in depth ib draft 04 30 13 - utah legislaturele.utah.gov/interim/2013/pdf/00001946.pdf · by...

TRANSCRIPT

UTAH STATE LEGISLATURE 2013 INTERIM

OFFICE OF THE LEGISLATIVE FISCAL ANALYST i MAY 9, 2013, 10:15 AM

LFA LEGISLATIVE FISCAL ANALYST

FIVE YEAR PROJECTIONS

EXECUTIVEAPPROPRIATIONSCOMMITTEESTAFF:THOMASYOUNG,PH.D.,ANDREAWILKO,PH.D.,ANGELAJ.OH,&STEVENALLRED I S SUE BR I E F

EXECUTIVESUMMARY

Thisstudypresentsafiveyearoutlookofcashinflow,cashoutflow,financialobligations,anddebtservicecommitmentsoftheStateofUtahbaseduponamethodologyproposedbytheGovernmentalAccountingStandardsBoard(GASB).Itisintendedtoprovidelegislatorswithusefulinformationtomakelongtermrevenueandexpendituredecisions,whilesimultaneouslytestingtoseeifGASB’sguidelinesarepracticable.ThestudyconcludesthattheGeneralandEducationFundsareonsustainabletrajectoriesandthatUtahisontargettomeetlong‐termfinancialobligationslikedebtserviceandretirement.Itfindsthatprojectedtransportationoutlaylevelsarenotsustainableoverthefiveyearperiodgivenassociatedincomeprojections.Thestudynotesthatthesinglelargestcomponentofcashinflow–federalgrantsandaid–iscurrentlyatriskduetofederaldeficitreduction.Finally,thestudycomparesGASB’sproposedmethodologytoobservedexperienceinFY2013andrecommendsusingtheGASBmethodologyonlywhendonesoinconjunctionwithUtah’sexistingconsensusprocesses.

Fund Type / Area

Education Fund General Fund Transportation

Budget Position

Cash Inflow

Cash Outflow

Budget Position

Cash Inflow

Cash Outflow

Budget Position

Cash Inflow

Cash Outflow

-10B

0B

10B

20B

30B

40B

50B

Am

ount 1

7,8

57

,85

6,0

00

18

,47

7,7

53

,00

0

61

9,8

97

,00

0

36

,98

6,4

70

,00

0

37

,32

6,4

16

,00

0

33

9,9

46

,00

0

15

,97

7,5

93

,00

0

11

,07

0,0

61

,00

0

-4,9

07

,53

2,0

00

Five Year Budget Position ProjectionFY 13 - FY 17

Area

Budget Position

Cash Inflow

Cash Outflow

Source: LFA

MAY 9, 2013, 10:15 AM ii OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

Theprojectionscontainedinthisstudyarebaseduponhistoricalexperienceadjustedforknownfactors,suchasearmarkadjustmentsortaxpolicychanges.Onthecashinflowsideofthebalancesheet,best‐fitmodelsfor14broadrevenuesourcecategoriesdepositedintofivefundswereforecast.Thecashoutflowportionincludedbest‐fitprojectionsforninebroadexpenditurecategories.Themajorcashoutflowareasincludepubliceducation,humanservices,healthandenvironmentalquality,highereducation,andallothergovernmentalexpenditures.HistoricaltrendmodelsindicatethatcashinflowassociatedwiththeGeneralFundandEducationFundwillbemorethanenoughtocoveranticipatedcashoutflow,withanestimatedGeneralFundbudgetpositionattheendofFY2017of+$340.0millionon$37.0billionincashoutflowandanestimatedEducationFundbudgetpositionattheendofFY2017of+$620.0millionon$17.9billionincashoutflow.Theoppositeholdstruefortransportationrelatedexpenditures,withthecumulativeprojectedshortfallfromFY2012toFY2017of$4.9billiononprojectedcumulativecashoutflowof$16.0billion.Thismayberelatedtohigherlevelsofdebtfinancedinvestmentoverthepastfiveyears.ArecentredefinitionoftheTransportationInvestmentFundasacapitalprojectfundmaychangethetreatmentoftransportationexpendituresunderGASBproposedguidelines.Ifcurrenttrendsandlegislativepracticeshold,UtahshouldalsobeontracktopayourconstitutionallyrequireddebtobligationsandotherfinancialobligationssuchasretirementandOtherPost‐EmploymentBenefits(OPEB).Utah’sConstitutionrequiresrepaymentofbondedindebtednessasafirstpriority.TheLegislaturehasreflectedthisinitsbudgetrulesandfullyfundsdebtserviceasapractice.LegislatorsconsistentlycommittomeetingretirementandOPEBobligationsbyfullyfundingannualrequiredcontributionsandpayrollrates.Further,theLegislatureisregularlyreformingretirementandOPEBbenefitplanstoreducefutureobligations.UnderGASB’spreliminaryview,statesmustalsoexamineandcommentonanyfinancialinterdependencies.Federalcontracts,grantsandaidareUtah’ssinglelargestcashinflowdefinedinthisstudy.Thiscashinflowisatrisknotonlyduetoknownpolicieslikesequestrationandthedebtceilings,butwilldiminishasthefederalgovernmentreducesitsdeficitinthelongrun.ThisreportrecognizesanddisclosestheriskassociatedwithfederalinterdependencyinComponent5.GASB’sproposedguidelineslimittheinputstoaprojectionmodel.Bydesign,theGASBmethodologydoesnotallowforchangingeconomicindicatorsnordoesitreflectpolicymakerdiscretion.Thus,theresultsofthismethodologywilldifferfromthoseofUtah’sexistingconsensusforecastandbudgetingprocesses.ComparingourinterpretationoftheGASBguidelinestoactualresultsfromtheFY2013GeneralSessionshowstheGASBmodeltoslightlyunder‐estimatecashinflowandslightlyover‐estimatecashoutflow.Assuch,thisreportrecommendsusingGASB’smethodologyonlywhendonesoinconcertwithUtah’sestablishedprocessessothatthedifferencescanbefullyknown,understood,andexplained.

OFFICE OF THE LEGISLATIVE FISCAL ANALYST iii MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

TableofContents

EXECUTIVESUMMARY................................................................................................................................................I

INTRODUCTION.........................................................................................................................................................1

RECOMMENDATIONS.................................................................................................................................................1

BACKGROUND............................................................................................................................................................1

GOVERNMENTALACCOUNTINGSTANDARDSBOARD(GASB)................................................................................2

COMPONENTSOFFISCALSUSTAINABILITY...............................................................................................................2

PURPOSEOFGASBPROPOSEDGUIDELINES............................................................................................................2

DEFINITIONS.............................................................................................................................................................3

GASB’SPROPOSEDMETHODOLOGYFORFINANCIALPROJECTION.........................................................................3

METHODOLOGY.........................................................................................................................................................4

COMPONENT1:PROJECTIONSOFCASHINFLOWS....................................................................................................4

GENERALFUNDCASHINFLOW................................................................................................................................................................7 GENERALFUNDKNOWNCAUSESOFFLUCTUATION........................................................................................................................7

GENERALFUNDRESTRICTEDCASHINFLOW......................................................................................................................................10 GENERALFUNDRESTRICTEDKNOWNCAUSESOFFLUCTUATIONS............................................................................................10

EDUCATIONFUNDCASHINFLOW.........................................................................................................................................................11 EDUCATIONFUNDKNOWNCAUSESOFFLUCTUATIONS...............................................................................................................11

TRANSPORTATIONFUNDCASHINFLOW.............................................................................................................................................14 TRANSPORTATIONFUNDKNOWNCAUSESOFFLUCTUATIONS...................................................................................................14

TRANSPORTATIONINVESTMENTFUNDCASHINFLOW.....................................................................................................................17 TRANSPORTATIONINVESTMENTFUNDKNOWNCAUSESOFFLUCTUATIONS...........................................................................17

ALCOHOLICBEVERAGECONTROL’SENTERPRISEFUNDCASHINFLOW..........................................................................................19 DABCKNOWNCAUSESOFFLUCTUATIONS...................................................................................................................................19

COMPONENT2:PROJECTIONSOFMAJORAREACASHOUTFLOWS......................................................................20

GENERALFUNDCASHOUTFLOW.........................................................................................................................................................20

HUMANSERVICESCASHOUTFLOW......................................................................................................................................................21 HUMANSERVICESKNOWNCAUSESOFFLUCTUATIONS...............................................................................................................22

HEALTHANDENVIRONMENTALQUALITYCASHOUTFLOW.............................................................................................................24 HEALTHANDENVIRONMENTALQUALITYKNOWNCAUSESOFFLUCTUATIONS.......................................................................24

HIGHEREDUCATIONCASHOUTFLOW.................................................................................................................................................26 HIGHEREDUCATIONKNOWNCAUSESOFFLUCTUATIONS...........................................................................................................26

PUBLICEDUCATIONCASHOUTFLOW..................................................................................................................................................28 PUBLICEDUCATIONKNOWNCAUSESOFFLUCTUATIONS............................................................................................................28

TRANSPORTATIONCASHOUTFLOW.....................................................................................................................................................30 TRANSPORTATIONKNOWNCAUSESOFFLUCTUATIONS..............................................................................................................30

DEPARTMENTOFALCOHOLICBEVERAGECONTROLCASHOUTFLOW............................................................................................33

ALLOTHERGOVERNMENTCASHOUTFLOW.......................................................................................................................................34

MAY 9, 2013, 10:15 AM iv OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

GASBMODELSVERSUSCURRENTPROJECTIONSOFREVENUE...........................................................................35

GENERALFUNDREVENUE.....................................................................................................................................................................35

EDUCATIONFUNDREVENUE.................................................................................................................................................................36

