implementation completion and results report (icr)...

TRANSCRIPT

Document of

The World Bank FOR OFFICIAL USE ONLY

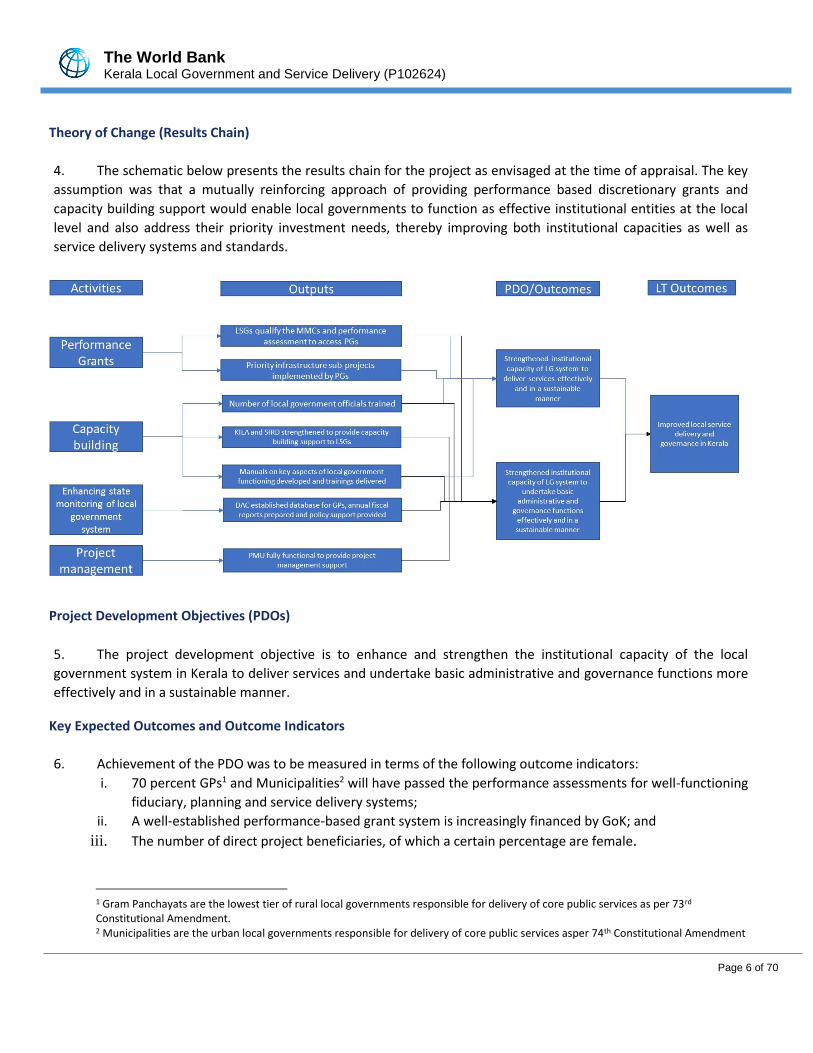

Report No: ICR00004319

IMPLEMENTATION COMPLETION AND RESULTS REPORT

ON A

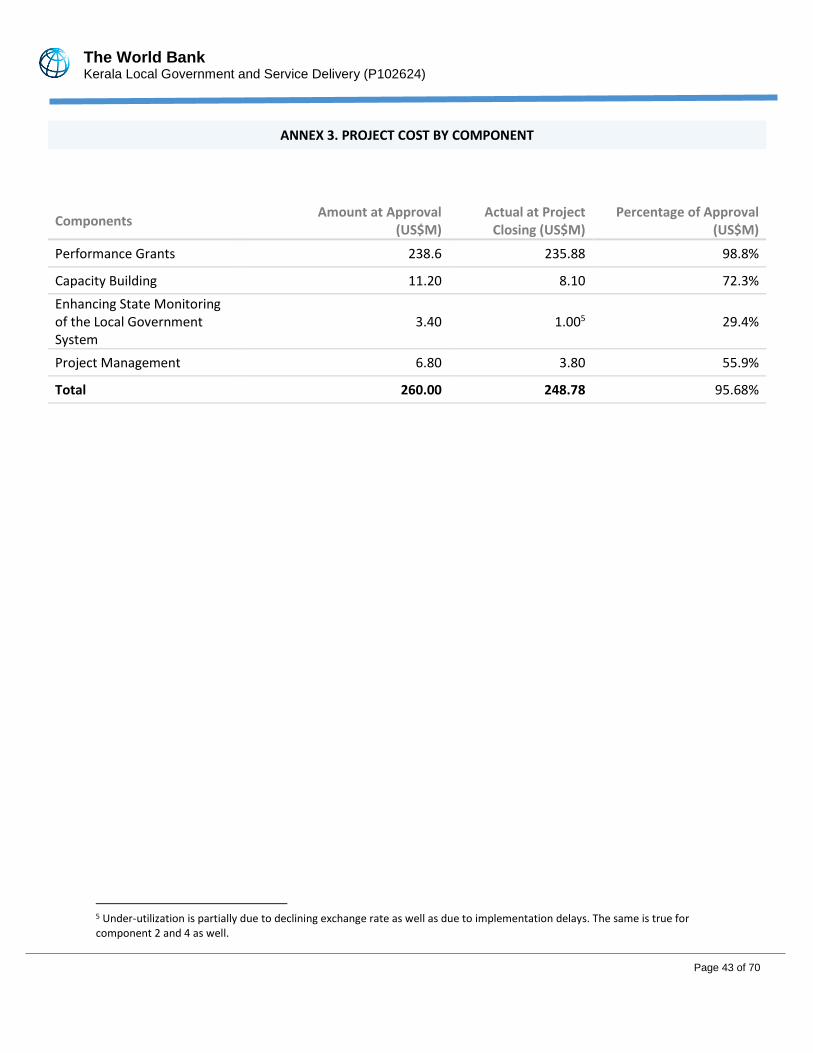

LOAN/CREDIT/GRANT

IN THE AMOUNT OF SDR 128.1 MILLION

(US$ 200 MILLION EQUIVALENT)

