impact of privatization in africa: uganda...

TRANSCRIPT

IMPACT OF PRIVATIZATION IN

AFRICA: UGANDA TELECOMMUNICATIONS

One of Eight Papers from a Project Entitled: Assessing the Impact of Privatization in Africa

Funded by the Norwegian Trust Fund and co-funded by Public-Private Infrastructure Advisory Facility

Managed by the Investment Climate Department and Africa Private Sector and Infrastructure Department of the World Bank

Yahya Jammal

Leroy Jones

Boston Institute for Developing Economies (BIDE)

October, 2006

These studies focus on identifying and explaining results of various forms of privatization, defined broadly to include any significant transfer of management or ownership from the public to the private sector (that is, management contracts, leases, affermage contracts, concessions and full and partial divestiture). The first goal is to measure performance quantitatively to the extent possible with available data. The second goal is to explain that performance in terms of how the privatization was conducted. A key feature of the study is that performance covers equity as well as efficiency. That is, we attempt to measure the impact on various stakeholders: primarily consumers, workers, the government, and the new owner or operator. In sum, a successful privatization is not just one where the deed gets done, but where performance improves substantially and the results of that change are distributed equitably with sizeable public benefits to help build and sustain political support. The cases include failures as well as successes. One can learn at least as much from the former as the latter. The goal is to help replace faith-based policies with ones that are fact-based. The opinions expressed here are the sole responsibility of the authors and do not reflect those of the World Bank.

October, 2006 IPA: Uganda Telecom Page ii of 36

TABLE OF CONTENTS

EXECUTIVE SUMMARY 6

1. WHAT WAS DONE? 8 1.1. The Sector Prior to Reform 8 1.2. The Reforms 8 1.3. Privatization 10 1.4. Some Issues 11

2. WHAT WERE THE SECTORAL RESULTS & WHY? 12 2.1. The Growth Record 12 2.2. What Explains Sectoral Growth? 13

2.2.1. The Questions 13 2.2.2. Technical Change 13 2.2.3. Macroeconomic Growth 17 2.2.4. External Factors versus Policy 17

3. WHAT WERE THE UTL RESULTS? 19 3.1. Enterprise Performance 19

3.1.1. Surplus Generation 19 3.1.2. Price/Quantity Breakdown 20

3.2. Employee Impact 22 3.3. Government Impact 24 3.4. Consumer Impact 25

3.4.1. Mobile 25 3.4.2. Fixed Line 27 3.4.3. Quality of Service 28

3.5. Economy-Wide Impact 28 3.6. Impact Summary 29

4. WHAT EXPLAINS THE RESULTS? 29 4.1. Overview 29 4.2. Competition & Technical Change 29 4.3. Privatization, Investment and Competition 30 4.4. Sequencing 30

4.4.1. Competition or Privatization First? 30 4.4.2. Regulation or Private Participation First? 30

4.5. Speed 30 4.6. Executive Commitment 31 4.7. Highly Capable Technocrats 32

5. CONCLUSION 32

October, 2006 IPA: Uganda Telecom Page iii of 36 APPENDIX A: ADDITIONAL TABLES 33

APPENDIX B: BIBLIOGRAPHY 35

October, 2006 IPA: Uganda Telecom Page iv of 36

TABLE OF TABLES Table 1: Operators in the Telecommunications Sector Since 1994 11 Table 2: Penetration Levels & Growth in Sub-Saharan Africa 16 Table 3: Summary of Price and Quantity Effects: Pre vs Post Privatization 22 Table 4: Government Revenues from UTL (million Ush.) 24 Table 5: Indicators of Service Quality 28 Table 6: Performance of UTL Using Economically Relevant Accounts (million Ush.) 33 Table 7: Performance of UTL Using Flows at Constant 1999 Prices 33 Table 8: Reconciliation of Total Return to Capital & Accounting Profit (billion Ush.) 33 Table 9: Decomposition of UTL Profit Into Price & Quantity Effects 34

October, 2006 IPA: Uganda Telecom Page v of 36

TABLE OF FIGURES Figure 1: Number of Fixed Lines per 100 Inhabitants in Sub-Saharan Africa in 1996 9 Figure 2: Number of Fixed and Mobile Subscribers per 100 Inhabitants in Uganda 12 Figure 3: Semi-Log of Fixed and Mobile Subscribers per 100 Inhabitants in Uganda 12 Figure 4: Number of Fixed and Mobile Subscribers per 100 Inhabitants in Uganda & SSA-SA 14 Figure 5: Semi-Log of Fixed and Mobile Subscribers per 100 Inhabitants in Uganda & SA-SSA 14 Figure 6: Number of Fixed and Mobile Subscribers per 100 Inhabitants: Uganda/(SSA-SA) 15 Figure 7: Initial Penetration versus Growth in Penetration 17 Figure 8: Number of Fixed line Connections (& Mobile for 96-98) 18 Figure 9: Return to Capital vs. Accounting Profit After Tax 20 Figure 10: Return to Capital (current vs constant prices) 21 Figure 11: Number of Employees 23 Figure 12: Average Cost of Labor (million Ush.) 23 Figure 13: Connection Charges: Land Lines vs Mobile 25 Figure 14: Monthly Subscription Fee: Land Lines vs Mobile 26 Figure 15: Selected Local Mobile Prepaid Rates 26 Figure 16: Mobile Tariffs in East Africa: December 2003 27 Figure 17: Fixed Line Tariffs in East Africa: December 2003 28

October, 2006 IPA: Uganda Telecom Page 6 of 36

EXECUTIVE SUMMARY In the mid-1990’s, Uganda’s telephone penetration ratio (lines per hundred inhabitants) was only 0.24, ranking it 32nd of 39 countries in Sub-Saharan Africa less South Africa (SA-SSA). Financial performance of Uganda Post and Telecommunications Corporation (UPTC) was comparable. Reform was initiated with a 1993 Presidential directive to privatize UPTC in a month. A more measured process was adopted which led to the following key reforms:

• Unbundling of UPTC with post, banking and telecom separated in February, 1998;

• Corporatization of UPTC into Uganda Telecom Limited UTL, also in February, 1998;

• Introduction of competition, with one cellular-only private firm (Celtel) beginning operations in 1995 and a Second National Operator (MTN) beginning operations in 1998;

• Regulation in the form of a modestly independent Uganda Communications Commission (UCC) backed by the Uganda Communications Tribunal for dispute resolution in August 1998; and

• Partial privatization of UTL with 51% of the shares sold (February, 2000). Resulting sectoral performance was spectacular, with 1.1 million lines added by 2004, compared to a base of only 30,000 in 1992. New mobile technology was also adopted elsewhere, but Uganda still moved from 40% of the regional average penetration ratio in1994 to 80% in 2004. Changing technology made the dramatic change possible, but the reforms were equally responsible in enabling Uganda to take advantage of them. Entry of Celtel and MTN were the key reform. UTC was late to the cellular table, not entering the market until after privatization and would have been later still had it remained public. So competition policy was the key to success, without which gains would have delayed for perhaps seven years and then likely progressed more slowly. So what difference did privatization make, given the introduction of competition? In the cellular market, very little. MTN/Celtel competition was sufficient to drive the price to the lowest levels in East Africa and the customers MTN eventually did attract would otherwise have been served by MTN/Celtel. Of course having a third party in the market is always better than two in the long run, but no short run effects are apparent. In the fixed line market, there were two effects. First, the number of fixed lines doubled from 1994 to 1999 after having been flat for five years. We suggest this may be an example of the well-know announcement effect whereby performance turns around, not after privatization, but when the policy is first announced. The 1993 Presidential Directive to privatize UPTC immediately got managerial attention and they responded with improved performance. Secondly, there is some evidence that the privatized company priced a bit more aggressively. Prices rose more rapidly after privatization and contrary to the mobile market were higher than elsewhere in East Africa. There is also evidence that efficiency rose significantly at MTN after privatization of UTL and so benefited the government and the private owner with higher returns. But the fixed line

October, 2006 IPA: Uganda Telecom Page 7 of 36 market is less than a tenth the size of the mobile market so these net gains were small compared to the cellular gains due to competition policy. The factors responsible for success of the reforms illustrate the validity of conventional privatization wisdom. These include: competitive and transparent bidding, taking the time to “do it right” with full information; generating consensus, leadership commitment and having skilled technocrats to implement the reforms; and careful attention to the regulatory and legal framework. This paper breaks little new ground at the sector level. The process and consequences of the reforms were already well known because of three previous excellent papers.. The success of the reform package was manifest in the rapid adoption of the new mobile technology, with Uganda gaining on a rapidly moving target by going from 40% of the Sub-Saharan average penetration ratio in1994 to 80% in 2004. One of our tasks was to ask how privatization per se contributed to these results. We conclude that it contributed only a little, with the introduction of private competition being the primary factor behind the impressive gains. We had hoped to add further value by doing an explicit quantification of costs and benefits by stakeholder, but data limitations precluded this. It is nonetheless a useful addition to our set of eight case studies because it shows that divesting into a functionally competitive market will generate no gains for consumers because other suppliers would otherwise have provided equivalent products. The same is true for government so far as taxes go and for any impact on the broader economy. The government, the buyer and workers can still benefit from improved efficiency, but total gains are likely to be smaller than for non-competitive privatizations because output effects are not available.

October, 2006 IPA: Uganda Telecom Page 8 of 36 1. WHAT WAS DONE?1

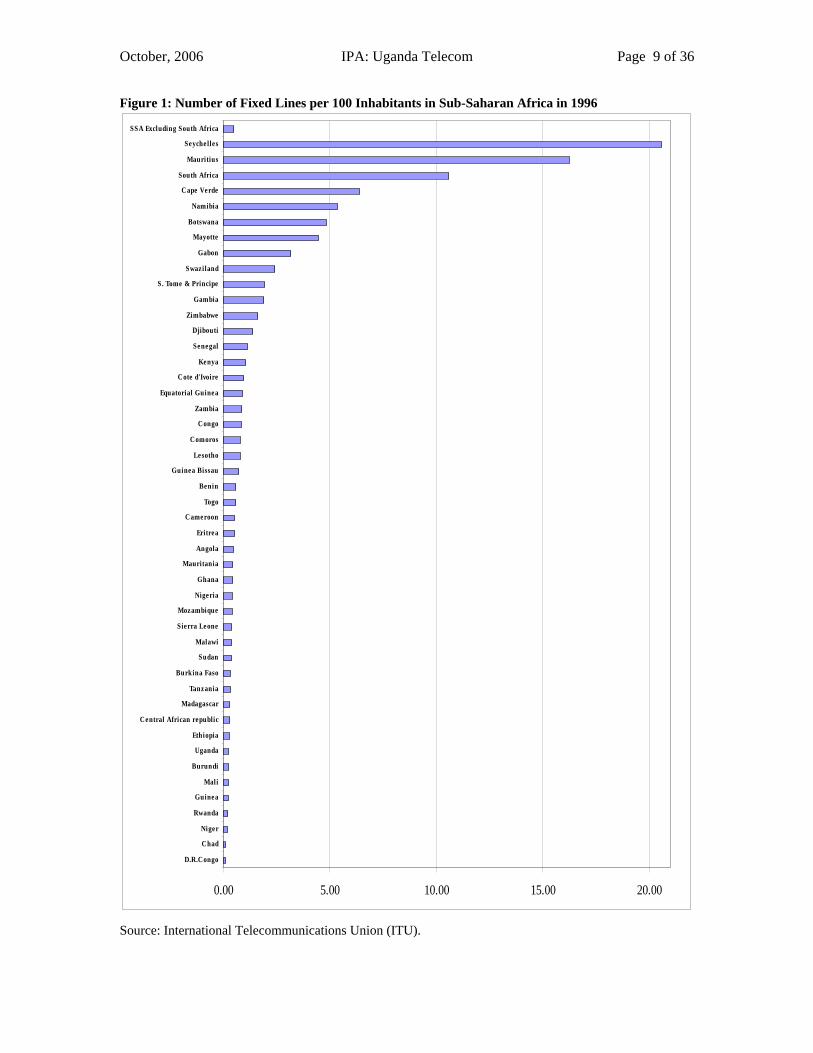

1.1. The Sector Prior to Reform In 1977 Uganda Posts and Telecommunications Corporation (UPTC) devolved from the East African Posts and Telecommunications Corporation. Given the country’s poverty (per capita GDP in 1994 was $190 in 1994 dollars) and the lack of progress under Idi Amin (when per capita GDP dropped 40%), the telecommunications sector was in terrible shape in the mid-1980’s and not a lot of progress was made in the ensuing decade. As Figure 1 shows, in 1996, just after the start of reforms, Uganda’s total connections per 100 inhabitants was only 0.24, ranking it 32nd of the 39 countries the ITU tracks in Sub-Saharan Africa minus South Africa (SSA-SA). Financial management and condition were chaotic.

1.2. The Reforms In the early 1990’s the GOU’s economic management philosophy shifted from its earlier socialist orientation to a liberal market oriented approach.2 In the telecom sector this first manifested itself in a Presidential Directive to privatize UPTC within a month. But calmer heads prevailed and a measured design phase was adopted which lasted three years. A Committee on Investment in Telecommunications was appointed in1993 and, with World Bank assistance, laid out the basic outlines of the reform package in its report of November 1993. While discussions were ongoing, Celtel Uganda, a private operator,3 was given a 15-year license in 1994 to provide mobile services in Entebbe/Kampala/Jinja and began operating in May 1995. Meanwhile, the policy debate continued, with a stakeholders’ workshop to disseminate information, gather views and move towards consensus. A Technical Working Committee of experts was appointed to work out the details. In January of 1996 a joint ministerial policy paper was produced setting out most details and these were embodied in The Communications Act approved in 1997. The key elements of the final package, and the dates of implementation, were:

1 This section will be relatively brief because there are three excellent papers in the public domain. We only provide a summary of

the key facts germane to this paper. Those interested in more detail can see: Shirley Mary M., F. F. Tusubira, Frew Gebreab and Luke Haggarty, Telecommunications Reform in Uganda, World Bank Policy Research Working Paper 2864, June 2002. Byaruhanga, Charles, Managing Investment Climate Reform: Case Study of Uganda Telecommunications, Background paper for the World Development Report 2005, April 16, 2004. Econ One research, Inc. in association with ESG International, Uganda Telecommunications A Case Study in the Private Provision of Rural Infrastructure, July 30, 2002.

