improving economic backdrop & reasonable valuations...

TRANSCRIPT

Anand Rathi Shares and Stock Brokers Limited (hereinafter “ARSSBL”) is a full service brokerage and equities research firm and the views expressed therein are solely of ARSSBL and not of the companies which have been covered in the Research Report. This report is intended for the sole use of the Recipient and is to be circulated only within India and to no countries outside India. Disclosures and analyst certifications are present in Appendix. Anand Rathi Research India Equities

Dhaval Dama+9122 66266728

Logistics

Sector ReportIndia I Equities

17 January 2013

India Logistics

Improving economic backdrop & reasonable valuations

Indian logistics industry is set to witness robust growth as the economy crosses the threshold of US$1.6trn. Industrial compulsions and customer preferences are slowly forcing systemic acceptance of containerisation & organized logistics. We prefer Gateway Distriparks for its presence across various segments, and Container Corporation of India, the largest container-train operator (CTO) in the country.

Containerisation story to continue in India. Containerized traffic though at a low ~15%, is slowly growing and is likely to gradually level with global average of 80%. Moreover, post the slight decline in trade volumes during 9MFY13, EXIM trade is expected to recover during FY14, which would benefit Indian companies in container freight stations (CFS), multi-modal transport operations (MTO) and CTOs.

Rising thrust on infrastructure brightens prospect. GoI efforts to improve the existing infrastructure facilities to connect major metropolitan cities with the hinterlands would benefit the sector. Indian Railways (IR) is undertaking its most ambitious project, the dedicated freight corridor (DFC), which would traverse 3,300km connecting major cities. It would help CTOs significantly improve operations. Also, under the draft lines of XIIth plan the GoI plans to construct 35,000kms of 2/4 lane highways. We believe this additional thrust on infrastructure would benefit the sector immensely.

Regulatory reforms, new segments to drive growth. GoI plans to introduce the Goods and Services Tax (GST), abolishing several state taxes and leading to centralised warehousing for companies. Recent reforms such as of FDI in retailing would also boost trade in India, leading to more demand for logistical services. New segments like organised warehousing, 3PL, 4PL logistics would also benefit the sector.

Our take. We prefer Gateway Distriparks for its presence across various segments and believe it would be a key beneficiary of improving EXIM trade and FDI in retail. Container Corporation of India (Concor), the largest CTO in the country could be a direct beneficiary of increasing rail freight.

Overweight Sensex: 19818

Nifty: 6002

Key Data RatingCurrent

Price (`) Target Price

(`)M. Cap

(US$ m)FY14 EPS

|(`)EV/Sales

(x)EV/EBIDTA

(x)P/E (x)

PBV (x)

RoAE (%)

RoACE (%)

Container Corporation of India Buy 937 1,132 2,233 75.5 2.0 8.0 12.4 1.8 14.9 15.3

Gateway Distriparks Buy 135 196 275 16.3 1.3 4.5 8.4 1.7 22.1 25.2

Allcargo Logistics Hold 132 159 311 17.7 0.4 3.3 7.4 0.9 14.0 13.1

Source: Company, Anand Rathi Research Note: Prices as on 14 Jan’ 2013

17 January 2013 India Logistics – Improving economic backdrop & reasonable valuations

Anand Rathi Research 2

India Logistics

Improving economic backdrop & reasonable valuations

Containerisation story to continue..................................................................... 3

Rising thrust on infrastructure ........................................................................... 5

Reforms, new segments to aid growth............................................................. 9

Valuation......................................................................................................... 11

Company Section............................................................................................ 12

Container Corporation of India .................................................................13

Gateway Distriparks .................................................................................26

Allcargo Logistics......................................................................................38

Annexure.........................................................................................................50

17 January 2013 India Logistics – Improving economic backdrop & reasonable valuations

Anand Rathi Research 3

Containerisation story to continue

Strong growth in EXIM trade Strong trade growth in India, a favourable investment environment and the country’s position as a key outsourcing hub for MNCs have led to a significant increase in EXIM trade. Over FY00-12, India’s exports have increased from `1.6trn to `14.6trn and imports excl. oil, gold & silver have increased from `1.4trn to `13.1trn at CAGR of 20.2% and 20.5% respectively.

Over the same period, engineering goods, which contributed ~14% to overall exports in FY00, has grown significantly and contributed ~22% in FY12. We believe that, with the pick-up in the global economy, exports of engineering goods could increase again after a slight dip in FY12.

India’s exports to Asia (excl. the Middle East) contribute the highest to export trade and accounted for ~31% of exports during FY12. Europe is the second-highest contributor and exports to the region were ~20% during FY12. With European countries showing signs of improvement in their economies, exports to countries in the region would improve, we believe.

Fig 1 – EXIM trade v/s GDP growth

-5

0

5

10

15

20

25

30

35

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

GDP growth EXIM growth

(%)

Source: CMIE

Fig 2 – Exports v/s imports

0

3,000

6,000

9,000

12,000

15,000

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

-10-5051015202530354045

Exports Imports (excl oil, gold & silver)Growth in Exports (RHS) Growth in Imports (RHS)

(`bn) (%)

Source: CMIE

Fig 3 – Product-wise exports

0

25

50

75

100

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

Agri products Ores & minerals Leather itemsChemicals Engg goods TextilesReadymade garments Others Petroleum productsOther commodities

(%)

Source: CMIE

Fig 4 – Region-wise break-up

0

25

50

75

100

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

Africa America Asia (excluding Middle East) the Middle East Europe OceaniaOthers

(%)

Source: CMIE

17 January 2013 India Logistics – Improving economic backdrop & reasonable valuations

Anand Rathi Research 4

Over FY00-12 India’s imports (excl. oil and bullion) have increased from `1.4trn to `13.1trn. Its non-POL imports excl. oil & gold accounted for ~52% of imports during FY12. Asia & Europe form major share of imports for India and their share has been improving over the years. Pick-up in Indian economy expected during FY14, we believe, would lead to higher demand for such imported products.

Containerisation on the rise

Significant growth in EXIM over the years has led to an increase in containerised trade. Over FY01-12 container traffic at major ports has increased from 2.47m TEUs to 7.76m at a 10.1% CAGR.

Globally, 80% of cargo is containerised, compared to ~15% in India. Thus, vast scope for containerisation still exists. Given the government’s sharper focus on exports, this is expected to increase. In its Maritime Agenda 2010-20, GoI projected that traffic at major ports is likely to register an 8% CAGR (from 561m tons in FY10 to 1,215m by FY20). At minor ports, traffic would record a 16% CAGR (from 289m tons in FY10 now to 1,270m tons by FY20). India’s trade is expected to pick-up during FY14, which we believe, would lead to an increase in containerised trade in India.

Fig 5 – Product-wise imports

0

25

50

75

100

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

Food products TextilesChemicals Capital goodsNon-POL items (excl gold & silver) Other commodities

(%)

Source: CMIE

Fig 6 – Region-wise break up

0

25

50

75

100

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

Africa America Asia (excl. Middle East) the Middle East Europe OceaniaOthers

(%)

Source: CMIE

Fig 7 – Container trade at major ports (000 TEU's) FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

Kolkata Dock System 138 98 106 123 159 203 239 297 302 378 377 412

Haldia Dock Complex 51 93 117 137 128 110 110 128 127 124 149 139

Visakhapatnam 20 22 22 20 45 47 56 71 86 98 145 234

Chennai 352 344 425 539 617 735 886 1,128 1,143 1,216 1,524 1,558

Tuticorin 157 214 213 254 307 321 377 450 439 440 468 477

Cochin 143 152 166 170 185 203 227 254 261 290 312 328

Mumbai 321 254 213 197 219 159 138 118 92 58 72 58

JNPT 1,190 1,573 1,930 2,269 2,371 2,667 3,298 4,060 3,952 4,062 4,270 4,321

Kandla 92 126 157 170 181 148 178 167 138 147 160 166

Total: 2,470 2,884 3,366 3,900 4,233 4,615 5,541 6,712 6,585 6,865 7,539 7,768

Source: Indian Ports Association

17 January 2013 India Logistics – Improving economic backdrop & reasonable valuations

Anand Rathi Research 5

Rising thrust on infrastructure Logistics in India on growth path

The Indian logistics sector has registered vast growth in the past decade, fuelled by consistent growth in the economy and in various sectors such as automobiles, pharmaceuticals, engineering, etc. As per industry estimates during FY12, the logistics sector contributed ~12-13% to GDP. In India, road transport is handled by private operators; rail transport by the Central government. With the second-largest network in the world, roads carry ~60% of freight transport. Road transport is preferred because of its cost effectiveness and flexibility. On the other hand, rail transport is sought for its container facility and ease in transporting containers and wooden crates. (Sea is a complementary mode of transport. Ninety-five per cent of India’s foreign trade is by sea).

Fig 9 – Logistics in India

Indian warehousing industry

Transportation Warehousing Value addedservices

Cold chain3PL, 4PL & 5PLPackeging services

Freight consolidation

Contanier stuffing-de stuffing

LCL consolidation (NVOCC)

Freight forwarding

Customs clearance

GodownsICD’sFTWZ’s

Logistic packs

CFS

Shipyards

Air cargo centres

Express cargoHub

RoadRailWater

Air

Source: Industry

Road transportation needs to improve

Road transportation in India is highly fragmented and largely un-organized – a large number of independent operators with regional or national permits carry freight by road. Often they have a small fleet size - one or two single-axle trucks. This segment carries a large percent of the national load and almost the entire regional load.

Fig 10 – Fleet size in India

Medium fleet operator

(6-20 trucks)15%

Small fleet operator

(1-5 trucks)75%

Large fleet operator

(>20 trucks)10%

Source: Industry

Fig 8 – % of transportation by modes

Road60%

Rail32%

Others8%

Source: Industry

17 January 2013 India Logistics – Improving economic backdrop & reasonable valuations

Anand Rathi Research 6

India has the second-largest road network in the world covering 4.24m km. Its road density is one of the highest in the world -- 1.29 km of roads per sq. km. India’s national highways and expressways, however, constitute only 1.67% of its road length but carry 40% of its road traffic. The percentage of paved roads is only 49.3%, lagging behind both the U.S. and China. Industry sources say India has a meagre 600-700 km of access-controlled expressways compared to 74,000 km of expressways in China. While India’s road freight volumes are rising at a 9.08% CAGR and the number of vehicles (all types) is increasing at a 10.76% CAGR, road length is increasing at only a 4.01% CAGR, indicating the paucity of, and dire need for, roads.