TO THE

REPUBLIC OF INDIA

FOR THE

KERALA LOCAL GOVERNMENT AND SERVICE DELIVERY PROJECT

June 19, 2018

Social, Urban, Rural and Resilience Global Practice

South Asia Region

Pub

lic D

iscl

osur

e A

utho

rized

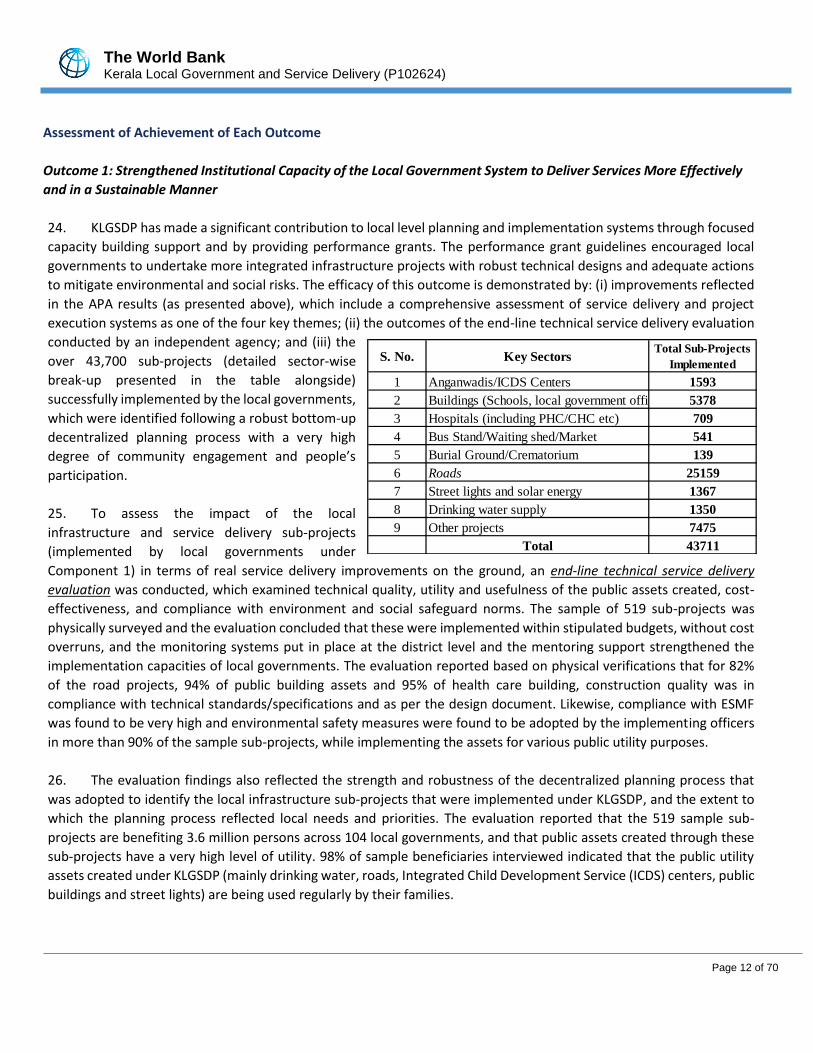

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

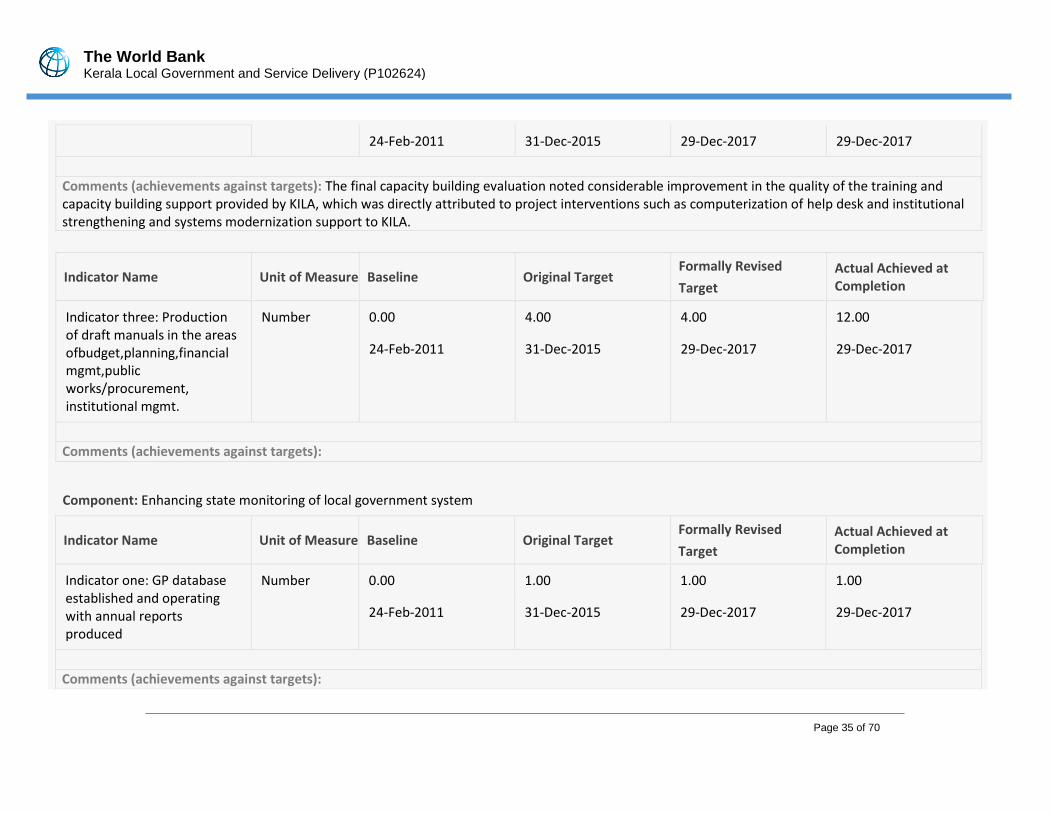

utho

rized

Pub

lic D

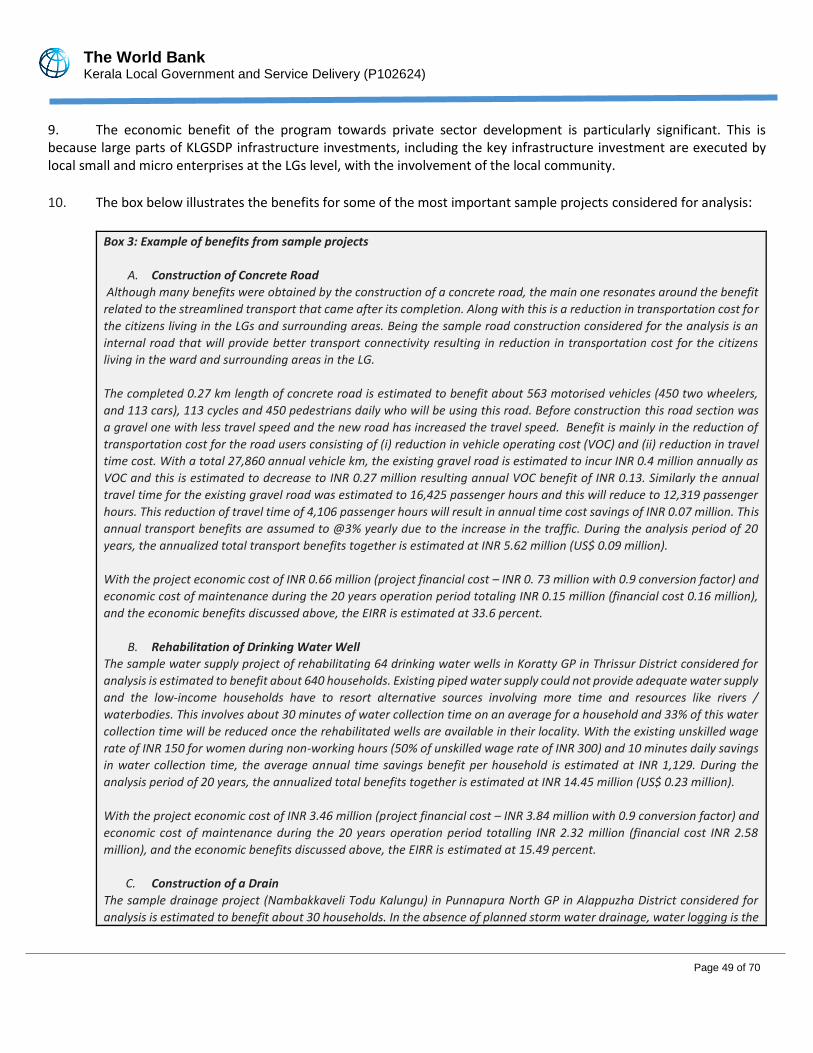

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective {June 15, 2018})

Currency Unit = Indian Rupee (INR)

INR 68.16 = US$1

US$ 1.41 = SDR 1

FISCAL YEAR

July 1 - June 30

Regional Vice President: Ethel Sennhauser

Country Director: Junaid Kamal Ahmad

Senior Global Practice Director: Ede Jorge Ijjasz-Vasquez

Practice Manager: Catalina Marulanda

Task Team Leader(s): Harsh Goyal

ICR Main Contributor: Harsh Goyal

APA Annual Performance Assessment

BTOR Back to Office Report

CAA Constitutional Amendment Act

CFC Central Finance Commission

CPS Country Partnership Strategy

DAC Decentralization Analysis Cell

DPR Detailed Project Report

EIRR Economic Internal Rate of Return

ESMF Environment and Social Management Framework

FFM Financial Management

GBV Gender Based Violence

GEWE Gender Equality and Women Empowerment

GIFT Gulati Institute of Finance and Taxation

GOI Government of India

GOK Government of Kerala

GP Gram Panchayat

ICDS Integrated Child Development Service

IDA International Development Association

IFR Interim Financial Report

IKM Information Kerala Mission

INR Indian Rupees

ISM Implementation Support Mission

IT Information Technology

IUFR Interim Unaudited Financial Report

KILA Kerala Institute of Local Administration

KLGSDP Kerala Local Government Service Delivery Project

LESA Limited Environment and Social Assessment

LFA Local Fund Audit

LG/LSGIs Local Governments/Local Self Government Institutions

LSGD Local Self Government Department

MIS Management Information System

MMC Minimum Mandatory Conditions

MTR Mid-Term Review

OP/BP Operational Policies/Business Procedures

PAD Project Appraisal Document

PDO Project Development Objective

PFM Public Financial Management

PG Performance Grant

PMU Project Management Unit

SCD Systematic Country Diagnostic

SC/ST Scheduled Caste/Scheduled Tribe

SDR Special Drawing Rights

SFC State Finance Commission

SIRD State Institute for Rural Development

SPAO State Performance Audit Office

TTL Task Team Leader

VGDF Vulnerable Group Development Framework

ABBREVIATIONS AND ACRONYMS

TABLE OF CONTENTS

DATA SHEET ....................................................................... ERROR! BOOKMARK NOT DEFINED.

I. PROJECT CONTEXT AND DEVELOPMENT OBJECTIVES ....................................................... 5

A. CONTEXT AT APPRAISAL .........................................................................................................5

B. SIGNIFICANT CHANGES DURING IMPLEMENTATION ................................................................8

II. OUTCOME ...................................................................................................................... 9

A. RELEVANCE OF PDOs ..............................................................................................................9

B. ACHIEVEMENT OF PDOs (EFFICACY) ...................................................................................... 10

C. EFFICIENCY ........................................................................................................................... 17

D. JUSTIFICATION OF OVERALL OUTCOME RATING .................................................................... 19

E. OTHER OUTCOMES AND IMPACTS (IF ANY) ............................................................................ 19

N/A .......................................................................................................................................... 20

III. KEY FACTORS THAT AFFECTED IMPLEMENTATION AND OUTCOME ................................ 20

A. KEY FACTORS DURING PREPARATION ................................................................................... 20

B. KEY FACTORS DURING IMPLEMENTATION ............................................................................. 21

IV. BANK PERFORMANCE, COMPLIANCE ISSUES, AND RISK TO DEVELOPMENT OUTCOME .. 23

A. QUALITY OF MONITORING AND EVALUATION (M&E) ............................................................ 23

B. ENVIRONMENTAL, SOCIAL, AND FIDUCIARY COMPLIANCE ..................................................... 24

C. BANK PERFORMANCE ........................................................................................................... 27

D. RISK TO DEVELOPMENT OUTCOME ....................................................................................... 29

V. LESSONS AND RECOMMENDATIONS ............................................................................. 29

ANNEX 1. RESULTS FRAMEWORK AND KEY OUTPUTS ........................................................... 31

ANNEX 2. BANK LENDING AND IMPLEMENTATION SUPPORT/SUPERVISION ......................... 41

ANNEX 3. PROJECT COST BY COMPONENT ........................................................................... 43

ANNEX 4. EFFICIENCY ANALYSIS ........................................................................................... 44

ANNEX 5. BORROWER’S COMMENTS ................................................................................... 54

ANNEX 6. SUMMARY OF BORROWER IMPLEMENTATION COMPLETION REPORT .................. 55

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 1 of 70

DATA SHEET

BASIC INFORMATION

Product Information

Project ID Project Name

P102624 Kerala Local Government and Service Delivery

Country Financing Instrument

India Investment Project Financing

Original EA Category Revised EA Category

Partial Assessment (B) Partial Assessment (B)

Organizations

Borrower Implementing Agency

Government of Kerala Local Self Government Department

Project Development Objective (PDO) Original PDO

To enhance and strengthen the institutional capacity of the local government system in Kerala to deliver services and undertake basic administrative and governance functions more effectively and in a sustainable manner.