TRANSPORTATIONFUNDREVENUE.....................................................................................................................................................39

TRANSPORTATIONINVESTMENTFUNDREVENUE.............................................................................................................................41

DABCREVENUE.....................................................................................................................................................................................43

GASBMODELSVERSUSCURRENTPROJECTIONSOFEXPENDITURES..................................................................45

HUMANSERVICESEXPENDITURES.......................................................................................................................................................45

HEALTHANDENVIRONMENTALQUALITYEXPENDITURES...............................................................................................................48

HIGHEREDUCATIONEXPENDITURES...................................................................................................................................................50

PUBLICEDUCATIONEXPENDITURES....................................................................................................................................................52

TRANSPORTATIONEXPENDITURES.......................................................................................................................................................54

TRANSPORTATIONINVESTMENTEXPENDITURES..............................................................................................................................56

DABCEXPENDITURES...........................................................................................................................................................................58

ALLOTHERGOVERNMENTALEXPENDITURES....................................................................................................................................60

COMPONENT3:TOTALFINANCIALOBLIGATIONS................................................................................................62

COMPONENT4:DEBTSERVICE.............................................................................................................................65

COMPONENT5:GOVERNMENTALINTERDEPENDENCE.........................................................................................67

ECONOMICANDDEMOGRAPHICFACTORSIMPACTINGFUTURESTATERESOURCES...........................................71

CAUTIONARYNOTICEPROPOSEDBYGASB.........................................................................................................72

DATACOLLECTION.................................................................................................................................................73

FORECASTINGISSUES.............................................................................................................................................77

CONCLUSION...........................................................................................................................................................78

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 1 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

INTRODUCTION

Thefive‐yearbudgetprojectionthatfollowsservesatwofoldpurpose:

1) TotesttheviabilityofGASB’sproposalonEconomicConditionReporting:FinancialProjections;and

2) ToassesstheeconomicsustainabilityofUtah’scurrentrevenueandexpendituretrends.

Toaccomplishthesetwoobjectives,weusedbest‐fitmodelsappliedonlytohistoricalexperienceandknownfactorstoprojectthetrendinrevenuesandexpenditures.ThemodelingemployedeitherStatisticalAnalysisSoftware(SAS)orForecastProanalysissoftware.DuetothelimitationsimposedbytheproposedGASBmethodology,weexcludedprojectedeconomicindicatorsfromtheanalysis.

Thetrendapproachledtothefollowingconclusions:

1) OverthecomingfiveyearsUtahisonasustainabletrajectorywhencomparingthetrendrevenuesagainstthetrendexpendituresforallexpenditurestypesexcepttransportation;

2) UtahisalsoonasustainabletrajectorywithrespecttodebtpaymentandotherfinancialobligationsincludingretirementandOPEBaslongascurrenttrendscontinue;and

3) Onlyusingtrenddatacreatessomesignificantshortcomingsintheforecastresults.Inparticular,thepoliticalwilloftheoversightbodyisnottakenintoconsideration.Additionally,theoveralleconomicwellbeingoftheStateanddiversificationoftheState’seconomyarenotconsideredundertheproposedGASBmethodology.

RECOMMENDATIONS

PresumingtheStateisrequiredtouseGASB’sproposedmethodology,werecommendthatitbeusedincombinationwiththeState’sconsensusrevenueprocessinordertoassessthelimitationsofone‐factortrendmodelingandtoaddresspotentialconcernsinthebudgetingprocess.

Wealsorecommendallowingsufficientleadtimetoproduceareport.Datafortheyear‐endisusuallynotavailableuntillateSeptember.IncludingthedataintheState’sComprehensiveAnnualFinancialReport(CAFR)coulddelaythepublicationofthereport.

BACKGROUND

JointRule3‐2‐502statesthat,“eachyear,theExecutiveAppropriationsCommitteeshallselectastateagency,institution,orprogramtobethesubjectofanin‐depthbudgetreview.”BecauseUtahisknownforearlyadoptionofgoodfinancialpractices,duringtheMay15,2012ExecutiveAppropriationsCommitteemeeting,theLegislativeFiscalAnalyst(LFA)recommendedafive‐yearfiscalsustainabilityreviewtohelplegislatorsassessUtah’seconomiccondition.

Thisin‐depthbudgetreviewismeanttoprovidelegislatorswithusefulinformationinplanninglongtermrevenueandexpendituredecisions,whilesimultaneouslytestingtoseeifGASB’sguidelinesarepracticable.Thein‐depthbudgetreviewprimarilyfocusesontheGeneral,Education,Transportation,andTransportationInvestmentfunds.

BecauseofitsimpactontheGeneralFund,theDepartmentofAlcoholicBeverageControl’sEnterpriseFundhasalsobeenincludedintheanalysis.

MAY 9, 2013, 10:15 AM 2 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

GOVERNMENTALACCOUNTINGSTANDARDSBOARD(GASB)

TheGovernmentalAccountingStandardsBoard(GASB)isanindependentorganizationthatestablishesandimprovesstandardsofaccountingandfinancialreportingforstateandlocalgovernmentsintheUnitedStates.GASBwasestablishedin1984byagreementoftheFinancialAccountingFoundation(FAF)and10nationalassociationsofstateandlocalgovernmentofficials.GASBisrecognizedbygovernments,theaccountingindustry,andthecapitalmarketsastheofficialsourceofgenerallyacceptedaccountingprinciples(GAAP)forstateandlocalgovernments.

GASBisnotagovernmententity;instead,itisanoperatingcomponentoftheFAF,whichisaprivatesectornot‐for‐profitentity.Itsstandardsarenotfederallawsorregulationsandtheorganizationdoesnothaveenforcementauthority.CompliancewithGASB’sstandards,however,isenforcedthroughthelawsofsomeindividualstatesandthroughtheauditprocess,whenauditorsrenderopinionsonthefairnessoffinancialstatementpresentationsinconformitywithGAAP1.

COMPONENTSOFFISCALSUSTAINABILITY

Fiscalsustainabilityistheabilityandwillingnessofagovernmentalentitytohonorcurrentservicecommitmentsandfinancialobligationswithouttransferringpresentobligationstofutureperiods.Fiscalsustainabilityistheforwardlookingaspectofeconomiccondition.Inthisreport,thecomponentsoffiscalsustainabilitywillbepresentedfortheGeneralFund,EducationFund,TransportationFund,TransportationInvestmentFund,andDepartmentofAlcoholicBeverageControl’sEnterpriseFund.

FivecomponentsoffiscalsustainabilityarebeingconsideredbyGASBforinclusionintheCAFR.Theyare:

Projectionsofthetotalcashinflowsandmajorindividualinflowsofresourcesinbothpercenttermsandtotaldollaramounts.

Projectionsofthetotalcashoutflowsandmajoroutflowsofresourcesbyfunctioninbothpercenttermsandtotaldollaramounts.

Projectionsofmajorindividualfinancialobligationsandtotalfinancialobligationsincludingbonds,pensions,OPEB,andlong‐termcontracts.

Projectionsofannualdebtservicerequirements.

Narrativediscussionofmajorintergovernmentalserviceinterdependenciesandthenatureofthoseserviceinterdependencies.

IfGASBproceedswiththisproposal,Utahwouldberequiredtocomplybecause,bystatute(UCA63A‐3‐204(1)(a)andUCA51‐5‐4),UtahadoptsGAAP.

ThesectionsbelowwilldetailthebackgroundandrationaleforincludingeachofthesecomponentsandwillelaborateonwhatthedatashowsforUtah.

PURPOSEOFGASBPROPOSEDGUIDELINES

Recenteconomicconditionssuchasjoblosses,creditmarketproblems,theailingconstructionsector,andreducedconsumerspendinghaveincreasedriskanduncertaintyintheprivateandpublicsector.Asvariousgovernmentalentitiesarenotimmunefromfinancialstress,thereisaneedtoeducatethepublicsectoronfiscalstrengthsandweaknessesthatcontributetotheeconomicsustainabilityoflocalgovernments,states,andthefederalgovernment.

1Source:www.gasb.org“FactsAboutGASB.”

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 3 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

Governmentspendingandgovernmentdeficitsgenerallyincreaseduringeconomicdownturnsduetoaddeddemandsbyeconomicallydisadvantagedpopulationsanddecliningrevenues.Whileeconomicdeclinesareunpleasant,theyforcegovernmentalentitiestofindefficiencieswithintheirrespectiveorganizations.

Thegoalofafive‐yearprojectionistoprospectivelyassessagovernmentalentity’sfinancialviability.ThisreportaimstomeetGASB’sgoalsbyaddressingthefivecomponentsoffiscalsustainability,providingfinancialprojectionsthroughFY2017,andbyincludingnarrativediscussionsrelatedtoeach.

DEFINITIONS

ThefollowingtermsaredefinedbyGASBandareusedfrequentlythroughoutthisreport.2

Accrualaccounting:recordingalltransactionsinthebookswhentheyoccur,evenifnocashchangeshands.

Cashbasisaccounting:recordingalltransactionsinthebookswhencashactuallychangeshands,meaningwhencashpaymentisreceivedbytheentityfromcustomersorpaidoutbytheentityforpurchasesorotherservices.

Economiccondition:acompositeoffinancialposition,fiscalcapacityandservicecapacity.Economicconditionismeanttoembodyacomprehensiveassessmentoffinancialhealth.

Financialposition:thestatusofagovernment’sassets,deferredoutflows,liabilities,deferredinflows,andnetposition,asofapointintime.

Fiscalcapacity:agovernmentalentity’sabilitytomeetfinancialobligationsastheycomedueonanongoingbasis.

