impact of globalisation challenges and opportunities for ... · impact of globalisation challenges...

TRANSCRIPT

1

IMPACT OF GLOBALISATION CHALLENGES AND OPPORTUNITIES

FOR INDIAN AQUACULTURE

G.MOHAN KUMARMARINE PRODUCTS EXPORT DEVELOPMENT

AUTHORITY, INDIA

OECD Workshop on Globalization, 16-17 April, 2007, Paris.

2

0

20000

40000

60000

80000

100000

120000

195019

5319

5619

5919

6219

6519

6819

7119

7419

7719

8019

8319

8619

8919

9219

9519

9820

0120

04

Qua

ntity

(MT)

0

5

10

15

20

25

30

35

Sha

re o

f cul

ture

%

Capture Culture Share of Culture %

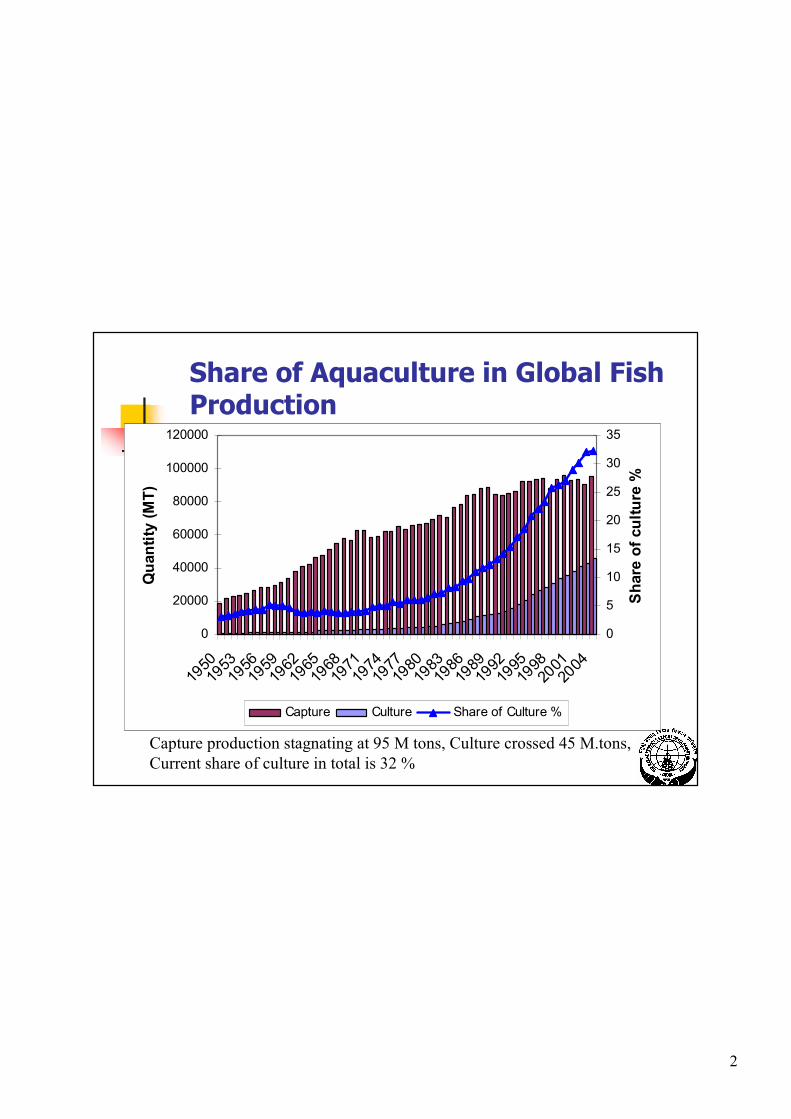

Share of Aquaculture in Global Fish Production

Capture production stagnating at 95 M tons, Culture crossed 45 M.tons, Current share of culture in total is 32 %

3

Aquaculture and fish trade

Increasing Importance of Aquaculture in trade.

Very important for 26 % of international fish tradeFor another 21 % aquaculture is starting to gain important.

