implementation of the cap reform in various countries: variations and...

TRANSCRIPT

Slide number 1

Implementation of the CAP reform in various countries: variations and consequencesBeef Task Force, Dublin, August 24th, 2007Daniel Brüggemann, Dr. Claus Deblitz

German Agricultural SocietyFrankfurt

Institute of Farm EconomicsFederal Agricultural Research CentreBraunschweig

Brüggemann, August 2007 Slide number 2

Content

EU beef production

Common Agriculture Policy (CAP)– Overview– From a beef perspective– On farm level– The German case

Summary

Brüggemann, August 2007 Slide number 3

EU Beef Production

Brüggemann, August 2007 Slide number 4

Total cattle Inventory EU-251,000 head in 2005

2,69913,035

5,973

19,454

6,998

6,261

3,759 5,482

10,507

Source: ZMP Marktbilanz Vieh und Fleisch 2007

Comments: Data are basedon the year 2003 for:DK, GR, ES, FR, IE, IT, CY, HU, NL, AT, PT, SK, FI, GB

Total: 87,749

EU

–be

efpr

oduc

tion

Brüggemann, August 2007 Slide number 5

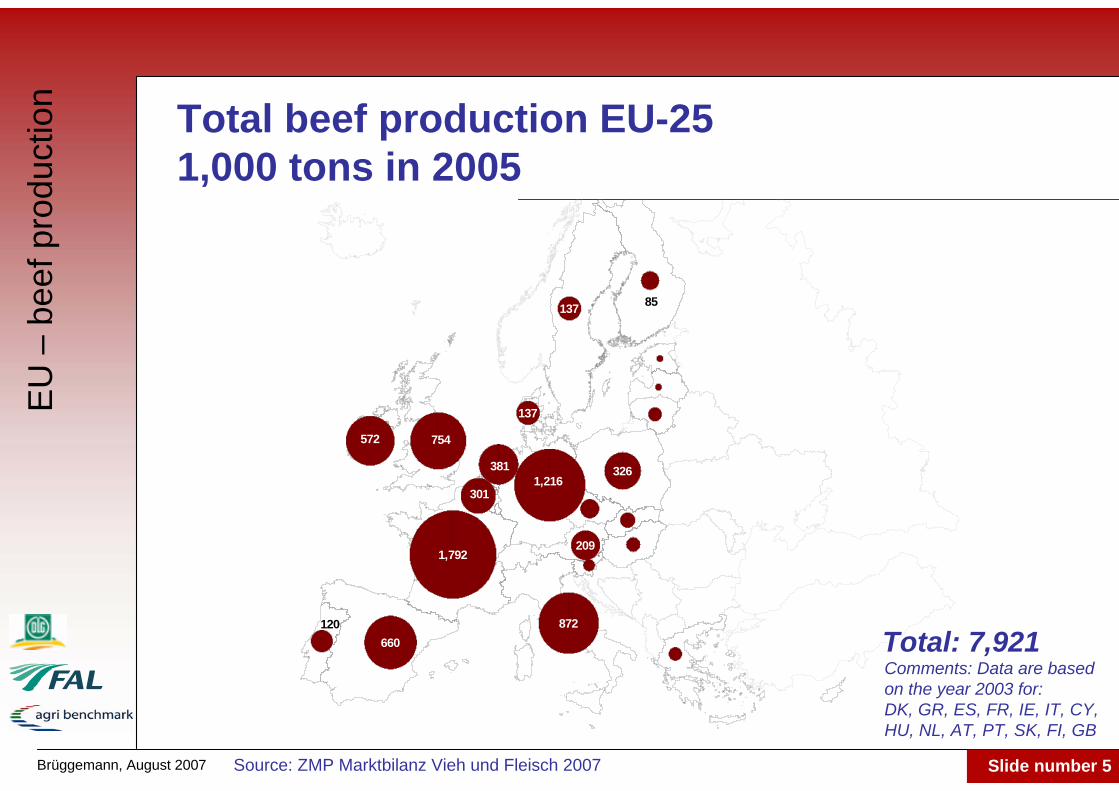

Total beef production EU-251,000 tons in 2005

209

3011,216

137

660

85

1,792

572

872

381 326

120

137

754

Source: ZMP Marktbilanz Vieh und Fleisch 2007

Comments: Data are basedon the year 2003 for:DK, GR, ES, FR, IE, IT, CY, HU, NL, AT, PT, SK, FI, GB

Total: 7,921

EU

–be

efpr

oduc

tion

Brüggemann, August 2007 Slide number 6

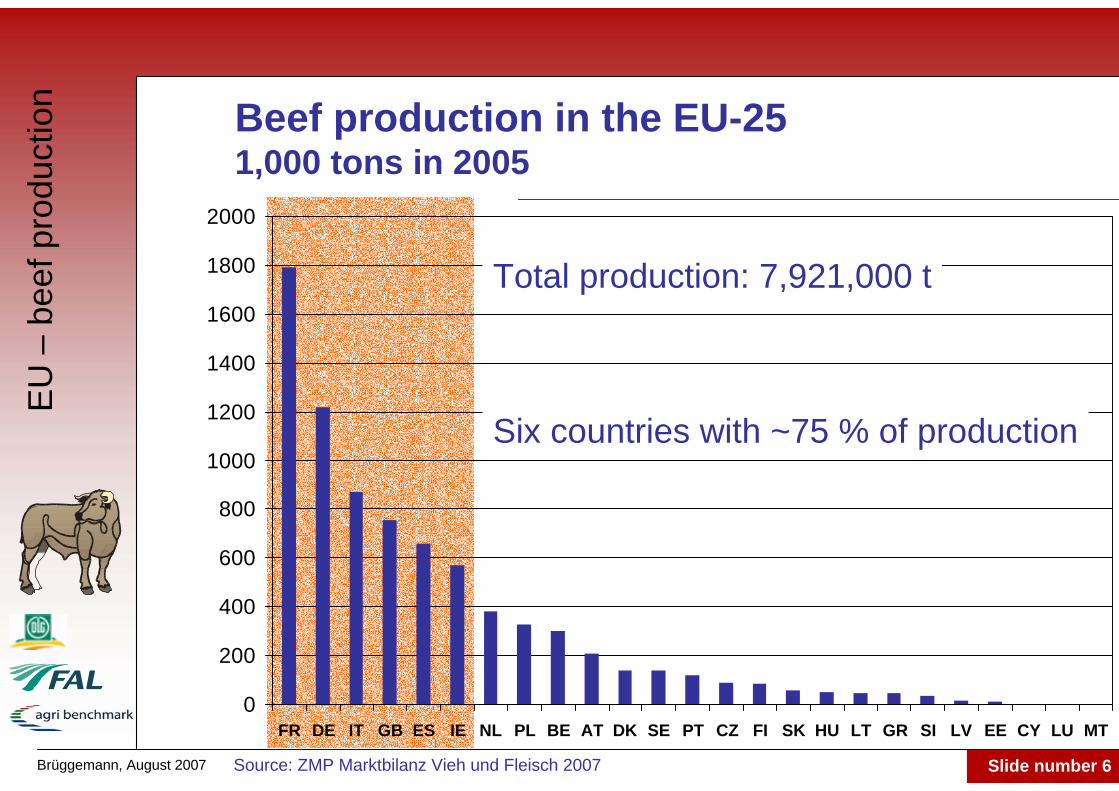

Beef production in the EU-251,000 tons in 2005

0

200

400

600

800

1000

1200

1400

1600

1800

2000

FR DE IT GB ES IE NL PL BE AT DK SE PT CZ FI SK HU LT GR SI LV EE CY LU MT

Six countries with ~75 % of production

Total production: 7,921,000 t

Source: ZMP Marktbilanz Vieh und Fleisch 2007

EU

–be

efpr

oduc

tion

Brüggemann, August 2007 Slide number 7

0

500

1000

1500

2000

2500

3000

3500

4000

4500

FR ES GB IE DE IT BE PT AT SE GR NL CZ DK SI HU LU SK PL FI LT EE LV CY MT

Suckler Cows in the EU-25 1,000 Head in 2005

Six Countries with ~80 % of suckler cows

EU-15: 11,800,000NMS EU-25: 300,000 (appr.)