Fiscalsustainability:theabilityandwillingnessofagovernmentalentitytohonorcurrentservicecommitmentsandfinancialobligationswithouttransferringpresentobligationstofutureperiods.Fiscalsustainabilityistheforwardlookingaspectofeconomiccondition.

Intergovernmentalserviceinterdependency:whenonegovernmentalentityprovidesaserviceonbehalfofanothergovernmentalentityortogetherwithoneormoregovernmentalentities.

Majorcategory:anindividualinflow,outflow,andfinancialobligationthatrepresentsatleast10percentoftotalinflows,outflows,andfinancialobligationsforallactivitiesofthattype.Allcashoutflowsforcapitaloutlaysandcapital‐relatedcashinflowsfrombondproceeds,capitalgrants,orothercashinflowsrestrictedorcommittedtocapitaloutlaysareconsideredmajor.

Resourceinterdependency:cashinflowsfromonegovernmentalentitytoanothergovernmentalentity.

Servicecapacity:agovernmentalentity’sabilitytomeetserviceobligationsonanongoingbasis.

Vulnerability:theextenttowhichanentityisfiscallydependentuponfundingsourcesoutsideitscontrol.GASB’SPROPOSEDMETHODOLOGYFORFINANCIALPROJECTION

GASBrecommendsusingaforecastbasedoncurrentlaws,regulations,andrulessuchthatthefollowingcriteriaaremet3:

Forecastsshouldusecurrentpolicyandadjusttheforecastonlyforknownchangesthatareeffectiveinfutureperiods.

2Source:GovernmentalAccountingStandardsSeries:PreliminaryViews3Source:GovernmentalAccountingStandardsSeries:PreliminaryViews

MAY 9, 2013, 10:15 AM 4 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

Forecastsshouldbeinformedbyhistoricalinformationandadjustedforknowneventsorconditionsthataffectfutureperiods.

Projectionsshouldextendatleastfiveyearsbeyondthereportingperiod.

Projectionsofcashinflowsandoutflowsshouldbebasedonacashbasis4asdefinedbyGASB.

ProjectionsoffinancialobligationsshouldbemadeonanaccrualbasisasdefinedbyGASB.

STUDYMETHODOLOGY

EmployingtheGASBmethodologydetailedabove,dataweretakenfromtheUtah’sComprehensiveAnnualFinancialReport.Thestatisticalmethodologywaslimitedtoknownvariables;meaningonlyhistoricalexperienceisincludedinconstructingtheprojection,withadjustmentstakenonlyforknownlegislativechanges.ThemethodologyutilizedSASorForecastProtimeseriesprojectionsoftwaredependinguponthesoftware’sabilitytominimizehistoricalerrors.Inalmostallcases,someformofanautoregressivemodelfitthehistoricalexperiencethebest,andthereforewaschosenastheforecastmodel.

Wecontrolledforsomeongoingandone‐timepolicychangesthataffectedtheforecast.Thepolicychangesincludeadjustmentstothesalestaxonunpreparedfood,cigaretteandtobaccotaxrateincreases,incometaxratereductions,earmarkingchanges,andARRAfunding.

COMPONENT1:PROJECTIONSOFCASHINFLOWS

Cashinflowsallowgovernmentalentitiestoassesstheincomesideoftheirbalancesheet.Thesourceandmixoftherevenuearenecessaryforanevaluationofvolatility.Tothisend,GASBrequiresabreakoutofcashinflowsbetweenmajorandnon‐majorsources.Majorsourcesofcashinflowsareforecastforanyspecificcomponentthatis10.0percent5oftherevenueorgreater.Anythingbelow10.0percentofthetotalisreportedintheaggregate.Numbersarepresentedinbothabsolutetermsandasapercentoftotalinflows.

Datashouldbeusedtoassessagovernment’srelianceononesourceofrevenuetotheexclusionofothers.Usingtheinformationrelatedtothesourcesandmixofrevenue,userswillbeabletodrawtheirownconclusionsrelatedtoagovernments’sustainability.GASBalsorequiresanarrativediscussionontheknowncausesoffluctuationsinmajorindividualcashinflowsandthepotentialimpacttheymayhaveongovernmentalsustainability.

Weevaluatedthiscashinflowrequirementforfivefunds:GeneralFund(andGeneralFundRestricted),EducationFund,TransportationFund,TransportationInvestmentFund,andtheDepartmentofAlcoholicBeverageControl’sEnterpriseFund.

Asabroadoverviewofthecashinflowsection,Figure1showscashinflowbyrevenuesourceacrossfunds,whileFigure2showscashinflowbyfund.Onthewhole,FederalFunds6representthelargestsourceofstategovernmentrevenue,followedbytheindividualincometax,andsalestax.Theoverallimportanceofagivenrevenuesourcevariesbyfund,with,forinstance,salestaxrepresentingthelargestsourceofrevenuetotheGeneralFundortheTransportationInvestmentFund,whilemotorfueltaxrepresentingthelargestsourceofrevenuetotheTransportationFund.

4Forpurposesofthisreport,afivedayaccrualadjustmentisconsideredcashbasis.5GASBisunclearastotheyearinwhichthe10percentruleapplies.Thisstudyassumesthe10percentruleappliestothemostrecentfiscalyear(FY2012)unlessotherwisestated.6Inadditiontothe$2.6billioninFederalFundsreportedhere,thestatewidefederalfundsaudit(OMBCircularA‐133)anddepartmentspecificrevenueincludesanadditionalamountofabout$4.2billioninexpendituresforsuchitemsasfederalloanstostudentsathighereducationinstitutions,unemploymentinsurance,andothers.

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 5 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

Figure1‐CashInflowbyRevenueSource(AllSources)

MAY 9, 2013, 10:15 AM 6 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

Figure2‐CashInflowbyFund(StateSources)

Fund Type Type

0M 500M 1000M 1500M 2000M 2500M 3000M

Amount

DABC DABC Receipts

Education Fund Individual Income Tax

Corporate Income Tax

All Other Education Fund

Education Fund Restricted

Federal Contracts and Grants

All Other Department Specific Revenue

General Fund Sales Tax

All Other General Fund

General Fund Restricted

Federal Contracts and Grants

All Other General Fund Restricted

Higher Education Collections

Departmental Collections

Transportation Fund

Motor Fuel Tax

Special Fuel Tax

All Other Transportation Fund Revenue

Transportation Fund Restricted

Federal Contracts and Grants

Departmental Collections

All Other Department Specific Revenue

Sales and Aviation Fuel Taxes

Transportation Investment Fund

Sales Tax

Motor Vehicle Registration Fees

All Other TIF Revenue

326,100,000

30,880,000

272,355,000

2,478,638,000

80,118,000

544,833,000

408,864,000

1,582,530,000

421,125,000

624,958,000

670,549,000

2,550,694,000

79,168,000

104,099,000

252,954,000

74,283,000

94,141,000

89,122,000

454,343,000

69,606,000

71,706,000

269,313,000

On-Book Cash Inflow by Fund (FY 2012)

Fund Type

DABC

Education Fund

Education Fund Restricted

General Fund

General Fund Restricted

Transportation Fund

Transportation Fund Restricted

Transportation Investment Fund

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 7 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

GENERALFUNDCASHINFLOW

Approximately79.5percentoftotalGeneralFundcashinflowstemmedfromsalestaxinFY2012,withtheremaining20.5percentcomingfrominsurancetaxes,severancestaxes,cigaretteandtobaccotaxes,andothermiscellaneoussources.LookingatGeneralFundcashinflowfromFY1999forward,salestaxrevenuehasdeclinedasapercentoftotalinflow;goingfrom88.4percentinFY1999to79.5percentinFY2012(Figure3).Amongthereasonsforthisarelegislativeadjustmentstobudgetingprioritiesthroughsalestaxearmarking,taxincreasesordecreasesonvarioussources,andshiftingofpurchasingdecisionsawayfromitemssubjecttosalestax.

Theongoingandone‐timechangesfortheGeneralFundincludethecigaretteandtobaccotaxincrease,decreasesintheState’staxonunpreparedfood,andadjustmentsduetoongoing,one‐timesalestaxearmarkadjustments,andfiscalnotebills.

Overall,themodelsproducetotalgrowthof$362.8millionfromFY2013toFY2017(Figure4),oranaverageannualgrowthrateof3.4percent.Mostoftheprojectedgrowthisinthesalestax,accountingfor$273.4million,withanaverageannualgrowthrateof3.2percent;theremainingamount,$89.3millionstemsfromallothersources,withananticipatedaverageannualgrowthrateof4.0percent.

GENERALFUNDKNOWNCAUSESOFFLUCTUATION

ChangesinthenumberoftaxabletransactionsduetoeconomicforcessuchasconsumerconfidenceandemploymentarethelargestfactorsinGeneralFundrevenuefluctuations.Inadditiontoeconomics‐driventaxabletransactions,changesinprices(inflationordeflation),legislativeadjustmentstosalestaxratesandtaxablebases,andprioritizationthroughearmarksalsocontributetothevolatilityofthesalestax.

Thelargestnon‐economicorpolicyrelatedchangetoGeneralFundrevenue,butnotoverallsalestaxrevenue,implementedoverthepastfewyearshasbeenbudgetprioritizationthroughearmarkingofsalestax.Overthepast14yearssalestaxearmarkshaveincreasedfromabout$9.0millionoftotalrevenue(0.7percent)to$332.0million(17.3percent)inFY2012.

AnewearmarkbeginsinFY2013,stemmingfromS.B.229ofthe2011VetoOverrideSession,whichallocates30.0percentoftotalsalestaxgrowthfromFY2011toanygivenfiscalyearthereaftertotheTransportationInvestmentFund,uptoamaximumof17.0percentoftotalsales,whichrepresentsanestimateoftotaltaxablesalesduetotheautomobileindustry.Totalearmarksareanticipatedtorepresentapproximately22.0percentofprojectedFY2013GeneralFundrevenue,or$473.0million.

