implementation of auditor early-warnings pre going concern...

TRANSCRIPT

The Asymmetric Market Reaction of Stockholders and Bondholders to the

Implementation of Early-Warnings Pre Going Concern Opinion

Keren Bar-Hava

The Hebrew University of Jerusalem [email protected]

And

Roi Katz

The Hebrew University of Jerusalem [email protected]

Abstract

Auditing standards requiring auditors to issue going concern opinions (GCOs) have existed for several decades. The FASB exposure draft of June 2013 suggests early disclosures of uncertainties about an entity’s ability to continue as going concerns (GCUs). The FASB’s board argues that the proposed amendments would improve the timeliness and the quality of disclosures of going concern opinions. In Israel, since 2008, about 70% of the publicly traded companies implemented the two-phase models for going concern auditors’ opinions. We utilize a hand-collected dataset of 143 GCOs of publicly traded companies for the years 2007-2013. We examine the stockholders’ and bondholders’ asymmetric market reactions to GCOs preceded by early warnings of uncertainty (GCUs) compared to companies where the GCO disclosure tracks a “clean” opinion. The findings indicate that the equity and debt market reacts to GCUs in a negative and economically significant fashion. In addition, we find that GCUs reduce the negative market reaction to GCOs. This finding indicates that GCU announcements improve the timing and quality of the financial statement disclosure. Keywords: Going-concern Uncertainty; International Auditing Standards; International Auditing Practices; Audit opinions; Disclaimer of opinion; Financial condition; Short-term market reaction. JEL classification: M41, M42, G14, G24.

I. Introduction

Since the financial crisis in 2007-2008, the accounting discipline has reformed dramatically. In

order to improve financial statement disclosure standards, the going concern opinion (GCO)

became the focus of discussion of the relevant regulators. Just recently, after countless

discussions and suggestions for changes, the generally accepted accounting principles (GAAP)

concerning the GCO have stabilized. For example, in August 2014, the American FASB already

published an update regarding going concern conventions (the FASB's first draft of the issue was

published in October 2008).

The going concern assumption is the core of the accounting discipline. If this convention

is compromised, the usual accounting principles lose meaning and must change to suit the

situation of an entity that is about to cease to exist as a going concern. Accordingly, the two sets

of standards disciplines – the generally accepted accounting principles (GAAP) and the generally

accepted auditing standards (GAAS) – engage extensively with the issue in an attempt to create

standardization, which is the essence of the accounting discipline. Naïve questions are asked in

order to understand why there must be duplication when two separate regulatory systems, which

are written by regulatory bodies, differ, discuss and establish separate standards regarding the

going concern assumption. It is important to understand that while corporate management is

committed solely to the provisions of GAAP, the auditor must examine the proper existence of

those provisions that make the accounting rules, but this is through the application of generally

accepted auditing rules (GAAS).

Recently in the US, the FASB published an update of the accounting standard ASU 2014-

15 (August 2014). The process began in October 2008, and included several rounds of public

comments and drafts. In fact, from the time the standard update will be enforced in late 2016

(although firms may have voluntarily adopted the standard earlier), the GAAP in all Western

countries will lay the responsibility for evaluating the entity's ability to continue as a going

concern on the shoulders of management and not on the external auditor. Essentially, the

updating accounting standard issued by the FASB, is similar to international accounting standard

IAS 1 and the new Israeli standard 34, which came into force at the beginning of 2014. All of

these standards specify a set of requirements for the management of a company to deal with

substantial doubt about the existence of the going concern assumption. Actually, even after the

1

amendment's implementation we can still find differences between the American, International

and Israeli GAAP (mainly for the required examination period, where the American and Israeli

standards are satisfied with 12 months, while the International Standards consider 12 months to

be the minimum test period), but most of the parameters regarding this issue were created

uniformly.

Thus, we learn that the GAAP in the western markets, following the financial crisis,

determine that a firm's management should be responsible for evaluating the entity's ability to

continue as a going concern in the process of preparing the financial statements. Management's

responsibility is reflected in cases where the executives believe that there are significant doubts

about the appropriateness of the going concern assumption, therefore the management will attach

a detailed explanation regarding the financial statements that disclose in detail what the main

factors are behind the significant doubts about the appropriateness of the going concern

assumption. Last year, both the International Accounting Standards Board (IASB), and the

American counterpart (FASB), published guidelines that are supposed to create uniformity

regarding the circumstances that should bring a corporation's management to determine that there

is significant doubt about the appropriateness of the going concern assumption. In fact, according

to the accounting standard's update in the US (ASU 2014-15), the main role of management

responsibility is to anchor the issue and reduce the differences in content and timing of the note

that management must include in the financial statements. It should be noted that the US

Financial Accounting Standard Update (ASU 2014-15) was supposed to bring further reforms

that were rejected and were ruled out after public comments. Two major reforms were canceled:

the obligation to extend the period examined from 12 months to 24 months from the date of the

financial statements, and the proposal to add a GCU before significant doubt about the

appropriateness of the going concern assumption was not created. Ultimately, after public

comments, the last reform, which proposed early warning disclosure in a period of uncertainties,

was not approved by the FASB. Since the concept of the early warning disclosure reform was

implemented in the Israeli capital market starting in 2009, we examine this issue thoroughly in

our paper.

2

After discussing the GAAP-related going concern assumption, we must relate to the

generally accepted auditing standards (GAAS) of the western capital market in order to complete

the overall picture. Israeli audit standard number 58, which was implemented in 1994 (long

before the financial crisis of 2008), is analogous and almost identical in content to the US

standard, SAS 126. The standard states that the auditor should consider the risk of the validity of

the going concern assumption by examining warning signs that come to his attention from the

financial statements or other sources. In such cases, the auditor's duty is to consider whether the

warning signs point to considerable doubt as to the existence of a going concern assumption. If

the auditor comes to the conclusion that the going concern assumption is not appropriate in light

of the doubts that emerged on the issue, he should ensure that the management provide

disclosure in the financial statements, and he also needs to draw attention in his opinion (the

auditor's report), to that note given by the management. The international auditing standard issue

ISA 570 is very similar to the major demands expected of the auditor on this subject.

In this section, we shall discuss the GAAS that are the key to understanding the two-stage

model implemented in Israel, and thus provide the missing piece of the puzzle of the auditing

standard relating to the issue of the going concern assumption. The Israeli auditing standard no.

72 is similar to the American standard SAS 122, which requires the auditor to direct the financial

statement user's attention, through an “emphasis of matter paragraph” that stating the auditor's

opinion and refers the reader to the notes or data written by management in the financial

statements, which he finds necessary to emphasize. The American standard requires diverting

attention to the following specific situations, which are shown as examples in the Standard: (1)

an expectation of significant regulatory change; (2) when a significant catastrophe exists or is

expected, which will affect the entity’s financial position; (3) significant transactions with

affiliates; (4) significant and unusual events after the balance sheet date. In contrast, the Israeli

standard does not provide a list of examples, and specifies two types of situations in which we

divert attention when the resulting uncertainty may have a significant impact on the financial

statements: (1) a going concern qualification in accordance with the provisions of Standard 58,

which is discussed further in this paper; (2) uncertainty which constitutes a matter whose results

depend on future actions or events that are not directly under the entity’s control.

