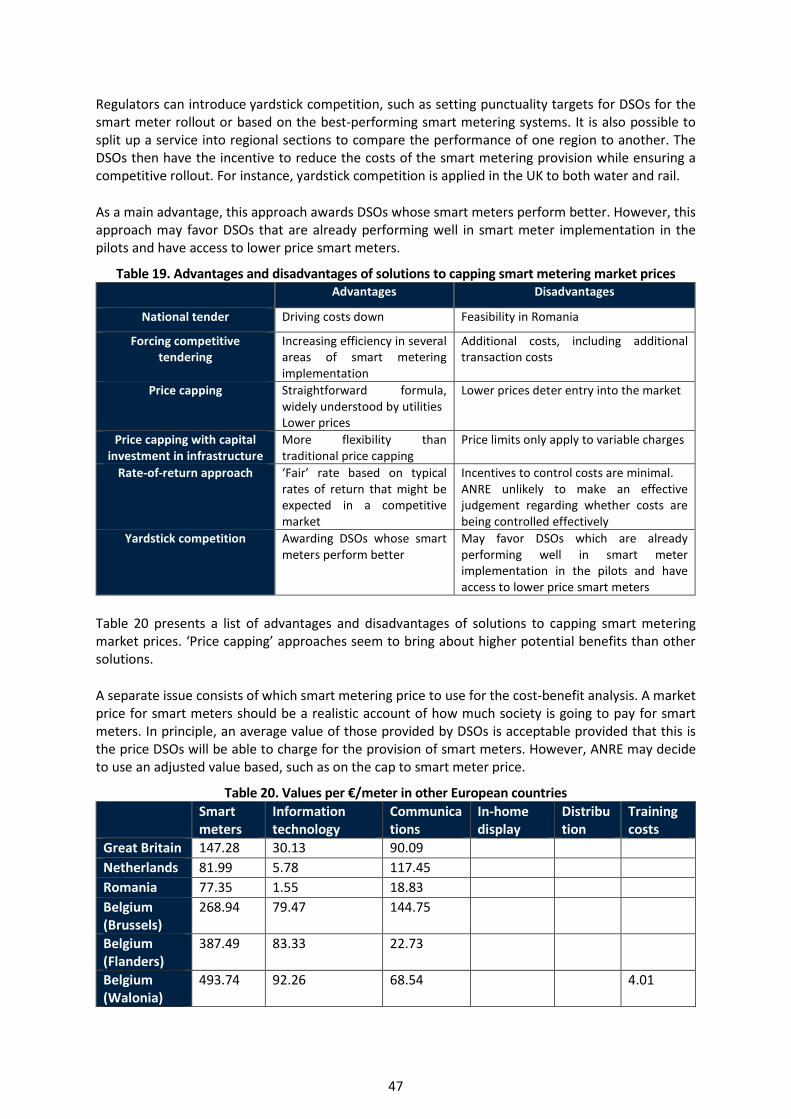

impact assessment on smart metering · table 20. advantages and disadvantages of solutions to...

TRANSCRIPT

ROMANIA

Advisory Services Agreement on

Developing the Capacity of the Central Public Administration to Carry Out Impact Studies

Impact Assessment on Smart Metering:

Data and methodologies for a cost-benefit analysis of smart metering implementation in Romania

National Regulatory Authority for Energy

2

TABLE OF CONTENTS

Acknowledgements .......................................................................................................... 6

Executive Summary .......................................................................................................... 7

1. Status quo .................................................................................................................... 9

1.1. The importance of cost-benefit analysis for smart metering implementation in Romania ............ 9

1.2. Scope and objectives of this report ............................................................................................... 10

1.3. Background: What has been done thus far in the area of costs and benefits of smart meters in Romania ................................................................................................................................................ 11

2. Cost-benefit analyses of smart meters in other European countries............................. 14

2.1. Germany ......................................................................................................................................... 16

2.2. The United Kingdom ...................................................................................................................... 19

2.3. The Netherlands ............................................................................................................................. 23

2.4. Ireland ............................................................................................................................................ 27

2.5. Hungary .......................................................................................................................................... 31

2.6. France ............................................................................................................................................. 33

2.7. Lessons learned for Romania ......................................................................................................... 34

3. Costs of Smart Meters in Romania .............................................................................. 37

3.1. Data from DSOs’ 2015-2016 pilot studies ...................................................................................... 37

3.2. Issues with smart metering cost data ............................................................................................ 44

3.3. Solutions to issues with smart metering cost data ........................................................................ 45

4. Benefits of smart meters in Romania .......................................................................... 53

4.1. Data from Distribution System Operators’ 2015-2016 pilot studies ............................................. 53

4.2. Identification of affected stakeholders .......................................................................................... 58

4.3. Key societal benefits ...................................................................................................................... 59

4.4. Issues with missing data ................................................................................................................ 61

4.5. Recommendations on carrying out a full cost benefit analysis on smart meters ......................... 61

Annex A. Previous cost-benefit analysis costs and benefits estimates: summary ............. 67

Annex B. Previous cost-benefit analysis benefits estimates – detailed ............................. 69

Annex C. Benefits types and metrics used as part of the pilot studies .............................. 75

Annex D. Sources for cost-benefit analysis in other European countries .......................... 76

Annex E. Smart metering trials, net conservation effects, and sample sizes ..................... 77

Annex F. Interoperability: issues for RIA ......................................................................... 79

3

LIST OF FIGURES Figure 1. Discounted costs (€/metering point) ..................................................................................... 17

Figure 2. Discounted benefits (€/metering point) ................................................................................ 18

Figure 3. One-page summary of the impact assessment by DECC (2014) ............................................ 21

Figure 4. Typologies of costs (percentages and absolute spending) .................................................... 22

Figure 5. Typologies of benefits (percentages and absolute amount) ................................................. 22

Figure 6. Costs of smart meters (in € per meter, from international review) ...................................... 25

Figure 7. DSO annual costs (in € per meter, from international review) .............................................. 25

Figure 8. Net cashflow (undiscounted) ................................................................................................. 26

Figure 9. Cumulative net present values’ impact on smart meter rollout ........................................... 26

Figure 10. Sensitivity analysis of main categories of costs and benefits .............................................. 27

Figure 11. Assumed rollout schedule .................................................................................................... 28

Figure 12. Suppliers’ capital costs of smart metering ........................................................................... 29

Figure 13. NPVs for different stakeholders (in thousands of Euros) .................................................... 30

Figure 14. Sensitivities of different variables (in thousands of Euros) ................................................. 31

Figure 15. Cumulative penetration of smart meters and standard meters .......................................... 32

Figure 16. Benefits and costs in the Hungarian cost-benefit analysis (€ per metering point) ............. 33

Figure 17. Costs in cost-benefit analyses of smart metering implementation ..................................... 35

Figure 18. Benefits in cost-benefit analyses on smart metering implementation ............................... 35

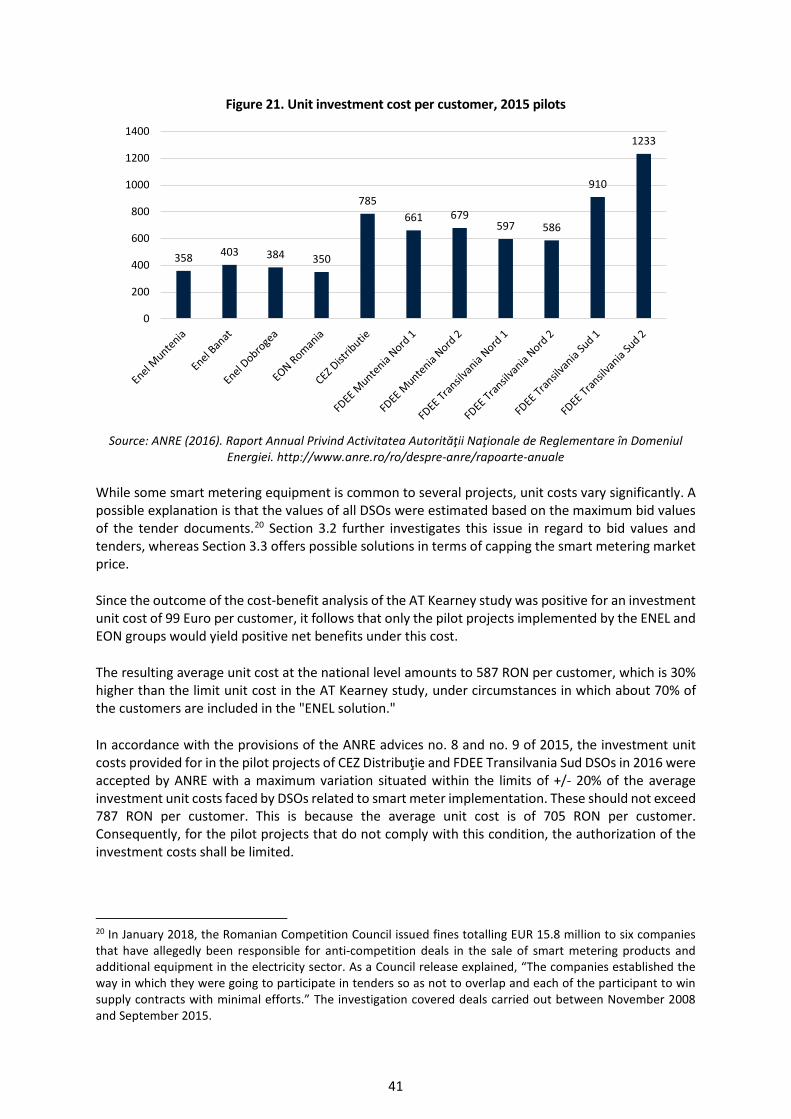

Figure 19. Average unit cost per consumer (RON) ............................................................................... 38

Figure 20. Breakdown of costs per meter ............................................................................................. 38

Figure 21. Unit investment cost per customer, 2015 pilots ................................................................. 41

Figure 22. Investment costs for the purchase of single-phase smart meters in 2015 pilots ................ 42

Figure 23. Investment cost for the purchase of three-phase smart meters......................................... 42

Figure 24. Investment cost for the purchase of balance meters, 2015 pilots ...................................... 43

Figure 25. Cost of the communication system (per meter) in 2015 pilots ........................................... 43

Figure 26. Share of benefits (data from pilot studies) .......................................................................... 56

Figure 27. Reductions in meter reading costs and O&M costs (RON per meter) ................................. 57

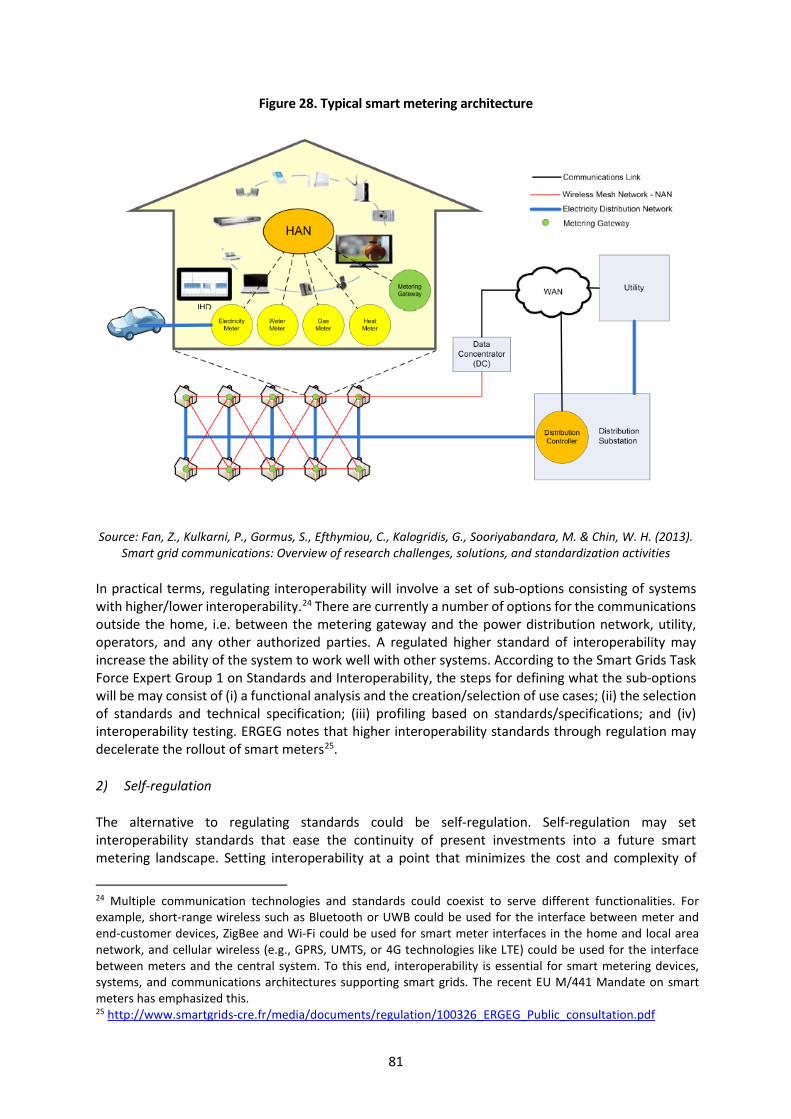

Figure 28. Typical smart metering architecture .................................................................................... 81