Source: ZMP Marktbilanz Vieh und Fleisch 2007

EU

–be

efpr

oduc

tion

Brüggemann, August 2007 Slide number 8

0%

10%

20%

30%

40%

50%

60%

70%E

S PT IE FR BE

GR LU GB

EU

SE SI

AT IT CZ

DK

DE

SK

HU NL FI EE LV LT PL

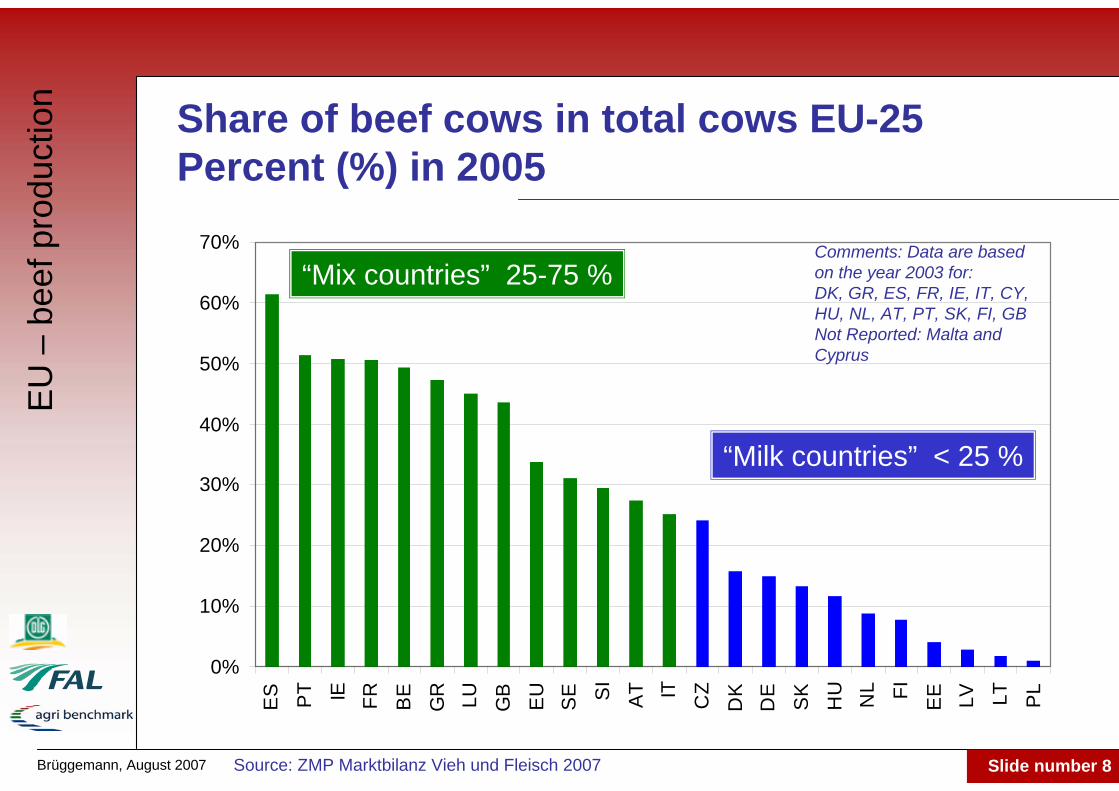

Share of beef cows in total cows EU-25 Percent (%) in 2005

“Milk countries” < 25 %

“Mix countries” 25-75 %

Source: ZMP Marktbilanz Vieh und Fleisch 2007

Comments: Data are basedon the year 2003 for:DK, GR, ES, FR, IE, IT, CY, HU, NL, AT, PT, SK, FI, GBNot Reported: Malta and Cyprus

EU

–be

efpr

oduc

tion

Brüggemann, August 2007 Slide number 9

CAPOverview

EU

-po

licy

Brüggemann, August 2007 Slide number 10

The evolution of the CAP

1960: Protectionism price policy

1984: Milk-Quota

1987: Set aside (facultative)

1992: McSharry Reform (Uruguay Round)

1999: Agenda 2000

2003: MTR – Luxembourg Agreement

2009: Health Check

2013: ???

EU

-po

licy

Brüggemann, August 2007 Slide number 11

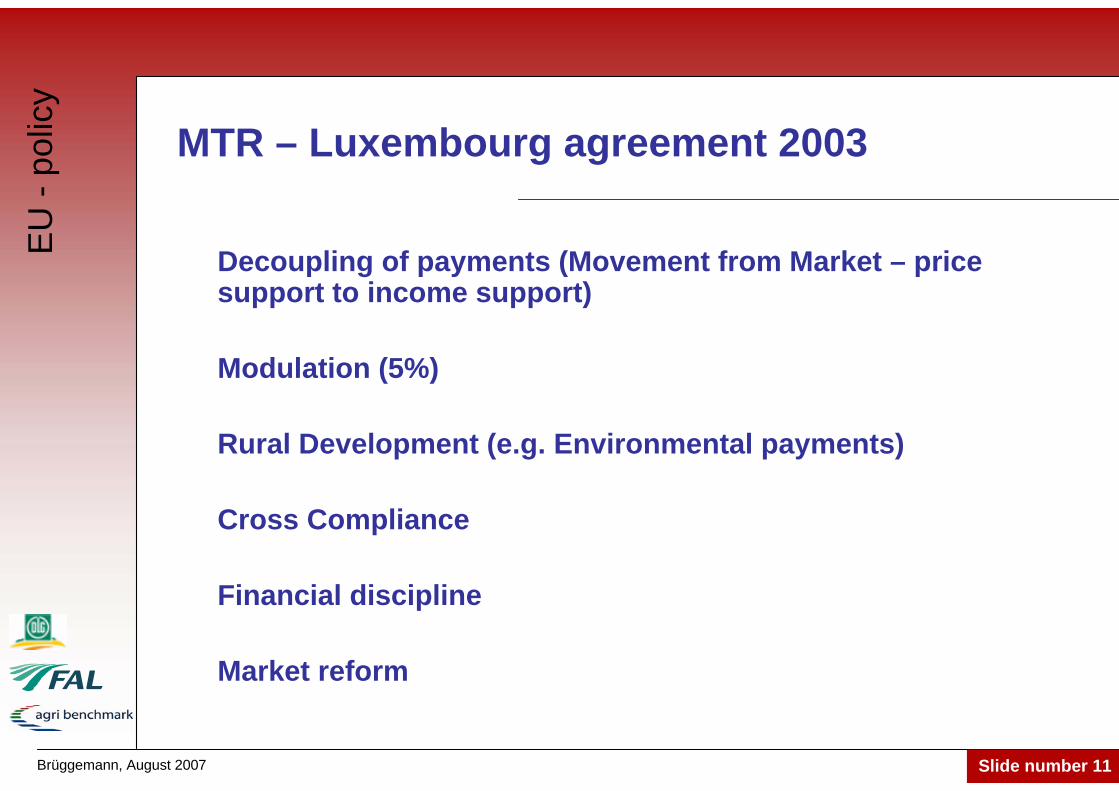

MTR – Luxembourg agreement 2003

Decoupling of payments (Movement from Market – pricesupport to income support)

Modulation (5%)

Rural Development (e.g. Environmental payments)

Cross Compliance

Financial discipline

Market reform

EU

-po

licy

Brüggemann, August 2007 Slide number 12

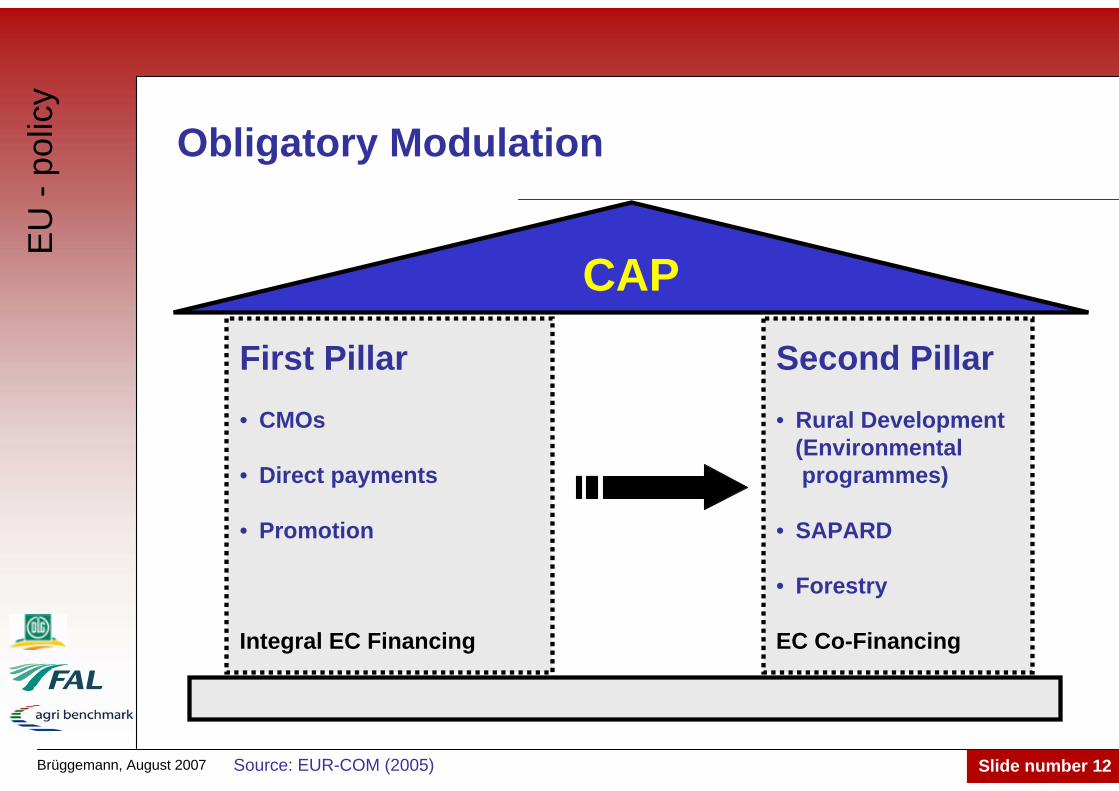

Obligatory Modulation

CAPFirst Pillar• CMOs

• Direct payments

• Promotion

Integral EC Financing

Second Pillar• Rural Development

(Environmentalprogrammes)

• SAPARD

• Forestry

EC Co-Financing

Source: EUR-COM (2005)

EU

-po

licy

Brüggemann, August 2007 Slide number 13

Decoupling Models

Historical model (SPS)

Regional model

Hybrid or combi model– Static– Dynamic

Partial coupling possible

Source: EU-COM (2006)