2 Byaruhanga is particularly good on this period. 3 Owned by Vodafone, and Mobile Services International with stakes by the International Finance Corporation and The

Commonwealth Development Corporation as well.

October, 2006 IPA: Uganda Telecom Page 9 of 36 Figure 1: Number of Fixed Lines per 100 Inhabitants in Sub-Saharan Africa in 1996

0.00 5.00 10.00 15.00 20.00

D.R.Congo

Chad

Niger

Rwanda

Guinea

Mali

Burundi

Uganda

Ethiopia

Central African republic

Madagascar

Tanzania

Burkina Faso

Sudan

Malawi

Sierra Leone

Mozambique

Nigeria

Ghana

Mauritania

Angola

Eritrea

Cameroon

Togo

Benin

Guinea Bissau

Lesotho

Comoros

Congo

Zambia

Equatorial Guinea

Cote d'Ivoire

Kenya

Senegal

Djibouti

Zimbabwe

Gambia

S. Tome & Principe

Swaziland

Gabon

Mayotte

Botswana

Namibia

Cape Verde

South Africa

Mauritius

Seyche lles

SSA Excluding South Africa

Source: International Telecommunications Union (ITU).

October, 2006 IPA: Uganda Telecom Page 10 of 36

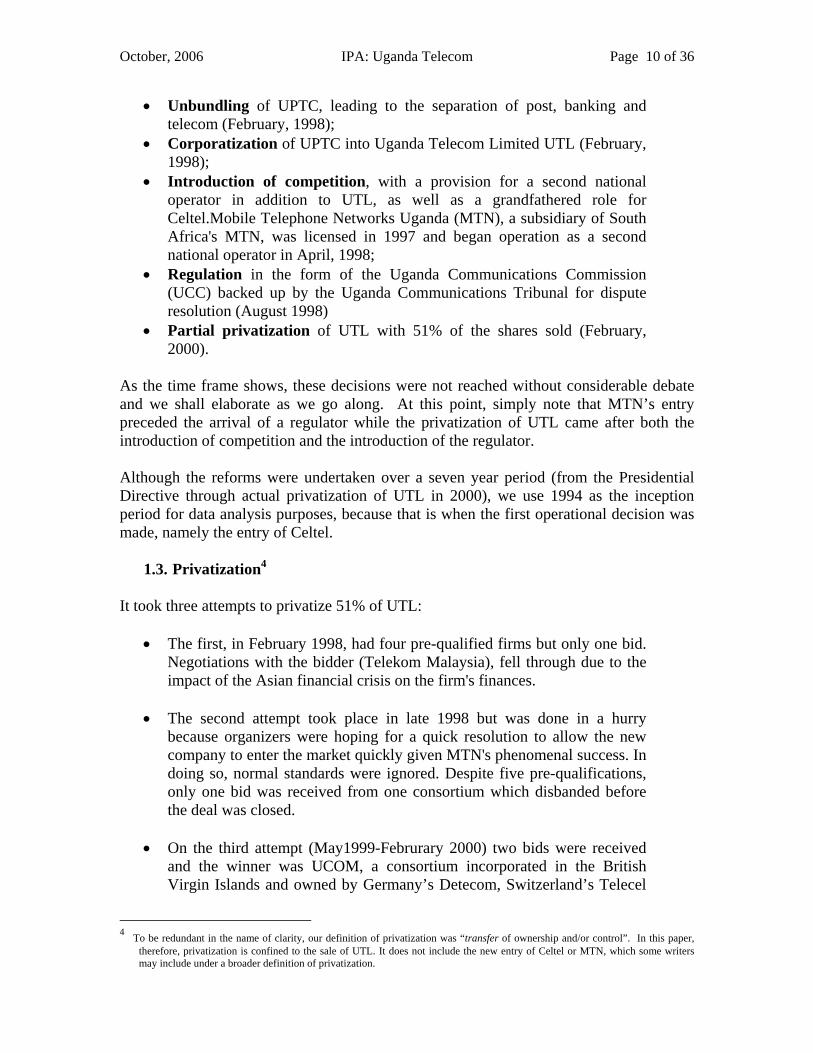

• Unbundling of UPTC, leading to the separation of post, banking and telecom (February, 1998);

• Corporatization of UPTC into Uganda Telecom Limited UTL (February, 1998);

• Introduction of competition, with a provision for a second national operator in addition to UTL, as well as a grandfathered role for Celtel.Mobile Telephone Networks Uganda (MTN), a subsidiary of South Africa's MTN, was licensed in 1997 and began operation as a second national operator in April, 1998;

• Regulation in the form of the Uganda Communications Commission (UCC) backed up by the Uganda Communications Tribunal for dispute resolution (August 1998)

• Partial privatization of UTL with 51% of the shares sold (February, 2000).

As the time frame shows, these decisions were not reached without considerable debate and we shall elaborate as we go along. At this point, simply note that MTN’s entry preceded the arrival of a regulator while the privatization of UTL came after both the introduction of competition and the introduction of the regulator. Although the reforms were undertaken over a seven year period (from the Presidential Directive through actual privatization of UTL in 2000), we use 1994 as the inception period for data analysis purposes, because that is when the first operational decision was made, namely the entry of Celtel.

1.3. Privatization4 It took three attempts to privatize 51% of UTL:

• The first, in February 1998, had four pre-qualified firms but only one bid. Negotiations with the bidder (Telekom Malaysia), fell through due to the impact of the Asian financial crisis on the firm's finances.

• The second attempt took place in late 1998 but was done in a hurry

because organizers were hoping for a quick resolution to allow the new company to enter the market quickly given MTN's phenomenal success. In doing so, normal standards were ignored. Despite five pre-qualifications, only one bid was received from one consortium which disbanded before the deal was closed.

• On the third attempt (May1999-Februrary 2000) two bids were received

and the winner was UCOM, a consortium incorporated in the British Virgin Islands and owned by Germany’s Detecom, Switzerland’s Telecel

4 To be redundant in the name of clarity, our definition of privatization was “transfer of ownership and/or control”. In this paper,

therefore, privatization is confined to the sale of UTL. It does not include the new entry of Celtel or MTN, which some writers may include under a broader definition of privatization.

October, 2006 IPA: Uganda Telecom Page 11 of 36

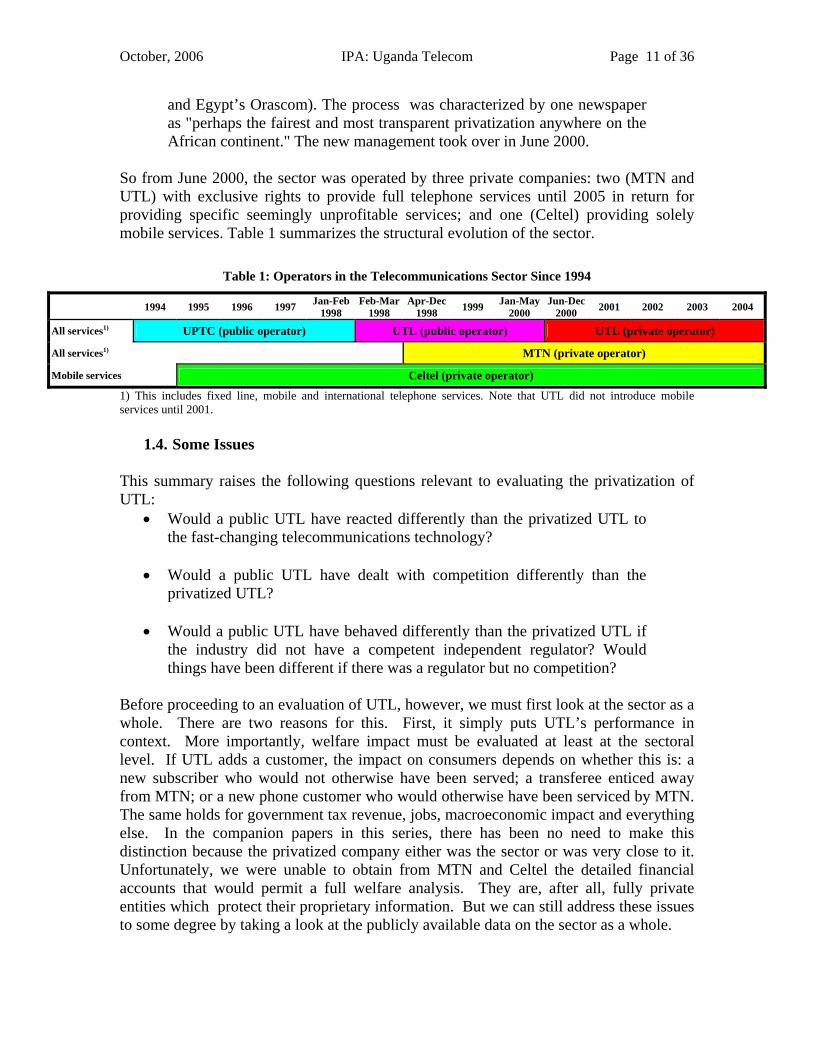

and Egypt’s Orascom). The process was characterized by one newspaper as "perhaps the fairest and most transparent privatization anywhere on the African continent." The new management took over in June 2000.

So from June 2000, the sector was operated by three private companies: two (MTN and UTL) with exclusive rights to provide full telephone services until 2005 in return for providing specific seemingly unprofitable services; and one (Celtel) providing solely mobile services. Table 1 summarizes the structural evolution of the sector.

Table 1: Operators in the Telecommunications Sector Since 1994

1994 1995 1996 1997 Jan-Feb1998

Feb-Mar1998

Apr-Dec 1998 1999 Jan-May

2000 Jun-Dec

2000 2001 2002 2003 2004

All services1) UPTC (public operator) UTL (public operator) UTL (private operator)

All services1) MTN (private operator)

Mobile services Celtel (private operator)

1) This includes fixed line, mobile and international telephone services. Note that UTL did not introduce mobile services until 2001.

1.4. Some Issues This summary raises the following questions relevant to evaluating the privatization of UTL:

• Would a public UTL have reacted differently than the privatized UTL to the fast-changing telecommunications technology?

• Would a public UTL have dealt with competition differently than the

privatized UTL?

• Would a public UTL have behaved differently than the privatized UTL if the industry did not have a competent independent regulator? Would things have been different if there was a regulator but no competition?

Before proceeding to an evaluation of UTL, however, we must first look at the sector as a whole. There are two reasons for this. First, it simply puts UTL’s performance in context. More importantly, welfare impact must be evaluated at least at the sectoral level. If UTL adds a customer, the impact on consumers depends on whether this is: a new subscriber who would not otherwise have been served; a transferee enticed away from MTN; or a new phone customer who would otherwise have been serviced by MTN. The same holds for government tax revenue, jobs, macroeconomic impact and everything else. In the companion papers in this series, there has been no need to make this distinction because the privatized company either was the sector or was very close to it. Unfortunately, we were unable to obtain from MTN and Celtel the detailed financial accounts that would permit a full welfare analysis. They are, after all, fully private entities which protect their proprietary information. But we can still address these issues to some degree by taking a look at the publicly available data on the sector as a whole.

October, 2006 IPA: Uganda Telecom Page 12 of 36 2. WHAT WERE THE SECTORAL RESULTS & WHY?

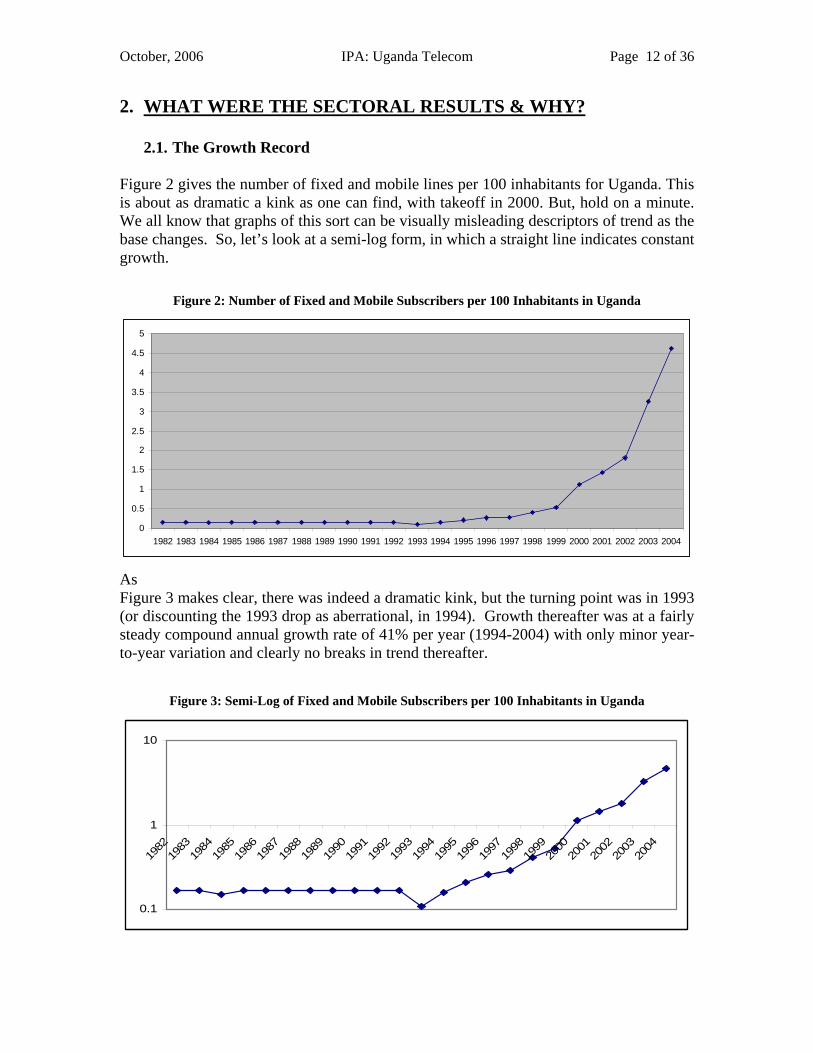

2.1. The Growth Record Figure 2 gives the number of fixed and mobile lines per 100 inhabitants for Uganda. This is about as dramatic a kink as one can find, with takeoff in 2000. But, hold on a minute. We all know that graphs of this sort can be visually misleading descriptors of trend as the base changes. So, let’s look at a semi-log form, in which a straight line indicates constant growth.