Share of Shrimps in Int. trade-16.5 %Contribution of Farmed Shrimps-40 %

4

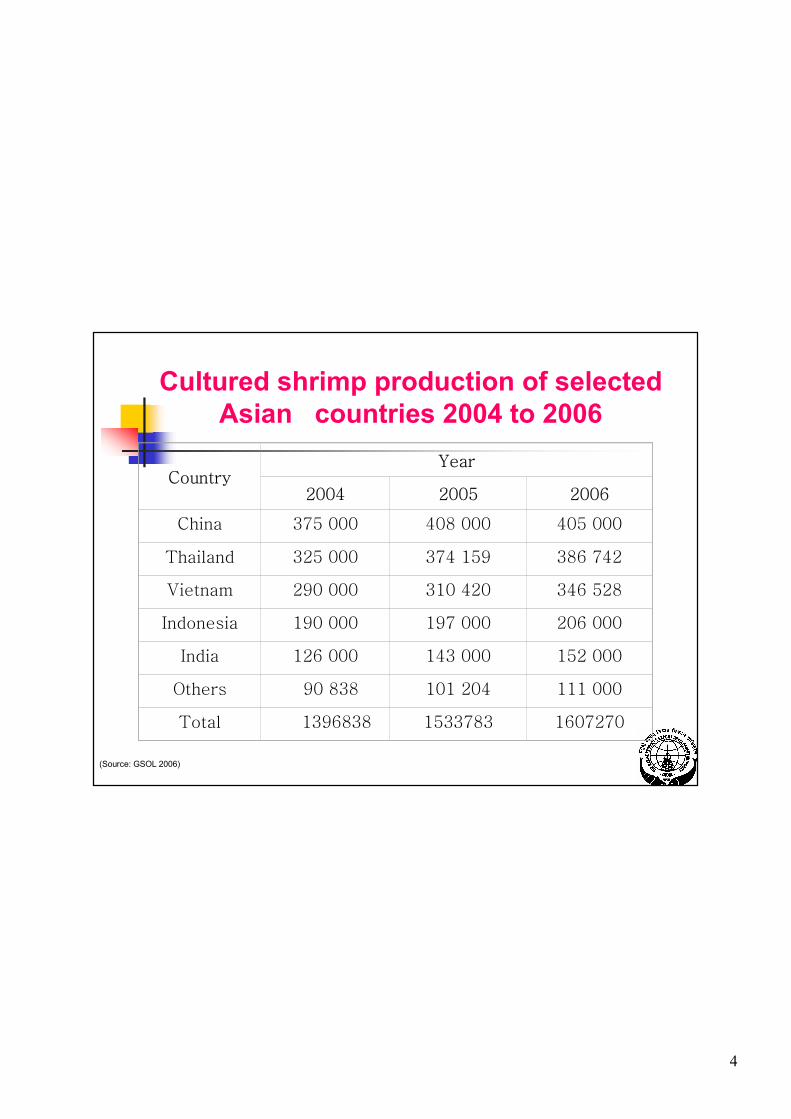

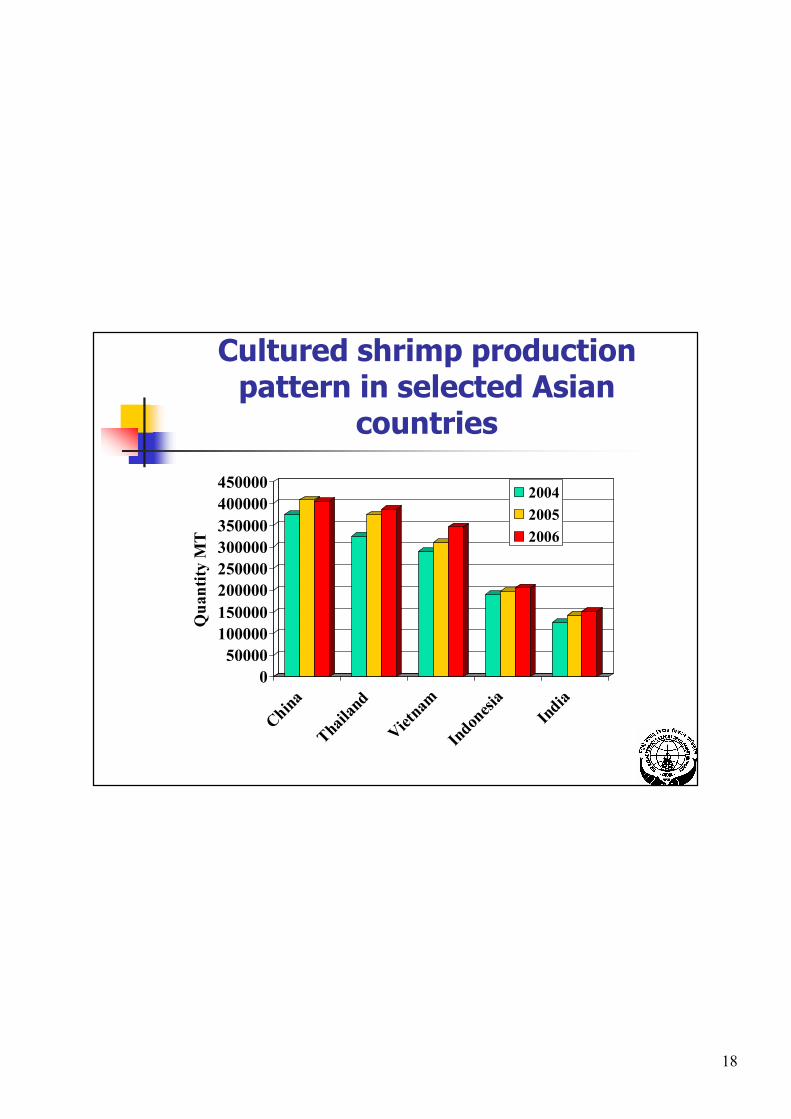

Cultured shrimp production of selected Asian countries 2004 to 2006

CountryYear

2004 2005 2006

China 375 000 408 000 405 000

Thailand 325 000 374 159 386 742

Vietnam 290 000 310 420 346 528

Indonesia 190 000 197 000 206 000