4

LIST OF TABLES Table 1. List of costs and cost-related assumptions ............................................................................. 11

Table 2. Benefits and benefits-related assumptions ............................................................................ 12

Table 4. List of benefits (from EU 2012/148/EU Recommendation) .................................................... 15

Table 5. Main assumptions underpinning German Cost-Benefit Analysis ............................................ 17

Table 6. Energy savings ......................................................................................................................... 18

Table 7. Sensitivity analysis: changes that induce negative net present values ................................... 19

Table 8. Changes in results of cost-benefit analyses of smart metering carried out by UK governments between 2011 and 2014 (million pounds) ............................................................................................ 23

Table 9. Categories of DSO costs .......................................................................................................... 24

Table 10. Profile of usage-related benefits ........................................................................................... 28

Table 11. Electricity generation benefits and costs .............................................................................. 30

Table 12. Benefits associated with lower system marginal prices ....................................................... 30

Table 13. Key assumptions in the Hungarian cost-benefit analysis ...................................................... 32

Table 14. Costs in the French cost-benefit analysis .............................................................................. 34

Table 15. Benefits in the French cost-benefit analysis ......................................................................... 34

Table 16. Summary of costs from pilots in 2015-2016 ......................................................................... 38

Table 17. Average cost by equipment type as of data from 2016 pilots by 12.31.2016 ...................... 39

Table 18. Unit cost per meter: 2015 pilots and 2016 pilots ................................................................. 39

Table 19. Auxiliaries installed in the pilot projects in order to ensure communication ....................... 44

Table 20. Advantages and disadvantages of solutions to capping smart metering market prices ...... 47

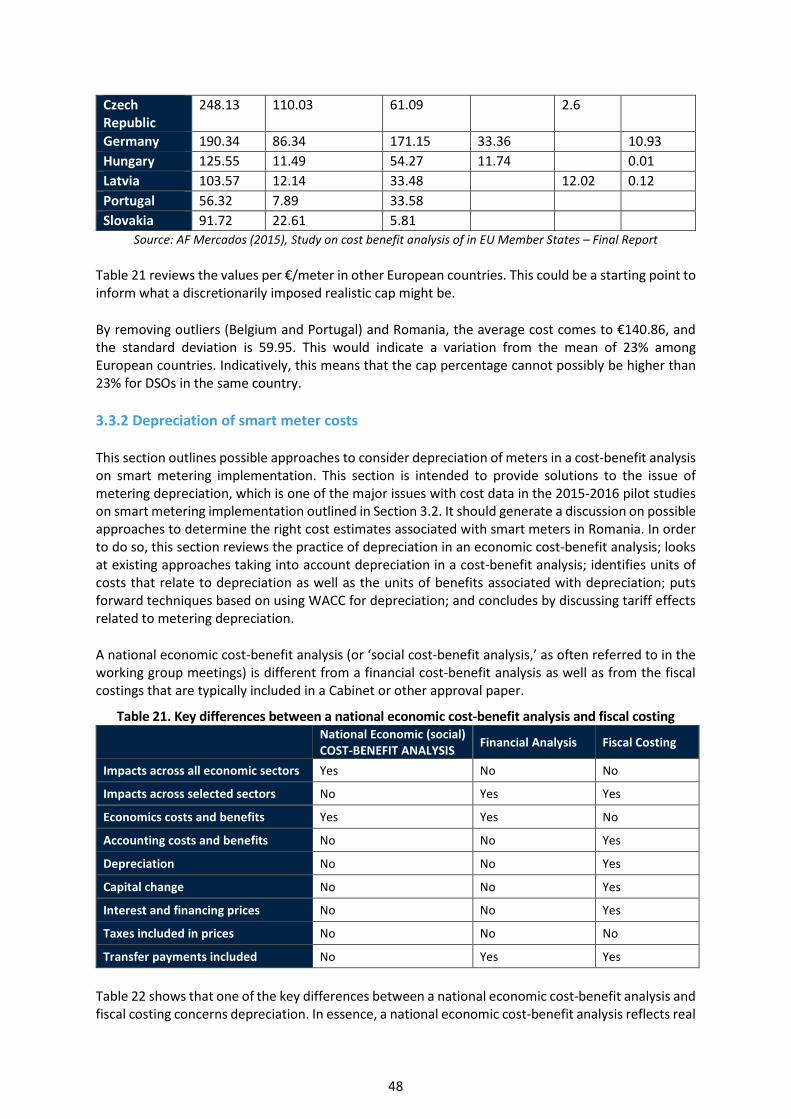

Table 21. Values per €/meter in other European countries ................................................................. 47

Table 22. Key differences between a national economic cost-benefit analysis and fiscal costing ...... 48

Table 23. Depreciation of CAPEX in the Irish cost-benefit analysis ...................................................... 50

Table 24. The main benefits of smart meters (from 2015 pilot studies) .............................................. 54

Table 25. Smart meter additional benefits (from 2015 pilot studies) .................................................. 55

Table 26. Calculations for deriving reductions in technical losses ....................................................... 57

Table 27. Studies filling gaps in terms of wider stakeholder data ........................................................ 63

Table 28. Comparison between four approaches ................................................................................. 66

5

LIST OF ACRONYMS Acronyms Explanation

ANRE National Regulatory Authority for Energy (Autoritatea Naţională de Reglementare în Domeniul Energiei)

CAPEX Capital expenditure CBA Cost-benefit analysis DCC Data and Communications Company DSO Distribution system operator ERGEG European Regulators' Group for Electricity and Gas GPRS General packet radio services HV High voltage IA Impact assessment ICT Information communication technologies IEA International Energy Agency IHD In-home display LV Low voltage MV Medium voltage NPV Net present value OPEC Operational expenditure PLC Power line communication RIA Regulatory Impact Assessment SAIDI System average interruption duration index SAIFI System average interruption frequency index SM Smart meter SN Substantiation note ToU Time of use

6

ACKNOWLEDGEMENTS

This report is delivered under the Advisory Services Agreement on “Developing the Capacity of the Central Public Administration to Carry Out Impact Studies” between the General Secretariat of the Government and the International Bank for Reconstruction and Development, signed on March 9, 2016. It is part of Output 1, “Two reports on impact assessment, one report on data collection and analytical methodology used for the impact assessment in emergency medicine, one report on analytical methodology for the impact assessment in smart metering, and one report documenting the dissemination event to share international experience on smart metering, as set forth in Component A.1(b) and A.1(c)” under the above-mentioned agreement, respectively under the Amendment No. 1 to the agreement.

This report was prepared by a World Bank team that includes: Francesca de Nicola, Arabela Aprahamian, Mădălina Prună and Oana Franț. The following international and Romanian experts provided technical and methodological guidance: Jacopo Torriti and Otilia Nutu.

The team would like to thank Marialisa Motta, Paulo Guilherme Correa, Tatiana Proskuryakova, Elisabetta Capannelli, and the Romania Portfolio Team for the continuous advice and support provided. The report benefitted from helpful comments from the following colleagues and peer-reviewers: Catalin Pauna, Alfredo Briseno, and Varun Nangia.

The team would also like to thank the counterparts in the Department for the Coordination of Policies and Priorities in the Chancellery of the Prime Minister led by Oana Pintilei, Ramona Oana Lohan, Radu Puchiu, Dragos Negoita and Anca Lupu for the precious support and collaboration provided.

Disclaimer

This report is a product of the International Bank for Reconstruction and Development/the World Bank. The findings, interpretation, and conclusions expressed in this paper do not necessarily reflect the views of the Executive Directors of the World Bank or the Governments they represent. The World Bank does not guarantee the accuracy of the data included in this work.

This report does not necessarily represent the position of the European Union or the Romanian Government.

Copyright Statement

The material in this publication is copyrighted. Copying and/or transmitting portions of this work without permission may be a violation of applicable laws.

For permission to photocopy or reprint any part of this work, please send a request with the complete information to either: (i) General Secretariat of the Government - Chancellery of the Prime Minister, Directorate for Coordination of Policy and Programs (Victoriei Square, No 1, Bucharest, Romania) or (ii) the World Bank Group Romania (Vasile Lascăr Street, No 31, Et 6, Sector 2, Bucharest, Romania).

7

EXECUTIVE SUMMARY

Romania needs to make important decisions on smart metering implementation, but has yet to conduct an up-to-date cost-benefit analysis that fully measures the economic impacts of this radical change in electricity systems. A cost-benefit analysis is the most diffused economic tool for appraising the costs and benefits of different policies and regulations. The importance of a cost-benefit analysis is higher for policies that are associated with substantial investments of public resources. The implementation of smart meter implementation systems falls within the category of investments. This report summarizes the data on costs and benefits available to date and provides information about methodologies for carrying out a cost-benefit analysis of smart metering in Romania.

The report presents the main features of existing cost-benefit analyses of smart metering in the following European countries: Germany, the UK, the Netherlands, Ireland, Hungary, and France. The main lessons learned for Romania relate to reductions in electricity consumption and loss reductions. Consumption reduction critical for cost-benefit analysis because of the long-term savings it can generate: a relatively small percentage of benefits in terms of savings are multiplied by millions of users.

The total cost of smart metering implementation generally ranges between €50 and €100 per meter. In Germany, where the most expensive communications technology (GPRS) is adopted, the cost for the entire system is estimated at over €233 per metering point. On the other hand, the cheapest communications technology (PLC) is principally applied in the countries with the lowest reported cost, including Romania and Hungary. About 93% of the costs are associated with communications, IT, and meters. Overall, the total discounted costs for the UK, Germany, the Netherlands, Ireland, and Hungary are, respectively, €281.65, €492.12, €240.28, €260.49, and €242.42. These are significantly high compared to the Romanian estimate of costs, i.e. €97.73, from the AT Kearney study.

In regard to benefits, reductions in meter reading operations vary from €14.5 per meter (in Hungary) to €145.8 (in the UK). The discrepancies between reduction meter reading costs can be connected to divergent regulatory and operational arrangements with regard to the billing cycle and differences in labor costs (as explained above about installation costs). Reductions in the technical losses of electricity are high only for the UK and Romania. Reductions in commercial losses are significantly higher (€43.6) in the AT Kearney study for Romania than in any other country, with Hungary as the second highest at €19.6. Overall, the total discounted benefits for the UK, Germany, Netherlands, Ireland, and Hungary are, respectively, €308.9, €484.9, €287.3, €187.7, €164.6, and €129.4.

The report also presents available Romanian data from the distribution system operators (DSOs) as part of the 2015-2016 pilot studies on smart metering implementation. Overall, the average cost per meter varied significantly from the initial cost appraisal in the AT Kearney study, which was estimated as 98 EUR per consumer. Actual costs in the 2015 pilots were 126 EUR per consumer and 60 EUR RON per consumer in the 2016 pilots. Initial costs per consumer in the pilot projects submitted to ANRE for approval in 2016 were 93 EUR. Overall, costs decreased substantially between the pilots in 2015 and 2016. Regarding communication costs, cheaper PLC solutions were widely adopted with costs as low as 15 EUR per consumer; however, communication costs reached 57-61 EUR per consumer where GSM/GPRS and RF were installed.

Benefits from the 2015-2016 pilot studies on smart metering implementation point to meter reading costs reductions of 55-97%, a reduction of operating costs for activities requiring the physical presence of specialized teams of 27-97%, and CPT reduction varying from increases of 38% to reductions of up to 100%.

8

These findings point to the challenges of carrying out a precise cost-benefit analysis for smart metering implementation. A set of technical and methodological issues is raised in regard to issues with missing benefits data, smart metering cost data, the depreciation of meters, and tariff effects.

The report does not cover emerging areas of costs and benefits associated with the digitalization of metering infrastructure. These include cybersecurity and the standardization of interoperability. In addition, recent evidence from the rollout process in other European countries suggests that the non-acceptance of meters at the end-user level may increase the costs of meter replacement and reduce benefits.

It is concluded that Romania is in a good position to perform a meaningful cost-benefit analysis, but more attention needs to be paid to the entirety of stakeholders, including end-users. The following recommendations are provided in regard to carrying out a full cost benefit analysis of smart meters in Romania:

1. embedding findings from pilot studies in decisions on smart metering rollout;

2. focusing on societal costs and benefits; and

3. quantifying electricity cost savings for consumers.

The report provides an indication of the implications regarding time and different data and methodology options associated with these recommendations.

9

1. STATUS QUO

Romania needs to make important decisions on smart metering implementation, but has yet to conduct an up-to-date cost-benefit analysis that fully measures the economic impacts of this radical change in electricity systems. This report summarizes the data on costs and benefits available to date and provides information about methodologies for carrying out a cost-benefit analysis on smart metering in Romania.

Similar to other countries, decisions concerning substantial public investments in smart metering infrastructure are very difficult for policy-makers without the support of strong empirical evidence.

Advocates of smart metering list several benefits, including lower metering cost, energy savings for residential customers, greater supply reliability, variable pricing schemes to attract new customers, and easier detection of fraud. In addition, other benefits are foreseen in relation to distributed generation as the smart meter can be used to separately measure electricity delivered by distributed generation to the grid. Moreover, the smart metering communication infrastructure can be used to remotely control distributed generation. Demand side response and dynamic pricing can be enabled via the smart meter.

