implementation strategy for the system of environmental

TRANSCRIPT

2

Implementation Strategy for the System of Environmental-

Economic Accounting (SEEA)

United Nations Committee of Experts on Environmental-Economic Accounting (UNCEEA) UNCEEA Taskforce on the Implementation Strategy for the System of Environmental-Economic Accounting (SEEA)

3

Implementation Strategy for the System of Environmental-

Economic Accounting (SEEA) Contents

I. Introduction ................................................................................................................... 5

II. Assessment of the current level of SEEA implementation and planned

programs/activities.................................................................................................................. 6

II.a. SEEA implementation by countries................................................................................ 6

II.b. Relevant activities by international organisations......................................................... 7

• Natural Capital Accounting (formerly known as: WAVES)............................................. 7

• The Green Growth Strategy ........................................................................................... 7

• Green Economy Initiative............................................................................................... 8

• Beyond GDP ................................................................................................................... 8

• EU Strategy for Environmental Accounting ................................................................... 9

III. Proposed strategy for global implementation of the SEEA Central Framework ........... 9

III.a. Objective, approach and scope...................................................................................... 9

III.b. Flexible and modular approach ................................................................................... 10

IV. Activities for the Implementation of the SEEA Central Framework ............................ 12

IV.a. Training and technical cooperation ............................................................................. 12

IV.b. Manuals and training material..................................................................................... 13

IV.c. Cooperation with research community ....................................................................... 13

IV.d. Advocacy ...................................................................................................................... 13

V. Mechanism for coordination, monitoring progress and facilitating cooperation ....... 14

V.a. Information structure for coordination, monitoring and reporting ............................ 14

V.b. Mechanism for coordination, monitoring progress and facilitating cooperation ....... 15

VI. Strategy for funding ..................................................................................................... 16

Literature............................................................................................................................... 17

Annex A: Diagnostic tool to perform a self-assessment ....................................................... 18

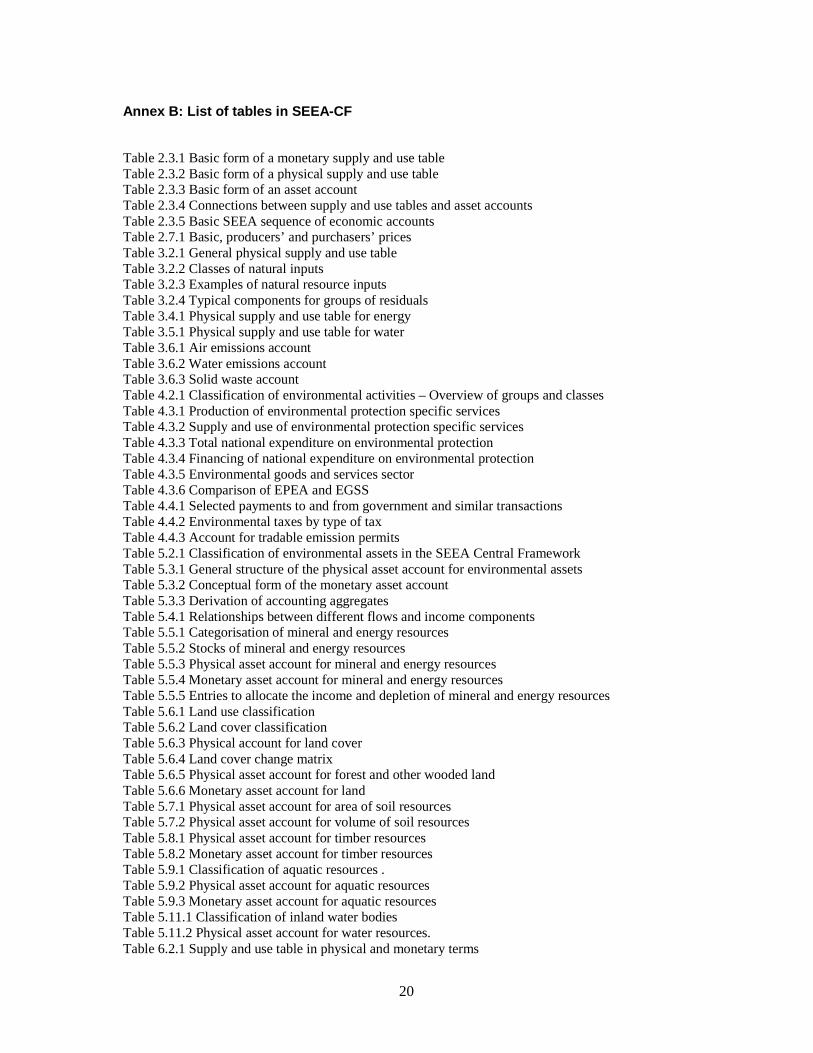

Annex B: List of tables SEEA-CF ............................................................................................. 20

Annex C: An overview of the curent level of SEEA implementation in countries ................. 21

Annex D: Communication Strategy for the Implementation of the System of Environmental

Economic Accounting Central Framework (SEEA-CF).......................................................... 212

4

5

I. Introduction

1 In February 2012, at its forty-third session, the Statistical Commission adopted the 2012 System of Environmental-Economic Accounting (SEEA) Central Framework as the initial version of the international standard for environmental-economic accounts.

2 The Commission recognized that the SEEA implementation should be considered as a long-term program, to be implemented flexibly and incrementally, giving full consideration to national circumstances and requirements; And urged the Committee of Experts on Environmental-Economic Accounting (UNCEEA) to continue its work on the development of a detailed strategy for the global and regional implementation program for SEEA, in particular a road map for countries to follow, and encouraged Member States and regional or international organizations to initiate compilation activities in accordance with the Central Framework.

3 Also at the forty-third session the Commission

- Recognized that the detailed implementation strategy for SEEA should reflect the need for regional and sub-regional coordination, given the different levels of statistical development, and emphasize an advocacy strategy to engage users, especially those in policy formulation and analysis; and

- Requested international agencies and other donors to make resources available for technical assistance for the implementation of SEEA and the development of basic economic and environmental statistics in countries, in particular in developing countries.

4 Later that year, at the Rio+20 – United Nations Conference on Sustainable Development (June 2012) – the need to strengthen the monitoring of sustainable development, through improved data collection and the establishment of indicators, has been stressed.

5 According to the requests of the Statistical Commission (2012) the proposed strategy for the implementation of the SEEA Central Framework takes into account, as point of departure, the different levels of development of environmental statistics and economic statistics in various countries and regions. It is recognized that the implementation strategy should reflect the need for regional and sub-regional coordination, given the different levels of statistical development between countries. An assessment of the current level of SEEA implementation (including planned programs and activities) by Member States and international agencies is presented in section II.

6 Like other international statistical standards, it is expected that SEEA Central Framework will be implemented incrementally taking into account policy demands, national statistical office and other line ministries resources and requirements. To support this, the SEEA Central Framework accommodates a flexible and modular approach to implementation within national statistical systems which can be aligned with the particular policy context, data availability and statistical capacity of countries. The proposed implementation strategy of the SEEA Central Framework is described in Section III, showing how the Committee envisages flexible and incremental implementation through specific instruments and modalities.

6

7 Environmental accounts do not necessarily require a large amount of new data. The amount of new data depends on the availability of source statistics and also on the scope of the initial start of a particular country. The SEEA provides the organizational structure to bring all the available data together to improve understanding of their interrelationships and verify consistency. This facilitates the identification of data gaps and overlaps as well as the improvement the quality of the data. Complete implementation of SEEA clearly is a long term objective. The current implementation strategy will only provide guidance for the short and medium term.

