implementation of beps action 13 in argentina and … of beps action 13 in argentina and mexico - tp...

TRANSCRIPT

1 Taking control of the future tpa-global.com

22 November 2017

Implementation of BEPS Action 13 in Argentina and

Mexico - TP regulations in Central America

Sonia Catalina Muñoz RRamón Lavara

Belisa SeveriniFrancisco Arballo

2 Taking control of the future tpa-global.com

Presenters

Belisa Severini Transfer Pricing Associates [email protected]+54 9 291 57098 79

Sonia Catalina Muñoz R.Transfer Pricing AssociatesNetherlands [email protected] +31 20 262 0022

Ramon LavaraLavara Transfer Pricing Consulting, S.C.Mexico+52 55 91 71 11 [email protected]

Francisco ArballoGrupo Consultor EFE™Mexico+52 (664) 634 [email protected]

3 Taking control of the future tpa-global.com

Index

• General presentation of the Argentine and Mexican transfer pricing legislation incorporated in accordance with Action 13 of BEPS

• Regional integration of transfer pricing in Center America (Costa Rica, Guatemala, El Salvador, Honduras, Nicaragua and Panama)

4 Taking control of the future tpa-global.com

BEPS Action 13 - Mexico

Panelist: Ramón Lavara

5 Taking control of the future tpa-global.com

Content

1. Background 2. BEPS implementation in Mexico

6 Taking control of the future tpa-global.com

BEPS Background in Mexico

• 2015: Inclusion of new information to be disclosed in Appendix 9 of the Informative Return of Transactions with Foreign Related Parties

• 2015: Inclusion of Article 76-A in the LISR incorporating the following sections

o Section I: Informative Master Return Declaración (Master File)

o Section II: Informative Local Return (Local File)

o Section III: Country by Country Return (Country by Country Report)

7 Taking control of the future tpa-global.com

Implementation in México

Document LISR Approach

Master File Taxpayers considered in Article 32 H, sections I, II, III and IV of the Federal Tax Code

I. Taxpayers referred in Section II of the LISR that in the previous year had taxable income for income taxpurposes of or more than $671,414,320* pesos (35,000,000 USD). Also, Companies with shares traded withinvestors in a recognized stock exchange market.

II. Taxpayers referred in Chapter VI Section II of the LISR “Special Tax Regime for Groups of Companies”

III. Companies with Government Participation

IV. Permanent Establishments in Mexico of foreign corporations only for the activities conducted by such PEsin Mexico

* Annually Updated for Inflation

Local File

Country by Country Report

• Mexican Corporations or Holdings with consolidated income for the previous year of or more than $12,000 million pesos (USD 632)

• Entities designated by their holding companies to file such return on its behalf

8 Taking control of the future tpa-global.com

Objectives and Approach

Document Objetive and ApproachReturn

Master File• Objetive: To evaluate the Risks of the MNE• Approach: Provide an overview of the MNE and its business

Local File

• Objetive: To review compliance with the arm’s length principle in related party transactions

• Approach: Provide additional details regarding the intercompany transactions conducted in a given tax jurisdiction

Country by Country Report(CbC)

• Objetive: To provide key and relevant information to the tax authorities about the MNE

• Approach: Provide tax and financial information summarized by jurisdiction considering the Value Chain of the MNE

9 Taking control of the future tpa-global.com

Master File y Local File

Master and Local Returns

Master File for MNEsOrganizational Structure, Description of the MNE business model, intangibles, intercompany financial transactions and

structure, tax and financial information

Local File for Entity A■ Description of local entity (management & strategy)■ Description of intercompany transactions■ Functional Analysis■ Selection of Transfer Pricing Method■ Economic Analysis ■ Financial Information

Local File for Entity B■ The same as Entity

A

Local File for Entity C■ The same as Entity

A

\

1 0 Taking control of the future tpa-global.com

Considerations

• Information will be filed before the tax authorities where the MNE operates

• Information must be coherent and consistent Challenges

• How to prepare the Master File? (i.e. By line of product / business ?)