3

4

Thus, we see that the Israeli standard grades two types of emphasis of matter paragraphs

in the auditor's report concerning uncertainty. The more severe one will receive a GCO

according to a predefined wording in line with accounting standard no. 58. The wording of the

less severe type is not predefined and is subject to auditor’s judgment in line with accounting

standard 72.1 The 2008 financial crisis brought back the focus of regulators and financial

markets to the importance of the timing of such auditor’s notices. Many companies had their

auditors settle for the softer notice according to accounting standard 72, drafting their opinion as

a vague and non-decisive text. Consequently, the Israeli SEC has issued specific instructions

highlighting the differences between the two types of notice and the correct reasoning for

choosing one over the other.

Nowadays, based on several Israeli SEC announcements on this subject, the best practice

applied to most public companies is a two-stage notice for uncertainties related to going concern

assumption. According to this practice, the auditor will first apply a notice according to

accounting principal no. 72, describing the financial or operational uncertainty as well as the

management’s proposed solutions (hereinafter GCU). At a second stage, and only if the business

activity continues to deteriorate, the auditor will apply a notice based on accounting standard No.

58 (hereinafter GCO). The Israeli SEC supports this two-stage model for application by public

companies.

The two-stage model applied in Israel provides a solution for the post-financial crisis era,

with the aim of informing financial markets in due time, allowing investors to make informed

decisions regarding potential debt restructuring or liquidation, as applicable. This being said, it

has not been proved that such a model increases the chances of recovery for a business that is

subject to operational or financial difficulties. In fact, there is ongoing debate as to whether

disclosing the business difficulties in due time outweighs the obvious risk that the same

disclosure of negative information about the company’s performance will actually push the

company towards an irreversible state, forcing investors to acknowledge equity losses.

1 In Appendix A, we present examples of both types of emphasis of matter paragraphs as explained above.

Our research is innovative in two respects. First, we examine the efficiency and

effectiveness of the two-stage model that includes early disclosures of uncertainties about an

entity’s ability to continue as a going concern (GCU) before providing a going concern opinion

(GCO). Second, we examine the immediate market reaction of bondholders, those stakeholders

who are the primary losers if the company ceases operations, to the GCO in general, and to the

two-stage model in particular. To our understanding, testing the immediate bond market reaction

is essential to complete the puzzle of the timing and quality of the two-stage model. Use of the

two-stage model is a conventional practice of the publicly traded companies' managements in

Israel and their auditors, and is encouraged by the Israeli SEC. The generally accepted auditing

standard in the US enables the auditor to draw attention to material matters, and thus, the model

can be implemented in the US as well without any change of regulation.

In the following sections, we will first present an explanation in section II of the statutory

requirement of management disclosure in Israel in addition to the two-stage model. In section III

we review relevant literature that focuses on the going concern opinion (GCO) and the

bondholders market reaction to accounting information. The hypotheses and methodology are

described in section IV; the empirical results are described in section V; and section VI

concludes our paper.

II. Statutory disclosure requirement for publicly traded companies that suffer from

financial instability

In this section, we describe different phases of disclosure of the Israeli financial statement

system that are used as warning signs. The two-stage model is in the auditor’s opinion, and the

other are solely the management's responsibility. We decided to describe all the warnings that

influence the stakeholders, including those that come from the management to convey all the

information that can be relevant for publicly traded companies suffering from financial

uncertainty.

5

Figure 1

Figure 1 below depicts the phases that are warning signs for the various stakeholders in

the company's financial statements, reflected in the financial reporting package, on both the

quarterly financial statements and the annual financial statements. We define "Warnings" as

those that are found in the Management Discussion and Analysis (MD&A). We define "PCF" as

the projected cash flow for the next two years that is mandatory and will be shown in the MD&A

in cases where the warnings include signs of liquidity problems. We define "GCU" as early

disclosures of uncertainties about the entity’s ability to continue as a going concern, and "GCO"

as a going concern opinion.

The first issue that should awaken a warning light in the heart of readers of the statements

is the determination by the company's board of directors in the MD&A that in spite of warning

signs in the company's financial statements, there is no liquidity problem and therefore a decision

to refrain from publishing a projected cash flow statement (PCF). This situation will occur, in

accordance with the new directives of the Israel Securities Authority, if and when there is a

deficit in working capital but inspections conducted by the board of directors show that there is

no liquidity problem. In this situation, although the board of directors is not required to publish a

projected cash flow statement (PCF), it must provide public disclosure of its inspections and

findings. This being the case, the user of the financial statements can and should view the

determination of the board of directors as a disturbing warning sign. Although there is no

liquidity problem in the business, financial warning signs have arisen for the first time.

6

The second phase is a statutory duty by virtue of Regulation 10(b)(14) of the Securities

Regulations (Periodic and Immediate Reports), 1970. To the best of our knowledge, Israel is the

only country in the world that requires companies undergoing difficulties to publish, as part of

the board of directors' report, forward looking information in the form of a projected cash flow

statement (PCF). As set forth in the regulation, a projected cash flow statement for two years

ahead is to be added when there are one or more of the following warning signs (in consolidation

or alone): a shareholder deficit; a deficit in working capital or in 12 months' working capital and

also an ongoing negative cash flow from operating activities; an emphasis of matter paragraph of

the auditor relating to the financial condition of the corporation (GCU); an emphasis of matter

paragraph of the auditor regarding significant doubts about the corporation's ability to continue

as a going concern (GCO); a deficit in working capital or in 12 months' working capital, or an

ongoing negative cash flow from operating activities, if the board of directors has not determined

that this is not an indication of a liquidity problem in the corporation.

This being the case, the disclosure required in Israel when there are significant warning

signs in the financial statements is exceptional. We cannot trivialize the regulation's requirement

for the company's Board of Directors to give positive and active confirmation that the expected

financial resources of the corporation will suffice to cover the future uses over the next two

years. The Board of Directors is responsible for examining the reasonability of the scope and the

timing of the resources and uses reported in the projected cash flow statement, which is

structured according to the guidelines of the cash flow statement, appearing as part of the

company's financial statement, i.e., with a division into cash flow from operating activities, from

financing activities and from investment activities.

This requirement for the Board of Directors, which relates to all the conceivable warning

signs (including some of the subsequent phases of the process that we will review, GCU and

GCO), as stated, does not exist as a binding regulation in other countries. For example, in the

United States, a projected cash flow statement is a voluntary statement. Wasley and Wu (2006)

showed that companies that decide to add a projected cash flow statement are companies that

believe that the report will improve the investors' reactions in the case of a higher than expected

loss and will lend credibility to a higher than expected profit. Moreover, it seems that the use of a

projected cash flow statement is more common in the American market among young companies

that wish to project credibility. In England, in October 2013, the FRC published a directive that

7

stresses the importance of voluntary publication of a projected cash flow statement for public

companies undergoing financial difficulties and for those that will want to raise additional debt

from investors.

In this case, we have seen that the two first phases are obligatory disclosure under the

responsibility of the company's Board of Directors, which is unique to the Israeli economy. The

third phase that should signal and constitute a warning sign to users of the financial statements is

an emphasis of matter paragraph that the auditor adds with regard to financial uncertainty that

afflicts the corporation (GCU). As can be seen according to the conditions that we described, a

GCU and GCO in the auditor's opinion will necessitate a PCF, but not every projected cash flow

will necessitate a deviation from the uniform version of the auditor's opinion. Since the findings

that we gathered illustrate that a PCF precedes the GCU by three quarters on average, there is no

doubt that this stage is distinguished from the others and should be addressed.