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 2 of 70

FINANCING

Original Amount (US$) Revised Amount (US$) Actual Disbursed (US$)

World Bank Financing IDA-48720

200,000,000 192,775,692 169,987,288

Total 200,000,000 192,775,692 169,987,288

Non-World Bank Financing

Borrower 60,000,000 78,800,000 78,800,000

Total 60,000,000 78,800,000 78,800,000

Total Project Cost 260,000,000 271,575,692 248,787,288

KEY DATES

Approval Effectiveness MTR Review Original Closing Actual Closing

29-Mar-2011 16-Sep-2011 20-Jan-2014 31-Dec-2015 29-Dec-2017

RESTRUCTURING AND/OR ADDITIONAL FINANCING

Date(s) Amount Disbursed (US$M) Key Revisions

24-May-2017 182.83 Change in Results Framework Change in Components and Cost

02-Jun-2017 182.83 Change in Loan Closing Date(s)

KEY RATINGS

Outcome Bank Performance M&E Quality

Satisfactory Satisfactory Modest

RATINGS OF PROJECT PERFORMANCE IN ISRs

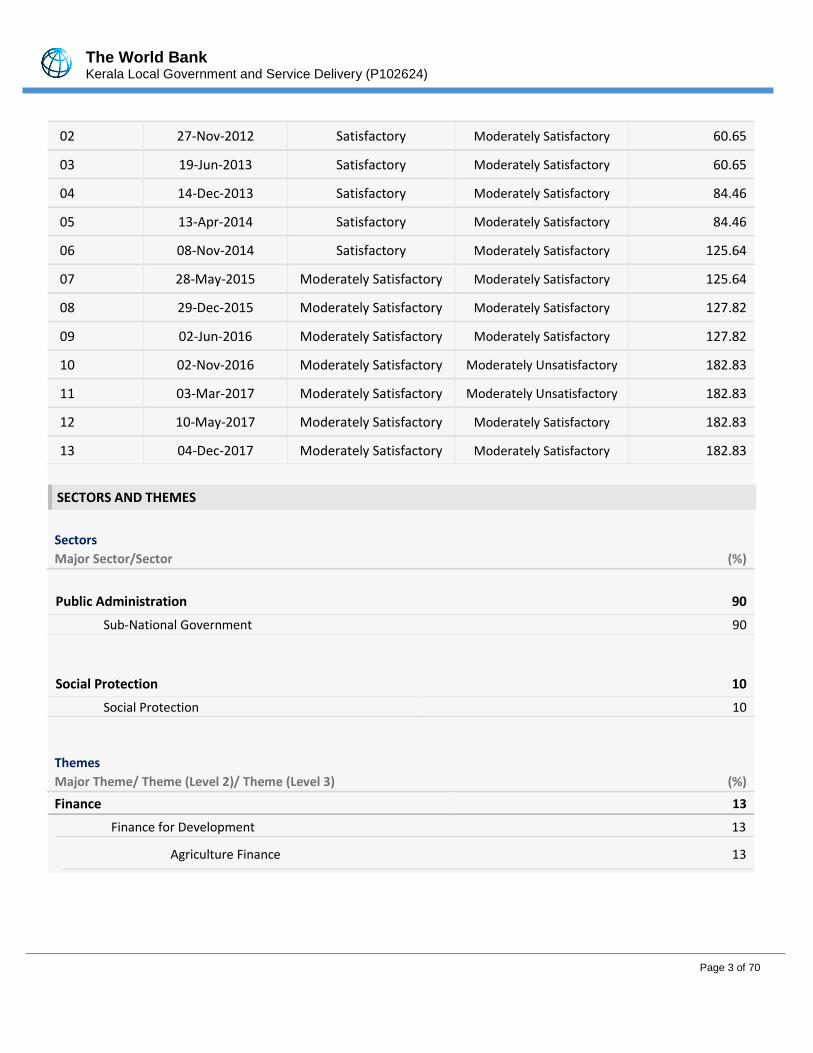

No. Date ISR Archived DO Rating IP Rating Actual

Disbursements (US$M)

01 03-Jan-2012 Satisfactory Satisfactory 29.02

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 3 of 70

02 27-Nov-2012 Satisfactory Moderately Satisfactory 60.65

03 19-Jun-2013 Satisfactory Moderately Satisfactory 60.65

04 14-Dec-2013 Satisfactory Moderately Satisfactory 84.46

05 13-Apr-2014 Satisfactory Moderately Satisfactory 84.46

06 08-Nov-2014 Satisfactory Moderately Satisfactory 125.64

07 28-May-2015 Moderately Satisfactory Moderately Satisfactory 125.64

08 29-Dec-2015 Moderately Satisfactory Moderately Satisfactory 127.82

09 02-Jun-2016 Moderately Satisfactory Moderately Satisfactory 127.82

10 02-Nov-2016 Moderately Satisfactory Moderately Unsatisfactory 182.83

11 03-Mar-2017 Moderately Satisfactory Moderately Unsatisfactory 182.83

12 10-May-2017 Moderately Satisfactory Moderately Satisfactory 182.83

13 04-Dec-2017 Moderately Satisfactory Moderately Satisfactory 182.83

SECTORS AND THEMES

Sectors

Major Sector/Sector (%)

Public Administration 90

Sub-National Government 90

Social Protection 10

Social Protection 10

Themes

Major Theme/ Theme (Level 2)/ Theme (Level 3) (%) Finance 13

Finance for Development 13

Agriculture Finance 13

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 4 of 70

Public Sector Management 63

Public Finance Management 7

Public Expenditure Management 7

Public Administration 56

Administrative and Civil Service Reform 7

Transparency, Accountability and Good Governance

7

Municipal Institution Building 42

Social Development and Protection 13

Social Inclusion 13

Participation and Civic Engagement 13

Urban and Rural Development 13

Rural Development 13

Rural Markets 13

ADM STAFF

Role At Approval At ICR

Regional Vice President: Isabel M. Guerrero Ethel Sennhauser

Country Director: N. Roberto Zagha Junaid Kamal Ahmad

Senior Global Practice Director: John Henry Stein Ede Jorge Ijjasz-Vasquez

Practice Manager: Ming Zhang Catalina Marulanda

Task Team Leader(s): Roland White Harsh Goyal

ICR Contributing Author: Harsh Goyal

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 5 of 70

I. PROJECT CONTEXT AND DEVELOPMENT OBJECTIVES

A. CONTEXT AT APPRAISAL 1. At the time of appraisal, India was on a high economic growth trajectory owing to its consistency in pursuing

economic reforms over the previous two decades. India’s high economic growth was accompanied by parallel

increases in spending on health, education, drinking water and sanitation, rural and urban infrastructure, and

employment programs. However, the progress on improving service delivery in rural and urban areas was limited.

Rural areas continued to lag in social and economic indicators as well as quality of services, with widening regional

disparities between and within states. Likewise, in urban areas, cities continued to struggle with inadequate levels of

basic urban services, coupled with the pressure of increasing pace of urbanization. Overall, at the local level service

delivery continued to remain poor and improvements were not commensurate with the levels of public expenditures.

2. The 73rd and 74th Constitutional Amendments established States as the constitutional entities with legal

jurisdiction over local government matters. India has since demonstrated a high level of heterogeneity with respect

to progress on decentralization; Kerala was a notable outlier within the country in this regard. Since the late 1990s,

Kerala devolved more responsibilities and resources to the lowest levels of local government, than any other Indian

state. On the fiscal side, the State has implemented the recommendations of successive State Finance Commissions

(SFCs) and at the time of appraisal, local government transfers constituted 20 percent of state tax revenue, with a

fixed annual increase. Moreover, in line with SFC recommendations, Kerala introduced an objective, formula-based

approach to the horizontal distribution of SFC transfers between local governments, which other Indian states were

yet to do. However, despite the impressive track record of the state in decentralization, there were many core

challenges with respect to limited expenditure autonomy, weak institutional and organizational capacities, and

inadequate state management and oversight mechanisms. Addressing these core challenges was a critical priority for

the state of Kerala to enable local governments to be adequately empowered, resourced and capacitated to deliver

services in a sustainable and accountable manner within a strong and robust state level oversight and management

framework. The Kerala Local Government and Service Delivery Project (KLGSDP) was designed to address the above

identified core challenges with the ultimate objective of strengthening the local government system for effective

service delivery.