EU

-po

licy

Brüggemann, August 2007 Slide number 14

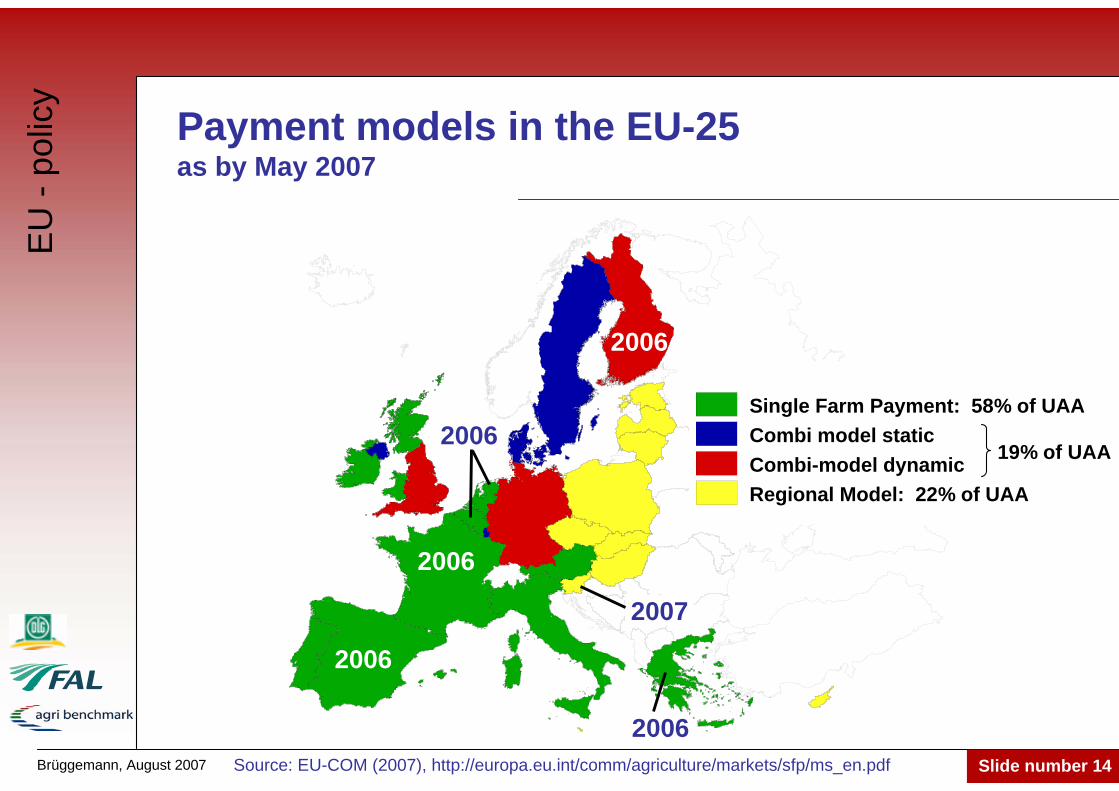

Payment models in the EU-25as by May 2007

Source: EU-COM (2007), http://europa.eu.int/comm/agriculture/markets/sfp/ms_en.pdf

EU

-po

licy

2006

2006

2006

2006

2006Single Farm Payment: 58% of UAA Combi model staticCombi-model dynamicRegional Model: 22% of UAA