On the other hand, some argue that smart meters at the societal level may bring about more costs than benefits. For instance, there is limited evidence so far that smart meters will save energy (or money) to end-users. The presence of smart meters may not end estimated billing and may even make it more difficult for consumers to switch suppliers. Other drawbacks of smart metering rollouts include making a long-term financial commitment to the new metering technology and related software; managing and storing vast quantities of metering data; and ensuring the security of metering data.

The decision on whether and how to spend several millions of Euros on such a radical change for electricity systems cannot be based solely on perceptions, lobbying, and private interests. The decision on smart metering implementation in Romania will have to be based on the economic rationale of a cost-benefit analysis and emphasize costs and benefits associated with end users.

This report sets out to inform the smart metering community of public policy-makers, regulators, the industry, and civil society about data and methodologies that should be adopted when carrying out a cost-benefit analysis of Smart Metering implementation in Romania. The report takes into account work carried out as part of the World Bank Group pilot project and international experiences with cost-benefit analyses of smart metering.

1.1. The importance of cost-benefit analysis for smart metering implementation in Romania

Cost-benefit analysis is the most diffused economic tool for appraising the costs and benefits of different policies and regulations. The importance of cost-benefit analysis is greater for policies that feature large investments of public resources. Cost-benefit analyses on smart meter implementation are within this category.

Cost-benefit analysis determines whether the benefits of a project or decision outweigh its costs. When, as is the case for national energy policies and regulations, public authorities perform cost-benefit analyses, the costs and benefits consist of broad and societal impacts from a public perspective. In other words, public cost-benefit analyses take a wider societal perspective,

10

determining whether a project is a good allocation of societal resources, without regard to the distribution of benefits.

Like other European Union (EU) Member States, the Romanian government has an obligation to carry out a cost-benefit analysis as a result of the EU Third Energy Package requirement in order to determine the viability of a smart rollout. The recommended methodological approach to developing a cost-benefit analysis on smart meters is presented in the European Commission’s Recommendation 2012/148/EU1. Key aspects of the methodology involve (i) the approach; (ii) minimum functionality of the smart metering system; (iii) costs; and (iv) benefits.

In addition to the EU obligation, carrying out an updated cost-benefit analysis will inform the complex decision-making associated with a sizable investment for the Romanian government. The impacts from a rollout of smart meters will involve a range of actors: (i) consumers (in terms of accurate costs and real-time information to enable them to manage energy consumption and potentially receive new services), (ii) DSOs (in terms of the management of frequent data on consumption and changes in costs to serve), and (iii) society (in terms of carbon emissions). There are also benefits for the transmission system operator stemming from the use—subject to appropriate data, privacy, and access controls—of data collected through smart metering to better manage the network and to inform long-term investment in the electricity grid. Assessing the costs and benefits of intervention also means taking into account the volumes of smart metering implementation that would occur without direct government investment.

DSOs regularly invest large sums in utility equipment devoted to public service in pursuit of their regulatory or charter obligations to serve. Extending and maintaining the service of deprived or underdeveloped distribution networks, for example, is a generally accepted unit of cost that is often implicit in the regulatory obligations. DSOs are well placed to assess the costs and benefits of these investments as they routinely fulfill these non-discretionary obligations while minimizing the cost of doing so. Regulators are also prepared to defend their decisions in this cost-minimization framework while relying on data supplied by utilities. However, smart metering development may not fit into this time-tested paradigm of cost minimization because it brings about a higher level of innovation and relates to the whole network. For instance, if a smart meter in a low-voltage distribution network can improve reliability beyond currently acceptability levels, it is unclear whether it is mandatory to invest resources to do so. This may depend on how much must be invested to obtain the improvements for DSOs, suppliers and consumers and whether the improvement gained is worth the money.

These complexities call for a consistent approach when selecting the type of data and methodologies that should be included in any cost-benefit analysis of smart metering implementation.

1.2. Scope and objectives of this report

The main aim of this report is to provide guidance in regard to the data and methodologies for a cost-benefit analysis of smart metering implementation in Romania. The report takes into account work carried out as part of the World Bank Group pilot project as well as examples of cost-benefit analyses performed in Europe for smart metering.

The report is to be read as the technical accompanying document of “Report 1 - How to carry out a RIA on smart metering in Romania.” It presents a comprehensive set of guidelines and specific instructions for estimating the benefits and costs of smart meter implementation. It combines

1 European Commission Recommendation 2012/148/EU of March 9, 2012 on preparations for the rollout of smart metering systems (OJ L 73, 13.3.2012, p.9).

11

economic techniques for cost-benefit analysis with smart meter specific knowledge, hence pointing to possible methodological and data-related solutions. It is not a cost-benefit analysis of smart meters in Romania per se; rather, it offers guidance regarding methodological and data issues that should be considered when carrying out such an analysis.

Performing a cost-benefit analysis of smart meters poses interesting and challenging problems in terms of measuring physical impacts and estimating economic benefits from them. However, when smart meters are part of first-of-kind or pilot projects (as is the case in Romania), there are additional challenges to producing a meaningful cost-benefit analysis.

1.3. Background: What has been done thus far in the area of costs and benefits of smart meters in Romania

The AT Kearney study was carried out in 2012 for the European Bank of Reconstruction and Development.

The overall approach of the AT Kearney cost-benefit analysis consists of an engineering bottom-up costing technique. The cost-benefit analysis considers different cost layers (i.e., meter layer, middleware layer, and application layer), system maintenance, and costs of financing. The layers consist of data concentrators and balancing meters placed on each substation. The data communication takes place through PLC wiring from the meters to the concentrators and through various communication channels from concentrators to the central application.

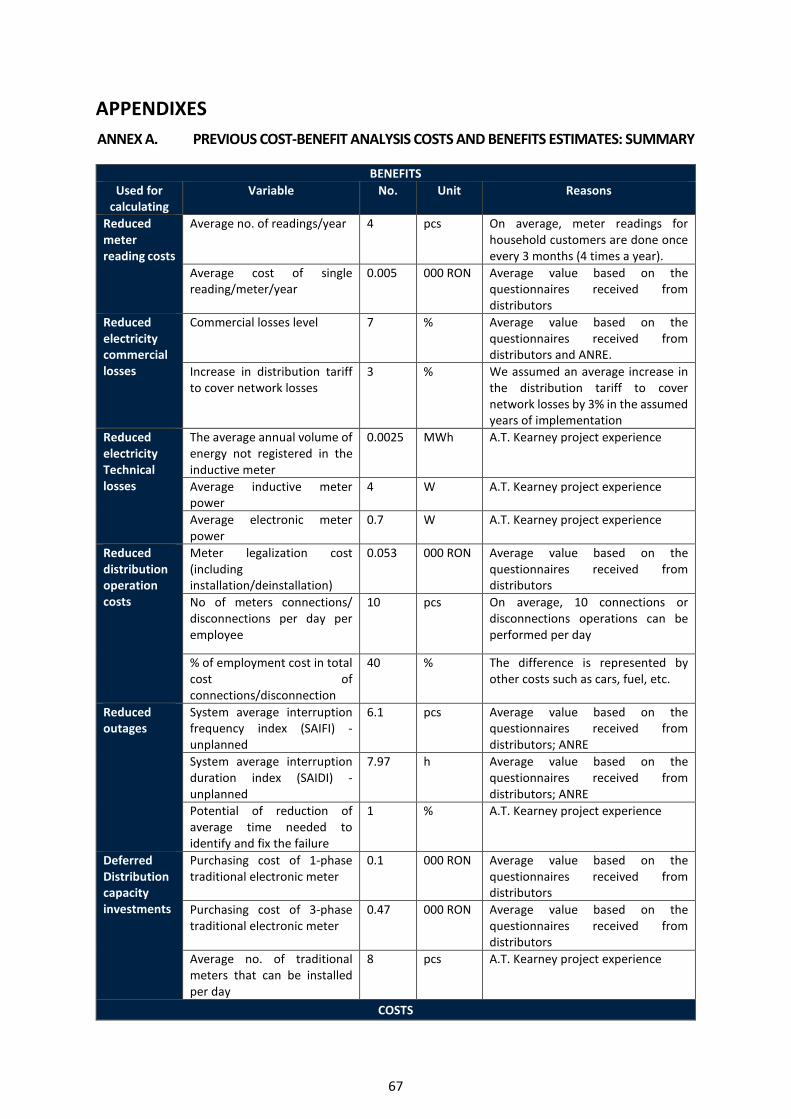

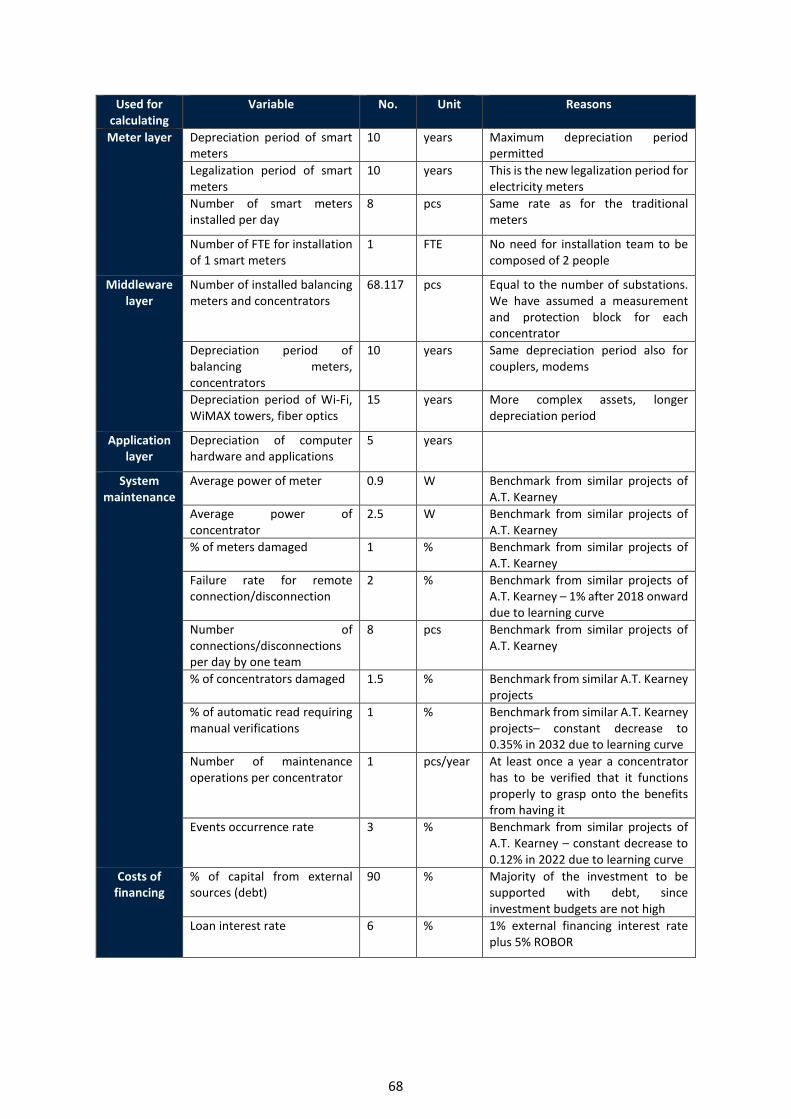

Table 1. List of costs and cost-related assumptions Used for

calculating Variable No. Unit Reasons

Meter layer

Depreciation period of smart meters

10 years Maximum depreciation period permitted

Legalization period of smart meters

10 years This is the new legalization period for electricity meters

Number of smart meters installed per day

8 pcs Same rate as for the traditional meters

Number of FTE for the installation of 1 smart meter

1 FTE No need for installation team to be composed of 2 people

Middleware layer

Number of installed balancing meters and concentrators

68.117 pcs Equal to the number of substations. We have assumed a measurement and protection block for each concentrator

Depreciation period of balancing meters, concentrators

10 years Same depreciation period for couplers, modems

Depreciation period of Wi-Fi, WiMAX towers, fiber optics

15 years More complex assets, longer depreciation period

Application layer

Depreciation of computer hardware and applications

5 years

System maintenance

Average power of meter 0.9 W Benchmark from similar projects of A.T. Kearney

Average power of concentrator 2.5 W Benchmark from similar projects of A.T. Kearney

% of meters damaged 1 % Benchmark from similar projects of A.T. Kearney

12

Failure rate for remote connection/disconnection

2 % Benchmark from similar projects of A.T. Kearney – 1% after 2018 onward due to learning curve

Number of connections/disconnections per day by one team

8 pcs Benchmark from similar projects of A.T. Kearney

% of concentrators damaged 1.5 % Benchmark from similar projects of A.T. Kearney

% of automatic read requiring manual verifications

1 % Benchmark from similar projects of A.T. Kearney – constant decrease to 0.35% in 2032 due to learning curve

Number of maintenance operations per concentrator

1 pcs/ year

At least once a year a concentrator has to be verified that it functions properly to grasp onto the benefits from having it

Events occurrence rate 3 % Benchmark from similar projects of A.T. Kearney – constant decrease to 0.12% in 2022 due to learning curve

Costs of financing

% of capital from external sources (debt)

90 % Majority of the investment to be supported with debt since investment budgets are not high

Loan interest rate 6 % 1% external financing interest rate plus 5% ROBOR

The original AT Kearney cost categories and cost-related assumptions are summarized in Table 1.