3. The project was well aligned with the Government of India’s Eleventh Five-Year Plan (2007-12), which clearly

laid out strengthening decentralization and empowering local governments for local service delivery as a key priority

for improving governance. It was also aligned with Kerala state’s Eleventh Five-Year Plan (2007-12), which allocated

24.5% of its total plan outlay for decentralized planning and service delivery by local governments. By supporting local

infrastructure and service delivery needs, as well as the institutional arrangements for promoting an enabling

environment for long term sustainability, the project contributed directly to pillar three of the World Bank Group’s

India Country Partnership Strategy for 2009-12, which focused on increasing the effectiveness of public service

delivery. This project was one of four Bank supported local government projects (two were already under

implementation in Karnataka and West Bengal and the third was under preparation in Bihar) in diverse state

environments.

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 6 of 70

Theory of Change (Results Chain)

4. The schematic below presents the results chain for the project as envisaged at the time of appraisal. The key

assumption was that a mutually reinforcing approach of providing performance based discretionary grants and

capacity building support would enable local governments to function as effective institutional entities at the local

level and also address their priority investment needs, thereby improving both institutional capacities as well as

service delivery systems and standards.

Project Development Objectives (PDOs)

5. The project development objective is to enhance and strengthen the institutional capacity of the local

government system in Kerala to deliver services and undertake basic administrative and governance functions more

effectively and in a sustainable manner.

Key Expected Outcomes and Outcome Indicators

6. Achievement of the PDO was to be measured in terms of the following outcome indicators:

i. 70 percent GPs1 and Municipalities2 will have passed the performance assessments for well-functioning

fiduciary, planning and service delivery systems;

ii. A well-established performance-based grant system is increasingly financed by GoK; and

iii. The number of direct project beneficiaries, of which a certain percentage are female.

1 Gram Panchayats are the lowest tier of rural local governments responsible for delivery of core public services as per 73rd Constitutional Amendment. 2 Municipalities are the urban local governments responsible for delivery of core public services asper 74th Constitutional Amendment

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 7 of 70

Components

7. The project had four components with an estimated cost equivalent to US$260 million, briefly described below.

8. Component 1: Performance Grants (US$238.6 million - IDA and Government of Kerala, GoK). This component

provided an annual, performance-based grant to all 978 GPs and 60 Municipalities (collectively referred to as ‘local

governments’) in Kerala. The local governments were allocated additional formula-driven discretionary funds for local

infrastructure investments in a manner which incentivized the strengthening of their institutional capacity. The

performance grants (PGs) were spent both on the creation of capital assets used in service delivery and for their

maintenance and operation. The PG was introduced in two phases for strengthening the institutional capacities of

local governments incrementally. The administrative and institutional systems necessary for the introduction of a full

performance grant were established in the first two years of the project (Phase 1). From year three onwards, the

performance dimension of the grant, where qualification to receive grant is based on annual performance assessment,

was applied (Phase 2).

9. Component 2: Capacity Building (US$11.2 million – IDA). This component provided capacity building inputs to

strengthen and supplement the existing systems and human resources of local governments to enhance their

institutional performance through: (i) development of training manuals on key aspects of local government

functioning and imparting formal training to local government officials; (ii) on the job mentoring support to local

governments for human resource capacity improvement and supplementation; and (iii) strengthening the institutional

capacities and training delivery systems of the key organizations responsible for providing capacity building support

to local governments in Kerala (Kerala Institute of Local Administration, KILA, and the State Institute of Rural

Development, SIRD).

10. Component 3: Enhancing State Monitoring of the Local Government System (US$3.4 million - IDA). This

component supported the strengthening of the state’s performance monitoring systems for Local Self Governments

(LSGs) in Kerala, and comprised four sub-components:

(a) Database of GP and municipal information. The project established a database of GP and municipal level

information comprising basic data on GP and municipal profiles: population, vital statistics, livelihoods, employment,

education, water and sanitation, budget expenditures and physical assets.

(b) LSG Service Delivery Survey. This sub-component funded the surveys to gauge delivery trends state-wide in sectors

where GPs and Municipalities have some responsibility, explored citizen satisfaction, and usage of basic services, as

well as awareness of GP planning and budget processes.

(c) Project Evaluations. The project supported evaluations on (i) the quality of capacity building efforts (Component 2)

and service delivery of Performance Grant investments (Component 1).

(d) Decentralization Analysis Cell (DAC). The DAC focused on collecting, storing, compiling and reporting

GP/Municipality level and service delivery data; and (ii) providing policy advisory inputs based on an independent

analysis of the state ‘s intergovernmental fiscal system and service delivery system.

11. Component 4: Project Management (US$6.8 million - IDA). This component supported the Project Management

Unit (PMU) within the Local Self-Government Department (LSGD) for overall coordination, implementation,

monitoring and evaluation of the project.

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 8 of 70

B. SIGNIFICANT CHANGES DURING IMPLEMENTATION

Revised PDOs and Outcome Targets

N/A

Revised PDO Indicators

N/A

Revised Components

12. New activities added under Component 1. In 2014-15 the project had accrued savings of US$62 million as a

result of the depreciation of the Indian Rupee vis-à-vis the US dollar. These savings were utilized for: (i) a one-time

additional financial assistance to 50 backward and tribal Gram Panchayats and 10 revenue-deficit municipalities for

undertaking priority investment sub-projects focusing on service delivery improvement and local economic

development; and (ii) Annual Performance Assessment 3(APA) based Performance Grants to all local governments for

an additional year.

Other Changes

13. Extensions to Credit Closing Date. The original Credit closing date of December 31, 2015 was first extended by

18 months till June 30, 2017 to allow the Government of Kerala to complete the new activities indicated above. The

second extension for an additional six months till December 29, 2017 was to allow local governments to complete the

new activities in Component 1.

14. Credit Cancellation. IDA Credit equivalent to US$7.2 million was cancelled in May 2017 as these funds were

unlikely to be utilized before the Credit closing date.

Rationale for Changes and Their Implication on the Original Theory of Change

N/A

3 APA is the performance assessment tool adopted by GOK under KLGSDP to measure the performance of all the local governments every year.

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 9 of 70

II. OUTCOME

A. RELEVANCE OF PDOs

15. The relevance of the PDO should be assessed in the context of the decentralized service delivery framework

enshrined by the 73rd and 74th Constitutional Amendments (CAA) in the early 1990s and the importance of the agenda

to date. At the time of ICR preparation, the PDO is fully aligned with current national policies and the inter-

governmental fiscal framework that seeks to strengthen decentralization and federalism. The ongoing fourteenth

Central Finance Commission (14CFC, 2015-20) has recommended an unprecedented increase in tax devolution to

states from 32 percent to 42 percent of the sharable central tax, which is the largest increase in the history of Indian

fiscal federalism. In this context, the PDO is highly relevant in terms of showcasing the outcomes of a well-established

robust performance based inter-governmental fiscal transfer system for local governments, aimed at incentivizing the

institutional performance of local governments for improving service delivery standards and systems. The mutually

reinforcing approach of capacity building support and performance based transfers, that was adopted by the project

for achieving the desired objective of strengthening the local government system, demonstrates a huge potential for

a national scale-up and to influence the design of the entire inter-governmental fiscal transfer system for local

governments across the country in the upcoming fifteenth Central Finance Commission as well. The Government of

India is strongly supportive of this approach, as evidenced by the new performance based grant systems introduced

in 2017 for allocation of 10% of the total fiscal transfers under 14th CFC, as well as the GoI support for the follow-on

Bank project that has been requested by Kerala.

16. Kerala’s most recent five-year plan (2012-17) and the ongoing fifth State Finance Commission (2016-21)

highlight the importance attached to deepening decentralization by empowering the local governments and

strengthening their role, systems and capacities for efficient service delivery, both in terms of policy recommendations

as well as higher fiscal transfers to local governments. Hence the PDO remains fully aligned with, and is relevant to,

the state’s current vision of advancing the decentralization agenda and policy priorities. This is also evident from the

strong interest that the GOK has shown in requesting a follow-on engagement with the Bank to continue this

partnership for undertaking the next generation reforms to further strengthen local governments.

17. The PDO is aligned with the Bank Group’s current Country Partnership Strategy (CPS) for India for 2013-2017,

which called for three main engagement areas of “Integration, Transformation, and Inclusion”, as well as the

challenges and priorities identified by the India Systematic Country Diagnostics (SCD) 2018 for the new Country

Partnership Framework that is being prepared currently. The SCD recognizes the importance of empowering and

resourcing local governments adequately (as noted in page 33 of the SCD) for improving service delivery in a

decentralized set-up. It also recognizes that incentivizing local governments in a competitive federalism framework

can bring about a paradigm shift in their delivery of services (as noted in page 80 of the SCD). Going forward, the SCD

identifies strengthening local governments as a key priority for strengthening India’s federal compact and public

delivery systems.

Assessment of Relevance of PDOs and Rating

Rating: High

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 10 of 70

B. ACHIEVEMENT OF PDOs (EFFICACY)

18. The PDO is focused on strengthening two important and interrelated elements of local governance in an

effective and sustainable manner: capacity to deliver services and capacity to undertake basic administrative and

governance functions. Achievement of the PDO was measured through three PDO level results indicators: (i) by the

end of the project, 70% of the GPs and municipalities will have passed the annual performance assessments for well-

functioning fiduciary, planning and service delivery systems; (ii) a well-established performance based grant system is

increasingly financed by the Government of Kerala; and (iii) the number of direct project beneficiaries, of which a

certain percentage are female (core indicator).

