impact of microfinance on women entrepreneurship …€¦ · impact of microfinance on women...

TRANSCRIPT

Pag

e1

IMPACT OF MICROFINANCE ON WOMEN ENTREPRENEURSHIP

SUBMITTED IN PARTIAL FULFILMENT OF THE REQUIREMENTS

OF THE POST GRADUATE DIPLOMA IN MANAGEMENT

CHANDRAGUPT INSTITUTE OF MANAGEMENT PATNA

BY

ADARSHA CHAUBEY

27/06/2019

CHANDRAGUPT INSTITUTE OF MANAGEMENT PATNA

Pag

e2

SYNOPSIS

INTRODUCTION

Bihar rural livelihood promotion society (Jeevika) aims at identifying the women who belongs

to the poorest of the poor society and helping them. These women are then told to make a group

of around 10-15 members which is known as the Self Help Group(SHG),few SHGs together

make a village organisation. Few Vos together form a CLF. Jeevika provides loan and project

fund to the CLFs and it is further divided among the VOs and then the SHGs. These SHG

members have meetings where they discuss about their need and the priority is given to the one

who has the most urgent need. This is decided by the SHG members themselves. The members

borrow loans and start small businesses which has a great impact on their lives. Therefore we

can see that the provision of loans and funds includes the entire working structure of Jeevika

because through these loans and provisions the members are able to perform the major

activities relate to Farm, Non-farm, financial inclusion, etc. The linkage to all the factors among

them is microfinance. It includes micro savings, micro credits, micro insurance and other

banking services. Therefore, a research on microfinance will gives the core idea of the entire

framework.

THE PROBLEM STATEMENT

Whether to increase the amount of loans beings provide or to train the SHG members

and advise them regarding the start-up of the business.

Some of the SHG members don’t get the proper idea regarding start- ups.

Pag

e3

It becomes difficult for the members to record their business transactions.

THEORITICAL FRAMEWORK

The dilemma regarding upliftment of the SHG members is whether to provide more loan or to

give them better idea to start a new business or expand an existing one. If we provide more

loan to the members then there are chances that the members will invest a decent sum of money

in their business but there will be risk of growth in the business. Therefore, provision of more

loan won’t solve the problem of poverty moreover it can be wasteful.

If we give an idea to the members and advise them on issues related to the start-ups they will

have a clarity through which the members can choose a business idea that will be suitable for

them, provided they are advised to start a business they have information and skill related to it.

There are meetings held after regular intervals wherein the members discuss about the issues

they are facing. They get into the habit of saving weekly. They also learn the way to socialise,

interact and behave in a proper manner. The members get information about healthy lifestyle,

budgeting and eating habits.

METHODOLOGY

The best way to know about the problems of a person is to interact with them and try to see

their life from their eyes. Spending time with them makes us understand the basic day to day

problems they are facing and what are their needs. To make sure they interact openly it is

needed to be one of them to make them feel comfortable and easy so that there is no pressure

in their minds.

Methods that had been used to collect data are as follows:

Pag

e4

Observation: By looking at the lives of the members in the village and spending time

with them, makes us aware of the happenings and the circumstances they have to go

through in their daily lives

Attending meetings: Sitting with the members and being a part of their meetings helps

to understand the issues related to society, health, food, sanitation, education and

uncertainty of the future, etc.

Personal interview: To interact with the members individually and know about their

entire life and the major changes that took place in their lives.

Survey forms or questionnaire: Asking them a list of questions which would be helping

to form a quantitative data and analysed later in time to study the conditions and its’

impact.

Focussed group discussion: A topic related to the study was given to the members and

they were told to discuss on their without intervention from any outsider.

FINDINGS

There has been increase in the incomes of the SHG members.

Increase in savings

Members have become self-dependent

The number of SHG members having life insurance has increased

The SHG members are able to access banking facilities

Increase in consumption

The members are repaying the loans on time with very less NPA

Most of the members have become signature literate

RECOMMENDATIONS

More loans should be provided to the SHG members who are skilled and are potential

workers

Pag

e5

Action should be taken against the members who have not returned the borrowed

amount back without having a valid reason for it

The members should be advised regarding the business to be taken up by them.

There should be proper monitoring of the community mobiliser and community

coordinator.

Pag

e6

DECLARATION

I hereby declare that the Summer Internship Project entitled “Impact of microfinance on

women entrepreneurship” submitted to Chandragupt Institute of Management Patna in

partial fulfilment of the requirements for the award of Post Graduate Diploma in Management

is my original work and has been prepared by me under the general supervision of my Industry

Mentor(s) Manish Kumar and Mukesh Chandra Saran and Faculty Supervisor(s) V.Mukunda

Das. I have not submitted the work earlier, either to any other Institute or University for the

award of any diploma, degree or certificate. I have followed the CIMP guidelines to prepare

the report. I have also given due credit to the sources of data, theoretical analysis, text and other

materials by citing them in the text of the report and producing the details in the reference

section.

Place: Patna (Signature of student)

Date: 27/06/2019 Adarsha Chaubey

Roll no: 110066

Pag

e7

CERTIFICATE

This is to certify that the work incorporated in this Summer Internship Project entitled “ Impact

of microfinance on women entrepreneurship” by Ms. Adarsha Chaubey bearing Roll no.

110066, comprises the results of her independent and original investigations carried out under

my supervision and guidance in partial fulfilment of the requirements for the award of Post

Graduate Diploma in Management. To the best of my knowledge, the work has not been

submitted earlier, either to any other Institute or University for the award of any diploma,

degree or certificate.

Place: Patna (Signature of the Faculty guide)

Date: 27/06/19 Dr. V.Mukunda Das

Pag

e8

CERTIFICATE

This is to certify that Ms. Adarsha Chaubey bearing Roll no 110066 a student of

Chandragupt Institute of Management Patna, has successfully completed Summer

Internship Project ent itled “Impact of microfinance on women entrepreneurship” under my

supervision and guidance in partial fulfilment of the requirements for the award of

Post Graduate Diploma in Management for a period from 8/04/19 to 8/06/2019. The work

has not been submitted to any other institution or University for the award of any

degree/diploma or certificate to the best of my knowledge.