8 Section IV describes specific activities planned by the UNCEEA for the implementation of the SEEA Central Framework. An explicit communication strategy is described in Annex D.

9 Proposed mechanisms for coordination, monitoring progress and for facilitating cooperation and a funding strategy are outlined in section V and section VI, respectively.

II. Assessment of the current level of SEEA implementation and planned programs/activities

II.a. SEEA implementation by countries

10 An increasing number of countries are compiling or planning to compile environmental accounts (see Annex C for an overview). These countries cover both developed and developing regions. Examples of countries with extensive EA programmes can be found across all continents e.g. Australia; Canada; China; Colombia; Italy; Mexico; Norway; Philippines; South Africa; Sweden.

11 An important recent development in the EU context has been that in July 2011 the European Parliament and Council adopted the first EU Regulation (and law) on environmental accounts which requires all Members States to compile annual data for three modules in a first stage (first data delivery at the End of 2013). The legal base contains three modules that countries within the European Economic Area need to conform to. These modules are Air emission accounts, Environmental related taxes by industry and Economy-wide material flow accounts. An extension of the legal base is being discussed within the European Commission and with the statistical offices. The SEEA-CF provides overall guidance in the development of the modules for EU-regulation.

12 The overall picture that emerges from assessments is that whereas in the EU the focus has been to a large extent on physical flow accounts and monetary accounts (environmental expenditure, environmental taxes, subsidies and EGSS), outside the EU there seems to be a greater interest in natural resource (asset) accounting. This difference in compilation practices may be due to differences in environment related policy perspectives. The policy demand in developing countries may be understood from the need for resource management of their endowments of natural resources and specific security issues related to water and energy. This developing country perspective differs from the developed world, where flow issues of expenditures, economic instruments, resource efficiency and environmental degradation related to economic production and consumption take prominence and preference. Also data availability issues may be a

7

relevant factor in this context. Emission accounts require energy statistics and emission inventories which may be less readily available in developing countries.

13 These experiences underline the need for a flexible and modular approach towards implementation.

II.b. Relevant activities by international organisations

14 Several initiatives have been taken by international agencies to encourage countries to compile statistics in economic and environmental statistics. Many more initiatives are likely to be undertaken in the context of the follow up to the “Future we Want” (UNCSD 2012) adopted in Rio. By way of examples, below some initiatives that hinge on the SEEA as the multi-purpose statistical system to answer policy demand are described below. The SEEA Central Framework implementation strategy should harness on the synergies of these initiatives, which may respond to particular policy demands.

• Natural Capital Accounting (formerly known as: WAVES)

15 To support countries with the move to Natural Capital Accounting, the World Bank initiated a partnership called WAVES - Wealth Accounting and the Valuation of Ecosystem Services − which includes several UN agencies (e.g. UNEP, UNDP, UNCEEA, etc.), national governments, NGOs, academic and other institutions. WAVES works as a global partnership. Some are developing countries – Botswana, Colombia, Costa Rica, Madagascar, Philippines – working to establish environmental accounts in practice. Developed countries like Australia, Canada, Japan, Norway, France, and the United Kingdom that have extensive experience in the compilation of the accounts and are already exploring environmental accounting and have valuable lessons to share are also part of the partnership. Others include UN agencies – UNEP, UNDP, UN Statistical Commission – that will help implement environmental accounting in countries and review scientific evidence and methods.

16 SEEA-CF will serve as the reference point in implementing environmental accounting. At the same time the WAVES project will contribute to the further development of ecosystem accounting.

17 Over the next four years, it is hoped that this partnership will nurture a vibrant community that shares experience and expertise and raises awareness of the importance of environmental accounting for sustainable development.

• The Green Growth Strategy

18 The Green Growth Strategy, delivered at the 2011 OECD Ministerial Council Meeting, marks the start of OECD’s longer term agenda to support national and international efforts to achieve green growth. The Strategy aims to help countries foster economic growth and development while ensuring that natural assets continue to provide the resources and environmental services on which our well-being relies. It develops a flexible policy framework that can be tailored to different national circumstances and

8

stages of development. An important part of the Green Growth strategy is a measurement framework which provides a set of indicators for Green Growth.

19 Following the delivery of the Strategy in May 2011, green growth is being integrated into OECD analytical work to provide concrete, targeted advice as member and partner countries advance with the design and implementation of green growth strategies. The OECD is building green growth considerations into national policy surveillance, such as Economic Surveys, Environmental Performance Reviews, Investment Policy Reviews and Innovation Reviews. These will cover OECD, emerging and other economies.

20 The OECD advocates that indicators for green growth should, where possible, be directly obtained from the SEEA framework. Future work will focus on the selection of a small set of core indicators. The OECD is working closely with other organizations, such as the United Nations Environment Program (UNEP), the United Nations Statistics Division, other UN agencies, the World Bank, EUROSTAT, and the European Environment Agency, to develop a common set of core indicators for green growth.

• Green Economy Initiative

21 The United Nations Environment Program (UNEP) launched the Green Economy Initiative in late 2008. This initiative consists of several components whose collective overall objective is to provide the analysis and policy support for investing in green sectors and in greening environmental unfriendly sectors.

22 The Green Economy Report ‘Towards a Green Economy: Pathways to Sustainable Development and Poverty Eradication’ (2011) is compiled by UNEP’s Green Economy Initiative in collaboration with economists and experts worldwide. It demonstrates that the greening of economies is not generally a drag on growth but rather a new engine of growth; that it is a net generator of decent jobs, and that it is also a vital strategy for the elimination of persistent poverty. The report also seeks to motivate policy makers to create the enabling conditions for increased investments in a transition to a green economy.

23 Beyond UNEP, the Green Economy Initiative is one of the nine UN-wide Joint Crisis Initiatives (JCI) launched by the UN System's Chief Executives Board in early 2009. In this context, the Initiative includes a wide range of research activities and capacity building events from more than 20 UN agencies including the Bretton Woods Institutions, as well as an Issue Management Group (IMG) on Green Economy, launched in Washington, DC, in March 2010.

• Beyond GDP

24 The high level conference "Beyond GDP" in November 2007 at which Commissioner Dimas concluded that "we [The European Commission] will also need to speed up and improve the development of integrated accounting in the social and environmental spheres" increased the interest for SEEA. The idea of Beyond GDP is to increase the use of indicators related to environment and social aspects in relation to indicators such as the Gross Domestic Product (GDP) "...to address global challenges

9

such as climate change, poverty, resource depletion and health" (Beyond GDP web-site). In 2009 the European Commission issued a communication GDP and beyond Measuring progress in a changing world describing the need to complement economic indicators such as the GDP with social and environmental indicators. According to this communication, the European Commission plans to extend the existing data collection further, ready for policy analysis by 2013.

• EU Strategy for Environmental Accounting

25 In June 2006, the European Council adopted "an ambitious and comprehensive renewed EU Strategy for Sustainable Development". It was then stated that: "For better understanding of interlinkages between the three dimensions of SD [Sustainable Development], the core system of national income accounting could be extended by inter alia integrating stock and flow concepts and non-market work and be further elaborated by satellite accounts, e.g., environmental expenditures, material flows and taking into consideration international best practices." The strategy has been revised in 2009. As part of the strategy, a legal base on Environmental Accounting was established.