Figure 2: Number of Fixed and Mobile Subscribers per 100 Inhabitants in Uganda

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

As Figure 3 makes clear, there was indeed a dramatic kink, but the turning point was in 1993 (or discounting the 1993 drop as aberrational, in 1994). Growth thereafter was at a fairly steady compound annual growth rate of 41% per year (1994-2004) with only minor year-to-year variation and clearly no breaks in trend thereafter.

Figure 3: Semi-Log of Fixed and Mobile Subscribers per 100 Inhabitants in Uganda

0.1

1

10

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

October, 2006 IPA: Uganda Telecom Page 13 of 36

2.2. What Explains Sectoral Growth?

2.2.1. The Questions What explains this dramatic break in trend? It obviously correlates with the onset of reforms. But before attributing all of the dramatic improvement to reforms we need to look at other possible causal factors. To what extent was the rapid growth of the sector due to external factors, namely technical change in the telecommunications industry (especially mobile) and macro-economic growth; and to what extent to internal policy variables? And to the extent it was due to policy, how much was due to the introduction of competition, how much to privatization, and how much to regulation?

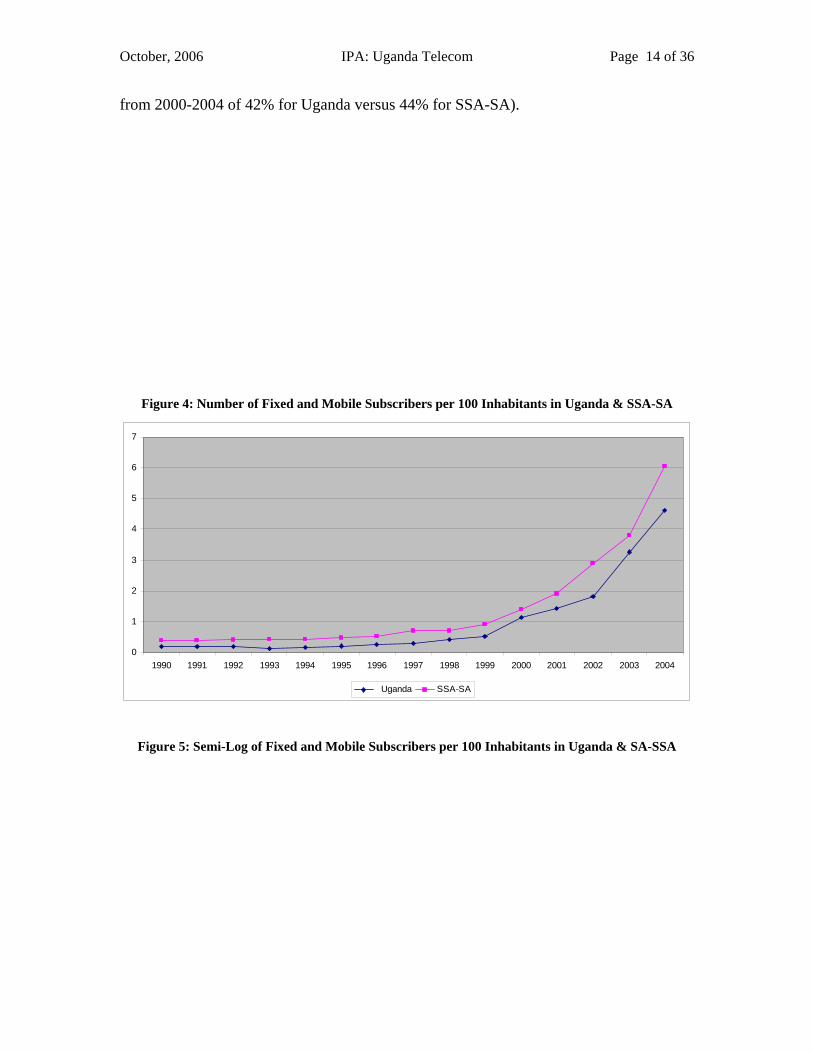

2.2.2. Technical Change Mobile technology has revolutionized telephony. We adjust for the role of technical change by noting that it also affected the rest of Sub-Saharan Africa (less South Africa: SSA-SA). We therefore proxy a technical change adjustment by comparing Uganda’s performance with that of SSA-SA. One way to do this is to observe that Uganda only moved up two places, to 30th in 2004. But there are a lot of small high-performing countries on the list so it is probably fairer to compare Uganda with the average for the region.

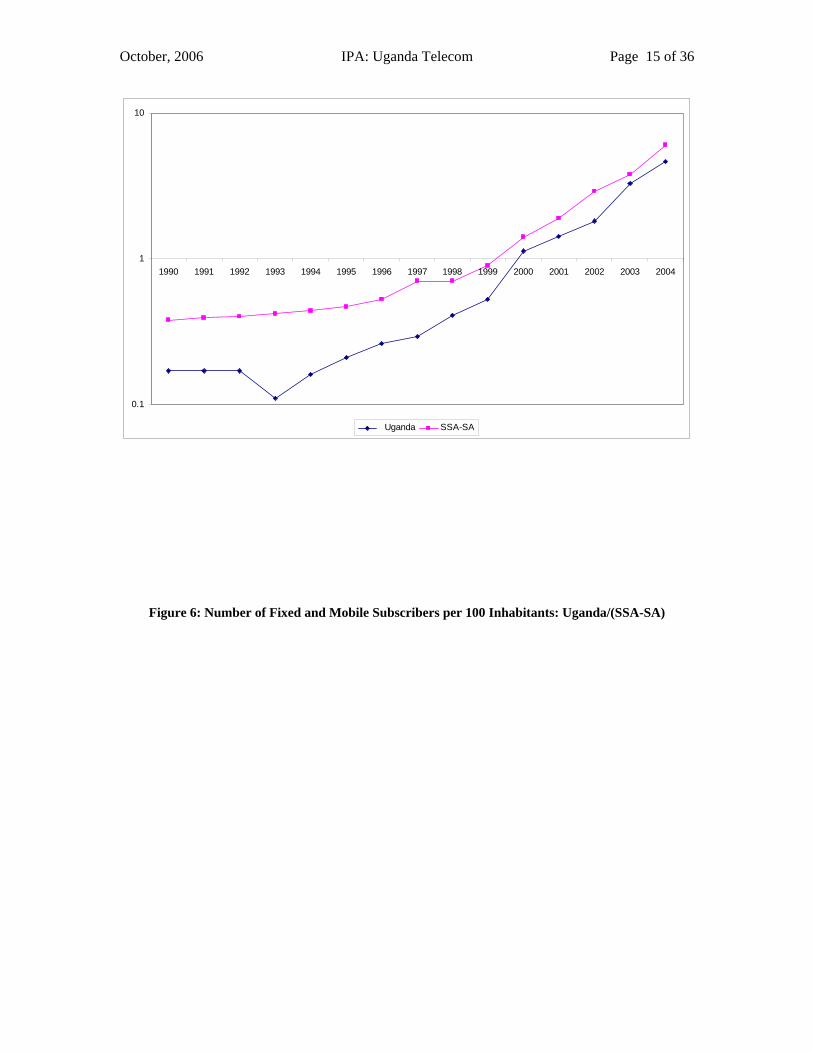

Figure 4 seems to show that as a first approximation, Uganda’s trajectory matches that of the SSA-SA average; it was only doing what everyone else was doing. But, as usual, a semi-log variant in Figure 5 gives a more accurate trend comparison. For the log averse, pretty much the same information can be had from Figure 6 which gives the Ugandan penetration ratio relative to that of SSA-SA. Both show clearly that from 1994 or 1995 through 2000, Uganda was playing catch-up, growing much more rapidly than SSA-SA (average annual compound rate of 40% versus 24%). Or, in Figure 6 terms, in this brief period it went from about 40% of the regional average to about 80%. After 2000, however, it only matched the regional growth rate and did not make further progress relative to the regional average. This was not because Uganda slowed down, but because the region speeded up (average annual compound growth rates

October, 2006 IPA: Uganda Telecom Page 14 of 36 from 2000-2004 of 42% for Uganda versus 44% for SSA-SA).

Figure 4: Number of Fixed and Mobile Subscribers per 100 Inhabitants in Uganda & SSA-SA

0

1

2

3

4

5

6

7

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Uganda SSA-SA

Figure 5: Semi-Log of Fixed and Mobile Subscribers per 100 Inhabitants in Uganda & SA-SSA

October, 2006 IPA: Uganda Telecom Page 15 of 36

0.1

1

10

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Uganda SSA-SA

Figure 6: Number of Fixed and Mobile Subscribers per 100 Inhabitants: Uganda/(SSA-SA)