Place: Patna (Signature of the Industry Mentor)

Date: 27/06/2019 Manish Kumar

State Project Manager ,Microfinance

Pag

e9

TABLE OF CONTENTS

SERIAL

NO.

CHAPTER PAGE NO.

1 TITLE PAGE 1

2 SYNOPSIS 2-5

3 DECLARATION 6

4 CERTIFICATE 7

5 CERTIFICATE 8

6 ACKNOWLEDGEMENT 10

7 LIST OF ABBREVIATION 11-12

8 LIST OF FIGURES 13

9 INTRODUCTION 14

10 OVERVIEW OF THE STUDY 15-17

11 ABOUT THE ORGANISATION 18-20

12 LITERATURE REVIEW 21-22

13 METHODOLOGY 23-24

14 RESULT ANALYSIS AND DISCUSSION 25-33

15 CASE STUDY 34-37

16 LIMITATIONS OF THE STUDY 38

17 CONCLUSION 39

18

BIBLIOGRAPHY 40

Pag

e10

ACKNOWLEDGEMENT

I would like to thank Dr.V.Mukunda Das (Director, CIMP) for giving me this opportunity to

work in Bihar Rural livelihood promotion society(Jeevika) as an intern. It was really interesting

to work over there. It was a project which made me explore, meet people, interact with them

and observe their lifestyle. It was almost impossible for me to work and get motivated at the

same time without the guidelines of my mentor in BRLPS. Therefore, I would like to thank

Abhijeet Mukherjee(YP-KMC) who was extremely supportive throughout.

I acknowledge the guidance and support that Manish Kumar (SPM-MF) and I am thankful to

him to be such an inspiring and kind mentor. Kajal ma’am( YP-FI) who was also an alumnus

of CIMP helped me in deciding a title for my study, she supported me and helped me whenever

needed.

Besides, I would like to thank Mukesh Chandra Saran(Programme coordinator- FI,COO) to

keep checking my work and giving me his valuable input. Special thanks to Nirmala

Ma’am(BPM, Bihta) who supported me a lot during the visit to Bihta field. Last but not the

least I would like to thank my director once again who was also my Faculty guide from CIMP

for being there throughout the study and guiding me throughout.

Pag

e11

LIST OF ABBREVIATIONS

SHG- Self Help Group

VO- Village organisation

CLF- Cluster level federation

CC- Community coordinator

CM- Community Mobiliser

DRD- Department of rural development

GoB- Government of Bihar

GoI- Government of India

SPIP- State perspective and implementation plan

NRLM- national rural livelihood mission

SRLM- State rural Livelihood Mission

BRLPS- Bihar rural livelihood promotion society

A/C- Account

DEV.- Development

AO- administrative officer

PC- Project coordinator

RES CELL- Resource cell

Pag

e12

MANG.- management

ADMIN.- Administration

HRM- Human resource management

COMM.- Communication

MF- Micro finance

Pag

e13

LIST OF FIGURES

1. Income graph of Bihta

2. Income graph of Danapur

3. Income graph of Bochahan, Muzaffarpur

4. Graph showing average income of Bihta, Danapur and Muzaffarpur

5. Savings graph of Bihta

6. Savings graph of Danapur

7. Savings graph of Bochahan, Muzaffarpur

8. Graph showing the average savings of Bihta , Danapur and Muzaffarpur

9. Insurance Graph

10. Graph showing the increase in the number of self- Dependent SHG members

Pag

e14

CHAPTER 1 : INTRODUCTION

MOTIVATION

Microfinance has a major role in the fulfilling the aim of BRLPS. The first step towards the

upliftment of the rural poor is identifying them and then providing them loans at lower rate to

start a new business so that they can become self-employed and earn their livelihood.

Therefore, this includes all the factors that BRLPS deals with and the Themes that it has, be it

Farm, Non- farm, Banking, Textile or poultry, etc. All the activities taking place are rooted to

microfinance.

While studying the overall impact of micro finance we get the overview of the entire framework

of the organisation and hence it is really impactful to depict the final results. It makes us well

versed with financial understanding and helps to gain knowledge regarding the practicality of

working condition in an organisation.

Microfinance is a financial service which in the case of BRLPS is provided to poorest of the

poor members of the society. It is provided to those who lack in the accessibility of financial

services available generally. It includes microcredit, microinsurance and micro savings.

Microcredit facility : It helps the members to borrow funds or loans.

Microinsurance : It serves as a safeguard for poor people so that they can invest some money

and get protection against various mishaps.

Micro savings facility: There are small bank accounts which helps in saving money keeping

the deposit amount low.

Pag

e15

CHAPTER 2 :OVERVIEW OF THE STUDY

BRLPS has given me the opportunity to study the financial inclusion sector of their

organisation wherein a study had to be in order to get to know the changes that had taken place

in the life of the SHG members. Therefore, my title for the research is “impact of microfinance

on women entrepreneurship” wherein a detailed study on the life of the SHG members had to

be done. To know the impact that any factor had brought one must have the past and present

information about the person, so that their condition can be compared and the impact can be

known. The study requires to identify the members who has seen the change in their lives and

to assess around how many have not been impacted at all or if their has been a negative change.

The research deals with evaluating the lifestyle, income, savings, insurance related awareness

and other detailed information about the members. This will help to know the impact and get

the accurate data at the same time. The data was collected from Bihta, Danapur and Bochahan,

Muzaffarpur. The respondents from these locations were totally different and they were

selected randomly.

The motive of the study is to decide whether provision of high amount as loan will prove to be

beneficial for the SHG members or providing appropriate suggestions and guidelines would

help them in the growth of their business.