MAY 9, 2013, 10:15 AM 8 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

Figure3‐ComponentsofGeneralFundCashInflow

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

PercentofTotalGeneralFundCashInflow

Sales&UseTax AllOtherGeneralFund

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 9 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

Figure4‐GeneralFundCashInflow(Thousands)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,0001999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

GeneralFundCashInflowProjections

Sales&UseTax AllOtherGeneralFund

Sales&UseTaxProjection AllOtherGeneralFundProjection

MAY 9, 2013, 10:15 AM 10 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

GENERALFUNDRESTRICTEDCASHINFLOW

InadditiontothefreerevenueportionoftheGeneralFund,GASBrequiresaprojectionofcashinflowfromGeneralFundRestrictedsources,whichincludeFederalcontractsandgrants,departmentalcollections(feesandotherservices),highereducationcollections,andallotherGeneralFundrevenue.Amodeledhistoricaltrendprojectionofthesesourcesisgiven(Figure5).Overall,themodelsproduce$1.2billioningrowthoverthecomingfiveyears,with$727.0millionofthatbeingFederalcontractsandgrants,followedby$274.0millioninallotherGeneralFundRestrictedcashinflow,$108.0millionfromhighereducationcollections,and$50.0millionindepartmentalcollections.ThecashinflowprojectionsrelatedtoFederalcontractsandgrantsisproducedbaseduponhistoricalexperience,butmaybeoverstatedgivencurrentfederalbudgetconditions.Theprojectionisleftas‐isbecausewedonotknowhowthefederalgovernmentwillbalanceitsbudgetinthecomingfivefiscalyears.Itappearsslowerfederalexpendituregrowthascomparedtohistoricalexperienceisthemostlikelyoutcomeovertheperiodoftheforecast.

GENERALFUNDRESTRICTEDKNOWNCAUSESOFFLUCTUATIONS

Asshown(Figure5),thelargestinfluencerofoverallGeneralFundRestrictedrevenuechangeisthebusinesscycle,withjumpsinfederalfundsinFY2009andFY2010andlargerthanexpectedincreasesinhighereducationcollections(tuitionincreases),amongotherchanges.

Figure5‐GeneralFundRestrictedCashInflowProjections(Thousands)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

GeneralFundRestrictedCashInflowProjections

FederalContracts&Grants FederalContracts&GrantsProjection

DepartmentalCollections DepartmentalCollectionsProjection

HigherEducationCollections HigherEducationCollectionsProjection

AllOtherGeneralFundRestricted AllOtherGeneralFundRestrictedProjection

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 11 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

EDUCATIONFUNDCASHINFLOW

Approximately89.1percentoftotalEducationFundcashinflowstemmedfromincometaxinFY2012,followedbycorporateincometaxat9.8percent7,andtheremaining1.1percentcomingfromothermiscellaneoussources.InlookingatEducationFundcashinflowfromFY1999forward,incometaxrevenuehasgrownasapercentoftotalinflow,goingfrom88.0percentinFY1999to89.1percentinFY2012(Figure6).Incometaxhasrepresentedasmuchas91.9percentoftotalrevenue(FY2002)toaslowas84.9percent(FY2006).ThelowyearofFY2006waslargelyduetocorporateincometaxexpandingrapidlyduringthepeakofthebusinesscycle.

Themodelswereadjustedformajortaxchanges,suchastheincometaxratesgoingtoaflatfivepercenttaxfromthetiered7.0percenttaxrate.

Overall,themodelsproducetotalgrowthof$577.6millionfromFY2012toFY2017(Figure7),oranaverageannualgrowthrateof3.9percent.Mostoftheprojectedgrowthisintheincometax,accountingfor$441.3million,withanaverageannualgrowthrateof3.4percent;corporateincometaxrepresentsthenextlargestgrowthcomponentat$130.9million,foranaverageannualgrowthrateof8.5percent;theremainingamountof$5.4millionstemsfromallothersources,withananticipatedaverageannualgrowthrateof5.7percent.

EDUCATIONFUNDKNOWNCAUSESOFFLUCTUATIONS

FluctuationsinEducationFundrevenuearelargelytheresultofthreefactors:1)changesineconomicconditions(accountingforatleast80.0percentofthevolatilityinrecentyears);2)changesintheEconomicDevelopmentIncentivesauthorizedoverthepastseveralyears;and3)legislativechanges(suchasreducingtheincometaxburden).Includedintheincentivesare:theEconomicDevelopmentTaxIncrementFinancingIncentiveTaxCredits,theMotionPictureIncentiveCredit,theRenewableEnergyIncentive,andtheResearchandDevelopmentIncentive.Undermostoftheseincentivesacompanyisrebatedbackaportiontothefullamountofthetaxestheymayhavepaidforaperiodofupto20years.

7Corporateincometaxisprojectedseparatelyeventhroughincertainyearsthe10percentGASBthresholdrequirementisnotmet.

MAY 9, 2013, 10:15 AM 12 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

Figure6‐ComponentsofEducationFundCashInflow

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

PercentofTotalEducationFundCashInflow

IndividualIncomeTax CorporateTax AllOtherEducationFund

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 13 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

Figure7‐EducationFundCashInflowProjections(Thousands)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,0001999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

EducationFundCashInflowProjections

IndividualIncomeTax CorporateTax

AllOtherEducationFund IndividualIncomeTaxProjection

CorporateTaxProjection AllOtherEducationFundProjection

MAY 9, 2013, 10:15 AM 14 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

TRANSPORTATIONFUNDCASHINFLOW

Approximately58.0percentoftotalTransportationFundcashinflowstemmedfrommotorfueltaxinFY2012,followedbyspecialfueltaxesat23.9percent,andtheremaining18.1percentcomingfromothermiscellaneoussources.InlookingatTransportationFundcashinflowfromFY1999forward,motorfueltaxrevenuehasdeclinedasapercentoftotalinflow,goingfrom63.0percentinFY1999to58.0percentinFY2012(Figure8).Theslowdeclinehasbeenfairlysteadythroughouttheprior14years,althoughthemostrecentfiscalyearexperiencedanincreaseinmotorfueltax’sshareoftotalrevenue,from57.8percentto58.0percent.

Overall,themodelsproducetotalgrowthof$40.3millionfromFY2012toFY2017(Figure9),oranaverageannualgrowthrateof1.8percent.Theprojectedgrowthisspreadout,with$7.3millionanticipatedfromthemotorfueltax(0.6percentaverageannualgrowth),$18.9millionfromspecialfueltaxes(3.4percentaverageannualgrowth),and$14.0million(3.3percentaverageannualgrowth)fromallothersources.

TRANSPORTATIONFUNDKNOWNCAUSESOFFLUCTUATIONS

Besidestheeconomy,fluctuationinTransportationFundrevenuegrowthstemfromchangesintheairlineandtruckingindustry’sdemandforfuelsubjecttothespecialfueltaxandapotentiallong‐termshiftbyconsumerstowardsmorefuelefficientvehicles,whichreducesdemandforfuelsubjecttothemotorfueltaxmorethanitincreasesthenumberofmilesdriven.Inadditiontofuelefficiencyandindustrydemandforcertainfueltypes,anotherfactorinfluencingTransportationFundcashinflowarethingsthataffectregistrationfees,suchaseconomicgrowthandpopulationchanges.

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 15 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

Figure8‐ComponentsofTransportationFundCashInflow

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

PercentofTotalTransportationFundCashInflow

MotorFuelTax SpecialFuelTax AllOtherTransportationFundRevenue

MAY 9, 2013, 10:15 AM 16 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

Figure9‐TransportationFundCashInflowProjections(Thousands)

0

50,000

100,000

150,000

200,000

250,000

300,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

TransportationFundCashInflowProjections

MotorFuelTax

SpecialFuelTax

AllOtherTransportationFundRevenue

MotorFuelTaxProjection

SpecialFuelTaxProjection

AllOtherTransportationFundRevenueProjection

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 17 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

TRANSPORTATIONINVESTMENTFUNDCASHINFLOW

InadditiontogeneralTransportationFund,GASBrequiresaprojectionofcashinflowfromTransportationFundRestrictedsources,whichincludeearmarkedsalestax,vehicleregistrationfees,andallotherTransportationRestrictedFundrevenue.Anhistoricaltrendprojectionofthesesourcesisgiven(Figure10).Overall,themodelsproduce$181.0millioningrowthoverthecomingfiveyears,with$176.2millionofthatbeingearmarkedsalestaxrevenue,followedby$19.2millioninallotherTransportationFundRestrictedcashinflow,and$4.7millioninearmarkedvehicleregistrationfees.ThejumpinsalestaxrevenuefromFY2011toFY2012isduetoareinstatementofaoneyearreductioninthe8.3percentoftotalsalestaxcollectionsearmark.ThediagonalgrowthfromFY2013forwardstemsfromS.B.229TransportationFundingRevisionsofthe2011VetoOverrideSession,whichprioritizes30percentofsalestaxgrowthoverthe2011basetotheTransportationInvestmentFund.Therestofthevolatilityistheresultofbudgetingpractices.Inthe2009GeneralSession,H.B.139increasedthecarregistrationfeesbyaround$20.0pervehicle8,thusthebumpinmotorvehicleregistrationfeesfrom2009to2010.OnAllOtherTIFrevenue,whichistheCriticalHighwayNeedsFund,salestaxearmarkswereadjustedeachyear,suchasthe$90.0millionfixedearmarkbeingreducedto$55.0millioninFY2012.