The unit costs of the proposed system are low when compared with other European countries (Section 2 of this report). The average expenditure per metering point is estimated at just under €100. The report includes total costs and unit costs of meters, data concentrators, and balancing meters, though the total costs are not broken down into capital and operating expenditures. These originally did not include a €25 per metering point cost of distribution investment. Areas of costs and benefits that are not included in the AT Kearney study (and should be included, as stated by the EU Recommendation (2012/148/EU) are call center costs, consumption impact (apart from via commercial losses), CO2 costs (though these are considered separately), and the deferral of network investment benefits.

Table 2. Benefits and benefits-related assumptions Used for calculating Variable No. Unit Reasons

Reduced meter

reading costs

Average no. of readings/year 4 pcs On average, meter readings for household customers are done once every 3 months (4 times a year)

Average cost of single reading/meter/year

0.001 000 EUR Average value based on the questionnaires received from distributors

Reduced electricity

commercial losses

Commercial losses level 7 % Average value based on the questionnaires received from distributors and ANRE

Increase in distribution tariff to cover network losses

3 % We assumed an average increase in the distribution tariff to cover network losses by 3% in the assumed years of implementation

Reduced electricity Technical

losses

The average annual volume of energy not registered in the inductive meter

0.0025 MWh A.T. Kearney project experience

Average inductive meter power 4 W A.T. Kearney project experience

13

Average electronic meter power

0.7 W A.T. Kearney project experience

Reduced distribution operation

costs

Meter legalization cost (including installation/deinstallation)

0.011 000 EUR Average value based on the questionnaires received from distributors

No. of meters connections/ disconnections per day per employee

10 pcs On average, 10 connections or disconnections operations can be performed per day

% of employment cost in total cost of connections/disconnection

40 % The difference is represented by other costs like cars, fuel, etc.

Reduced outages

System average interruption frequency index (SAIFI) - unplanned

6.1 pcs Average value based on the questionnaires received from distributors; ANRE

System average interruption duration index (SAIDI) – unplanned

7.97 h Average value based on the questionnaires received from distributors; ANRE

Potential of reduction of average time needed to identify and fix the failure

1 % A.T. Kearney project experience

Deferred Distribution

capacity investments

Purchasing cost of 1-phase traditional electronic meter

0.21 000 EUR Average value based on the questionnaires received from distributors

Purchasing cost of 3-phase traditional electronic meter

0.1 000 EUR Average value based on the questionnaires received from distributors

Average no. of traditional meters that can be installed per day

8 pcs A.T. Kearney project experience

Almost 70% of the overall benefits of the project are accounted for by two variables– reduced manual meter reading costs, which is based on a savings of 4 manual reads per meter per year; and reduced commercial losses. In the core scenario, it is assumed that commercial losses—estimated at 7%—will be reduced by 60% of this amount. The only end-user level demand impact included under the benefits is indirectly related to the commercial losses, as it is assumed that 50% of the reduction in commercial losses will be subsequently invoiced to customers, and 50% manifest in a reduction in consumption.

14

2. COST-BENEFIT ANALYSES OF SMART METERS IN OTHER EUROPEAN COUNTRIES

Romania is not alone when it comes to conducting cost-benefit analyses of smart metering implementation. This section presents the main features of existing cost-benefit analyses of smart metering in the following European countries: Germany, the UK, the Netherlands, Ireland, Hungary, and France. It concludes by identifying key lessons learned for Romania in terms of data and methodological issues associated with categories of costs and benefits.

All European countries had to follow the recommendations of the European Commission, though their cost-benefit analyses all varied, as it is explained in this section of the report. To facilitate the take-up of this new technology the European Commission published Recommendation (2012/148/EU) to prepare for the rollout of smart-metering systems. The recommendation provides step-by-step guidelines for Member States regarding how to conduct a cost-benefit analysis. It also refers to the common minimum functionalities of smart metering systems and addresses data protection and security issues.

The recommendation puts forward a four-stage approach consisting of the following:

1. Tailoring to local conditions - Pilot programs and “real-life” experience should be used in assumptions. At least two scenarios should be contemplated: (a) BAU; and (b) an 80% rollout by 2020.

2. Cost-benefit analysis – This is supposed to follow “seven CBA steps,” indicating costs to be incurred by the consumer and to be compared with long-term benefits.

3. Sensitivity analysis – The analysis should identify “critical variables” and analyze the magnitude of the cost-benefit analysis’ outcome for the positive rollout conditions (i.e., when benefits exceed costs).

4. Performance assessment, externalities, and social impact – The analysis is supposed to assess externalities (e.g., in terms of the environment and carbon implications), as well as the impact of public policy measures and social benefits (i.e., ensuring appropriate weighting factors).

The seven CBA steps are not mandatory and involve the following:

1. Reviewing and describing technologies, elements, and goals. 2. Mapping assets into functionalities. 3. Mapping functionalities into benefits. 4. Establishing the baseline. 5. Monetizing benefits and identifying beneficiaries. 6. Identifying and quantifying costs. 7. Comparing costs and benefits.

In the implementation of this methodological approach, various factors need to be considered, including the following:

• The distinction between social and private costs and benefits. The principal purpose of the cost-benefit analysis is to determine if a widespread rollout of smart meters is economically viable for the country as a whole. In practice, certain participants may bear a disproportionate share of the costs, which by itself does not provide grounds for overturning the results. However, benefits distribution issues are critical at the implementation stage and, in particular, during the development of policy recommendations.

15

• The period of analysis, including whether the replacement of “new” assets (smart meters/communications equipment) is to be considered and, in any case, the terminal value of these assets at the end of the modelling period, where a residual value of assets will be present.

• The time profile of costs and benefits, particularly in the period of the rollout. • The discount rate to be applied.

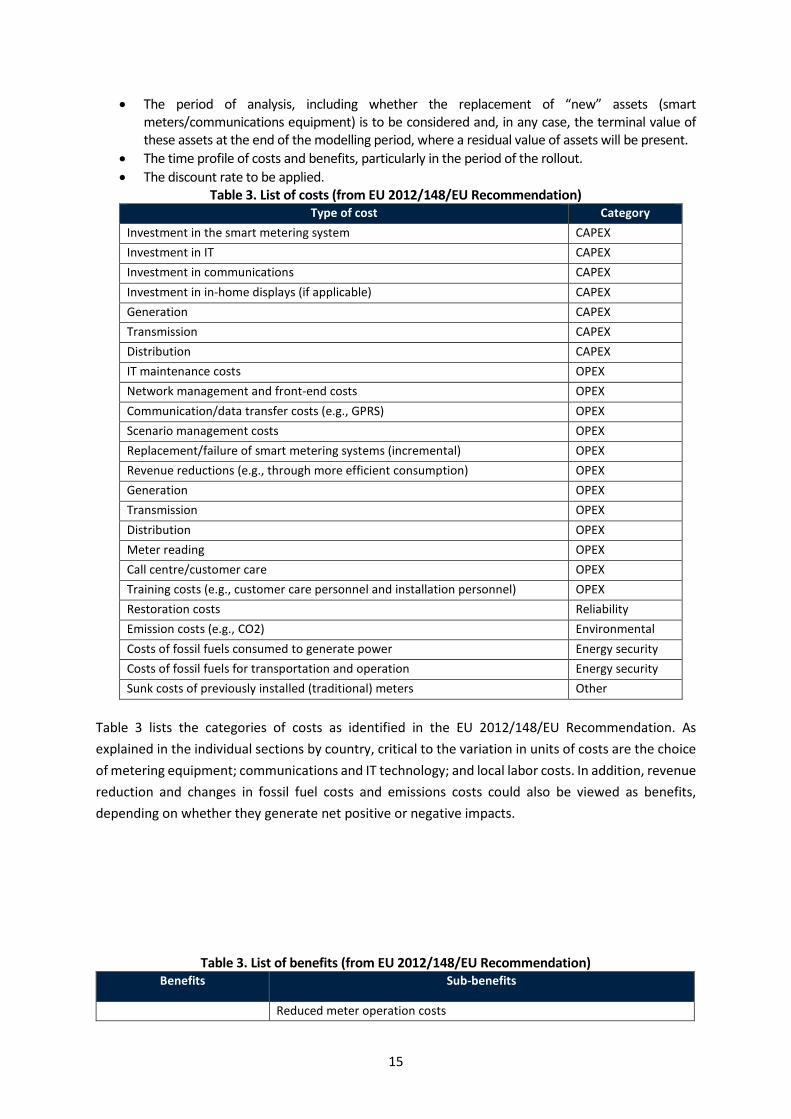

Table 3. List of costs (from EU 2012/148/EU Recommendation) Type of cost Category

Investment in the smart metering system CAPEX Investment in IT CAPEX Investment in communications CAPEX Investment in in-home displays (if applicable) CAPEX Generation CAPEX Transmission CAPEX Distribution CAPEX IT maintenance costs OPEX Network management and front-end costs OPEX Communication/data transfer costs (e.g., GPRS) OPEX Scenario management costs OPEX Replacement/failure of smart metering systems (incremental) OPEX Revenue reductions (e.g., through more efficient consumption) OPEX Generation OPEX Transmission OPEX Distribution OPEX Meter reading OPEX Call centre/customer care OPEX Training costs (e.g., customer care personnel and installation personnel) OPEX Restoration costs Reliability Emission costs (e.g., CO2) Environmental Costs of fossil fuels consumed to generate power Energy security Costs of fossil fuels for transportation and operation Energy security Sunk costs of previously installed (traditional) meters Other

Table 3 lists the categories of costs as identified in the EU 2012/148/EU Recommendation. As explained in the individual sections by country, critical to the variation in units of costs are the choice of metering equipment; communications and IT technology; and local labor costs. In addition, revenue reduction and changes in fossil fuel costs and emissions costs could also be viewed as benefits, depending on whether they generate net positive or negative impacts.

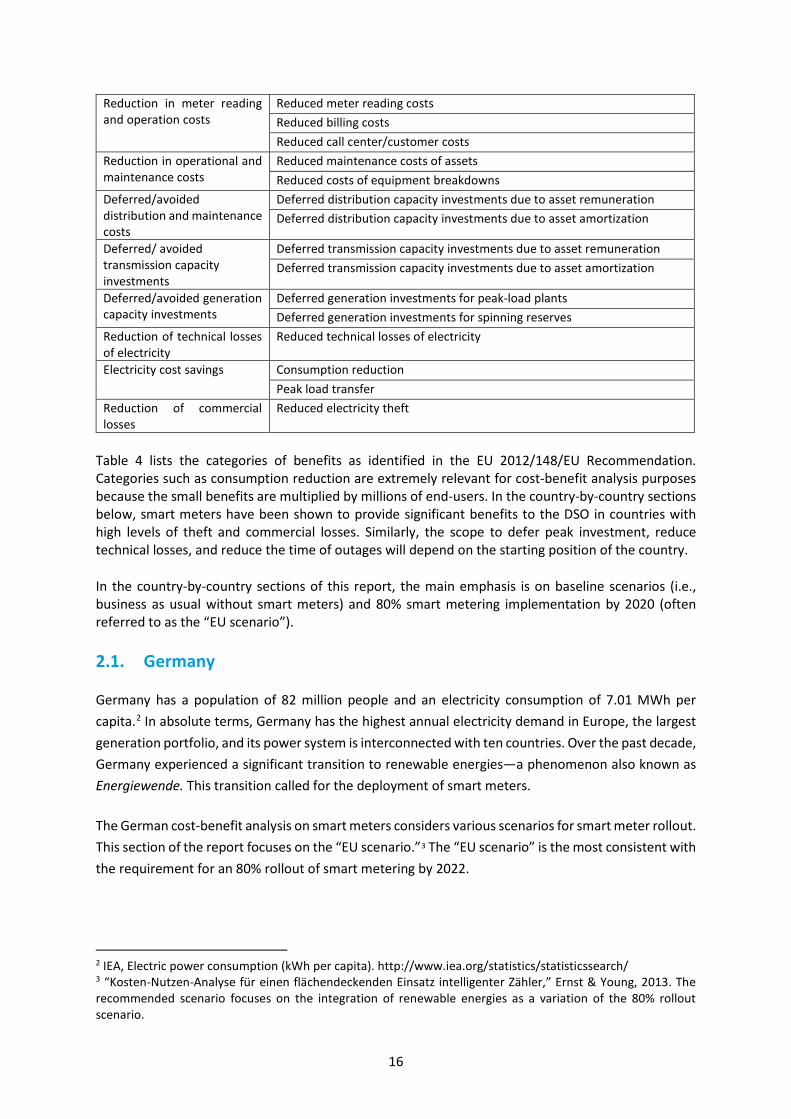

Table 3. List of benefits (from EU 2012/148/EU Recommendation) Benefits Sub-benefits

Reduced meter operation costs

16

Reduction in meter reading and operation costs

Reduced meter reading costs Reduced billing costs Reduced call center/customer costs

Reduction in operational and maintenance costs

Reduced maintenance costs of assets Reduced costs of equipment breakdowns

Deferred/avoided distribution and maintenance costs

Deferred distribution capacity investments due to asset remuneration Deferred distribution capacity investments due to asset amortization

Deferred/ avoided transmission capacity investments

Deferred transmission capacity investments due to asset remuneration Deferred transmission capacity investments due to asset amortization

Deferred/avoided generation capacity investments

Deferred generation investments for peak-load plants Deferred generation investments for spinning reserves

Reduction of technical losses of electricity

Reduced technical losses of electricity

Electricity cost savings Consumption reduction Peak load transfer

Reduction of commercial losses

Reduced electricity theft

Table 4 lists the categories of benefits as identified in the EU 2012/148/EU Recommendation. Categories such as consumption reduction are extremely relevant for cost-benefit analysis purposes because the small benefits are multiplied by millions of end-users. In the country-by-country sections below, smart meters have been shown to provide significant benefits to the DSO in countries with high levels of theft and commercial losses. Similarly, the scope to defer peak investment, reduce technical losses, and reduce the time of outages will depend on the starting position of the country.