Fig 11 – Road lengths and densities for the U.S., India, China and Brazil Country Road length (m km) Road density (km/sq. km) Year

U.S. 6.5 0.68 2009

India 4.24 1.29 2010

China 3.7 0.39 2008

Brazil 1.75 0.21 2004

Source: World Bank (http://www.worldbank.org), Ministry of Road Transport and Highways, GOI (http://www.morth.nic.in), Bureau of Transportation Statistics, Govt. of U.S. (http://www.bts.gov)

Indian roads can broadly be broken down into four groups: National highways/expressways, state highways, major district roads and rural roads. While national highways and expressways connect important cities and towns of different states across the country, state highways and major district roads connect cities, towns and rural roads within a state with the national highway network.

Fig 12 – Lengths and percentages of different categories of highways/roads Category of highway/road Length (km) % of total road network

National highways/Expressways 70,934 1.67

State highways 154,522 3.65

Major district roads 2,577,396 60.84

Rural roads 1,433,577 33.84

Source: Source: Ministry of Road Transport and Highways, GOI (http://www.morth.nic.in)

Of the 70,934 km of national highways/expressways, 17,752 km (25%) are single/intermediate lanes, 36,995 km (52%) double lanes and 16,187 km (23%) four/six/eight lanes. The shortage of multi-lane highways, coupled with poor road conditions and stoppages and delays, causes congestions, accidents, break-downs and high maintenance costs of roads and vehicles.

A vehicle on Indian roads can clock an average speed of only 20-25 km an hour, covering 250-400 km in a day. In developed countries, a vehicle can cover 700-800 km in a day. Vehicles in India cover only 80,000-100,000 km in a year; in the U.S., vehicles cover up to 400,000 km in a year.

Considering this, it is important for the government to invest heavily in extending, widening and upgrading the highway network, build more quality arterial roads, implement access-control mechanisms and allocate adequate funds for road maintenance. The government should expedite the introduction of the GST across all states. This would significantly reduce paperwork and delays at check-posts.

Rail transport – awaiting the big leap through DFC

The rail network in India traverses the length and breadth of the country, covering 64,015 km (39,777 miles). It is the largest rail network in Asia and the fourth in the world, next to the USA, Russia and Canada. Till 2006, cargo transportation by rail was dominated by Concor. In order to develop

17 January 2013 India Logistics – Improving economic backdrop & reasonable valuations

Anand Rathi Research 7

infrastructure and generate more competition, the government allotted rail licenses to 15 private operators in 2006. They signed concession agreements with IR to run container trains for 20 years, extendable by another 10.

Steady growth in rail freight

Rail transportation in India currently handles ~22% of container trade, lower than other developed nations. Over FY07-12 volumes carried by the Indian Railways have registered a 13.6% CAGR to 38.4m tons. In the same period EXIM volumes at major ports have increased from 73.4m tons in FY07 to 120.2m tons in FY12. We believe that rail freight is less expensive over long distances, compared with road transport; it generally turns more cost effective for distances of over 400 km.

Fig 14 – Volumes transported by rail

0

8

16

24

32

40

FY07

FY08

FY09

FY10

FY11

FY12

EXIM Domestic

(m tons)

Source: Indian Railways

Dedicated freight corridor to boost rail freight business

IR routes connecting the four metropolitan cities of Delhi, Mumbai, Chennai and Howrah, and its Delhi-Chennai and Mumbai-Howrah routes add up to a length of 10,122 km, carrying more than 55% of its revenue-earning freight traffic. The present trunk routes of Howrah-Delhi on the Eastern Corridor and Mumbai-Delhi on the Western Corridor are highly

Fig 13 – List of CTO operators Name Group Rakes Rail Terminals Exim (%) Domestic (%) Other Activities

Adani Logistics Adani 6 2 33 67 Ports, Container terminals, CTO, CFS

Concor IR 253 63 80 20 Multi modal operator

CRRS* DPW 8 - 100 - Ports, Container terminal

CWC PSU - - 100 - Warehousing, CFS

ETA Star Group Dubai 11 - 80 20 Shipping and port services

Gateway Rail Freight GDL 21 3 84 16 CFS, CTO

Hind Terminals MSC 14 - 100 - Shipping/ Freight Forwarding

India Infra. APL 9 - 98 2 Container shipping, infra

SICAL Logistics - 8 - - 100 CFS, container terminal

Boxtrans (India)** JM Baxi & Co. 12 - 10 90 Container terminal, CFS,

TransRail Logistics - 2 - - 100 Trucking

Arshiya Rail Infra. - 20 1 5 95

KRIL - 8 - 4 96 Fertilizers

Inlogistics NOL, Singapore 15 - - -

Total 387 69 76 24

Source: Industry

17 January 2013 India Logistics – Improving economic backdrop & reasonable valuations

Anand Rathi Research 8

saturated, their line capacity utilization varying between 115% and 150%. The surging power needs in the country, booming infrastructure construction and growing international trade have led to the conception of Dedicated Freight Corridors (DFCs) along the eastern and western routes.

The DFCs would have world-class and state-of-the-art technology. Significant improvements are proposed to be made in the present carrying capacity by modifying basic design features. New lines will be constructed with significantly better designs to withstand heavier loads at higher speeds. Simultaneously, in order to optimize productive use of the right of way, dimensions of the rolling stock are proposed to be enlarged. Both these improvements would allow longer and heavier trains to ply on the DFCs.

Project phasing of eastern and western corridors

Both corridors are being constructed simultaneously. By 2017, they are likely to be fully operational over their entire lengths. The following table indicates tentative phases.

Fig 15 – Project phasing Western Corridor Year

Phase I Rewari - Vadodara (920 Kms) 2009-2016

Phase II Vadodara – JNPT (430Kms) 2010-2017

Phase III Rewari – Dadri (140 Kms) 2010-2017

Eastern Corridor

Phase I-APL1 Khurja - Kanpur (343 Kms) 2009-2016

Phase II-APL2 Kanpur - Mughalsarai (390 Kms) 2010-2016

Phase III-APL3 Khurja-Ludhiana (397 Kms) 2011-2016

Phase IV (Funding through PPP) Dankuni - Sonnagar (550 Kms) 2011-2016

Phase Ia (Funding by Ministry of Railways) Sonnagar - Mugal Sarai (125 Kms) 2010-2016

Source: DFCIL

Eastern dedicated freight corridor

The eastern DFC will cover 1,839 km, traversing six states. It is expected to cater to a number of traffic streams - coal from the eastern coal fields for power plants in U.P., Delhi, Haryana, Punjab and parts of Rajasthan; finished steel, food grain, cement, fertilizers, limestone from Rajasthan to steel plants in the east, and general goods. The total traffic in UP direction is projected to go up to 116m tons in 2021-22. Similarly, in the down direction, the traffic level has been projected to increase to 28m tons in 2021-22. The incremental traffic on the route since 2005-06, is expected to increase by a staggering 92m tons and DFC is expected to carry a significant proportion of the same.

Western dedicated freight corridor

The western corridor will cover 1,483 km of double-line electric tracks from JNPT to Dadri via Vadodara, Ahmedabad, Palanpur, Phulera and Rewari. Traffic on the Western Corridor mainly comprises containers from JNPT and the Mumbai port in Maharashtra and ports of Pipavav, Mundra and Kandla in Gujarat destined for inland container depots (ICDs) in northern India, especially at Tughlakabad, Dadri and Dandharikalan. Besides containers, other commodities moving on the Western DFC are POL, fertilizers, foodgrain, salt, coal, iron, steel and cement. The rail share of container traffic on this corridor is slated to increase from 0.69m twenty-feet equivalent units (TEUs) in 2005-06 to 6.2m in 2021-22.

Fig 16 – E-DFC details States KMs

Punjab 88

Haryana 72

Uttar Pradesh 1,049

Bihar 93

West Bengal/Jharkhand 538

Total 1,839

Source: DFCIL

Fig 17 – W-DFC details States KMs

Haryana 192

Rajasthan 553

Gujarat 588

Maharashtra 150

Total 1,483

Source: DFCIL

17 January 2013 India Logistics – Improving economic backdrop & reasonable valuations

Anand Rathi Research 9

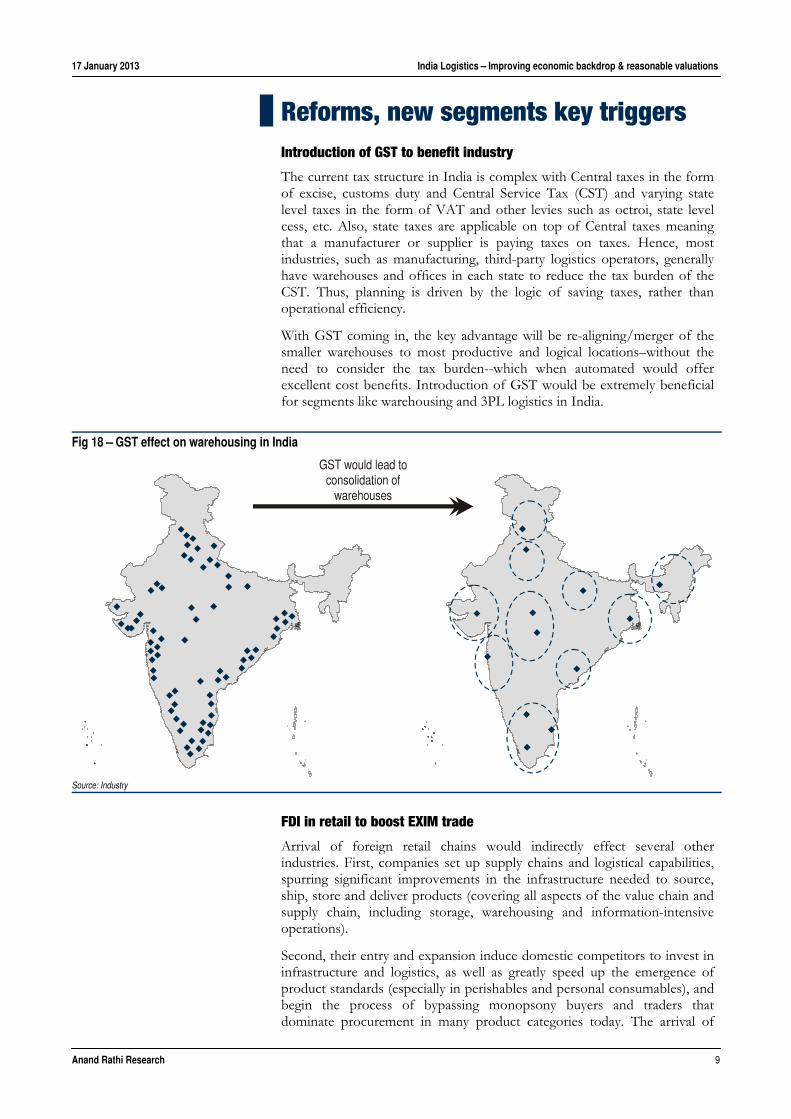

Reforms, new segments key triggers Introduction of GST to benefit industry

The current tax structure in India is complex with Central taxes in the form of excise, customs duty and Central Service Tax (CST) and varying state level taxes in the form of VAT and other levies such as octroi, state level cess, etc. Also, state taxes are applicable on top of Central taxes meaning that a manufacturer or supplier is paying taxes on taxes. Hence, most industries, such as manufacturing, third-party logistics operators, generally have warehouses and offices in each state to reduce the tax burden of the CST. Thus, planning is driven by the logic of saving taxes, rather than operational efficiency.