In accordance with our findings, the third phase – GCU, in which the accountant adds to

his opinion an emphasis of matter paragraph as to financial uncertainty, is also a phenomenon

unique to Israel. As stated above, in accordance with auditing standard 72, an emphasis of matter

paragraph is provided in situations where there is significant uncertainty with respect to the

condition of the corporation. The accepted practice in Israel since the financial crisis, with active

encouragement of the Securities Authority, has led to the fact that on average, based on empirical

data that we have gathered, a GCU appears four quarters before the addition of a GCO by the

auditor. It is important to note that in the United States the possibility of adding the

aforementioned stage to the financial reporting arrangement has recently been examined by the

FASB, but the proposal was rejected. Although in the United States the going concern notices

come too late by all accounts, the fear of adopting the preliminary stage, which stems from the

risk that the company will be drawn into distress prematurely, led to the idea being rejected. It

should be noted that numerous studies illustrate that a going concern notice in itself could lead to

a survival problem for the company, so that there is substance to the decision of the professional

entities in the United States (Carson et al., 2013).

8

Those with discerning eyes surely took note of an intriguing empirical finding. As stated,

on average three quarters elapse between PCF and GCU, and four quarters between GCU and

GCO. This means that on an average, between the initial publication of the cash flow statement

and the addition of a going concern notice to the financial statements, less than two years elapse,

only seven quarters. The significance of this figure is that within the period of time of the two-

year projected cash flow statement, the company's condition deteriorates and its accountants add

an emphasis of matter paragraph as to financial uncertainty, and subsequently a going concern

notice, which we will present below as the fourth phase.

In the fourth phase, the accountant adds to his opinion an emphasis of matter paragraph

with respect to significant concerns with regard to the appropriateness of the going concern

convention (GCO). The same "going concern notice", in market parlance, is defined in Israeli

auditing standard 58 and similarly also in the United States under U.S. auditing standard SAS

126 - as notice that is added by the auditor, according to his judgment, by way of an emphasis of

matter paragraph, when there are significant doubts with regard to the continued existence of the

audited entity as a going concern. In March 2012, the Israel Securities Authority published an

auditing enforcement decision regarding the going concern notice (AU-12-01), whereby in

certain cases the inspection should be extended for a period exceeding one year. The decision

precedentially establishes that the duration of the inspection is a function of the company’s

financial condition and is not necessarily limited to one year. This directive is relevant to what

we have said thus far, since if the company publishes a two-year projected cash flow statement

(PCF), it is reasonable to assume that it can predict a significant deterioration that requires the

addition of a going concern notice even if it involves an event that is expected to occur more than

an entire year later.

The fifth and last phase that is relevant to the matter at hand is liquidation, stay of

proceedings or debt restructuring. Not all companies that have reached the fourth phase and

published financial statements with a going concern notice will reach this stage, but the

probability is fairly high. The fifth phase is also reflected in the financial reporting package,

either by way of modification and adaptation of the auditor's opinion or by way of a note in the

financial statements. It should be noted that the company can in many cases continue to exist

even subsequent to the fifth phase. Here the economic aspect is already reflected, where by

attaching valuations, the companies may prove solvency despite the financial difficulties

9

afflicting them. As stated, the aim of the above article is to explain the accounting aspect, and

from the fifth phase on the jurists and the appraisers take the stage, whereas the auditors have no

more tools in their arsenals. In line with this, we will now advance to the third chapter, in which

a review of the literature relevant to this paper will be presented, while delving into the two core

subjects of the article: the going concern convention and the various effects of adding the going

concern notice to the financial statements; and the reactions of stakeholders who are not equity

holders of the company, but are only bondholders, to the publication of accounting information.

III. Literature Review

The accounting field focusing on GCOs attached to financial statements developed in the

beginning of the 1980s. Kida's (1980) research for example, based on a survey of auditors,

teaches that merely referring to the GCO in financial statements might bring a company to

financial distress. This may happen even though the company never had any actual problems

prior to the publication of the financial statements. Carson (2013) recently showed that the

percent of public companies in the United States that include GCOs in their financial statements

has risen from 9.82% in 2000 to 17.1% in 2010. His findings teach us that 60.1% of the

companies with GCOs reached insolvency, and only 15.7% of the companies with GCOs

survived. This data shows that there is a high probability that a GCO will indeed lead to a

survival problem. These studies, in addition to papers such as Vanstraelen's (2003), demonstrate

one of the known claims about GCOs, that it has a golem effect because of its self-fulfilling

prophecy.

Several researchers have examined the market's reaction to GCOs in the past. For

example, Chen and Church (1996) tested the relationship between the market's reaction to the

attachment of GCOs to financial statements and to the declaration of bankruptcy that arrived

later. In the framework of the research, they tested whether the publication of a GCO before the

declaration of bankruptcy reduces the market reaction because of publicly declaring bankruptcy.

The researchers found that a GCO does indeed provide useful information to the companies'

investors and creditors. The research concluded that a GCO reduces the surprise and conferment

that exists in the market at the time of the declaration of bankruptcy. It was found that at the time

of the declaration of bankruptcy, there is a difference in the rate of the excess return between

companies that received a GCO and those that didn’t receive a GCO prior to bankruptcy. In the

10

incidents where a GCO was published prior to the declaration of bankruptcy, the rate of negative

change in the price of corporate bonds was lower at the time of the declaration than when no

GCO was published. As stated, the explanation for this difference is that investors saw the GCO

that was published in the past as relevant to them, and therefore the information regarding

bankruptcy was not new to them and its publication caused only a moderate negative market

reaction. Similarly, Holder-Webb & Wilkins (2000) found that the market reaction at the time of

a company's bankruptcy declaration is more moderate for companies that received a GCO from

an auditing accountant than for companies that didn’t receive a GCO prior to declaring

bankruptcy. On the contrary, studies such as Al-Thuneibat et al., 2008, Dodd et al., 1984; Elliote,

1982; Herbohn et al., 2007; Ogneva, 2007; which tested the market reaction to GCOs, found that

there is a non-significant market reaction or none at all to GCO announcements.

Menon and Williams (2010) tested the contradictory results in the existing literature by

means of processing a large number of GCOs for the first time in a short period of time. They

found that the market reaction to a GCO is more negative when the company reports financial

problems, and even more so when there is a violation of covenants. In addition, the researchers

found that the more the institutional investors' holdings grow, the more negative the market

reaction, and their holdings decrease immediately after the appearance of a GCO.

As can be seen, the relevant research in the literature thus far focused on the influence of

GCOs on the stock market. We will add to the existing literature with an innovative test of the

two-phase model customary in Israel, and will examine it thoroughly in relation to the stock

market and to the bond market, which is unique in Israel as it is an active market with daily

returns. Before that, we will now turn to a short literature review about the reactions of

stakeholders who are not shareholders, but only bondholders, to the publication of financial data.

This follows the first part of the literature review focusing on the first core subject of this paper –

the influence of publishing GCUs and GCOs in financial statements.

Easton, Monahan and Vasvari (2009) recently conducted a study of the connection

between accounting data and the bond market yield. It is based on the notion that the structure of

the return on an investment in bonds is not linear, and therefore the profit potential from the good

performance of the issuing company is limited. Also, DeFond and Zhang (2009) find similar

results; they examine the reaction of the bond market to positive and negative public notices, and

show that, in relation to the stock market, the bond market is more sensitive with respect to

11

negative announcements and more skeptical with respect to positive announcements. This is due

to the limited upside inherent in the nature of bonds as an investment tool.

