impact of covid-19 in home care and consumer appliances

TRANSCRIPT

Impact of COVID-19 in Home Care and Consumer Appliances

The Mechanism of Consumption

Ian Bell, Global Lead

© Euromonitor International

2

This PowerPoint presentation includes proprietary information from Euromonitor International and cannot be used or stored with the intent of republishing, reprinting, repurposing or redistributing in any form without explicit consent from Euromonitor International.

For usage requests and permission, please contact us http://www.euromonitor.com/locations.

2

© Euromonitor International

Overview

© Euromonitor International

3

Euromonitor COVID-19 reporting

A global event

Threat as a driver

Who does hygiene

Three time horizons

A new normal

© Euromonitor International

4

Home and Tech industries

Durables ConsumablesConnectivity

© Euromonitor International

6

© Euromonitor International

7

Euromonitor COVID-19 reporting

1.

Forecast restatement

Industry Forecast Model (IFM) update

Price and availability tracker (VIA)

Briefings/Webinar/Opinion/Podcasts

Ad-hoc

A global event

2.

Photo by Martin Sanchez on Unsplash

Disruption

This is extreme disruption and in many cases nothing short of complete inversion

© Euromonitor International

13

Economic Political Environmental

Society Technology Corporate

© Euromonitor International

© Euromonitor International

15

COVID-19 and the economic impact

Recession Great Recession Depression COVID-19

Event -3 -7.5 -25 -30

-35

-30

-25

-20

-15

-10

-5

0

% G

PD

ch

ange

Source: Euromonitor International

Spend out of recession?

Traditional thinking would be for government to spend out of recession, stimulate economic activity and demand. Under COVID-19 the opposite is the case, many governments are pumping billions into the economy as a form

of ‘fiscal insurance’ in the hope that after a period of lockdown large parts of the economy will spring back into life without wholesale layoffs and business failures.

© Euromonitor International

At what cost?

There is little to no chance that the majority of the worlds developed economies will

emerge from COVID-19 without long term

increases in personal taxation. The levels of debt incurred in 2020 will be astronomical, the UK for example ran a USD70 billion deficit in 2019, this will easily triple to support its ‘fiscal insurance’ schemes. After a decade of ‘austerity’ the country will be back to square one.

© Euromonitor International

Economic Political Environmental

Society Technology Corporate

© Euromonitor International

© Euromonitor International

Economic Political Environmental

Society Technology Corporate

© Euromonitor International

Sustainability

Although COVID-19 will push the developed world back on track to meet GHG emission targets with the suspension of large parts of the economy, including the widespread suspension of air and personal transportation during lockdown. Domestic energy and chemical consumption has increased as well as a

resurgence of cleaning wipes and similar

disposable formats which were on the verge of being banned in some geographies.

© Euromonitor International

Economic Political Environmental

Society Technology Corporate

© Euromonitor International

Society

In the absence of a vaccine, COVID-19 mitigation strategies will likely be implemented for some months if not years to come. Meaning

various forms of isolation will continue to be in place, working from home more frequently than before, the ubiquity of face masks and the long term absence of the more vulnerable from

public life. Where technology helps bridge the gap there are many societies around the world where low contact lifestyles are unimageable.

© Photo by Markus Spiske on Unsplash

Economic Political Environmental

Society Technology Corporate

© Euromonitor International

Technology

Technology is supporting the dissemination of public information, contact free shopping trips and working from home for many consumers in

the developed world. Equally our enthusiasm for

the touch screen, especially those found in public or commercial spaces, will likely take a hit when life returns to some semblance of ‘normal’. Suddenly voice control makes a lot more sense in many more situations.

© Photo by pan xiaozhen on Unsplash

Economic Political Environmental

Society Technology Corporate

© Euromonitor International

© Euromonitor International

27

Source: Coca Cola

Threat as a driver

3.

© Euromonitor International

R0

Duration Opportunity

Transmission Susceptibility

© Euromonitor International

Consumer education

Brand experiences with attempts at consumer education are generally time intensive, expensive and outcomes are not commensurate with the resources expended. Add the weight of national government, penalties for non adoption and existential threat then consumer education suddenly becomes more effective and long

lasting.