III. Proposed strategy for global implementation of the SEEA Central Framework

26 In response to the above demands the statistical community has developed the SEEA Central Framework. A first version of the SEEA was presented at the World Conference on Sustainable Development in 1993. Building on increasing experience by countries and international organisations, the SEEA was gradually developed, and eventually adopted as an international statistical standard. The implementation of the SEEA over the next years will ensure the statistical infrastructure on the environment and its relationship with the economy in countries.

III.a. Objective, approach and scope

27 The proposed global implementation strategy has a twofold objective:

- to assist countries in the adoption of the SEEA Central Framework as the measurement framework for environmental-economic accounts and supporting statistics, and

- to establish incrementally the technical capacity for regular reporting on a minimum set of environmental-economic accounts with the appropriate scope, detail and quality.

28 A key element of the proposed SEEA implementation strategy is to allow for a flexible and modular approach. This entails that rather than proposing a ‘one size fits all approach’, it takes as its point of departure the recognition that countries differ in terms of their specific environmental-economic policy issues and their level of statistical

10

development. Accordingly, countries may prioritize the accounts they want to implement over the short to medium-term based on the most pressing policy demands.

29 This approach recognizes that countries do not have to implement all accounts at the same time. Few, if any country, compiles all possible accounts. It is up to individual countries to decide upon scope and coverage of their envisaged environmental accounting programs. In addition, it should be up to countries to develop a specific time frame for implementation. A flexible and modular approach for individual countries is compatible to efforts by international organizations (such as Eurostat and the OECD) that wish to collect data from SEEA for regional or global monitoring efforts

30 In situations of partial statistics and pressing policy needs, indicators could be developed first, however effort should be made to ensure that such indicators are consistent with accounting rules and principles.

31 The implementation strategy covers both developed and developing countries. The focus of the implementation strategy lies on the assistance of countries with ‘poor’ statistical systems on the one hand and on the other hand, have shown commitment for SEEA activities through their own initial funding.

III.b. Flexible and modular approach

32 The flexible and modular approach for SEEA implementation is operationalized by a number of phases. The first phase of the implementation strategy consists of the establishment of a national institutional mechanism that will drive the implementation strategy. This includes an initial screening to identify whether there is commitment and potential to sustain a program over time. Minimum institutional support is needed before a successful implementation can start.

33 The second phase of the implementation strategy consists of a self-assessment phase. Figure 1 in Annex A provides a possible diagnostic tool designed to assist countries in performing such a self-assessment concerning their SEEA implementation. Using this tool countries identify which accounts have to be implemented to serve certain policy needs and what basic data sources are needed to compile these accounts.

34 In several ways this self-assessment accommodates a flexible and modular approach towards implementation:

35 First, implementation should be as much as possible a demand driven process whereby those accounts are developed first that address the most pressing policy needs. For example, countries that aim at reducing the air emissions to meet climate change commitments, may decide to develop air emission accounts on a priority basis, while countries affected by resource scarcity may wish to consider developing natural resource accounts. The diagnostic tool may help countries to prioritize during the self-assessment phase which accounts should be developed first, using a top-down approach.

36 Second, environmental accounting is in essence about integrating various data sources such as environment statistics, energy statistics and economic statistics. As evidenced by environmental accounting programs in several developed countries, when

11

relevant data sources are readily available, environmental accounts can be compiled with relatively little effort. However, when basic data sources required for compilation of specific types of accounts are either nonexistent or of low quality, investments may need to be made first in developing these basic data sources. For example, when the policy interest is reducing the air emissions to meet climate change commitments, but an emission inventory is not available, an outcome of the self-assessment could be that the implementation strategy should focus on making a specific investment in development of such a data source first (either by establishing a survey program or developing administrative data). An important aspect is therefore to perform a quality assessment of the data sources required for the compilation of the prioritized types of accounts.

37 The third phase is the data quality assessment. When the accounts for implementation have been prioritized, the next step is an assessment of the basic data sources that are needed for the compilation of these accounts. Such an assessment can be performed using the data quality assessment framework (DQAF) which was originally developed by the IMF, or country equivalent1. The DQAF was developed as an assessment methodology that aims to provide structure and a common language for the assessment of data quality. The DQAF comprehensively covers the various quality aspects of data collection, processing, and dissemination. The Framework is organized in a cascading structure that progresses from the abstract/general to the more concrete/specific details. It covers five dimensions of quality, namely integrity, methodological soundness, accuracy and reliability, serviceability and accessibility, and a set of prerequisites for the assessment of data quality. The coverage of these dimensions recognizes that data quality encompasses characteristics related to the institution or system behind the production of the data as well as characteristics of the individual data product.

38 The fourth phase. Following the outcome of the self-assessment and the data quality assessment a strategic development plan for environmental accounting can be drafted, which contains at minimum a prioritization of types of accounts and an assessment of the status of the required data sources. The development plan should also be explicit about improvement activities related to the source data. Subsequently, capacity building efforts could be tailor-made to these country specific circumstances and needs. At national level, strategic planning refers to formulation of a strategic vision based on a detailed national assessment of existing capacity and needs, followed by the formulation of a national implementation program.

39 The international community could develop common diagnostic tools to aid countries to undertake self-assessments and common guidelines for the drafting of strategic visions and national implementation plans for the various modules. These diagnostic tools would typically cover the evaluation of the existing institutional arrangements for managing integrated statistics like a) legislative, operation and process management frameworks, b) coordination and governance arrangements like advisory committees, service level agreements and c) human and financial resources. Moreover, tools would include the assessment of the existing statistical production processes which cover the components of: a) the use of agreed standards and scientific statistical methods,

1 http://dsbb.imf.org/pages/dqrs/dqaf.aspx

12

data editing, metadata and data warehousing and data quality frameworks, b) business registers and frames, c) use of survey and administrative data sources and d) dissemination and communication practices, e) planning about improvement activities related to the source data.

40 In order to guide the prioritization process, countries may use a predefined set of tables. A set of tables as initial scope may help to identify options for countries to choose from. SEEA-CF provides a long list of tables / accounts (see Annex B). Under the guidance of UNCEEA, a core set of tables and accounts may be developed from which indicators could be derived as part of the implementation strategy. A core set of tables may in the future also serve as a reference point for regular reporting on a minimum set of environmental-economic accounts.

IV Activities for the Implementation of the SEEA Central Framework

41 The SEEA Central Framework is expected to be implemented with a flexible and modular approach taking into account national statistical office resources and requirements. The most important issues of the implementation process are institutional capacity building and the development of data sources. This section provides an overview of the activities by the Partnership Group (see section V.b.) to facilitate and stimulate the (global and national) implementation process: training and technical cooperation, the development of training materials, cooperation with the research community, and advocacy.

IV.a. Training and technical cooperation

42 Training and technical cooperation programs for countries requesting assistance put a further emphasis on direct country involvement. The training and technical cooperation programs will emphasize the integration of statistical capacity building in national planning and programming cycles to secure resources for sustainable statistical programs for environmental economic accounting and basic environmental statistics..

43 Training and technical cooperation is dependent on the availability of people who can teach. The number of experts on environmental accounting available for this type of training needs to increase. The training of people who can become teachers is one of the challenges that lies ahead. Training and technical cooperation by institutional capacity building like the WAVES project and by other twinning projects for transferring know-how has proven to be a successful way of acting and is recommended, but need more resources (see chapter VI on funding).