With GST coming in, the key advantage will be re-aligning/merger of the smaller warehouses to most productive and logical locations–without the need to consider the tax burden--which when automated would offer excellent cost benefits. Introduction of GST would be extremely beneficial for segments like warehousing and 3PL logistics in India.

FDI in retail to boost EXIM trade

Arrival of foreign retail chains would indirectly effect several other industries. First, companies set up supply chains and logistical capabilities, spurring significant improvements in the infrastructure needed to source, ship, store and deliver products (covering all aspects of the value chain and supply chain, including storage, warehousing and information-intensive operations).

Second, their entry and expansion induce domestic competitors to invest in infrastructure and logistics, as well as greatly speed up the emergence of product standards (especially in perishables and personal consumables), and begin the process of bypassing monopsony buyers and traders that dominate procurement in many product categories today. The arrival of

Fig 18 – GST effect on warehousing in India

GST would lead to consolidation of

warehouses

Source: Industry

17 January 2013 India Logistics – Improving economic backdrop & reasonable valuations

Anand Rathi Research 10

large retailers then increases sourcing of products from abroad and increases container volumes in the country. All the above mentioned factors would benefit the logistics sector in India in the long run.

Emerging segments in logistics

3PL logistics

Third-party logistics (3PL) or logistics outsourcing is gaining importance as more and more corporations across the world, unable to manage their complex supply chains, are outsourcing logistics activities to the 3PL or logistics service providers. By outsourcing logistics activities, corporations are able to not only concentrate on their core business operations, but also achieve cost-efficiency and improve delivery performance and customer satisfaction. According to industry sources, companies in India outsource ~50% of logistics. This has led to the rise of third-party logistics (3PL). These operators specialize in integrated transportation and warehousing services customized to meet clients’ needs.

3PL logistics in India is currently restricted to a few industries like autos, retail, telecom, IT hardware. We believe that with increasing demand for such services from other sectors, 3PL logistics service providers will stand to benefit from the same.

Warehousing at a nascent stage

Warehousing plays a key role in inventory management, product safety, last-mile value addition, etc. It constitutes a major cost component of the supply chain and accounts for ~20% of the Indian logistics sector. According to industry sources, India has ~1,800m sq.ft. of warehousing. Of this, only 8% or 144m sq.ft. are in the organised sector. The paucity of modern warehouses has resulted in the colossal waste of farm produce, reckoned at between 20% and 40% of the harvest. The shortage indicates the huge potential for vast quality warehousing space.

With the rapid growth of organised retail and manufacturing sectors, the need for warehousing is increasing. On the entry of foreign manufacturing, retail and 3PL companies, world-class warehousing with all modern amenities is on the rise. Moreover, the coming GST regime has necessitated organised and consolidated warehousing at well-run logistics parks.

Fig 19 – Indian warehousing sector

433m sq ftIndian warehousing

industry

Domestic367m sq ft

Unorganised398m sq ft

Organised36m sq ft

Exim66m sq ft

Source: Industry

The warehousing sector is expected to grow 35-40% annually with nearly 45m sq. ft. expected to be developed in the next five years. About 110 logistics parks are being set up across the country by several leading private players.

17 January 2013 India Logistics – Improving economic backdrop & reasonable valuations

Anand Rathi Research 11

Valuation We expect the logistics sector to be re-rated on account of higher EXIM trade volumes, increase in containerized trade, improving cash flow generation, government thrust on infrastructure spend, emergence of new segments like organized warehousing, 3PL, 4PL logistics etc which will lead to higher revenues and improving profitability for the companies. We prefer Gateway Distriparks (integrated logistics player having presence in CFS, rail transport & cold chain segment), followed by Container corporation (largest player in the CTO segment). Risks are slowdown in global trade, adverse government policies and delay in infrastructure development.

Container Corporation of India. At our price target of `1,132, the stock would trade at 15x Mar’14 earnings (in line with its past three-year average). Its one-year-forward PE in the past three years has largely ranged between 14x and 15x.

Gateway Distriparks. At our price target of `196, the stock would trade at 12x Mar’14e earnings (in line with its past three-year one-year-forward average). GD’s one-year-forward PE in the past three years has largely ranged between 10x and 14x.

Allcargo Logistics. At our price target of `159, the stock would trade at 9x Mar’14e earnings (in line with its past two-year one-year-forward average). ACG’s one-year-forward PE in the past three years has largely ranged between 9x and 11x.

Risks

Rising competition in CFS. Increasing competition at Mumbai CFS has led to slight reduction in margins. Any further increase in competition could be negative for the company.

Slowdown in capex cycle. Delayed pick up in capex cycle would have a negative effect on the P&E segment of the company.

Slowdown in world trade. Further slowdown in trade could have a negative effect on the business.

Fig 20 – Peer comparison Revenues (`m) P/E (x) P/Bv (x) EV/EBITDA (x)

Company M. Cap (US$m) FY12 FY13e FY14e FY12 FY13e FY14e FY12 FY13e FY14e FY12 FY13e FY14e

Container Corporation of India 2,233 41,009 44,337 50,757 13.7 12.5 11.6 2.1 1.9 1.7 8.7 8.9 7.7

Gateway Distriparks 275 8,215 9,653 11,532 10.9 10.6 8.4 2.0 1.9 1.7 5.7 5.5 4.5

Allcargo Logistics 311 42,711 40,706 45,375 6.1 7.9 7.4 1.2 1.0 0.9 4.0 4.0 3.3

Source: Company, Anand Rathi Research

17 January 2013 India Logistics – Improving economic backdrop & reasonable valuations

Anand Rathi Research 12

Company Section

Anand Rathi Shares and Stock Brokers Limited (hereinafter “ARSSBL”) is a full service brokerage and equities research firm and the views expressed therein are solely of ARSSBL and not of the companies which have been covered in the Research Report. This report is intended for the sole use of the Recipient and is to be circulated only within India and to no countries outside India. Disclosures and analyst certifications are present in Appendix Anand Rathi Research India Equities

India I Equities Logistics

Initiating Coverage

Key financials (YE Mar) FY11 FY12 FY13e FY14e FY15e

Sales (`m) 38,992 41,009 44,337 50,757 56,950

Net Profit (`m) 8,764 8,657 9,199 9,812 10,881

EPS (`) 67.4 66.6 70.8 75.5 83.7

Growth (%) 12.7 (1.2) 6.3 6.7 10.9

PE (x) 13.9 14.1 13.2 12.4 11.2

P BV (x) 2.5 2.2 2.0 1.8 1.6

RoE (%) 19.0 16.5 15.6 14.9 14.9

RoCE (%) 17.7 16.3 15.2 15.3 15.6

Dividend Yield (%) 1.7 1.8 1.8 1.9 2.1

Net Gearing (%) (45.5) (48.8) (32.0) (27.3) (25.4)

Source: Company, Anand Rathi Research

Dhaval Dama+9122 66266728

Relative price performance

CCRI

Sensex

800

900

1,000

1,100

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov

-12

Jan-

13

Source: Bloomberg

Key data CCRI IN / CCRI.BO52-week high / low `825 / `1104Sensex / Nifty 19987 / 60573-m average volume US$0.9m Market cap `122bn / US$2233mShares outstanding 130m

Shareholding pattern (%) Sep ’12 Jun ’12 Mar ’12

Promoters 63.1 63.1 63.1 - of which, Pledged - - -Free Float 36.9 36.9 36.9 - Foreign Institutions 26.1 25.5 25.6 - Domestic Institutions 7.3 7.1 7.3 - Public 3.5 4.3 4

Rating: Buy Target Price: `1,132

Share Price: `937

17 January 2013

Container Corporation of India

Dominant in rail freight; initiating with Buy

Container Corporation of India (CCI) is the leading container train operator (CTO) in India, with 63 terminals and 253 rakes. It will be the prime beneficiary of Indian Railways’ increased focus on raising rail transport, along with implementation of goods and service tax (GST) and foreign direct investment (FDI) in retail. It is leveraging its balance sheet strength to undertake pre-emptive capex of `62bn during FY13-17 to gear up for taking advantage of the dedicated freight corridors (DFC). We initiate coverage with Buy and price target of `1,132.

Strong network, capex for long-term gains. CCI has access to Indian Railways’ (IR) surplus land at strategic locations at attractive long-term lease rates. It has ~63 rail terminals across the country and operates ~253 rakes. It plans to incur capex of ~`62bn over FY13-17 to set up 12 logistics parks and gear up for the DFC, which would significantly benefit the country’s rail transport.

DFC, other reforms to aid business growth. IR is in the process of implementing its most ambitious project, a direct freight corridor (DFC) spanning ~3,300 km. This will significantly increase rail operators’ asset turnover and cut turnaround time sharply, improving profitability. Rise in EXIM and container trade, along with implementation of reforms such as GST and FDI in retail would immensely benefit CCI.

Leveraging strong balance sheet to fund capex. CCI had cash balance of ~28bn in FY12 and revenue is expected at 11.6% CAGR over FY12-15. We expect it to fund its own capex (~`62bn) through strong cash flows from operations. Net debt-to-equity is expected at (25.4)% in FY15.