19. Annual Performance Assessments (APAs). The APA is the primary tool used in KLGSDP as an objective, robust

and standardized mechanism to measure the performance of the GPs and municipalities in terms of their fiduciary,

planning, governance, and service delivery systems in a fair and transparent manner. The APA tool captures both

elements of the PDO (as described above) well by covering the key performance aspects of local government systems

through a combination of minimum mandatory conditions and performance benchmarks, and also serves as the basis

for the allocation of performance based grants to GPs and municipalities that qualified based on APA results.

Performance grants were allocated only to those local governments that met the mandatory conditions and achieved

a minimum performance score. Thus, they laid a solid foundation for a well-established performance grant system in

the state.

20. The APA was introduced in two phases. In the first phase (comprising years 1 and 2 of the project), all GPs and

municipalities received performance based grants subject to certain basic minimum mandatory conditions being met

that ensured that local governments will have in place the basic financial reporting systems, auditing procedures,

decentralized annual plans and budgets. In the second phase (years 3 to 5), the full APA was introduced, comprising a

set of mandatory conditions and performance benchmarks in four key aspects of local government functioning: (i)

decentralized planning and budgeting, that focused on ensuring timely preparation of annual decentralized plans and

budgets with adequate levels of community engagement and participation; (ii) project execution and service delivery,

that focused on basic systems for design, planning and implementation of local infrastructure projects that lead to

good quality asset creation and improve access to basic services; (iii) public financial management (PFM) and

accounting and auditing, that focused on detailed financial reporting and accounting practices, as well as timely

completion of external audits with no major qualifications/disclaimers; and (iv) transparency and accountability, that

focused on the local governments’ level of community engagement, grievance redress, and public disclosure norms.

Because of its comprehensiveness, the APA tool served as a reliable and authentic source of information for measuring

the achievement of the PDO through PDO level results indicators #1 and #2. However, the project faced some

challenges during the implementation of the APA, as noted in Section III. B. Key Factors During Implementation.

Achievement of PDO Level Indicator Targets

21. PDO Indicator 1: By end of project, 70% of the GP and municipalities will have passed the annual performance

assessments for well-functioning fiduciary, planning and service delivery systems – ACHIEVED. As shown in the graph

below, the number of GPs and municipalities that met all minimum mandatory conditions and scored above the

threshold qualifying marks in the performance scoring was consistently in the range of 85-90% and hence the project

consistently exceeded the annual targets of PDO indicator 1. The average performance scores of the GPs also showed

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 11 of 70

a positive trend over the three APA cycles and reflect a consistent improvement in local government functioning. This

improvement in the performance of local governments is principally due to the systems development and capacity

building support system that the project put in place during the first phase of the APA.

22. PDO Indicator 2: A well-established performance based grant system is increasingly financed by GoK –

ACHIEVED. The performance based grant system was

implemented based on the APA, wherein allocations were made to

qualified GPs and municipalities based on the SFC recommended

grant allocation formula, i.e., weighted by population size and area

of the local governments. The overall size of the annual

performance based grants increased over the project period from

US$3.3 million in FY11-12 to US$93 million in FY15-16. GoK’s

contribution increased from US$5.4 million in FY12-13 to US$37.4

million in FY15-16. At the end of the project, GoK resources

amounted to 31.5% of the performance based transfers disbursed

to the local governments in Kerala. The table below provides yearly details of IDA and GoK contributions.

23. PDO Indicator 3: The Number of Direct Project Beneficiaries, of which a Certain Percentage are Female -

ACHIEVED. Most of the local governments implemented multiple sub-projects (on average 40-50 sub-projects per local

government), which mostly focused on shared public infrastructure asset creation. As such, the beneficiary target of

29.54 million, of which 52% is women was achieved.

4 The cumulative number of beneficiaries for all the sub-projects exceeded the total population, and was reported by the Project to be about 43 million.

FY IDA Resources

(US$ million)

GoK Resources

(US$ million)

11-12 23.3 0.0

12-13 28.6 5.4

13-14 22.5 9.6

14-15 39.5 26.3

15-16 56.1 37.4

Total 169.9 78.8

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 12 of 70

Assessment of Achievement of Each Outcome

Outcome 1: Strengthened Institutional Capacity of the Local Government System to Deliver Services More Effectively

and in a Sustainable Manner

24. KLGSDP has made a significant contribution to local level planning and implementation systems through focused

capacity building support and by providing performance grants. The performance grant guidelines encouraged local

governments to undertake more integrated infrastructure projects with robust technical designs and adequate actions

to mitigate environmental and social risks. The efficacy of this outcome is demonstrated by: (i) improvements reflected

in the APA results (as presented above), which include a comprehensive assessment of service delivery and project

execution systems as one of the four key themes; (ii) the outcomes of the end-line technical service delivery evaluation

conducted by an independent agency; and (iii) the

over 43,700 sub-projects (detailed sector-wise

break-up presented in the table alongside)

successfully implemented by the local governments,

which were identified following a robust bottom-up

decentralized planning process with a very high

degree of community engagement and people’s

participation.

25. To assess the impact of the local

infrastructure and service delivery sub-projects

(implemented by local governments under

Component 1) in terms of real service delivery improvements on the ground, an end-line technical service delivery

evaluation was conducted, which examined technical quality, utility and usefulness of the public assets created, cost-

effectiveness, and compliance with environment and social safeguard norms. The sample of 519 sub-projects was

physically surveyed and the evaluation concluded that these were implemented within stipulated budgets, without cost

overruns, and the monitoring systems put in place at the district level and the mentoring support strengthened the

implementation capacities of local governments. The evaluation reported based on physical verifications that for 82%

of the road projects, 94% of public building assets and 95% of health care building, construction quality was in

compliance with technical standards/specifications and as per the design document. Likewise, compliance with ESMF

was found to be very high and environmental safety measures were found to be adopted by the implementing officers

in more than 90% of the sample sub-projects, while implementing the assets for various public utility purposes.

26. The evaluation findings also reflected the strength and robustness of the decentralized planning process that

was adopted to identify the local infrastructure sub-projects that were implemented under KLGSDP, and the extent to

which the planning process reflected local needs and priorities. The evaluation reported that the 519 sample sub-

projects are benefiting 3.6 million persons across 104 local governments, and that public assets created through these

sub-projects have a very high level of utility. 98% of sample beneficiaries interviewed indicated that the public utility

assets created under KLGSDP (mainly drinking water, roads, Integrated Child Development Service (ICDS) centers, public

buildings and street lights) are being used regularly by their families.

S. No. Key SectorsTotal Sub-Projects

Implemented

1 Anganwadis/ICDS Centers 1593

2 Buildings (Schools, local government offices, others)5378

3 Hospitals (including PHC/CHC etc) 709

4 Bus Stand/Waiting shed/Market 541

5 Burial Ground/Crematorium 139

6 Roads 25159

7 Street lights and solar energy 1367

8 Drinking water supply 1350

9 Other projects 7475

Total 43711

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 13 of 70

27. The end-line evaluation confirmed that the mutually reinforcing approach of providing focused capacity building

support for improving institutional systems and organizational capacities in local governments, coupled with an

objective, robust performance (APA) based fiscal transfer system led to significant systemic improvements in real terms

on the ground on service delivery aspects. The APA and the capacity building support also strengthened community

engagement and participation in the decentralized planning process in Kerala, with a particular focus on gender issues

and vulnerable/marginalized groups. (For further details on gender and vulnerable/marginalized groups, see Section E.)

The decentralized planning and implementation mechanism generated strong community ownership for

implementation and maintenance of local infrastructure assets and is one of the key sustainability measures supported

under the project.

28. A mutually reinforcing approach of APA based performance grant allocation and the focused capacity building

support led to substantial improvements in service delivery systems in the local governments. Capacity building support

provided by Kerala Institute of Local Administration (KILA), State Institute of Rural Development (SIRD) and the Project

Management Unit (PMU) through the preparation of local government manuals, delivery of formal training sessions,

and continuous mentoring/handholding support (provided by district coordinators at the local level) on service delivery

systems (including detailed project report preparation, technical design and planning, environmental and social

awareness, implementation and compliance with ESMF, procurement, contract management and asset management)

played a critical role in improving the institutional capacity of the local governments to implement local infrastructure

sub-projects and deliver services. The capacity building support through a mix of formal training and on the ground

handholding support for improving the local government’s service delivery system led to sustainable improvements in

project design/DPR preparation and execution systems for various types of local infrastructure projects.