44 The training programs will be implemented mainly through organizing training seminars, workshops and meetings. Actively pursuing these initiatives at a (sub) regional level should enable regional organizations and their member countries to share experiences (peer-to-peer) in developing sustainable economic statistics programs.

13

IV.b. Manuals and training material

45 The implementation of the Framework could also benefit from the activities undertaken in different countries to implement the 2008 SNA. To support the implementation of the 2008 SNA there will be a series of new and revised manuals and handbooks that also could be of good support for the implementation of the Framework.

46 The European development of environmental account2 has involved networking and cooperation between countries to agree on measurement practices. Similar regional cooperation networks would be valuable to identify and to develop local training material.

47 There is already a lot of training material available. In the last years several workshops on environmental accounting have already been organized (for example by Eurostat etc.). The challenge will be to put it all together and make it available is a consistent way. Also certain IT-tools that have been developed to compile specific accounts maybe helpful in this regard (for example the IT-tool that is currently being developed by Eurostat to compile energy flow accounts).

IV.c. Cooperation with research community

48 The users of environmental accounts data can often be found in the research community. In countries that do not produce accounts, researchers and consultancies often are the ones to provide similar analyses on an ad-hoc basis. A close cooperation with the research community can therefore be a means to recruit potential teachers, increase the number of users and implement the environmental accounts ideas in a broader context. The scheduled handbooks SEEA2 on ecosystem accounts and SEEA3 applications and extensions will be realized in close operation with universities and research institutes.

49 Cooperation can be established in different ways. Applying for research grants in cooperation between researchers and statistical offices and joining forces in common projects is one. It has proven a good way to increase the understanding for the principles of the statistical system and the advantages of using statistical classifications in analyses related to environmental socio-economic issues.

IV.d. Advocacy

50 As an integral component of the implementation strategy, advocacy aims to support an ongoing dialogue among statistical producers, the various levels of government, business sector, the academic community, and the general public about user needs for official statistics and the progress in meeting those needs. This recurrent communication can be established through targeted workshops, conferences, press releases and promotional materials that highlight the benefits of good quality official statistics in general, and environmental-economic accounts in particular. These regular engagements between the producers of statistical outputs and the providers of basic data

2 http://epp.eurostat.ec.europa.eu/portal/page/portal/environmental_accounts/introduction

14

on one hand and the users of environmental-economic accounts on the other will reinforce a better funded and more effective environmental-economic accounts program that provides reliable data for an evidence-based economic policy formulation. The focus of the advocacy should be on stimulating demand and engaging with users.

51 Advocacy should be achieved through the development of a communication strategy promoting the Central Framework of the SEEA. This strategy will be described in a separate document. The objective of the Communication strategy is to effect information sharing with all stakeholders (target groups). The communication strategy makes it clear that through statistical integration of basic statistics with macroeconomic accounts, a coherent set of statistics and indicators can be derived for evidence-based policy formulation for green growth/green economy and sustainable development at regional, national and international levels. Therefore, promoting good quality environmental-economic accounts statistics is essential in establishing a sound sustainable policy within a coherent medium-term budgetary framework.

52 An explicit communication strategy will become an integral component of technical assistance and training programs undertaken by the UNCEEA member organizations, Eurostat, IMF, OECD, UNSD and World Bank. Supporting materials and guidelines are to be developed for this purpose by the UNCEEA in cooperation with PARIS213.

V. Mechanism for coordination, monitoring progress and facilitating cooperation

V.a. Information structure for coordination, monitoring and reporting

53 The principle of coordination, monitoring and reporting ensures that the roles of international and regional organizations, other donors and recipient countries are clear and their actions are complementary, effective and efficient. Coordination comprises the timing and sequencing of events. Monitoring comprises assessing the efficiency of technical assistance programs, evaluating lessons learned, and using resources effectively. Reporting communicates progress and operational issues to interested stakeholders. Better coordination, monitoring and reporting collectively help meet national and regional goals, as well as providing a means to evaluate and to assess the progress of the implementation of SEEA. Monitoring, reporting and evaluating should also be used to identify risks to the implementation process so that timely interventions can be made to keep plans on track.

54 The UNCEEA proposes to apply the proven program information structure to facilitate the coordination, monitoring and reporting on the SEEA Central Framework implementation in this multi-stakeholder environment. This proposed information system, as was successfully used in the Implementation Strategy of 2008 SNA, is built on the structure of the statistical production process and an established data quality assessment framework for evaluating statistical project outcomes. Together, the two

3 PARIS21 focuses its efforts on encouraging and assisting all low-income and lower middle income countries to design, implement, and monitor National Strategies for the Development of Statistics (NSDS) and to have nationally owned and produced data for all Millennium Development Goals (MDG) indicators.

15

dimensions will allow the UNCEEA to develop a coherent information system for programming, monitoring and reporting. The statistical process dimension will be used to program and monitor the implementation and the Data Quality Assessment Framework (DQAF) dimension will be used to evaluate and report on outcomes.

55 As described for the implementation of SNA 20084, the SEEA Central Framework implementation strategy uses standards for the statistical production process to support programming and monitoring, and the DQAF to support program reporting. Both are vital for overall coordination at regional and country level and, the UNCEEA will work with the regional commissions to seek the adoption of an information system. A commonly accepted system is highly desirable for effective project programming, monitoring and reporting, especially in the SEEA Central Framework context with multiple compiler stakeholders within a country and often multiple funding agencies within and across countries.

V.b. Mechanism for coordination, monitoring progress and facilitating cooperation

56 In the multi-stakeholder environment for the SEEA Central Framework implementation strategy, a mechanism is needed in order to coordinate, monitor and report progress at (sub) regional and international level. The purpose of this mechanism would be to share information on the development and the execution of the SEEA Central Framework implementation strategy.

57 UNCEEA proposes to install a Partnership Group, consisting of the partners active in this field (see section II). This partnership will be responsible for facilitating and stimulating the implementation of SEEA Central Framework. A trust fund for the implementation will be created by a separate entity. The role for UNCEEA will be the overall global coordinating body. In particular, it is proposed that this group will consist of representatives of (existing5) regional coordinating mechanisms and will advise the UNCEEA on maintaining and managing a coherent program of work to implement SEEA Central Framework. If these proposals are accepted, the UNCEEA would further reflect on the modalities of the mechanisms.

58 The new project information model described in this document (section V.a) will be used to facilitate cooperation among agencies in delivering technical assistance and training through more timely and effective communication on work programs and program developments. Agencies will characterize their program activities in terms of the statistical process and in terms of DQAF indicators to evaluate and report the activities in the recipient countries. This coherent information system will assist in providing timely notice of possible synergies and impending duplications and gaps in work programs. For the review of national and regional SEEA Central Framework implementation plans, regional coordination mechanisms may wish to establish such advisory groups to share

4 Implementation Strategy for the System of National Accounts, 2008; Prepared by the Intersecretariat Working Group on National Accounts; Statistical Commission Background document; Fortieth session, 24 - 27 February 2009 5 In the case of Africa UN Econ Commission for Africa as an example.

16

information on the development and the execution of the SEEA Central Framework implementation strategy on the regional level.