Valuation. At our target, the stock would trade at a P/E of 15x Mar’14 earnings (in line with its past two-year average P/E). Risks. Slowdown in trade, government policies.

17 January 2013 Container Corporation of India – Dominant in rail freight; initiating with Buy

Anand Rathi Research 14

Quick Glance – Financials and ValuationsFig 1 – Income statement (`m)

Year-end: Mar FY11 FY12 FY13e FY14e FY15e

Net sales 38,992 41,009 44,337 50,757 56,950 Sales growth (%) 4.5 5.2 8.1 14.5 12.2 - Op. expenses 26,664 28,125 30,460 34,870 39,011 EBIDTA 10,153 10,230 10,907 12,486 14,124 EBITDA margins (%) 26.0 24.9 24.6 24.6 24.8 - Interest 46 50 - - - - Depreciation 1,489 1,621 1,889 2,324 2,621 + Other income 1,971 3,135 3,086 2,749 2,815 - Tax 1,800 3,037 2,905 3,099 3,436 Effective tax rate (%) 17.0 26.0 24.0 24.0 24.0 Reported cons.PAT 8,764 8,657 9,199 9,812 10,881 +/- Extraordinary items - - - - -+/- Minority interest - - - - -Adjusted cons. PAT 8,764 8,657 9,199 9,812 10,881 Adj. FDEPS (`/share) 67.4 66.6 70.8 75.5 83.7 Adj. FDEPS growth (%) 12.7 (1.2) 6.3 6.7 10.9 Source: Company, Anand Rathi Research

Fig 3 – Cash-flow statement (`m) Year-end: Mar FY11 FY12 FY13e FY14e FY15e

Consolidated PAT 8,764 8,657 9,199 9,812 10,881 + Non Cash Items 1,667 1,771 1,889 2,324 2,621 Cash profit 10,431 10,428 11,088 12,136 13,502 - Incr/(Decr) in WC 851 2,622 828 913 787 Operating cash flow 9,580 7,806 10,260 11,223 12,715 - Capex 4,214 212 14,849 9,500 9,000 Free cash flow 5,366 7,595 (4,590) 1,723 3,715 - Dividend 2,345 2,493 2,585 2,737 3,042 + Equity raised (0) - - (0) (0)+ Debt raised 49 45 - - -- Investments 34 491 - - -- Misc. items (0) 0 (1) - -Net cash flow 3,036 4,655 (7,174) (1,014) 674 + Opening cash 19,925 22,961 27,616 20,442 19,428 Closing cash 22,961 27,616 20,442 19,428 20,102 Source: Company, Anand Rathi Research

Fig 5 – PE band

4x

8x

12x

16x

20x

0

200

400

600

800

1,000

1,200

1,400

1,600

Apr-0

8

Aug-

08

Dec

-08

Apr-0

9

Aug-

09

Dec

-09

Apr-1

0

Aug-

10

Dec

-10

Apr-1

1

Aug-

11

Dec

-11

Apr-1

2

Aug-

12

Dec

-12

Source: Bloomberg, Anand Rathi Research

Fig 2 – Balance sheet (`m) Year-end: Mar FY11 FY12 FY13e FY14e FY15e

Share capital 1,300 1,300 1,300 1,300 1,300 Reserves & surplus 48,088 54,252 60,866 67,941 75,780 Shareholders’ fund 49,388 55,552 62,165 69,240 77,080 Debt 473 519 519 519 519 Minority interests - - - - -Deferred Tax Liab (net) 2,288 2,438 2,438 2,438 2,438 Capital employed 52,149 58,508 65,122 72,197 80,036 Net Fixed assets 27,148 25,739 38,699 45,875 52,254 Investments 1,956 2,447 2,447 2,447 2,447 - of which liquid 1,956 2,447 2,447 2,447 2,447 Working capital 84 2,705 3,533 4,446 5,233 Cash 22,961 27,616 20,442 19,428 20,102 Capital deployed 52,149 58,508 65,122 72,197 80,036 Net Debt/Equity (%) (45.5) (48.8) (32.0) (27.3) (25.4)W C turn (days) (3.2) 12.4 25.7 28.7 31.0 Book Value (`/share) 380.0 427.4 478.3 532.7 593.0 Source: Company, Anand Rathi Research

Fig 4 – Ratio analysis @ `937 Year-end: Mar FY11 FY12 FY13e FY14e FY15e

P/E (x) 13.9 14.1 13.2 12.4 11.2 Cash P/E (x) 11.7 11.7 11.0 10.0 9.0 P/B (x) 2.5 2.2 2.0 1.8 1.6 EV/sales (x) 2.5 2.2 2.2 2.0 1.8 EV/EBITDA (x) 9.6 9.0 9.1 8.0 7.1 RoE (%) 19.0 16.5 15.6 14.9 14.9 RoCE (%) 17.7 16.3 15.2 15.3 15.6 Dividend yield (%) 1.7 1.8 1.8 1.9 2.1 Dividend payout (%) 26.8 28.8 28.1 27.9 28.0 Debt to equity (x) 0.0 0.0 0.0 0.0 0.0 Int Coverage (x) 188.8 170.8 - - -Receivables days 2.3 2.7 2.8 2.9 2.9 Payables days 61.0 57.1 59.0 55.0 53.0 Working capital days (3.2) 12.4 25.7 28.7 31.0 Fixed asset T/O (x) 1.5 1.6 1.4 1.2 1.2 Source: Company, Anand Rathi Research

Fig 6 – FY12 revenue breakdown

EXIM80%

Others1%

Domestic19%

Source: Company

17 January 2013 Container Corporation of India – Dominant in rail freight; initiating with Buy

Anand Rathi Research 15

Widest network in industry Strong infrastructure network a key advantage

CCI’s widest rail network is its chief edge over peers. It has 63 strategically located rail terminals, 12 dedicated for domestic traffic, 18 for EXIM and 33 for both. Even six years after 15 private CTOs entered the business, cumulatively they have set up only seven terminals. Of course, CCI benefits from attractive long-term lease rates for IR’s surplus land at strategic locations. Also, it has ~253 rakes, more than its peers’ combined capacity. We believe its strong rail network affords it a greater leverage with major shipping lines which handle most EXIM trade. Also, it is able to pass on to end-customers any rise in rail haulage charges.

Fig 7 – Concor’s infrastructure network

Source: Company

High-margin EXIM business to be highest contributor

The Indian rail CTO business stands at ~38m tons, valued at ~`58bn. It can be divided into two segments – EXIM and domestic. EXIM accounts for ~75% of the market and domestic segment ~25%. At present, 15 container train operators (besides CONCOR) have signed concession agreements with IR to run container trains.

Over FY07-12, volumes transported by rail have increased from 20.3m tons to 38.4m tons, indicating a CAGR of 13.6%.During the same period volumes transported by CCI have increased from 2.1m TEU’s to 2.6m TEU’s.

17 January 2013 Container Corporation of India – Dominant in rail freight; initiating with Buy

Anand Rathi Research 16

Fig 8 – Volumes transported by rail

0

8

16

24

32

40

FY07

FY08

FY09

FY10

FY11

FY12

2.00

2.15

2.30

2.45

2.60

2.75

Total rail volumes Volumes transported by Concor (RHS)

(m tons) (m TEUs)

Source: Company, Anand Rathi Research

About 80% of CCI’s revenues arise from the high-margin EXIM traffic, commanding EBIT margins of ~26-27%. Its domestic traffic generally has margins of ~8-10% (nearly 55% of its business comes from the northern region and from ferrying goods to JNPT and nearby ports.) We expect EXIM trade to pick up in FY14, leading to more container traffic in India, raising CCI’s volumes. Over FY12-15, we expect CCI’s EXIM volumes to record an 8% CAGR and domestic volumes 7% CAGR. In the same period, we expect its overall CTO revenues to record a 12% CAGR.

Fig 11 – TEUs handled, by region FY06 FY07 FY08 FY09 FY10 FY11 FY12

Western 282,853 290,625 395,144 320,262 324,161 372,574 352,282

Eastern 80,612 82,594 101,168 90,865 121,845 129,029 119,018

Southern 289,061 303,468 340,659 345,805 284,357 334,532 355,944

Central 79,665 97,151 107,028 104,897 123,092 127,734 151,705

North Central 152,114 204,973 283,092 288,398 316,980 288,858 282,595

Northern 836,574 889,615 936,362 857,929 898,915 917,029 948,849

South central 82,999 81,846 102,013 111,275 135,053 152,243 139,587

North Western 126,684 154,994 181,843 188,801 216,844 240,298 254,331

Total 1,930,562 2,105,266 2,447,309 2,308,232 2,421,247 2,562,297 2,604,311

Source: Company

Fig 9 – TEUs - EXIM and domestic

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

FY09

FY10

FY11

FY12

FY13

e

FY14

e

FY15

e

EXIM Domestic

(TEU)

Source: CMIE

Fig 10 – Realisation trend - EXIM and domestic

0

4,000

8,000

12,000

16,000

20,000

FY09

FY10

FY11

FY12

FY13

e

FY14

e

FY15

e

EXIM Domestic

(`/TEU)

Source: Industry

17 January 2013 Container Corporation of India – Dominant in rail freight; initiating with Buy

Anand Rathi Research 17

Fig 12 – EXIM and domestic business FY09 FY10 FY11 FY12 FY13 FY14 FY15

Exim

TEU's 1,854,959 1,882,277 2,018,551 2,136,000 2,264,160 2,445,293 2,689,822

Segment revenue (`bn) 27 29 30 33 36 41 46

Revenue/TEU 14,696 15,399 14,832 15,288 15,747 16,692 17,026

EBIDTA (`bn) 8.68 8.59 9.35 9.84 10.34 12.04 13.74

EBIDTA margin % 32 30 31 30 29 30 30

EBIDTA/TEU 4,680 4,565 4,633 4,605 4,567 4,924 5,108

EBIT (`bn) 7.82 7.59 8.28 8.63 9.09 10.53 11.91

EBIT margin % 29 26 28 26 26 26 26

EBIT/TEU 4,215 4,033 4,103 4,040 4,015 4,306 4,427

Domestic

TEU's 453,273 538,970 543,746 468,311 496,410 536,122 589,735

Segment revenue (`bn) 6.91 8.07 8.40 7.95 8.68 9.94 11.15

Revenue/TEU 15,246 14,977 15,440 16,983 17,493 18,542 18,913

EBIDTA (`bn) 1.14 1.45 1.17 1.03 1.11 1.29 1.45

EBIDTA margin % 17 18 14 13 13 13 13

EBIDTA/TEU 2,521 2,692 2,154 2,203 2,239 2,411 2,459

EBIT (`bn) 0.87 1.12 0.80 0.66 0.71 0.84 0.95

EBIT margin % 13 14 10 8 8 9 9

EBIT/TEU 1,911 2,079 1,474 1,420 1,434 1,576 1,608

Source: Company, Anand Rathi Research

Capex of ~`62bn to drive future growth

Gearing up for completion of IR’s most ambitious project, DFC, in FY17, CCI is undertaking capex of ~`62bn over FY13-17. For this, it is acquiring land to set up 12 strategically located multi-modal logistics parks (MMLP) across India, providing transportation services and value-added ones required for import or export of goods. It also plans to invest a significant amount in acquiring additional rakes and purchasing new equipment. We believe that this capex would reduce its short-term FCF and help in building up base for future growth. During FY13, it has planned a capex of~`15bn.