October, 2006 IPA: Uganda Telecom Page 16 of 36

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

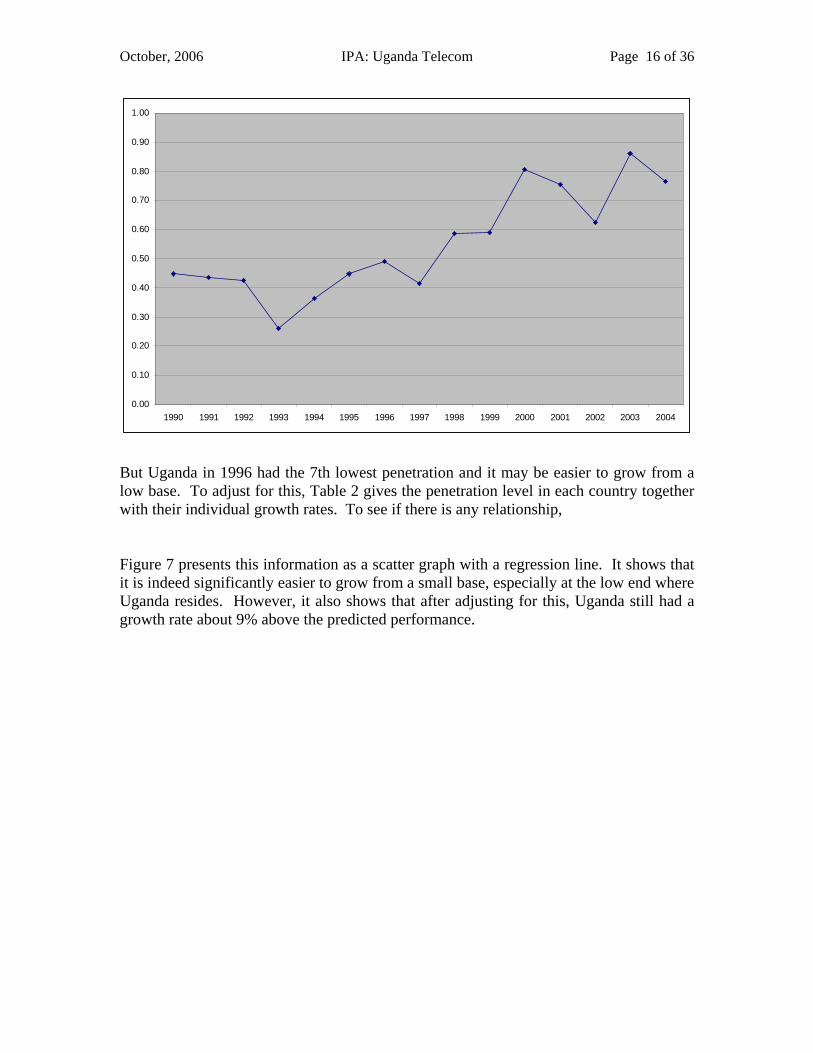

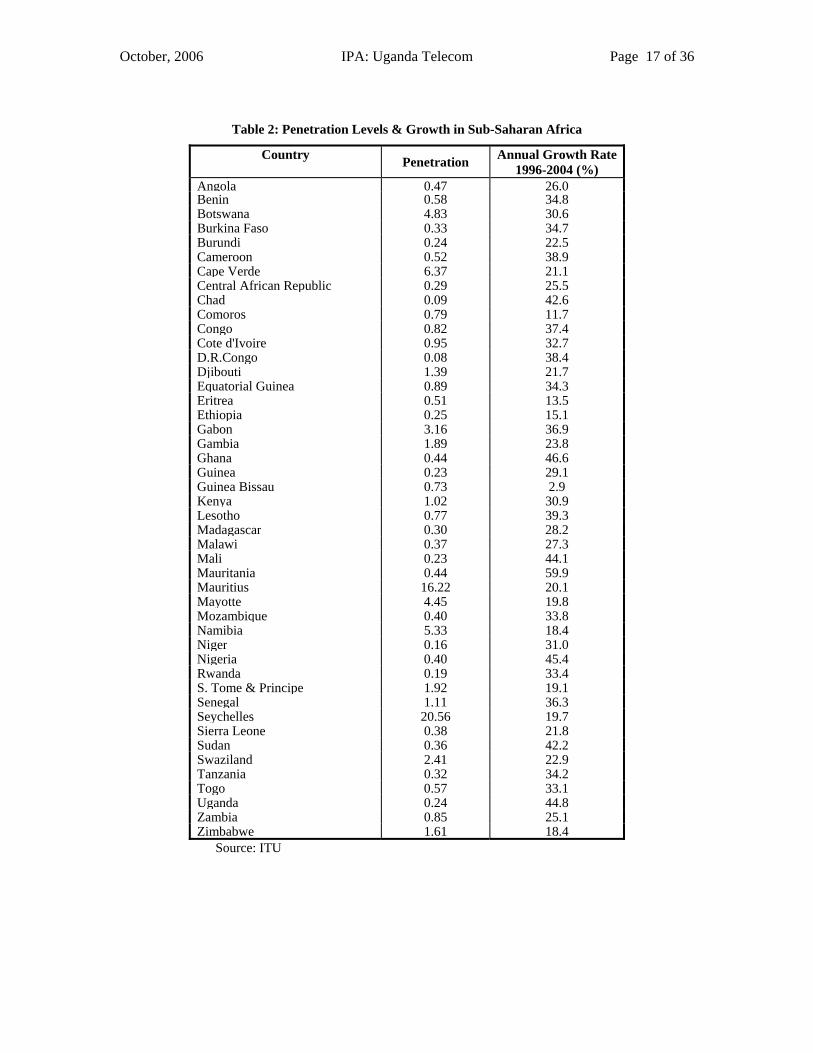

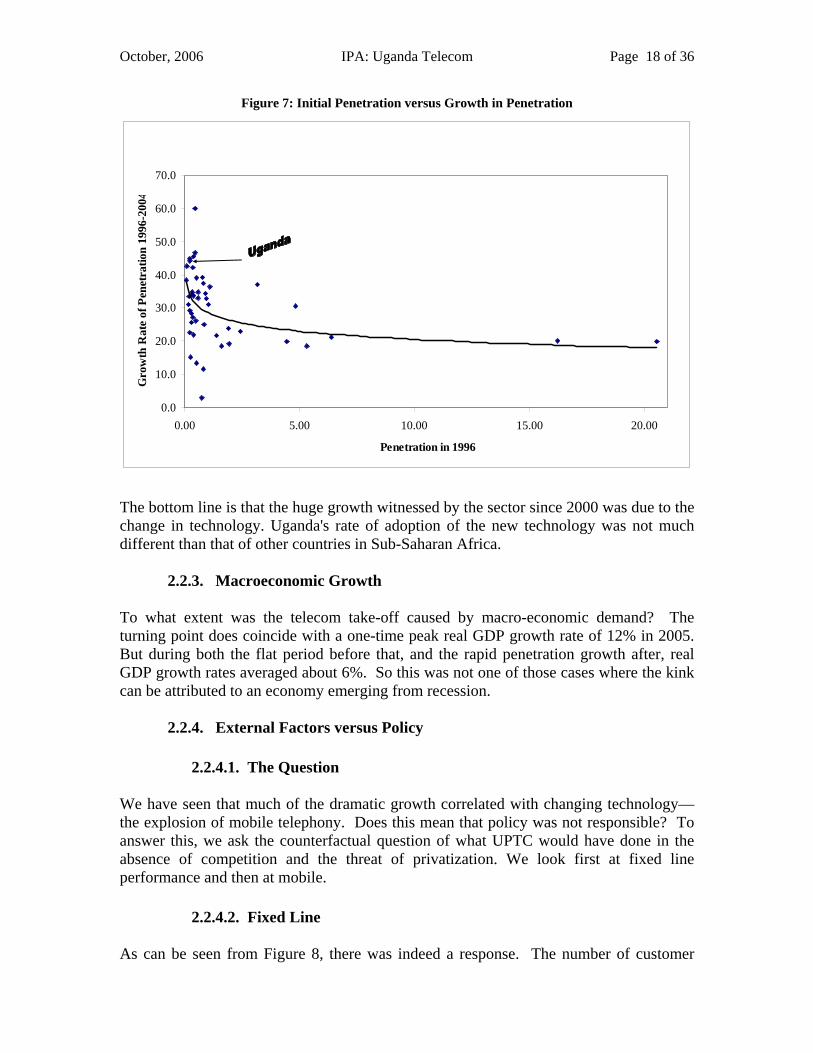

But Uganda in 1996 had the 7th lowest penetration and it may be easier to grow from a low base. To adjust for this, Table 2 gives the penetration level in each country together with their individual growth rates. To see if there is any relationship, Figure 7 presents this information as a scatter graph with a regression line. It shows that it is indeed significantly easier to grow from a small base, especially at the low end where Uganda resides. However, it also shows that after adjusting for this, Uganda still had a growth rate about 9% above the predicted performance.

October, 2006 IPA: Uganda Telecom Page 17 of 36

Table 2: Penetration Levels & Growth in Sub-Saharan Africa

Country Penetration Annual Growth Rate 1996-2004 (%)

Angola 0.47 26.0Benin 0.58 34.8Botswana 4.83 30.6Burkina Faso 0.33 34.7Burundi 0.24 22.5Cameroon 0.52 38.9Cape Verde 6.37 21.1Central African Republic 0.29 25.5Chad 0.09 42.6Comoros 0.79 11.7Congo 0.82 37.4Cote d'Ivoire 0.95 32.7D.R.Congo 0.08 38.4Djibouti 1.39 21.7Equatorial Guinea 0.89 34.3Eritrea 0.51 13.5Ethiopia 0.25 15.1Gabon 3.16 36.9Gambia 1.89 23.8Ghana 0.44 46.6Guinea 0.23 29.1Guinea Bissau 0.73 2.9Kenya 1.02 30.9Lesotho 0.77 39.3Madagascar 0.30 28.2Malawi 0.37 27.3Mali 0.23 44.1Mauritania 0.44 59.9Mauritius 16.22 20.1Mayotte 4.45 19.8Mozambique 0.40 33.8Namibia 5.33 18.4Niger 0.16 31.0Nigeria 0.40 45.4Rwanda 0.19 33.4S. Tome & Principe 1.92 19.1Senegal 1.11 36.3Seychelles 20.56 19.7Sierra Leone 0.38 21.8Sudan 0.36 42.2Swaziland 2.41 22.9Tanzania 0.32 34.2Togo 0.57 33.1Uganda 0.24 44.8Zambia 0.85 25.1Zimbabwe 1.61 18.4

Source: ITU

October, 2006 IPA: Uganda Telecom Page 18 of 36

Figure 7: Initial Penetration versus Growth in Penetration

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

0.00 5.00 10.00 15.00 20.00

Penetration in 1996

Gro

wth

Rat

e of

Pen

etra

tion

1996

-200

4

The bottom line is that the huge growth witnessed by the sector since 2000 was due to the change in technology. Uganda's rate of adoption of the new technology was not much different than that of other countries in Sub-Saharan Africa.

2.2.3. Macroeconomic Growth To what extent was the telecom take-off caused by macro-economic demand? The turning point does coincide with a one-time peak real GDP growth rate of 12% in 2005. But during both the flat period before that, and the rapid penetration growth after, real GDP growth rates averaged about 6%. So this was not one of those cases where the kink can be attributed to an economy emerging from recession.

2.2.4. External Factors versus Policy

2.2.4.1. The Question We have seen that much of the dramatic growth correlated with changing technology—the explosion of mobile telephony. Does this mean that policy was not responsible? To answer this, we ask the counterfactual question of what UPTC would have done in the absence of competition and the threat of privatization. We look first at fixed line performance and then at mobile.

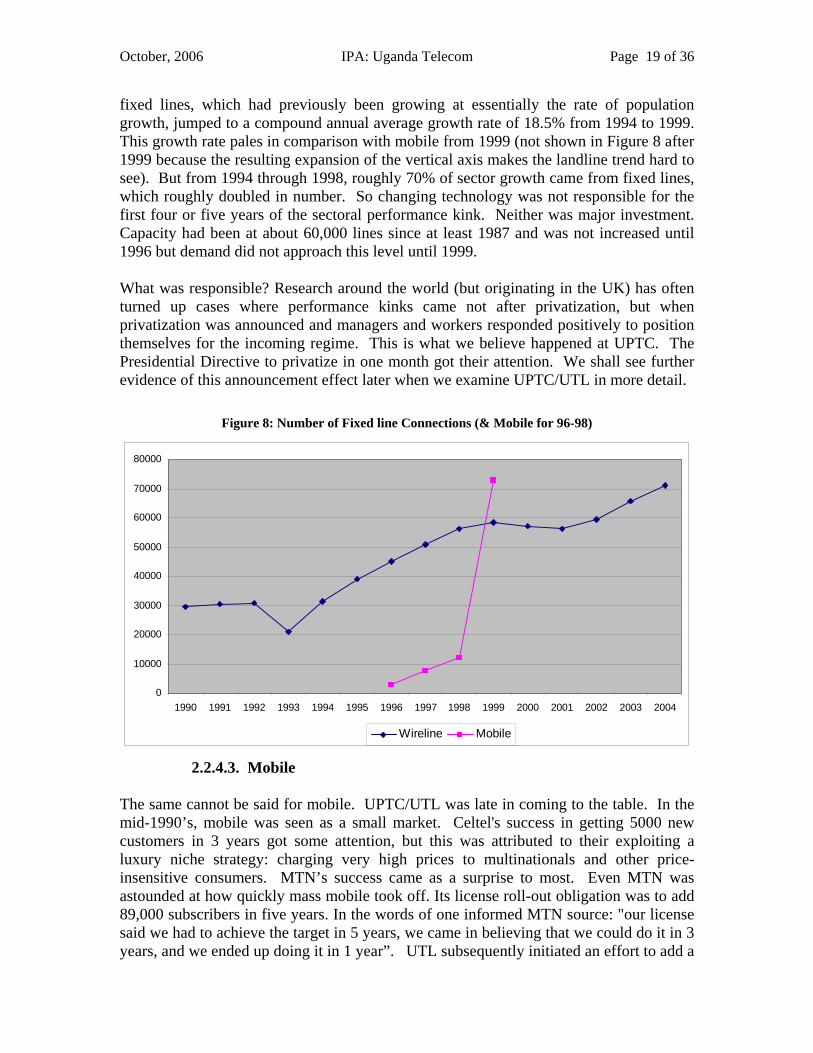

2.2.4.2. Fixed Line As can be seen from Figure 8, there was indeed a response. The number of customer

October, 2006 IPA: Uganda Telecom Page 19 of 36 fixed lines, which had previously been growing at essentially the rate of population growth, jumped to a compound annual average growth rate of 18.5% from 1994 to 1999. This growth rate pales in comparison with mobile from 1999 (not shown in Figure 8 after 1999 because the resulting expansion of the vertical axis makes the landline trend hard to see). But from 1994 through 1998, roughly 70% of sector growth came from fixed lines, which roughly doubled in number. So changing technology was not responsible for the first four or five years of the sectoral performance kink. Neither was major investment. Capacity had been at about 60,000 lines since at least 1987 and was not increased until 1996 but demand did not approach this level until 1999. What was responsible? Research around the world (but originating in the UK) has often turned up cases where performance kinks came not after privatization, but when privatization was announced and managers and workers responded positively to position themselves for the incoming regime. This is what we believe happened at UPTC. The Presidential Directive to privatize in one month got their attention. We shall see further evidence of this announcement effect later when we examine UPTC/UTL in more detail.

Figure 8: Number of Fixed line Connections (& Mobile for 96-98)

0

10000

20000

30000

40000

50000

60000

70000

80000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Wireline Mobile

2.2.4.3. Mobile The same cannot be said for mobile. UPTC/UTL was late in coming to the table. In the mid-1990’s, mobile was seen as a small market. Celtel's success in getting 5000 new customers in 3 years got some attention, but this was attributed to their exploiting a luxury niche strategy: charging very high prices to multinationals and other price-insensitive consumers. MTN’s success came as a surprise to most. Even MTN was astounded at how quickly mass mobile took off. Its license roll-out obligation was to add 89,000 subscribers in five years. In the words of one informed MTN source: "our license said we had to achieve the target in 5 years, we came in believing that we could do it in 3 years, and we ended up doing it in 1 year”. UTL subsequently initiated an effort to add a

October, 2006 IPA: Uganda Telecom Page 20 of 36 mobile arm, but difficulties getting government approval for the necessary investment meant that a go-ahead was not given until after privatization and their mobile service did not begin until 2001.

2.2.4.4. Conclusion So, our conclusion is that the reforms indeed were responsible for the improved performance. This is obviously the case for MTN and Celtel mobile, but also for UTL mobile, as privatization released the investment constraint which precluded entry under public ownership. For fixed line as well, it was the threat of privatization which focused the company’s attention and turned things around. These policy reforms were enabling, in that without them, Uganda would not have been able to take advantage of the mobile revolution until much later and then much more slowly. 3. WHAT WERE THE UTL RESULTS?

3.1. Enterprise Performance We now look at the impact on stakeholders. We start with the enterprise and then look at employees, government and consumers.

3.1.1. Surplus Generation

3.1.1.1. Data Limitations The data for the privatized UTL were derived from the company's detailed audited financial statements. Financial statements for the public UTL (February 1998-June 2000) were audited but provided no details of revenues or expenses. For the pre-February 1998 period, financial statements were not audited and were provided for UPTC, including both postal and telecommunications activities. A documented attempt to separate telecommunications from postal accounts was made by an outside consulting firm for the year ending June 1995. We applied that year's breakdown of revenues and of operating expenses to the totals for the other years of pre-private operation to obtain consistent historical series for 1994-2004. Therefore, one needs to exercise caution in interpreting financial numbers for the pre-private UTL: they should be looked at as "order-of-magnitude" rather than precise figures. Because of this caveat we shall do a less detailed analysis then we usually do.