29. Additional support to backward, tribal and revenue-deficit local governments. The project also provided a one-

time financial assistance to a select set of sixty backward, tribal and revenue-deficit local governments to enable them

to implement additional local priority infrastructure

projects to address their local economic and social

needs. This was one of the two new activities taken up

to utilize the savings accrued in the project (as

explained in section I. B Major Changes During

Implementation) in response to the state’s priority to

provide additional financial support to those local

governments which have high levels of poverty or are

geographically/ demographically/ economically

disadvantaged, so as to enable them to address their

specific challenges that are responsible for their

backwardness. This activity also contributed directly

to the PDO and to the Bank’s twin goals of reducing

poverty and enhancing shared prosperity. The local

governments were selected based on an objective

assessment of their degree of backwardness,

measured through: (i) high concentration of Scheduled Caste/Scheduled Tribe population, poverty level (number of

below poverty line families), poor accessibility/remoteness, and non-availability of basic amenities (e.g., roads, drinking

water, health facilities, electricity, and crematoria); and (ii) low levels of own source revenues. Tribal local governments

S. No. Sectors No. of

projects

1 Integrated Child Development Service Centres 42

2 Schools 27

3 Hospitals (including PHC/CHC etc. 39

4 Bus Stand/Waiting shed/Markets 16

5 Burial Ground/Crematorium 5

6 Other Utilities 28

7 Roads 39

8 Street lights 10

9 Drinking water supply 16

10 Other Projects 30

Total 252

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 14 of 70

were selected based on the government notified tribal clusters in the state with high concentration of indigenous tribal

population. Each of these local governments was screened to ensure that they met the minimum mandatory conditions

(MMCs) relating to basic fiduciary and planning systems. The table alongside summarizes the types of sub-projects

implemented by the sixty backward and tribal local governments that were provided funds. However, the component

faced multiple implementation challenges due to weak capacity of these local governments, which was addressed

through deployment of additional mentors/district coordinators for close implementation support and supervision.

30. The table below presents the status of the relevant intermediate results indicators that contribute to the

achievement of this outcome:

S. No. IR Indicators End of Project target Status

1 Number of backward, tribal and revenue deficit

LGs that execute its additional block grant support

on time

51 Target exceeded, 60 LGs

received and executed

the support

2 By EOP, #/types of sub projects built by GPs and

Municipalities through block grants

No fixed target, framework

approach followed

43,711 sub-projects

implemented

3 Performance of all GPs and Municipalities is

assessed each year

100% Achieved, 100% GPs and

municipalities were

assessed every year

31. Based on the above discussion, Outcome 1 of the project has been fully achieved.

Outcome 2: Strengthened Institutional Capacity of the Local Government System in Kerala to undertake Basic

Governance and Administrative Functions More Effectively and in a Sustainable Manner

32. As noted above, the efficacy of this outcome can be ascertained through the APA results and the extensive

capacity building support provided to the local governments on key issues of local governance, local administration and

service delivery. Implementation of APA as an objective and transparent tool for measuring the improvements in local

government’s functioning and allocation of performance grants, enabled many sustainable institutional improvements

in the local government systems on aspects relating to public financial management, decentralized planning,

accountability and transparency in local government functioning, and project execution systems. One of the key

achievements has been the timely preparation of annual financial statements by all the local governments and external

audits, which was a mandatory condition for all local governments to qualify for PG. Likewise, the streamlined process

for the preparation of annual plans with high levels of citizen engagement and community participation has been

institutionalized.

33. The project provided capacity building support to local governments for institutional strengthening through: (i)

preparation and formal state government notification of 12 administrative manuals on key aspects of local government

functioning (including budgeting, procurement, asset management, gender budgeting, public reporting, grievance

redressal, performance audit, financial management, LSGD public works, administration manual for transferred

functions, social audit, and state audit); (ii) formal training for all 1,028 local governments by KILA, SIRD and PMU on the

administrative manuals, APA, Environmental and Social Management Framework, and Vulnerable Groups Development

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 15 of 70

Framework; and (iii) orientation and refresher courses for elected representatives and local government officials on

Detailed Project Report (DPR) preparation, environmental audits, social audits, gender budgeting, gender based

violence, and financial accounting/reporting. One of the key KLGSDP achievements is the formal adoption and

institutionalization of the Procurement Manual by the state government, which all local governments are required to

comply with for all procurement activities undertaken by them. This would improve local governance and service

delivery through transparent and competitive procurement procedures. The state government also institutionalized

ESMF compliance by all local governments for investment and development activities being carried out in their

jurisdictions, irrespective of the funding source. Another achievement is the production of 12 administrative manuals

that would streamline and improve the local government functioning, which is one of the most important measures

for sustainable capacity building and institutional strengthening of the local governments in the long run. However,

owing to the initial delays in implementation, even though the project was able to deliver the 12 administrative manuals,

training and handholding support to local governments for the adoption and implementation of these manuals at the

local level was not adequate. GOK/KILA have committed to take on this responsibility as a part of KLGDSP’s sustainability.

34. An end-line capacity building evaluation was conducted by an independent agency to assess the impact of all the

capacity building interventions under KLGSDP on the local government systems and capacities for local governance and

service delivery. The evaluation covered assessment of systems improvement support and formal trainings provided to

local governments, on the ground mentoring support provided through district coordinators, and institutional

strengthening of KILA and SIRD.

a. Systems Improvement through APA. The evaluation highlighted that the project, through the APAs, has made a

significant positive impact on the institutional systems of the local governments. More than 90% of the local

government officials surveyed responded that the APAs encouraged them to improve their institutional systems for

local governance, administration and service delivery, in order to enable them to qualify for accessing additional

discretionary grant resources for addressing the local service delivery related investment needs. The survey also

highlighted that the APA fostered a high degree of political will and commitment in the elected local government

representatives to perform better and seek a higher performance score. More than 95% of the local government

secretaries interviewed responded that the APAs motivated them to improve their accounting, financial reporting

and audit systems, including timely recording of expenditures and closing the books of account, timely external

audit, and achieving a clean audit opinion from the external auditors.

b. Formal Trainings. Formal trainings were imparted by KILA, SIRD and PMU. KILA provided trainings on local

governance, local planning, local development, financial management, e-governance, skill development, child

development, panchayat administration, and social accountability. SIRD provided trainings on social audit, gender

budgeting, local economic development, women’s empowerment, implementation of GOI schemes, and computer

training. PMU provided trainings on ESMF, APA, Refresher training for new elected representatives, DPR preparation

and project execution, and Gender Based Violence. The evaluation assessed the timeliness, relevance, mix of

participants, relevance of learning material and overall outcomes of training. The evaluation noted that around 75%

of sample participants across different categories confirmed that the trainings that were delivered to them were

useful, relevant and needed at that time. Likewise, around 70% of the sample participants confirmed that the

training material was highly relevant to local government operations. 75% of sample participants confirmed that

the formal training improved the overall efficiency of local government functioning.

c. Mentoring support. The project also provided on the ground mentoring and handholding support on specific areas

of expertise, such as accounting and IT, and monitoring project execution (for district coordinators). The end-line

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 16 of 70

capacity building evaluation noted that the handholding and mentoring support provided by the project played a

critical role in building the capacity of the local government officials in terms of familiarizing, understanding and

implementing the new accounting and IT systems. More importantly it supplemented the formal training support

and enhanced the effectiveness of the overall capacity building support.

d. Institutional Strengthening of KILA and SIRD. This included support for training management information systems,

computerization of helpdesk and expansion of faculty base. These interventions enhanced the sustainability of the

training and capacity building support that was being provided by these institutes to the local governments.

e. The evaluation specifically assessed the impact of capacity building interventions on local governance and service

delivery. More than 75% of sample participants reported that various capacity building interventions have helped

the local governments’ elected representatives and officials in terms of improved transparency in governance,

improved planning systems, improved understanding and knowledge of service delivery systems, as well as in the

adoption of ESMF.

35. Finally, the project supported the development and integration of institutional systems for service delivery,

financial management, financial reporting and monitoring project execution, through the Information Kerala Mission

(IKM), including the creation of a local government fiscal database, the development of a comprehensive MIS system,

and the integration of IKM software for local governments (Sulekha, Sankhya etc,). However, while the complete MIS

system was developed, the roll-out of this system across all local governments (including the training and handholding

support) could not be completed due to significant delays as noted in Section III.B. Key Factors During Implementation.

However, IKM has committed to completing the roll-out with its own resources, as this is key for the future success of

IKM interventions and for improving local government management systems.

36. The table below presents the status of the relevant intermediate results indicators that contribute to the

achievement of this outcome:

S. No. IR Indicators End of Project target Status

1 LSGs received training over life of project 1028 Achieved

2 KILA's capacity developed to provide enhanced

training to GPs and Municipalities

Quality improved Achieved, as ascertained

by the end-line

evaluation

3 Production of draft manuals in the areas of

budget, planning,financial managementt,public

works/procurement, institutional managementt

4 Exceeded the target; 12

manuals were produced

and notified by GOK.

4 GP database established and operating with

annual reports produced

1 Achieved

5 Decentralization Analysis Cell (DAC) providing

annual fiscal reports

3 Partially achieved, only

two fiscal reports

prepared

6 Project studies/surveys complete 4 Achieved

37. Based on the above discussion, Outcome 2 of the project has been fully achieved.

Justification of Overall Efficacy Rating

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 17 of 70

Rating: Substantial, based on the discussions on the achievements of the two PDO outcomes.

C. EFFICIENCY

38. At appraisal, it was noted that sub-project investments would reflect local preferences and would be identified

through a local planning process. However, a priori, it would be difficult to determine the exact types of sub-projects

that would be carried out in a GP. The PAD highlighted that evaluations of similar sub-projects such as those anticipated

under the project have shown positive economic rates of return.

39. Ex-post Evaluation. Under Component 1, which utilized 92 percent of the IDA Credit, nearly 44,000 sub projects

were implemented using performance grants provided by the project for a total investment of INR14,103 million ($225

million). Tables in the Efficacy section above provide details of the types and numbers of sub-projects implemented. As

anticipated at appraisal, these sub-projects were identified through participatory processes and were in line with existing

GoK procedures. Various project capacity building activities, particularly in procurement and environmental and social

management, as well as project management support, contributed to efficient implementation of these sub-projects.