19% of UAA

2007

Brüggemann, August 2007 Slide number 15

CAPBeef and cow-calf

Brüggemann, August 2007 Slide number 16

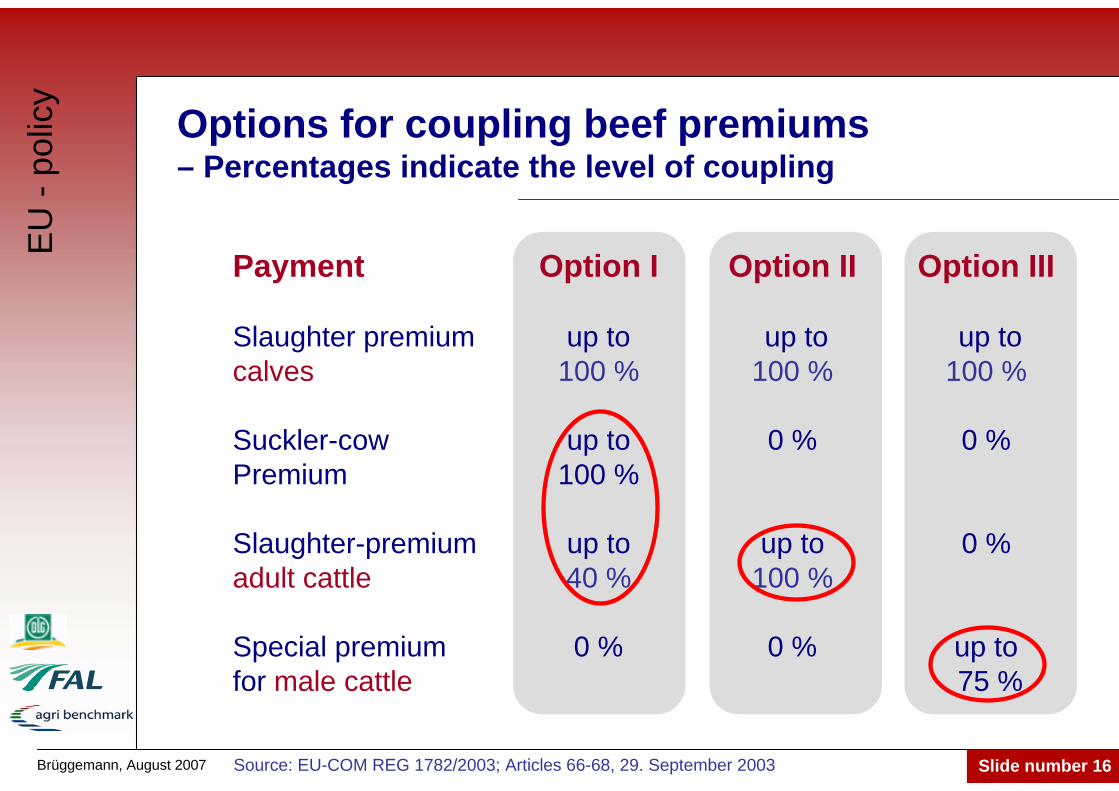

Options for coupling beef premiums– Percentages indicate the level of coupling

Payment Option I Option II Option III

Slaughter premium up to up to up tocalves 100 % 100 % 100 %

Suckler-cow up to 0 % 0 %Premium 100 %

Slaughter-premium up to up to 0 %adult cattle 40 % 100 %

Special premium 0 % 0 % up tofor male cattle 75 %

Source: EU-COM REG 1782/2003; Articles 66-68, 29. September 2003

EU

-po

licy

Brüggemann, August 2007 Slide number 17

Options for coupling beef premiums by country

EU

-po

licy

Total decoupling partly withmodification

I Coupling suckler-cowand slaughter premium

II Coupling slaughter premiums

III Coupling special male bovine premium

Source:http://ec.europa.eu/agriculture/markets/sfp/ms_en.pdf

Slaughter premium calves not coupled in: BE Zone Sud: Wallonia, DK, SI, FI, SE

Brüggemann, August 2007 Slide number 18

Coupled suckler cow premiums by country

EU

-po

licy

Suckler cow premium100 % coupled

Source:http://ec.europa.eu/agriculture/markets/sfp/ms_en.pdf

Brüggemann, August 2007 Slide number 19

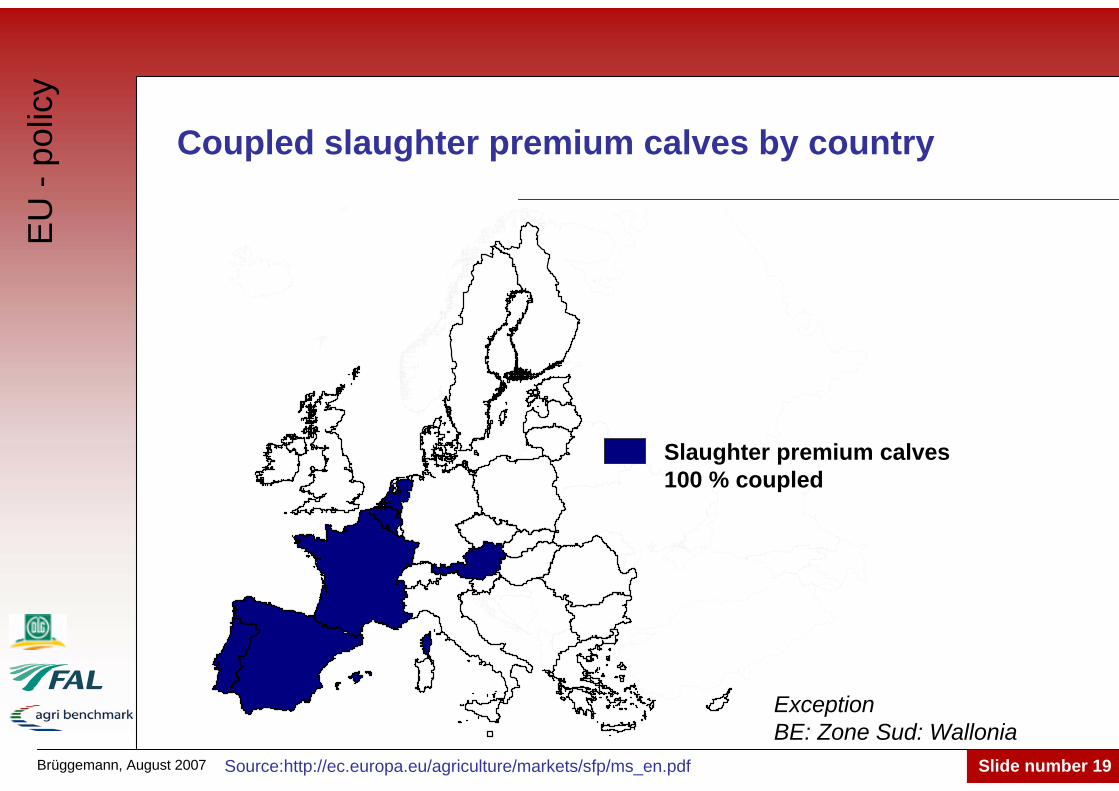

Coupled slaughter premium calves by country

EU

-po

licy

Slaughter premium calves100 % coupled

Source:http://ec.europa.eu/agriculture/markets/sfp/ms_en.pdf

ExceptionBE: Zone Sud: Wallonia

Brüggemann, August 2007 Slide number 20

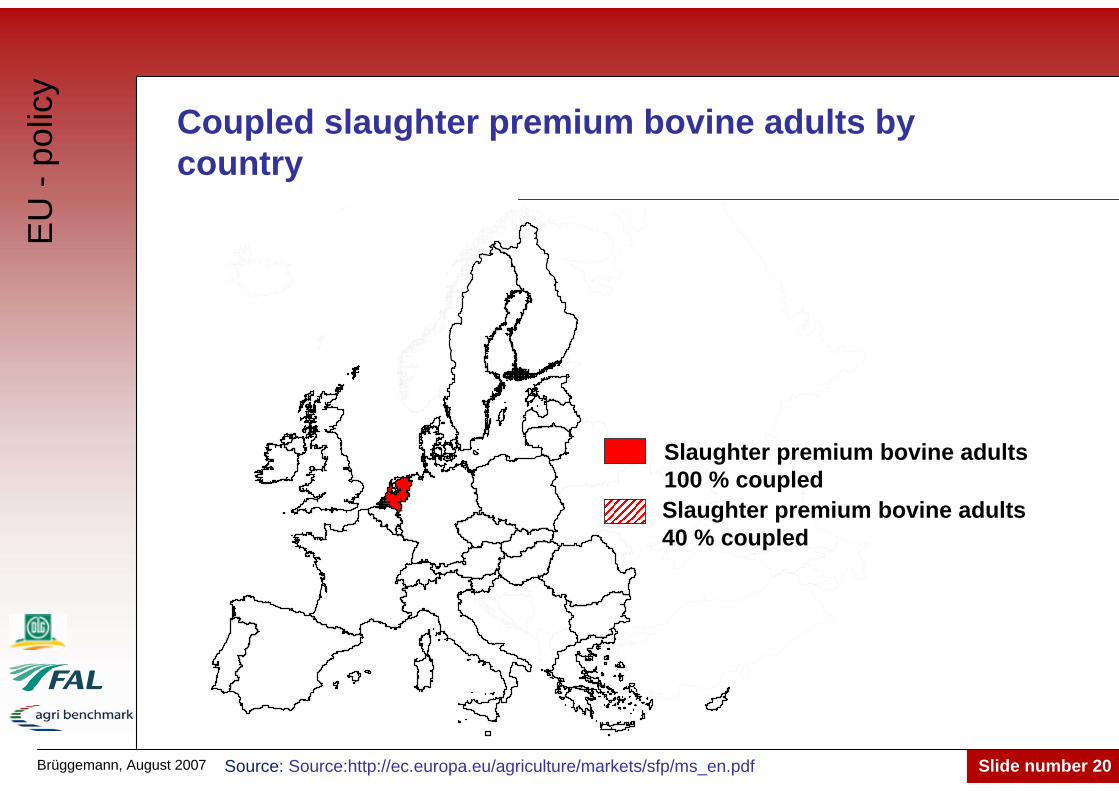

Coupled slaughter premium bovine adults bycountry

EU

-po

licy

Slaughter premium bovine adults100 % coupled

Source: Source:http://ec.europa.eu/agriculture/markets/sfp/ms_en.pdf

Slaughter premium bovine adults40 % coupled

Brüggemann, August 2007 Slide number 21

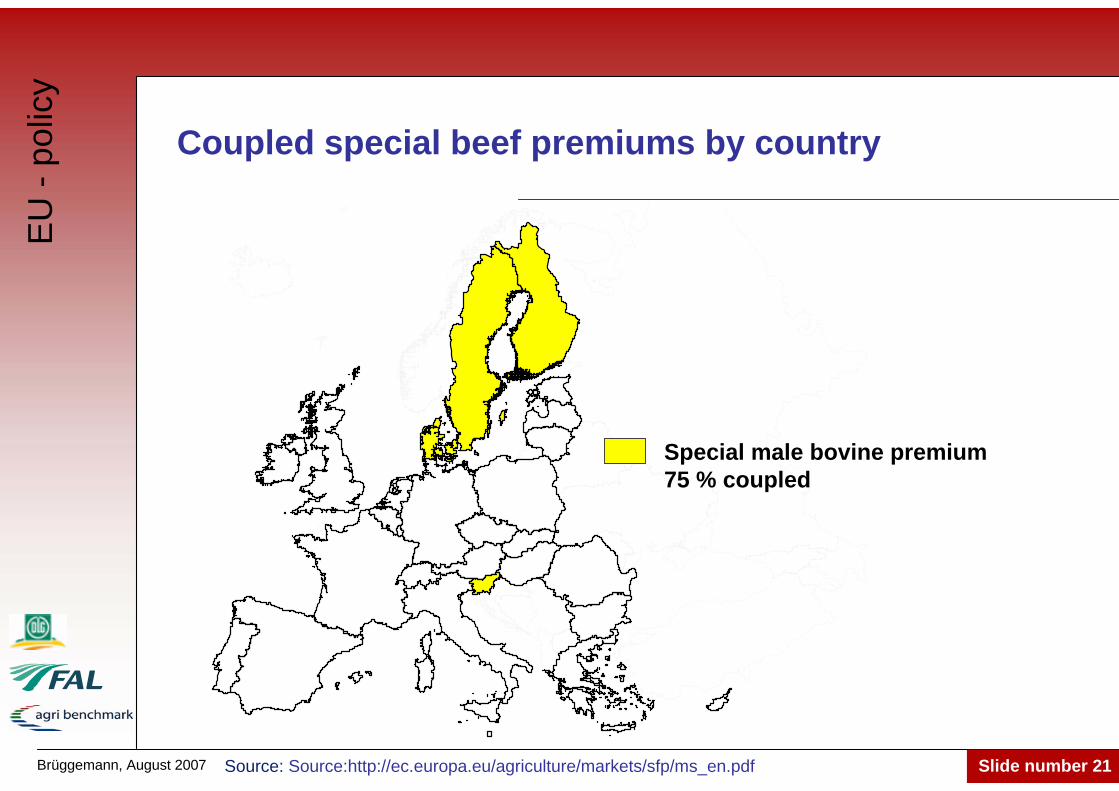

Coupled special beef premiums by country

EU

-po

licy

Special male bovine premium75 % coupled

Source: Source:http://ec.europa.eu/agriculture/markets/sfp/ms_en.pdf

Brüggemann, August 2007 Slide number 22

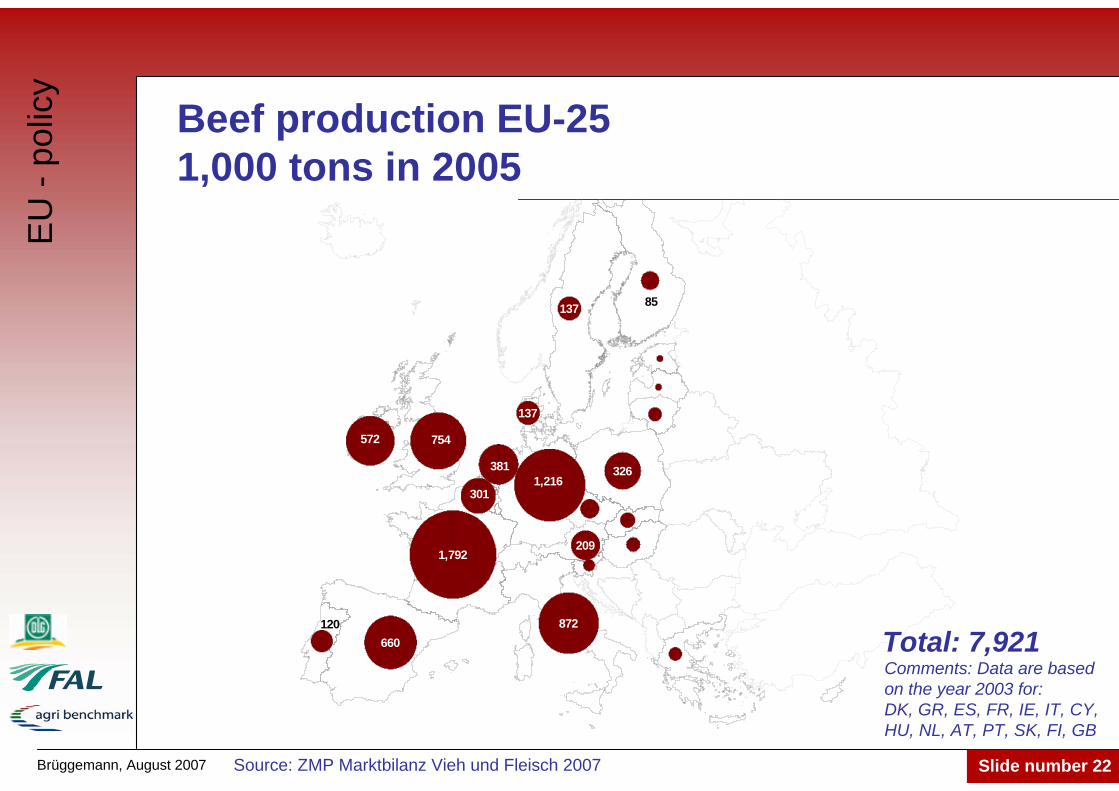

Beef production EU-25 1,000 tons in 2005

209

3011,216

137

660

85

1,792

572

872

381 326

120

137

754

Source: ZMP Marktbilanz Vieh und Fleisch 2007

Comments: Data are basedon the year 2003 for:DK, GR, ES, FR, IE, IT, CY, HU, NL, AT, PT, SK, FI, GB