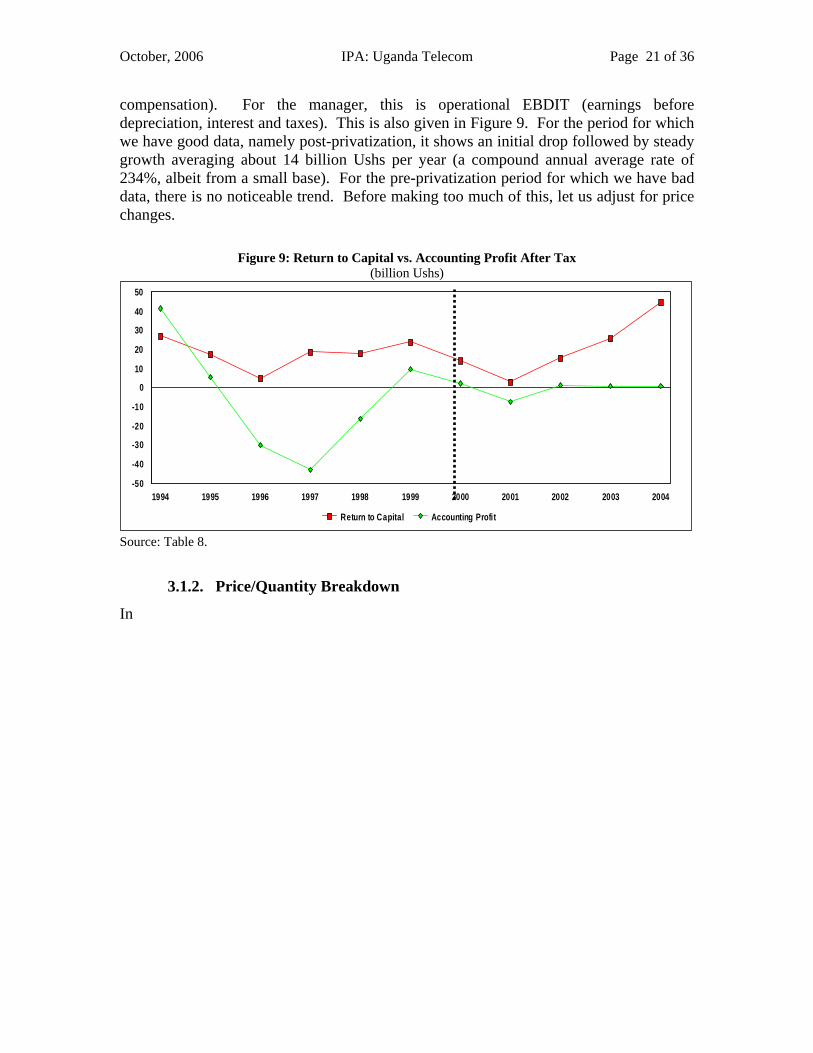

3.1.1.2. Profit and Total Return to Capital Figure 9 gives the profit trend, for convention's sake and not because it tells much about efficiency. As a single example, the very high profit of 41 million Ushs in 1994 included 16 million for write-back of debts previously written off and 16 million for gain on foreign exchange (primarily the reduced Ushs value of debt due to currency appreciation). We therefore prefer to look at what we call Total Return to Capital (TRC). For economists, this is quasi-rents (sales revenue less intermediates less total employee

October, 2006 IPA: Uganda Telecom Page 21 of 36 compensation). For the manager, this is operational EBDIT (earnings before depreciation, interest and taxes). This is also given in Figure 9. For the period for which we have good data, namely post-privatization, it shows an initial drop followed by steady growth averaging about 14 billion Ushs per year (a compound annual average rate of 234%, albeit from a small base). For the pre-privatization period for which we have bad data, there is no noticeable trend. Before making too much of this, let us adjust for price changes.

Figure 9: Return to Capital vs. Accounting Profit After Tax (billion Ushs)

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004-50

-40

-30

-20

-10

0

10

20

30

40

50

Return to Capital Accounting Profit

Source: Table 8.

3.1.2. Price/Quantity Breakdown In

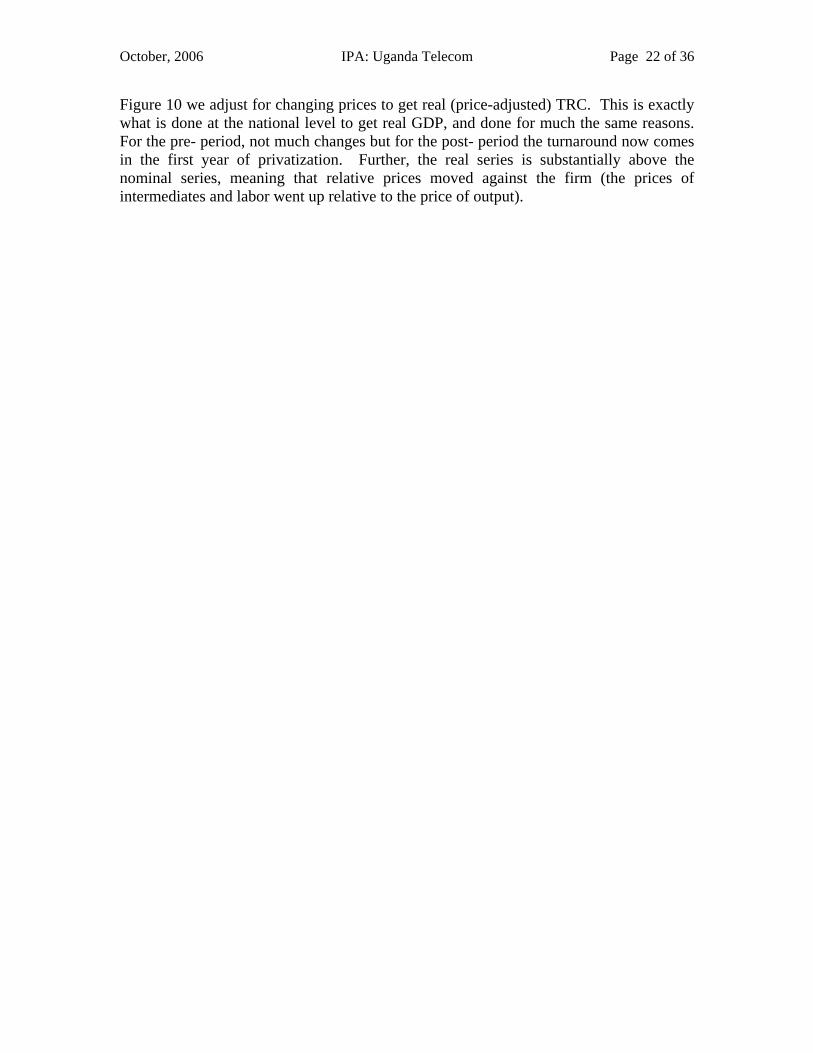

October, 2006 IPA: Uganda Telecom Page 22 of 36 Figure 10 we adjust for changing prices to get real (price-adjusted) TRC. This is exactly what is done at the national level to get real GDP, and done for much the same reasons. For the pre- period, not much changes but for the post- period the turnaround now comes in the first year of privatization. Further, the real series is substantially above the nominal series, meaning that relative prices moved against the firm (the prices of intermediates and labor went up relative to the price of output).

October, 2006 IPA: Uganda Telecom Page 23 of 36

Figure 10: Return to Capital (current vs constant prices) (billion Ushs)

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 20040

10

20

30

40

50

60

70

80

90

Current Prices Constant 1999 Prices

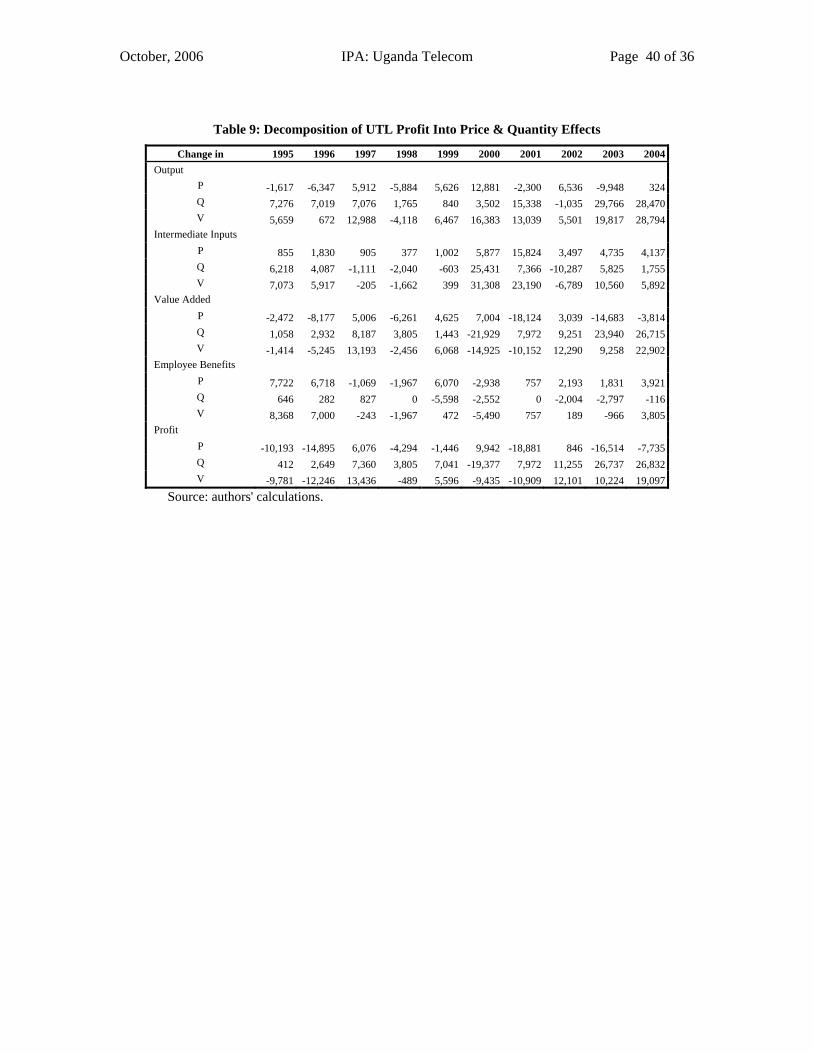

Sources: Table 6 and Table 7. To see this more clearly, we have decomposed changes in each category into price and quantity effects (

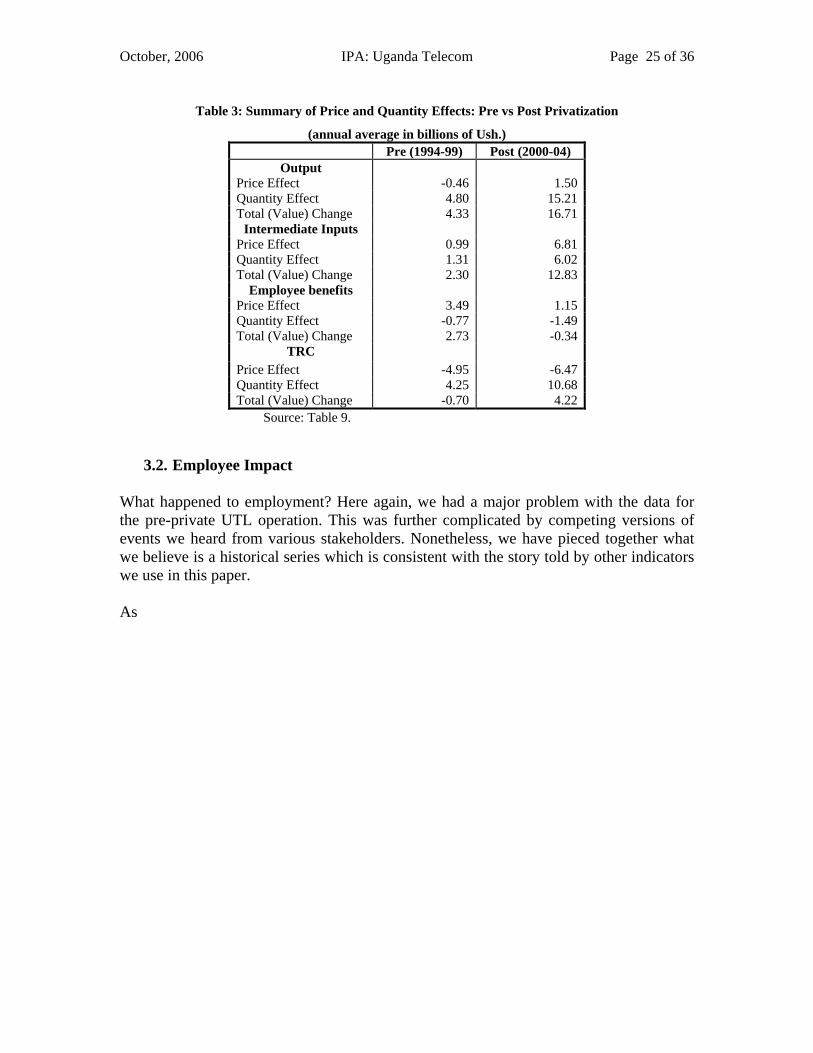

October, 2006 IPA: Uganda Telecom Page 24 of 36 Table 3).5 To interpret the table, look at the lower right hand triplet. It says that after privatization TRC increased by an average of 4 billion Ushs. But prices moved against the firm, lowering profits by 7 billion, more than offset by an 11 billion gain in real terms. That is, efficiency improved post privatization. This is a common result. But the pre-privatization result is uncommon. Typically one sees negative quantity effects compensated for by large output price increases as the government tries to keep the inefficient enterprise financially viable. Not in this case. Here we have positive quantity effects offset by negative price effects. This may well be an artifact of imperfect data. But it is consistent with an intriguing hypothesis. First, we would conjecture that prior to 1993 the traditional relationship held (policy pricing masking inefficiency). Then the numbers below would reflect another manifestation of the announcement effect we saw in fixed line expansion, with efficiency also improving after the Presidential Directive. It did not improve nearly as rapidly pre-privatization as it did post-, but it did improve.

5 Using a discrete Divisia indexing procedure and allocating the cross product proportionally to the main products.

October, 2006 IPA: Uganda Telecom Page 25 of 36

Table 3: Summary of Price and Quantity Effects: Pre vs Post Privatization

(annual average in billions of Ush.) Pre (1994-99) Post (2000-04)

Output Price Effect -0.46 1.50 Quantity Effect 4.80 15.21 Total (Value) Change 4.33 16.71

Intermediate Inputs Price Effect 0.99 6.81 Quantity Effect 1.31 6.02 Total (Value) Change 2.30 12.83

Employee benefits Price Effect 3.49 1.15 Quantity Effect -0.77 -1.49 Total (Value) Change 2.73 -0.34

TRC Price Effect -4.95 -6.47 Quantity Effect 4.25 10.68 Total (Value) Change -0.70 4.22

Source: Table 9.