• Amount and transactions threshold • New processes year after year

Planning required

• If countries do not adopt 100% of the rules (i.e. US) this could affect their subsidiaries

How many MNEs will be affected?

• There is information that has not been required and disclosed beforeWhat is New?

1 1 Taking control of the future tpa-global.com

Country by Country Return

CbC

Income

CountryRelated

partyThird party Total

Profit

(Loss)

before

taxes

Income tax

Paid

(paid)

Income tax

accrued –

Current

year_

EquityRetained

profits

Number of

employees

Tangible

assets

different than

cash and

cash

equivalents

Country A

Country B

No Residents in

any tax jurisdiction

¿How reasonable these transactions are agreed?

¿Ratio of Income / Equity or Income / Assets etc. in each country and it relation with the taxes paid

¿How much of the income of the group is non taxable?

¿Where are the Group profits allocated ?¿Magnitude of deductions vs income and

relation of such deductions with regards to assets and employees ?

1 2 Taking control of the future tpa-global.com

Deadlines / Other Considerations

• The returns must be filed by December 31 of the following fiscal year that is being reported or if therelated party that prepares the Master File / Return has a tax year that do not match the calendaryear, the deadline will be the month in which the company’s fiscal year ends (up to may)

• In case the tax authorities are not be able to obtain the information of the “Country by Country Return”of certain MNE Group through the exchange of information mechanisms established, the taxpayerswill have 120 days after the request is received from the tax authorities to provide the correspondinginformative Country by Country Return.

1 3 Taking control of the future tpa-global.com

Deadline and other considerations

• Penalties go from $140,540 pesos to $200,090 pesos for not filing the required information or if it is incomplete or with errors or inconsistencies

• Impossibility of being a government provider

• Cancellation of the registration on the importers records

• Cancellation of the Companies Digital Stamp

1 4 Taking control of the future tpa-global.com

BEPS Action 13 - Argentina

Panelist: Belisa Severini

1 5 Taking control of the future tpa-global.com

Action 13 of BEPS Plan in Argentina

• Until now, the Federal Administration of Public Revenues (AFIP) required the presentation of the TP Local Report (regulated by General Resolution(GR) 1122/2001) and the Informative Returns related to::

➢ Transactions carried out with related companies from abroad and local and with companies located in countries considered non-cooperative;and

➢ Import and export transactions carried out with independent third parties.

• GR N° 4130-E, published in the Official Gazette on September 20, 2017, issued by the AFIP, introduced:➢ An annual reporting regime consisting of the submission of a Country-by-Country (CbC) Report for certain taxpayers who are members of

Multinational Entity (MNE) Groups.

➢ Additionally, GR 4130-E introduced the obligation to provide the AFIP with some information of a more general nature for all the entitiesresident in Argentina that are members of MNE Groups.

• Application for the fiscal years of each ultimate parent entity (UPE) of the MNE Groups initiated as of January 1, 2017, inclusive.

• These new rules are added to the existing obligations related to TP.

• These modifications are made within the framework of the recommendations established in Action 13 of the BEPS Plan, to which Argentinaadhered.

• Likewise, Argentina signed the Multilateral Competent Authority Agreement on the Exchange of CbC Reports (CbC MCAA), which establishes theprocedures for the Tax Administrations to automatically exchange the CbC reports, within a framework of protection and confidentiality of data,submitted by the reporting entities of the MNE Groups in the corresponding tax jurisdictions. Currently the CbC MCAA is composed of 65 countries.

1 6 Taking control of the future tpa-global.com

Country by Country Report – Entities subject to theobligation to report

• The regime applies to MNE Groups whose total consolidated annual revenues, attributable to the fiscal year preceding the fiscal year to bereported, are equal to or greater than € 750 million or its equivalent converted into the local currency of the UPE´s fiscal jurisdiction, at theexchange rate effective in said jurisdiction as of January 31, 2015 (i.e. if the UPE is located in Argentina, the threshold will be approx. AR$7.240 million).