Total: 7,921

EU

-po

licy

Brüggemann, August 2007 Slide number 23

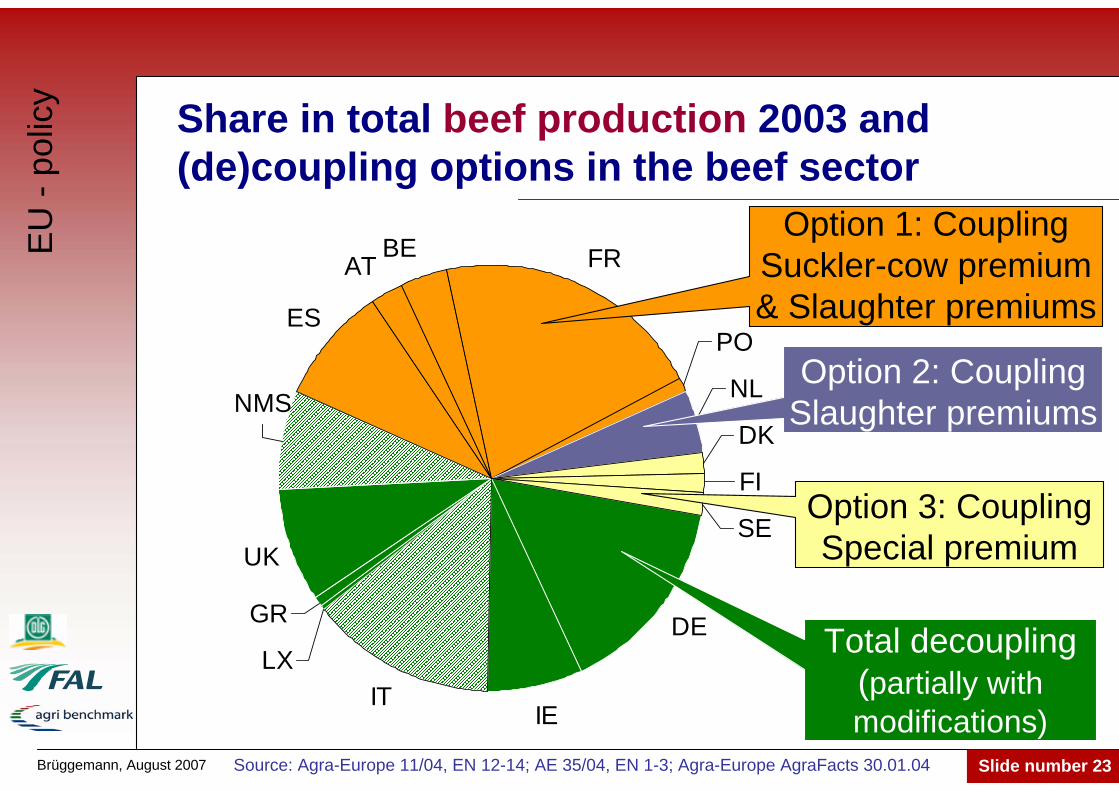

Share in total beef production 2003 and (de)coupling options in the beef sector

DE

IEIT

LX

GR

UK

ES

ATBE FR

PO

NL

DK

FI

SE

NMS

Total decoupling(partially with modifications)

Option 1: CouplingSuckler-cow premium& Slaughter premiums

Option 2: CouplingSlaughter premiums

Option 3: CouplingSpecial premium

Source: Agra-Europe 11/04, EN 12-14; AE 35/04, EN 1-3; Agra-Europe AgraFacts 30.01.04

EU

-po

licy

Brüggemann, August 2007 Slide number 24

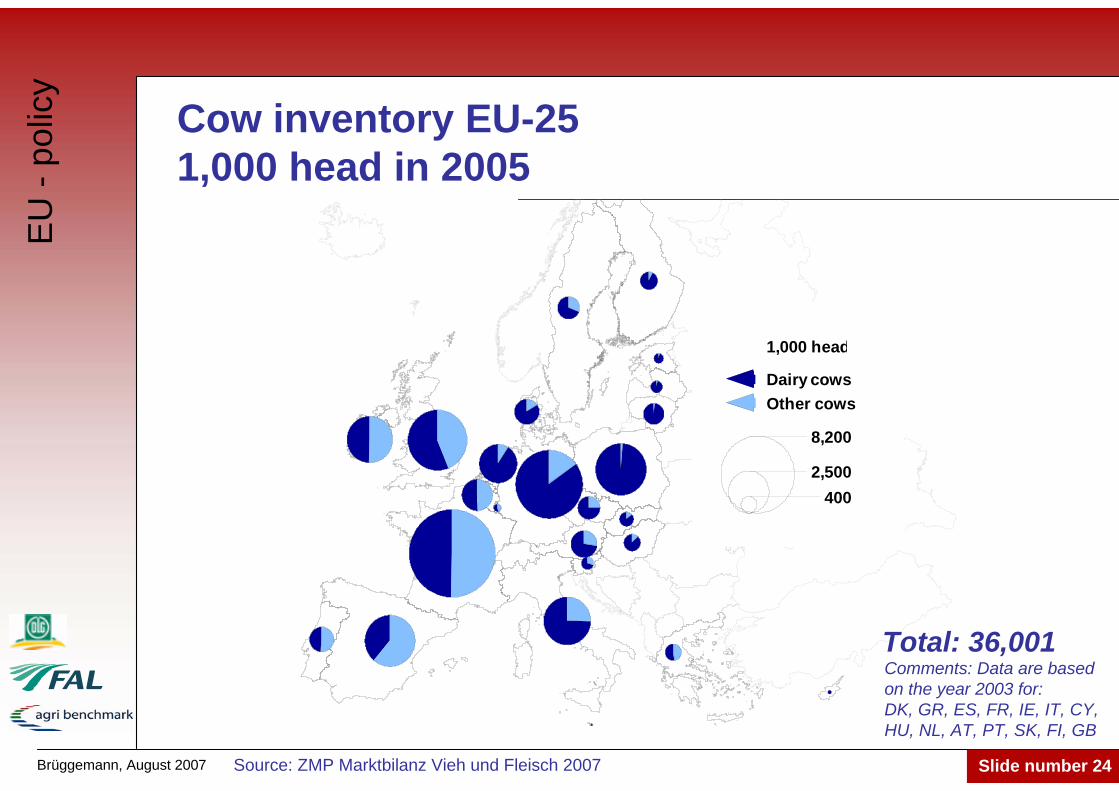

Cow inventory EU-25 1,000 head in 2005

1,000 head

Dairy cowsOther cows

8,200

2,500400

Source: ZMP Marktbilanz Vieh und Fleisch 2007

Comments: Data are basedon the year 2003 for:DK, GR, ES, FR, IE, IT, CY, HU, NL, AT, PT, SK, FI, GB

Total: 36,001

EU

-po

licy

Brüggemann, August 2007 Slide number 25

DEIE

ITLXUK

NMS

ES

AT

BE

FR

PO

NL

DK

FI

SE

GR

Source: EUROSTAT; NMS: 2001; ES+PO: 2002; Other countries 2003

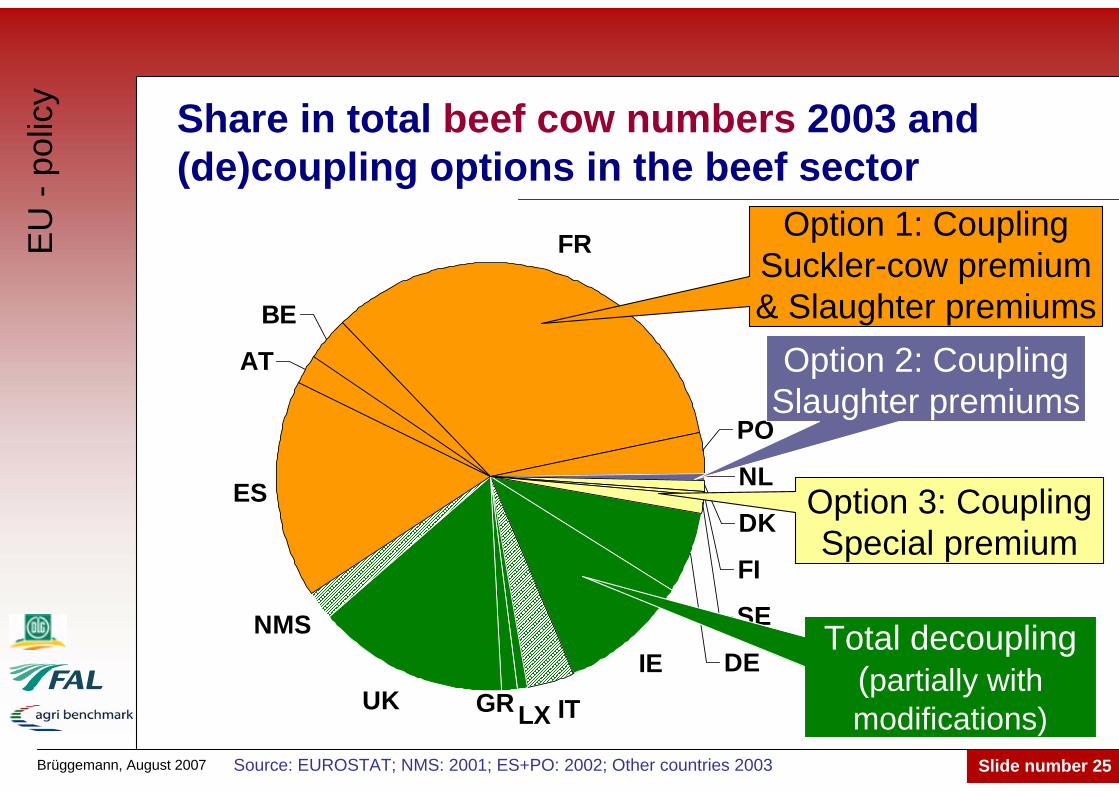

Share in total beef cow numbers 2003 and (de)coupling options in the beef sector

Total decoupling(partially with modifications)

Option 1: CouplingSuckler-cow premium& Slaughter premiums

Option 2: CouplingSlaughter premiums

Option 3: CouplingSpecial premium

EU

-po

licy

Brüggemann, August 2007 Slide number 26

Conclusion

Different payment models used

Different share of decoupled and coupled directpayment

Different economic situation for beef farmerswithin Europe => „COMMON Agriculture Policy“?