Photo from UK Government public information campaign in 1980

© Euromonitor International

© Euromonitor International

32

Home care

Home care has an incredibly low barrier to entry, literally a bar of soap and a bucket of

water make for a ‘consumer’. Ubiquity has

helped drive penetration in the developing world but also at times brought with it lack of engagement in the developed where clean clothing and surfaces have become the norm. COVID-19 is driving a radical reengagement with home care products and reassessment of cleaning practices.

© Photo by Fabien Bazanegue on Unsplash

Efficacy

In keeping with the earlier theme of ‘inversion’ until very recent times (literally a few weeks ago) home care brands, especially in the developed world, often sought to positioned

themselves with softer claims around scent, softness and gentleness. COVID-19 has seen a rapid about face in consumers’ focus which is challenging prevailing trends around sustainability and chemophobia.

© Photo by Dorné Marting on Unsplash

© Photo by Mike Dorner on Unsplash

© Euromonitor International

35

Empire of trust

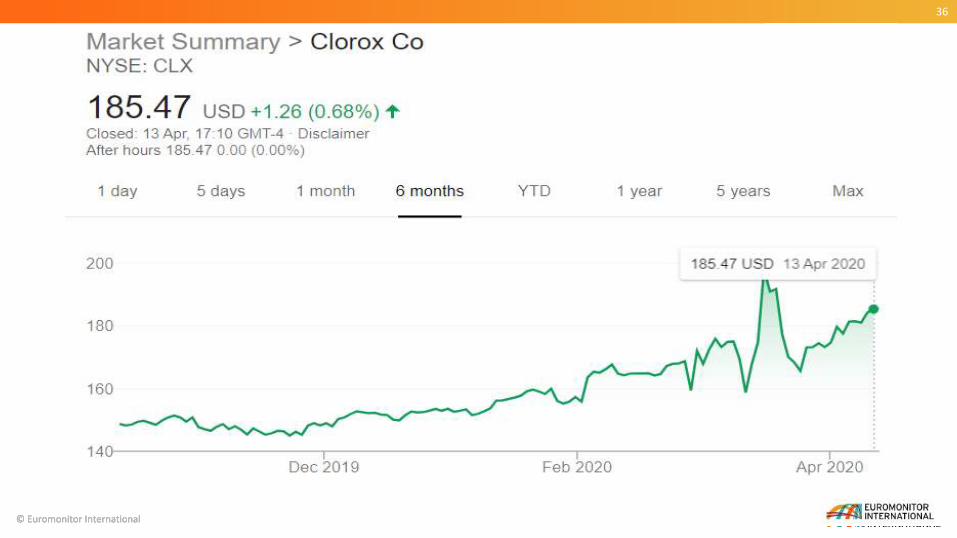

Brands which promise uncompromising efficacy, often older more traditional brands and formats, have reported a comeback according to trade interviews. Brands such as Dettol, Clorox and Domestos have all reported strong growth across a wide range of geographies in 2020. As home care practice is often handed down from generation to generation it is no surprise these ‘classic’ home care brands have responded well.

© Photo by Егор Камелев on Unsplash

© Euromonitor International

36

© Euromonitor International

© Euromonitor International

37

A proxy

Although with only boating very modest average

household disposable income levels, the Indian market for home insecticides is ranked the third largest globally. Faced with the threat of vector diseases such as malaria and dengue households face a very stark choice on where to prioritise expenditure. COVID-19 will encourage much boarder considerations of ‘threat’ and

‘response’ for many more households around the world.

© Photo by Егор Камелев on Unsplash

Who does hygiene

3.

© Euromonitor International

Home hygiene

In a COVID-19 threat environment products that offer uncompromising hygiene are in high demand and generating additional revenue. Home hygiene is however not a single dripline restricted to trigger sprays. The home hygiene ecosystems paints a picture of future collaboration across industries as well as the

landscape for the inevitable battle over expenditure in a increasingly connected world.