India 126 000 143 000 152 000

Others 90 838 101 204 111 000

Total 1396838 1533783 1607270

(Source: GSOL 2006)

5

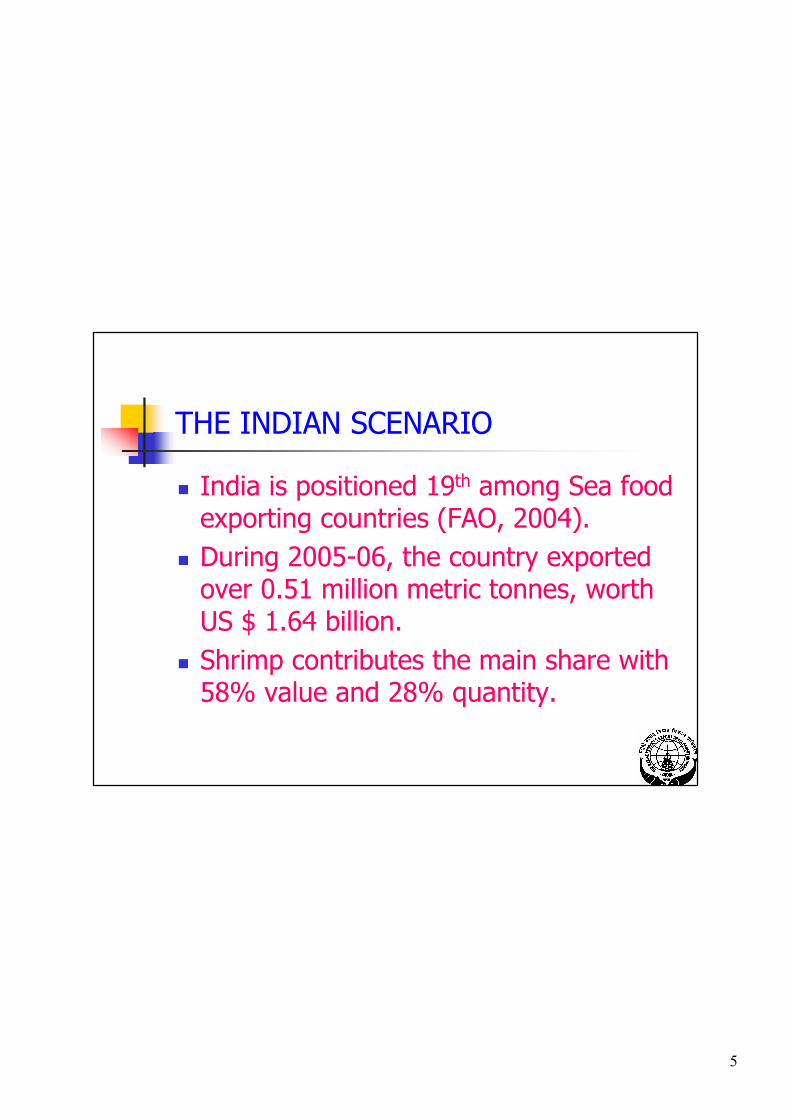

THE INDIAN SCENARIO

India is positioned 19th among Sea food exporting countries (FAO, 2004).During 2005-06, the country exported over 0.51 million metric tonnes, worth US $ 1.64 billion.Shrimp contributes the main share with 58% value and 28% quantity.