EU

-po

licy

Brüggemann, August 2007 Slide number 27

CAPOn farm level

Brüggemann, August 2007 Slide number 28

Coupled situation until 2004 / 2005– Beef finishingEUR per 100 kg carcass weight

0

100

200

300

400

500

600

700

AT-

7

AT-

30

DE

-190

DE

-240

DE

-280

DE

-360

FR-4

5

FR-9

0A

FR-9

0B

ES-9

50

ES-6

950

IE-7

5

CZ-

160

CZ-

780

HU

-80

HU

-440

PL-1

2

PL-3

0

DepreciationOther cash costAnimal purchase

Beef returns + government paymentsBeef returns

Sumgovernmentpayments

Source: Own calculations after IFCN Beef Report 2004

Part of thepayment thatmust be used to compensate a loss that occurswithoutpayments

Ana

lysi

ngpo

licy

impa

ct

Brüggemann, August 2007 Slide number 29

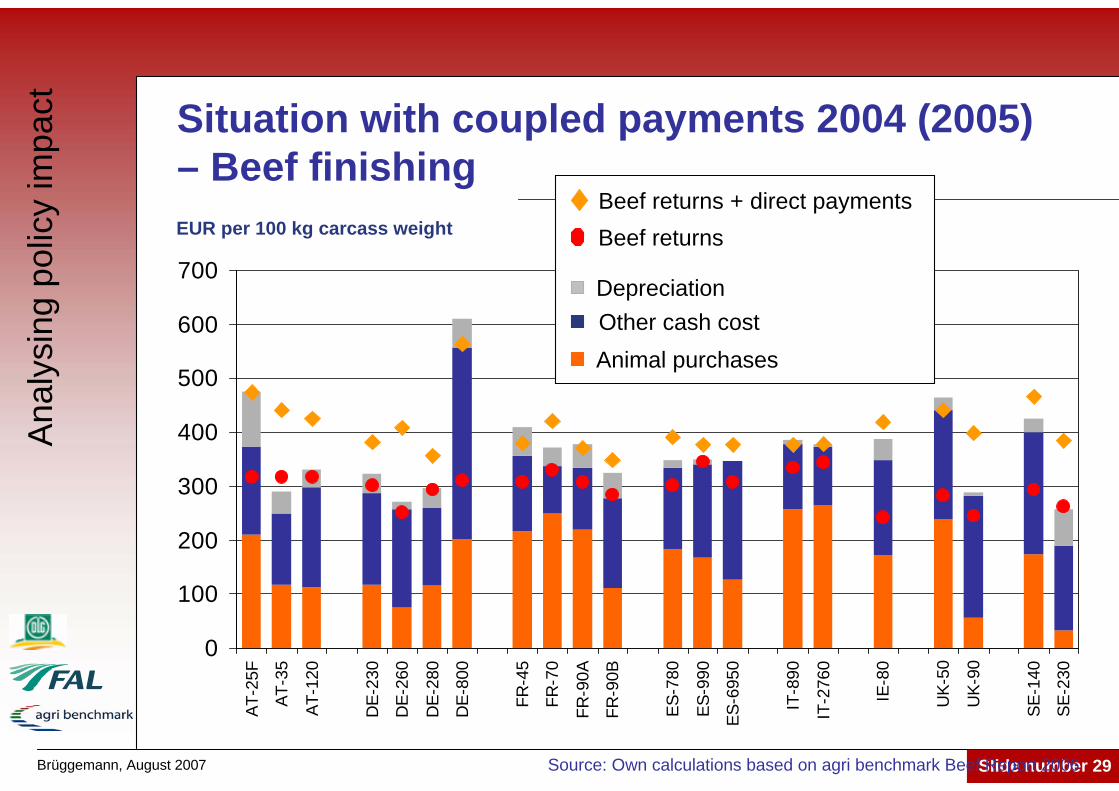

Situation with coupled payments 2004 (2005)– Beef finishingEUR per 100 kg carcass weight

0

100

200

300

400

500

600

700AT

-25F

AT-3

5

AT-1

20

DE-

230

DE-

260

DE-

280

DE-

800

FR-4

5

FR-7

0

FR-9

0A

FR-9

0B

ES-7

80

ES-9

90

ES-6

950

IT-8

90

IT-2

760

IE-8

0

UK-

50

UK-

90

SE-1

40

SE-2

30

Source: Own calculations based on agri benchmark Beef Report 2006

Depreciation

Beef returns

Other cash costAnimal purchases

Beef returns + direct payments

Ana

lysi

ngpo

licy

impa

ct

Brüggemann, August 2007 Slide number 30

Situation with decoupled payments 2005 (2006)– Beef finishing

0

100

200

300

400

500

600

700AT

-25F

AT-3

5

AT-1

20

DE-

230

DE-

260

DE-

280

DE-

800

FR-4

5

FR-7

0

FR-9

0A

FR-9

0B

ES-7

80

ES-9

90

ES-6

950

IT-8

90

IT-2

760

IE-8

0

UK-

50

UK-

90

SE-1

40

SE-2

30

Source: Own calculations based on agri benchmark Beef Report 2006

EUR per 100 kg carcass weight

Depreciation

Beef returns

Other cash costAnimal purchases

Beef returns + direct payments

Ana

lysi

ngpo

licy

impa

ct

Brüggemann, August 2007 Slide number 31

0

100

200

300

400

500

600

700

800AT

-25C

AT-3

0

DE-

1100

DE-

1400

FR-6

5

FR-8

0

FR-8

5

ES-7

5

ES-1

50

IE-2

5

UK-

60F

UK-

60C

SE-1

50

HU

-150

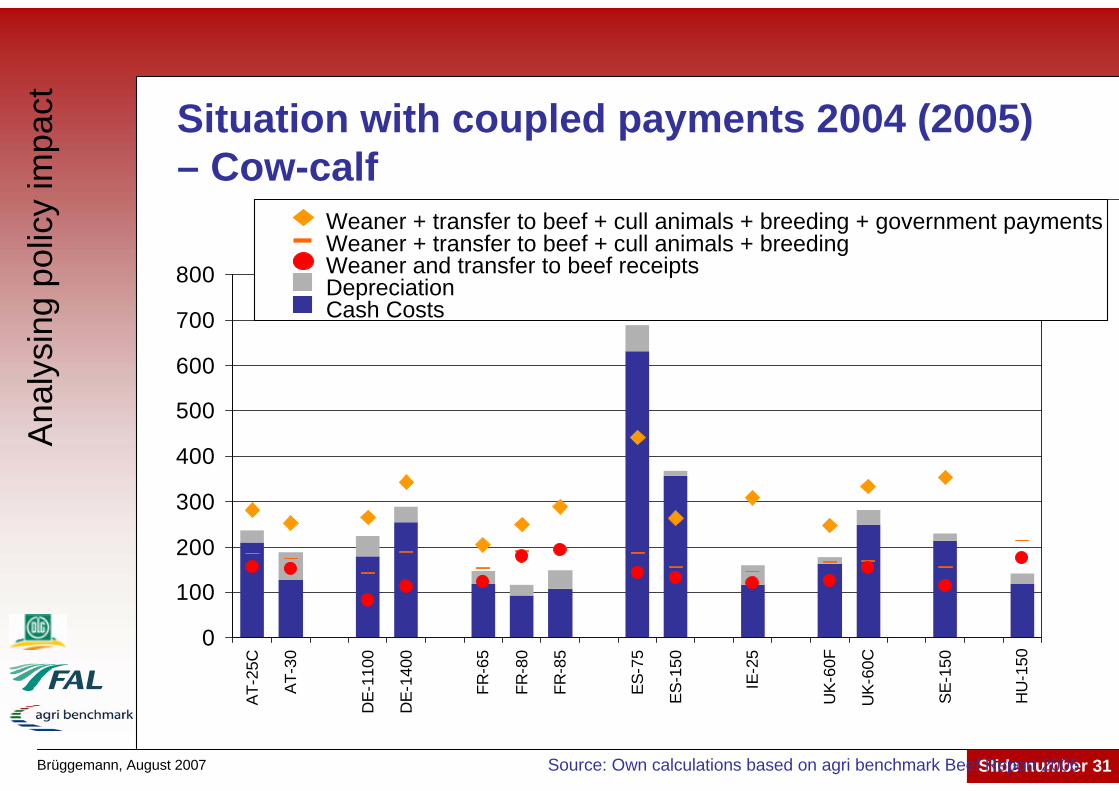

Situation with coupled payments 2004 (2005)– Cow-calf

Source: Own calculations based on agri benchmark Beef Report 2006

Ana

lysi

ngpo

licy

impa

ct

DepreciationCash Costs

Weaner and transfer to beef receipts

Weaner + transfer to beef + cull animals + breeding + government paymentsWeaner + transfer to beef + cull animals + breeding

Brüggemann, August 2007 Slide number 32

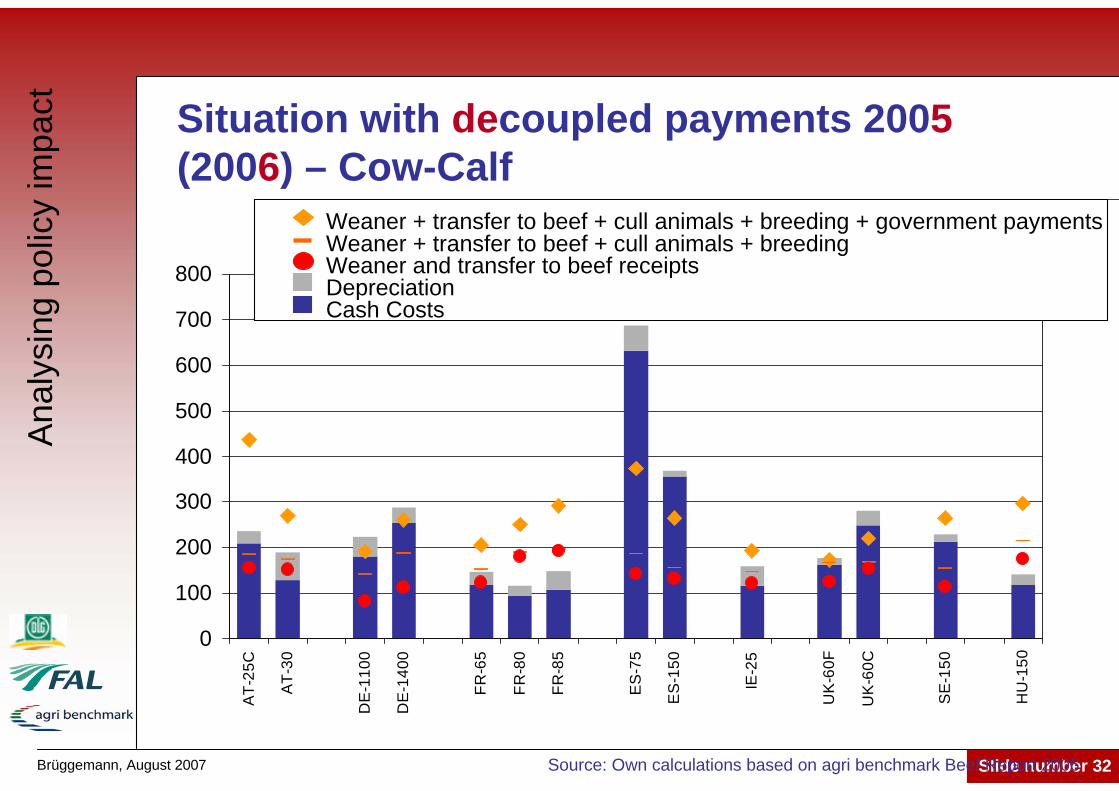

Situation with decoupled payments 2005 (2006) – Cow-Calf

Ana

lysi

ngpo

licy

impa

ct

0

100

200

300

400

500

600

700

800A

T-25

C

AT-

30

DE

-110

0

DE

-140

0

FR-6

5

FR-8

0

FR-8

5

ES

-75

ES

-150

IE-2

5

UK

-60F

UK

-60C

SE

-150

HU

-150

DepreciationCash Costs

Weaner and transfer to beef receipts

Weaner + transfer to beef + cull animals + breeding + government paymentsWeaner + transfer to beef + cull animals + breeding

Source: Own calculations based on agri benchmark Beef Report 2006

Brüggemann, August 2007 Slide number 33

Which policy has beenimplemented in Germany?