© Photo by JESHOOTS.COM on Unsplash

© Euromonitor International

The home hygiene ecosystem

Chemistry Abrasion Energy

© Photo by Bill Oxford on Unsplash © Photo by Daniel Straub on Unsplash © Photo by Hal Gatewood on Unsplash

© Euromonitor International

Ultraviolet

Is widely used for hygiene especially in commercial applications. The technology is also in development in domestic appliances with Vestel one of the first brands to introduce ultraviolet into a commercial washing machine in 2019.

Steam

High temperature steam has long been used as a source of hygiene although in the domestic setting the trend for steam surface cleaning could be due a renaissance in the current climate. Laundry brands also report steam to be more widely used both in machine and cabinet format.

Ionisation

Negative ions are attracted to and then collect positively charged particles in the air. In enough concentration, this leads to air being “cleansed” taking bacteria and virus materials straight out of the air, blocking opportunities for airborne infections to spread.

© Euromonitor International

Robotics

Domestic robots are tireless in their pursuit of hygiene. Where abrasion, which is most frequently related to manual labour, plays a role in maintaining high standards of domestic hygiene it is inconceivable that robots won’t play a much more significant role in the future.

20

21

20

14

© Euromonitor International

© Euromonitor International

44

40

41

42

43

44

45

46

47

48

49

50

Ave

rage

Was

h T

emp

erat

ure

Average Washing Temperature

Average EU wash temperature 2000-2020

Source: AISE

© Euromonitor International

© Photo by Mike Dorner on Unsplash

Asian century

Shifting Market Frontiers – The Asian Century is one of Euromonitor’s megatrends series of reports. While globalisation, population and

economics are all part of this ‘trend’, hygiene is also to be considered. In a COVID-19 world where facemasks are becoming the norm (and mandated in some instances) and the use of

sanitising products is booming, we could all emerge from the pandemic with much more Asia-centric view and behaviours around hygiene.

© Photo by Markus Spiske on Unsplash

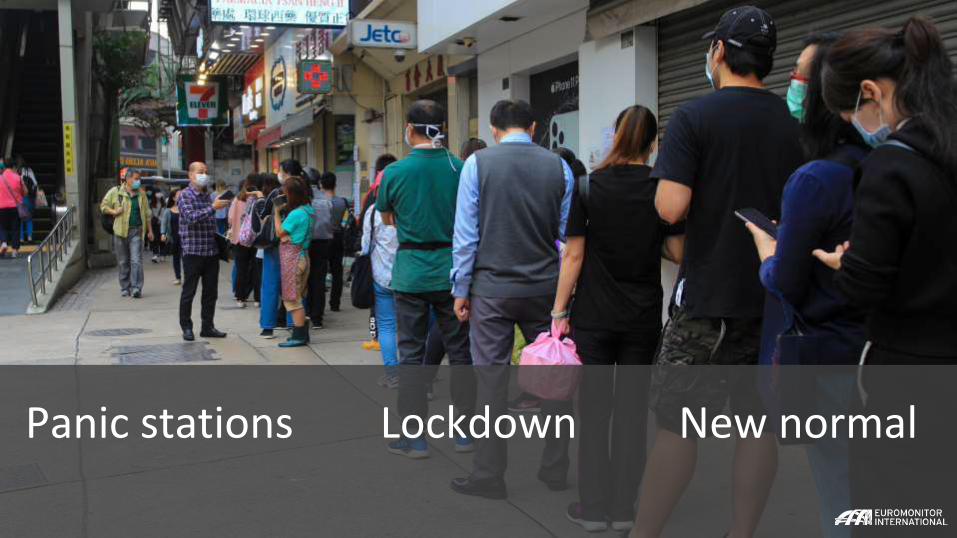

Three time horizons

4.

New normalPanic stations Lockdown

© Euromonitor International

49

Brave new world?