40. Six sample sub-projects with costs ranging between US$2,000 and US$60,000 were selected for quantitative

economic analysis: (i) construction of a new gravel road; (ii) converting an earthen road to a concrete road; (iii)

rehabilitation of public wells to improve water supply; (iv) construction of a bus terminal; (v) construction of a drainage

system; and (vi) street light improvement. The results of the economic analysis are presented in the table below. The

estimated EIRRs for the sample projects are in the 15.5 percent to 43.5 percent range, well above the social discount

rate (SDR) of 8 percent. Sensitivity analysis confirms that the economic returns are robust. Annex 4 provides details of

the efficiency analysis.

Economic Internal Rate of Return (EIRR)

Sample

Project 1:

Construction

of Concrete

Road

Sample

Project 2:

Constructio

n of Gravel

Road

Sample

Project 3:

Rehabilitation

of drinking

water wells

Sample

Project 4:

Construction

of Drain

Sample Project

5: Construction

of Bus Stand

with a Link Road

Sample Project

6: Replacing

Tube lights with

CFL lamps in

street lighting

Base Case 33.65% 43.49% 15.49% 20.50% 20.17% 19.36%

20% increase in

O&M Cost 11.01% 18.99% 14.52% 19.71% 19.75% 18.64%

20% decrease

in project

benefit

8.11% 15.05% 10.87% 15.22% 15.65% 14.22%

41. Design and Implementation Efficiency. Over 1,000 local governments spread across the state participated in

the introduction of the APA process and the selection, design, and implementation of a very large number of sub-

projects. Project implementation resulted in both elements of the PDO being achieved. Environmental, Social, and

Fiduciary compliance was effective, and contributed to the overall efficiency of the project.

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 18 of 70

42. Utilization of IDA Credit, accrued savings and closing date extensions. The original Credit closing date required

an extension of 24 months for utilization of the savings that accrued because of the significant depreciation of the Indian

Rupee against the US dollar. The equivalent of US$7.2 million was cancelled from the Credit in May 2017. At project

closure, the equivalent of US$6.3 million remained unutilized, while an additional amount of US$ 6.5 million was incurred

as an exchange loss by the GOK. Accordingly, out of the total disbursed Credit of US$ 182.83 million, US$ 169.98 million

was utilized by end of the project. Section III. B. Key Factors During Implementation, highlights that the extension of the

Credit closing date was in part due to the original ambitious target of completing the entire project, including four cycles

of annual performance grants, in a little over four years. In addition, the last two years of the project also witnessed two

elections within a span of 18 months (each election imposed a three-month long code of conduct when, as per election

laws, no new procurement could be initiated) and unusually long spells of monsoon rains (ranging between 3 and 6

months, when no physical works can be carried out on the field), which further added to implementation delays.

43. The project successfully supported fifty backward/tribal GPs and ten revenue-deficit municipalities with

additional financial assistance for poverty alleviation and local economic development projects as a new activity

during the extension that was granted for use of IDA credit savings. GoK proposed that this additional activity, which

was supported by GoI and accepted by the Bank, as it was directly aligned with the Bank’s priority of poverty alleviation.

Despite the serious challenges posed by the weak institutional capacity and the remote locations of these sixty local

governments, the project (through the deployment of additional manpower and by establishing rigorous mechanisms

for implementation supervision) ensured that the activities supported under this sub-component were completed as

planned and led to real on the ground results in terms of improved access to services.

44. PMU Leadership. The project faced a high turnover of Project Directors (around 5 transfers) during the last two

years of the project, which impacted project implementation. However, the last project Director (who was deputed in

November 2016 and continued till the end of the project) provided stable, proactive and dedicated leadership, and

ensured extensive monitoring and supervision by the PMU to complete the final stages of implementation satisfactorily.

45. Implementation Arrangements and inter-institutional coordination. The necessarily complex implementation

arrangements, with involvement of multiple institutions and conflicting reporting relationships, as well as weak inter-

institutional coordination issues (as noted later in Section III. B. Key Factors During Implementation) led to delays in the

implementation of Components 2 and 3 during the initial years.

46. At the time of project closure, less than 1% of the total sub-projects (approximately 323 sub-projects, as per

the last AM) remained incomplete, most of which were in advanced stages of implementation and had to be completed

with GOK’s budgetary sources, in compliance with the technical and safeguards requirements. Implementation was

monitored closely by the Bank after the project closure, and GoK reported that these were completed by March 2018.

Assessment of Efficiency and Rating

Rating: Substantial. The efficiency analysis of the sample sub-projects shows strong results in terms of economic cost-

benefits at the local level. Project implementation was overall quite efficient in terms of completing the implementation

of almost 99% of sub-projects and completing the implementation of sub-projects in backward/tribal GPs and revenue-

deficit municipalities, despite various exogenous factors (elections, monsoon rains) and capacity challenges.

Implementation delays experienced can be attributed to the overly ambitious design in terms of the implementation

period, weak PMU leadership at a critical period, and complex implementation arrangements. In the context of the

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 19 of 70

complexity and wide geographical coverage of the project, the impact of these delays is not considered significant.

Hence, the efficiency is rated as Substantial.

D. JUSTIFICATION OF OVERALL OUTCOME RATING

Rating: Satisfactory, based on the discussions on, and ratings of, relevance of PDO, achievement of PDO, and efficiency.

E. OTHER OUTCOMES AND IMPACTS

Gender

47. The project implemented many gender focused activities which have led to substantial outcomes in terms of

gender mainstreaming, inclusion and gender based violence related issues. The project issued specific guidelines to local

governments to identify and prioritize sub-projects with substantial focused benefits to women and vulnerable sections

of society. The project integrated gender mainstreaming in the Environment and Social Management Framework (ESMF)

and the Vulnerable Group Development Framework (VGDF). This was supplemented by focused and periodic trainings to

elected representatives and local government officials across the state on integrating gender aspects as a part of the

annual planning and implementation processes. As a result, many KLGSDP sub-projects targeted women and vulnerable

groups. Some of the major sub-projects targeting women include Kudumbasree Centres/Canteens, Skill Development

Centres, and Working Women’s Hostels.

48. A gender budgeting manual was prepared by KILA after a series of consultations and was formally notified by the

GoK for implementation by local governments as a part of the annual planning and budgeting exercise. KILA provided

trainings to local government officials to implement the manual as a part of the annual training calendar. In addition,

KLGSDP supported the preparation of Gender Action Plans mandated by GoK as per the state’s Gender Equality and

Women’s Empowerment Policy (GEWE Policy). The Gender Action Plan for KLGSDP aimed to build the requisite capacity

for implementing the GEWE policy at the local government level and lays down processes to ensure that gender

considerations are systematically and strategically integrated into interventions proposed by the local governments.

49. KLGSDP also supported several interventions on gender based violence. The PMU conducted Stale Level

Workshops for Elected Representatives and Implementing officers of Local Governments and District Coordinators of

KLGSDP to address Gender Based Violence (GBV) in collaboration with the Police Department and the Social Justice

Department. Subsequently, the performance grant was used for financing sub-projects focusing on the creation and

maintenance of assets for supporting the local governments to address the GBV; these include increased infrastructure

facilities to accommodate GBV Victims, facilities for Legal Assistance, rehabilitation programs for livelihood generation,

awareness creation against GBV by installation of boards and bulletins, strengthening existing Jagratha Samitis, regular

medical camps for periodic checkups & counseling, promotion of Self Protection programs for women, and increased

surveillance mechanisms to address GBV in collaboration with the Police and the Social Justice Department.

Institutional Strengthening

50. Strengthening local government institutions to deliver public services and undertake administrative functions was

one of the core objectives of the project and is prominently captured in the PDO and the project design. The mutually

reinforcing approach of providing performance grants based on institutional performance and focused capacity building

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 20 of 70

support worked very well, as recorded in the end-line project evaluations. The key interventions and outcomes have been

highlighted in the section on Efficacy.

51. The project also supported the institutional strengthening of KILA and SIRD as the two key nodal state agencies

responsible for capacity building and institutional strengthening of local governments. The focus was on modernizing

training infrastructure, training facilities and organizing faculty development programs. The end-line capacity building

evaluation noted that this support has been beneficial to KILA and SIRD in enhancing their in-house capacities.

Mobilizing Private Sector Financing

N/A

Poverty Reduction and Shared Prosperity

52. The project contributed to reducing poverty and enhancing shared prosperity. Sub-projects implemented through

performance grants were identified through a robust decentralized bottom-up planning process that reflected the needs

and priorities of the local communities and were largely focused on services that directly contributed towards poverty

reduction through boosting rural connectivity, creating local employment opportunities, providing good quality social

infrastructure through ICDS, health centers, and schools, as well as core public services that lead to improved public health

outcomes. In addition, the project also supported backward, tribal and revenue-deficit local governments through

additional financial assistance to finance local priority infrastructure requirements.