Brüggemann, August 2007 Slide number 34

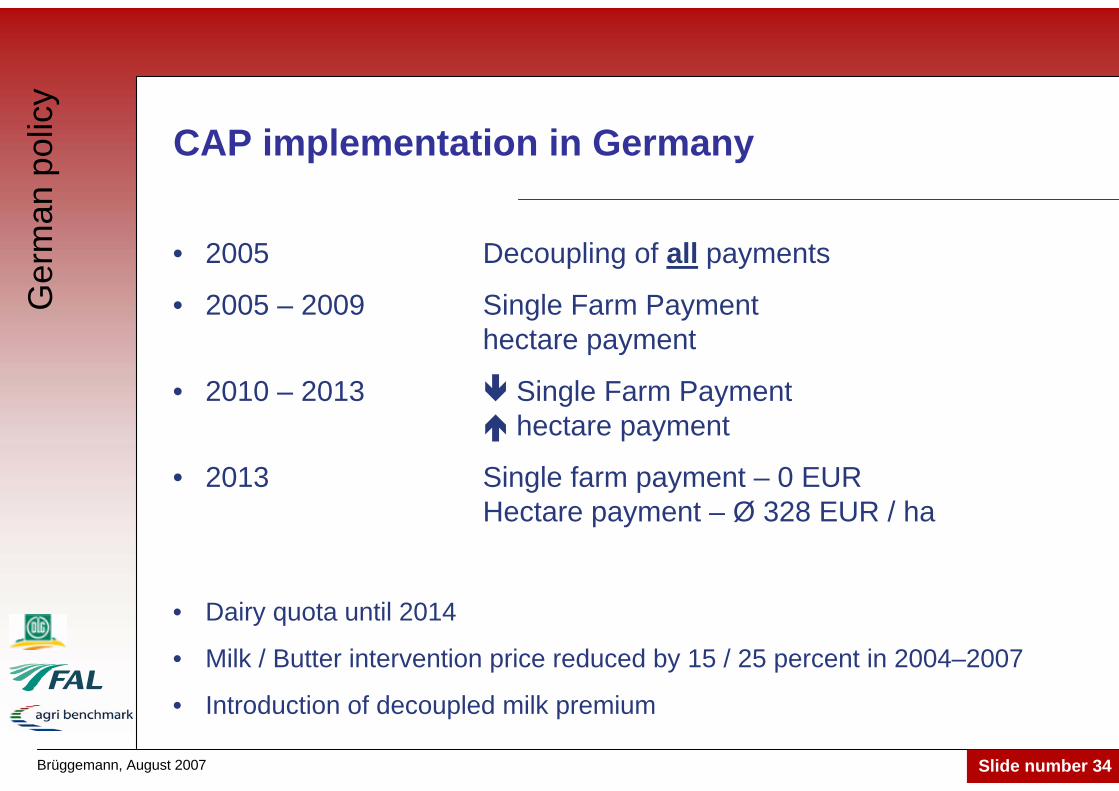

CAP implementation in Germany

• 2005 Decoupling of all payments

• 2005 – 2009 Single Farm Paymenthectare payment

• 2010 – 2013 Single Farm Paymenthectare payment

• 2013 Single farm payment – 0 EURHectare payment – Ø 328 EUR / ha

• Dairy quota until 2014

• Milk / Butter intervention price reduced by 15 / 25 percent in 2004–2007

• Introduction of decoupled milk premium

Ger

man

pol

icy

Brüggemann, August 2007 Slide number 35

Allocation of coupled premiums to SFP and hectare payments in Germany 2005-2009

Hectare payment Single farm payment

Source: DBV (German Farmers Association)

Grand Cultures p/Seed production p/

75 % dec. starch payments p/

Decoupled hop p/

Dairy p/

Suckler cow p/

Special p/ male cattle

Slaughter p/ calves

50% extensific. p/cattle

Ewe p/25 % dec. starch payments

Decoupled part tobacco and dry feed

Slaughter p/ adults

National p/ cattle

50% extensification p/ cattle

Cro

plan

dG

rass

land

Ger

man

pol

icy

Brüggemann, August 2007 Slide number 36

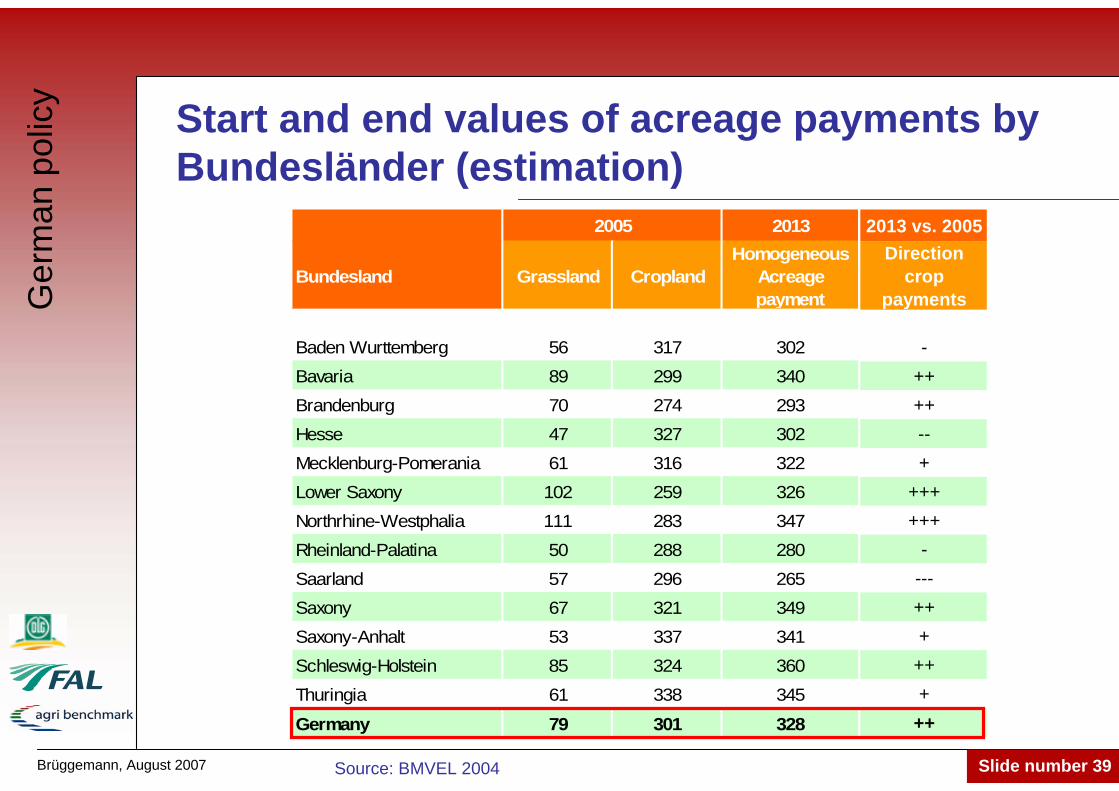

Bundesland Grassland Cropland

Baden Wurttemberg 56 317Bavaria 89 299Brandenburg 70 274Hesse 47 327Mecklenburg-Pomerania 61 316Lower Saxony 102 259Northrhine-Westphalia 111 283Rheinland-Palatina 50 288Saarland 57 296Saxony 67 321Saxony-Anhalt 53 337Schleswig-Holstein 85 324Thuringia 61 338

Germany 79 301

2005

Start values of acreage payments by Bundesländer (estimation)