Source: Euromonitor International:

Lockdown

Panic stations

New normal

© Euromonitor International

COVID-19 over three/four time horizons

Pandemic in waves

The four horizons set out to cover the different impact stages for the COVID-19 assume the pandemic is experienced n a single wave. It is probably naïve to expect this in reality as evidence from the Spanish Flu experience is the pandemic came in three waves. Also at time of writing, the latest data from Germany suggests less than 10% of the population are estimated to have been infected, meaning we are some way from heard immunity and at least 18 months from a vaccine according to various press sources

©Photo by Markus Spiske on Unsplash

© Euromonitor International

51

Source: Euromonitor International

Lockdown

Panic stations

New normal

© Euromonitor International

COVID-19 over three time horizons

Panic is viral

Images of empty shelves shot around the world from Australia to Zimbabwe in March 2020. Experiencing rapidly emptying shelves in retail certainly helped to convince hitherto non panic buyers that something was wrong and so the cycle progressed until lockdown was imposed and distribution could catch up. In the UK for example, March 2020 was the biggest month for grocery sales ever recorded which is unheard of for a month outside of the Christmas period.

© Photo by Егор Камелев on Unsplash

© Euromonitor International

© Euromonitor International

54

Extreme stockpiling?

According to UK based industry contacts, ‘extreme’ stockpiling was a behaviour only exhibited by 5-10% of shoppers. For many categories it was households who chose to purchase one or two additional items per trip which led to empty shelves. That said, in March 2020 store visits were up by close to 20% in many locations and spend per trip showed similar increases. Taken as a whole, panic buying was an unprecedented event which stretched supply chains to the limit

© Photo by Егор Камелев on Unsplash

rInternational

55

5050

© Euromonitor International

© Euromonitor International

56

Trialling

Out of stocks forced consumers into trialling new brands, new price points as well as unfamiliar product categories. This is also true of the retail environment, out of stocks in one store forced consumers into other local retailers.

Storage

Where to find space in the home for additional storage is a feature of the panic phase of consumption. Add to this reports of oversized and additional refrigeration appliances sales growth then the domestic space for consumers evolved in the aspect of storage and this is significant to the overall mechanism.

Discounters

Stockpiling requires resources, there was a 20% increase in expenditure in the UK grocery in March 2020 for example. Realty is likely much higher with evidence showing that discounts stores (Dollar Stores) reported very significant uplift in footfall and sales, consumers looking to avoid out of stock and stockpiling within their means.

Overdosing

Got more? Use more! This is a simple equation but anecdotal evidence from consumer survey sources suggests that especially in laundry and toilet care consumers have been significantly over dosing which is also driven by the level of perceived threat at large.

© Euromonitor International

New mechanisms

By introducing new dedicated storage areas in the home consumers have been complicit in setting their own mechanism for reordering and maintaining stocks. COVID-19 is such a significant event and anxiety in the mind of the consumer that those who have the space and the income are unlikely to run down their reserves any time soon.

© Euromonitor International

© Euromonitor International

58

Home storage

© Euromonitor International

© Euromonitor International

59

Lockdown metamorphosis

Roughly a third of the global population are in

some kind of lockdown with a variety of forms of severity and length of internment. We are tracking this information across major markets in the developed and developing world in order to help illustrate how significant this experience is to consumers, consumption and why it will be regarded as the source of very significant long term trends.

© Photo by Егор Камелев on Unsplash

© Euromonitor International

60

Source: Euromonitor International

Lockdown

Panic stations

© Euromonitor International

COVID-19 over three time horizons

New normal

time x space© Euromonitor International

Portfolio

Broader portfolio of products used as well as higher

propensity for over dosing driving both volume and

value.

Frequency

Higher frequency of use, driven by threat and also

government advice, sees key activity such as

laundry increasing

Opportunity

More things to clean around the home related to

physical space, heightened hygiene awareness as

well as time spent indoors.

Penetration

Household penetration of key products such as

antibacterial surface care and bleach has surged

on higher participation.

© Euromonitor International

Singapore example

Singapore is a country famed for its eclectic

food service sector. With low prices and broad availability, lockdown in Singapore has had a profound effect on food trade. It is encouraging much more cooking in the home and all that comes with it for home care.