Relevance of the study

Studying the impact of microfinance on the lives women entrepreneurs gives entire picture of

the reality. It will help the organisation to know the real condition of the SHG members and by

Pag

e16

knowing the condition they will be able to know the advantages and disadvantages of the

services they are providing to the members. This will provide them numeric data of the

respondents from different localities which would not show a biased result.

The drawbacks in the provision of microfinance will help them to identify its’ root cause and

they will be able to solve the problems or find ways to reduce it. This study helped me

understand the theoretical things better and know the reality. I was able to gain knowledge

regarding the real work structure of Jeevika and how people are getting benefits from the

facilities it is providing.

The study was a reality check of the working structure of the organisation which gave it an

insight of the happenings. It gave me a broader vision and the ability to understand other’s

problem by spending time with them. It helps in understanding the entire framework followed

by Jeevika and a link between them.

Objectives:

To identify the barriers of women entrepreneurs in utility service business

To study the factors motivating the women to start a business and running it

successfully.

To study the impact of financial assistance provided to the SHG members

The objective of this study is to know about the condition of the SHG members in detail

and to identify the bottlenecks of the entire structural framework. In order to understand

the get a detailed understanding, it becomes utmost important to interact with the SHG

members.

Therefore, the objective for the study was made specific and was divided so that it becomes

easier to get accurate results. The first step for this is to identify the barriers that is stopping

Pag

e17

the women to start a business or to provide service to others. The positive and negative

factors needs to be identified so that it would be easier to get rid of the negatively affecting

factors.

And lastly, it is important to know the overall impact on the lives of the women

entrepreneur and assess the drawbacks which leads to unsuccessful results.

These objectives helped to get a way as the goal was clear and specific to get the results.

Scope of work

This study focuses on the life of the SHG members and examines whether they are getting

benefit from the provisions being provided to them or not. In this study the main agenda was

to interact with the SHG members personally and know about their life. This conversation was

sort of an ordinary conversation which could make the members feel free and talk about their

personal problems. The study includes the members irrespective of any factor associated with

their status so that the results could be real and dependable.

Through this study the impact on the life of the respondents is known in detail. These details

will help in maintaining a database of the respondents and analysing the factors which help in

the growth of their business and the factors which are affecting them negatively. The data helps

us evaluate the change that the organisation has been able to bring in the lives of the SHG

members quantitatively.

The accessibility power that the members had related to the financial institutions earlier and

have now after associating with the Self help group helps to understand the impact on their

lives in relation to the condition that they are facing outside their homes. This will help in

increasing the services of Bank mitra in the areas where the facilities provided by the banking

sector can’t be accessed.

Pag

e18

CHAPTER 3 : ABOUT THE ORGANISATION

Bihar rural livelihood promotion society is an autonomous body which is working under DRD

backed by GoB. It is locally known by people as “Jeevika”. MoRD of GOI has reframed the

Swarnajayanti Gram Swarozgar Yojna as NRLM. This had a aim of providing access of self-

employment to the rural poor and this was the reason for foundation of SGSY in the year 1999.

This scheme was impactful in the areas where skilled workers were present and the functioning

was systematic. Meanwhile GoI had launched NRLM at its’ place which was basically built

keeping all the core strength of the scheme and modifying the drawbacks of it. The

implementation of NRLM in state was done at first, which was known as State rural livelihood

mission(SRLM). GoB has designed BRLPS as SRLM and it aims at improving the economic

condition of the rural poor. They targeted the women of the society so that they could be

empowered and become self-dependent too.

To guide the strategic functioning of the NRLM in state an SPIP has been prepared. It is

prepared after consulting with various departments of government and other advisory body. So

that the strategic plan does not get obsolete in long run. The SPIP aims at providing self-

employment opportunities to the rural poor.

The SPIP stands on four pillars of NRLM, which are as follows:

Social mobilisation

Financial inclusion

Reduction of vulnerability

Sensitive and dedicated support framework

Pag

e19

Organisational structure of BRLPS

Support structure of state project management unit

MISSION DIRECTOR

ADDITIONAL CEO

ceo DIRECTOR,AO,PC

C

O

R

E

T

H

E

M

A

T

I

C

I

C

U

S

U

P

P

O

R

T

T

H

E

M

A

T

I

C

I

C

U

IB & CB

MF

COM A/C

SOCIAL DEV.

FARM

OFF FARM

NON FARM

H & N

JOBS

HRM

M E & L

MIS

COMM.

RES. CELL

ADMIN.

PROCUREMEN

T

FINANCE

F MANG. TEAM

SPMs AND PMs

Theme

Related

officer

Pag

e20

Support structure at DPCU

Support structure BPIU

DPM

Mngr- IBCB to theme based MANAGER- HR & ADM

MANAGER(FARM) MANAGER MF & MI

MANAGER BANK LINKAGE

MANAGER SOCIAL DEV.

MANAGER(DAIRY

&LS)

MANAGER- NF & ME

MANAGER- JOBS

MANAGER M & E

MANAGER COMM

FM

BPM

ACC. 3 ACs Livelihood sp. 9 CC OFF ACC.

Pag

e21

CHAPTER 4: LITERATURE REVIEW

Cheston and Kuhn in the year 2004 examined that providing Microfinance facility to the poor

women is a better idea then giving it to the men. It not only helps them to get empowered but

also has been seen that the women are more conscience about the repayment of the money

borrowed. They also analysed that family in which a woman is working does not only develop

economically but also socially. They made a comparison on the basis of the data that those

women who were working or were helping her family in availing credit in any way were treated

well and they were respected whereas the ones who were not self- dependent were ill-treated

in her family. The working women were allowed to take active participation in the decision

making within the family whereas the non-working were not.

Susy Cheston in the year 2002 came to know about the importance of microfinance wherein he

stated that MF has the ability to bring changes in the life of the women. The changes can’t be

for all. It depends on women to women whether they have the potential to make the opportunity

large or not. Providing credits giving them the access to financial services makes them

empowered to an extent.