• Entities subject to the obligation to report:

1. The UPE is resident in Argentina for tax purposes.

2. A surrogate entity resident in Argentina, appointed by the UPE to file the report on its behalf.For this purpose, only entities whose shareholders´ equity is equal to or greater than AR$ 50 million or who possess an operative and / orfunctional structure that allows them to gather the necessary information to comply with the submission of the CbC Report may bedesignated as surrogate entities.

3. An entity resident in Argentina that is a member of a MNE Group, that is not the aforementioned entities, provided that at least one of thefollowing assumptions is verified:

• The UPE is not required to file the CbC Report in its fiscal jurisdiction..

• On the deadline for the submission of the CbC Report, the tax jurisdiction of the UPE has not signed a qualified competent authorityagreement for the automatic exchange of CbC reports on of which Argentina is a party.

• There would be a systematic failure by the UPE´s fiscal jurisdiction in the exchange of information regarding the CbC Report.

1 7 Taking control of the future tpa-global.com

Country by Country Report - Entities subject to theobligation to report - Exception

• An entity resident in Argentina that is a member of a MNE Group included in subsection 3) above, will be exemptfrom filing the CbC Report if it has already been submitted by a surrogate entity not residing in Argentina to the taxauthority of its local fiscal jurisdiction and provided the following conditions are met:

• The fiscal jurisdiction has established a regime for the submission of the CbC Report.• On the deadline for the submission of the CbC Report, the fiscal jurisdiction has signed an qualified

competent authority agreement for the automatic exchange of CbC reports on of which Argentina is a party.• There is no systematic failure by the fiscal jurisdiction in the exchange of information regarding the CbC

Report.• The fiscal jurisdiction has been notified by the entity member of the MNE Group resident in that jurisdiction of

its designation as a surrogate entity.

1 8 Taking control of the future tpa-global.com

Country by Country Report - Information to be provided

1) For each jurisdiction in which the MNE Group operates:

• Total amount of the group´s revenue, differentiating those obtained from related entities and from independent parties.• Result - profit or loss - obtained before the income tax.• Income tax paid, including withholdings applied.• Income tax accrued in the current fiscal year.• Equity.• Accumulated earnings not distributed.• Number of employees.• Tangible assets, other than cash and cash equivalents.

2) For each member entity of the MNE Group within each of said jurisdictions:• Argentine Tax Identification Number (CUIT) or Fiscal Identification Number (NIF) in the country of tax residence of each of

the entities from abroad.• Corporate name.• Tax jurisdiction or country of incorporation.• Main economic activities and description of its nature.

3) All other information considered relevant as well as an explanation of the data included in the information that facilitate its understanding

1 9 Taking control of the future tpa-global.com

Country by Country Report – Submission and Deadline

• Submission: through the service called "CbC Information Regime" option "Report Submission",available on the AFIP´s website. As proof of the submission made, the system will issue theform F. 8097.

• Deadline: the CbC Report will be submitted annually until the last business day of the 12th monthimmediately following the closing date of the fiscal year to be reported, of the UPE of the MNEGroup (i.e. if the closing fiscal date is 31/12/2017, the deadline will be in December 2018).

2 0 Taking control of the future tpa-global.com

General information for all entities resident in Argentinathat are members of MNE Groups (1)

Data UPE Reporting Entity, if it is not the same as the UPE

Corporate name X X

Argentine Tax Identification Number (CUIT), Foreign Investor Identification Number (CIE) or Fiscal IdentificationNumber (NIF) in the country of residence, as applicable X X

Type of entity X X

Tax and legal address X X

Place and date of incorporation X X

Tax Jurisdiction X X

Closing date of the fiscal year X X

Amount of total consolidated revenues, disclosed in the consolidated financial statements of the fiscal yearimmediately preceding the fiscal year to be reported X

If the MNE Group is subject to the CbC information regime, for exceeding the threshold of € 750 million X

If it is required to act as reporting entity regarding the CbC Report X

If it submits the CbC report as a surrogate entity appointed by the UPE or as a member entity X

2 1 Taking control of the future tpa-global.com

General information for all entities resident in Argentinathat are members of MNE Groups (2)

• Deadline: obligation to provide the data to the AFIP until the last business day of the 3rd monthimmediately following the closing date of the fiscal year to be reported of the UPE (i.e. if the closingfiscal date is 31/12/2017, the deadline will be in March 2018).