© Photo by Егор Камелев on Unsplash

© Euromonitor International

64

As a service

© Euromonitor International

© Euromonitor International

65

Maid in Brazil

Back in 2013 we covered how the introduction of minimum wage and other employment legislation had transformed the income of Brazil’s army of domestic workers. This, coupled with a decline in middle class incomes as a result of the country’s economic problems, forced many households to dispense with domestic help and start doing it for themselves. Convenience added value products from toilet care to dishwashing responded well as a result.

© Photo by Rafaela Biazi on Unsplash

© Euromonitor International

66

© Euromonitor International

© Euromonitor International

67

Channel change

Lockdown has introduced many consumers to restricted access to traditional retail

channels. Even where retailers are operating the threat of infection and also the prospect of long queues and out of stocks has disrupted grocery forcing down

the number of store visits but also spend per trip according to industry sources.

© Euromonitor International67

© Euromonitor International

68

© Euromonitor International

© Euromonitor International

69

US E-Commerce as a % of category sales 2004-2019

0

10

20

30

40

50

60

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

% r

etai

l val

ue

Toys & Games Apparel & Footwear Pet Care Home & Garden

Tissue & Hygiene Home Care Alcoholic Drinks Packaged Food

© Euromonitor International

© Euromonitor International

70

E-commerce as a % of Home Care Value 2019

0

2

4

6

8

10

12

14

16

18

20

% o

f to

tal

val

ue

sale

s

© Euromonitor International

Scale up

Major chained retailers around the world are having to build scale for deliveries quickly to meet unprecedented demand from consumers. Tesco announces an expansion of its home delivery and click & collect capacity

to 780,000 slots per week (+120,000 or

+15%) from pre-crisis levels, by securing 200 new vans, hiring 2,500 new drivers and 5,000 store pickers. With disruption in the rest of the economy this could be viewed as a one time event to drive scale and cost structures required for a new era for grocery retail.

© Euromonitor International

71

New normal

5.

© Euromonitor International

73

Source: Euromonitor International

Lockdown

Panic stations

© Euromonitor International

COVID-19 over three time horizons

New normal

© Euromonitor International

74

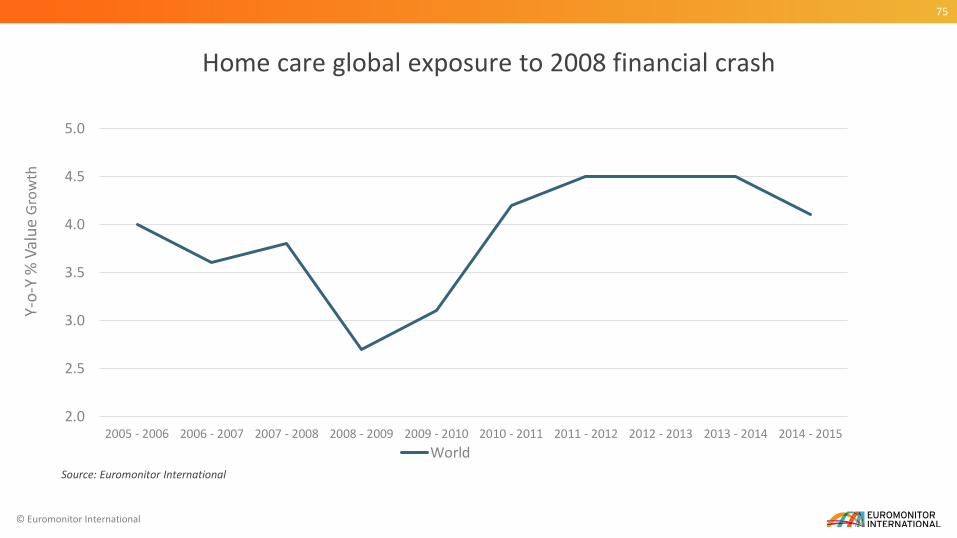

An income event

While being very much a public health experience, COVID-19 is also an income event. How consumers rationalise and re-prioritise expenditure as a reaction to this event. With unemployment rates rocketing across the worlds leading economies there is an element which suggests we will return to 2009 market performance which for home care meant flagging sales and markets most exposed to

the financial crisis.