59 In addition to implementing a standard program documentation structure across its member agencies, the UNCEEA proposes to support an extension of the web-based knowledge base6 on economic statistics and macroeconomic standards sources from and hyperlinked to other organizations as relevant to ensure a single point access to normative documents, compilation guidance and country experiences. This instrument, developed by UNSD as part of the Implementation Strategy for the SNA 2008, will help ensure that UNCEEA organizations are delivering a consistent message on the implementation of the SEEA Central Framework and related macroeconomic standards.

60 The Partnership Group will further assist in promoting practical instruments of implementation across the (sub) regions such as handbooks, compilation guides, textbooks, advocacy modules, software tools for the various components of the statistical production process and the use of SDMX as a common data transmission system.

VI. Strategy for funding

61 The strategy for funding arrangements for the SEEA implementation can only be based on a cooperative and partnership model. It should build largely on the existing resources and comparative advantages of all stakeholders and partners, as described in section IV (preferably resulting in a trust fund created by the partnership). Various sources of funding are viable:

- countries should include funding needs for 2012 SEEA Central Framework implementation in their national plans and actively seek additional sources of funding for their plans;

- international agencies providing technical assistance and financial support and other donors are requested (by the Statistical Commission) to make resources available for technical assistance for the implementation of SEEA Central Framework and the development of basic economic and environmental statistics in countries, in particular in developing countries; and

- all agencies involved should build on synergies with the other similar programs such as work of PARIS21, provision of training and technical assistance.

62 The limited resources (of the trust fund) should be focused on assistance of countries that have shown commitment for SEEA activities through their own initial funding to assist them in achieving some success, rather than being used mostly for “seed” money where the chance of continued activity is limited.

6 http://unstats.un.org/unsd/EconStatKB

17

Literature

1) Statistical Commission (2012), Report on the forty-third session (28 February – 2 March, 2012), Economic and Social Council, Official Records 2012, Supplement No. 4., E/2012/24, E/CN.3/2012/34

2) European Commission et al. (2012) System of Environmental-Economic Accounting Central Framework, White cover publication, pre-edited text subject to official editing, available on http://unstats.un.org/unsd/envaccounting/White_cover.pdf

3) UNCSD, The Future We Want, outcome document.; available at: http://www.uncsd2012.org/content/documents/774futurewewant_english.pdf

4) UNSD (2012) Initial Thoughts on a Global Strategy for Implementation of the SEEA Central Framework, Paper prepared by UNSD (for discussion), Seventh Meeting of the UN Committee of Experts on Environmental-Economic Accounting, Rio de Janeiro, 11-13 June 2012 ESA/STAT/AC.255, UNCEEA/7/13

5) Edens et al. (2011) Initiating a SEEA Implementation Program – A First Investigation of Possibilities, Paper prepared by Statistics Netherlands (for discussion), Sixth Meeting of the UN Committee of Experts on Environmental-Economic Accounting, New York, 15-17 June 2011, ESA/STAT/AC.238, UNCEEA/6/19

6) WAVES (Wealth Accounting and the Valuation of Ecosystem Services). 2012. Moving Beyond GDP: How to factor natural capital into economic decision making. Available online at www.wavespartnership.org/waves/sites/waves/files/images/Moving_Beyond_GDP.pdf

7) UNEP, 2011, Towards a Green Economy: Pathways to Sustainable Development and Poverty Eradication, Available online at www.unep.org/greeneconomy

18

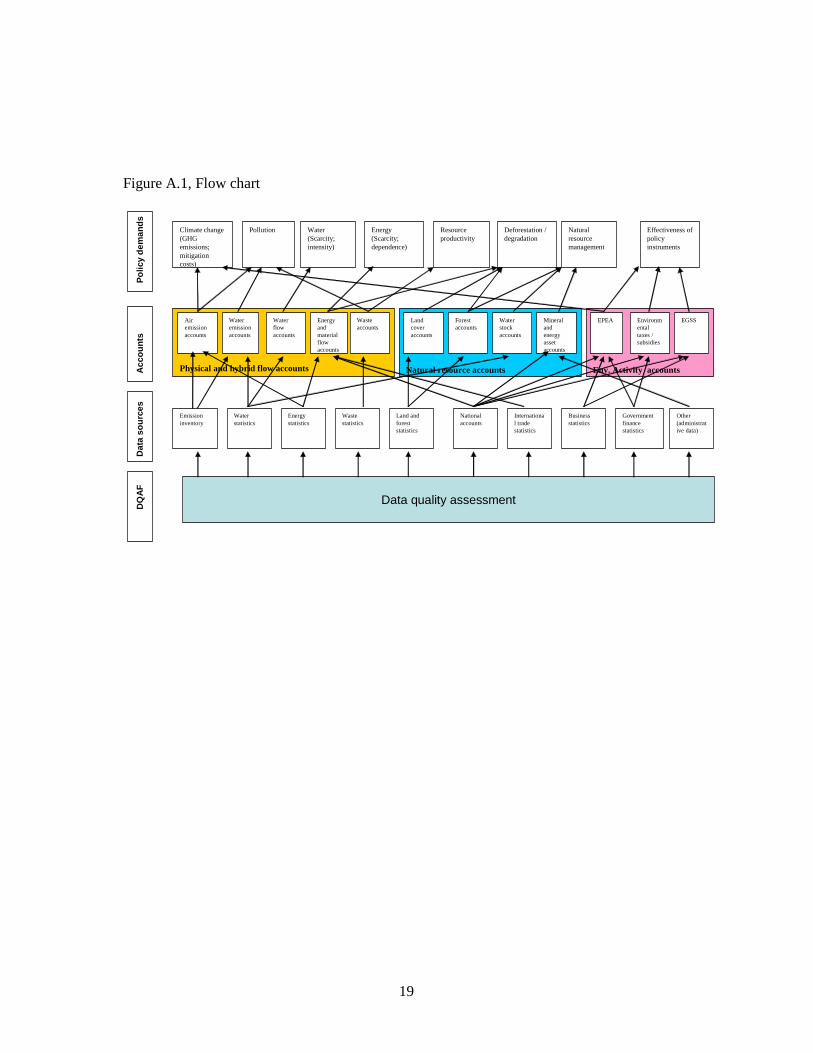

Annex A: Diagnostic tool to perform a self-assessment

A.1 The flexible and modular approach for SEEA implementation is operationalized by a number of phases. The first step of the implementation strategy consists of a self-assessment phase. Figure A.1 provides an example of a diagnostic tool designed to assist countries in performing such a self-assessment concerning their SEEA implementation.

A.2 The diagnostic tool consists of multiple layers.

A.3 At the top-level, in the first layer, examples of key policy issues are shown which form the main elements of these policy frameworks. For instance, assessments of the natural capital base (and its depletion) are important to sustainable development, whilst resource productivity is a key element of green growth. Other examples are policy issues such as pollution, climate change, water scarcity, etc.

A.4 The 2nd layer depicts a list of the various types of environmental accounts (i.e modules) as described in SEEA-CF and indicates through the connecting arrows which accounts can be used to address the various types of policy issues. Not shown in this figure are the overarching policy frameworks which are usually connected to the objectives of environmental accounting, namely sustainable development and green economy / green growth. The measurement framework needed for these two general policy issues are often assessed through selected indicator sets, that can in part be derived from the SEEA-CF.

A.5 The 3rd layer indicates the main data sources that are commonly required to compile specific types of environmental accounts. There may be differences between countries in terms of the specific data sources used, but the diagram is meant to provide a general overview of basic data requirement.