TRANSPORTATIONINVESTMENTFUNDKNOWNCAUSESOFFLUCTUATIONS

ThesamefactorsaffectingTransportationFundrevenuefluctuationsaffectTransportationInvestmentFundcashinflow.Additionally,threepolicychangesareresponsiblefortherestofthelargefluctuations,whichare:1)areductioninthe8.3percentearmarkto1.9percentinFY2011;2)anincreaseinthecostofregisteringavehiclebyabout$20.0pervehicle,implementedinFY2010;3)anewshiftingofsalestaxrevenuefromtheGeneralFundtotheTransportationInvestmentFund(FY2013forward,S.B.229ofthe2011VetoOverrideSession);and4)adjustmentstotheCriticalHighwaysNeedsFund.

8The$20pervehiclefeeincreaseappliedtomostvehiclesdriven;adifferentfeeincreasestructurewasimposedonheavytrucksbaseduponweight.

MAY 9, 2013, 10:15 AM 18 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

Figure10‐TransportationInvestmentFundCashInflowProjections(Thousands)

0

100,000

200,000

300,000

400,000

500,000

600,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

TransportationInvestmentFundCashInflowProjections

Salestax SalestaxprojectionMotorVehicleRegistrationFees MotorVehicleRegistrationFeesProjectionAllOtherTIFRevenue AllOtherTIFRevenueProjection

Note: The drop in sales tax in FY 2011 is due to a decline in the 8.3% earmark to 1.93% for FY 2011 only; the increases and decreases in the "All Other TIF Revenue" is due to budgeting changes made to the Critical Highway Needs Fund; the diagonal growth in sales tax for FY 2013 onward is due to SB 129 of the 2011 Veto Override Session, which prioritizes 30% of sales tax growth to the TIF

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 19 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

ALCOHOLICBEVERAGECONTROL’SENTERPRISEFUNDCASHINFLOW

Inadditiontothemajorstatefunds,thisreportincludestheDepartmentofAlcoholicBeverageControl(DABC)asanexampleofprojectingtheState’sbusinessactivities.Thefittedhistoricaltrendprojectionisgiven(Figure11).Onthewhole,DABC’stotalcashinflowisanticipatedtogrowby$68.0millionoverthenextfiveyears,or21.0percent.

DABCKNOWNCAUSESOFFLUCTUATIONS

ReceiptsfromDABC’sbusinessactivitiesareaffectedbyaforementionedeconomicfactors,suchasacontinualshiftinthepopulationmixfromnon‐alcoholicdrinkerstoalcoholicdrinkersandpopulationgrowthfromnetmigration.

Figure11‐DABCCashInflowProjections(Thousands)

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

DABCCashInflowProjections

Receipts ReceiptsProjections

MAY 9, 2013, 10:15 AM 20 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

COMPONENT2:PROJECTIONSOFMAJORAREACASHOUTFLOWS

Cashoutflowsrepresentagovernment’scostsofoperation.Projectionsofcashoutflowsinformusersoflikelyfuturecommitments.Similartocashinflows,cashoutflowslessthan10.0percentarereportedintheaggregate.Majorcashoutflowsarereportedbyprogramorfunction.Numbersarepresentedinabsolutetermsandasapercentoftotaloutflows.TheDepartmentofFinanceusescashflowaccounting.Asaresultwedonotaccountforexpendituresbyfundtype.Thismeansthatwecannotforeachbudgetareashowhoweachwoulddobyfundtype.Forthisreasontheoutflowspresentedinthisreportincludeallfundingsources.Incuttingacrossallexpendituretypes,PublicEducationisthehighestcostarea,followedbyHealthandEnvironmentalQuality,HigherEducation,AllOtherGovernmentalcosts,andTransportation(Figure12).

Figure12‐CashOutflowbyExpenditureArea

GENERALFUNDCASHOUTFLOW

Thefollowingrepresentshowfundinghasbeenallocatedfrom1999‐2012inareasmostlycoveredbyGeneralFundrevenue(Figure13).Asisindicated,costsassociatedwithHealthandEnvironmentalQualityhaveseenthelargestincreasefromtheGeneralFund,growingfrom30.7percentinFY1999to37.2percentinFY2012.ThelargestdeclinersareHumanServices,goingfrom14.9percentinFY1999to10.1percentinFY2012andAllOtherGovernment,decliningfrom23.1percentinFY1999to20.2percentinFY2012.

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 21 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

Figure13–PercentofTotalGeneralFundExpendituresbyMajorExpenditureArea,1999‐2012

HUMANSERVICESCASHOUTFLOW

TheDepartmentofHumanServicesembodiesservicesinvolvingindividualswithdisabilities,childwelfare,substanceabuseandmentalhealthtreatment,childsupportcollections,andprogramsassociatedwiththeelderly.CashoutflowsassociatedwithHumanServicesreachedamaximumasapercentoftotalGeneralFundexpendituresinFY2000,afterwhichcostshavedeclinedrelativetotheotherexpendituretypeswithintheGeneralFund,withtheFY2012figureforHumanServicesat10.1percent.CostsassociatedwithHumanServicesbasedonthehistoricaltrendGASBrequirementsindicateanadditional$134.0inexpendituresfromFY2013toFY2017,oranaverageof$27.0millionperyear.CashoutflowsfromactivitiesclassifiedasHumanServicesfollowthebusinesscycle,withthemostrecentbusinesscycleassociatedsavingsof$56.0million.

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

All Other Government 23.1% 23.1% 22.9% 22.2% 20.8% 20.3% 19.9% 20.6% 22.0% 22.5% 22.0% 20.9% 20.4% 20.2%

Employment and Family Services 9.8% 8.8% 8.3% 8.4% 9.2% 9.2% 9.1% 8.4% 8.0% 7.8% 8.9% 11.2% 11.4% 11.2%

Higher Education ‐ All 21.6% 21.5% 21.8% 22.6% 22.2% 21.3% 21.5% 21.2% 21.5% 22.0% 20.8% 20.7% 21.1% 21.4%

Health and Environmental Quality 30.7% 31.1% 32.2% 32.8% 34.4% 36.3% 36.8% 37.7% 36.2% 35.4% 36.3% 36.2% 36.7% 37.2%

Human Services 14.9% 15.5% 14.7% 13.9% 13.5% 13.0% 12.6% 12.2% 12.3% 12.2% 11.9% 11.0% 10.4% 10.1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Percent of Total General Fund Expenditures by Major Expenditure Area

MAY 9, 2013, 10:15 AM 22 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

HUMANSERVICESKNOWNCAUSESOFFLUCTUATIONS

Historically,fundingfortheDepartmentofHumanServiceshasbeendrivenbythefollowingfactors:1)changesinrulesguidingfederalfundingparticipation;2)economicpressuresonUtah’sgovernmentoperations;and3)highprioritysocialissues.

SeveralofthemajoreconomicpressuresonoperationsoftheDepartmentofHumanServiceshaveincludedtworecessionsoverthepastdecadeandthepressureforcost‐of‐livingincreasesforthevariousprovidergroupsdeliveringservices.TheDepartmentofHumanServiceshasgonethroughseveralroundsofprogramreductionsfromFY2002throughFY2003andfromFY2009throughFY2011.

Additionally,theDepartmentofHumanServiceshasexperiencedpressurefromprovidersforcost‐of‐livingincreasesincludingmeetingthestatutoryrequirementsofmaintaininglargegroupsettingfacilitiessuchastheUtahStateHospitalandtheUtahStateDevelopmentalCenter.

ChangesinrulesguidingfederalfundingparticipationhavehadamajorimpactontheDepartment’sneedforadditionalstatefunding.TheDepartmentofHumanServiceshaseitheradaptedorrequiredadditionalstatefundingbecauseofthelossoffederalrevenueduetofederalpolicychanges,mandatedactionsrequiredwhenacceptingfederalfunds,orchangesintheState’srateoftheFederalMedicalAssistancePercentage(FMAP).

Whenrevenuesareavailable,theDepartmentofHumanServiceshasreceivedfundingforitemssuchasTheDrugOffenderReformAct(DORA),supportservicesforindividualswithdisabilities,mentalhealthtreatment,subsidizedmealsforseniorsandsupportforlow‐incomeseniorsremainingintheirownhomes,substanceabusetreatment,andchildabuseandneglectissues.

TheprojectionsforcashoutflowsclassifiedasHumanServicesaregiven(Figure14).

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 23 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

Figure14‐HumanServicesCashOutflowProjections(Thousands)

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

HumanServicesCashOutflowProjections

HumanServices HumanServicesProjection HumanServicesAppropriated

See DetailView

MAY 9, 2013, 10:15 AM 24 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

HEALTHANDENVIRONMENTALQUALITYCASHOUTFLOW

CostsassociatedwithHealthandEnvironmentalQualityhaveconsistentlygrownfromalowinFY1999of30.7percenttoahighof37.2percent.TotalcostsinFY2012amountedto$2.4billion,anincreaseof$1.4billionfromthe$963.0millionofcostsincurredinFY1999.Thelargestportionofthe7.0percentaverageannualgrowthratestemsfromcostsassociatedwithMedicaid.Onthehistoricaltrendprojection,thetrendindicatesadditionalcostsfromFY2013toFY2017of$644.0million,orabout$129.0millioneachyear.HEALTHANDENVIRONMENTALQUALITYKNOWNCAUSESOFFLUCTUATIONS

ThemissionoftheUtahDepartmentofHealthistoprotectthepublic’shealthbypreventingavoidableillness,injury,disability,andprematuredeath;assuringaccesstoaffordable,qualityhealthcare;andpromotinghealthylifestyles.