Fig 13 – FY13 capex plans (~`15bn)

Land43%

Civil6%

ons / Rakes21%

Equipments / Others30%

Source: Company

Fig 14 – FY13-17 capex plans (~`62bn)

Land19%

Civil8%

Equipments / Others41%

Wagons / Rakes32%

Source: Company

17 January 2013 Container Corporation of India – Dominant in rail freight; initiating with Buy

Anand Rathi Research 18

DFC, reforms to grow business Dedicated freight corridor to transform CTO business

DFC is one of the largest infrastructure projects of IR since independence. IR’s routes - connecting the four metropolises (Delhi, Mumbai, Chennai, Kolkata) and the two diagonals (Delhi-Chennai, Mumbai-Howrah) - add up to a route length of 10,122 km. They carry over 55% of the revenue-earning freight traffic.

The present trunk routes of Howrah-Delhi (Eastern Corridor) and Mumbai-Delhi (Western Corridor) are highly saturated, with line-capacity utilization of 115% to 150%. Surging power needs in the country require vast coal movements, booming infrastructure construction and growing international trade. All this had led to the conception of the DFCs.

For this, under the administrative control of the Ministry of Railways, the Dedicated Freight Corridor Corporation of India (DFCCI), a special purpose vehicle was set up. It is constructing two corridors, the Western DFC (Dadri to Mumbai, passing through Delhi, Haryana, Rajasthan, Gujarat and Maharashtra) and the Eastern DFC – from Ludhiana (Punjab) to Dankuni (West Bengal) crossing Haryana, Uttar Pradesh and Bihar. The first phase of the two corridors covers ~3,300 km.

DFCCI envisages long-haul operations, with trailer loads rising from ~4,000 to ~15,000 tons, carrying capacity from 90 containers to 400 (double stacking), maximum speed from 75kmph to 100kmph and station spacing of 7-10 km to 40 km. CTOs would thus be able to reduce costs through greater efficiencies (higher asset turnover and faster turnaround time) and become the reliable/preferred mode for longer-haul freight movement. CCI would, of course, be the chief beneficiary.

Fig 15 – DFC to improve CTO efficiency

Moving dimensions

Feature Existing On DFC

Height7.1m for Western DFC5.1m for Eastern DFC4.265m

Width

3,200 mm 3,660 mm

Containerstack Single stack Double stack

Train length

700 mm 1,500 mm

Train load 4,000 ton 15,000 ton

Source: DFCCIL

17 January 2013 Container Corporation of India – Dominant in rail freight; initiating with Buy

Anand Rathi Research 19

The project cost is `930bn, including `70bn for land. The net requirement for the DFC project is `880bn. Of this, `100bn of Sonnagar- Dankuni (Eastern DFC) will be funded on a PPP basis – IDC: `60bn; Bridges: `60bn. Thus, DFCCI requires funding of `680bn – debt of `420bn (JICA: `280bn and WB: `140bn) and equity of `260bn.

Key reforms such as GST, FDI in retail augur well

Implementation of GST by the Centre would be a significant positive for the logistics sector, particularly for multimodal operators like CCI. At present, multiple and varied state taxes compel most companies to set up warehouses in each state to minimize inter-state movement and associated taxes. Implementation of GST, which aims to level such taxes, would obviate the need for multiple warehouses.

Consequently, companies would function effectively with fewer strategically-located warehouses across the country and adopt a hub-and-spoke model to reduce inventory and carrying costs. Transport requirements would shift from shorter-haul ‘warehouse-to-warehouse’ to longer-haul ‘factory-to-factory’, boosting operators such as CCI, which effectively handles the entire logistics chain.

FDI in multi-brand retail

To transport perishable products from source to end users, CCI has been setting up cold chains. At present, only 10-15% of cold storage operators have such capabilities, primarily due to absence of reefer container links and high cost of power. CCI has huge plans to tap agricultural business opportunities through cold storages. For this, it has constituted a 100% subsidiary, Fresh and Healthy Enterprises (FHE). The approval of FDI in retail could attract established MNCs which could become CCI’s customers.

17 January 2013 Container Corporation of India – Dominant in rail freight; initiating with Buy

Anand Rathi Research 20

Leveraging strong balance sheet

Capex to be funded by internal accruals

The company is incurring capex of ~`62bn over FY13-17. We believe it would generate strong FCF over FY12-15, which would help fund the capex required. We expect it to be debt free with a net debt-to-equity of (25.4)% in FY15. On the completion of its capex, we expect it to generate higher cash flows.

Fig 16 – FCF v/s net D/E

-5,000

-2,500

0

2,500

5,000

7,500

10,000

FY09

FY10

FY11

FY12

FY13

e

FY14

e

FY15

e

-50

-46

-42

-38

-34

-30

-26

FCF Net D/E (RHS)

(`m) (%)

Source: Company, Anand Rathi Research

Strategic JVs to aid business CCI has entered into strategic JVs with others in logistics, from CFS operators to road transport operators. This has helped position it as a total logistics solutions provider, offering door-to-door services to suit customers’ needs. We believe that many of these JVs, which are still at a very nascent stage, would further strengthen its position in logistics.

Cold-chain business to benefit from FDI in retail

CCI’s 100% subsidiary, Fresh and Healthy Enterprises, manages a cold chain. Its major clients are large retailers in India (Walmart, More, Big Bazaar, etc.) and those in the dairy segment (Mother Dairy, etc.). On implementation of FDI in retail, demand would rise considerably, benefiting CCI.

Fig 17 – Details of JVs Particulars Type Holding (%)

Star Track Terminals JV with Maersk India for CFS at Dadri, U.P. 49

Albatross Inland Ports JV with Transworld Group for CFS at Dadri, U.P. 49

Gateway Terminals India JV with APM Terminals for third berth at JN Port, Mumbai 26

CMA-CGM Logistics Park* JV with Ameya Logistics for CFS at Dadri, UP 49

Himalayan Terminals JV with Nepalese Ent & Transworld for management and operation of rail CTO at Birgunj (Nepal) 40

HALCON A arrangement with Hindustan Aeronautics for operating air cargo complex & ICD at Ozar airport, Nasik 50

India Gateway Terminal JV with Dubai Port Int. (DPI) for setting up and managing Container Terminals at Cochin 15

Hind CONCOR Terminals* JV with Hind Terminals for CFS at Dadri, U.P. 49

Infinite Logistics Solutions JV with TCI Ltd.to establish logistics freight terminals and provide integrated logistics services 49

Container Gateway JV with Gateway Rail for operations of existing rail/ road container terminal at Garhi Harsaru, Gurgaon 49

Allcargo Logistics Park JV with Allcargo Global for setting up and running CFS at Dadri 49

CONYK Cartrac JV with NYK Auto Logistics for setting up & dealing in CBU vehicle logistics 50

Source: Company

17 January 2013 Container Corporation of India – Dominant in rail freight; initiating with Buy

Anand Rathi Research 21

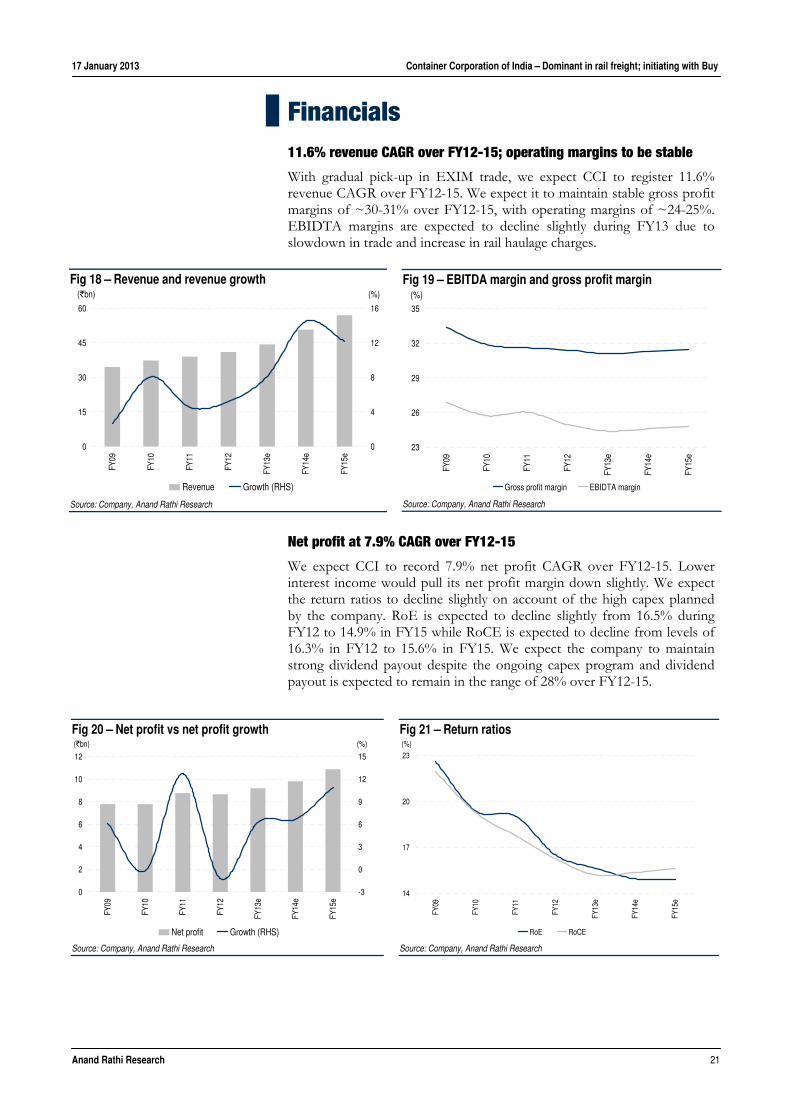

Financials 11.6% revenue CAGR over FY12-15; operating margins to be stable

With gradual pick-up in EXIM trade, we expect CCI to register 11.6% revenue CAGR over FY12-15. We expect it to maintain stable gross profit margins of ~30-31% over FY12-15, with operating margins of ~24-25%. EBIDTA margins are expected to decline slightly during FY13 due to slowdown in trade and increase in rail haulage charges.

