impact of mobile wallet on customer satisfaction …

TRANSCRIPT

Page 39

International Journal of Information System and Engineering

www.ftms.edu.my/journals/index.php/journals/ijise

Vol. 8 (No 2.), November, 2020

ISSN: 2289-7615 DOI: 10.24924/ijise/2020.11/v8.iss2/39.49

This work is licensed under a Creative Commons Attribution 4.0 International License.

Research Paper

IMPACT OF MOBILE WALLET ON CUSTOMER SATISFACTION MEDIATED BY TRUST IN MALAYSIA

Ooh Hui Ling,

MBA Alumni, FTMS Global Malaysia

Parthiban A/L Mogana Sondaram,

Lecturer School of Accounting and Business Management,

FTMS Global Malaysia [email protected]

ABSTRACT

This research paper aimed at assessing the impact of mobile wallets on consumer satisfaction mediated by trust among consumers in Malaysia which focuses on 3 dimensions: - mobile wallet, consumer satisfaction, and trust. The study will focus on consumers, both online and offline in Malaysia. This paper adopted a survey using questionnaires using Likert 5-scaling from 1 (strongly disagree) to 5 (strongly agree) distributed among consumers from a different industry, age, and different designation. The study is conducted among 324 respondents using explanatory study, convenience sampling technique method with 3 factors on the 16 items instrument in measuring the consumer satisfaction from the hypotheses developed. The positivism paradigm is adopted in this strategy. The theoretical framework consists of an independent variable, mobile wallet; dependent variable the consumer satisfaction and mediated factor the trust. The data collected were tested on its reliability and validity from the 311 valid responses using SPSS software version 22. This software analyzes the data on demographic, normality, and regression to determine the relationship between variables. The correlation coefficient is tested using the identified hypotheses. The results from this study give a better understanding of the challenges faced on the mobile wallet. Therefore, management from corporations and banks need to broaden their initiative in building trust among consumers to attract them towards this initiative among Malaysians.

1. Introduction This paper investigates the impact of mobile wallets on consumer satisfaction mediated by trust among consumers in Malaysia. It is important to identify the criteria and conditions considered in mobile wallets, and the challenges towards its adoption. It has

Page 40

significantly assisted the consumer with a higher level of satisfaction as per their preferences and perception. These have been discussed in this research paper. This paper investigates the impact of mobile wallets on consumer satisfaction mediated by trust among consumers in Malaysia. It is important to identify the criteria and conditions considered in the mobile wallet, and the challenges towards its adoption. It has significantly assisted consumers with a higher level of satisfaction as per their preferences and perception. These have been discussed in this research paper. The development of mobile wallet foresees full potential that led to higher convenience in product purchase both from online and office (Oh, 2018). However, cash transaction is still reported at 80% by Aleeddin, et al. (2018). No doubt this initiative will influence consumers in a long-term battle that will change their behavior and intention towards the adoption of these new changes and new applications. This research paper was adopted to study the impact and challenges of the mobile wallet in Malaysia. From the outcome, organizations will have a clear understanding of determining the acceptable level of mobile wallet and customer satisfaction mediated by the trust factor. Therefore, this paper can be used as a guideline for further investigation of these variables whereby policies and development are used for the improvement of mobile wallets on the mobile wallet. Research objectives:

1. To examine the impact of mobile wallets on trust. 2. To examine the impact of mobile wallets on customer satisfaction To examine the

impact of trust on customer satisfaction. 3. To examine the impact of mobile wallets on consumer satisfaction mediated by

trust. 2. Literature Review Definition of Key Concepts

A. Mobile Wallets

The mobile wallet or mobile payment has become a necessity in daily life among consumers globally as it creates a multitude of dimensions in building value (Aydin, 2016). The increase in usage and adoption of mobile payment led to e-commerce as the backbone (Bezhovski, 2016) and eventually emerged into m-commerce. Mobile payment also defined as “prepaid payment instruments” by RBI guidelines in India, as mentioned under the act 2005 (P., 2018). The mobile wallet adds to consumers’ convenience so they can have access to their banking accounts through mobile devices. Hence, from a business perspective, the process of conducting business using mobile devices can provide new ways to provide a monetary exchange. The advancement of mobile technology using the platform on new payment is not unanimous as mentioned by researchers.