Historically,fundingfortheUtahDepartmentofHealthhasbeendrivenbythefollowingfactors:1)expansionsinwhichpeopleareeligible;2)morepeoplearebecomingeligible;and3)increasingcostofhealthcare.

TheforecastislargelybasedoncontinualcostsassociatedwithsuchprogramsasMedicaidandenvironmentalquality.Theforecastdoesnotcaptureanyexpendituresavingsfromimprovementintheeconomy.

Therearetwosourcesofexpansionsforeligibility:mandatorychangesfromthefederalgovernmentandoptionalexpansionschosenbytheState.Therehavebeenfivefederallymandatedexpansionsandninestateoptionalexpansions(includingsigningupfortheMedicaidprogram)from1966tothepresent.

OnemaincriterionforreceivingMedicaidisaclient'sincome;whenpeoplelosetheirjobs,thedemandforMedicaidincreases.TheannualgrowthratefromFY2009throughFY2011was14.3percentcomparedtonegative0.4percentaverageannualgrowthrateforthethreeprecedingyears.

Theaverageannualgrowthinmedicalinflationforthelast10yearshasbeen3.1percent.Additionally,MedicaidhassomefederalandstatelawsthatrequireadditionalincreasesforcertaincostsintheMedicaidprogram.ForFY2013,theagencyanticipatescostincreasesof$5.0millionGeneralFund.

Thesefactorswillcontinuetoimpactfuturecostincreases.Additionally,changesinincentiveforpeopletosignupforMedicaidareexpectedtoimpactfuturecostaswellaschangesinmandatorycoverage.OutsideofMedicaid,theLegislatureoftenprovidesincreasestotheBabyWatch/EarlyInterventionprogram.Thisprogramalsomustserveallclientswhoqualify.

TheprojectionsforcashoutflowsclassifiedasHealthandEnvironmentalQualityaregiven(Figure15).

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 25 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

Figure15‐HealthandEnvironmentalQualityCashOutflowProjections(Thousands)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

HealthandEnvironmentalQualityCashOutflowProjections

HealthandEnvironmentalQuality HealthandEnvironmentalQualityProjection

MAY 9, 2013, 10:15 AM 26 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

HIGHEREDUCATIONCASHOUTFLOW

CashoutflowsconnectedwithprovidingHigherEducationserviceshavebeengenerallyflatfromFY1999toFY2012asapercentoftotalGeneralFundcashoutflow,goingfrom21.6percentto21.4percent.CostsassociatedwithHigherEducationreachedahighof22.6percentininFY2002,fallingtoalowof20.7percentinFY2010.SincetheFY2010low,cashoutflowshaveincreased,standingat21.4percentattheendofFY2012.Overall,cashoutflowconnectedwithHigherEducationisanticipated,baseduponGASB’shistoricaltrendmethodology,togrowby$277.0millionfromFY2012toFY2017,oranaverageannualincreaseofabout$55.0million.Incontrasttotheprojectedaverageannualincreaseof$55.0million,costsgrewbyanaverageof$50.0millioneachyearfromFY1999toFY2012.HIGHEREDUCATIONKNOWNCAUSESOFFLUCTUATIONS

TheUtahSystemofHigherEducation(USHE)iscomprisedofnineinstitutionsofhigherlearning.USHEpromotesresearch,aswellaseconomic,academic,cultural,andothersocialprogramsforthecitizensofUtah.

Historically,fundingforhighereducationhasbeendrivenbythefollowingfactors:1)studentenrollmentfigures;2)operationsandmaintenance(O&M)fornewfacilities;and3)fundingforscholarships.

Theprojectionsreflectavirtualstraight‐linedmodelbaseduponthehistoricalexperiencethathighereducationcontinuallyincreasesoperatingcostswitheitherincreasedstatefundingorincreasedfees(tuition).

Severalyearsago,theStateBoardofRegentswouldprojectenrollmentfigures,andthenrequestfundingbasedonthoseestimates.Morerecently,thisshiftedtotheenrollmentthatwasactuallyseenoncampusesduringthepreviousyear.Thiswaschangedtoreflectamoreaccurateandrealisticstudentfull‐timeequivalent(FTE)number.However,fortheinstitutions,whenthisfundingwasapproved,itwasaftertheinitialenrollmentincreasehadoccurred.

Overthepastseveralyears,increasesinfundingforhighereducationincludedtheO&Mforstate‐fundedandnon‐statefundedfacilities.However,sinceFY2008,fundingforO&Mfornon‐statefundedfacilitieshasnotbeenapproved.Forstate‐fundedfacilities,thisfundinghasbeennear$2.0millioneachyear.

Inrecentyears,fundingforscholarships,mainlytheRegents’ScholarshipandtheNewCenturyScholarship,hasbeenanincreasingpartofthehighereducationbudgets.FundingfortheEngineeringInitiativehasbeensignificantsinceitsinceptioninFY2001.Atotalof$11.5millionisintheInitiative’songoingbase.Anadditional$9.7millionhasbeenappropriatedinone‐timefunds.

SinceFY2008,whenbudgetshavebeenreduced,someoftheabove‐mentionedfundingwasnecessarilyeliminated.Thingsthattraditionallywerefunded,suchasenrollmentgrowth,werenotfunded.Thiswasduringatimewhenstudentenrollmentwasincreasingatasignificantrate.

Lastyear,S.B.97,“MissionBasedFunding”wasapproved,whichmovedtoemphasizeeachinstitution’smission,whichinsomecasesisenrollmentgrowthandinothersisnot.Thispastsessionsawanappropriationof$4.0millionforMissionBasedFunding,whichinstitutionsareusingtoenhanceparticipation,completion,andeconomicdevelopment.

Lookingforward,theGovernorhasadoptedagoalofhaving66.0percentoftheadultpopulationwithapost‐secondarydegreeorcertificatebytheyear2020.However,uptothispoint,therehasbeennodiscussionofcostsassociatedwiththisgoal.

TheprojectionsforcashoutflowsclassifiedasHigherEducationaregiven(Figure16).

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 27 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

Figure16‐HigherEducationCashOutflowProjections(Thousands)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

HigherEducationCashOutflowProjections

HigherEducation HigherEducationProjection

MAY 9, 2013, 10:15 AM 28 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

PUBLICEDUCATIONCASHOUTFLOW

CashoutflowassociatedwithPublicEducationhasgrownbyabout$1.2billionfromFY1999toFY2012,representinganaverageannualincreaseofabout$89.0million,oranaverageannualgrowthrateofapproximately3.8percent.Theprojectedaverageannualgrowthratecomesoutat4.1percent,representingtotalcostincreasefromFY2013toFY2017of$641.0million,orabout$128.0millionannually.PUBLICEDUCATIONKNOWNCAUSESOFFLUCTUATIONS

PubliceducationintheStateisconcernedwithUtah'spublicschools,includingpre‐kindergarten,kindergarten,generaleducation,specialeducation,careerandtechnicaleducation,charterschools,andstatewideadministration.

Historically,fundingforpubliceducationhasbeendrivenbythefollowingfactors:1)studentenrollmentgrowth;and2)localpropertytaxrevenues.

GASB‐basedpubliceducationcashoutflowisbasedonthehistoricalexperienceofcontinuedcostincreases,specificallytheboomyearsof2004to2008.

EnrollmentinUtah’spublicschoolshasincreasedannuallysincebeforeFY2000andisprojectedtocontinueincreasingatabout2.0percenteachyearfortheforeseeablefuture.FundingincreasedenrollmentsinthepubliceducationsystemrepresentsoneoftheprimarychallengesfacingtheLegislatureeachyear.

Utahusesafundingconceptknownas“prior‐yearplusgrowth”whenfundingpublicschools.Schooldistrictsandcharterschools,knownasLocalEducationAgencies(LEAs),receivebasefundingasdeterminedbytheirprior‐yearenrollment(definedinstatuteasAverageDailyMembership).AgrowthfactoristhenappliedforLEAswithayear‐over‐yearincreaseinstudentenrollment.Growthfactorisdeterminedbycomparingtheprioryearfall‐enrollmenttothecurrent‐yearfallenrollment.LEAswithdecliningenrollmentareheldharmlessfromfundingreductioninthefirstyearofenrollmentdecline.

StudentenrollmentfiguresareconvertedintoWeightedPupilUnits(WPUs)usingformulasdefinedinstatute.InestablishingtheFY2013budget,anestimatedenrollmentof600,224generated782,017WPUs.Eachyear,theLegislaturesetsadollarvalueprovidedforeachWPU.SinceFY2012,theLegislaturehasestablishedtwoWPUValues.TheBaseWPUValueissetat$2,842inFY2013with685,076WPUsqualifyingforthisamount.TheAdd‐onWPUValueissetat$2,607inFY2013with96,941WPUsqualifyingforthisamount.

LEAsgenerateWPUsbasedonvariousdemographicorprogrammaticvariablesdefinedinstatute.Forexample,onestudentinaveragedailyattendanceequalsoneWPU.Astudentenrolledinhalf‐daykindergartenisvaluedat0.55ofaWPU.Studentsthatreceivespecialeducationservicesmaygenerateupto2.53WPUs.InadditiontoWPUfunding,LEAsmayreceiveadditionalfundingbasedontheirparticipationincategoricalprogramsfundedbytheLegislature.

InFY2013,nearly$2.2billionwasdistributedtoLEAsthroughWPUprogramsandanadditional$866.0millionwasdistributedthroughcategoricalprograms.