In the country-by-country sections of this report, the main emphasis is on baseline scenarios (i.e., business as usual without smart meters) and 80% smart metering implementation by 2020 (often referred to as the “EU scenario”).

2.1. Germany

Germany has a population of 82 million people and an electricity consumption of 7.01 MWh per capita.2 In absolute terms, Germany has the highest annual electricity demand in Europe, the largest generation portfolio, and its power system is interconnected with ten countries. Over the past decade, Germany experienced a significant transition to renewable energies—a phenomenon also known as Energiewende. This transition called for the deployment of smart meters.

The German cost-benefit analysis on smart meters considers various scenarios for smart meter rollout. This section of the report focuses on the “EU scenario.”3 The “EU scenario” is the most consistent with the requirement for an 80% rollout of smart metering by 2022.

2 IEA, Electric power consumption (kWh per capita). http://www.iea.org/statistics/statisticssearch/ 3 “Kosten-Nutzen-Analyse für einen flächendeckenden Einsatz intelligenter Zähler,” Ernst & Young, 2013. The recommended scenario focuses on the integration of renewable energies as a variation of the 80% rollout scenario.

17

The technological choice of Germany consisted of a gateway located in the consumer premises that manages the transfer of data to necessary parties. It provides high levels of data protection (privacy and security) to the customer. There are two important considerations: (i) the gateway configuration involves higher costs than other approaches; and (ii) the benefit of allowing the connection of other utility services to the same infrastructure (e.g., gas and heating).

Table 4. Main assumptions underpinning German Cost-Benefit Analysis Key assumption Unit Value

Rollout period Years 2012-2022 Proportion of metering points covered % 80% by 2022 Modeling period Years 2012-2032 Discount rate % 5% commercial, 3.1% residential and industrial Asset life of meters Years 13 Number of avoided meter readings Number/meter 1 Reduction in consumption % Between 0.5% and 2.5% Peak load transfer GW 6.1 Reduction in non-supplied energy % 1% Reduction in theft % 20%

Table 5 shows the main assumptions in the cost-benefit analysis. The benefits and costs are assessed and discounted for a period of twenty years (from 2012 to 2032). The main assumption regards changes in consumption as associated with the presence of smart meters in end-users’ premises. These vary between 0.5% and 2.5%. This is a five-fold variation that can significantly distort the net impacts of smart meters in Germany.

Figure 1. Discounted costs (€/metering point)

Figure 1 shows the discounted costs of smart meters, IT, communications, in-home display, and training. Although the cost-benefit analysis does not provide a full breakdown of costs and benefits of the EU rollout scenario, there are assessments of costs and volumes. Hence, in Figure 1, the values are expressed in terms of Euro per smart meter. The average cost of communications is particularly high when compared with other cost-benefit analyses. This is because the communications configuration opted for includes an 80% use of GPRS technology and only a 20% use of PLC. Hence, the high proportion of GPRS is a key driver of overall communications costs. GPRS technology allows for the remote control of various devices (for instance, solar panels) rather than solely for remote meter reading. Overall, costs are broken down between capital and operating expenditure, with 38.5 million

190.34

86.34

171.15

33.36

10.93

0 20 40 60 80 100 120 140 160 180 200

Average cost of smart meters

Average cost of IT

Average cost of communications

Average cost of in-home displays

Training

18

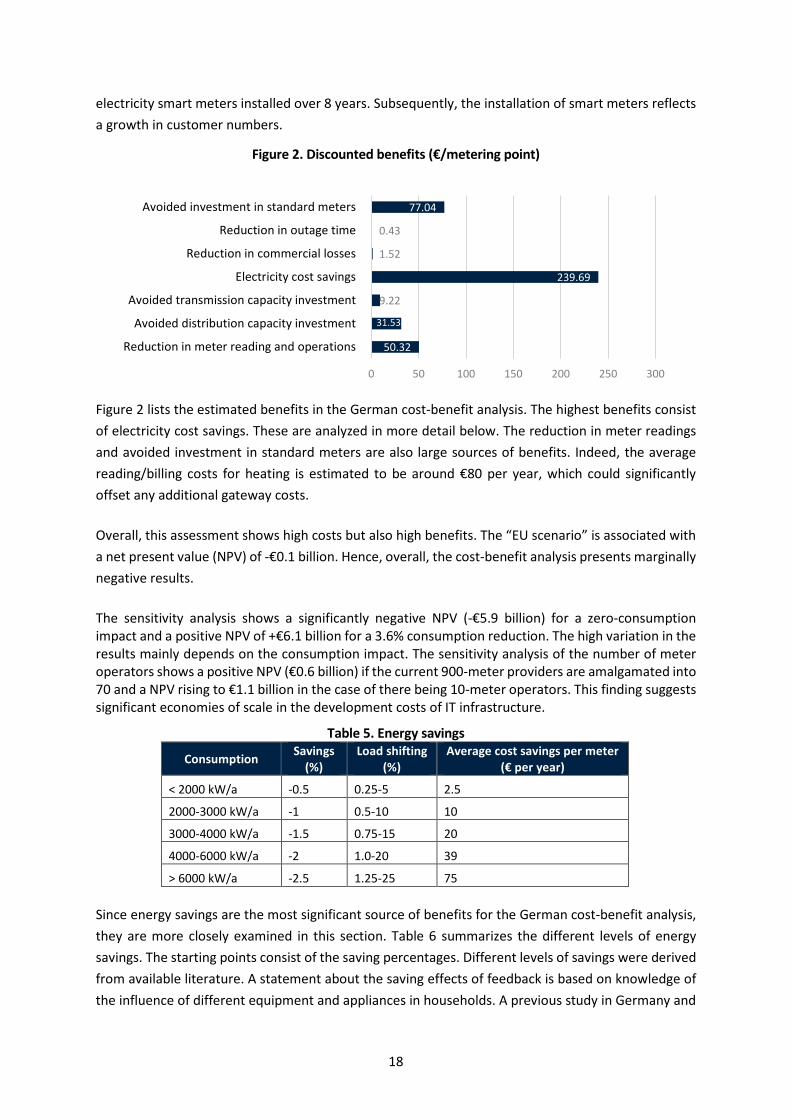

electricity smart meters installed over 8 years. Subsequently, the installation of smart meters reflects a growth in customer numbers.

Figure 2. Discounted benefits (€/metering point)

Figure 2 lists the estimated benefits in the German cost-benefit analysis. The highest benefits consist of electricity cost savings. These are analyzed in more detail below. The reduction in meter readings and avoided investment in standard meters are also large sources of benefits. Indeed, the average reading/billing costs for heating is estimated to be around €80 per year, which could significantly offset any additional gateway costs.

Overall, this assessment shows high costs but also high benefits. The “EU scenario” is associated with a net present value (NPV) of -€0.1 billion. Hence, overall, the cost-benefit analysis presents marginally negative results.

The sensitivity analysis shows a significantly negative NPV (-€5.9 billion) for a zero-consumption impact and a positive NPV of +€6.1 billion for a 3.6% consumption reduction. The high variation in the results mainly depends on the consumption impact. The sensitivity analysis of the number of meter operators shows a positive NPV (€0.6 billion) if the current 900-meter providers are amalgamated into 70 and a NPV rising to €1.1 billion in the case of there being 10-meter operators. This finding suggests significant economies of scale in the development costs of IT infrastructure.

Table 5. Energy savings

Consumption Savings (%)

Load shifting (%)

Average cost savings per meter (€ per year)

< 2000 kW/a -0.5 0.25-5 2.5

2000-3000 kW/a -1 0.5-10 10

3000-4000 kW/a -1.5 0.75-15 20

4000-6000 kW/a -2 1.0-20 39

> 6000 kW/a -2.5 1.25-25 75

Since energy savings are the most significant source of benefits for the German cost-benefit analysis, they are more closely examined in this section. Table 6 summarizes the different levels of energy savings. The starting points consist of the saving percentages. Different levels of savings were derived from available literature. A statement about the saving effects of feedback is based on knowledge of the influence of different equipment and appliances in households. A previous study in Germany and

50.32

31.53

9.22

239.69

1.52

0.43

77.04

0 50 100 150 200 250 300

Reduction in meter reading and operations

Avoided distribution capacity investment

Avoided transmission capacity investment

Electricity cost savings

Reduction in commercial losses

Reduction in outage time

Avoided investment in standard meters

19

Austria by Fraunhofer4 showed that the group which received feedback on their electricity demand had a 3.7 % lower energy consumption than the reference group. This amounts to an average of 125 kWh per year. The difference between the groups with and without feedback is somewhat smaller than expected—older studies from other countries found savings of 7%, although the circumstances were very different in those cases. In Linz, the effect remained at the same level during the entire field trial, whereas in Germany no reliable statement about the stability of the effects can be made, as the data basis was too small there.

Table 6. Sensitivity analysis: changes that induce negative net present values Changes/sensitivities Variations in NPV (billions of €)

No energy savings -5.7 Shortfall of grid efficiency -2.9 Extension of the deadline to smart meters from 2018 to 2022 -0.7 Periodic replacement after 24 years -0.6 Shortfall of economies of scale of procurement -2.2

Table 7 illustrates the findings from the sensitivity analysis regarding those changes that induce a negative variation in NPV. The highest sensitivity is associated with energy savings. This means that a null effect of smart meters on end-users would reduce the societal benefits of smart meters to an extent that the NPV would decrease by €5.7 billion. A shortfall in terms of grid efficiency would also generate a substantial reduction in benefits (€2.9 billion). An extension of the deadline to smart meters from 2018 to 2022, periodic replacement after 24 years, and a shortfall of economies of scale of procurement were also considered as sensitivities that bring about negative changes to the overall profitability of smart metering implementation.

2.2. The United Kingdom

The UK has a population of 65 million people and an electricity consumption of 5.08 MWh per capita.5 The country has a rapidly evolving electricity system in which renewable energy sources account for around a quarter of electricity generation. In addition to smart meters, other technological innovations (electric vehicles and new types of storage) are also changing how the British market operates.

The UK government decided to mandate a rollout of meters in October 2009—a year and a half before the results of the pilot trials were published. The UK rollout is characterized by its voluntary (for consumers) nature and by the fact that it is supplier-led.

The UK government produced five cost-benefit analyses on smart meters. The first one was commissioned over ten years ago6, whereas t the Department of Energy and Climate Change (DECC) produced the most recent in 20167. The main reason for the multitude of cost-benefit analyses is that the UK government revised timetables under which suppliers are required to take all reasonable steps

4 Intellekion Project: Achieving Sustainable Energy Consumption with Smart Metering, Communication and Tariff Systems. https://www.intelliekon.de/ergebnisse/downloads/307_Ergebnisbericht_engl_klein.pdf 5 IEA, Electric power consumption (kWh per capita). http://www.iea.org/statistics/statisticssearch/ 6 MacDonald, M. (2007). Appraisal of Costs & Benefits of Smart Meter Roll Out Options. Final Report. Report for Department of Business Enterprise and Regulatory Reform, London. 7 BEIS (2016). Smart Meter Rollout Cost-Benefit Analysis, available at: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/567167/OFFSEN_2016_smart_meters_cost-benefit-update_Part_I_FINAL_VERSION.PDF

20

to complete their rollout by the end of 2020. These developments were reflected in the different version of impact assessments published between 2009 and 2016.

In between these assessments, the UK government conducted other impact assessments. In 2009, impact assessments informed the appraisal of alternative options for the preferred market model for the rollout. Options previously considered and discarded include a fully competitive model, a fully centralized model, and a DNO-led deployment.

In 2010 and 2011, the government considered options for the implementation of the preferred market model: a supplier-led rollout with a centralized provision of communications and data services. Detailed policy design options were considered and assessed. These included the completion date, the establishment and scope of the Data and Distribution Company (DCC), the functionality of the smart meter, the rollout strategy, and the strategy for consumer engagement.

The 2011 Impact Assessment set out the government’s overall approach and timeline for achieving smart metering rollout. In 2012, the impact assessment was further updated with an additional evidence base and supported the introduction of the first tranches of smart metering regulations.