B. Trust

Trust is defined as customers’ willingness to rely on the products that are sold base on confidence level which will significantly lead to positive purchase intentions (Setiawan & Sayuti, 2017). Trust is considered to be a major barrier for consumers to adopt mobile wallets (David, Bagozzi & Warshaw, 1992). Moreover, e-commerce is known to be the key requirement for more secure payments online by being authentic, confident, and

Page 41

maintain data integrity (Bezhovski, 2016). The advanced technology development can develop trust that will eventually build the habit of using mobile wallet when the transactions are transparent and convenient (Aigbe & Akpojaro, 2014). Trust is known to be central between an interpersonal and commercial relationship (Teas, 1993). Due to the uncertainty of risk and existence on inter-dependence (Yuksel & Rimmington, 1998), the conditions can be used to thrive the crucial relationship in the social distance (Fornell, 1992). A study by Prakash & Lounsbury (1992) mentioned for e-commerce, trust is the most important factor. This is supported in studies by (Lemke, Clark & Wilson, 2011 and Chen, Tseng, and Lin, 2010). The uncertainty of condition can impact the complex transaction (Loureiro, 2010 and Kim, 2008). Hence, growing trust is very important to build a mobile platform (Suh & Youjae, 2006). C. Customer Satisfaction

Customer satisfaction is referred to as a bond from the emotional relationship of buyer and seller (Roman and Ruiz, 2003 cited in Rachel and Zubair, 2015). According to a study by Westbrook, et al. (1978) “consumers find enjoyment and satisfaction in their buying experiences”. (Westbrook, Newman, & Taylor, 1978). Customer satisfaction is seen as an evaluation of the chosen alternatives involving consistency with their beliefs psychologically (Oh & Parks, 1997 cited in Mill, n.d.). This is the ultimate factor towards repetition of business from customers’ behavior and experience (Anderson and Fornell, 1994 cited in Sergio, R., 2003). According to studies by Anderson & Fornell (2000) and IIleska, Risteska, and Miladinoski (2002), customer satisfaction is where it focuses on marketing activities concerning fulfilling the needs of consumers (Reck, 1991). D. ACSI Methodology

The American Customer Satisfaction Index is launched to identify the determinants factors towards customer satisfaction (Naylor & Greco, 2002). This is known as the cause-and-effect model that will be considering the consumer expectations, perceived value, and perceived quality (Naylor & Greco, 2002) using the ACSI. The outcome from this will be used to determine customer loyalty and customer retention (Oliver, 1999 and Morgan, Islam, Ariffin & Karim, 2011). This includes fixing customer complaints and pricing tolerance (Reichheld & Sasser,1990, Fornell, 1992). The model uses the interrelated model and complementary model to measure and analyze customer satisfaction based on the econometric modeling, and to interview consumers

E. Technology Acceptance Model (TAM)

The technology acceptance model uses the perceived usefulness and ease of use to predict the buyer-seller (Morgan, Islam, Ariffin & Karim, 2011). This information can be applied on usage and for user acceptance. This model was proposed in 1989 by Davis, and it is believed to be robust and predictive (Venkatesh & Davis, 2000). The complicated identification of human behavior has complicated the efforts of Information Technology (Chircu & Davis, 2000 and Davis, 1986). Hence TAM is used to determine the user acceptance behavior. Based on various empirical findings, the relationship between the consumer.

Page 42

Conceptual Framework and Hypotheses

Figure 1 Conceptual framework

3. Research Design and Methodology (important for research papers) Research Paradigm

This research paradigm refers to the conceptual framework that is used to examine the right solution on the problems, variables, and concepts that correspond using approaches and tools (Kuhn, 1962). The agreement and belief are known as the research paradigm. It highlights how challenges faced by the organization will be addressed, and the method of investigation (Guba & Lincoln, 1994) is discussed for the right interpretation (Wong, 2014). The researcher will adopt the positivism research paradigm as the hypotheses need to be tested and verified using quantitative methods. The logical factor on human behavior and social reality will be measured and the observation used for interpretation (Fedhel, 2002 and Comte, 1856). Hence, the causal relationship among the variables can be predicted, and determine the impact of the independent variable, the mobile wallet on the dependent variable, the customer satisfaction mediated by the trust (Burns, 2000).