Source: BMVEL 2004

Ger

man

pol

icy

Single farm payment

Calculated individuallyfor each farm

based on average ofthe years

2000 -2002

Brüggemann, August 2007 Slide number 37

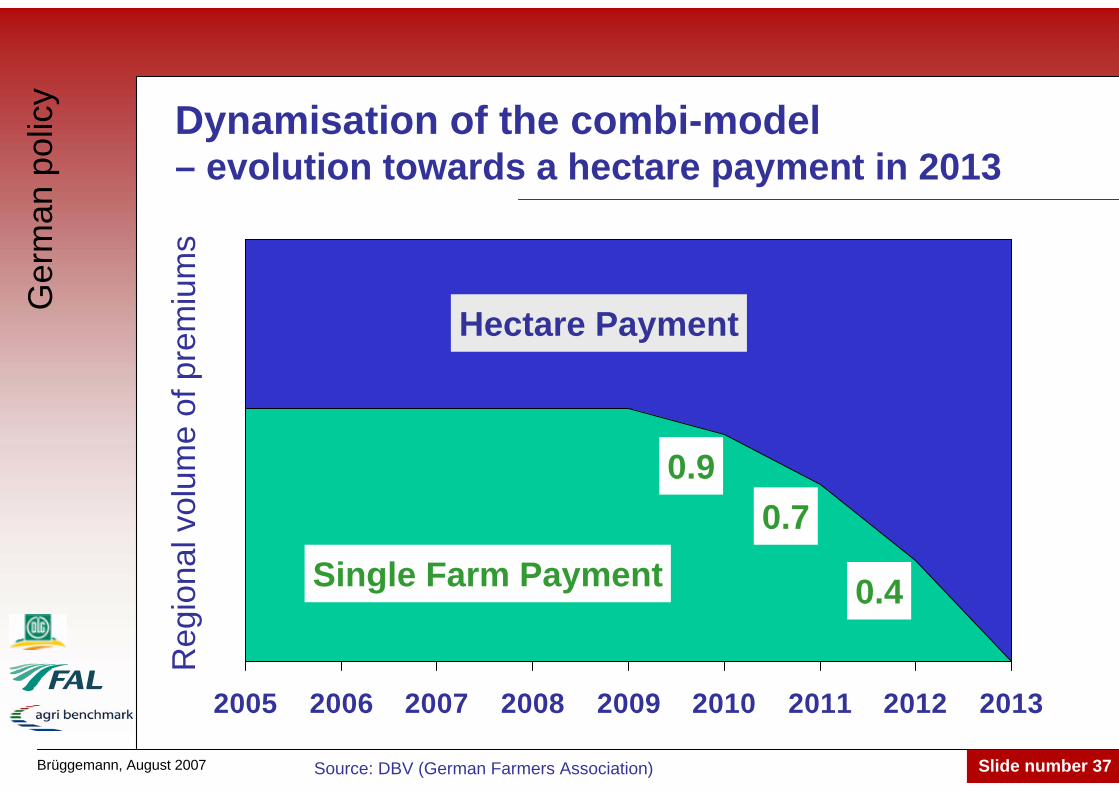

Dynamisation of the combi-model– evolution towards a hectare payment in 2013

Source: DBV (German Farmers Association)

2005 2006 2007 2008 2009 2010 2011 2012 2013

Hectare Payment

Single Farm Payment

Reg

iona

l vol

ume

of p

rem

ium

s

0.90.7

0.4

Ger

man

pol

icy

Brüggemann, August 2007 Slide number 38

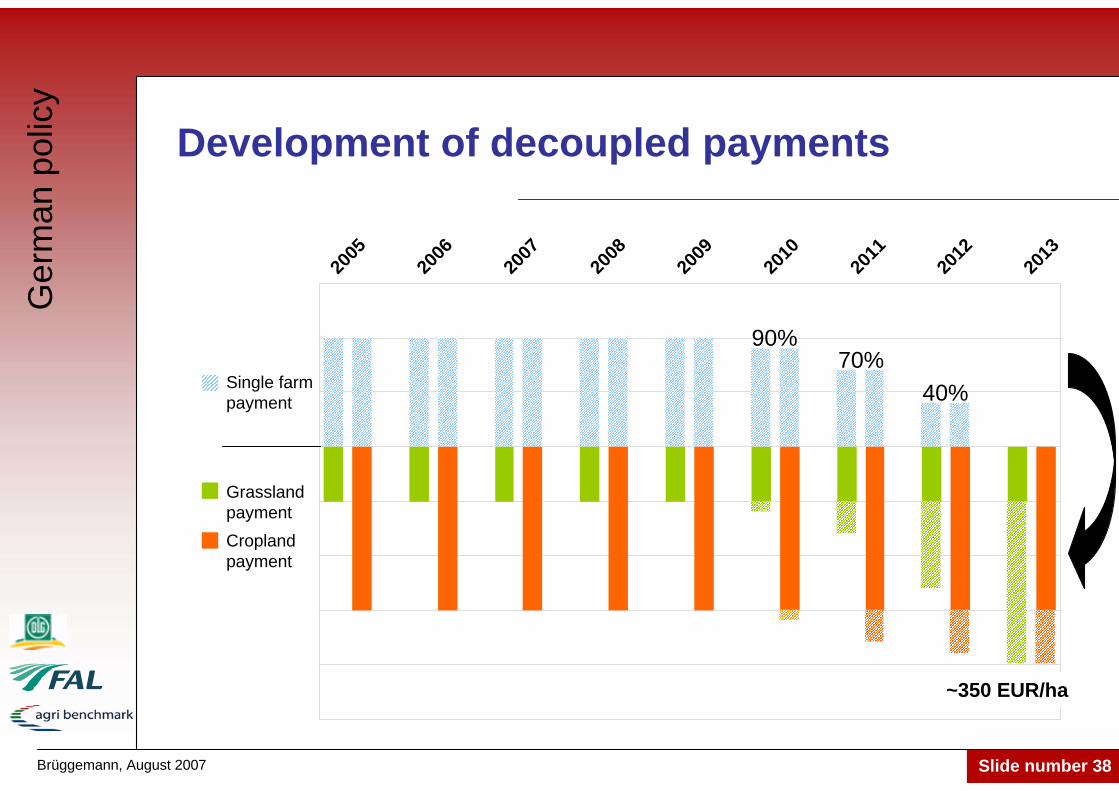

Development of decoupled payments

Ger

man

pol

icy

~350 EUR/ha

90%70%

40%

2005

2006

2007

2008

2009

2010

2011

2012

2013

Single farmpayment

Grassland paymentCroplandpayment

Brüggemann, August 2007 Slide number 39

2013 vs. 2005Direction

crop payments

-++++--+

++++++

----+++

+++

++

Start and end values of acreage payments by Bundesländer (estimation)

2013

Bundesland Grassland CroplandHomogeneous

Acreage payment

Baden Wurttemberg 56 317 302Bavaria 89 299 340Brandenburg 70 274 293Hesse 47 327 302Mecklenburg-Pomerania 61 316 322Lower Saxony 102 259 326Northrhine-Westphalia 111 283 347Rheinland-Palatina 50 288 280Saarland 57 296 265Saxony 67 321 349Saxony-Anhalt 53 337 341Schleswig-Holstein 85 324 360Thuringia 61 338 345

Germany 79 301 328

2005

Source: BMVEL 2004

Ger

man

pol

icy

Brüggemann, August 2007 Slide number 40

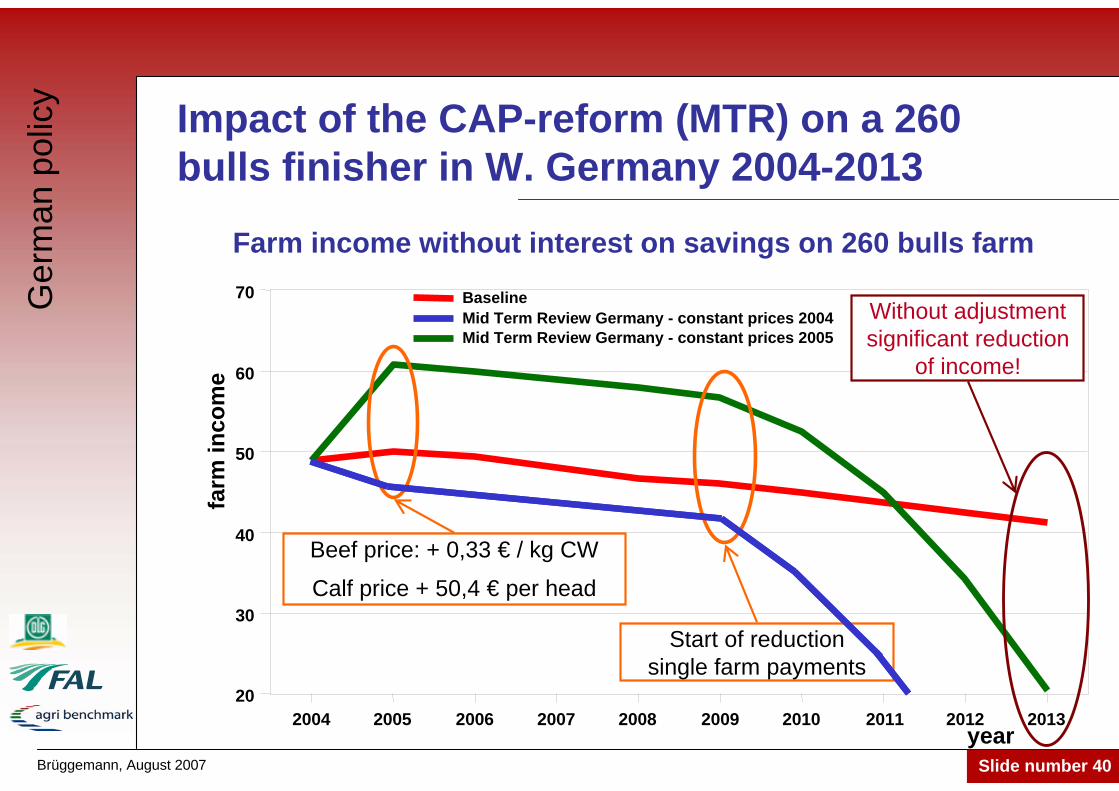

Impact of the CAP-reform (MTR) on a 260 bulls finisher in W. Germany 2004-2013

Farm income without interest on savings on 260 bulls farm

2004 2005 2006 2007 2008 2009 2010 2011 2012 201320

30

40

50

60

70 Baseline

Mid Term Review Germany - constant prices 2005

Beef price: + 0,33 € / kg CW

Calf price + 50,4 € per head

Start of reductionsingle farm payments

farm

inco

me

year

Without adjustmentsignificant reduction

of income!

Mid Term Review Germany - constant prices 2004

Ger

man

pol

icy

Brüggemann, August 2007 Slide number 41

Implications

• Full decoupling: no obligation to produce anymore

• The SFP until 2009 reduces the liquidity problems for intensive (dairy and beef finishing) farms

• To receive payments the land must be maintained in a defined status (cross compliance), basically kept ‘open’

• This can be done mechanically by mulching once a year at cost of approx. 40 EUR/ha

• If the loss from beef production is below –40 EUR/ha, mechanical maintenance is the better alternative

Ger

man

pol

icy

Brüggemann, August 2007 Slide number 42

Summary

Beef and suckler-cow herd are dominated by a few countries within the EU-25

Different decoupling models have beenimplemented and will last until 2013

Currently beef farmers face a different economicsituation, e.g. total decoupling in Germany

In a long term view this policy should beconsidered as preliminary

Environment, Rural Development, AnimalWelfare, etc. will be of increasing interest and important challenges in the near future