6

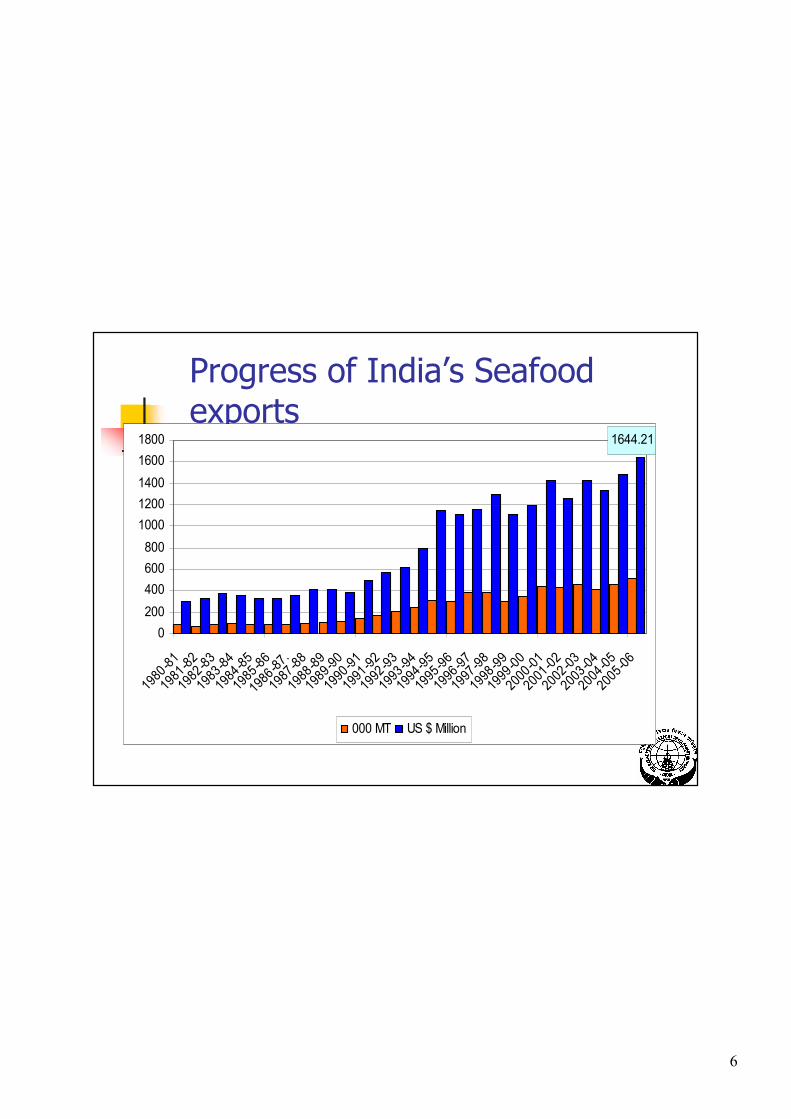

Progress of India’s Seafood exports

1644.21

0200400600800

10001200140016001800

1980

-81

1981

-82

1982

-83

1983

-84

1984

-85

1985

-86

1986

-87.

1987

-88

1988

-89

1989

-90

1990

-91

1991

-92

1992

-93

1993

-94

1994

-95

1995

-96

1996

-97

1997

-98

1998

-99

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

000 MT US $ Million

7

Japan12%

USA11%

EU26%

MIDDLE EAST

4%

S.E. ASIA12%

CHINA27%

OTHERS8%

Japan16%

EU29%

MIDDLE EAST

4%

USA23%

S.E. ASIA8%

CHINA12%

OTHERS8%

Quantity Value

Major Markets & Their Share 2005-06

EEXXPPOORRT T SS

8

Fr. Fish

14%

Fr.

Cuttlefish

8%Fr. Shrimp

58%

Fr. Squid

8%

Others

12%

Fr. Cuttlefish

10%

Fr. Squid10%

Others16%

Fr. Fish36%

Fr. Shrimp28%

Share of shrimp in India’s total exports

Quantity Value

9

Market-wise export of Fr. Shrimp

Japan20.26%

USA31.94%

EU27.93%

S.E. Asia4.64%

Middle East4.12%

Australia1.93%

Others7.56%

China1.62%

JapanUSAEUChinaS.E. AsiaMiddle EastAustraliaOthers

10

Export of Frozen shrimp to OECD Countries

104000

106000

108000

110000

112000

114000

116000

118000

120000

122000

2001-02 2002-03 2003-04 2004-05 2005-06720

740

760

780

800

820

840

860

Quanit(MT) Value (USD Million)

11

INDIA - Culture Fisheries

India - 5th top most shrimp producer and 2nd

largest aquaculture producer in the world Total production from culyure– 2.47 m. tonnes1.2 million ha. of brackish water area spread over 10 maritime States/Union Territories (Only 15% is presently under farming) 8.5 million ha. available for sea farming5.4 million ha. available for fresh water aquaculture

12

INDIA - CULTURED SHRIMP &SCAMPI PRODUCTION (MT)

