures’.

IAS 28 allows venture capital organisations, mutual funds, unit trusts and similar entities to elect measuring their investments in associates or joint ventures at fair value through profit or loss (FVTPL). The Board clarified that this election should be made separately for each associate or joint venture at initial recognition.

Should be applied retrospectively for annual periods beginning on or after 1 January 2018.

Effective date

See final column in table below.

普华永道—洞察—2017年国际财务报告准则的变化 37

2014-2016年年度改进项目

2014-2016年年度改进项目

准则/解释 修改 生效日期

对《国际财务报告准则第1号—首次采用国际财务报告准则》的修改

该修改删除了IFRS 7、IAS 19及IFRS 10过渡条款涉及的短期豁免。相关过渡条款适用于主体的过往报

告期间,因此不再继续适用。

于2018年1月1日或以后开始的年度期间。

国际财务报告准则第12号—在其他主体中的权益披露》

该修改作出澄清,IFRS 12的披露要求适用于被分类为持有待售的在其他主体中的权益,但不包含披露汇

总财务信息的要求(IFRS 12第B17段)。此前,尚不明确IFRS 12所有其他要求是否适用于该等权益。

IFRS 12旨在提供下列情况的相关信息:在其他主体中权益的性质及相关风险;以及该等权益对财务报

表的影响。理事会指出,该目标与在其他主体中的权

益相关,无论该等权益是否被分类为持有待售。

应于2017年1月1日或以后开始的年度期间追溯适用。

《国际会计准则第28号—对联营和合营的投资》

IAS 28允许风险资本组织、共同基金、信托公司及 类似主体选择以公允价值计量且其变动计入损 益(“FVTPL”)的方式对联营投资或合营投资进行计量。理事会澄清,该选择应当分别针对每项联营投资

或合营投资在初始确认时做出。

应于2018年1月1日或以后开始的年度期间追溯适用。

生效日期

请参见下表最后一列。

38 PwC - In depth - New IFRSs for 2017

IFRIC 22

Foreign currency transactions and advance consideration

Effective date

Annual periods beginning on or after 1 January 2018. Early adoption is permitted.

IssueThis interpretation considers how to determine the date of the transaction when applying the standard on foreign currency transactions, IAS 21. The Interpretation applies where an entity either pays or receives consideration in advance for foreign currency-denominated contracts.

The date of the transaction determines the exchange rate to be used on initial recognition of the related asset, expense or income. The issue arises because IAS 21 requires an entity to use the exchange rate at the ‘date of the transaction’, which is defined as the date when the transaction first qualifies for recognition. The question therefore is whether the date of the transaction is the date when the asset, expense or income is initially recognised, or the earlier date on which the advance consideration is paid or received, resulting in recognition of a prepayment or deferred income.

The Interpretation provides guidance for when a single payment/receipt is made, as well as for situations where multiple payments/receipts are made. The guidance aims to reduce diversity in practice.

Key provisionsSingle payment/receiptThe Interpretation states that the date of the transaction, for the purpose of determining the exchange rate to use on initial recognition of the related item, should be the date on which an entity initially recognises the non-monetary asset or liability arising from the advance consideration.

Example - Single upfront paymentSupplier enters into a contract with a customer on 1 January 20x1 and receives the full consideration of CU50 on this date. The goods are delivered and revenue is recognised on 31 March 20x1.

The Interpretation requires that:

• Supplier will recognise a non-monetary contract liability, translating CU50 at the exchange rate on 1 January 20x1.

• Supplier will recognise revenue at 31 March 20x1 (that is, the date on which the goods are transferred to the customer). Supplier will derecognise the non-monetary contract liability. Revenue will be recognised at the same amount in functional currency, using the exchange rate at the date of the transaction, which is 1 January 20x1. In this case, the amount of revenue is the same as the amount of the non-monetary contract liability derecognised.

Multiple receipts/paymentsThe Interpretation states that, if there are multiple payments or receipts in advance of recognising the related item, the entity should determine the date of the transaction for each payment or receipt.

The illustrative examples accompanying the Interpretation provide guidance on multiple receipts/payments when:

• revenue is recognised at a single point in time;

• services are purchased over a period of time; and

• revenue is recognised at multiple points in time.

普华永道—洞察—2017年国际财务报告准则的变化 39

外币交易和预付/预收对价

国际财务报告解释公告第22号

生效日期

适用于起始日在2018年1月1日或以后开始的年度期间。允许

提前采用。

问题 本项解释公告考虑在适用外币交易准

则(国际会计准则第21号)时如何确定交易

日期。该解释公告适用于涉及主体预付或

预收对价的外币合同。

交易日期决定了初始确认相关资产、费用或

收入时所用的汇率。这一问题源自国际会计

准则第21号关于主体必须使用“交易日”汇

率的要求,交易日的定义是交易首次符合确

认条件的日期。因此,关键问题是,交易日

是否是资产、费用或收入的初始确认日,还

是预付款或递延收入确认的支付或收取预

付对价的更早日期。

该解释公告为单笔付款 /收款和多笔付

款/收款均提供了指引,以便减少实务操作

中的不一致。

主要条款

单项付款/收款

解释公告规定,为确定用于相关项目初始确

认的汇率,交易日应为主体初始确认预付/

预收对价产生的非货币资产或负债的日期。

示例—单笔预付款

某供应商与客户于20x1年1月1日订立一项合

同,并于当日收到全部对价50元。供应商于

20x1年3月31日交付商品并确认相关收入。

该解释公告规定:

• 供应商应确认一项非货币性合同负

债,并按照20x1年1月1日的汇率对50元

进行折算。

• 供应商应于20x1年3月31日(向客户转

让商品当日)确认收入。同时,供应商

应终止确认上述非货币合同负债,并以

功能货币确认相同金额的收入,按交易

日(20x1年1月1日)汇率进行折算。在此

情况下,确认的收入金额应等于终止确

认的非货币合同负债金额。

多笔收款/付款

该解释公告规定,若在确认相关项目前存

在多笔付款或收款,则主体应分别针对每

笔付款或收款确定交易日。

解释公告中的示例针对多笔收款/付款提供

指引,适用下列情形:

• 于单个时点确认收入;

• 在一段时间内购买服务;及

• 分多个时点确认收入。

40 PwC - In depth - New IFRSs for 2017

Example - Revenue recognised at a single point in time with multiple paymentsSupplier enters into a contract with a customer on 1 January 20x1 to deliver goods in exchange for total consideration of CU50 and receives an upfront payment of CU20 on this date. The goods are delivered and revenue is recognised on 31 March 20x1. CU30 is received on 1 April 20x1 in full and final settlement of the purchase consideration.

The Interpretation requires that:

• Supplier will recognise a non-monetary contract liability, translating CU20 at the exchange rate on 1 January 20x1.

• Supplier will recognise revenue at 31 March 20x1 (that is, the date on which it transfers the goods to the customer).

• On 31 March 20x1, Supplier will:

– derecognise the non-monetary contract liability of CU20 and recognise CU20 of revenue using the same exchange rate (that is, the exchange rate at 1 January 20x1); and

– recognise revenue and a receivable for the remaining CU30, using the exchange rate on 31 March 20x1.

• The receivable of CU30 is a monetary item, so it should be translated using the closing rate until the receivable is settled.

ImpactThis Interpretation will impact all entities that enter into foreign currency transactions for which consideration is paid or received in advance. The most significant impact is expected for entities that enter into long-term crossborder/foreign currency contracts, with significant upfront payments. Such arrangements are common in the construction industry and will impact both the supplier and their customers (for example, shipping and airlines).

Effective date and transitionThe amendment is effective for annual periods beginning on or after 1 January 2018. Earlier application is permitted. Entities can choose to apply the Interpretation:

• retrospectively for each period presented;

• prospectively to items in scope that are initially recognised on or after the beginning of the reporting period in which the Interpretation is first applied; or

• prospectively from the beginning of a prior reporting period presented as comparative information.

普华永道—洞察—2017年国际财务报告准则的变化 41

示例—于单一时点针对多笔付款确认收入

某供应商与客户于20x1年1月1日订立一项

总对价为50元的商品交付合同,并于当日收

到20元的预付款。供应商于20x1年3月31日

交付商品并确认相关收入。随后于20x1年4

月1日收到所有剩余对价30元。

该解释公告规定:

• 供应商应确认一项非货币性合同负债,

并按照20x1年1月1日的汇率对20元进

行折算。

• 供应商应于20x1年3月31日(即其向客户

转移商品的日期)确认收入。

• 于20x1年3月31日,供应商将:

– 终止确认非货币性合同负债20元,并

按相同的汇率(即20x1年1月1日的汇

率)确认20元收入;及

– 针对30元的未付尾款确认收入和应

收款,并按20x1年3月31日的汇率进

行折算。

• 30元的应收款为一项货币项目,因此在

付清之前应按期末汇率进行折算。

影响

该解释公告将对从事涉及预付或预收对价

外币交易的所有主体产生影响。预计订立涉

及大笔预付款的长期跨境/外币合同的主体

所受影响最大。该等合同在建筑行业中较

为普遍,供应商及客户(例如航运公司及航

空公司)均将受影响。

生效日期及过渡期

该修改将于2018年1月1日或以后开始的年

度期间生效,并允许提前采用。主体在应用

该解释公告时可选择:

• 对每个列报期间追溯适用;

• 对在首次采用解释公告的报告期期初或

之后初始确认的、属于范围内的项目未

来适用;或

• 作为比较信息列报的的上一报告期期初

开始未来适用。

42 PwC - In depth - New IFRSs for 2017

Acknowledgements致谢

Dorothy Leung | 梁少宝Accounting Consulting Services Director会计专业咨询服务总监

Yuhui Sun | 孙宇辉Accounting Consulting Services Director 会计专业咨询服务总监

Lisa Zhang | 张宇晖Accounting Consulting Services Director 会计专业咨询服务总监

Yinan Lu | 卢翊楠Accounting Consulting Services Senior Manager会计专业咨询服务高级经理

Li Chen | 陈立Accounting Consulting Services Senior Manager会计专业咨询服务高级经理

Mercury Ye | 叶子Accounting Consulting Services Manager会计专业咨询服务经理

Sepcial thanks to the following individuals for their contributions to the translation and production of this publication.

特别感谢以下参与本出版物翻译及编制的普华永道成员及其所做的贡献。

普华永道—洞察—2017年国际财务报告准则的变化 43

PwC assurance services contacts联系普华永道审计业务部

Beijing | 北京梁伟坚 Thomas Leung+86 (10) 6533 [email protected]

Chengdu | 成都黄锦龙 Bob Huang+86 (28) 6287 [email protected]

Chongqing | 重庆李松波 Bobby Lee+86 (23) 6393 [email protected]

Dalian | 大连 关兆文 Dorman Kwan+86 (411) 8379 [email protected]

Guangzhou | 广州张展豪 A1bert Cheung+86 (755) 8261 [email protected]