Pillai made a study and examined that the women are suffering basically after liberalisation as

well as globalisation has come into the picture. These women are mostly suffering as they have

lost their livelihood. MF has helped basically in this sector and mostly to those members who

are deprived and have formed SHG as the banks find more potential in them and some

platforms helps to create that bank linkage that helps a group of women collectively. The focus

is on the team as it will make the women conscience and goal oriented

Pag

e22

Dr Jyotish Prakash Basu made a study on the basis of two questions. The questions that he

based his study upon are as follows:

The linkage between the tendency of women to invest in non- risky project and her need

to increase her position to bargain in the household sector.

The linkage between the choice of investing in any project and women empowerment

The main factor that he tried to examine through this study in 2006 was whether controlling

factors like savings, income, loans, etc impact to empower women or the choice of investment

has the tendency to make them empowered. He came to a conclusion that the if the women

invest in safer investments they would be empowered. Therefore there are banks who are ready

to provide loan to different SHGs and help them to become strong as a team.

Linda Mayoux in the year 2006 examined that microfinance is a programme that is helping

the people not only to save more or get more credit but also bringing the people together as

various groups are being formed. These groups are self Help groups which are basically

working as whole. It is not only helping them to get financed but only promoting the

mobilisation of the funds. It is also helping the unreached women who are unable to survive

with a support which is making them empowered by giving them a way to work and the path

to walk on. This does not benefit the group alone but also helps the women involved

individually as well as the family. There is a great impact on the household of the women the

lifestyle of their families have changed and their children are getting better education too.

Therefore, we can say that micro finance has brought change in the lifestyle of the women and

they have become self- dependent and aware of the world around around them which makes

them confident.

Pag

e23

CHAPTER 5: METHODOLOGY

Research methodology is a framework that helps to collect data in a specific way. The research

methodology used in the study is descriptive. Entire information about the SHG members that

was needed to analyse has been collected. Three locations were chosen to collect the data.

These locations were totally different in to respect to the duration of service provided.

Muzaffarpur was the area where BRLPS was working for the longest time, Bihta was another

area where the duration of service provided by BRLPS was comparatively less and it was least

in Danapur area. The samples were randomly chosen in these areas. This was done to get the

true representation of the sample.

After the title for study had been decided and the information needed to make the study

impactful is determined then data collection actually starts.

There are two types of data:

TYPE OF DATA

PRIMARY SECONDARY

Pag

e24

Primary data

It is the data which is first hand and collected by the person who is conducting the study. I

have collected data from Bihta block, Danapur block, Muzaffarpur block. The data has been

collect from 107 respondents. It comprises of all the information needed to conduct the study.

The primary data was collected using the following measures :

Secondary data:

It is the information that is not collected by the researcher directly and is collected from an

existing set of data.

The data from collected from the following sources:

Magazine

Internet

Journals

Office documents

PRIMARY DATA

OBSERVATION QUESTIONNAIRE INTERVIEW FOCUSED GD

Pag

e25

CHAPTER 6 : RESULT AND ANALYSIS

There is a positive impact on the lives of the SHG members and there is a change which is

definitely in a good way. The change is evident and has the potential to reduce the poverty and

make their future better. The analysis has been done on the basis of the primary data collected

and the information that is by the people are totally unbiased and get no gain in manipulating

the real data. The data has been collected from three different locations and from different Self

Help Groups so that it becomes a true representation of the real scenario.

All the information about the SHG members were taken which would help to infer the impact

on their lives after making small loans available. There were evident changes in the income,

saving habits, consumption pattern, number of people having life insurance, change in the

condition of the women, treatment in their family, level of domestic violence, the details about

their business.

The impact on the income and savings has been evaluated on the basis of the primary data

which are as follows:

Change in income due to microfinance

The graph below shows the change in income of the SHG members after getting

the facility of micro finance in the Danapur block :

Pag

e26

This graph represents the change in income of Bihta location

INCOME(BIHTA)

-400000

-200000

0

200000

400000

600000

800000

1000000

1200000

1400000

INCOME(DANAPUR)

Change in income Danapur region before Change in income Danapur region after

Change in income Danapur region increase Change in income Danapur region decrease