3.2. Employee Impact What happened to employment? Here again, we had a major problem with the data for the pre-private UTL operation. This was further complicated by competing versions of events we heard from various stakeholders. Nonetheless, we have pieced together what we believe is a historical series which is consistent with the story told by other indicators we use in this paper. As

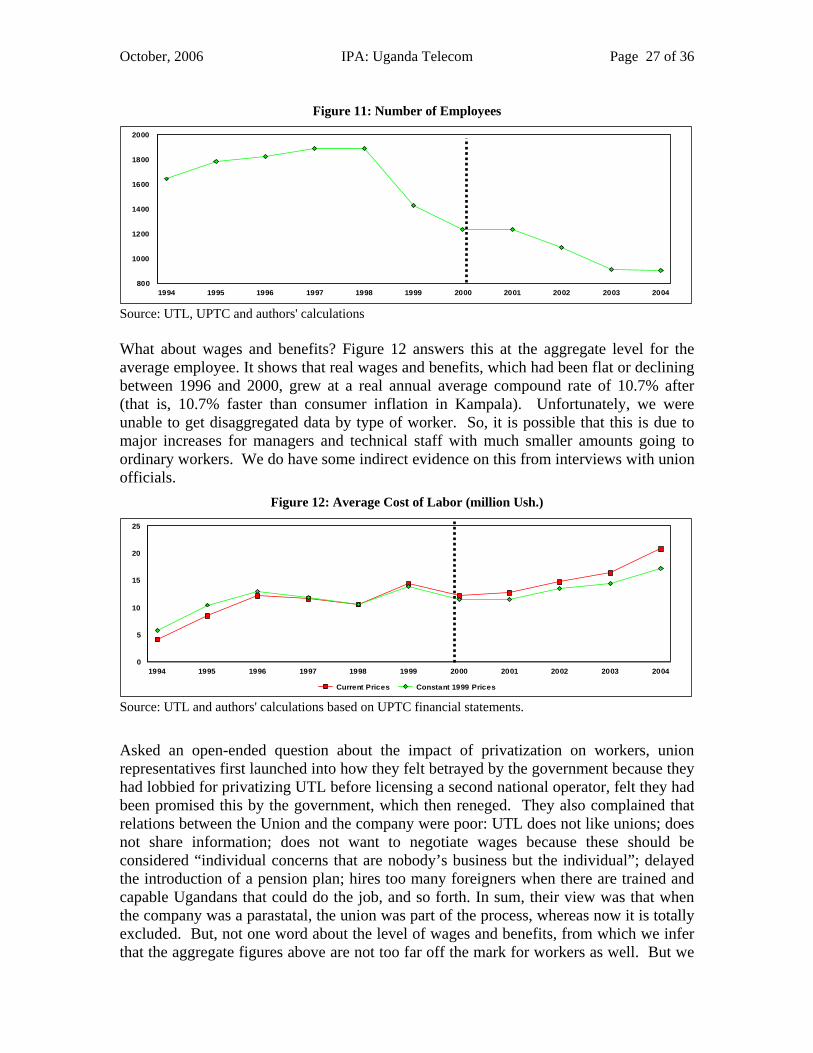

October, 2006 IPA: Uganda Telecom Page 26 of 36 Figure 11 shows, privatization resulted in a noticeable decline which continued until 2003. The new public UTL shed 25% of its workforce (461 employees) within one year of operation and another 13% in the following year. So by the time the private UTL took over, the company had only 65% of its 1997 workforce. This decline can, therefore, be fully attributed to the reform. The private UTL found it necessary, we believe most probably because of competitive pressure, to introduce further cuts of 12% and 16% in 2001 and 2002 respectively to stabilize its workforce at the 2004 level of 907 workers. So in terms of number of workers, there is little doubt that a significant number was cut.

October, 2006 IPA: Uganda Telecom Page 27 of 36

Figure 11: Number of Employees

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004800

1000

1200

1400

1600

1800

2000

Source: UTL, UPTC and authors' calculations What about wages and benefits? Figure 12 answers this at the aggregate level for the average employee. It shows that real wages and benefits, which had been flat or declining between 1996 and 2000, grew at a real annual average compound rate of 10.7% after (that is, 10.7% faster than consumer inflation in Kampala). Unfortunately, we were unable to get disaggregated data by type of worker. So, it is possible that this is due to major increases for managers and technical staff with much smaller amounts going to ordinary workers. We do have some indirect evidence on this from interviews with union officials.

Figure 12: Average Cost of Labor (million Ush.)

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 20040

5

10

15

20

25

Current Prices Constant 1999 Prices Source: UTL and authors' calculations based on UPTC financial statements.

Asked an open-ended question about the impact of privatization on workers, union representatives first launched into how they felt betrayed by the government because they had lobbied for privatizing UTL before licensing a second national operator, felt they had been promised this by the government, which then reneged. They also complained that relations between the Union and the company were poor: UTL does not like unions; does not share information; does not want to negotiate wages because these should be considered “individual concerns that are nobody’s business but the individual”; delayed the introduction of a pension plan; hires too many foreigners when there are trained and capable Ugandans that could do the job, and so forth. In sum, their view was that when the company was a parastatal, the union was part of the process, whereas now it is totally excluded. But, not one word about the level of wages and benefits, from which we infer that the aggregate figures above are not too far off the mark for workers as well. But we

October, 2006 IPA: Uganda Telecom Page 28 of 36 can’t be sure without disaggregated data. To summarize our findings on labor: a substantial amount of labor shedding occurred following the privatization announcement but pre-dating privatization; the private operator continued the layoffs but at a much reduced pace; but benefits of remaining employees rose continuously after privatization. So this group of workers certainly gained. Should this gain (and job losses since 2000) be attributed to privatization or to competition? To answer this question we need to do a comparative unit labor analysis with UTL's competitors, which unfortunately we were not able to obtain. But if we had to guess, we would lean toward attributing the lion's share of this development to competition: the market is a far more effective and ruthless disciplinarian than government regulations.

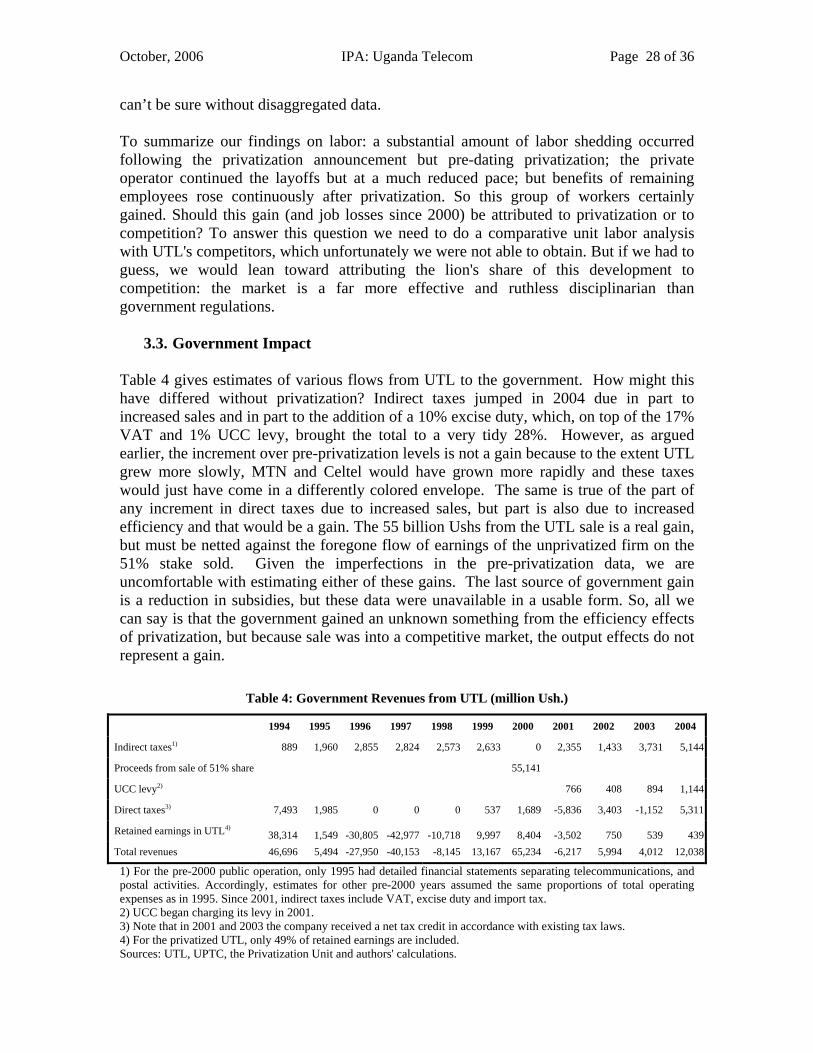

3.3. Government Impact Table 4 gives estimates of various flows from UTL to the government. How might this have differed without privatization? Indirect taxes jumped in 2004 due in part to increased sales and in part to the addition of a 10% excise duty, which, on top of the 17% VAT and 1% UCC levy, brought the total to a very tidy 28%. However, as argued earlier, the increment over pre-privatization levels is not a gain because to the extent UTL grew more slowly, MTN and Celtel would have grown more rapidly and these taxes would just have come in a differently colored envelope. The same is true of the part of any increment in direct taxes due to increased sales, but part is also due to increased efficiency and that would be a gain. The 55 billion Ushs from the UTL sale is a real gain, but must be netted against the foregone flow of earnings of the unprivatized firm on the 51% stake sold. Given the imperfections in the pre-privatization data, we are uncomfortable with estimating either of these gains. The last source of government gain is a reduction in subsidies, but these data were unavailable in a usable form. So, all we can say is that the government gained an unknown something from the efficiency effects of privatization, but because sale was into a competitive market, the output effects do not represent a gain.

Table 4: Government Revenues from UTL (million Ush.)

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Indirect taxes1) 889 1,960 2,855 2,824 2,573 2,633 0 2,355 1,433 3,731 5,144

Proceeds from sale of 51% share 55,141

UCC levy2) 766 408 894 1,144

Direct taxes3) 7,493 1,985 0 0 0 537 1,689 -5,836 3,403 -1,152 5,311

Retained earnings in UTL4) 38,314 1,549 -30,805 -42,977 -10,718 9,997 8,404 -3,502 750 539 439 Total revenues 46,696 5,494 -27,950 -40,153 -8,145 13,167 65,234 -6,217 5,994 4,012 12,038

1) For the pre-2000 public operation, only 1995 had detailed financial statements separating telecommunications, and postal activities. Accordingly, estimates for other pre-2000 years assumed the same proportions of total operating expenses as in 1995. Since 2001, indirect taxes include VAT, excise duty and import tax. 2) UCC began charging its levy in 2001. 3) Note that in 2001 and 2003 the company received a net tax credit in accordance with existing tax laws. 4) For the privatized UTL, only 49% of retained earnings are included. Sources: UTL, UPTC, the Privatization Unit and authors' calculations.

October, 2006 IPA: Uganda Telecom Page 29 of 36

3.4. Consumer Impact

3.4.1. Mobile

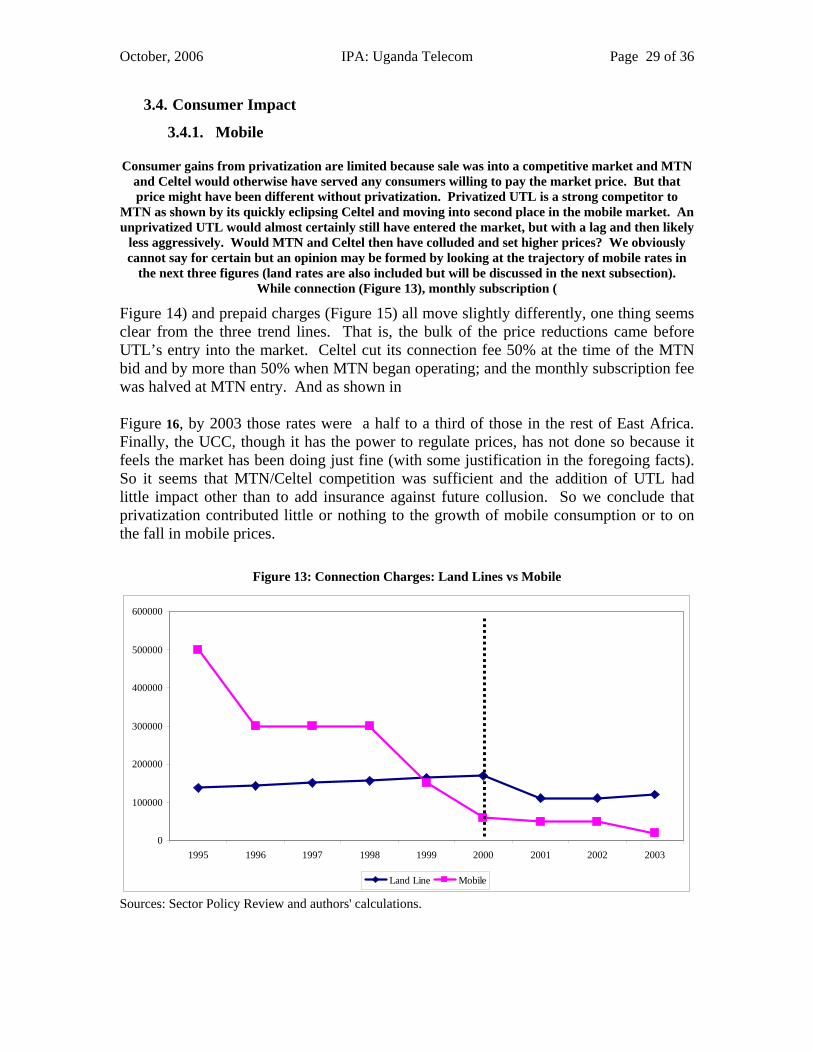

Consumer gains from privatization are limited because sale was into a competitive market and MTN and Celtel would otherwise have served any consumers willing to pay the market price. But that price might have been different without privatization. Privatized UTL is a strong competitor to

MTN as shown by its quickly eclipsing Celtel and moving into second place in the mobile market. An unprivatized UTL would almost certainly still have entered the market, but with a lag and then likely

less aggressively. Would MTN and Celtel then have colluded and set higher prices? We obviously cannot say for certain but an opinion may be formed by looking at the trajectory of mobile rates in

the next three figures (land rates are also included but will be discussed in the next subsection). While connection (Figure 13), monthly subscription (

Figure 14) and prepaid charges (Figure 15) all move slightly differently, one thing seems clear from the three trend lines. That is, the bulk of the price reductions came before UTL’s entry into the market. Celtel cut its connection fee 50% at the time of the MTN bid and by more than 50% when MTN began operating; and the monthly subscription fee was halved at MTN entry. And as shown in Figure 16, by 2003 those rates were a half to a third of those in the rest of East Africa. Finally, the UCC, though it has the power to regulate prices, has not done so because it feels the market has been doing just fine (with some justification in the foregoing facts). So it seems that MTN/Celtel competition was sufficient and the addition of UTL had little impact other than to add insurance against future collusion. So we conclude that privatization contributed little or nothing to the growth of mobile consumption or to on the fall in mobile prices.