Research Design

In this research, the explanatory research design will be adopted by the researcher, while using the quantitative method rather than qualitative methods that test hypotheses and formulation based on the definition on operations to derive a conclusion (Walsham, 1995 and Henning, et al., 2004). The data on the targeted population are quantifiable. Hence, the validity of the relationship between the variables, mobile wallet, customer satisfaction, and moderated factor, trust can be determined (McNabb, 2010). This explanatory also can be used to emphasize in this research on the cause and effect of relationship (Malhotra, 1999). Therefore, the researcher can be sure the fit of the research towards determining the relationship among the variables, mobile wallet and customer satisfaction, and the correlation using trust as moderated factor using the changes that take place particular to the research problem (Zikmund, et al., 2012). This method will explain further the challenges that have been happening (Rahi, 2017) while arguing the impact of mobile wallet affected by the dependent variable and moderated variable. The factors that are considered will not impact changes or use for comparison (Kowalczyk & Buxmann, 2014). Therefore, a better research structure can determine the deriving conclusion (Kowalczyk & Buxmann, 2014).

Page 43

Data Collection Method

In this research, primary data will be used to develop a questionnaire in collecting information from the targeted population. in this paper, the researcher will not be using qualitative research methods using primary data such as using experiments, interviews, and observations as it requires perception and experience for different people (Morten & Flora, 2015). This requires a highly skilled team and time to conduct the investigation which is not practical as this study has a time constraint. The secondary data also will not be used in this study which needs information from the social-cultural setting and economy, that is relevant to mobile wallet and consumer satisfaction that may not be applicable in Malaysia yet. Human behavior and intention change in the macro and microenvironments. However, the secondary data can be used as a reference point only (Johnston, 2014).

Data Collection Instruments In this research, the statistical sample will be used in the sample size for data collection. An adequate sample will be collected to ensure time is saved during the high data collection using the available resources and results being generalized (Bartlett, et al., 2001). Therefore, the data need to be assured it is valuable and reliable. The sample size needs to be descriptive, experimental, and correlational as mentioned by Roschoe (1975) that the total population needs to be at least 10% based on the margin of error, total population, standard deviation, and confidence level (Hill, 1998 and Areck & Settle, 1995). The researcher adopted non-probability sampling, or also known as the self-selected. This gives opportunity towards accessibility and availability from the convenience sampling (Abrams, 2010) as the targeted population is selected voluntarily (Sharma, 2017).

The non-profitability sampling will be used to determine new insights that can be less expensive and easy to use in the approach (Sharma, 2017). The convenience sampling method is cheaper to use and lesser time. Hence, the selection of the targeted population will be more committed to the survey (Showket & Parveen, 2017). This paper will be using the five-point Likert rating scale (Likert, 1932) to develop the questionnaire using fundamental scaling 1 as strongly disagree and 5 as strongly agree (Clasem & Dormody, 1994) as below.

Table 1: The Likert rating scale

Rating 1 2 3 4 5

Scale Strongly Disagree Neutral Agree Strongly Agree

Disagree

The questionnaires are developed using 16 items with 3 variables in Section B, while

Section A focuses on the demographic questions.

Page 44

Population & Sample Size

The questionnaire was sent to 525 targeted respondents, but only 324 replied. However, 311 were valid with 13 rejected due to incomplete data. The effectiveness and reliability of the test were done using Cronbach’s test using the construct as below. The acceptable value for this test should be >0.70 (Michael, 2004). Table 2: Acceptable Value

Variable Cronbach's Alpha Based on No of

Standardized Items Items

OVERALL .877 16

MOBILE WALLET .771 6

CONSUMER SATISFACTION .752 5

TRUST .791 5

Data Analysis Plan

The data need to be verified. Hence, the Statistical Package Social Sciences (SPSS) is used for this purpose. The accuracy of data from the respondents is important to generate the graphical diagram from the hypotheses for analysis, reporting, presenting, and publication purpose. The fit of the model is also important to determine, along with the causal relationship (Noorazah & Juhana, 2012 and Ringle, 2012).