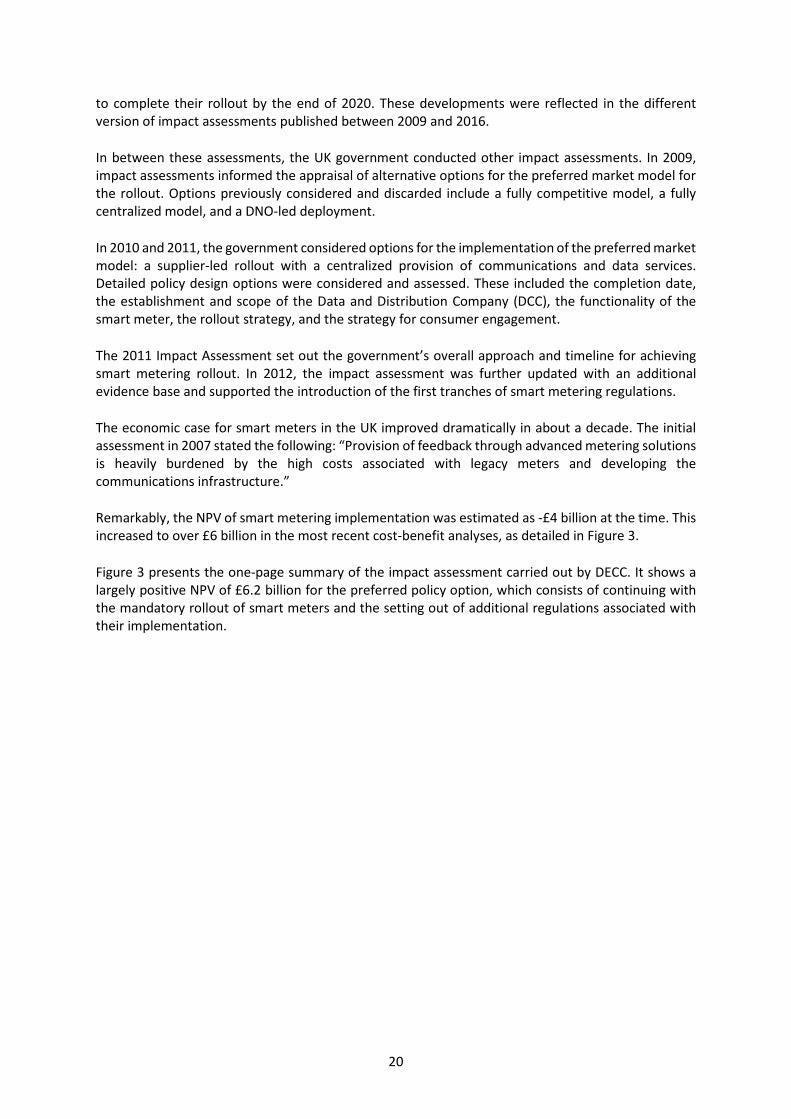

The economic case for smart meters in the UK improved dramatically in about a decade. The initial assessment in 2007 stated the following: “Provision of feedback through advanced metering solutions is heavily burdened by the high costs associated with legacy meters and developing the communications infrastructure.”

Remarkably, the NPV of smart metering implementation was estimated as -£4 billion at the time. This increased to over £6 billion in the most recent cost-benefit analyses, as detailed in Figure 3.

Figure 3 presents the one-page summary of the impact assessment carried out by DECC. It shows a largely positive NPV of £6.2 billion for the preferred policy option, which consists of continuing with the mandatory rollout of smart meters and the setting out of additional regulations associated with their implementation.

21

Figure 3. One-page summary of the impact assessment by DECC (2014)

The overall findings of the cost-benefit analysis (i.e., the economic assessment underpinning the impact assessment) are as follows.

In regard to costs, in-home displays (IHDs) as well as meters and their installation and operation amount to £6.36 billion. Data and Communications Company (DCC) related costs, including a

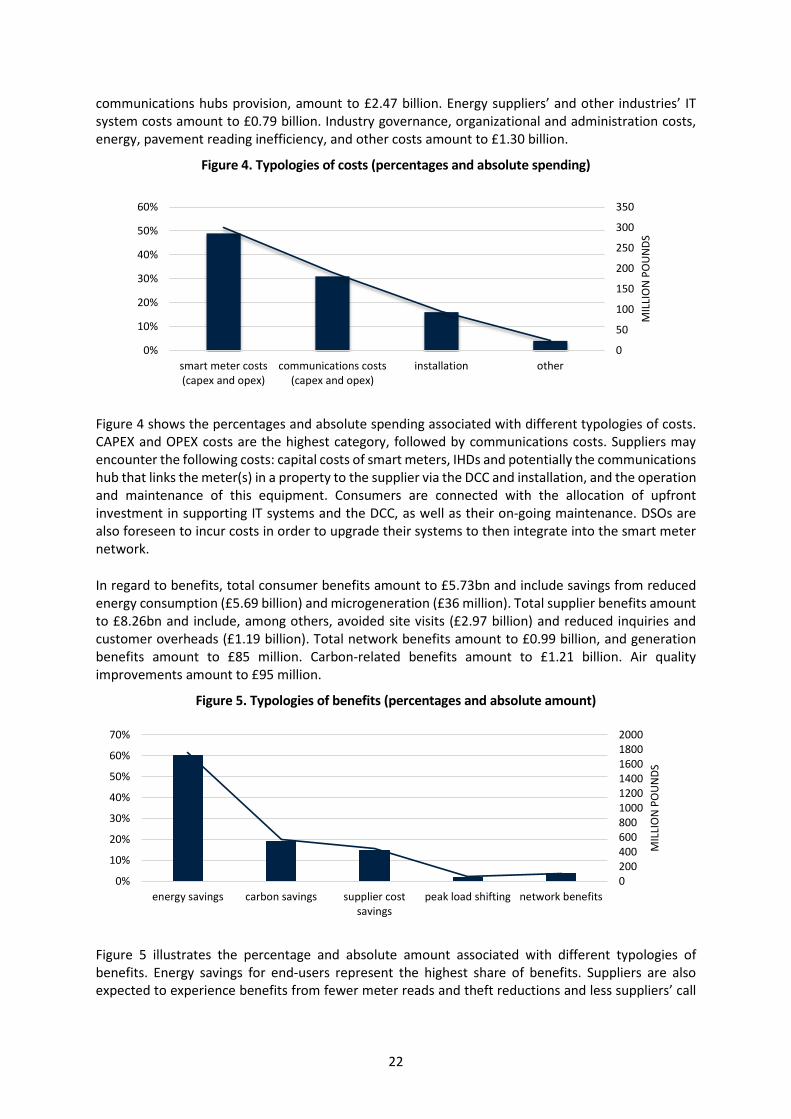

22

communications hubs provision, amount to £2.47 billion. Energy suppliers’ and other industries’ IT system costs amount to £0.79 billion. Industry governance, organizational and administration costs, energy, pavement reading inefficiency, and other costs amount to £1.30 billion.

Figure 4. Typologies of costs (percentages and absolute spending)

Figure 4 shows the percentages and absolute spending associated with different typologies of costs. CAPEX and OPEX costs are the highest category, followed by communications costs. Suppliers may encounter the following costs: capital costs of smart meters, IHDs and potentially the communications hub that links the meter(s) in a property to the supplier via the DCC and installation, and the operation and maintenance of this equipment. Consumers are connected with the allocation of upfront investment in supporting IT systems and the DCC, as well as their on-going maintenance. DSOs are also foreseen to incur costs in order to upgrade their systems to then integrate into the smart meter network.

In regard to benefits, total consumer benefits amount to £5.73bn and include savings from reduced energy consumption (£5.69 billion) and microgeneration (£36 million). Total supplier benefits amount to £8.26bn and include, among others, avoided site visits (£2.97 billion) and reduced inquiries and customer overheads (£1.19 billion). Total network benefits amount to £0.99 billion, and generation benefits amount to £85 million. Carbon-related benefits amount to £1.21 billion. Air quality improvements amount to £95 million.

Figure 5. Typologies of benefits (percentages and absolute amount)

Figure 5 illustrates the percentage and absolute amount associated with different typologies of benefits. Energy savings for end-users represent the highest share of benefits. Suppliers are also expected to experience benefits from fewer meter reads and theft reductions and less suppliers’ call

0

50

100

150

200

250

300

350

0%

10%

20%

30%

40%

50%

60%

smart meter costs(capex and opex)

communications costs(capex and opex)

installation other

MIL

LIO

N P

OU

NDS

0200400600800100012001400160018002000

0%

10%

20%

30%

40%

50%

60%

70%

energy savings carbon savings supplier costsavings

peak load shifting network benefits

MIL

LIO

N P

OU

NDS

23

center traffic. Network operators are expected to improve electricity outage management and more efficiently resolve any network failures. However, smart grid benefits were not quantified in the CBA.

The main unique aspect of cost-benefit analyses of smart meters in the UK is that the main stakeholders involved are not the DSOs8 but the suppliers.9 A key feature of the CBA in Great Britain is that it foreshadows a dual fuel electricity and gas smart meter rollout. A CBA of this nature reflects the fact that the metering market is de-regulated and that many customers use the same provider for gas and electricity supplies. Hence, in the British supplier-led model, there will be strong incentives to replace both electricity and gas meters with smart meters at the same time. This dynamic will not be applicable in all the other countries.

The different impact assessments (IAs) present dissimilar net present values (NPVs). In 2014, the NPV increased by £184m in comparison to the IA published in August 2011.

Table 7. Changes in results of cost-benefit analyses of smart metering carried out by UK governments between 2011 and 2014 (million pounds)

NPV Total Costs Total Benefits NPV difference

2011 CBA non-domestic £2,154 £604 £2,759 0

2012 CBA non-domestic £2,338 £608 £2,946 £187

2013 CBA (all end-users) £6,659 £12,115 £18,774 0

2014 CBA (all end-users) £6,214 £10,927 £17,141 £445

Table 8 presents the different findings of the CBAs performed between 2011 and 2014. Over the years, the CBA was updated to account for the changes in assumptions and projections on fossil fuel prices, carbon prices, carbon emission factors, energy consumption, and the number of meters in both domestic and non-domestic sectors. In regard to non-domestic CBAs, both total costs and benefit estimates increased. This is mainly a result of changes in carbon and energy prices as well as the move of the present value base year. The move of the PV base year results in an increase in both costs and benefits, but with the benefit increase having a stronger impact. Updated planning and rollout profiles as well as cost uplift to early meters slightly counteract this effect. Updated planning and rollout profiles resulted in fewer meters expected to be in place by the end of 2014 than previously modeled, with some benefits and costs from smart meters occurring slightly later in time.

2.3. The Netherlands

The Netherlands has a population of 17 million people and an electricity consumption of 6.71 MWh per capita.10 Historically, the main sources of electricity in the Netherlands have been fossil fuels (e.g., natural gas and coal). More recently, renewable energy sources (e.g., wind energy and solar energy) generated an increasing share of electricity.11 Consumption increased an average of 4.5% per year over the six decades.12

8 The UK electricity system does not comprise DSOs; instead, it consists of 14 DNOs (Distribution System Network Operators). 9 Details of the roll-out can be seen here: https://www.smartenergygb.org/en/smart-future/about-the-rollout/the-stages-of-the-rollout 10 IEA, Electric power consumption (kWh per capita). http://www.iea.org/statistics/statisticssearch/ 11 IEA, Netherlands - Energy System Overview. https://www.iea.org/media/countries/Netherlands.pdf 12 CBS, National Energy Outlook 2016, available at: https://www.cbs.nl/-/.../45/national%20energy%20outlook%202016_summary.pdf

24

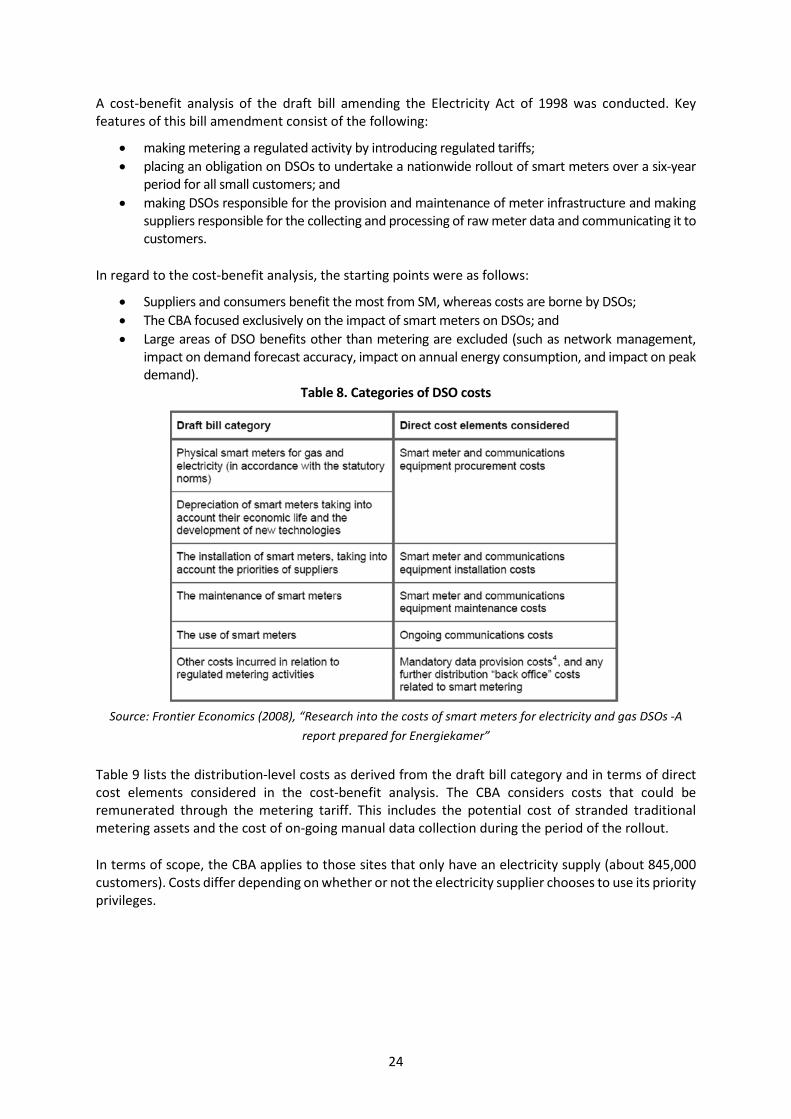

A cost-benefit analysis of the draft bill amending the Electricity Act of 1998 was conducted. Key features of this bill amendment consist of the following:

• making metering a regulated activity by introducing regulated tariffs; • placing an obligation on DSOs to undertake a nationwide rollout of smart meters over a six-year

period for all small customers; and • making DSOs responsible for the provision and maintenance of meter infrastructure and making

suppliers responsible for the collecting and processing of raw meter data and communicating it to customers.