Studies published lately have begun to discuss the influence of the accounting

information upon bondholders. For example, Costello & Wittenberg-Moerman (2010) tested the

prices of bond contracts following faults found in internal auditing. Because these faults may

indicate a lack of credibility in the financial statements, the researchers tested their effect on

bond prices. The researchers found an increase in bond prices following internal auditing failure

as opposed to bonds purchased before the failure. This outcome implies that there is a connection

between the quality of the financial statements and the bond price. In a study recently published

about bondholders' reactions to financial data, Givoly et al. (2014), we learn that the significance

of financial data in the bondholders' view has not decreased over the years. On the contrary, the

researchers explain that examining the bondholders' reactions is indeed important, however it has

yet to be examined due to lack of daily commerce data with an emphasis on bond value and daily

trade volume in those bonds. Our intention is to fill this gap thanks to the uniqueness of the

Israeli corporate bond market, which is traded unprecedentedly in the main stock exchange, in

comparison to the western world, and not over the counter (OTC).

Our research tests specific components in company financial statements – the GCU and

the GCO. These components include negative information and therefore should affect

bondholders more than positive information. A recently published research by Chen et al. (2014)

deals with this aspect of the influence of GCOs on bondholders and bond contracts, but focuses

on private bonds and not public bonds. Their findings show that GCOs are relevant and valuable

as they increase the cost of debt.

Additional researchers that test the connection between bonds yields, accounting data and

financial data are Rosen and Zhou (2012), and Hotchkis and Rosen (2002). They find that the

content of the information in the financial statements on the day the statements are published is

reflected quickly in the bond prices, and that the standard of efficiency in implementing the

information for the corporate bond market is no less than as for the stock market. Furthermore,

Rosen and Zhou (2012) indicate that the reaction of the bond market to new information about

significant trading by institutional holders is quicker, upon publication of surprising financial

statements, in comparison to series traded among private investors.

12

Other studies describe the bond market’s reaction to a variety of macroeconomic news.

Those studies create a distinction between the types of bonds and the extent of the reaction to the

new information. The findings show that there is variance in the reaction of corporate bonds to

publications in accordance with bond characteristics, such as average duration, rating level

(investment or speculative rating), and the yield-to-maturity rate (Huang & Kong, 2005,

Kosturov & Stock, 2010).

IV. Methodology and Hypothesis

Our research is empirical and based on data collected manually about Israeli public

companies traded on the Tel-Aviv Stock Exchange in the years 2009-2013. These are companies

that issue stocks and/or bonds (see Table 1). We use the Maya TASE website, which publishes

all relevant public announcements and prices of publicly traded stocks and bonds. We describe

and explain our hypotheses below, one by one, and the methodology we used to test these

hypotheses.

H1a: Stock and bondholders react negatively and significantly to early disclosures of

uncertainties about an entity’s ability to continue as a going concern (GCU).

H1b: Stock and bondholders react negatively and significantly to disclosures of going

concern opinions about an entity’s ability to continue as a going concern (GCO).

We divided the first hypothesis into two parts, in order to test the two-stage model

implemented in Israel. We assume that the stock and bond market is efficient and that the market

reacts negatively to announcements with a negative impact on all the stakeholders. Our unique

dataset includes daily bond prices and thus enables the testing of the bondholders' immediate

reactions to uncertainties about the companies. Testing and understanding the debtholders'

reactions in an active market and not over the counter (OTC) is very important, since

bondholders become significant victims in situation of financial distress. We also test whether

and how stockholders and bondholders respond to the early warnings. We assume that the

immediate market reaction should be negative for all stakeholders.

13

The methodology that we use for the first hypothesis and as a basic tool for the

subsequent hypotheses is the market model. We examine abnormal returns (AR) in a window of

28 days (-22, +5) while the period of estimation is 200 days before the announcement. For

calculating returns, we look at the daily closing prices of stocks and bonds. We use the Tel-Aviv

100 index (TA-100, the index of the hundred largest stock companies traded on the TASE) as the

stock market portfolio; we define Rm as the return on the TA-100 for calculating abnormal stock

returns, and the Tel Bond 60 Index for calculating abnormal returns on the relevant bonds. We

examine the statistical significance of our empirical findings by using a one-tailed t-test. Below

is the equation we used to examine the excess return:

ARi,t = Ri,t – (αi + βi Rm,t)

ARi,t = Abnormal return for firm i at time t

Ri,t = Return for firm i at time t

H2: Auditors' opinions that include emphasis of matter paragraphs as to financial

uncertainty (GCU) are a significant indication of a corporation's instability and thus lead to

opinions that include going concern qualifications (GCO).

The objective of the second hypothesis is to examine the probability that the financial

uncertainties about the entity's ability to continue as a going concern, the GCU, would later lead

to significant doubt about the going concern assumption, the GCO. In fact, this hypothesis tests

the practice of implementing the two-phase model. Since there is no clear link between auditors'

opinions that include emphasis of matter paragraphs as to financial uncertainty and opinions of a

going concern qualification, then this is not a model of two integral stages. On the other hand, if

the relationship is perfect, then you can say with 100% complete probability that the first step

leads the second step; this is not actually a two-stage model but one stage that extends over a

specific time period, no more.

The methodology we chose to examine the second hypothesis is logistic regression. We

test how a GCU affects the chances of receiving a GCO. We add a control variable of the

industry for each firm. We divided the companies into six industries: high-tech, investment and

finance, oil and gas exploration, real estate, services, and commerce. Below is the logistic

regression equation:

14

GCO = Log [Pi/(1-Pi)]=

α + β 1 GCU+ β 2 INDUSTRY + ε

GCU – early disclosures of uncertainties about an entity’s ability to

continue as a going concern

INDUSTRY– six industries: high-tech, investment and finance, oil

and gas exploration, real estate, services, and commerce.

H3: Early disclosures of uncertainties about an entity’s ability to continue as a going

concern, GCU, moderate the stock and bond market reaction to going concern opinions, GCO.

The third hypothesis is that the GCU gives relevant information and thus serves as

reliable and timely information for investors. Accordingly, we believe that the shareholders and

bondholders will react moderately to a GCO when previously warned by GCU, in comparison to

a GCO that surfaced without preliminary audit information.

We use linear regression for testing the third hypothesis. We test the influence of GCU

cumulative abnormal return (CAR) on the GCO CAR. We add the above control variables:

projected cash flow (PCF), warnings on the MD&A (WARNINGS), auditor firm and industry.

Below is the linear regression equation that we use:

CAR(GCO)= α + β 1 CAR(GCU) + β 2 PCF +

β 3 WARNINGS + β 5 AUDITOR + β 6 INDUSTRY + ε

Dependent Variable – CAR (GCO) cumulative abnormal return (-22, +5) for a going concern opinion.

Explanatory variable – CAR (GCU) cumulative abnormal return (-22,+5) for uncertainty of a going concern.

Control Variables:

PCF – projected cash flow that management attached to the MD&A.

WARNINGS – warnings of management on the MD&A.

AUDITOR – identity of the auditing firm.

INDUSTRY –six industries: high-tech, investment and finance, oil and gas exploration, real estate, services,

and commerce.