4. Results and Discussion Demographics Analysis

A total of 525 questionnaires were distributed. However, only 324 data were collected with only 311 (68.6%) valid data, and 13 (3.09%) were rejected due to invalid data. The illustration of the data collection is shown below.

Table 3: Data Collection

DEMOGRAPHIC

SUB- FREQUENCY

PERCENT

VALID CUMULATIV

E

DEMOGRAPHIC

PERCENT

PERCENT

GENDER

MALE

99

22.0

22.0

22.0

FEMALE 212 78.0 78.0 100.0

TOTAL 311 100.0 100.0

Page 45

The gender population is shown as above for this research paper, whereby male

constitute of 99 (22.0%) while the female is 212 (78.0%).

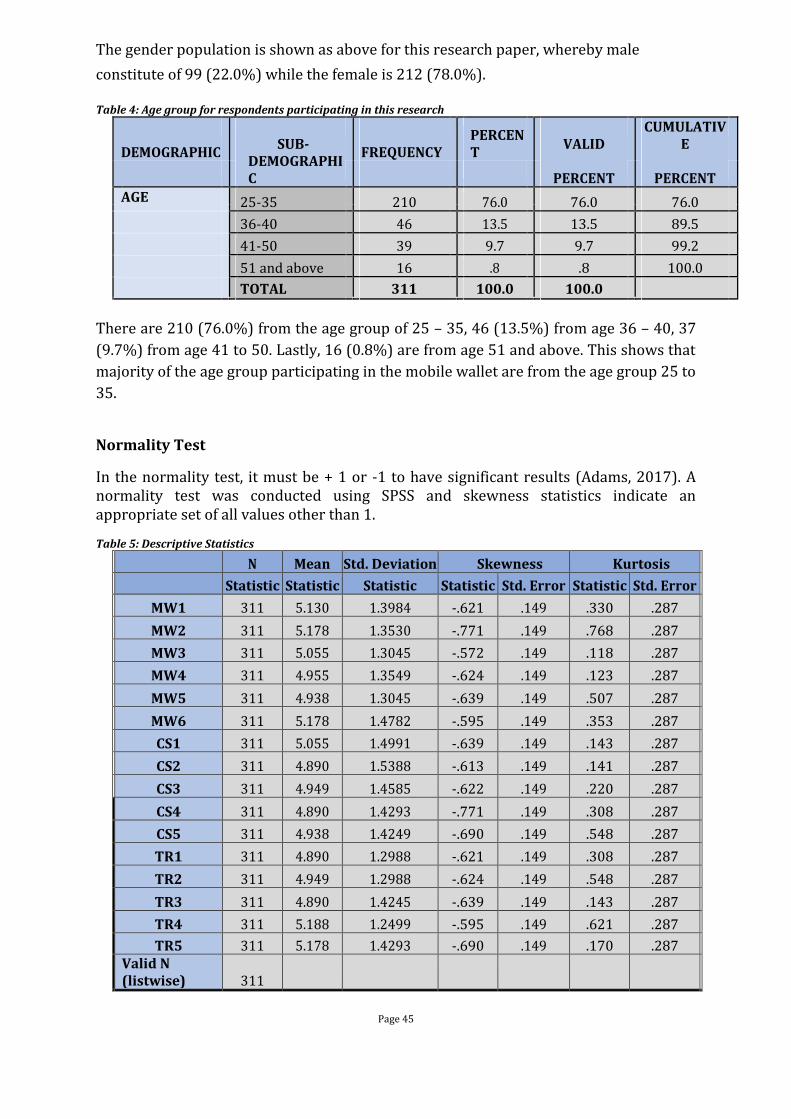

Table 4: Age group for respondents participating in this research

DEMOGRAPHIC

SUB- FREQUENCY

PERCENT

VALID CUMULATIV

E DEMOGRAPHI

C

PERCENT

PERCENT

AGE 25-35 210 76.0 76.0 76.0

36-40 46 13.5 13.5 89.5

41-50 39 9.7 9.7 99.2

51 and above 16 .8 .8 100.0

TOTAL 311 100.0 100.0

There are 210 (76.0%) from the age group of 25 – 35, 46 (13.5%) from age 36 – 40, 37

(9.7%) from age 41 to 50. Lastly, 16 (0.8%) are from age 51 and above. This shows that

majority of the age group participating in the mobile wallet are from the age group 25 to

35.