Net profit at 7.9% CAGR over FY12-15

We expect CCI to record 7.9% net profit CAGR over FY12-15. Lower interest income would pull its net profit margin down slightly. We expect the return ratios to decline slightly on account of the high capex planned by the company. RoE is expected to decline slightly from 16.5% during FY12 to 14.9% in FY15 while RoCE is expected to decline from levels of 16.3% in FY12 to 15.6% in FY15. We expect the company to maintain strong dividend payout despite the ongoing capex program and dividend payout is expected to remain in the range of 28% over FY12-15.

Fig 18 – Revenue and revenue growth

0

15

30

45

60

FY09

FY10

FY11

FY12

FY13

e

FY14

e

FY15

e

0

4

8

12

16

Revenue Growth (RHS)

(`bn) (%)

Source: Company, Anand Rathi Research

Fig 19 – EBITDA margin and gross profit margin

23

26

29

32

35

FY09

FY10

FY11

FY12

FY13

e

FY14

e

FY15

e

Gross profit margin EBIDTA margin

(%)

Source: Company, Anand Rathi Research

Fig 20 – Net profit vs net profit growth

0

2

4

6

8

10

12

FY09

FY10

FY11

FY12

FY13

e

FY14

e

FY15

e

-3

0

3

6

9

12

15

Net profit Growth (RHS)

(`bn) (%)

Source: Company, Anand Rathi Research

Fig 21 – Return ratios

14

17

20

23

FY09

FY10

FY11

FY12

FY13

e

FY14

e

FY15

e

RoE RoCE

(%)

Source: Company, Anand Rathi Research

17 January 2013 Container Corporation of India – Dominant in rail freight; initiating with Buy

Anand Rathi Research 22

Fig 22 – Income statement (`m) Year-end: Mar FY11 FY12 FY13e FY14e FY15e Revenue 38,992 41,009 44,337 50,757 56,950 - Op. expenses 12,328 12,884 13,878 15,887 17,939 - Employee Costs 889 1,018 1,153 1,320 1,481 - Other Administrative 1,287 1,636 1,818 2,081 2,335 EBIDTA 10,153 10,230 10,907 12,486 14,124 - Interest 46 50 - - -- Depreciation 1,489 1,621 1,889 2,324 2,621 + Other income 1,971 3,135 3,086 2,749 2,815 - Tax 1,800 3,037 2,905 3,099 3,436 PAT 8,789 8,657 9,199 9,812 10,881 Consolidated PAT 8,764 8,657 9,199 9,812 10,881 Dividend 876 878 2,585 2,737 3,042 FDEPS (` / share) 67.4 66.6 70.8 75.5 83.7 CEPS (` / share) 80.3 80.2 85.3 93.4 103.9 DPS (` / share) 15.5 16.5 17.0 18.0 20.0 BV (` / share) 380.0 427.4 478.3 532.7 593.0 Shares outstanding 130.0 130.0 130.0 130.0 130.0 Growth Rates Revenue (%) 4.5 5.2 8.1 14.5 12.2 EBIDTA (%) 5.8 0.8 6.6 14.5 13.1 Net PAT (%) 12.7 (1.2) 6.3 6.7 10.9 Diluted EPS (%) 12.7 (1.2) 6.3 6.7 10.9 FY12-15e Revenue CAGR(%) 11.6 FY12-15e EBITDA CAGR (%) 11.3 FY12-15e EPS CAGR (%) 7.9 Margins EBIDTA (%) 26.0 24.9 24.6 24.6 24.8 EBIT (%) 22.2 21.0 20.3 20.0 20.2 Net Profit (%) 22.5 21.1 20.7 19.3 19.1

Source: Company, Anand Rathi Research

Fig 23 – Balance sheet (`m) Year-end: Mar FY11 FY12 FY13e FY14e FY15e Sources of Funds Share capital 1,300 1,300 1,300 1,300 1,300 Reserves & surplus 48,088 54,252 60,866 67,941 75,780 Shareholders’ fund 49,388 55,552 62,165 69,240 77,080 Debt 473 519 519 519 519 Deferred Tax Liab (net) 2,288 2,438 2,438 2,438 2,438 Capital employed 52,149 58,508 65,122 72,197 80,036 Application of Funds Gross Fixed Assets 33,678 35,931 49,931 59,431 68,431 Less: Depreciation 9,722 11,343 13,232 15,556 18,177 Net Fixed Assets 23,956 24,588 36,699 43,875 50,254 Capital Work in Progress 3,191 1,151 2,000 2,000 2,000 Investments 1,956 2,447 2,447 2,447 2,447 Current Assets Inventories 125 360 369 417 468 Debtors 296 303 377 429 476 Loans and Advances 4,469 7,478 8,424 9,644 10,820 Current Liab and Provisions 5,539 6,570 6,885 7,416 8,041 Net Current Assets 23,044 30,321 23,976 23,874 25,335 Working Capital 84 2,705 3,533 4,446 5,233 Cash 22,961 27,616 20,442 19,428 20,102 Capital deployed 52,149 58,508 65,122 72,197 80,036 Net Debt/Equity (%) (45.5) (48.8) (32.0) (27.3) (25.4)

Source: Company, Anand Rathi Research

17 January 2013 Container Corporation of India – Dominant in rail freight; initiating with Buy

Anand Rathi Research 23

Fig 24 – Cash flow statement (`m) Year-end: Mar FY11 FY12 FY13e FY14e FY15e

Consolidated PAT 8,764 8,657 9,199 9,812 10,881

+ Depreciation 1,489 1,621 1,889 2,324 2,621

+ Deferred Tax 179 150 - - -

+ Other non cash - - - - -

Cash profit 10,431 10,428 11,088 12,136 13,502

- Incr/(Decr) in WC 851 2,622 828 913 787

Operating cash flow 9,580 7,806 10,260 11,223 12,715

- Capex 4,214 212 14,849 9,500 9,000

Free cash flow 5,366 7,595 (4,590) 1,723 3,715

- Dividend 2,345 2,493 2,585 2,737 3,042

+ Equity raised - - - - -

+ Debt raised 49 45 - - -

- Investments 34 491 - - -

- Misc. items - - (1) - -

Net cash flow 3,036 4,655 (7,174) (1,014) 674

+ Opening cash 19,925 22,961 27,616 20,442 19,428

Closing cash 22,961 27,616 20,442 19,428 20,102

Source: Company, Anand Rathi Research

Fig 25 – Ratio analysis @ `937 Year-end: Mar FY11 FY12 FY13e FY14e FY15e

Valuations

P / E 13.9 14.1 13.2 12.4 11.2

P / BV 2.5 2.2 2.0 1.8 1.6

M Cap / Sales 3.1 3.0 2.7 2.4 2.1

EV / Sales 2.5 2.2 2.2 2.0 1.8

EV / EBIDTA 9.6 9.0 9.1 8.0 7.1

Dividend

Dividend yield (%) 1.7 1.8 1.8 1.9 2.1

Dividend payout (%) 26.8 28.8 28.1 27.9 28.0

Leverage

Net Debt / Equity (46) (49) (32) (27) (25)

Int Coverage 189 171 - - -

Return Ratios ROE (%) 19.0 16.5 15.6 14.9 14.9

ROCE (%) 17.7 16.3 15.2 15.3 15.6

Source: Company, Anand Rathi Research

17 January 2013 Container Corporation of India – Dominant in rail freight; initiating with Buy

Anand Rathi Research 24

Valuation At our price target of `1,132, the stock would trade at 15x Mar’14 earnings (in line with its past three-year average). Its one-year-forward PE in the past three years has largely ranged between 14x and 15x. At the current market price of `937, it trades at PE of 13.2x and 12.4x FY13e and FY14e earnings, respectively, and EV/EBITDA of 9.1x and 8x. We initiate coverage with a Buy and a target price of `1,132.

Fig 26 – 12-month-forward PE: Mean and standard deviation

Mean

+1SD

+2SD

-1SD

-2SD

0

5

10

15

20

25

Mar

-08

Jun-

08

Sep-

08

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Source: Bloomberg, Anand Rathi Research

Risks

Slowdown in EXIM trade. Any slowdown in the world economy would lead to decelerating EXIM trade, hitting CCI.

Increase in rail haulage charges. Further increase in rail haulage charges could affect the company if it isn’t able to pass on the increase in prices. It could lead to higher preference by end customers for other modes of transportation.

Increase in competition. Any further increase in competition by the private players could have a negative effect on the volumes for Container corp.

17 January 2013 Container Corporation of India – Dominant in rail freight; initiating with Buy

Anand Rathi Research 25

Company Overview Established in 1988 to take over the network of seven ICDs from the Indian Railways, the state-owned Container Corp. of India is today the leading CTO operator in the country with a network spanning 63 ICDs/CFSs.

Background

Container Corporation of India Ltd. (CONCOR), was incorporated in March 1988 and commenced operation from November 1989 taking over the existing network of 7 ICDs from the Indian Railways. The company has gone on to become an undisputed market leader having the largest network of 62 ICDs/CFSs in India. In addition to providing inland transport by rail for containers, it has also expanded to cover management of Ports, air cargo complexes and establishing cold-chain. It has and will continue to play the role of promoting containerization of India by virtue of its modern rail wagon fleet, customer friendly commercial practices and extensively used Information Technology. The company developed multimodal logistics support for India’s International and Domestic containerization and trade.