In regard to the cost-benefit analysis, the starting points were as follows:

• Suppliers and consumers benefit the most from SM, whereas costs are borne by DSOs; • The CBA focused exclusively on the impact of smart meters on DSOs; and • Large areas of DSO benefits other than metering are excluded (such as network management,

impact on demand forecast accuracy, impact on annual energy consumption, and impact on peak demand).

Table 8. Categories of DSO costs

Source: Frontier Economics (2008), “Research into the costs of smart meters for electricity and gas DSOs -A report prepared for Energiekamer”

Table 9 lists the distribution-level costs as derived from the draft bill category and in terms of direct cost elements considered in the cost-benefit analysis. The CBA considers costs that could be remunerated through the metering tariff. This includes the potential cost of stranded traditional metering assets and the cost of on-going manual data collection during the period of the rollout.

In terms of scope, the CBA applies to those sites that only have an electricity supply (about 845,000 customers). Costs differ depending on whether or not the electricity supplier chooses to use its priority privileges.

25

Figure 6. Costs of smart meters (in € per meter, from international review)

Figure 6 shows site-specific and meter-specific costs in the Dutch cost-benefit analysis. The collection of input data on costs and benefits involved a review of published data sources as well as a bilateral discussion with Dutch market participants and meter manufacturers. Purchase costs, the installation of new meters, and GPRS communication costs are the highest costs.

Figure 7. DSO annual costs (in € per meter, from international review)

Figure 7 shows that DSOs are assumed to be able to save between EUR 4.40 and EUR 6.50 per meter per annum due to the combined impact of network management benefits and cost savings achieved as a result of the transfer of responsibility regarding data collection and validation.

The review of costs and benefits was used to generate a range for each element of costs and benefits. An economic model was developed to estimate the likely level of net cost relative to the tariffs. The model was used to assess the impacts of smart meter rollout on DSOs.

One of the most relevant features of this cost-benefit analysis is that direct feedback is not included as a category of benefits. It is instead assumed that bi-monthly readings are provided to end-users, with additional information on electricity consumption. In addition, several benefits in Recommendation 2012/148/EU are not included in the cost-benefit analysis. For instance, deferred investment, technical losses, CO2 emissions, and air pollution are not listed as benefits in the analysis. An additional benefit consists of increased competitiveness following smart metering installation. The benefit is accounted as an allowance associated with the ability for competitors to develop new market niches in a market with a full rollout of smart meters.

0 10 20 30 40 50 60 70 80 90

Purchase cost electricity meter

Maintanance cost

Data management cost

Communication costs-GPRS

Communication costs-PLC

Installation costs-separate

Installation costs-joint (new meters)

Maximum (€) Minimum (€)

0 1 2 3 4 5 6

Network Management benefits

Cost savings due to transfer ofresponsibility

Maximum (€) Minimum (€)

26

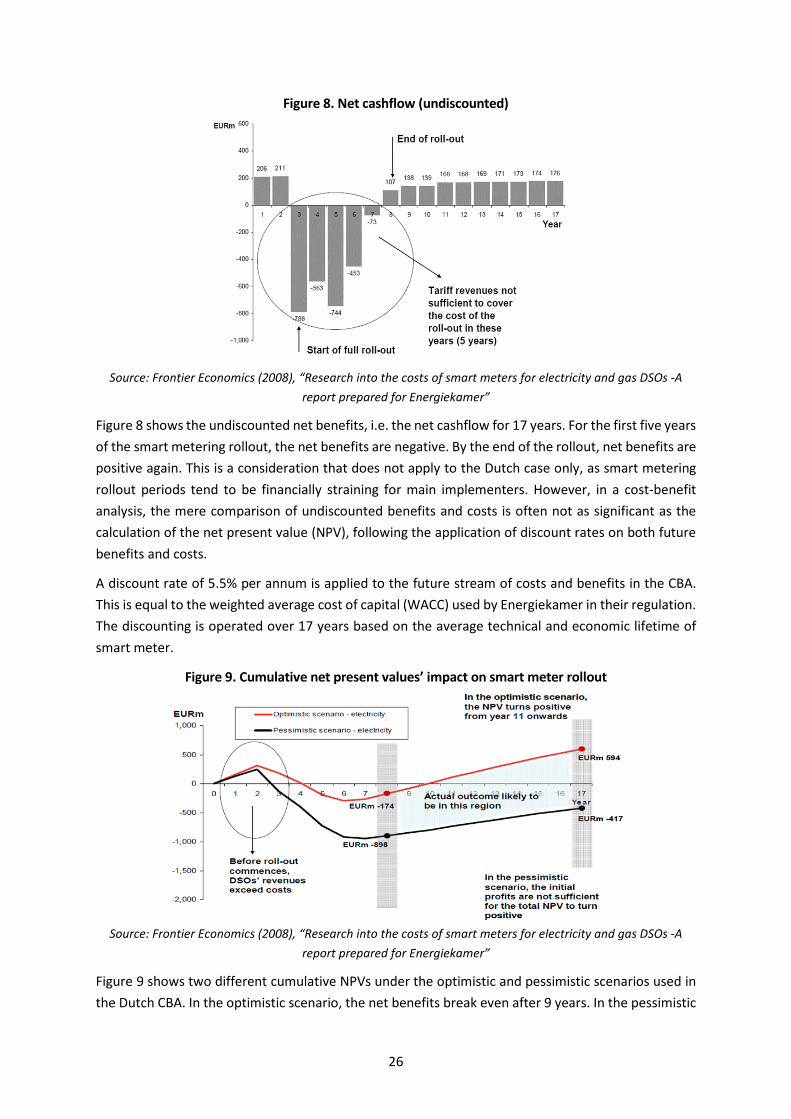

Figure 8. Net cashflow (undiscounted)

Source: Frontier Economics (2008), “Research into the costs of smart meters for electricity and gas DSOs -A report prepared for Energiekamer”

Figure 8 shows the undiscounted net benefits, i.e. the net cashflow for 17 years. For the first five years of the smart metering rollout, the net benefits are negative. By the end of the rollout, net benefits are positive again. This is a consideration that does not apply to the Dutch case only, as smart metering rollout periods tend to be financially straining for main implementers. However, in a cost-benefit analysis, the mere comparison of undiscounted benefits and costs is often not as significant as the calculation of the net present value (NPV), following the application of discount rates on both future benefits and costs.

A discount rate of 5.5% per annum is applied to the future stream of costs and benefits in the CBA. This is equal to the weighted average cost of capital (WACC) used by Energiekamer in their regulation. The discounting is operated over 17 years based on the average technical and economic lifetime of smart meter.

Figure 9. Cumulative net present values’ impact on smart meter rollout

Source: Frontier Economics (2008), “Research into the costs of smart meters for electricity and gas DSOs -A report prepared for Energiekamer”

Figure 9 shows two different cumulative NPVs under the optimistic and pessimistic scenarios used in the Dutch CBA. In the optimistic scenario, the net benefits break even after 9 years. In the pessimistic

27

scenario, the NPV remains negative for the entire duration of the assessment (i.e., 17 years). The figure can also be interpreted as the overall NPV for each year of the rollout as if the investment had been terminated in that specific year.

Figure 10. Sensitivity analysis of main categories of costs and benefits

Figure 10 shows the sensitivity analysis of main categories of costs and benefits. The sensitivity analysis emphasizes uncertainty about smart metering failure costs (higher failure rate than legacy meters). Similarly, the sensitivity analysis points to uncertainty especially about DSO communications costs (i.e. PLC vis-à-vis GPRS).

In the sensitivity analysis, a key item consists of competitiveness. Removing such item would trigger negative net benefits (i.e. -€19 per metering point, equivalent to -€127 million total).

2.4. Ireland

Ireland has a population of 5 million people and an electricity consumption of 5.81 MWh per capita.13 Overall Ireland is a net energy importer, which relies heavily on electricity imported through the interconnector with the UK.14 Electricity demand in Ireland has been decreasing since 2010, but in 2015 there was an increase by 2.9% in conjunction with economic growth. Ireland’s smart meter rollout involves about 2.2 million electricity consumers with an investment of up to €1 billion.

It is expected to yield a net benefit of around €229 million over 20 years.

13 IEA, Electric power consumption (kWh per capita), available at: http://www.iea.org/statistics/statisticssearch/ 14 SEAI (2015), Energy in Ireland 1990-2014, available at: http://www.seai.ie/resources/publications/Energy-in-Ireland-1990-2015.pdf

Smart meter failure costs

33%

Ongoing smart meters costs

32%

One-off costs 19%

Meter and communications purchase costs

16%

28

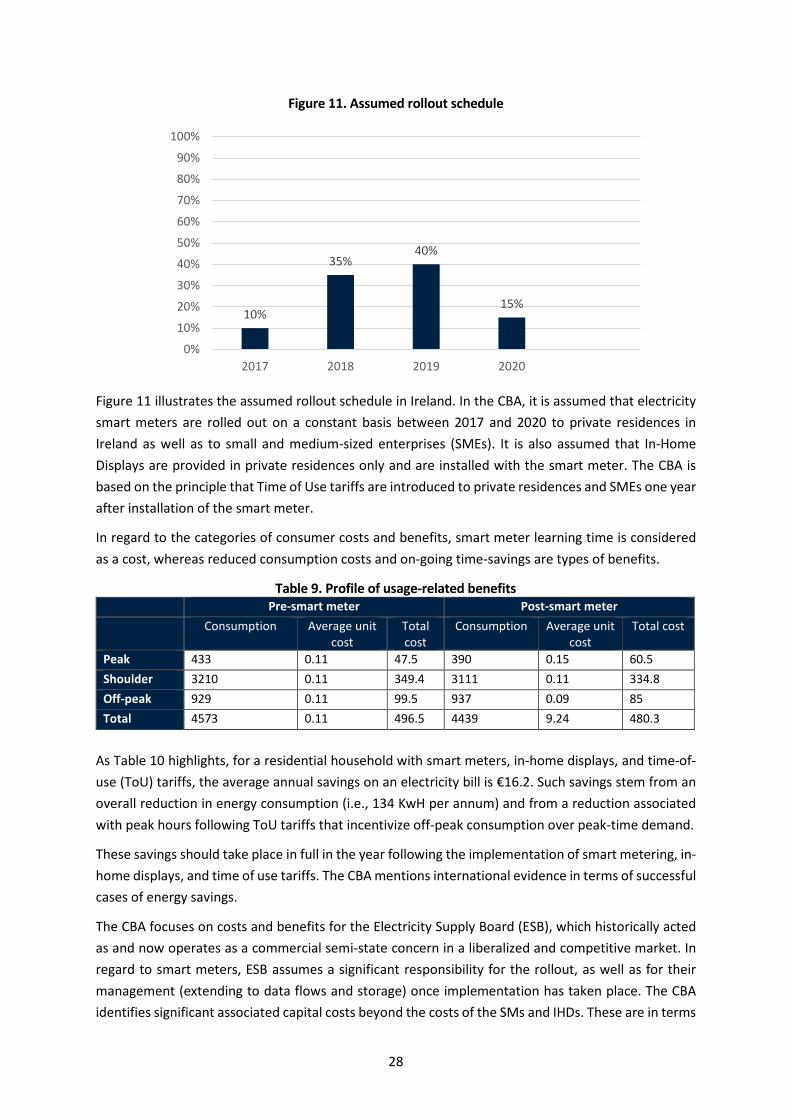

Figure 11. Assumed rollout schedule

Figure 11 illustrates the assumed rollout schedule in Ireland. In the CBA, it is assumed that electricity smart meters are rolled out on a constant basis between 2017 and 2020 to private residences in Ireland as well as to small and medium-sized enterprises (SMEs). It is also assumed that In-Home Displays are provided in private residences only and are installed with the smart meter. The CBA is based on the principle that Time of Use tariffs are introduced to private residences and SMEs one year after installation of the smart meter.