Normality Test

In the normality test, it must be + 1 or -1 to have significant results (Adams, 2017). A normality test was conducted using SPSS and skewness statistics indicate an appropriate set of all values other than 1.

Table 5: Descriptive Statistics

N Mean Std. Deviation Skewness Kurtosis

Statistic Statistic Statistic Statistic Std. Error Statistic Std. Error

MW1 311 5.130 1.3984 -.621 .149 .330 .287

MW2 311 5.178 1.3530 -.771 .149 .768 .287

MW3 311 5.055 1.3045 -.572 .149 .118 .287

MW4 311 4.955 1.3549 -.624 .149 .123 .287

MW5 311 4.938 1.3045 -.639 .149 .507 .287

MW6 311 5.178 1.4782 -.595 .149 .353 .287

CS1 311 5.055 1.4991 -.639 .149 .143 .287

CS2 311 4.890 1.5388 -.613 .149 .141 .287

CS3 311 4.949 1.4585 -.622 .149 .220 .287

CS4 311 4.890 1.4293 -.771 .149 .308 .287

CS5 311 4.938 1.4249 -.690 .149 .548 .287

TR1 311 4.890 1.2988 -.621 .149 .308 .287

TR2 311 4.949 1.2988 -.624 .149 .548 .287

TR3 311 4.890 1.4245 -.639 .149 .143 .287

TR4 311 5.188 1.2499 -.595 .149 .621 .287

TR5 311 5.178 1.4293 -.690 .149 .170 .287

Valid N (listwise) 311

Page 46

As shown in the above table, the analysis is done in the numerical method. The data

fulfilled the rule of thumb with a significant range of between +1 and -1 (Ghasemi &

Zahediasl, 2012). Therefore, the above table indicates the data Skewness is within the

value range between -1 to +1. On the other side, the Kurtosis statistic in the above

indicates values lower than 1. Hence, it is within the significance of acceptable range on

distribution. Therefore, the overall data in the above table are considered reliable and

valid in using further for this research.