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

95-96 96-97 97-98 98-99 99-00 00-01 '01-02 '02-03 '03-04 '04-05 05_06

13

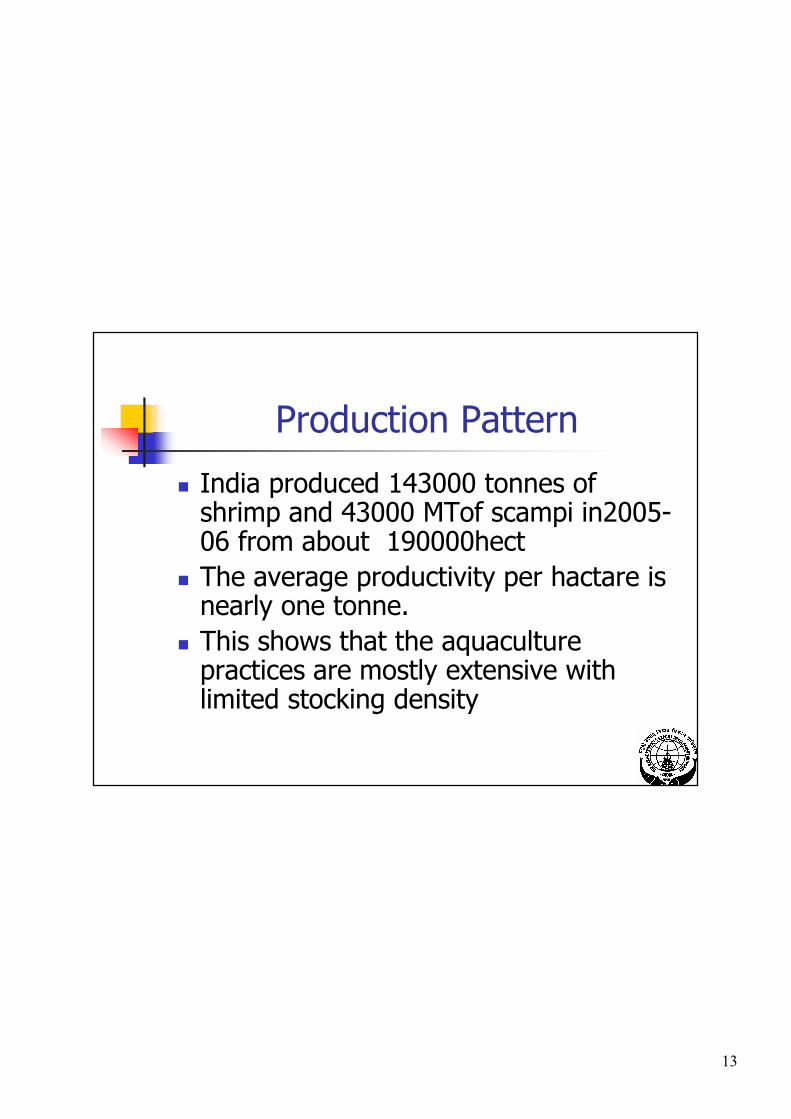

Production Pattern

India produced 143000 tonnes of shrimp and 43000 MTof scampi in2005-06 from about 190000hectThe average productivity per hactare is nearly one tonne.This shows that the aquaculture practices are mostly extensive with limited stocking density

14

0-2 Ha90%

> 10Ha2%

5-10 Ha2%

2-5 Ha6%

Composition of Shrimp Farmers (based on farm holdings)

Shrimp culture is basically an enterprise of Small and marginal farmers

15

Globalization Effects

Increased popularity of fish as health food Greater demand for ready-to-eat & ready to cook productsEmergence of the super-market as a major outlet for convenience productsIncreasing awareness of consumers. Food safety and quality requirements. Non-tariff barrierGrowing concern for environmental sustainabilityChoice of species trade drivenAnti-dumping measures

16

Coping with the challenges of Globalization

Increasing demand vs. disease problems in the shrimp aquacultureIntroduction of L. vannamei in major Asian countries as an alternative species Unprecedented increase in shrimp aquaculture productionPrice fall in international marketsImports into USA crossed 500,000 MT(2004)