A.6 The 4th layer shows the data quality assessments that can be done on these required data sources. The data quality assessment framework (DQAF) covers five dimensions of quality (integrity, methodological soundness, accuracy and reliability, serviceability and accessibility) and a set of prerequisites for the assessment of data quality. The coverage of these dimensions recognizes that data quality encompasses characteristics related to the institution or system behind the production of the data as well as characteristics of the individual data product.

19

Data quality assessment

Emissioninventory

Energy statistics

Other(administrative data)

Water statistics

Land and foreststatistics

Waste statistics

National accounts

International tradestatistics

Governmentfinancestatistics

Business statistics

Physical and hybrid flow accounts

Air emissionaccounts

Water emissionaccounts

Water flowaccounts

Energy and materialflowaccounts

Waste accounts

Natural resource accounts

Land cover accounts

Water stock accounts

Mineraland energyassetaccounts

Forestaccounts

Env. Activity accounts

Environmentaltaxes / subsidies

EPEA EGSS

Water (Scarcity; intensity)

Climate change(GHG emissions; mitigationcosts)

Energy (Scarcity; dependence)

Deforestation / degradation

Pollution Resource productivity

Effectiveness of policy instruments

Naturalresourcemanagement

Po

licy

dem

and

sA

cco

un

tsD

QA

FD

ata

sou

rces

Figure A.1, Flow chart

20

Annex B: List of tables in SEEA-CF

Table 2.3.1 Basic form of a monetary supply and use table Table 2.3.2 Basic form of a physical supply and use table Table 2.3.3 Basic form of an asset account Table 2.3.4 Connections between supply and use tables and asset accounts Table 2.3.5 Basic SEEA sequence of economic accounts Table 2.7.1 Basic, producers’ and purchasers’ prices Table 3.2.1 General physical supply and use table Table 3.2.2 Classes of natural inputs Table 3.2.3 Examples of natural resource inputs Table 3.2.4 Typical components for groups of residuals Table 3.4.1 Physical supply and use table for energy Table 3.5.1 Physical supply and use table for water Table 3.6.1 Air emissions account Table 3.6.2 Water emissions account Table 3.6.3 Solid waste account Table 4.2.1 Classification of environmental activities – Overview of groups and classes Table 4.3.1 Production of environmental protection specific services Table 4.3.2 Supply and use of environmental protection specific services Table 4.3.3 Total national expenditure on environmental protection Table 4.3.4 Financing of national expenditure on environmental protection Table 4.3.5 Environmental goods and services sector Table 4.3.6 Comparison of EPEA and EGSS Table 4.4.1 Selected payments to and from government and similar transactions Table 4.4.2 Environmental taxes by type of tax Table 4.4.3 Account for tradable emission permits Table 5.2.1 Classification of environmental assets in the SEEA Central Framework Table 5.3.1 General structure of the physical asset account for environmental assets Table 5.3.2 Conceptual form of the monetary asset account Table 5.3.3 Derivation of accounting aggregates Table 5.4.1 Relationships between different flows and income components Table 5.5.1 Categorisation of mineral and energy resources Table 5.5.2 Stocks of mineral and energy resources Table 5.5.3 Physical asset account for mineral and energy resources Table 5.5.4 Monetary asset account for mineral and energy resources Table 5.5.5 Entries to allocate the income and depletion of mineral and energy resources Table 5.6.1 Land use classification Table 5.6.2 Land cover classification Table 5.6.3 Physical account for land cover Table 5.6.4 Land cover change matrix Table 5.6.5 Physical asset account for forest and other wooded land Table 5.6.6 Monetary asset account for land Table 5.7.1 Physical asset account for area of soil resources Table 5.7.2 Physical asset account for volume of soil resources Table 5.8.1 Physical asset account for timber resources Table 5.8.2 Monetary asset account for timber resources Table 5.9.1 Classification of aquatic resources . Table 5.9.2 Physical asset account for aquatic resources Table 5.9.3 Monetary asset account for aquatic resources Table 5.11.1 Classification of inland water bodies Table 5.11.2 Physical asset account for water resources. Table 6.2.1 Supply and use table in physical and monetary terms

21

Table 6.2.2 Connections between supply and use tables and asset accounts Table 6.2.3 SEEA Central Framework sequence of economic accounts Table 6.5.1 Possible structure and typical content for combined presentations Table 6.5.2 Combined presentation for energy data Table 6.5.3 Combined presentation for water data Table 6.5.4 Combined presentation for forest products Table 6.5.5 Combined presentation for air emissions

Annex C: An overview of the current level of SEEA implementation in countries

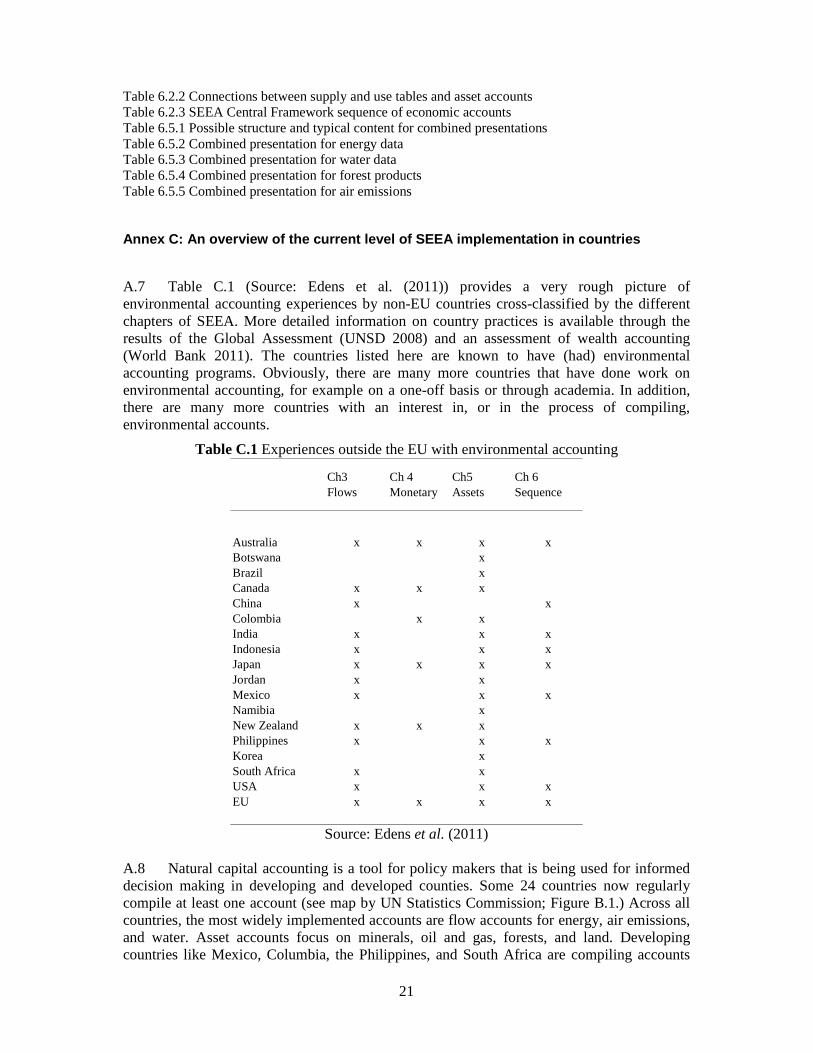

A.7 Table C.1 (Source: Edens et al. (2011)) provides a very rough picture of environmental accounting experiences by non-EU countries cross-classified by the different chapters of SEEA. More detailed information on country practices is available through the results of the Global Assessment (UNSD 2008) and an assessment of wealth accounting (World Bank 2011). The countries listed here are known to have (had) environmental accounting programs. Obviously, there are many more countries that have done work on environmental accounting, for example on a one-off basis or through academia. In addition, there are many more countries with an interest in, or in the process of compiling, environmental accounts.