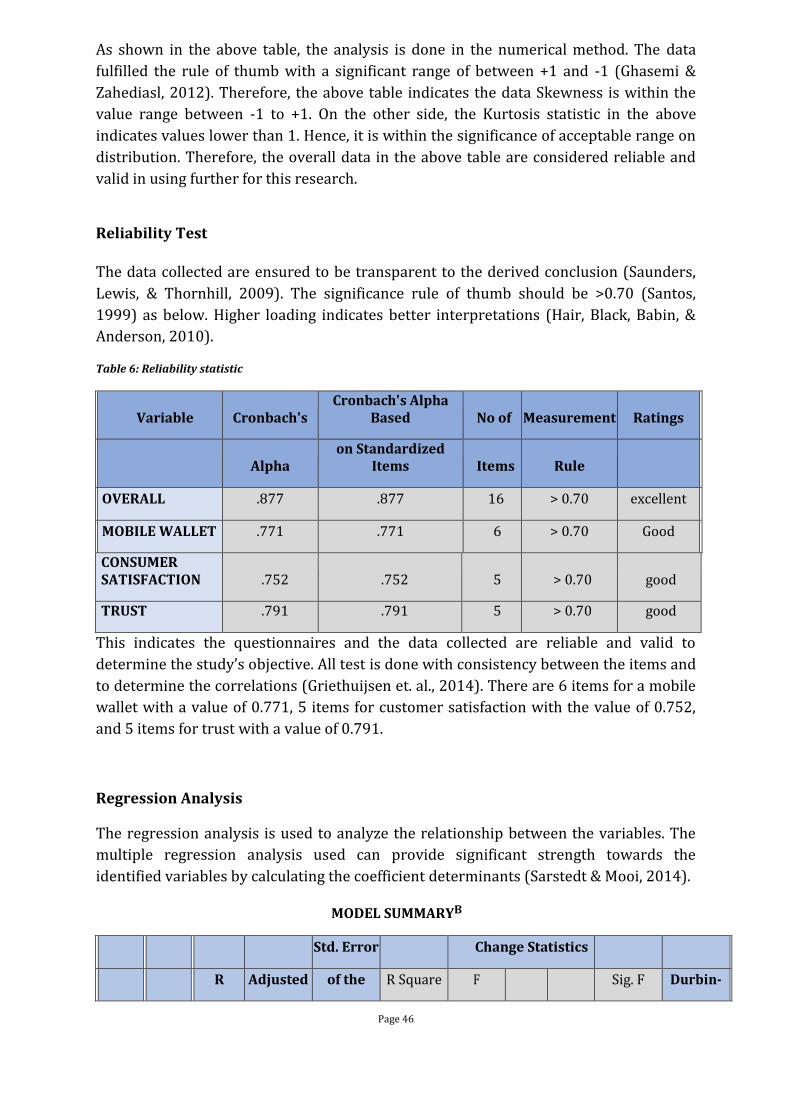

Reliability Test

The data collected are ensured to be transparent to the derived conclusion (Saunders,

Lewis, & Thornhill, 2009). The significance rule of thumb should be >0.70 (Santos,

1999) as below. Higher loading indicates better interpretations (Hair, Black, Babin, &

Anderson, 2010).

Table 6: Reliability statistic

Variable Cronbach's Cronbach's Alpha

Based No of Measurement Ratings

Alpha on Standardized

Items Items Rule

OVERALL .877 .877 16 > 0.70 excellent

MOBILE WALLET .771 .771 6 > 0.70 Good

CONSUMER SATISFACTION .752 .752 5 > 0.70 good

TRUST .791 .791 5 > 0.70 good

This indicates the questionnaires and the data collected are reliable and valid to

determine the study’s objective. All test is done with consistency between the items and

to determine the correlations (Griethuijsen et. al., 2014). There are 6 items for a mobile

wallet with a value of 0.771, 5 items for customer satisfaction with the value of 0.752,

and 5 items for trust with a value of 0.791.

Regression Analysis

The regression analysis is used to analyze the relationship between the variables. The

multiple regression analysis used can provide significant strength towards the

identified variables by calculating the coefficient determinants (Sarstedt & Mooi, 2014).

MODEL SUMMARYB

Std. Error Change Statistics

R Adjusted of the R Square F Sig. F Durbin-

Page 47

Model R Square R Square Estimate Change Change df1 df2 Change Watson

1 .754a .679 .656 .76491 .679 190.551 2 311 .000 2.142

a. Predictors: (Constant), MOBILE WALLET

b. Dependent Variable: CUSTOMER SATISFACTION

From the table shown above, the R square value is 0.679. This means that 67.9% of the

customer satisfaction (dependent variable) can be predicted using other variables;

mobile wallet (independent variables). The adjusted R square value is 0.656. This

means the model is a good fit model as the significance value complies with the rule of

thumb above 0.60. The Durbin-Watson value in the above table should be within the

significance value of 1.5 to 2.5. Therefore, there is no autocorrelation needed for this

research, and there is no inter-influencing of variables among the targeted respondents.