In regard to the categories of consumer costs and benefits, smart meter learning time is considered as a cost, whereas reduced consumption costs and on-going time-savings are types of benefits.

Table 9. Profile of usage-related benefits Pre-smart meter Post-smart meter

Consumption Average unit cost

Total cost

Consumption Average unit cost

Total cost

Peak 433 0.11 47.5 390 0.15 60.5 Shoulder 3210 0.11 349.4 3111 0.11 334.8 Off-peak 929 0.11 99.5 937 0.09 85 Total 4573 0.11 496.5 4439 9.24 480.3

As Table 10 highlights, for a residential household with smart meters, in-home displays, and time-of-use (ToU) tariffs, the average annual savings on an electricity bill is €16.2. Such savings stem from an overall reduction in energy consumption (i.e., 134 KwH per annum) and from a reduction associated with peak hours following ToU tariffs that incentivize off-peak consumption over peak-time demand.

These savings should take place in full in the year following the implementation of smart metering, in-home displays, and time of use tariffs. The CBA mentions international evidence in terms of successful cases of energy savings.

The CBA focuses on costs and benefits for the Electricity Supply Board (ESB), which historically acted as and now operates as a commercial semi-state concern in a liberalized and competitive market. In regard to smart meters, ESB assumes a significant responsibility for the rollout, as well as for their management (extending to data flows and storage) once implementation has taken place. The CBA identifies significant associated capital costs beyond the costs of the SMs and IHDs. These are in terms

10%

35%40%

15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2017 2018 2019 2020

29

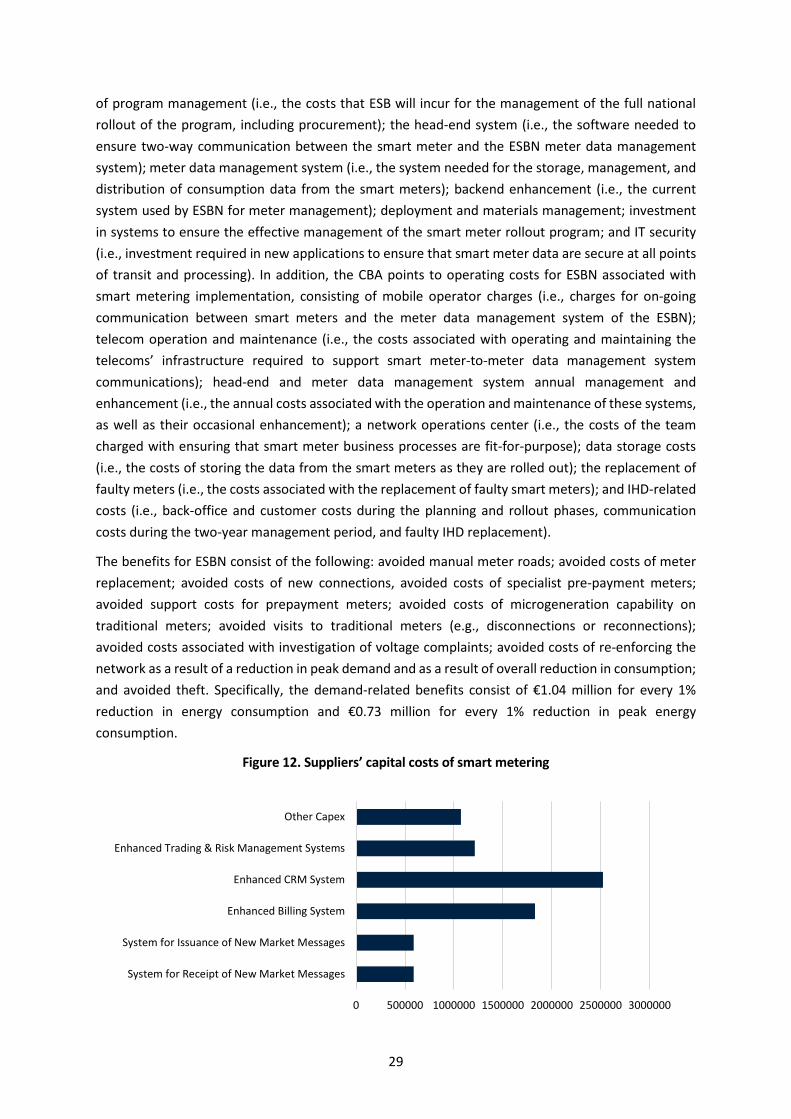

of program management (i.e., the costs that ESB will incur for the management of the full national rollout of the program, including procurement); the head-end system (i.e., the software needed to ensure two-way communication between the smart meter and the ESBN meter data management system); meter data management system (i.e., the system needed for the storage, management, and distribution of consumption data from the smart meters); backend enhancement (i.e., the current system used by ESBN for meter management); deployment and materials management; investment in systems to ensure the effective management of the smart meter rollout program; and IT security (i.e., investment required in new applications to ensure that smart meter data are secure at all points of transit and processing). In addition, the CBA points to operating costs for ESBN associated with smart metering implementation, consisting of mobile operator charges (i.e., charges for on-going communication between smart meters and the meter data management system of the ESBN); telecom operation and maintenance (i.e., the costs associated with operating and maintaining the telecoms’ infrastructure required to support smart meter-to-meter data management system communications); head-end and meter data management system annual management and enhancement (i.e., the annual costs associated with the operation and maintenance of these systems, as well as their occasional enhancement); a network operations center (i.e., the costs of the team charged with ensuring that smart meter business processes are fit-for-purpose); data storage costs (i.e., the costs of storing the data from the smart meters as they are rolled out); the replacement of faulty meters (i.e., the costs associated with the replacement of faulty smart meters); and IHD-related costs (i.e., back-office and customer costs during the planning and rollout phases, communication costs during the two-year management period, and faulty IHD replacement).

The benefits for ESBN consist of the following: avoided manual meter roads; avoided costs of meter replacement; avoided costs of new connections, avoided costs of specialist pre-payment meters; avoided support costs for prepayment meters; avoided costs of microgeneration capability on traditional meters; avoided visits to traditional meters (e.g., disconnections or reconnections); avoided costs associated with investigation of voltage complaints; avoided costs of re-enforcing the network as a result of a reduction in peak demand and as a result of overall reduction in consumption; and avoided theft. Specifically, the demand-related benefits consist of €1.04 million for every 1% reduction in energy consumption and €0.73 million for every 1% reduction in peak energy consumption.

Figure 12. Suppliers’ capital costs of smart metering

0 500000 1000000 1500000 2000000 2500000 3000000

System for Receipt of New Market Messages

System for Issuance of New Market Messages

Enhanced Billing System

Enhanced CRM System

Enhanced Trading & Risk Management Systems

Other Capex

30

Figure 12 shows suppliers’ capital costs associated with smart metering. Enhancing the customer relationship management (CRM) system and the billing system represent the highest costs for suppliers. These estimates on capital costs are based on the fact that all suppliers were interviewed regarding the impacts of smart metering implementation on their financials. Only three suppliers provided comprehensive responses. In addition to the capital costs in Figure 12, OPEX cost categories consist of staff training, an IT OPEX, customer awareness raising, smart bill production and the printing of shadow statements, and additional communications costs.

In regard to suppliers’ benefits, the main categories consist of avoided ad hoc meter reads, bad debt reduction, and a reduction in dunning cycles.

Table 10. Electricity generation benefits and costs Type of change Benefit/cost Return on Investment residential capacity pot (in MW) 1,869 Average cost per MW € 78,730 Reduction in Peak Demand -9% Benefit deflation factor 32%

Table 11 shows the benefits and costs of changes brought about by smart meters in regard to electricity generation. Reductions in peak demand bring about cost saving due to avoided generation. The NPV of this benefit is €68 million.

Table 11. Benefits associated with lower system marginal prices Value of total, residential, ROI smart metering in 2011 €1,730,510,620

Percentage reduction achieved 0.40%

Table 12 shows the benefits associated with lower system marginal prices as a result of lower demand. This is caused by the assumption that a fall in residential demand brings about a fall in wholesale prices, which leads to lower system marginal prices.

Figure 13. NPVs for different stakeholders (in thousands of Euros)

-600000 -400000 -200000 0 200000 400000 600000

Residential consumers

Small Medium Enterprises

ESBN - Smart meter and In-Home Displays

ESBN - other Capex and Opex costs

ESBN - Benefits (avoided costs)

Suppliers

Generation

TOTAL

31

Figure 13 presents the full CBA findings with different NPVs for all stakeholders. ESBN and electricity suppliers face negative NPV values. The scale of the net cost in the case of networks is substantial and reflects, in large part, the assumed national use of a GPRS communications solution with a high attendant annual operating cost. In regard to consumers, residential households are associated with positive net present values in aggregate, while SMEs’ net present values are negative.

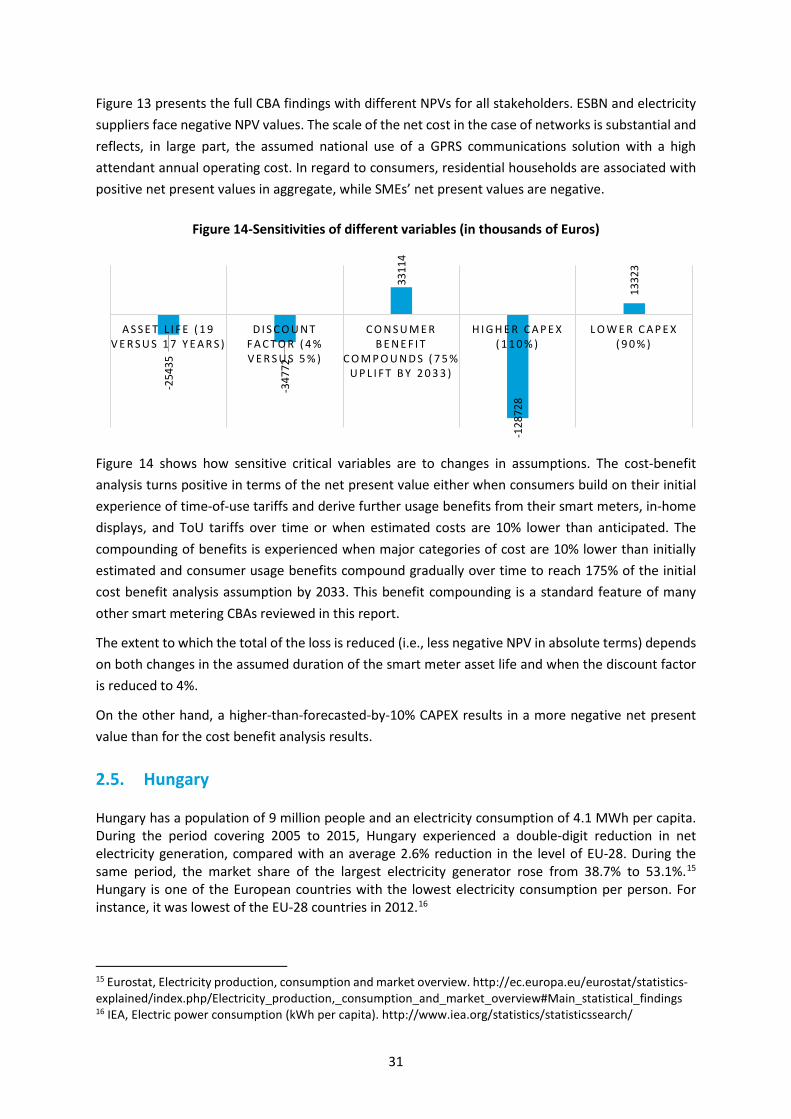

Figure 14-Sensitivities of different variables (in thousands of Euros)

Figure 14 shows how sensitive critical variables are to changes in assumptions. The cost-benefit analysis turns positive in terms of the net present value either when consumers build on their initial experience of time-of-use tariffs and derive further usage benefits from their smart meters, in-home displays, and ToU tariffs over time or when estimated costs are 10% lower than anticipated. The compounding of benefits is experienced when major categories of cost are 10% lower than initially estimated and consumer usage benefits compound gradually over time to reach 175% of the initial cost benefit analysis assumption by 2033. This benefit compounding is a standard feature of many other smart metering CBAs reviewed in this report.

The extent to which the total of the loss is reduced (i.e., less negative NPV in absolute terms) depends on both changes in the assumed duration of the smart meter asset life and when the discount factor is reduced to 4%.

On the other hand, a higher-than-forecasted-by-10% CAPEX results in a more negative net present value than for the cost benefit analysis results.

2.5. Hungary

Hungary has a population of 9 million people and an electricity consumption of 4.1 MWh per capita. During the period covering 2005 to 2015, Hungary experienced a double-digit reduction in net electricity generation, compared with an average 2.6% reduction in the level of EU-28. During the same period, the market share of the largest electricity generator rose from 38.7% to 53.1%.15 Hungary is one of the European countries with the lowest electricity consumption per person. For instance, it was lowest of the EU-28 countries in 2012.16