17

Global cultured shrimp production 1995-2004

0

500000

1000000

1500000

2000000

2500000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Quantity MT

18

Cultured shrimp production pattern in selected Asian

countries

050000

100000150000200000250000300000350000400000450000

Qua

ntity

MT

China

Thaila

nd

Vietnam

Indon

esia

India

200420052006

19

Black Tiger Price In World Shrimp Market

0

2

4

6

8

10

12

14

16

8/12 16/20 21/25 26/30 31/35

200320042005

20

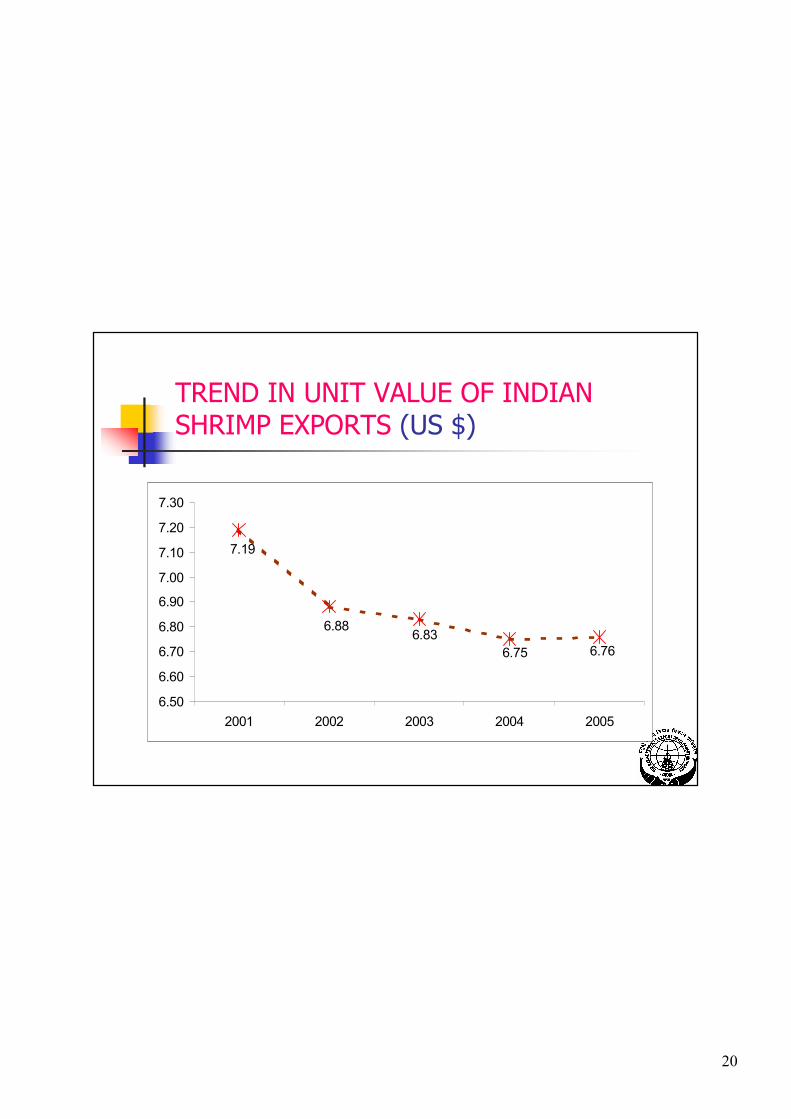

TREND IN UNIT VALUE OF INDIAN SHRIMP EXPORTS (US $)