Figure 13: Connection Charges: Land Lines vs Mobile

0

100000

200000

300000

400000

500000

600000

1995 1996 1997 1998 1999 2000 2001 2002 2003

Land Line Mobile

Sources: Sector Policy Review and authors' calculations.

October, 2006 IPA: Uganda Telecom Page 30 of 36

Figure 14: Monthly Subscription Fee: Land Lines vs Mobile

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

1995 1996 1997 1998 1999 2000 2001 2002 2003

Land Line Mobile

Sources: Sector Policy Review and authors' calculations.

Figure 15: Selected Local Mobile Prepaid Rates

0

50

100

150

200

250

300

350

400

450

500

1995 1996 1997 1998 1999 2000 2001 2002 2003

Within Own Network Other Mobile Network To Fixed Line

Sources: Sector Policy Review and authors' calculations.

October, 2006 IPA: Uganda Telecom Page 31 of 36

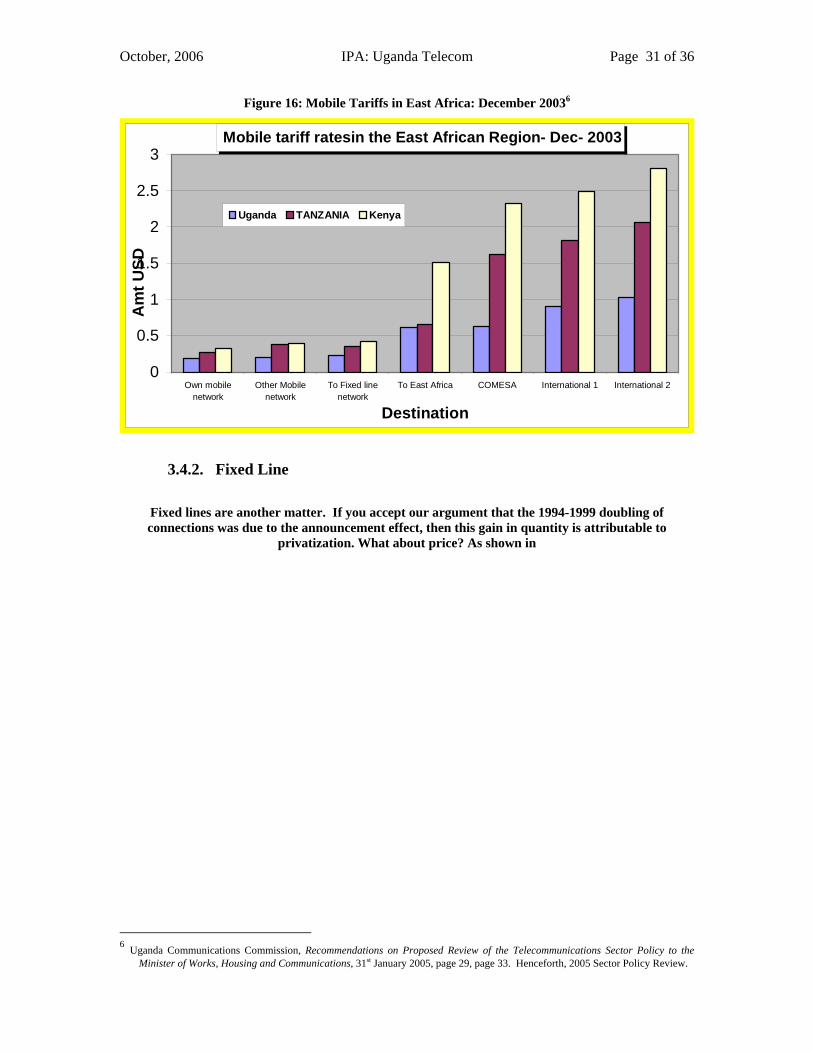

Figure 16: Mobile Tariffs in East Africa: December 20036

Mobile tariff ratesin the East African Region- Dec- 2003

0

0.5

1

1.5

2

2.5

3

Own mobilenetwork

Other Mobilenetwork

To Fixed linenetwork

To East Africa COMESA International 1 International 2

Destination

Am

t USD

Uganda TANZANIA Kenya

3.4.2. Fixed Line

Fixed lines are another matter. If you accept our argument that the 1994-1999 doubling of connections was due to the announcement effect, then this gain in quantity is attributable to

privatization. What about price? As shown in

6 Uganda Communications Commission, Recommendations on Proposed Review of the Telecommunications Sector Policy to the

Minister of Works, Housing and Communications, 31st January 2005, page 29, page 33. Henceforth, 2005 Sector Policy Review.

October, 2006 IPA: Uganda Telecom Page 32 of 36

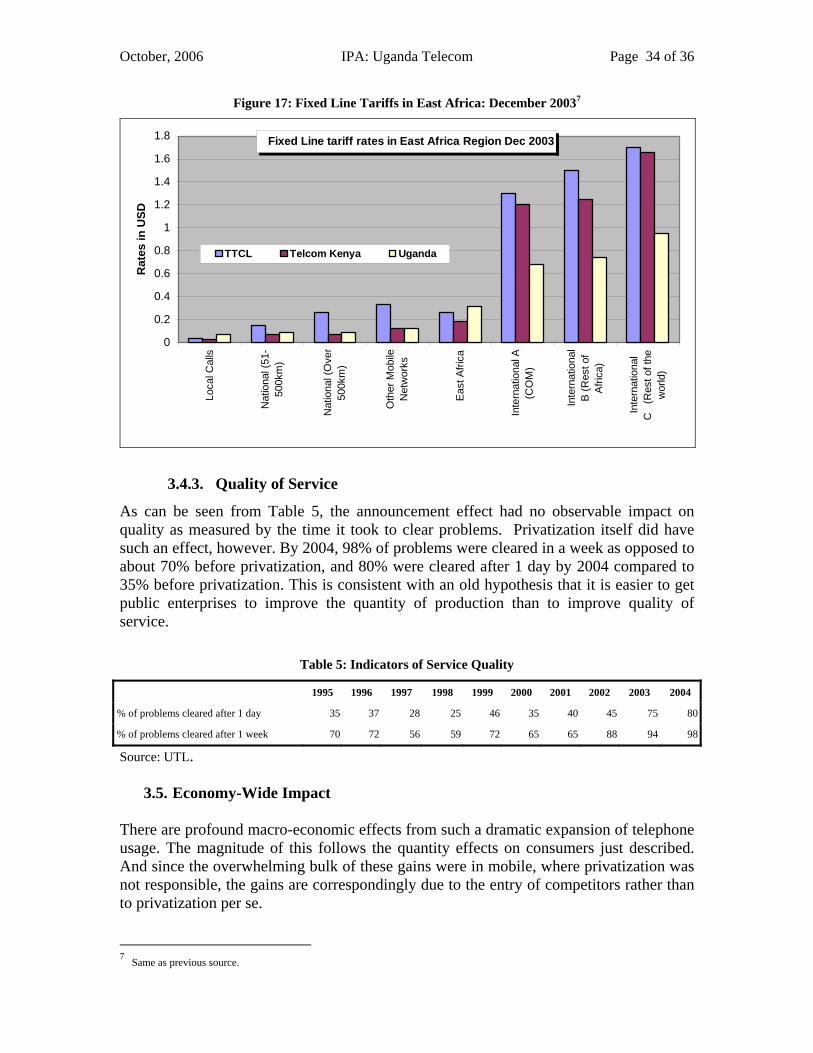

Figure 17, in marked contrast to mobile prices, fixed line prices in Uganda are higher than elsewhere in East Africa in 2003. How did they get this way? As show above in Figure 13 and

Figure 14, connection and subscription fees both moved up steadily pre-privatization (compound average annual growth rates of 4.4% and 10.8% respectively) and then were rebalanced in 2001 with a sharp drop in connection fees offsetting a sharp increase in subscription fees. As shown in Table 7 in the appendix, the net effect of the rebalancing (including changes in other charges and changes in product mix) was to lower prices. But that was only one year, and as was shown in

October, 2006 IPA: Uganda Telecom Page 33 of 36 Table 3, the net effect of pre-privatization output price charges was to annually increase revenues by only 0.08 Ushs billion, versus 1.59 after. So a case can be made that privatized UTL was either more profit-oriented or smarter about mixing prices to maximize revenue and therefore consumers lost about 1.5 billion due to privatization. But the gain in consumer surplus on the 30,000 additional lines pre-privatization still made them net winners.

October, 2006 IPA: Uganda Telecom Page 34 of 36

Figure 17: Fixed Line Tariffs in East Africa: December 20037

Fixed Line tariff rates in East Africa Region Dec 2003

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Loca

l Cal

ls

Nat

iona

l (51

-50

0km

)

Nat

iona

l (O

ver

500k

m)

Oth

er M

obile

Net

wor

ks

Eas

t Afri

ca

Inte

rnat

iona

l A(C

OM

)

Inte

rnat

iona

lB

(Res

t of

Afri

ca)

Inte

rnat

iona

lC

(R

est o

f the

wor

ld)

Rat

es in

USD

TTCL Telcom Kenya Uganda

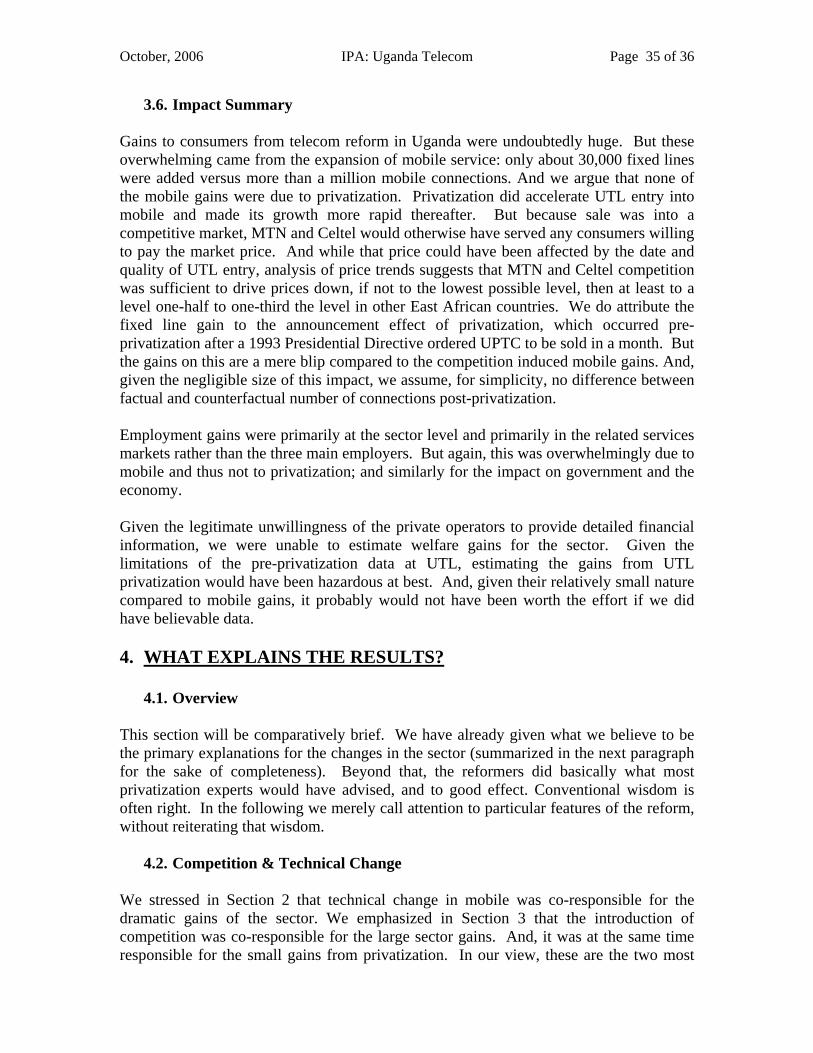

3.4.3. Quality of Service As can be seen from Table 5, the announcement effect had no observable impact on quality as measured by the time it took to clear problems. Privatization itself did have such an effect, however. By 2004, 98% of problems were cleared in a week as opposed to about 70% before privatization, and 80% were cleared after 1 day by 2004 compared to 35% before privatization. This is consistent with an old hypothesis that it is easier to get public enterprises to improve the quantity of production than to improve quality of service.

Table 5: Indicators of Service Quality

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

% of problems cleared after 1 day 35 37 28 25 46 35 40 45 75 80

% of problems cleared after 1 week 70 72 56 59 72 65 65 88 94 98

Source: UTL.

3.5. Economy-Wide Impact There are profound macro-economic effects from such a dramatic expansion of telephone usage. The magnitude of this follows the quantity effects on consumers just described. And since the overwhelming bulk of these gains were in mobile, where privatization was not responsible, the gains are correspondingly due to the entry of competitors rather than to privatization per se. 7 Same as previous source.