-200000

-100000

0

100000

200000

300000

400000

500000

600000

700000

Before After Increase Decrease

Pag

e27

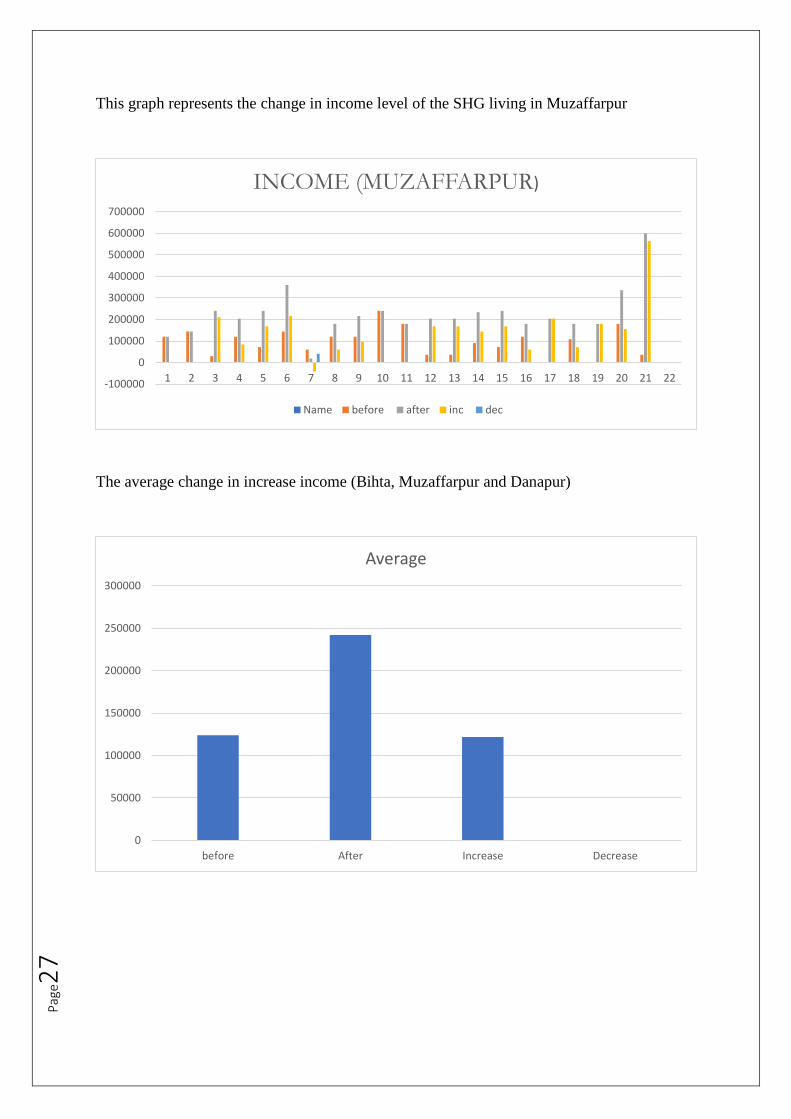

This graph represents the change in income level of the SHG living in Muzaffarpur

The average change in increase income (Bihta, Muzaffarpur and Danapur)

-100000

0

100000

200000

300000

400000

500000

600000

700000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

INCOME (MUZAFFARPUR)

Name before after inc dec

0

50000

100000

150000

200000

250000

300000

before After Increase Decrease

Average

Pag

e28

Analysis

Average income of the SHG members was around Rs.1,23,819p.a before joining

the SHG

It has increased to Rs.2,41,984.7p.a after joining the SHG and starting a new

business.

That means there has been an increase in the average income by Rs.1,21,758p.a

The SHG members who were not in the habit saving have started saving as it is a common

practice of the members within every group. This makes the women understand the value of

saving and in which way even a small amount of saving can help the members at the time of

uncertainty. The women whose income has not increase upto a level where they can save

anything have also started saving an amount of Rs 10 every week as a group member.

Moreover, the members whose income has increased have started depositing their money in

banks by saving the surplus after meeting all the expenses.

There has been an evident change in the saving pattern of the members and this can be known

by the graphs below:

Savings graph of the people belonging to Danapur block

-200000

0

200000

400000

600000

800000

1000000

1200000

before after increase decrease

SAVINGS(DANAPUR)

Pag

e29

Savings graph of the SHG members of Bochahan block(Muzaffarpur)

Savings graph of the SHG members of Bihta block

0

50000

100000

150000

200000

250000

IMPACT ON SAVINGS(BOCHAHAN)

before after increase decrease

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

before after increase Decrease

Savings(Bihta)

Pag

e30

The average of three savings graph of Danapur, Bihta and Muzaffarpur

IMPACT OF MICROFINANCE ON SAVINGS

Average savings of a women before joining the group was 35,081.13 p.a.

Out of 107 respondents 66 of them didn’t use to save which is around 61.17%

After joining the group 91 SHG members out of 107 save regularly and the others

are getting into the habit of saving by joining SHG.

Around 85.05% members out of the total respondents are saving money

0

20000

40000

60000

80000

100000

120000

BEFORE AFTER INC DEC

AVERAGE

Pag

e31

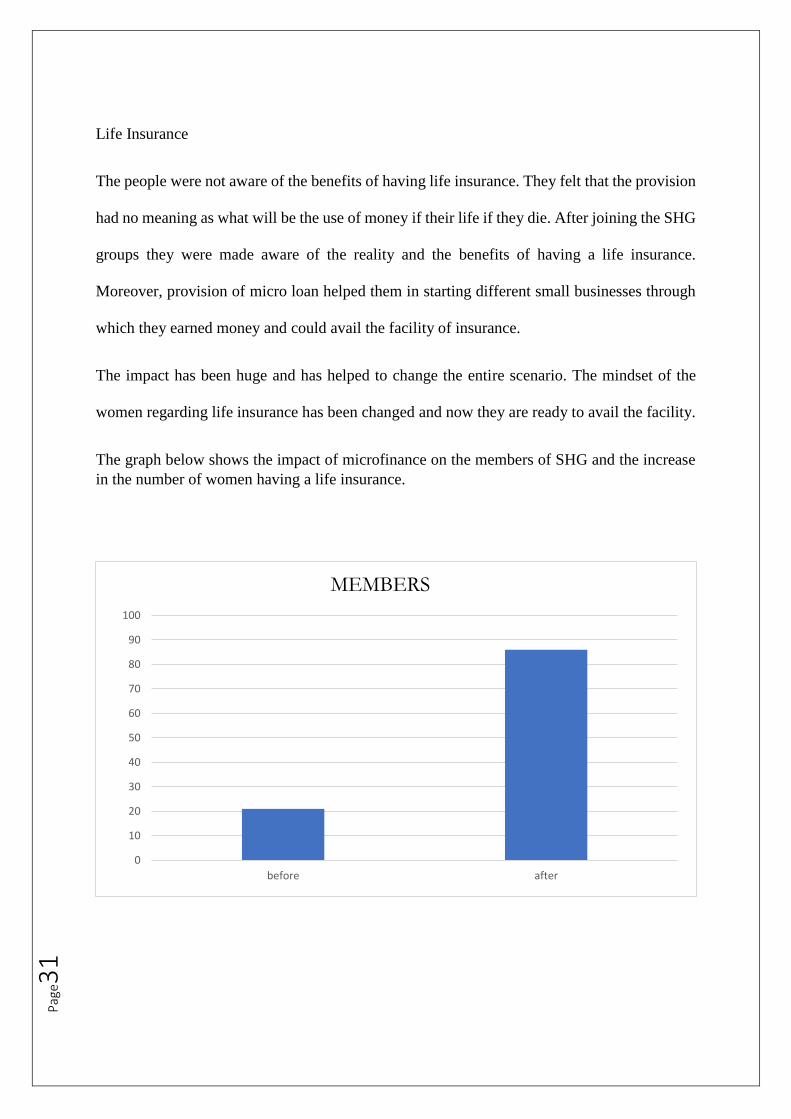

Life Insurance

The people were not aware of the benefits of having life insurance. They felt that the provision

had no meaning as what will be the use of money if their life if they die. After joining the SHG

groups they were made aware of the reality and the benefits of having a life insurance.