Localpropertytaxrevenuesplayauniqueroleinstatefundingforpubliceducation.InorderforaschooldistricttoreceivestateWPUfunding,thedistrictmustimposeabasicpropertytaxrateonpropertieswithinthedistrict.ThisBasicRateisthesameforallschooldistrictsandsetatthestateleveltogenerateacertainamountofrevenuestatewideasprovidedinstatute.InFY2013,theBasicRateisestimatedat.001665togenerate$289.0million.TherevenuegeneratedbyeachschooldistrictthroughtheBasicRate

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 29 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

isappliedtothecostofthedistrict’sWPUs.Theremainingbalanceiscoveredwithstaterevenues.Charterschoolsdonothavetheabilitytotax.Asaresult,charterschoolWPUsareentirelystatefunded.

Inthebudgetingprocesseachyear,aninformalgroupcalledtheCommonDataCommittee(CDC)convenestoprojectstudentenrollmentanddistrictpropertyvaluesforthecomingyear.TheCDCincludesrepresentativesfromtheUtahStateOfficeofEducation,Governor’sOfficeofPlanningandBudget,theLegislativeFiscalAnalyst,andtheUtahStateTaxCommission.TheconsensusenrollmentandpropertyvalueprojectionsdevelopedbytheCDCareusedtoestimateWPUsanddeterminethelevelofstatefundingrequired.

TheprojectionsforcashoutflowsclassifiedasPublicEducationaregiven(Figure17).

Figure17‐PublicEducationCashOutflowProjections(Thousands)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

PublicEducationCashOutflowProjections

PublicEducation PublicEducationProjections

MAY 9, 2013, 10:15 AM 30 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

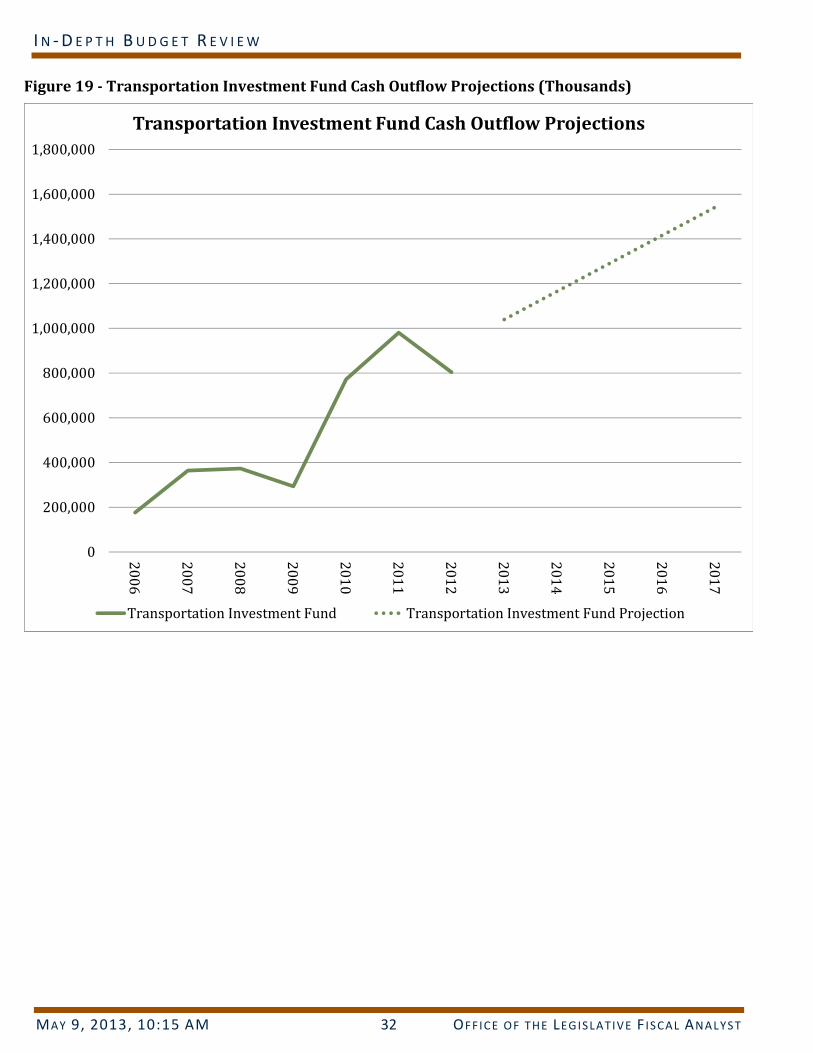

TRANSPORTATIONCASHOUTFLOW

CashoutflowassociatedwithTransportationhavegrownby$577.0millionfromFY1999toFY2012,anaverageannualincreaseof$41.0million,oranaverageannualgrowthrateof5.5percent.GASB‐informedprojectioncomesoutatanaverageannualgrowthrateof5.4percent,oratotalcashoutflowincreaseof$404.0millionfromFY2012toFY2017.TRANSPORTATIONKNOWNCAUSESOFFLUCTUATIONS

DepartmentofTransportation(DOT)aimstopreserveinfrastructure,optimizemobilityandimprovesafetythroughouttheState.

Historically,fundingfortransportationhasbeendrivenbythefollowingfactors:1)populationgrowth;and2)higherpercapitauseofthehighwayinfrastructuresystem.

Between1990and2010,Utah’spopulationincreasedby60.0percentandthenumberofvehiclemilestraveledincreasedby82.0percent,buthighwaycapacityincreasedbyonly6.0percent.Projectionsshowthatby2015,travelwillincreaseby85.0to90.0percent,populationby70.0to80.0percent,andnewhighwaycapacityby7.0percent.Populationgrowthandhigherpercapitasystemusehavecreateddemandforincreasedcapacity.

TheLegislaturehashelpedmitigatesomeoftheincreaseddemandsbyprovidingfundingforhighwaycapacityprojectsoverthepast15years.ThoseprogramsincludetheCentennialHighwayProgram(41projects),theCriticalHighwayNeedsProgram(41projects),andtheTransportationInvestmentFund(3majorprojectstodate).TheongoingfundingsourcesthatenabledDOTtobuildtheseprojectsremaininplacetoaddressfuturecapacityprojects.

Increasedinfrastructuresystemusehasputastrainonscarceresourcestopreserveandextendthelifeofroadsandbridges.DOTestimatesthatanadditional$80.0millionperyearwillbenecessarytomaintainthecurrentmaintenancestandardofUtahhighways.

AnotherissueaffectingrevenueavailableintheTransportationFundistherelationshipofhighwaymilestraveledtotheefficiencyofvehiclesonthehighway.Whilemilestraveledoverthe15yearperiod,from1990to2010increasedby82.0percent,theincreaseintheTransportationFundaveragedlessthan3.0percentannualgrowth.ThispresentsachallengeforrevenueavailableforpreservationandcapacityneedsforUtahhighwayinfrastructure.

TheprojectionsforcashoutflowsclassifiedasTransportationaregiven(Figure18andFigure19).

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 31 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

Figure18‐TransportationFundCashOutflowProjections(Thousands)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

TransportationCashOutflowProjections

Transportation TransportationProjection

MAY 9, 2013, 10:15 AM 32 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

Figure19‐TransportationInvestmentFundCashOutflowProjections(Thousands)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

TransportationInvestmentFundCashOutflowProjections

TransportationInvestmentFund TransportationInvestmentFundProjection

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 33 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

DEPARTMENTOFALCOHOLICBEVERAGECONTROLCASHOUTFLOW

Theprojectionforcashoutflowsincurredbythestate’sDABCbusinessisgiven(Figure20).Thelargestcomponentofcashoutflowcoversthecostsofgoodssold(i.e.PaymentstoSuppliers/Claims/Grants),followedbythecashtransferredtooverprogramswithinstategovernment(salestax,schoollunchtax,publicsafety),andemployeecosts/allothercosts.CashoutflowassociatedwithDABC’sbusinessactivityisanticipatedtogrowby$54.0million,oranaverageannualgrowthrateof3.3percent.Theprojected3.3percentgrowthrateisabout2.6percentbelowthehistoricalgrowthratefromFY1999toFY2012of5.9percent.

Figure20‐DABCCashOutflowProjection(Thousands)

0

50,000

100,000

150,000

200,000

250,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

DABCCashOutflowProjection

PaymentstoSuppliers/Claims/Grants

PaymentstoSuppliers/Claims/GrantsProjection

PaymentsofSales,SchoolLunch,andPremiumTaxes

PaymentsofSales,SchoolLunch,andPremiumTaxesProjection

DABC,Employeecosts,allother

DABC,Employeecosts,allotherProjection

MAY 9, 2013, 10:15 AM 34 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

ALLOTHERGOVERNMENTCASHOUTFLOW

TheprojectionsforcashoutflowsclassifiedasAllOtherGovernmentaregiven(Figure21).TheprojectedcashoutflowgrowthfromFY2012toFY2017comesoutat$269.0million,oranaverageannualincreaseof3.2percent.

Theprojectedgrowthrateisabout1.1percentbelowthehistoricalaverageannualgrowthrateof4.3percentfromFY1999toFY2012.

Figure21‐AllOtherGovernmentCashOutflowProjections(Thousands)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

AllOtherGovernmentCashOutflowProjections

AllOtherGovernment AllOtherGovernmentProjection

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 35 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

GASBMODELSVERSUSCURRENTPROJECTIONSOFREVENUE

TotesttheaccuracyofGASBguidelines,wecomparedtheseforecaststoactionstakenduringthe2013GeneralSession.Ineverycase,therearedifferencesbetweentheadoptedforecastsandGASBforecastsforFY2013andFY2014,thedetailsofwhicharediscussedherefortheGeneralFund,EducationFund,TransportationFund,andDepartmentofAlcoholicBeverageControl.ThedifferencesarelikelyduetoGASB’srelianceontrenddataratherthanconsideringtheimpactsofeconomicindicators.