• In addition, all entities resident in Argentina that are members of MNE Groups must inform AFIP thatthe CbC Report has been submitted in the corresponding fiscal jurisdiction until the last business dayof the 2nd month immediately following the deadline for the submission of the CbC Report (i.e. if theclosing fiscal date is 31/12/2017, the deadline for the submission of the CbC Report will be December2018 and the Argentine entity must inform it in February 2019).

• Submission: through the service called "CbC Information Regime" option "Registration", available on theAFIP´s website. As proof of the submission made, the system will issue the form F. 8096.

2 2 Taking control of the future tpa-global.com

Use of Information by the AFIP

• Use the information included in the CbC Report for the assessment of TP risks, base erosion andprofit shifting, and for the development of economic and statistical analysis.

• Not make use of such information as a conclusive tool by itself for the determination of fiscaladjustments of TP.

• Preserve the confidentiality of information.

• Automatically annual exchange of the CbC Report with the competent authorities of thejurisdictions that have signed the qualified competent authority agreement for the automaticexchange of CbC reports and in which one or more member entities of the MNE Group reside forfiscal purposes.

2 3 Taking control of the future tpa-global.com

Penalties for Non-compliance

• Failing to comply with the obligations set forth in this new resolution will be subject tothe penalties established by Law No. 11,683 of Tax Procedure.

• In addition, those taxpayers may be subject for any of the following actions::

• Rating under a higher risk category of being audited, under the provisions setforth in the Risk Assessment System (SIPER).

• Suspension or exclusion from any AFIP´s Special Tax Registries in which theentity may be registered.

• Suspension of any application for Exemption or Non-withholding Certificatesrequested by the taxpayer.

2 4 Taking control of the future tpa-global.com

Final Considerations

• Important challenges for the Argentine entities that are required to submit the CbC Report, due to thelarge amount of information they need to collect from all the member entities of the MNE Group.

• Information must be submitted in only one currency (USD, AR$ or EUR) and in only one language(Spanish).

• The reporting entity must systematically use the same data source, all fiscal years, to file the CbC Report.• It may choose as the source of information the consolidated financial statements, the individual

financial statements of each entity, the financial / accounting statements for regulatory purposes orinformation of its internal management systems.

• The lack of compliance, partial or total, by the parties subject to the two information regimesincorporated will be considered as a relevant indicator of the need for assessment and verification of therisks associated with their TP, the base erosion and profit shifting related to the member entities of theMNE Groups of which they are a part.

• The AFIP web service is not yet operational.

• Tax reform in process of analysis contemplates the introduction of the Advanced Pricing Agreements(APAs).

2 5 Taking control of the future tpa-global.com

Regional Summary of TP Regulations for Central America

Panelist: Francisco Arballo

2 6 Taking control of the future tpa-global.com

ITL obligates taxpayers to value their transactions with foreignrelated parties at arms length since 2013. However, thisobligations were suspended in for 2014 and then re-activated as of2015.

Since 2016, the Tax Authority has requested a lot of taxpayers tofile their TP Report, giving them 17 business days to comply.

In 2016 also, the tax authorities published their technical guide forTP Reports, in which they establish the minimum requirements aTP Report must comply with in order to be acceptable by the TA.

Domestic Tax Code establishes the the obligation to valueintercompany transactions (domestic and international) at armslength.

The TP Informative Tax Disclosure must be filed no later than March31st, physically at the TA office. Taxpayers are only subject to theInformative Tax Disclosure when intercompany transactions amountmore than 571,429 USD. The TP report must be kept by the taxpayerfor 10 years.

There is a comprehensive guide for taxpayers on Transfer Pricing andthe information that should be included in the TP Report.

In 2011, the TP domestic law was published, where taxpayers are obligated to value their intercompanytransactions at arms length (domestic and international). Starting on Fiscal Year 2014.

This law also obligated taxpayers deemed as “large” and “medium” that amount intercompanytransactions of more than $ 1,00,000 USD per year to file an informative tax disclosure every April 30th.