Moreover, provision of micro loan helped them in starting different small businesses through

which they earned money and could avail the facility of insurance.

The impact has been huge and has helped to change the entire scenario. The mindset of the

women regarding life insurance has been changed and now they are ready to avail the facility.

The graph below shows the impact of microfinance on the members of SHG and the increase

in the number of women having a life insurance.

0

10

20

30

40

50

60

70

80

90

100

before after

MEMBERS

Pag

e32

Analysis

Out of 107 SHG members only 21 had Life insurance before joining the group

After joining the group 86 members out of 107 have life insurance

That means 80.3% of the total sample have life insurance

21 members are still not insured out of which 2 of them are not eligible for it due

to their age

Therefore, we can say that 17.75% of the total respondents are not insured.

Self-dependency

The women belonging to villages and to the poor or middle class families are mostly dependent

on their husband or family for everything they need and every decision they take. They have

almost forgotten the need to become self-dependent and feel no need of becoming independent

until they are mistreated or disrespected in their families by their closed ones but this realisation

has no value after one has suffered. Therefore it becomes really important for a women to

become self-dependent and take decisions on her own.

The members of SHG were made aware of the worth of becoming self-dependent and their

basic rights. This helped the members to understand that it is never compulsory to follow orders

until one feels that whatever has been asked to do is right. The women are mostly depended on

their husbands financially and husbands are mostly the head of the families and take the

decisions on the behalf of their wives as well.

After joining the SHG the members were made aware and motivated to step out of their houses

and earn for their family. This helped the women in gaining the respect as they were also the

earning members of the family. The meetings that are held weekly also proved to be a boon for

those ladies who were not allowed to step out of their houses.

Pag

e33

The graph shows the level of self-dependency of the SHG members before and after joining

the SHG wherein the change in the number of self-dependent women can be seen.

Analysis:

Out of 107 members only 27 were self-depended before joining the SHG.

At present around 100 women out of 107 are self -depended and are earning for

their families

this means that around 93.4% of the respondents have become self-dependent

and are working to earn money

0

20

40

60

80

100

120

before after increase decrease

Self dependent

Pag

e34

CASE STUDY

There has been a great impact on the lives of the SHG members out of 107 respondents each

of them had a beautiful and unique story of their life, but some were experiences where the

members lost all the hope but BRLPS has came forward as a real hero for them.

The study on their life and the impact have been detailed below

Jeevika: A blessing

Quresha Khatoon lost her house, her family members and her happiness in the age of 37. She

was married to a worker who used to make bangles in the year 1990 and shifted to Bochahan

in Muzaffarpur. Her family was really good and supportive. There was her in laws and husband.

Her father in law was a farmer and used to earn Rs3000 per month and her husband earned Rs

200/day. She was happy and content with whatever she was getting. They had a small house in

Bochahan and a beautiful garden. Quresha was really happy and loved her family members a

lot. She was enjoying a new phase in her life. After a year she gave birth to a boy and her

happiness knew no bounds. She felt like she wanted nothing more from god and was blessed

to have a beautiful life. Years passed and she gave birth to a girl and a boy within 10 years of

time. She was totally busy in taking care of her children and her responsibilities increased.

Suddenly one afternoon when she went to her garden she saw her father in law lying on the

cot but it was not normal. She went to him and asked him to have lunch but there was no reply

from his side. She called other people from inside and couldn’t stop crying as her father in law

was lying dead. Her family was shocked and helpless. It was a great loss to her family and

nothing could make things better in that situation. It took more than two months for her family

to recover from the shock but her mother in law was getting weak day by day. She was

depressed and had no reason to live, she started getting ill and didn’t talk to anybody.

After few more months Quresha tried to control her emotions and think for future as life had

to go on. The financial condition of her family became really poor. As her father in law was an

active earning member of her family and due to his death things got worse. Her husband was

not capable enough to take the responsibility of whole family. It was becoming really difficult

for Quresha to manage the expenses and survive. She was having three children and it became

really difficult to take care of there education and basic requirements.

One more moth passed Quresha’s mother in law fell sick, her condition was really critical.

Quresha’s husband took her to good hospital but the charges over there was really high. There

was no way he could earn that much money. Therefore, Quresha and her husband decided to

mortgage their house and took money from a lender who was really rich and powerful. They

spent all the money in the treatment, somehow her mother in law recovered.

Quresha and her husband was clueless about returning the money to the lender. There was no

option apart from giving their house to him. The lender( pawn broker) visited them for money

and gave 2 month time to them to return the money after he was requested. Quresha and her

Pag

e35

family members broke. They somewhere made up their mind to leave their house but the

thought of it was also making them restless.

A community mobiliser from Jeevika came to know the condition of Quresha and her family

after which she decided to meet her. Next day she visited to her house and assured to help her

and take her out from that situation. The CM made Quresha join the Sahara Self Help Group

and processed the loan within a month to take her out of that situation. Quresha took a loan of

Rs 30000 from the group and went to the lender. She gave the money to him and requested him

to give some more time so that she could return him the whole sum. A ray of hope knocked her

door and she had faith that now she could solve all the problems soon.

She started working in someone’s field and earning Rs300 per day but she did not spend that

money. She somehow managed her expenses from the money that her husband was earning.

She was able to save Rs 60000 by the end of the year which she returned to the lender. Now

she only had to return Rs 20000 that was the interest amount. She took a sigh of relief.