October, 2006 IPA: Uganda Telecom Page 35 of 36

3.6. Impact Summary Gains to consumers from telecom reform in Uganda were undoubtedly huge. But these overwhelming came from the expansion of mobile service: only about 30,000 fixed lines were added versus more than a million mobile connections. And we argue that none of the mobile gains were due to privatization. Privatization did accelerate UTL entry into mobile and made its growth more rapid thereafter. But because sale was into a competitive market, MTN and Celtel would otherwise have served any consumers willing to pay the market price. And while that price could have been affected by the date and quality of UTL entry, analysis of price trends suggests that MTN and Celtel competition was sufficient to drive prices down, if not to the lowest possible level, then at least to a level one-half to one-third the level in other East African countries. We do attribute the fixed line gain to the announcement effect of privatization, which occurred pre-privatization after a 1993 Presidential Directive ordered UPTC to be sold in a month. But the gains on this are a mere blip compared to the competition induced mobile gains. And, given the negligible size of this impact, we assume, for simplicity, no difference between factual and counterfactual number of connections post-privatization. Employment gains were primarily at the sector level and primarily in the related services markets rather than the three main employers. But again, this was overwhelmingly due to mobile and thus not to privatization; and similarly for the impact on government and the economy. Given the legitimate unwillingness of the private operators to provide detailed financial information, we were unable to estimate welfare gains for the sector. Given the limitations of the pre-privatization data at UTL, estimating the gains from UTL privatization would have been hazardous at best. And, given their relatively small nature compared to mobile gains, it probably would not have been worth the effort if we did have believable data. 4. WHAT EXPLAINS THE RESULTS?

4.1. Overview This section will be comparatively brief. We have already given what we believe to be the primary explanations for the changes in the sector (summarized in the next paragraph for the sake of completeness). Beyond that, the reformers did basically what most privatization experts would have advised, and to good effect. Conventional wisdom is often right. In the following we merely call attention to particular features of the reform, without reiterating that wisdom.

4.2. Competition & Technical Change We stressed in Section 2 that technical change in mobile was co-responsible for the dramatic gains of the sector. We emphasized in Section 3 that the introduction of competition was co-responsible for the large sector gains. And, it was at the same time responsible for the small gains from privatization. In our view, these are the two most

October, 2006 IPA: Uganda Telecom Page 36 of 36 important determinants of the results.

4.3. Privatization, Investment and Competition The contribution of privatization to the process came primarily through the conversion of a non-competitive competitor into a competitive one. The standard reasons for this apply: conversion from public incentive systems to private ones and the removal of bureaucratic obstacles. However, we suggest that a particularly large constraint on the public firms competitiveness was the unwillingness of the government to approve new investments. Relaxing that constraint was a key contribution of privatization.

4.4. Sequencing

4.4.1. Competition or Privatization First? The executive branch wanted to issue the SNO permit expeditiously, without waiting for privatization. But Parliament specified the reverse in the 1997 Telecom Act, (that is, first privatize, then allow the SNO). Their argument was that this would maximize revenue from the sale. The executive branch stuck to its guns, and got a reversal on the very day MTN was announced as the winning bidder. This was a critical decision and the executive branch is to be congratulated for persevering.. Experience in country after country shows that the largest share of government returns come not from the initial sale price but from taxes on increasingly productive and profitable operations. As a single illustration for Uganda, UTL’s sale brought in 55 Ushs billion, but by 2004, annual indirect taxes alone on the sector were about 200 billion. The argument here is not that competition should always come first. Rather, it is that both are good and should be done as quickly as possible given political, legal and market constraints. Neither should be delayed for the other.

4.4.2. Regulation or Private Participation First? Conventional privatization wisdom has it that regulation should precede any form of private participation in infrastructure. Otherwise, responsible bidders will either not bid, or will bid low in the face of infinite uncertainty of how price, the principle determinant of their profitability, will be set. Uganda violated this in that the regulator did not come on board until 4 years after Celtel and 3 years after MTN. But key regulation was in place in the form of the licenses, which critically specified a price cap. So the key feature of uncertainty was removed.

4.5. Speed The initial decision to privatize UPTC in a month was a bit fast. The actual privatization of UTL took seven years, which was a bit slow. What would have been “just right”, and why did it take so long in Uganda? A key temporal constraint is the time needed to be sure that all parties know just what is being sold. UPTC accounts were unreliable at best and needed in any event telecom to be disentangled from post and banking. Failure to do

October, 2006 IPA: Uganda Telecom Page 37 of 36 this has led to buyer’s curse in other privatizations and led to either exit or serious disputes when the new owners discovered that information in the bid documents was erroneous. This step also included introducing competition, setting up a regulatory regime and clarifying the legal environment, because for an imperfectly competitive sector, that is a key determinant of the market that is being bought. After that the buyer needs time to do due diligence on the results. Then the seller needs to do its due diligence on the buyer, to avoid seller’s curse, a fate suffered by governments in several of our companion studies. A second key temporal constraint is the time necessary to generate consensus among important stakeholders. On each of these counts, Uganda did these jobs well. But why did it take so long? Because there was considerable opposition, especially among workers and their supporters in Parliament

4.6. Executive Commitment We have seen that when the President acted in 1993, UPTC responded. We saw the same thing in our study of Uganda’s water sector, where reforms were initiated in 1998 but performance turned around in 1995 or earlier. We don’t want to generalize to an entire economy from two examples, but the two do make us very sympathetic to Byaruhanga’s argument that a key factor was the executive branch’s commitment to liberalizing the economy.

“The new Government, having taken power from a largely socialist, though pragmatic ideological base was initially averse to private entrepreneurship and by extension private investment, opting for a command style approach to economic management…. (Various problems)…led to major re-think of this approach to economic management. The shift in economic management paradigm largely took place within the President’s Economic Council (PEC), where over time debate between ministers and senior officials shifted thinking towards increasing market orientation to economic management.“ 8 “Critical to the success of the reform was the unequivocal support provided by political leadership in the Executive. The President was particularly concerned about the constraints to investment posed by the malaise and inefficiencies in the sector and actively promoted reform and implementation. While there were interventions from Parliament that seemingly sought to reverse aspects of the reform process, particularly the sale of the Second National Operator license and UTL itself, unwavering commitment on the part of the Executive enabled the reform to stay on track.”9

8 Byarahunga, page 7. 9 Byarahunga, page 22.

October, 2006 IPA: Uganda Telecom Page 38 of 36

4.7. Highly Capable Technocrats One important manifestation of the foregoing is that merit was apparently the primary criterion for appointing the technocrats responsible for designing, motivating and implementing the reforms. That, at least, is the conclusion we draw from interacting with some of them and viewing the written work of others. 5. CONCLUSION This paper breaks little new ground at the sector level. The process and consequences of the reforms were already well known because of three previous excellent papers.. The success of the reform package was manifest in the rapid adoption of the new mobile technology, with Uganda gaining on a rapidly moving target by going from 40% of the Sub-Saharan average penetration ratio in1994 to 80% in 2004. One of our tasks was to ask how privatization per se contributed to these results. We conclude that it contributed only a little, with the introduction of private competition being the primary factor behind the impressive gains. We had hoped to add further value by doing an explicit quantification of costs and benefits by stakeholder, but data limitations precluded this. It is nonetheless a useful addition to our set of eight case studies because it shows that divesting into a functionally competitive market will generate no gains for consumers because other suppliers would otherwise have provided equivalent products. The same is true for government so far as taxes go and for any impact on the broader economy. The government, the buyer and workers can still benefit from improved efficiency, but total gains are likely to be smaller than for non-competitive privatizations because output effects are not available.

October, 2006 IPA: Uganda Telecom Page 39 of 36

APPENDIX A: ADDITIONAL TABLES

Table 6: Performance of UTL Using Economically Relevant Accounts (million Ush.)

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Output 40,098 45,757 46,429 59,417 55,299 61,765 78,148 91,187 96,688 116,505 145,299- Intermediate Inputs 5,873 12,946 18,864 18,658 16,996 17,395 48,703 71,893 65,104 75,664 81,556= Value added 34,225 32,811 27,566 40,759 38,303 44,370 29,445 19,294 31,584 40,841 63,743- Return to Labor 6,948 15,316 22,316 22,073 20,107 20,579 15,089 15,846 16,036 15,069 18,874= Total Return to Capital/ Profit/ Quasi-rent 27,277 17,495 5,249 18,685 18,196 23,791 14,356 3,448 15,548 25,772 44,869

Source: UTL, UPTC and authors' calculations.

Table 7: Performance of UTL Using Flows at Constant 1999 Prices

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Output 37,331 44,332 51,664 59,057 60,853 61,765 65,124 78,235 77,356 103,083 128,204- Intermediate Inputs 8,517 16,607 21,418 20,190 18,020 17,395 38,170 43,445 37,450 40,677 41,605= Value added 28,814 27,725 30,246 38,867 42,832 44,370 26,955 34,791 39,905 62,406 86,599- Return to Labor 23,699 25,741 26,207 27,199 27,199 20,579 17,830 17,830 15,715 13,153 13,052

= Total Return to Capital 5,115 1,985 4,039 11,668 15,634 23,791 9,124 16,960 24,191 49,253 73,547Source: UTL, UPTC and authors' calculations.

Table 8: Reconciliation of Total Return to Capital & Accounting Profit (billion Ush.)

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Total Return to Capital 27.28 17.50 5.25 18.69 18.20 23.79 14.36 3.45 15.55 25.77 44.87 - Depreciation 2.16 4.77 6.95 6.87 6.26 6.41 10.33 19.81 19.21 22.72 25.32 - Net Financial Expenses -24.93 2.38 24.04 50.83 24.40 3.98 -0.09 0.48 2.23 9.96 13.30 + Miscellaneous Income -8.51 -4.72 -4.05 -3.96 -3.61 -4.21 -2.04 9.69 7.41 8.01 -5.36

= Accounting Profit After Tax 41.53 5.62 -29.79 -42.98 -16.08 9.19 2.08 -7.15 1.53 1.10 0.90

Sources: UTL, UPTC and authors' calculations.

October, 2006 IPA: Uganda Telecom Page 40 of 36

Table 9: Decomposition of UTL Profit Into Price & Quantity Effects

Change in 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 Output

P -1,617 -6,347 5,912 -5,884 5,626 12,881 -2,300 6,536 -9,948 324Q 7,276 7,019 7,076 1,765 840 3,502 15,338 -1,035 29,766 28,470V 5,659 672 12,988 -4,118 6,467 16,383 13,039 5,501 19,817 28,794

Intermediate Inputs P 855 1,830 905 377 1,002 5,877 15,824 3,497 4,735 4,137Q 6,218 4,087 -1,111 -2,040 -603 25,431 7,366 -10,287 5,825 1,755V 7,073 5,917 -205 -1,662 399 31,308 23,190 -6,789 10,560 5,892

Value Added P -2,472 -8,177 5,006 -6,261 4,625 7,004 -18,124 3,039 -14,683 -3,814Q 1,058 2,932 8,187 3,805 1,443 -21,929 7,972 9,251 23,940 26,715V -1,414 -5,245 13,193 -2,456 6,068 -14,925 -10,152 12,290 9,258 22,902

Employee Benefits P 7,722 6,718 -1,069 -1,967 6,070 -2,938 757 2,193 1,831 3,921Q 646 282 827 0 -5,598 -2,552 0 -2,004 -2,797 -116V 8,368 7,000 -243 -1,967 472 -5,490 757 189 -966 3,805

Profit P -10,193 -14,895 6,076 -4,294 -1,446 9,942 -18,881 846 -16,514 -7,735Q 412 2,649 7,360 3,805 7,041 -19,377 7,972 11,255 26,737 26,832V -9,781 -12,246 13,436 -489 5,596 -9,435 -10,909 12,101 10,224 19,097

Source: authors' calculations.

October, 2006 IPA: Uganda Telecom Page 41 of 36

APPENDIX B: BIBLIOGRAPHY Byaruhanga, Charles, Managing Investment Climate Reform: Case Study of Uganda Telecommunications, Background paper for the World Development Report 2005, April 16, 2004. Chance, Clifford, The Changing International Telecommunications Environment: Country Case Studies-Uganda, Booz Allen & Hamilton, 1998. Econ One research, Inc. in association with ESG International, Uganda Telecommunications A Case Study in the Private Provision of Rural Infrastructure, July 30, 2002. International Monetary Fund, Uganda: Statistical Appendix, IMF Country Report No. 03/84, March 2003. KPMG, Uganda Telecom Limited Financial Statements for the Year ended 31 December 2004, 9 February 2004. KPMG, Uganda Telecom Limited Financial Statements for the Year ended 31 December 2003. KPMG, Uganda Telecom Limited Financial Statements for the Year ended 31 December 2002. KPMG, Uganda Telecom Limited Financial Statements for the Year ended 31 December 2001. KPMG, Uganda Telecom Limited Financial Statements for the Year ended 31 March 2000. KPMG (in association with Jasper-Semu and Associates), Uganda Posts & Telecommunications Corporation (UPTC) Pre-Divestiture Audit Report as at 30 June 1997, Final Report, 15 December 1997. KPMG (in association with Jasper-Semu and Associates), Uganda Posts & Telecommunications Corporation (UPTC), Uganda Telecom Limited (UTL), Uganda Post Limited (UPL) and Uganda Communications Commission (UCC) Proforma Balance Sheets and Audit Report as at 28 February 1998, Final Draft Report, 26 June 1998. KPMG Peat Marwick, Uganda Telecom Limited, Audit Report and Financial Statements for the Thirteen Month Period ended 31 Month 1999, Final Report. Ministry of Works, Housing and Communications of the Republic of Uganda and The Uganda Communications Commission, License for the Operation of a Telecommunications System Providing Telecommunications Services in the Republic of Uganda, 5 June 2000.

October, 2006 IPA: Uganda Telecom Page 42 of 36 Reinikka, Ritva and Paul Collier ed., Uganda's Recovery: The Role of Farms, Firms, and Government, World Bank Regional and Sectoral Studies, March 2001. Shirley Mary M., F. F. Tusubira, Frew Gebreab and Luke Haggarty, Telecommunications Reform in Uganda, World Bank Policy Research Working Paper 2864, June 2002. Uganda Bureau of Statistics, 2004 Statistical Abstract, November, 2004. Uganda Communications Commission and International Development Research Center, Uganda's Approach to Universal Access & Communications Development Funding, A guide-book for Policy Makers and Regulators, April 2004. Uganda Communications Commission, Recommendations on Proposed Review of the Telecommunications Sector Policy to the Minister of Works, Housing and Communications, 31st January 2005.