Table C.1 Experiences outside the EU with environmental accounting

Ch3 Ch 4 Ch5 Ch 6Flows Monetary Assets Sequence

Australia x x x xBotswana xBrazil xCanada x x xChina x xColombia x xIndia x x xIndonesia x x xJapan x x x xJordan x xMexico x x xNamibia xNew Zealand x x xPhilippines x x xKorea xSouth Africa x xUSA x x xEU x x x x

Source: Edens et al. (2011)

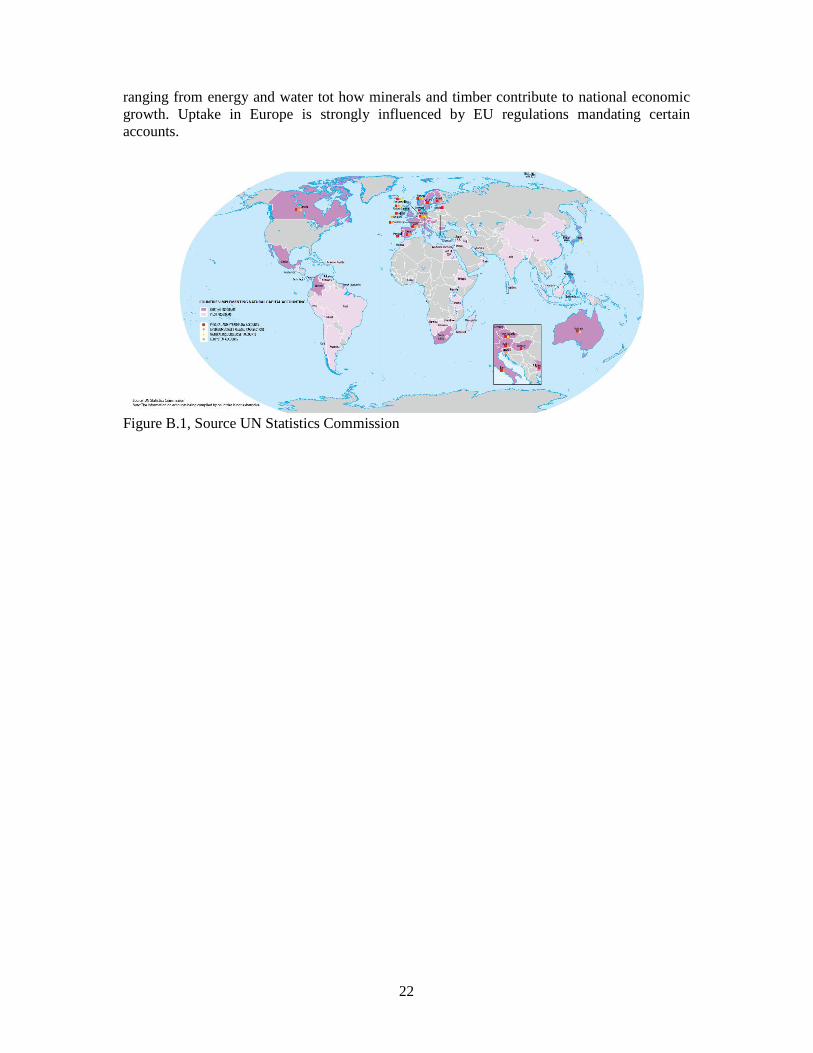

A.8 Natural capital accounting is a tool for policy makers that is being used for informed decision making in developing and developed counties. Some 24 countries now regularly compile at least one account (see map by UN Statistics Commission; Figure B.1.) Across all countries, the most widely implemented accounts are flow accounts for energy, air emissions, and water. Asset accounts focus on minerals, oil and gas, forests, and land. Developing countries like Mexico, Columbia, the Philippines, and South Africa are compiling accounts

22

ranging from energy and water tot how minerals and timber contribute to national economic growth. Uptake in Europe is strongly influenced by EU regulations mandating certain accounts.

Figure B.1, Source UN Statistics Commission

23

Annex D: Communication Strategy for the Implementation of the System of Environmental Economic Accounting Central Framework (SEEA-CF)

1. Introduction

The objective of the Communication strategy for the Implementation of the System of Environmental-Economic Accounts (SEEA) is to effect information sharing with all stakeholders (target groups). The formal Communication Plan will allow UNCEEA to optimize the effectiveness of the Implementation Strategy. The Communication Strategy contains the following:

• Communications Purpose and Objectives

• Communication Principles

• Target groups identification, Communication, Media and Timing

• Communication mechanisms and Activities

The Communication Strategy is leading in the development of a detailed Communication Plan. In the Communication Plan an estimate of the costs of communication should be made and an adequate budget should be allocated.

2. Communication Purpose and Objectives

The purpose of the Communication Plan is to contribute to the successful (global, regional and national) implementation of the SEEA-CF in as many countries as possible with the right communication delivered to the right audiences at the right time. The communication should stress the importance of the SEEA-CF as a multi-purpose information system from which various indicators responding to specific demands on the environment and its relationship with the economy can be derived. The objectives of the Communication Plan are:

• Enable Leadership Advocacy: provide information to enable leaders to be advocates of the Implementation of SEEA.

• Build Synergy of UNCEEA: Provide communication that increases the effectiveness of UNCEEA in coordinating and facilitating the implementation of SEEA.

• Prepare the Statistical Community: create awareness and understanding of the impacts and implications of the Implementation of SEEA.

• Enroll the Statistical Community: Generate interest in and create buy-in of the Implementation of SEEA. Inform the Statistical Community about progress so that the feel involved, ask for feedback and acknowledge their contributions.

• Manage expectations of Leaders and Statistical Community

24

3. Communication Principles

Communications should be developed and delivered according to the following guidelines/principles:

• Tailor communications to discrete audiences according to needs analysis.

• Design information using fact-based information to deliver openly, regularly and in a straight forward manner.

• Ensure that all communications contain consistent core messages.

• Continually reinforce the reasons for implementation SEEA.

• Consistently ask for feedback and lessons learnt.

• Evaluate communication to ensure messages are understood and to assess use of different media..

• Share knowledge with the international community on implementation issues in knowledge systems of UNSD and others.