In the year 2009, Quresha took a loan of Rs40000 and she got it as her repayment was done on

time. She started making lac bangles in her compound of her house as her husband was doing

this work for someone else, so, they thought why not for them. Quresha started learning the art

of bangle making from her husband and both of them started working together. They use to

work for more than 8 hours and make bangles in abundance. Quresha’s husband had perfection

in the skill which attracted many customers. They started getting orders from customers and

then the wholesalers. There happiness knew no bounds but they were not sufficient to complete

the order alone they needed to hire staffs. Therefore they hired four staffs and all of them

worked simultaneously.

Finally they were able to complete the order on time. The wholesaler got great reviews from

the retailers and the demand for those bangles increased. Quresha kept on doing the hard work

and completing orders on time and never compromising on the quality. After five years of her

dedication she was rewarded a refrigerator for her hard work.

Quresha is in the bangle business since 10 years and now her monthly income is Rs 50000. She

has hired six staffs and is one of the finest bangle supplier from Bochahan. She has made her

house two storeyed and there are trees of seasonal fruits and vegetables in her garden which

she uses for consumption purpose and sell the excess. Quresha’s life has been like a roller

coaster ride but at the end she is a happy person and her family is content. She feels that Jeevika

has come to her life as a blessing.

Pag

e36

You are never too old to follow your dreams: Jeevika

Minta Devi lived in a kuccha house in Amarha, Bihta. She was not send to school and got

married at 16 when she was really young. She was totally dependent on her husband’s income

and soon gave birth to a boy. Her husband used to work in someone’s farm and earned

3000/month. They had no savings but could get food and were happy with what they had. As

her husband did not earn well they couldn’t provide proper education to their child and he

married in the age of 23. One more member joined the family and it became really difficult for

them to get their basic needs fulfilled.

34 years of her life passed but suddenly she lost her husband and her life took a turn she was

unable to find a way. Her husband was the only member who earned in the family and now

they had no hope left. Minta was unable to solve the problem and till that time she had a grand

son and a granddaughter. She lost all hopes from life and sold her belongings to fulfil the basic

needs of her family member. Every passing day she felt more helpless and her faith in god

begin to fade. Every new morning was a fight for her that she had to face but initially she was

able to offer food to her family but as her savings was getting over, her stress was increasing.

After a few more days she reached to a level where she was left with no food and no money

and she had to go to people living nearby to ask for help but nobody cared. Then she reached

out to her relatives for help but they made excuses to avoid her and nobody helped her. One

day while she was sitting near the gate, she heard her neighbours talking to each other about

Jeevika. She got curious and enquired about the organisation and how it is helping people to

promote their livelihood. She thought to become a member of the SHG and joined

Satyanarayan self- help group. She got motivated after looking at the women in her SHG as

they were independent and started a business which was helping them to work and earn but

soon came to know that they had to save a sum of Rs10 every week which was a burden for

her as she thought she could buy more food for her family as she has really less money. After

attending few meeting she understood the importance of savings and how that saving will help

her in future. She thought for a long period and recognised the skill she had which could also

help her earn money, and that was cooking. She had a plan ready and after 2 months of struggle

she borrowed a loan of Rs 10,000 from the SHG. She went home bought ingredients necessary

for making samosa and started frying samosa out of her house. Surprisingly, People started

coming to her and buying samosa at her place. She was elated and earned Rs 150 after selling

just for two days. It not only raised her hope but also gave her internal happiness. Soon she was

earning enough to feed herself and her family Members properly. And now she had dreams to

increase her earnings and help her son and daughter in law in getting employed. She borrowed

a some of Rs 20000 next and gave it to her son to start fruit business. His son bough a stall and

is now selling fruits in Bihta market. Her family was at a better stage and they had enough

income to live their lives properly. She now recommended her daughter in law to become a

community mobiliser being an old member of the SHG people trusted her recommendation and

Durgawati Devi her daughter in law became the CM of Satyanaryan VO.

Later in life when she was free from all the responsibilities then she decided to start a grocery

shop for which she saved a decent amount from her samosa shop and took a loan of 30,000 to

Pag

e37

start the grocery shop. Recently she was able to make a house for herself by taking loan. She

never expected her life to teach her so much and never thought that an uneducated women who

never went to school could do so much.

Other details:

Village Organisation Ujjwal

Educational qualification No education

Others 5 years earlier As on date

Source of income None Samosa shop, grocery shop, CM, Fruit seller

Earning nil 45600/month

Assets fan Fan, TV, Cooler, Refrigerator, Cattle

Loan borrowed nil 50,000

Pag

e38

CHAPTER 7: LIMITATIONS OF THE STUDY

The study is done on the basis of primary data which has been collected from the SHG

members. At the time of data collection the facial expression, actions and gestures of the

respondents were clealry visible which helped in drawing inferences about the thoughts that

was going through the minds of the SHG members. But there were some limitations too which

are mentioned below:

External environment: At the time of conducting the research, elections were

going on. Due to this the respondents were thinking that the data is being

collected for some party and that was the reason which made them restricted at

times and some were hesitating to speak.

Language Barrier: The SHG members of from various blocks were speaking in

different languages. It was difficult for them to understand Hindi and English

due to which making them understand the question was difficult.

Location: The SHG members lived in villages which were at distant places and

were not safe. Meeting some of the members was difficult as there was no

conveyance facility available which could help me reach the village.

Unavailability of resources: It was very difficult to meet large number of people

in a day as the season was not favourable. Moreover, time was less to as it was

important to collect detailed information about all the SHG members in

particular.

Pag

e39

CHAPTER 8 : CONCLUSION

Microfinance has shown positive impact on the lives of the SHG member.

Although the result may not be immediate but then it is long term.

Priority should be given to the women having skill so that the borrower does not

fall in debt trap.

The women who does not have money are rejected for credit for many years on

giving resources and proves to be better borrowers in comparison to men.