7.19

6.886.83

6.75 6.76

6.50

6.60

6.70

6.80

6.90

7.00

7.10

7.20

7.30

2001 2002 2003 2004 2005

21

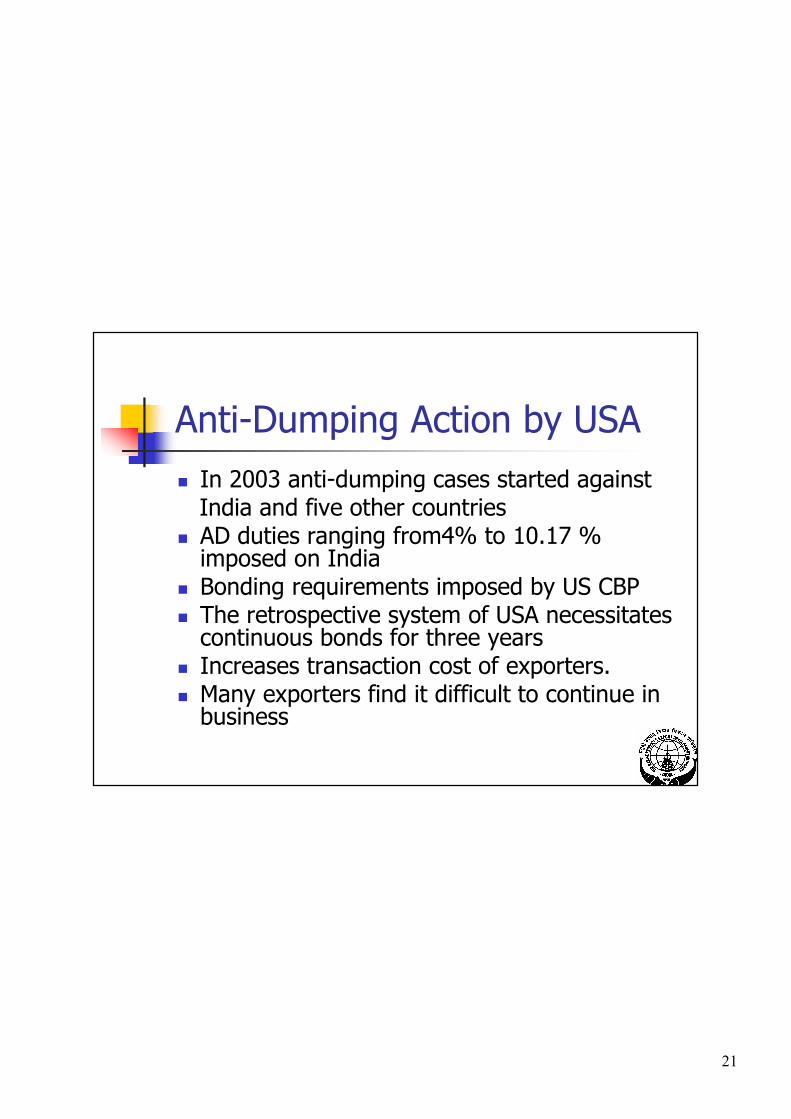

Anti-Dumping Action by USAIn 2003 anti-dumping cases started againstIndia and five other countries AD duties ranging from4% to 10.17 % imposed on India Bonding requirements imposed by US CBPThe retrospective system of USA necessitates continuous bonds for three yearsIncreases transaction cost of exporters.Many exporters find it difficult to continue in business

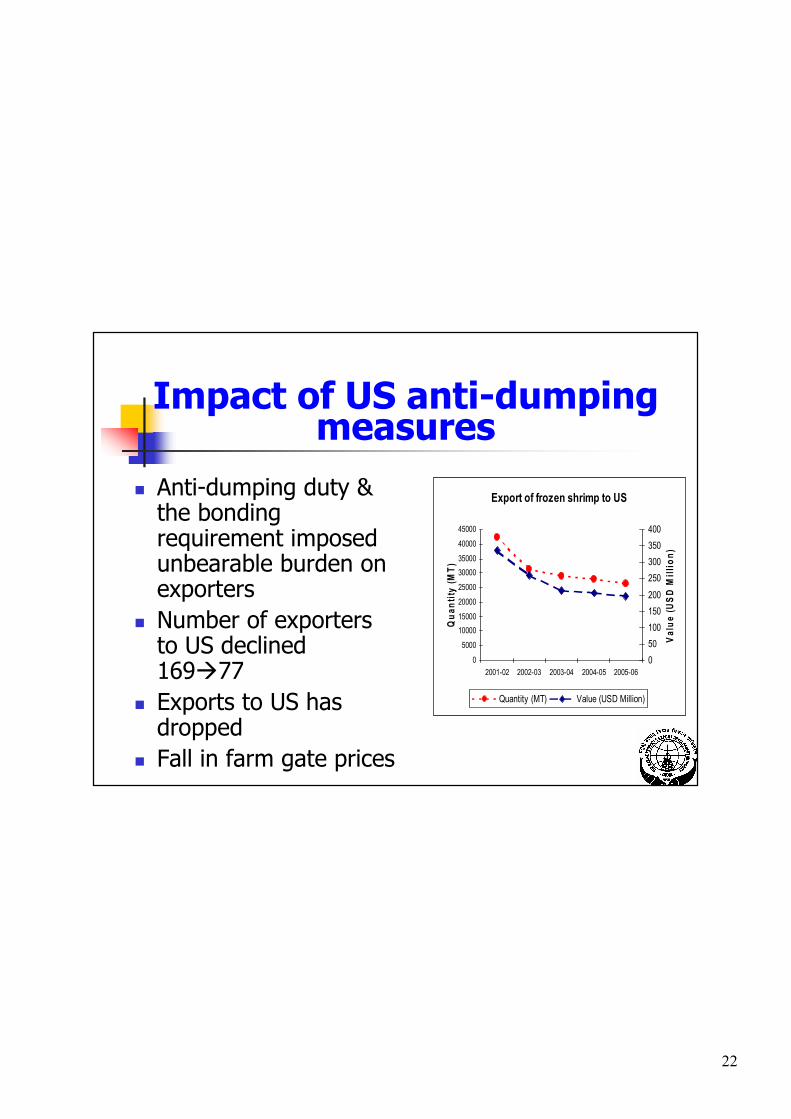

22

Impact of US anti-dumping measures

Anti-dumping duty & the bonding requirement imposed unbearable burden on exportersNumber of exporters to US declined 169 77Exports to US has droppedFall in farm gate prices

Export of frozen shrimp to US

0

5000

1000015000

20000

25000

3000035000

40000

45000

2001-02 2002-03 2003-04 2004-05 2005-06

Qua

ntity

(MT)

050100150200

250300350400

Val

ue (U

SD

Mill

ion)

Quantity (MT) Value (USD Million)