TA executed fines of $10,000 USD per fiscal year to taxpayers who failed to comply with the informativetax disclosure, there is still a lot of taxpayers refuting this fines with the TA.

Starting on fiscal year 2017, domestic intercompany transactions are not subject to TP Rules.

No TP rules yet, no lesgilative proyects expected.

BELICE

GUATEMALA

EL SALVADOR

HONDURAS

2 7 Taking control of the future tpa-global.com

Decree 37898-H was published in 2013, containing the TPRegulations and obligating taxpayers to value their intercompanytransactions at arms length. (domestic and international).

It also obligates taxpayers labeled as “large” and taxpayers operatingunder “Special Regimes” known as “Zona Libre” (Free Zone) to file aninformative TP Tax Disclosure.

TP Informative tax disclosure is still pending by the TA, the obligationis currently suspended.

TA is already looking into incorporating Action 13 documentationrequirements. TP regulations update expected in coming months.

TP Regulations where postponed in different occasions. Finally, TP ruleswhere approved and came into force on June 2017.

There is still no Informative TP Tax Disclosure.

The TA is currently evaluating 5 firms to provide technical guidance toits team. EFE Consulting Group is among this firms.

TP Regulations where introduced in 2011, obligating taxpayers tovalue their intercompany transactions with foreign relatedparties resident in countries where Panama has an internationalagreement on information exchange.

In 2012, TP regulations apply to international transactions,regardless of the counterparty country of residence.

Las year, TA issues a decree to regulate the Arms LengthPrinciple, establishing the minimum requirements that TPReports must meet. Ando also incorporating aspects of Action13.

TP informative tax disclosure has to be filed before June 30.

TA working on bill to incorporate APA rules for taxpayers.Expected to come into force in coming months.