15

V. Results

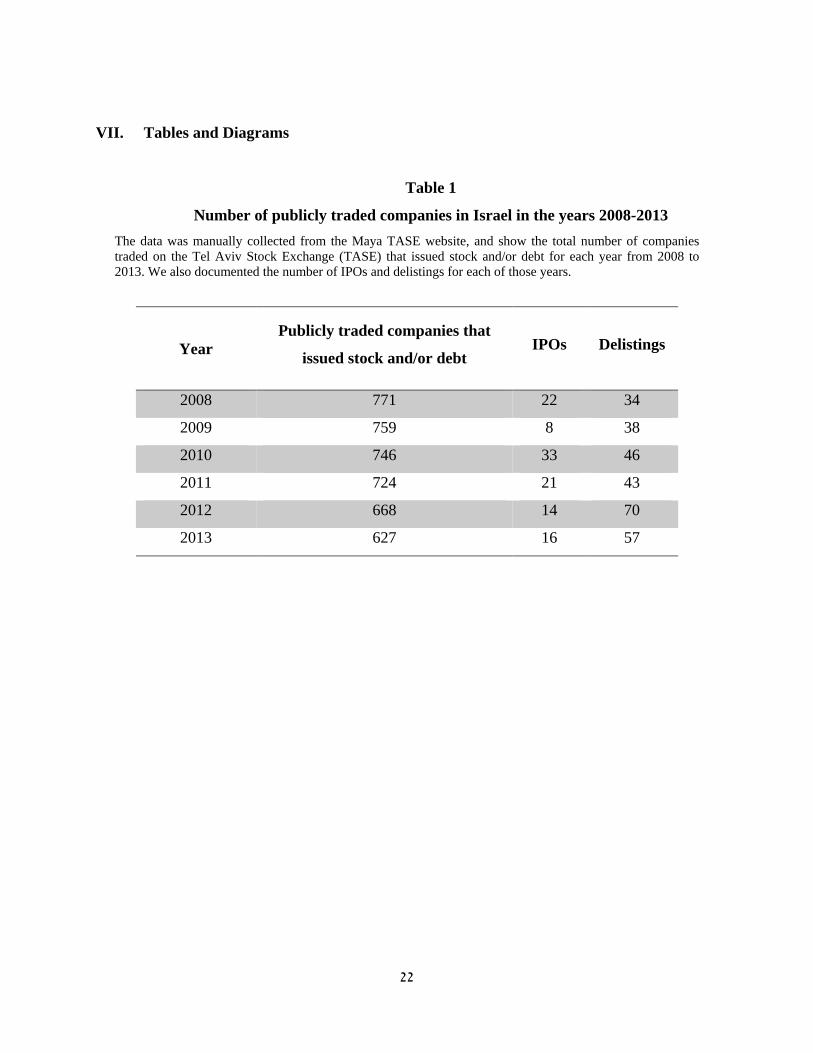

We began with a sample of all the public (stock and/or bond) companies in Israel traded

in the years 2008-2013 on the Tel-Aviv Stock Exchange (TASE). We also collected the prices of

all the relevant stock and bonds.

[Insert Table 1]

As concluded from Table No. 1, during the period with respect to which we gathered the

data in the post latest financial crisis in the years 2008-2013, the number of reporting

corporations that were traded on the Israeli stock exchange ranged from 627 to 771. The table

shows the progression of the number of corporations with marketable debt or equity on the Tel

Aviv Stock Exchange, while indicating the information with respect to the number of

corporations listed for trade and the number of corporations that were delisted. Listing for trade

is mainly possible following an initial public offering (IPO), whereas delisting can stem from

many reasons: merger of companies, tender offer of a controlling shareholder, bankruptcy,

liquidation, etc. It can be observed that as of the height of the crisis in 2008, there has been a

worrisome trend in the Israeli stock exchange of delisting, which can be attributed, inter alia,

both to the economic situation that adversely affected businesses and to the regulatory changes

that were introduced in Israel as lessons learned from the financial crisis.

[Insert Table 2]

As stated, one of the reasons for delisting companies is encountering financial difficulties

resulting from the financial crisis that has been sweeping the world in recent years. Indeed, as

can be concluded from Table No. 2, in 2008-2013 a GCU or GCO appeared in the financial

statements of roughly one fifth to one quarter of the corporations traded on the stock exchange in

Israel (the two-stage model practiced in Israel). It is interesting to discover that while the number

of companies to which the auditors attached a going concern notice was on the rise during those

years, the number of companies to which a GCU added was actually on the decline. This finding

can be viewed as confirmation of the assumption that there is an accepted practice in Israel of a

two-stage model in the auditor's work in this regard. Thus, companies to whose statements GCU

(first stage) had been added previously, have already "progressed" and published in the

subsequent years a GCO (second stage). In line with this, it can theoretically be argued that the

height of the crisis is behind us, as fewer and fewer companies enter the first stage, which, as we

16

will see further on, leads with fairly high probability to the second stage, which is a very

worrisome indication for all the stakeholders of the company – a going concern notice.

With respect to every reporting company in Israel, we examined whether and when it

published forward looking information in the board of directors' report in the form of a projected

cash flow (PCF) statement for two years ahead pursuant to the statutory requirement that was

presented in the previous chapters as the second phase in the process of a company entering

financial difficulties. Furthermore, we located the first auditor's report with respect to each

reporting company that contained a GCU (third phase above), as well as the first date when the

auditor attached a GCO (fourth phase) to the company's statements. Table No. 3 shows the

period in quarters between phases two, three and four.

[Insert Table 3]

As can be concluded from Table No. 3, on average three quarters elapse between the

initial publication of a PCF and the publication of a GCU, and four quarters between the initial

publication of a GCU and the initial publication of a GCO. This illustrates that while the cash

flow statement is supposed to constitute a forward looking statement by the company's board of

directors, as during the period of the next two years a cash flow problem is not anticipated, in

fact, within only seven quarters the financial condition of the company deteriorates to the extent

that its accountants add a going concern notice to its financial statements.

[Insert Table 4]

Table no. 4 empirically verifies our first hypothesis, whereby the holders of the share

capital and the bondholders react significantly negatively to the publication of a GCU and to the

publication of a GCO. It can be concluded from the table that the excess return in a time window

of 28 days (+5, -22) is indeed significantly negative statistically. It is interesting to see that the

reaction is negative in approximately the same degree to both parts of the two-stage model. The

holders of the share capital reacted -10.59% and -9.31% to the publication of a GCU and to the

addition of a GCO respectively; whereas the bondholders reacted -5.46% and -5.50%

respectively. It can be understood from these empirical findings that a GCU constitutes an

important signal and a serious warning sign in the eyes of the investors, both the equity holders

and the debt holders. Furthermore, it can be seen that the intensity of the shareholders' reaction is

stronger than that of the debt holders. We can cling to the crediting order in a limited company as

17

an explanation for this phenomenon, since the shareholders are last and therefore they have more

to lose in a bankruptcy situation than the bondholders.

[Insert Table 5]

As part of our attempt to deepen the examination of the shareholders' and bondholders'

reactions to the regulation reflected in the reporting package of public companies in times of

financial instability, we chose to also examine the identity of the auditor who added a GCO to

the financial statements of public companies in Israel during the years 2008-2013. As can be

concluded from Table No. 5, the Big Four firms were responsible for the publication of only

14.67% of the going concern notices during this period if we take into consideration their

average market share in Israel during those years. In other words, the rest of the firms, which are

not members of the four largest firms in the world, were the ones that audited most of the

companies (85.33%) for which going concern notices were added. Two different and perhaps

opposite conclusions can be drawn from this in our opinion. The first, that the major firms have

stricter quality control so that companies with a higher potential for financial instability are not

audited by them in the first place. The second, that the auditors of the major firms are less

reluctant to add going concern notices for the companies they audited, even when the economy is

in a slowdown that stems from a worldwide economic crisis.