Fig 27 – Revenue breakdown (FY12)

EXIM80%

Domestic19%

Others1%

Source: Company

Key management personnel Managing director – Mr Anil Kumar Gupta

Finance director – Smt P.Alli. Rani

Director, Projects & Services – Mr Harpreet Singh

Director, International Marketing and Operations – Mr Yash Vardhan

Anand Rathi Shares and Stock Brokers Limited (hereinafter “ARSSBL”) is a full service brokerage and equities research firm and the views expressed therein are solely of ARSSBL and not of the companies which have been covered in the Research Report. This report is intended for the sole use of the Recipient and is to be circulated only within India and to no countries outside India. Disclosures and analyst certifications are present in Appendix Anand Rathi Research India Equities

Dhaval Dama+9122 66266728

India I Equities Logistics

Initiating Coverage

Key financials (YE Mar) FY11 FY12 FY13e FY14e FY15e

Sales (`m) 5,991 8,215 9,653 11,532 13,429

Net Profit (`m) 968 1,356 1,402 1,769 2,146

EPS (`) 8.9 12.5 12.9 16.3 19.8

Growth (%) 22.2 40.2 3.4 26.2 21.3

PE (x) 15.3 10.9 10.6 8.4 6.9

P BV (x) 2.1 2.0 1.9 1.7 1.5

RoE (%) 14.7 18.9 18.8 22.1 24.4

RoCE(%) 10.3 15.5 22.1 25.2 28.1

Dividend Yield (%) 4.4 4.4 5.1 5.8 7.3

Net Gearing (%) (5.1) (8.4) (0.2) 0.4 (7.1)

Source: Company, Anand Rathi Research

Relative price performance

GDPL

Sensex

125

135

145

155

165

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov

-12

Jan-

13

Source: Bloomberg

Key data GDPL IN / GATE.BO52-week high / low `160 / `125Sensex / Nifty 19987 / 60573-m average volume US$0.3m Market cap `15bn / US$275mShares outstanding 108.4m

Shareholding pattern (%) Sep ’12 Jun ’12 Mar ’12

Promoters 40.4 40.4 40.4 - of which, Pledged 37.3 37.3 43.8Free Float 59.6 59.6 59.6 - Foreign Institutions 24.1 23.4 27.4 - Domestic Institutions 20.2 20.8 17.4 - Public 15.3 15.4 14.8

Rating: Buy Target Price: `196 Share Price: `135

17 January 2013

Gateway Distriparks

Integrated play on logistics; initiating with Buy

Gateway Distriparks (GD), an integrated logistics company in container freight stations, rail freight and cold storage, is expected to be a key beneficiary of the rising containerization in India. Over FY12-15, its revenue and profit are expected to record CAGR of 17.8% and 16.5% respectively. We recommend Buy with a price target of `196.

CFS business to be the cash cow. In Q2FY13, the slowing global trade hit volumes at its JNPT container freight station (CFS) facility. On the expected revival in EXIM traffic after FY13, its JNPT CFS volumes are expected to record 6% CAGR over FY12-15. We expect 9.6% CAGR in its CFS revenue over FY12-15. Its net profit margin is expected to remain high (~33%) and bring in 66% to profit in FY15 (from 79% at present).

Rail business to normalize soon. India’s largest private container train operator (21 rakes, +700 wagons), GD, plans to add 6-9 rakes in FY13. It has inland container depots (ICD) at Garhi, Ludhiana, Kalamboli and one coming up at Assauti (Faridabad). With new ICDs (and new routes) commencing, we expect its rail volumes to rise. In FY14, profit would rise on pass-through of higher rail-haulage charges. Over FY12-15, we expect 18.4% revenue CAGR from the rail segment.

FDI in retail to benefit subsidiary. Snowman Frozen Foods (SFF), a subsidiary, is engaged in transportation and storage of frozen foods. It has 28,000 pallets, over 100 reefer trucks and operations spanning more than 14 major cities. SFF plans to raise its pallet capacity to 46,000 by end-FY13. This could benefit GD immensely in view of GoI’s recent directive allowing 51% FDI in multi-brand retailing.

Valuation. At our price target, the stock would trade at a P/E of 12x Mar’14 earnings (in line with its last two-year average P/E). Risks. Slowdown in trade, adverse government policies.

17 January 2013 Gateway Distriparks – Integrated play on logistics; initiating with Buy

Anand Rathi Research 27

Quick Glance – Financials and ValuationsFig 1 – Income statement (`m)

Year-end: Mar FY11 FY12 FY13e FY14e FY15e

Net revenues 5,991 8,215 9,653 11,532 13,429 Revenue growth (%) 16.0 37.1 17.5 19.5 16.4 - Op. expenses 3,342 4,527 5,551 6,573 7,655 EBIDTA 1,597 2,484 2,688 3,333 3,908 EBITDA margin (%) 26.7 30.2 27.8 28.9 29.1 - Interest expenses 182 135 174 239 232 - Depreciation 502 628 681 758 824 + Other income 129 144 169 202 235 - Tax 44 508 546 692 841 Effective tax rate (%) 4.2 27.3 27.3 27.3 27.3 Reported PAT 997 1,356 1,456 1,846 2,245 +/- Extraordinary items - - - - -+/- Minority interest (30) - (54) (77) (99)Adjusted PAT 968 1,356 1,402 1,769 2,146 Adj. FDEPS (`/share) 8.9 12.5 12.9 16.3 19.8 Adj. FDEPS growth (%) 22.2 40.2 3.4 26.2 21.3 Source: Company, Anand Rathi Research

Fig 3 – Cash-flow statement (`m) Year-end: Mar FY11 FY12 FY13e FY14e FY15e

PAT 968 1,356 1,402 1,769 2,146 + Non-cash items 455 628 681 758 824 Cash profit 1,422 1,984 2,083 2,527 2,970 - Incr./(Decr.) in WC 369 173 416 113 87 Operating cash-flow 1,054 1,812 1,667 2,414 2,883 - Capex 1,625 973 1,386 1,450 900 Free-cash-flow (572) 838 281 964 1,983 - Dividend 756 755 887 1,013 1,267 + Equity raised 10 50 - - -+ Debt raised (945) (117) 600 400 (500)- Investments (20) (130) - - -- Misc. items 4 (9) - - -Net cash-flow 711 156 (6) 350 216 + Op. cash & bank bal. 795 1,506 1,662 1,656 2,006 Cl. cash & bank bal. 1,506 1,662 1,656 2,006 2,223 Source: Company, Anand Rathi Research

Fig 5 – PE band

3x

6x

9x

12x

15x

0

50

100

150

200

250

Apr-0

8

Aug-

08

Dec

-08

Apr-0

9

Aug-

09

Dec

-09

Apr-1

0

Aug-

10

Dec

-10

Apr-1

1

Aug-

11

Dec

-11

Apr-1

2

Aug-

12

Dec

-12

Source: Bloomberg, Anand Rathi Research

Fig 2 – Balance sheet (`m) Year-end: Mar FY11 FY12 FY13e FY14e FY15e

Share capital 1,080 1,083 1,083 1,083 1,083 Reserves & surplus 5,799 6,395 6,910 7,666 8,545 Net worth 6,879 7,478 7,993 8,749 9,628 Total debt 1,154 1,037 1,637 2,037 1,537 Minority interest 610 663 663 663 663 Def. tax liab. (net) 140 140 140 140 140 Capital employed 11,741 12,276 13,391 14,547 14,926 Net fixed assets 9,825 9,861 10,559 11,251 11,327 Investments 130 310 317 317 317 - of which, Liquid 90 - - - -Net working capital 270 443 859 972 1,059 Cash and bank balance 1,506 1,662 1,656 2,006 2,223 Capital deployed 11,741 12,276 13,391 14,547 14,926 Net debt/Equity (%) (5.1) (8.4) (0.2) 0.4 (7.1)WC days 5.2 15.9 24.6 29.0 27.6 Book value (`/sh) 63.7 69.1 73.8 80.8 88.9 Source: Company, Anand Rathi Research

Fig 4 – Ratio analysis @ `135 Year-end: Mar FY11 FY12 FY13e FY14e FY15e

P/E (x) 15.3 10.9 10.6 8.4 6.9 Cash P/E (x) 10.4 7.5 7.1 5.9 5.0 P/B (x) 2.1 2.0 1.9 1.7 1.5 EV/sales (x) 2.4 1.7 1.5 1.3 1.1 EV/EBITDA (x) 9.0 5.7 5.5 4.5 3.6 RoE (%) 14.7 18.9 18.8 22.1 24.4 RoCE (%) 10.3 15.5 22.1 25.2 28.1 Dividend yield (%) 4.4 4.4 5.1 5.8 7.3 Dividend payout (%) 78.1 55.6 63.2 57.3 59.0 Debt to equity (x) 0.2 0.1 0.2 0.2 0.2 Int Coverage (x) 6.0 13.7 11.5 10.8 13.3 Receivables days 39.8 28.6 35.0 40.0 37.0 Payables days 92.4 57.4 55.0 55.0 52.0 Working capital days 5.2 15.9 24.6 29.0 27.6 Fixed asset T/O (x) 0.6 0.8 0.9 1.1 1.2 Source: Company, Anand Rathi Research

Fig 6 – FY12 revenue break-up

Rail54%

CFS38%

Snowman8%

Source: Company

17 January 2013 Gateway Distriparks – Integrated play on logistics; initiating with Buy

Anand Rathi Research 28

CFS business to be the cash cow Strategic CFS locations advantageous

One of the largest CFS operators in India, GD operates four CFSs (two at Navi Mumbai and one each at Chennai and Vizag). It has recently started operations at its new CFS at Kochi. All its operational CFSs are strategically located near major container ports (JNPT, Chennai and Vizag, which collectively handle ~75% of India’s container traffic), giving it an unparalleled edge over other CFS operators.