rInternational

© Euromonitor International

75

Home care global exposure to 2008 financial crash

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2005 - 2006 2006 - 2007 2007 - 2008 2008 - 2009 2009 - 2010 2010 - 2011 2011 - 2012 2012 - 2013 2013 - 2014 2014 - 2015

Y-o

-Y %

Val

ue

Gro

wth

World

Source: Euromonitor International

© Euromonitor International

76

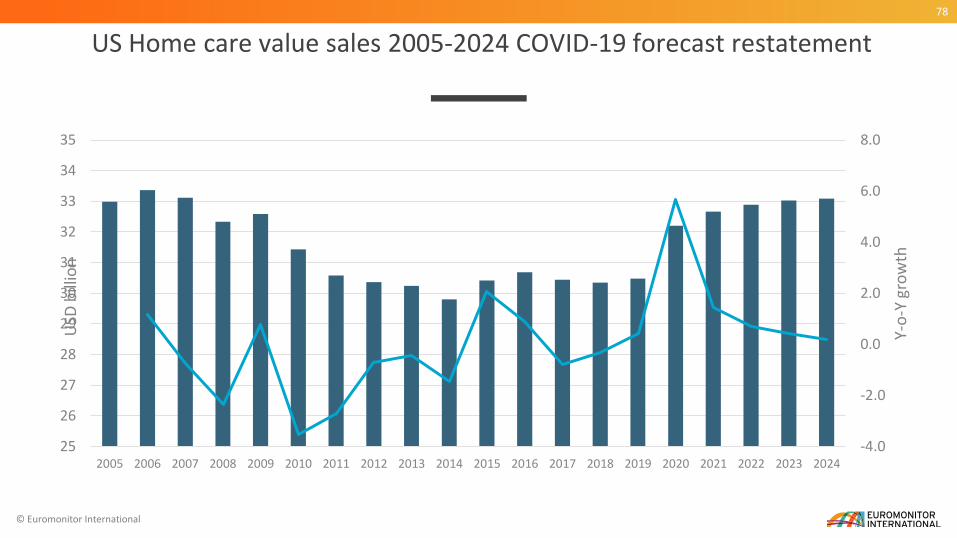

US Home care value sales 2005-2024 COVID-19 forecast restatement

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

25

26

27

28

29

30

31

32

33

34

35

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Y-o

-Y g

row

th

USD

bill

ion

R0

Duration Opportunity

Transmission Susceptibility

© Euromonitor International

78

US Home care value sales 2005-2024 COVID-19 forecast restatement

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

25

26

27

28

29

30

31

32

33

34

35

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Y-o

-Y g

row

th

USD

bill

ion

© Euromonitor International

79

Last year, we were discussing whether it was OK to wee in a public toilet and not flush. Now we are way beyond that.

Fiona Kinsey, Office Worker

Psychology of Abundance Psychology of CrisisPsychology of Compromise

This is a complacent state of mind with stakeholders seeing only a cheap continuous water supply as “normal”. While scarcity means being told you can’t fill a swimming pool or use a garden hose (which still generates protests) This group is in for something of a water shock, this either directly via physical scarcity or indirectly via imbedded water imports.

This tends to be the result of either long term mild water shortages or the “new normal” balanced state of mind once a full crisis has abated. Once you have faced a day when taps could run dry, it is impossible to go all the way back to water complacency and it affects all decisions as a much higher priority than had previously the case.

Life and death are immediate concerns and emergency measures such as rationing and water ‘surveillance’ will be in place and widely prosecuted against. A water crisis resets all purchasing priorities, credible and specific data on water consumption becomes a valued commodity, and in many cases appliance use is unfairly discouraged out of ignorance.

Homes of the future

It is unlikely that civil life will go back to normal any time soon, vaccine or no vaccine. The threat of the next episode will live large in collective consciousness for

many years to come. Society will of course adapt to this ‘new normal’ although hygiene will very likely be build in ‘by design’. The products we use, the systems we develop and the homes we build all with this guiding

principal.

© Euromonitor International

82

Economic Political Environmental

Society Technology Corporate

© Euromonitor International