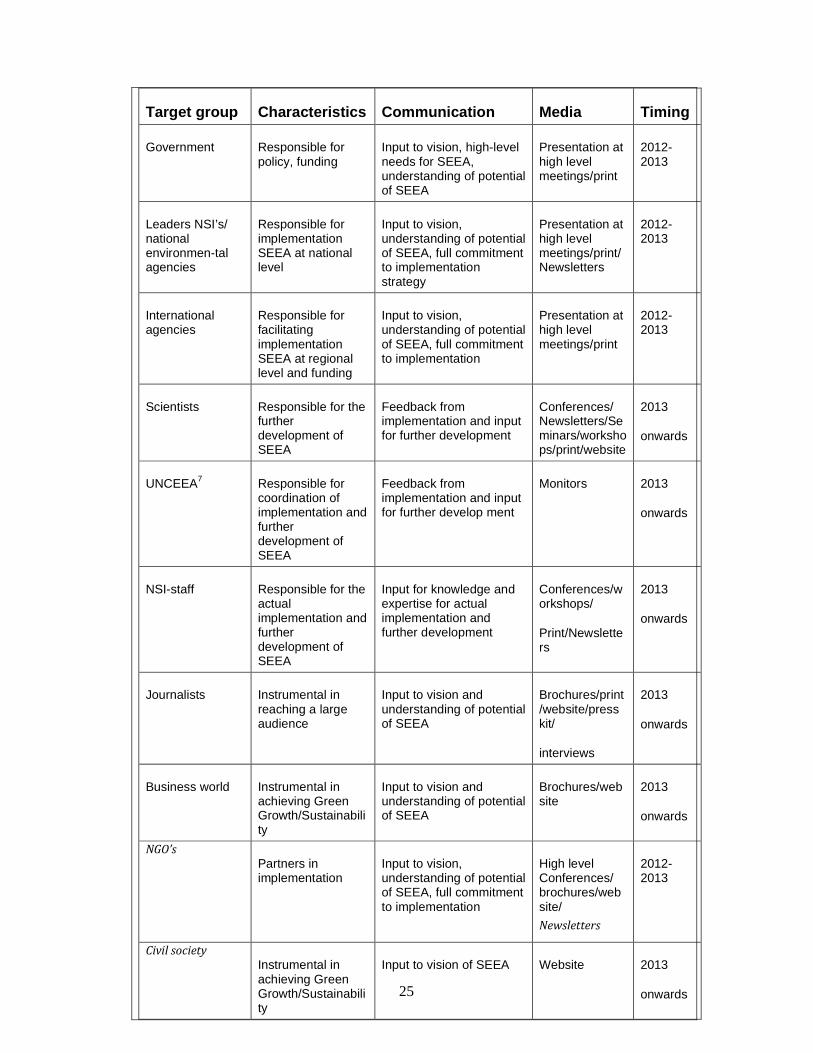

4. Target groups identification, Communication, Media and Timing

As the SEEA Central Framework has been accepted as the international standard it is of paramount importance to implement a suitable communication strategy which facilitates the successful implementation of the System of Environmental Economic Accounting Central Framework in the global and national statistical systems. This communication strategy must assure a communication with all stakeholders/target groups involved. For every target group an objective has to be set according to the commitment desired for that group. Depending on the present knowledge and commitment of each target group a dedicated strategy should be developed leading the target groups to the desired level of commitment varying from 1st contact via awareness to understanding, engagement, involvement and finally to full commitment. The following target groups are identified: Government, Leaders of NSI’s and national environmental agencies, International agencies, Scientists, UNCEEA, NSI-staff, Journalists, Business world NGO’s and Civil Society. For each target group the desired level of commitment should be identified. The communication plan should be based upon an analysis of the present and the desired level of commitment of the different target groups.

25

Target group Characteristics Communication Media Timing

Government Responsible for policy, funding

Input to vision, high-level needs for SEEA, understanding of potential of SEEA

Presentation at high level meetings/print

2012-2013

Leaders NSI’s/ national environmen-tal agencies

Responsible for implementation SEEA at national level

Input to vision, understanding of potential of SEEA, full commitment to implementation strategy

Presentation at high level meetings/print/Newsletters

2012-2013

International agencies

Responsible for facilitating implementation SEEA at regional level and funding

Input to vision, understanding of potential of SEEA, full commitment to implementation

Presentation at high level meetings/print

2012-2013

Scientists Responsible for the further development of SEEA

Feedback from implementation and input for further development

Conferences/ Newsletters/Seminars/workshops/print/website

2013

onwards

UNCEEA7 Responsible for coordination of implementation and further development of SEEA

Feedback from implementation and input for further develop ment

Monitors 2013

onwards

NSI-staff Responsible for the actual implementation and further development of SEEA

Input for knowledge and expertise for actual implementation and further development

Conferences/workshops/

Print/Newsletters

2013

onwards

Journalists Instrumental in reaching a large audience

Input to vision and understanding of potential of SEEA

Brochures/print/website/press kit/

interviews

2013

onwards

Business world Instrumental in achieving Green Growth/Sustainability

Input to vision and understanding of potential of SEEA

Brochures/website

2013

onwards

NGO’s

Partners in implementation

Input to vision, understanding of potential of SEEA, full commitment to implementation

High level Conferences/ brochures/website/

Newsletters

2012-2013

Civil society

Instrumental in achieving Green Growth/Sustainability

Input to vision of SEEA Website 2013

onwards

26

In the short term the communication efforts should be targeted at Government leaders, NSI-leaders, International agencies and NGO’s to get full commitment, funding and to get the implementation process started.

5. Communications mechanisms and Activities

The following communication mechanisms and activities will be used: • Workshops

Workshops may be very effective to train NSI-staff in the ins and outs of SEEA-CF and to produce a practical way forward in the formulating of a modular approach in implementing SEEA-CF for specific countries. Workshops may also be organized to settle specific scientific issues in the further development of SEEA-CF.

• Conferences/Seminars

Conferences and (mini)seminars are to be organized to reach senior leaders of NSI’s, governmental bodies and NGO’s to provide opportunities for these target groups to learn more about the vision behind SEEA-CF and the (policy) potentials of SEEA-CF and to achieve further commitment. These conferences and seminars may be very effective when organized as side events to formal meetings of the target groups. In this way the more important constituencies may be reached and committed. For the further development of SEEA-CF scientific conferences should be organized to present and discuss results of further research and to share feedback from experiences with the implementation by the scientific community of researchers and statistical experts. Promotion of SEEA-CF in existing forums like conferences of EAERE and IARIW should also take place.

• Newsletters/Flyers/Brochures

Attractive newsletters, flyers and brochures in print and in digital form should be widely distributed regularly within the target groups to keep them informed on all on going activities (and especially successes) and to keep awareness and commitment at a high level.

• Websites

Reaching a large audience (all target groups) and to facilitate communication and discussion within specific interested communities (for example the groups of environmental economists, methodologists and national accountants) requires that documents as well as other communication materials are posted on time and distributed as appropriate and that discussion groups are facilitated. This may be well served by a dedicated website (the UNSD site on the revision of the SEEA-CF) with a general and open character and sub sites with a specific and (more) closed character. For all sites moderators should be appointed to assure consistency in official communications. Communities may make use of social media to accommodate discussions and sharing of views. The potential of Environmental and economic accounting may be illustrated in short video’s on YouTube (for example video’s on Carbon footprints, decoupling and best practices). These video’s may also be used in presentations.

• Presentations

27

To assure consistency in presenting the vision behind SEEA-CF and the (policy) potentials of SEEA-CF for all the different target groups it advisable to use one presentation which has to updated on a regular basis. This presentation should make use of modern presentation techniques.

• Interviews

To assure consistency in communication to different media a communication set on SEEA-CF should be available for all interested parties to be interviewed by the media. The communication set should contain a press kit and fact sheets and should be updated at a regular basis.

• Monitors

The monitors of the progress of all the implementation projects of SEEA-CF provide useful information for the further development of SEEA-CF and successes and lesson learnt for other countries in implementation projects.