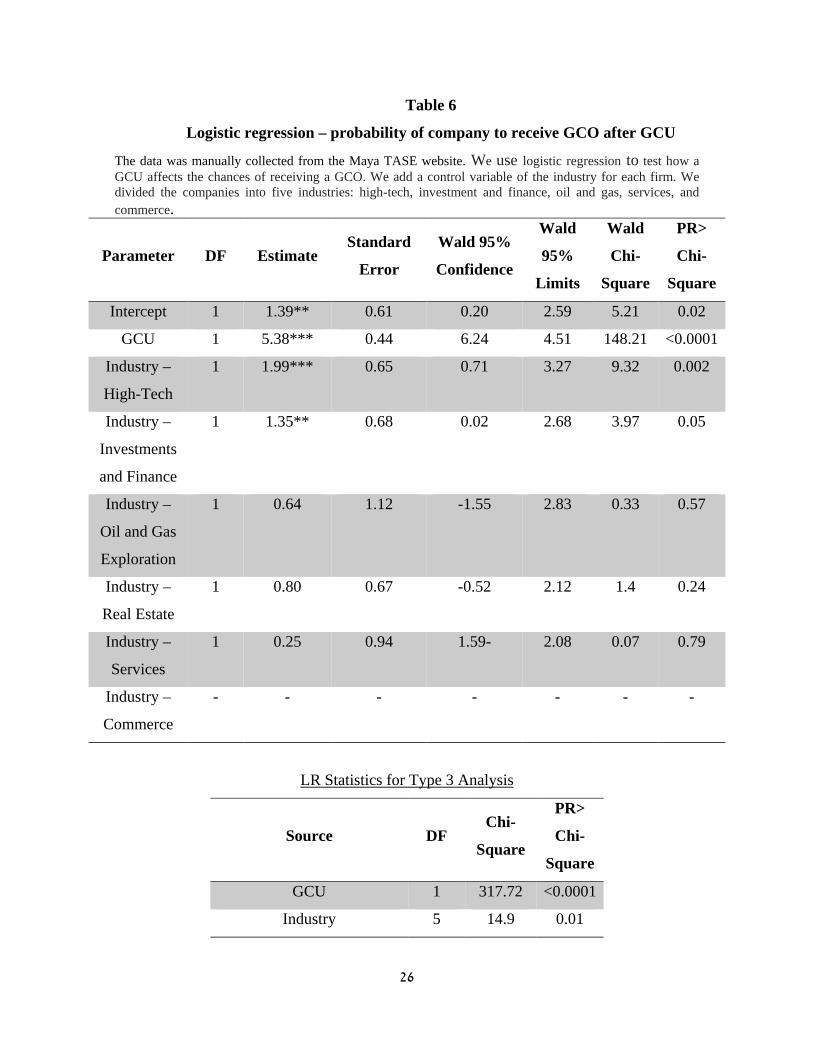

[Insert Table 6]

In accordance with the logistic regressive output data shown in Table No. 6 above, it can

be determined that our second hypothesis was correct and indeed the publication of a GCU

constitutes a significant indication of the corporation's instability and therefore clearly leads to

the publication of a GCO. It can be concluded from the table that this does indeed involve a two-

stage model, as on the one hand, not in every industry in the economy does the publication of a

GCU lead with high probability and clearly to the addition of a GCO by the auditor to the

financial statements; whereas on the other hand, we conclude that there clearly is an unequivocal

empirical relationship between both stages so that they are indeed dependent on one another.

[Insert Table 7]

Our third hypothesis, whereby the shareholders and the bondholders react significantly

more moderately to a GCO in cases when it was received after the publication of a GCU,

compared to situations in which GCU had not been published, was tested while distinguishing

between the excessive reaction of the holders of the share capital and the excessive reaction of

18

the bondholders. In Table No. 7 the linear regressive output data is shown, which indicates the

intensity of the excessive reaction of the holders of the share capital to receiving a GCO given a

number of different parameters. This includes previous publication of a GCU, previous

publication of a PCF, previous publication of warning signs at the company, the identity of the

auditor, and the industry with which the company is affiliated. As can be seen from the table, the

only variable found to have a significant effect on the reaction of the shareholders is the

company's affiliation with the service sector.

[Insert Table 8]

In Table No. 8 the linear regressive output is shown. It indicates the intensity of the

excessive reaction of the bondholders to receiving a GCO given a number of different parameters

which includes previous publication of a GCU, previous publication of a PCF, previous

publication of warning signs at the company, the identity of the auditor and the industry with

which the company is affiliated. We conclude from the table that the third hypothesis is valid

with respect to the stakeholders of the company who are not the holders of the share capital, but

the bondholders. The table illustrates that with very high significance, the previous publication of

a GCU affects the intensity of the bondholders' reaction to the addition of a GCO to the financial

statements of the company by its auditor. As can be seen, among all the variables that we tested,

only the publication of a GCU affects the reaction of the debt holders of the company. In our

opinion this demonstrates that the investors consider the first stage of the two-stage model to be a

meaningful signal that provides relevant, reliable and effective timely information from their

point of view.

19

VI. Conclusions

In this study, we examine the two-stage model of the auditor's opinion on the financial

statements for companies with financial stress, using the unique laboratory that is the Israeli

market. We also refer to management responsibility in cases of distress; the Israel Securities

Authority (ISA) imposes warnings and requires a projected cash flow in such cases. We examine

three hypotheses: First, the holders of the share capital and the bondholders react clearly

negatively to the publication of a GCU and the publication of a GCO. Second, that the

publication of GCU is a significant indication of a corporation's instability and thus clearly leads

to publication of a GCO. Third, that the holders of the share capital and the bondholders react

significantly more moderately to a GCO in cases when it was received after the publication of

GCU compared to situations in which GCU had not been published.

Our findings are based on data collected manually about public companies in Israel which

own share capital and/or negotiable bonds, and show that GCUs and GCOs jointly and separately

constitute very significant signals for company stakeholders, both shareholders and bondholders ,

who find such information to be relevant and reliable indications that a public company is in a

situation of financial instability that could end in liquidation, receivership, debt settlement or

bankruptcy.

We have seen that the two-stage model that is common practice in Israel, encouraged by the

Israel Securities Authority and relying on generally accepted auditing standards, is an important

regulatory tool for investors in the capital market in particular and stakeholders in general. These

are two distinct phases that are indeed likely to come one after the other, but they do not bind

each other. They enable the company's management, its board of directors and its auditors to

shed light, for the users of financial statements, on the financial instability afflicting the

company, which is highly likely, but not certain, to damage the going concern assumption.

20

As we have seen at the outset, the two-stage model that is reviewed and examined

empirically in this article can be manifested in the US capital market almost immediately. The

regulation reflected by the principles of accounting and auditing accepted in the United States

enables the auditor to attach GCU just like his Israeli counterpart. Yet the data show that the

Israeli regulator did well when he set statutory rules reflected in the reporting package of public

companies in times of financial instability. The Israeli capital market views the activity resulting

from the financial crisis that peaked in 2008 as a blessing that enhances the capital market,

solves market failures and helps alleviate the agency problem.