NICARAGUA

COSTA RICA

PANAMA

2 8 Taking control of the future tpa-global.com

BEPS Action Plan

BEPS Action Guatemala Honduras El Salvador Nicaragua Panama Costa Rica

1. Digital Economy

2. Hybrid Mismatch Agreements

3. CFC Rules

4. Interest Deductions

5. Harmful Tax Practices

6. Treaty Abuse

7. Permanent Establishment Status

8 – 10. Aligning TP Outcomes with Value Creation x x x x

11. Measuring and Monitoring BEPS

12. Mandatory disclosure rules

13. Transfer Pricing Documentation x x x

14. Dispute Resolution

15. Multilateral Instrument x x x

2 9 Taking control of the future tpa-global.com

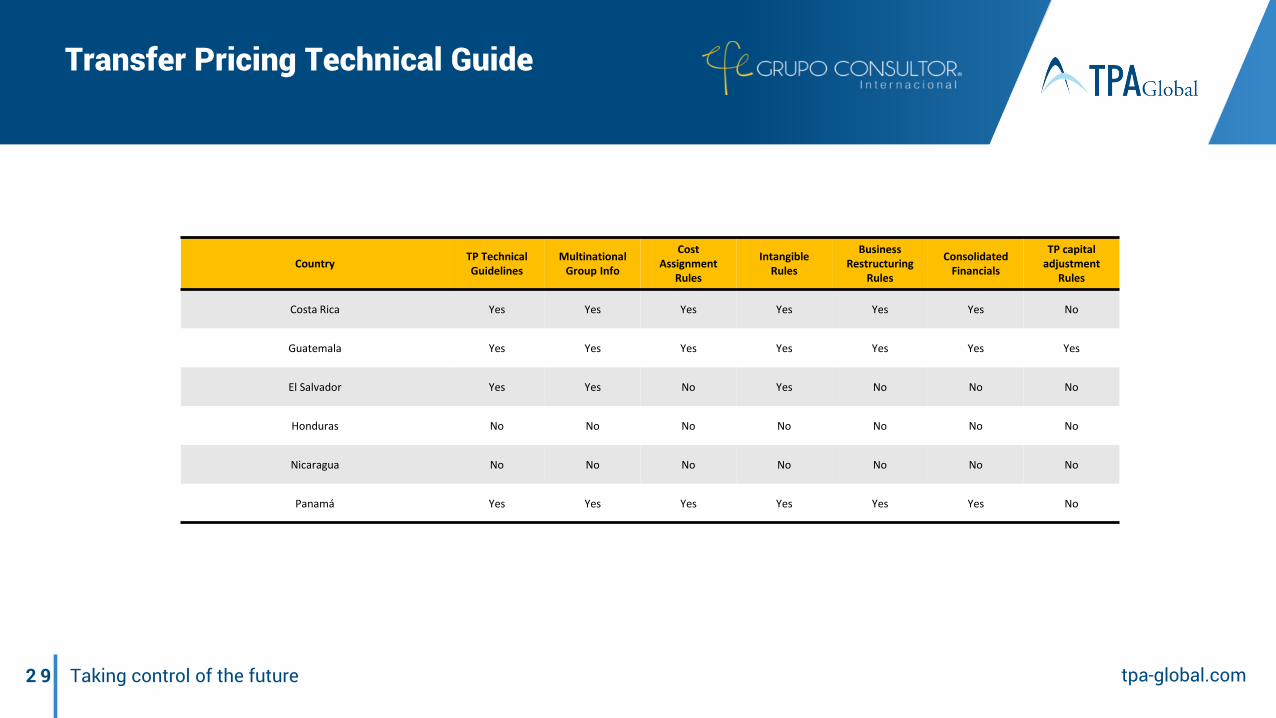

Transfer Pricing Technical Guide

CountryTP Technical Guidelines

Multinational Group Info

CostAssignment

Rules

Intangible Rules

BusinessRestructuring

Rules

Consolidated Financials

TP capitaladjustment

Rules

Costa Rica Yes Yes Yes Yes Yes Yes No

Guatemala Yes Yes Yes Yes Yes Yes Yes

El Salvador Yes Yes No Yes No No No

Honduras No No No No No No No

Nicaragua No No No No No No No

Panamá Yes Yes Yes Yes Yes Yes No

3 0 Taking control of the future tpa-global.com

¿Questions?

3 1 Taking control of the future tpa-global.com

Presenters

Belisa Severini Transfer Pricing Associates [email protected]+54 9 291 57098 79

Sonia Catalina Muñoz R.Transfer Pricing AssociatesNetherlands [email protected] +31 20 262 0022

Ramon LavaraLavara Transfer Pricing Consulting, S.C.Mexico+52 55 91 71 11 [email protected]

Francisco ArballoGrupo Consultor EFE™Mexico+52 (664) 634 [email protected]

www.tpa-global.com/latam

TPA Global introduces the TPA Global team for Latin America (“TPA LATAM team”) which specializes in the development andimplementation of LATAM Transfer Pricing systems to assist multinational enterprises (MNEs) operating in the region, toproactively and efficiently manage and implement their transfer pricing policies in a cost-effective, practical and swift manner;ensuring compliance with local transfer pricing legislation and BEPS regulations across LATAM.

TPA LATAM Team

3 3 Taking control of the future

TPA Global provides international businesses with integrated and value-addedsolutions in improving financial performance, operational efficiency, strategicdevelopment and talent coaching through a cross-border and cross-discipline teamof professionals which identifies the right solutions for customers and targets;efficient and streamlined advisory and implementation processes which cutthrough operational complexities across functions and borders; and superiorcustomer service and support which proactively anticipate the evolving needs ofthe clients.

H.J.E. Wenckebachweg 210 . 1096 AS Amsterdam . The Netherlands . +31 (0)20 462 3530 . tpa-global.com

The views expressed and the information provided in this material are of general nature andis not intended to address the circumstances of any particular individual or entity. The abovecontent should neither be regarded as comprehensive nor sufficient for making decisions.No one should act on the information or views provided in this publication withoutappropriate professional advise. It should be noted that no assurance is given for any lossarising from any actions taken or to be taken or not taken by anyone based on thispublication.

© 2017 Transfer Pricing Associates Holding B.V. All Rights Reserved.

tpa-global.com