23

Farm gate prices offered to shrimp farmers

0

2

4

6

8

10

12

USD

per

Kg

1999 2000 2001 2002 2003 2004 2005 2006

24

Concerns of Shrimp Farmers

Recurring disease problems & Repeated crop losses.Price fall – International markets & farm gateIncreasing cost of production – High feed cost (fish meal issue) & other inputsRising quality requirementsLack of insurance and financial support Exploitation by middlemen, moneylenders

25

Major Issues In International Trade In Fish And Fishery Products

1.Market access issues

2.Food safety issues

3.Environmental issues

26

Market Access Issues

Tariff escalation:1. Value added products attract higher tariff

levels. This perpetuates the dominance of Developed countries in the production and marketing of value-added products

27

1. Increased dominance of supermarkets in retail trade in fish and value-added products

2. Entry barriers create difficulty in accessing supermarkets

a) Supply logistics difficult for a new entrant.b) Shelf space expensivec) High costs of market promotiond) Brand barrier.Acquisition of brands

prohibitively expensive3. The above constraints force exporters to

pack in the name of private labels and forego margins heavily.

Supermarkets

28

Non-Tariff Barriers

Sanitary and Phyto-sanitary StandardsEU directives pertaining to the residue levels - the most challenging

The detection levels for chloramphenicol and Nitrofuransnecessitate heavy investment in analytical equipment.

Japanese market also becoming more sensitive to residues

Rejection of shrimp consignments lead to financial crisis for the export industry

29

Measures to Meet the Challenges

Short term measures:

Notification banning the use of anti biotics in hatcheries ,farms etc

Village level campaigns against use of anti-biotics and other pharmacologically active substances in shrimp farms

30

National Residue control programme

National Residue Control Programme (NRCP) put in place.

Establishment of state-of-the -art laboratories for residue analyses

Training and recruitment of staff for residue analysis

31

Medium and long term measuresLegislation and Regulation of Aquaculture through Coastal Aquaculture Authority Act (2005)Probiotic mode of operation of shrimp hatcheriesCode of practices for shrimp hatcheries and farms and their registrationDomestication and selection for SPF shrimpRegulation on import of exotics

32

Traceability:

Since farming is highly fragmented, traceability becomes difficult.

Certification becomes unaffordable

Comprehensive database on shrimp farms in the country under preparation

Assigning identification code to individual farms

GIS mapping of farms in association with National Remote Sensing Agency

33

Environmental sustainability and economic viabilty

Adoption of FAO Code of Conduct for sustainable aquaculture practices

MPEDA-NACA programme for sector-wide adoption of BMPs.

Introduction of Participatory farming through formation of Aqua Clubs

34

MPEDA-NACA Experiment

BMPs based on FAO CCRFEmphasis on pond bottom/water quality,screening of seeds ,optimisationof feeding ,low stocking densityandminimisation of water exchangeCo-ordination of farm activities by group formation(self-help groups)Empowerment and self reliance.

35

Outcomes of MPEDA-NACA Project

Successful crops and improved profitsReduced disease prevalenceAquaculture without use of antibiotics Group traceability through aqua clubsIncreased cooperation among farmersMore interaction of farmers and stakeholdersIncreased awareness on environmentBetter Price for BMPshrimp

36

MPEDA-NACA Programme

37

The Cluster Concept in IndiaInstitutionalisation of cluster farming by formation of Aqua farmers’ Societies

Registration of societies by MPEDA based on adoption of code of practices

Financial support to the societies.

Bottom-up appraoach country-wide

Financial assistance for societies for promoting sustainability

New outreach Agency National Centre for Sustainable Aquaculture (NACSA) established for promotion of sustainable aquaculture though capacity building

38

Regulatory system

Coastal Aquaculture Authority set up in Dec 2005Regulation within 2kms of high tide lines of seas ,rivers , creeks and backwatersGuidelines for farming and allied activities.

39

Guideline for Farming Ecologically sensitive areas not to be usedNo farming within 200 metres of the HTLMaintain 100 m distance from the nearest drinking water source.Farms not to be located across natural drainage canals and flood drains.Control on stocking densityFarms to maintain a distance of 50-100 m from the nearest agricultural landProhibition of use of banned anti- biotics

40

Diversification Challenges

Pressure on diversificationShort term solutions difficult because of lack of hatchery technology. MPEDA has embarked on several R&D projects –Indian seabass, mud crab,Grouper, CobiaEnormous potential for cage farming

41

Value Addition

Value addition key to betterment of farmersInvestment needed in processing Technology up-gradationAccess to retail chains difficult for small& medium exportersBetter brand equity needed.

42

Value addition of seafood products

More FDI inflow in Seafood sector

Promotion of Brand equity

Promotion of organic shrimp

MPEDA-SIPPO technical collaboration

The Way Forward

43

Opportunities

Increased demand for productsDiversification opportunities Benchmarking practices with the most advanced in the world .Capacity building Emergence of sustainability as an integral part of Aquaculture practices

44