21

VII. Tables and Diagrams

Table 1

Number of publicly traded companies in Israel in the years 2008-2013 The data was manually collected from the Maya TASE website, and show the total number of companies traded on the Tel Aviv Stock Exchange (TASE) that issued stock and/or debt for each year from 2008 to 2013. We also documented the number of IPOs and delistings for each of those years.

Delistings

IPOs Publicly traded companies that

issued stock and/or debt Year

34 22 771 2008

38 8 759 2009

46 33 746 2010

43 21 724 2011

70 14 668 2012

57 16 627 2013

22

Table 2

Timeline of the two-stage model: going concern uncertainty (GCU) and going

concern opinion (GCO) in Israel in the years 2008-2013 The data was manually collected from the Maya TASE website, and show the total number of companies traded on the Tel Aviv Stock Exchange (TASE) issuing stock and/or debt that published financial statements including early-warning uncertainty opinions (GCU) and going concern opinions (GCO) for the years 2008-2013.

Total no. of GCU + GCO as a percentage of the publicly traded

companies in Table no. 1

GCU + GCO GCO GCU Year

20.75% 160 51 109 2008

20.42% 155 57 98 2009

22.52% 168 64 104 2010

20.72% 150 55 95 2011

26.80% 179 87 92 2012

26.95% 169 100 69 2013

23

Table 3

The gap between the first projected cash flow (PCF), the first early warning

uncertainty opinion (GCU) and the first going concern opinion (GCO) The data was manually collected from the Maya TASE website. We show the time elapsed (in quarters) between the initial publication of a projected cash flow (PCF) in the MD&A and the first GCU, and then between the first GCU and the first GCO.

No. of quarters

between GCU and

GCO

No. of quarters

between PCF and

GCU

No. of quarters

between Warnings

and PCF

4 3 2 Mean

2 1 2 Median

14 13 9 Maximum

110 54 12 No. of observations

Table 4

Market reaction to GCU and GCO The data from the financial reports of the publicly traded Israeli companies that issued stock and/or debt was manually collected from the Maya TASE website. The data show the number of early-warning uncertainty opinions (GCU) and going concern opinions (GCU) in the years 2008-2013. We also collected prices of the relevant stocks and bonds. We examine abnormal returns (AR) in a window of 28 days (-22, +5). The period of estimation is 200 days before the announcement; for calculating returns, we look at the daily closing prices of stocks and bonds. We use the Tel-Aviv 100 index (TA-100, the index of the hundred largest stock companies traded on the TASE) as the stock market portfolio; we define Rm as the return on the TA-100 for calculating abnormal stock returns, and the Tel Bond 60 Index for calculating abnormal returns on the relevant bonds. We examine the statistical significance of our empirical findings by using a one-tailed t-test. *, **, *** indicate significance at the levels of 10%, 5%, and 1% respectively.

Bond market reaction Stock market reaction

GCO GCU GCO GCU

-5.50*** -5.46*** -9.31*** -10.59*** CAR(-22,+5)

-1.89 -2.24 -6.45 -9.42 Median

15.64 13.57 28.03 24.33 Standard deviation

50 44 93 71 No. of observations

24

Table 5

Descriptive statistics of the accounting firm segments

We examine the identity of the auditor who added a GCO to the financial statements of public companies in Israel during the years 2008-2013.

Subdivision of

GCO

standardized to

market share

Subdivision

of GCO Name of Accounting Firm

%4.11 %24.12 Deloitte Touche Tomatsu

%8.15 %23.68 Ernst and Young

%1.48 %11.4 PriceWaterhouseCoopers

%0.93 %6.58 KPMG

%14.67 %65.78 Total share of the Big Four

%85.33 %34.22 Other

25

Table 6

Logistic regression – probability of company to receive GCO after GCU

The data was manually collected from the Maya TASE website. We use logistic regression to test how a GCU affects the chances of receiving a GCO. We add a control variable of the industry for each firm. We divided the companies into five industries: high-tech, investment and finance, oil and gas, services, and commerce.

PR>

Chi-

Square

Wald

Chi-

Square

Wald

95%

Limits

Wald 95%

Confidence

Standard

Error Estimate DF Parameter

0.02 5.21 2.59 0.20 0.61 1.39** 1 Intercept

0.0001< 148.21 4.51 6.24 0.44 5.38*** 1 GCU

0.002 9.32 3.27 0.71 0.65 1.99*** 1 Industry –

High-Tech

0.05 3.97 2.68 0.02 0.68 1.35** 1 Industry –

Investments

and Finance

0.57 0.33 2.83 -1.55 1.12 0.64 1 Industry –

Oil and Gas

Exploration

0.24 1.4 2.12 -0.52 0.67 0.80 1 Industry –

Real Estate

0.79 0.07 2.08 -1.59 0.94 0.25 1 Industry –

Services

- - - - - - - Industry –

Commerce

LR Statistics for Type 3 Analysis

PR>

Chi-

Square

Chi-

Square DF Source

0.0001< 317.72 1 GCU

0.01 14.9 5 Industry

26

Table 7

Linear regression – Stockholders' excess return to going concern opinion (GCO) The data was manually collected from the Maya TASE website. The linear regression equation that we use is as follows:

CAR(GCO)= α + β 1 CAR(GCU) + β 2 PCF+ β 3 WARNINGS +

β 4 AUDITOR + β 5 INDUSTRY + ε

Dependent Variable – CAR (GCO) cumulative abnormal return

(-22,+5) for a going concern opinion.

Explanatory variable – CAR (GCU) cumulative abnormal return (-22,+5) for uncertainty of a

going concern.

Control Variables:

GCU – uncertainties about an entity’s ability to continue as a going concern

PCF – projected cash flow that management attached to the MD&A

WARNINGS – warnings of management on the MD&A

AUDITOR – identity of the auditing firm.

INDUSTRY - high-tech, investment and finance, oil and gas, real estate, services, and

commerce.

PR>|T| T

Value

Standard

Error Estimate Parameter

0.37 -0.91 16.26 -14.73 Intercept

0.15 -1.44 7.11 10.26- GCU

0.38 0.89 7.91 7.03 PCF

0.59 -0.55 11.52 6.29- WARNINGS

0.91 0.11 6.46 0.73 AUDITOR

0.50 0.68 12.63 8.62 Industry – High-Tech

0.35 0.93 12.67 11.83 Industry – Investments and

Finance

0.92 -0.10 18.16 1.73- Industry – Oil and gas

exploration

0.97 0.04 13.57 0.57 Industry – Real Estate

0.03 2.22 18.23 40.50** Industry – Services

- - - - Industry –Commerce

27

LR Statistics for Type 3 Analysis

PR>F F Value Mean-

Square DF Source

0.15 2.08 1600.19 1 GCU

0.38 0.79 606.00 1 PCF

0.59 0.30 229.01 1 WARNINGS

0.91 0.01 9.94 1 AUDITOR

0.16 1.62 1243.86 5 Industry

Table 8

Linear regression – bondholders' excess return to going concern opinion (GCO) The data was collected manually from the Maya TASE website. The linear regression equation that we use is as follows:

CAR(GCO)= α + β 1 CAR(GCU) + β 2 PCF+ β 3 WARNINGS +

β 4 AUDITOR + β 5 INDUSTRY + ε

Dependent Variable – CAR (GCO): cumulative abnormal return (-22,+5) for a going

concern opinion.

Explanatory variable – CAR (GCU): cumulative abnormal return (-22,+5) for uncertainty

about an entity’s ability to continue as a going concern.