Fig 8 – Details about CFS facilities

Location Capacity

(TEUs) Expansion

Expected (TEUs) Remarks

Mumbai (1 & 2) 3 300,000 60,000 Mild capacity addition expected, 150 owned trailers

Chennai 90,000 Scouting for land for expansion

Vizag 50,000 Minor capacity expansion possible

Kochi 50,000 Not yet fully operational

Source: Company

CFS the key contributor to profits so far

JNPT CFS handles more than 65% of the company’s total TEUs. During Q2FY13 volumes handled at the JNPT CFS declined while the ‘dwell time’ at the CFS also came down. Mumbai CFS’ EBIDTA margin declined due to reduced dwell time, in line with one of its larger peers, and is expected to be subdued in FY13. Volumes are expected to pick up in H2FY13 when its Punjab Conware facility would be restored. This would help it provide various value-added services which would, in turn, help improve realisations. We expect EXIM trade to pick up during FY14, adding to volumes in its CFS business at JNPT. Also, planned expansion at JNPT terminal will augur well for CFS operators in the region. We expect volumes at the JNPT CFS to record a 6% CAGR over FY12-15 while revenues are expected to come at a 4% CAGR.

Fig 9 – Volume & realisation trend at JNPT CFS

0

60,000

120,000

180,000

240,000

300,000

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

e

FY14

e

FY15

e

6,000.0

7,000.0

8,000.0

9,000.0

10,000.0

11,000.0

Volume Revenue/TEU (RHS)

(TEUs) (`/TEUs)

Source: Company, Anand Rathi Research

Since its second-largest CFS, at Chennai, has been operating at peak capacity, the company plans to purchase land to raise capacity there. In the past few quarters heavy congestion at Chennai port has led to a slight decline in volumes at GD’s CFS facility. We expect volumes to recover in FY14 and GD to benefit from the same. The company might also look to acquire additional land at Chennai to increase its capacity.

Fig 7 – CFS locations Location Distance from port

Navi Mumbai 15 km from JNPT

Vizag 10 km from Vizag port

15 km of Chennai port Chennai

15 km from Ennore port

Source: Company

17 January 2013 Gateway Distriparks – Integrated play on logistics; initiating with Buy

Anand Rathi Research 29

In Aug’05 GD started operating at Vizag (capacity: 50,000 TEUs) and hiked tariffs during Q1FY13. In volumes (and revenues, realizations as well) this CFS has grown steadily over FY09-FY12 increasing from `3,570/TEU to `5,430/TEU. It operated at peak capacity during FY12, which is expected to continue through FY13. Realisations have risen considerably due to the great degree of congestion, and we expect this to continue. We expect Chennai and Vizag to register 22% CAGR in revenues over FY12-15 due to the high utilization levels, price hikes and longer ‘dwell time’ stemming from congestion.

Also, GD has recently commissioned a CFS at Vallarpadam, near the fast-growing Kochi port, in a 60:40 joint venture with Chakiat Agencies. The Cochin Port Trust has leased 2.58 hectares at Vallarpadam for 30 years. Operations at Kochi have recently commenced and management expects capacity utilization to touch ~80% in the first year itself. Initial capacity at Kochi would be 50,000 TEUs, which the company plans to expand, and towards which it has already acquired land. We expect Kochi terminal to benefit from lesser competition and locational advantage of the facility.

Revenue from CFS to record 9.6% CAGR

The CFS business, which contributed ~38% of revenue and ~79% of profits in FY12, is expected to grow them at 9.6% and 9% CAGR respectively. Cash flows from this segment are expected to be strong, given the commissioning of capacity and no major capex in the pipeline.

Fig 12 – Revenue and growth in CFS

0

900

1,800

2,700

3,600

4,500

FY07

FY08

FY09

FY10

FY11

FY12

FY13

e

FY14

e

FY15

e

-20

-8

4

16

28

40

Revenue Growth (RHS)

(`m) (%)

Source: Company, Anand Rathi Research

Fig 13 – Net profit and margins in CFS

-100

200

500

800

1,100

1,400

FY07

FY08

FY09

FY10

FY11

FY12

FY13

e

FY14

e

FY15

e 25

33

41

49

57

Net profit Margin (RHS)

(`m) (%)

Source: Company, Anand Rathi Research

Fig 10 – TEUs at various CFS

0

80,000

160,000

240,000

320,000

400,000

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

e

FY14

e

FY15

e

Mumbai Chennai Vizag

(TEU)

Source: Company, Anand Rathi Research

Fig 11 – Realisation trend at various CFS

0

3,500

7,000

10,500

14,000FY

06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

e

FY14

e

FY15

e

Mumbai Chennai Vizag

(`/TEU)

Source: Company, Anand Rathi Research

17 January 2013 Gateway Distriparks – Integrated play on logistics; initiating with Buy

Anand Rathi Research 30

Rail business to normalize in FY14 Leading private operator in container rail freight

After the state-run Container Corp. of India, GD is the largest, private, operator in rail freight in India, operating through subsidiary Gateway Rail Freight (GRF). Infrastructure comprises 21 rakes, three operational ICDs (Garhi, Ludhiana and Kalamboli), more than 700 wagons and 1,500 containers.

Fig 14 – Rail business infrastructure Rakes 21

Garhi

Kalamboli

LudhianaICDS / Rail Terminals

Faridabad

Wagons +700

Containers +1,500

Source: Company

At present, all operational ICDs have combined capacity of ~0.2m TEUs, which is expected to go up to ~0.3m by FY13 on the commencement of the Faridabad ICD. Further, the company is planning to have ICDs/rail terminals at other locations across the country.

In addition to running container trains through its own ICDs, GRF uses the container rail terminals (CRT) of the Indian Railways for container loading and unloading. At present, it has 21 rakes and plans to add six to eight rakes in the next two years. GRF now makes 5-6 trips per rake per month. It runs scheduled container trains on five routes as mentioned in fig 15.

Fig 16 – ICD wise capacity Location Train Services Capacity (TEUs) per year Area (acres)

Garhi Services to JNPT, Mundhra, Pipavav; Double stack services to Mundhra and Pipavav, Reefer Services to Kalamboli

120,000 90

Kalamboli Sanand, Jodhpur 75,000 17

Ludhiana Mundhra, JNPT, Pipavav 144,000 57

Faridabad Rail Work in Progress. Expected to scale up capacity to 120,000 by FY14.

50,000 66

Source: Company

Rise in haulage charges to hit profitability in FY13

IR recently increased container-rail-freight charges, to be implemented in two phases (Dec’12 and Feb’13). It has divided the present 20-ton category into two: up to 10 tons and 10-20 tons. It expects to improve viability of rail-freight movement up to 10-ton capacity. Haulage rates for 20-foot-equivalent containers are expected to increase ~31% for containers weighing between 10 and 20 tons, and 16% for containers weighing above that. At present, GD obtains ~15% of its revenue from the 0 to 20-ton category.

GD expects to pass on ~75-80% of the increase in charges to its end-customers. This would have an impact of ~`90m a year on its rail segment EBIDTA.

Fig 15 – Major routes for GD Garhi (NCR) - Kalamboli (Navi Mumbai) - Garhi

Garhi/Ludhiana - JNPT/Mundra - Garhi/Ludhiana

Orissa - NCR/Punjab

Rajasthan - JNPT/Mundra

Surat - Kolkatta/Orissa

Rajasthan - Kolkatta/ Orissa

Source: Company

17 January 2013 Gateway Distriparks – Integrated play on logistics; initiating with Buy

Anand Rathi Research 31

Fig 17 – Rail haulage rates Distance (km) (JNPT- NCR)

Effective date 0-10 tonnes 10-20 tonnes 20-26 tonnes >26 tonnes

Empty container

Empty flat wagons

1351 - 1400 Jan-11 14,672 14,672 18,914 21,196 9,537 8,804

1351 - 1400 1-Dec-12 13,371 17,898 20,514 22,931 11,634 10,739

1351 - 1400 1-Feb-13 14,334 19,188 21,992 24,584 12,472 11,513

1-Dec-12 -9 22 8 8 22 22

1-Feb-13 7 7 7 7 7 7Haulage rate hike (%)

Overall hike -2 31 16 16 31 31

Source: Indian Railway

Sharper focus on EXIM

GD is one of the few private railway operators focused on the high-margin EXIM segment (accounts for ~85% of GD’s turnover). It has successfully managed to turn around its rail-freight business from a loss-making segment in FY11 to a profitable one. GRF brought in ~55% to GD’s FY12 consolidated revenue. Volume growth in this business in 1HFY13 was subdued owing to the general slowdown in trade. We expect trade to pick up during FY14 on account of the improving global economic scenario which would benefit GD’s rail freight business.

The company has started double-stack operations on the Garhi-Mundra and Garhi-Pipavav routes from Oct’11. At present, the proportion of double-stack operations to total operations is less than 5% and is expected to increase in future. The company also plans to set up rail-linked terminal ICDs at Jaipur, Ahmadabad and Nagpur, a domestic rail-linked terminal at Chennai and a bonded rail-linked warehouse at Mundra.

We expect margins in the segment to improve post FY13, following deeper penetration, new routes and pass through of increase in rail haulage charges. Supported by these factors, over FY12-15 we expect GRF to register CAGR of 18.4% in revenue and 21.1% in EBITDA.

GD’s rail freight business will also benefit from the Dedicated freight corridors which are being established by the Indian Railways and the company will be in a strong position to take advantage of the same.

Fig 18 – Volume and volume growth

0

70,000

140,000

210,000

280,000

350,000

FY09

FY10

FY11

FY12

FY13

e

FY14

e

FY15

e

0

20

40

60

80

100

Volume Growth (RHS)

(TEUs) (%)

Source: Company, Anand Rathi Research

Fig 19 – Revenue and growth in its rail freight segment

0

2,000

4,000

6,000

8,000

FY09

FY10

FY11

FY12

FY13

e

FY14

e

FY15

e

-25.00

35.00

95.00

155.00

215.00

Revenue Growth (RHS)

(`m) (%)

Source: Company, Anand Rathi Research

17 January 2013 Gateway Distriparks – Integrated play on logistics; initiating with Buy

Anand Rathi Research 32

Cold chain business to grow rapidly Organized pan-India operator in the segment

In Nov’06, to enter the cold-chain logistics business, GD acquired 50.1% stake in Snowman Frozen Foods (SFF). Subsequently, it raised its stake to 53%. At present, SFF has +19 cold storages in major Indian cities, including Mumbai, Bangalore, Chennai and Hyderabad. Its storage capacity includes 28,000 freezer pallets, 622 chilled pallets and cold warehousing space of over 117,000 sq. ft. Besides, its portfolio includes more than 100 refrigerated trucks, handling over 20,000 tons of goods. GD plans to increase the number of pallets from present levels to 46,000 by end-FY13 and further to 0.1m pallets by FY15.

Marquee clientele & huge opportunity