Hypotheses Test Results

Table 7 Hypotheses and findings HYPOTHESIS SIG BETA RESULT INTERPRETATION

H1: MW on TR 0.000 0.6781 Accepted MW has 67.81% impact on TR

H2: MW on CS 0.000 0.5144 Accepted MW has 51.44% impact on CS

H3: TR on CS 0.000 0.6456 Accepted TR has 64.56% impact on CS

H4: MW on CS 0.000 0.4321 Accepted MW on CS mediated by TR has

mediated by TR 43.21% impact

The identified variables as shown in the above table are shown using hypotheses. The highest results are shown on the mobile wallet on trust with results of 67.81%; followed by the impact of trust on customer satisfaction at 64.56% and impact of mobile wallet on customer satisfaction with results of 51.44%. The impact of mobile wallets on customer satisfaction mediated by trust has an impact value of 43.21%. Therefore, the model is shown to be fit, and the influence is determined to be between moderate to high. 5. Conclusion This paper has been providing the scope of research on the impact of mobile wallets on consumer satisfaction mediated by trust among consumers in Malaysia. The findings suggested that trust need to be developed among consumers as this has impact the intentions among consumers to adopt mobile wallet. Using the combination of TAM and ACSI from a different perspective will highlight the consideration of outcome from data

Page 48

collection, and the viewpoint of merchants. With regards to the research model used in this paper, TAM and ACSI are the preferred frameworks in the extension of other research papers. Limitations & Future Research Opportunities

The mobile payment or mobile wallet has been evolving throughout the years. This

research paper sheds some light on the models used on payment systems over the

years. Besides, choosing the mobile payment is an ongoing implementation process.

Since Malaysia is still at an early stage of the process, the outcome from this research

and discussion can be used to investigate further the in-depth impact of mobile wallets

on consumer satisfaction using trust as a mediated factor. Furthermore, new research

models can be developed in giving new insights towards the adoption of the mobile

wallet. The investigation will also determine the trust level using different factors,

whereby the information will be compared and contrast in future researchers.

Reference

Aigbe, P., & Akpojaro, J. (2014). Analysis of Security Issues in Electronic Payment Systems. Nigeria: International Journal of Computer Applications. Alaeddin, O., Zainudin, Z., Altounjy, R., & Kamarudin, F. (2018). From Physical to Digital: Investigating Consumer Behaviour of Switching to Mobile Wallet. Polish Journal of Management Studies. Aydin, G. (2016). Adoption of Mobile Payment Systems: A Study on Mobile Wallets. Journal of Business, Economics and Finance. Bezhovski, Z. (2016). The Future of the Mobile Payment as Electronic Payment System. European Journal of Business and Management. Burns, B. (2000). Introduction to Research Methods (4th Ed. ed.). French Forest, Pearson Education. Chircu, A.M., Davis, G.B. & Kauffman, R.J. (2000). The Role of Trust and Expertise in the Adoption of Electronic Commerce Intermediaries. Technical Report, WP 00-07, Carlson School of Management, University of Minnesota, Minneapolis, MN. Feilzer, M. (2010). Doing mixed methods research pragmatically: Implications for the Rediscovery of Pragmatism as a Research Paradigm. Journal of Mixed Methods Research, 4(1). Kuhn, T. (1962). The Structure of Scientific Revolutions. International Encyclopedia of United Science, 2(2), 43-51. Oh, A. (2018, December 12). The E-wallet Infinity War in Malaysia - Everything You Need to Know About E-Wallet Starts Here. Retrieved from EC Insider: https://www.ecinsider.my/2018/12/malaysia-ewallet-battle-landscape-analysis.html Rachel, B., & Zubair, H. (2015). Employees Ethical Behaviour and Its Effect on Customer Satisfaction and Retention: An Empirical Study on Multinational Fast Food Restaurants in Malaysia. International Journal of Accounting & Business Management. Salkind, N. (2010). Causal-Comparative Design. Sage Research Methods. Saunders, M., Lewis, P., & Thornhill, A. (2009). Research Methods for Business Students (5th ed.). Harlow: Pearson Education Limited. Setiawan, H., & Sayuti, A. (2017). Effects of Service Quality, Customer Trust, and Corporate Image on Customer Satisfaction and Loyalty: An Assessment of Travel

Page 49

Agencies Customer in South Sumatra Indonesia. Journal of Business and Management, 31-40. Wallets, D. B. (2016, August 29). Business Insider Intelligence. Retrieved from https://www.businessinsider.com/data-breaches-could-cripple-the-growth-of-mobile-wallets-2016-8/?IR=T Westbrook, R., Newman, J., & Taylor, J. (1978). Satisfaction/Dissatisfaction in The Purchase Decision Process. Journal of Marketing.