Control Variables:

GCU – uncertainties about an entity’s ability to continue as a going concern

PCF – projected cash flow that management attached to the MD&A

WARNINGS – warnings of management on the MD&A

AUDITOR – identity of the auditing firm.

INDUSTRY - high-tech, investment and finance, oil and gas exploration, real estate, services,

and commerce.

28

PR>|T| T

Value

Standard

Error Estimate Parameter

0.61 -0.51 14.42 -7.37 Intercept

0.02 2.35 9.03 21.24** GCU

0.26 1.13 6.32 7.15 PCF

0.81 -0.25 7.93 -1.95 WARNINGS

0.60 -0.52 6.40 -3.34 AUDITOR

0.68 -0.41 13.92 -5.71 Industry – High-Tech

0.79 -0.27 13.06 -3.53 Industry – Investments and

Finance

0.55 0.61 11.77 7.18 Industry – Real Estate

0.74 -0.34 15.75 5.34- Industry – Services

- - - - Industry – Industry and

Commerce

LR Statistics for Type 3 Analysis

PR>F F Value Mean-

Square DF Source

0.02 5.53 2510.99 1 GCU

0.26 1.28 581.81 1 PCF

0.81 0.06 27.32 1 WARNINGS

0.60 0.27 123.62 1 AUDITOR

0.48 0.89 402.12 4 Industry

29

VIII. Bibliography

Al-Thuneibat, A., Khamees, B. A. and Al-Fayoumi, N. A., 2008, "The Effect of

Qualified Auditors’ Opinions on Share Prices: Evidence from Jordan." Managerial Auditing

Journal, 23 (1), pp. 84-101.

Behn, B., Kaplan, S. and Krumwiede, K., 2001, “Further Evidence on the Auditor’s Going-

Concern Report: The Influence of Management Plans.” Auditing: A Journal of Practice &

Theory, 20, pp. 13-28.

Bryan, D., Tiras, S. and Weatley, C, 2005, "Do Going Concern Opinions Serve as Early

Warnings of Financial Collapse?"

Chan, Li, 2009, "Does Client Importance Affect Auditor Independence at the Office Level?

Empirical Evidence from Going-Concern Opinions." Contemporary Accounting Research, 26

(1), pp. 201-230.

Chen, K. and Church, B., 1996, “Going Concern Opinions and the Market’s Reaction to

Bankruptcy filings”, The Accounting Review, 71 (1), pp. 117-128.

Dodd, P., Dopuch, N., Holthausen, R., and Leftwich, R., 1984, "Qualified Audit Opinions

and Stock Prices: Information Content, Announcement Dates, and Concurrent Disclosures."

Journal of Accounting and Economics, 6, pp. 3-38.

Datta, S., & Dhillon, U.S., 1993, “Bond and Stock Market Response to Unexpected

Earnings Announcements”. Journal of Financial and Quantitative Analysis, 28, pp. 565-577.

DeFond, M. and Zhang, J., 2009, “The Asymmetric Magnitude and Timeliness of the

Bond Market Reaction to Earnings Surprises”. Working Paper, University of Southern

California.

Easton, P. D., Monahan, S. J., and Vasvari, F. P., 2009, “Initial Evidence on the Role of

Accounting Earnings in the Bond Market”, Journal of Accounting Research, 47 (3), pp. 721-766.

Ehoff, C. and Gray, D., 2014, "Going Concern: Where is it Going?" Journal of Business

& Economics Research, 12 (2), pp. 121-124.

Elliott, J., 1982, “'Subject To' Audit Opinions and Abnormal Security Returns: Outcomes

and Ambiguities." Journal of Accounting Research, 20, pp. 617-638.

Freeman, R. E., 1984, Strategic management: A stakeholder approach, Pitman Press,

Boston.

30

Herbohn, K., Ragunathan, V., and Garsden, R., 2007, "The Horse has Bolted: Revisiting

the Market Reaction to Going-Concern Modifications of Audit Reports." Accounting and

Finance, 47, pp. 473-493.

Holder-Webb, L. and Wilkins, M., 2000, “The Incremental Information Content of SAS

No. 59 Going-Concern Opinions.” Journal of Accounting Research, 38, pp. 209-219.

Hotchkiss, E. S. and Ronen, T., 2002, “The Informational Efficiency of the Corporate

Bond Market: An Intraday Analysis”, Review of Financial Studies, 15, pp. 1325-1354.

Huang, J. Z. and Kong, W., 2005, “Macroeconomic News Announcements and Corporate

Bond Credit Spreads”. Working Paper, Penn State University.

Kosturov, N. and Stock, D., 2010, “The Sensitivity of Corporate Bond Volatility to

Macroeconomic Announcements”. In Lee, C., Lee, A. C., and Lee, J. (Eds.) Handbook of

Quantitative Finance and Risk Management, Springer US Publishers, pp. 883-913.

Menon, K. and Schwartz, K. 1987, “An Empirical Investigation of Audit Qualification

Decisions in the Presence of Going-Concern Uncertainties.” Contemporary Accounting Research

3, pp. 302-315.

Menon, K. and Williams, D., 2010, "Investor Reaction to Going Concern Audit Reports."

The Accounting Review, 85 (6), pp. 2075-2105.

Ogneva, M., 2007. "Does the Stock Market Underreact to Going Concern opinions?

Evidence from the U.S. and Australia." Journal of Accounting and Economics, 43 (2/3), pp. 439-

452.

Radin, A. and Katowitz, M., 2013, "Should Auditors opine on going concern?" The CPA

Journal,(10), pp. 6-9.

Ronen, T., and Zhou, X., 2012, “Trade and Information in the Corporate Bond Market”,

Journal of Financial Markets, 6, pp. 61-103.

Vanstraelen, A., 2003, "Going-Concern Opinions, Auditor Switching, and the Self-

Fulfilling Prophecy Effect Examined in the Regulatory Context of Belgium." Journal of

Accounting, Auditing and Finance, 18 (2), pp. 231-253.

Wasley, C. and Wu, J. S., 2006, "Why do Managers Voluntarily Issue Cash Flow

Forecasts?" Journal of Accounting Research, 14 (2), pp. 589-429.

31

IX. Appendix A – Difference in phrasing between types of auditor's opinions

Phrasing of the auditor's opinion Auditing

standard

in Israel

The

essence

of the

commen

t

Example of the standard requirement:

Without qualifying our opinion, we draw attention to Note X in the financial

statements. The company has incurred losses amounting to $Y in the year ended

December 31 ABCD and has a working capital deficit of $X on that date. These

factors, together with other factors detailed in the above note, raise substantial

doubt about the Company's ability to continue as going concern. "The

management plans regarding these matters are described in Note X. The

financial statements do not include any adjustments to the values of assets and

liabilities and their classification, which may be necessary If the company will

not be able to continue operate as a going concern.

58 GCO

Example from a financial report published in 2013:

Without qualifying our opinion, we draw attention to the fact that in XX

(month) 2014 our company is scheduled to repay debt of Y million US dollars.

Repayment will be made from the Company's available cash balances, cash

arising from the repayment of loans to the company from certain investee

companies, from the realization of certain assets, and from raising cash against a

pledge of available assets pledged or raising capital. The successful realization

of the company plans is not a certainty, because it is not under its complete

control. However, management believes that the company can repay its

obligations as they come due in the foreseeable future.

72 GCU

32