GENERALFUNDREVENUE

FortheGeneralFund,GASB’ssalestaxprojectionforFY2013isabout$31.8millionbelowthecurrentconsensusforecast,whileGASB’sFY2014salesforecastisabout$19.5millionbelowthecurrentconsensussalestaxforecast.

OnallothersourcestotheGeneralFund,GASB’sFY2013forecastisabout$29.2millionbelowthecurrentconsensusforecast,andGASB’sFY2014forecastisabout$24.4millionbelowthecurrentconsensusforecast(Figure22andFigure23).Thecombineddifferenceis$61.1millioninFY2013and$43.9millioninFY2014.Inbothcases,GASB’sforecastisbelowthecurrentforecast.

Figure22‐DifferencesbetweenGeneralFundGASB/CurrentConsensusForecasts(Thousands)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

GeneralFundCashInflowProjections

Sales&UseTax AllOtherGeneralFund

Sales&UseTaxProjection AllOtherGeneralFundProjection

Sales&UseTaxAdopted AllOtherGeneralFundAdopted

See Detail View

MAY 9, 2013, 10:15 AM 36 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

Figure23–DetailView:DifferencesbetweenGeneralFundGASB/CurrentConsensusForecasts(Thousands)

EDUCATIONFUNDREVENUE

IncontrasttotheGeneralFundforecasts,GASBmodelsproducehigherEducationFundforecastsoverallforthetwolargestsources:individualincometaxandcorporateincometax.TheFY2013individualincometaxdifferenceis$27.9millionandtheFY2013corporateincometaxdifferenceis$15.3million.TheforecastsforFY2014differby$85.3millionforindividualincometaxand$86.9millionforcorporateincometax.ThecurrentforecastforallothersourcesishigherthanGASB’sforecast,withthecurrentconsensusforecastforallothersourcesbeing$16.5millionhigherinFY2013and$6.7millionhigherinFY2014.TheoveralldifferencebetweenGASBmodelsandthecurrentconsensusforecastsis$26.8millioninFY2013and$165.5millioninFY2014(Figure24andFigure25).

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 37 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

Figure24‐DifferencesbetweentheEducationFundGASB/CurrentConsensusForecasts(Thousands)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,0001999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

EducationFundCashInflowProjections

IndividualIncomeTax CorporateTax

AllOtherEducationFund IndividualIncomeTaxProjection

CorporateTaxProjection AllOtherEducationFundProjection

IndividualIncomeTaxAdopted CorporateTaxAdopted

AllOtherEducationFundAdopted

See Detail View

MAY 9, 2013, 10:15 AM 38 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

Figure25‐DetailView:DifferencesbetweentheEducationFundGASB/CurrentConsensusForecasts(Thousands)

Fiscal Year / Type / Projection Type

2013

All

Oth

er

Edu

catio

n

Fun

d

Cor

pora

te

Inco

me

Tax

Indi

vidu

al

Inco

me

Tax

2014

All

Oth

er

Edu

catio

n

Fun

d

Cor

pora

te

Inco

me

Tax

Indi

vidu

al

Inco

me

Tax

Ado

pted

GA

SB

Ado

pted

GA

SB

Ado

pted

GA

SB

Ado

pted

GA

SB

Ado

pted

GA

SB

Ado

pted

GA

SB

01

23

Am

ount

21,0

20

37,4

79 327,

928

312,

600

2,68

0,07

5

2,65

2,15

6

22,2

59

28,9

50 372,

371

285,

450

2,83

4,23

0

2,74

8,95

0

Detail View: Education Fund Differences

Projection Type

Adopted

GASB

Sources: LFA

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 39 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

TRANSPORTATIONFUNDREVENUE

OntheTransportationFund,threesourcesareprojected:motorfueltax,specialfueltax,andallothersources.InFY2013andFY2014andforallthreesources,GASB’sforecastsarehigherthanthecurrentconsensus.GASB’sforecastformotorfueltaxis$3.0millionhigherinFY2013and$0.9millionhigherinFY2014;GASB’sforecastforspecialfueltaxis$10.1millionhigherinFY2013and$16.1millioninFY2014;andGASB’sforecastforallothersourcesis$3.0millionhigherinFY2013and$3.8millionhigherinFY2014(Figure26andFigure27).Insummingallsources,GASB’sforecastis$16.0millionhigherinFY2013and$20.8millionhigherinFY2014.

Figure26‐DifferencesbetweentheTransportationFundGASB/CurrentConsensusForecasts(Thousands)

0

50,000

100,000

150,000

200,000

250,000

300,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

TransportationFundCashInflowProjections

Motor Fuel Tax Special Fuel Tax

All Other Transportation Fund Revenue Motor Fuel Tax Projection

Special Fuel Tax Projection All Other Transportation Fund Revenue Projection

Motor Fuel Tax Adopted Special Fuel Tax Adopted

All Other Transportation Fund Adopted

See Detail View

MAY 9, 2013, 10:15 AM 40 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

Figure27–DetailView:DifferencesbetweentheTransportationFundGASB/CurrentConsensusForecasts(Thousands)

Fiscal Year / Type / Projection Type

2013

All

Oth

er

Tra

nspo

rtat

ion

F

und

Rev

enue

Mot

or F

uel

Tax

Spe

cial

Fue

l T

ax

2014

All

Oth

er

Tra

nspo

rtat

ion

F

und

Rev

enue

Mot

or F

uel

Tax

Spe

cial

Fue

l T

ax

Ado

pted

GA

SB

Ado

pted

GA

SB

Ado

pted

GA

SB

Ado

pted

GA

SB

Ado

pted

GA

SB

Ado

pted

GA

SB

0K

50K

100K

150K

200K

250K

300K

Am

ount

85,2

86

82,3

00

253,

670

250,

700

109,

569

99,5

00

87,4

14

83,5

94

255,

325

254,

400

115,

552

99,5

00

Detail View: Transportation Fund Differences

Projection Type

Adopted

GASB

Sources: LFA

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 41 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

TRANSPORTATIONINVESTMENTFUNDREVENUE

OntheTransportationInvestmentFund,threesourcesareprojected:salestax,motorvehicleregistrationfees,andallothersources.GASB’sforecastforsalestaxis$22.0millionbelowinFY2013and$13.6millionlowerinFY2014;GASB’sforecastformotorvehicleregistrationfeesis$0.7millionlowerinFY2013and$1.5millioninFY2014;andGASB’sforecastforallothersourcesis$33.0millionhigherinFY2013and$38.0millionhigherinFY2014(Figure28andFigure29).Insummingallsources,GASB’sforecastis$10.3millionhigherinFY2013and$22.9millionhigherinFY2014.

Figure28–DifferencebetweentheTransportationInvestmentFundGASB/CurrentConsensusForecasts(Thousands)

0

100,000

200,000

300,000

400,000

500,000

600,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

TransportationInvestmentFundCashInflowProjections

Salestax SalestaxprojectionMotorVehicleRegistrationFees MotorVehicleRegistrationFeesProjectionAllOtherTIFRevenue AllOtherTIFRevenueProjectionSalestaxadopted MotorVehicleRegistrationFeesAdoptedAllOtherTIFRevenueAdopted

See Detail View

Note: The drop in sales tax in FY 2011 is due to a decline in the 8.3% earmark to 1.93% for FY 2011 only; the increases and decreases in the "All Other TIF Revenue" is due to budgeting changes made to the Critical Highway Needs Fund; the diagonal growth in sales tax for FY 2013 onward is due to SB 129 of the 2011 Veto Override Session, which prioritizes 30% of sales tax growth to the TIF

MAY 9, 2013, 10:15 AM 42 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

Figure29‐DetailView:DifferencebetweentheTransportationInvestmentFundGASB/CurrentConsensusForecasts(Thousands)

Fiscal Year / Type / Projection Type

2013

All

Oth

er T

IF

Rev

enue

Mot

or V

ehic

le

Reg

istr

atio

n

Fee

s

Sal

es T

ax

2014

All

Oth

er T

IF

Rev

enue

Mot

or V

ehic

le

Reg

istr

atio

n

Fee

s

Sal

es T

ax

Ado

pted

GA

SB

Ado

pted

GA

SB

Ado

pted

GA

SB

Ado

pted

GA

SB

Ado

pted

GA

SB

Ado

pted

GA

SB

0K

100K

200K

300K

400K

Am

ount

138,

704

105,

733

72,8

57

73,5

70

351,

572

373,

531

144,

069

106,

156

74,0

27

75,4

83

395,

633

409,

240

Detail View: Transportation Investment Fund (thousands)

Projection Type

Adopted

GASB

Sources: LFA

OFFICE OF THE LEGISLATIVE FISCAL ANALYST 43 MAY 9, 2013, 10:15 AM

I N ‐DE P T H BUDG E T R E V I EW

DABCREVENUE

OnrevenuefromDABCbusinessactivities,theadoptedreceiptsfigureis$1.8millionbelowtheFY2013GASBforecastand$2.6millionbelowtheFY2014GASBforecastasshown(Figure30andFigure31).

Figure30–DifferencebetweentheDABCCashInflowGASB/CurrentConsensusForecasts(Thousands)

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

DABCCashInflowProjections

Receipts ReceiptsProjections DABCReceiptsAdopted

See Detail View

MAY 9, 2013, 10:15 AM 44 OFFICE OF THE LEGISLATIVE FISCAL ANALYST

I N ‐DE P T H BUDG E T R E V I EW

Figure31‐DetailView:DifferencebetweenDABCCashInflowGASB/CurrentConsensusForecasts(Thousands)

Fiscal Year / Type / Projection Type

2013

Rec

eipt

s

2014

Rec

eipt

s