Other Unintended Outcomes and Impacts

N/A

III. KEY FACTORS THAT AFFECTED IMPLEMENTATION AND OUTCOME

A. KEY FACTORS DURING PREPARATION

53. Lessons learned from other projects were incorporated. KLGSDP design benefited from lessons learned in other

recent World Bank local government projects in India and in South Asia. In particular, the project drew on the experience

of the Karnataka PRI project, which experienced a number of difficulties since the beginning of its implementation. Some

of the key learnings incorporated in KLGSDP design included: (i) allowing complete discretion to local governments over

performance grant expenditures; (ii) performance grants being disbursed in a single tranche at the beginning of the

financial year and local governments being permitted to draw these funds according to their cash-flow requirements; and

(iii) commitment of significant counter-part funding by GoK.

54. GoK demonstrated strong commitment and provided an enabling environment. The political and policy

environment in Kerala was very committed to the decentralization agenda and this cut across political lines. This was

demonstrated by GoK committing significant counterpart funding for the performance based grant allocation system.

The commitment of GoK was also evident from some of its important initiatives, such as the People’s Plan Campaign, as

well as embedding the decentralized planning process in the local government system with a high level of community

engagement and participation.

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 21 of 70

55. Risks were assessed and mitigated. It was recognized that poor decision-making on some of the key aspects of

design and implementation may hinder the achievement of the PDO. Accordingly, a detailed governance and

accountability action plan was prepared based on a thorough analysis of the key transactions which are intrinsic to the

project design and included the potential risks thereof at every stage, along with the corresponding mitigation measures.

The action plan also identified the responsible agency for implementing the mitigation measures and the cost of their

implementation.

56. The project was designed in a detailed and meticulous manner based on robust analysis. The APA based

performance grant system was designed carefully with a phased implementation approach, being mindful of the learning

curve that the local governments would go through. This design of the APA and the performance grant system struck the

right balance between motivation and performance factors from local governments’ perspective. In addition, the

mutually reinforcing approach of providing capacity building and awareness generation support to local governments

through multiple channels (formal training, on the ground mentoring and systems development) under Components 2, 3

and 4 addressed the supply side constraints and contributed to improvements in institutional performance. Financial

management systems, fund flow and procurement systems were also designed based on capacity and risk assessments

of the implementing agencies. However, considering the scale of the operation in terms of geographical coverage and

the inherent challenges of implementing the APA, performance grants, an enormous number of sub-projects, and

capacity building, as well as exogenous (but known) factors such as state and local elections and currency depreciation,

the original implementation period of the project was overly ambitious and did not leave any room for slippages.

57. Implementation arrangements were complex and involved too many execution support agencies. While the roles

of the PMU, as well as the other execution support agencies were spelt out clearly, inter-institutional coordination issues

were not fully assessed and the reporting/accountability relationships were not well defined. In addition, many of the

execution support agencies were superior to the PMU in the institutional hierarchy of the state government system and

the project specific reporting requirements were not completely aligned with the state government’s reporting systems.

B. KEY FACTORS DURING IMPLEMENTATION

58. Implementation delays in Components 2 and 3. Activities under Component 1 started in September 2011 after

the Credit was declared effective. However, actions agreed during project preparation to strengthen the capacities of

KILA, SIRD, Information Kerala Mission (IKM) and Gulati Institute of Finance and Taxation (GIFT) to ensure implementation

readiness of Components 2 and 3 were not implemented until much later. As a result, activities under Components 2 and

3 began to make progress only by the time the mid-term review (MTR) in early 2014. The PMU stepped-in to compensate

for some of these delays during the initial years of implementation, e.g., by conducting training sessions for local

governments on key topics such as project orientation, procurement, ESMF, and APA.

59. Weak institutional coordination between PMU and execution support agencies. For the reasons discussed earlier,

institutional coordination suffered and many key project activities, such as finalization of training manuals and the

development of the fiscal database for local governments were significantly delayed.

60. Implementation modality of APA was changed mid-course. Overall, implementation of the APA was one of the

key success of the project. However, the APA implementation modality was changed mid-course, wherein the state

government decided to hand over the mandate of conducting the APA to the State Performance Audit Office (SPAO)

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 22 of 70

instead of an independent agency (which conducted the first year of APA). This led to some transitional issues that

occurred during this process of internalization as the SPAO was not completely geared up in terms of organizational

capacity (skills and adequacy of the staff needed). Consequently, the robustness and technical soundness of the APA

declined in the later years, which was reflected in the rising number of formal appeals by local governments against the

incorrect APA results in these years. However, the results were rectified during the formal appeal process instituted by

the GOK to examine the claims of the local governments on a case-by-case basis, and final correct results were used for

PG allocation.

61. Decentralization Analysis Cell (DAC) faced multiple implementation issues that led to sub-optimal outputs in

Component 3. Since inception DAC faced issues relating to its institutional positioning (finally anchored in GIFT) and

organizational capacity, which resulted in a delay of two years before it was fully operationalized. This was followed by

institutional coordination issues with IKM due to which some of the key deliverables were further delayed. The quality of

some of the 27 policy studies completed by DAC was not satisfactory, as reflected in the DAC’s decision to publish only

14 policy studies. While DAC completed most of its KLGSDP activities, the overall objective of DAC providing policy

advisory support to the state government and developing/maintaining a comprehensive local government fiscal and

service delivery database was not fully accomplished.

62. Monitoring and reporting systems at the state level were inadequate. Monitoring and evaluation systems for

tracking the utilization of grants was an area of concern throughout the project period. The project relied on a manual

system of monitoring with the help of the district coordinators, with inadequate mechanisms at the state and the local

levels for periodic monitoring of project execution, fund utilization, quality of assets being created, and compliance with

technical design specifications. The district coordinator led field level monitoring also had its own constraints in terms of

periodicity, reliability and accuracy. Owing to this, the physical and financial progress monitoring of the large number of

sub-projects that were implemented by the local governments every year continued to be a challenge through-out.

During the later years of the project, the PMU developed a sub-project implementation database based on information

provided by district coordinators, as well as information fed by the local government officials on Sulekha and Saankhya

software in IKM. This constrained the implementation monitoring capacity of the project and made it much more

resource intensive for the PMU.

63. The original time-frame for project implementation proved to be inadequate. For the reasons highlighted in the

earlier section, the project was unable to complete four cycles of performance grants in a period of four years. In practice

it took an average of 15-18 months to complete each cycle of performance grants, i.e., from APA to utilization of the

performance grants; effectively three to four months were rendered unworkable every year due to heavy monsoon rains.

64. The full Credit amount was not utilized by the project closing date. The project accumulated savings of US$62

million as the Indian Rupee depreciated from INR46 for US$1 (PAD estimate) to nearly INR65/67 per US$ in 2017. While

the financing agreement was signed for US4 200 million, US$ 182.83 million of Credit was actually disbursed and a small

portion of the Credit, equivalent to US$7.2 million, was cancelled in May 2017. US$6.3 million of Credit remained

unutilized which will need to be returned by GOK to the Bank along with additional amount of US$6.5 million that

accounts for the exchange rate loss that accumulated over the implementation period for the Credit resources that were

disbursed at a lower exchange rate but documented at a higher exchange rate at different points in time. Accordingly,

out of the total disbursed Credit of US$ 182.83 million, US$ 169.98 million was utilized by end of the project.

The World Bank Kerala Local Government and Service Delivery (P102624)

Page 23 of 70

IV. BANK PERFORMANCE, COMPLIANCE ISSUES, AND RISK TO DEVELOPMENT OUTCOME

A. QUALITY OF MONITORING AND EVALUATION (M&E)

M&E Design

65. The results framework comprised three PDO indicators (including one core sector indicator) and eight

intermediate results indicators (two for each of the four components). The PDO indicators were well targeted to

measure the achievement of the PDO through APA results. The intermediate results indicators were clearly measurable

and time bound. Baselines, data/information sources, and responsible agencies for data collection/compilation were

clearly defined for all indicators. The APA was made the focus of M&E, as it ensured 100% coverage in terms of the local

governments which participated in KLGSDP. Annual targets were well defined for the PDO indicators; however, annual

targets were not defined accurately for one IR indicator relating to the number and type of sub-projects being

implemented by LSGs, owing to the framework approach adopted for the project. The targets defined for a few unlinked

IR indicators including intended beneficiaries aware of project info. and project investments (female) and intended

beneficiaries (female) were not defined accurately and hence led to their partial achievement, although they were fully

achieved based on actual population data.

66. Institutional responsibility for M&E was clearly defined for results monitoring: the PMU had the overall

responsibility, while KILA, SIRD and GIFT were responsible for specific component focused IR indicators. Component 3

was to conduct baseline and end-line service delivery surveys, as well as project evaluations to evaluate the results on

service delivery and capacity building aspects. For Component 1, a system of semi-annual administrative reporting

system was defined for upward accountability and budget/plan execution report dissemination for downward

accountability. Standard reporting procedures, comprising semi-annual progress reports and quarterly IUFRs, were also

put in place. A mid-term review was to be conducted within 30 months of project implementation.

M&E Implementation

67. M&E systems were implemented as per the original design. The PMU took the prime responsibility for putting

in place the required arrangements for M&E. Project surveys and evaluations were undertaken jointly by the PMU and

the DAC. The baseline service delivery survey was delayed due to the initial implementation related challenges described

earlier. However, the end-line survey and the two evaluations were conducted on time and were completed by the end

of the project. The APAs were conducted timely on an annual basis. The execution support agencies provided

information for IR indicators for their respective components.

68. The PMU struggled with the monitoring of sub-project implementation, owing to the lack of appropriate

systems for the local governments to report on financial and physical progress. IKM software (Sulekha and Sankhya)