The women have become self-dependent and aware

Most of them are taking important decisions in their family along with the other

members

They are not only earning but have become goal oriented and aspires for better

future

Most have them have life insurance cover and are aware of its’ benefits

Not all but many are getting proper health and sanitation facility

The members have started saving and make timely repayments

Many members who were illiterate are now able to sign on their own.

Women who were not allowed to step out of their houses, now they attend

meetings, goes to banks and for trainings.

The change is evident and it is for the benefit of the people. There is an upliftment in the

lifestyle of the SHG members and in their mindset which has helped the society as a whole.

Pag

e40

BIBLIOGRAPHY

The project has been made with the help of data which involves the Primary as well as the

secondary data. The primary data has been taken mostly from the SHG. The members of the

self help group were asked about their personal life as well as the life they were living before

associating with Jeevika and the life they haver currently, so that the change could be marked.

The secondary data has been collected from the official documents of BRLPS and some

references have been taken from the internet which are as follows:

1. https://en.wikipedia.org/wiki/Microfinance

2. https://www.omicsonline.org/open-access/impact-of-microfinance-on-women-

empowerment-an-empirical-evidence-from-andhra-pradesh--2169-026X-

1000141.php?aid=56415

3. http://brlp.in/

4. http://projects.worldbank.org/P090764/bihar-rural-livelihoods-project-

jeevika?lang=en

The secondary data used was basically related to facts and the figures of the company which

was extracted from various sources including BRLPS web page and other data uploaded

on the internet. Other secondary data has been taken from the employees of BRLPS as they

provided training of a week wherein I was briefed about the organisation.

Pag

e41

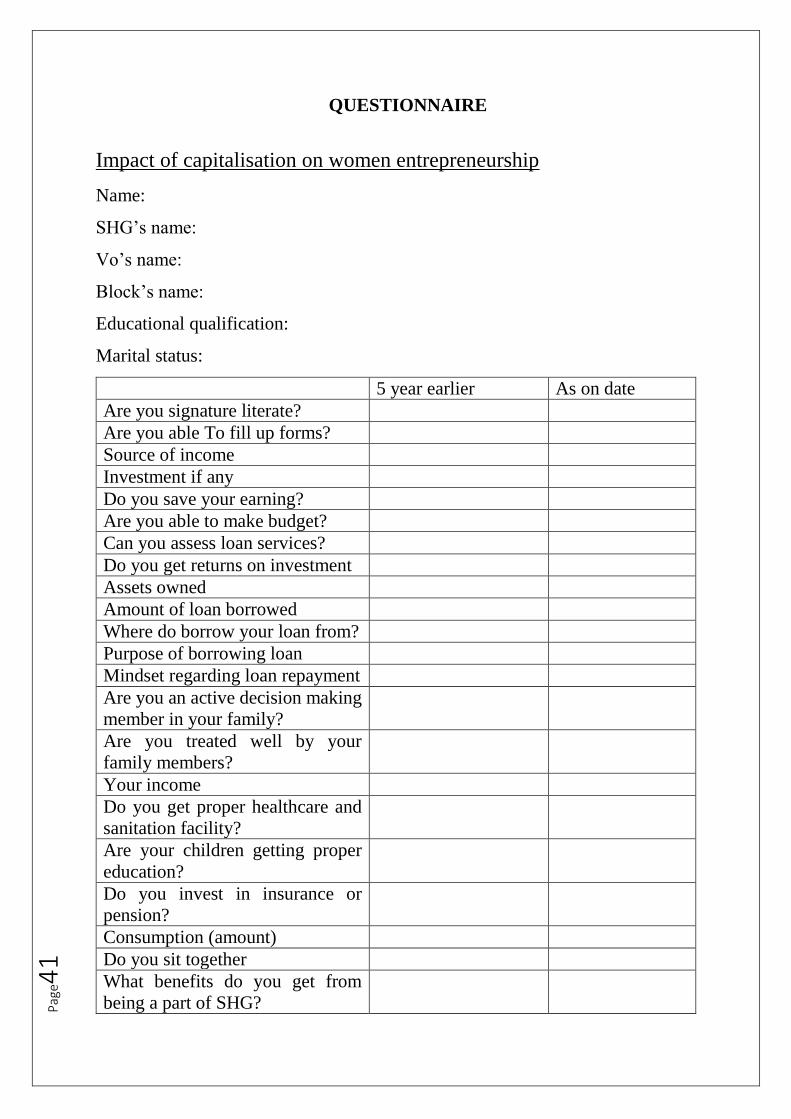

QUESTIONNAIRE

Impact of capitalisation on women entrepreneurship

Name:

SHG’s name:

Vo’s name:

Block’s name:

Educational qualification:

Marital status:

5 year earlier As on date

Are you signature literate?

Are you able To fill up forms?

Source of income

Investment if any

Do you save your earning?

Are you able to make budget?

Can you assess loan services?

Do you get returns on investment

Assets owned

Amount of loan borrowed

Where do borrow your loan from?

Purpose of borrowing loan

Mindset regarding loan repayment

Are you an active decision making

member in your family?

Are you treated well by your

family members?

Your income

Do you get proper healthcare and

sanitation facility?

Are your children getting proper

education?

Do you invest in insurance or

pension?

Consumption (amount)

Do you sit together

What benefits do you get from

being a part of SHG?

Pag

e42

Are you self -dependent?

Activities undergone through the project fund?

__________________________________________________

Have you started any business? If yes, what is it all about?

__________________________________________________

Capital invested in starting the business?

__________________________________________________

Earnings through that business. Is your business profitable?

__________________________________________________

How do you manage to keep a track of your day to day transaction ?

__________________________________________________

Do you repay your instalment of your loan on time?

__________________________________________________

How has Jeevika helped you to change your mindset?

__________________________________________________

Do you have a bank account? If yes, where?

__________________________________________________

Do you have your own house?

__________________________________________________

How did you decide to start this business?

__________________________________________________

Pag

e43